spline garch as a measure of unconditional volatility and its global macroeconomic causes

DESCRIPTION

Spline Garch as a Measure of Unconditional Volatility and its Global Macroeconomic Causes. Robert Engle and Jose Gonzalo Rangel NYU and UCSD. HISTORY OF THE US EQUITY MARKET VOLATILITY: S&P500. PLOT PRICES AND RETURNS HOW MUCH DO RETURNS FLUCTUATE?. MEAN REVERSION QUOTES. - PowerPoint PPT PresentationTRANSCRIPT

Spline Garch as a Measure of Unconditional Volatility and its Global Macroeconomic Causes

Robert Engle and Jose Gonzalo RangelNYU and UCSD

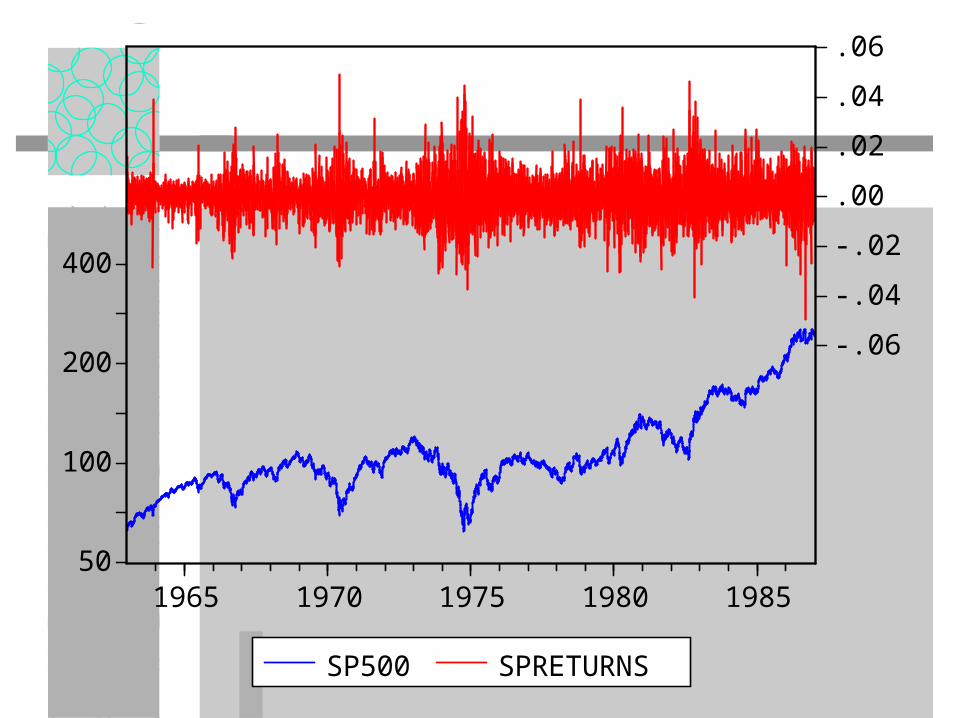

HISTORY OF THE US EQUITY MARKET VOLATILITY: S&P500

PLOT PRICES AND RETURNS

HOW MUCH DO RETURNS FLUCTUATE?

50

100

200

400

800

1600

-.3

-.2

-.1

.0

.1

65 70 75 80 85 90 95 00

SP500 SPRETURNS

50

100

200

400

-.06

-.04

-.02

.00

.02

.04

.06

1965 1970 1975 1980 1985

SP500 SPRETURNS

200

400

800

1600-.08

-.04

.00

.04

.08

1988 1990 1992 1994 1996 1998 2000

SP500 SPRETURNS

800

1000

1200

1400

1600

-.08

-.04

.00

.04

.08

1998 1999 2000 2001 2002 2003

SP500 SPRETURNS

MEAN REVERSION QUOTES

“Volatility is Mean Reverting”– no controversy

“The long run level of volatility is constant”– very controversial

“Volatility is systematically higher now than it has been in years”– Very controversial. Cannot be answered by

simple GARCH

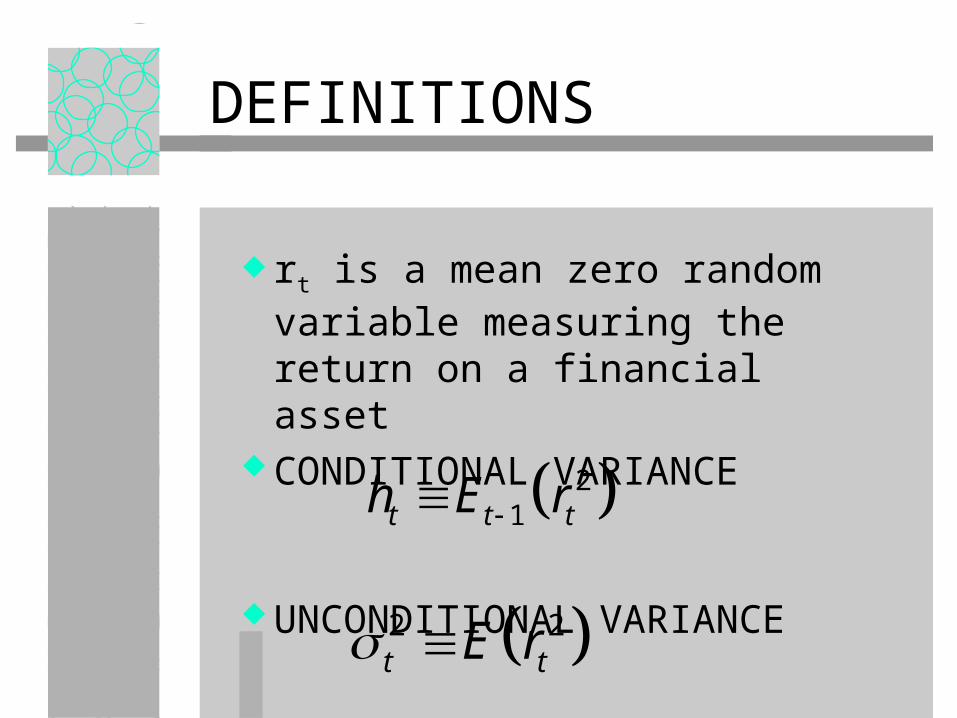

DEFINITIONS

rt is a mean zero random variable measuring the return on a financial asset

CONDITIONAL VARIANCE

UNCONDITIONAL VARIANCE

21t t th E r

2 2t tE r

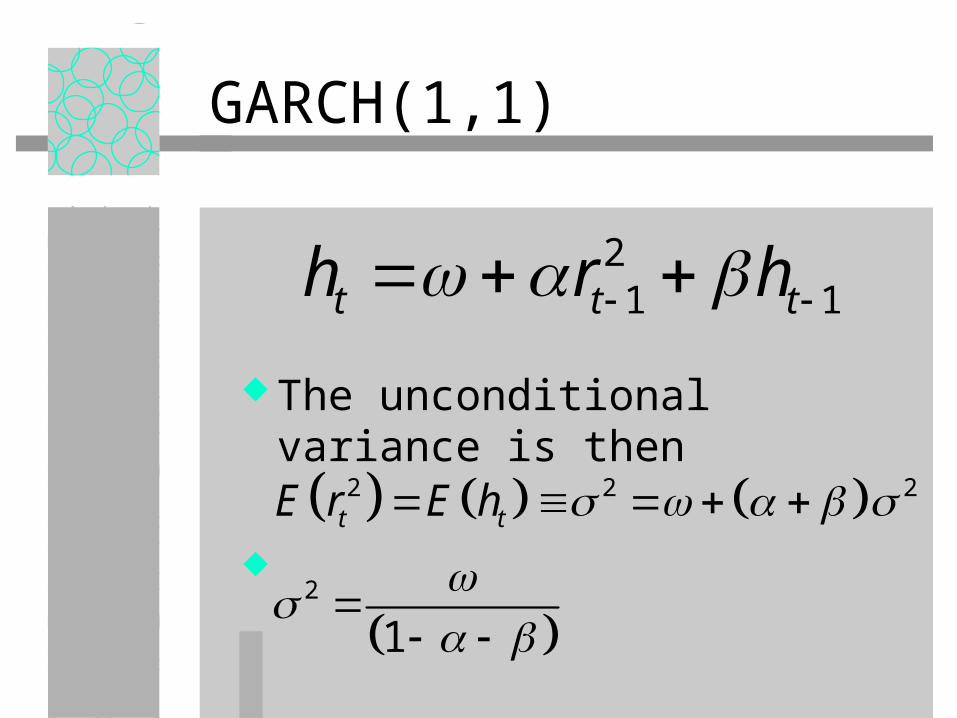

GARCH(1,1)

