st. landry parish housing authority · pdf file-^so ,,. received 2009apr-i flhi0-!.8 st....

TRANSCRIPT

-^SO

, , . RECEIVED

2009APR-I flHI0-!.8

ST. LANDRY PARISH HOUSING AUTHORITY

Washington, Louisiana

AUDITED FINANCIAL REPORT

YEAR ENDED JUNE 30, 2008

jnder provisions of state law, this report is a public document-Acopy ofthe reporthas been submitted to the entity and other appropriate public officials. The report is available for public inspection at the Baton Rouge office ofthe LegislativeAuditor and, where appropriate, at the office ofthe parish clerk of court.

Release Date

TABLE OF CONTENTS

FINANCIAL SECTION Page

Management's Discussion and Analysis i-viii

Independent Auditor's Report 1-2

Basic Financial Statements:

Statement of Net Assets 4-5

Statement of Revenues, Expenses, and Changes in Net Assets 6

Statement of Cash Flows 7-8

Notes to Financial Statements 9-16

Other Reports and Schedules:

Schedule of Expenditures of Federal Awards 18

Report on Intemal Control over Financial Reporting And On Compliance And Other Matters Based on an Audit of fmancial Statements Performed In Accordance With Government Auditing Standards 19-20

Report on Compliance with Requirements Applicable to Each Major Program And On Intemal Control over Compliance In Accordance With OMB Circular A-133 21-22

Status of Prior Audit Findings 23

Findings and Questioned Costs 24

Financial Data Schedules 25-29

Housing Authority of St Landry, LA

Management's Discussion and Analysis (MD&A) June 30, 2008

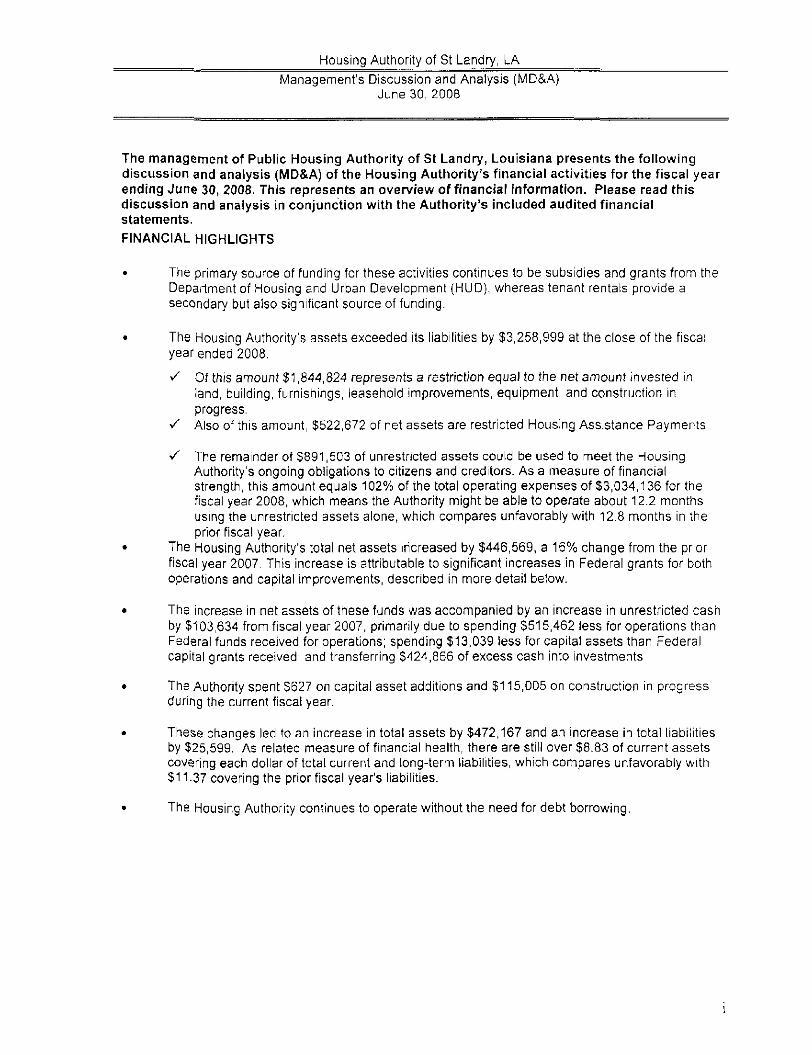

The management of Public Housing Authority of St Landry, Louisiana presents the following discussion and analysis (MD&A) of the Housing Authority's financial activities for the fiscal year ending June 30, 2008. This represents an overview of financial information. Please read this discussion and analysis in conjunction with the Authority's included audited financial statements.

FINANCIAL HIGHLIGHTS

• The primary source of funding for these activities continues to be subsidies and grants from the Department of Housing and Urban Development (HUD), whereas tenant rentals provide a secondary but also significant source of funding,

• The Housing Authority's assets exceeded its liabilities by $3,258,999 at the close of the fiscal year ended 2008,

^ Of this amount $1,844,824 represents a restriction equal to the net amount invested in land, building, furnishings, leasehold improvements, equipment, and construction in progress.

-/ Also of this amount, $522,672 of net assets are restricted Housing Assistance Payments

^ The remainder of $891,503 of unrestricted assets could be used to meet the Housing Authority's ongoing obligations to citizens and creditors. As a measure of financial strength, this amount equals 102% ofthe total operating expenses of $3,034,136 for the fiscal year 2008, which means the Authority might be able to operate about 12.2 months using the unrestricted assets alone, which compares unfavorably with 12.8 months in the phor fiscal year.

• The Housing Authority's total net assets increased by $446,569, a 16% change from the prior fiscal year 2007, This increase is attributable to significant increases in Federal grants for both operations and capital improvements, described in more detail below.

• The increase in net assets of these funds was accompanied by an increase in unrestricted cash by $103,634 from fiscal year 2007, primarily due to spending $515,462 less for operations than Federal funds received for operations; spending $13,039 less for capital assets than Federal capital grants received; and transferring $424,866 of excess cash Into Investments

• The Authority spent $627 on capital asset additions and $115,005 on construction In progress during the current fiscal year.

• These changes led to an increase In total assets by $472,167 and an Increase in total liabilities by $25,599, As related measure of financial health, there are still over $8.83 of current assets covehng each dollar of total current and long-term liabilities, which compares unfavorably with $11.37 covering the prior fiscal year's liabilities.

• The Housing Authority continues to operate without the need for debt borrowing.

Housing Authority of St Landry, LA

Management's Discussion and Analysis (MD&A) June 30, 2008

OVERVIEW OF THE FINANCIAL STATEMENTS

This MD&A IS intended to serve as an introduction to the Housing Authority's basic financial statements The Housing Authority is a special-purpose government engaged in business-type activities. Accordingly, only fund financial statements are presented as the basic financial statements, comprised of two components: (1) fund financial statements and (2) a series of notes to the financial statements. These provide Information about the activities of the Housing Authority as a whole and present a longer-term view of the Housing Authority's finances. This report also contains other supplemental information in addition to the basic financial statements themselves demonstrating how projects funded by HUD have been completed, and whether there are inadequacies In the Authority's Internal controls

Reporting on the Housing Authority as a Whole

One of the most important questions asked about the Authority's finances is, "Is the Housing Authority as a whole better off, or worse off, as a result of the achievements of fiscal year 2008?" The Statement of Net Assets and the Statement of Revenues, Expenses, and Changes in Net Assets report information about the Housing Authority as a whole and about Its activities In a way that helps answer this question. These statements include all assets and liabilities using the accrual basis of accounting, which Is similar to the accounting used by most private-sector companies. All of the current year's revenues and expenses are taken into account regardless of when cash is received or paid.

Fund Financial Statements

All of the funds of the Housing Authority are reported as proprietary funds, A fund is a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives, The Housing Authority, like other enterprises operated by state and local governments, uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements.

The Housing Authority's financial statements report its net assets and changes in them. One can think of the Housing Authority's net assets - the difference between assets and (labilities - as one way to measure the Authority's financial health, or financial position. Over time, Increases and decreases in the Authority's net assets are one indicator of whether Its financial health Is Improving or deteriorating. One will need to consider other non-flnanclai factors, however, such as the changes In the Authority's occupancy levels or Its legal obligations to HUD, to assess the overall health of the Housing Authority.

USING THIS ANNUAL REPORT

The Housing Authority's annual report consists of financial statements that show combined information about the Housing Authority's most significant programs:

Low Rent Public Housing Housing Choice Vouchers Component Unit Public Housing Capital Fund Program Other Federal Program 1 Disaster Voucher Program

The Housing Authority's auditors provided assurance in their Independent auditors' report with which this MD&A Is included, that the basic financial statements are fairly stated. The auditors provide varying degrees of assurance regarding the other Information included in this report, A user of this report should read the independent auditors' report carefully to determine the level of assurance provided for each of the other parts of this report

Housing Authority of St Landry, LA

Management's Discussion and Analysis (MD&A) June 30, 2008

Reporting the Housing Authority's Most Significant Funds

The Housing Authority's financial statements provide detailed information about the most significant funds. Some funds are required to be established by the Department of Housing and Urban Development (HUD). However, the Housing Authority establishes other funds to help It control and manage money for particular purposes, or to show that It is meeting legal responsibilities for using grants and other money.

The Housing Authority's enterprise funds use the following accounting approach for Proprietary funds: All of the Housing Authority's services are reported In enterprise funds. The focus of proprietary funds IS on income measurement, which, together with the maintenance of net assets. Is an Important financial indicator, FINANCIAL ANALYSIS

The Housing Authority's net assets were $3,258,999 as of June 30, 2008, Of this amount, $1.844,824 was Invested In capital assets, and the remaining $891,503 was unrestricted. There were $527,791 in specific assets restricted Housing Assistance Payments Also, there were $527,791 of general net assets restricted Housing Assistance Payments

CONDENSED FINANCIAL STATEMENTS

Condensed Balance Sheet (Excluding Interfund Transfers)

As of June 30, 2008

ASSETS

Current assets

Assets restricted Housing Assistance Payments

Capital assets, net of depreciation

Total assets

LIABILITIES Current liabilities Non-current liabilities

Total liabilities

NET ASSETS

Invested in capital assets, net of depreciation

Net assets restricted Housing Assistance Payments

Unrestricted net assets

Total net assets

Total liabilities and net assets

2008

999,574

3,258,999

3,372,189

2007

996,339

527,791

1,844,824

3.372,189

76,624 36,566

113,190

5,960

1,897,723

2,900,022

50,908 36,683

87,591

1,844,824 1,897,723

522,672 5,960

891,503 908,748

2,812,431

2,900,022

Housing Authority of St Landry; LA

Management's Discussion and Analysis (MD&A) June 30, 2008

CONDENSED FINANCIAL STATEMENTS (Continued)

The net assets of these funds increased by $446,569, or by 16%, from those of fiscal year 2007, as explained below. In the narrative that follows, the detail factors causing this change are discussed:

Condensed Statement of Revenues, Expenses, and Changes in Fund Net Assets (Excluding Interfund Transfers) Fiscal Year Ended June 30, 2008

2008

OPERATING REVENUES Tenant rental revenue Other tenant revenue

Total operating revenues

OPERATING EXPENSES

Federal Housing Assistance Payments (HAP) to landlords

Administration

Maintenance and repairs

Depreciation

General

Utilities Tenant services Protective services

Total operating expenses

(Losses) from operations

NON-OPERATING REVENUES

Federal grants for operations Other non-tenant revenue Interest Income Fraud Recovery

Total Non-Operating Revenues

NON-OPERATING EXPENSES Casualty losses

Total non-operating expenses

Income (loss) after non-operating revenues

OTHER CHANGES IN NET ASSETS

2007

211,951 4,287

216,238

1,968,079

482,462

230,047

191,651

109,204 52,474

219 -

3,034,136

(2,817,898)

3,114,056 14,386 13,122

8,398

3,149,962

.

_

173,866 4,750

178,616

2,203,172

438,694

247,797

171,893

115,625 49,694

-

3,240

3,230,115

(3,051,499)

2,702,974 16,541 10,658

11,632

2,741,805

667

667

332,064 (310,361

IV

Housing Authority of St Landry, LA

Management's Discussion and Analysis (MD&A) June 30. 2008

Federal grants for capital expenditures 114,505 261,927

NET INCREASE (DECREASE) IN NET ASSETS 446,569 (48,434)

NET ASSETS, Beginning of Year 2,823,998 2,860,864

Prior penod adjustments (11,568) -_

NET ASSETS, end of fiscal year 3,258,999 2,812,430

EXPLANATIONS OF FINANCIAL ANALYSIS

Compared with the prior fiscal year, total operating and non-operating revenues Increased $297,845, or by 9%, from a combination of larger offsetting factors. Reasons for most of this change are listed below in order of impact from greatest to least:

• Federal revenues from HUD for operations increased by $411,082, or by 15% from that ofthe prior fiscal year, The determination of operating grants is based in part upon operations performance of prior years. This amount fluctuates from year-to-year because of the complexities of the funding formula HUD employs. Generally, this formula calculates an allowable expense level adjusted for inflation, occupancy, and other factors, and then uses this final result as a basis for determining the grant amount. The amount of rent subsidy received from HUD depends upon an eligibility scale of each tenant. There was an Increase In the number of eligible tenants receiving subsidies, so Housing Assistance Grants increased accordingly, lowering the overall total.

• Federal Capital Funds from HUD decreased by $147,422, or by 56% from that of the prior fiscal year. The Housing Authority was still In the process of completing projects funded from grants by HUD for fiscal years 2005 through 2007, and submitted a new grant during fiscal year 2009.

