strategy to double sales in china and group update to double sales in china and group update...

TRANSCRIPT

Investor DayStrategy to double sales in China and Group update

ShanghaiNovember 11, 2014

Investor Day

ShanghaiNovember 11, 2014

China MarketFaurecia China

Jingcheng LiNovember 11, 2014

China believes that a strong central government will lead to a powerful Nation based on its 5,000 year history

Investor Day – Shanghai – November 11, 2014 4

Foundation of the Republic of China

Foundation of CPC

Foundation of the People’s Republic of China

The 100th Anniversary of CPC

The 3rd Plenary Session of the 18th Central Committee of the CPC for “Deepening Reform”

The 100th Anniversary of the People’s Republic of China

People’s Republic of China: 100 Years Development

Communist Party of China: 100 Years Development

1911 1921 1949 1978 2013 2021 2049

In 35 years:• 2nd World Eco Power• GDP +142 times• Urban revenue +71 times• Rural revenue +59 times

China is now going for the Chinese Dream: 1921 – 2021: 100 years of CPC foundation,

China will reach a comfortable level at the whole nation 1949 – 2049: 100 years of PRC foundation,

China will reach the same level as that of the developed countries

By the end of 21st century: China rejuvenationwill be realized step by step and China re-becomes the world first powerful country

The 3rd Plenary Session of the 11th

Central Committee of the CPC for “Reform and Opening “

Chinese Dream realization will improve people living conditions and boost consumption

2014 China dilemma: Stimulus or Reform China government has chosen to deepen the reforms

Investor Day – Shanghai – November 11, 2014 5

China GDP

Drivers

Export

Investment

Consumption

Super-imposed effect in 2014 Speed shift of GDP growth Pain of structure reform Digestion of post 4tr. Plan

30 “Golden Years” now limited by Natural resources Environment impact Labor force and cost

GDP drivers shift becomes must Public debt control & reduction Consumption and wage policy Core technologies & Innovation

“Global weak demand"

"Debubble! –post 4 trillion

Plan"

“Limited social protection"

China is committed to conduct further reforms aiming at the new development model

"The Rule of Law": main theme of 4th plenary session of 18th Central Committee of CPC, historical milestone

Investor Day – Shanghai – November 11, 2014 6

What does it mean?

What does it include?

How to understand?

Direction & Consequences

China history and culture deeply marked by Confucianism Confucianism privileges moralisim rather than laws In ancient China, "Law" means punishment, different from Western "Law" has no link to human rights and powers’ separation notion

Legislation: reinforcement of the role of People’s Congress Administration: the rule of the law for government Judicial organ: more independent and justice Respect of Law: population with law mindset in daily life

Under the leadership of CPC and socialist market economy Better balance between the rule of law and individual perfection Restriction of government power, thus reduce corruption source New reforms need to be conducted on the basis of laws

China will provide a more healthy business environment

2014 China automotive industry is marked by top level government exchange between Europe and China

Investor Day – Shanghai – November 11, 2014 7

Jan Mar May July Sept

Anti Trust InvestigationEuro V from

1/1/2015Scrap of Yellow Label vehicles

Incentivesfor new

energy cars

Car air Purifier

standardChild seats

In carsGerman PM Merkel

China visit

Anti trust fineOn OEM and

Auto parts

XI JinpingEurope visitDF / PSADaimlerBMWVW

Volvo

DF / Renault JV Yanfeng JCI Interior merger

DF Infiniti new JV

DF PSAChengdu new site

FVW new sitesIn Qingdao &

Tianjin

OctCapital increase of VW in

its JV with FAW: 49% vs. 40%

PV growth High H1 and Low H2 Local brands losing some share

Global OEMs capacity expansion Regulation: anti-trust, environment, safety

Main market trends

China automotive industry continues to grow, with more regulation and new norms

China market is maturing in terms of regulation and normsAir cleaning becomes a priority for government

Investor Day – Shanghai – November 11, 2014 8

Environment Safety Health

Emission

2010

China IV (EU IV)

2018Gasoline

China V (EU V)

Diesel2013

China IV

2015

China V

2018

China VI (TBD)

Fuel consumption limits (PV)

NEV subsidy plan

2015

6.9 L / 100 km

2020

5.0 L / 100 km

2025

4.0 L / 100 km

2010

• Pilot in 25 cities• Subsidy by battery energy

2013

• Focus on Beijing, Yangtze & Pearl river delta regions

• Subsidy by battery endurance distance

Request continuous attention and development on new material

Potential cost-up pressure

Product quality improvement is a priority

International standards move

Constant innovation required in emission technology to meet environment requirements

Lightweight solutions contribute to reach fuel consumption targets

Implications Implications Implications

2013, enlarge vehicle scope, defects definition, clarify responsible party, increase fine for OEMs who refuse recall

Recall policy

China Three Guarantees2013, Guarantee for repair, replacement, & return within 3 years cf car lifetime, provide more protection to consumer

Child seat2012, Restraint system of vehicles for children (ECER44), enhance the protection of children safety

Air quality (PV)2015, Air quality standards inside vehicles (PV), set mandatory standards for volatile organic compounds & specified pollutants' limits

CAR MODEL CAR PRICE (€)EU CAR PRICE (€) CN JV CAR PRICE (€) CAR MODEL

Car selling price comparison between China and Europe Margin on Premium and SUV under pressure

Investor Day – Shanghai – November 11, 2014 9

Global Brand Chinese Brand

A00

A0

A

B

C

D/E

SUV

4,000-7,000

5,000-7,000

8,000-14,000

11,000-23,000

10,000-13,000

Segment

9,000-14,000

12,000-18,000

19,000-26,000

24,000-42,000

36,000-56,000

71,000-134,000

24,000-31,000

Not produced

10,000-15,000

13,000-22,000

22,000-39,000

38,000-90,000

89,000-350,000

22,000-42,000

Note: EU car price incl. sales tax, exchange rate: EURO/RMB=1/8.2 Source: www.cars-of-europe.com, www.bitauto.com

Not present

Not present

Geely Panda

Geely SC6

Geely EC8

Geely GX7

Geely EC7

VW Tiguan

VW UP

VW Polo

VW Golf

Audi A6

BMW 7 Series

VW Passat

Six automakers share over 80% of the market

Investor Day – Shanghai – November 11, 2014 10

SAIC 26% 3,013FAW 16% 1,857

DongFeng 17% 1,977Chang'an 10% 1,121

BAIC 8% 961GAC 6% 750

GreatWall 3% 357Geely-Volvo 2% 241

BYD 2% 261Brilliance 3% 317

Chery 2% 257Others 5% 606

Market share 20% 4% 2% 1% 0% 10% 4% 5% 5% 5% 10% 3% 32%Volume ['000] 2,369 472 197 89 42 1,116 524 591 612 563 1,116 299 3,729

Others ChineseBrand

Market Share

Volume['000]

European U.S Japanese & Korean

JV

59%

24%

12%

Chinese OEM groupsPV brands

Source: Auto 2000 Aug, Faurecia internal analysis

Global OEMs enjoys 2014 market growth with continuous capacity expansion

2015 auto growth continues despite some pressure from macro economy and will be key for new China auto industry policy

Investor Day – Shanghai – November 11, 2014 11

Domestic Economic

Growth

Automotiveindustry

Development

Potential ImpactsForecasts

GDP between 7.0% to 7.3% Population at 1.37 billion Urbanization rate at 55.4% High pressure on CO2 control

PV volume growth around +9.9% Euro V nationally implemented New industrial policy release 13th Five Year Plan direction

Unemployment rate to increase Big consumer market to stimulate Public debt control and financing innovation Pillar industries support to maintain growth

2015 PV production volume at 18.7m units Yellow Label vehicles scrap plan results China local brands development Emission control, light weight, safety

Source: China State Information Center

2015 main focus: 3rd Edition of China Automotive Industry Policy

China automotive industry faces some strategic topics to be clarified in 2015 with long term impact

Investor Day – Shanghai – November 11, 2014 12

3rd Edition of China Automotive Industry Policy

1st Edition in 1994: Market against Technology Market open mainly to global OEMs2nd Edition in 2004: Consolidation by SOE OEMs Own Brands development difficulties3rd Edition in 2015: Powerful automotive country Mastering core technology / innovation

China Local Brand Support PolicyEach Chinese OEM will find out its own way to develop further the local brands

Anti-Trust Scrutiny EvolutionChina moves toward the international practices

13th Five Year Plan DirectionCO2 focus: China CO2 peak forecasted between 2025 and 2030, light weight and emission controls

OEM 50/50 JV EvolutionOEM Joint Venture Agreements extension, the latest is FVW for 25 yearsChinese and global OEMs relationship will be closer via different forms: cross participation, M&A etc.

