strong execution driving growth and value

TRANSCRIPT

S C O T I A H O W A R D W E I L 2 0 1 8 E N E R G Y C O N F E R E N C E

Strong Execution DrivingGrowth and Value

Monday, March 26, 2018, New Orleans

Forward-looking andCautionary Statements

Forward-looking Statement: All statements, other than statements of historical fact, appearing in this presentation constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements include, among other things, statements about our expectations, beliefs, intentions or business strategies for the future, statements concerning our outlook with regard to the timing and amount of future production of oil, natural gas liquids and natural gas, price realizations, the nature and timing of capital expenditures for exploration and development, plans for funding operations and drilling program capital expenditures, the timing and success of specific projects, operating costs and other expenses, proved oil and natural gas reserves, liquidity and capital resources, outcomes and effects of litigation, claims and disputes and derivative activities. Forward-looking statements may include words such as anticipate, believe, could, estimate, expect, forecast, foresee, intend, may, plan, potential, predict, project, seek, will, or other words or expressions concerning matters that are not historical facts. These statements involve certain risks and uncertainties that may cause actual results to differ materially from expectations as of the date of this presentation. Except as otherwise disclosed, the forward-looking statements do not reflect the impact of possible or pending acquisitions, investments, divestitures or restructurings. The absence of errors in input data, calculations and formulas used in estimates, assumptions and forecasts cannot be guaranteed. We base our forward-looking statements on information currently available to us, and we undertake no obligation to correct or update these statements whether as a result of new information, future events or otherwise. Additional information regarding our forward-looking statements and related risks and uncertainties that could affect future results of Energen, can be found in the Company’s periodic reports filed with the Securities and Exchange Commission and available on the Company’s website (www.energen.com).

Cautionary Statements: The SEC permits oil and gas companies to disclose in SEC filings only proved, probable and possible reserves that meet the SEC’s definitions for such terms, and price and cost sensitivities for such reserves, and prohibits disclosure of resources that do not constitute such reserves. Outside of SEC filings, we use the terms “estimated ultimate recovery” or “EUR,” reserve or resource “potential,” “contingent resources” and other descriptions of volumes of non-proved reserves or resources potentially recoverable through additional drilling or recovery techniques. These estimates are inherently more speculative than estimates of proved reserves and are subject to substantially greater risk of actually being realized. We have not risked EUR estimates, potential drilling locations, and resource potential estimates. Actual locations drilled and quantities that may be ultimately recovered may differ substantially from estimates. We make no commitment to drill all of the drilling locations that have been attributed these quantities. Factors affecting ultimate recovery include the scope of our ongoing drilling program, which will be directly affected by the availability of capital, drilling, and production costs, availability of drilling and completion services and equipment, drilling results, lease expirations, regulatory approvals, and geological and mechanical factors. Estimates of unproved reserves, type/decline curves, per-well EUR, and resource potential may change significantly as development of our oil and gas assets provides additional data. Additionally, initial production rates contained in this presentation are subject to decline over time and should not be regarded as reflective of sustained production levels.

2

Execution Continues to Deliver Superior Results

3

Strong Execution Leads to Excellent Results in 4Q17 4Q17 production beat guidance by 14% and surpassed 3Q17 by 20% 4Q17 oil production grew to 58.1 mbopd and exceeded guidance by 8% 4Q17 per-unit LOE and SG&A beat guidance midpoints by 10% and 9%, respectively CY17 production of 76.1 mboepd grew 39% from CY16 on strength of Generation 3

completions and increased activity level Additions replaced 415% of 2017 production, driving 40% increase in YE17 proved

reserves Updated inventory supports net undeveloped resource potential of 2.7 billion BOE

Gen 3 Pattern Wells Continue to Generate Outstanding Results Gen 3 performance drives strong IRRs through higher EURs and/or acceleration Updated type curves support superior economics 25 gross/21 net wells were turned to production in 4Q17; 64% were multi-zone

pattern wells completed in batches New wells reflect outstanding 24-hour and 30-day IP rates in Midland and Delaware

basins, with 4Q17 Delaware Basin wells generating average 24-hour IP rate of 402 boepd/1,000’ and average 30-day IP rate of 272/1,000’.

Results reflect Energen’s transformation into low-cost Permian pure-play with strong

foundation for profitable growth

Focus on Value Creation

4

Bringing Value Forward in CY18 Drilling & development capital estimated to range from $1.1B to $1.3B Plans include drilling approximately 130 gross/120 net horizontal wells and

completing approximately 123 gross/113 net horizontal wells (including 30 gross/28 net DUCs at YE17)

2018 YOY production growth estimated at 25% at guidance midpoint

3-Year Outlook Leverages Superior Economics to Further Drive Shareholder Value 3-year production CAGR expected to exceed 28% Annual production estimated to reach ≈160 mboepd in 2020, with 4Q exit rate of

≈170 mboepd Drilling & development capital estimated to increase to $1.6B-$1.8B in 2020 3-year EBITDAX CAGR estimated at approximately 35% Balance sheet ensures capital flexibility as net debt to EBITDAX estimated to remain

within 1.0x-1.5x each year

Three-year outlook reflects commitment to bringing forward NAV of high quality assets

while maintaining strong balance sheet

3Q17a 4Q17 Guidance 4Q17a

7.9 7.8 8.2

44.8 45.4 51.7

28.7 32.437.4

Central Basin/Other Midland Basin Delaware Basin

3Q17a 4Q17 Guidance 4Q17a

16.6 16.8 20.0

15.7 14.919.4

49.0 54.058.1

Gas NGL Oil

Another Production Beat in 4Q17

By Basin (mboepd) By Commodity (mboepd)

5

85.7

97.485.7

Total production up 14% over guidance and 20% over prior quarter Midland and Delaware Basin production each up approximately 14% over guidance Oil production up 8% over guidance and 19% sequentially