• Total tenant revenue increased by $37,622, or by 21% from that of the prior fiscal year, due to these major factors: Tenant rental revenues increased by $38,085, or by 22%, because occupancy rates decreased by 3%, and because the amount of rent each tenant pays Is based on a sliding scale of their personal income. Some tenants' personal incomes increased, so rent revenue from these tenants increased accordingly, raising the overall total. Finally, other tenant revenues (such as fees collected from tenants for late payment of rent, damages to their units, and other assessments) decreased by $463, or by 10%.

• Total other non-operating revenue decreased by $5,167 from that of the prior fiscal year their revenue decreased by $5,167, or by 30%, because the Authority received proceeds from casualty Insurance claims, which are recorded as other income by the Authority in the year received.

• Interest income increased by $2,464, or by 23% from that of the prior fiscal year. The Housing Authority transferred $421,988 into temporary Investments during the current fiscal year, since the Authority spent available cash mostly on capital assets instead of temporary investments.

• Interest Income and Tenant revenues totaling $229,360, did not change significantly from the prior to the current year.

Housing Authority of St Landry, LA

Management's Discussion and Analysis (MD&A) June 30, 2008

Compared with the prior fiscal year, total operating and non-operating expenses decreased $196,646, or by 6%, but this also was made up of a combination of offsetting factors. Again, reasons for most of this change are listed below In order of Impact from greatest to least:

• Housing Assistance Payments to landlords decreased by $235,093, or by 11 % from that of the prior fiscal year, because there was a decrease in the number of tenants qualifying for subsidy during the year. Consequently, revenues from HUD for these subsidies Increased by S471,603

• Administrative Expenses Increased by $43,768, or by 10% from that of the prior fiscal year, due to a combination of offsetting factors: Administrative staff salaries increased by $15,944, or by 7%, but staff vacation and sick leave pay decreased by $365, or by 5%, however, related employee benefit contributions Increased by $27,383, or by 34%; therefore, total staff salaries and benefit costs increased by 14%, In addition, audit fees Increased by $5,820, or by 74%, accounting fees Increased by $13,769 legal fees Increased by $643. Finally, staff travel reimbursements increased by $9,103, but sundry expenses decreased by $29,527, or by 28%. therefore, other staff administrative expense decreased by 24%,

• Depreciation expense increased by $19,758, or by 11% from that of the prior fiscal year, because there was an increase In capital assets by $115,632,

• Maintenance and repairs decreased by $17,750, or by 7% from that of the prior fiscal year, due to several major factors: Repair staff wages Increased by $11,036, or by 10%, although, related employee benefit contributions decreased by $5,397, or by 9%, Also, materials used decreased by $5,182, or by 12%, and contract labor costs decreased by $18,208, or by 55%

» General Expenses decreased by $6,422 or by 6% from that of the prior fiscal year, primarily because Insurance premiums decreased by $4,873, or by 5%, since property and casualty insurance premiums decreased. Other general expenses also decreased by $654, Also, payments In lieu of taxes (PILOT) Increased by $1,167, or by 9%. PILOT Is calculated as a percentage of rent (which Increased by 22%) minus utilities (which increased 6%), and therefore changed proportionately to the changes In each of these. Uncollectible rents from vacated units decreased by $2,062, or by 29%, because these changed roughly proportional to rent, which increased by 22%,

• Protective services decreased by $3,240 from that of the prior fiscal year.

• Utilities Expense Increased by $2,780, or by 6% from that of the prior fiscal year, because water cost increased by $482, and electricity cost Increased by $1,062 and gas cost increased by S1,117. Finally, other utilities expense (such as garbage, sewage, and waste removal) increased by $119, or by 1%,

• Casualty losses decreased by $667 from that of the prior fiscal year, because.

• Tenant Sen/lces Increased by $219 from that of the prior fiscal year.

CAPITAL ASSET AND DEBT ADMINISTRATION

Capital Assets

\ !

Housing Authority of St Landry, LA

Management's Discussion and Analysis (MD&A) June 30, 2008

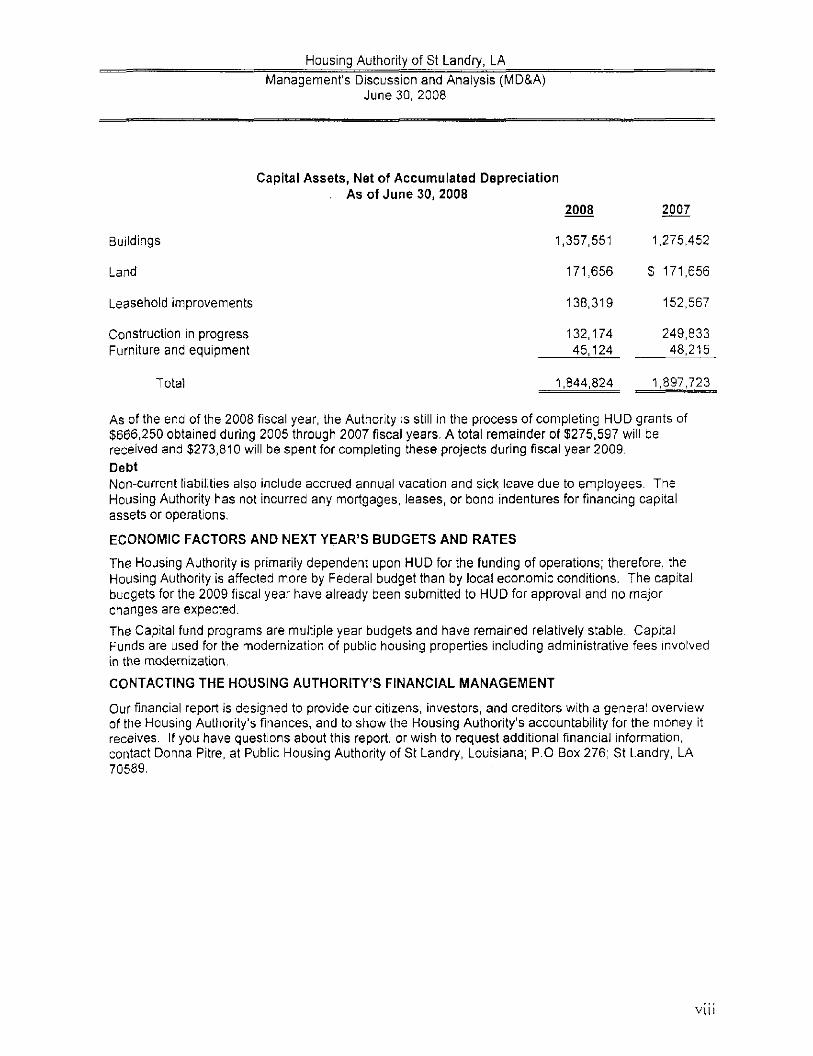

At June 30, 2008, the Housing Authority had a total cost of $7,263,992 invested In a broad range of assets and construction In progress from projects funded in 2005 through 2007, listed below. This amount, not including depreciation, represents Increases of $115,632 from the prior year. More detailed information about capital assets appears in the notes to the financial statements.

Vll

Housing Authority of St Landry, LA

Management's Discussion and Analysis (MD&A) June 30, 2008

1,357,551

171,656

138,319

132,174 45,124

1,844,824

1,275,452

$ 171,656

152,567

249,833 48,215

1,897,723

Capital Assets, Net of Accumulated Depreciation . As of June 30, 2008

2008 2007

Buildings

Land

Leasehold improvements

Construction in progress Furniture and equipment

Total

As of the end of the 2008 fiscal year, the Authority is still in the process of completing HUD grants of $666,250 obtained during 2005 through 2007 fiscal years. A total remainder of $275,597 will be received and $273,810 will be spent for completing these projects during fiscal year 2009. Debt Non-current liabilities also include accrued annual vacation and sick leave due to employees. The Housing Authority has not Incurred any mortgages, leases, or bond indentures for financing capital assets or operations.

ECONOMIC FACTORS AND NEXT YEAR'S BUDGETS AND RATES

The Housing Authority is primarily dependent upon HUD for the funding of operations; therefore, the Housing Authority is affected more by Federal budget than by local economic conditions. The capital budgets for the 2009 fiscal year have already been submitted to HUD for approval and no major changes are expected.

The Capital fund programs are multiple year budgets and have remained relatively stable. Capital Funds are used for the modernization of public housing properties including administrative fees involved In the modernization.

CONTACTING THE HOUSING AUTHORITY'S FINANCIAL MANAGEMENT

Our financial report is designed to provide our citizens, investors, and creditors with a general overview of the Housing Authority's finances, and to show the Housing Authority's accountability for the money it receives. If you have questions about this report, or wish to request additional financial Information, contact Donna Pitre, at Public Housing Authority of St Landry, Louisiana; P.O Box 276; St Landry, LA 70589,

vu:

RICHARD C . URBAN

CERTIFIED PUBLIC ACCOUNTANT

MEMBER.

AMERICAN INSTITUTE OF

CERTIFIED PUBLIC ACCOUNTANTS

SOCIETY OF LOUISIANA

CERTIFIED PUBLIC ACCOUNTANTS

OFFICE:

1112 HEATHER DRIVE

OPELOUSAS, LOUISIANA 70570

PHONE (337) 942-2154

FAX (337) 948-3813

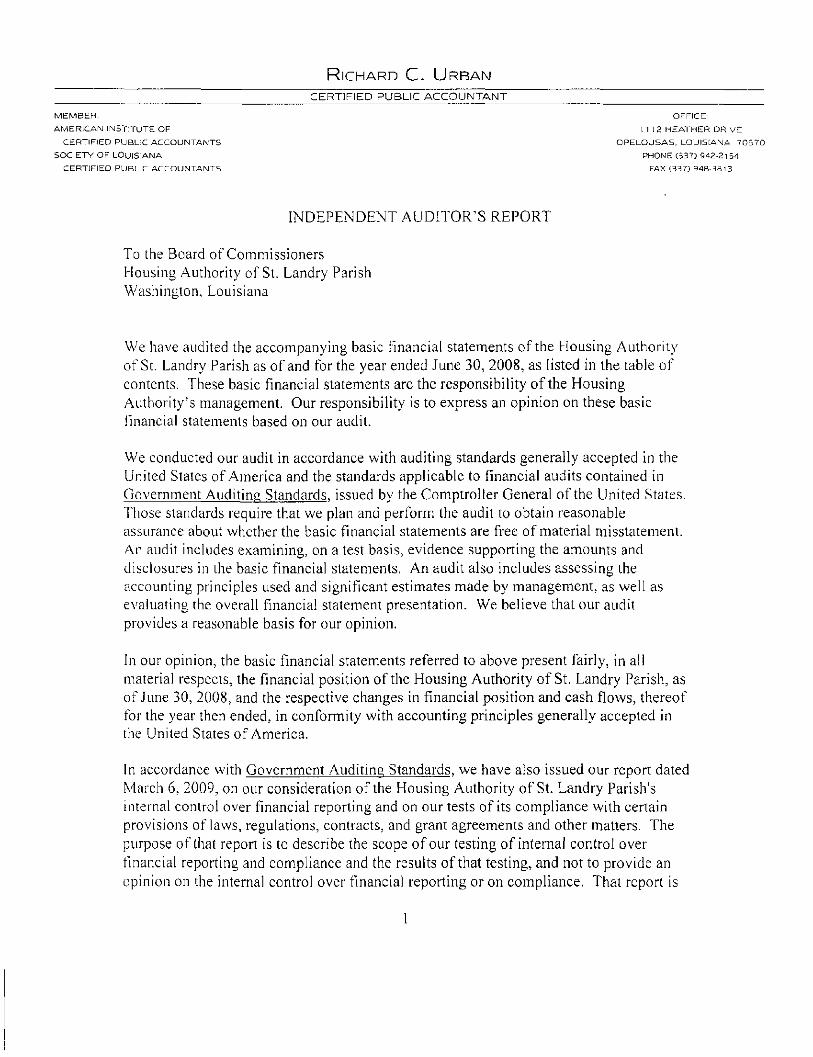

INDEPENDENT AUDITOR'S REPORT

To the Board of Commissioners Housing Authority of St. Landry Parisli Washington. Louisiana

We have audited the accompanying basic fmancial statements ofthe Mousing Authority of St. Landry Parish as of and for the year ended June 30, 2008, as listed in the table of contents. These basic financial statements are the responsibility ofthe Housing Authority's management. Our responsibility is to express an opinion on these basic financial statements based on our audit.

We conducted our audit in accordance with auditing standards generally accepted in the United Slates of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General ofthe United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the basic financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the basic financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the basic financial statements referred to above present fairly, in all material respects, the financial position ofthe Housing Authority of St. Landry Parish, as of June 30, 2008, and the respective changes in financial position and cash flows, thereof for the year then ended, in conformity with accounting principles generally accepted in the United States of America.

