strategic intent - · pdf fileamong the first to apply the concept of strategy to management...

TRANSCRIPT

Harvard Business Review

Jb revitalize corporate performance,we need a whole new model of strategy.

May-funel989

STRATEGIC INTENTby Gary Hamel and C.K. Prahalad

"oday managers in many industries are workinghard to match the competitive advantages oftheir new global rivals. They are moving manu-facturing offshore in search of lower labor

costs, rationalizing product lines to capture globalscale economies, instituting quality circles and just-in-time production, and adopting Japanese human re-source practices. When competitiveness still seemsout of reach, they form strategic alliances-oftenwith the very companies that upset the competitivehalance in the first place.

Important as these initiatives are, few of them gobeyond mere imitation. Too many companies are ex-pending enormous energy simply to reproduce thecost and quality advantages their global competitorsalready enjoy. Imitation may be the sincerest form offlattery, hut it will not lead to competitive revitaliza-tion. Strategies based on imitation are transparent tocompetitors who have already mastered them. More-over, successful competitors rarely stand still. So it isnot surprising that many executives feel trapped in aseemingly endless game of catch-up-regularly sur-prised hy the new accomplishments of their rivals.

For these executives and their companies, regain-ing competitiveness wiU mean rethinking many of

1. Among the first to apply the concept of strategy to management wereH. Igor Ansoff in Corporate Strategy: An Analytic AppToach to Bii.sinessPolicy for GrowJb and Expansion (New York: McGraw-Hill, 1965| andKenneth R, Andrews in The Concept of Cozpoiate Strategy IHomewood,ni.: Dow Jones-Irwin, 1971).

the basic concepts of strategy.' As "strategy" hasblossomed, the competitiveness of Western compa-nies has withered. This may be coincidence, but wethink not. We believe that the application of conceptssuch as "strategic fit" (hetween resources and oppor-tunities), "generic strategies" (low cost vs. differenti-ation vs. focus), and the "strategy hierarchy" (goals,strategies, and tactics) have often ahetted the processof competitive decline. The new global competitorsapproach strategy from a perspective that is funda-

A company's strategiccrthodoxies aremere dangerous than itswell-financed rivais.

mentally different from that which underpins West-ern management thought. Against such competi-tors, marginal adjustments to current orthodoxiesare no more likely to produce competitive revitali-zation than are marginal improvements in operat-

Gary Hamel is lecturer in business policy and manage-ment at the London Business School. C.K. Prahalad isprofessor of corporate strategy and international busi-ness at the University of Michigan. Their most recentHBR article is "Collaborate with Your Compeititors-and Win" (January-February 1989), with Yves L. Doz.

HARVARD BUSINESS REVIEW May-June 1989 63

STRATEGIC INTENT

ing efficiency. (The insert, "Remaking Strategy,"describes our research and summarizes the two con-trasting approaches to strategy we see in large,multinational companies.)

ew Western companies have an enviable trackrecord anticipating the moves of new globalcompetitors. Why? The explanation beginswith the way most companies have approached

competitor analysis. Typically, competitor analysisfocuses on the existing resources (human, technical,and financial) of present competitors. The onlycompanies seen as a threat are those with the re-sources to erode margins and market share in tbenext planning period. Resourcefulness, the pace atwhich new competitive advantages are being built,rarely enters in.

In tbis respect, traditional competitor analysis islike a snapshot of a moving car. By itself, the photo-graph yields little information about the car's speedor direction-whether the driver is out for a quietSunday drive or warming up for the Grand Prix. Yetmany managers have learned through painful experi-ence that a business's initial resource endowment(whether bountiful or meager) is an unreliable predic-tor of future global success.

Think back. In 1970, few Japanese companies pos-sessed the resource base, manufacturing volume, ortechnical prowess of U.S. and European industryleaders. Komatsu was less than 35% as large as Cater-pillar (measured by sales), was scarcely representedoutside Japan, and relied on just one product l ine-small bulldozers - for most of its revenue. Honda wassmaller than American Motors and had not yet be-gun to export cars to tbe United States. Canon's first

ITraditional competitoranaiysis is iike a snapsinotof G moving car.

halting steps in the reprographics business lookedpitifully small compared with tbe $4 bilhon Xeroxpowerhouse.

If Western managers had extended their competi-tor analysis to include these companies, it wouldmerely have underlined how dramatic the resourcediscrepancies between them were. Yet by 1985, Ko-matsu was a $2.8 billion company with a productscope encompassing a broad range of earth-movingequipment, industrial robots, and semiconductors.Honda manufactured almost as many cars world-wide in 1987 as Chrysler. Canon had matched Xerox'sglobal unit market share.

Tbe lesson is clear: assessing the current tacticaladvantages of known competitors will not help youunderstand the resolution, stamina, and inventive-ness of potential competitors. Sun-tzu, a Chinesemilitary strategist, made the point 3,000 years ago:"All men can see the tactics whereby I conquer," hewrote, "but what none can see is the strategy out ofwhich great victory is evolved."

y' Sy ompanies that have risen to global leader-( ship over the past 20 years invariably beganY with ambitions that were out of all propor-V . ^ . . ^ tion to their resources and capabilities. But

they created an obsession with wirming at all levelsof the organization and then sustained that obsessionover the 10-to 20-year quest for global leadership. Weterm tbis obsession "strategic intent."

On the one hand, strategic intent envisions a de-sired leadership position and establishes the crite-rion the organization will use to chart its progress.Komatsu set out to "Encircle Caterpillar." Canonsought to "Beat Xerox." Honda strove to become asecond Ford-an automotive pioneer. All are expres-sions of strategic intent.

At tbe same time, strategic intent is more thansimply unfettered ambition. (Many companies pos-sess an ambitious strategic intent yet fall short oftheir goals.} The concept also encompasses an activemanagement process that includes: focusing the or-ganization's attention on the essence of winning;motivating people by communicating the value ofthe target; leaving room for individual and teamcontributions; sustaining enthusiasm by providingnew operational definitions as circumstances change;and using intent consistently to guide resourceallocations.

Strategic intent captures the essence of winning.The Apollo program-landing a man on the moonahead of the Soviets-was as competitively focusedas Komatsu's drive against Caterpillar. The space pro-gram became the scorecard for America's technologyrace with the USSR. In the turbulent informationtechnology industry, it was hard to pick a single com-petitor as a target, so NEC's strategic intent, set in theearly 1970s, was to acquire the technologies thatwould put it in the best position to exploit the con-vergence of computing and telecommunications.Otber industry observers foresaw this convergence,but only NEC made convergence tbe guiding themefor subsequent strategic decisions by adopting "com-puting and communications" as its intent. For Coca-Cola, strategic intent has been to put a Coke within"arm's reach" of every consumer in the world.

Strategic intent is stable over time. In battles forglobal leadership, one of the most critical tasks is to

64 HARVARD BUSINESS REVIEW May-[une 1989

Remaking StrategyOver the last ten years, our research on global

competition, international alliances, and multina-tional management has brouglit us into close con-tact with senior managers in America, Europe, andJapan. As we tried to unravel the reasons for successand surrender in glohal markets, we became moreand more suspicious that executives in Western andFar Eastern companies often operated with very dif-ferent conceptions of competitive strategy. Under-standing these differences, we thought, might helpexplain the conduct and outcome of competitivebattles as well as supplement tradi-tional explanations for Japan's as-cendance and the West's decline.