Main Target "Perceived" Results

New China Automotive Industry Policy may focus on new energy cars and local brands

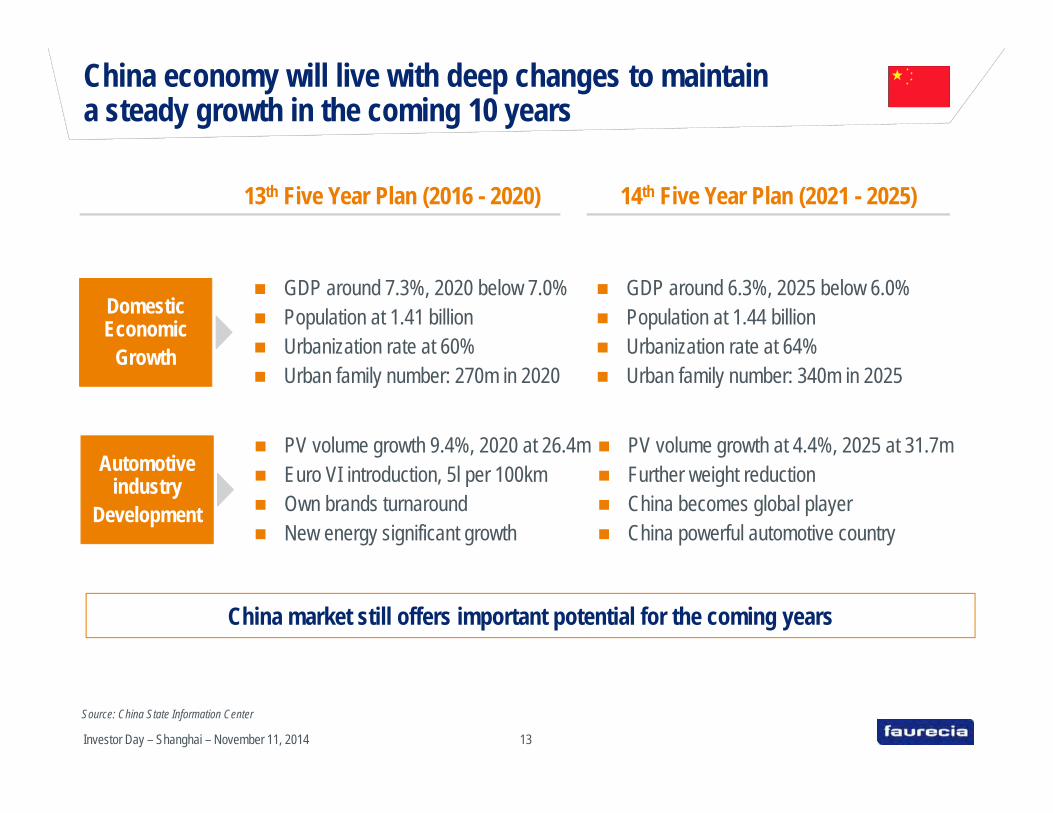

China economy will live with deep changes to maintain a steady growth in the coming 10 years

Investor Day – Shanghai – November 11, 2014 13

Source: China State Information Center

Domestic Economic

Growth

Automotiveindustry

Development

14th Five Year Plan (2021 - 2025)13th Five Year Plan (2016 - 2020)

GDP around 7.3%, 2020 below 7.0% Population at 1.41 billion Urbanization rate at 60% Urban family number: 270m in 2020

PV volume growth 9.4%, 2020 at 26.4m Euro VI introduction, 5l per 100km Own brands turnaround New energy significant growth

PV volume growth at 4.4%, 2025 at 31.7m Further weight reduction China becomes global player China powerful automotive country

GDP around 6.3%, 2025 below 6.0% Population at 1.44 billion Urbanization rate at 64% Urban family number: 340m in 2025

China market still offers important potential for the coming years

China vehicle production hits 22 m units in 2013, and will exceed 30 m units by 2017

Investor Day – Shanghai – November 11, 2014 14

Source: IHS 2014 Aug, Faurecia China internal analysis1) CVE refers to truck/bus above 3.5 tons 2) LCV refers to commercial vehicles up to 3.5 tons 3) PV refers to cars, incl. MPV and SUV 4) incl. Pickup

2017 E

31

22

6

33

2010

18

11

4

3

LCV

CVE

2020 E

33

2442

2011

19

12

6

3

2013

22

16

CAGR = ~6%

CAGR = 7%3

4

3

2012

19

13

PV

China vehicle production volume 2009 – 2020 E [m units]

1)

3)

CAGR

‘10-'13 '13-'20

Key figures of PV Market - 2013

Car owner -ship[units/1,000 people]

Total car parc[m units]

8% 6%

17% 6%

Total ProductionVolume[m units]

81111

16

63

490740

470

60

235213

85

W. Europe

4)

4)

1% 3%

2)

Market consensus on China automotive volume turn-point: 40m units

29% 29% 29%

66% 63% 61%

8% 10%

20% 28% 29%

16%15% 15%

47%40% 39%

12% 11% 11%

30% 31% 32%

26% 27% 27%

20% 19% 19%

14% 14% 14%10% 9% 8%

SUVs are increasingly favored by Chinese OEMs, premium and entry segments are also gradually gaining share

Investor Day – Shanghai – November 11, 2014 15Source: IHS 2014 Aug

China PV market is still dominated by C segment, accounting for ~40% M/S

SUVs are increasingly favored by Chinese customers, esp. for 2nd-time purchase, due to their roominess

As premium brands are pushingforward their localization in China, their share is expected to increase

Entry brands are now recovering and expected to achieve ~30% M/S

In general, the market is relatively stable, with Chinese brands increasing thanks to government support

Japanese OEM performance to be impacted by bilateral relationship

2013 2020 E2017 E 2013 2020 E2017 E 2013 2017 E 2020 E

16 2422 16 2422Sedan 16 24225% Premium

Entry

MID

U.S.Korea

China

Europe

Japan

SUV

MPVD/E

C

A/B

6%4%

6%

Growth and mix trend still support profitability improvement

Share of body-type[m units]

Share of brand tier[m units]

Share of brand origin[m units]

Chinese OEMs will become more and more global via partnership reinforcement and cross-border M&A operations

Investor Day – Shanghai – November 11, 2014 16

In the past In the future

Value chain coverage

Technology direction

Market focus

Missing to China

Work split

Market players

Vehicle, mainly PV Localizing foreign cars

Impact on suppliers

Full value chain including auto parts Specific car development for China

JV with OEM as key strength Differentiation and innovation

Passive Chinese partner In learning curve

More active Chinese partner More confident to drive decisions

Customer intimacy to focus Address decision makers

Chinese market Global car makers in China

Global market and own brands Chinese OEMs focus export / go global

6 SOEs / Global OEMs Captive and capitalistic

Internal combustion engine

Funds, market, HR Technology, brands

SOEs / POEs / Global OEMs All kinds of cooperation

New energy, hybrid, EV

Core technology Brands

China full service capabilities Global footprint

Business model challenge Capability and competitiveness

Regulation Light weighting

M&A - Partnership Local brands support

China has spent US$15bn for OEM and Auto Part acquisition outside ChinaStarting from Oct. 2014, 98% cross border M&A need no more approval from Beijing

China auto part market competition is well structured

Investor Day – Shanghai – November 11, 2014 17

China Top OEM have auto part integration strategy Global ambition to be realized via M&A operations Market is getting more and more open

Technology and innovation driven suppliers Market mix requiring higher technology and quality

performance Capable of managing global platforms

Cost driven competition and customer intimacy focus Lack of global presence and access to technology

OEM CAPTIVE PLAYERS

Faurecia is well armed to face the competition in China with a strong team

Technology, engineering localization rate and platform capabilitiesremain key success drivers

GLOBAL PLAYERS

LOCAL PLAYERS

Key takeaway for China market

Investor Day – Shanghai – November 11, 2014 18

1

2

3

4

China new government team has defined the development objectives, strategy and roadmap for the coming 10 years, positive impact on automotive industry is expected

China‘s PV market will continue to grow with 1.5 million units more per year till 2020 with a mix moving up and tightened regulation toward the international standards

China government support focuses on local brand and new energy solution development

Chinese partners will increase their decision power in the JV with global OEMs and 50/50 business model can be in further evolution in 5 to 10 years period

5 China market environment is positive for Faurecia who has already a solid presence and will accelerate the deployment of its strategy

Faurecia China development strategy definition takes fully into account market and Group’s expectations

