superannuation & smsfs an industry overview tracey besters – smsf design

TRANSCRIPT

Superannuation & SMSFsAn industry overview

Tracey Besters – SMSF Design

Superannuation & SMSFs - An industry overview

DISCLAIMER

Please note this presentation is to be considered as general advice only. The opinions of the presenter should not be relied upon as providing specific advice for you or your clients.

The information contained within this presentation is based upon our understanding of the relevant legislation, regulations and other materials as at May 2015.

Superannuation & SMSFs - An industry overview

Topics

1. Insurance changes from 1 July2014

2. Related party LRBAs

3. Excess non-concessional contributions

4. Superstream

5. Other

6. What will not be changing

Superannuation & SMSFs - An industry overview

1. Insurance changes from 1 July 2014

ATOID 2015/10 Life insurance - Buy sell agreement - financial assistance - sole purpose

Does a self managed superannuation fund (SMSF) contravene section 62 and paragraph 65(1)(b) of the Superannuation Industry (Supervision) Act 1993 (SISA) by purchasing a life insurance policy over the life of a member of the SMSF where the purchase is a condition and consequence of a buy-sell agreement the member has entered into with his brother as co-owners of their business?

Superannuation & SMSFs - An industry overview

1. Insurance changes from 1 July 2014

ATOID 2015/10 Life insurance - Buy sell agreement - financial assistance - sole purpose SMSF member and brother run a business SMSF’s only other member is spouse Member and brother enter into buy-sell agreement SMSF purchases life insurance policy over life of member with

amount based on agreed market value of member’s interest in company

Superannuation & SMSFs - An industry overview

1. Insurance changes from 1 July 2014

ATOID 2015/10 Life insurance - Buy sell agreement - financial assistance - sole purpose The company makes additional contributions with the agreement

stating these amounts are to pay for the insurance premiums

Superannuation & SMSFs - An industry overview

1. Insurance changes from 1 July 2014

ATOID 2015/10 Life insurance - Buy sell agreement - financial assistance - sole purpose

Upon death of member: Insurance policy proceeds to be paid to SMSF’s trustee The trustee adds proceeds to member’s benefits Trustee pays all member’s benefits to spouse Member’s shareholding in company transferred to brother

Superannuation & SMSFs - An industry overview

1. Insurance changes from 1 July 2014

ATOID 2015/10 Life insurance - Buy sell agreement - financial assistance - sole purpose

Consequence – contravention of sections 62 and 65(1)(b): The additional benefits sought by the parties entering into

agreement not regarded as being merely incidental to the core retirement income purposes of the SMSF (section 62)

Financial assistance is given to the member’s brother by allowing him to obtain total ownership of company for no consideration (section 65(1)(b)

Superannuation & SMSFs - An industry overview2. Related party LRBAs

ATOID 2014/39 non-arm's length income - related party non-commercial limited recourse borrowing arrangement to acquire listed shares

The fund borrowed money to acquire shares in several ASX listed companies A separate LRBA was used for each parcel The total of the loans is several million dollars Term of the loan is 20 years Fund trustee must repay each loan as a single lump sum at the

end of the loan term but may repay loan earlier if agreed

Superannuation & SMSFs - An industry overview

2. Related party LRBAs

ATOID 2014/39 Related Party LRBAs The fund borrowed money to acquire shares in several ASX listed

companies A separate LRBA was used for each parcel The total of the loans is several million dollars Term of the loan is 20 years Fund trustee must repay each loan as a single lump sum at the

end of the loan term but may repay loan earlier if agreed

Superannuation & SMSFs - An industry overview

2. Related party LRBAs

ATOID 2014/39 Related Party LRBAs The interest rate is 0% or such other rate as agreed between the

borrower and lender The lender’s rights against borrower in relation to any default on

any particular loan is limited to the particular asset(s) The LVR was 100% A first ranking mortgage or charge in favour of lender granted

over shares acquired with borrowing No personal guarantees or other security given to lender

Superannuation & SMSFs - An industry overview

2. Related party LRBAs

ATOID 2014/39 Related Party LRBAs

The loan was considered non-arm’s length because of the following: Lender is not charging interest Lender not compensated for opportunity cost in lending or for

additional risk in relation to recover of principal in event of default

Lack of other security No regular periodic repayments of principal

Superannuation & SMSFs - An industry overview

2. Related party LRBAs

ATOID 2014/40 Non-arm's length income - related party non-commercial limited recourse borrowing arrangement to acquire real property

Will ordinary or statutory income derived by a self-managed superannuation fund (the Fund) under the arrangement described below, which involves a limited recourse borrowing arrangement (LRBA), be non-arm's length income of the fund pursuant to section 295-550 of the Income Tax Assessment Act 1997 (ITAA 1997)?

