situation of the french photovoltaic market - … · situation of the french photovoltaic market ....

TRANSCRIPT

„Erneuerbare Energien in Frankreich“ Frankfurt – May 10, 2012

Situation of the French photovoltaic market photovoltaic market

Situation of the French photovolatïcmarket

1.1. Regulations governing the production of photovoltaïc energy in France

1.2 Current purchase tariffs

1.3 Keys points to be checked when purchasing a portfolio of

2

1.3 Keys points to be checked when purchasing a portfolio of solar roofs or plants

Véronique LagardeAvocat associé

Lefèvre Pelletier & Associés

1.1. Regulations governing the production of photovoltaïc energy in France : Main regulations

� Law of 10 february 2000 : Creates an obligation upon French electricity providers to purchase photovoltaïc electricity from producers(art. 10)

� The conditions to be met by producers are embodied in numerous

implementation decrees and orders, mainly :

3

�Decree of 7 september 2000 : Sets an « Autorisation/Declaration » regime�Decree of 6 december 2000 : Sets production caps (12MW for PV plants)�Decree of 10 may 2001 : Sets to conditions be met by an electricity producerto benefit from the « obligation d’achat » (mandatory purchase of electricity)�Decree of 13 march 2003 and decree and order of 23 april 2008 : Sets the conditions be met to connect to the PV electricity on the ERDF public network

� In 2011- 2012, this regime was simplified :� A single petition file triggers both a request to connect to the PV electricityon the ERDF public network and to sign a purchase contract with EDF OA

�« Autorisation/Declaration » regime suppressed for plants ≤ à 12 kW

1.2. Current purchase tariffs

� The purchase prices to be paid by electricity providers (EDF or others) to producers are set by orders

� The purchase prices dropped from approximatly 0,60€/Kwh (for intergrated PV roofs) in 2006 to 0,10€/Kwh

� Current tariff : Order of 4 March 2011

4

Current tariff : Order of 4 March 2011

� Alternatively, public tenders (where the price is proposed by bidders) are organized by the « Energy regulation commission -CRE »

� Next deadlines for energy producers willing to file a tender offer :

� Plants > 100kw < 250kw : 5 deadlines from 30/06/12 to 30/06/13

� Plants > 250kw : expired (February 8 , 2012)

1.3 Keys points to be checked when purchasing a portfolio of solar roofs or plants : Ensure that the conditions to benefit from the former purchasetariffs were/remain met

2006 tariff (order of 10 July 2006) subject to:

•Various conditions includingapproval of the « PTF » and payment of the first installmentbefore 11 January 2010•Petition for a purchasecontract filed before 1st

November 2009

5

2010 tariff (order of 12 January 2010) subject to:

• Full request for connection to the public network (as provided under article 3 of order of 12 January 2010) filed before 1st

September 2010 (Art. 8 order of 31 August 2010 )

1.3 Keys points to be checked when purchasing a portfolio of solar roofs or plants : Ensure that the conditions to benefit from the former purchasetariffs were/remain met (2)

2010 tariff (order of 31 August 2010)

Abrogation of order of 12 January 2010

Suspension order

No more purchase contract can be executed, save for files meeting the following

6

Suspension order « moratoire » (decree of 9 December 2010)

files meeting the following conditions :- Approval of the « PTF » before 2 December 2010- Plant to enter into service within 18 months from the approval of the PTF or 2 months further termination of connection works

1.3 Keys points to be checked when purchasing a portfolio of solar roofs or plants : Other main issues

� Criteria to benefit from the highest tariffs for “integrated” plants must be checked and are sometimes non easy to control (technical issues)

� The various authorizations (constructions permits, operating permits) may be granted to various legal entities (the developer, the seller) and not the propco to be purchased by the investor : these permits

7

and not the propco to be purchased by the investor : these permits may not be transferable to propco

� When transferable, the transfer is subject to prior agreement from the administration

� The rights over the pieces of land or the roofs where the plants will be build must be carefully checked

Contact

QUESTIONS /ANSWERS

8

Lefèvre Pelletier & associés136, avenue des Champs Elysées

75008 Paris

Tél : +33 (0)1 53 93 30 00Fax : +33 (0)1 53 93 30 30

Email : [email protected]

www.lpalaw.com

1.3 Keys points to be checked when purchasing a portfolio of solar roofs or plants : Other main issues

Cri

tère

s d’a

pplica

tion Le système PV est installé :

- sur la toiture d’un bâtiment clos (sur toutes les faces latérales) et couvert, assurant la protection des personnes, des animaux, des biens ou des activités - dans le plan de toiture

Le système PV remplace les éléments du bâtiment qui assurent le clos et couvert, et assure la fonction

Exce

pti

ons

Le système PV est installé sur un bâtiment clos (sur toutes les faces latérales) et clos, assurant la protection des personnes, des animaux, des biens ou des activités

9

Cri

tère

s d’a

pplica

tion

éléments du bâtiment qui assurent le clos et couvert, et assure la fonction d’étanchéité

Le démontage du module ou du film PV ne peut se faire sans nuire à la fonction d’étanchéité ou rendre le bâtiment impropre à l’usage

- si modules rigides : ils constituent l’élément principal d’étanchéité du système

- si modules souples : l’assemblage est effectué en usine ou sur site. Dans ce dernier cas, il doit faire l’objet d’un contrat de travaux unique

Exce

pti

ons

des biens ou des activités

Le système PV remplit au moins l’une des fonctions suivantes :

Allège ; Bardage ; Brise Soleil ; Garde corps de fenêtre, de balcon ou de terrasse ; Mur-rideau

Critères immobiliers seulement, d’autres critères tenant à la puissance et la localisation sont prévus à l’arrêté du 4 mars 2011

1.1. Cadre réglementaire de la production d’énergie solaire : Arrêté du 4 mars 2011 Critères d’intégration simplifiée au bâti *

Cri

tère

s d’a

pplica

tion

Le système PV est installé :

- sur la toiture d’un bâtiment assurant la protection des personnes, des animaux, des biens ou des activités- parallèle au plan de toiture E

xce

pti

ons

Le système PV est installé sur un bâtiment assurant la protection des personnes, des animaux, des biens ou des activités

Le système PV remplit au moins l’une des fonctions suivantes :