Investor Day – Shanghai – November 11, 2014 19

Key AssumptionsImpact on

Strategy Design

Faurecia ChinaStrategy

2018 plan> € 4.0 bn

2016 plan> € 3.0 bn

2014 Forecast≈ € 2.3 bn

+ 17% vs. 2013

NeutralPolitical stability Geopolitical and social tension

PositiveGDP ≈7% per yearInflation ≈4%

PositiveNeutral

Local Brand supportNew energy car support

PositiveEnvironment focusSafety and health focus

Positive Challenging

Footprint strategyIncreasing decision power

PositiveChallenging

International standard moveM&A development

ChallengingTechnology and InnovationDifferentiation focus

Positive15% to 20% of Group salesProfitable and cash generating

ChinaPolitical Environment

ChinaMacro Economy

China AutomotiveIndustrial Policy

China Regulation

ChinaGlobal & Local OEMs

ChinaAuto Parts

China Competition

Faurecia GroupExpectation

Market components

Faurecia has solid presence and clear strategy roadmap in China

Investor Day

ShanghaiNovember 11, 2014

China StrategyFaurecia China

Jean-Michel VallinNovember 11, 2014

Faurecia celebrates in 2014 its 20 years’ localization in China, providing a solid base for business acceleration

Investor Day – Shanghai – November 11, 2014 22

2002 2011 2014 2015

Raw material, components, process, equipment

Quality system, lean production system

Manufacturing Engineering

and validation Program

management

Industrialization Tech Center fully autonomous Advanced development

for China market needs Local innovation

R&D and Innovation

WAVE 1 WAVE 2 WAVE 3 & 4

1994 2005 2013

>€1bn >€2bn

2010

A consistent strategy focused on 6 dimensionsto sustain profitable long term growth

Investor Day – Shanghai – November 11, 2014 23

Global program acquisition Customer portfolio diversification Product portfolio diversification

OEM connection Regional presence Business development booster

Organic growth with core and emerging clients

Partnership as OEM intimacy leverage

Manufacturing operational excellence at benchmark level

Quality & HSE best in class Flawless new launches Operation and cost optimization

KPI constant improvement ECRs efficient management VA/VE portfolio enhancement

Fully-owned, worldwide network Deep expertise localization Innovation and industrial style

Program development to drive profitability and cash

World class R&D providing value to customers

Strong leadership team to drive the growth plan

A strong Chinese mgmt. team Training and development plan Organization and resources

1

4 5 6

32

Faurecia has 23% CAGR for the past years and forecasts €2.3 Bn sales in 2014, a new faster-than-market growth year

Investor Day – Shanghai – November 11, 2014 24

≈ €2.3 Bn Sales*

38 Plants

≈ 12,800 employees

Present in 21 cities

R&D4 centers

750 engineersTotal Plants

€ bn

Total Sales

* Including €0.2bn non consolidated sales

2014 Forecast

1.0 1.21.5

2.0~2.3

2010 2011 2012 2013 2014

2530

35 36 38

2010 2011 2012 2013 2014

CAGR = 23%

Faurecia has now deployed its 4 Business Groups in China FECT and FAS Metal in market leading position

Investor Day – Shanghai – November 11, 2014 25

1) Consolidated sales 2) Consolidated and non-consolidated sales ; 3) mainly non-consolidated

First operation1994: Wuhan

16 plantsTotal sales: ≈ € 1,150m 1)

≈ 4,400 employees27% Market Share

First operation2002: Changchun (Structures)2003: Wuhan (Complete seat)

2004: Wuxi (Mechanism)

10 plantsTotal Sales: ≈ € 830m 1)

≈ 4,900 employees15% Market Share Metal5% M/S Complete Seat

First operation2005: Changchun

11 plantsTotal Sales: ≈ € 260m 2)

≈ 2,800 employees4% Market Share

First operation2011: Changchun

1 plantTotal Sales: ≈ € 80m 3)

≈ 550 employees2% Market Share

2014 Forecast 2014 Forecast 2014 Forecast 2014 Forecast

A manufacturing footprint of 38 plants in 2014, covering the 6 main auto regions

Investor Day – Shanghai – November 11, 2014 26

North1996200220052010201120112012

ChangchunChangchunChangchunChangchun ChangchunShenyangChangchun

West Region200320072010201120122012

ChongqingChongqingChengduChengduChongqing Chengdu

Central Region1994 200320062010201220132014

Wuhan WuhanWuhanWuhanXiangyangNanchangChangsha

East Region200020042005

2008201220122012201220132014

ShanghaiWuxiShanghaiShanghaiShanghaiNanjingShanghaiCixiYanchengNanjingCixiBeilun

★

South Region

ExhaustInteriorSeats R&D centersChina Headquarter Exterior★

201020102012

GuangzhouFoshanFoshan

201220122013

FoshanShenzhenShenzhen

YantaiQingdaoBeijing

200420072012

North-East Region

6

3

76

6

10

Investor Day – Shanghai – November 11, 2014 27

R&D Strategy FECT Tech Center Opened in April 2011

China HQ & New Tech Center Opened in March 2013 R&D and Program headcount evolution

3 fully owned R&D centers integrated in the global network with 750 engineers

Application centers in six regions Continuous reinforcement of local team

and competences More innovation focus Design and style as differentiation factor

R&D Strategy focused on competence and expertize full localization under 100% Faurecia control

2014 2015 2017

750900

1,200

Manufacturing strategy focused on best in class operations through full FES deployment and margin enhancement

Investor Day – Shanghai – November 11, 2014 28

Recognized by CustomersAmong best performing plants Customer PPM [2014]

New Plant Launching Model

8 Chinese Plants in Group Top 10 22 Chinese Plants audited

82%@A Rank; Average 64%(All plant managers are Chinese)

Dated on Sep. 2014

#1

#4

#8

Wuxi FASNanjing

Guangzhou FAS#9 Yantai FECT

#1 Anting FAS

#9 Chengdu FAS

#5 Wuhan FECTFIS

#9 Wuhan FIS

GM “2013 GM

Supplier Quality Excellence Award”

DPCA“2013 GM Special

Award”

FAW-VW“Top 10 Excellent

Quality Award”

KM&I“2013 Best

Supplier Award”

FAS FIS FECT FAE

1

6

4

8

Faurecia China targets to double its size in the coming years thanks to OEM volume growth and portfolio expansion

Investor Day – Shanghai – November 11, 2014 29

Faurecia to grow twice as fastas the market (15% CAGR)

Strengthening relationshipswith Chinese automakers: ChangAn for FIS, to extend Geely for FIS, FECT JMC for FECT Other opportunities

2016 20182014

> € 3bn

> € 4bn

≈ € 2.3bn

Sales forecast Comments

Investor Day – Shanghai – November 11, 2014 30

Partnerships objectives ChangAn Affiliated OEMs

JV footprintInterior Systems sales evolution

50/50 JV established in 2013 Interior business as first step scope Potential extension to other Faurecia product lines Significant businesses award since creation

Faurecia‘s partnership with China ChangAn Group progresses smoothly in line with the strategic plan

PV VolumeGrowth

2014 YTD1.7m+26%

Chang'an

2016 2018 2020

~20

~150~ 210

Faurecia will continute to deploy this strategy with other Chinese OEMs

€ M

Footprint strategy focused on business support and capex optimization through volume massification

Investor Day – Shanghai – November 11, 2014 31

New footprint focus regions – OEM new entry points

Shenyang

Wuhan

ChangchunBeijing

Nanjing

ShanghaiChengdu

Guangzhou

Chongqing

Changsha

Hangzhou

Key Strategy Core technology / standard

product / techno plants: densification of volume

JIT to follow customers Cross BG building solution Capex optimization Vertical integration

to catch added value

Plant Number 2014: 38 2018: 55 5 YR Investment: € 400 M

Human Resources strategy focused on supportinggrowth through leadership and competence build up

Investor Day – Shanghai – November 11, 2014 32

Balance of nationality, seniority and competence Chinese people in key Division Management Positions 100% Plant Managers are Chinese

Regular staffing reviews New employees induction and training plans Regular benchmarking to be competitive HR KPI close monitoring

University campus campaigns for new graduates Clear career path for management evolution FES China School to prepare Faurecia mindset

DEVELOP A STRONG LEADERSHIP TEAM Multi-cultural Highly motivated Result oriented

REINFORCE HR FOUNDATIONS Group key values in team’s daily behavior Full deployment of all Group HR tools C&B in line with Group guidelines and market

PROVIDE RIGHT RESOURCES FOR GROWTH Reservoir and retention Career path anticipation Training in China and abroad

Key takeaways

Investor Day – Shanghai – November 11, 2014 33

A solid presence and good financial results A clear vision and target A clear strategic roadmap A motivated team

Market providing significant growth potential toward international standards

Customer and product portfolio diversification focus Competition close follow-up and constant benchmarking

Deliver budget year by year Raise contribution to Group earnings in mid-term plan HR and management development

