south african baseline study on financial...

TRANSCRIPT

Regional Dissemination Conference on Building Financial Capability

30-31 January 2013

Nairobi, Kenya

South African Baseline Study

on Financial Literacy

Lyndwill ClarkeHead: Consumer Education

Outline

• Why a baseline study

• Measurement challenges in SA

• From OECD Pilot to FSB Baseline (The Questionnaire)

• Study methodology (Sampling)

• Some Findings

• Findings per Domain

• How to use findings

• Way forward

2

3

Why a Baseline Study

• Develop and implement a survey of financial literacy of adults in South Africa consistent with emerging measurement best practice internationally

• Identifying potential needs and gaps and groups at risk

• Developing a composite financial literacy score for monitoring purposes

• Inform the elements of a National Strategy for SA

• OECD Financial literacy definition:

“a combination of awareness, knowledge, skills, attitude and behaviours necessary to make sound financial decisions and ultimately achieve

individual financial wellbeing”

4

• Heterogeneous Middle Income Country (MIC) with one of world’s highest income inequality levels

– apartheid history and inequality of opportunity

• Trends in International Mathematics and Science Study (TIMSS) 2003: South African students’ maths and sciences scores ranked lowest of 50 countries surveyed (Reddy 2006)

Measurement Challenges in SA

68 60

36 3511 19

4 30

20406080

100Poverty level, 2008 (%)

South African average poverty headcount (54%)

First and third world economies in SA

Poverty: 54% below national poverty line in 2008; large disparities by race (Leibbrandt et al. OECD 2010)

Labour market: vast inequalities that characterize both access to and the quality of employment.

Unemployment : 24% (Q4, 2010) – 28% (black) vs. 6% (white)

From Pilot to Baseline Study

Behaviour9 Q

Keeping track of money

Making ends meet

Choosing and using products

Short and long term planning

Knowledge8 Q

Simple and compound

interest

Inflation-time value of

money

Risk and return

Risk diversification

Attitudes4 Q

Propensity to save vs

spend

Time preference (present vs

future)

Risk preference

(explanatory variable)

Financial inclusion

Awareness of products

Holding and using

products

Savings habits

Socio-demographic information

Age

Gender

Education

Work

Income

5

OECD Questionnaire Content

FINANCIALCONTROL

8(23)

FINANCIAL PLANNING

5(18)

PRODUCTS CHOICE

12(63)

FINANCIAL KNOWLEDGE

8 (35)

Questionnaire Transformation

BEHAVIOUR

9

ATTITUDE

4

KNOWLEDGE

8

FINANCIAL INCLUSION

FINANCIAL CONTROL

23Q

Personal Money

Management

Meeting Financial

Needs

Household Budgets

Long-term Financial

Goals

FINANCIAL PLANNING

18 Q

Financial Reserve Funds

Emergency Financial Planning

Propensity to Save vs Spend

Retirement Planning

PRODUCTS CHOICE

63 Q

Awareness of Products

Holding Products

Choosing and Using products

Selecting Advice Givers

FINANCIAL KNOWLEDGE

35 Q

Simple and Compound

Interest

Inflation-time Value of Money

Risk, Diversification

and Return

Self-Rated Knowledge

SOCIO-DEMOGRAPHIC

Age

Rural/Urban

Living std.

Province

Language

Gender

Education

Work

Income

FSB Questionnaire Content

ANALYTICAL GUIDELINES FOLLOWED TO

CONSTRUCT THE INDEXFinancial control

• Q1; Q5; Q16-Q18; Q27; Q29; Q38 (8 Questions)

Financial planning

• Q19; Q32; Q35; Q36; Q70 (5 Questions)

Choosing products

• Q42-Q43;Q51-Q52;Q64-Q65;Q71-Q72;Q98-Q100; Q102 (12 Questions)

Financial Knowledge

• Q108-Q115 (8 Questions)

The theoretical conceptual framework used in this study was derived from the OECD which specifies certain questions to be used in order to be able to determine scores.

In measuring financial literacy in the various domains, certain questions had to be isolatedand included as core measures.