We began by mapping the im-plicit strategy models of managerswho had participated in our re-search. Then we built detailed his-tories of selected competitivebattles. We searched for evidence ofdivergent views of strategy, com-petitive advantage, and the role oftop management.

TWo contrasting models of strat-egy emerged. One, which mostWestern managers will recognize, centers on theproblem of maintaining strategic fit. The other cen-ters on the problem of leveraging resources. The twoare not mutually exclusive, but they represent a sig-nificant difference in emphasis-an emphasis thatdeeply affects how competitive battles get playedout over time.

Both models recognize the problem of competingin a hostile environment with limited resources.But while the emphasis in the first is on trimmingambitions to match available resources, the empha-sis in the second is on leveraging resources to reachseemingly unattainable goals.

Both models recognize that relative competitiveadvantage determines relative profitability. Thefirst emphasizes the search for advantages thatare inherently sustainable, the second emphasizesthe need to accelerate organizational learning tooutpace competitors in building new advantages,

Both models recognize the difficulty of compet-ing against larger competitors. But while the first

leads to a search for niches (or simply dissuades thecompany from challenging an entrenched competi-tor), the second produces a quest for new rules thatcan devalue the incumbent's advantages.

Both models recognize that balance in the scopeof an organization's activities reduces risk. The firstseeks to reduce financial risk by building a balancedportfolio of cash-generating and cash-consumingbusinesses. The second seeks to reduce competitiverisk by ensuring a well-balanced and sufficientlybroad portfolio of advantages.

Both models recognize the needto disaggregate the organization ina way that allows top managementto differentiate among the invest-ment needs of various planningunits. In the first model, resourcesare allocated to product-marketunits in which relatedness is de-fined by common products, chan-nels, and customers. Each businessis assumed to own all the criticalskills it needs to execute its strat-egy successfully. In the second, in-vestments are made in core com-

petences (microprocessor controls or electronicimaging, for example) as well as in product-marketunits. By tracking these investments across busi-nesses, top management works to assure that theplans of individual strategic units don't underminefuture developments by default.

Both models recognize the need for consistency inaction across organizational levels. In the first, con-sistency between corporate and business levels islargely a matter of conforming to financial objec-tives. Consistency between business and functionallevels comes by tightly restricting the means thebusiness uses to achieve its strategy-establishingstandard operating procedures, defining the servedmarket, adhering to accepted industry practices. Inthe second model, business-corporate consistencycomes from allegiance to a particular strategic in-tent. Business-functional consistency comes fromallegiance to intermediate-term goals, or chal-lenges, with lower level employees encouraged toinvent how those goals will be achieved.

lengthen the organization's attention span. Strategicintent provides consistency to short-term action,while leaving room for reinterpretation as new op-portunities emerge. At Komatsu, encircling Caterpil-lar encompassed a succession of medium-termprograms aimed at exploiting specific weaknesses in

Caterpillar or building particular competitive ad-vantages. When Caterpillar threatened Komatsu inJapan, for example, Komatsu responded by first im-proving quality, tben driving down costs, then cul-tivating export markets, and then underwriting newproduct development.

DRAWING BY GARISON WEILAND 65

STRATEGIC INTENT

Strategic intent sets a target that deserves per-sonal effort and commitment. Ask the chairmen ofmany American corporations how they measuretheir contributions to their companies' success andyou're likely to get an answer expressed in terms ofshareholder wealth. In a company that possesses astrategic intent, top management is more likely totalk in terms of global market leadership. Marketshare leadership typically yields shareholder wealth,to be sure. But the two goals do not have the samemotivational impact. It is hard to imagine middlemanagers, let alone blue-collar employees, wakingup each day with the sole thought of creating moreshareholder wealth. But mightn't they feel differ-ent given the challenge to "Beat Benz"-the rallyingcry at one Japanese auto producer? Strategic intentgives employees the only goal that is worthy ofcommitment: to unseat the best or remain thebest, worldwide.

any companies are more familiar withstrategic planning than they are withstrategic intent. The planning processtypically acts as a "feasibility sieve."

Strategies are accepted or rejected on the basis ofwhether managers can be precise about the "how" aswell as the "what" of their plans. Are the milestonesclear? Do we have the necessary skills and resources?How will competitors react? Has the market beenthoroughly researched? In one form or another, theadmonition "Be realistic!" is given to line managersat almost every turn.

But can you plan for global leadership? Did Ko-matsu, Canon, and Honda have detailed, 20-year"strategies" for attacking Western markets? Are Jap-anese and Korean managers better planners thantheir Western counterparts? No. As valuable as stra-tegic planning is, global leadership is an objectivethat lies outside the range of planning. We know offew companies with highly developed planning sys-tems that have managed to set a strategic intent. Astests of strategic fit become more stringent, goalsthat cannot be planned for fall hy the wayside. Yetcompanies that are afraid to commit to goals that lieoutside the range of planning are unlikely to becomeglobal leaders.

Although strategic planning is billed as a way ofbecoming more future oriented, most managers,when pressed, will admit that their strategic plans re-veal more about today's problems than tomorrow'sopportunities. With a fresh set of problems confront-ing managers at the beginning of every planning cy-cle, focus often shifts dramatically from year to year.And with the pace of change accelerating in most in-dustries, the predictive horizon is becoming shorter

and shorter. So plans do little more than project thepresent forward incrementally. The goal of strategicintent is to fold the future back into the present. Theimportant question is not "How will next year be dif-ferent from this year?" but "What must we do differ-ently next year to get closer to our strategic intent?"Only with a carefully articulated and adhered to stra-tegic intent will a succession of year-on-year planssum up to global leadership.

ust as you cannot plan a 10- to 20-year quest forglobal leadership, the chance of falling into aleadership position by accident is also remote.We don't believe that global leadership comes

from an undirected process of intrapreneurship. Noris it the product of a skunkworks or other techniquesfor internal venturing. Behind such programs lies anihilistic assumption: the organization is so hide-bound, so orthodox ridden that the only way to inno-vate is to put a few bright people in a dark room, pourin some money, and hope that something wonderfulwill happen. In this "Silicon Valley" approach to in-novation, the only role for top managers is to retrofittheir corporate strategy to the entrepreneurial suc-cesses that emerge from below. Here the value addedof top management is low indeed.

Sadly, this view of innovation may be consistentwith the reality in many large companies.^ On theone hand, top management lacks any particular pointof view about desirable ends beyond satisfying share-holders and keeping raiders at bay. On the other, theplanning format, reward criteria, definition of servedmarket, and belief in accepted industry practice all

Planners ask "How will nextyear be different?"Winners ask "What mustwe do differentiy?"

work together to tightly constrain the range of avail-able means. As a result, innovation is necessarily anisolated activity. Growth depends more on the inven-tive capacity of individuals and small teams than onthe ability of top management to aggregate the ef-forts of multiple teams towards an ambitious strate-gic intent.

In companies that overcame resource constraintsto build leadership positions, we see a different rela-tionship between means and ends. While strategic in-tent is clear about ends, it is flexible as to means-it

2. Robert A. Burgelman, "A Process Model of Internal Corporate Venturingin the Diversified Major Finn," Administrative Science Quarterly, [une1983.

