successfully managing payment innovation...successfully managing payment innovation steve bernstein...

TRANSCRIPT

Successfully Managing

Payment Innovation

Steve Bernstein

Executive

Director

J.P. Morgan

Jeffrey Clennon

Director, Cash

Management

Discover

Karen Redwood

Director, Global

Core Payments

PayPal

Kristin Walle

VP, Global

Money

Movement &

Compliance

ADP

Karen Redwood Director, Global Core Payments

PayPal

PayPal Enables New Commerce

130+ million accounts

75% of online shoppers

C u s t om ers

$145B total payment volume/ 2012

$266M volume/day

B u y i n g P o we r Tr a f f i c

99% brand awareness

Brand Awareness: Q10. Aided Awareness: How familiar are you with each of the following? {Have you heard of brand} (N=550)

Comscore Mobile Wallet Study, April 2012: PayPal is #1 choice for smartphone purchases over Visa, MC, AMEX, Discover, Amazon Payments, Store branded cards, Google Wallet.

#1 for smartphone purchases

WORLD-CLASS SECURITY | FRAUD EXPERTS | 190 MARKETS | 25 CURRENCIES | 20 LANGUAGES

Digital Wallet > Mobile Wallet

• Any device or

operating

system

• Accessible

anywhere,

anytime

• Compatible with

and value-

creating for the

ecosystem

Card

Free

Mobile

Check-In NFC

Card

Mobile

Bar Code

Tablet 120+ million

Wallets in

the Cloud

5

Weekday Device Usage Patterns

MOBILE PHONES BRIDGES THE GAP

DESKTOP DOMINATES WORK

TABLETS RULE THE HOME

Mobile Payments a Reality Today at PayPal

0.1 0.8

4.0

14.0

20.0

2009 2010 2011 2012 2013E

PayPal Mobile Payment Volume ($US Billion)

275% COMPOUND

ANNUAL GROWTH

Requirements for Mobile Payments Success

Consumer &

Account Base

Merchant

Acceptance

FOOD MART

DRUG STORE

Pet Store

Barber Shop

Ecosystem

Partners

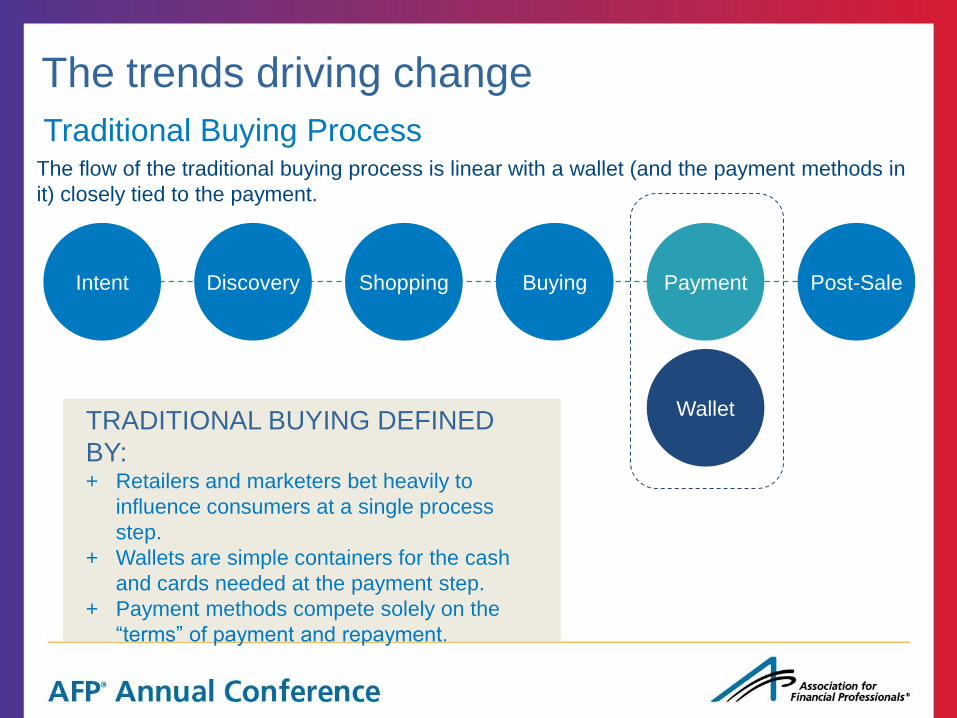

The trends driving change

Traditional Buying Process

Intent Discovery Shopping Buying Payment Post-Sale

Wallet

The flow of the traditional buying process is linear with a wallet (and the payment methods in

it) closely tied to the payment.

