state universities retirement system of illinois (surs ... · 3 state universities retirement...

TRANSCRIPT

State Universities Retirement System of Illinois (SURS)

Request for Proposal

Private Equity Emerging Manager Fund of Funds Provider Search

December 2012

2

Table of Contents

I. Request For Proposal Summary Statement 3 II. Background Information 3 III. Description of Mandate 5

IV. RFP Specifications 6 V. Projected Schedule of Events 8 VI. Evaluation Criteria 9 VII. Appendices

Appendix A Sudan Divestment Law in Illinois 11 Appendix B Questionnaire 12 Appendix C Questionnaire Accompanying Excel File

3

State Universities Retirement System of Illinois (SURS) Request for Proposal (RFP)

December 2012

Private Equity Emerging Manager Fund of Funds Provider Search

I. RFP Summary Statement The State Universities Retirement System (SURS) requests proposals from qualified private equity fund of funds providers to develop an Emerging Manager portfolio. Emerging Manager is defined as being focused on Ethnic Minority, Women, and Disabled-own Business Enterprises (MWDBE), and initiatives that will assist SURS to comply with Illinois Pension Code 40 ILCS 5/1-109.1. See the Description of Mandate section for a fuller discussion and examples of suitable direct partnerships and strategies. SURS prefers to invest in a commingled fund of funds for diversification enhancement, but will also consider traditional separate account and fund-of-one proposals. Preferred candidates will generally have an established investment history of investing in Emerging Manager partnerships as a stand-alone product. SURS seeks a portfolio that is broadly diversified across key private equity strategies, including venture capital, buyouts, special situations, mezzanine debt and distressed/restructuring partnerships. SURS prefers a portfolio that is primarily (preferably solely) U.S. domestic in geographic orientation, but well-diversified across the various U.S. geographic regions. The key considerations driving the search and selection will be prior experience and success with the Emerging Manager strategy, and appropriate diversification of portfolios by time, industry, and U.S. geography. Respondents must answer all applicable questions in the Questionnaire (Exhibit B) and separate Excel file (Exhibit C) in order to be considered.

II. Background Information Agency Description SURS is the administrator of a cost-sharing, multiple employer public employee retirement system. SURS membership includes employees of public universities, community colleges and other affiliated organizations. Currently, SURS membership totals more than 212,000 active, inactive and retired participants. SURS maintains both a defined benefit and defined contribution plan. Proposals are being solicited for the defined benefit plan. Defined Benefit Plan Investment Program SURS investment program, as of June 30, 2012, totaled $13.6 billion. The approved target asset allocation as of June 30, 2012 is as follows: U.S. Equities – public markets 30.0%

U.S. Equities – private markets 6.0% Non-U.S. Equities 20.0% Global Equities 10.0% Fixed Income 19.0% TIPS 4.0% Real Estate 10.0% Opportunity Fund 1.0%

4

Legislated Investment Restrictions Relating to the Republic of the Sudan and Iran In 2007 the Illinois General Assembly passed Public Act 095-0521, restricting investment in companies domiciled in, managed or controlled by, or doing business with the Republic of the Sudan. SURS investment managers are required by law to abide by the restrictions contained in that Public Act. Appendix A provides information relating to these Sudan-related investment restrictions. The Public Act can be found at http://www.ilga.gov/legislation/publicacts/fulltext.asp?Name=095-0521&GA=95. Additionally, information pertaining to the Iran divestment law, Public Act 095-0616, approved by the Illinois General Assembly on September 11, 2007, can be found at http://www.ilga.gov/legislation/publicacts/fulltext.asp?Name=095-0616. State & Federal Ethics Laws SURS Investment Managers must comply with all applicable laws and regulations of the State of Illinois and the United States of America, including without limitation, the provisions of SEC Rule 206(4)-5. On April 3, 2009, Illinois Governor Pat Quinn signed Public Act 96-0006 into law. Public Act 96-0006 amends the Illinois Governmental Ethics Act and provides guidelines for ethical practices concerning state pension plans. Investment managers seeking to be considered for this mandate should be familiar with, and must comply with, the provisions of this Act. Public Act 96-0006 encourages the Board of Trustees of SURS (“Board”) to increase the racial, ethnic, and gender diversity of its fiduciaries, to the greatest extent feasible within the bounds of financial and fiduciary prudence. In furtherance of this Act, it is the goal of the Board to use its best efforts to increase the racial, ethnic, and gender diversity of its fiduciaries, including its investment managers. The Board encourages minority, female and disabled-owned firms to submit proposals to this RFP. A section of the Illinois Procurement Code concerning prohibitions of political contributions for certain vendors, 30 ILCS 500/50-37 may or may not apply to SURS investment managers. SURS is generally not subject to the Illinois Procurement Code (30 ILCS 500/1-15.100). However, each investment manager should be familiar with the provisions of this section and comply with this section if the investment manager deems it appropriate.

