south australia model financial statements 2016 model... · provisions for reinstatement,...

TRANSCRIPT

South Australia

Model Financial Statements

2016

Published by the Local Government Association of South Australiaunder the technical guidance of theSouth Australian Local Government Financial Management Group Inc.

Prepared for the LGA of SA by

Coalface Software & Training Solutions Pty Ltd PO Box 5450 Wagga Wagga NSW 2650

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

CO

NTE

NTS

SOU

TH A

UST

RA

LIA

MO

DEL

FIN

AN

CIA

L S

TATE

MEN

TS 2

016

CONTENTS

INTRODUCTIONMateriality 2

CONTENTS PAGENumbering of Notes .......................................................................................................... 4Note Descriptions .............................................................................................................. 4Comparative Figures ......................................................................................................... 4

COUNCIL CERTIFICATE

STATEMENT OF COMPREHENSIVE INCOMEImpairment Expense 8Discontinued Operations 9Other Comprehensive Income 9

Sub-classifications within Other Comprehensive Income ............................................... 10Other Comprehensive Income - Equity accounted Council businesses ......................... 10

Council Restructures 10Minority Interests 11

STATEMENT OF FINANCIAL POSITIONNon-current assets held for sale 13Investment property 13Liability - Equity accounted council businesses 13Reserves 13Minority Interests 14

STATEMENT OF CHANGES IN EQUITYOther Comprehensive Income - equity accounted Council businesses .......................... 14Other equity adjustments - equity accounted Council businesses .................................. 15

Council Restructures 15Minority Interests 15Accumulated Surplus 17

Revised Australian Accounting Standards ...................................................................... 17Changes in Accounting Policy ........................................................................................ 17Accounting Errors ........................................................................................................... 18Changes in Accounting Estimates .................................................................................. 18

Asset Revaluation Reserve 19Infrastructure, Property, Plant & Equipment ................................................................... 19Available-for-sale Financial Instruments ......................................................................... 19

Other Reserves 19

STATEMENT OF CASH FLOWSInvesting Activities 20Financing Activities 22Statement of Cash Flows Balance 22

Note 1 - SIGNIFICANT ACCOUNTING POLICIESBasis of Preparation ........................................................................................................ 24The Local Government Reporting Entity ......................................................................... 25Income recognition .......................................................................................................... 26

Prepared for the Local Government Association of South Australia.

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

CO

NTEN

TSSO

UTH

AU

STRA

LIA M

OD

EL FINA

NC

IAL STA

TEMEN

TS 2016

CONTENTS

Cash and Cash Equivalent Assets ...................................................................................28Other Financial Instruments .............................................................................................28Inventories .......................................................................................................................28Infrastructure, Property, Plant & Equipment ....................................................................29Payables ..........................................................................................................................31Borrowings .......................................................................................................................32Provisions ........................................................................................................................32

Employee benefits ....................................................................................................................32Provisions for reinstatement, restoration, rehabilitation, etc. ....................................................33Provision for Carbon Taxation ..................................................................................................33

Leases .............................................................................................................................34Joint Ventures and Associated Entities ............................................................................34Goods and Services Tax ..................................................................................................35Comparative Information ..................................................................................................35New Accounting Standards ..............................................................................................35Other accounting policies .................................................................................................35

Note 2 - INCOME (1)Other Comprehensive Income .........................................................................................36

General Rates 36Discretionary Rebates, Remissions & Write-offs .............................................................38

Other Rates 38Other Charges - penalties for late payment .....................................................................39Other Charges - Legal & other costs recovered. .............................................................39Remissions and write-offs - from other rates ...................................................................39

Note 2 - INCOME (2)Deciding the disclosures to be made ...............................................................................40

Statutory Charges 40User Charges 41

Construction Contract Revenue ................................................................................................41Commercial Activity Revenue ...................................................................................................41Subsidies received on behalf of users ......................................................................................41

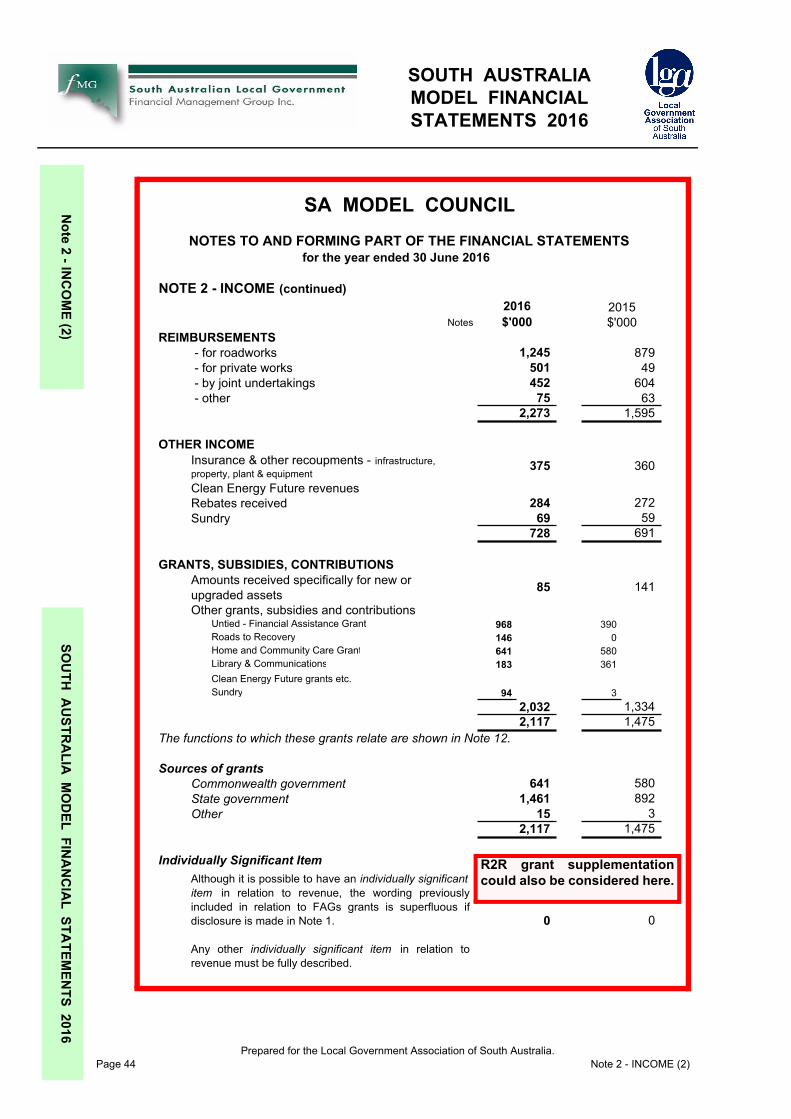

Investment Income 42Reimbursements 43Other Income 43

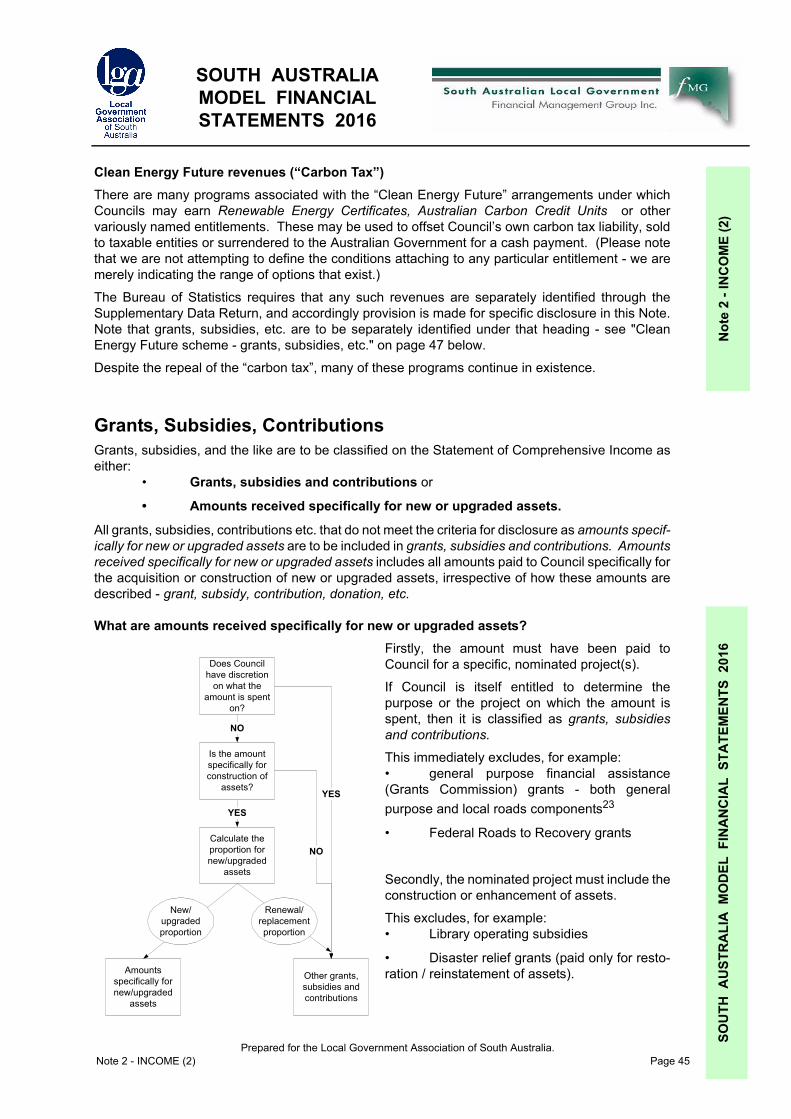

Insurance & other recoupments .......................................................................................43Clean Energy Future revenues (“Carbon Tax”) ...............................................................45

Grants, Subsidies, Contributions 45What are amounts received specifically for new or upgraded assets? ............................45

Grants for both new/upgraded and renewal/replacement of assets .........................................46Disclosure Guidance ........................................................................................................46Clean Energy Future scheme - grants, subsidies, etc. ....................................................47Sources of Grants, etc. ....................................................................................................48Conditions over grants and contributions .........................................................................48Listing of grants, subsidies, etc. received ........................................................................48

Physical resources received free of charge 48

Note 3 - EXPENSESDeciding the disclosures to be made ...............................................................................49

Prepared for the Local Government Association of South Australia.

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

CO

NTE

NTS

SOU

TH A

UST

RA

LIA

MO

DEL

FIN

AN

CIA

L S

TATE

MEN

TS 2

016

CONTENTS

Employee Costs 49Salaries & Wages ........................................................................................................... 51Employee leave expense ................................................................................................ 51Superannuation contributions ......................................................................................... 51Workers Compensation Insurance .................................................................................. 51Capitalised and Distributed Costs ................................................................................... 51

Direct Labour Oncosting Procedures .......................................................................................51Employee numbers ......................................................................................................... 52

Materials, Contracts & Other Expenses 52Prescribed Expenses ...................................................................................................... 52

Auditors fees .............................................................................................................................52Bad and Doubtful Debts Expense ............................................................................................52Elections & Elected Members’ Expenses .................................................................................53Operating Lease Payments ......................................................................................................53

Other Materials, Contracts and Expenses ...................................................................... 53Individually significant items .....................................................................................................53Legal expenses ........................................................................................................................54Levies paid to government .......................................................................................................54Capitalised and Distributed Costs ............................................................................................54Plant Hire “Profit” or “Loss” .......................................................................................................54

Depreciation, Amortisation & Impairment 56Capitalised and Distributed Costs ................................................................................... 56Impairment Offsets .......................................................................................................... 57

Finance Costs 57Bank Charges ...........................................................................................................................57

Discounts and Premiums ................................................................................................ 57Unwinding of Present Value Discounts ........................................................................... 57Capitalisation of Interest ................................................................................................. 57

Investment Property expenses 58

Note 4 - ASSET DISPOSAL & FAIR VALUE ADJUSTMENTSInfrastructure, Property, Plant & Equipment 59Investment Property 61Available-for-sale Financial Assets 61Real Estate Developments 62Fair Value Adjustments 62

Fair Value Adjustment - Investment Property ................................................................. 62Revaluation decrements previously expensed, now recouped ....................................... 62Revaluation decrements expensed ................................................................................. 62

Note 5 - CURRENT ASSETSCash & Equivalent Assets 63Trade & Other Receivables 63

Deciding the disclosures to be made .............................................................................. 63Rates - General & other .................................................................................................. 64Rates postponed for State Seniors ................................................................................. 64Accrued Revenues .......................................................................................................... 64Debtors - general ............................................................................................................ 64

Fines & Expiation Notices .........................................................................................................64Other levels of government ............................................................................................. 66

Prepared for the Local Government Association of South Australia.

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

CO

NTEN

TSSO

UTH

AU

STRA

LIA M

OD

EL FINA

NC

IAL STA

TEMEN

TS 2016

CONTENTS

GST Recoupment ............................................................................................................66Prepayments ....................................................................................................................66Loans to Community Organisations .................................................................................66

No- and Low- Interest Loans ....................................................................................................67Aged Care Facility Deposits .............................................................................................69

Accounting for Aged Care Facility Deposits .............................................................................69Sundry ..............................................................................................................................69Disclosure of Amounts Not Realised within 12 Months ...................................................70

Other Financial Assets 70Inventories 70

Stores and materials ........................................................................................................70Trading Stock ...................................................................................................................70Work in Progress .............................................................................................................70Real Estate Developments ..............................................................................................71

Classification as Current and Non-Current Assets ...................................................................71Other Real Estate held for resale .....................................................................................71Inventory write-downs ......................................................................................................71

Note 6 - NON-CURRENT ASSETSFinancial Assets 71

Deciding the disclosures to be made ...............................................................................71Rates & General Receivables ..........................................................................................72Council Rate Postponement Scheme ..............................................................................72Prepayments ....................................................................................................................72Other Financial Assets .....................................................................................................72

Equity accounted investments in Council businesses 74Other Non-current Assets 74

Inventory ..........................................................................................................................74Capital works-in-progress ................................................................................................75Interests in Regional Local Government Associations .....................................................75Other Assets ....................................................................................................................75

Note 7 - “FIXED” ASSETSInfrastructure, Property, Plant & Equipment 76

Capital v. Maintenance Expenditure ................................................................................76Maintenance Expenditure .........................................................................................................77Capital Expenditure ..................................................................................................................77

Definition - new/upgraded & renewal/replacement of assets ...........................................78Capitalisation Thresholds .................................................................................................79Determining Asset Components ......................................................................................80

Gravel Re-sheeting ...................................................................................................................81“Collection” Assets ....................................................................................................................82Land Under Roads ....................................................................................................................83

Cost Model or Fair Value Model ......................................................................................83The Fair Value Model .......................................................................................................84

Assets to be measured using the Fair Value Model .................................................................84Transition to AASB 13 Fair Value Measurement ......................................................................84Revaluation Methods ................................................................................................................85Determining “Classes” of Assets ..............................................................................................85Frequency of Revaluations .......................................................................................................86Accounting for Revaluations .....................................................................................................87

Prepared for the Local Government Association of South Australia.

