state of the nation’s housing markets 2 nd quarter 2010 update kevin p. kane chief housing market...

TRANSCRIPT

State of the Nation’s Housing Markets

2nd Quarter 2010 Update

Kevin P. KaneChief Housing Market Analyst

Office of Policy Development and ResearchSpecial Thanks – Randall Goodnight (Ft. Worth)

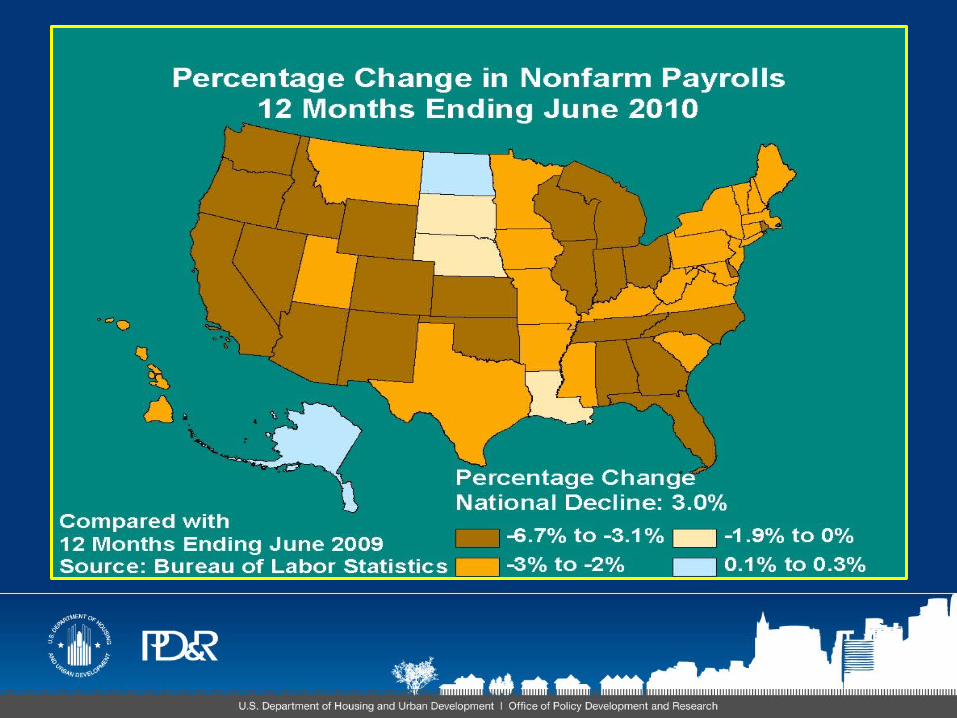

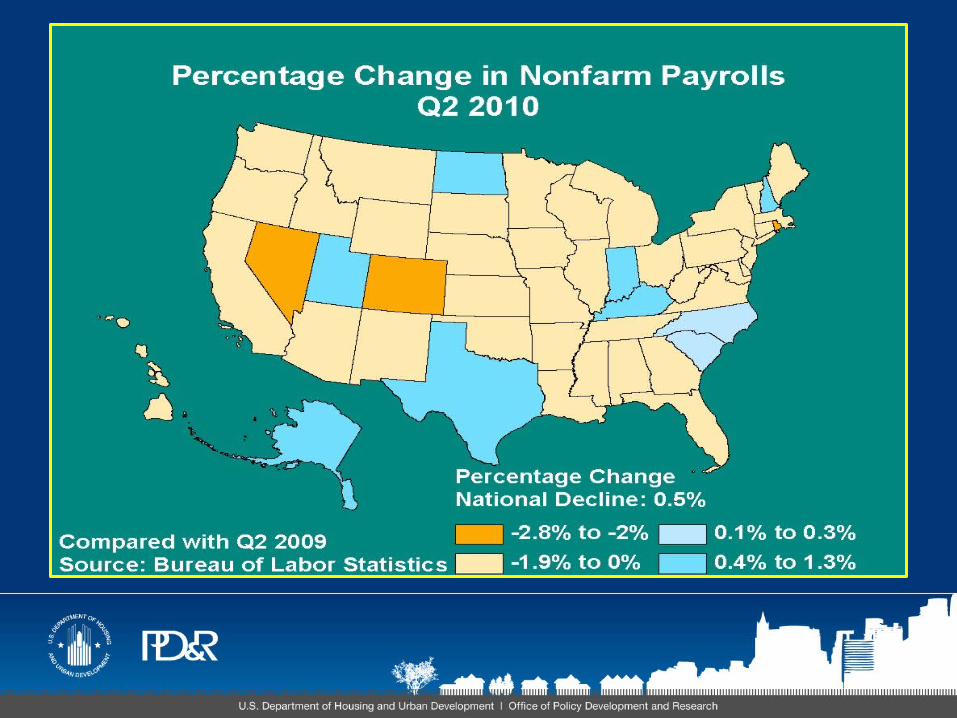

Nonfarm Payrolls 12-month Averages

200020002000200020002000200020002000200020002000200120012001200120012001200120012001200120012001200220022002200220022002200220022002200220022002200320032003200320032003200320032003200320032003200420042004200420042004200420042004200420042004200520052005200520052005200520052005200520052005200620062006200620062006200620062006200620062006200720072007200720072007200720072007200720072007200820082008200820082008200820082008200820082008200920092009200920092009200920092009200920092009201020102010201020102010124000

126000

128000

130000

132000

134000

136000

138000

140000

Tot

al J

obs

(in

thou

sand

s)

Nonfarm PayrollsAnnual Percentage Change (12-month avg.)

200120012001200120012001200120012001200120012001200220022002200220022002200220022002200220022002200320032003200320032003200320032003200320032003200420042004200420042004200420042004200420042004200520052005200520052005200520052005200520052005200620062006200620062006200620062006200620062006200720072007200720072007200720072007200720072007200820082008200820082008200820082008200820082008200920092009200920092009200920092009200920092009201020102010201020102010-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

Per

cent

age

Cha

nge

Regional Nonfarm PayrollsPercentage Change 12 months ending June 2010

New E

nglan

d

Mid-

Atlant

ic

Midw

est

Great

Plai

ns

Pacific

-6-5-4-3-2-10

Nonfarm Change by SectorPercentage Change 12 months ending June 2010

Mini

ng &

Log

ging

Who

lesale

Tra

de

Info

rmat

ion

Ed. &

Hea

lth S

erv.

Govt.

