sunil's recievable management at karvy

TRANSCRIPT

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 1/54

PROJECT REPORT

ON

“Comparative Study on Portfolio Construction at

Karvy computer share pvt ltd

BY

I.CHANDAN

(H.NO. 131209672213)

Submitted to the

OSMANIA UNIVERSITY

Hyderabad

Under the guidance of

Mr. VENU MADAV SIR

(ASST.PROF)

In partial fulfillment of the Award of degree of

MASTER OF BUSINESS ADMINISTRATION

MALLA REDDY INSTITUTE OF MANAGEMENT(Affiliated TO Osmania University)

DULLAPALLY, SECUNDERABAD

2009-2011

DECLARATION

I hereby declare that this project Report titled “ Comparative Study on

portfolio construction at karvy computershare pvt ltd” submitted by me to the

department of OSMANIA UNIVERSITY is a Bonafide Work undertaken by me and it is notsubmitted to any other university or institution for the award of any degree diploma/ certificate

or published any time before.

MRIM

` 1

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 2/54

I.CHANDAN

Ht.No. 131209672213

TABLE OF CONTENTS

S.NO. TITLE S.NO

CHAPTER-I

1.1. Introduction 02

1.2. Objectives 03

1.3. Need of Study 04

1.4. Scope 04

1.5. Limitations 05

1.6. Methodology 06

CHAPTER-II

2.1 Industry Profile 17

2.2 Company profile 24

MRIM

` 2

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 3/54

CHAPTER-III

3.1 DATA ANALYSIS AND INTERPRETATION 40

CHAPTER-IV

4.1. Findings 49

4.2. Suggestions 50

4.3. Conclusions 51

CHAPTER-V

5.1 Bibliography 53

MRIM

` 3

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 4/54

CHAPTER-1

INTRODUCTION

MRIM

` 4

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 5/54

RECEIVABLES MANAGEMENT

The term receivables are defined as ‘debt owned to the firm by customers arising from sale of goods o

services in the ordinary course of business’ . when a firm makes ordinary sale of good or services and

does not receive a payment, the firm grants credit and creates accounts receivables which could be

collected in the future receivable management is also called trade credit management. Thus, accounts

receivables represent an extension of credit to customer, allowing them a reasonable period of time in

which to pay for the goods receivable.

The objectives of receivables management is ‘to promote sales and profits until that point is reached

where the return on investment in further funding receivables is les than the cost of funs raised to

finance that addition credit. The specific cost and benefit which are relevant to the determination of th

objectives of the receivables management.

MRIM

` 5

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 6/54

OBJECTIVES OF THE STUDY

1. To understand important credit aspect of the organization as part of the study and there by

understand the changes in financial position.

2. To understand KARVY’S credit policies credit terms collection policies.

3. To identify the strength and weakness of the organization in relation to credit management.

4. To give a detailed account of the problem involved in management receivables of KARVY and

appropriate to help them to make informed decision.

MRIM

` 6

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 7/54

SCOPE OF THE STUDY

The scope and period of study is restricted to the following.

1. The scope is limited to the operations of the KARVY.

2. The information obtained from the primary and secondary data was limited

to the KARVY.

3. The key information performances indicated were taken from 2009-10.

4. Comparison analysis was done in comparison of sister units.

MRIM

` 7

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 8/54

LIMITAIONS OF STUDY

1. The study is confined to a period of last six years.

2. As most of the data is from secondary sources, hence the accuracy is limited

MRIM

` 8

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 9/54

METHODOLOGY

The study basically depends on:

1. PRIMARY DATA.

2. SECONDARY DATA.

PRIMARY DATA COCLLECTION

The information collected directly without any reference is primary data. In th

study it is mainly through concerned officers or staff member either

individually or collectively, the data includes.

1. Conducting personal interview with officers of the company.

2. Individual observation inference.

3. From the people who are directly involved with transaction of the firm.

SECONDARY DATA COLLECTIN

Study has been taken from secondary sources i.e, published annual report of

the company. Editing, classifying and tabulation of the data for this purpose

performance data of KARVY.

MRIM

` 9

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 10/54

CHAPTER-2

MRIM

` 10

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 11/54

COMPANY’S PROFILE

MRIM

` 11

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 12/54

COMPANY PROFILE

3. 1 MISSION OF KARVY :

Their mission is to be a leading, preferred service provider to our customer, and they aim T

achieve this leadership position by building an innovative, enterprising, and technology drive organizatio

which will set the highest standards of service and business ethics.

3.2 INTRODUCTION:

The birth of Karvy was on a modest scale in 1981. It began with the vision and enterprise of a sma

group of practicing Chartered Accountants who founded the flagship company Karvy Consultants Limite

We started with consulting and financial accounting automation, and carved inroads into the field of regist

and share accounting by 1985.Karvy Stock Broking Ltd is a member of National Stock Exchange (NSE), Th

Bombay Stock Exchange (BSE), and The Hyderabad Stock Exchange (HSE).

Karvy Stock Broking Limited, one of the cornerstones of the Karvy edifice, flows freely towar

attaining diverse goals of the customer through varied services. Creating a plethora of opportunities for th

customer by opening up investment vistas backed by research-based advisory services. Here, growth know

no limits and success recognizes no boundaries. Helping the customer create waves in his portfolio an

empowering the investor completely is the ultimate goal.It is an undisputed fact that the stock market

unpredictable and yet enjoys a high success rate as a wealth management and wealth accumulation optio

The difference between unpredictability and a safety anchor in the market is provided by in-depth knowledg

of market functioning and changing trends, planning with foresight and choosing options with care.

Karvy offers services that are beyond just a medium for buying and selling stocks and share

Instead they provide services which are multi dimensional and multi-focused in their scope. There are sever

advantages in utilizing their Stock Broking services, which are the reasons why it is one of the best in t

country.