In accordance with Government Auditing Standards, we have also issued our report dated N4arch 6, 2009, on our consideration ofthe Housing Authority of St. Landry Parish's internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of intemal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. That report is

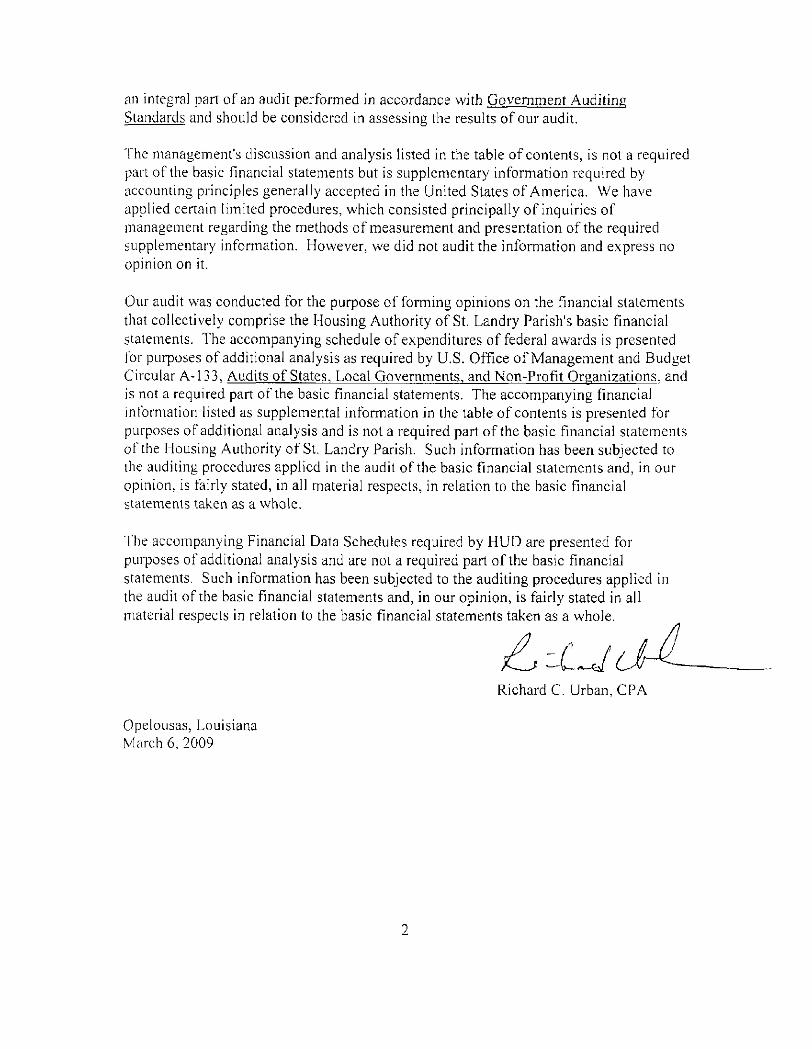

an integral part of an audit performed in accordance with Government Auditing Standards and should be considered in assessing the results of our audit.

The management's discussion and analysis listed in the table of contents, is not a required part ofthe basic financial statements but is supplementary information required by accounting principles generally accepted in the United States of America. We have applied cenain limited procedures, which consisted principally of inquiries of nianagement regarding the methods of measurement and presentation ofthe required supplementary information. However, we did not audit the information and express no opinion on it.

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the Housing Authority of St. Landry Parish's basic financial statements. The accompanying schedule of expenditures of federal awards is presented for purposes of additional analysis as required by U.S. Office of Management and Budget Circular A-133, Audits of States. Local Governments, and Non-Profit Organizations, and is not a required part ofthe basic financial statements. The accompanying fmancial information listed as supplemental information in the table of contents is presented for purposes of additional analysis and is not a required part ofthe basic fmancial statements ofthe Housing Authority of St. Landry Parish. Such information has been subjected to the auditing procedures applied in the audit ofthe basic financial statements and, in our opinion, is fairly stated, in all material respects, in relafion to the basic financial statements taken as a whole.

The accompanying Financial Data Schedules required by HUD are presented for purposes of additional analysis and are not a required part ofthe basic financial statements. Such information has been subjected to the auditing procedures applied in the audit ofthe basic financial statements and, in our opinion, is fairly stated in all material respects in relation to the basic financial statements taken as a whole.

Richard C. Urban. CPA

Opelousas, Louisiana N4arch 6, 2009

BASIC FINANCIAL STATEMENTS

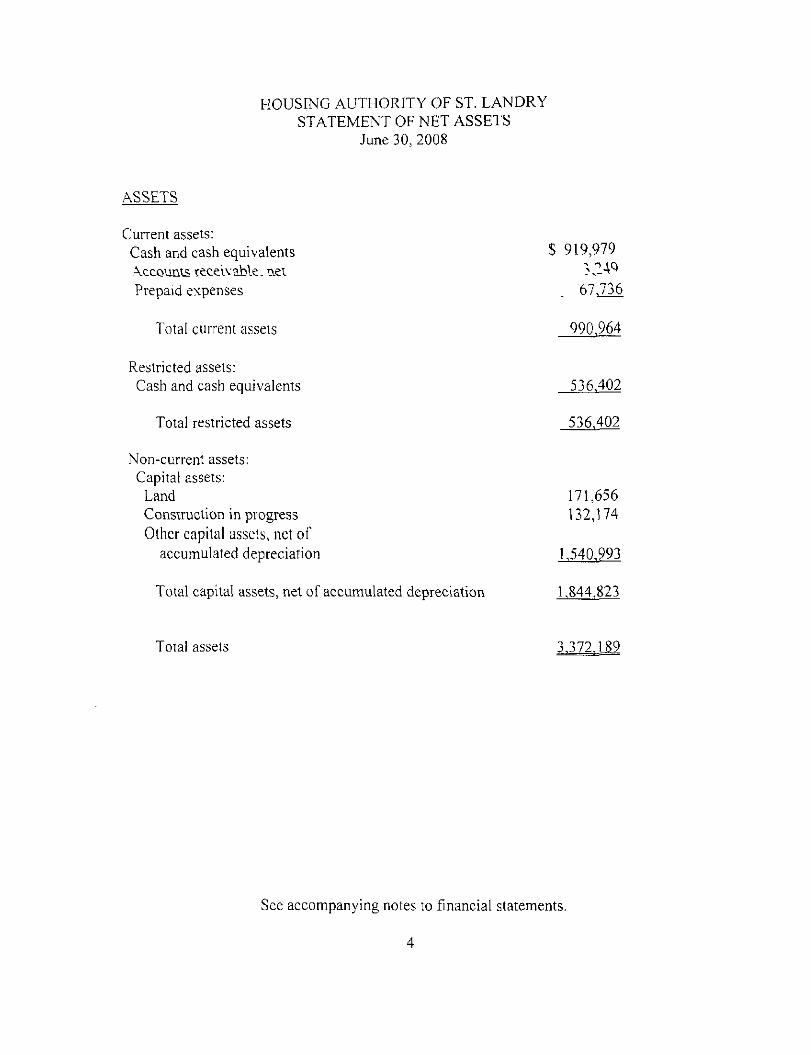

HOUSING AUTHORITY OF ST. LANDRY STATEMENT OF NET ASSETS

June 30, 2008

ASSETS

Current assets: Cash and cash equivalents $ 919,979 Accounts receivable, aei ?',-A^ Prepaid expenses 67.736

Total current assets 990,964

Restricted assets: Cash and cash equivalents 536.402

Total restricted assets 536.402

Non-current assets: Capital assets:

Land 171,656 Construction in progress 132,174 Other capital assets, net of

accumulated depreciation 1.540.993

Total capital assets, net of accumulated depreciation 1,844.823

Total assets 3.372.189

See accompanying notes to fmancial statements.

4

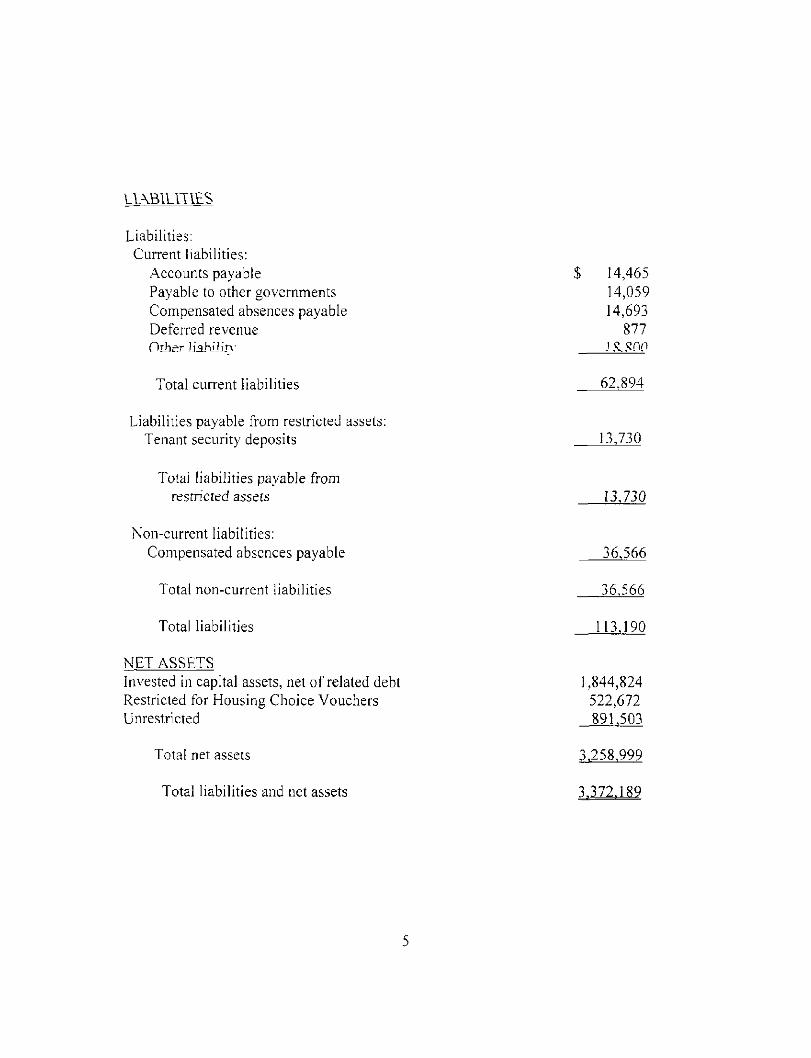

$ 14,465 14,059 14,693

877

62.894

13,730

LIABILITIES

Liabilities: Current liabilities:

Accounts payable Payable to other governments Compensated absences payable Deferred revenue OtlDcir Ji^hiJifA-

Total current liabilities

Liabilities payable from restricted assets; Tenant security deposits

Total liabilities payable from restricted assets 13J30

Non-current liabilities:

Compensated absences payable 36,566

Total non-current liabilities 36,566

Total liabilities 113,190

NET ASSETS Invested in capital assets, net of related debt 1,844,824 Restricted for Housing Choice Vouchers 522,672 Unrestricted 891.503

Total net assets 3.258.999

Total liabilities and net assets 3.372.189

HOUSING AUTHORITY OF ST. LANDRY STATEMENT OF REVENUES, EXPENSES AND

CHANGESIN NET ASSETS Year Ended June 30, 2008

OPERATING REVENUES Annual contributions - Housing Assistance Payments $ 2,323,455 HUD administrafive fee 361,190 Public housing operating subsidy 429,412 Tenant rental revenue 211,951 Other income 4,287

Total operating revenues 3,330.295

OPERATING EXPENSES Housing Assistance Payments 1,968,079 General and administrative 591,665 Repairs and maintenance 230,047 Utilities 52,474 Tenant services 219 Depreciation and amortization 167,906

Total operating expenses 3.010.390

Operating income (loss) 319,905

NON-OPERATING REVENUE (EXPENSE) Investment income 13,121 Miscellaneous expenses ( 27,294) Miscellaneous revenues 22,784

Total non-operating revenue (expense) 8.611

Income (loss) before other revenues, expenses, gains, losses

and transfers 328,516

Capital contributions (grants) 114,505

Increase (decrease) in net assets 443,021

Net assets, beginning of year 2.815,978

Net assets, end of year 3.258.999

See accompanying notes to financial statements. 6

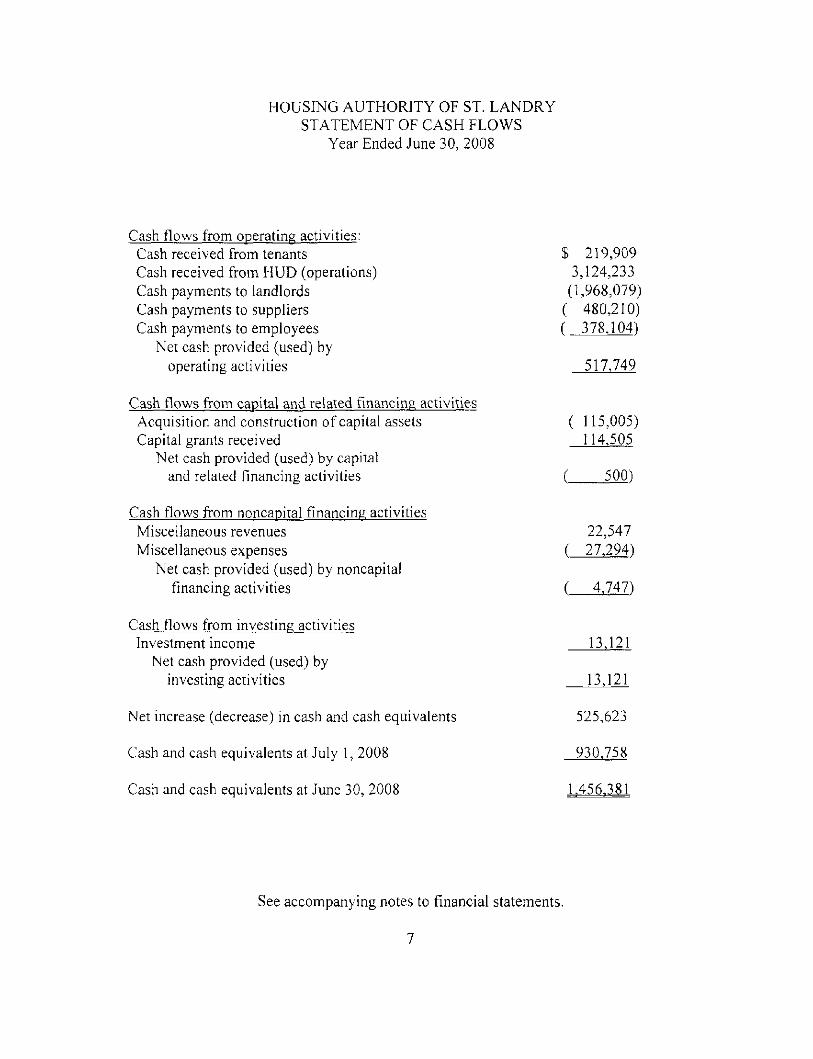

HOUSING AUTHORITY OF ST. LANDRY STATEMENT OF CASH FLOWS

Year Ended June 30, 2008

Cash flows from operating activities: Cash received from tenants Cash received from HUD (operations) Cash payments to landlords Cash payments to suppliers Cash payments to employees