Allège ; Bardage ; Brise Soleil ; Garde corps de fenêtre, de balcon ou de terrasse ; Mur-rideau

10

Cri

tère

s d’a

pplica

tion

Le système PV remplace les éléments du bâtiment qui assurent le clos et couvert, et assure la fonction d’étanchéité

L’installation PV est continue et recouvre au moins l’ensemble du plancher haut du bâtiment donnant sur l’extérieur

L’installation PV protège l’ensemble du bâtiment du soleil et est étanche à l’eau

L’installation PV permet l’accès aux équipements et locaux techniques et à la maintenance de l’étanchéité

Critères immobiliers seulement, d’autres critères tenant à la puissance et la localisation sont prévus à l’arrêté du 4 mars 2011

Project Financing

Renewable Energies

Thursday 10 May 2012 – Frankfurt am Main

1. Renewable energies project financing

1.1. Project structuring

1.2. Banking audit

1.3. Term-sheet drafting and signing

2

1.3. Term-sheet drafting and signing

1.4. Finance and Security Documents drafting

Value of using project financing as part of a renewable energy project

Clients mostly structure renewable energy project financings as projectfinancing since those financings aim at:

� Obtaining other sources of capital

Sponsor do not usually have a large debt carrying capacity and usually, project companiesare unprofitable in the development phase of the project.

� Minimizing the amount of invested capital and increasing project profitabilitywith leverage

Sponsors usually invest between 10% and 30% in equity on a renewable energy project.

3

Sponsors usually invest between 10% and 30% in equity on a renewable energy project.

� Lengthening the duration of the funding.

� Sharing the risks and thus mitigate their impact.

� Avoid damaging the Sponsor’s balance sheet structure with a significant loan.

� Ensuring debt repayment through the operating cash flows which is doublysecured from the Bank’s perspective by (i) EDF’s power purchase obligation atcommissioning and (ii) the assignment by way of security to the Bank of theclaim held by the Borrower on EDF under the power purchase agreement.

Actors of the financing

� The Sponsor� The Project

company(the Borrower) - SPV

� Lenders(Banks)

� Technical Advisors� Lawyers� Insurers� The Contractor� Suppliers and

4

� Lenders(Banks)� The Arranger� The Agent� The Security Agent

� Suppliers and Subcontractors

� The Operator� ERDF and EDF (Agence

Obligation d’Achat)

� Administrative Authorities, as the case may be

Schedule for a Renewable Energy Project

Creation of a SPV

Due diligence

Grid connection request

Power Purchase Agreement request

(CODOA)

Draft of building contract

(usually EPC)

Drafts of suppliers contracts

Term sheet

The duration of the project is based on the power purchase agreement’s: 20 years

5

- Grid connection Agreement

- Operating Agreement

- Network Access Agreement

Facility Agreement and Inter-creditor Agreement

Hedging Agreement

- Operation and Maintenance Agreement

- Asset Management Agreement

Power Purchase Agreement

Finance Agreements

Project Agreements

“Power” Agreements

1.1. Project structuring

� Setting-up of the corporate structure

� Creation of an ad hoc company or use of a subsidiary

� Choice of the form of company

A joint stock company (société par actions simplifiée (SAS)) is usually used to set up a projectcompany (“special purpose vehicle” or “SPV”). However, many projects may have formerly beenheld by limited liability companies (sociétés à responsabilité limitée (SARL)) or more rarely bypartnerships (sociétés en nom collectif (SNC)).

6

� Necessary administrative and planning authorisations to theproject’s development and operation

� Common authorisation for most renewable energy project:

� Building permit (except for dams);� Operating authorisation (Autorisation d’exploiter) delivered by the Ministry1;� Power purchase certificate (Certificat ouvrant droit à l’obligation d’achat (CODOA))

delivered by the Direction Régionale de l’Environnement, de l’Aménagement et du Logement(DREAL) ;

� Grid connection request (Demande de raccordement) and ERDF’s technical and financialproposal (Proposition technique et financière (PTF)) duly accepted by the Borrower;

� Request for a power purchase agreement with an EDF OA receipt.

1Ministre délégué à l’Industrie – contact: Ministère de l’Écologie, de l’énergie, du développement durable et de l’aménagement du territoire -DGEC - Direction de l’énergie - Sous-direction des systèmes électrique et énergies renouvelables

1.1. Project structuring

� Additional administrative and planning authorisations to theproject’s development and operation

� Some additional environmental and urban planning authorisations orproceedings may be required, depending on the type of renewableenergy, the plant’s capacity and project’s location.

This may entail:

7

This may entail:

� Construction on a wind energy development area (ZDE) in the case of wind energyprojects,

� Compliance with “Classified installations” legislation (ICPE) – implying, among others,specific financial guarantees to ensure dismantling - in the case of wind energy andbiomass projects,

� impact studies (études d’impact) (a new regime is to enter into force on June 1st,2012) in the case for instance of wind energy projects, > 250 kWp ground solar energyprojects, private hydroelectric projects,

� public inquiries (enquêtes publiques) (a new regime is to enter into force on June 1st,2012) in the case for instance of wind energy projects, > 250 kWp ground solar energyprojects, private hydroelectric projects,

� Compliance with the water law regulation (loi sur l’eau).

1.1. Project structuring

� Agreements to be entered into for most renewable energy projects

� Land agreements

� Leases (preferably emphyteutic leases (baux emphytéotiques), more rarely civil leases oradministrative emphyteutic leases (baux emphytéotiques administratifs) under certaincircumstances).

� “Power” Agreements

� Grid connection agreement to be entered into with ERDF (Convention deraccordement)

8

raccordement)� Operating agreement to be entered into with ERDF (Convention d’exploitation)� Network access agreement to be entered into with ERDF (Contrat d’accès au

réseau (CARD))� Power purchase agreement to be entered into with EDF OA (Contrat d’achat)

� Project Agreements

� Building contracts (turnkey contract, EPC, property development contract (contrat depromotion immobilière), suppliers contract for solar panels, wind turbines, inverters,electrical equipment...)

� Operation and maintenance contract� Asset management contract� Insurance contracts

� Credit Agreements – see below in 1.4.