Karvy offer trading on a vast platform; National Stock Exchange, Bombay Stock Exchange an

Hyderabad Stock Exchange. More importantly, they make trading safe to the maximum possible extent, b

accounting for several risk factors and planning accordingly. They are assisted in this task by their in-dep

research, constant feedback and sound advisory facilities. Their highly skilled research team, comprising

MRIM

` 12

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 13/54

technical analysts as well as fundamental specialists, secure result-oriented information on market trend

market analysis and market predictions. This crucial information is given as a constant feedback to the

customers, through daily reports delivered thrice daily; The Pre-session Report, where market scenario for th

day is predicted, The Mid-session Report, timed to arrive during lunch break, where the market forecast f

the rest of the day is given and The Post-session Report, the final report for the day, where the market and th

report itself is reviewed. To add to this repository of information, they publish a monthly magazine; Karvy;

The Fin polis; which analyzes the latest stock market trends and takes a close look at the vario

investment options, and products available in the market, while a weekly report, called; Karvy Baza

Baatein; keeps the investor more informed on the immediate trends in the stock market. In addition, the

specific industry reports give comprehensive information on various industries. Besides this, they also off

special portfolio analysis packages that provide daily technical advice on scrip for successful portfol

management and provide customized advisory services to help the investors to make the right financial mov

that are specifically suited to their portfolio.

To empower the investor further they have made serious efforts to ensure that their research calls a

disseminated systematically to all their stock broking clients through various delivery channels like ema

chat, SMS, phone calls etc.

In the future, their focus will be on the emerging businesses and to meet this objective, they hav

enhanced their manpower and revitalized their knowledge base with enhances focus on Futures and Optio

as well as the commodities business.

Respect for the individual:

Each and every individual is an essential building block of our organization.

We are the kilns that hone individuals to perfection. Be they our employees, shareholders or investors. We d

so by upholding their dignity & pride, inculcating trust and achieving a sensitive balance of their professiona

MRIM

` 13

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 14/54

and personal lives.

Teamwork:

None of us is more important than all of us.

Each team member is the face of Karvy. Together we offer diverse services with speed, accuracy and quality

to deliver only one product: excellence. Transparency, co-operation, invaluable an individual contribution fo

a collective goal, and respecting individual uniqueness within a corporate whole, is how we deliver again an

again.

Responsible Citizenship:

A social balance sheet is as rewarding as a business one.

As a responsible corporate citizen, our duty is to foster a better environment in the society where we live and

work. Abiding by its norms, and behaving responsibly towards the environment, is some of our growing

initiatives towards realizing it.

Integrity:

Everything else is secondary.

Professional and personal ethics are our bedrock. We take pride in an environment that encourages honesty

and the opportunity to learn from failures than camouflage them. We insist on consistency between works an

actions.

3.3 BOARD OF DIRECTORS:

1. Mr. C Parthasarathy

Chairman and Managing Director

MRIM

` 14

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 15/54

2. Mr. M Yugandhar

Managing Director

3. Mr. M S Ramakrishna

Director

4. Mr. Prasad V Potluri

Director

3.4 KARVY GROUPS OF COMPANIES ARE:

1) Karvy Consultants Ltd

2) Karvy Stock Broking Ltd

3) Karvy Investors Service Ltd

4) Karvy Computershare Pvt Ltd

5) Karvy Global Service Ltd

6) Karvy Commodities Broking Ltd

7) Karvy Insurance Broking Private Ltd

8) Karvy alliances

MRIM

` 15

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 16/54

1. KARVY CONSULTANTS LIMITED:

As the flagship company of the Karvy Group, Karvy Consultants Limited has always at remained t

helm of organizational affairs, pioneering business policies, work ethic and channels of progress.

Having emerged as a leader in the registry business, the first of the businesses that Karvy ventured int

company have now transferred this business into a joint venture with Computer share Limited of Austral

the world’s largest registrar. With the advent of depositories in the Indian capital market and the relationship

that Company have created in the registry business, Karvy believe that they were best positioned to ventu

into this activity as a Depository Participant. Karvy were one of the early entrants registered as Deposito

Participant with NSDL (National Securities Depository Limited), the first Depository in the country and the

with CDSL (Central Depository Services Limited). Today, Karvy service over 6 lakhs customer accounts

this business spread across over 250 cities/towns in India and are ranked amongst the largest Deposito

Participants in the country. With a growing secondary market presence, they have transferred this business

Karvy Stock Broking Limited (KSBL), their associate and a member of NSE, BSE and HSE.

2. KARVY STOCK BROKING LIMITED:

MRIM

` 16

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 17/54

Karvy Stock Broking Limited, one of the cornerstones of the Karvy edifice, flows freely towar

attaining diverse goals of the customer through varied services. Creating a plethora of opportunities for thcustomer by opening up investment vistas backed by research-based advisory services. Here, growth know

no limits and success recognizes no boundaries. Helping the customer create waves in his portfolio an

empowering the investor completely is the ultimate goal.

Karvy is a Member of National Stock Exchange (NSE), The Bombay Stock Exchange (BSE), and Th

Hyderabad Stock Exchange (HSE).

3. KARVY INVESTORS SERVICES LIMITED:

Merchant Banking- Recognized as a leading merchant banker in the country, Karvy are registered

with SEBI as a Category I merchant banker. This reputation was built by capitalizing on opportunities in

corporate consolidations, mergers and acquisitions and corporate restructuring, which have earned us the

reputation of a merchant banker. Raising resources for corporate or Government Undertaking successfully

over the past two decades have given us the confidence to renew company focus in this sector.

Karvy quality professional team and their work-oriented dedication have propelled company to offe

value-added corporate financial services and act as a professional navigator for long term growth of

companies clients, which includes leading corporate, State Governments, foreign institutional investors,

public and private sector companies and banks, in Indian and global markets.