Superannuation & SMSFs - An industry overview

2. Related party LRBAs

ATOID 2014/40 Related Party LRBAs

Non-arm's length income on asset acquired with LRBA because: Lender not charging interest on the loan No regular periodic payments of principal in loan agreement 80% LVR No insistence by lender on giving personal guarantee as security No mechanism to protect underlying value of the asset acquired

Superannuation & SMSFs - An industry overview

3. Excess non-concessional contributions

Releasing excess non-concessional contributions

Upon receiving an excess NCC determination for a financial year members may elect to release from their superannuation interest: NCCs that exceed their NCC cap for the financial year and 85% of

any associated earnings Members may elect to release the total amount stated in the

determination or elect not to release the amount, for example their superannuation interest may be nil or less than the amount in the determination

Superannuation & SMSFs - An industry overview

3. Excess non-concessional contributions

Releasing excess non-concessional contributions

The released amount will be non-assessable non-exempt income however the associated earnings on the excess contributions to be included in the members’ assessable income in accordance with section 303-17 of the ITAA 1997

Superannuation & SMSFs - An industry overview

3. Excess non-concessional contributions

Releasing excess non-concessional contributions

Commissioner may issue release authority stating: Total amount to be released The date of the release authority Any other information the Commissioner considers relevant

Superannuation & SMSFs - An industry overview

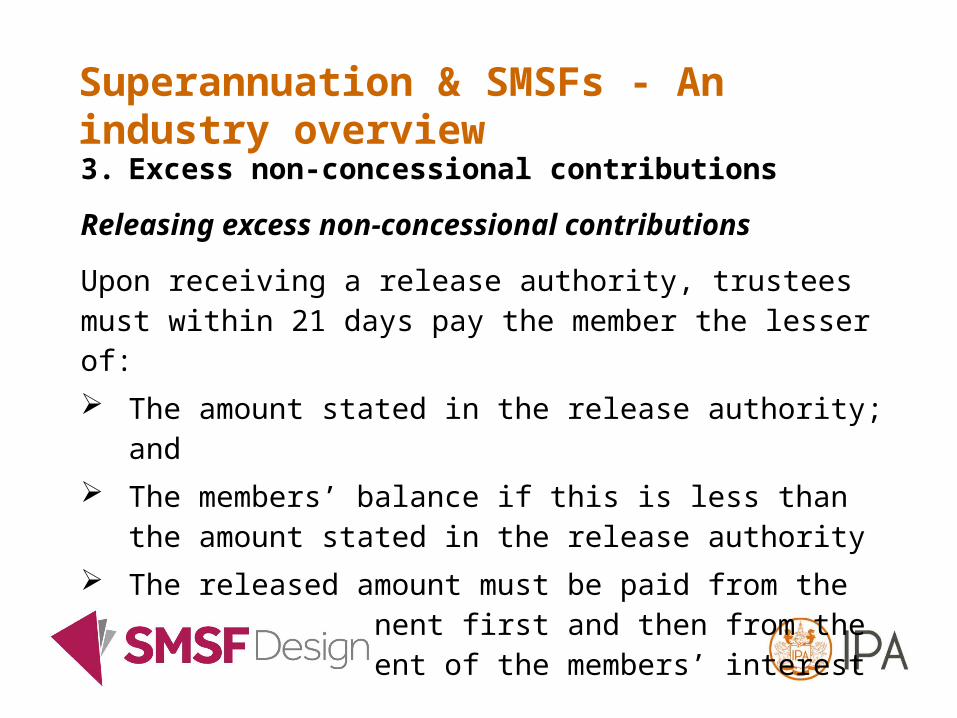

3. Excess non-concessional contributions

Releasing excess non-concessional contributions

Upon receiving a release authority, trustees must within 21 days pay the member the lesser of: The amount stated in the release authority; and The members’ balance if this is less than the amount stated in

the release authority The released amount must be paid from the tax free component

first and then from the taxable component of the members’ interest

Superannuation & SMSFs - An industry overview

3. Excess non-concessional contributions

Releasing excess non-concessional contributions

Upon receipt of a release authority must notify the member of a payment made to the member in the approved form and within 21 days after the release authority is issued

Could pose cash flow problems

Superannuation & SMSFs - An industry overview

3. Excess non-concessional contributions

Associated earnings

Associated earnings to be included in the tax return of the individual for the income year in which the NCC was made: Individual entitled to non-refundable 15% tax offset May require amendment to previously lodged tax return; and Possible GIC to apply to the amount payable per the amended

assessment

Superannuation & SMSFs - An industry overview

3. Excess non-concessional contributions

Implication for member not choosing to refund excess NCC

Excess NCC tax to still apply Potentially leading to 95% taxation Potential for large penalties where BFR has been used