1.1. Project structuring

� Structure of the Project

SPV

Holding

Institutional InvestorsOther Shareholders

Banks(Lenders)

Sponsors

Contractor

Guarantees / Inter-creditors agreement

Securities

EPC or turnkey contract

9

Insurers

Sub-contractors

Distributor(ERDF)

Buyer(EDF OA)Managers

(Asset management contract)

Operation and maintenance

Administrative AuthoritiesSuppliers

Lessor

1.2. Banking audit

� Risks identified upstream – Risks identified by the Bank, during the audit and the drafting of the term-sheet (1/2)

� Works execution risk

� Sponsors undertake to deliver the work on a specific date under threat of financialpenalties.

� Indeed, securing EDF’s feed-in tariff implies that the plant must be built and connectedby a given date.

10

� The Bank must also assess the availability and capacity of the Contractor and thecompliance of the construction from a technical point of view in order to be able todeliver a given and guaranteed amount of power, together with the financial soundnessof the Contractor.

� Operational risk

� It is primarily subject to the conclusion of a long term power sale contract with apurchase obligation and guaranteed price with EDF Agence Obligation d’Achat (EDF OA).

� It is also subject to the project’s operational daily management which may entail theconclusion of an operation and maintenance agreement with a qualified external serviceprovider in the event the Sponsor does not hold adequate in-house resources.

� It is finally subject to the plant’s performance, guaranteed by the daily operationalmanagement on the one hand and the plant’s equipment on the other hand, which areunder a manufacturer guarantee provided by the suppliers.

1.2. Banking audit

� Risks identified upstream – Risks identified by the Bank, during theaudit and the drafting of the term-sheet (2/2)

� Financial and treasury risk

�Sponsors’ or financial institutions’ insolvency and non-coverage, through the funding, ofthe full costs of the project (including dismantling in the event of a wind energy project).

�Addressed by various types of clauses (restriction on the possibility to leave the project,change of control or dividend distribution to Sponsors), the syndication of the debt, the

11

change of control or dividend distribution to Sponsors), the syndication of the debt, theconclusion of hedging agreements, the obligation to form a cash reserve, the obligation forthe Sponsors to supply the SPV’s working capital or to grant subordinated loans or comfortletters, etc.

� Legal and political risk

�Legislative changes affecting the proceeding to benefit from the feed-in tariff or theproject’s taxation (moratorium, TEPA Act…),

�Changes in applicable environmental rules,

�Foreign law (mainly Chinese and German laws) governing the contracts which arenecessary to the project (inverters, wind turbines, solar panels supply contracts), etc.

1.2. Banking audit

� Prior technical studies (wind or sunshine studies made by specialised consulting firms)

� Insurance audit (during the construction phase: all risks policies (tous risques chantier and tous risques montage essai), public liability (responsabilité civile); and then during the operation phase: ten-year warranty, two-year warranty, damage to works insurance (dommage-ouvrage), property damage insurance (dommages aux biens) providing compensation to the replacement value of the plant, loss of operation insurance (perte d’exploitation) (12 months), public liability (responsabilité civile)).

� Legal audit which shall verify in particular :

� Validity and capacity of the borrowing project company and its guarantors;

� Protection of rights over land (type of lease);

12

� Protection of rights over land (type of lease);

� Finality, validity and regularity of necessary planning and administrative authorisations obtained:impact studies (études d’impact), public inquiries (enquêtes publiques) as the case may be to obtain abuilding permit, water law authorisation (autorisation loi sur l’eau), operating authorisation(autorisation d’exploiter), compliance with local development plan (PLU), construction on a windenergy development area (ZDE);

� “Power agreements” to secure the feed-in tariff: ERDF technical and financial proposal (PTF), gridconnection agreement, operation agreement and network access agreement (CARD) entered into withERDF, DREAL power purchase certificate (CODOA), power purchase agreement entered into with EDFOA;

� Project agreements (development agreement, property development contract, building contract,equipment supply agreement (modules, inverters, cables, wind turbines…) and operation andmaintenance agreement) and warranties of those equipments;

� As the case may be, in the solar sector, impact of the moratorium, possibility to benefit from specificpremiums such as the prime d’intégration au bâti or the prime d’intégration simplifiée au bâti (forroof solar plant).

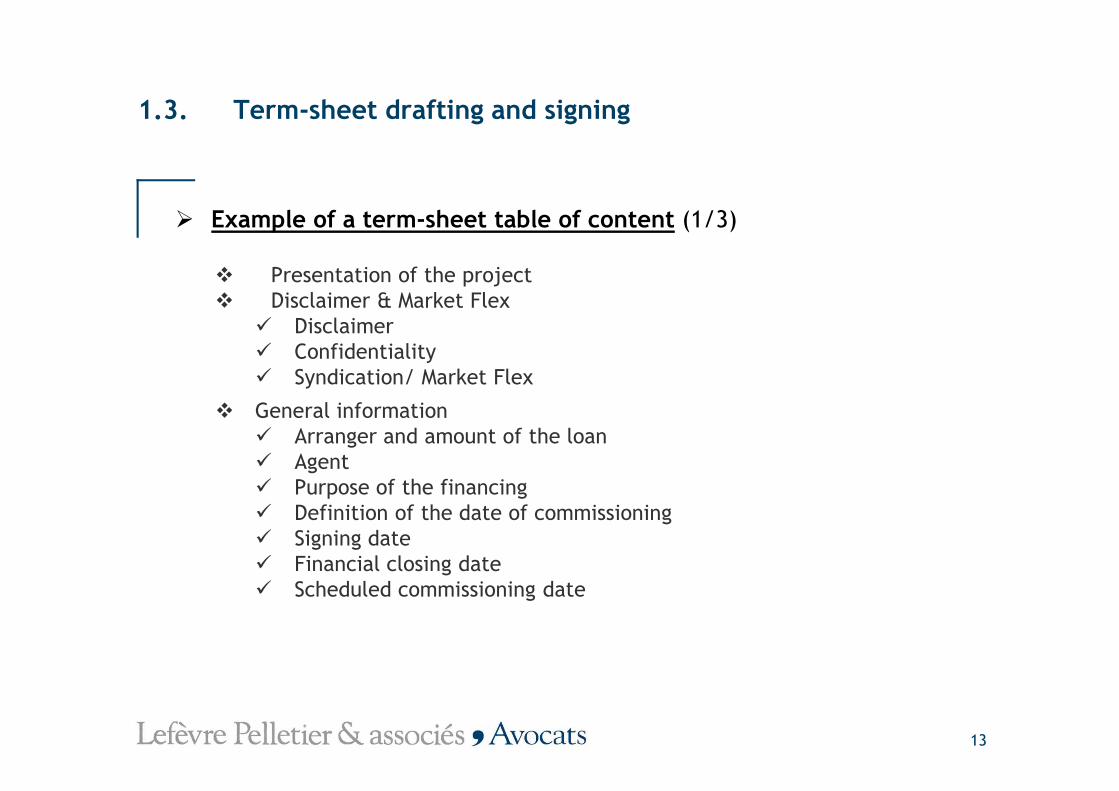

1.3. Term-sheet drafting and signing

� Example of a term-sheet table of content (1/3)