Net cash provided (used) by operating activities

Cash flows from capital and related financing activities Acquisition and construction of capital assets Capital grants received

Net cash provided (used) by capital and related financing activities

Cash flows from noncapital financing activities Miscellaneous revenues Miscellaneous expenses

Net cash provided (used) by noncapital financing activities

Cash flows from investing activities Investment income

Net cash provided (used) by investing activities

Net increase (decrease) in cash and cash equivalents

Cash and cash equivalents at July 1, 2008

Cash and cash equivalents at June 30, 2008

$ 219,909 3,124,233

(1,968,079) ( 480,210) ( 378.104)

517,749

( 115,005) 114,505

500)

22,547 ( 27,294)

( 4,747)

13,121

13,121

525,623

930,758

.456.381

See accompanying notes to fmancial statements.

7

Reconciliation of operating income (loss) to net cash provided (used) by operating activities:

Operating income (loss) $ 319,905 Adjustments to reconcile operating

income (loss) to net cash provided (used) by operating activities: Depreciation 167,906 Changes in assets and liabilities: (Increase) decrease in accounts

receivable 10,847 (Increase) decrease in prepaid

expenses and other assets ( 6,743) Increase (decrease) in accounts

payable 4,476 Increase (decrease) in wages

and benefits payable ( 896) Increase (decrease) in payable to other governments 1,166 Increase (decrease) in other liability 12,364 Increase (decrease) in compensated

absences payable 7,047 Increase (decrease) in tenant security deposits 800 Increase (decrease) in deferred

revenue 877 Total adjustments 197,844

Net cash provided (used) by operating activities 517.749

-lOUSING AUTHORITY OF ST. LANDRY PARISH Washington, Louisiana

NOTES TO FINANCIAL STATEMENTS June 30, 2008

INTRODUCTION

The Housing Authority of St. Landry Parish (authority) was created by Louisiana Revised Statute (LSA-R.S.) 40.391 to engage in the acquisition, development, and administration of a low rent housing program to provide safe, sanitary, and affordable housing to the residents of St. Landry Parish, Louisiana.

The authority is administered by a six-member board appointed by the parish. Members ofthe board serve five-year staggered terms.

Under the United States Housing Act of 1937, as amended, the U.S. Department of Housing and Urban Development (HUD) has direct responsibility for administering low rent housing programs in the United States. Accordingly, HUD has entered into an annual contributions contract with the authority for the purpose of assisting the authority in financial the acquisition, construction, and leasing of housing units and to make annua! contributions (subsidies) to the authority for the purpose of maintaining this low rent character.

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The accompanying financial statements ofthe authority have been prepared in conformity with accounting principles generally accepted in the United States of America (GAAP) as applied to governmental units. The Governmental Accounting Standards Board (GASB) is the accepted standard setting body for establishing governmental accounting and fmancial reporting principles.

Financial Reporting Entitv

GASB Codification Section 2100 defines criteria for determining the governmental reporting entity and component units that should be included within the reporting entity. Because the authority is legally separate and fiscally independent, the authority is a separate governmental reporting entity.

The authority is a related organization ofthe Parish of St. Landry, since the parish appoints a voting majority ofthe authority's governing board. The parish is not financially accountable for the authority as it cannot impose its will on the authority

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

authority and there is no potential for the authority to provide financial benefit to, or impose financia! burdens on, the parish. Accordingly, the authority is not a component unit ofthe financia! reporting entity ofthe parish of St. Landry, Louisiana.

GASB Codification Section 2100 defines criteria for determining which component units should be considered part ofthe authority for financial reporting purposes. The basic criterion for including a potential component unit within the reporting entity is financial accountability. The GASB has set forth criteria to be considered in determining financial accountability. These criteria include:

1. Appointing a voting majority of an organization's governing body, and a. The ability ofthe authority to impose its will on that organization and/or b. The potential for the organization to provide specific fmancial benefits to, or

impose specific financial burdens on the authority. 2. Organizations for which the authority does not appoint a voting majority, but are

fiscally dependent on the authority. 3. Organizations for which the reporting entity financial statements would be

misleading if data ofthe organization is not included because ofthe nature or significance ofthe relationship.

Based on the previous criteria, the authority has determined that the following componeni unit should be considered as part ofthe authority reporting entity:

Si. Landry Public Housing Corporation is a legally separate entity. The members of the authority's board of commissioners also serve as the board of directors ofthe enlily. The authority has the ability to impose its will on the entity.

The Corporation was formed for the purpose of facilitating the development and financing of an affordable housing facility within the parish limits of St. Landry Parish. The Corporation is a partner in the developer partnership. However, since the investment limited partner owns 99+% interest in the partnership, the Corporation lakes the position that eventual control ofthe partnership rests with the investment limited partnership.

The partnership has entered into loan agreements and other financing arrangements that may have incurred contingent liabilities on behalf of the Corporation, but not any that would obligate the PHA. No contingencies have been reported in the PHA financial statements.

The material Corporation financial activities are included in the PHA fmancials through blended presentation.

Fund Accounting

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

The authority uses funds to report on its fmancial position and the results of its operations. Fund accounting is designed to demonstrate legal compliance and to aid financial management by segregating transactions relating to certain government functions or activities. A fund is a separate accounting entity with a self-balancing sei of accounts.

The authority accounts for its business-type activities as proprietary funds.

Proprietary funds are used to account for activities similar to those found in the private sector, Vv here the determination of net income is necessary or useful to sound fmancial administration. Operating income reported in proprietary fund financial statements includes revenues and expenses related to the primary, continuing operations ofthe fund. Principal operating revenues for proprietary funds are charges to tenants for rents or other services as well as operating subsidies received from HUD. Principal operating expenses are the costs of providing these services and include administrative expenses and depreciation of capital assets. Other revenues and expenses are classified as non-operating in the financial statements.

Basis of Accounting

The accrual basis of accounting is utilized by proprietary funds. Under this method, revenues are recorded when earned and expenses are recorded at the time liabilities are incurred.

Budgets

The authority prepares its financial statements in accordance with generally accepted accounting principles. In accordance with the provisions of its armual contributions contract with the Department of Housing and Urban Development, the authority prepares an annual budget. This budget is prepared in conformity with the accounting practices prescribed by HUD, which is a comprehensive basis of accounting other than generally accepted accounting principles. Because ofthe differences in accounting practices, no budgetary information is provided in this report.

The following are the budgetary practices prescribed by HUD and used by the authority:

The Executive Director prepares a proposed budget and submits same to the Board of Commissioners no later than thirty days prior to the beginning of each fiscal year. Following discussion and acceptance ofthe budget by the Board, it is sent to FIUD for approval. Upon approval by HUD, the budget is formally adopted. Any budgetary amendments require the approval ofthe Executive Director and the Board of CommhsiouQrs. Any budgetary appropriations lapse at the end of each fiscal year.

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

Cash and Cash Equivalents

Cash includes amounts in demand deposits, interest-bearing demand deposits. Cash equivalents include amounts in certificates of deposit with original maturides of 90 days or less. Under state law, the authority may deposit funds in demand deposits, interest-bearing demand deposits, money market accounts, or time deposits with state banks organized under Louisiana law and national banks having their principal offices in Louisiana.

Under state law, the authority may invest in United States bonds, treasury notes, or certificates. These are classified as investments if their original maturities exceed 90 days; however, if the original maturities are 90 days or less, they are classified as cash equivalents.

Prepaid Items

Payments made to insurance companies for coverage that will benefit the period beyond June 30, 2008 are recorded as prepaid insurance.

Capital Assets

Depreciation of all exhaustible capital assets used by the proprietary fund is charged as an expense against their operations. Depreciation has been provided over the estimated useful lives using the straight-line method. The estimated useful lives are as follows:

Dwelling structures 33 years Building improvements 15 years Vehicles, machinery and equipment 3-7 years

All fixed assets are stated at historical cost.

Compensated Absences

The authority follows Civil Service guidelines pertaining to the accumulation of vacation and sick leave for all employees other than the execudve director. The Board of Commissioners approved a resolution allowing the director to be paid for all accumulated annual leave upon his leaving. For all employees other than the executive director, this leave may be accumulated and carried over between fiscal years, with a maximum of 300 hours of payment of leave upon termination or retirement at their then current rate of pay. Employees do not receive payment for unused sick leave upon termination or retirement. The cost of current leave privileges, computed in accordance with GASB Codification Section C60, is recognized as a current expense in the proprietary fund. The unpaid

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

portion of leave privileges is recorded as a current liability in the proprietary fund.

\ 0 T £ 2 - C ASH W D C ASH tQV\V \ L t \ T S

At June 30, 2008, the authority has cash and cash equivalents totaling $1,456,381 as follows:

Interest-bearing demand deposit $ 1,034,343 Certificates of deposit 421,988 Other 50

Total 1,456,381

These deposits are stated at cost, which approximates market. Under state law, these deposits must be secured by federal deposit insurance or the pledge of securities owned by the fiscal agent. The market value ofthe pledged securities plus the federal deposit insurance must at all times equal the amount on deposit with the fiscal agent. These securities are held in the name ofthe pledging fiscal agent bank in a holding or custodial bank that is mutually acceptable to both parties. At June 30, 2008, the authority has $ 1,456,331 in deposits (bank balances), categorized below to reflect the amount of risk assumed by the authority.

GASB Category 1 GASB Category 2 GASB Category 3

$118,849 -

1,337.482 1,456,331

Even though the pledged securities are considered uncollateralized (Category 3) under the provisions of GASB Statement 3, Louisiana Revised Statue 39:1229 imposes a statutory requirement on the custodial bank to advertise and sell the pledged securities within 10 days of being notifled by the authority that the fiscal agent has failed to pay deposited funds upon demand.

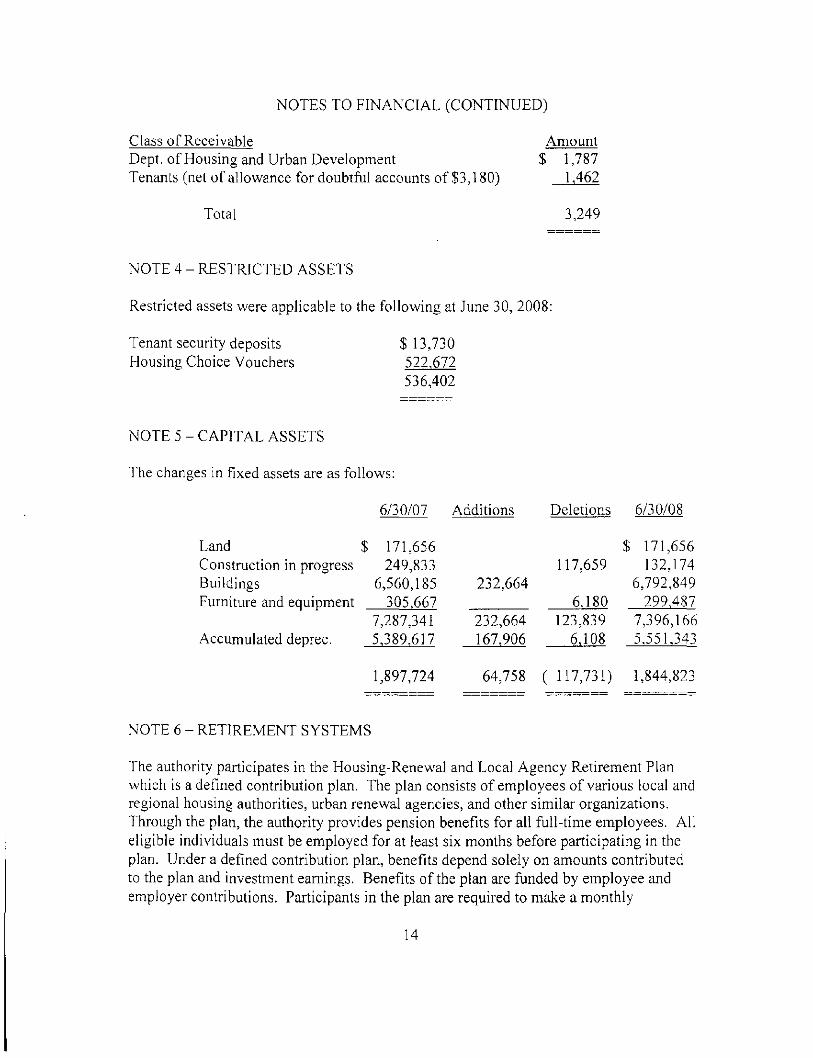

NOTE 3 - RECEIVABLES

The receivables of $3,249 at June 30, 2008, are as follows:

NOTES TO FINANCIAL (CONTINUED)

Class of Receivable Amount Dept. of Housing and Urban Development $ 1,787 Tenants (net of allowance for doubtful accounts of $3,180) 1,462

Total 3,249

NOTE 4 - RESTRICTED ASSETS

Restricted assets were applicable to the following at June 30, 2008:

Tenant security deposits $ 13,730 Housing Choice Vouchers 522.672

536,402

NOTE 5 - CAPITAL ASSETS

The changes in fixed assets are as follows:

6/30/07 Additions Deletions 6/30/08

Land $ 171,656 $ 171,656 Construction in progress 249,833 117,659 132,174 Buildings 6,560,185 232,664 6,792,849 Furniture and equipment 305.667 6,180 299,487

7,287,341 232,664 123,839 7,396,166 Accumulated deprec. 5,389.617 167,906 6,108 5.551,343

1,897,724 64,758 ( 117,731) 1,844,823

NOTE 6 - RETIREMENT SYSTEMS

The authority participates in the FIousing-Renewal and Local Agency Refirement Plan which is a defined contribution plan. The plan consists of employees of various local and regional housing authorities, urban renewal agencies, and other similar organizations. Through the plan, the authority provides pension benefits for all full-time employees. All eligible individuals must be employed for at least six months before participating in the plan. Under a defined contribution plan, benefits depend solely on amounts contributed to the plan and investment earnings. Benefits ofthe plan are funded by employee and employer contributions. Participants in the plan are required to make a monthly

14

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

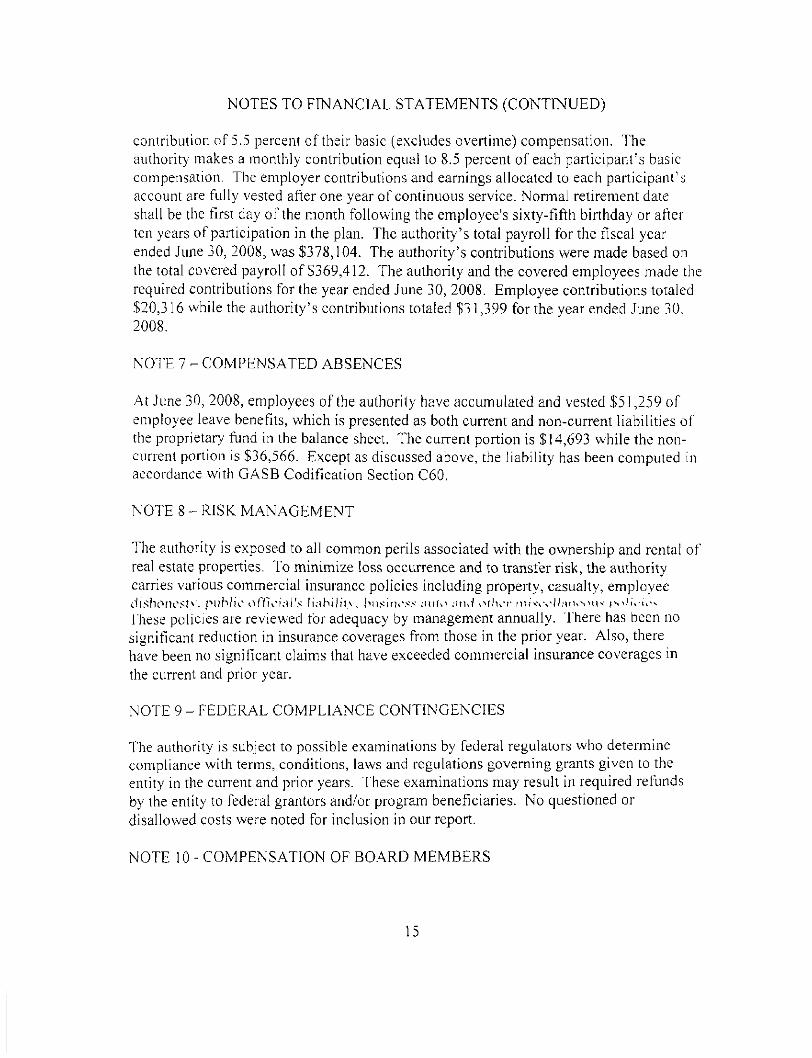

contribution of 5.5 percent of their basic (excludes overtime) compensation. The authority makes a monthly contribution equal to 8.5 percent of each participant's basic compensation. The employer contributions and earnings allocated to each participant's account are fully vested after one year of continuous service. Normal retirement date shall be the first day ofthe month following the employee's sixty-fifth birthday or after ten years of participation in the plan. The authority's total payroll for the fiscal year ended June 30, 2008, was $378,104. The authority's contribufions were made based on the total covered payroll of $369,412. The authority and the covered employees made the required contributions for the year ended June 30, 2008. Employee contributions totaled $20,316 while the authority's contributions totaled $31,399 for the year ended June 30. 2008.

NOTE 7 - COMPENSATED ABSENCES

At June 30, 2008, employees of the authority have accumulated and vested $51,259 of employee leave benefits, which is presented as both current and non-current liabilities of the proprietary fund in the balance sheet. The current portion is $14,693 while the non-current portion is $36,566. Except as discussed above, the liability has been computed in accordance with GASB Codification Secfion C60.

NOTE 8 - RISK MANAGEMENT

The authority is exposed to all common perils associated with the ownership and rental of real estate properties. To minimize loss occurrence and to transfer risk, the authority carries various commercial insurance policies including property, casualty, employee dishonesh". nubh'c offK'i.-il's li.-)hi!iM . bns inoss :i\iu> .•uuf ^^rhv'^ nu'vv-v'ir'UKN^n^- ^s>li\-u'v

These policies are reviewed for adequacy by management annually, fhere has been no significant reduction in insurance coverages from those in the prior year. Also, there have been no significant claims that have exceeded commercial insurance coverages in the current and prior year.

NOTE 9 - FEDERAL COMPLIANCE CONTINGENCIES

The authority is subject to possible examinations by federal regulators who determine compliance with terms, conditions, laws and regulations governing grants given to the entity in the current and prior years. These examinations may result in required refunds by the entity to federal grantors and/or program beneficiaries. No questioned or disallowed costs were noted for inclusion in our report.

NOTE 10 - COMPENSATION OF BOARD MEMBERS

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

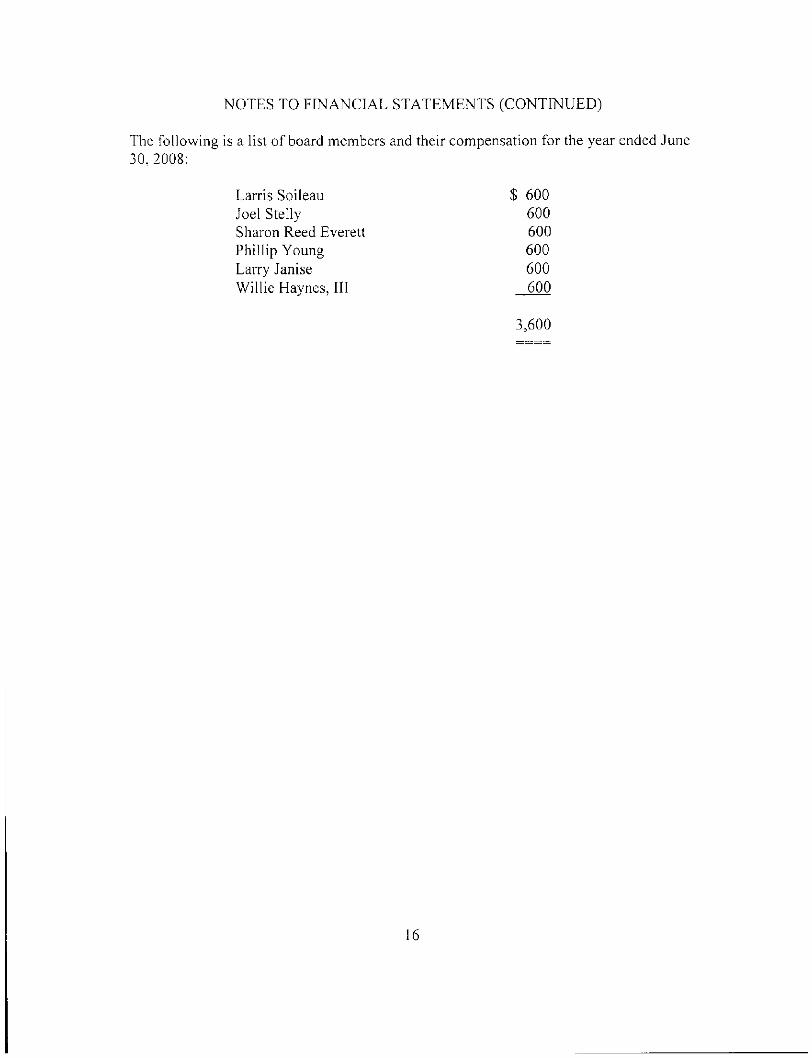

The following is a list of board members and their compensation for the year ended June 30,2008:

Larris Soileau $ 600 Joel Stelly 600 Sharon Reed Everett 600 Phillip Young 600 Larry Janise 600 Willie Haynes, III 600

3,600

OTHER REPORTS AND SCHEDULES

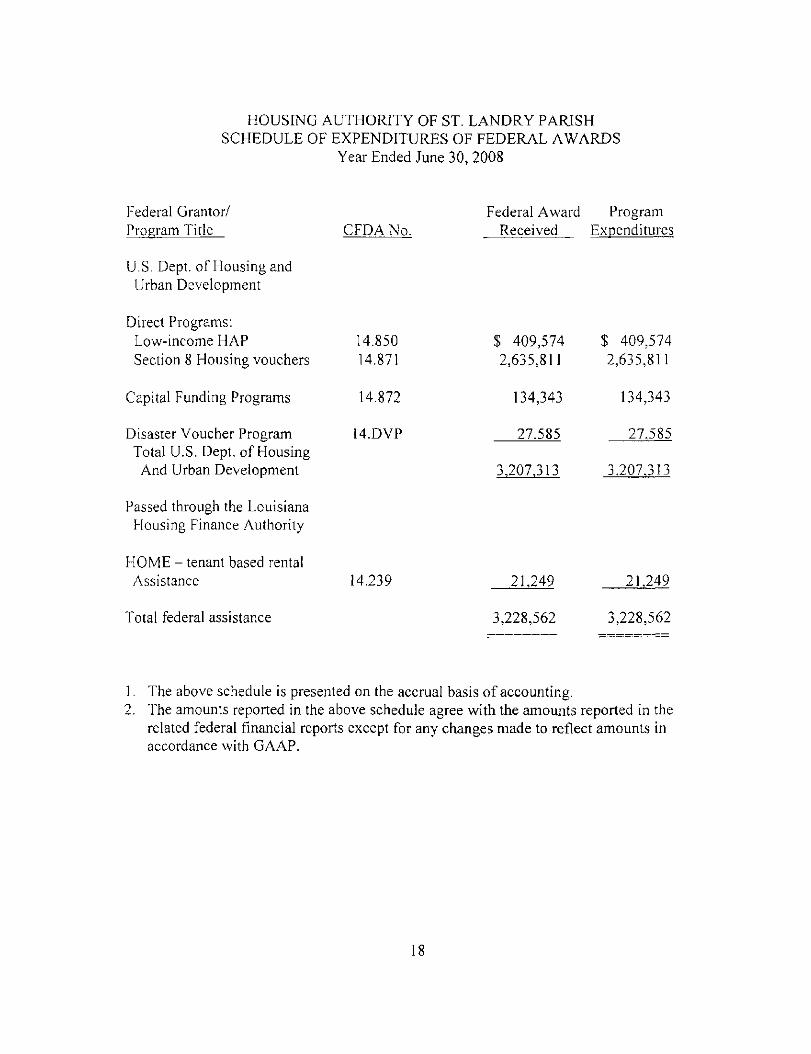

HOUSING AUTHORITY OF ST. LANDRY PARISH SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS

Year Ended June 30. 2008

Federal Grantor/ Program Title CFDA No.

Federal Award Program Received Expenditures

U.S. Dept. of Housing and Urban Development

Direct Programs: Low-income HAP Section 8 Housing vouchers

Capital Funding Programs

Disaster Voucher Program Total U.S. Dept. of Housing And Urban Development

14.850 14.871

14.872

4.DVP

$ 409,574 2,635,811

134,343

27,585

3.207,313

$ 409,574 2,635,811

134,343

27,585

3,207,313

Passed through the Louisiana Housing Finance Authority

HOME - tenant based rental Assistance 4.239 21,249 21,249

Total federal assistance 3,228,562 3,228,562

1. The above schedule is presented on the accrual basis of accounting. 2. The amounts reported in the above schedule agree with the amounts reported in the

related federal financial reports except for any changes made to reflect amounts in accordance with GAAP.