66 HARVARD BUSINESS REVIEW May-June 1989

leaves room for improvisation. Achieving strategicintent requires enormous creativity with respect tomeans: witness Fujitsu's use of strategic alliances inEurope to attack IBM. But this creativity comes inthe service of a clearly prescribed end. Creativity isunbridled, but not uncorralled, because top manage-ment establishes the criterion against which em-ployees can pretest the logic of their initiatives.Middle managers must do more than deliver onpromised financial targets,- they must also deliver onthe broad direction implicit in their organization'sstrategic intent.

trategic intent implies a sizable stretch for anorganization. Current capabilities and re-sources will not suffice. This forces the organi-zation to be more inventive, to make the most

of limited resources. Whereas the traditional view ofstrategy focuses on the degree of fit between existingresources and current opportunities, strategic intentcreates an extreme misfit between resources and am-bitions. Top management then challenges the organi-zation to close the gap by systematically buildingnew advantages. For Canon this meant first under-standing Xerox's patents, then licensing technologyto create a product that would yield early market ex-perience, then gearing up internal R&D efforts, thenlicensing its own technology to other manufactur-ers to fund further R&D, then entering market seg-ments in Japan and Europe where Xerox was weak,and so on.

In this respect, strategic intent is like a marathonrun in 400-meter sprints. No one knows what the ter-rain will look like at mile 26, so the role of top man-agement is to focus the organization's attention onthe ground to be covered in the next 400 meters. Inseveral companies, management did this by present-ing the organization with a series of corporate chal-lenges, each specifying the next hill in the race toachieve strategic intent. One year the challengemight be quality, the next total customer care, thenext entry into new markets, the next a rejuvenatedproduct line. As this example indicates, corporatechallenges are a way to stage the acquisition of newcompetitive advantages, a way to identify the focalpoint for employees' efforts in the near to mediumterm. As with strategic intent, top management isspecific about the ends (reducing product develop-ment times by 75%, for example) but less prescrip-tive about the means.

Like strategic intent, challenges stretch the organi-zation. To preempt Xerox in the personal copier busi-ness. Canon set its engineers a target price of $1,000for a home copier. At the time. Canon's least expen-sive copier sold for several thousand dollars. Trying to

reduce the cost of existing models would not havegiven Canon the radical price-performance improve-ment it needed to delay or deter Xerox's entry intopersonal copiers. Instead, Canon engineers were chal-lenged to reinvent the copier-a challenge they metby substituting a disposable cartridge for the com-plex image-transfer mechanism used in other copiers.

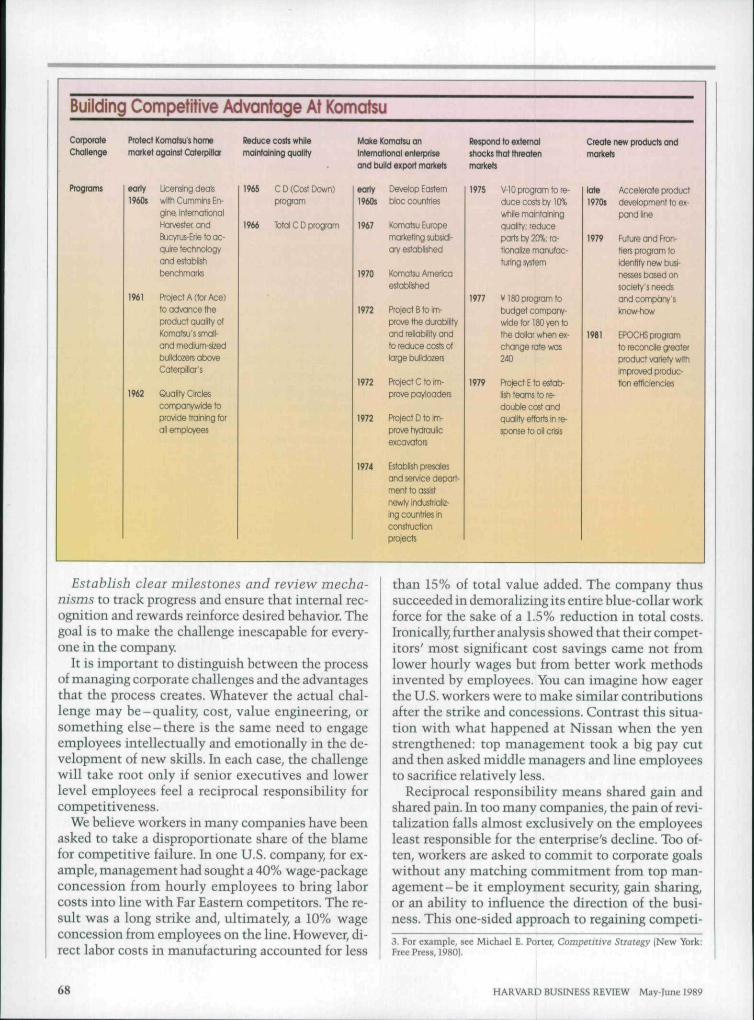

Corporate challenges come from analyzing com-petitors as well as from the foreseeable pattern ofindustry evolution. Together these reveal potentialcompetitive openings and identify the new skillsthe organization will need to take the initiativeaway from better positioned players. The exhibit,"Building Competitive Advantage at Komatsu," il-lustrates the way challenges helped that companyachieve its intent.

For a challenge to be effective, individuals andteams throughout the organization must understandit and see its implications for their own jobs. Compa-nies that set corporate challenges to create new com-petitive advantages (as Ford and IBM did with qualityimprovement) quickly discover that engaging the en-tire organization requires top management to:

Create a sense of urgency, or quasi crisis, by am-plifying weak signals in the environment that pointup the need to improve, instead of allowing inaction

The "Silicon Valley" approachto innovation: put a fewbright peopie in a dark room,pour in money, and hope.

to precipitate a real crisis. (Komatsu, for example,budgeted on the basis of worst case exchange ratesthat overvalued the yen.)

Develop a competitor focus at every level throughwidespread use of competitive intelligence. Everyemployee should be able to benchmark his or her ef-forts against best-in-class competitors so that thechallenge becomes personal. (For example. Fordshowed production-line workers videotapes of opera-tions at Mazda's most efficient plant.)

Provide employees with the skills they need towork effectively-tiainin^ in statistical tools, prob-lem solving, value engineering, and team building,for example.

Give the organization time to digest one challengebefore launching another When competing initia-tives overload the organization, middle managers of-ten try to protect their people from the whipsaw ofshifting priorities. But this "wait and see if they'reserious this time" attitude ultimately destroys thecredibility of corporate challenges.