� Presentation of the project� Disclaimer & Market Flex

� Disclaimer� Confidentiality� Syndication/ Market Flex

13

� General information� Arranger and amount of the loan� Agent� Purpose of the financing� Definition of the date of commissioning� Signing date� Financial closing date� Scheduled commissioning date

1.3. Term-sheet drafting and signing

� Example of a term-sheet table of content (2/3)

� Key financial information� Project cost� Equity� Total investment cost� Amount of the loan� Loan instalments� VAT loan

14

� VAT loan

� Loan stipulation� Reimbursement� Interest rate

� Guarantees� Securities

� Margin and fees� Margin� Administration fee� Commitment fee� Arrangement fee

1.3. Term-sheet drafting and signing

� Example of a term-sheet table of content (3/3)

� Required documents� Project documents� Financial documents

� Condition precedent or subsequent

� Terms and conditions� Project financial statements

15

� Project financial statements

� Project proceeds allocation

� Consultants

� Hedging in compliance with standard market practice at closing date

� Covenants in compliance with standard market practice

� Representations and warranties

� Event of Default

� Language, applicable law and offer expiry date

1.3. Term-sheet drafting and signing

� Renewable energy project term-sheet structure (1/5)

The structure of a renewable energy project term-sheet does not change whatever thenature of the project

�Presentation of the Project

16

�Presentation of the Project

� Actors of the project: shareholding structure, Sponsors and SPV Shareholders,project company.

� Kind of power plant: description of the equipment used (inverters, solar panels,wind turbines, insulation process for rooftop equipment).

1.3. Term-sheet drafting and signing

� Renewable energy project term-sheet structure (2/5)

�Legal and financial engineering

�Contractual engineering: land management, supply and installation of the plant,power purchase agreement, obligations relating to operation and maintenance andinsurance policies.

Banks get involved in the drafting of the construction contract since they require that asa minimum the following guarantees be provided for:

17

a minimum the following guarantees be provided for:

o a Bank guarantee for advance payment

o A Bank guarantee for good execution/good completion amounting up to 5% of theconstruction contract price.

�Financial engineering: project cost, funding, operating assumptions/ building of thebase case financial model, financing plan.

�Due diligences : Technical and insolation or wind second expert opinion, Insurances, Legaldocumentation and legal audit of the Project.

1.3. Term-sheet drafting and signing

� Renewable energy project term-sheet structure (3/5)

� Funding modalities (1/3)

� General definition: parties, project agreements and financial terms.

� Main clauses of Finance agreements:

o Terms and conditions: Facility amount, maturity, early repayment,consolidation date at commissioning, expiry date of the offer.

18

consolidation date at commissioning, expiry date of the offer.

o Funds availability under the commercial facility: funds availability date.

o Commercial credit repayment: amortization period of the loan, loanmaturity, fixed rate maturities and repayment of principal.

1.3. Term-sheet drafting and signing

� Renewable energy project term-sheet structure (4/5)

� Funding modalities (2/3)

o conditions precedent or subsequent

• Condition precedent to the signing of the credit facility: corporatedocuments, satisfactory audits (namely insurances) and legal opinion oncapacity.

• Condition precedent to the drawdown:

19

• Condition precedent to the drawdown:

• Signing of project agreements and securities, non withdrawal and nonclaim certificates with respect to administrative authorisations andbuilding permits, product guarantee certificates (minimum 2 yearsfor inverters, 5 years for solar modules) and performance certificate(minimum 80% over 25 years for solar modules, 97% over 15 to 20years for wind turbines), compliance with financial ratios and theaudit reports conditions, no event of default;

• Equity investment;

• Insurances: subscribed under the agreed scheme and allowingcreditors to receive direct compensation.

o Condition subsequent: failure to provide the grid connection agreement,the power purchase agreement, the operation and maintenance agreement,to subscribe to the insurances, to register a mortgage within 6 months.

1.3. Term-sheet drafting and signing

� Renewable energy project term-sheet structure (5/5)

� Funding modalities (3/3)

o Securities and Borrower’s and Shareholder’s undertakings

• securities,

• covenants (limitation of indebtedness, ownership stability, insurancepolicies…),

20

• credit of the debt service reserve account,

• conditions for distribution to the Shareholders after loan consolidation,

• operation and maintenance,

• waterfall,

• information undertakings,

• Payment of fees and costs and reports.

� Financial conditions: interest rate, commissions, fees and payment date fromthe commissioning date.