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

CO

NTE

NTS

SOU

TH A

UST

RA

LIA

MO

DEL

FIN

AN

CIA

L S

TATE

MEN

TS 2

016

CONTENTS

Disclosures of Valuations .........................................................................................................89The Fair Value Hierarchy ..........................................................................................................90Example Valuation Disclosures ................................................................................................91Example Disclosures for Individual Asset Classes ...................................................................97

Depreciation .................................................................................................................... 98Depreciation Methods ...............................................................................................................99Depreciation of Components ....................................................................................................99Useful Life .................................................................................................................................99Residual Value .......................................................................................................................100

Impairment .................................................................................................................... 102Future reinstatement cost ............................................................................................. 103Disclosures ................................................................................................................... 103

Investment Property 103Cost Model or Fair Value Model ................................................................................... 105Fair Value Model ........................................................................................................... 105Cost Model .................................................................................................................... 105

Note 8 - LIABILITIESDeciding the disclosures to be made ............................................................................ 106Classification of Current and Non-Current Liabilities .................................................... 106

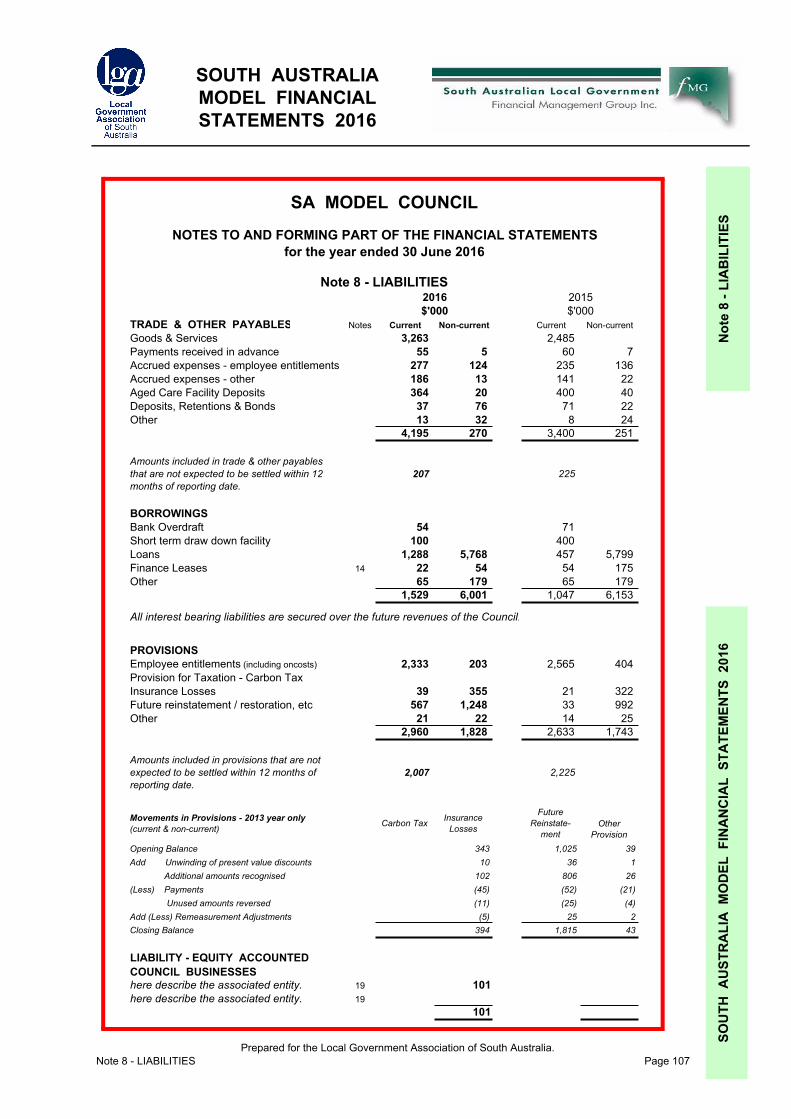

Trade & other payables 106Trade Payables ............................................................................................................. 106Payments received in advance ..................................................................................... 108Accrued expenses - employee benefits ........................................................................ 108

Sick leave ...............................................................................................................................108Maternity leave .......................................................................................................................108Parental leave .........................................................................................................................108

Accrued expenses - other ............................................................................................. 109Aged Care Facility Deposits .......................................................................................... 109Deposits, Retentions & Bonds ...................................................................................... 109Other payables .............................................................................................................. 109

Suspense Accounts ................................................................................................................109Borrowings 109

Borrowings for periods of less than 12 months ............................................................. 109Borrowings .................................................................................................................... 111

Provisions 111Employee Entitlements ................................................................................................. 111

Annual Leave ..........................................................................................................................111Long Service Leave ................................................................................................................112Funding Long Service Leave ..................................................................................................112Long Service Leave Payments from other Councils ...............................................................112Vesting Sick Leave .................................................................................................................113Attributable on-costs ...............................................................................................................113

Provision for Carbon Taxation ...................................................................................... 113Insurance Losses .......................................................................................................... 114Future Reinstatement / Restoration, etc. ...................................................................... 114

Legal or Constructive Obligation ............................................................................................114Present Obligation arising from a Past Event .........................................................................114Best Available Estimate ..........................................................................................................115Present Value .........................................................................................................................115Changes in Provision ..............................................................................................................115

Prepared for the Local Government Association of South Australia.

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

CO

NTEN

TSSO

UTH

AU

STRA

LIA M

OD

EL FINA

NC

IAL STA

TEMEN

TS 2016

CONTENTS

For all provisions - Unwinding of Present Value Discounts ...........................................116Movements in Provisions 116Equity accounted entities with negative equity 117Other Liabilities 117

Note 9 - RESERVESAsset Revaluation Reserve 117

Infrastructure, Property, Plant & Equipment ..................................................................117Available for Sale Investments .......................................................................................117

Other Reserves 119Section 155 Charges ..............................................................................................................119

Note 10 - RESTRICTIONS ON ASSETSLimitations on the Use of Assets 122

Note 11 - CASH FLOW RECONCILIATIONThe Definition of “Cash” .................................................................................................124The Reconciliation .........................................................................................................124Non-cash Financing & Investing Activities .....................................................................124Financing Arrangements ................................................................................................124

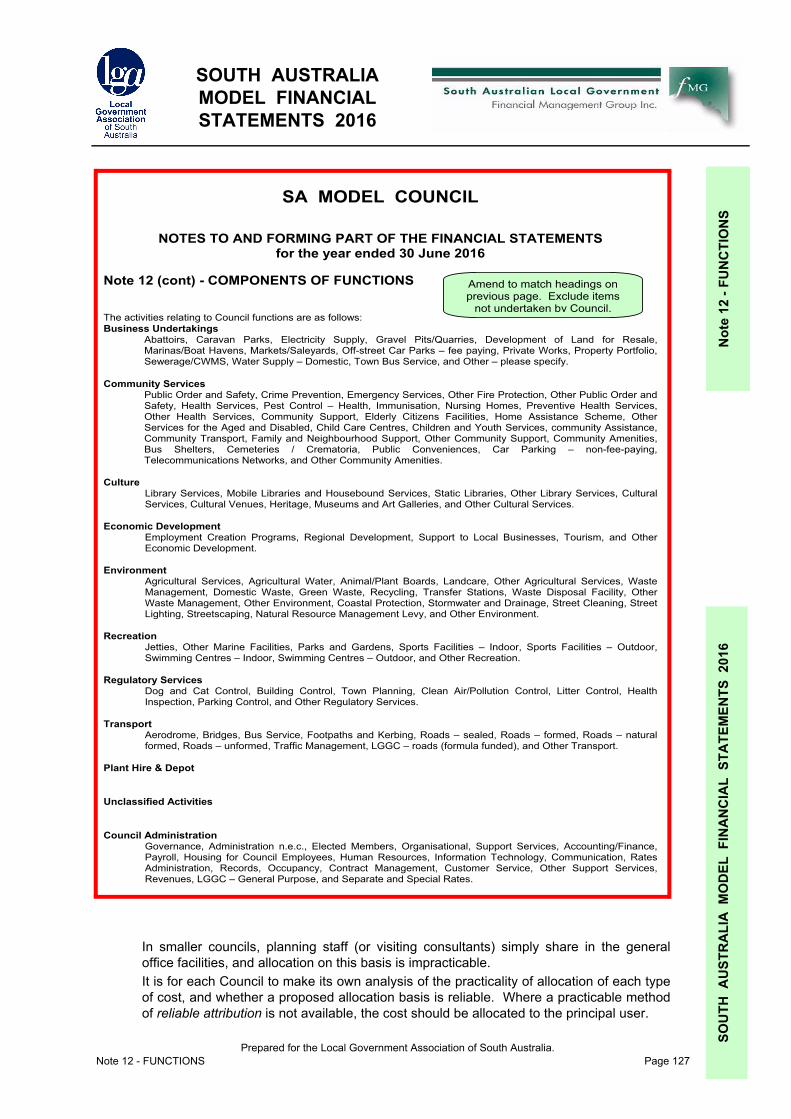

Note 12 - FUNCTIONS

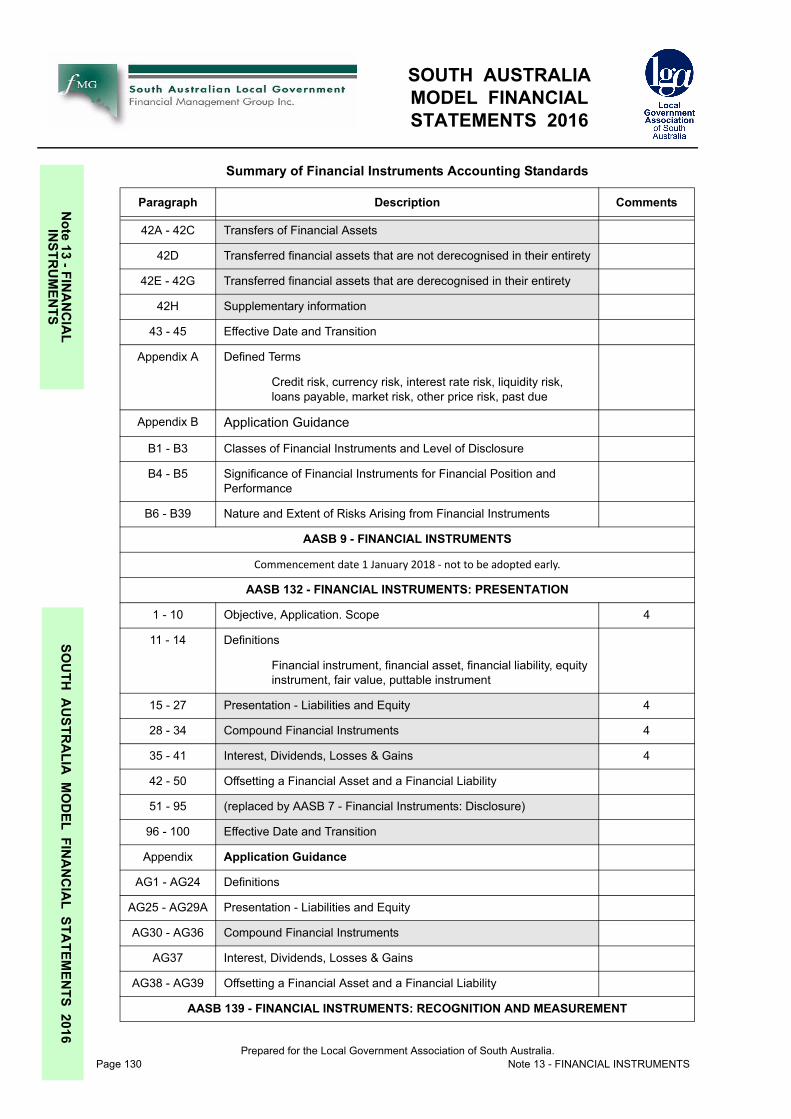

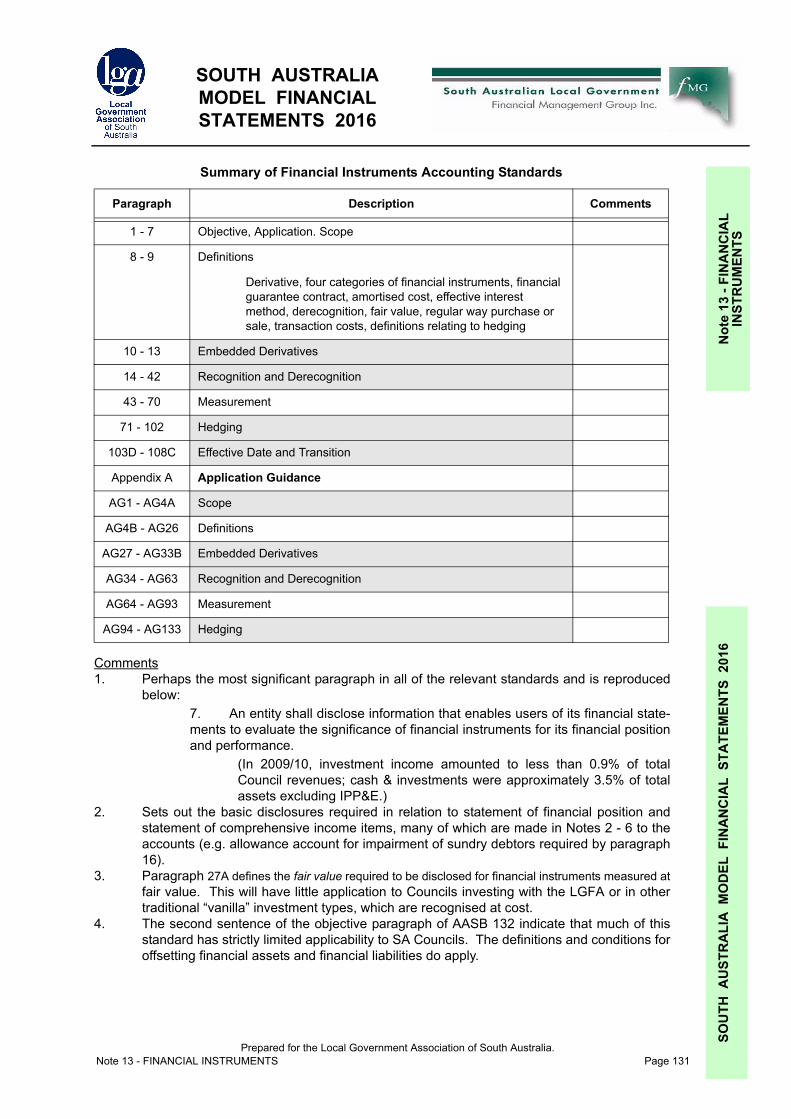

Note 13 - FINANCIAL INSTRUMENTSA summary of the Financial Instruments Accounting Standards 129