HARVARD BUSINESS REVIEW Maylune 1989 67

Building Competitive Advantage At Komatsu

Cofporate Pfotecl Komatsu s home Reduce costs while

Challenge morket agoinst Caterpillar maintaining quality

Programs early Licensing deols

1960$ witti Cummins En-

gine, International

Harvester, and

Bucyrus-Erie to ac-

quire technology

ond estabii^

benctvnorks

1961 Project A (tor Ace)

to advance the

product quality of

Komotsu'ssmall-

and rrodiunvsizedbulldozers above

Coterpiitar's

m2 Quality Circles

companywide to

provide training far

all employees

1965 C D (Cost Down)

program

1966 Total C D progrom

Malte Komatsu an

International enterprise

and build export markets

early Develop Eastern

1960s bloc countries

1967 tomatsu Europe

marketing subsidi-

ary established

1970 Komatsu America

established

1972 Project B to Im-

prove the durability

and reliobility and

to reduce costs of

large bulldozers

1972 Project C to im-

prove payioaders

1972 Project D to im-

prove li^raulic

excavators

1974 Establish presoles

artd service depart-

ment to ossist

newly industrializ-

ing countries inconstruction

prajects

Respond to extemai

stiocks that ttireaten

markets

1975 V-iO program to re-

duce costs b/ 10%

while maintaining

quolity: reduce

parts t v 20%, ra-

tionailze monufoc-

turing system

1977 V 180 program tobudget compan)'-

widetor 180 yen to

the ddlaf when ex-

change rale was

240

1979 Project E to estab-

lish teoms to re-

double cost ond

quality efforts in re-

SJonse to oii crisis

Cieate new products andmarkets

kite Accelerate product

1970s development to ex-

pand line

1979 Future and Fron-

tiers program to

Identify new txisi-

nesses based on

society's needs

and company'sknow-how

1961 EPOCHSprogram

to reconcile greater

product variety with

Improved produc-

tion etticiencies

Establish clear milestones and review mecha-nisms to track progress and ensure that internal rec-ognition and rewards reinforce desired behavior. Thegoal is to make the challenge inescapable for every-one in the company.

It is important to distinguish between the processof managing corporate challenges and the advantagesthat the process creates. Whatever the actual chal-lenge may be-quality, cost, value engineering, orsomething else-there is the same need to engageemployees intellectually and emotionally in the de-velopment of new skills. In each case, the challengewill take root only if senior executives and lowerlevel employees feel a reciprocal responsibility forcompetitiveness.

We believe workers in many companies have beenasked to take a disproportionate share of the blamefor competitive failure. In one U.S. company, for ex-ample, management had sought a 40% wage-packageconcession from hourly employees to bring laborcosts into line with Far Eastern competitors. The re-sult was a long strike and, ultimately, a 10% wageconcession from employees on the line. However, di-rect labor costs in manufacturing accounted for less

68

than 15% of total value added. The company thussucceeded in demoralizing its entire blue-collar workforce for the sake of a 1.5% reduction in total costs.Ironically, further analysis showed that their compet-itors' most significant cost savings came not fromlower hourly wages but from better work methodsinvented by employees. You can imagine how eagerthe U.S. workers were to make similar contributionsafter the strike and concessions. Contrast this situa-tion with what happened at Nissan when the yenstrengthened: top management took a big pay cutand then asked middle managers and line employeesto sacrifice relatively less.

Reciprocal responsibility means shared gain andshared pain. In too many companies, the pain of revi-talization falls almost exclusively on the employeesleast responsible for the enterprise's decline. Too of-ten, workers are asked to commit to corporate goalswithout any matching commitment from top man-agement-be it employment security, gain sharing,or an ability to influence the direction of the busi-ness. This one-sided approach to regaining competi-

3. For example, see Michael E. Porter, Competitive Strategy (New York:free Press, 1980).

HARVARD BUSINESS REVIEW May-June 1989

STRATEGIC INTENT

tiveness keeps many companies from hamessing theIntellectual horsepower of their employees.

reating a sense of reciprocal responsibilityis crucial because competitiveness ulti-mately depends on the pace at which acompany embeds new advantages deep

within its organization, not on its stock of advan-tages at any given time. Thus we need to expand theconcept of competitive advantage beyond the score-card many managers now use: Are my costs lower?Will my product command a price premium?

Few competitive advantages are long lasting. Un-covering a new competitive advantage is a bit likegetting a hot tip on a stock: the first person to act onthe insight makes more money than the last. Whenthe experience curve was young, a company thatbuilt capacity ahead of competitors, dropped prices tofill plants, and reduced costs as volume rose went tothe bank. The first mover traded on the fact that com-petitors undervalued market share - they didn't priceto capture additional share because they didn't un-derstand how market share leadership could betranslated into lower costs and better margins. Butthere is no more undervalued market share wheneach of 20 semiconductor companies builds enoughcapacity to serve 10% of the world market.

Keeping score of existing advantages is not thesame as building new advantages. The essence ofstrategy lies in creating tomorrow's competitive ad-vantages faster than competitors mimic the ones youpossess today. In the 1960s, Japanese producers reliedon labor and capital cost advantages. As Westernmanufacturers began to move production offshore,Japanese companies accelerated their investment inprocess technology and created scale and quality ad-vantages. Then as their U.S. and European competi-tors rationalized manufacturing, they added anotherstring to their bow by accelerating the rate of productdevelopment. Then they built global brands. Thenthey deskilled competitors through alliances andoutsourcing deals. The moral? An organization's ca-pacity to improve existing skills and leam new onesis the most defensible competitive advantage of all.

"o achieve a strategic intent, a company mustusually take on larger, better financed competi-tors. That means carefully managing competi-tive engagements so that scarce resources are

conserved. Managers cannot do that simply by play-ing the same game better-making marginal im-provements to competitors' technology and businesspractices. Instead, they must fundamentally changethe game in ways that disadvantage incumbents-devising novel approaches to market entry, advan-

tage building, and competitive warfare. For smartcompetitors, the goal is not competitive imitationbut competitive innovation, the art of containingcompetitive risks within manageable proportions.

Four approaches to competitive innovation are ev-ident in the global expansion of Japanese companies.These are: building layers of advantage, searching forloose bricks, changing the terms of engagement, andcompeting through collaboration.

The wider a company's portfolio of advantages, theless risk it faces in competitive battles. New globalcompetitors have built such portfolios by steadily ex-panding their arsenals of competitive weapons. Theyhave moved inexorably from less defensible advan-tages such as low wage costs to more defensible ad-vantages like global brands. The Japanese colortelevision industry illustrates this layering process.

By 1967, Japan had become the largest producer ofblack-and-white television sets. By 1970, it was clos-ing the gap in color televisions. Japanese manufactur-ers used their competitive advantage-at that time,primarily, low labor costs-to build a base in theprivate-label business, then moved quickly to estab-

To keep the pressure on.Komatsu set itsbudgets on the basis of aneven stronger yen.

Ush world-scale plants. This investment gave themadditional layers of advantage-quality and reli-ability-as well as further cost reductions from pro-cess improvements. At the same time, they recog-nized that these cost-based advantages were vulner-able to changes in labor costs, process and producttechnology, exchange rates, and trade policy. Sothroughout the 1970s, they also invested heavily inbuilding channels and brands, thus creating anotherlayer of advantage, a global franchise. In the late1970s, they enlarged the scope of their products andbusinesses to amortize these grand investments, andby 1980 all the major players-Matsushita, Sharp,Toshiba, Hitachi, Sanyo-had established related setsof businesses that could support global marketing in-vestments. More recently, they have been investingin regional manufacturing and design centers to tai-lor their products more closely to national markets.

These manufacturers thought of the varioussources of competitive advantage as mutually desir-able layers, not mutually exclusive choices. Whatsome call competitive suicide - pursuing both costand differentiation-is exactly what many competi-tors strive for.' Using flexible manufacturing tech-

HARVARD BUSINESS REVIEW May-June 1989

STRATEGIC INTENT

nologies and better marketing intelligence, theyare moving away from standardized "world prod-ucts" to products like Mazda's mini-van, developedin Califomia expressly for the U.S. market.