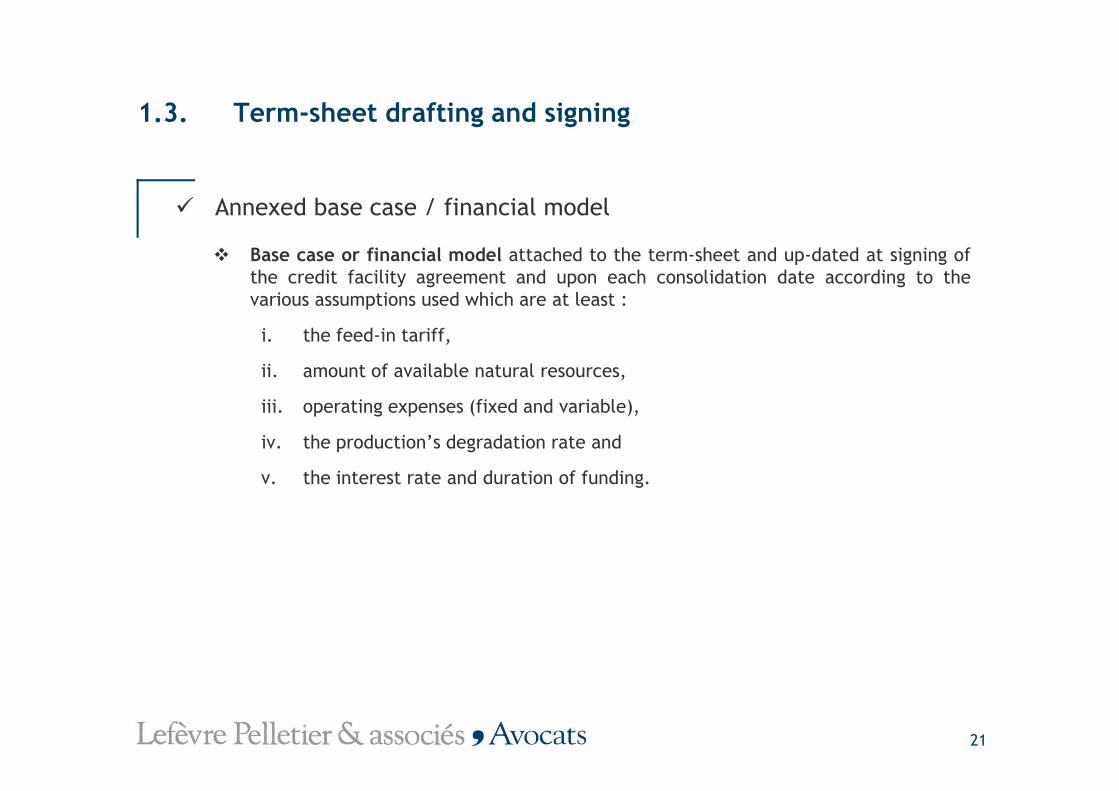

1.3. Term-sheet drafting and signing

� Annexed base case / financial model

� Base case or financial model attached to the term-sheet and up-dated at signing ofthe credit facility agreement and upon each consolidation date according to thevarious assumptions used which are at least :

i. the feed-in tariff,

ii. amount of available natural resources,

iii. operating expenses (fixed and variable),

21

iii. operating expenses (fixed and variable),

iv. the production’s degradation rate and

v. the interest rate and duration of funding.

1.3. Term-sheet drafting and signing

� Used ratios

Banks also rely mainly upon two ratios to assess the “Bankability” of theproject:

� Gearing ratio

Net debtEquity

22

It measures the debt ratio and thus the company’s financial structure risk(leverage), the higher it is, the more the company is considered to be at risk fromthe Lender’s perspective.

� Debt Service Coverage Ratio (DSCR) (110%-120% on average)

(EBITDA – Company Income Tax)Interests + capital amortization

It is a tool commonly used to assess the ability of a company to generate sufficientoperating margin to cover interests and principal and to define an acceptableminimum threshold for the Lender. The higher the ratio, the easier it is to obtain afinancing.

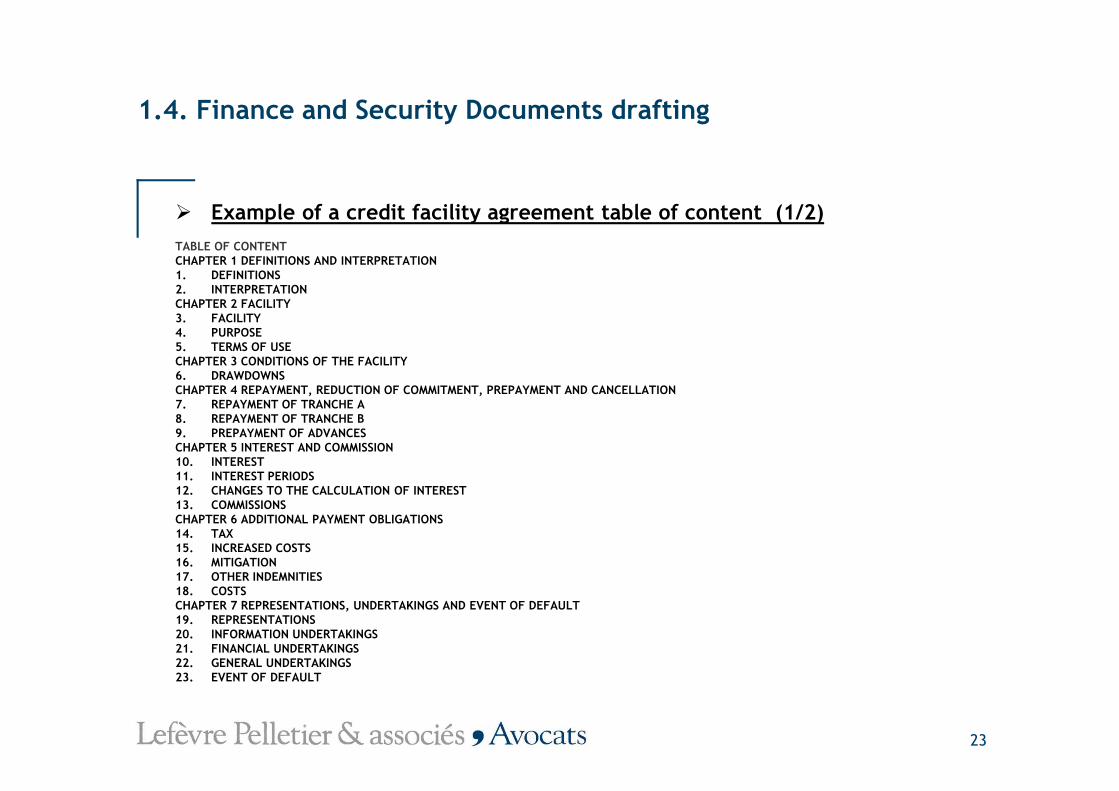

1.4. Finance and Security Documents drafting

� Example of a credit facility agreement table of content (1/2)

TABLE OF CONTENTCHAPTER 1 DEFINITIONS AND INTERPRETATION1. DEFINITIONS2. INTERPRETATIONCHAPTER 2 FACILITY3. FACILITY4. PURPOSE5. TERMS OF USECHAPTER 3 CONDITIONS OF THE FACILITY6. DRAWDOWNSCHAPTER 4 REPAYMENT, REDUCTION OF COMMITMENT, PREPAYMENT AND CANCELLATION