5

III. Description of Mandate

SURS has retained Callan Associates, Inc. to assist in the evaluation and prospective selection of a discretionary private equity manager-of-managers to expand the Fund’s exposure to Emerging Manager Strategy-focused partnerships. Emerging Manager Strategy Defined For the purpose of this mandate, Emerging Manager is defined as focused on Ethnic Minority, Women, and Disabled Business Enterprises (MWDBE). Examples MWD-focused strategies would be commitments to direct partnerships that: 1. Are owned by general partners who qualify as MWDBEs, by virtue of having more than 50%

ownership by MWD individuals 2. Have a strategy of investing in MWD-owned portfolio companies or that have senior

management teams that are primarily constituted of MWD individuals 3. Target companies whose products target MWD end-markets 4. Pursue investments that will enhance employment and career opportunities for MWD

individuals and communities 5. Otherwise promote, through private equity investments, the furthering of opportunity,

advancement and success of MWD individuals 6. Would otherwise allow SURS to comply with Illinois Pension Code 40 ILCS 5/1-109.1. SURS is cognizant that the term Emerging Manager is also used to refer to general partners that are “newer manager organizations”, which are typically firms raising Funds I, II and sometimes III, but are not pursuing an MWD-oriented strategy. For the purpose of this search, that type of partnership investment strategy will be referred to as Developing Managers. While a small amount of Developing Managers may be allowed in the SURS portfolio, Emerging Managers is the sole goal of this mandate. Of note, this search is not focusing on the manager-of-manager organization being qualified as a MWDBE, it is focused on the strategy being MWDBE-oriented. To the degree that the proposing manager-of-managers is a qualified MWDBE, that characteristic will be noted. Portfolio Diversification SURS is seeking a portfolio that will be diversified across key private equity strategies to the broadest degree possible, and prefers the inclusion of venture capital, buyout, special situation, mezzanine and distressed/restructuring partnerships. SURS prefers the portfolio to be domestic U.S. in orientation, but geographically diversified across U.S. regions. SURS intends for this initiative to be ongoing and is seeking diversification across vintage year and by industry sector. Vehicle Structure While SURS prefers to invest in a commingled fund-of-funds to enhance its diversification, it will also accept proposals for traditional separate accounts and fund-of-one vehicles. (A

6

traditional separate account arrangement is where SURS directly takes title to the underlying direct partnerships, and which does not involve an investment in a partnership vehicle that in turn invests in the underlying partnerships.) SURS Overview and Emerging Mandate Size As of June 30, 2012, SURS’ total plan assets were $13.6 billion. The plan has a mature global private equity portfolio that represents 8.3% of total plan assets. Its core private equity program is managed by two large global private equity manager-of-manager firms. SURS does have a dedicated exposure to Emerging Managers through a specialty manager, which the new commitment allocation for this mandate will seek to expand. It is anticipated that SURS will deploy approximately $10 million to $15 million per year to underlying Emerging Manager partnerships. That would equate to an Emerging Manager fund-of-funds commitment of up to $45 million to $60 million, every three to four years.

IV. RFP Specifications If, in response to this RFP, trade secrets or commercial or financial information are furnished under a claim that they are proprietary, privileged or confidential and that disclosure of the trade secrets or commercial or financial information would cause competitive harm to the person or business, such claim must be clearly made and such information must be clearly identified. The information must be identified in the RFP response and provided separately from the remainder of the RFP response. Nevertheless, such a claim is not definitive. SURS has the right, and obligation, to determine whether such information is exempt from disclosure under the Illinois Freedom of Information Act (5 ILCS 140/1 et seq.). In any event, no information will be determined to be proprietary, privileged or confidential unless it is identified and separated as indicated herein. Submission Deadline The completed electronic version of the RFP must be received by 4:00 pm CST Wednesday, January 23, 2013. Earlier responses are welcome. Any RFP received after the deadline will not be considered. Please send an electronic copy (MS Word & Excel format) to the following individuals:

7

Three (3) Bound and (1) Electronic: Two (2) Bound and One (1) Electronic: Kim Pollitt, CFA Michael Bise Senior Investment Officer Investment Consultant State Universities Retirement System Callan Associates Inc. of Illinois 101 California Street, Suite 3500 1901 Fox Drive San Francisco, CA 94111 Champaign, IL 61820 Phone: (415) 291-4127 Phone: (217) 378-8843 Fax: (415) 291-4017 Fax: (217) 378-9802 Email: [email protected] Email: [email protected]