The unconditional variance is then

21 1t t th r h

2 2 2

2

1

t tE r E h

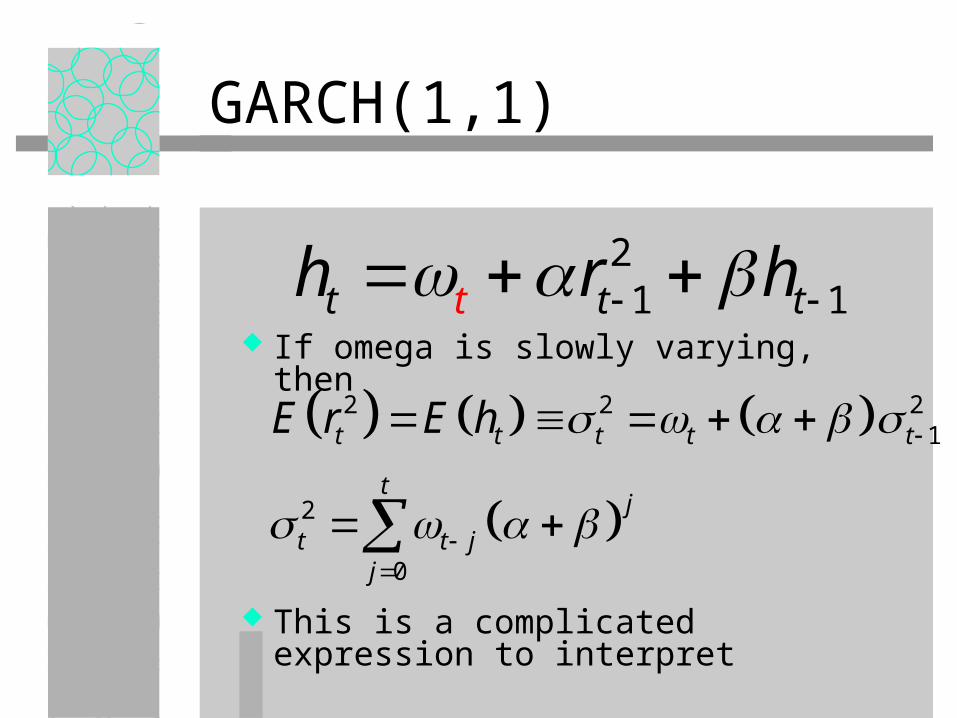

GARCH(1,1)

If omega is slowly varying, then

This is a complicated expression to interpret

21 1t t tth r h

2 2 21

2

0

t t t t t

tj

t t jj

E r E h

SPLINE GARCH

Instead, use a multiplicative form

Tau is a function of time and exogenous variables

1, where | (0,1)t t t t t tr g N

21

11

(1 ) tt t

t

rg g

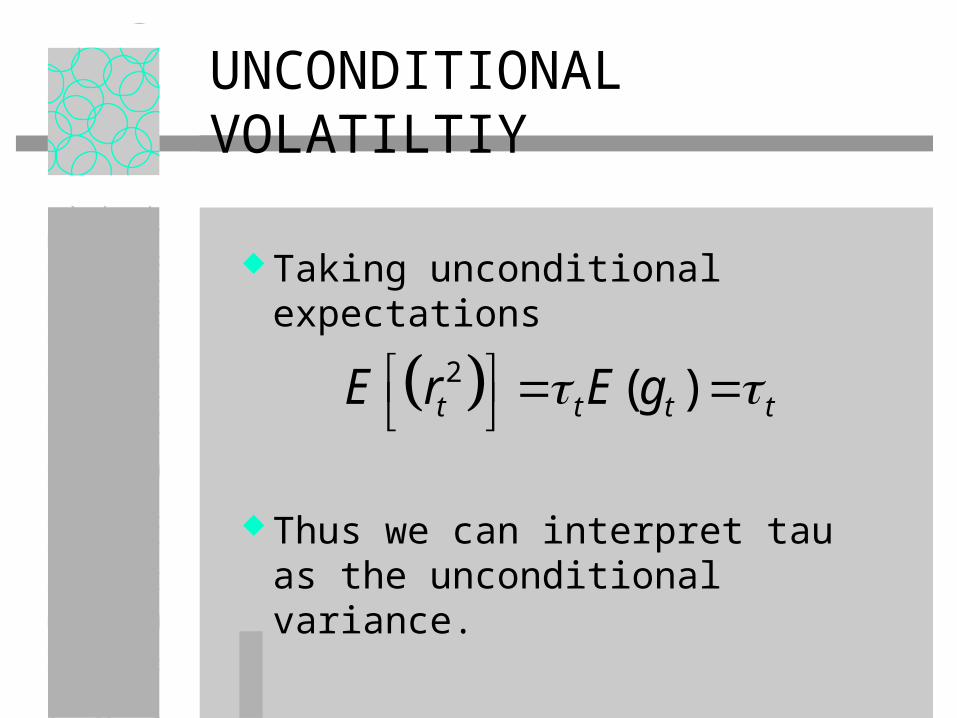

UNCONDITIONAL VOLATILTIY

Taking unconditional expectations

Thus we can interpret tau as the unconditional variance.