23

CHAPTER 4 REPAYMENT, REDUCTION OF COMMITMENT, PREPAYMENT AND CANCELLATION7. REPAYMENT OF TRANCHE A8. REPAYMENT OF TRANCHE B9. PREPAYMENT OF ADVANCESCHAPTER 5 INTEREST AND COMMISSION10. INTEREST11. INTEREST PERIODS12. CHANGES TO THE CALCULATION OF INTEREST13. COMMISSIONSCHAPTER 6 ADDITIONAL PAYMENT OBLIGATIONS14. TAX15. INCREASED COSTS16. MITIGATION17. OTHER INDEMNITIES18. COSTSCHAPTER 7 REPRESENTATIONS, UNDERTAKINGS AND EVENT OF DEFAULT19. REPRESENTATIONS20. INFORMATION UNDERTAKINGS21. FINANCIAL UNDERTAKINGS22. GENERAL UNDERTAKINGS23. EVENT OF DEFAULT

� Example of a credit facility agreement table of content (2/2)

CHAPTER 8 CHANGE OF PARTIES24. ASSIGNMENT AND TRANSFER BY THE BORROWER25. CHANGE OF LENDERSCHAPTER 9 THE AGENT, THE ARRANGER AND THE LENDERS26. THE AGENT’S SECURITY AGENT’S AND ARRANGER’S ROLE27. OTHER BUSINESS RELATIONSHIPS28. SHARING AMONG THE FINANCE PARTIESCHAPTER 10 FACILITY MANAGEMENT29. PAYMENT MECHANISMS30. SET-OFF31. NOTICES

1.4. Finance and Security Documents drafting

24

31. NOTICES32. CALCULATIONS AND CERTIFICATES33. PARTIAL INVALIDITY34. REMEDIES AND WAIVERS35. ADDITIONAL CLAUSESCHAPTER 11 APPLICABLE LAW AND POWER OF JURISDICTION36. APPLICABLE LAW37. POWER OF JURISDICTIONANNEX1 LENDERSANNEX 2 CONDITIONS PRECEDENTANNEX 3 FORM OF REQUESTANNEX 4 FORM OF TRANSFER AGREEMENTANNEX 5 TEMPLATE FINANCIAL RATIO CERTIFICATEANNEX 6 SECURITIESANNEX 7 AUTHORISATIONSANNEX 8 DESCRIPTION OF LAND RIGHTS AND EASEMENTSANNEX 9 LOAN AMORTIZATION SCHEDULEANNEX 10 WORKS SCHEDULE ANNEX 11 BASE CASE FINANCIAL MODEL

� Finance document drafting

� Long term commercial loan comprise several tranches and VATloan – Mostly a single contract that documents two contracts.

NB: The VAT loan is exclusively intended to finance the VAT payable by theBorrower under the building of the plant.

� Main clauses (1/5)

1.4. Finance and Security Documents drafting

25

� Main clauses (1/5)

o Terms and conditions of use of the facilities and drawdowns (cf. chapters 2 and 3)

Receipt of certain documents by the Agent, no occurrence of an event of default, accuracyof representations, achievement of equity contributions of the Borrower, satisfactoryconclusions of audit reports.

o Terms of repayment and prepayment of advances (cf. chapter 4)

Strict supervision of voluntary or automatic repayment terms - Start of repayment on the date of the plant’s commissioning, total early repayment in case of change of control of the Borrower and / or its Partner.Repayment of VAT tranche implies in particular the delivery of the copies of the requests for recovery of VAT from the Treasury.

1.4. Finance and Security Documents drafting

� Main clauses (2/5)

o Interest and Commission- Calculation of Interest (cf. chapter 5)

Method of calculating interest before and after consolidation date (generally EURIBOR plusthe margin and costs then fixed rate) and default interest (usually 3 months EURIBORincreased by up to 2% per year), generally quarterly interest period, compulsory display ofthe annual percentage rate (APR).

o Representations, undertakings and event of default (cf. chapter 7) (1/3)

• Reprensations on power and authority, authorizations needed to conduct theCompany’s business have been obtained, no collective proceedings, no litigations,

26

Company’s business have been obtained, no collective proceedings, no litigations,no other financial indebtness, no event of default, pari passu ranking.

• Information undertaking and namely to communicate technical follow-up andmonitoring of the realization of the works reports (Taking-over certificate andconsuel compliance certificate), reports and statements regarding the operationand maintenance, letter from ERDF on the commissioning and bailiff statementsregarding the commissioning.

• Financial undertakings regarding the compliance with the financial ratios and thefinance documents.

• General undertakings:

• Undertakings on the maintenance and compliance with the authorizations, thesuppliers’ instructions, the suppliers’ warranties and the maintenance of the plantas well as the equipment.

1.4. Finance and Security Documents drafting

� Main clauses (3/5)

o Representations, undertakings and event of default (2/3)

• Corporate undertakings in order to limit changes made in the articles ofassociation, to inform the Lenders in the event of a change of control whichwould not result in an event of default.

• Undertaking to subscribe insurances in accordance with the requirements of

27

Undertaking to subscribe insurances in accordance with the requirements ofthe insurance audit report:

• During the construction phase: civil liability insurance guaranteeing theBorrower in its capacity as owner, all-risks insurance guaranteeing theBorrower and the financial parties, minimum 12-month loss ofanticipated revenue guarantee.

• During the operation phase: civil liability insurance guaranteeing theBorrower in its capacity as operator, losses and damage to propertyinsurance (all risks excepting).

1.4. Finance and Security Documents drafting

� Main clauses (4/5)

o Representations, undertakings and event of default (3/3)

• Event of default:

Default, misrepresentation, cross default, dissolution, merger or demerger,insolvency or Bankruptcy proceedings, foreclosures, event having a materialadverse effect, new circumstances, market disruption event, no insurance,termination or significative reduction of a granted collateral, refusal to

28

termination or significative reduction of a granted collateral, refusal tocertify the financial statements, non compliance with the agreed ratios.

o Change of parties – Assignment and Transfer by the Borrower (cf chapter 8)

In most cases, non-assignability for the Borrower.

o The Agent, the Security Agent and the Arranger’s role (cf chapter 9)

o Payment Mechanisms (cf chapter 10)

Payment is made to the Agent. The Borrower, unlike the financial parties, refrainfrom performing any compensation.