Submission of Questions In order to clarify any issues in this Request for Proposals, the System will respond only to questions that are presented in writing via e-mail to Michael Bise at [email protected]. All questions should be submitted to Callan Associates by 8:00 AM CST Wednesday, January 2, 2013. These questions will be consolidated into a single Q&A document and responded to by SURS or Callan Associates on or about January 14, 2013. The Q&A document will be posted on the SURS web site at www.surs.org without divulging the source of the query. SURS Investment Policy Please note the Quiet Period Policy that establishes guidelines by which Board Members and staff will communicate with prospective service providers during a search process. The SURS Board of Trustees initially adopted this Policy at the December 8, 2006 meeting. Currently in force, the Policy is available at http://www.surs.org/pdfs/invinfo/policy.pdf. Please review Section VIII of the Policy and be familiar with all Quiet Period guidelines. Rights Reserved SURS reserves the right to amend any segment of the RFP prior to the announcement of a successful contractor. In such an event, all responders will be afforded the opportunity to revise their proposal to accommodate the RFP amendment. SURS reserves the right, without prejudice, to reject any or all proposals submitted. There is no express or implied obligation for SURS to reimburse for any expenses incurred in preparing proposals in response to this request. Ex-parte Communications Public Act 93-617, effective December 9, 2003, brought about new Illinois ethics procedures. All “ex parte communications” concerning investment, rulemaking or quasi-adjudicatory matters pending before a State agency must be documented and some must be reported. An “ex parte communication” is any written or oral communication by any person that imparts or requests material information or makes a material argument regarding potential action concerning an investment, a rulemaking process, or a quasi-adjudicatory matter. An ex parte communication

8

does not include statements publicly made in a public forum or communications among employees of the State agency. An ex parte communication from an interested party, or his or her official representative or attorney, to a SURS employee or the agency must be memorialized and made a part of the record. An “interested party” is a person or entity whose rights, privileges, or interests are the subject of,or are directly affected by, an investment, regulatory or quasi-adjudicatory matter. Any ex parte communication other than that just described must be immediately reported by the staff member or Trustee to the agency’s Ethics Officer. The communication must be memorialized and made a part of the record. The communication will be filed with the Executive Ethics Commission, accompanied by a memorandum from the Ethics Officer. Specific Items Requested from Respondent Firms Enumerated below are the specific items requested from respondent firms.

1) Letter of Transmittal. A letter of transmittal must be submitted on the Proposer’s official letterhead. The letter must identify all documents provided collectively as a response to the RFP, and must be signed by an individual authorized to bind the Proposer contractually. An unsigned proposal shall be rejected. The letter must also contain the following:

a) Statement that the proposal is being made without fraud or collusion; that the Proposer has not offered or received any finder’s fees, inducements or any other form of remuneration, monetary or non-monetary, from any individual or entity relating to the RFP.

b) Statement that discloses the nature of any personal or business relationship (including any negotiations for prospective business) you now have, or have had in the past five years, with the Consultant, any SURS Board Member, or SURS Staff.

c) Statement that the proposing firm has been in compliance with the System’s Quiet Period Policy and Ex-Parte Communications Policy.

2) Questionnaire. The proposer must address the questionnaire items in the RFP in the order in which they appear in the RFP. Further, each question number and question in the RFP shall be repeated in its entirety before stating the answer. Certain questions may require supporting documentation, which should be submitted as attachments to the questionnaire. Please complete the attached Appendix B and C.

V. Projected Schedule of Events

December 10, 2012 Dissemination of RFP January 2, 2013 Deadline for questions to Callan January 14, 2013 Responses to questions submitted to Callan January 23, 2013 RFP responses due by 4:00 p.m. CST February/March 2013 Identify firms for further consideration April/May 2013 Staff interviews with selected firms June 13, 2013 Firms recommended to SURS Board of Trustees

9

VI. Evaluation Criteria SURS will consider the following in making its decision: A. Organization: The candidate firms will be evaluated for organizational structure, personnel

and staffing, systems and infrastructure resources, ownership and succession planning, and organizational stability.

B. Experience: It is preferred that managers have meaningful experience making the specific

types of investments intended for the emerging manager private equity program.

C. Asset Base: The manager should have significant discretionary private equity assets under management, preferably with a meaningful asset base in the Emerging Manager strategy being proposed. The firm’s AUM, client base and historical fundraising success, should indicate that the manager and strategy will be viable and growing in the future.

D. Client Base: The manager should have experience managing assets for institutional tax-exempt

institutions, with preference given to managers that have public pension funds in their client base.

E. Access to Recognized Top Tier Emerging Manager Partnerships: The manager should exhibit

historical investor relationships with partnerships generally recognized as being among the best at employing an Emerging Manager strategy.

F. Investment Breadth and Experience: Demonstrated experience addressing the broad spectrum of

private equity strategies in the Emerging Manager universe.

G. Candidates should demonstrate the capability to address strategy diversification across key strategy types such as venture capital, buyouts of various sizes, special situations, mezzanine debt and distressed/restructuring funds.