4. KARVY COMPUTERSHARE PVT. LIMITED:

MRIM

` 17

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 18/54

Karvy have traversed wide spaces to tie up with the world’s largest transfer agent, the leadin

Australian company, Computer share Limited. The company that services more than 75 million shareholde

across 7000 corporate clients and makes its presence felt in over 12 countries across 5 continents has entere

into a 50-50 joint venture with KARVY.

Mutual Fund Services:

Karvy have attained a position of immense strength as a provider of across-the-board transfer agen

services to AMC’s, Distributors and Investors.

Nearly 40% of the top-notch AMC’s including prestigious clients like Deutsche AMC and UTI swe

by the quality and range of services that company offer. Besides providing the entire back office processin

Karvy provide the link between various Mutual Funds and the investor, including services to the distributo

the prime channel in this operation.

Issue Registry:

In company voyage towards becoming the largest transaction-processing house in the Indi

Corporate segment, KARVY have mobilized funds for numerous corporate, and emerged as the large

transaction-processing house for the Indian Corporate sector. With an experience of handling over 700 issue

Karvy today, has the ability to execute voluminous transactions and hard-core expertise in technolo

applications have gained company the No.1 slot in the business. Karvy is the first Registry Company

receive ISO 9002 certification in India that stands testimony to its stature.

Corporate Shareholder Services:

Karvy has been a customer centric company since its inception. Karvy offers a single platfor

servicing multiple financial instruments in its bid to offer complete financial solutions to the varying needs

both corporate and retail investors where an extensive range of services are provided with great volum

management capability

.

5. KARVY GLOBAL SERVICES LIMITED:

The specialist Business Process Outsourcing unit of the Karvy Group. The legacy of expertise an

experience in financial services of the Karvy Group serves us well as company enter the global arena with t

MRIM

` 18

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 19/54

confidence of being able to deliver and deliver well. Here company offers several delivery models on th

understanding that business needs are unique and therefore only a customized service could possibly fit t

bill.

KARVY is in re-engineering and managing processes or delivering new efficiencies, companyservice meets up to the most stringent of international standards.Providing productivity improvemen

operational cost control, cost savings, improved accountability and a whole gamut of other advantage

KARVY Operate in the core market segments that have emerging requirements for specialized services. The

wide vertical market coverage includes Banking, Financial and Insurance Services (BFIS), Retail a

Merchandising, Leisure and Entertainment, Energy and Utility and Healthcare.

6.KARVY COMMODITIES BROKING LIMITED:

At Karvy Commodities, they are focused on taking commodities trading to new dimensions of

reliability and profitability. They have made commodities trading, an essentially age-old practice, into a

sophisticated and scientific investment option.

Company enables trade in all goods and products of agricultural and mineral origin that include

lucrative commodities like gold and silver and popular items like oil, pulses and cotton through a well-

systematized trading platform. The technological and infrastructural strengths and especially the street-smart

skills make them an ideal broker. Their service matrix is holistic with a gamut of advantages, the first and

foremost being their legacy of human resources, technology and infrastructure that comes from being part of

the Karvy Group.

7. KARVY INSURANCE BROKING PRIVATE LIMITED:

At Karvy Insurance Broking Pvt. Ltd., they provide both life and non-life insurance products to ret

individuals, high net-worth clients and corporate. With the opening up of the insurance sector and with a larg

MRIM

` 19

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 20/54

number of private players in the business, they are in a position to provide tailor made policies for differe

segments of customers. In their journey to emerge as a personal finance advisor, they will be better positione

to leverage their relationships with the product providers and place the requirements of their custome

appropriately with the product providers. With Indian markets seeing a sea change, both in terms

investment pattern and attitude of investors, insurance is no more seen as only a tax saving product but also

an investment product. By setting up a separate entity, we would be positioned to provide the best of th

products available in this business to the customers.

KARVY have wide national network, spanning the length and breadth of India, further suppor

these advantages. Further, personalized service is provided here by a dedicated team committed in givin

hassle-free service to the clients.

8. KARVY ALLIANCES:

Karvy Computer share Private Limited is a 50:50 joint venture of Karvy Consultants Limited an

Computer share Limited, Australia. Computer share Limited is world's largest -- and only global -- sha

registry, and a leading financial market services provider to the global securities industry.

The joint venture with Computer share, reckoned as the largest registrar in the world, servicing over

million shareholder accounts for over 7,000 corporations across eleven countries spread across fi

continents. Computer share manages more than 70 million shareholder accounts for over 13,000 corporatio

around the world.

Karvy Computer share Private Limited, today, is India's largest Registrar and Share Transfer Age

servicing over 300 corporate and mutual funds and 16 million investors.

Distribution of Financial Products:

MRIM

` 20

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 21/54

The paradigm shift from pure selling to knowledge based selling drives the business today. With their wi

portfolio offerings, they occupy all segments in the retail financial services industry.

A 1600 team of highly qualified and dedicated professionals drawn from the best of academic an

professional backgrounds are committed to maintaining high levels of client service delivery. This hpropelled them to a position among the top distributors for equity and debt issues with an estimated mark

share of 15% in terms of applications mobilized, besides being established as the leading procurer in all publ

issues.

To further tap the immense growth potential in the capital markets they enhanced the scope of the

retail brand, Karvy – the Finapolis, thereby providing planning and advisory services to the mass affluen

Here they understand the customer needs and lifestyle in the context of present earnings and provide adequa

advisory services that will necessarily help in creating wealth. Judicious planning that is customized to me

the future needs of the customer deliver a service that is exemplary. The market-savvy and the ignora

investors, both find this service very satisfactory. The edge that they have over competition is their portfol

of offerings and their professional expertise. The investment planning for each customer is done with

unbiased attitude so that the service is truly customized on market trends, investment options, opinions etc.

