svm corporate presentation

TRANSCRIPT

0

Corporate Presentation September 30, 2016

The Premier Silver Producer in China

OTC: SVMLF

1

Safe Harbor Statement under the United States Private Securities Litigation Reform Act of 1995:

Except for the statements of historical fact contained herein, the information presented constitutes "forward-looking statements" within the

meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements, including but not limited to those with

respect to the price of silver, lead and zinc, the possibility, timing and amount of estimated future production, costs of production, reserve

determination and reserve conversion rates involve known and unknown risks, uncertainties and other factors which may cause the actual

results, performance or achievement of Silvercorp to be materially different from any future results, performance or achievements expressed

or implied by such forward-looking statements. Such factors include, among others, risks related to international operations, risks related to

Chinese government issuance of mining and related development permits, risks related to joint venture operations, the actual results of

current exploration activities, conclusions of economic evaluations, changes in project parameters as plans continue to be refined, future

prices of silver, lead and zinc, as well as other Risk Factors.

Although Silvercorp has attempted to identify important factors that could cause actual results to differ materially, there may be other factors

that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate

as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place

undue reliance on forward-looking statements.

The shares of Silvercorp Metals Inc. trade on the Toronto Stock Exchange (TSX: SVM). The TSX has not approved or disapproved the form

or content of this presentation.

Cautionary Note To U.S. Investors Concerning Estimates Of Measured, Indicated And Inferred Resources

This presentation uses the terms “Measured”, “Indicated” and Inferred” Resources. U.S. investors are advised that while such terms are

recognized and required by Canadian regulations, the Securities and Exchange Commission does not recognize them. “Inferred Resources”

have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed

that all or any part of an inferred resource will ever be upgraded to a higher category. Under Canadian rules, estimates of Inferred Resources

may not form the basis of feasibility or other economic studies. U.S. investors are cautioned not to assume that all or any part of

Measured or Indicated Resources will ever be converted into reserves. U.S. investors are also cautioned not to assume that all or

any part of an Inferred Mineral Resource exists, or is economically or legally mineable.

Forward Looking Statements

1

2

Overview: Strategically Focused on Silver Mining in China

2

Reserves &

Resources1

Silver

(MOz)

Lead

(Kt)

Zinc

(Kt)

Proven & Probable

Reserves 101.0 442.5 267.5

Measured & Indicated

Resources 137.3 613.1 408.0

Inferred Resources 91.9 358.0 286.8

Ying Mining District,

Henan Province FY2017: 4.6Moz Silver

BYP Mine,

Hunan Province

(On Care and Maintenance)

GC Project,

Guangdong Province FY2017: 0.5Moz Silver

1 Excludes BYP Gold Mine Resource. See appendix III-V for breakout.

China

XHP Project

Henan Province

3

Silvercorp’s Strategy

Ten Years of Proven Execution

• Successfully acquired and developed multiple projects

• Built 800,000 t/a mining + milling capacity at Ying Mining District and built 500,000 t/a mine

and mill capacity at GC Project.

• Consolidated mine life remains above 10 years after 10 years of production (46.6 million Oz

silver produced to date)

• Strong Operating Performance and Financial Position

3

Our Strategy

• Grow existing assets organically through land expansion and drilling

• Acquire under-explored, smaller-scale mining projects with resource growth potential

• Apply leading edge mine techniques to optimize operations, reducing dilution and costs

• Leverage underutilized milling capacity as commodity prices improve

4

Three Months Ended

June 30, 2016

(millions US$)

Three Months Ended

June 30, 2015

(millions US$)

Revenue $35.3 $32.2

Gross Profit $15.7

$11.5

Net Income $6.5

$3.8

Cash Flow from Operations $20.2 $13.3

Cash, cash equivalents and short-term investments: $73.4 Million, up $11.4 million

since year end.