TRADITIONAL BUYING DEFINED

BY: + Retailers and marketers bet heavily to

influence consumers at a single process

step.

+ Wallets are simple containers for the cash

and cards needed at the payment step.

+ Payment methods compete solely on the

“terms” of payment and repayment.

‘Mashable’ Buying Process

Intent Discovery Shopping Buying Payment Post-Sale

The buying process is now reconfigured in an infinite number of ways, creating opportunity

for a “digital wallet” critical to each step of the process.

NEW COMMERCE DEFINED BY: + Fluid, non-linear process.

+ Retailers and consumers engaged in

constant conversation, no longer a locked

negotiation.

+ Old wallet, holding cash, is insufficient.

+ Smarter wallet provides capabilities to

facilitate and navigate process.

Wallet

The trends driving change

Mission Control Device

SEARCHING IN-

STORE

INSTANTLY BUYING CHECKING-IN

Consumer Driven approach

• Designing experiences that resonate with consumers

and merchants is critical to success

– Simple & easy

– Wallet as ‘holder’ of all payment options

• Technology is enabling giant steps forward in commerce

experience

• The world is getting smaller….Global payments

Kristin Walle VP, Global Money Movement & Compliance

ADP

Compliance Challenges

• Payments

• Tax

• Employment

How to solve for them?