Graph 3.1 Showing Milestones of Karvy

MRIM

` 21

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 22/54

Figure no. 3.1 Showing Steps to Stock Selection Process in Karvy

3.5 Portfolio Schemes of karvy :

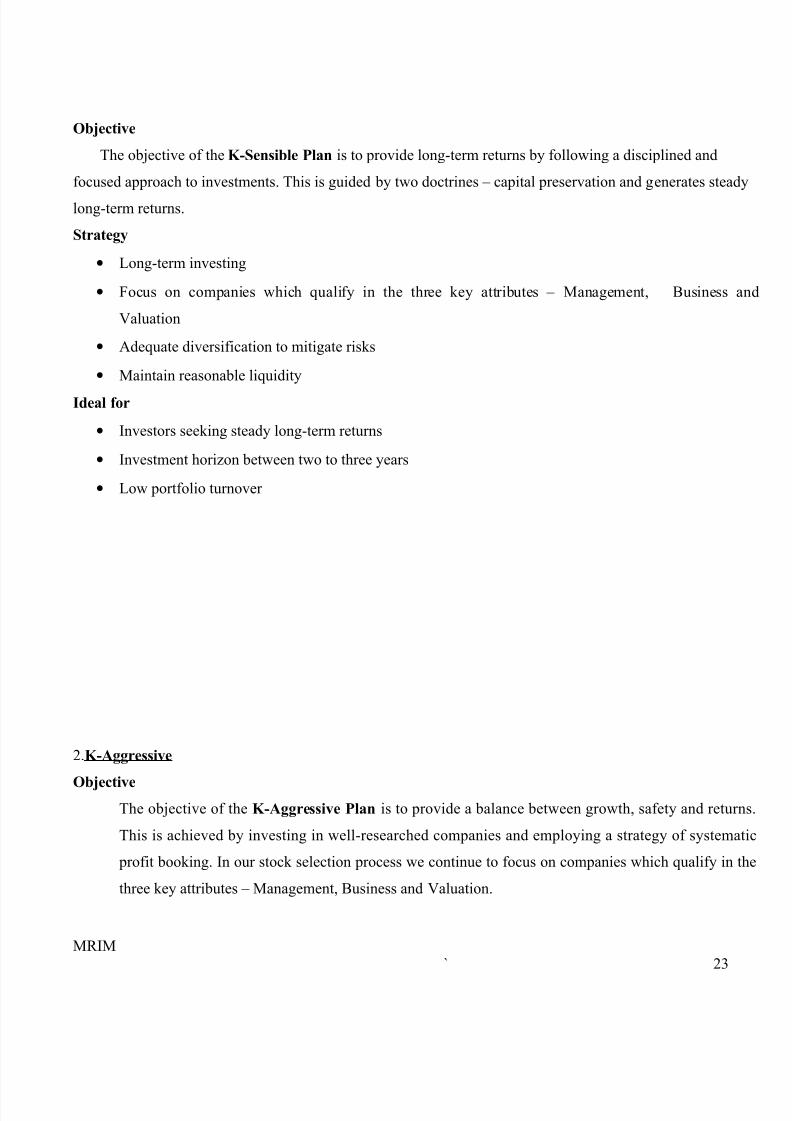

1. K-Sensible

MRIM

` 22

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 23/54

Objective

The objective of the K-Sensible Plan is to provide long-term returns by following a disciplined and

focused approach to investments. This is guided by two doctrines – capital preservation and generates steady

long-term returns.

Strategy

• Long-term investing

• Focus on companies which qualify in the three key attributes – Management, Business a

Valuation

• Adequate diversification to mitigate risks

• Maintain reasonable liquidity

Ideal for

• Investors seeking steady long-term returns

• Investment horizon between two to three years

• Low portfolio turnover

2.K-Aggressive

Objective The objective of the K-Aggressive Plan is to provide a balance between growth, safety and return

This is achieved by investing in well-researched companies and employing a strategy of systemat

profit booking. In our stock selection process we continue to focus on companies which qualify in th

three key attributes – Management, Business and Valuation.

MRIM

` 23

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 24/54

Strategy

• Medium to long-term investing

• Top-down and bottom-up approach

• Judicious mix of growth and value stocks

• Systematic profit booking

• Adequate diversification to mitigate risks

• Maintain reasonable liquidity

Ideal for

• Investors seeking gains from systematic profit booking

• Investment horizon between one to two years

• Medium portfolio turnover

3.K-Energetic

Objective

The objective of the K-Energetic Plan is to provide returns by following an aggressive

style of investing which entails higher risks.