97.4

Note: Totals may not sum due to rounding

81.3 81.3

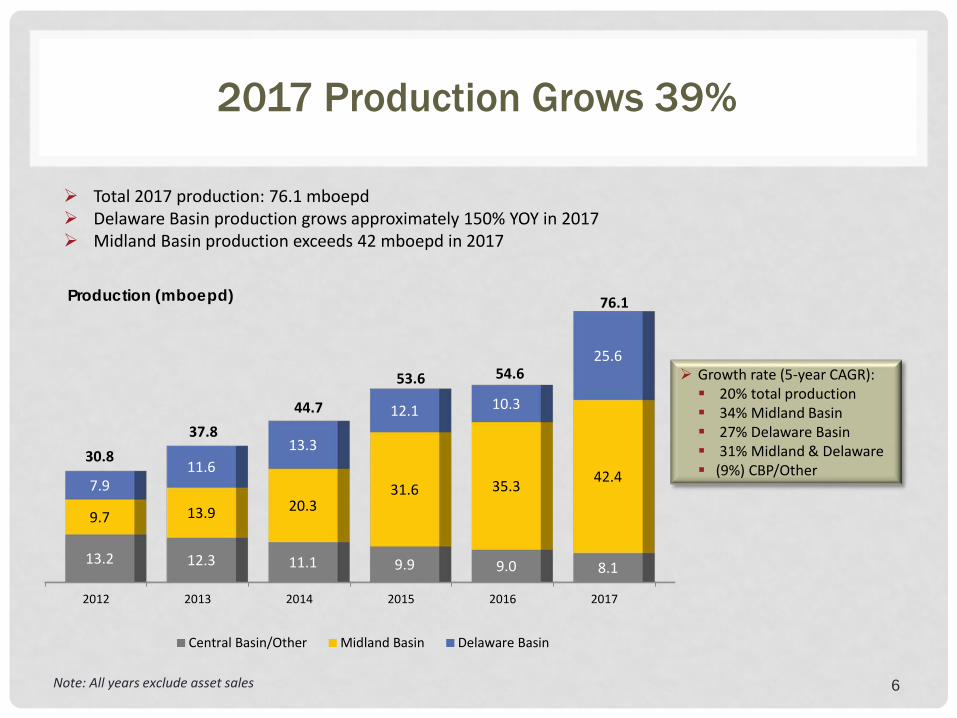

2017 Production Grows 39%

6

Total 2017 production: 76.1 mboepd Delaware Basin production grows approximately 150% YOY in 2017 Midland Basin production exceeds 42 mboepd in 2017

2012 2013 2014 2015 2016 2017

13.2 12.3 11.1 9.9 9.0 8.1

9.7 13.9 20.331.6 35.3 42.47.9

11.613.3

12.1 10.3

25.6

Central Basin/Other Midland Basin Delaware Basin

54.6

30.837.8

44.7

53.6

76.1

Growth rate (5-year CAGR): 20% total production 34% Midland Basin 27% Delaware Basin 31% Midland & Delaware (9%) CBP/Other

Production (mboepd)

Note: All years exclude asset sales

4Q17 Expenses Beat Guidance Midpoints

LOE ($/boe)

7

SG&A/boe down 9% from guidance SG&A/boe down 39% from 4Q16

LOE/boe down 10% from guidance LOE/boe down 23% from 4Q16

4Q16a 4Q17 GuidanceMdpt

4Q17a

$4.25

$2.85 $2.58

4Q16a 4Q17 GuidanceMdpt

4Q17a

$7.85

$6.70$6.02

* Per-unit LOE for Midland/Delaware basins totaled $4.94/boeNote: 4Q16a excludes asset sales

Net SG&A ($/boe)

($4.94*)

8

2016 2017

$6.23

$5.28

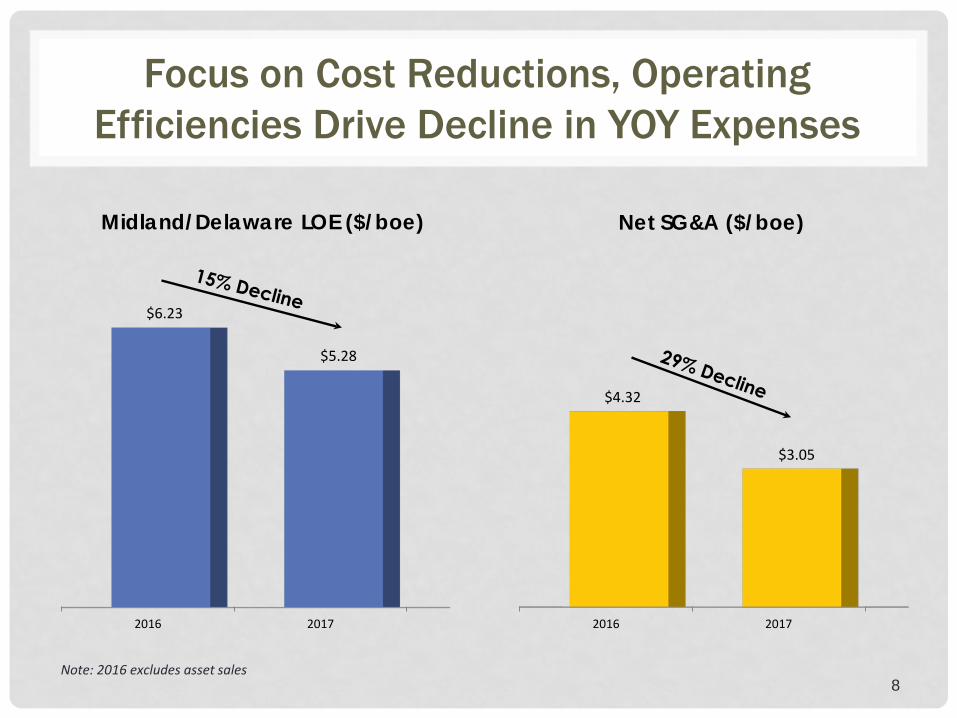

Focus on Cost Reductions, Operating Efficiencies Drive Decline in YOY Expenses

Net SG&A ($/boe)

2016 2017

$4.32

$3.05

Midland/Delaware LOE ($/boe)