2 ( )t t t tE r E g

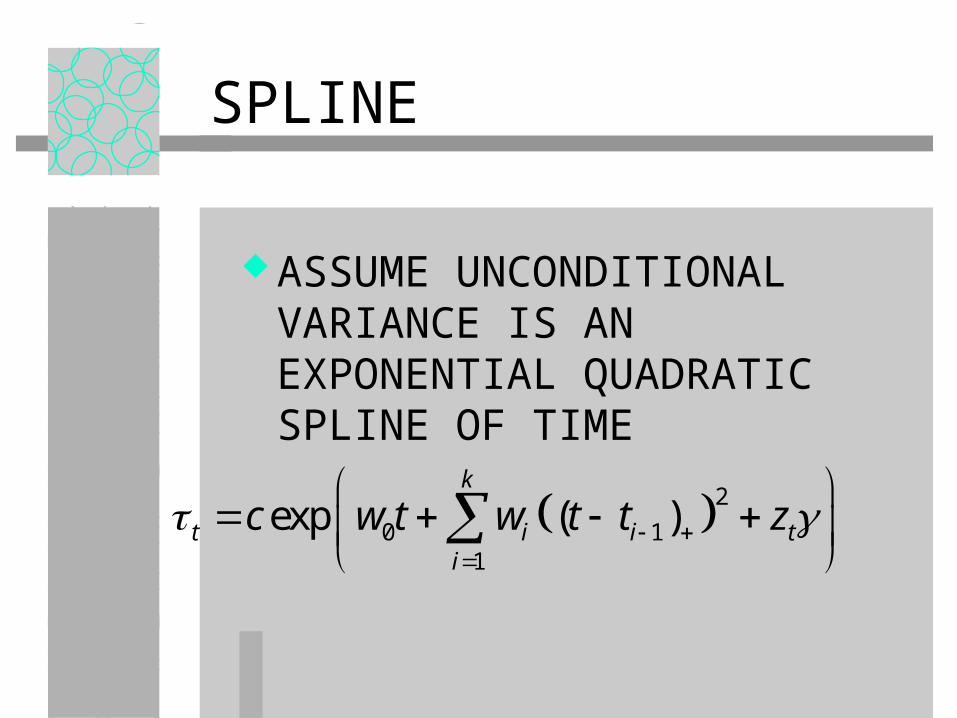

SPLINE

ASSUME UNCONDITIONAL VARIANCE IS AN EXPONENTIAL QUADRATIC SPLINE OF TIME

2

0 11

exp ( )k

t i i ti

c w t w t t z

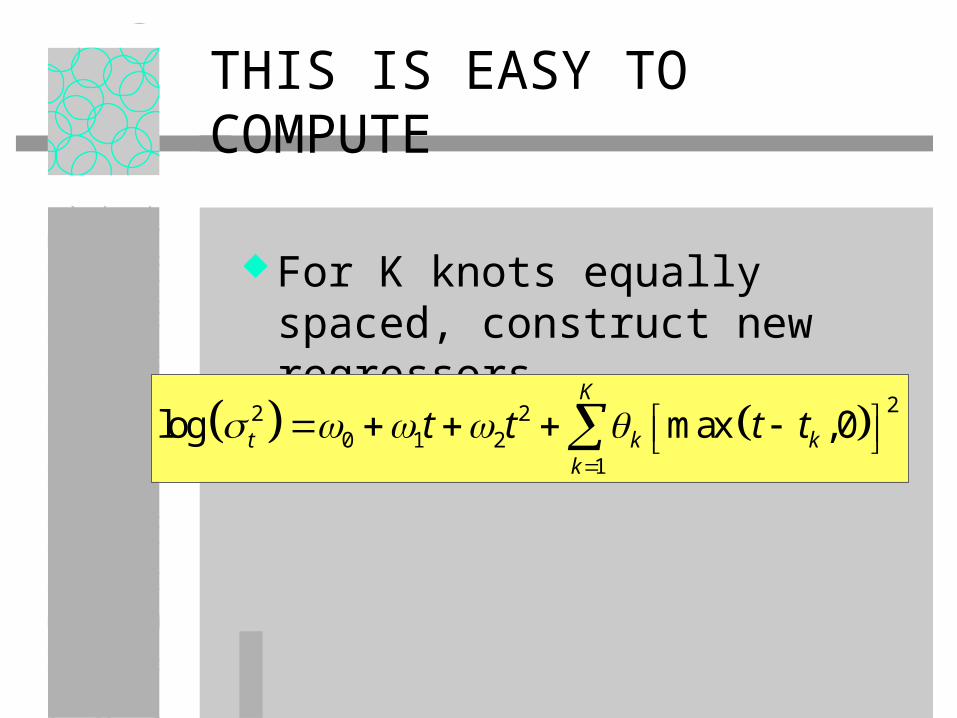

THIS IS EASY TO COMPUTE

For K knots equally spaced, construct new regressors

22 20 1 2

1

log max ,0K

t k kk

t t t t

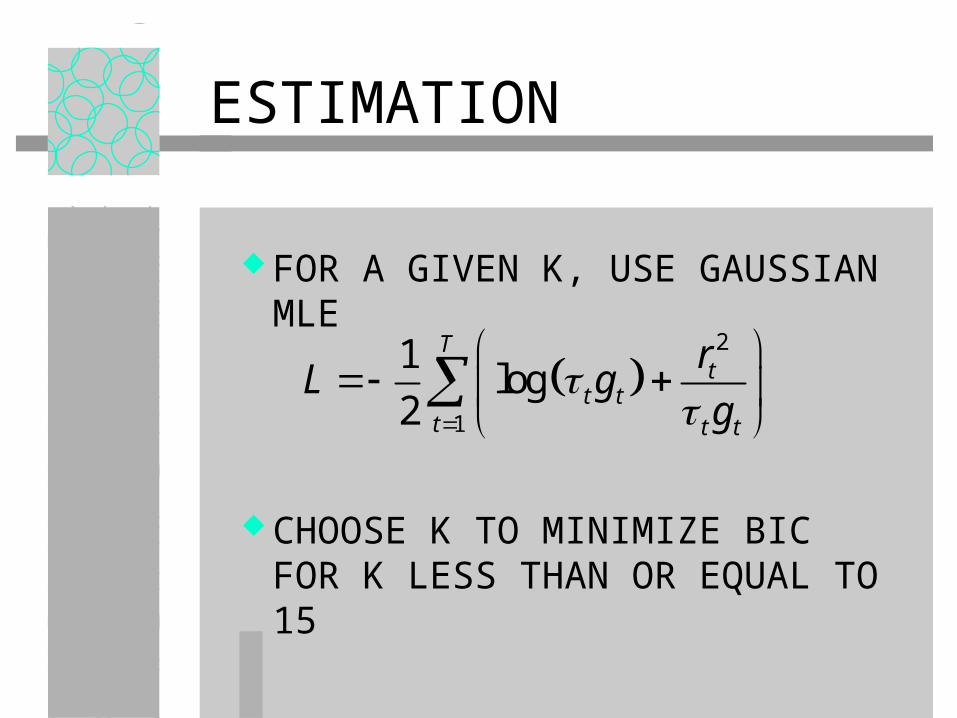

ESTIMATION

FOR A GIVEN K, USE GAUSSIAN MLE

CHOOSE K TO MINIMIZE BIC FOR K LESS THAN OR EQUAL TO 15

2

1

1log

2

Tt

t tt t t

rL g

g

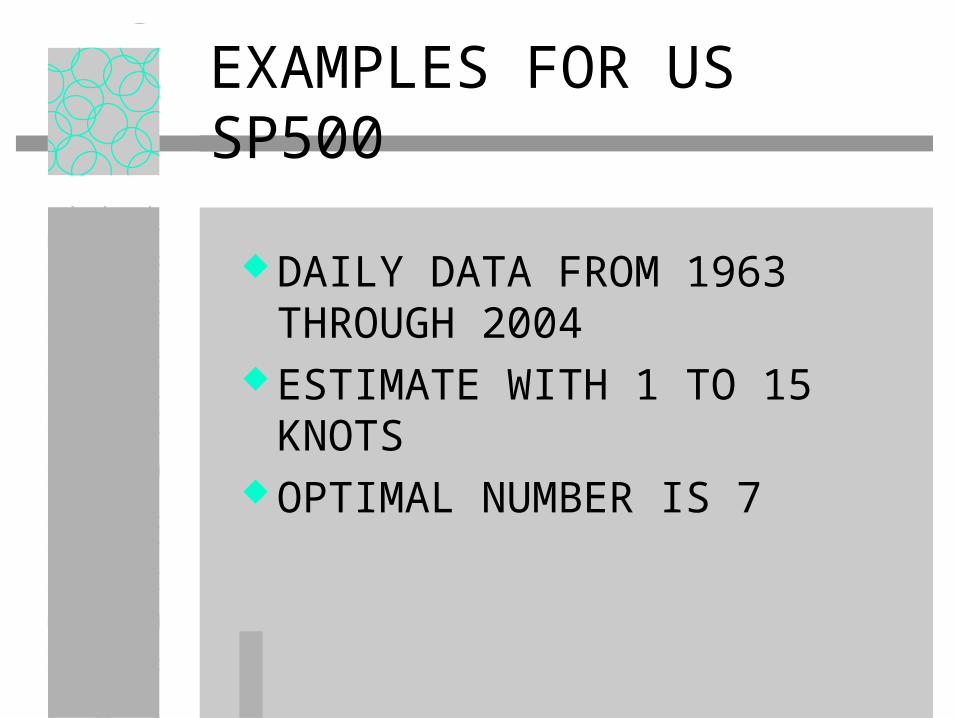

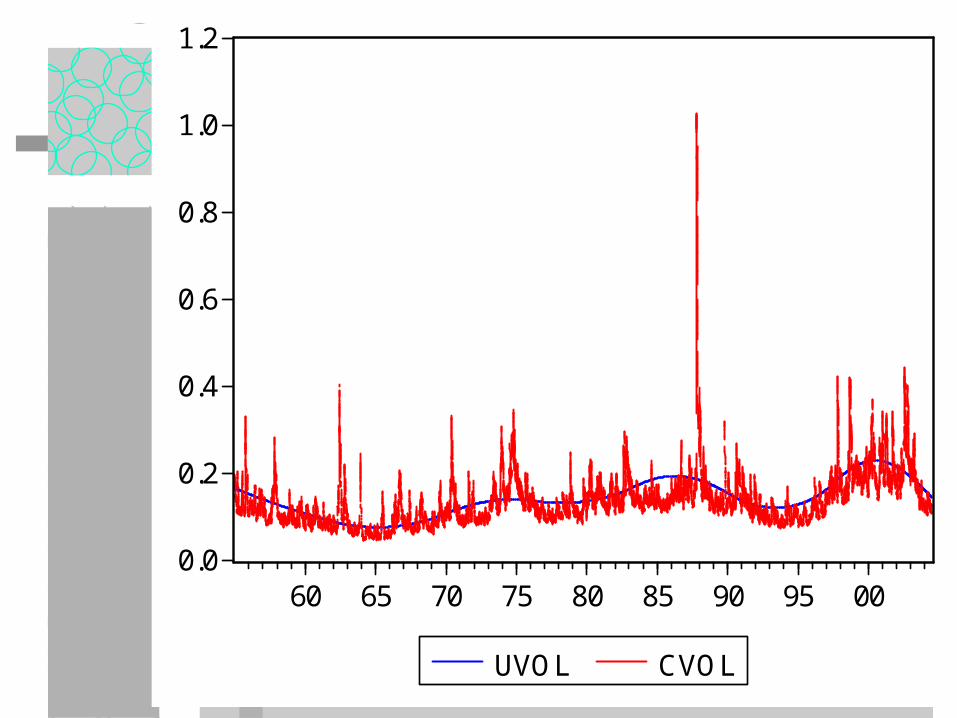

EXAMPLES FOR US SP500

DAILY DATA FROM 1963 THROUGH 2004

ESTIMATE WITH 1 TO 15 KNOTS OPTIMAL NUMBER IS 7

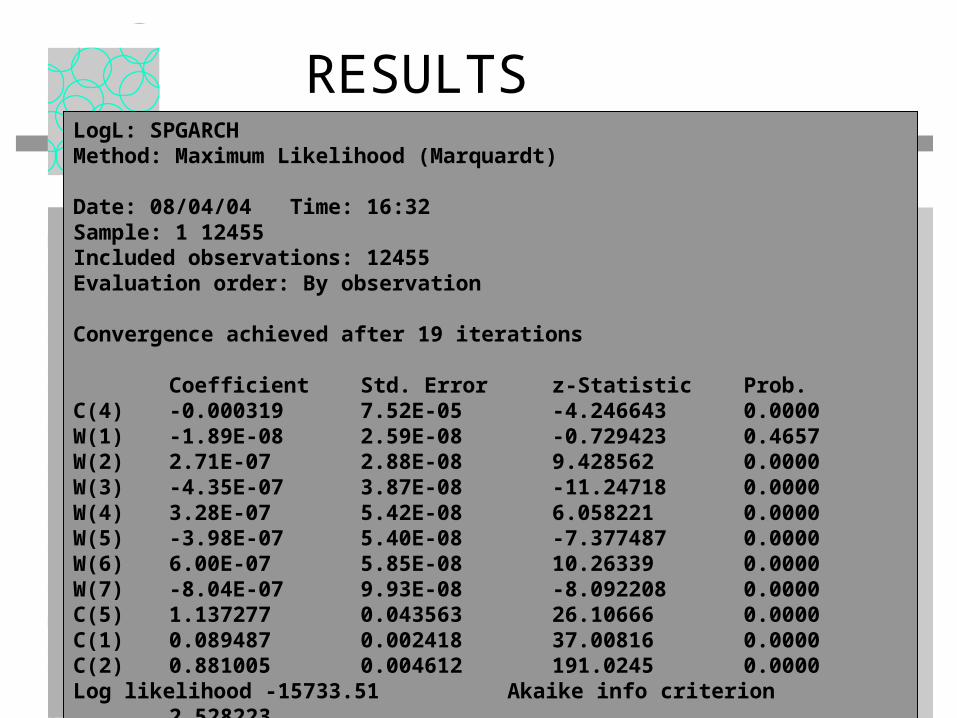

RESULTSLogL: SPGARCHMethod: Maximum Likelihood (Marquardt)

Date: 08/04/04 Time: 16:32Sample: 1 12455Included observations: 12455Evaluation order: By observationConvergence achieved after 19 iterations

Coefficient Std. Errorz-Statistic Prob. C(4) -0.000319 7.52E-05 -4.246643 0.0000W(1) -1.89E-08 2.59E-08 -0.729423 0.4657W(2) 2.71E-07 2.88E-08 9.428562 0.0000W(3) -4.35E-07 3.87E-08 -11.24718 0.0000W(4) 3.28E-07 5.42E-08 6.058221 0.0000W(5) -3.98E-07 5.40E-08 -7.377487 0.0000W(6) 6.00E-07 5.85E-08 10.26339 0.0000W(7) -8.04E-07 9.93E-08 -8.092208 0.0000C(5) 1.137277 0.043563 26.10666 0.0000C(1) 0.089487 0.002418 37.00816 0.0000C(2) 0.881005 0.004612 191.0245 0.0000Log likelihood -15733.51 Akaike info criterion 2.528223Avg. log likelihood -1.263228 Schwarz criterion 2.534785Number of Coefs. 11 Hannan-Quinn criter. 2.530420