Comments ..............................................................................................................................131Accounting Policies 132Financial Instrument Risks 134Categorisation of Financial Instruments 134Recognition of Financial Instruments 137The fair value hierarchy 138Liquidity Analysis 138Local Government Finance Authority of SAFinancial Products 139

Loans to Council ............................................................................................................139Deposits by Council .......................................................................................................139

Note 14 - EXPENDITURE COMMITMENTSCapital Commitments 140Other Expenditure Commitments 140Commitments for Intangible Assets 140Finance Leases 140

Note 15 - FINANCIAL INDICATORSIndicator 1 - Operating Surplus Ratio 142

Adjustments to Operating Surplus Ratio ........................................................................143Indicator 2 - Net Financial Liabilities Ratio 144Indicator 3 - Asset Sustainability Ratio 145

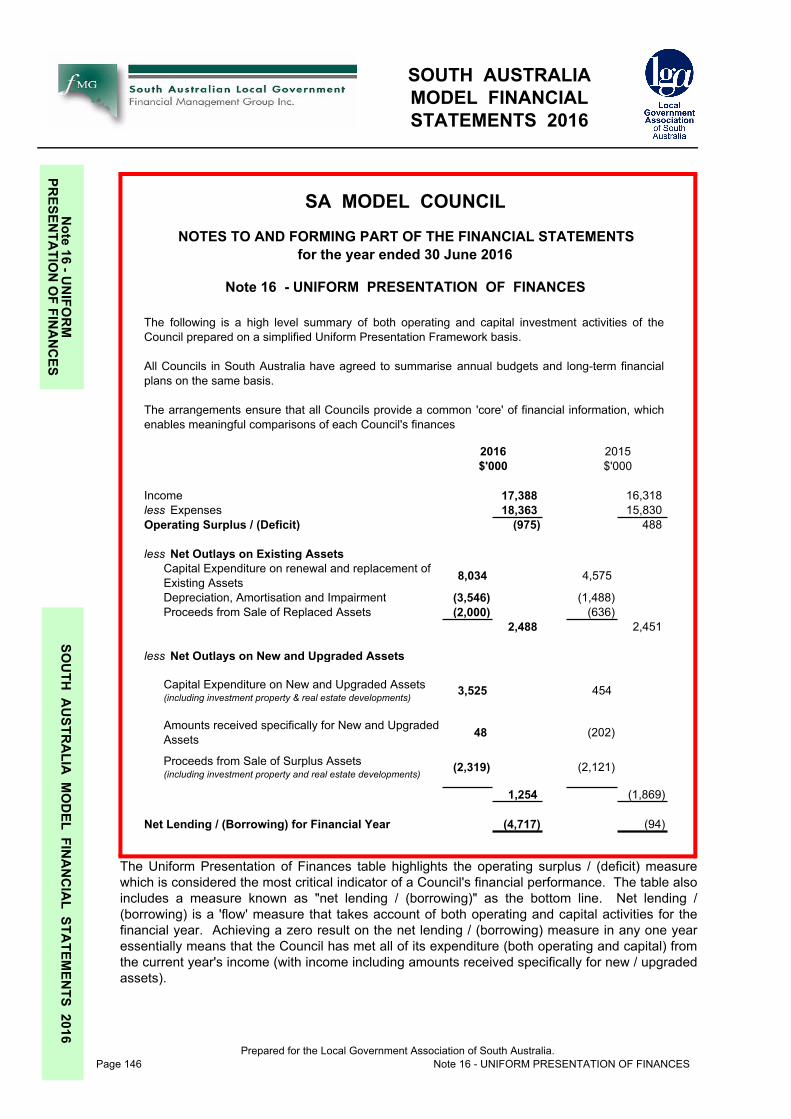

Note 16 - UNIFORM PRESENTATION OF FINANCESCompilation ....................................................................................................................147

Prepared for the Local Government Association of South Australia.

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

CO

NTE

NTS

SOU

TH A

UST

RA

LIA

MO

DEL

FIN

AN

CIA

L S

TATE

MEN

TS 2

016

CONTENTS

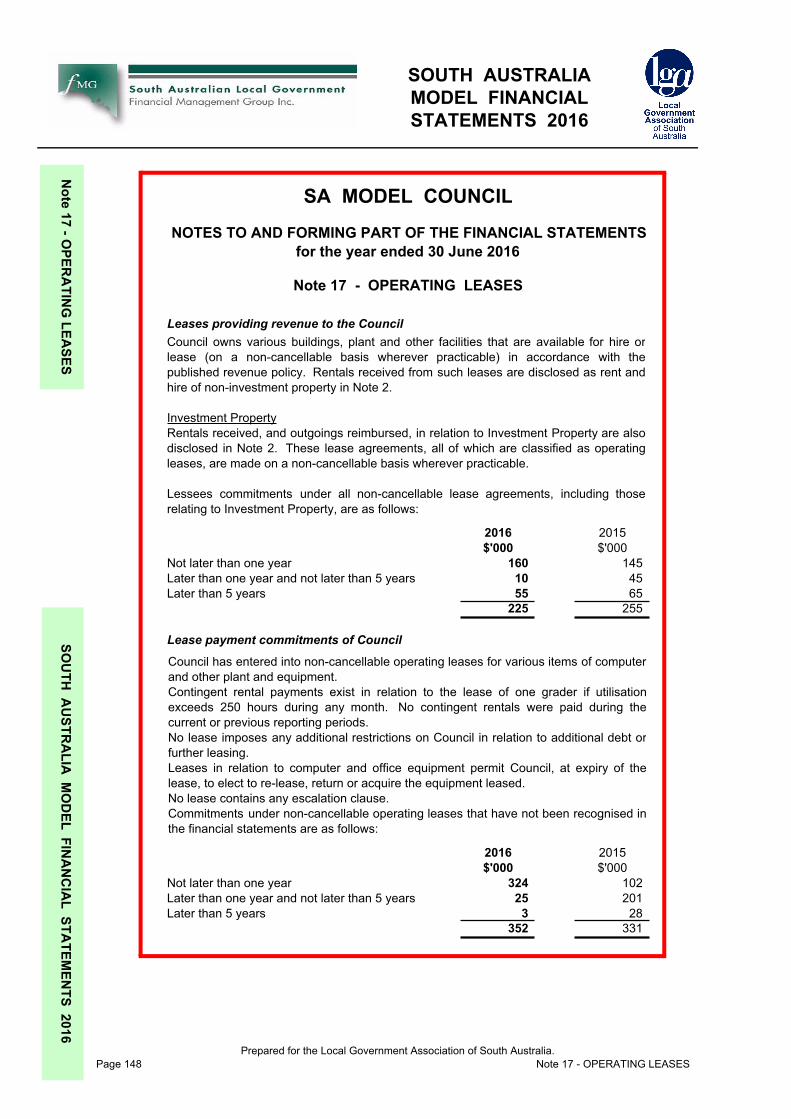

Note 17 - OPERATING LEASESLeases providing revenue to the Council ...................................................................... 149Lease payment commitments of Council ...................................................................... 149

Note 18 - SUPERANNUATION

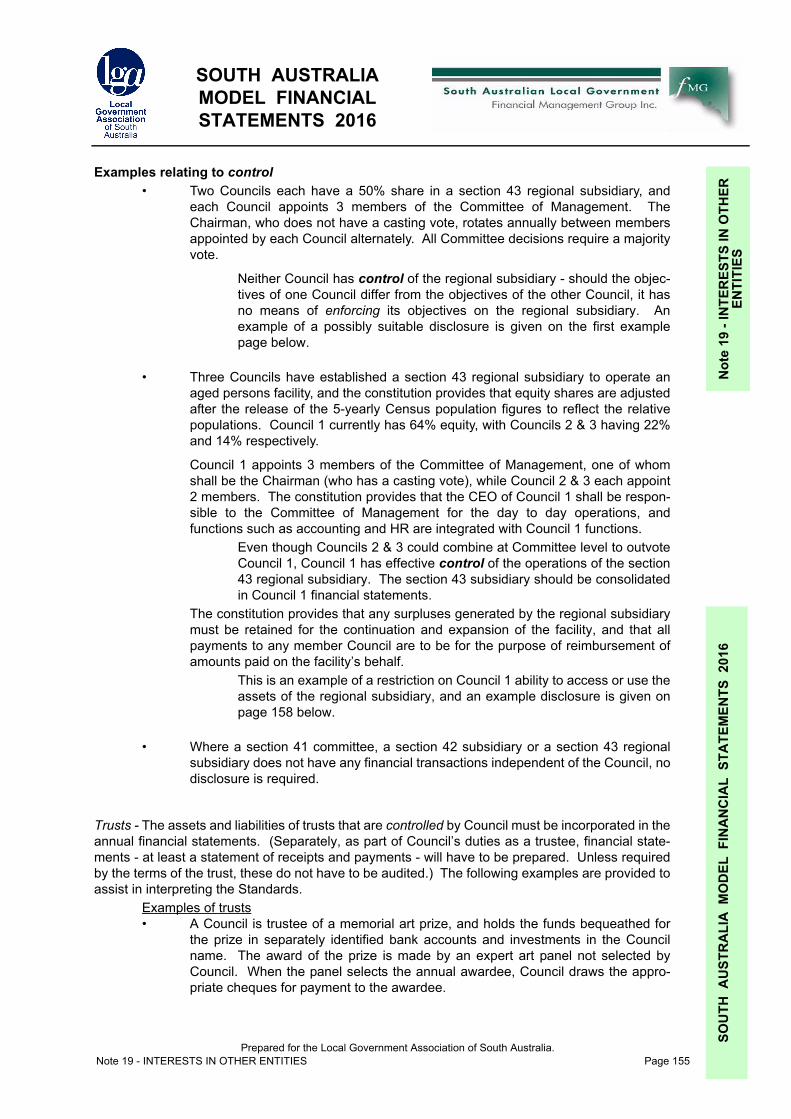

Note 19 - INTERESTS IN OTHER ENTITIESTrivial Interests 151The Importance of Variable Returns 151The Structure of Note 19 152Interests in Other Entities - a decision chart 153Consolidation - Council has control 154

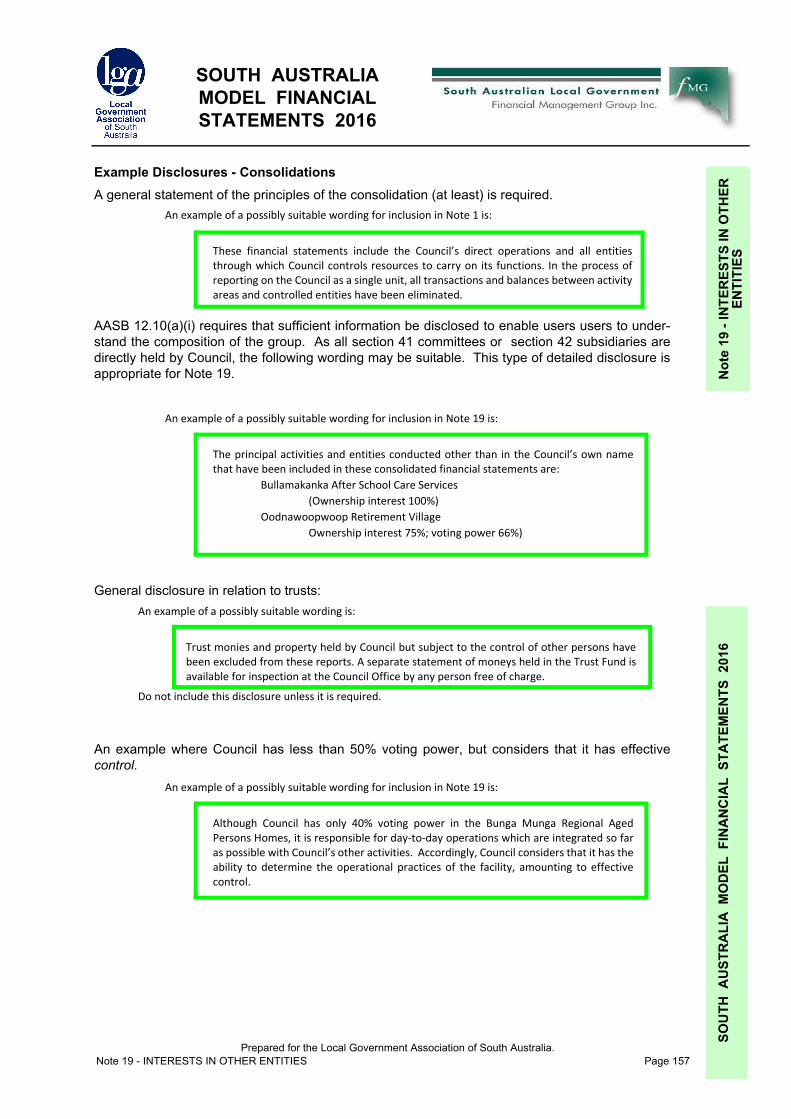

Outside Equity Interests ................................................................................................ 154Examples relating to control ........................................................................................ 155Example Disclosures - Consolidations .......................................................................... 157