Note: 2016 excludes asset sales

2017 Capitalization ($mm)

Net debt at YE16 $ 165

Plus: Total Capital Expenditures* $ 1,189

Less: After-tax Cash Flows $ 571

Net Debt at YE17 $ 783

Net Debt/EBITDAX at YE17 1.20

Cash at YE17 $ --

Amount outstanding on revolver at YE17 $ 255

Notes at YE17 $ 528

Undrawn borrowing base $ 795

2017 2018 2019 2020 2021 2022 2023+

$400

$20

$110

Maturity Schedule of Notes

* Includes $287 mm for leasehold, mineral acquisitions, and miscellaneous costs incurred during 2017

Corporate Debt Ratings

Moody’s: Ba3-StableS&P: BB-Stable

9

CY17 Ends with Strong Balance Sheet

Reserve additions replaced production by 415% 2017 proved developed F&D cost totaled $8.38 per boe1

Value of PDP reserves increased from $1.1B to $2.7B Delaware Basin proved reserves jumped 177% due to increased activity levels, Gen 3 performance, and higher pricing 3P and Contingent Resources totaled 3.0 billion BOE, up 33% from 2016

10

Proved Reservesby Basin YE16 Production Acq/(Div) Additions Price

RevisionsOther

Revisions YE17

Midland Basin 236.4 15.5 0.0 49.0 7.0 16.9 293.8Delaware Basin 39.1 9.4 0.2 66.3 0.9 10.9 108.1Platform/Other 40.9 3.0 0.0 0.1 3.7 0.4 42.1

TOTAL 316.3 27.8 0.2 115.5 11.6 28.2 444.0

Proved Reserves by Commodity 2017 2016

Oil 257 200Natural gas liquids 91 58Natural gas 96 58

TOTAL 444 316

Basin Proved Probable Possible Contingent Resources Total

Midland Basin 294 154 130 979 1,557Delaware Basin 108 40 46 1,243 1,437Platform/Other 42 0 0 1 43

TOTAL 444 194 176 2,223 3,037NOTE: Totals may not sum due to rounding

YE17 Proved Reserves Increase >40%

(mmboe)

YE17 Reserves Pricing: oil $51.34/barrel WTI; NGL (before T&F) $0.57/gallon; natural gas $2.98/mcf Henry Hub

1 Proved developed finding and development (F&D) cost per boe is defined as exploration and development costs divided by the sum of reserves associated with discoveries and extensions placed on production during 2017, transfers from proved undeveloped reserves at year end 2016, and revisions (excluding price-related revisions) of previous estimates of proved developed reserves in 2017.

Identified Inventory 4,023 Net Locations on 148,987 Net Acres

† Potential drilling locations as of 12/31/2017; engineered based on company’s acreage and spacing plans and may change materially overtime as the company and offset operators gain additional data in each zone; actual lateral lengths may vary depending on various factorsincluding lease geometry, relationship with offset operators, allowed spacing, reservoir characteristics, and other relevant criteria.

Dawson: 15

Howard: 229Martin: 805

Midland: 292 Glasscock: 868

Reagan: 195(Crockett: 5)Upton: 23

EGN Acres w/ Identified Horizontal Locations (YTD acquisitions, trades, increased WI shown in blue)Potential acreage addition of ≈10,000 net acres

11

Midland Basin (WC, SPB, Cline): 2,431 Net Locations† on 88,298 net acres

EGN Acres w/ Identified Horizontal Locations (YTD acquisitions, trades, increased WI shown in blue)

New MexicoTexas

Loving: 545Winkler:

35

Ward: 338

Reeves: 540

Lea: 135

Delaware Basin (WC, BS, Avalon, BC): 1,592 Net Locations † on 60,689 net acres

25 Wells Turned to Production in 4Q17

12

Area # Wells

Avg. Completed

Lateral Length

Avg. Peak 24-Hr IP Avg. Peak 30-Day IP

Boepd Boepd/ 1,000’ % Oil Boepd Boepd/

1,000’ % Oil

Delaware Basin 5 Wolfcamp A (4)3rd BS Sand (1) 6,297’ 2,529 402 74 1,716 272 73

N. Midland Basin 4 Wolfcamp A (2)Wolfcamp B (2) 7,548‘ 1,469 195 90 1,020 135 84

N. Midland Basin 5 Lower Spraberry 7,451‘ 1,779 239 93 1,425 191 90

N. Midland Basin * 9 Mid. Spraberry (5)Jo Mill (4) 7,964‘ 867 109 89 676 85 86

C. Midland Basin 2 Wolfcamp A 9,160‘ 1,766 193 91 1,159 126 82

Note: Excludes 2 test wells (one in Northern Midland Basin and one in Central Midland Basin) drilled in other formations

* Includes one Middle Spraberry well and one Jo Mill well turned to production in 3Q17 but not previously disclosed due to timing of first production

64% of wells turned to production in 4Q17 were multi-zone pattern wells completed in batches

2018 Delaware Basin ProgramType Curves, EURs Updated

0

50

100

150

200

250

300

350

400

450

500

550

600

0 30 60 90 120 150 180 210 240 270 300 330 360 390

Cum

ulat

ive

Prod

uctio

n (M

BOE)

Days

Prior Midpoint of Possible EURs Ryder Scott Composite Curve for 2018 Program Cessna 601H Avg Alameda Lease (6 Wells)Avg Goldfinger Lease (2 Wells) Avg New Mexico Well (1 WCA, 1 3rd Bone)2017 Gen 3 Wolfcamp A/B Avg (30 Wells)

Production and type curves normalized to 10,000’ 2017 Gen 3 avg. production (red line) includes operational downtime Individual well/lease production normalized for operational downtime Day 0 = first oil

New Ryder Scott Composite Curve for 2018 Delaware Basin program features 2.2 MMBOE EUR, up from prior midpoint of possible EURs of 1.75 MMBOE (59% oil).

Higher EURs and acceleration driving higher IRRs. Recent wells continue to show outstanding results, as does average of 30 Delaware Basin Gen 3 Wolfcamp A/B wells

brought on line in 2017 (red line); 50% are multi-zone pattern wells completed in batches.