H. Candidates should demonstrate the capability to address diversification by time (vintage

year), industry sector, and U.S. geographic region. International diversification is not necessarily viewed as desirable.

I. Investment Strategy: The investment strategy should be predominantly targeted to

investments in primary partnership interests. Funds with modest allocations to other strategies (e.g., secondary purchases or direct co-investments) will also be considered, recognizing that primary partnerships are the key investments sought.

J. Indications of Performance: Tenure in the business, and specifically with the Emerging

Manager strategy, where historical performance is sufficient to demonstrate above median returns compared to the Thomson Reuters Private Equity database. Performance will not be the primary decision point in the selection process, but is an important element of the review process.

K. Unrelated Business Income Tax (UBIT): The ability to shield UBIT may be a consideration

in the selection process, as well as the intention to avoid or incur UBIT.

10

L. Allocation Policy: The manager’s investment allocation policy should not disadvantage new

clients’ ability to access high quality partnerships with which the manager has a legacy relationship.

M. Fees: Management fees, expenses and other economic considerations must be institutional in

composition and amount. Generally, proposals without incentive compensation components are preferred to those with profit participation.

N. Terms and Conditions: Proposals will be reviewed for investor rights and other governance

provisions. Proposals with stronger investor governance provisions will be viewed more favorably.

11

Appendix A

Sudan Divestment Law in Illinois

SURS must obtain an annual certificate from each manager confirming that the investments in SURS’ account comply with the requirements of the Sudan Law. You must deliver the first such manager certificate upon completion of the legal documents. Thereafter, annual compliance certificates must be delivered to us as of June 30 of each year.

Managers of publicly traded securities will need to contract with a firm that specializes in global risk management to identify companies that are considered forbidden entities under the Sudan Law, and will be required to screen the investments in SURS’ account in order to avoid holding such securities.

The Sudan Law contains the following provisions that may impact compliance by SURS’ managers:

Mutual Funds

Mutual funds are excluded from the definition of “forbidden entity” if they satisfy the requirements under Section 1-113.2 of the Illinois Pension Code, which are:

The mutual fund is managed by an investment company as defined and registered under the federal Investment Company Act of 1940 and registered under the Illinois Securities Law of 1953.

The mutual fund has been in operation for at least 5 years. The mutual fund has total net assets of $250 million or more. The mutual fund is comprised of diversified portfolios of common or preferred

stocks, bonds, or money market instruments. We are aware that under the National Securities Market Improvement Act of 1986 (“NSMIA”) states were pre-empted from requiring registration of federally "covered securities," and that Section 1-113.2 of the Illinois Pension Code, which predated NSMIA, may also be pre-empted to the extent it would require such dual registration. However, you should rely on your own counsel to advise you on compliance with your duties under the Sudan Law. Private Market Funds

The Sudan Law includes special rules applicable to a “Private Market Fund”, which is defined as “any private equity fund, private equity fund of funds, venture capital fund, hedge fund, hedge fund of funds, real estate fund, or other investment vehicle that is not publicly traded.” A Private Market Fund will not be deemed to be a forbidden entity if it delivers either an affidavit or certificate confirming essentially that it does not own or control assets in the Republic of Sudan and does not conduct business operations in the Republic of Sudan. (See paragraph (d) of the Sudan Act for the specific affidavit or certificate requirements).

12

Appendix B

Private Equity Emerging Manager Fund of Funds Questionnaire The Emerging Manager Strategy Private Equity Fund of Funds Questionnaire will be the primary source of information for SURS and Callan Associates to select which candidates will be invited to become finalists in this search. Therefore, it is important that the information provided be complete and in the format requested. Please keep your response to no more than 25 pages excluding attachments. Most questions can be answered with a brief response. Callan has modified many questions in this version of the questionnaire. If you are working from the text of a prior response please ensure that the answers and data tables reflect the new formats. ORGANIZATION 1. Name of Firm:

Main Address: City: State: Zip Code: Phone: Fax: Federal Employer Identification Number:

Contact Person(s): Name: Title: Phone: Fax: Email:

Please list all other branch offices, domestic and international:

2. Type of Firm:

(i.e. independent; affiliate of bank, insurance company, broker, other - specify) Is the firm a Registered Investment Advisor under the Investment Company Act of 1940? If yes, please separately enclose a copy of your most recent SEC Form ADV. If not does the firm intend to register and when?

3. Year Founded: Firm: Parent: (If applicable) Comments: Please provide an organizational chart depicting the relationship of firm/division to parent and affiliated companies.

4. A) Ownership Structure: (Check most appropriate one)

_____ Corporation (Public/Private) _____ Partnership _____ Employee-owned _____ Joint Venture _____ Subsidiary of: _______________________________________ _____ Other (Describe)

13

B) Please provide a schedule detailing the amount of ownership in the firm by employees and

third parties.