Superannuation & SMSFs - An industry overview

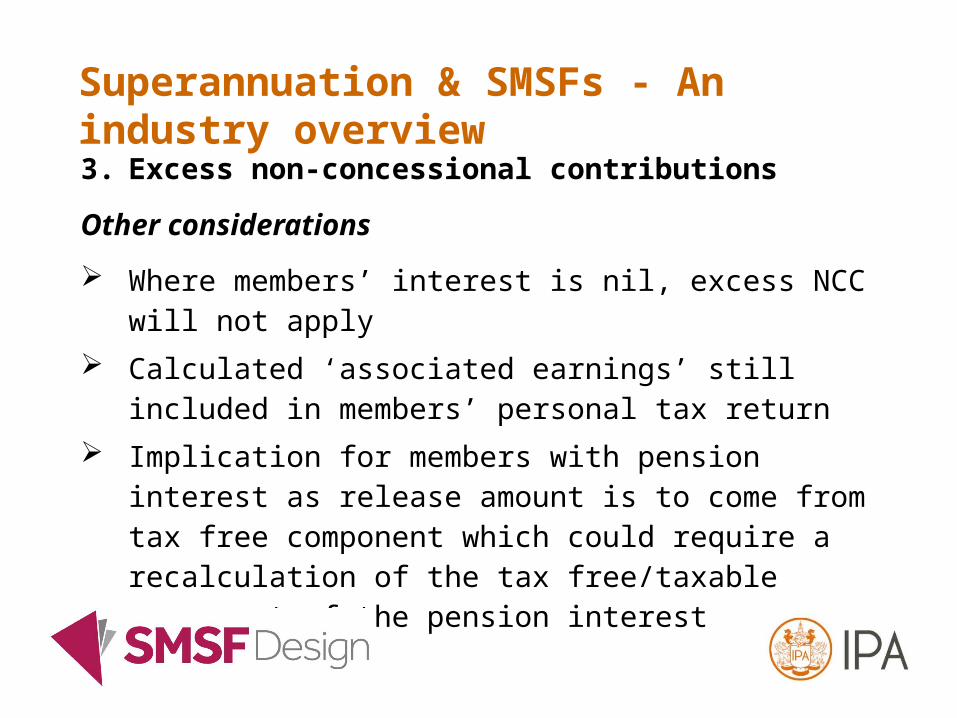

3. Excess non-concessional contributions

Other considerations

Where members’ interest is nil, excess NCC will not apply Calculated ‘associated earnings’ still included in members’

personal tax return Implication for members with pension interest as release

amount is to come from tax free component which could require a recalculation of the tax free/taxable component of the pension interest

Superannuation & SMSFs - An industry overview

3. Excess non-concessional contributions

Other considerations

The excess NCC can be released from any superannuation interest, i.e. does not have to come from the SMSF

Therefore it provides a member the opportunity to release the amount from a superannuation interest with a large taxable component

Superannuation & SMSFs - An industry overview

4. Superstream

From 1 July 2014: Employers with 20 or more employees started using the

SuperStream standard to send contribution data payments electronically

All super funds (including SMSFs) must receive any employer contributions sent to their fund in accordance with the SuperStream standard

Superannuation & SMSFs - An industry overview

4. Superstream

From 1 July 2015: Employers with 19 or fewer employees will also be required to

send contributions data and payment electronically – however, some may choose to implement SuperStream sooner.

Superannuation & SMSFs - An industry overview

4. Superstream

Related party employers & SMSFs: Contributions sent to a SMSF from a related party employer are

exempt from SuperStream and can be made using existing processes.

Superannuation & SMSFs - An industry overview

4. Superstream

Meeting your obligations:

Members need to provide their employer with SMSFs: Australian Business Number Fund’s bank BSB and account number Electronic service address

Superannuation & SMSFs - An industry overview

4. Superstream

Meeting your obligations: If your employer does not have all the details to send

contributions to your SMSF electronically, they can ask request that you complete a standard choice form within a reasonable period of time (for example, within 28 days).

If you do not provide them with a completed form, your employer may direct contributions made on your behalf to the employer's default fund.

Superannuation & SMSFs - An industry overview

5. Other – Penalty units

Penalty units to increase from $170 to $180 meaning trustees breaching sections 65, 67 and 84 may be penalised $10,800

Changes to ATO approved auditors report

Superannuation & SMSFs - An industry overview5. Other – Pension changes

Proposed that from 1 July 2017 the following changes will be made to the asset test for the Age Pension

Pensioner type Current – Lower Threshold

Proposed – Lower Threshold

Current – max cut off limit

Proposed – max cut off limit

Single Homeowner

$202,000 $250,000 $755,500 $547,000

Single non-Homeowner

$348,500 $450,000 $922,000 $747,000

Couple Homeowner

$286,500 $375,000 $1,151,500 $823,000

Couple Non-Homeowner

$433,000 $575,000 $1,298,000 $1,023,000

6. What has not changed

No changes to the LRBA requirements i.e. Financial Systems Enq. No change to taxation of income derived by superannuation

funds in either the pension or accumulation phase No change to taxation of pensions received by persons 60+ No change to contribution cap limits No change to taxation of lump sum benefit payments No change to deductibility rules for personal superannuation

contributions

Superannuation & SMSFs - An industry overview