# Wells: 30 29 27 26 19 19 17 16 9 3 2 2

13

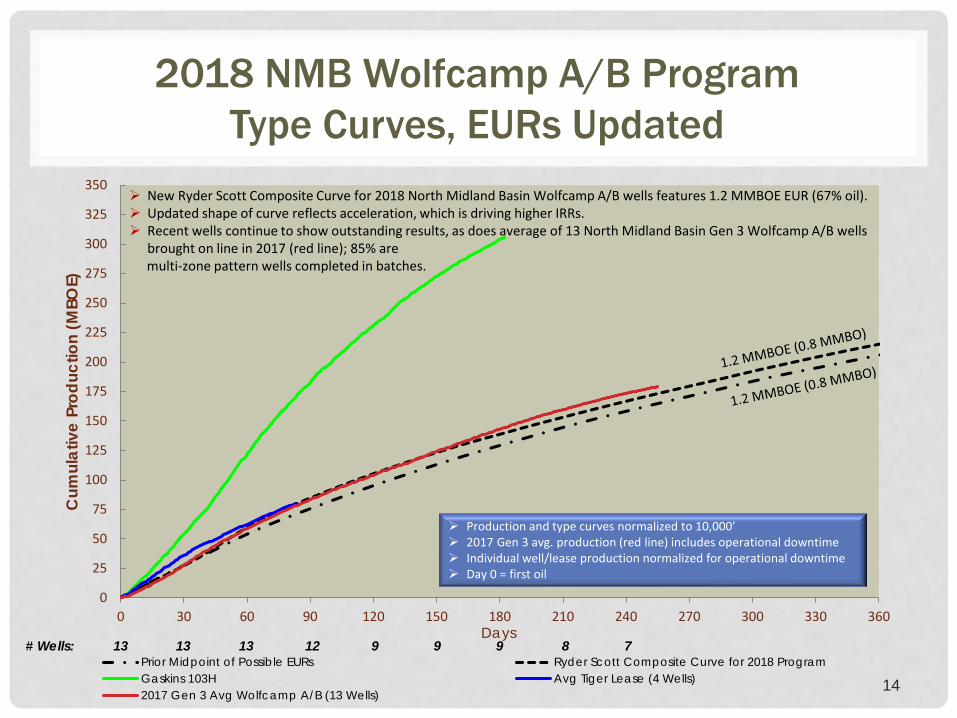

2018 NMB Wolfcamp A/B ProgramType Curves, EURs Updated

# Wells: 13 13 13 12 9 9 9 8 7

0

25

50

75

100

125

150

175

200

225

250

275

300

325

350

0 30 60 90 120 150 180 210 240 270 300 330 360

Cum

ulat

ive

Prod

uctio

n (M

BOE)

Days

Prior Midpoint of Possible EURs Ryder Scott Composite Curve for 2018 ProgramGaskins 103H Avg Tiger Lease (4 Wells)2017 Gen 3 Avg Wolfcamp A/B (13 Wells)

14

New Ryder Scott Composite Curve for 2018 North Midland Basin Wolfcamp A/B wells features 1.2 MMBOE EUR (67% oil). Updated shape of curve reflects acceleration, which is driving higher IRRs. Recent wells continue to show outstanding results, as does average of 13 North Midland Basin Gen 3 Wolfcamp A/B wells

brought on line in 2017 (red line); 85% are multi-zone pattern wells completed in batches.

Production and type curves normalized to 10,000’ 2017 Gen 3 avg. production (red line) includes operational downtime Individual well/lease production normalized for operational downtime Day 0 = first oil

0

25

50

75

100

125

150

175

200

225

250

275

300

0 30 60 90 120 150 180 210 240 270 300 330 360

Cum

ulat

ive

Prod

uctio

n (M

BOE)

Days

Prior Midpoint of Possible EURs Ryder Scott Composite Curve for 2018 ProgramAvg Tiger Lease (5 wells) 2017 Gen 3 Avg Lower Spraberry (9 Wells)

Production and type curves normalized to 10,000’ 2017 Gen 3 avg. production (red line) includes operational downtime Individual well/lease production normalized for operational downtime Day 0 = first oil

New Ryder Scott Composite Curve for 2018 North Midland Basin Lower Spraberry wells features 1.15 MMBOE EUR (73% oil).

Updated shape of curve reflects acceleration, which is driving higher IRRs. Recent wells continue to show outstanding results, as does average of 9 North Midland Basin Gen 3 Lower Spraberry

wells brought on line in 2017 (red line); 100% are multi-zone pattern wells completed in batches.

2018 NMB Lower Spraberry ProgramType Curves, EURs Updated

# Wells: 9 7 7 4 4 4 4 4 4 115

2018 NMB Middle Spraberry/Jo Mill ProgramType Curves, EURs

0

25

50

75

100

125

150

175

200

225

250

275

0 30 60 90 120 150 180 210 240 270 300 330 360

Cum

ulat

ive

Prod

uctio

n (M

BOE)

Days

Prior Midpoint of Possible EURs Ryder Scott Composite Curve for 2018 ProgramGaskins 803H Adams 601HAvg Tiger Lease (5 Wells) 2017 Gen 3 Avg MSprb/Jo Mill (14 Wells)

16

# Wells: 14 14 14 13 9 9 8 7 7 5 3

New Ryder Scott Composite Curve for 2018 North Midland Basin Middle Spraberry and Jo Mill wells features 1.3 MMBOE EUR (72% oil).

Higher EURS driving higher IRRs. Shape of curve adjusted to better reflect flowback profiles as compared to Lower Spraberry. Recent wells continue to show outstanding results, as does average of 14 North Midland Basin

Gen 3 Middle Spraberry and Jo Mill wells brought on line in 2017 (red line); 86% aremulti-zone pattern wells completed in batches.