Strategy

• Higher proportion of mid cap stocks

• Short to medium-term investing

MRIM

` 24

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 25/54

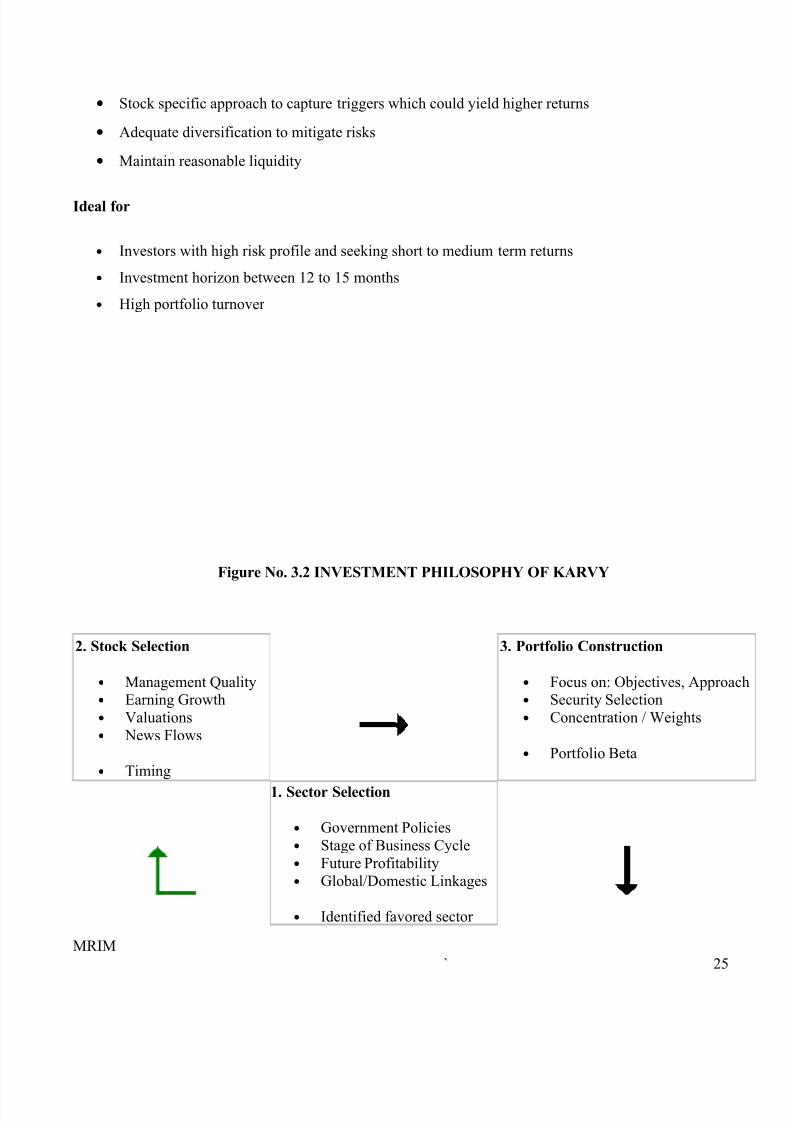

• Stock specific approach to capture triggers which could yield higher returns

• Adequate diversification to mitigate risks

• Maintain reasonable liquidity

Ideal for

• Investors with high risk profile and seeking short to medium term returns

• Investment horizon between 12 to 15 months

• High portfolio turnover

Figure No. 3.2 INVESTMENT PHILOSOPHY OF KARVY

2. Stock Selection

• Management Quality• Earning Growth

• Valuations

• News Flows

• Timing

3. Portfolio Construction

• Focus on: Objectives, Approac• Security Selection

• Concentration / Weights

• Portfolio Beta

1. Sector Selection

• Government Policies

• Stage of Business Cycle

• Future Profitability

• Global/Domestic Linkages

• Identified favored sector

MRIM

` 25

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 26/54

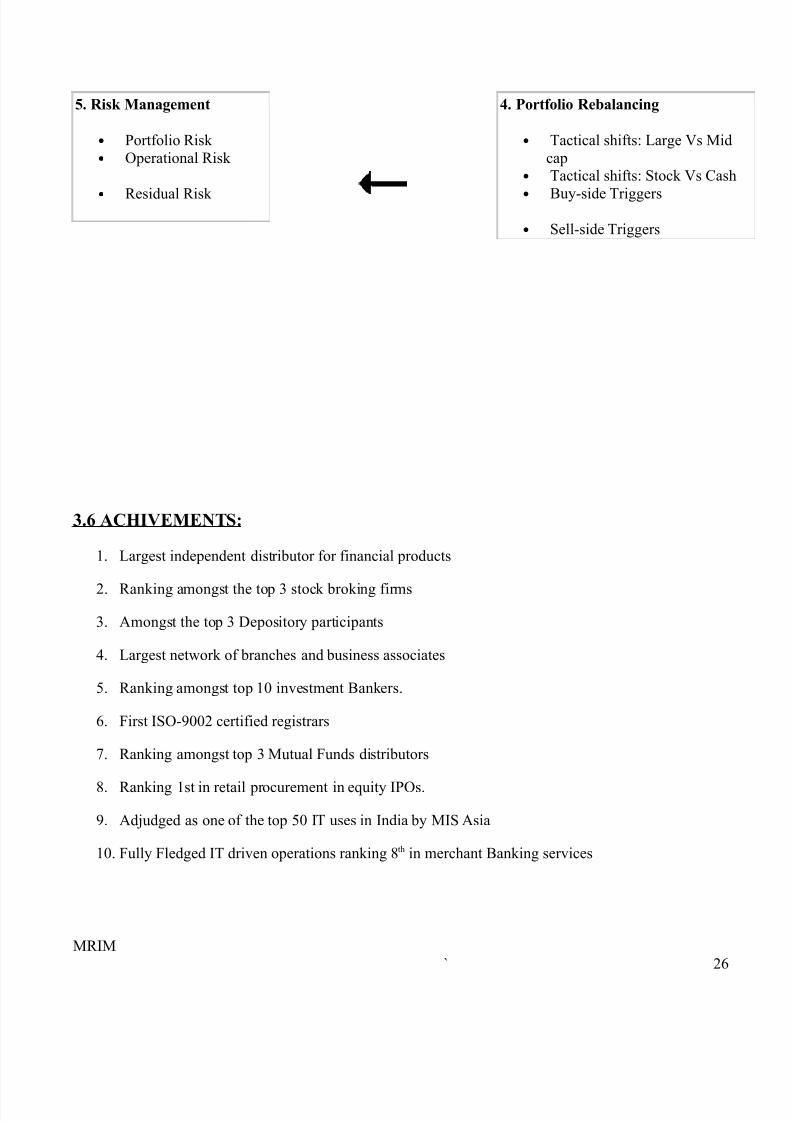

5. Risk Management

• Portfolio Risk

• Operational Risk

• Residual Risk

4. Portfolio Rebalancing

• Tactical shifts: Large Vs Mid

cap• Tactical shifts: Stock Vs Cash

•

Buy-side Triggers

• Sell-side Triggers

3.6 ACHIVEMENTS:

1. Largest independent distributor for financial products

2. Ranking amongst the top 3 stock broking firms

3. Amongst the top 3 Depository participants

4. Largest network of branches and business associates

5. Ranking amongst top 10 investment Bankers.

6. First ISO-9002 certified registrars

7. Ranking amongst top 3 Mutual Funds distributors

8. Ranking 1st in retail procurement in equity IPOs.

9. Adjudged as one of the top 50 IT uses in India by MIS Asia

10. Fully Fledged IT driven operations ranking 8 th in merchant Banking services

MRIM

` 26

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 27/54

CHAPTER-4

MRIM

` 27

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 28/54

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 29/54

Costs :