Each subgroups of question was converted to a 0-100 scale to enable the researchers to compare and plot findings of the various domains on a single platform.

www.fsb.co.za

Financial

Literacy

Financial

control

Financial

planning

Choosing

financial

products

Knowledge &

understanding

Baseline Study Domains

10

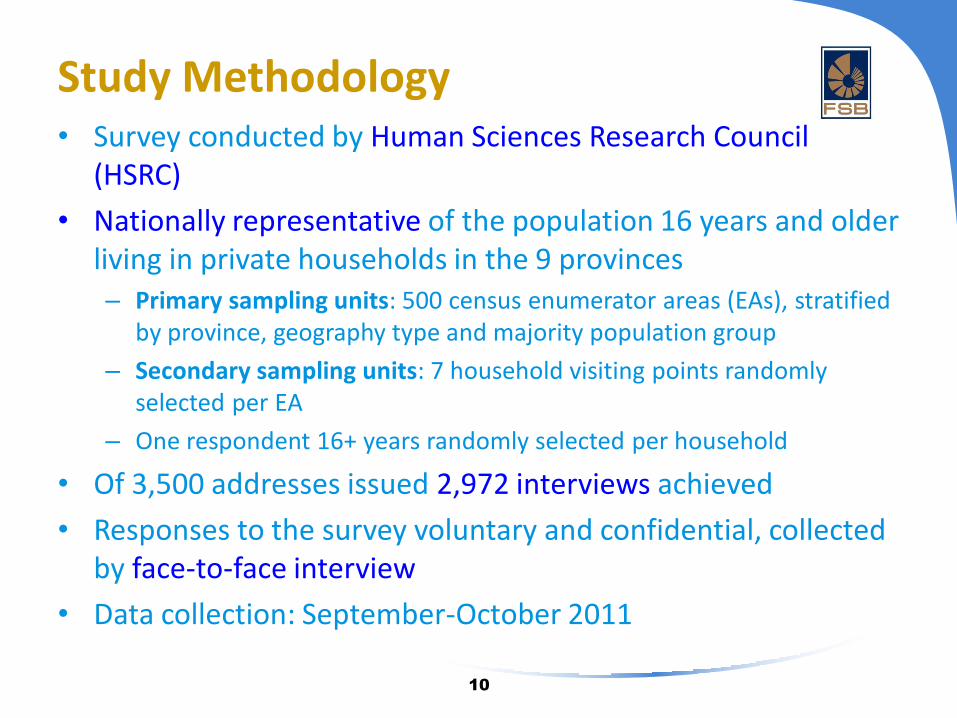

Study Methodology• Survey conducted by Human Sciences Research Council

(HSRC)

• Nationally representative of the population 16 years and older living in private households in the 9 provinces– Primary sampling units: 500 census enumerator areas (EAs), stratified

by province, geography type and majority population group

– Secondary sampling units: 7 household visiting points randomly selected per EA

– One respondent 16+ years randomly selected per household

• Of 3,500 addresses issued 2,972 interviews achieved

• Responses to the survey voluntary and confidential, collected by face-to-face interview

• Data collection: September-October 2011

11

Findings: Managing Money

Making ends meet

44% personally experienced income shortfalls in the previous year

Two common coping responses: borrowing from family/friends (57%); cutting back on spending or doing without (36%) – nominal reliance of financial products.

48% find it difficult to cover expenses and pay bills in a typical month.

Attitudes to saving and spending

South Africans have a broadly favourable view of their approach to financial management – tend not to make impulsive purchases, pay bills on time, closely watch personal finances.

36% experienced lack

of food to eat

39% went without

necessary medicine or treatment

38% no energy

source to cook food

12

Findings: Financial planning

Forms of savings in last year (multiple response):% of

cases

Saving cash at home or in your wallet 30%

Paying money into a savings account 26%

Building up a balance of money in your bank account 19%

Saving in a stokvel or other informal savings club 11%

Giving money to family to save on your behalf 9%

Buying financial investment products, other than pension funds

5%

Or saving in some other way (including remittances, buying livestock or property)

4%

None of the above 6%(Do not know) 17%(Refused to answer) 8%

Question producedconsiderable item

non-response

(25%)

Significant majority saved in at least

one type of savings instrument

those with no schooling

and rural residents

60% among those with low

living standards, low education

and rural dwellers.