Production and type curves normalized to 10,000’ 2017 Gen 3 avg. production (red Line) includes operational downtime Individual well/lease production normalized for operational downtime Day 0 = first oil

2018 CMB Wolfcamp A/B ProgramType Curves, EURs Updated

0

25

50

75

100

125

150

175

200

225

250

275

300

0 30 60 90 120 150 180 210 240 270 300 330 360 390 420

Cum

ulat

ive

Prod

uctio

n (M

BOE)

Days

Prior Midpoint of Possible EURs Ryder Scott Composite Curve for 2018 ProgramAvg Pecos Lease (6 Wells) Avg Moore 11-2 Lease (2 Wells)2017 Gen 3 Avg Wolfcamp A/B (12 Wells)

Production and type curves normalized to 10,000’ 2017 Gen 3 avg. production (red line) includes operational downtime Individual well/lease production normalized for operational downtime Day 0 = first oil

17

# Wells: 12 10 10 10 10 10 10 10 9 4 3 3 1

New Ryder Scott Composite Curve for 2018 Central Midland Basin Wolfcamp A/B wells features 1.3 MMBOE EUR(48% oil); Wolfcamp A has higher oil mix at 50% as compared with 41% for Wolfcamp B.

Higher EURS driving higher IRRs. Latest wells continue to show outstanding results, as does average of 12 Central Midland Basin

Gen 3 Wolfcamp A/B pattern wells brought on line in 2017 (red line); 83% aremulti-zone pattern wells completed in batches.

Attractive IRRs Support 2018 Program

0%20%40%60%80%

100%120%140%160%

$50 $60 $70NYMEX Oil $/bbl

-$1.0MM $8.3MM +$1.0MM

Gross EUR:1,650 mboe

18

10,0

00’ L

ater

al

0%20%40%60%80%

100%120%

$50 $60 $70NYMEX Oil $/bbl

-$1.0MM $6.8MM +$1.0MM

Gross EUR:915 mboe

0%10%20%30%40%50%60%70%80%

$50 $60 $70NYMEX Oil $/bbl

-$1.0MM $6.9MM +$1.0MM

Gross EUR:975 mboe

IRR

IRR

IRR

DB Wolfcamp A/B

0%20%40%60%80%

100%120%140%160%

$50 $60 $70NYMEX Oil $/bbl

-$1.0MM $10.8MM +$1.0MM

Gross EUR:2,200 mboe

NMB 5-Zone Average

0%20%40%60%80%

100%120%140%

$50 $60 $70NYMEX Oil $/bbl

-$1.0MM $8.3MM +$1.0MM

Gross EUR:1,200 mboe

CMB Wolfcamp A/B

0%10%20%30%40%50%60%70%80%

$50 $60 $70NYMEX Oil $/bbl

-$1.0MM $8.5MM +$1.0MM

Gross EUR:1,300 mboe

IRR

IRR

IRR

EURs based on Ryder Scott composite curves for 2018 program Gas and NGL prices held constant at $3/MMBTU and 35% of WTI, respectively

7,50

0’ L

ater

al

Estimated 2018 DC&E Cost

81%

13%

6%

Capital Breakdown*

Operated Drilling & DevelopmentFacilitiesNon-Operated/Other

19

2018 Drilling & Development Capital Estimated to Range from $1.1B - $1.3B

* Graphed at midpoint of capital guidance range

Drilling & Development Capital: $1.1B-$1.3B Hz new drills: approximately 130 gross/120 net wells Hz completions: approximately 123 gross/113 net wells, including 30

gross/28 net YE17 DUCs Hz DUCs at YE18: approximately 37 gross/35 net wells 7 gross/7 net vertical wells to be drilled (6 completions) Average of 8-10 drilling rigs and 4-5 frac crews Completed wells in 2018 program expected to have average lateral

lengths of ≈8,000’ and average working interests of ≈90%

2018 Horizontal Drilling Program Midland Basin: $550MM-$650MM

• Primary targets NMB: WC A/B, Spraberry package • Primary targets CMB: WC A/B

Delaware Basin: $550MM-$650MM• Primary targets: WC A/B

YOY Production Growth at Guidance Midpoint: ≈25% Annual production estimated to be 95.0 mboepd at midpoint

(range: 91.5-98.5 mboepd) Production estimated to range from 103.5-110.5 mboepd in 4Q Delaware Basin production estimated to grow 48% YOY

Note: 2018 capital plan assumes prices of $58/bbl WTI, $0.65/gal NGL (before T&F) and $2.75/mcf Henry Hub

50%

40%

10%

Capital by Area*

Delaware BasinNorth Midland BasinCentral Midland Basin

20

Production Estimated to Increase to103.5-110.5 MBOEPD in 4Q18

1Q18 2Q18 3Q18 4Q18

19.0 20.0 20.0 21.0

17.5 18.0 17.5 19.0

53.0 53.0 55.566.5

Production by Commodity*(mboepd)

Gas NGL Oil

107.0

93.091.089.5 2018 Operated Horizontal ProgramFirst Production/Flow Back (Gross/Net)

MidlandBasin

DelawareBasin

1Q18e 9/8 4/4

2Q18e 16/15 12/10

3Q18e 15/14 14/13

4Q18e 26/22 21/21

CY18e 66/58 51/48

* Guidance at midpoint

Note: Totals may not sum due to rounding

21

2018e YOY Production Growth: ≈25%

2013 2014 2015 2016 2017 2018e

12.3 11.1 9.9 9.0 8.1 7.0

13.9 20.331.6 35.3 42.4 50.011.6

13.3

12.1 10.3

25.6

38.0

Platform/Other Midland Basin Delaware Basin

76.1

95.0

54.653.6

44.737.8

Production (mboepd)

Five-year total production CAGR: approximately 20% Delaware Basin estimated to grow 48% YOY in 2018 (at guidance midpoint)

Note: Guidance at midpoint; all years exclude asset sales

Per BOE, except as noted 2018e 2017LOE (production costs, marketing & transportation) $6.40 - $6.60 $6.61Production & ad valorem taxes (% of revenues, excluding hedges) 6.2% 6.0%DD&A expense $14.00 - $14.50 $17.23Salaries and general & administrative expenses $2.30 - $2.70 $3.05Exploration expense (seismic, delay rentals, etc.) $0.15 - $0.20 $0.29Interest expense ($mm) $46.5 - $51.5 $38.4Effective tax rate (%) 22%-24% 37%

CY18e Salaries and G&A, net ($ per BOE) Total $2.30 - $2.70 Cash $1.85 - $2.05 Non-cash equity-based comp $0.45 - $0.65