The major categories of cost associated with the extension of credit and accounts receivables

are :

1. Collection cost.

2. Capital cost

3. Delinquency cost

4. Default cost.

Collection cost :

Collection costs are administrative cost incurred in collection the receivables form the

customer to whom credit sales have been made included in this category of costs are

(A)additional expenses on the creation and maintenance of credit department with staff,

accounts records, stationery, postage and other related items; (B) expenses involved in

acquiring credit information either through outside specialist agencies or by the staff firm

itself.

Capital cost :

The increased level of accounts receivables is an investing in assets. They have to be

financial involving a cost. There is a time-lag between the sales goods to and payments

by, the customers, meanwhile, the firm has to pay employees and supplies of raw

materials, thereby implying that the firm should for additional funds to meet its own

obligations while for payment from its customers.

MRIM

` 29

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 30/54

Delinquency cost:

This cost arises out of the failure to meet their obligations when payments on credit

sales become due after the expiry of the credit period. Such costs are called delinquenc

cost. The important components of this cost are:1)blocking-up of funds for and

extended period.2)cost associated with steps that have to be initiated to collect the

overdue, such as reminders and other collection efforts, legal charges, where necessary

and so on.

Default cost :

The firm may not be able to recover the over dues because of the inability of the

customer. Such debts are treated as bad debts and have to be written off as they canno

be realized. Such costs are know has default cost associated credit sales and accounts

receivables.

Credit policies :

In the preceding discussion it has been clearly shown that the firm’s objective with

respect to receivables management is not merely to collect receivables quickly but

attention should also be given to the benefits-cost trade- off involved in the various

areas of accounts receivables management. The first decision area is credit policies.

The credit policies of a firm provides the framework to determine a)whether or not toextent credit to a customer and b) how much credit to extent. The credit policy decision

firm has two broad dimension.

i. Credit standards; and

ii. Credit analysis.

MRIM

` 30

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 31/54

Credit standards :

The term credit standards represents the basic criteria for the extension of credit to

customer. The quantitative basis of establishing credit standards are factors such a cred

rating, credit renerence. Average payments period and certain financial ratios. Since w

are interested in illustrating the trade-off between benefits and cost to the firm a whole

we do not consider here these individual components of credits standards. The trade-of

with reference to credit standards covers.

i. The collections cost .

ii. The average collection period/ investment in accounts receivables.

iii. Level of bad debt losses and

iv. Level of sales.

Collection costs :

The implication of relaxed credit standards are :

i. More credit.

ii. A large credit department to service receivable and related matters.

iii. Increase in collection cost.

Investment in receivables or the averagm collection period :

MRIM

` 31

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 32/54

The investment in accounts receivables involves a capital cost as funds to be arrange by

the firm to finance them customers make payments. Moreover, the higher the average

accounts receivables, the higher is the capital or carrying cost. A change in the credit

standards-relaxation or tightening –leads to a change in the level of accounts receivable

either.

a) Through a change in sales, or

b) Through a change is collections.

Bad debt expenses :

Another factor which is expected to the affected by change in the credit standards is ba

debt expense. They can be expected to increase with relation in credit standards and

decrease it credit standards become more restrictive.

Sales volume :

Change credit standards can also be expected to change the volume of sales. As

standards are relaxed, sales are expected to increase, conversely, a tightening is

expected to cause a decline.

Credit analysis :

Besides establishing credit standards, a firm should develop procedures for evaluating

credit application. The second aspects of credit policies of a firm are credit analysis andinvestigation. Two basic steps are involved in the credit investigation process.

a) Obtaining credit information, and

b) Analysis of credit information.

MRIM

` 32

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 33/54

Obtaining credit information :

The first step in credit analysis is obtaining credit information on which to have the

evaluation of a customer. The sources of information, broadly speaking are:

i. Internal.

ii. External.

Internal :

Usually, firm require their customer to fill various form and documents giving details

about finance operations. They are also required to furnish reference with whom the

firm can have contacts to judge the suitability of the customer for credit. The type of

information is obtained form internal sources of credit information. Another internal

sources of credit information is derived from the records of the firms contemplating an

extension of credit

External :

The availability of information from external sources to assess the creditworthiness of

customers depends upon the development of institution facilities and industry practicesin India, the external sources of credit information are not as development as in the

industrially advanced countries of the world.

MRIM

` 33

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 34/54

Financial statements :

one external sources of credit information is the published financial statements. That is

the balance sheet and loss account. Thm financial statements contain very useful

information they throw light on an application’s financial viability, liquidity,

profitability and debt capacity. Although the financial statement do not directly reveal

the past payment of the application. They are very helpful in assessing the overall

financial position of firm.

Bank references :

Another useful of credit information is the bank of the firm which is contemplating the

extension of credit, the modus operandi here is that the firm’s banker collects the necessary

information from the application’s bank. Alternatively, the applicant may be required to ask

his bankers to provide the necessary information either directly to the firm or to its bank.

Trade references:

These refers to the collection of the information from firms with whom the applicant has

dealing and who on the basis of their experience would vouch for the applicant.

Credit bureau reports :

Finally, specialist credit bureau repost from organization specializing in supplying credit

information can also be utilized.