13

Findings: Retirement Planning

2

10

2

1

2

3

3

4

6

8

9

10

13

23

33

48

0 20 40 60

(Refused)

(Don’t know)

Other

Sell financial assets

Sell non-financial assets

Drawing income from own business

Moving to a cheaper property in same…

Moving to a cheaper area

Use inheritance

Financial support from wider family

Financial support from spouse / partner

Financial support from children

Continue to work after retirement age

Personal retirement savings plan

Work-place pension

Government old age pension

Options included in financial plan for retirement (% of cases)

27% Relying on

family members

48%adults plan to

draw on a government

pension

13% recognise the need to work

beyond retirement age

24

2

2

2

3

3

3

9

9

5

13

6

10

12

6

6

11

12

10

12

29

45

1

33

38

38

41

41

42

42

47

48

49

49

51

51

55

62

65

68

72

72

76

86

0 10 20 30 40 50 60 70 80 90

None of the above

Unit trusts

Savings book at bank

Shares on stock exchange

Informal money guard

Home loan from big bank

Garage / petrol card

Retirement annuity

Investment / savings policy

Fixed deposit bank account

Debit card / Cheque card

Provident fund

Keep cash / savings at home

Current / Cheque account

Education policy / plan

Post Office savings account

Credit Card

Stokvel / savings club

Mzansi account

Pension fund

ATM card

Savings account

Heard of productsCurrently holds

14

Choosing savings and investment products

Awareness

Relatively good awareness of very basic bank products; low awareness of other formal products such as shares and unit trusts.

Significant respondents have banking products, but relatively low holding of other products

Product holding

15

Choosing insurance products

2

44

1

2

3

2

5

6

8

5

9

13

9

19

16

12

16

1

4

16

21

35

40

42

44

50

52

53

56

61

64

67

68

69

0 20 40 60 80

Don't know / Refused

None of the above

Funeral cover from any other source

Funeral cover from an spaza shop or stokvel

Insurance that pays your loan or borrowing when you die

Disability insurance or cover

Homeowners’ insurance on building or house structure

Funeral policy with a bank - including Post Bank

Funeral policy with an insurance company

Hospital cash plan

Household content insurance

Funeral cover through undertaker/funeral parlour

Cellphone insurance

Belong to a burial society

Medical aid scheme

Vehicle or car insurance

Life insurance or life cover

Heard of productsCurrently hold

40%of adult South

Africans have some form of funeral

insurance (formal or informal)

16

Financial AdviceNormal source of financial advice

• 26% ask friends

• 18% approach banks, 4% independent brokers, and 13% other financial advisors

• Large difference by living standard:

– Poor are more reliant on family, friends and informed community members.

Getting quality advice

• 65% report no problem getting relevant and good advice; 8% experience difficulty;

Recent advice from financial professional

• 78% did not seek professional financial advise in the last year

• 13% sought advice on savings /investments and 8% in relation to insurance.

35%ask professionals

18% do not ask anyone

for help

1 % In low LSM rely on

independent brokers compared to

27% in high LSMs

50% ask family members

17

Financial Control Domain

Someone with high financial control tends to be involved in daily financial decision-making processes, exhibits

careful approach to personal finances, prefers saving over spending money, and lives in a household that budgets

and is able to make ends meet.