1.4. Finance and Security Documents drafting

� The facility agreement also provides for other clauses:

Calculation of Agent fee, Arrangement fee, Commitment fee, Termination fee, additionalcosts.

� Attached to the facility agreement, are:

the list of the Lender and their undertakings, the list of conditions precedent to thesigning of the facility and drawdowns, form of request, form of transfer agreement, list ofrequired authorisations under the project, list of the securities and even the security

29

required authorisations under the project, list of the securities and even the securitydocuments, the loan amortization schedule and the base case financial model.

� Clauses in the facility agreement do not vary according to the type of project butrather according to the state of work at the moment of the signing of the facilityagreement and according to land rights protection.

1.4. Finance and Security Documents drafting

� Intercreditor AgreementSigned by the Financial Parties, the Shareholders and the Borrower. It contains the Shareholder’sagreement on distribution rules and describes the subordination undertakings of the Shareholders andthe Shareholders’ equity contributions and complementary contributions.

� Main clauses

o Subordination of claims held by the Borrower’s Shareholders (advances oncurrent account) in relation to those of the Lenders

30

o Authorized payments

Subject to the commissioning of the plant, to the compliance with the DSCR ratio, themaintaining of the debt service reserve account level and of the operation and maintenancereserve account level as the case may be, to the non occurrence of an event of default.

o Subordinated creditors’ undertaking to re-transfer to the Agent any sums whichwould have been unduly paid to them

o Default interests

o Representations and warranties

o Events of default referring to the facility agreement

� Intercreditors agreement clauses do not vary according to the type of project but ratheraccording to the Borrower’s Shareholders’ capacity (especially if those are individuals, it mayprove difficult to obtain a complementary contribution from them).

1.4. Finance and Security Documents drafting

� Hedging agreementalmost always imposed by Banks in order to protect the project company against an increase in theinterest rate which would diminish its cash-flows and could compromise its debt service. It takes theform of a swap between a fixed rate against a floating rate for at least part of the facility amount.This contract is structured by the Banks along the ISDA or FBF guidelines and models and takes the formof a confirmation which shall be subject to either of those framework agreements.

� Main clauses

o Notional amount

31

o Notional amount

o Fixed rate amount

o Floating rate amount

o Maturity

o Schedule

1.4. Finance and Security Documents drafting

� Granting of securities and warranties

� Securities on the project’s financial flows

� Assignment by way of securities (Dailly Assignment) (articles L.313-23 et seq. of theFrench Monetary and Financial Code) of the claims held by the Borrower:

o On EDF under the Power Purchase Agreement;

o Under the Development contract and the related Bank guarantees;

o On the contractor under the construction contract and the operation and

32

o On the contractor under the construction contract and the operation andmaintenance contract and the related Bank guarantees. The Bank ensures thatan advance payment first demand guarantee is granted to the Borrower in caseof delay in commissioning which could adversely impact the feed-in tariff or incase of the plant’s underachievement;

o On suppliers under the equipment guarantees they supplied;

o On public treasury (VAT claims).

� Delegation to the Lenders of all technical insurances taken out by the Borrower orassignment by way of security (articles L.313-23 et seq. of the French Monetary andFinancial Code) of the insurance benefits payable under the insurance contractsentered into by the Borrower as of their subscription (under the construction phaseand then during the operation phase of the plant, all site risks insurance).

1.4. Finance and Security Documents drafting

� Securities on the plant and its equipments

Regarding solar plant, there is a debate regarding the movable or immovable nature ofphotovoltaic panels. It seems that solar farms, organised compound occupying space anddurably attached to the ground, may be regarded as immovable by nature and bemortgaged. However, the costs of such a mortgage would be too significant.Therefore, since the panels may be dismantled and re-assembled without damaging thestructure and may thus be compared to movables, it is customary to use, despite therequalification risk:

33

� Non-possessory pledge (article 2333 of the French civil code) on the equipments(panels, inverters, transformers...). In this case, the Bank shall pay attention to anyreservation of title clause which may delay the pledge’s effective date;

� First ranking mortgage over rights in rem arising from emphyteutic leases, up to thepercentage or the totality of the cost of the plant or a pledge over a civil lease if theland rights are not secured by an emphyteutic lease.

1.4. Finance and Security Documents drafting

� Other types of securities commonly found in renewable energy projects

� Financial Instrument Account Pledge;

� Debt Service Reserve Account Pledge Agreement ie pledge to the benefit of theLenders over the Bank account into which are credited 6 months interest fromcommissioning by the Borrower, upon request of the Lenders;

� OPEX Account Pledge Agreement ie pledge to the benefit of the Lenders over the Bankaccount into which are credited for a given period of time (usually from the 4th year until

34

account into which are credited for a given period of time (usually from the 4th year untilthe 12th year from the consolidation date) all distributable profits, for the purpose ofreplacing any equipment;

� Borrower Share Pledge.

NB: A first demand guarantee may be requested from the Sponsor to guarantee the Borrower’s obligations under the facility agreement.

� Types of securities do not vary according to the type of project but rather accordingto the Borrower’s Shareholders’ capacity (especially if those are individuals, apersonal guarantee could be requested).

Contacts

Thank you for your attention. Please do not hesitate to contact us should you have any question

Christophe Jacomin / [email protected]

Lefèvre Pelletier & associés

136, avenue des Champs-Elysées75008 Paris

Tel: + 33 1 53 93 30 00Fax: + 33 1 53 93 30 30

www.lpalaw.com

36

Erneuerbare Energien in Frankreich -Neuigkeiten 2011-2012

Recht – Windparks

136 avenue des Champs-Elysées 75008 Paris - Tel. : +33 (0)1 53 93 30 00 – Fax : +33 (0)1 53 93 30 30 – www.lpalaw.com136 avenue des Champs-Elysées 75008 Paris - Tel. : +33 (0)1 53 93 30 00 – Fax : +33 (0)1 53 93 30 30 – www.lpalaw.com

Silke Nadolni, MRICS

Lefèvre Pelletier & associésSeminar 10. Mai 2012 in Frankfurt a. M.