RICHARD C . U R B A N CERTIFIED PUBLIC ACCOUNTANT

MEMBER-

AMERICAN INSTITUTE OF

CERTIFIED PUBLIC ACCOUNTANTS

SOCIETV OF LOUISIANA

CERTIFIED PUBLIC ACCOUNIANTS

OFFICE:

1112 HEATHER DRIVE

OPELOUSAS, LOUISIANA 7057C

PHONE (3371 9 4 2 . i i 5 4

FAX (337) 948 35 i ^

Board of Commissioners Housing Authority of St. Landry Parish Washington. Louisiana

REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COIVIPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF

FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

We have audited the financial statements ofthe business-type activities ofthe Housing Auiliority of St. Landry Parish, as of and for the year ended June 30, 2008, which collectively comprise the Housing Authority's basic financial statements and have issued our report thereon dated March 6, 2009. We conducted our audit in accordance with audiiing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General ofthe United States.

Internal Control Over Financial Reporting

In planning and performing our audit, we considered the Housing Authority's internal control over financial reporting as a basis for designing in our auditing procedures for the purpose of expressing our opinions on the financial statements, but not for the purpose of expressing an opinion on the effectiveness ofthe Housing Authority's intemal control over financial reporting. Accordingly, we do not express an opinion on the effectiveness ofthe Housing Authority's internal control over financial reporting.

A control deficiency exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent or detect misstatements on a timely basis. A significant deficiency is a control deficiency, or combination of control deficiencies, that adversely affects the Housing Authority's ability to initiate, authorize, record, process, or report financial data reliably in accordance with generally accepted accounting principles such that there is more than a remote likelihood that a misstatement ofthe Housing Authority's financial statements that is more than inconsequential will not be prevented or detected by the Housing Authority's internal control.

A material weakness is a significant deficiency, or combination of significant deficiencies, that results in more than a remote likelihood that a material misstatement of

the financial statements will not be prevented or detected by the Housing Authority's internal control.

Our consideration of intemal control over financial reporting was for the limited purpose described in the first paragraph of this section and would not necessarily identify all deficiencies in internal control that might be significant deficiencies or material weaknesses. We did not identify any deficiencies in intemal control over financial reporting that we consider to be material weaknesses, as defined above.

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Housing Authority ofthe City of Alexandria, Louisiana's financial statements are free of material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards.

This report is intended for the information ofthe Board of Commissioners, management, the Department of Housing and Urban Development, and the Legislative Auditor of the State of Louisiana, and is not intended to be and should not be used by anyone other than these specified parties. Under Louisiana Revised Statute 24:513, this report is distributed by the Legislative Auditor as a public document.

/ i dj-Richard C. Urban, CPA

Opelousas, Louisiana March 6, 2009

20

RICHARD C . URBAN

CERTIFIED PUBLIC ACCOUNTANT

MEMBER:

AMERICAN INSTITUTE OF

CERTIFIED PUBLIC ACCOUNTANTS

SOCIETY OF LOUISIANA

CERTIFIED PUBLIC ACCOUNTANTS

OFFICE.

1112 HEATHER DRIVE

OPELOUSAS. LOUISIANA l O ' j ' O

PHONE (337) 9A2-?.^'y,

FAX C337) 948-381 i

Board of Commissioners Housing Authority of St. Landry Parish Washington. Louisiana

REPORT ON COMPLIANCE WITH REQUIREMENTS APPLICABLE TO EACH MAJOR PROGRAM A.\D 0 . \ INTERNAL CO.\TROL 0 \ ER CO.MPi.LWCK IN

ACCORDANCE WITH OMB CIRCULAR A-133

Compliance

We have audited the compliance ofthe Housing Authority of St. Landry Parish, with the types of compliance requirements described in the U.S. Office of Management and Budget (OMB) Circular A-133 Compliance Supplement that are applicable to each of its major federal programs for the year ended June 30, 2008. The Housing Authority's major federal programs are identified in the summary of auditor's results section ofthe accompanying schedule of findings and questioned costs. Compliance with the requirements of laws, regulations, contracts and grants applicable to each of its major federal programs is the responsibility ofthe Housing Authority's management. Our responsibility is to express an opinion on the Housing Authority 's compliance based on our audit.

We conducted our audit of compliance in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General ofthe United States, and OMB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations. Those standards and OMB Circular A-133 require that we plan and perform ihe audit to obtain reasonable assurance about whether noncompliance with the types of compliance requirements referred to above that could have a direct and material effect on a major federal program occurred. An audit includes examining, on a test basis, evidence about the Housing Authority's compliance with those requirements and performing such other procedures as we considered necessary in the circumstances. We believe that our audit pro^•ides a reasonable basis for our opinion. Our audit does not provide a legal delerminaiion on the Housing Authority of St. Landry Parish's compliance with those require;77enrs.

In our opinion, the Housing Authority of St. Landry Parish complied, in all material respects, with the requirements referred to above that are applicable to each of its major federal programs for the year ended June 30, 2008.

21

Internal Control Over Compliance

The management ofthe Housing Authority is responsible for establishing and maintaining effective internal control over compliance with requirements of laws, regulations, contracts and grants applicable to federal programs. In planning and performing our audit, we considered the Housing Authority's intemal control over compliance with requirements that could have a direct and material effect on a major federal program in order to determine our auditing procedures for the purpose of expressing our opinion on compliance, but not for the purpose of expressing an opinion on the effectiveness of internal control over compliance. Accordingly, we do not express an opinion on the effectiveness ofthe Housing Authority's internal control over compliance.

A control deficiency in an entity's internal control over compliance exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent or detect noncompliance with a type of compliance requirement of a federal program on a timely basis. A significant deficiency is a control deficiency, or combination of control deficiencies, that adversely affects the entity's ability to administer a federal program such that there is more that a remote likelihood that noncompliance with a type of compliance requirement of a federal program that is more than inconsequential will not be prevented or detected by the entity's internal control.

A material weakness is a significant deficiency, or combination of significant deficiencies, that results in more than a remote likelihood that material noncompliance with a type of compliance requirement of a federal program will not be prevented or detected by the entity's internal control.

Our consideration of intemal control over compliance was for the limited purpose described in the first paragraph of this section and would not necessarily identify all deficiencies in internal control that might be significant deficiencies or material weaknesses. We did not identify any deficiencies in internal control over compliance that we consider to be material weaknesses, as defined above.

This report is intended for the information ofthe Board of Commissioners, management, the Department of Housing and Urban Development, and the Legislative Auditor ofthe State of Louisiana, and is not intended to be used by anyone other than these specified parties. Under Louisiana Revised Statute 24:513, this report is distributed by the Legislative Auditor as a public document.

Richard C. Urban, CPA

Opelousas, Louisiana March 6. 2009

22

HOUSING AUTHORITY OF ST. LANDRY PARISH STATUS OF PRIOR AUDIT FEMDINGS

The previous audit contained no findings or quesfioned costs.

23

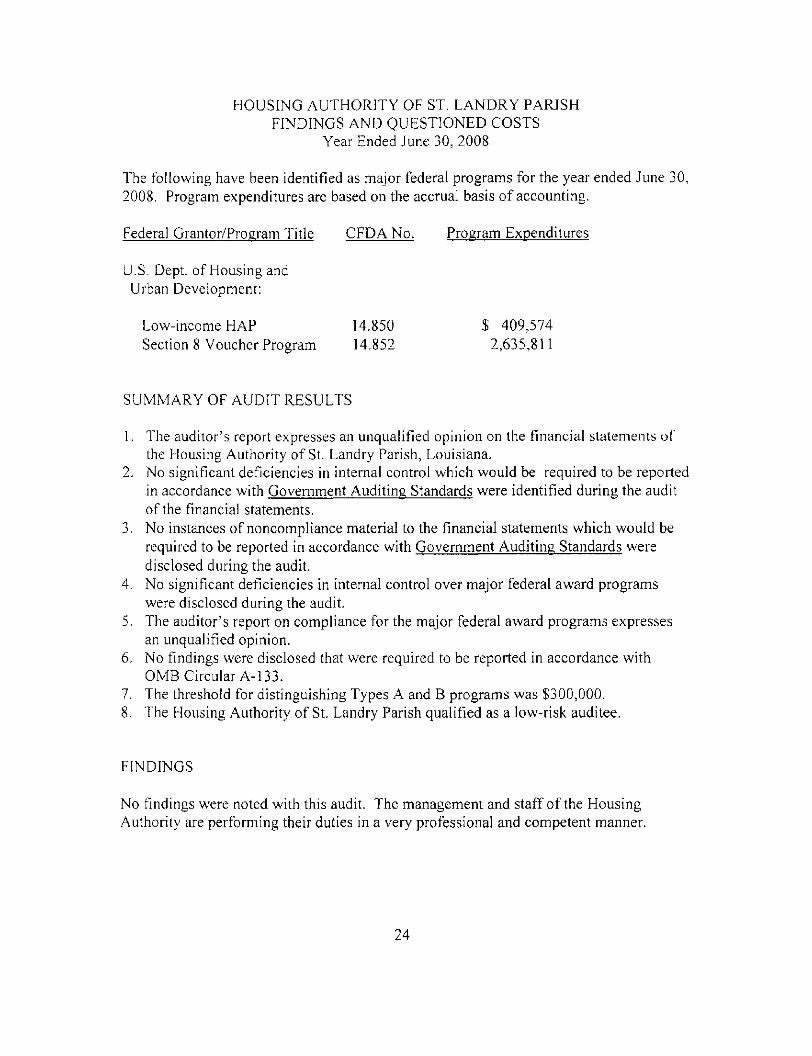

HOUSING AUTHORITY OF ST. LANDRY PARISH FINDINGS AND QUESTIONED COSTS

YearEnded June 30, 2008

The following have been identified as major federal programs for the year ended June 30, 2008. Program expenditures are based on the accrual basis of accounting.

Federal Grantor/Program Title CFDA No. Program Expenditures

U.S. Dept. of Housing and Urban Development:

Low-income HAP 14.850 $ 409,574 Section 8 Voucher Program 14.852 2,635,811

SUMMARY OF AUDIT RESULTS

1. The auditor's report expresses an unqualified opinion on the financial statements of the Housing Authority of St. Landry Parish, Louisiana.

2. No significant deficiencies in intemal control which would be required to be reported in accordance with Government Auditing Standards were identified during the audit ofthe financial statements.

3. No instances of noncompliance material to the financial statements which would be required to be reported in accordance with Government Auditing Standards were disclosed during the audit.

4. No significant deficiencies in internal control over major federal award programs were disclosed during the audit.

5. The auditor's report on compliance for the major federal award programs expresses an unqualified opinion.

6. No findings were disclosed that were required to be reported in accordance with OMB Circular A-133.

7. The threshold for distinguishing Types A and B programs was $300,000. 8. The Housing Authority of St. Landry Parish qualified as a low-risk auditee.

FINDINGS

No findings were noted with this audit. The management and staff of the Housing Authority are performing their duties in a very professional and competent manner.

24

{ y:in - Co lured Cfll.s art' Self- l*o|>ululin^

"i ollu\s - folori'd Celh line Detiiil Links

(jr;iv - Colori'd Ccll.s iiri' Disallowi-d Knlrv'

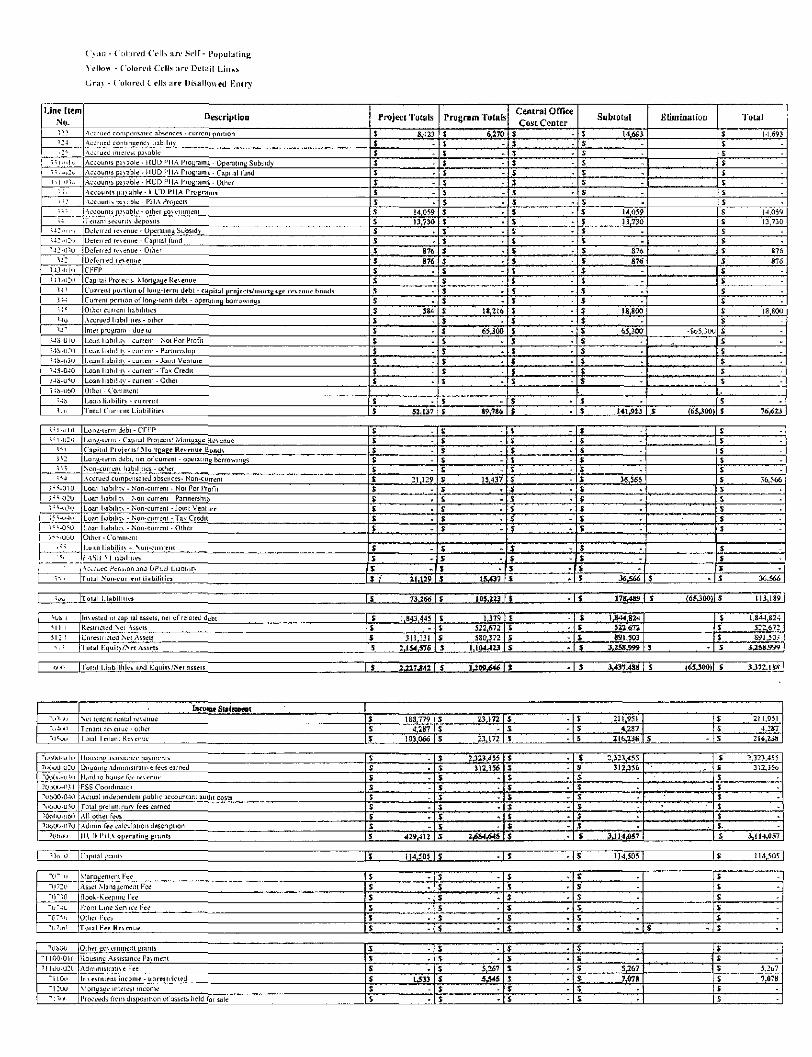

Line Item No.