18

Financial Control Domain Score - 58

0

10

20

30

40

50

60

70

80

MaleFemale

16-19 years20-29 years

30-39 years

40-49 years

50-59 years

60-69 years

70+ years

Black African

Coloured

Indian

White

Married (customary only)

Married (civil only)

Married (both customary & civil)

Widow/widower

Divorced/separated

Never married

Low living standard

Medium living standard

High living standardNo schooling

PrimarySome secondaryMatric or equivalent

TertiarySelf-employed (30 hours+/week)Self-employed (<30 hours/week)

Paid employment (30 hours+/week)

Paid employment (<30 hours/ week)

Looking for work

Looking after the home

Unable to work

Retired

Student

Not working, not looking

Urban formal

Urban informal

Rural, trad. auth. areas

Rural farms

Western Cape

Eastern Cape

Northern Cape

Free State

KwaZulu-Natal

North WestGauteng

MpumalangaLimpopo

Financial control South African avg. (M=58)

19

Financial Planning Domain

Someone with a high financial planning score tends to set financial goals and work hard to meet them, prefers to save for the long term and worries about tomorrow, has emergency funds in place and has managed to save recently (through a formal savings product or informal

means).

0

10

20

30

40

50

60

70

80Male

Female16-1920-29

30-3940-49

50-59

60-69

70+

Black African

Coloured

Indian

White

Married (customary only)

Married (civil only)

Married (both)

Widow/widower

Divorced/separated

Never married

Low living std.

Medium living std.High living std.

No schoolingPrimarySome secondary

MatricTertiarySelf-employed (30 hrs+/week)

Self-employed (<30 hrs/week)Paid employment (30 hrs+/week)

Paid employment (<30 hrs/week)

Looking for work

Looking after home

Unable to work (illness)

Retired

Student

Not working, not looking

Urban formal

Urban informal

Rural, trad auth areas

Rural farms

WC

EC

NC

FS

KZNNW

GPMP LP

Financial Planning South African avg. (M=53)

20

Financial Planning Domain Score - 53

21

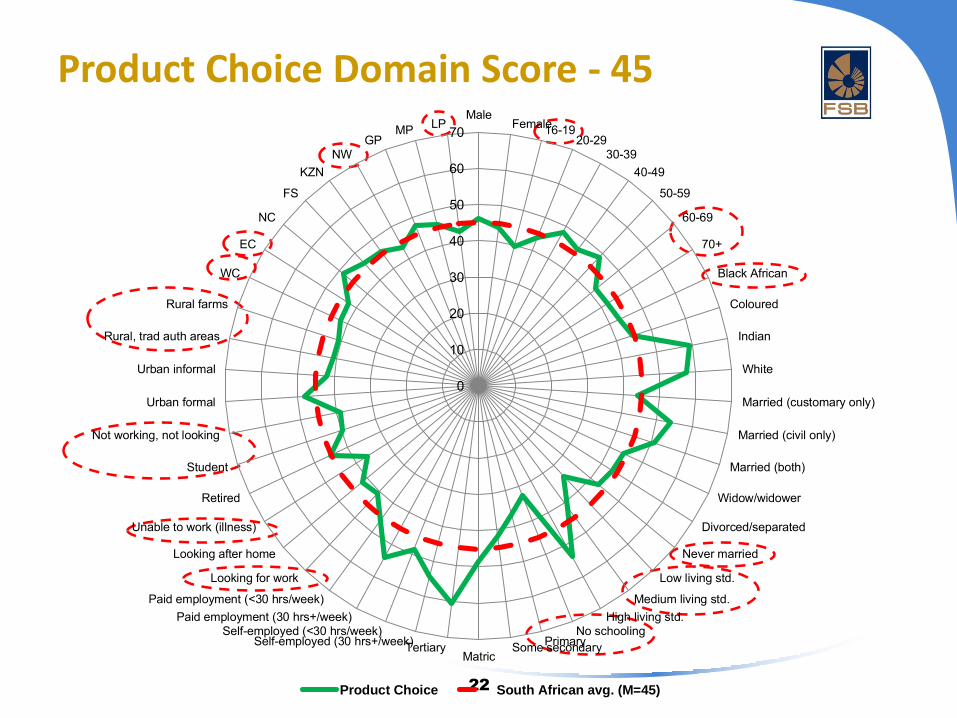

Product Choice Domain

A higher product choice score is given to someone ....