-15

-10

-5

0

5

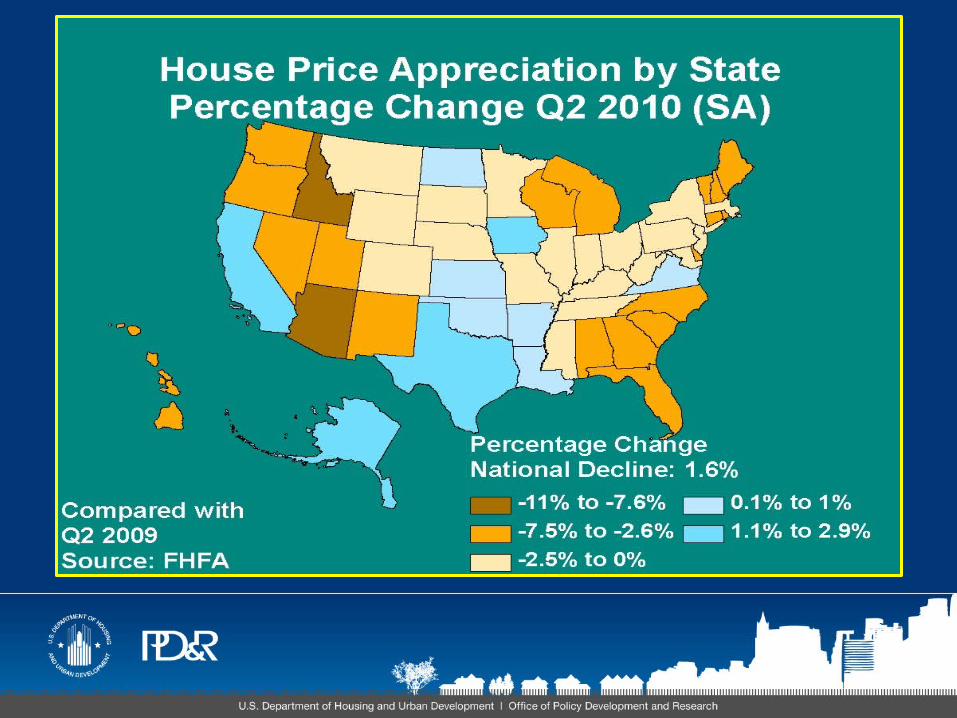

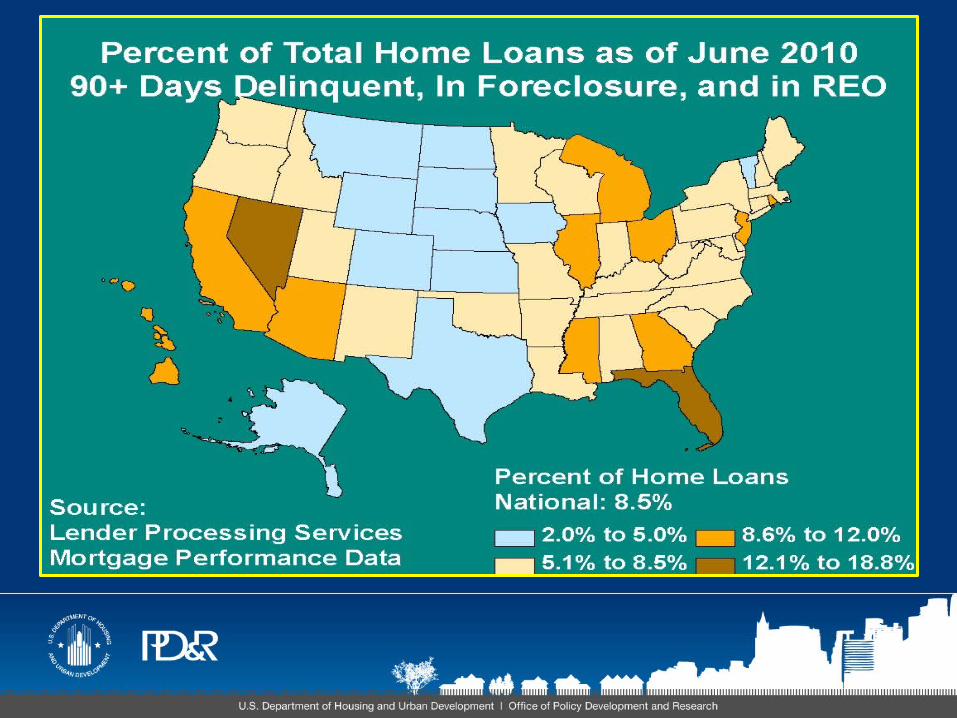

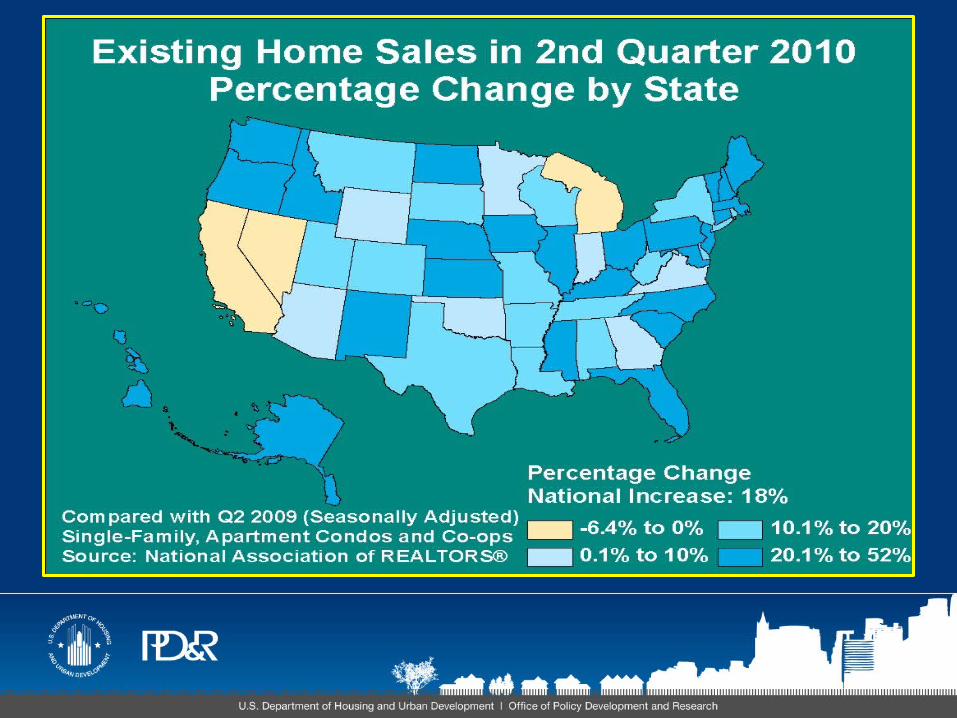

U.S. Housing Market Conditions: 2Q 2010 • Sales market conditions remain soft in much of the

country but continue to improve in many areas

• Data on home sales prices indicate improvement

• Home sales are up (homebuyer tax credit)

• Inventories of new and existing homes for sale are down from a year ago and coming closer to balance

• Rental market conditions are mixed throughout the country

• Significant declines in multifamily permits have continued

Regional Conditions 2Q 2010Sales Markets Rental Markets

Region I (New England) Balanced BalancedRegion II (NY/NJ) Slightly Soft Balanced (NYC Tight)Region III (Mid-Atlantic Slightly Soft MixedRegion IV (Southeast-Caribbean) Soft SoftRegion V (Midwest Soft Mixed (soft/balanced)Region VI (Southwest) Slightly Soft Soft

Region VII (Great Plains) Balanced (Soft in MO) SoftRegion VIII (Rocky Mountains) Soft MixedRegion IX (Pacific) Soft Mixed Region X (Northwest) Soft Balanced