Shares Outstanding: 167 million (basic and diluted)

TSX Exchange: SVM (OTC:SVMLF)

No Long-term Debt, Unhedged

Financial Snapshot – Q1 FY2017 Results

4

5

45%

36% 34%

29%

24% 23%

15%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Gross Profit Margins*

Low Cost Silver Producer - Fiscal 2017 Q1 Results

5

Low cost producer of silver - cash cost of

$0.08** per Ag ounce for Q1 FY2017 Q1 FY2017 Sales Mix by Metal

** Net of by-product credits. AISCC of $7.06 per Oz

* Quarter ended Jun. 30, 2016.

Silver, 59.1%

Gold, 2.5%

Lead, 29.7%

Zinc, 8.4%

Other, 0.3%

6

7.06

8.16

9.62

10.53 10.97

11.31

14.92

0.00

3.00

6.00

9.00

12.00

15.00AISCC

6

Low All in Sustaining Cost Relative to Peers

* Quarter ended Jun. 30, 2016.

7

0.0

5.0

10.0

15.0

SVM CDE PAAS FVI EDR FR

EV/EBITDA

2016E 2017E

0.0

4.0

8.0

12.0

16.0

20.0

CDE SVM PAAS FVI EDR FR

P/CF

2016E 2017E

7

Source: Raymond James Report September 22, 2016.

Low Valuation Matrix Relative to Peers

SVM SVM

8

Ying Mining District: Silvercorp’s Flagship Asset

• Flagship Ying District consists of underground mines including SGX, TLP, LM, and HPG mines

• Over 70km2 land package

• Extensive underground drilling has maintained mine life at >10 years

• Has produced over 46.6 million Oz silver since 2006

• Two centralized mills with 3,200 t/d capacity

• Producing silver-lead and zinc concentrates

• 6 smelters within 200km of the district

• Opportunity for further acquisitions in local area

8

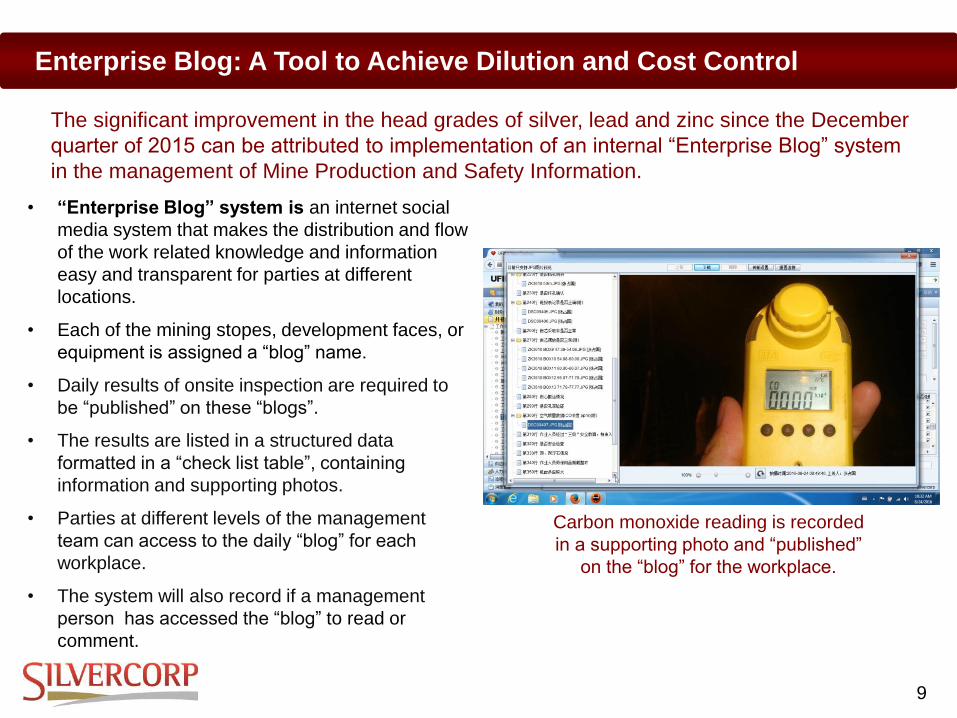

9 9

• “Enterprise Blog” system is an internet social

media system that makes the distribution and flow

of the work related knowledge and information

easy and transparent for parties at different

locations.