5. If the firm is a subsidiary or division of a financial service organization, please describe the reporting and control functions existing between the Private Equity Group and the parent.

6. Does the equity ownership structure qualify the firm as a Minority, Women, or Disabled-

owned Business Enterprise (MWDBE)? 7. Is your Private Equity organization covered by errors and omissions insurance? If yes, how

much $________. List any other insurance types and amounts covering your Private Equity group.

8. Have there been any changes in the ownership structure of the firm in the last 10 years?

If yes, when? Please describe the nature of the change.

9. Legal and regulatory actions:

a) Has the firm ever been sued or has it ever sued another party? Please comment. Is the firm currently involved in any litigation? If so, please provide a detailed list of outstanding litigation to which the firm is a party.

b) Are you currently out of compliance with the SEC, DOL, or any other regulatory agency?

(Yes or No). If Yes, please explain.

c) Please describe any litigation or administrative actions directed against your organization or any of its offices or directors related to the operation of your organization during the last 5 years.

10. Please provide a brief historical summary of the organization's involvement in:

a) Private equity investments. b) With the Emerging Manager strategy.

11. Will your firm act as a fiduciary with respect to the work performed by your firm and for

specific partnership investment recommendations made by your firm? 12. Has your firm adopted the Principles for Responsible Investment? If so, when? If adopted,

please include a discussion of actions taken as a result of the adoption of PRI.

13. If your firm has not adopted the PRI, have there been any discussions regarding the Principles? If so, what were the key issues, concerns, or obstacles surrounding the PRI?

14

14. Please describe your firm’s commitment to organizational diversity. What policies or procedures do you have in place to support that commitment?

15. Illinois law would prohibit the use of contingent and placement fees. According to the

statute, no person or entity shall retain a person or entity to attempt to influence the outcome of an investment decision of or the procurement of investment advice or services of a retirement system for compensation, contingent in whole or in part upon the decision or procurement. (40 ILCS 5/1-145). Please discuss what, if any, impact this would have on your potential selection.

PERSONNEL 16. Key Personnel - List below those individuals who are involved in the firm's Private Equity

decision making process (add additional rows as necessary): Name Title A B C D

(A) = % Time spent on investment activities (vs. non-investment such as firm management, client service, business development, etc.) (B) = Years with this firm (C) = Years of private equity investment experience (D) = Years of overall investment experience

17. Please include brief biographies for all the Private Equity Investments professionals in the firm, including the year they joined the firm and their office location.

18. A) Provide the number of professional and support personnel in each of the following

categories:

Position #

Persons Sr. Professionals/Partners Jr. Professionals Monitoring and Support Marketing/Client Service Other Total

B) What is the number of the firm’s total staffing and private equity-specific employees?

19. Indicate the turnover (number of people) that occurred in your private equity investments’

staff during the years listed below.

15

Partners & Partners & Staff Staff Key Personnel Key Personnel Net Additions Terminations Additions Terminations Totals 2012 2011 2010 2009 2008 2007

20. Please explain any unusual turnover and turnover of senior professionals. Please include

statistics for partners and key investment decision-makers, including whether they were replaced and whether any replacement was internal or a new hire.

21. What would you consider your key professionals’ competitive advantage in making

emerging manager private equity investments? 22. What private equity research does your firm’s investment professionals’ conduct specifically

regarding the emerging manager strategy and universe as part of or in addition to their normal responsibilities?

PRIVATE EQUITY INVESTMENTS UNDER MANAGEMENT AND SERVICES 23. Please provide a breakdown of the private equity investments (PE) assets under management

of the firm as of 6/30/12, by number of accounts, uncalled commitments, NAV and both combined. A fund-of-funds should be listed as a single “account,” but number of clients should represent the number of investors in fund-of-funds vehicles, please do not double count clients in multiple vehicles. Please provide any comments or footnotes necessary to clarify your firm’s assets under management.

By Mandate Type:

Account Type #

AccountsUncalled

Commitments NAV

($ mil) Uncalled+NAV

Emerging PE Assets Fund-of-funds Direct Co-Investments Separate Accounts: Discretionary Non-Discretionary Fund-of-Ones Total Emerging PE Accts Developed/Other PE Assets Fund-of-Funds Direct Co-Investments Separate Accounts:

16

Discretionary Non-Discretionary Fund-of-Ones Total Developed/Other Accts

Total Accounts

By Tax Status:

Tax Status #

AccountsUncalled

Commitments NAV

($ mil) Uncalled+NAV

Emerging PE Assets Total Tax-Exempt Total Taxable Assets Total Emerging PE Accts Developed/Other PE Assets

Total Tax-Exempt Total Taxable Assets Total Developed/Other Accts

Total Accounts Client Base

By Investor Type:

Investor/Client Type #

Clients

Uncalled Commit-

ments

NAV ($ mil)

Uncalled+NAV

Emerging Manager Strategy Public Pension Plans Corporate Pension Plans Foundations and Endowments

Financial Institutions (Banks, Ins.)