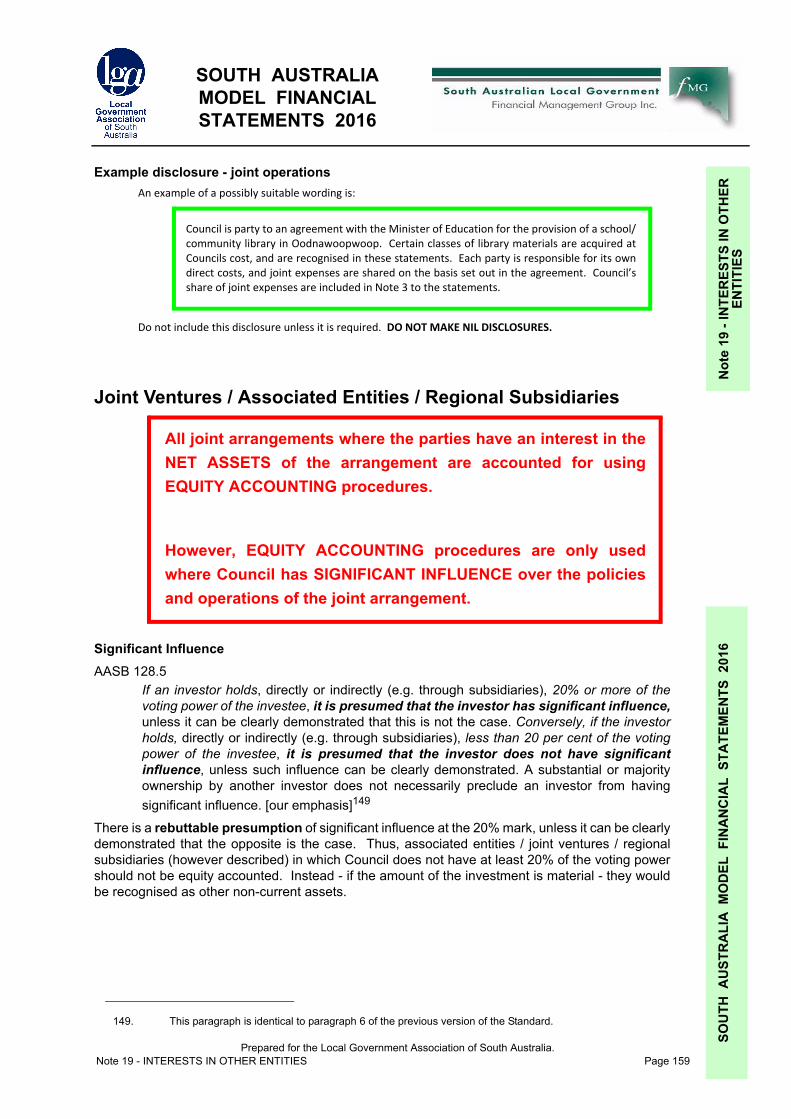

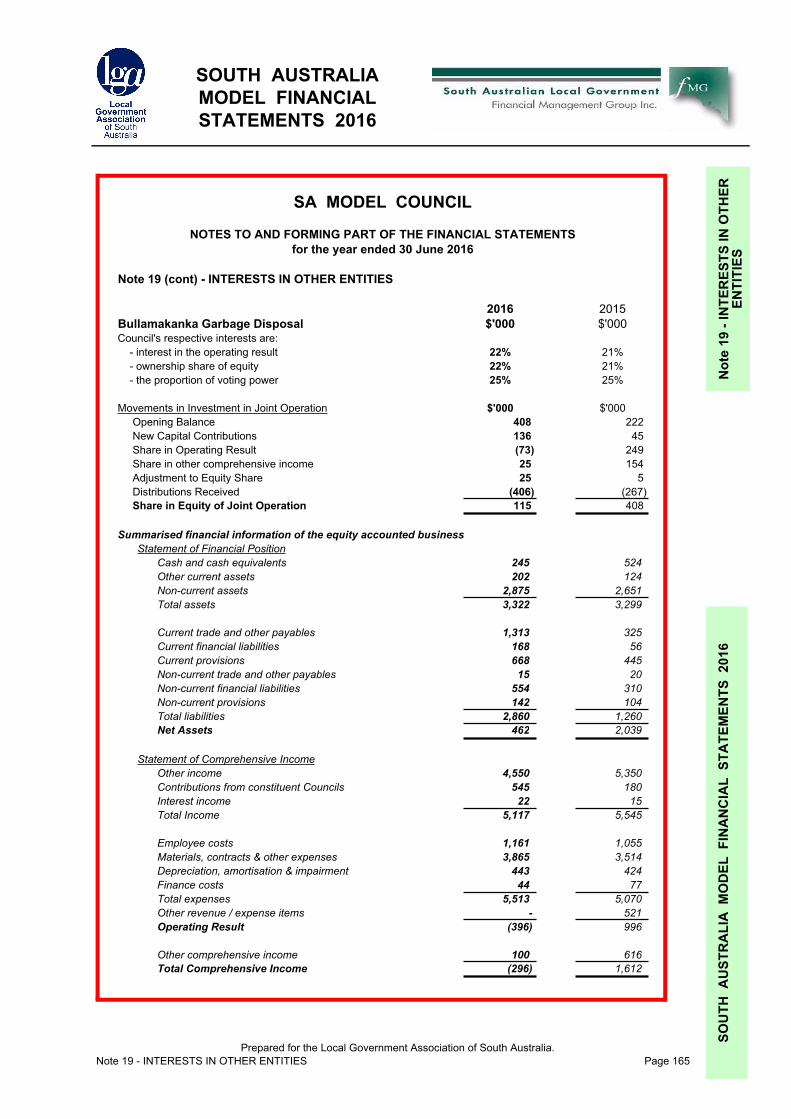

Joint Operations and Joint Ventures 158Example of joint operations ........................................................................................... 158Example disclosure - joint operations .......................................................................... 159

Joint Ventures / Associated Entities / Regional Subsidiaries 159Significant Influence ...................................................................................................... 159Section 43 Regional Subsidiaries ................................................................................. 160Requirements of the Local Government (Financial Management) Regulations 2011 .. 162

................................................................................................................................................163“BOO” & “BOOT” Schemes ....................................................................................................163

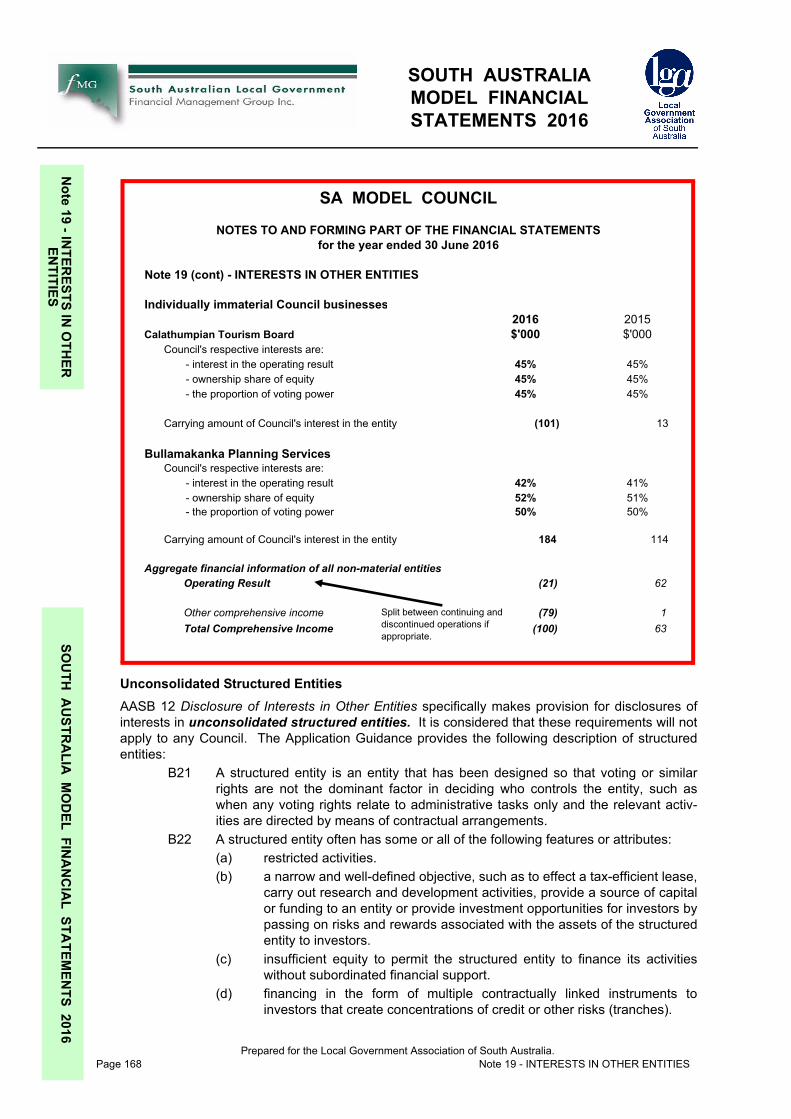

Accounting Procedures for Equity Accounted Associated Entities (Regional Subsidiaries) 163Material and Non-Material Interests in Associated Entities ........................................... 164

................................................................................................................................................165Disclosures for Equity Accounted Entities .................................................................... 166

General Disclosures ...............................................................................................................166 ................................................................................................................................................166Disclosures for Material Interests ..........................................................................................166Disclosures for Non-material Interests ..................................................................................167

Unconsolidated Structured Entities ............................................................................... 168

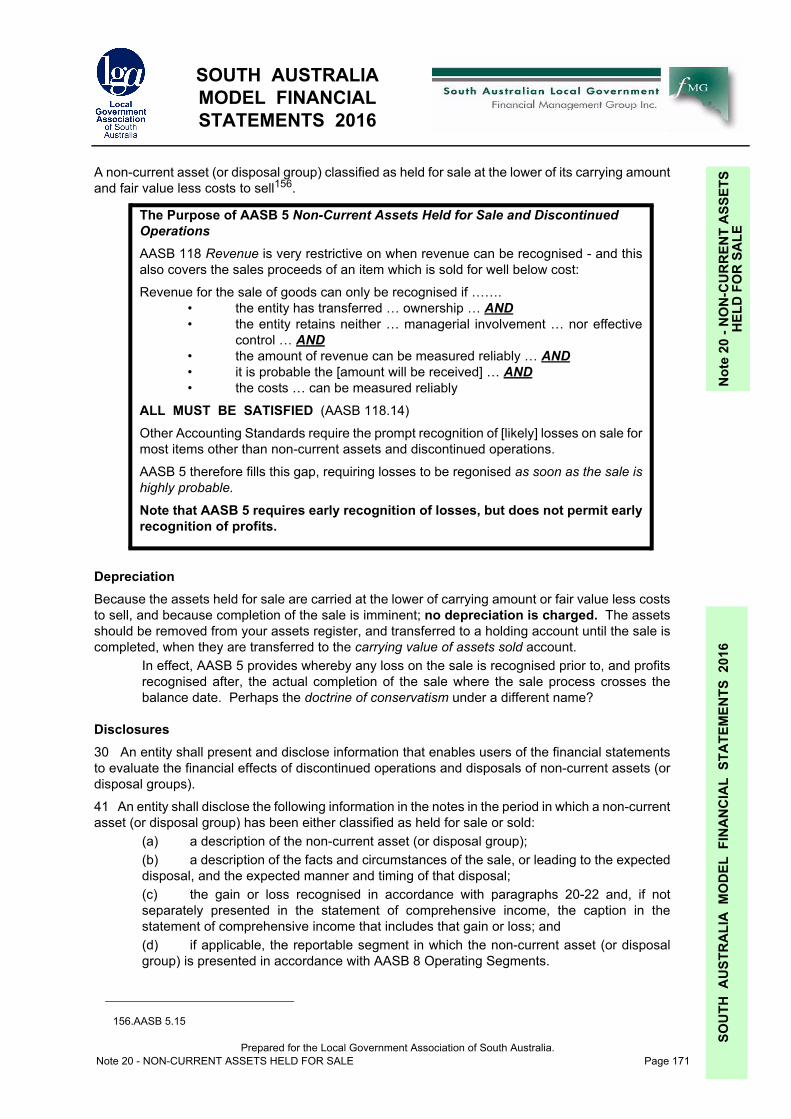

Note 20 - NON-CURRENT ASSETS HELD FOR SALEThe Purpose of AASB 5 Non-Current Assets Held for Sale and Discontinued Operations 171Depreciation .................................................................................................................. 171Disclosures ................................................................................................................... 171

Note 21 - ASSETS & LIABILITIES NOT RECOGNISED

Note 22 - EVENTS AFTER THE STATEMENT OF FINANCIAL POSITION DATE

Note 23 - RELATED PARTY DISCLOSURESRelated Parties 174Key Management Personnel 175Disclosures of Related Party Transactions 176

COUNCIL CERTIFICATES OF AUDIT INDEPENDENCE

Prepared for the Local Government Association of South Australia.