FaureciaChina

Market environment remains positive

High confidence to respect commitment

to Group

Investor Day

ShanghaiNovember 11, 2014

Human ResourcesFaurecia China

Kathy SunNovember 11, 2014

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

China demography overview

Source: Desktop research

The most populous country: 1.37 billion, 20% of total worldwide population; of which the 770 million workforce (56% of total Chinese population)

Dense population in East & Central China and sparse in West; 240 million migrant workers

Birth rate decreases becauseof the family planning policy from last century

Unemployment rate is about 4.3% in recent 5-year average

Manufacturing takes a larger proportion of GDP (40%) & fiscal revenue (50%)

Investor Day – Shanghai – November 11, 2014 36

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

CAGR = +11%

CAGR = +28%

1 0032 080

2 870 3 200

5 271

10 985

13 900

16 900

2010 2013 2015 2017

M&P* China all

Total Faurecia workforce in China reaches approx. 12,800 people in 2014 and will reach ~16,900 in 2017

Changchun

Shenyang

Beijing QingdaoYantai

Nanchang

NanjingYanchengWuxi

ShanghaiAntingCixiNingbo

GuangzhouFoshan

Shenzhen

Chongqing

Chengdu

Wuhan

Xiangyang

Xiangtan

NORTHERN REGIONTotal: 3,020

EASTERN REGIONTotal: 3,280

SOUTH WESTERN REGIONTotal: 2,350

CENTRAL REGIONTotal: 2,750

SH Office: 1,400SHANGHAI OFFICE

Distribution of Faurecia’s workforce in China (2014)

Total workforce in 2014: ≈12,800

Evolution of Faurecia’s workforce

With CAGR at 28% in the past, the increase in the coming years

is still significant, but at a moderate rate.

Investor Day – Shanghai – November 11, 2014 37

* Managers and professionals

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

Faurecia China has developed a local management team with limited expatriate support

The expatriate structure analysis

Expat vs total M&P Expat category Expat in mgt team

All Plant Managers are Chinese. With 27 expatriates dedicated to China, 14 are for Technical/Expert positions

The strategy is to promote Chinese people for the management functions and to have technical expatriates to transfer the know how

38Source: Desktop research

1%

99%

Expatriate

Total M&P

48%52%

ManagementTechnical expert 15%

85%Local

Expatriate

38Investor Day – Shanghai – November 11, 2014

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

HR Mission

HR STRATEGY

Develop strong leadership team and ensure key technical competence on board

Anticipate key resources growth to meet future business needs

Retain talents with Faurecia Values

HR foundation: make sure country alignment while managing diversity

Work on Employer Branding to boost company attractiveness

Promote in media communication channel Deploy CSR program in China Extend cooperation with target universities

Golden Triangle and localization deployment Strategic recruitment for next generation leaders Young Talents program to stabilize talent foundation

Promote Management & Technical parallel career path Prepare new leaders through Leadership & Management

program and Individual Development Plan

Focus on talent identification and internal mobility Individual Career path designed in advance Provide competitive package for talents

Ensure legal compliance and group alignment Respect regional guidelines HR Information System fully on board

KEY ACTIVITIES

Provide talented and committed people on time through systematic anticipation to enrich talent pipeline and develop Faurecia Culture

Investor Day – Shanghai – November 11, 2014 39

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

Faurecia golden triangle plan has been developed to ensure that new plants launch at Faurecia standards

New plantMother plant

28

54

82 peoplemoved

& promoted

Plant mgr

1 key funct. Mgr

1 key funct. Mgr

Golden Triangle: 1+2 1 plant manager 2 of 6 key functions filled internally

6 key functions = HR, ME, Quality, UAP, FES, PC&L

Local hiring in advance and train in mother plant For tech. plant, internal transfer experience

JP: "Young Talents Program" Operator: train in mother plant and involve from PMS phase 2

1st level: Plant Management Team

2nd level: Engineer & Professional

Below level: Junior Professional & operator

Investor Day – Shanghai – November 11, 2014 40

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

Faurecia university in Asia is also aimed at developing the Faurecia culture/value and strengthening the competency management

Mana

gem

ent S

kill

FES

Know

ledge

Func

tiona

l Kno

wled

ge

Lead

ersh

ip

Induction Program

Faurecia University in Asia

No. of trainees covered: 2014 – 1,000; 2015 – 1,200

41Investor Day – Shanghai – November 11, 2014

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

2012113 hired

2013177 hired

2014140 planned

Faurecia China talent acquisition strategy … Acquire Talents for Future

Executive

Sr. Manager

1st Line Manager

Junior Professional

Professional Experienced

Strategic Recruitment

Young Talents Program

83% RetainedTill 2013

201225 hired

201330 hired

201450 planned

Investor Day – Shanghai – November 11, 2014 42

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

In 2014 the Group launched a cultural transformation project calledBeing Faurecia based on three key managerial values

Entrepreneurship Autonomy Accountability

Culture transformation in line with new values fully underway in China

Investor Day – Shanghai – November 11, 2014 43

In China this has been receivedwith enthusiasm as it is in line withthe way that we manage ourbusiness through taking initiatives, focus on performance and resultsand celebrating success

Exemplarity: Tracy LI (Chengdu FAS Plant Manager, Value: Entrepreneurship)

Wuxi Model LineValue: Autonomy

Accountability

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

Key take-away for Faurecia China HR

1

2

3

4

5

Investor Day – Shanghai – November 11, 2014 44

China headcount will increase from 12,800 today to 16,900 in 2017

China Government trend is to support the workers with more protection through regulations and salary increase in order to maintain social harmony.

Productivity is becoming a key objective.

Faurecia HR KPIs are globally outperforming the market, which is well highlighted by the company's internal Employee Engagement Survey of 2013

Internal promotion, talent attraction, retention and management development remain the key challenges, as the market will grow even more competitive,

especially at the manager level

Faurecia China organization has been reinforced with creation of Divisions supported by corporate functions, keeping Faurecia culture and value as a priority

Investor Day

ShanghaiNovember 11, 2014

Automotive SeatingFaurecia China

Sam XiaNovember 11, 2014

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

FAS China growth at 18% CAGR in the past 4 years

Investor Day – Shanghai – November 11, 2014 47

≈ € 830m Total Sales

10 Plants

≈ 4,900 employees

€M €M

2014: 10 Plants Complete Seat (3 Plants) Front Seat Frame (5 Plants) Mechanisms - Recliners (1 Plant) Mechanisms -Tracks (1 Plant)

R&D2 centers

300 engineers

CAGR = 18%

2014 Forecast Total Sales

Plant Number

Business Awards

5

89

10 10

2010 2011 2012 2013 2014

1,5601,920

> 2,400

2009+2010 2011+2012 2013+2014e

423 466583

712

2010 2011 2012 2013 2014e

≈ 830

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

FAS China is composed of 4 product families

Investor Day – Shanghai – November 11, 2014 48

First operation2003: Wuhan

2014 operation scale650k carsets /year

2014 Market Share 5%

First operation2002: Changchun

2014 operation scale2,700k carsets /year

2014 Market Share 13%

First operation2004: Wuxi

2014 operation scale15M recliners /year

15M tracks/year

2014 Market Share 16%

Frames Comfort &Trim

First operation2013: Wuhan

2014 operation scale350k carsets /year

Complete Seat Mechanisms

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

FAS China business development strategy3 priorities to secure the sales growth

Investor Day – Shanghai – November 11, 2014 49

1

2

3

"Partnership for Complete Seat"

"Global Platform for Frames"

"New Customers"

Leverage the existing Faurecia JV Develop new partnership projects Other opportunities

Secured the business awards of Global Generic Platforms with VW, PSA, Nissan, BMW, GM and Ford

Benefit from the new generation of Mechanisms Product 100% localization strategy for cost competitiveness

Further develop new emerging customers in Chinae.g. Renault, Fiat-Chrysler

Confirm 2013 business breakthrough with Ford Opportunities with Japanese/Korean OEMs following

global approach, e.g. Hyundai

Top

Line

Initi

ative

s

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

FAS China profitability enhancement strategy6 Priorities to sustain profitability

Investor Day – Shanghai – November 11, 2014 50

1

2

4

"Customer mix"

"Vertical integration"

"Footprint optimization"

Focus on Premium brands: BMW, Audi, Cadillac … Focus on product innovation & generic system solutions

Vertical integration for Complete Seat (Foams, Covers & Accessories) Stamping & painting for Frames

Maximum loading of current metal plants (fixed cost optimization) Low CAPEX JIT Plants

Botto

m L

ine I

nitia

tives

5 "Cost improvement" Purchasing (supplier panel, mandatory supplier management) Focus on value analysis / value engineering (VA/VE) & 6 sigma Engineering Change Request (ECR) managements in serial life phase

6 "Business Development & Program Management"

Constantly improve operating income / Upfront costs / IRR / Max Cash Out during each program phase