Another approach to competitive innova-tion-searching for loose bricks-exploitsthe benefits of surprise, which is just as use-ful in business battles as it is in war Par-

ticularly in the early stages of a war for global mar-kets, successful new competitors work to stay be-low the response threshold of their larger, morepowerful rivals. Staking out underdefended territoryis one way to do this.

To find loose bricks, managers must have feworthodoxies about how to break into a market orchallenge a competitor. For example, in one large U.S.multinational, we asked several country managers todescribe what a Japanese competitor was doing in thelocal market. The first executive said, "They're com-ing at us in the low end. Japanese companies alwayscome in at the bottom." The second speaker foundthe comment interesting but disagreed: "They don'toffer any low-end products in my market, but theyhave some exciting stuff at the top end. We reallyshould reverse engineer that thing." Another col-league told still another story. "They haven't takenany business away from me," he said, "but they'vejust made me a great offer to supply components." Ineach country, their Japanese competitor had found adifferent loose brick.

The search for loose bricks begins with a carefulanalysis of the competitor's conventional wisdom:How does the company define its "served market"?What activities are most profitable? Which geo-graphic markets are too troublesome to enter? Theobjective is not to find a corner of the industry (orniche) where larger competitors seldom tread but tobuild a base of attack just outside the market terri-

Honda was building a oorecompetence in engines,its U.S. rivais saw oniy 50 ccmotoroycies.

tory that industry leaders currently occupy. The goalis an uncontested profit sanctuary, which could be aparticular product segment (the "low end" in motor-cycles), a slice of the value chain (components in thecomputer industry), or a particular geographic mar-ket (Eastern Europe).

When Honda took on leaders in the motorcycle in-dustry, for example, it began with products that were

just outside the conventional definition of the lead-ers' product-market domains. As a result, it couldbuild a base of operations in underdefended territoryand then use that base to laimch an expanded attack.What many competitors failed to see was Honda'sstrategic intent and its growing competence in en-gines and power trains. Yet even as Honda was sell-ing 50cc motorcycles in the United States, it wasalready racing larger bikes in Europe-assemblingthe design skills and technology it would need for asystematic expansion across the entire spectrum ofmotor-related businesses.

Honda's progress in creating a core competencein engines should have wamed competitors that itmight enter a series of seemingly unrelated indus-tries-automobiles, lawn mowers, marine engines,generators. But with each company fixated on itsown market, the threat of Honda's horizontal di-versification went unnoticed. Today companies likeMatsushita and Toshiba are similarly poised to movein unexpected ways across industry boundaries. Inprotecting loose bricks, companies must extend theirperipheral vision by tracking and anticipating themigration of global competitors across product seg-ments, businesses, national markets, value-addedstages, and distribution channels.

Changing the terms of engagement-refus-ing to accept the front runner's definitionof industry and segment boundaries-represents still another form of competi-

tive innovation. Canon's entry into the copier busi-ness illustrates this approach.

During the 1970s, both Kodak and IBM tried tomatch Xerox's business system in terms of segmen-tation, products, distribution, service, and pricing. Asa result, Xerox had no trouble decoding the new en-trants' intentions and developing countermoves.IBM eventually withdrew from the copier business,while Kodak remains a distant second in the largecopier market that Xerox still dominates.

Canon, on the otber hand, changed the terms ofcompetitive engagement. While Xerox built a widerange of copiers. Canon standardized machines andcomponents to reduce costs. Canon chose to distrib-ute through office-product dealers rather than try tomatch Xerox's huge direct sales force. It also avoidedthe need to create a national service network by de-signing reliability and serviceability into its productand then delegating service responsibility to the deal-ers. Canon copiers were sold rather than leased, free-ing Canon from the burden of financing the leasebase. Finally, instead of selling to the heads of cor-porate duplicating departments. Canon appealed tosecretaries and department managers who wanted

70 HARVARD BUSINESS REVIEW May-June 1989

distributed copying. At each stage. Canon neatlysidestepped a potential barrier to entry.

Canon's experience suggests that there is an im-portant distinction between barriers to entry and bar-riers to imitation. Competitors that tried to matchXerox's business system had to pay the same entrycosts - the barriers to imitation were high. But Canondramatically reduced the barriers to entry by chang-ing the rules of the game.

Changing the rules also short-circuited Xerox'sability to retaliate quickly against its new rival Con-fronted with the need to rethink its business strategyand organization, Xerox was paralyzed for a time. Xe-rox managers realized that the faster they downsizedthe product line, developed new channels, and im-proved reliability, the faster they would erode thecompany's traditional profit base. What might havebeen seen as eritical success factors-Xerox's na-tional sales force and service network, its large in-stalled base of leased machines, and its reliance onservice revenues-instead became barriers to retaha-tion. In this sense, competitive innovation is likejudo: the goal is to use a larger competitor's weightagainst it. And that happens not by matching theleader's capabilities but by developing contrasting ca-pabilities of one's own.

Competitive innovation works on the premisethat a successful competitor is likely to be wedded toa "recipe" for success. That's why the most effectiveweapon new competitors possess is probably a eleansheet of paper. And why an incumbent's greatest vul-nerability is its belief in accepted practice.

'hiough licensing, outsourcing agreements, andjoint ventures, it is sometimes possible to winwithout fighting. For example, Fujitsu's alli-ances in Europe with Siemens and STC (Brit-

ain's largest computer maker) and in the UnitedStates with Amdahl yield manufacturing volumeand access to Western markets. In the early 1980s,Matsushita established a joint venture with Thorn(in the United Kingdom), Telefunken (in Cermany),and Thomson (in France), whieh allowed it toquiekly multiply the forces arrayed against Philips inthe battle for leadership in the European VCR busi-ness. In fighting larger global rivals by proxy, Japaneseeompanies have adopted a maxim as old as humanconflict itself: my enemy's enemy is my friend.

Hijacking the development efforts of potential ri-vals is another goal of competitive collaboration. Inthe consumer electronics war, Japanese competitorsattacked traditional businesses like TVs and hi-fis

4. Strategic frameworks for resource allocation in diversified companiesare summarized in Charles W. Hofer and Dan E. Schendel, Strategy Formu-lation: Analytical Concepts (St. Paul, Minn.: West Publishing, 1978).

while volunteering to manufacture "next genera-tion" products like VCRs, camcorders, and compactdisc players for Western rivals. They hoped their ri-vals would ratchet down development spending, andin most cases that is precisely what happened. Butcompanies that abandoned their own developmentefforts seldom reemerged as serious competitors insubsequent new product battles.

Collaboration can also be used to ealibrate com-petitors' strengths and weaknesses. Toyota's jointventure with GM, and Mazda's with Ford, give theseautomakers an invaluable vantage point for assess-ing the progress their U.S. rivals have made in costreduction, quality, and technology. They can also

Competitive innovation is likejudo: upset your hvols by usingtheir size against them.

leani how GM and Ford compete-when they willfight and when they won't. Of course, the reverseis also true: Ford and GM have an equal opportu-nity to leam from their partner-competitors.

The route to competitive revitalization we havebeen mapping implies a new view of strategy. Strate-gic intent assures consistency in resource allocationover the long term. Clearly articulated corporatechallenges focus the efforts of individuals in themedium term. Finally, competitive irmovation helpsreduce competitive risk in the short term. Thisconsistency in the long term, focus in the mediumterm, and inventiveness and involvement in theshort term provide the key to leveraging limited re-sources in pursuit of ambitious goals. But just asthere is a process of winning, so there is a process ofsurrender. Revitalization requires understandingthat process too.