0.0

0.2

0.4

0.6

0.8

1.0

1.2

60 65 70 75 80 85 90 95 00

UVOL CVOL

.0

.1

.2

.3

.4

.5

.6

.7

.8

60 65 70 75 80 85 90 95 00

CVOL UVOL

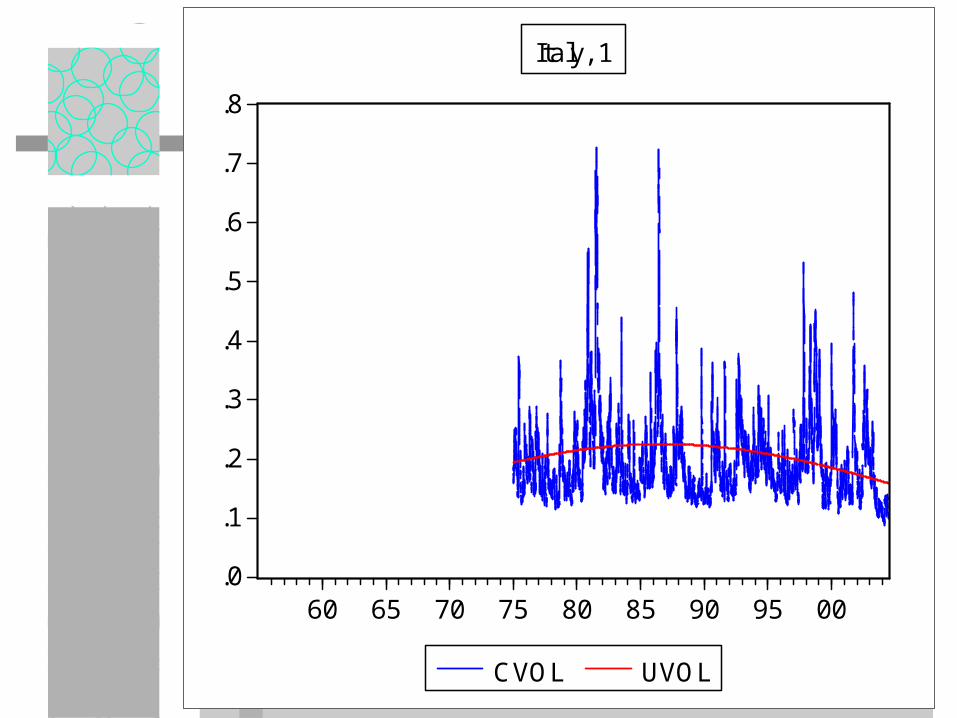

Italy, 1

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

60 65 70 75 80 85 90 95 00

CVOL UVOL

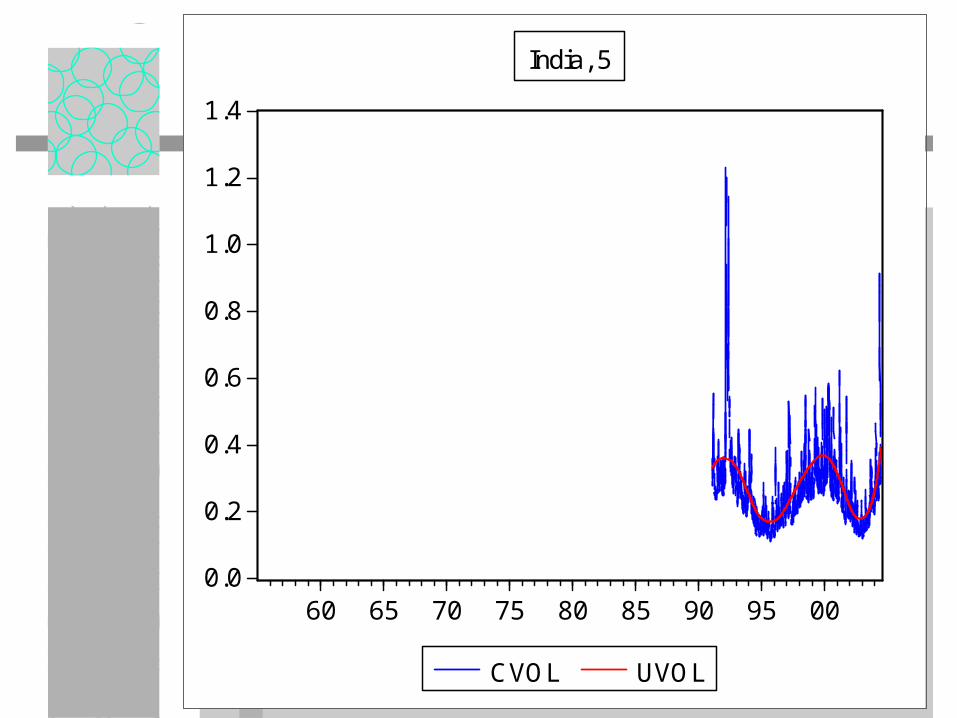

India, 5

0.0

0.2

0.4

0.6

0.8

1.0

1.2

60 65 70 75 80 85 90 95 00

CVOL UVOL

Japan, 4

0.0

0.5

1.0

1.5

2.0

2.5

3.0

60 65 70 75 80 85 90 95 00

CVOL UVOL

Brazil, 6

.0

.1

.2

.3

.4

.5

.6

.7

.8

.9

60 65 70 75 80 85 90 95 00

CVOL UVOL

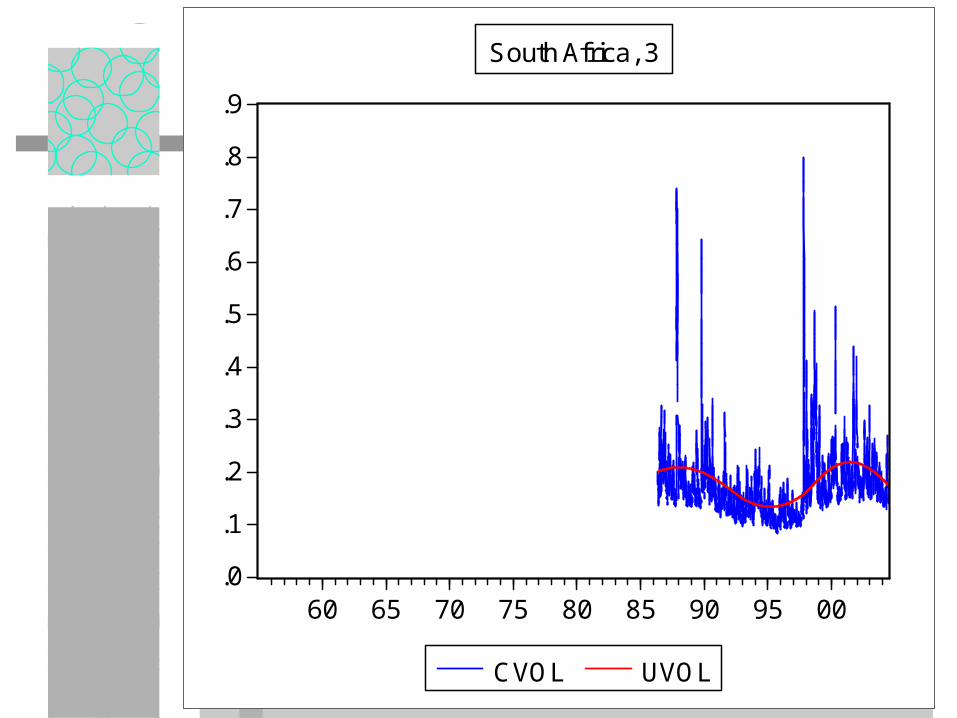

South Africa, 3

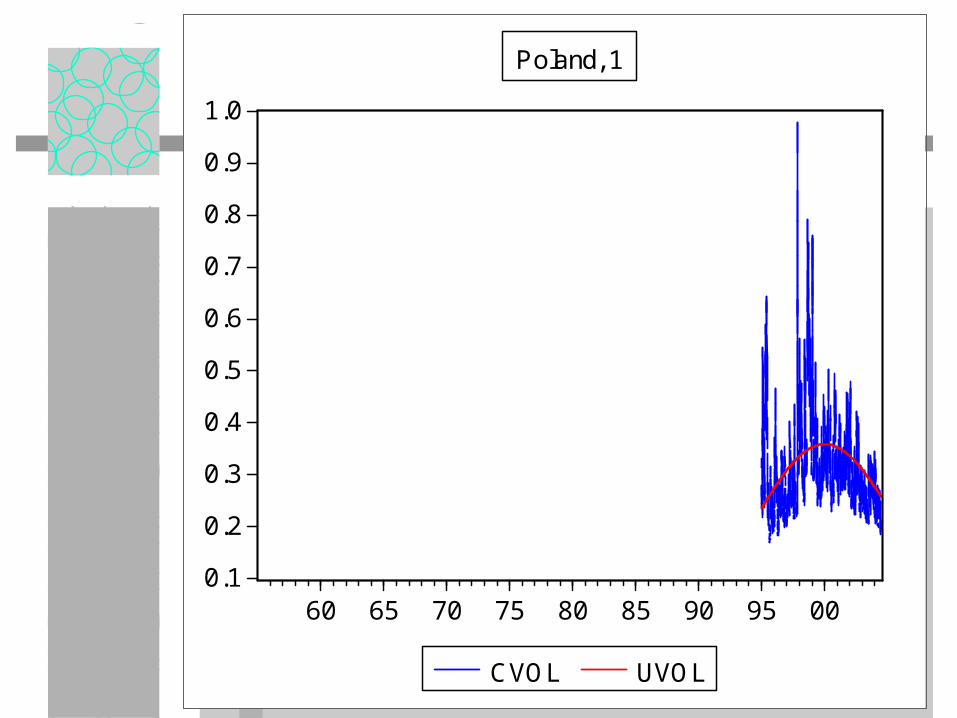

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

60 65 70 75 80 85 90 95 00

CVOL UVOL

Poland, 1

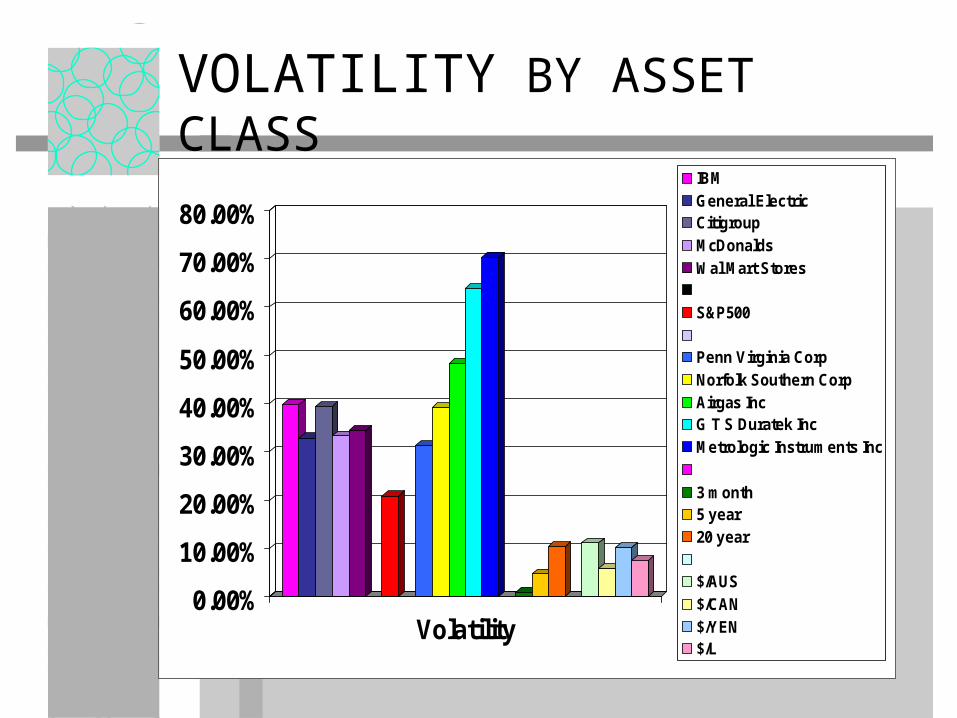

PATTERNS OF VOLATILITY

ASSET CLASSES– EQUITIES– EQUITY INDICES– CURRENCIES– FUTURES– INTEREST RATES– BONDS

VOLATILITY BY ASSET CLASS

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

Volatility

IBMGeneral ElectricCitigroupMcDonaldsWal Mart Stores

S&P500

Penn Virginia CorpNorfolk Southern CorpAirgas IncG T S Duratek IncMetrologic Instruments Inc