Other (HNW Individuals) Total Emerging Manager Clients

Developed/Other PE Public Pension Plans Corporate Pension Plans Foundations and Endowments

Financial Institutions (Banks, Ins.)

17

Other (HNW Individuals) Total Developed/Other Clients

Total Firm Clients 24. By fund, please attach a list of representative institutional investors in the firm’s emerging

manager strategy. 25. What amount of “dry powder,” or capital needs to be deployed over the next five years? Please

estimate future funding (commitment) requirements over the next five years for all clients and/or commingled vehicles in the table below. Separate the deployment into Emerging Strategy and Developed/Other Strategy as outlined in the tables. Please provide actual client or vehicle name.

Emerging Manager Strategy Estimated Future Client Investment Requirement Analysis (in $millions) Client 2013 2014 2015 2016 2017 Client/Commingled Vehicle

$1,000 $1,000 $1,000 $1,000 $1,000

Client/Commingled Vehicle

$1,000 $1,000 $1,000 $1,000 $1,000

Client/Commingled Vehicle

$1,000 $1,000 $1,000 $1,000 $1,000

Etc. $1,000 $1,000 $1,000 $1,000 $1,000 Total $4,000 $4,000 $4,000 $4,000 $4,000

Developed Manager/Other Estimated Future Client Investment Requirement Analysis (in $millions) Client 2013 2014 2015 2016 2017 Client/Commingled Vehicle

$1,000 $1,000 $1,000 $1,000 $1,000

Client/Commingled Vehicle

$1,000 $1,000 $1,000 $1,000 $1,000

Client/Commingled Vehicle

$1,000 $1,000 $1,000 $1,000 $1,000

Etc. $1,000 $1,000 $1,000 $1,000 $1,000 Total $4,000 $4,000 $4,000 $4,000 $4,000

26. What is the firm's plan for future growth and capacity for future growth in the Emerging

Manager strategy? 27. Please describe your firm’s allocation policy for allocating investments among clients and

vehicles and attach a copy of the firm’s allocation policy. What is the waterfall for allocating

18

partnership investment opportunities where client-base appetite exceeds the available commitment?

INVESTMENT APPROACH Philosophy 28. How do you define the firm’s Emerging Manager strategy, what types of partnership strategies

meet your emerging manager criteria? 29. For the Emerging Manager strategy, how do you approach allocation across different types of

private equity strategies?

30. Do you include non-MWDBE partnerships in the Emerging Manager portfolios? If so, describe the types of other non-MWDBE partnerships included. What is the expected amount of non-MWDBE partnerships included in portfolio (both number of partnership and percent of portfolio committed capital) and what would be the maximum amount of non-MWDBE exposure?

31. Please describe your diversification considerations in building a portfolio. In the table use the target asset size for SURS (up to $45 million to $60 million of commitments over four years), and describe your Emerging Manager strategy private equity “model portfolio”. Please use the following exact format (please add or delete rows as necessary):

Strategy Type(1)

% to Strategy

# of Invs

Total $ to Strategy ($)

Expected Range of Returns

100% $60,000,000

(1) Make selections from list in Question 35. 32. Given that SURS commitment pace of $10 million to $15 million per year is small by private

equity standards, in order to meet partnership minimum commitments requirements and achieve diversification within a vintage year, please describe how you achieve the prudent diversification necessary for the portfolio’s success.

33. What is the historical and expected future commitment size range for partnerships in your Emerging Managers strategy? Do you invest in partnerships structured as SBICs or SSBICs? If so, please discuss their usage?

34. Do you include international investing in your Emerging Manager strategy? If so, please explain why non-US partnerships are included and their role in the Emerging Manager strategy. What is the expected amount of non-US partnerships (both number of partnership and percent of portfolio committed capital)?

19

35. Do you include direct or secondary investments in your Emerging Manager strategy. If so, please describe their roles in your portfolios, the amount of each and any maximum limits.

36. What distinguishes your firm’s Emerging Manager strategy from other private equity manager-of-managers’ Emerging Manager strategy?

37. What is your firm’s approach to mitigating risk and diversifying Emerging Manager portfolios? Investment 38. Describe your firm’s methods for proactively accessing Emerging Manager partnership deal

flow and process for screening investments.