G iven their technological leadership and ac-cess to large regional markets, how didU.S. and European companies lose theirapparent birthright to dominate global in-

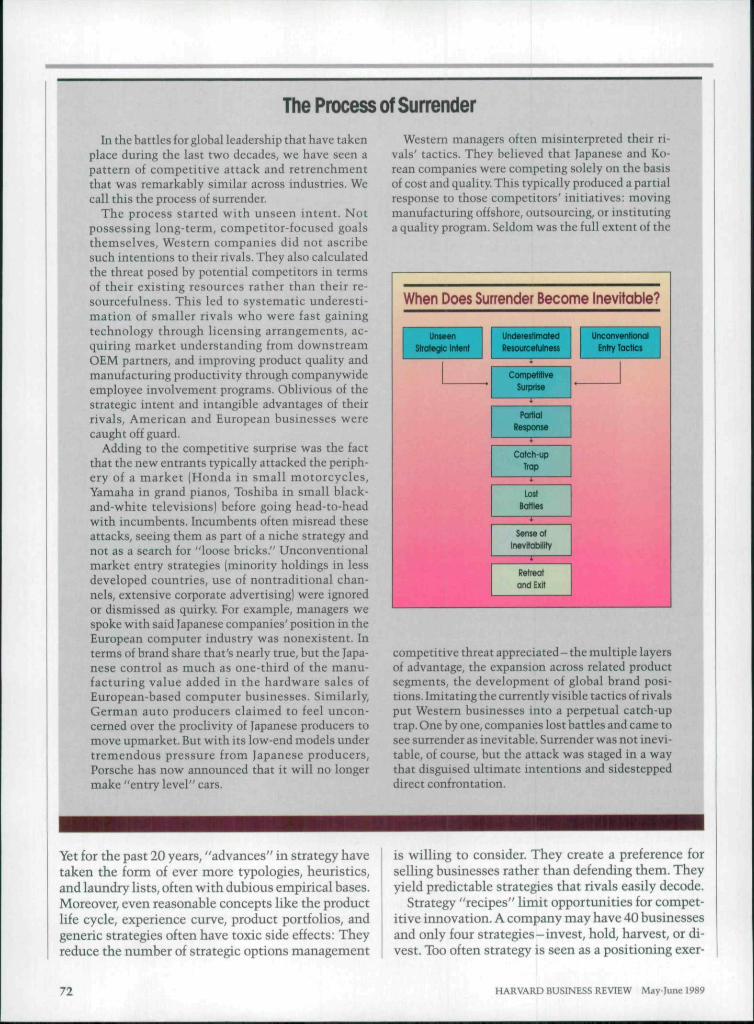

dustries? There is no simple answer. Few companiesrecognize the value of documenting failure. Fewerstill search their own managerial orthodoxies for theseeds for competitive surrender. But we believe thereis a pathology of surrender (surrmiarized in "The Pro-cess of Surrender") that gives some important clues.

It is not very comforting to think that the essenceof Western strategic thought can be reduced to eightrules for excellence, seven S's, five competitiveforces, four product life-cyele stages, three genericstrategies, and innumerable two-by-two matrices.*'

HARVARD BUSINESS REVIEW May-June 1989 71

The Process of SurrenderIn the battles for global leadership that have taken

place during the last two decades, we have seen apattern of competitive attack and retrenchmentthat was remarkably similar across industries. Wecall tbis the process of surrender.

The process started witb unseen intent. Notpossessing long-term, competitor-focused goalsthemselves, Western companies did not ascribesuch intentions to their rivals. They also calculated

JJ the threat posed by potential competitors in termsof their existing resources ratber than their re-sourcefulness. This led to systematic underesti-mation of smaller rivals who were fast gainingtechnology through hcensing arrangements, ac-quiring market understanding from downstreamOEM partners, and improving product quality andmanufacturing productivity through companywideemployee involvement programs. Oblivious of thestrategic intent and intangible advantages of theirrivals, American and European businesses werecaught off guard.

Adding to the competitive surprise was the factthat the new entrants typically attacked the periph-ery of a market (Honda in small motorcycles,Yamaha in grand pianos, Toshiba in small black-and-white televisions) before going head-to-headwith incumbents. Incumbents often misread theseattacks, seeing them as part of a niche strategy andnot as a search for "loose bricks." Unconventionalmarket entry strategies (minority holdings in lessdeveloped countries, use of nontraditional chan-nels, extensive corporate advertising) were ignoredor dismissed as quirky. For example, managers wespoke with said Japanese companies' position in theEuropean computer industry was nonexistent. Interms of brand share that's nearly true, but the Japa-nese control as much as one-third of the manu-facturing value added in the hardware sales ofEuropean-hased computer businesses. Similarly,German auto producers claimed to feel uncon-cerned over the proclivity of Japanese producers tomove upmarket. But with its low-end models undertremendous pressure from Japanese producers,Porsche has now announced that it will no longermake "entry level" cars.

Western managers often misinterpreted their ri-vals' tactics. They believed that Japanese and Ko-rean companies were competing solely on the basisof cost and quality. This typically produced a partialresponse to tbose competitors' initiatives: movingmanufacturing offshore, outsourcing, or institutinga quality program. Seldom was the full extent of the

When Does Surrender Become Inevitable?

UntMn

1 —»Underestimated

Resourcefulness

*Compvlittve

Surprise

Partial

Response

*Catch-up

+

Lost

Battles

*Sense of

Irwvltablltty

+Retreat

and Exit

*—

Unconventional

Entry Toctics

competitive threat appreciated - the multiple layersof advantage, the expansion across related productsegments, the development of global brand posi-tions. Imitating the currently visible tactics of rivalsput Western businesses into a perpetual catch-uptrap. One by one, companies lost battles and came tosee surrender as inevitable. Surrender was not inevi-table, of course, but the attack was staged in a waythat disguised ultimate intentions and sidesteppeddirect confrontation.

Yet for the past 20 years, "advances" in strategy havetaken the fonn of ever more typologies, heuristics,and laundry lists, often with dubious empirical bases.Moreover, even reasonable concepts like the productlife cycle, experience curve, product portfolios, andgeneric strategies often have toxic side effects: Theyreduce the numher of strategic options management

is willing to consider. They create a preference forselling businesses rather than defending them. Theyyield predictable strategies that rivals easily decode.

Strategy "recipes" limit opportunities for compet-itive innovation. A company may have 40 businessesand only four strategies - invest, hold, harvest, or di-vest. Too often strategy is seen as a positioning exer-

72 HARVARD BUSINESS REVIEW May-June 1989

STRATEGIC INTENT

cise in which options are tested by how they fit theexisting industry structure. But current industrystructure reflects the strengths of the industryleader; and playing by the leader's rules is usuallycompetitive suicide.

Armed with concepts like segmentation, the valuechain, competitor benchmarking, strategic groups,and mobility barriers, many managers have becomebetter and hetter at drawing industry maps. But whilethey have been busy map making, their competitorshave heen moving entire continents. The strategist'sgoal is not to find a niche within the existing indus-try space hut to create new space that is uniquelysuited to the company's own strengths, space that isoff the map.