Reduce D&D, development core team cost Control the total upfront / CAPEX optimization

3 “Product mix" Maintain leadership in highly profitable mechanisms business Value-creating innovation in mechanisms and frames

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

FAS China is balancing its customer portfolioKey accounts remain global OEMs

Investor Day – Shanghai – November 11, 2014 51

VW remains 1st key account

2018 Sales split European 65% Japan/Korean 19% American 11% Chinese 5%

4 customers above € 200m Sales2016 20182014

€ 1.2bn

€ 1.7bn

€ 830m

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

Mechanisms

FAS China will have 17 plants in 2018: 6 new JIT plants and 1 new metal plant are in preparation

Investor Day – Shanghai – November 11, 2014 52

Number of plants every year

+ 1 plant+ 6 plants + 0 plant

• Northeast 1• Central 2

• Northeast 1• Central 2• East 1• South 1

• East 2

5 plants3 plants 2 plants

"Footprint Centralization""JIT Module" "Base Area"

JIT plants: Plan 6 new footprints

Metal plants: Densify the production by main automotive regions to benefit from volume effect

Mechanisms plants: Fully load the current ones

JIT Frame

‘13 ‘14 ‘15 ‘16 ‘17 ‘18Year

10 10 14 15 16 17Plan number

201410 plants

2018+7 plants

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

Investor Day – Shanghai – November 11, 2014 53

FAS China R&D strategyGlobal network and local presence with customer proximity

R&D Strategy China HQ & New Tech Center Opened in March 2013

Validation Recognized by OEMVW 100%

Ford 85%

GM

Local OEM

R-N

100%PSA

90%

100%

100%146

196244

300

2011 2012 2013 2014

CAGR 28%

Headcount Evolution

2 (Shanghai and Wuxi) fully owned R&D centers, 1 D&D plateau in Wuhan, 1 JV R&D in Changchun, integrated in the global R&D network,

Test facilities certified by global OEMs Continuous reinforcement of local team and competences Industrial style as differentiation factor “East Works” for advanced innovation

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

FAS China product plan on Complete Seats Global & Customization – Next generation

Investor Day – Shanghai – November 11, 2014 54

We Focus

We Focus

Offboard Wellness Assessment

Foot massage module 2nd social row Removable cover Safety Cover Carving

Air CleanerBamboo

Luxury trend for brand

Personalized trend

Environment trend

OEM Focus

End User Focus

Global Concern

Self Adjustment Connected with smart accessories Shape adjustment for comfort Tactile Seat Display Smart Fit

Audio & comfort Health “Magic” flexibility Heat & Vent

We Focus Customization - Integrated Intelligence

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

FAS China product plan on Front Seat Structure Generic & Modular – Next generations with weight & cost reduction

Investor Day – Shanghai – November 11, 2014 55

1-2

3-1

1-1

3-2

10.5 Kg

2009 SOP2011 20132012 20142006 2015 2016

8.5 Kg

12.0 Kg

11.5 Kg

5-1

11.9 Kg

2013-2018 CHINA

2013-2022 CHINA

2013-2022 CHINA

2014-2021 CHINA

Next generation

5-2

11.5 Kg

11.5 Kg

~15.0 Kg

2-1

17.07 Kg

2-2

15.59 Kg

2015-2023 CHINA

Developed in China

4-2

11.5 Kg

4-1

13.7 Kg

4-3

Customer A

Customer C

Customer D

Customer E

Customer B

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

FAS China product plan on MechanismsGlobal & Standard – Next generations with size, weight & cost reduction

Investor Day – Shanghai – November 11, 2014 56

Recliner III Recliner IVRecliner II

Track IIITrack IITrack I

E-Pump I E-Pump II

2006 SOP2008 20112010 20122003 2013 2014

Recliners

Tracks

E-Pumps

2015 2016

Recliner I

-19% vs. Recliner I -35% vs. Recliner III

-16% vs. Track II

-10% vs. E-pump1

Only 1 worldwide production facility in China

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

Key takeaways

Investor Day – Shanghai – November 11, 2014 57

1

2

3

4

FAS China achieved 18% CAGR in the past 4 years, reaching €830m by 2014.It has developed leading market shares in Frames (#2 at 13%)

and Mechanisms (#1 at 16%)

FAS China targets to maintain sales at 20% CAGR in the next 4 years which will lead to 3% to 6% market share increase per product line,

sales of €1.7b in 2018

FAS China has formulated clear customer, product, manufacturing strategies to ensure growth and profitability, including customer mix, footprint optimization,

vertical integration, and program cost improvements

FAS China benefits from solid HR foundation on which it will further develop the organization strength and competitiveness, with 7,700 people in 2018

Investor Day

ShanghaiNovember 11, 2014

Emissions Control TechnologiesFaurecia China

Thierry AubryNovember 11, 2014

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

Investor Day – Shanghai – November 11, 2014 60

CAGR = 23%

2014 Forecast Total Sales

Total Plants

Business Awards

2009+2010 2011+2012 2013+2014e2010 2012 2014e

≈ € 1.1bn Total Sales

≈ € 660m Product Sales

15 Plants

> 4,400 employees

R&D1 center

288 engineers 911 12

14 15

2010 2011 2012 2013 2014

2011 2013

FECT is the market leader of emission control in China

499607

778990

≈ 1,100

1,680

2,440 ~2,300

€m €m

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

FECT China is composed of 4 product families

Investor Day – Shanghai – November 11, 2014 61

Catalytic Converters Complete LinesManifolds Mufflers

First operation2008: Qingdao

2014 operation scale> 2 Mio parts / year

First operation1998: Changchun

2014 operation scale> 4 Mio parts / year

First operation1994: Wuhan

2014 operation scale> 3 Mio parts / year

First Operation1994: Wuhan

2014 operation scale> 1 Mio parts / year

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

3 priorities have been strategically planned for the next 5 years by FECT

FECT China strategy

62

Strengthen customer partnerships through JV activities Reinforce customer relationship to improve business opportunity Achieve win-win for both OEM and FECT

Build customer alliance throughout China

Reinforce market driveninnovation

Marketing driven innovation focus on China requirements Speed up innovation to market Build up innovation experts and specialists team locally in China

Drive the growth of commercial vehicle emission business

Strengthen China CVE product portfolio to meet the demand of stricter China emission standards

Alliance market approach with Cummins Emission System Leverage LVE footprint, experience and size to support CVE

China Innovation

Commercial Vehicles

OEM Alliance

Investor Day – Shanghai – November 11, 2014

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

63

FECT in superior position through technology and global organization

FECT is clear market leader with 27% market share

Diversified competition

Technology is FECT strength

Global program management is key competitive advantage

Market share in 2013

Competition landscape in China

Source: FECT China

Tenneco

27% Faurecia

Sejong

Calsonic KanseiSangoLihe

OthersTotal

of around 20 Competitors

Investor Day – Shanghai – November 11, 2014

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

FECT China with very balanced customer portfolio

64

2016 20182014

€ 1.4bn€ 1.6bn

€ 1.1bn

LVE

CVE

Investor Day – Shanghai – November 11, 2014

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

FECT China will reach 30% market share in CVE in 2018

Investor Day – Shanghai – November 11, 2014 65

CVE Business development

Market volume evolution on road (M Units)

Driving CVE business growth by the alliance with CES (Cummins Emission System) and partnership with local players

Develop technology co-operation with Chinese CV OEMs

After treatment systems shall reach 3.6 M Units in 2018

FECT is targeting to reach 30% market share in the next 5 years

After treatment systemNon emissionized

2014 2015 2016 2017 2018

3.6 3.8 4.1 4.4 4.5

2020

3.6

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

CVE

FECT China Footprint

Investor Day – Shanghai – November 11, 2014 66

Number of plants every year

+ 3 plants+ 0 plant + 0 plant

6 plants8 plants 1 plant

"JIT Sequence delivery""Technology capacity"

JIT plants: Plan 3 new footprints Techno plants: Complete exhaust systemproduction capacity, key components manufacturingCVE: Fully loading the current one and use LVE actual footprints

Techno plants JIT plants

201415 plants

2018+3 plants

‘13 ‘14 ‘15 ‘16 ‘17 ‘18Year

14 15 16 17 18 18Plan number

• Central 2• East 3• South 1

• Central• Northeast:1• Central 2• East: 4• West: 1

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

Acoustic Performance EDST (3) Noise dampersEVO valve/Electric valve

Emissions reduction ASDS (2) GPF (1)

Weight reduction LW hot endBrazed cold end

Energy recovery EHRM (4) Compact EHRS (5) RankineDirect oil gear box heating

Fabricated T ManifoldMono and Airgap

Closed couple SCR : U shape – C-mixer

Ultra light-weight cold end

Modular NVH solution

Our focus in the next 5 years will be reinforcing product strategy and promoting innovation