3 month5 year20 year

$/AUS$/CAN$/YEN$/L

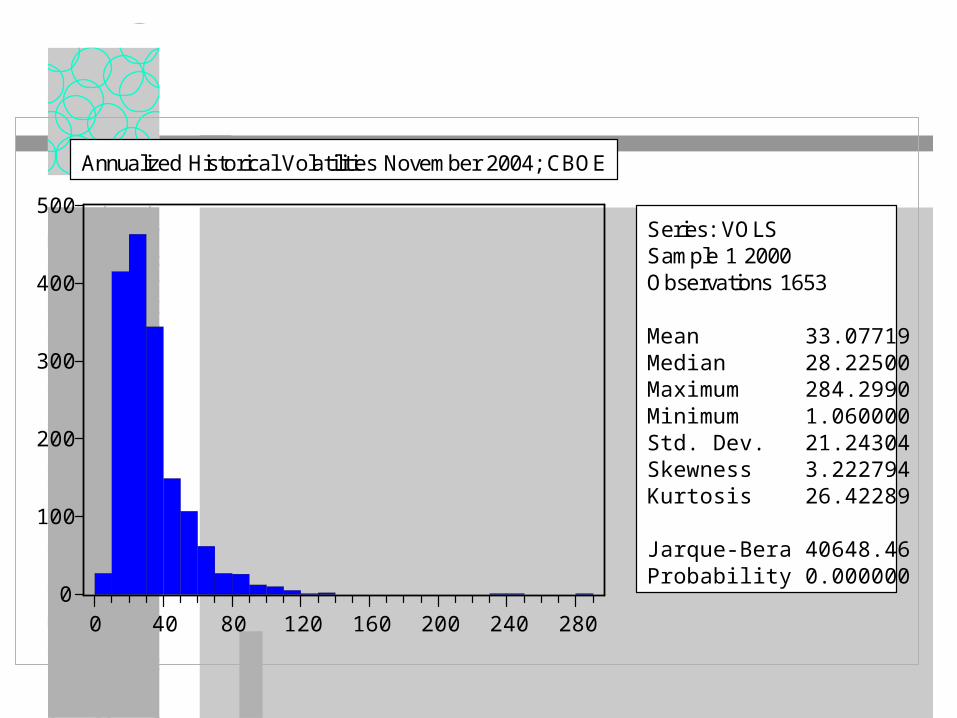

0

100

200

300

400

500

0 40 80 120 160 200 240 280

Series: VOLSSample 1 2000Observations 1653

Mean 33.07719Median 28.22500Maximum 284.2990Minimum 1.060000Std. Dev. 21.24304Skewness 3.222794Kurtosis 26.42289

Jarque-Bera 40648.46Probability 0.000000

Annualized Historical Volatilities November 2004; CBOE

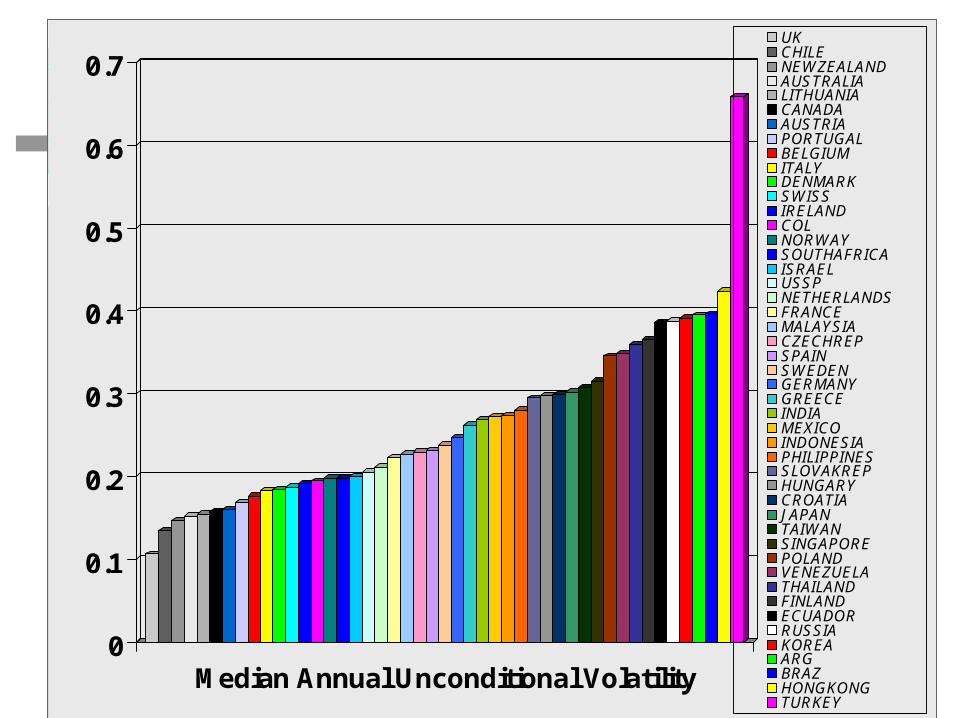

PATTERNS OF EQUITY VOLATILITY

COUNTRIES– DEVELOPED MARKETS– EUROPE– TRANSITION ECONOMIES– LATIN AMERICA– ASIA– EMERGING MARKETS

Calculate Median Annualized Unconditional Volatility 1997-2003 using daily data

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Median Annual Unconditional Volatility

UKCHILENEWZEALANDAUSTRALIALITHUANIACANADAAUSTRIAPORTUGALBELGIUMITALYDENMARKSWISSIRELANDCOLNORWAYSOUTHAFRICAISRAELUSSPNETHERLANDSFRANCEMALAYSIACZECHREPSPAINSWEDENGERMANYGREECEINDIAMEXICOINDONESIAPHILIPPINESSLOVAKREPHUNGARYCROATIAJAPANTAIWANSINGAPOREPOLANDVENEZUELATHAILANDFINLANDECUADORRUSSIAKOREAARGBRAZHONGKONGTURKEY

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Median Annual Unconditional EmergingMarket Volatility

UKCHILENEWZEALANDAUSTRALIALITHUANIACANADAAUSTRIAPORTUGALBELGIUMITALYDENMARKSWISSIRELANDCOLNORWAYSOUTHAFRICAISRAELUSSPNETHERLANDSFRANCEMALAYSIACZECHREPSPAINSWEDENGERMANYGREECEINDIAMEXICOINDONESIAPHILIPPINESSLOVAKREPHUNGARYCROATIAJAPANTAIWANSINGAPOREPOLANDVENEZUELATHAILANDFINLANDECUADORRUSSIAKOREAARGBRAZHONGKONGTURKEY

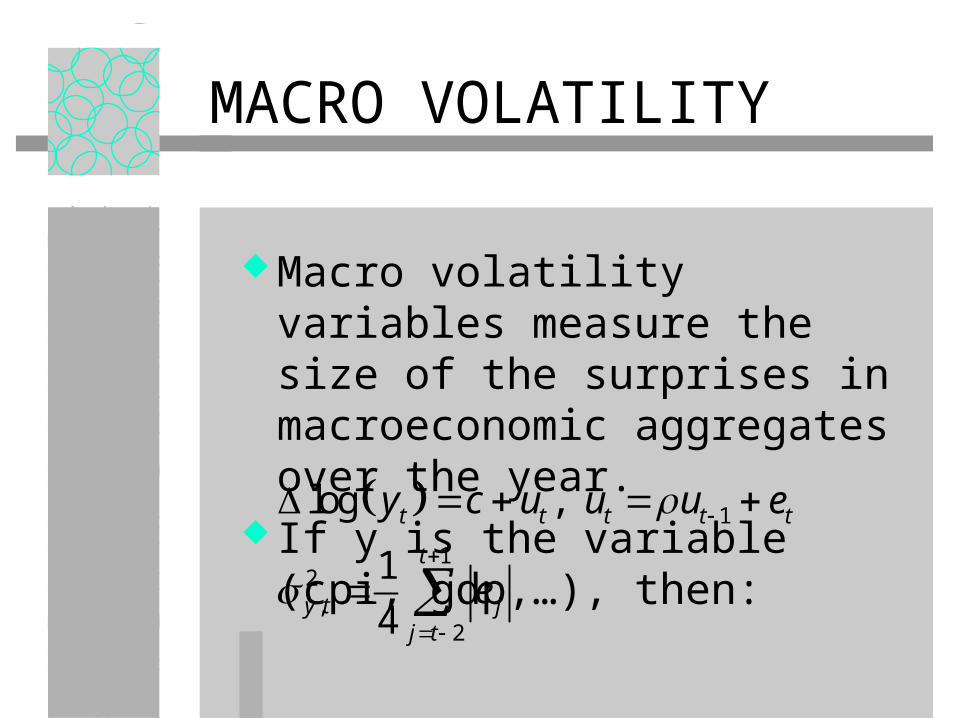

MACRO VOLATILITY

Macro volatility variables measure the size of the surprises in macroeconomic aggregates over the year.