MRIM

` 34

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 35/54

Analysis of credit information :

Once the credit information has been collected from different sources, it should be analyzed t

determine the credit-worthiness of the applicant. There are no established procedures to

analyze, the firm should devise one to suit its needs. The analysis should cover two aspects:

i. Quantitative. And

ii. Qualitative.

Quantitative:

The assessment of the quantitative aspects is based on the factual information available

from the financial statement, the past records of the from, so on. The first step involved

in this type of assessment is to prepare an Aging Schedule of the account payable of th

application as well as calculate the average age of the accounts payable. This exercise

will give an insight into the past payment pattern of the customer.

Qualitative :

The qualitative assessment should be supplemented by a qualitative subjective

interpretation of the application’s credit-worthiness . the subjective judgment would

cover aspects related to the quality of management. Here , the reference from other

suppliers, bank references and specialist bureau reports would form the basis for the

conclusion to be drawn.

MRIM

` 35

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 36/54

CREDIT TERMS :

The second decision in accounts receivable management is the credit terms. After the credit

standards been establishment and credit-worthiness of the customer has been assessed, the

management of a firm must determine the terms and conditions on which trade credit will be

made available. The stipulations under which goods are sold on credit are referred to as term

The credit term have three components.

1. Credit period, in terms of the duration of time for which trade credit extended-during

this period the overdue amount be paid the customer.

2. Cash discount, if any, which the customer can take advantage of, that is, the overdue

amount be reduce by this amount: and

3. cash discount period, which refers to the duration during which the discount can be

availed of.

Cash discount :

The cash discount has implications for the sales volume, average collection period/average

investment in receivables, bad debt expenses and profit per unit. In taking a decision regardinthe grant of cash discount, the management has to see what happens to the factors of if it

initiates increase, or decrease rate. The changes in the discount rate would both positive

effects. The implications of increasing or initiating cash discount are as follows.

i. The sales volume will increase. The grant of discount implies reduce prices. If the

demand for the produce for the products is elastic in price will result it higher sales

volume.

ii. Since the customers, to take advantage of the discount, would like to pay within the

discount period, the average collection period would be reduced. The reduced in the

collection period would lead to a reduction in the investment in receivable as also caus

fall in bad expense. As a results would increase

MRIM

` 36

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 37/54

iii. The discount would have a negative effect on the profile. This is because the decrease

in price would affect the profit margin per unit of sale

COLLECTION POLICIES :

The third areas involved in the accounts receivables management is collection policies

they refer to the procedures followed to collection accounts receivables when after the

expiry of the credit period, they become due. These policies cover two aspects :

1 Degree of effort to collect the over dues, and

2.Types of collection efforts.

Degree of collection effort :

To illustrate the effect of the collection effort, the credit policies of a firm may be

categorized into.

i. Strict/light, and

ii. Lenient.

The collection policies would be tight if rigorous procedures are following. A

tight collection policy has implications which involves as well as costs. The

management has to consider a trade-off. The effect of tightening the collection

is in the first place, the bad debt expense would decline. Moreover, the average

collection period will be increase. But there would negative effects also. A ver

rigorous collection strategy would involve increased collection costs. Yet

another negative effect may be in the decline in the volume of sales.

MRIM

` 37

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 38/54

Type of collection efforts :

The second aspect of collection policies relation to the steps that should be taken to

collection over dues from the customer. A well-established collection policy should

have clear- cut guidelines as to the sequence of collection efforts. After the period is

over and payment remains due, the firms should initiate measure to collection them.

The effort should in the beginning be polite , but, with passage of time should in thbeginning be polite, but with passage of tune,, it should gradually becomes strict.

The steps usually taken are :

Letters, including reminders, to expedite payment.

Telephone calls for personal contract.

Personal visits.

Help of collection agencies.

Legal action.

The Firm should take recourse to vary stringent measures, like legal action,

only after all other avenues have been fully exhausted. They not only involved

a cost but also affect the relationship with customers should be given due

consideration.

MRIM

` 38

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 39/54

Credit granting decision :

Once the firm has assessed the creditworthiness of a customer, it has to decide

whether or not credit should be granted. The firm should is the NPV rule to make th

decision. If the NPV is positive, credit should be granted and if the firm chooses not

to grant any credit, then it will benefit if the customer pays, there is probability that

the customer will default, then the firm may lose its investment. The expected net

payoff of the firm is the difference between the present value of net benefit and

present value of the expected.

MRIM

` 39

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 40/54

CHAPTER-6

MRIM

` 40

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 41/54

RECEIVABLEMANAGEMENT OF KARVY

MRIM

` 41

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 42/54

RECEIVABLES MANAGEMENT OF KARVY

There are regional operating divisions at various places, which are authorized by

KARVY to the credit amount from customer and deposit the same in the bank.

The ROD, which is nearest to the customer. Will go and collect from the customer.

The debtors are classified in to collectable debtors and deferred debtors collectable

debts are further classified in collectable as verified under verified old and withheld

collectable debts.

The collectable and deferred debts are(reviewed periodically may be fortnightly or

monthly. Such review will be done at the meeting where all department heads are

present.

During such meeting, the concerned of finance or head of commercial department

discuss the necessary steps to be taken to collect and reduce constrains. The actual

cash collected is compared with the budgeted and outstanding balances.

MRIM

` 42

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 43/54

PURPOSE OF RECEIVABLES :

If a firm insists on cash sales, the customer will not ready to purchase from firm

since he may not be in a position to pay the cash. So if the firm sells goods in credit

the customer may purchase more than that on cash. This is run will result in the

increase of profits. On the other hand, the credit is also offered to meet competition

the firm can easily attract customers by offering better credit facilities than

competitors.