• Each of the mining stopes, development faces, or

equipment is assigned a “blog” name.

• Daily results of onsite inspection are required to

be “published” on these “blogs”.

• The results are listed in a structured data

formatted in a “check list table”, containing

information and supporting photos.

• Parties at different levels of the management

team can access to the daily “blog” for each

workplace.

• The system will also record if a management

person has accessed the “blog” to read or

comment.

Enterprise Blog: A Tool to Achieve Dilution and Cost Control

Carbon monoxide reading is recorded

in a supporting photo and “published”

on the “blog” for the workplace.

The significant improvement in the head grades of silver, lead and zinc since the December

quarter of 2015 can be attributed to implementation of an internal “Enterprise Blog” system

in the management of Mine Production and Safety Information.

10 10

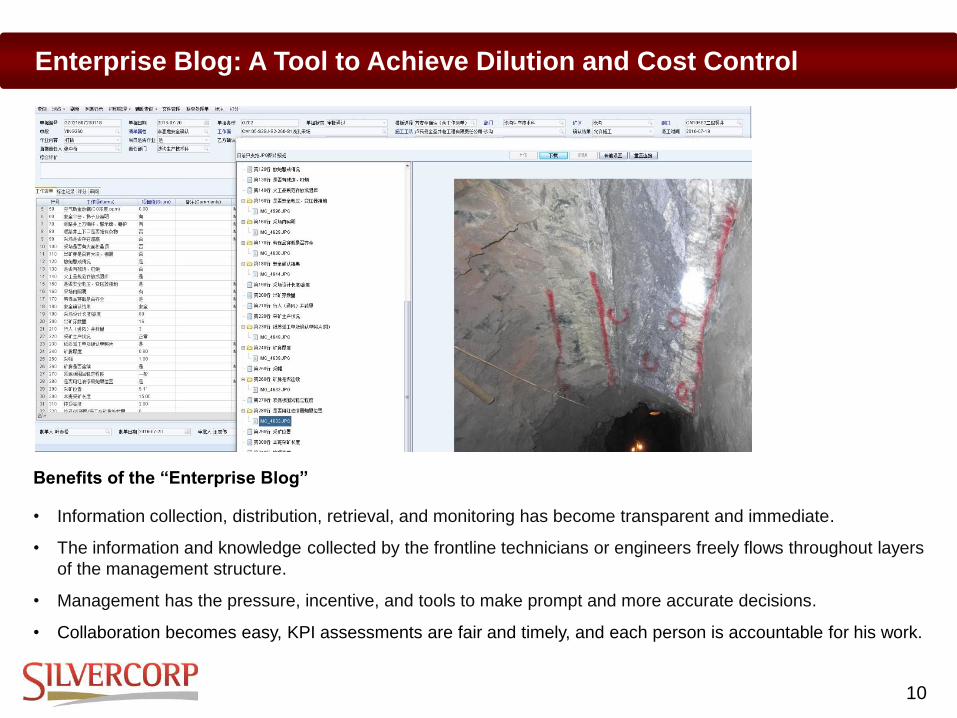

Benefits of the “Enterprise Blog”

• Information collection, distribution, retrieval, and monitoring has become transparent and immediate.

• The information and knowledge collected by the frontline technicians or engineers freely flows throughout layers

of the management structure.

• Management has the pressure, incentive, and tools to make prompt and more accurate decisions.

• Collaboration becomes easy, KPI assessments are fair and timely, and each person is accountable for his work.