Investor Day – Shanghai – November 11, 2014 67

2015 20202013 2017

1. Gasoline Particulate Filter

Product & Technology roadmap

3. Exhaust Dynamic Sound Technologies

2015 20202013 2017

5. Exhaust Heat Recovery System4. Exhaust Heat Recovery Manifold 2. Ammonia Storage and Delivery System

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

Key takeaways

Investor Day – Shanghai – November 11, 2014 68

1

2

3

4

FECT has a clear market leader position on China market with over 25% market share

With 10% CAGR over the 2014-2018 period, FECT will increase market share in China

Innovation and technology, strong growth in CVE market and alliance strategy with OEMs as main pillars of FECT China strategy plan

FECT China has proven operational excellence including program management, footprint optimization and talent management and retention

Investor Day

ShanghaiNovember 11, 2014

Interior SystemsFaurecia China

Richard ZhangNovember 11,2014

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

FIS China Growth at 24% CAGR in the past 4 years

Investor Day – Shanghai – November 11, 2014 71

≈ € 270m Total Sales

13 Plants

≈ 2,800 employees

€m €m

2014: 13 Plants 12 Technology Plants 1 JIT Plant

R&D1 center

300 engineers

CAGR = 24%

2014 Forecast Total Sales

Plant Number

Business Awards

257477

>1,000

2009+2010 2011+2012 2013+2014e

116 136

~270

2010 2012 2014e

5

8

13

2010 2012 2014

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

FIS China is Composed of 4 product families

Investor Day – Shanghai – November 11, 2014 72

Instrument Panel Acoustic ModulesCockpit Door Panel

First operation2006: Chongqing

2013 operation scale> 300k units / year

First operation2005: Changchun

2013 operation scale1 Mio parts / year

First operation2005: Changchun

2013 operation scale2.2 Mio parts / year

First operation2010: Changchun

2013 operation scale0.7 Mio parts / year

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

Investor Day – Shanghai – November 11, 2014 73

Current merging of the market leaders open great opportunities for Faurecia Interior Systems

Market share in 2014 Market consolidation underway

Current merging of both leaders combined with an "over-splitting" of the market by local players is creating a very favorable business and partnership momentum for Faurecia Interior System

Yanfeng and Visteon had long-standing joint venture covering all automotive regions and OEMs

Yanfeng purchased all shares of joint venture in 2013

Yanfeng Interior China estimated sales € 2.1 bnin 2012

Yanfeng is now in the process of absorbing JCI Interiors (excluding electronics)

JCI Interiors has JVs with FAW, BAIC and GAC groups

JCI China Interior sales (excluding electronics) € 1.04 bn

Yanfeng

JCI

Yanfeng

Others

MobisCalsonic Kansei Faurecia

4%

Numberof player

42 (mainly Chinese)

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

Our sustainable business model is based on 4 key drivers

Toward 10% Market Share through a sustainable business model

Strategic Partnership

Product &Innovation

Programs & Operations efficiency

Entrepreneur and committed People

74Investor Day – Shanghai – November 11, 2014

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

Partnership and customer strategyStrategic partnership will be a key success factor

Standalone approach DiversificationStrategic Partnerships

Select Relevantand Sustainable Business

SVW FVWGeely

Diversify customer portfolioGuangdong Auto Group-CFA

Others

Enhance Market ShareChang An

(Ford , DS and CA own brand)Other opportunities

Reinforced customer intimacy, to better address: 1

Ford remains our Number one customer 2018 Sales split

European 38% Japan/Korean 18% American 32% Chinese 12%

CAGR around 30%

75Investor Day – Shanghai – November 11, 2014

Expected turnover

€ 270m~ € 400m

~ € 750m

2014 2016 2018

2 3 4

Our customer strategy is based on 4 main pillars

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

Industrial StrategyPriority is to saturate our existing "Technology" footprint

Investor Day – Shanghai – November 11, 2014 76

Number of plants every year

+ 6 plants+ 1 plant

201413 plants

2018+7 plants

1 plant12 plants

"Fast response""Ensure capacity"

Techno plants: To saturate our existing footprint which covers the main automotive basins.

JIT plants: To set up 6 new JITs supplied by our technoplant an ensuring quick responseto customer needs while limiting investments.

Techno JIT

‘14 ‘15 ‘16 ‘17 ‘18Year

13 14 15 18 20Plan number

• Northeast 1• East 3• South 2• Central 2

• Central 1

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

Product & innovation strategyAddressing upgrading, personalization and environment trend

Upgrading Premium Quality Cut & SewLOCOPSlush Lite Decostitich PipingIMP

Personalized trend Aluminum Ambient LightingSliding Dock Wi-charging

Environment trend

Air PurificationNAFI

77Investor Day – Shanghai – November 11, 2014

Matching with growing perceived quality expectations of Chinese market

Addressing enrichment and technology trends of Chinese market

Introducing global green technologies as well as specific technologies for China

Prop

erty

of Fa

urec

ia-D

uplic

ation

pro

hibite

d

Key Takeaways

78Investor Day – Shanghai – November 11, 2014

1

2

3

4

FIS China has engaged a successful growth and profitability allowing to target more than € 750m total sales by 2018

Strategic partnership with OEM is a key driver to address this ambitious plan. Our recent but successful CCAG JV is demonstrating the relevance of this approach

Operations and programs optimization are a must to be able to propose a competitive and profitable business model in China Interior market

People are at the center of this strategy. Priority is to develop and reinforce our team, enhancing entrepreneurship, continuous improvement and execution mindset

Investor Day

ShanghaiNovember 11, 2014

Investor DayStrategy update

Yann DelabrièreNovember 11, 2014

Benefit from selective resource allocation strategy

Accelerate in Asia

Leverage global platforms

Develop value-added technologies

2014 - 2016: Selective growth strategy confirmed

Investor Day – Shanghai – November 11, 2014 81

Faurecia Automotive SeatingOn track to meet its 2016 targets

Investor Day – Shanghai – November 11, 2014 82

Key drivers Mechanisms leadership and Generic frames China and Asian customer growth Customer diversification in particular growth with Nissan and Ford Value creating innovations based on fuel economy (weight reduction) and

smart comfort

Update on priorities Mechanisms and frames on track to reach over 8% operating margin in 2016 Back to growth in North America, with significant launches in H2 2014

and operational turnaround confirmed Single European division successfully created, profitability improving Renault-Nissan on track to become second largest client China opportunities confirmed

2016 Targets Total sales > € 7.1bn Operating margin > 5.0% ROCE* > 20%

Faurecia Emissions Control TechnologiesAhead of its roadmap, 2016 targets upgraded

Investor Day – Shanghai – November 11, 2014 83

Key drivers Capture the growth of the Commercial Vehicle markets especially in China Increase value-added through innovations: environmental performance

(NOx and particulates); fuel economy (weight reduction, energy recovery); acoustic performance (sound design)

Update on priorities Europe recovery is well engaged, further optimization to come North America turnaround ahead of plan Product and process standardization well underway CVE growth rate of around 20% CAGR confirmed, driven by partnership

with Cummins and regulation introduction especially in China moving to Euro 5

Business awards for energy recovery systems and SCR and interest in sound design demonstrate relevance of technology strategy

2016 new Targets Total sales > € 7.4bn (value-added sales > € 4.0bn) Operating margin close to 5.0%, (up from > 4.0%)

now above 8.0% on value-added sales ROCE* > 25% (up from around 25%)

*: Pre-tax and including goodwill

Faurecia Interior SystemsImproving in evolving environment, 2016 targets adjusted

Investor Day – Shanghai – November 11, 2014 84

Key drivers Selective growth strategy with focus on cash model Profitability increased through operational improvement Benefit from trend towards consolidation in the market Accelerate in Asia Expand higher profitability product lines (decoration, HMI)

Update Consolidation underway should improve competitive environment Strong operational improvement in Europe, North America

is progressing China growth acceleration confirmed Breakthrough in bio materials with clear roadmap

towards 30% weight reduction

2016 Targets Total sales > € 4.5bn Operating margin > 4.0% (from > 4.5%) ROCE* around 15% (from around 20%)

*: Pre-tax and including goodwill

Faurecia Automotive ExteriorsOn track to meet its 2016 targets

Investor Day – Shanghai – November 11, 2014 85

Key drivers Remain market leader in Europe Front End Modules (FEM) strategic review South America turnaround Develop long term potential for Composite Technologies

Priorities update Awarded first composite tailgate business and composite floorsco-development with OEMs