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

CO

NTEN

TSSO

UTH

AU

STRA

LIA M

OD

EL FINA

NC

IAL STA

TEMEN

TS 2016

CONTENTS

AUDIT CERTIFICATE OF AUDIT INDEPENDENCE

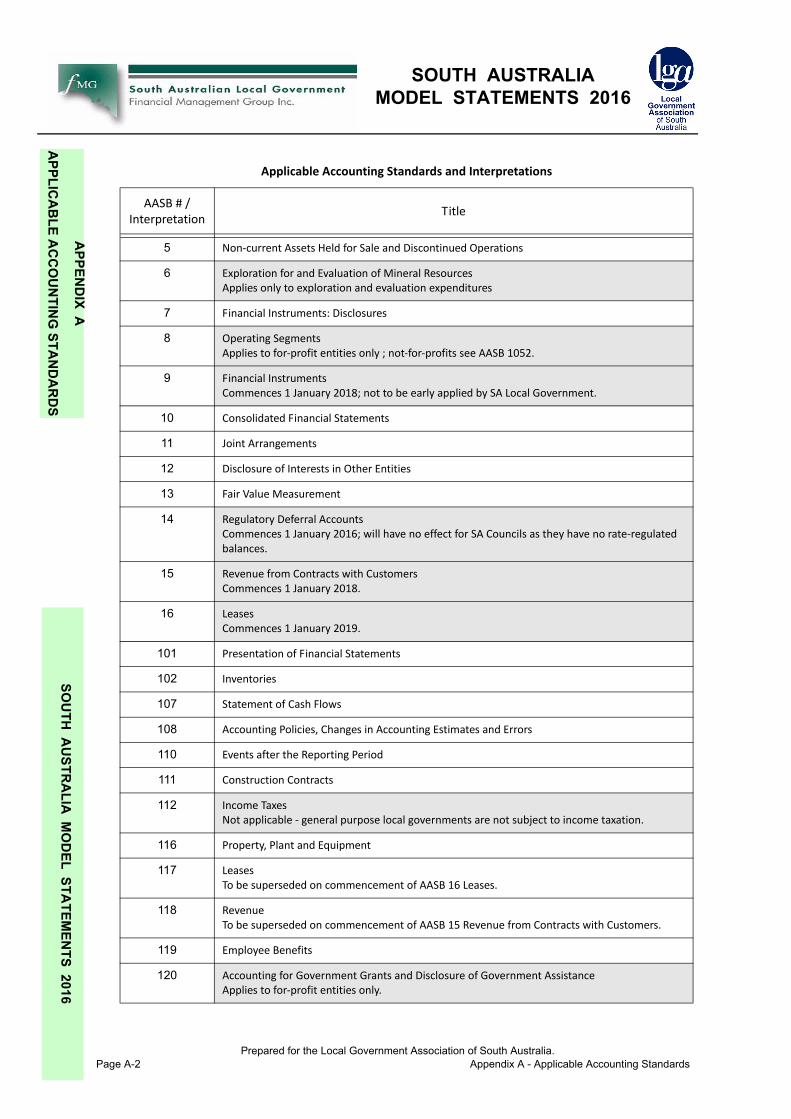

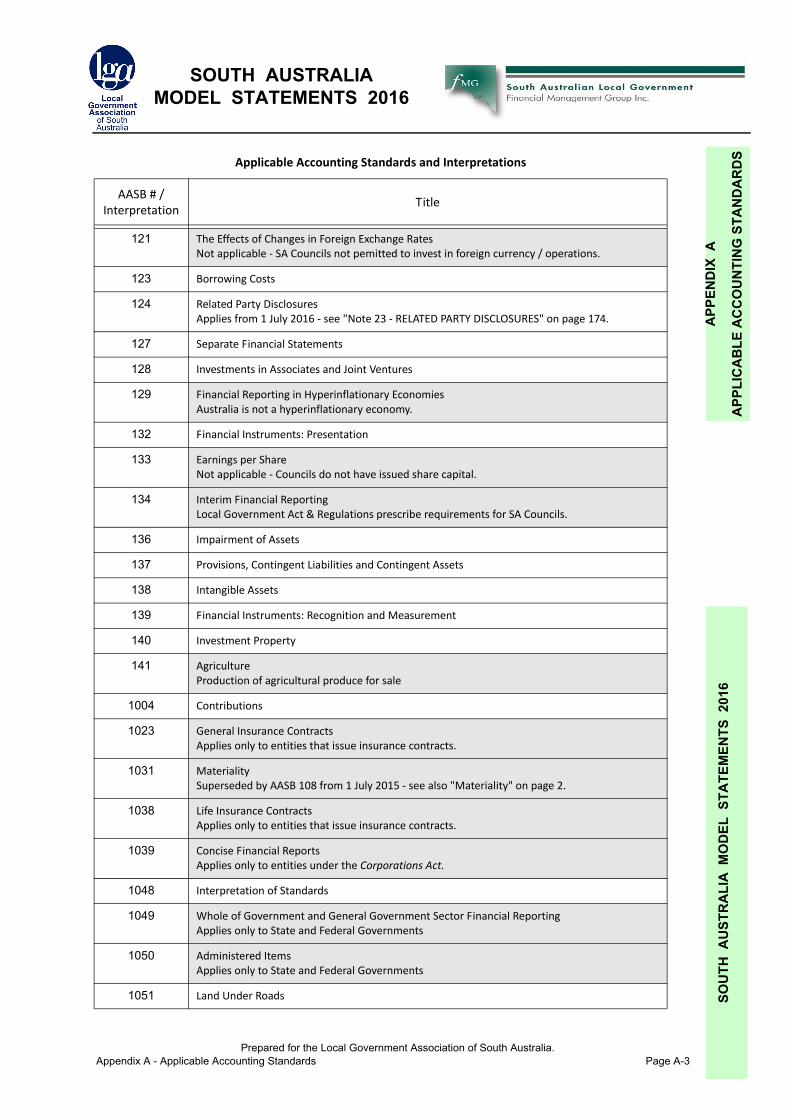

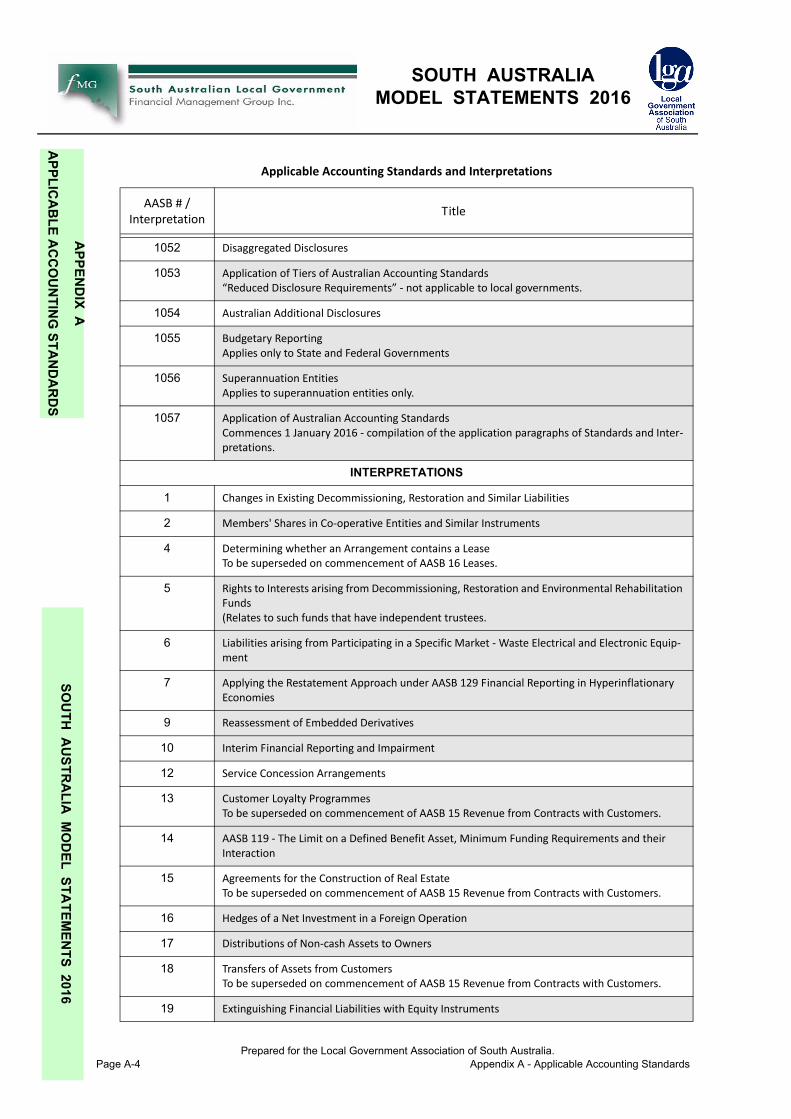

ADDITIONAL MATERIALSWP 1 - GRANTS RECEIVED & EXPENDED 179LIST OF CURRENT ACCOUNTING STANDARDS 180ABS / LGGC CLASSIFICATIONS 180

APPENDIX A - APPLICABLE AUSTRALIAN ACCOUNTING STANDARDS & IN-TERPRETATIONSHOW TO USE THIS APPENDIX 1TABLE OF ACCOUNTING STANDARDS & INTERPRETATIONS 1TABLE OF NEW & AMENDED STANDARDS 5TABLE OF NEW & AMENDED INTERPRETATIONS 8Exposure Drafts Pending 9

Income from Transactions of NFP entites ..........................................................................9Leases ...............................................................................................................................9

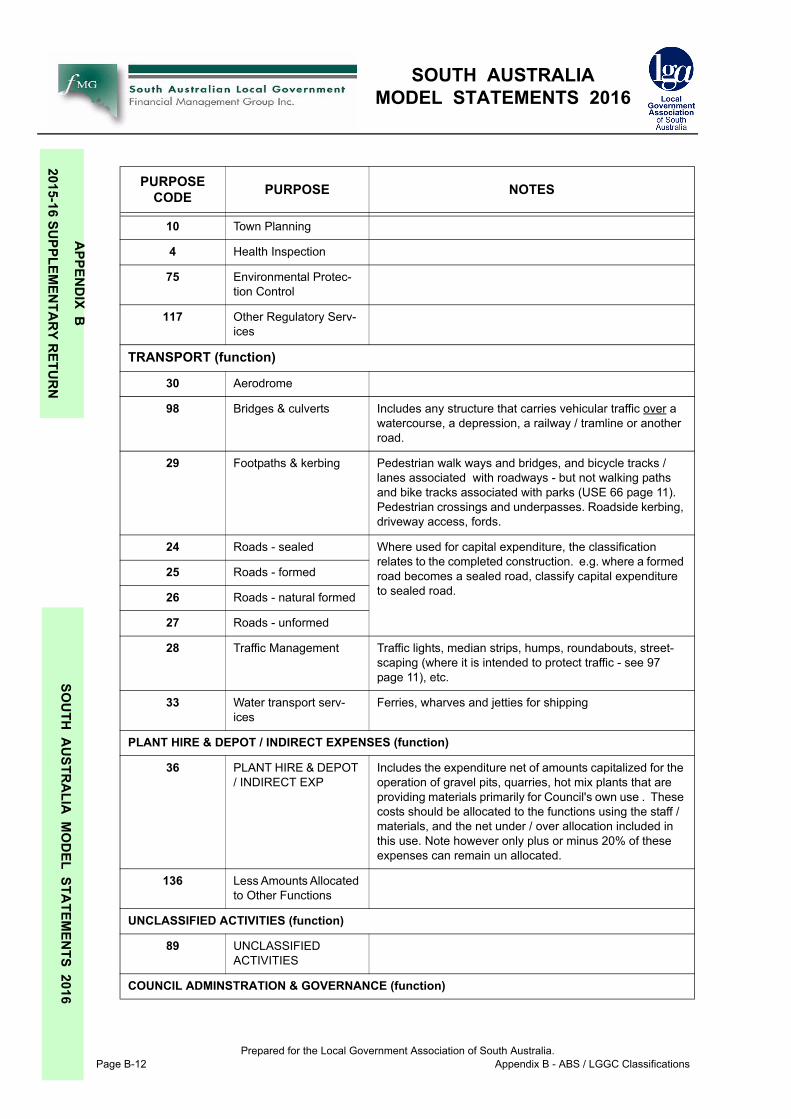

APPENDIX B - 2015-16 SUPPLEMENTARY RETURNINTRODUCTION 1EXECUTIVE SUMMARY 1INSTRUCTIONS / TIPS ON COMPLETION OF THE RETURN 3ASSIGNMENT OF ACTIVITIES TO PURPOSES 5

Index of activity by purpose code table - use of "Function", or "Facility Code" instead of a purpose code: ....................................................................................................................5Multi-purpose activities ......................................................................................................6