.-111 11:

I H 1 14

11^ HKt

D e s c r i p f i o n

••'• . ' > •BalaneftSfceM ' Cash-unri'sincicd C^sh-rcsiriclcd-iTiodcrniMliori and devclopmcnl

Cash-oihLT resirniLcd

Caih-lenaiiL ic i 'unu di-posili

Caih • Hcsiticifd tor pin mem of current liabiliiv

Joi-.tl Cadi

Project lotals Program Totals Central Omce

Cost Center Subtotal £Uiainatioa Total

$ 200.752 s

J 13,730

S J 2M.482

S •" 297.239 S

% S22.672

S S «19.9n s

y 497,991

$ X 522,672 S .13,730

$ S 1 ,03433 s

S 497,991-s J 522.671 S 13.730

S S l , f l l 4 3 W

\2\

i 2 : - u i u

1 : : - i o o

i : : - ' i30 i : :

A l l i ums ruceiv a bit' - PI i A pio|i,'i:li

Accounu (oCfiv able - HUD mher projCcis - Operaiinu Subiidv

Accounts receivable - HUD oiher proiecis - Capital fund

Accounis receivable; - HUD other projecis - Other

Arcounl i rrcci*iible - 1 HID other proifCIs

i r - Accouni lijCL'ivable • olhci i:o\ctnmi:ni

i ;^-Ol i j Accouni rcciiisabk-- miscellariiMus - Nul For Piofii

1Z5-U20 lAccouni rei:ei\-ablc - miscellainious - Panncrship

i:.'-OjO 1 :5-04U I ; . ' - O N J

1 :^-i.k6" 12^

l l f .

1 2b 1

1 : o : 12^

i :s 1 : . i 1

i ] ' i

i :u

Accouni n^Tdivable - miscellaneous - Joini Venture Accouni receivable - miscellaneous - Tax Credit Accouni receivable - miscellaneous - Oiher

Other - Comment

Accuuni lecriv^ible - miicclliiiieous

Account receivable - lenaiils

Allovvance lor Joubiful accounis - lenanis Allowance for doubiful accounis - oiher

Notei. Loans, A Monijanes Receivable • Curreni Fraud recoverv

Allovviince lor doubtful accounts • fraud Accrued inleresi leceivable

Total receivable, net of allowance for doublfu) accounij

$ S i.7B7

S

S 1,787

$ $ S

$ r

* s

5

$ 4,642

S, (3.180)

$ I

J

s s S 304?

$ s

$ - J

s $ s - . $ . • . - .

' $ . . • . , " . -

s

J ' - , - • •

%' ' ' '

s S 1,737

$ 5 1,787

S

$

-S ^4.643

S- . . a i 8 0 )

s

$ 3 0 4 9

..-

.' , . . , - .

• : - • ; •

. - . i . •, .-_ . t ' l , . -\ - . • „ - -•

I , ; ..t. • ,

S

s S 1.787 £

5 1.787

S

s

s s s

5 4,642

5 (3,180)

$

S 3049

1.51

1 • : \ 'si

u : U i

U.! 1

NJ

l-;^

1^0

Investments • unresiricicd Investments • restricted Inveiimenii • Resiricled for pavmem ofcurrent liabililv Prepaid e.\pen5C5 and oiher assets

Inventories Allowance lor obsolete inventories

Inier prouram - due from

Asseis held for sale

' lotal Curreni AisrH

$ 45,000

$ $ 5 6 , 3 «

S s $ 65.300

$ -S 3S4397

$ . 371.869

S. • • • S,U9 5 ' . - . . • .

•S - • 11,170

5 ' •

5 ' S

$ u o s ^ s

$ . $ s • • . ' t s . . -% ' ' • . ' ' -

S 416,869

$ 5,119

. s • . $ ' 67,736

V • •• -

$ - • . . $ '

$ • • • - iS 65,300

S . - . s S - J 1492,666

•S65..1O0

$ (653001

V 416.Sfa?

S 5.119

5 S 67,736 X

S . 1 J27,366 '

ih i

\< -z

l u i

IW

Land

!3uildini;s

Kurnilurc, ti|uipmeiii and machinery - dwellings

[•urniiuie. etiuipmeiu and machincrv - adnunisirauon

16- iLcasehold impio^ftiienis

U>"

lo"'

16a Icy)

Accumulated Jepreciaiion

Construction in prouress

Inlrastruciure

Total eapiul asietj, net of ticcumulalfd dturrc i i i l io i i

171-010 i 7 i . o : u

171-030

I7I.UJ0 jTI- i j -O |7l-(i(,.i1

l^'l

1'2-010

i 7 : . o : o i 7 : - u ; o

17:-040 172-0-0

I"2-Oo0 U2

r . i

Notes, Loans, & monuaues receivable - Non-current - Not For Ptofit Notes, Loans. & monuflgcs receivable - Non-current - Pannerihip

Notes, Loans, A mortnat;es receivable - Non-current • Joint Venture

Notes, Loans, & monnaues receivable - Non-current - Tax Credit Noies, Loans. & monuayes receivable - Non-currcnl - Other Other - Commeni .Noi.'i, l.oHiii, i i mongaEfs receivublc - Non-rurreni

Noirt, Loanj, & monyajtei ;eceivable • Non-current - pasi due • Not For Profit

NotL-s, Loans, .t monnauca receivable - Non-current • Pannership Notes, Loans, & monuaues receivable - Non-current - Joint Venture

Notes. Loans, A monjjaues receivable - Non-current - Tax Credit Noies. Loans, l i monuanes receivable • Non-current • Oiher Oilier - Comment

.Notes. Loans, J^ nionnHgej rrceivablc - N'on-currrnl - past due Grams receivable - Non-current

17-UOlO lOlhiT aSiCii - Noi i-orProlli 17-1-020 i7-i-o.;(j

1 74-LUO

IT-l-O^il

17-1-000 17.:

r i . - ( . i i i j

1 7(1-020

170-0.; 0

1 Itt-OAil

1 7^./i50

I't.-OoO

\ -b ISO

Other asseis - Pannership

Other assets - Joint Venture

Oiher i i iseii • Ta\ Credit

Other asseis - Other

Other • Commeni

Other assets

Invesimeni in Joini veniure- Not For Profii

nvestnicni in Joint venture - Pannership

Inv esimeiii in Joini v enture - Joint Venture

:n\estmeni in Joint venture- Ta.\ Credit

nvestmcnt m Joint veniure - Other

Other - Commeni

Invfstnirni in joint vml i i rc

Toial ,Non-curreni .Vssets

S 171.656 $ 5.781,494

S 98,896

$ 142,7M

ST 1,0I1,35S S . (5,JW.9I5)

S 132,174

S

S 1,*43,444

s

$ -$

- , I '7.

$ % s s s • • *;

" , 1 . , ; :

s s S T

$ J

s . -

s . ,. . jr

$ s

. . 1 ^ ^ . . . , - „ -

S , 1*13,444

$ t

$ $ • 57,807 S. . , .

i -. . (36,428)

J, • , - . " . - •

s '• • W W

S

s • \ . - '

% $ i . . . ' . . ' -. :• % • • - •

$ > - , •

S • . . ' -.

-$ 171,656 S 5,781,494

J . . - , 98.896

S . 200.591

$ -1,011.355 % • •(5,55].343)

•S . . 132,174

I ' . - . - - -

,'% \ M 4 » U S

$ 171,656

$ 5.7BI.491 V 98.S96 $ 200.591

S 1.01 l J 5 i S .(5,551,343)

5 132,174

5 1,844,823

S • . * '• S • - . r-

S . , , ^. . . .- ,

J J .. . . .

i _ " - ,.-.-..^ s • ' • " : ' . :

' i • ; : $ ' • " : • • ' '••••.•

.,' ,.» . ,.,.^, .. ',

$ %

• \ ' * ; ' • • ,

• - "- M . • 1 . . . )

J • • ' , ;

s : .' -- V

V • - . , . : • t-J79

s •

.s '

s

J •' --, '•- • • $ • * ;

s

$ ' S . . • • 'f

s s - • '• .

$

J • ^ , , _,'

s . - • •

J

. - . . . , . - • , , * - ~ ' - . .

'5 . ' "" *. ' . •

' • $ ' . , . - -

S ' - ' . ' ' -J . , - • .

$ •• • ' • - -•

:,"","":'; T -

s . •• ' • J . , ' y . .

J ,

• / : ' . / . i ' , " ' ; • - • , s '. .

$ " , ' ' ' ' .' s • , . - . • -

$ . • $ . ; . ' . - • " . : . ,

J . ;• , '" ".•.

$ -' . . -t '. • -

s . •

% . M344,a23

. , .:. , *. , - ' - ' ' • . . .

- - - - ' • • , • ,

i - . ' , ' : ;' <:y

.. -.

^ : . : , , y , - . ' f , ' '•

' ' • • - • • '

• ' • - , • • . ' . ; . . . . . _ ' ,

- . ; . ' - ' . - ' ' ' • ; , - . '

^ - ; • ' - • " •

^ -. ^ ', ;. .-

> , . . •-. t -.•- •

• , •, ^- V, ' '•-. -J

- .• . ' , u . , , .)

•. , - , . H ' • . ' I . ;

. . ; . , + . ' . .'.. . .;

- - • ' - " • . ' - ' . ' .

-'. . : ""' '\ . . ' - - ' - . • % . ,

, - . . - ^ - . . . ' . " . " - •

•

5 , -

% -• ^ . ' - , " • • - •

S

• j - ' - — — •

$ IJW4.S23 :

l-Ay iToial Ajsfis [. S , 3 J I 7 , 8 4 I | "5 • ' U » , M 8 | $ • . ' - ! J • 3 ^ 7 / 1 8 9 ! S ' (65300)1 S 3372,189!

i l 1 iBjnkovtftdrari

,H2

; i ;

321

•\ccounis pavable <= 'W davs

Accounts pavable > "SO davs past due

Accrued waud pavroll ia\es pavable

J ^ . ::• v : : . - , . ' , ' •. S 14.465 S $ ^ s . . -s • . • •- i . • . \ • -

I * -

$ J • -• •-s . . . •..

s -i : - H465

\ • • -v

.S .

S

$ M,46S

J

$

C'>iiii - (o lu i cd C\•ll^ ari' Self- Copula t ins

\ elloi\ - fo lor i ' i t Ccll.s lire Deliiil Links

C n n - Colored Cells arc Disalloucd Kn ln '

Line Item

No.

-.:: ' Z - l

; ; i - . . i v

" i ' ' . -u2- j

( i | l l i v .

•.;, ;::

Description

- \cc r i ied compensa ted absences - cu r ren t o o r l i o n

Acc rued con i i n i t cncv l i a b i l i t y

• \ cc iued i n i e r c i i pavab le

.Accounts pavab le • H U D P H A Pronrams - O p c r a t i n n Subs idy

.Accounts pavTible - H U D P H A Pro i ^ rami - Cap i t a l f und

.Accounts pavab le • H U D I ' H A Programs - O ther

A e c o u i i t i p a v - h l e - I I I T > I ' H A P r o e r . i m i

Accoun i s pavab le - P H A Proiects

• • '• 1 'Vccounis pavable - o ther u o v e i n m e n i

i-^ i T e n a n i seeur i iv depos i ts

• 4 r -1 r J 1J

U r - u Z i . ,

• . . i : - f l ; o

i - i :

i 4 . 1 - 0 | i )

; ; i - i ) : o

!-;' 3 ; - :

; , ; c

M o

;.!" . ' - IS-UlU

i - i s - u : i i

-4M-3U

^-i,^-0.:o

.i-lS-U'^U

i ;.s-nfii"j

M s

I j l .

D e l e r r e d revenue - O p e r a i m u Subs idy

Defe r red revenue - C a p i i a l f und

Defer red rev enue • O ther

D e f e r r e d l e v n u i r

C F F P

Cap i ta l P r o i e c i i M o r t u a u e Revenue

C u i i e i i t p o i l i u n o f l o n u - l e i m d e b t - c a p i t a l p r o j e c l i / i n o r i i j H K e r c v c m i r b o n d s

C u r r c n i p o r t i o n o f l o n n - i e r m debt - o p c n i t i n u b o r r o w i n g

Other c u r r e n i l i ab i l i t i e s

.Accrued l i ab i l i t i e s - o ther

Inter p r o g r a m - due 10

L o a n hab i l i i v • cu r ren t - No t For Prof i t

L o a n l i ab i l i i v - cu r ren i - Par tnersh ip

L o a n l i ab i l i i v - cu r ren i - Jo in t V e n t u r e

L o a n l i ab i l i l v - cu r ren t • Tax Cred i t

L o a n l i a b i l i t y - cur rent - O ther

Other • C o m m e n i

L o a n l i i i b i l t i v - r i i r m i t

T o t a l C i i r i e i i l L i i i b i l i l i e s

Project Totals

8,423

. -

s s

. 14,059 13.730

876 876

s

.

. 384

s

. 5

$ .

52,137

^ ^ , Central Office Procrain Totals _ „

** Cost Center 6,270 ! $

.

.

. -,

,

. S

.

.

. 18,216

$ 65J0O

. ,

.

.

89,786

Subtotal

14.693

$

. s

. $

14,059 13,730

. 876 876

.

. ,

s

18,800

. 63,300

s s i £

$

,

.