Enterprise Blog: A Tool to Achieve Dilution and Cost Control

11 11

200,000

180,000

160,000

140,000

120,000

100,000

80,000

60,000

40,000

20,000

0 0

50

100

400

350

300

250

200

150

Tonnes Grades

Silver Head Grades and Ore Production Monthly Data at Ying Mining District

(Jan 2012 to Jun 2016)

IMPROVING HEAD GRADES

Silv

er

Gra

de G

ram

/to

nn

e

To

nn

es

of

Ore

12

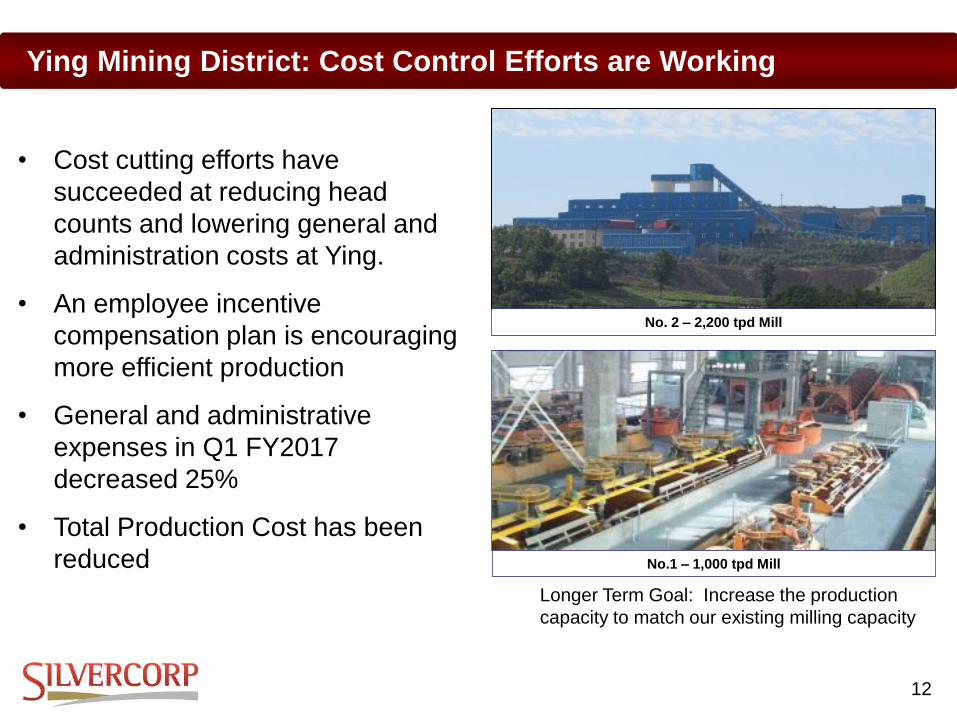

Longer Term Goal: Increase the production

capacity to match our existing milling capacity

Ying Mining District: Cost Control Efforts are Working

No.1 – 1,000 tpd Mill

No. 2 – 2,200 tpd Mill

12

• Cost cutting efforts have

succeeded at reducing head

counts and lowering general and

administration costs at Ying.