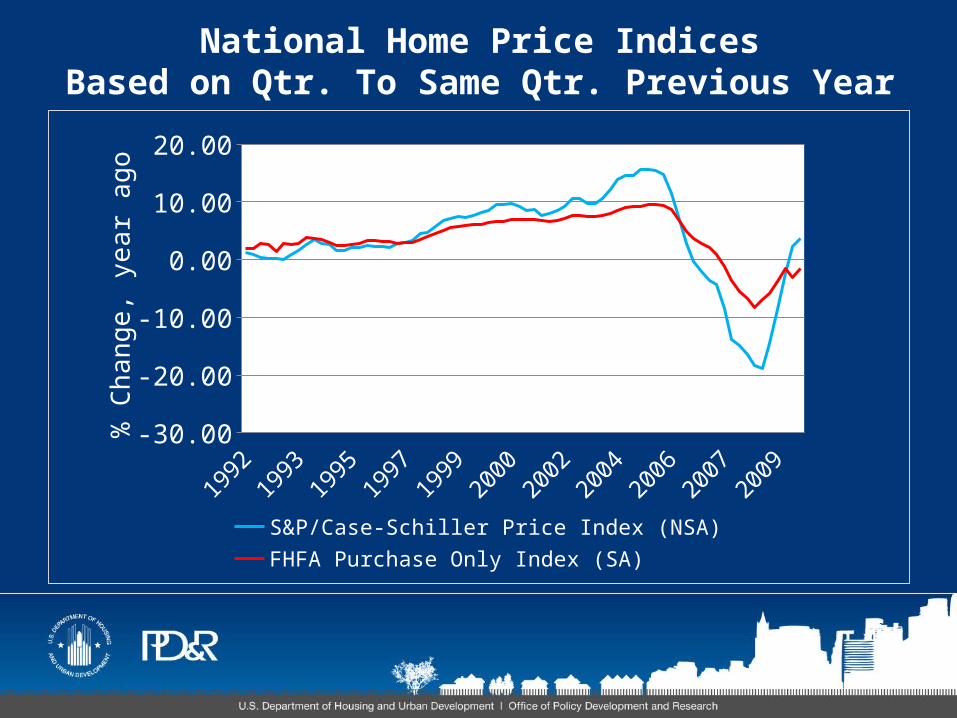

National Home Price IndicesBased on Qtr. To Same Qtr. Previous Year

1992

1993

1995

1996

1998

1999

2001

2002

2004

2005

2007

2008

2010

-25.00-20.00-15.00-10.00

-5.000.005.00

10.0015.0020.00

S&P/Case-Schiller Price Index (NSA)

FHFA Purchase Only Index (SA)

% C

hang

e, y

ear

ago

SF Permit ActivityDuring 12 Months Ending

June-09 June-100

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

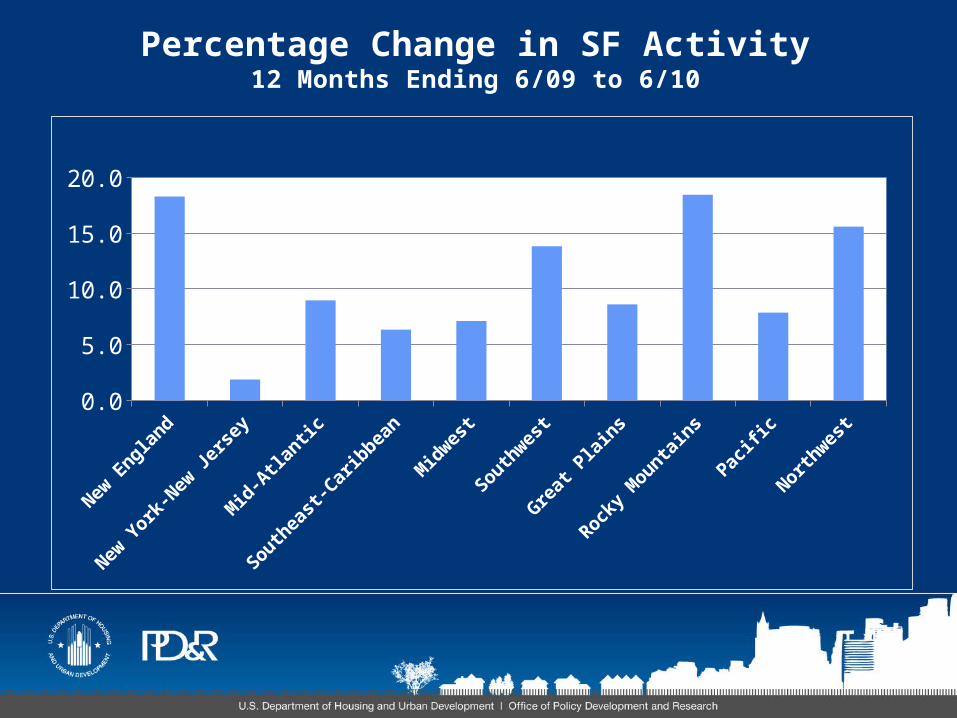

Percentage Change in SF Activity12 Months Ending 6/09 to 6/10

New E

ngland

New Y

ork-N

ew J

ersey

Mid

-Atla

ntic

Southeast-C

aribbean

Mid

west

Southw

est

Gre

at Pla

ins

Rocky Mounta

ins

Pacific

Northw

est0.0

5.0

10.0

15.0

20.0

MF Permit ActivityDuring 12 Months Ending

June-09 June-100

50,000

100,000

150,000

200,000

250,000

Percentage Change in MF Activity12 Months Ending 6/09 to 6/10

-60.0

-50.0

-40.0

-30.0

-20.0

-10.0

0.0

For additional information:

• U.S. Housing Market Conditions Report 2Q 2010 available at www.huduser.org

• Contact your local Regional or Field Economist

• Contact me at [email protected]