. s s

. 14U23

ElmiinatioD

'

-S65,3CKJ

S [65300)

Total

14,693

£

s s

-s

14 ,039

13 ,730

8 7 6

8 7 6

$

J ta.EOO

-: s -1

• 1

- . 1

76,623

> ^ 1 -0 1 1)

••"^l-ICH

1^1

3^:

;; t ' . j

y ^ ' ^ - o i o

3-^ '^-o:u

3 - ' ; . „ . i i j

; ^ s - i ) - i u

3 - ^ - 0 5 0

, ; > - - U ' J U

,> ' •.,

1

L o n n - t e r i n debt - CF i "P

L o m i - t e r n i - Cap i t a l Proiecis. ' M o n u a w e R e v e n u e

C i i p i l i i l P r u j e e l s / . M o r l c a E f H e v e n u e B o n d s

L o n u - i e r m debt , net o f c u r r e n t - opera i inH b o r r o w i n u s

N o n - c u r r e n t l i ab i l i t i es - o ther

A c c r u e d comp^ 'nsated absences- N o n - c u r r e n i

Loan l i a b i l i t y - N o n - c u r r e n t - No t For Pro f i t

Loan l i ab i l i t v - N o n - c u r r e m • Panne rsh ip

Loan hab ih i v - N o n - c u n e n i - Jo in t V e n t u r e

Loan l i a b i h i v • N o n - c u r r e n t - T a x Cred i t

Loan l i ab i l i t v - N o n - c u r r e n t - O t h e r

O ther - C o m m e n t

L u i i n l i a b i l i t v - N o n - c u i r r i i t

f ASIJ •' 1 l ab ih l i es

ACvr^-ei: f ' c n ; . . o n a n J O P t i b L i a n i n r ,

1 i^11 1 To la l .N 'on-cuMTr i l l i i i b i l i l i e s

s s

21,129

. s X

5 f

.

. _

s

.

. ,

1S,437 „

. s

.

2L129 S

.

. ,

IW37

$ £

$ S

S 5

* S J

$ s

s $ $ i

5

.

36,366 „

.

, _ ,

3 6 . 5 6 6

£ S

S

$ s %

•1

36,560

s • .1 s -£ -1 s $ s s s

s - s 3 6 . 5 6 6

1 ' . A J I I ' U I J I L i : <b i i i i i es s 73J66 1 S 10W23 1$ - 1$ 1 7 8 , 4 8 9 S (65J00)[J 1 1 3 , 1 8 9 1

•^Ob 1

> l 1 1

5 1 : 1

^ , •

Invested in capi ta l assets, net o f re la ie t l debt

Rest r i c ted ^ e l Asseis

Unres t r i c ted Net Asseis

F u l i i l F . q i i i i \ / . \ e i Asse is

s s s s

1,843,445

. 311,131

2,1S4J76

$ $ s s

1,379

3 2 2 , 6 7 2

3 8 0 , 3 7 2

l . l M y i Z ?

s s s s

s s s £

1 ,844 ,824

5 2 2 . 6 7 2

8 9 1 . 3 0 3

3 , 2 5 8 J>99 5

s £

£ S

1 .844 ,824 1

5 2 2 , 6 7 2

891 .50 - -

3 J 5 8 . 9 9 9

1 rjiK" 1 1 o i a l l . i a b i l i i i e s a n d K q i i i ( v / , N r t asseis s 2J27342 1 S U W J S 4 6 1 J - 1 5 W 3 7 v 4 8 8 j S (65J0O)| $ 3 J 7 2 . 1 S K i

l a c o i Q t S l a f e i n a a t I

^ n l . f j

" •u4 i " i

Net tenant l en ta l revenue

Tenan t revenue - o i h e r

" i J ^ u f To ta l Tenant Revenue |

! s s s

188,779 4.287

193,066

s 2 3 , 1 7 2 1

s -1 s 3 3 , 1 7 2 j

s s I

$ s 5

2 1 1 , 9 5 1

4 , 2 8 7

2 1 6 0 3 8 :

$ S

$ - s

2 1 1 . 9 5 1

4 . 2 8 7

2 1 6 , 2 3 8

" u t j i X I - u U i

7IK'0U-U:LI

' t > i ( K I - u ' i l l

7tjLK".M13|

~u(>tX)-040

•'iKikXJ-U'iO

^OoltU-'.IWl

' ' •J i j iU.-Ol l i

Tv t i i h l

l o u i i n u assistance [ lavnients

^ n i i o i n u admin i s i r a t i v e lees earned

• lard 10 bouse fee revenue

FSS C o o r d i n a t o r

A c i u a l i nde iK 'nden i p u b l i c accoun tan i aud i t costs

l o t a l p r e h m i n a r v fees earned

\ l l o ther fees

•Xdmin lee c a l c u l a t i o n desc r i p t i on

I l D P H , \ o p e r a t i n g g r u n i j 429.412 1

s $

2 J 2 3 , 4 5 5

3 1 2 , 1 3 6

.

5

-U -1 s -1

2 / S 4 ^ 5 | $ $ -

S s

2 , 3 2 3 , 4 5 3

3 1 2 , 3 3 6

J .1

s s

.

. •"s - ]

$ $ $

.

. 34I4J»57

'

•

2 . 3 2 3 , 4 5 5

312,35i>

-1 £ -1

3,114,057 1

"^i lt i lO ICap i i a l i t r an t i | s 114.503 1 $ • S - 5 . 114,305 1 £ 114,505 1

" ( ' " I I I

"1.17:0

" O ' l O

" U " - ; L

" ( ' " ^ H

• " ( . " i l l

M a n a u e m e n i Fee

A S J C I M a n a u e m e n i Fee

i o o t . - K e e p i n e Fee

• rom L i n e S e r \ i c e Fee

Other Fees

! ' o ia l Fee Rev enue

. s

.

.

. ,

s • -1 . .

% . 1 - 1

$ $ s s $

" U i W

- 1 100-0111

" 1 KKj-u: ( - i

T l l G v i

• i : u o

" : I l •

Dther uov e rnmen t ur i in ts

l o u s i n i ! .Assistance Pavment

\ d i i i i n i s i r a i i v e Fee

n v r s l n i f i i t i n c o m e - i i n i f H r i r t c d

M o r t u a u e interest i n c o m e

' r o c e e d i f r o m d i s p o s i t i o n o f assets he ld for sale

s - 1 . .

1333

$

s - j .

5,267 3J45

5 ' -1 -1

s $ X s $ 5

$ s s s $ s

.

. 5.267 7,«a

.

.

•

S -1

$ 5 S

-5 .2b7

7 , 0 7 8

£ S

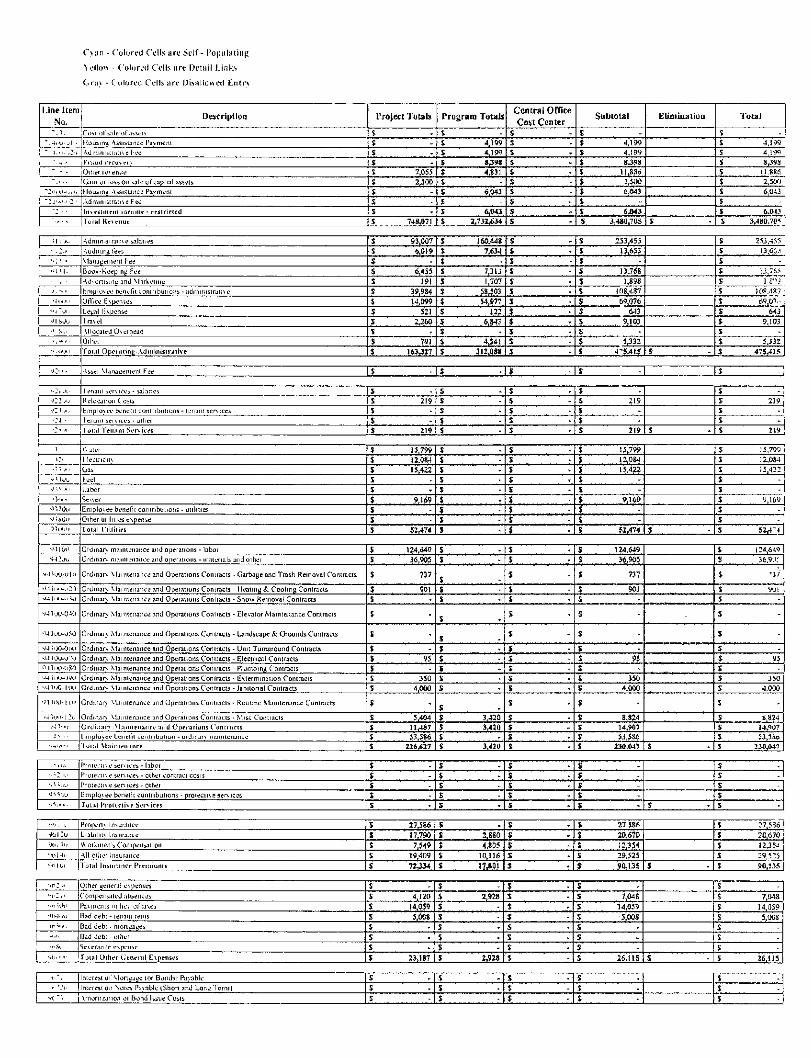

C'>an - Colored C"ells are Self- I'opulalint^

^ ello4* - Colored Cells are Detail Links

Cr; i \ - Colored Ci'll.s lire DisHllo«ed t n l n

Line Item .No.

~. •-, ~ . 4 , - u - j j .

" 1 , • . - , : • !

' ^ . . . .•

• ' : o , , i - , , , . ,

- : J , „ , . , . : ,

-: .-

Description

Coat ol sale of assets

Housinu Assistance Pavment

Admimsiraiive Fee

1 Fi:iu(l reruverv

Other revenue

(jam or iosj on sale of capital asseis

l louj inu Assistance Pavment

Administraiive Fee

InvI ' t imri i i incdme - rettr ir ied

Fulal Revenue

Project Totals

£ E

$ 7,055

£ 2.300

£

S

J 748,071

Program Totals

S 4,199

£ 4,19*>

S 8^98

$ 4.831

£ 6,043

S

S 6,043

S 2.732,634

Central Office Cost Center

Subtotal

$ 4,199

£ 4,199

S 8J98

S 11,836

S 2,500 S 6.043

S

£ 64t43

S 3,480,705

E U m l n a t i O D

£

T o t a l

S 4,199

S 4,190

S 8,393

S )1.8E6

$ 2.500

$ 6,043

S 6,043

S 3,480,70';

H ;'jv-

• . : > "

• • [ • • •

- M i l .

Admmisiraiive i,Tlaries

•\udilinLi lees

Manaecmeni 1 ee

BooF>-Keepinv; t'ee

Adveniiinu .ind M.irU'iiiiLj

1 !.• ' ." 1 h mplovee benefit coniributions - adniimstrative

" I ' ' • j i -

OlTice Espensei

Leital i:>.pense

-Jl^ ju |1 ravel

" s . .

' , 4 ^ . . .

• ' L'JV".'

.;:,.. • • 2 1 L H .

' J 2 2 j i j

1 . : . . .

• 2 i -

\ ' T •• 1

1

! ? •

• • . - . J , .

•• t t ^ ' L

' j ; s « ,

• ' l . H ,

•r.70vi

•; •sun

• > ! i - n i

•1.11 Cni

- ; J : ^

' J 4 ? I A I - U | "

• M ; ( " ' - > ' 2 0

s .41 .« i -u lv l

V - l l i X I - 0 4 0

•M3iK.J-iJ.-tO

V-l " . IW-OKI

•;-iioo-'j' 'o

o-r>i>il-iiSO

•^4 i i . l M I ' A j

•).noO-IO|i

• n i iHM HI

• • . t>^M. i : L .

IH ! • • )

: v . .

- . ^ . „ . .

.\llocated Overhead

Oihei

Toml Operii i inii-.Adminisliativf

S 93,007

$ 6,019

$ £ 6,455

S 191

X 39,984

£ 14,099

£ S21

S 2,260 5

£ 791

S - 163J?7

£ 160,448

£ 7,634

$ £ 7,313

S 1,707

$ 68,503

£ 54,977

£ i 22

S 6,843

$ £ 4,541

£ 3U4ISS

£ - t $ 253,455

£ 13,653

£ 13.768

£ 1,898

£ 108,487

£ 69,076

$ 643

£ 9.103

£

$ 3,332

$ 4"'5.4tS S

$ 253.4'.5

£ 13.6;..*

s u,:is $ I ?"?

£ 5 0fi..l87

J 69.0^.-

£ 643

£ 9.103

$ £ 5.332

£ 41SA1S

Asset Manacement Fee | £ . | £ . | $ - | £ - | | $ - ]

fenanl jerv iccj - salaries

Relocjtioii Costs

Eniplovee benet'it contribiiltons - lenanl services

1 enanl scrv ices - other

lu la l I f i i i in l Sei-vires

S 219 J

£ S 219

E

s

£

S

$ s

$

£ 219

s

S 219 S

£ 219

£ 2!9

U aiei

[ leciiiciiv

Gas

Fuel

Labor

Sewer

Emplovee benel'it contributions - utiliiies

Oiher utilities expense

lotal I'tiliiies

$ 15,799

$ 12.084

£ 15,422

$ S 9,169

s 5 52,474

£ 15,799

£ 12,084

£ 13,422

£ J 9,169

S 52/*74 £

S 15,799

S 12.084

£ 15,4: :

s £ 9,169 i

^ -| £ - , S 52,4-1 1

Ordinar. inainienance and operations - labor

Ordinar- niamienance and operations - materials and other

Ordmar% Maintenance and Operations Contracis - Garbage and Trash Removal Contracts