Fragmented Systems

Co

mp

lex

ity

SOURCE: March 2010 NACHA , FIS and eCom Advisor research study

Lack of Business Intelligence

Finance Executives’ Strategies

Payments & Compliance Innovation

Jeffrey Clennon Director, Cash Management

Discover

M

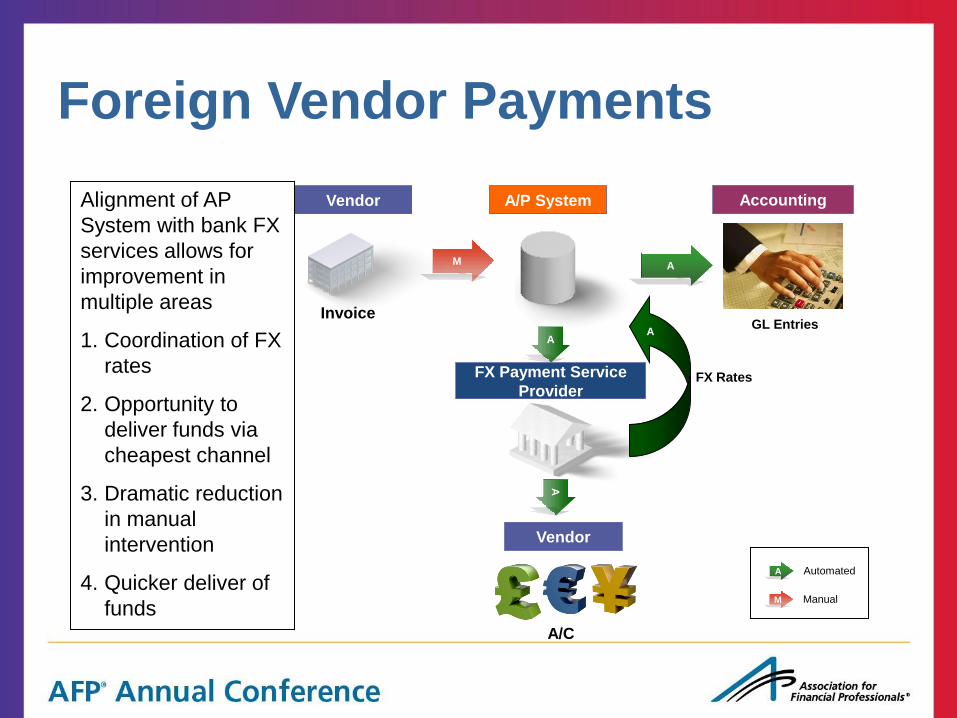

Foreign Vendor Payments

M A

Vendor

Invoice

A/P System Wire Report

M

Wire Request

Bank Wire Portal

Accounting Vendor

A/C FX Rates

M

• Foreign vendor

payments have

required

significant

manual

intervention

• Variety of FX rate

sources make

accrual recon

difficult

• Delays occur due

to differing

holiday calendars

Manual M

A Automated

Foreign Vendor Payments

M A

Vendor

Invoice

A/P System

FX Payment Service

Provider

Accounting

Vendor

A/C

FX Rates

A

A

Alignment of AP

System with bank FX

services allows for

improvement in

multiple areas

1. Coordination of FX

rates

2. Opportunity to

deliver funds via

cheapest channel

3. Dramatic reduction

in manual

intervention

4. Quicker deliver of

funds

A A A

GL Entries

M

A Automated

Manual

AribaPay

• Cloud-based service AribaPay will transform B2B payments by

eliminating paper transactions

• Provide buyers with a reliable and cost-effective way to create

purchase orders, receive invoices and send payments

• Discover’s transaction processing infrastructure will facilitate

electronic payments between buyers and sellers with more

detailed remittance information

• 100% electronic payments

• Limited release in the U.S. targeted for the first half of 2014

Discover & PayPal Partnership

• PayPal partnering with Discover to reach the physical POS

• Transactions governed by PayPal operating regulations and

program rules

• Acceptance of PayPal is seamless to participating merchants

• Discover serves as a 3rd Party service provider by leveraging its

U.S. merchant footprint

• Merchant payments executed on a straight through basis using

Discover technology

Steve Bernstein Executive Director, Transaction Services

J.P. Morgan

U.S. Payment Trends

• ACH and Check are the dominant payment methods – 82% of all

payments by value

• Wires dominate cross border payments – 69% of cross border

payments are wires and represent 12% of total payments by value

Sources – 2010 Federal Reserve Payments Study, and The Clearing House, Project Compass – Comprehensive Payments Study (2011)

US Transactions Volume

217 billion

US Transaction Value

$84,093 billion

Cash

Check

Debit/Prepaid Card

Credit Card

ACH

Wire

108 (50%)

24 (11%)

43 (20%)

22 (10%)

19 (9%)

$1,872 (2%)

$31,595 (38%)

$1,593 (2%)

$1,917 (2%)

$37,163 (44%)

$9,953 (12%)

Shift in Overall Payments Mix

• Check payment decline, 2000-2015

• Average yearly decline: -6.5%

• Aggregate decline: -49%

• The majority of volume migrated to ACH & Debit Card payments:

• ACH average yearly growth: 15%

• Debit Card average yearly growth: 15%

0

50

100

150

2000 2003 2006 2009 2012e 2015e

Check ACH Debit Credit

Source – 2010 Federal Reserve Payments Study and Company estimates

Global Payments

• 2011 Federal Reserve

Bank study:

– 2/3 of FIs process cross-

border transactions today,

as compared to only 1/3 in

2009

– Wire transfers remain the

most common cross-

border payment option

– 43% (and growing) utilize

cross-border ACH

payments

12%

86%

43%

39%

14%

69%

24%

48%

0% 50% 100%

Purchasing Card

Wire

ACH

Check

Global Payment Types 2009 2011

Global ACH Networks

Accessibility to global

ACH networks

continues to expand

Key Hurdles for Global Adoption

• Integration

– Integration with a global solution delivery state

– Need to have similar look/feel for U.S. and beyond for

on-boarding and customer experience

– Critical need for straight-through processing

• Incorporating future state opportunities

– Mobile payment adoption and integration

– Working with payment systems across the globe

– Integration with all payment players, e.g. Paypal,

Square, Western Union, Intuit, Google, etc.

Integrated Solutions

• Single file for initiating mixed

payments including:

– US Wire

– Domestic ACH

– Cross Border ACH

– Foreign Exchange

– Check Print

• Standard electronic formats

– EDI: ANSI X12, UN/EDIFACT

– ERP integration: SAP IDoc/XML

• Communications and data security

– Leased-line, internet, VAN, Internet

– Authentication, encryption

Wire

Transfers

US

ACH

Global

ACH FX

Check

Payment Services

Client

EDI

•ANSI X12

•EDIFACT

•XML

Proprietary

•GFF

•CSV

•Client-Specific

ERP

•SAP iDoc

(PEXR2002)