This is particularly true now that industry bound-aries are hecoming more and more unstahle. In in-dustries such as financial services and communica-

I Playing by the industry leader'srules is competitive suicide.

tions, rapidly changing technology, deregulation, andglobalization have undermined the value of tradi-tional industry analysis. Map-making skills areworth little in the epicenter of an earthquake. But anindustry in upheaval presents opportunities forambitious companies to redraw the map in theirfavor, so long as they can think outside traditionalindustry boundaries.

Concepts like "mature" and "declining" arelargely definitional. What most executives meanwhen they label a business mature is that salesgrowth has stagnated in their current geographicmarkets for existing products sold through existingcharmels. In such cases, it's not the industry that ismature, but the executives' conception of the indus-try. Asked if the piano husiness was mature, a seniorexecutive in Yamaha replied, "Only if we can't takeany market share from anyhody anywhere in theworld and still make money. And anyway, we're notin the 'piano' business, we're in the 'keyboard' busi-ness." Year after year, Sony has revitalized its radioand tape recorder businesses, despite the fact thatother manufacturers long ago ahandoned these busi-nesses as mature.

A narrow concept of maturity can foreclose a com-pany from a broad stream of future opportunities. Inthe 1970s, several U.S. companies thought that con-sumer electronics had become a mature industry.What could possibly top the color TV? they askedthemselves. RCA and CE, distracted by opportuni-ties in more "attractive" industries like mainframecomputers, left Japanese producers with a virtual

monopoly in VCRs, camcorders, and compact discplayers. Ironically, the TV business, once thought ma-ture, is on the verge of a dramatic renaissance. A $20billion-a-year husiness will he created when high-definition television is launched in the UnitedStates. But the pioneers of television may captureonly a small part of this bonanza.

Most of the tools of strategic analysis are focuseddomestically. Few force managers to consider globalopportunities and threats. For example, portfolioplanning portrays top management's investment op-tions as an array of businesses rather than as an arrayof geographic markets. The result is predictable: asbusinesses come under attack from foreign competi-tors, the company attempts to abandon them and en-ter others in which the forces of global competitionare not yet so strong. In the short term, this may he anappropriate response to waning competitiveness, butthere are fewer and fewer businesses in which adomestic-oriented company can find refuge. We sel-dom hear such companies asking: Can we move intoemerging markets overseas ahead of our glohal rivalsand prolong the profitability of this business? Can wecounterattack in our glohal competitors' home mar-kets and slow the pace of their expansion? A seniorexecutive in one successful glohal company made atelling comment; "We're glad to find a competitormanaging by the portfolio concept-we can almostpredict how much share we'll have to take away toput the business on the CEO's 'sell list.'"

Companies can also be overcommitted to or-ganizational recipes, such as strategic husi-ness units and the decentralization an SBUstructure implies. Decentralization is se-

ductive because it places the responsibility for suc-cess or failure squarely on the shoulders of linemanagers. Each business is assumed to have all theresources it needs to execute its strategies success-fully, and in this no-excuses environment, it is hardfor top management to fail. But desirable as clearlines of responsibility and accountability are, com-petitive revitalization requires positive value addedfrom top management.

Few companies with a strong SBU orientationhave huilt successful global distribution and brandpositions. Investments in a glohal brand franchisetypically transcend the resources and risk propensityof a single business. While some Western companieshave had global brand positions for 30 or 40 years ormore (Heinz, Siemens, IBM, Ford, and Kodak, for ex-ample), it is hard to identify any American or Euro-pean company that has created a new global brandfranchise in the last 10 to 15 years. Yet Japanese com-panies have created a score or more-NEC, Fujitsu,

HARVARD BUSIhfESS REVTEW May-Tune 1989 73

STRATEGIC INTENT

Panasonic (Matsushita), Toshiba, Sony, Seiko, Epson,Canon, Minolta, and Honda, among them.

Ceneral Electric's situation is typical. In many ofits businesses, this American giant has been almostunknown in Europe and Asia. GE made no coordi-nated effort to build a global corporate franchise. AnyGE business with international ambitions had tobear the hurden of establishing its credibility and cre-dentials in the new market alone. Not surprisingly,some once-strong GE businesses opted out of the dif-ficult task of building a glohal brand position. In con-trast, smaller Korean companies like Samsung,Daewoo, and Lucky Gold Star are busy buildinggiobal-hrand umbrellas that will ease market entry

Can you name onegiobai brand developedby a U.S. companyin the last ten years?

for a whole range of businesses. The underlying prin-ciple is simple: economies of scope may be as impor-tant as economies of scale in entering glohal markets.But capturing economies of scope demands inter-business coordination that only top managementcan provide.

We believe that inflexible SBU-type organizationshave also contributed to the deskilling of somecompanies. For a single SBU, incapable of sustaininginvestment in a core competence such as semicon-ductors, optical media, or combustion engines, theonly way to remain competitive is to purchase keycomponents from potential (often Japanese or Ko-rean) competitors. For an SBU defined in product-market terms, competitiveness means offering anend product that is competitive in price and perfor-mance. But that gives an SBU manager little incen-tive to distinguish between external sourcing thatachieves "product embodied" competitiveness andinternal development that yields deeply embeddedorganizational competences that can he exploitedacross multiple businesses. Where upstream com-ponent manufacturing activities are seen as costcenters with cost-plus transfer pricing, additionalinvestment in the core activity may seem a less prof-itable use of capital than investment in downstreamactivities. To make matters worse, internal account-ing data may not reflect the competitive value of re-taining control over core competence.

Together a shared glohal corporate brand franchiseand shared core competence act as mortar in manyJapanese companies. Lacking this mortar, a com-pany's husinesses are truly loose bricks-easily

knocked out by glohal competitors that steadily in-vest in core competences. Such competitors can co-opt domestically oriented companies into long-termsourcing dependence and capture the economies ofscope of global brand investment through interhusi-ness coordination.

Last in decentralization's list of dangers is the stan-dard of managerial performance typically used inSBU organizations. In many companies, husinessunit managers are rewarded solely on the basis oftheir performance against return on investment tar-gets. Unfortunately, that often leads to denominatormanagement because executives soon discover thatreductions in investment and head coun t - thedenominator-"improve" the financial ratios bywhich they are measured more easily than growth inthe numerator-revenues. It also fosters a hair-triggersensitivity to industry downturns that can be veryeostly. Managers who are quick to reduce investmentand dismiss workers find it takes much longer to re-gain lost skills and catch up on investment when theindustry turns upward again. As a result, they losemarket share in every husiness cycle. Particularlyin industries where there is fierce competition forthe hest people and where competitors invest re-lentlessly, denominator management creates a re-trenchment ratchet.

"he concept of the general manager as a mov-able peg reinforces the problem of denomina-tor management. Business schools are guiltyhere because they have perpetuated the no-

tion that a manager with net present value calcula-tions in one hand and portfolio pianning in the othercan manage any business anywhere.

In many diversified companies, top managementevaluates Une managers on numbers alone becauseno other basis for dialogue exists. Managers move somany times as part of their "career development"that they often do not understand the nuances of thebusinesses they are managing. At GE, for example,one fast-track manager heading an important newventure had moved across five businesses in fiveyears. His series of quick successes finally came toan end when he confronted a Japanese competitorwhose managers had been plodding along in the samehusiness for more than a decade.