– with a broad awareness of different types of banking, credit/loan, savings and investment, and insurance products;

– holding at least one of each of the four product types mentioned above;

– who believes they have a clear understanding of their product needs and who undertakes detailed research before choosing a product;

– who has no regrets about recent financial product decisions (last year) and who has not taken an unsuitable product (last 5 years)

22

Product Choice Domain Score - 45

0

10

20

30

40

50

60

70Male

Female16-1920-29

30-3940-49

50-59

60-69

70+

Black African

Coloured

Indian

White

Married (customary only)

Married (civil only)

Married (both)

Widow/widower

Divorced/separated

Never married

Low living std.

Medium living std.High living std.

No schoolingPrimarySome secondary

MatricTertiarySelf-employed (30 hrs+/week)

Self-employed (<30 hrs/week)Paid employment (30 hrs+/week)

Paid employment (<30 hrs/week)

Looking for work

Looking after home

Unable to work (illness)

Retired

Student

Not working, not looking

Urban formal

Urban informal

Rural, trad auth areas

Rural farms

WC

EC

NC

FS

KZNNW

GPMP LP

Product Choice South African avg. (M=45)

23

Financial Knowledge and Understanding Domain

Someone with high financial knowledge and understanding has a familiarity with most or all of the basic financial concepts as well as

the concepts below:

– Basic mathematical division

– Effects of inflation

– Interest paid on loans

– Interest on deposits

– Compound interest

– Risk of high return investments

– Effects of inflation on cost of living

– Risk diversification

24

Knowledge and Understanding Domain Score - 56

0

10

20

30

40

50

60

70

80Male

Female16-1920-29

30-3940-49

50-59

60-69

70+

Black African

Coloured

Indian

White

Married (customary only)

Married (civil only)

Married (both)

Widow/widower

Divorced/separated

Never married

Low living std.

Medium living std.High living std.

No schoolingPrimarySome secondary

MatricTertiarySelf-employed (30 hrs+/week)

Self-employed (<30 hrs/week)Paid employment (30 hrs+/week)

Paid employment (<30 hrs/week)

Looking for work

Looking after home

Unable to work (illness)

Retired

Student

Not working, not looking

Urban formal

Urban informal

Rural, trad auth areas

Rural farms

WC

EC

NC

FS

KZNNW

GPMP LP

Knowledge & understanding South African avg. (M=56)

25

Overall Financial Literacy Score

0

10

20

30

40

50

60

70

80South Africa

Male Female16-19

20-2930-39

40-49

50-59

60-69

70+

Black African

Coloured

Indian

White

Married (customary only)

Married (civil only)

Married (both)

Widow/widower

Divorced/separated

Never married

Low living std.Medium living std.

High living std.No schooling

PrimarySome secondaryMatricTertiarySelf-employed (30 hrs+/week)

Self-employed (<30 hrs/week)Paid employment (30…

Paid employment (<30…

Looking for work

Looking after home

Unable to work (illness)

Retired

Student

Not working, not looking

Urban formal

Urban informal

Rural, trad auth areas

Rural farms

WC

EC

NC

FS

KZNNW

GPMP LP

Overall Financial literacy score Financial Control Financial Planning Product Choice Knowledge

26

Using the Financial Literacy Survey to help design tailored interventions

Example A: 16-19 year-olds

Higher than average knowledge domain score but lower than average on other three domains due to lifecycle effect

Need to make sure this cohort receives targeted financial education messaging through schools about…

…financial control and money management

…planning for the future

…making informed and appropriate product decisions

Ensure that bring about cohort effect that increases societal financial literacy and well-being over time

Equipping youth with financial knowledge and skills so that, as they make the transition into adulthood, they are able to make informed choices to improve their long-run financial well-being

Financial Literacy in SA

27

FINANCIAL

LITERACY

54

Financial

Control

58

Financial

planning

53

Choosing

financial

products

45

Knowledge &

understanding

56

28

Baseline Study & National Strategy

Financial Education Policy and Strategy: Risk-based approach Survey data and measures assist in evidence-based policy-making

by….

…identifying target groups

…helping to design initiatives tailored to these groups

Also assisted to:

Show which socio-demographic groups are being reached

Which messages are getting through to risk groups

Way forward Repeat every 5 years,

Annual monitoring using 35 core questions as part of South African Social Attitudes Survey (SASAS)