•SAP iDoc XML

Connectivity & Translation

Network Connection,

Transport & Security

• Internet

• SWIFTNet

• VAN

• Leased Line

• IP VPN

Translation

• Authentication

• Validation

• Reformatting

• Distribution

Financial Institution

ISO 20022

• Next-generation of financial services industry messaging

standards addressing all service domains including

Payments, Security, Card, FX and other

• Partnership between multiple standards organizations

including SWIFT, IFX, OAGi, X9, and TWIST

• Enables efficient and consistent communications

between corporations and banks facilitating payment

straight-through processing (STP)

• Implemented by financial application providers (SAP,

Oracle) for use when interfacing ERP & treasury

applications with banks.

ISO 20022 Integration with SAP

• Have worked with SAP to develop an “adapter” which

when used in conjunction with SAP’s Payment Medium

Workbench (PMWB) utility, enable SAP to produce CGI

compliant pain.001 v3 payment and pain.008 v2 direct

debit ISO 20022 messages.

• Advantages of this ERP integration approach include:

– Significantly reduced tech resource and time required to deploy

CGI compliant corporate to bank interfaces

– Minimal configuration to address bank-specific formatting

requirements (per bank’s CGI specs)

– Official SAP sourced ISO 20022 CGI compliance

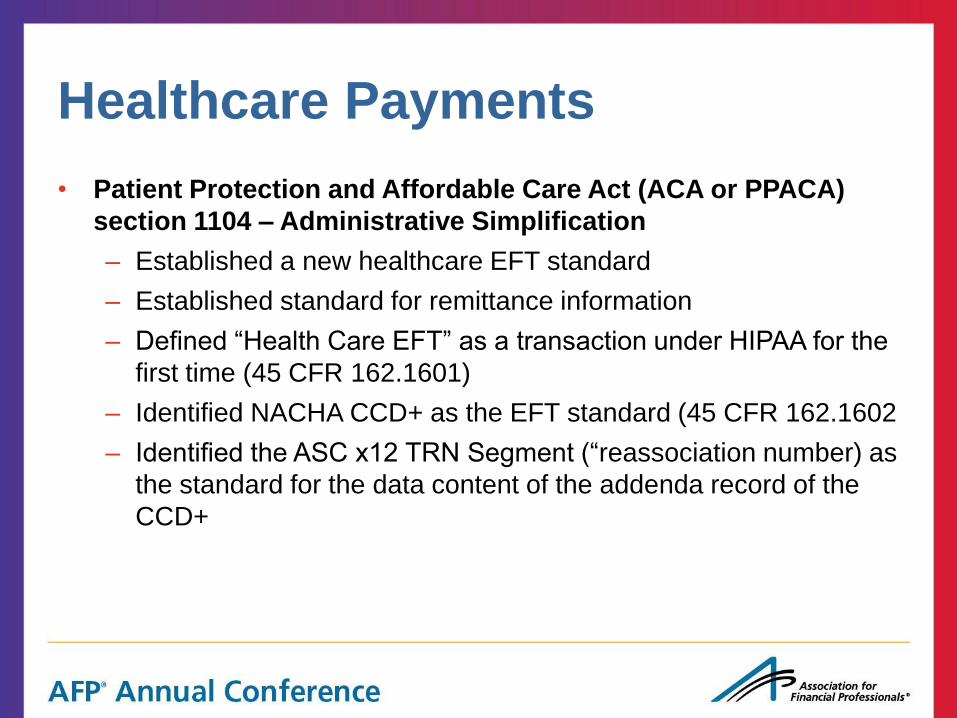

Healthcare Payments

• Patient Protection and Affordable Care Act (ACA or PPACA)

section 1104 – Administrative Simplification

– Established a new healthcare EFT standard

– Established standard for remittance information

– Defined “Health Care EFT” as a transaction under HIPAA for the

first time (45 CFR 162.1601)

– Identified NACHA CCD+ as the EFT standard (45 CFR 162.1602

– Identified the ASC x12 TRN Segment (“reassociation number) as

the standard for the data content of the addenda record of the

CCD+

Healthcare Payments

• The CCD+Addenda must contain the TRN Reassociation Trace

Number data segment as defined by ASC X12 version 005010 835

Implementation Guide

* * * \

Supporting Healthcare Clients

• Financial Institutions with health plan and provider clients are

making adjustments to support their clients’ implementation of the

mandated Healthcare EFT Standard, NACHA Operating Rule

changes and the EFT & ERA Operating rules

• Examples of what your bank may be doing include:

– Educating staff on the new standard and operating rules and

what is required of financial services

– Dedicating extra implementation support to ensure seamless

transitions for clients

– Upgrading products and services to support transaction flow and

compliance

– Identifying options to provide reassociation data to provider

clients

65%

73%

77%

85%

45%

63%

71%

75%

0% 50% 100%

2004

2006

2008

2009

Cell Phone Ownership Teens Adults

Mobile Trends

• Mobile payments are on the

rise

– 85% of all adults & 75% of

teenagers have a mobile

phone

– 20% of consumers who own

an Internet-capable mobile

phone had used the device

within the past 30 days to

pay bills through a financial

institution or a biller Web

site

SOURCE: March 2010 NACHA , FIS and eCom Advisor research study

Mobile Trends

• Those with the newest touchscreen Smartphones are

more likely to make purchases via their mobile phones

SOURCE: March 2010 NACHA , FIS and eCom Advisor research study

0%

10%

20%

30%

40%

50%

60%

70%

80%

Apps Songs Video Games Ringtones Online Store Purchase

Picture / Image

Food Movie Tickets

Mobile Purchase Trends by Phone Type

Basic Phone Non-Touch Smartphone Touchscreen Smartphone

Mobile Innovation

Chase QuickPay

• Online platform that enables

electronic payments between

two parties (Chase or non-Chase)

using only an email address.

• The parties involved do not share

personal financial information

(i.e. account numbers)

Mobile Innovation

Square & GoPayment

• Accept credit card payments on Android,

iPhone or iPad devices using card

reader accessory

• Funds from transactions are

deposited via ACH into a linked bank

account the next business day

• Card numbers and security codes are

not stored on devices

• Data is encrypted and transmitted

for processing via SSL and PGP

Mobile Security

Apple TouchID

• Fingerprint identity sensor built into the

new iPhone that can be used to unlock

the phone rather than using a passcode

• Fingerprints can also approve purchases

from iTunes Store, the App Store and the

iBooks Store

• Future: potential replacement for hard /

soft tokens and passwords enhancing

security on-the-go.

Mobile Payables Innovation

Business to Consumer Payments

• Gives businesses an electronic

payment alternative which

dramatically reduces payment

costs while overcoming electronic

migration constraints.

– Coordination costs of exchanging

bank account information

– Transmitting payment remittance

details to consumers

Originator J.P. Morgan ACH Network RDFI / Receiver

Payables Innovation

Artificial Intelligence

• Transaction scanning engine coupled with a collection of relational

databases which together reduce returns by correcting transactions

before they are processed through the ACH Network.

3

! 2

1

Payment

Receipt

Payment

Origination

Payment

Clearing Scanning

Receivables Innovation

Virtual Reference Number

• Consolidate electronic payment types into a single demand deposit

account (DDA) and manage this information centrally.

• Reference numbers are available to assign at your discretion to your

remitters. This improves matching rates and reduces exceptions.

• Balances are concentrated into a single master account. Reference

number to payer ID is a one-to-one match. You also gain greater

visibility across your receivables.

• Visibility on receipts helps you facilitate faster decision making when

releasing goods or extending credit to payers.

Receivables Innovation

eLockbox Transaction Repair

• Receive transactions that do not meet the edit/validation instructions

and correct these transactions securely online

• Minimize future exceptions, as any updates can be "remembered“

and applied to any incoming subsequent transactions, automatically

correcting them

!

Customers Financial Institution Client

How to Reengineer The Payments

Process • Considerations

– Understand all payment flows by analyzing payment mix, i.e., Check, Card, ACH

– Benchmark current payment practices to industry

– Recognize customer preferences such as risk, timeliness, cost

• Demographics

– Maturity and flexibility of customers

– Develop payment goals and plan to achieve

• Drivers

– New technologies and trends

– Industry-specific regulatory requirements and trends

Q&A

Steve Bernstein

J.P. Morgan

(212) 552-7960

Jeffrey Clennon

Discover

(224) 405-2868

Karen Redwood

PayPal

(408) 967-4532

Kristin Walle

ADP

(909) 394-6814