39. Please indicate how many Emerging Manager partnerships, by type, between 01/01/2000 and 12/31/2011 your firm has: A) Identified and preliminarily reviewed B) Began due diligence on C) Closed investments in; and D) Dollar amount you have invested

A B C D Early-Stage __________ __________ __________ __________

Middle-Stage __________ __________ __________ __________ Later-Stage __________ __________ __________ __________ Multi-Stage __________ __________ __________ __________ Small Buyouts __________ __________ __________ __________ Larger Buyouts __________ __________ __________ __________ Industry-focused __________ __________ __________ __________ Restructuring/Distressed __________ __________ __________ __________ Subordinated Debt __________ __________ __________ __________ International __________ __________ __________ __________ Secondary Purchases __________ __________ __________ __________ Other (Please Specify) __________ __________ __________ __________ Totals __________ __________ __________ __________ 40. What is your firm’s estimate of the total number of institutionally viable MWDBE-strategy

general partners? Of the universe of MWDBE-strategy oriented general partners, how many are included on your firm’s focus list as being eligible for serious consideration in your firm’s portfolio?

41. Describe your firm’s due diligence process. (Attach checklist as an exhibit.) A) Describe each step in your due diligence process, which would lead to an investment. B) Discuss qualitative versus quantitative aspects. C) Describe the most common critical areas of focus. D) Describe how you document your process. E) Provide an example of an internal investment memorandum pertaining to a recommended

investment.

20

42. Does your firm’s due diligence process for the Emerging Manager strategy differ from that

employed for Developed/Other partnerships? If so, please provide a brief description the differences.

43. Describe the internal decision-making dynamics of the organization. Negotiation

44. In negotiating a partnership agreement, or similar document, for Emerging Manager strategy partnerships, please describe areas the firm considers most important? Are there provisions the firm proactively seeks to include or improve upon?

45. Please describe how your legal capabilities are set up. Do you have general counsel that works with outside counsel, does your outside counsel report directly to a Managing Director, or do you do all your legal work in-house? Monitoring, Reporting and Exits

46. How frequently are you in contact with the Emerging Manager general partners in which your clients are invested?

47. Describe the methods you employ to determine whether the Emerging Manager strategy general partners are reporting reasonable investment carrying values. What do you do when you feel there is an inaccuracy? How are you currently complying with FASB 157 and how do you help your clients adhere to AU Section 9332?

48. Describe your typical reporting duties and responsibilities with your clients. Please describe your reporting analytics and provide an example quarterly report. Is the portfolio data available on-line or electronically? Please describe.

49. How do you modify your reports for clients subject to FOIA requirements – what level of information is provided and what is specifically excluded? What information is available to FOIA clients outside of the normal reporting process (e.g., visits to your firm’s offices). Please attach a sample of the year-end portfolio reports you prepare for FOIA clients.

50. How many Emerging Manager partnerships have you managed through to complete dissolution?

51. Please describe how the firm arrives at a hold or sell decision on an in-kind distribution, including the research and evaluation discipline employed.

21

INVESTMENT HISTORY

52. Please provide a copy of the firm's deal log for 2011. Please select two or more funds you declined to invest in during 2011 and provide a brief description of the key reasons for not investing.

53. To participate as a candidate in any of Callan’s Manager-of-Managers searches, your firm must have up-to-date information in Callan’s general private equity manager search database. All information in Callan’s database will be treated confidentially. If you are not sure if your information is up to date, please contact Callan’s Private Markets Group.

54. Attached is an MS Excel spreadsheet entitled “Appendix C - RFP Performance” which requests vintage year and cumulative performance data for all partnership investments made since January 1, 1990 through June 30, 2012. The investment performance is divided into three separate tables: 1) discretionary, 2) non-discretionary and 3) combined. While this is a separate account mandate, summary data is also requested for each unique fund-of-funds vehicle. Please complete the table and return both a hard copy in the RFP response and an MS Excel file. OTHER

55. Please state the firm’s policy on making political contributions by both the firm and employees.

56. Please explain the firm’s ability to shield clients from UBIT.

57. Please discuss any FOIA-related issues you may have regarding providing investment access to partnerships for SURS.

58. Please provide three Emerging Manager strategy client references that are similar to SURS and are current investors in the vehicle type being proposed. Provide name of contact and phone numbers. FEES

59. Please furnish your firm’s: A) Narrative fee schedule for the product being proposed. B) It is anticipated that SURS will deploy approximately $10 million to $15 million of annual

commitments per year in the Emerging Manager strategy. Please quantify a 15-year projection of your fee schedule for the four years of SURS commitments shown. Provide IRR and multiple assumptions for any carried interest, as appropriate.

C) If the amounts committed by SURS varies significantly from the projected amounts (either substantial increases due to strong total SURS asset growth, or a weak market for partnership offerings such as 2002), describe how the fees would vary (or if they would not).