If y is the variable (cpi, gdp,…), then:

1

12

,2

log ,

1

4

t t t t t

t

y t jj t

y c u u u e

e

0

0.01

0.02

0.03

0.04

0.05

0.06

Median Annual Volatility of GDP

UKCHILENEWZEALANDAUSTRALIALITHUANIACANADAAUSTRIAPORTUGALBELGIUMITALYDENMARKSWISSIRELANDCOLNORWAYSOUTHAFRICAISRAELUSSPNETHERLANDSFRANCEMALAYSIACZECHREPSPAINSWEDENGERMANYGREECEINDIAMEXICOINDONESIAPHILIPPINESSLOVAKREPHUNGARYCROATIAJAPANTAIWANSINGAPOREPOLANDVENEZUELATHAILANDFINLANDECUADORRUSSIAKOREAARGBRAZHONGKONGTURKEY

0

0.05

0.1

0.15

0.2

0.25

Median Annual Volatility of CPI

UKCHILENEWZEALANDAUSTRALIALITHUANIACANADAAUSTRIAPORTUGALBELGIUMITALYDENMARKSWISSIRELANDCOLNORWAYSOUTHAFRICAISRAELUSSPNETHERLANDSFRANCEMALAYSIACZECHREPSPAINSWEDENGERMANYGREECEINDIAMEXICOINDONESIAPHILIPPINESSLOVAKREPHUNGARYCROATIAJAPANTAIWANSINGAPOREPOLANDVENEZUELATHAILANDFINLANDECUADORRUSSIAKOREAARGBRAZHONGKONGTURKEY

0

0.05

0.1

0.15

0.2

0.25

0 0.2 0.4 0.6

VOLATILITY

MA

CR

O V

OL

GDP VOL

CPI VOL

EXPLANATORY VARIABLES

Name Descriptionemerging Indicator of Market Development (1=Emerging, 0=Developed)Transition Indicator of Transition Economies (Central European and Baltic Countries)log(mc) log Market Capitalization ($US)

log(gdp_dll) Log Nominal GDP in Current $USnlc Number of Listed Companies in the Exchange

grgdp GDP Growth Rategcpi Inflation Growth Rate

vol_irate Volatility of Short Term Interest Rate*

vol_forex Volatility of Exchange Rates*vol_grgdp Volatility of GDP*vol_gcpi Volatility of Inflation*

*Volatilities are obtained from the residuals of AR(1) models

Explanatory Variables

Table (2)

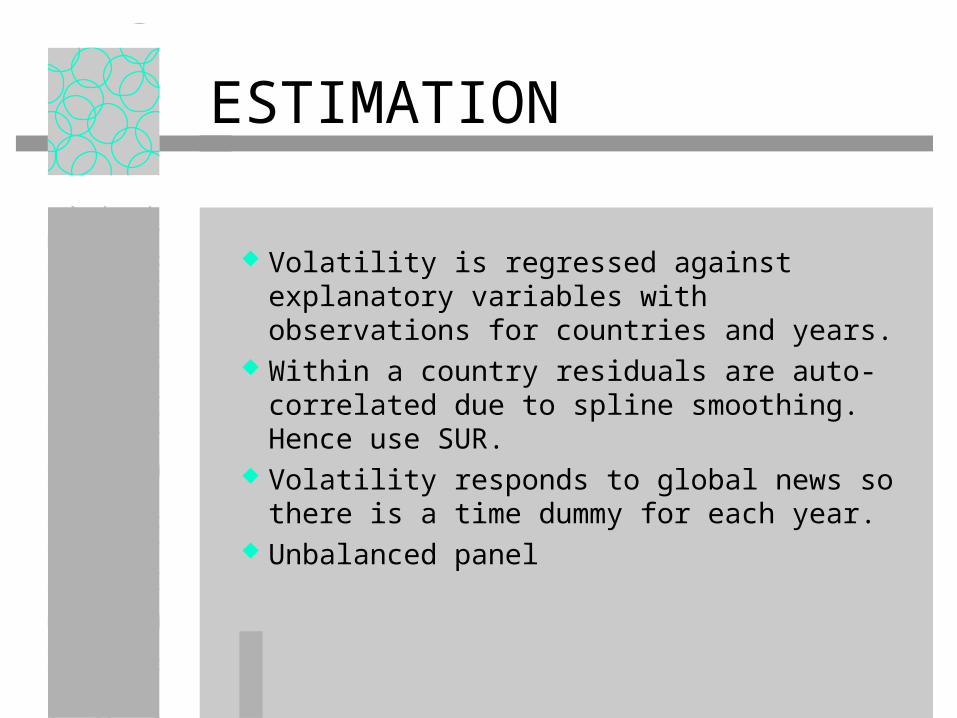

ESTIMATION

Volatility is regressed against explanatory variables with observations for countries and years.

Within a country residuals are auto-correlated due to spline smoothing. Hence use SUR.

Volatility responds to global news so there is a time dummy for each year.

Unbalanced panel

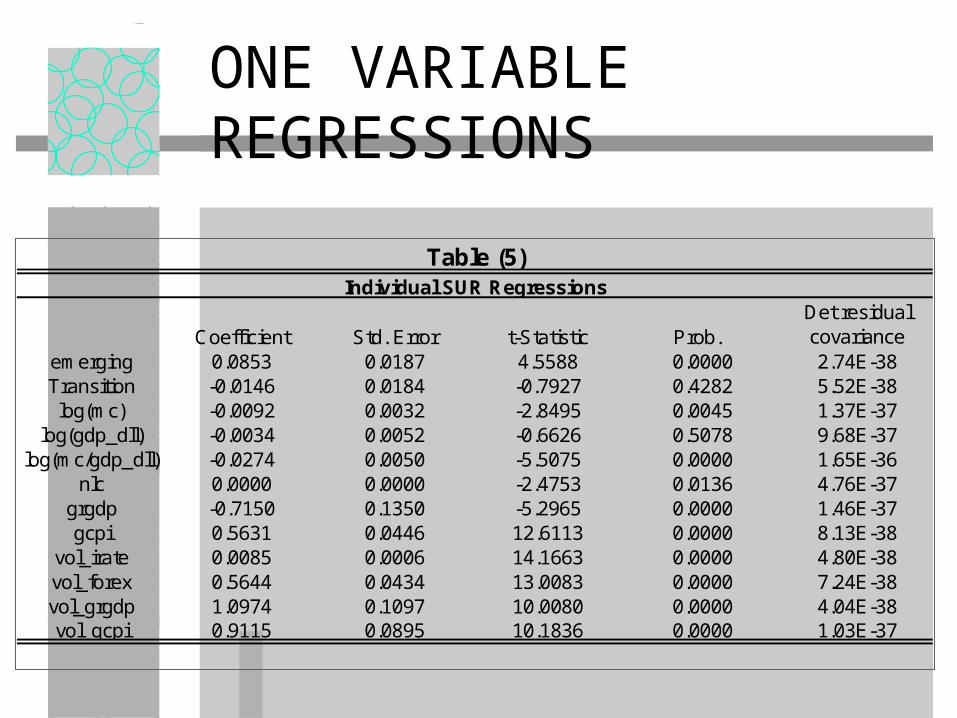

ONE VARIABLE REGRESSIONS

Coefficient Std. Error t-Statistic Prob. Det residual covariance

emerging 0.0853 0.0187 4.5588 0.0000 2.74E-38Transition -0.0146 0.0184 -0.7927 0.4282 5.52E-38log(mc) -0.0092 0.0032 -2.8495 0.0045 1.37E-37

log(gdp_dll) -0.0034 0.0052 -0.6626 0.5078 9.68E-37log(mc/gdp_dll) -0.0274 0.0050 -5.5075 0.0000 1.65E-36

nlc 0.0000 0.0000 -2.4753 0.0136 4.76E-37grgdp -0.7150 0.1350 -5.2965 0.0000 1.46E-37gcpi 0.5631 0.0446 12.6113 0.0000 8.13E-38

vol_irate 0.0085 0.0006 14.1663 0.0000 4.80E-38vol_forex 0.5644 0.0434 13.0083 0.0000 7.24E-38vol_grgdp 1.0974 0.1097 10.0080 0.0000 4.04E-38vol_gcpi 0.9115 0.0895 10.1836 0.0000 1.03E-37