• An employee incentive

compensation plan is encouraging

more efficient production

• General and administrative

expenses in Q1 FY2017

decreased 25%

• Total Production Cost has been

reduced

13

Net profit per tonne for Ying Mining District

13

14

Consolidated net profit per tonne

14

15 15

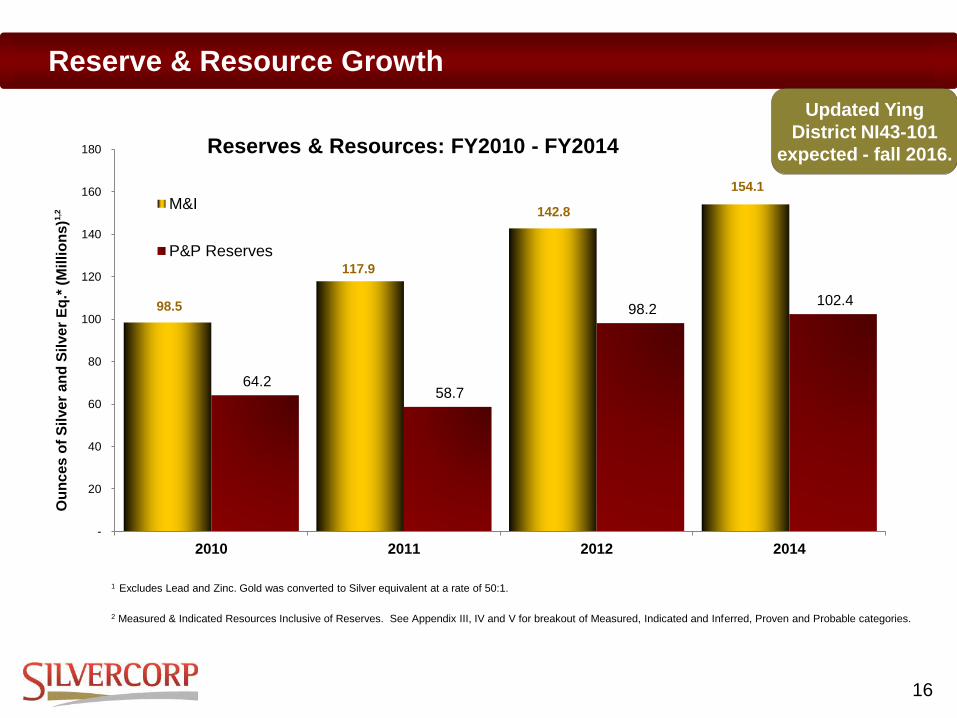

225,000m of drilling and 128,000m of tunnelling between 2013 - 2016

New 43-101 Report Expected at Ying Mining District

• Expansion and definition of previous known Mineral Resource blocks.

• New mineralization defined downdip and along strike within known

vein structures.

• New mineralized parallel and splay structures discovered beside major

structures.

• New mineralized structures in less-explored areas in the Ying property.

Results of the extensive exploration program have been incorporated into

the exploration database for the current 43-101 resource update which is

being prepared by AMC Consulting and expected in November 2016.

16

Reserve & Resource Growth

16

1 Excludes Lead and Zinc. Gold was converted to Silver equivalent at a rate of 50:1.

2 Measured & Indicated Resources Inclusive of Reserves. See Appendix III, IV and V for breakout of Measured, Indicated and Inferred, Proven and Probable categories.

98.5

117.9

142.8

154.1

64.2 58.7

98.2 102.4

-

20

40

60

80

100

120

140

160

180

2010 2011 2012 2014

Ou

nc

es

of

Sil

ve

r a

nd

Sil

ve

r E

q.*

(M

illi

on

s)1

,2

Reserves & Resources: FY2010 - FY2014

M&I

P&P Reserves

Updated Ying

District NI43-101

expected - fall 2016.

17

Concentrate Thickener

Mill Plant Shaft

110KV Power Substation

17

Dewatering Plant

Concentrate Warehouse

GC Mine: Commercial Mining Underway

18

• Underground silver/zinc mine

• Excellent infrastructure and access

• Construction completed and permits obtained

• Commercial production underway

• Producing zinc-silver, lead-silver, and pyrite concentrates

• Produced 0.15 million Oz Ag and 5.27 million lbs. Pb/Zn in Q1 FY2017

GC Mine in Guangdong – Our Newest Mine

18

Main Access Ramp

19

Flotation Mill Interior

• Sold 149,000 Oz Ag and 5.3 million lbs. Pb/Zn during Q1

FY2017.

• Contributed $4.6 million in revenue.

• Ongoing efforts being made to lower production costs and

fine tune milling and mining operations.