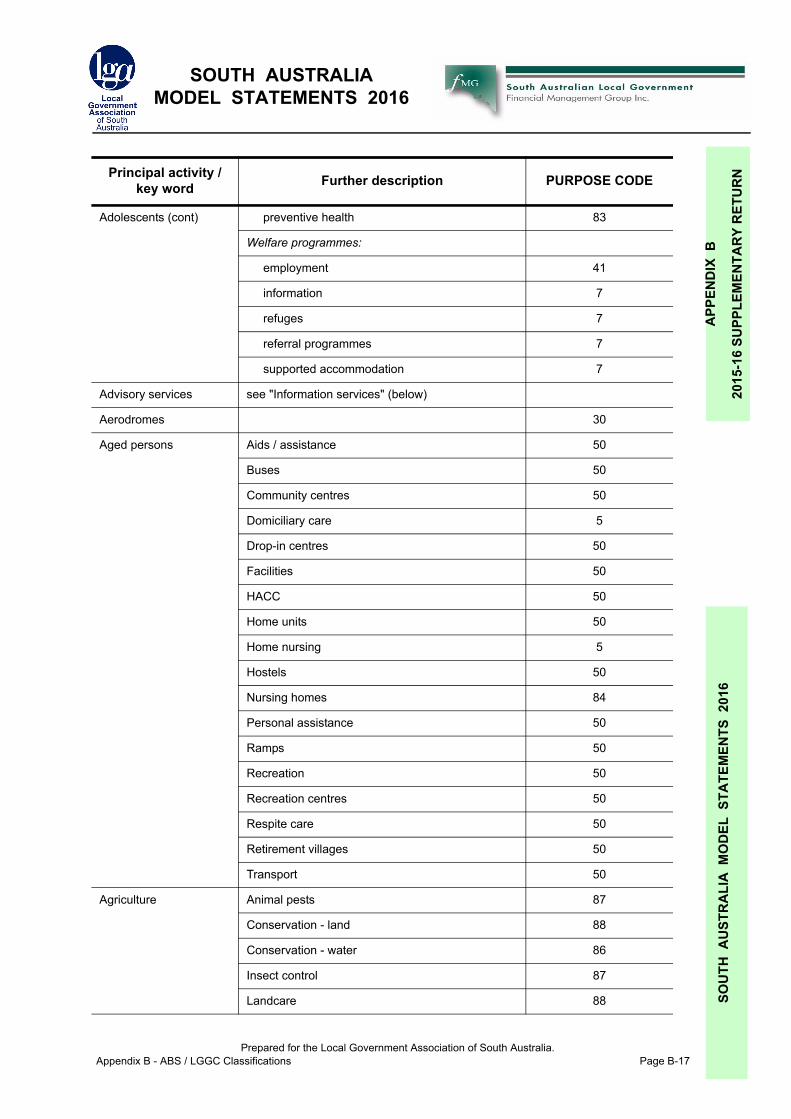

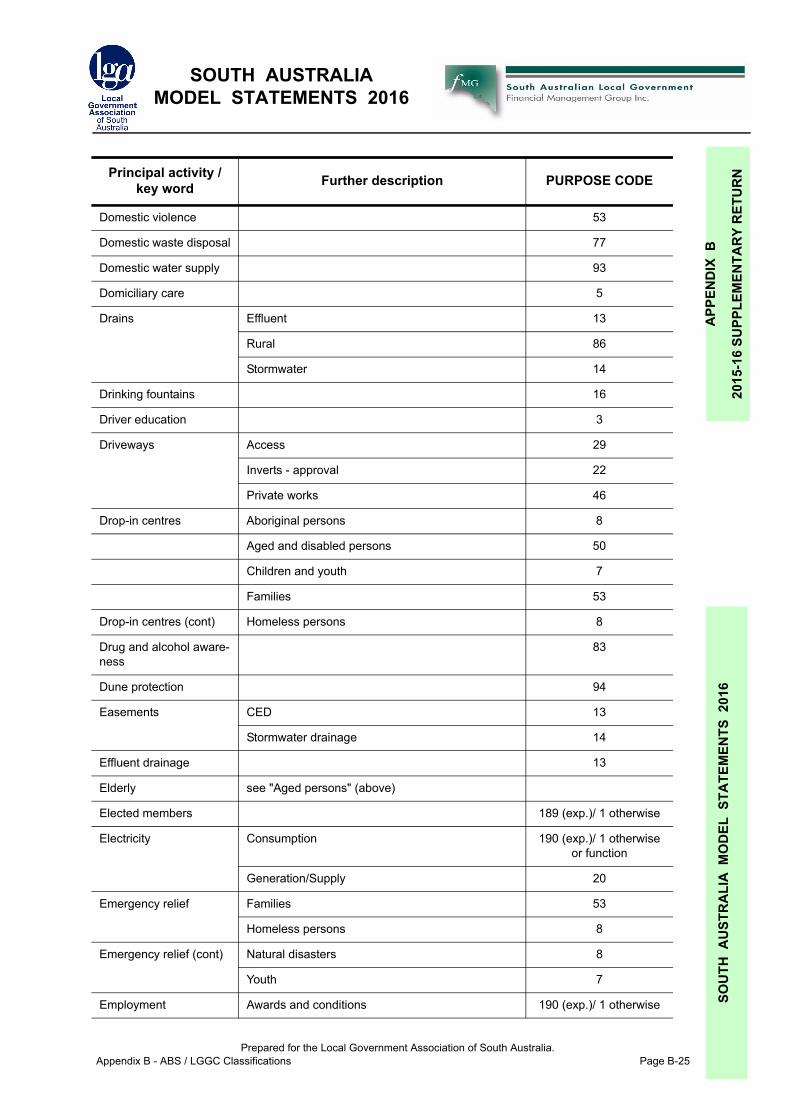

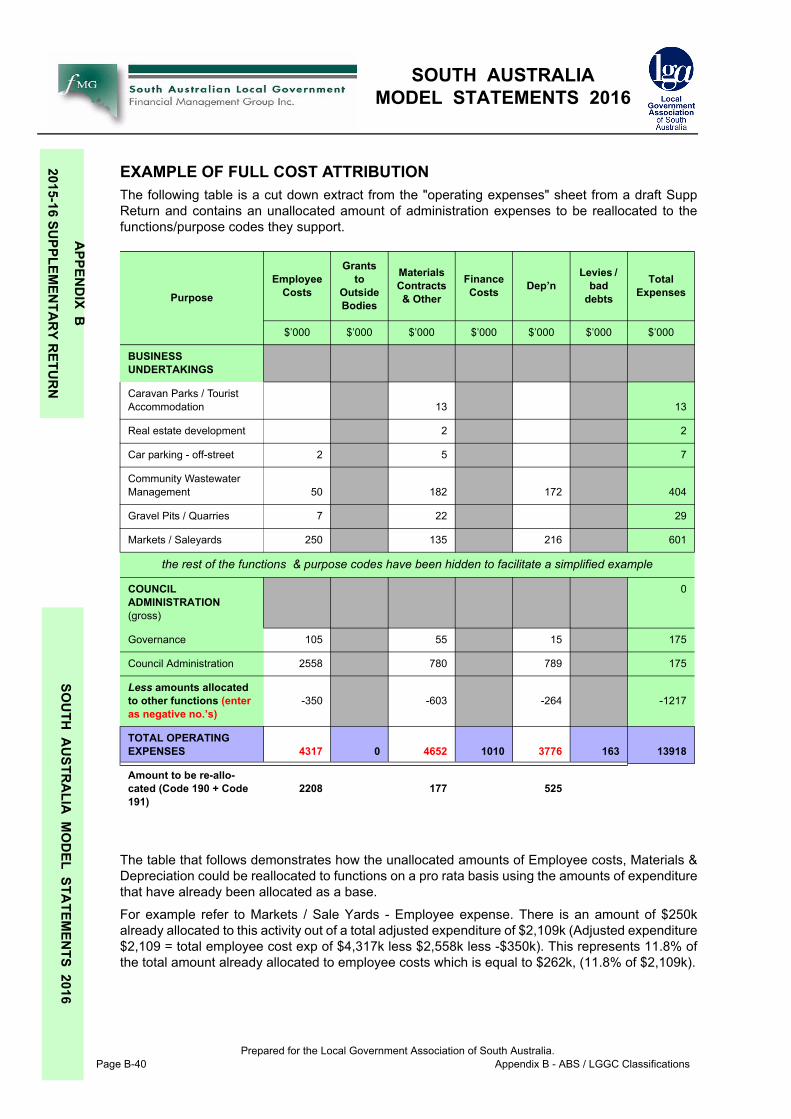

GLOSSARY OF PURPOSE CODES 7INDEX OF ACTIVITIES BY PURPOSE CODE 14EXAMPLE OF FULL COST ATTRIBUTION 40

Prepared for the Local Government Association of South Australia.

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

INTR

OD

UC

TIO

NO

UTH

AU

STR

ALI

A M

OD

EL F

INA

NC

IAL

STA

TEM

ENTS

201

6

INTRODUCTIONThese Model Financial Statements have been prepared by Coalface Software Solutions for theLocal Government Association of South Australia (LGA), under the technical guidance of the SALocal Government Financial Management Group Inc. (FMG).

The Local Government Act 1999 at section 127 requires that a council must prepare financial state-ments and notes in accordance with standards prescribed by the regulations, and other statementsor documentation relating to the financial affairs of the council required by the regulations for eachfinancial year. Regulation 13 of the Local Government (Financial Management) Regulations 2011requires that the financial statements of a council, council subsidiary or regional subsidiary (otherthan notes and other explanatory documentation) must be in accordance with the requirements setout in the Model Financial Statements.

For the purposes of the definition of Model Financial Statements, the document entitled the ModelFinancial Statements published by the LGA on 23 August 2006, as in force from time to time, isadopted by these regulations pursuant to section 303(4) of the Act.1 These Model Statements,when authorised by the Minister, become the Model Financial Statements referred to in Regulation4(3). The Local Government Association notifies all Councils when the statutory procedures havebeen completed.

The Model Financial Statements set out a recommended format for the presentation of the 2016Annual Financial Statements for South Australian Councils and all other bodies, including regionalsubsidiaries, established pursuant to the Local Government Act. As such, they provide an exampleof the level of information that the LGA and FMG consider is appropriate to provide, and an exampleof the manner in which this information may be presented. The amounts shown are entirely ficti-tious, and are intended only to illustrate the various relationships between different portions of thestatements. Amounts given are shown as being rounded to the nearest thousand dollars ($’000),and this is recommended, but rounding to the nearest dollar may also be used.

The Model Statements include disclosures that apply to a wide range of users, but it is unlikely thatany one user will find all of the disclosures appropriate to its circumstances. Similarly, it is likely thatmost users will need to make one or more disclosures not shown in the Model Statements, andguidance on many of these is given in the explanatory text.

In preparing annual financial statements in the Model Statements format, it is theresponsibility of each user to ensure that its reports comply with(a) the Australian Accounting Standards and Interpretations as they apply tonot-for-profit entities and local government, and having regard to interpretations inthese Model Statements, and(b) additional requirements (if any) imposed under South Australian legislation.

1. Local Government (Financial Management) Regulations 2011, Regulation 4(3).

Prepared for the Local Government Association of South Australia.

S

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

Pa

INTR

OD

UC

TION

SOU

TH A

USTR

ALIA

MO

DEL FIN

AN

CIA

L STATEM

ENTS 2016

A fundamental objective is that the format of the four principal financial statements together with thenotes entitled Financial Indicators (numbered Note 15 in these Model Statements) and UniformPresentation of Finances (numbered Note 16 in these Model Statements) be adopted by allCouncils in the format shown (other reporting entities are not required to supply Notes 15 & 16). Anyvariation from the format shown must be strongly supported. However, any user may:

(a) include additional disclosures not provided for in the Model Statements wherethese are required by any Australian Accounting Standard or Interpretation.(b) use more restricted descriptions of any accounting classification where this isappropriate to the user, not withstanding that a generic description appears in the ModelStatements.(c) omit descriptions on the face of the principal statements, policies in the Statementof Significant Accounting Policies, and detailed Notes in whole or in part, where thosedescriptions, policies and Notes do not have application to the affairs of the user, andwhere all disclosures for the current and previous reporting periods would be NIL.

With ongoing modifications to the Australian Accounting Standards, it is anticipated that theseModel Statements will be updated annually. These Model Statements have been designed to beprinted - if it is necessary to print - on both sides of the paper.

MaterialityExcept where these Model Statements describe a disclosure as prescribed or mandatory,Councils are expected to apply the key accounting concept of materiality to disclosures throughoutthe Annual Financial Statements. Materiality is defined in AASB 108 paragraph 5 as follows:

“omissions or misstatements of items are material if they could, individually or collectively,influence the economic decisions that users make on the basis of the financial statements.Materiality depends on the size and nature of the omission or misstatement judged in thesurrounding circumstances. The size or nature of the item, or a combination of both, couldbe the determining factor.”

The former Australian Accounting Standard AASB 1031 Materiality, withdrawn for reporting periodscommencing on and after 1 January 2014, provided quantitative quidelines for assessing whetheran amount was material:-

15 Quantitative thresholds used as guidance for determining the materiality of theamount of an item or an aggregate of items shall, of necessity, be drawn atarbitrary levels. Materiality is a matter of professional judgement influenced by thecharacteristics of the entity and the perceptions as to who are, or are likely to be,the users of the financial statements, and their information needs. Materialityjudgements can only be properly made by those who have the facts. In thiscontext, the following quantitative thresholds may be used as guidance in consid-ering the materiality of the amount of items included in the comparisons referred toin paragraph 13 of this Standard:(a) an amount which is equal to or greater than 10 per cent of the appropriate

base amount may be presumed to be material unless there is evidence orconvincing argument to the contrary; and

(b) an amount which is equal to or less than 5 per cent of the appropriatebase amount may be presumed not to be material unless there isevidence, or convincing argument, to the contrary.

In withdrawing AASB 1031, the Australian Accounting Standards Board “noted that it would notexpect the withdrawal to change practice regarding the application of materiality in financialreporting.”

Prepared for the Local Government Association of South Australia.ge 2 INTRODUCTION

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

CO

NTE

NTS

PA

GE

SOU

TH A

UST

RA

LIA

MO

DEL

FIN

AN

CIA

L S

TATE

MEN

TS 2

016

Acordingly, Councils may continue to apply the former guidelines, as shown above, in assessingmateriality for disclosures in the Annual Financial Statements.

CONTENTS PAGEIt is recommended that a Contents page be provided as a convenience to users.

SA MODEL COUNCIL

General Purpose Financial Reportsfor the year ended 30 June 2016

TABLE OF CONTENTSPage

Council Certificate 1

Principal Financial Statements

Statement of Comprehensive Income 2

Statement of Financial Position 3

Statement of Changes in Equity 4

Statement of Cash Flows 5

Notes to, and forming part of, the Principal Financial Statements

Note 1 - Significant Accounting Policies N1

Note 2 - Income N7

Note 3 - Expenses N10

Note 4 - Asset Disposal & Fair Value Adjustments N12

Note 5 - Current Assets N13

Note 6 - Non-Current Assets N14Note 7 - Infrastructure, Property, Plant & Equipment

& Investment PropertyN15

Note 8 - Liabilities N18

Note 9 - Reserves N19

Note 10 - Assets Subject to Restrictions N20

Note 11 - Reconciliation of Cash Flow Statement N21

Note 12 - Functions N22

Note 13 - Financial Instruments N24

Note 14 - Expenditure Commitments N26

Note 15 - Financial Indicators N27

Note 16 - Uniform Presentation of Finances N28

Note 17 - Operating Leases N29

Note 18 - Superannuation N30

Note 19 - Interests in Other Entities N31

Note 20 - Discontinued Operations and Non-Current Assets held for sale N32

Note 21 - Assets & Liabilities not Recognised N33

Note 22 - Events Occurring After Reporting Date N34

Audit Report - Financial Statements

Audit Report - Internal Controls

Council Certificate of Audit Independence

Audit Certificate of Audit Independence

Prepared for the Local Government Association of South Australia.CONTENTS PAGE Page 3

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

Pa

CO

NTEN

TS PAG

ESO

UTH

AU

STRA

LIA M

OD

EL FINA

NC

IAL STA

TEMEN

TS 2016

The Annual Financial Statements are not complete unless the Council Certificate and Audit Reports(including independence certificates) are supplied. Annual Financial Statements should only besupplied bound or stapled as a complete set.

Numbering of Notes AASB 101.112-116 requires that the Notes, as far as practicable, be presented in a systematicmanner, and that items in the principal statements be cross-referenced to any related information inthe notes.

The example Notes have been numbered at the “macro” level in accordance with the main headingson the Statement of Comprehensive Income and Statement of Financial Position, with separatesections within these notes for the line items shown on those statements. The main numberingsequence is then continued for notes that deal with the Council as a whole2, before continuing withspecific items required by the standards relating to a line item within a note (which are also the notesthat are required by a lesser number of Councils).

It is intended that this will result in increased commonality of note numbers across Councils, whichwill facilitate cross-Council comparisons, and increased familiarity with the differing areas containedwithin the reports.

It is anticipated that most Councils will use Notes 1 to 19 inclusive, and that subsequent notes thatare used will be numbered consecutively.

Councils may choose to adopt another numbering sequence if desired. However, all notesshould be listed on the contents page.

Notes that would have NIL disclosure are not required to be supplied, and subsequent notes shouldbe renumbered.