MAINTENANCE OF RECEIVABLES :

Maintenance of receivables results in blocking of the financial resources in them. Thenfirm has to arrange for additional funds. Which can acquire from outside or from the

profits. In case of the later, the firm bears the opportunity cost of the amount invested the

firm incurs additional administrative costs for maintaining accounting records for

determining the payment due from credit customers and from dmfault customers.

The size of the accounted receivable depends on the level of sales, credit policies, terms o

trade. A firm having a large volume of sales will have large amount of receivables. The

terms are the credit period and cash discount.

TERMS OF CREDIT SALES :

MRIM

` 43

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 44/54

The second step in this regard is to decide terms of credit sales and the level of cash

discount. Cash discounts have important bearing on the cost of capital and credit sales.

CREDIT COLLECTION POLICY :

The management should provide for bad debts to keep the losses minimum. A collection

procedure should be estimated and action be taken accordingly. The other step should be t

record the age of debt to facilitate the collection of debts.

SIZE AND POLICY OF CASH DISCOUNT :

Credit and collection policy of the firm affected to the extent the amount of investment in

receivables. The sales department of the concern to who credit should be granted. If the

credit will be extended even to those customer whose credit worthiness is not known. If

credit policy is stringent the credit will be extended only on selective basis to those whose

credit worthiness is proven hence the size of receivable in the account will be lower.

Moreover, if collection is made within stipulated or a sound collection policy is enforced

e investment in receivable will naturally be lower.

MRIM

` 44

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 45/54

CHAPTER-7

MRIM

` 45

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 46/54

IMPORTANT RATIO IN

RECEIVABLMES MANAGEMENT

MRIM

` 46

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 47/54

IMPORTANT RATIOS &

RECEIVABLMES MANAGEMENT :

Ratio analysis is a widely used tool of financial analysis. It is

defined as the systematic use ratio to interpret the financial statement so that

strength and weakness of a firm as its historical performance and current financia

conditions can be determined.

1).DEBTORS TURNOVER RATIO : debtors turnover ratio expresses the

relationship between and net credit sales. It is calculated as…

NET CREDIT SALES

DEBTORS TURNOVER RATIO = ----------------------------------------------

DEBTORS TURNOVER RATIO

2). AVERAGE COLLECTION PERIOD :

Average collection period expresses the relationship between number of days in the year and

debtors turnover ratio. It is calculated as….

MRIM

` 47

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 48/54

NUMBER OF DAYS IN A YEAR

AVERAGE COLLETION PERIOD = ---------------------------------------------

DEBTORS TURNOVER RATIO

DEBTORS TURNOVERS RATIO

Years 2000-

2001

2001-

2002

2002-

2003

2003-

2004

2004-

2005

2005-

2006

2006-

2007

2007-

2008

Net

creditsales

13193

7

15351

9

13783

8

17449

0

17466

8

26721

7

28949

1

310235

Average

debtors

84880 85001 81237 82829 11223

8

13532

2

17730

1

215291

Ratio’s 1.55 1.81 1.69 2.10 1.55 1.97 1.63 1.44

(Table-3)

0

100000

200000

300000

400000

RATIO

2000-

2001

2002-

2003

2004-

2005

2006-

2007

YEARS

DEBTORS TURNOVER RATIO

Net credit sales

Average debtors

Ratio’s

(Graph-3)

NET CREDIT SLESDEBTORS TURNOVER RATIO = ----------------------------------------

AVERAGE DEBTORS

MRIM

` 48

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 49/54

Interpretation :

the KARVY company net sale is continuously increase and average debtors alsoincrease and the debtors turnover ratio is in 2009 to 2010 it is decrease .

AVERAGE COLLECTION PERIOD

Years 2000-

2001

2001-

2002

2002-

2003

2003-

2004

2004-

2005

2005-

2006

2006-

2007

2007-

2008

N of

days

365 365 365 365 365 365 365 365

Debtors

turnover

ratio

1.55 1.81 1.69 2.10 1.55 1.97 1.63 1.44

Ratio’s 235.4

8

201.6

5

215.9

7

173.8

0

235.4

8

185.2

7

223.9

2

253.47

(Table-4)

050

100150200250300350400

RATIO

2000-2001

2002-2003

2004-2005

2006-2007

YEARS

AVERAGE COLLECTION PERIOD N of days

Debtor sturnover ratioRatio’s

(graph-4)MRIM

` 49

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 50/54

AVERAGE NUMBER OF DAYS A YAER

COLLECTION PERIOD = -------------------------------------

DEBTORS TURNOVER RATIO

Interpretation :

The average collection period of Bhel Company is decrease when compare to th

2000 it is 235.48 and in 2008 it is 253.47. and the debt turnover ratio is also decrease i2000 it is 1.55 and in 2008 it is 1.44.

CHAPTER -8

MRIM

` 50

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 51/54

CONCLUSIONS & SUGGESTIONS

I have studied in detail the procedure followed by karvy for receivable management.

The follow are the aspects studied.

1. Continuous monitoring of debtor movement.

2. Coordination with regional managers regarding timely collection of debtors.

3. debtors turnover ratio in 2005-2006 is 1.97. the ratio has increased than previous year

expect 2003-2004 which was 2.10. the decrease in ratio shows the inefficient

management. They should concentrate more on collection of the debts.

MRIM

` 51

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 52/54

CHAPTER -9MRIM

` 52

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 53/54

BIBLOGRAPHY

FINANCIAL MANAGEMENT : PRASANNA CHANDRA

FINANCIAL MANAGEMENT : I.M.PANDEY

FINANCIAL MANAGEMENT : M.Y. KHAN & P.R.JAIN

ANNUAL REPORT OF BHEL

CASH & RECEIVABLE MANAGEMENT OF BHEL.

MRIM

` 53

8/7/2019 SUNIL'S RECIEVABLE MANAGEMENT AT KARVY

http://slidepdf.com/reader/full/sunils-recievable-management-at-karvy 54/54