22

Attractive Per-Unit Expenses Expected in 2018

CY18e LOE per BOE by Basin: Midland Basin $5.05-$5.25 Delaware Basin $5.35-$5.55 Central Basin Platform/Other $21.55-$21.75

2018e Capitalization ($mm)

Net debt at YE17 $ 783

Plus: Total Capital Expenditures $ 1,100 – 1,300

Less: After-tax Cash Flows $ 877

Net Debt at YE18 $ 1,006 – 1,206

Net Debt/EBITDAX at YE18† 1.1 – 1.3

Cash at YE18 $ --

Amount outstanding on revolver at YE18 $ 478 – 678

Notes at YE18 $ 528

Undrawn line of credit $ 372 - 572

Energen Maintains Strong Balance Sheet

2018 2019 2020 2021 2022 2023 2024+

$400

$20

$110

Maturity Schedule of Notes

Corporate Debt Ratings

Moody’s: Ba3-StableS&P: BB-Stable

23

† EBITDAX reflects hedges, known commodity prices, and assumed prices for unhedged volumes of $58.00/barrel (January-December), $0.65/gallon (January-December), and $2.75 per Mcf (February-December).

Strong financial position provides foundation for future growth and value creation

2018 - 2019 Hedges Help Minimize Risk

Hedge Volumes % Hedged 2 Avg. NYMEX

Price

Oil 3-way Collars¹ 13.5 mmbo 65%

Call Price $ 60.04/bbl

Put Price $ 45.47/bbl

Short Put Price $ 35.47/bbl

Oil Swaps 1.4 mmbo 7% $ 60.24/bbl

Commodity HedgeVolumes % Hedged 2 Avg. NYMEXe

Price

NGL 128.5 mm gal 46% $ 0.60/gal

Natural gas 9.0 bcf 20% $ 3.04/mcf

24

Energen also has hedged the Midland to Cushing differential on 11.1 mmbo (≈60%) of its estimated 2018 sweet oil production at an average price of $(1.03).

2018 2019

Energen also has hedged the Midland to Cushing differential on 6.1 mmbo of its estimated 2019 sweet oil production at an average price of $(0.75).

¹ When the NYMEX price is above the call price, Energen receives the call price; when the NYMEX price is between the call price and the put price, Energenreceives the NYMEX price; when the NYMEX price is between the put price and the short put price, Energen receives the put price; and when the NYMEXprice is below the short put price, Energen receives the NYMEX price plus the difference between the put price and the short put price.

2 Assumes midpoint of guidance

Commodity HedgeVolumes Avg. Price

NGL 55.4 mm gal $ 0.64/gal

HedgeVolumes

Avg. NYMEX Price

Oil 3-way Collars¹ 5.8 mmbo

Call Price $ 61.65/bbl

Put Price $ 45.94/bbl

Short Put Price $ 35.94/bbl

Oil Swaps 2.9 mmbo $ 56.52/bbl

Three-Year Outlook Drives Further Value

25

Outlook for 2018-2020 underscores Company’s commitment to bringing value forward by developing its top-tier Permian inventory and operating efficiently

Capital Drilling & development capital estimated to increase to $1.6B-$1.8B in 2020 Three-year plan assumes continuation of approximate 50/50 capital allocation between

Midland and Delaware basins

Balance Sheet

3-year production CAGR (at midpoint) estimated to exceed 28% Annual production estimated to exceed 160 mboepd in 2020 4Q exit rates expected to increase from 107 mboepd (at midpoint) in 2018 to approximately 135

mboepd in 2019 and 170 mboepd in 2020

Cash Flow

Production

Three-year plan assumes continuation of backwardated price environment with WTI oil prices of $58/bbl in 2018, $54/bbl in 2019 and $52/bbl in 2020

EBITDAX estimated to exceed $1.6B in 2020 for 3-year CAGR ≈35%

Growth occurs as Company continues to maintain already outstanding balance sheet Net debt to EBITDAX estimated to be within 1.0x-1.5x in each year

Providing Strong Platform for Value Creation as Permian Pure-Play

Solid execution leads to superior results in 2017

Continued execution in 2018-2020 drives growth and value

Oil-focused inventory > 4,000 net locations in key Permian Basin trends support net, undeveloped resource potential of 2.7 billion BOE

Top-tier asset base and return potential

$1.1B-$1.3B capital investment estimated for drilling and completion activities in 2018

3-year production CAGR expected to exceed 28% per year

Strong balance sheet helps ensure capital flexibility

26

Appendix

27

EGN Frac Design Evolution

Midland BasinGeneration 1

(2013-2015)• 1,250-1,400 lbs./ft proppant• 250’-300’ stage spacing• 30-40 bbls/ft fluid• 65’-75’ cluster spacing

Generation 2(2016)

• 1,600-1,700 lbs./ft proppant• 200’-225’ stage spacing• 40-42 bbls/ft fluid• 50’-55’ cluster spacing

Generation 3(2017-2018)

• 1,700-2,000 lbs./ft proppant• 150’ stage spacing• 40-45 bbls/ft fluid• 30’ cluster spacing

Delaware Basin

Generation 1(2012-2014)

• 1,000 lbs./ft proppant• 240’ stage spacing• 39 bbls/ft fluid• 50’ cluster spacing

Generation 2(2015)

• 1,330 lbs./ft proppant• 260’ stage spacing• 39 bbls/ft fluid• 65’ cluster spacing

Generation 3(2016-2018)

• 1,800-2,400 lbs./ft proppant• 200’ stage spacing• 40 bbls/ft fluid• 33’ cluster spacing

28

Premium Permian Basin Acreage

29

Energen’s Permian Footprint (12/31/2017)

Basin Gross Acres Net Acres

Delaware 93,897 62,313

Midland 118,922 95,105

Platform 116,334 82,578

Identified Net Potential @ 12.31.17Midland Basin: >1.3 Billion BOE

MidlandBasin

30% of identified locations (897 gross/717 net) have lateral lengths of 10,000’; average WI is 80% 18% of identified locations (451 gross/440 net) have lateral lengths of 10,000’; average WI is > 90%

27% of identified locations (938 gross/658 net) have lateral lengths of 6,700’ & 7,500’; average WI is 70%1 Potential drilling locations engineered to the longest lateral allowed by lease geometry or current/expected agreement based on Energen’s acreage and

spacing plans; may change materially over time as Energen and offset operators gain additional data in each zone; actual lateral lengths may vary depending on various factors including lease geometry, relationship with offset operators, allowed spacing, reservoir characteristics, and other criteria.