Regional subsidiaries and other single purpose reporting entities will probably state theirpurpose in Note 1 (section 2 - the reporting entity) and dispense with Note 12, renumberingall subsequent notes. Regional subsidiaries and other single purpose reporting entitiesare also not required to supply Notes 15 & 16, and subsequent notes would also berenumbered.

Note DescriptionsCouncils may amend the descriptions of individual notes to more accurately reflect the content ofthe note as used by that Council.

Comparative FiguresAASB 101 defines a complete set of financial statements as:

10 A complete set of financial statements comprises: (a) a statement of financial position as at the end of the period; (b) a statement of comprehensive income for the period; (c) a statement of changes in equity for the period; (d) a statement of cash flows for the period; (e) notes, comprising a summary of significant accounting policies and otherexplanatory information; and (ea) comparative information in respect of the preceding period as specified inparagraphs 38 and 38A; and

2. i.e. Statement of Cash Flows Reconciliation, Financial Instruments, Expenditure Commitments and FinancialIndicators.

Prepared for the Local Government Association of South Australia.ge 4 CONTENTS PAGE

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

CO

UN

CIL

CER

TIFI

CA

TESO

UTH

AU

STR

ALI

A M

OD

EL F

INA

NC

IAL

STA

TEM

ENTS

201

6

(f) a statement of financial position as at the beginning of the precedingperiod when an entity applies an accounting policy retrospectively or makesa retrospective restatement of items in its financial statements, or when itreclassifies items in its financial statements in accordance with paragraphs40A-40D.

This requirement is in addition to the previous period comparatives required by paragraphs 38-44of the Standard. Consideration should also be given to providing the additional comparative infor-mation in the relevant Notes.

These additional comparative figures are not exampled in these Model Statements.

COUNCIL CERTIFICATEThe format of certification of the Annual Financial Statements is governed by Regulation 14 of theLocal Government (Financial Management) Regulations 2011.

The form of certification determined by the Minister under Regulation 14 is set out below:

An important consideration in locating Council’s Certificate at the head of the Annual FinancialStatements is that the legislation places the responsibility for preparing accurate statements uponthe Council, not the Auditor. The Auditor’s role is limited to forming and expressing an opinion asto whether those statements show a true and fair view of the matters reported. Accordingly, theCouncil’s Certificate prefaces the Annual Financial Statements, then the statements complete withnotes, then the Auditor’s Reports and the independence certificates.

Separately, the following procedures surrounding the certification process (which Councils are freeto adapt to meet their own requirements) are designed to integrate with Audit Committee require-ments in the legislation, and it is envisaged that they will operate in the following manner:

• Prior to the completion of the annual financial statements, the Council willauthorise the principal member of the Council and the Chief Executive Officer tosign the certification of the statements in their final form when completed.

• The officer responsible for preparing the financial statements, who may or may notbe the chief executive officer, will prepare draft statements for submission to theAudit Committee, and for external audit.

• The Audit Committee will review the draft statements to ensure that they presentfairly the affairs of the Council. This review will be conducted independently of theexternal audit. However, it is anticipated that the Audit Committee will have thebenefit of any information available (informal or otherwise) on particular mattersraised by the auditor up until the time of the review. Any suggested changes willbe provided to the officer responsible for preparing the statements.

• Following the external audit, the officer responsible for preparing the statementsand the auditor will propose any necessary amendments to the draft statements,which will be referred to the certifying officers for consideration.

• The certifying officers will review the proposed amendments to the draft state-ments and will either refer them to the Audit Committee for further consideration ormay, if satisfied that the proposed amendments are appropriate, complete anddate the certificate.

Prepared for the Local Government Association of South Australia.COUNCIL CERTIFICATE Page 5

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

Pa

CO

UN

CIL C

ERTIFIC

ATE

SOU

TH A

USTR

ALIA

MO

DEL FIN

AN

CIA

L STATEM

ENTS 2016

• The date of the certificate will be the date of authorisation for issue of the annualfinancial statements for the purpose of AASB 110 Events after the ReportingPeriod paragraph 17.

• As soon as practicable thereafter, the annual financial statements (including theaccompanying auditor's report and other certificates) will be sent to the LocalGovernment Grants Commission and will be tabled at an ordinary Councilmeeting.

SA MODEL COUNCIL

ANNUAL FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 June 2016

CERTIFICATION OF FINANCIAL STATEMENTS

We have been authorised by the Council to certify the financial statements in their final form. In our opinion:

the accompanying financial statements comply with the Local Government Act 1999, Local Government (Financial Management) Regulations 2011 and Australian Accounting Standards.

the financial statements present a true and fair view of the Council’s financial position at 30 June 2016 and the results of its operations and cash flows for the financial year.

internal controls implemented by the Council provide a reasonable assurance that the Council’s financial records are complete, accurate and reliable and were effective throughout the financial year.

the financial statements accurately reflect the Council’s accounting and other records.

…………………………………….(Insert name)

CHIEF EXECUTIVE OFFICER

……………………………………...(Insert name)

MAYOR/COUNCILLOR

Date:

Alternate wording for third dot point: “internal controls implemented by the Council provide a reasonable assurance that the Council’s financial records are complete, accurate and reliable and were effective throughout the financial year, with the exception of controls related to xxxx which will be improved during 20xx-xx.”

Prepared for the Local Government Association of South Australia.ge 6 COUNCIL CERTIFICATE

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

STA

TEM

ENT

OF

CO

MPR

EHEN

SIVE

IN

CO

ME

SOU

TH A

UST

RA

LIA

MO

DEL

FIN

AN

CIA

L S

TATE

MEN

TS 2

016

Shif tapam

Se9

STATEMENT OF COMPREHENSIVE INCOME

2016 2015Notes $'000 $'000

INCOMERates 2 5,734 5,431 Statutory charges 2 4,400 4,608 User charges 2 1,172 1,281 Grants, subsidies and contributions 2 2,032 1,334 Investment income 2 948 983 Reimbursements 2 2,273 1,595 Other income 2 728 691 Net gain - equity accounted Council businesses 19 101 395

Total Income 17,388 16,318

EXPENSESEmployee costs 3 5,824 5,710 Materials, contracts & other expenses 3 8,430 7,986 Depreciation, amortisation & impairment 3 3,546 1,488 Finance costs 3 389 598 Net loss - equity accounted Council businesses 19 174 48

Total Expenses 18,363 15,830

OPERATING SURPLUS / (DEFICIT) (975) 488

Asset disposal & fair value adjustments 4 624 874

Amounts received specifically for new or upgraded assets 2 85 141

Physical resources received free of charge 2 851 958

Operating result from discontinued operations 20 60 53

NET SURPLUS / (DEFICIT)

transferred to Equity Statement 645 2,514

Other Comprehensive IncomeAmounts which will not be reclassified subsequently to operating

result

Changes in revaluation surplus - infrastructure, property, plant & equipment

9 3,308 1,462

Share of other comprehensive income - equity accounted Council businesses

19 (33) 188

Impairment (expense) / recoupments offset to asset revaluation reserve

9 (279) -

Net assets transferred - Council restructure

Transfer to accumulated surplus on sale of revalued infrastructure, property, plant & equipment

- -

Amounts which will be reclassified subsequently to operating

result

Available-for-sale Financial Instruments - change in fair value

- -

Transfer to accumulated surplus on sale of available-for-sale Financial Instruments

- -

Total Other Comprehensive Income 2,996 1,650

TOTAL COMPREHENSIVE INCOME 3,641 4,164

This Statement is to be read in conjunction with the attached Notes.

SA MODEL COUNCIL

STATEMENT OF COMPREHENSIVE INCOMEfor the year ended 30 June 2016

own only here are plicable ounts.

e pages & 10.

Prepared for the Local Government Association of South Australia.STATEMENT OF COMPREHENSIVE INCOME Page 7

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

Pa

STATEM

ENT O

F CO

MPR

EHEN

SIVE IN

CO

ME

SOU

TH A

USTR

ALIA

MO

DEL FIN

AN

CIA

L STATEM

ENTS 2016

There is an expectation that no other line item descriptions will be used in the Statement ofComprehensive Income.

Details of the content of line items are given in the relevant notes below.

If a Council has no amounts in either the current or previous reporting period for any line item, itshould not be shown. If an amount is non-material, and a dissection is therefore not given in thesubsidiary Note, remove the Note cross-reference.

If there are no items of other comprehensive income, a line entitled “other comprehensiveincome”, with amounts of “0” in the value columns, must still be shown.

Impairment ExpenseThere is no mandatory requirement under the accounting standards that Impairment be separatelydisclosed on the face of the Statement of Comprehensive Income. These Model Statementsdisclose impairments of infrastructure, property, plant and equipment in Note 7, as permitted byAASB 136.128, and impairments of receivables through use of an allowance account, as permittedby AASB 139.63.

Where an asset that has previously been revalued is subsequently impaired, AASB 136.60-Aus61.1requires that the impairment loss is offset, through other comprehensive income, against the assetrevaluation reserve for that asset class, unless the reserve is exhausted (and the reverse, for therecoupment of an impairment loss - AASB 136.119-Aus121.1). For further commentary onimpairment, see "Impairment" on page 102 below.

In drafting the Statement of Comprehensive Income in the format presented, a largenumber of matters were considered.• AASB 101 insists that a Statement of Comprehensive Income MUST be

presented, even if there is a separate Income Statement.

• The Statement of Comprehensive Income must show, as a minimum, the NetSurplus / Deficit, and each item of other comprehensive income individually.

• It is very likely that most Councils will only have ONE item of other compre-hensive income, viz revaluation transfer arising from revaluations of infra-structure, property, plant and equipment.

• Presenting a Statement with only 3 (or even 2) lines of information is notconsidered acceptable.

• Items of other comprehensive income that do not apply to a Council should notbe shown.

Prepared for the Local Government Association of South Australia.ge 8 STATEMENT OF COMPREHENSIVE INCOME

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

STA

TEM

ENT

OF

CO

MPR

EHEN

SIVE

IN

CO

ME

SOU

TH A

UST

RA

LIA

MO

DEL

FIN

AN

CIA

L S

TATE

MEN

TS 2

016

Discontinued OperationsAASB 5.32 defines a discontinued operation as “a component of an entity that either has beendisposed of or is classified as held for sale and:

(a) represents a separate major line of business or geographical area of operations;(b) is part of a single co-ordinated plan to dispose of a separate major line of business orgeographical area of operations; or(c) is a subsidiary acquired exclusively with a view to resale.

It does not include a “restructuring of a local government3”. As such, the occasions when this willapply to Councils are considered to be rare. AASB 5.33 imposes disclosure requirements whichare exampled in "Note 20 - NON-CURRENT ASSETS HELD FOR SALE" on page 169.

Other Comprehensive IncomeOther comprehensive income is defined in the revised Standard as4:

“Other comprehensive income comprises items of income and expense (includingreclassification adjustments) that are not recognised in profit or loss as required orpermitted by other Australian Accounting Standards.

The components of other comprehensive income include: (a) changes in revaluation surplus (see AASB 116 Property, Plant and Equipmentand AASB 138 Intangible Assets); (b) actuarial gains and losses on defined benefit plans recognised in accordance withparagraph 93A of AASB 119 Employee Benefits; (c) gains and losses arising from translating the financial statements of a foreignoperation (see AASB 121 The Effects of Changes in Foreign Exchange Rates); (d) gains and losses on remeasuring available-for-sale financial assets (see AASB139 Financial Instruments: Recognition and Measurement); and (e) the effective portion of gains and losses on hedging instruments in a cash flowhedge (see AASB 139). (f) gains and losses where assets and liabilities are transferred to a local governmentfrom another local government at no cost, or for nominal consideration, pursuant to legis-lation, ministerial directive or other externally imposed requirement (see AASB 3 BusinessCombinations paragraphs Aus 63.1 - Aus 63.9).

Items which have NIL amounts for current and comparative reporting periods should be omitted.Many Councils will not have any items of other comprehensive income to report in any givenreporting period. In this case, the amount “0” should be shown against the sub-heading othercomprehensive income and the detailed rows hidden. The totals NET SURPLUS / (DEFICIT) trans-ferred to Equity Statement and TOTAL COMPREHENSIVE INCOME must still be shown.

3. AASB 5.Aus2.44. AASB 101.7 Definitions; additional information relating to other comprehensive income is provided in

paragraphs 81 - 86 and 90 - 96 of the Standard.

OTHER COMPREHENSIVE INCOME MAY BE POSITIVE OR NEGATIVEIN AMOUNT.Both are termed other comprehensive income.

Prepared for the Local Government Association of South Australia.STATEMENT OF COMPREHENSIVE INCOME Page 9

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

Pa

STATEM

ENT O

F CO

MPR

EHEN

SIVE IN

CO

ME

SOU

TH A

USTR

ALIA

MO

DEL FIN

AN

CIA

L STATEM

ENTS 2016

Sub-classifications within Other Comprehensive IncomeAASB 101.82A requires that other comprehensive income be grouped into those that, in accordancewith other Australian Accounting Standards:

(a) will not be reclassified subsequently to profit or loss; and (b) will be reclassified subsequently to profit or loss when specific conditions are met.

The description of this grouping MUST be shown unless there are no items of other compre-hensive income. If Council has only one item of other comprehensive income, show only therelevant group.

Other Comprehensive Income - Equity accounted Council businessesThis item includes your Council’s share of all amounts shown below the Operating Surplus / (Deficit)in the Statement of Comprehensive Income of the joint venture / associated entity / regionalsubsidiary, including

• Asset disposal & fair value adjustments• Amounts received specifically for new and upgraded assets• Physical resources received free of charge• Operating result from discontinued operations

(All of the above show in the Accumulated Surplus column in theStatement of Changes in Equity.)

• Changes in revaluation surplus - infrastructure, property, plant & equipment(Shown in Asset Revaluation Reserve column.)

• Available-for-sale Financial Instruments - change in fair value(Shown in Available-for-sale Financial Instruments column.)

• Impairment (expense) / recoupments offset to asset revaluation reserve(Shown in Asset Revaluation Reserve column.)

• Transfer to accumulated surplus on sale of revalued infrastructure, property, plant& equipment

(Shown DR in Asset Revaluation Reserve; CR in Accumulated Surplus;Net NIL.)

• Transfer to accumulated surplus on sale of available-for-sale Financial Instru-ments

(Shown in Available-for-sale Financial Instruments column.)

Thus the line in the Statement of Changes in Equity for Other Comprehensive Income - JointVentures and Associates may have amounts in up to 3 different columns.