• FY2017 capital ex budget of $1.0 million, including $0.5

million for tunnel development and $0.5 million to compete

the shaft development.

GC Mine: Commercial Production is Underway

19

Flotation Mill Testing

20

BYP Gold Mine – a non-core asset

Status:

• suspended mining operations in

August 2014

• Currently the Company is evaluating

to re-start the operation or other

options.

500 tpd Mill at the BYP Mine

20

21

FY2017 Production Guidance

21

• Guidance as of February 5, 2016

Ore processed (tonnes) 610,000 250,000 860,000

Silver (gram per tonne) 260 109

Lead (%) 4.1 1.3

Zinc (%) 0.8 3.0

Silver ('000 ounces) 4.6 0.5 5.1

Lead (million pounds) 50.7 6.3 57.0

Zinc (million pounds) 5.3 14.0 19.3

Total Cash Cost (US$/t) 74.3 47.0 66.4

AISCC (US$/Ag Oz) 8.13 8.86 9.67

Metal Production

Mining Costs

Project Ying Mining District GC Mine Grand Total

Head Grades

22

Silver Production – Over 46 Million Ounces to Date

1. Gold converted to silver at a rate of 50:1; Silvercorp’s fiscal year ends March 31st

2. FY2017E as of Feb 5, 2016.

22

1.9

4.1 4.3 4.7

5.5 5.8

5.2

3.9

4.6 4.4 4.6

0.5 0.6

0.5

-

1.0

2.0

3.0

4.0

5.0

6.0

M

i

l

l

i

o

n

s

o

f

O

u

n

c

e

s

AgEq Production – Actual and Forecast1,2

GC Ying MiningDistrict

5.0 5.1 5.1E

23

* includes tunnel development.

** includes $7.2 million for transportation tunnel and haul road construction, and $5.0 million of mining right fees.

*** in F2017 Company’s focus is shifting to increased usage of exploration tunneling based on previous year’s drilling.

Guidance as of Feb. 5, 2016.

Mines/

Projects

Mine Development*

Facilities/

Land Usage/

Equipment**

Drilling/Tunnelling

Exploration***

Total

US$

million

Cost

($million)

Work

(meters)

Cost

($million)

Cost

($million)

Drilling

(meters)