2 Reflects estimates of PUD, probable and possible reserves and contingent resources prepared by the company and reviewed by Ryder Scott; net of royalty interest of ≈25%. 30

334’

491’

388’

185’

266’

613’

637’

201’

387’

L. Spraberry Shale

DeanWolfcamp A

Wolfcamp B

Penn Shale

Cline

Wolfcamp C

M. Spraberry

Jo Mill

Net Operated Wells Drilled to Date

Net Acreage

Inventory:Engineered Locations1

(Gross/Net)

Remaining Horizontal Undeveloped Resource2

(Net MMBOE)

14 41,354 271/161 95

9 41,330 276/170 101

40 70,347 818/489 261

111 74,164 654/382 228

107 72,040 632/375 243

4 39,332 486/295 158

4 66,215 903/559 235

289 4,040/2,431 1,321

Identified Net Potential @ 12.31.17North Midland Basin: 695 MMBOE

L. Spraberry Shale

Dean

Wolfcamp A

Wolfcamp B

Penn Shale

Cline

M. Spraberry

Jo Mill

26% of identified locations (422 gross/343 net) have lateral lengths of 10,000’; average WI is 81% 18% of identified locations (245 gross/240 net) have lateral lengths of 10,000’; average WI is > 90%

25% of identified locations (441 gross/332 net) have lateral lengths of 6,700’ & 7,500’; average WI is 81%

Midland, Martin, Dawson& Howard Counties

Net Operated Wells Drilled to Date

Net Acreage

Inventory:Engineered Locations1

(Gross/Net)

Type CurveEUR per 1000’2

(Gross MBOE/MBO)

Remaining Horizontal Undeveloped Resource3

(Net MMBOE)

14 41,176 271/161 130/94 95

9 41,152 276/170 130/94 101

34 41,196 528/313 115/84 163

29 37,956 325/188 120/83 100

31 36,989 358/216 130/83 139

2 32,303 465/290 65/42 97

119 2,223/1,338 695

31

1 Potential drilling locations engineered to the longest lateral allowed by lease geometry or current/expected agreement based on Energen’s acreage and spacing plans; may change materially over time as Energen and offset operators gain additional data in each zone; actual lateral lengths may vary depending on various factors including lease geometry, relationship with offset operators, allowed spacing, reservoir characteristics, and other criteria.

2 Estimated gross EURs normalized to 1,000’ lateral lengths; based on various geological and engineering assumptions made by management using company and pubic data sources; EUR estimates may change materially over time as Energen and offset operators gain additional production data.

3 Reflects estimates of PUD, probable and possible reserves and contingent resources prepared by the company and reviewed by Ryder Scott; net of royalty interest of ≈25%.

249’

387’

405’

252’

243’

317’

374’

439’

Identified Net Potential @ 12.31.17Central Midland Basin: 626 MMBOE

34% of identified locations (475 gross/374 net) have lateral lengths of 10,000’; average WI is 79% 18% of identified locations (206 gross/200 net) have lateral lengths of 10,000’; average WI is > 90%

30% of identified locations (527 gross/326 net) have lateral lengths of 6,700’ & 7,500’; average WI is 62%

Glasscock, Upton & Reagan Counties

32

1 Potential drilling locations engineered to the longest lateral allowed by lease geometry or current/expected agreement based on Energen’s acreage and spacing plans; may change materially over time as Energen and offset operators gain additional data in each zone; actual lateral lengths may vary depending on various factors including lease geometry, relationship with offset operators, allowed spacing, reservoir characteristics, and other criteria.

2 Estimated gross EURs normalized to 1,000’ lateral lengths; based on various geological and engineering assumptions made by management using company and pubic data sources; EUR estimates may change materially over time as Energen and offset operators gain additional production data.

3 Reflects estimates of PUD, probable and possible reserves and contingent resources prepared by the company and reviewed by Ryder Scott; net of royalty interest of ≈25%.

334’

491’

388’

185’

266’

613’

637’

201’

387’

L. Spraberry Shale

DeanWolfcamp A

Wolfcamp B

Penn Shale

Cline

Wolfcamp C

M. Spraberry

Jo Mill

Net Operated Wells Drilled to Date

Net Acreage

Inventory:Engineered Locations1

(Gross/Net)

Type CurveEUR per 1000’2

(Gross MBOE/MBO)

Remaining Horizontal Undeveloped Resource3

(Net MMBOE)

6 29,150 290/176 105/85 98

82 36,208 329/194 130/65 128

76 35,050 274/159 120/49 104

4 37,285 486/295 100/54 158

2 33,912 438/269 95/43 138

170 1,817/1,093 626

30% of Wolfcamp locations (560 gross/330 net) have lateral lengths of > 10,000’; average WI is 59% 22% of locations (270 gross/242 net) have lateral lengths of > 10,000’; average WI is 90%

22% of Wolfcamp locations (316 gross/236 net) have average lateral lengths of approximately 7,500’; average WI is 75%

33

Identified Net Potential @ 12.31.17Delaware Wolfcamp Shale: >1.1 Billion BOE

1 Potential drilling locations engineered to the longest lateral allowed by lease geometry or current/expected agreement based on Energen’s acreage and spacing plans; may change materially over time as Energen and offset operators gain additional data in each zone; actual lateral lengths may vary depending on various factors including lease geometry, relationship with offset operators, allowed spacing, reservoir characteristics, and other criteria.

2 Estimated gross EURs normalized to 1,000’ lateral lengths; based on various geological and engineering assumptions made by management using company and pubic data sources; EUR estimates may change materially over time as Energen and offset operators gain additional production data.

3 Reflects estimates of PUD, probable and possible reserves and contingent resources prepared by the company and reviewed by Ryder Scott; net of royalty interest of ≈25%.