Council RestructuresCouncil restructures fall within the ambit of AASB 3 Business Combinations, particularly paragraphsAus 63.1 - Aus 63.9. Any gain or loss arising from the transfer “to a local government from anotherlocal government at no cost, or for nominal consideration, pursuant to legislation, ministerialdirective or other externally imposed requirement” (Aus 63.1) “shall be separately disclosed in thestatement of comprehensive income” (Aus 63.7).

A separate note must be included disclosing the assets and liabilities transferred (including classes)and the name of the transferring Council (Aus 63.6), and the note reference number shown.

Prepared for the Local Government Association of South Australia.ge 10 STATEMENT OF COMPREHENSIVE INCOME

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

STA

TEM

ENT

OF

FIN

AN

CIA

L PO

SITI

ON

SOU

TH A

UST

RA

LIA

MO

DEL

FIN

AN

CIA

L S

TATE

MEN

TS 2

016

Minority InterestsThere are a limited number of Councils whose interest in a joint venture / associated entity (e.g.regional subsidiary) is such that they are in a position of control. (For discussion and examplesof control, see "Note 19 - INTERESTS IN OTHER ENTITIES" on page 151 below.)In such cases the joint venture / associated entity must be consolidated into the financial state-ments. AASB 101.81B requires that the Council’s, and the non-controlling interest’s, share of theprofit or loss for the period, and of total comprehensive income must be shown.

In this case, a short summary should be shown at the foot of the Statement of ComprehensiveIncome:

STATEMENT OF FINANCIAL POSITIONDetails of the content of line items are given in the relevant notes below.

If a Council has no amounts in either the current or previous reporting period for any line item, itshould not be shown. If an amount is non-material, and a dissection is therefore not given in thesubsidiary Note, remove the Note cross-reference.

If your Council has applied an accounting policy retrospectively, or made a retrospectiverestatement of items in its financial statements, or reclassified items that affect the Statement ofFinancial Position, you must show an additional set of comparative figures - see "ComparativeFigures" on page 4 above. (Non-material reclassifications within a section of a Note, provided theydo not affect any amount transferred to the Statement of Financial Position may be exempted fromthis.) Where additional comparatives are shown, additional comparatives should also be shown forthe relevant section of the Note.

Share of Net Surplus / (Deficit)

Council $xxxx $xxxx

Minority Interest (or, non-controlling interest) $xxxx $xxxx $xxxx $xxxx

Share of other comprehensive income

Council $xxxx $xxxx

Minority Interest (or, non-controlling interest) $xxxx $xxxx $xxxx $xxxx

Total $xxxx $xxxx

In most of these instances the controlling Council has a majority equity share, and hence theterm minority interests has been retained here.

However, if your Council has control, but not majority equity share, use the term non-controlling interest instead.

Prepared for the Local Government Association of South Australia.STATEMENT OF FINANCIAL POSITION Page 11

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

Pa

STATEM

ENT O

F FINA

NC

IAL

POSITIO

NSO

UTH

AU

STRA

LIA M

OD

EL FINA

NC

IAL STA

TEMEN

TS 2016

2016 2015ASSETS Notes $'000 $'000

Current Assets

Cash and cash equivalents 5 3,791 3,712

Trade & other receivables 5 1,471 2,991

Other financial assets 5 1,445 3,504

Inventories 5 1,012 453

7,719 10,660

Non-current Assets held for Sale 20 836 822

Total Current Assets 8,555 11,482

Non-current Assets

Financial assets 6 1,016 1,212

Equity accounted investments in Council businesses 6 559 765

Investment property 7 1,538 1,588

Infrastructure, property, plant & equipment 7 246,632 238,046

Other non-current assets 6 2,784 2,591

Total Non-current Assets 252,529 244,202

Total Assets 261,084 255,684

LIABILITIES

Current Liabilities

Trade & other payables 8 4,195 3,400

Borrowings 8 1,529 1,047

Provisions 8 2,960 2,633

Other current liabilities 8 92 86

8,776 7,166

Liabilities relating to Non-current Assets held for Sale 20 44 36

Total Current Liabilities 8,820 7,202

Non-current Liabilities

Trade & Other Payables 8 270 251

Borrowings 8 6,001 6,153

Provisions 8 1,828 1,743

Liability - Equity accounted Council businesses 6 101 -

Other Non-current Liabilities 8 45 26

Total Non-current Liabilities 8,245 8,173

Total Liabilities 17,065 15,375

NET ASSETS 244,019 240,309

EQUITY

Accumulated Surplus 202,277 200,708

Asset Revaluation Reserves 9 39,398 36,402

Available for sale Financial Assets 9 81 81

Other Reserves 9 2,263 3,118

TOTAL EQUITY 244,019 240,309

SA MODEL COUNCIL

STATEMENT OF FINANCIAL POSITIONas at 30 June 2016

Prepared for the Local Government Association of South Australia.ge 12 STATEMENT OF FINANCIAL POSITION

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

STA

TEM

ENT

OF

FIN

AN

CIA

L PO

SITI

ON

SOU

TH A

UST

RA

LIA

MO

DEL

FIN

AN

CIA

L S

TATE

MEN

TS 2

016

Non-current assets held for saleAn asset may be classified under this heading in accordance with AASB 5 if:

• it is normally classified as a non-current asset, • its carrying amount will be recovered principally through a sale transaction rather

than through continuing use, • available for immediate sale in its present condition,• and its sale must be highly probable.

All elements must be satisfied5.

For practical purposes, it is suggested that for a sale to have been highly probable at balance date,by the time the accounts are being prepared a legally enforceable contract for sale would be inexistence.

Specific disclosure requirements apply - see AASB 101.54, AASB 5.41 - and these disclosures areexampled in "Note 20 - NON-CURRENT ASSETS HELD FOR SALE" on page 169 below.

Do not show this item - as asset or liability - if Council had no applicable amounts in either the currentor comparative reporting periods.

Investment propertyWhere a Council has investment property (see "Investment Property" on page 103 below fordefinition) it is required to be disclosed on the face of the Statement of Financial Position6. Councilswith no investment property do not show the item.

Liability - Equity accounted council businessesThe Accounting Standards do not provide for a line item of this nature, but the enabling legislationunder which some regional subsidiaries are established does not permit a Council to “walk away”from a negative equity situation, thus converting a provision to an actual liability. The matter isfurther discussed under "Note 19 - INTERESTS IN OTHER ENTITIES" on page 151 below.

ReservesThere are two basic types of reserves:

• Asset Revaluation Reserves arise in compliance with the accounting standards asa consequence of the disclosure of certain assets on the fair value basis.

• Reserves for future expenditure arise as a result of a formal resolution by Councilto set aside a portion of its resources for a specified future purpose. Appropriateuse of the reserves is discussed further in "Other Reserves" on page 119 below.

Accordingly, it is considered appropriate that the totals of the two types of reserves are separatelydisclosed in the Statement of Changes in Equity, and consequently on the face of the Statement ofFinancial Position.

5. AASB 5, paragraphs 6 - 8.6. AASB 101.54(b)

Prepared for the Local Government Association of South Australia.STATEMENT OF FINANCIAL POSITION Page 13

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

Pa

STATEM

ENT O

F CH

AN

GES IN

EQ

UITY

SOU

TH A

USTR

ALIA

MO

DEL FIN

AN

CIA

L STATEM

ENTS 2016

Minority InterestsFor those few Councils whose interest in a joint venture / associated entity (e.g. regional subsidiary)is such that they are deemed to be in a position of control, AASB 101.54(q) requires that total of theamounts attributable to the Council, and the minority interest, must be shown separately.

A short summary should be shown in the Equity section of the Statement of Financial Position:

STATEMENT OF CHANGES IN EQUITYMovements in Accumulated Surplus must always be shown. If a Council has no amounts in eitherthe current or comparative figures for a class of other comprehensive income, a type of reserve, ora line item, they should not be shown.

AASB 101.106A7 previously required that each item of other comprehensive income be shown inthe Statement of Changes in Equity, but now permits disclosure in the Notes. AASB 101.108requires that the balances of each class of other comprehensive income also be shown on theStatement of Changes in Equity. Thus, in the totals column, the Statement of Changes in Equitylargely duplicates the bottom section of the Statement of Comprehensive Income. The columns towhich the relevant movements are allocated are largely self-explanatory.

Other Comprehensive Income - equity accounted Council businessesThis item includes your Council’s share of all amounts shown below the Operating Surplus / (Deficit)in the Statement of Comprehensive Income of the joint venture / associated entity / regionalsubsidiary, including

EQUITY

Accumulated Surplus $xxxx $xxxx

Asset Revaluation Reserves $xxxx $xxxx

Available for sale Financial Assets $xxxx $xxxx

Other Reserves $xxxx $xxxx

Total Council Equity $xxxx $xxxx

Minority Interests $xxxx $xxxx

TOTAL EQUITY $xxxx $xxxx

7. 106 An entity shall present a statement of changes in equity showing in the statement: (a) total comprehensive income for the period, showing separately the total amounts attributable to owners of the

parent and to non-controlling interests; (b) for each component of equity, the effects of retrospective application or retrospective restatement recognised in

accordance with AASB 108; and (c) [deleted by the IASB] (d) for each component of equity, a reconciliation between the carrying amount at the beginning and the end of the

period, separately disclosing changes resulting from: (i) profit or loss; (ii) other comprehensive income; and (iii) transactions with owners in their capacity as owners, showing separately contributions by and distribu-tions to owners and changes in ownership interests in subsidiaries that do not result in a loss of control.

Prepared for the Local Government Association of South Australia.ge 14 STATEMENT OF CHANGES IN EQUITY

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

STA

TEM

ENT

OF

CH

AN

GES

IN

EQU

ITY

SOU

TH A

UST

RA

LIA

MO

DEL

FIN

AN

CIA

L S

TATE

MEN

TS 2

016

• Asset disposal & fair value adjustments• Amounts received specifically for new and upgraded assets• Physical resources received free of charge• Operating result from discontinued operations

(All of the above show in the Accumulated Surplus column in theStatement of Changes in Equity.)

• Changes in revaluation surplus - infrastructure, property, plant & equipment(Shown in Asset Revaluation Reserve column.)

• Available-for-sale Financial Instruments - change in fair value(Shown in Available-for-sale Financial Instruments column.)

• Impairment (expense) / recoupments offset to asset revaluation reserve(Shown in Asset Revaluation Reserve column.)

• Transfer to accumulated surplus on sale of revalued infrastructure, property, plant& equipment

(Shown DR in Asset Revaluation Reserve; CR in Accumulated Surplus;Net NIL.)

• Transfer to accumulated surplus on sale of available-for-sale Financial Instru-ments

(Shown in Available-for-sale Financial Instruments column.)

Thus the line for Other Comprehensive Income - Joint Ventures and Associates may have amountsin up to 3 different columns.

Other equity adjustments - equity accounted Council businessesSome Councils are involved in equity accounted operations where the equity share of the partici-pating Councils (and future contribution shares) are periodically adjusted based on a factor such aspopulation or use of a health service etc.

The change in Council share in the equity of the operation is recognised direct in Council’s equitystatement as part of Accumulated Surplus.

Council RestructuresCouncil restructures fall within the ambit of AASB 3 Business Combinations, particularly paragraphsAus 63.1 - Aus 63.9. Any gain or loss arising from the transfer “to a local government from anotherlocal government at no cost, or for nominal consideration, pursuant to legislation, ministerialdirective or other externally imposed requirement” (Aus 63.1) “shall be separately disclosed in thestatement of comprehensive income” (Aus 63.7).

A separate note must be included disclosing the assets and liabilities transferred (including classes)and the name of the transferring Council (Aus 63.6), and the note reference number shown.

Minority InterestsFor those few Councils whose interest in a joint venture / associated entity (e.g. regional subsidiary)is such that they are deemed to be in a position of control, AASB 101.106(a) requires that total ofthe amounts attributable to the Council, and the minority interest, must be shown separately.

To achieve this, 2 additional columns will need to be inserted between the Other Reserves andTOTAL EQUITY columns. The additional columns are entitled Total Council Equity and MinorityInterest respectively.

Prepared for the Local Government Association of South Australia.STATEMENT OF CHANGES IN EQUITY Page 15

SOUTH AUSTRALIAMODEL FINANCIALSTATEMENTS 2016

Pa

STATEM

ENT O

F CH

AN

GES IN

EQ

UITY

SOU

TH A

USTR

ALIA

MO

DEL FIN

AN

CIA

L STATEM

ENTS 2016

SA MODEL COUNCIL

Accumulated

Surplus

Asset

Revaluation

Reserve

Available for

sale Financial

Assets

Other

Reserves

TOTAL

EQUITY

2016 Notes $'000 $'000 $'000 $'000 $'000

Balance at end of previous reporting period 200,708 36,402 81 3,118 240,309

Adjustment due to compliance with revised Accounting

Standards-

Adjustment to give effect to changed accounting policies -

Restated opening balance 200,708 36,402 81 3,118 240,309

Net Surplus / (Deficit) for Year 645 645

Other Comprehensive Income

Gain on revaluation of infrastructure, property, plant &

equipment3,308 3,308

Available-for-sale Financial Instruments - change in

fair value-

Impairment (expense) / recoupments offset to asset

revaluation reserve(279) (279)

Transfer to accumulated surplus on sale of infrastructure,

property, plant & equipment- - -

Net assets transferred - Council restructure -

Transfer to accumulated surplus on sale of available-for-

sale Financial Instruments- -

Share of other comprehensive income - equity accounted

Council businesses(33) (33)

Other equity adjustments - equity accounted Council

businesses69 69

Transfers between reserves 855 (855) -

Balance at end of period 202,277 39,398 81 2,263 244,019

2015

Balance at end of previous reporting period 197,160 35,275 81 2,214 234,730

Adjustment due to compliance with revised Accounting

Standards-

Adjustment to give effect to changed accounting policies 1,403 1,403

Restated opening balance 198,563 35,275 81 2,214 236,133

Net Surplus / (Deficit) for Year 2,514 2,514

Other Comprehensive Income

Changes in revaluation surplus - infrastructure, property,

plant & equipment1,462 1,462

Available-for-sale Financial Instruments - change in

fair value- -

Impairment (expense) / recoupments offset to asset

revaluation reserve- -

Transfer to accumulated surplus on sale of infrastructure,

property, plant & equipment523 (523) -

Net assets transferred - Council restructure -