Ying Mining District 2.1 6,743 13.5 14.6 48,375 30.2

GC Mine 0.5 1,080 0.5 0 3,545 1.0

Total Budget 2.6 7,823 14.0 14.6 51,920 31.2

FY2017 Capital Expenditure Guidance

23

24

Recent Achievements

24

• Focus on improved monitoring resulting in continuous operating

improvements

• Strengthened management with new mine managers, & return of

Silvercorp’s founder, Rui Feng as CEO

• Addressed and improved relationships with contractors

• Head grade improvements achieved thru dilution control

• Mining costs are under control

• Production quantity is achieving targets

• Employee headcount reductions achieved

• Lowered G&A expenses

• GC in commercial production

• Repurchased 4.0 million shares in the latest 12 months

25

• Strong Financial Position - $73.4 million cash on hand. No LT. debt

• Low cost silver producer in a mining friendly jurisdiction

• Long life silver asset with a track record of resource growth

• Generated $20.2 million in cash flow from operations in Q1 FY2017

despite lower silver prices

• Optimized mine operating performance has succeeded

- Higher grades,

- Higher production,

- Lower All In Sustaining Cash Costs

• Low valuations relative to peer companies

Investment Highlights

25

26

Appendices

26

27

Top 10 Institutional Investors –

Firms and Funds % O/S

1 Van Eck Associates Corporation 10.34

2 Rafferty Asset Management LLC 4.15

3 Global X Management Company

LLC 1.38

4 Esposito Partners, LLC 0.95

5 Norges Bank Investment

Management (NBIM) 0.79

6 AMG Fondsverwaltung AG 0.70

7 Renaissance Technologies LLC 0.65

8 Stabilitas GmbH 0.60

9 BlackRock Institutional Trust

Company, N.A. 0.36

10 Old Mutual Global Investors (UK)

Limited 0.29

Analyst Coverage

Chris Thompson Raymond James

Source: Thomson One September 28, 2016 Data

Appendix I: Ownership and Coverage

27

28

Board of Directors

Rui Feng Malcolm Swallow

Yikang Liu Paul Simpson

David Kong

Management

Rui Feng, Ph.D., Geology

Chairman and CEO, Director

Derek Liu, CGA, CPA

Chief Financial Officer

Luke Liu, M. Eng. PhD (Mining Eng.)

Vice President China Operations

Lorne Waldman, MBA, LL.B.

Senior Vice President

Alex Zhang, M. Eng., M.Sci., P. Geo.

Vice President, Exploration

Gordon Neal,

Vice President, Corporate Development

Appendix II: Management & Board

28

29

1. Table excludes HPG mine Proven reserves of 16,900 oz Au (560,000 tonnes grading 0.94 g/t Au) and HPG mine Probable reserves of 12,200 00 oz Au (360,000 tonnes grading 1.05

g/t Au)

2. For further information please refer to the Technical Report for Ying Gold-Silver-Lead-Zinc Property (filed September 2014) and the GC Technical Report (filed February 2012). All reports

are available on SEDAR (www.sedar.com).

3. Rounding of some figures may lead to minor discrepancies in some totals

4. Mineral reserves include consideration of mining dilution

Appendix III: Summary of Silver Reserves1,2,3,4

29

Project Reserve

Category

Tonnes

(Million)

Head Grades Contained Metal Reserves

Ag (g/t) Pb (%) Zn (%) Ag (Moz) Pb (t) Zn (t)

Ying Mining

District

Proven 5.24 207 3.56 1.34 34.81 186,700 70,200

Probable 7.40 200 2.62 0.77 47.71 193,700 57,000

GC Project

Proven 0.46 199 1.12 3.18 3.0 5,200 14,800

Probable 4.29 113 1.33 2.93 15.5 56,900 125,500

Consolidated

Proven 5.70 37.81 191,900 85,000

Probable 11.69 63.21 250,600 182,500

Total 17.39 101.02 442,500 267,500

30

1. Table excludes HPG mine Measured resources of 23,900 oz Au (660,000 tonnes grading 1.12 g/t Au), Indicated resources of 20,000 oz Au (500,000 tonnes grading 1.25

g/t Au), Inferred resources of 14,600 oz Au (430,000 tonnes grading 1.07 g/t Au). Table also excludes BYP Au-Pb-Zn project resources (BYP resources summarized on

Slide 28).

2. For further information please refer to the revised Technical Report for Ying Gold-Silver-Lead-Zinc Property (filed September 2014) and the GC Technical Report (filed

February 2012). All reports are available on*SEDAR (www.sedar.com).

3. Rounding of some figures may lead to minor discrepancies in some totals

4. Resources are inclusive of resources converted in mineral reserves.

Appendix IV: Summary of Silver Resources1,2,3,4

30

Project Reserve

Category

Tonnes

(Million)

Head Grades Contained Metal Resources

(Inclusive of Reserves)

Ag (g/t) Pb (%) Zn (%) Ag (Moz) Pb (t) Zn (t)

Ying Mining

District

Measured 5.56 253 4.53 1.67 45.81 253,400 94,600

Indicated 8.45 226 3.05 0.92 61.49 258,800 78,100

Inferred 7.53 251 3.26 0.99 60.50 245,500 74,900

GC Project

Measured 0.59 230 1.41 3.33 4.4 8,400 19,800

Indicated 7.04 113 1.31 3.06 25.6 92,500 215,500

Inferred 7.96 123 1.41 2.66 31.4 112,500 211,900

Consolidated

Measured 6.15 50.21 261,800 114,400

Indicated 15.49 87.09 351,300 293,600

Inferred 15.49 91.90 358,000 286,800

31

Mineral Resources for Gold Zones as of December 31, 2011:

CLASS Cut-off

Grades (g/t)

Resource Grades Contained Metal

Resources

(tonne) Au (g/t) Au (oz)

Indicated 1.0 3,510,000 2.59 292,000

Inferred 1.0 2,470,000 1.84 146,000

Mineral Resources for Lead and Zinc Zones as of December 31, 2011:

CLASS

Cut-off

Grades

(g/t)

Resource Grades Contained Metal

Resources

(tonne) Pb(%) Zn(%) Pb (Tonnes) Zn (Tonnes)

Indicated 2.0

Pb+Zn 7,330,000 1.16 2.52 85,000 184,700

Inferred 2.0

Pb+Zn 7,550,000 0.85 2.75 64,200 207,600

Notes to Resource Tables:

1. CIM definitions apply

2. Mined tonnages deducted

3. Resources are rounded to nearest 10,000 tonnes

4. Cut-off grades are based on mining, processing and G & A costs of $38/t

5. Technical report filed on August 16, 2012 at www.sedar.com

Appendix V: BYP Mine Resource

31

32

Key Growth Catalysts

32

Ying Mining District :

• More efficient and lower cost mining

• Reduced management overhead and greater incentives

• Longer term opportunity to increase mining capacity to match milling capacity

• Further near district acquisitions

GC Project:

• Commercial production underway

• Fine tuning operations to improve efficiencies and lower costs

• Continue exploration to expand resources

• Growth:

• Grow existing assets organically through land expansion and drilling

• Acquire under-explored, smaller-scale mining projects, ideally in Asia, with resource

growth potential

33

Luke Liu, M. Eng. PhD Vice President China Operations is the Qualified Person within the meaning of

National Instrument 43-101 – Standards Of Disclosure for Mineral Projects (“NI 43-101”) who

supervised the preparation of the scientific and technical information of Silvercorp included in this

presentation.

For more information on Silvercorp’s projects, readers should refer to Silvercorp’s Annual Information Form,

dated June 16, 2016, and its technical reports, each of which is available on SEDAR at www.sedar.com.

The scientific and technical information related to Silvercorp’s projects included in this investor

presentation are derived from the technical reports entitled:

- NI 43-101 Technical Report for Ying Gold-Silver-Lead-Zinc Property, Henan Province, China, prepared July

29, 2014 by P R Stephenson, P. Geo., H A Smith, P.Eng., A Riles, MAIG, M Molavi, P.Eng

- NI 43-101 Technical Report on the BYP Gold-Lead-Zinc Property, Hunan Province, China, dated June 30,

2012, prepared by P R Stephenson, P. Geo., H A Smith, P.Eng., A Riles, MAIG, M Molavi, P.Eng, D.

Nussipakynova, P.Geo., A. Ross, P.Geo.

- NI 43-101 Technical Report on the GC Ag-Zn-Pb Project in Guangdong Province, People’s Republic of

China, dated January 23, 2012, prepared by Brian O’Connor, P. Geo, Peter Mokos, MAusIMM (CP), Alan

Riles, MAIG, Owen Watson, MAusIMM (CP), Mo Molavi, P. Eng, Patrick Stephenson, P. Geo, AMC Mining

Consultants (Canada) Ltd.

Endnotes and Cautionary Statements

33

34

Suite #1378 - 200 Granville St., Vancouver, BC, Canada V6C 1S4

Tel: 604-669-9397 | Fax: 604-669-9387 | Toll-Free: 1-888-224-1881

Email: [email protected] Website: www.silvercorp.ca

Head Office

Silvercorp’s disclosure

documents are available from the

System for Electronic Document

Analysis and Retrieval (SEDAR) at

www.sedar.com

Contact Information

34