Wolfcamp Upper A

Wolfcamp B

Wolfcamp C

Wolfcamp A

Wolfcamp BC

Texas

325’

250’

325’

425’

Net Operated WellsDrilled to Date

NetAcreage

Inventory:Engineered Locations1

(Gross/Net)

Type CurveEUR per 1000’2

(Gross MBOE/MBO)

Remaining Horizontal Undeveloped Resource3

(Net MMBOE)

27 48,994 497/269 210/130 300

25 46,694 438/259 210/130 287

5 41,111 429/264 190/80 255

41,111 432/264 190/80 25357 1,796/1,057 1,095

Net Operated WellsDrilled to Date

NetAcreage

Inventory:Engineered Locations1

(Gross/Net)

Type CurveEUR per 1000’2

(Gross MBOE/MBO)

Remaining Horizontal Undeveloped Resource3

(Net MMBOE)

1 6,192 113/34 130/110 22Wolfcamp Upper AWolfcamp A

New Mexico

375’

3rd Bone Spring/WC XY Sand

3rd Bone Spring Shale

2nd Bone Spring Sand

2nd Bone Spring Shale1st Bone Spring Sand

Avalon

Lwr Brushy Canyon

Net Operated WellsDrilled to Date

NetAcreage

Inventory:Engineered Locations1

(Gross/Net)

Type CurveEUR per 1000’2

(Gross MBOE/MBO)

Remaining Horizontal Undeveloped Resource3

(Net MMBOE)32,396 82/26 110/90 13

5,395 121/31 100/55 15

40,004 35/12 100/80 5

2 48,094 122/41 100/80 19

51,515 413/310 110/80 162

120 57,314 163/80 100/80 36122 939/501 250

34

Identified Net Potential @ 12.31.17Delaware “Other” Plays: 250 MMBOE

795’

257’

316’

442’

609’

294’

226’

106’

Other Plays

1 Potential drilling locations engineered to the longest lateral allowed by lease geometry or current/expected agreement based on Energen’s acreage and spacing plans; may change materially over time as Energen and offset operators gain additional data in each zone; actual lateral lengths may vary depending on various factors including lease geometry, relationship with offset operators, allowed spacing, reservoir characteristics, and other criteria.

2 Estimated gross EURs normalized to 1,000’ lateral lengths; based on various geological and engineering assumptions made by management using company and pubic data sources; EUR estimates may change materially over time as Energen and offset operators gain additional production data.

3 Reflects estimates of PUD, probable and possible reserves and contingent resources prepared by the company and reviewed by Ryder Scott; net of royalty interest of ≈25%.

Bone Spring

25% of Other locations (203 gross/126 net) have lateral lengths of ≥10,000’; average WI is 62% 19% of locations (105 gross/96 net) have laterals lengths of ≥10,000’; average WI is 91%

16% of Other locations (107 gross/80 net) have average lateral lengths of approximately 7,500’; average WI is 75%

* Subject to change based on continued testing and analysis of spacing and frac designs

NOTE: Additional horizontal potential from other intervals such as Clearfork, Atoka/Barnett, Woodford

Inventory Spacing: Northern Midland Basin

3524

9’38

7’40

5’25

2’24

3’31

7’37

4’43

9’

Inventory Spacing per 640-acre Section*

Dean

Wolfcamp A

Wolfcamp B

4

4

8

6

6

8

1 Mile

249’

387’

405’

252’

243’

317’

374’

439’

NOTE: Additional horizontal potential from other intervals such as Clearfork, Middle Spraberry, Jo Mill 36

* Subject to change based on continued testing and analysis of spacing and frac designs

Inventory Spacing per 640-acre Section*

6

6-8

8

6-8

8

185’

266’

613’

637’

201’

387’

388’

1 Mile

Inventory Spacing: Central Midland Basin

37

Inventory Spacing per 640-acre Section*

* Subject to change based on continued testing and analysis of spacing and frac designs

6

6

6

6

417’

364’

344’

400’

Wolfcamp BC

1 Mile

Inventory Spacing: Delaware Basin WC Shale

Inventory Spacing: Delaware Basin “Other”

38

Inventory Spacing per 640-acre Section*

* Subject to change based on continued testing and analysis of spacing and frac designs

3rd Bone SpringShale

795’

257’

316’

442’

609’

294’

159’

106’

226’

6

4

4

6

4

4

1 Mile

Non-GAAP Financial Measures

Standardized Measure of Discounted Future Net Cash Flows Relating to Proved Oil and Natural Gas Reserves (GAAP) / PV-10 (non-GAAP):

The standardized measure of discounted future net cash flows (SMOG) is the Company’s GAAP estimate of the present value of future net revenues from proved oil and gas reserves after deducting estimated production and ad valorem taxes, operating expenses, development costs, and income taxes discounted at an annual rate of 10%. PV-10 is a non-GAAP measure that excludes the Company’s estimates of future income taxes (discounted at an annual rate 10%). The Company believes that PV-10 allows for additional comparability among companies in the oil and gas industry due to the unique factors that may impact thetiming of future income taxes to be paid. The Company also believes PV-10 to be important for evaluating the relative significance of its oil and gas properties and that the presentation of the non-GAAP financial measure of PV-10 provides useful information to investors because it is widely used by professional analysts and investors in evaluating oil and gas companies. The Company believes disclosing the year-over-year change in the PV-10 for Proved Developed Producing (PDP) reserves is a meaningful indication of the increase in value of the Company’s producing properties.

The following table reconciles the Company’s standardized measure of discounted future net cash flows (the most directly comparable measure calculated and presented in accordance with GAAP) to PV-10. PV-10 should not be considered as an alternative to the standardized measure as computed under GAAP.

39

($ in millions) 2017 2016

Standardized measure of discounted future net cash flows (GAAP) $3,320 $1,350

Add: Present value of future income taxes discounted at 10% $418 $147

PV-10 Total Proved reserves $3,738 $1,497

Less: PV-10 Proved Developed Non-Producing reserves $1,014 $349

PV-10 Proved Developed Producing reserves $2,724 $1,148

For More Information

Julie S. RylandVice President – Investor Relations

www.energen.com

40