Margin improvement actions in North Europe (ex. Plastal) to accelerate South America capacity utilization rate close to 100% in 2016

and operational cost management underway

2016 Targets Total sales > € 2.0bn (or > € 1.5bn excl. FEM) Operating margin 4.5% - 5.0% ROCE* > 20%

*: Pre-tax and including goodwill

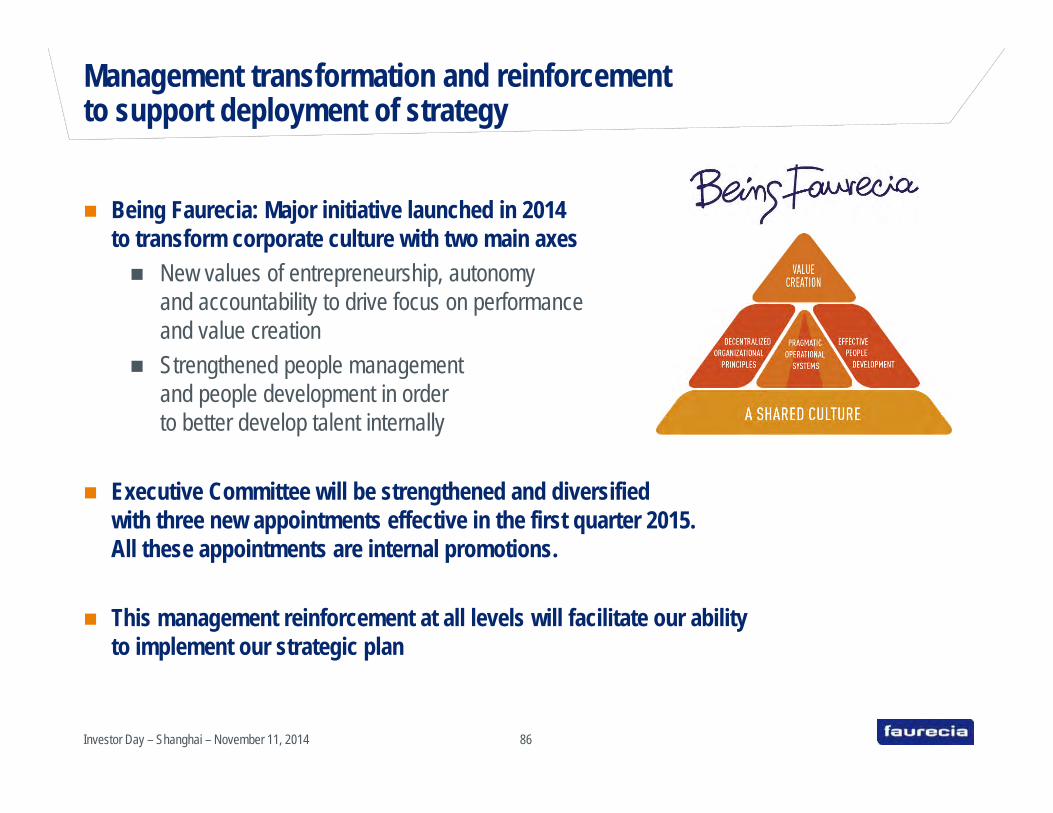

Being Faurecia: Major initiative launched in 2014 to transform corporate culture with two main axes New values of entrepreneurship, autonomy

and accountability to drive focus on performance and value creation

Strengthened people management and people development in order to better develop talent internally

Executive Committee will be strengthened and diversified with three new appointments effective in the first quarter 2015. All these appointments are internal promotions.

This management reinforcement at all levels will facilitate our ability to implement our strategic plan

Management transformation and reinforcement to support deployment of strategy

Investor Day – Shanghai – November 11, 2014 86

2016 Targets are fully confirmed

Investor Day – Shanghai – November 11, 2014 87

Sales above 21 billion eurosOperating margin 4.5 – 5.0%

Net cash flow around 300 million eurosROCE* > 20%

*: Pre-tax and including goodwill

Investor Day

ShanghaiNovember 11, 2014

Investor DayGroup financial strategy and targets

Michel FavreNovember 11, 2014

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

Increasing operating margin from 3.0% in 2013 to 4.5% - 5.0% in 2016

Capex + capitalized R&D around € 800m

Asset turn to improve by 20bp to close to 5x

* Pre-tax and including goodwill

2012 2013 2014 2015 2016

Reminder of financial targetsROCE to increase by 50% from 14% in 2013 to over 20% in 2016

> 20%

13% 14%

Investor Day – Shanghai – November 11, 2014 90

ROCE *

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

Increasing EBITDA margin (>150bps gain or > € 300m contribution)

Improved Capital Employed

Additional factoring of receivables in 2014

Reduced financial expenses (€ 150m objective in 2016 vs € 200m in 2013)

2013 2014 2016

Positive144

Around 300

Reminder of the financial targetsNet Free Cash Flow generation around € 300m in 2016

Investor Day – Shanghai – November 11, 2014 91

Net Free Cash Flow in €m

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

Priority to strategic OEMs

Priority to the two Business Groups (Emissions Control Technologies and Automotive Seating) which require lower Capex and capitalized R&D

Priority to new footprint expansion mainly in Asia

Negotiate better financing terms with OEMs for development cost

Reminder of the financial targetsOptimize resource allocation

4 key priorities

Investor Day – Shanghai – November 11, 2014 92

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

Financial priorities and resource allocation

€ 100m per year dedicated to research and innovation expenses (within the R&D budget)

€ 50m per year from 2015 onwards for restructuring expenses to continue to optimize the industrial footprint and increase the average size of our plants

€ 100m of Capex for process standardization

Around € 100m capital allocation over 2015-2016 to buy-back minorities

Investor Day – Shanghai – November 11, 2014 93

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

Main profitability drivers by regionAsia >8% and N. America and Europe >4% operating margin

Investor Day – Shanghai – November 11, 2014 94

Main drivers

Growth(volume & mix)

Asia is our top priority and it is where growth prospects are the best North America is restarting a cycle of secular growth

Commercial margin(Project management & re-pricing)

North America is where better project and commercial management should help the most

In South America, re-pricing to take into account high inflation, lower volumes and currency swing is key to a margin recovery

Footprint optimization Footprint optimization is an ongoing process and will lead to sizeable margin expansion

Standardization North America and Europe is where standardization is expectedto yield savings

Operational performance North America and to a certain degree South America will benefit from operational improvements

Geographical mix With Asia being the fastest growing region and also the most profitable region, it is helping overall margin expansion

Operating margin improvement(2014-2016)

100 – 150bp

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

Investor Day – Shanghai – November 11, 2014 95

Financial targets by region (updated vs initial)

> 21.0 (> 20.5 excl. FEM)

4.5% to 5.0%

Group total sales (in €bn)

Operating marginas % of total sales

> 10.7 (> 10.2 excl. FEM)> 5.4

Close to 4.0Close to 1.0

Total sales (in €bn)EuropeNorth AmericaAsiaSouth America & rest of world

4.5% - 5.0%> 4.0%> 8.0%

Breakthrough in profitabilityand focus on cash generation

Operating margin(% of total sales)

EuropeNorth AmericaAsiaSouth America & rest of world

2016 updatedFAURECIA Comment

Depending on strategicreview outcome

Depending on strategicreview outcome

UpgradedAdjusted

Upgraded

UpgradedAdjusted

> 21.0

4.5% to 5.0%

> 10.7> 5.4> 3.8> 1.1

4.0% - 5.0%5.0%

> 7.0%Breakthrough in profitability

and focus on cash generation

2016 initial

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

2014 2016

56%25%

14%5%

Europe

North America

South America & rest of world

Asia

26%

52% Europe

18%4%

South America & rest of world

North America

Asia

Investor Day – Shanghai – November 11, 2014 96

Regional perspectiveBetter balanced portfolio

Product sales by region

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

Investor Day – Shanghai – November 11, 2014 97

Main profitability drivers by Business GroupAll Business Groups above 4% operating margin

Main drivers

Growth(volume & mix)

Automotive Seating & Emissions Control Technologies are the fastest growing Business Groups

Commercial margin(Project management & re-pricing)

Interior Systems will benefit the most from improved project management and also re-pricing

Footprint optimization Automotive Seating, Emissions Control Technologies and Interior Systems will benefit the most from continuous footprint optimization

Standardization Automotive Seating with generic frames and Emissions Control Technologies with industrial standardization will generate sizeable savings

Operational performance Interior Systems is where improved operational performance especially in North America will yield significant margin expansion

Geographical mix Interior Systems will grow very fast in Asia where margins are higher and therefore will benefit from a favorable mix improvement.