Individual SUR Regressions

Table (5)

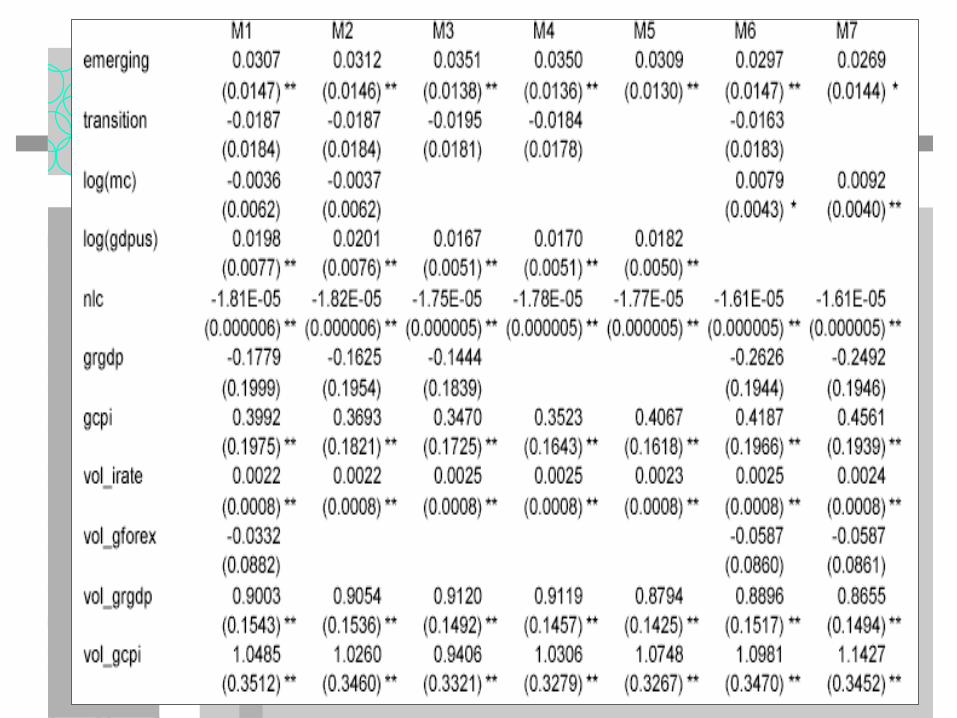

MULTIPLE REGRESSIONS

M1 M2 M3 M4 M5 M6 M7emerging 0.0307 0.0312 0.0351 0.0350 0.0309 0.0297 0.0269

(0.0147) ** (0.0146) (0.0138) (0.0136) (0.0130) (0.0147) ** (0.0144) *transition -0.0187 -0.0187 -0.0195 -0.0184 -0.0163

(0.0184) (0.0184) (0.0181) (0.0178) (0.0183)log(mc) -0.0036 -0.0037 0.0079 0.0092

(0.0062) (0.0062) (0.0043) * (0.0040)log(gdpus) 0.0198 0.0201 0.0167 0.0170 0.0182

(0.0077) ** (0.0076) (0.0051) (0.0051) (0.0050)nlc -1.81E-05 -1.82E-05 -1.75E-05 -1.78E-05 -1.77E-05 -1.61E-05 -1.61E-05

(0.000006) ** (0.000006) (0.000005) (0.000005) (0.000005) (0.000005) ** (0.000005)grgdp -0.1779 -0.1625 -0.1444 -0.2626 -0.2492

(0.1999) (0.1954) (0.1839) (0.1944) (0.1946)gcpi 0.3992 0.3693 0.3470 0.3523 0.4067 0.4187 0.4561

(0.1975) ** (0.1821) (0.1725) (0.1643) (0.1618) (0.1966) ** (0.1939)vol_irate 0.0022 0.0022 0.0025 0.0025 0.0023 0.0025 0.0024

(0.0008) ** (0.0008) (0.0008) (0.0008) (0.0008) (0.0008) ** (0.0008)vol_gforex -0.0332 -0.0587 -0.0587

(0.0882) (0.0860) (0.0861)vol_grgdp 0.9003 0.9054 0.9120 0.9119 0.8794 0.8896 0.8655

(0.1543) ** (0.1536) (0.1492) (0.1457) (0.1425) (0.1517) ** (0.1494)vol_gcpi 1.0485 1.0260 0.9406 1.0306 1.0748 1.0981 1.1427

(0.3512) ** (0.3460) (0.3321) (0.3279) (0.3267) (0.3470) ** (0.3452)d1990 0.1358 0.1349 0.1109 0.1079 0.1018 0.1148 0.1002

(0.0522) (0.0522) (0.0323) (0.0315) (0.0314) (0.0510) ** (0.0487)d1991 0.1442 0.1429 0.1202 0.1178 0.1112 0.1217 0.1066

(0.0523) (0.0522) (0.0317) (0.0311) (0.0308) (0.0512) ** (0.0487)d1992 0.1278 0.1262 0.1041 0.1014 0.0944 0.1074 0.0921

(0.0517) (0.0516) (0.0316) (0.0310) (0.0306) (0.0508) ** (0.0481) *d1993 0.1357 0.1344 0.1112 0.1082 0.1012 0.1107 0.0949

(0.0544) (0.0543) (0.0331) (0.0323) (0.0319) (0.0530) ** (0.0502) *d1994 0.1159 0.1146 0.0922 0.0889 0.0816 0.0922 0.0761

(0.0544) (0.0543) (0.0329) (0.0322) (0.0317) (0.0530) * (0.0501)d1995 0.1113 0.1101 0.0868 0.0836 0.0759 0.0877 0.0709

(0.0537) (0.0537) (0.0319) (0.0313) (0.0306) (0.0527) * (0.0495)d1996 0.1040 0.1029 0.0791 0.0754 0.0673 0.0805 0.0632

(0.0539) * (0.0539) * (0.0316) (0.0310) (0.0303) (0.0530) (0.0496)d1997 0.1218 0.1200 0.0954 0.0917 0.0842 0.0974 0.0806

(0.0543) (0.0541) (0.0314) (0.0308) (0.0303) (0.0532) * (0.0501) *d1998 0.1663 0.1645 0.1396 0.1375 0.1300 0.1385 0.1216

(0.0552) (0.0550) (0.0319) (0.0317) (0.0311) (0.0539) ** (0.0507)d1999 0.1832 0.1814 0.1549 0.1513 0.1435 0.1524 0.1346

(0.0565) (0.0563) (0.0319) (0.0314) (0.0307) (0.0550) ** (0.0516)d2000 0.1751 0.1734 0.1477 0.1442 0.1361 0.1467 0.1287

(0.0547) (0.0545) (0.0310) (0.0304) (0.0297) (0.0535) ** (0.0498)d2001 0.1578 0.1561 0.1309 0.1283 0.1207 0.1302 0.1126

(0.0539) (0.0538) (0.0307) (0.0303) (0.0297) (0.0529) ** (0.0494)d2002 0.1449 0.1429 0.1176 0.1148 0.1072 0.1197 0.1025

(0.0533) (0.0530) (0.0307) (0.0303) (0.0297) (0.0523) ** (0.0489)d2003 0.1185 0.1164 0.0905 0.0871 0.0797 0.0928 0.0753

(0.0553) (0.0550) (0.0314) (0.0308) (0.0303) (0.0541) * (0.0508)

2.29E-38 2.36E-38 2.01E-38 1.94E-38 2.06E-38 1.70E-38 1.82E-38

Standard errors reported in parentheses* Denotes significance at 10%**Denotes significance at 5%

0

0.05

0.1

0.15

0.2

1990 1994 1998 2002

Time Effects

ANNUAL REALIZED VOLATILITY

CONCLUSIONS AND IMPLICATIONS

Unconditional volatility changes in systematic ways.

Macro volatility is an important determinant of financial volatility

Potential justification for inflation targeting monetary policy as well as stabilization.

Big swings in global financial volatility are associated with US volatility.