Regardless of ahility and effort, fast-track manag-ers are unlikely to develop the deep business knowl-edge they need to discuss technology options, com-petitors' strategies, and global opportunities substan-tively. Invariahly, therefore, discussions gravitate to"the numbers," while the value added of managersis limited to the financial and planning savvy theycarry from job to job. Knowledge of the company's in-

74 HARVARD BUSINESS REVIEW May-June 1989

temal planning and accounting systems substitutesfor substantive knowledge of the business, makingcompetitive innovation unlikely.

When managers know that their assignments havea two- to three-year time frame, they feel great pres-sure to create a good track record fast. This pressureoften takes one of two forms. Either the managerdoes not commit to goals whose time line extendsbeyond his or her expected tenure. Or ambitiousgoals are adopted and squeezed into an unrealisti-cally short time frame. Aiming to be number one in abusiness is the essence of strategic intent; but impos-ing a three- to four-year horizon on the effort simplyinvites disaster. Acquisitions are made with littleattention to the problems of integration. The orga-nization becomes overloaded with initiatives. Col-laborative ventures are formed without adequate at-tention to competitive consequences.

Almost every strategic management theoryand nearly every corporate planning systemis premised on a strategy hierarchy in whichcorporate goals guide business unit strat-

egies and business unit strategies guide functionaltactics.^ In this hierarchy senior management makesstrategy and lower levels execute it. The dichotomybetween formulation and implementation is familiarand widely accepted. But the strategy hierarchy un-dermines competitiveness by fostering an elitistview of management that tends to disenfranchisemost of the organization. Employees fail to identifywith corporate goals or involve themselves deeply inthe work of becoming more competitive.

The strategy hierarchy isn't the only explanationfor an elitist view of management, of course. Themyths tbat grow up around successful top man-agers-"Lee Iacocca saved Chrysler," "De Benedet-ti rescued Ohvetti," "John Sculley turned Applearound"-perpetuate it. So does the turbulent busi-ness environment. Middle managers buffeted by cir-cumstances tbat seem to be beyond their controldesperately want to believe that top managementhas all the answers. And top management, in tum,besitates to admit it does not for fear of demoralizinglower level employees.

The result of all this is often a code of silence inwhich the full extent of a company's competitive-ness problem is not widely shared. We interviewedbusiness unit managers in one company, for example,wbo were extremely anxious because top manage-ment wasn't talking openly about the competitivechalienges the company faced. They assumed thelack of conmiunication indicated a lack of awareness

5- For example, see Peter Lorange and Richard f, Vancil, Strategic PlanningSystems lEnglewood Cliffs, N.f.; Prentice-Hal 1,1977).

on their senior managers' part. But when askedwhether tbey were open with tbeir own employees,these same managers replied tbat while they couldface up to the problems, the people below tbem couldnot. Indeed, the only time the work force heard abouttbe company's competitiveness problems was duringwage negotiations when problems were used to ex-tract concessions.

Unfortunately, a threat that everyone perceives butno one talks about creates more anxiety than a threatthat has been clearly identified and made the focalpoint for the problem-solving efforts of the entirecompany That is one reason honesty and humilityon the part of top management may be the first pre-requisite of revitalization, Another reason is the needto make participation more than a buzzword.

Programs such as quality circles and total cus-tomer service often fall short of expectations becausemanagement does not recognize tbat successful im-plementation requires more than administrativestructures. Difficulties in embedding new capabili-ties are typically put down to "communication"problems, with the unstated assumption that if onlydownward communication were more effective - "ifonly middle management would get the messagestraight" - tbe new program would quickly take root.The need for upward communication is often ig-nored, or assumed to mean nothing more tban feed-back. In contrast, Japanese companies win, notbecause they have smarter managers, but becausethey have developed ways to harness the "wisdom ofthe anthill." They realize tbat top managers are a bit

Top managers are likeastronauts-to perform well,they need the intelligenoethat's back on the ground.

like the astronauts who circle the earth in tbe spaceshuttle. It may be the astronauts who get all tbe glory,but everyone knows that the real intelligence behindthe mission is located firmly on the ground.

'here strategy formulation is an elitist ac-tivity it is also difficult to produce trulycreative strategies. For one thing, thereare not enough heads and points of view

in divisional or corporate planning departments tochallenge conventional wisdom. For another, crea-tive strategies seldom emerge from the annual plan-ning ritual. The starting point for next year's strategyis almost always this year's strategy. Improvementsare incremental. The company sticks to the seg-

HARVARD BUSINESS REVIEW May-June 1989 75

STRATEGIC INTENT

ments and territories it knows, even though the realopportunities may be elsewhere. The impetus forCanon's pioneering entry into the personal copierbusiness came from an overseas sales subsidiary-not from planners in Japan.

The goal of the strategy hierarchy remains valid-to ensure consistency up and down the organization.But this consistency is better derived from a clearly

Investors aren't hopelesslyshort-term. They'rejustitiably skeptical oftop management.

articulated strategic intent than from inflexibly ap-plied top-down plans. In the 1990s, the challenge willbe to enfranchise employees to invent the means toaccomplish ambitious ends.

We seldom found cautious administrators amongthe top managements of companies that came frombehind to challenge incumbents for global leader-ship. But in studying organizations that had surren-dered, we invariably found senior managers who, forwhatever reason, lacked the courage to commit theircompanies to heroic goals-goals that lay beyond thereach of planning and existing resources. The conser-vative goals they set failed to generate pressure andenthusiasm for competitive innovation or give theorganization much useful guidance. Financial targetsand vague mission statements just cannot provide

the consistent direction that is a prerequisite for win-ning a glohal competitive war.

This kind of conservatism is usually blamed on thefinancial markets. But we believe that in most casesinvestors' so-called short-term orientation simply re-flects their lack of confidence in the ability of seniormanagers to conceive and dehver stretch goals. Thechairman of one company complained bitterly thateven after improving return on capital employed toover 40% (by ruthlessly divesting lackluster busi-nesses and downsizing others), the stock marketheld the company to an 8:1 price/earnings ratio. Ofcourse the market's message was clear: "We don'ttrust you. You've shown no ability to achieve prof-itable growth. Just cut out the slack, manage the de-nominators, and perhaps you'll be taken over by acompany that can use your resources more creative-ly." Very little in the track record of most large West-ern companies warrants the confidence of thestock market. Investors aren't hopelessly short-term, they're justifiably skeptical.

We believe that top management's caution reflectsa lack of confidence in its own ability to involve theentire organization in revitalization-as opposed tosimply raising financial targets. Developing faith inthe organization's ability to deliver on tough goals,motivating it to do so, focusing its attention longenough to internalize new capabilities-this is thereal challenge for top management. Only by rising tothis challenge will senior managers gain the couragethey need to commit themselves and their compa-nies to global leadership. ^

Reprint 89308

'It's either a shift away from Reaganomics, a shift inmoral values, or an earthquake!"

76 HARVARD BUSINESS REVTEW May-runel989

Harvard Business Review Notice of Use Restrictions, May 2009

Harvard Business Review and Harvard Business Publishing Newsletter content on EBSCOhost is licensed for

the private individual use of authorized EBSCOhost users. It is not intended for use as assigned course material

in academic institutions nor as corporate learning or training materials in businesses. Academic licensees may

not use this content in electronic reserves, electronic course packs, persistent linking from syllabi or by any

other means of incorporating the content into course resources. Business licensees may not host this content on

learning management systems or use persistent linking or other means to incorporate the content into learning

management systems. Harvard Business Publishing will be pleased to grant permission to make this content

available through such means. For rates and permission, contact [email protected].