Operating margin improvement (2014-2016) 100 – 150bp

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

98

Financial targets by Business Group (updated vs initial)

> 21.0 (> 20.5 excl. FEM)4.5% to 5.0%

> 20%around 300

Group total sales (in €bn)Operating marginas % of total salesROCE *Net cash flow (in €m)

> 7.4

Total sales (in €bn)

Emissions Control Technologies> 4.5Interior Systems

> 2.0 (>1.5 excl. FEM)Automotive Exteriors

> 7.1Automotive Seating

close to 5.0%

Operating margin (% of total sales)

> 4.0%4.5% - 5.0%

> 5.0%Emissions Control TechnologiesInterior SystemsAutomotive Exteriors

Automotive Seating

around 15%

ROCE **> 20%> 25%

> 20%

Emissions Control TechnologiesInterior SystemsAutomotive Exteriors

Automotive Seating

* pre-tax and including goodwill

2016 updatedFAURECIA

Investor Day – Shanghai – November 11, 2014

Comment

Depending on strategic review outcome

Depending on strategic review outcome

Upgraded (> 8.0% on value-added sales) Adapted

UpgradedAdapted

> 21.04.5% to 5.0%

> 20%around 300

> 7.4> 4.5> 2.0

> 7.1

> 4.0%> 4.5%

4.5% - 5.0%

> 5.0%

around 20%

> 20%around 25%

> 20%

2016 initial

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

Significant profitability increase from 3.0% to 4.5% - 5.0% OM

Capex and capitalized R&Daround at € 800m

Tight WCR control€ 5m additional for 1%

sales change

Investor Day – Shanghai – November 11, 2014 99

Generate strong cash flow in 2016

Free cash flow before interest and tax of around 80% of operating income

Optimize financial expenses and taxes (around 32% tax rate)

Net cash flow around € 300m

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

Investor Day – Shanghai – November 11, 2014 100

Cash Flow generationMain drivers

EBITDA

Change in WCR

Capex + capitalized R&D

Restructuring

Finance expenses

Tax & Other

Net cash flow

Driver

Higher operating income (> 150bp margin improvement between 2013 and 2016) and higher D&A

Improvement partially offsetting sales growth

Strong discipline and selective capital allocation according to new footprint opportunities

Continuous footprint optimization

Refinancing will generate sizeable savings (Objective € 150m in 2016 vs€ 200m in 2013)

Higher taxes from higher PBT to be partially offset by recovery of tax lossescarry forward

Objective of around € 300m by 2016

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

Investor Day – Shanghai – November 11, 2014 101

WCR optimizationZoom on main drivers

Driver

Receivables Reduction of customer overdues & alignment of customer terms Factoring programs extension with additional lines in new countries and general

business growth

Inventories Reduction of minimum 1 day (out of 11 days)

Payables Gain of 1 day through alignment and reverse factoring

Other Geographical mix & contingencies will weigh on WCR

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

Objective to be 100% financed by capital markets (factoring customer receivables and issuing bonds)

Ensure liquidity and independence through a 5 year syndicated credit facility (€1.2bn) with our core international partner banks

Go back to the bond market to refinance our existing and expensive bonds through a new bond

Investor Day – Shanghai – November 11, 2014 102

Debt & financing

Financing strategy

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

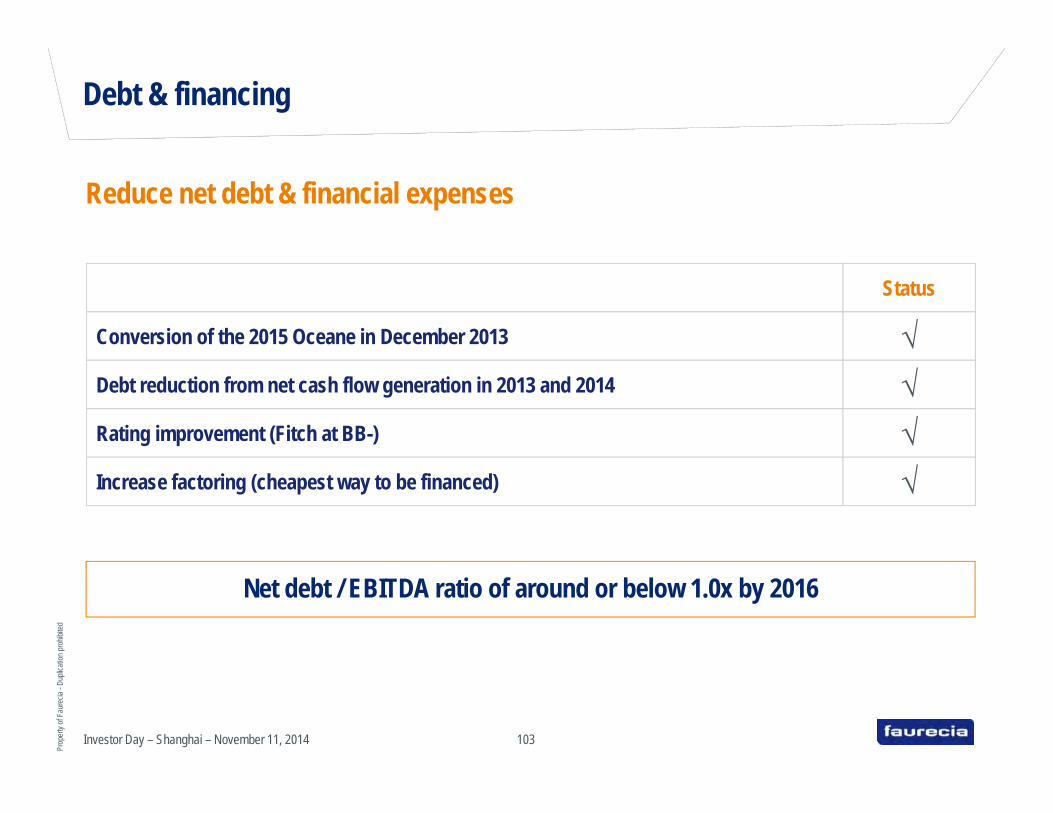

Investor Day – Shanghai – November 11, 2014 103

Debt & financing

Reduce net debt & financial expenses

Net debt / EBITDA ratio of around or below 1.0x by 2016

Status

Conversion of the 2015 Oceane in December 2013 √Debt reduction from net cash flow generation in 2013 and 2014 √Rating improvement (Fitch at BB-) √Increase factoring (cheapest way to be financed) √

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

Investor Day – Shanghai – November 11, 2014 104

Update on refinancing

Status

Renewal of the € 1.2bn, 5 year syndicated facility at better conditions √

Refinancing of the 2019 HY bond (€ 250m) at better conditions Call option in June 2015

Refinancing of the 2016 HY bond (€ 490m) at better conditions Maturity in December 2016

Conversion of the 2018 convertible bond (€ 250m) Option to force conversion in early January 2016 if share price above € 25

Net debt / EBITDA ratio of around or below 1.0x by 2016

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

Investor Day – Shanghai – November 11, 2014 105

Conclusion

Large opportunities with refinancingFirst phase is accomplished

Faurecia is well on track to achieve its 2016 targets

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

106

Contact & Share data

Investor Relations

Eric-Alain Michelis2, rue Hennape92735 NanterreFrance

Tel: +33 1 72 36 75 70Cell: +33 6 64 64 61 29Fax: +33 1 72 36 70 30E-mail: [email protected] site: www.faurecia.com

Share DataBloomberg Ticker: EO:FPReuters Ticker: EPED.PADatastream: F:BERTISIN Code: FR0000121147

ADR DataTicker: FURCYRatio: 2 ADRs for 1 shareAgent: Citi Group

2013 Results & 2014 Objectives – February 12, 2014

Bonds ISIN Codes2016 bonds : XS0704870392 2019 bonds : XS07789178142018 convertible : FR0011321363

Investor Day – Shanghai – November 11, 2014

Prop

erty

of Fa

urec

ia -D

uplic

ation

pro

hibite

d

107

Safe Habor Statement

This report contains statements that are not historical facts but rather forward-looking statements. The words"will," "may," "designed to," "outlook," "believes," "should," "anticipates," "plans," "expects," "intends,""estimates" and similar expressions identify these forward-looking statements. All such statements are basedupon our current expectations and various assumptions, and apply only as of the date of this report.

Our expectations and beliefs are expressed in good faith and we believe there is a reasonable basis for them.

However, there can be no assurance that forward-looking statements will materialize or prove to be correct.Because such statements involve risks and uncertainties such as automotive vehicle production levels, mixand schedules, financial distress of key customers, energy prices, raw material prices, the strength of theEuropean or other economies, currency exchange rates, cancellation of or changes to commercial contracts,liquidity, the ability to execute on restructuring actions according to anticipated timelines and costs, theoutcome could differ materially from those set out in the statements.

Except for our ongoing obligation to disclose information under law, we undertake no obligation to updatepublicity any forward-looking statements whether as a result of new information or future events.

Investor Day – Shanghai – November 11, 2014

Investor Day

ShanghaiNovember 11, 2014