22

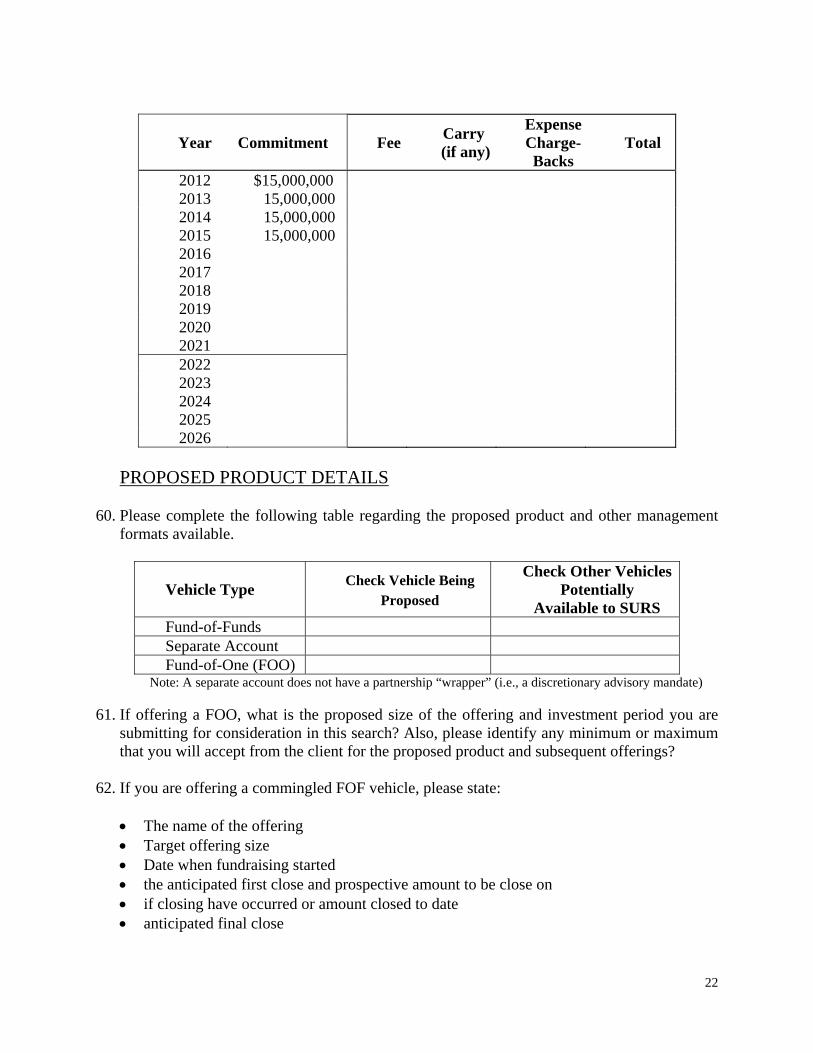

Year Commitment FeeCarry

(if any)

Expense Charge-Backs

Total

2012 $15,000,000 2013 15,000,000 2014 15,000,000 2015 15,000,000 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

PROPOSED PRODUCT DETAILS

60. Please complete the following table regarding the proposed product and other management formats available.

Vehicle Type Check Vehicle Being

Proposed

Check Other Vehicles Potentially

Available to SURS Fund-of-Funds Separate Account Fund-of-One (FOO)

Note: A separate account does not have a partnership “wrapper” (i.e., a discretionary advisory mandate)

61. If offering a FOO, what is the proposed size of the offering and investment period you are submitting for consideration in this search? Also, please identify any minimum or maximum that you will accept from the client for the proposed product and subsequent offerings?

62. If you are offering a commingled FOF vehicle, please state: The name of the offering Target offering size Date when fundraising started the anticipated first close and prospective amount to be close on if closing have occurred or amount closed to date anticipated final close

23

You may include additional narrative providing any comments of which you would like the client to be apprised. REPRESENTATIONS AND WARRANTIES To the best of our knowledge all information and representations provided are true and accurate. We warrant and represent that our firm did not confer with any other persons or organizations submitting information regarding the search in progress. All information submitted to Callan Associates is considered highly confidential and will be treated accordingly. We have read the complete materials and agree to the terms and requirements this Private Equity Manager-of-Managers search is conditioned upon. The offer in this questionnaire will remain valid for a period of 180 days from the submission deadline January 23, 2013. Authorized Signature: _______________________________________________________________________________ Print Name: _______________________________________________________________________________ Title: _______________________________________________________________________________ Firm: _______________________________________________________________________________ Phone: _________________________________ Date: _______________________________ Please send copies of your response to: Three (3) Bound and (1) Electronic: Two (2) Bound and One (1) Electronic: Kim Pollitt, CFA Michael Bise Senior Investment Officer Investment Consultant State Universities Retirement System Callan Associates Inc. of Illinois 101 California Street, Suite 3500 1901 Fox Drive San Francisco, CA 94111 Champaign, IL 61820 Phone: (415) 291-4127 Phone: (217) 378-8843 Fax: (415) 291-4017 Fax: (217) 378-9802 Email: [email protected] Email: [email protected]