Inhalt

1. Tendenz 2012 (neue Regierung)2. Bestandsaufnahme: Reformen in 20113. geltende Tarife 3. geltende Tarife 4. Baurecht

1. Projektfinanzierung

EPC Vertrag

General-Unternehmer

Betriebsführer O&M

WEA-Hersteller

Stromabnehmer (z.B. EDF)SPV

(Projekt-Kaufvertrag

O & M Vertrag

Stromkauf-Vertrag

3

Aktionäre / Ge-sellschafter

Bank

(Projekt-Gesellschaft)

Kaufvertrag Vertrag

Darlehen Eigenkapital

1. Projektfinanzierung

Die Finanzierung eines Projekts erfordert:

• Technische Prüfung des Projekts (Technical Due

Diligence)

• Wirtschaftliche Prüfung des Projekts / Cash- Flow-

4

Modell (Financial Due Diligence)

• Rechtliche Prüfung des Projekts (Legal Due Diligence)

1. Projektfinanzierung

Rechtliche Bedingungen:

I. Betreibergesellschaft/ SPVII. GrundstücksicherungIII. Sicherung des EinspeisetarifsIV. Sicherung des NetzanschlussesV. Erforderliche Genehmigungen

5

V. Erforderliche Genehmigungen

a. Baugenehmigungb. Betriebsgenehmigung (Industrieministerium)c. Neu : Betriebsgenehmigung für umweltgefährdende Anlagen

VI. WEA-Kaufverträge und Bauverträge/Generalunternehmerverträge

1. Projektfinanzierung

I. Betreibergesellschaft

• Konzentrierung aller Rechte, Verträge und Genehmigungen

• Wahl der Rechtsform: SARL oder SAS

• Eintrag im Handelsregister, Satzung

6

• Eintrag im Handelsregister, Satzung

• Unterschied zwischen beiden Rechtsformen

1. Projektfinanzierung

II. Grundstücksicherung (1)

• Grundstücksicherung in Form eines Erbpachtvertrages (bailemphytéotique) oder eines Baupachtvertrages (bail à construction)erforderlich (Vorvertrag: Pachtversprechen)

• Besonderheiten des Erbpachtvertrags öffentlichen Rechts:

7

• Besonderheiten des Erbpachtvertrags öffentlichen Rechts:Verwaltungsrechtlicher Erbpachtvertrag

1. Projektfinanzierung

II. Grundstücksicherung (2)

Pachtvertrag:� Betreibergesellschaft als Begünstigte� Kündigung des landwirtschaftlichen Pachtvertrags (so vorhanden)� Mindestvertragsdauer: Laufzeit der Finanzierung plus 2 Jahre� Klausel zufolge der der Pächter nach Ende des Pachtvertrags

8

� Klausel zufolge der der Pächter nach Ende des PachtvertragsEigentümer der Windenergieanlagen bleibt (gleich aus welchem Grundder Vertrag beendet wird)

� Während der Betriebsphase zu bildende finanzielle Garantien für denRückbau der Windenergieanlagen und die Wiederinstandsetzung desStandorts (Art. 34 des Gesetz Grenelle 2 sieht vor, dass diesefinanziellen Garantien bei Produktionsbeginn zu stellen sind)

� Zustimmung des Grundstückseigentümers zur Eintragung einerHypothek und zur Übertragung des Pachtvertrags auf einen Dritten

� Klauseln bezüglich der Finanzierung: Änderung oder Kündigung desPachtvertrags nur mit Zustimmung der Bank; Eintrittsrecht der Bank

� Eintragung der Pachtverträge ins Hypothekenregister

1. Projektfinanzierung

Dienstbarkeiten für Wege, Kabel,

Überhang

� Abschluss von Dienstbarkeitsvereinbarungen zugunsten der Betreiber-gesellschaft

� Veröffentlichung der Dienstbarkeitsvereinbarungen im Hypotheken-

9

� Veröffentlichung der Dienstbarkeitsvereinbarungen im Hypotheken-register

� Sicherung der kommunalen Wege durch Dienstbarkeitsverein-barungen, welche auf einen Beschluss des Gemeinderats hin vomBürgermeister erstellt werden, oder durch Genehmigungen für dieNutzung der kommunalen Wege

1. Projektfinanzierung

III. Einspeisetarif (1)

• Alte Projekte:Erteilung eines Kaufverpflichtungszertifikats (CODOA) vor dem 14. Juli2007 und Einhaltung der 12 MW- Grenze.

• Gegenwärtige Regelung:Das Windparkprojekt muss in einer ZDE liegen (Windvorragzone).

10

Das Windparkprojekt muss in einer ZDE liegen (Windvorragzone).

Neue Regelung bezüglich der Erteilung von Kaufver-pflichtungszertifikaten seit dem Erlass vom 6. März 2009.

Vollständiger Antrag auf einen Stromkaufvertrag zur Bestimmung desauf den Stromkaufvertrag anwendbaren Tarif.

Jährliche Indexierung des Strompreises ab Inbetriebnahme inAnwendung des Koeffizienten L.

1. Projektfinanzierung

III. Erlass vom 17.11.2008 bezüglich des Einspeiseta rifs für Strom aus Windenergie (in Kraft seit dem 29.12.2008)

Anwendbare Tarife für Onshore-Anlagen im französischen Festland Jährliche Referenzbetriebsdauer

Tarif für die 10 ersten Jahre (c€/kWh)

Tarif für die folgenden 5 Jahre

11

Referenzbetriebsdauer Jahre (c€/kWh) folgenden 5 Jahre (c€/kWh)

2.400 Stunden und weniger 8,2 8,2 Zwischen 2.400 und 2.800 Stunden

8,2 Lineare Interpolation

2.800 Stunden 8,2 6,8 Zwischen 2.800 und 3.600 Stunden

8,2 Lineare Interpolation

3.600 Stunden und mehr 8,2 2,8

1. Projektfinanzierung

IV. Sicherung des Netzanschlusses

• Sicherung des projektkonformen Netzanschlusses zugunsten der Betreibergesellschaft - PTF (Proposition technique et financière) (Leistung, WEA-Typ…)

• Fristgerecht akzeptierte und bezahlte PTF

12

• Netzanschlussvertrag

1. Projektfinanzierung

V. Genehmigungen (Baugenehmigung und Betriebsgenehm igung)

• Eine bestandskräftige Baugenehmigung zugunsten derBetreibergesellschaft für die Windenergieanlagen und dieÜbergabestation

• Eine Betriebsgenehmigung zugunsten der Betreibergesellschaft

13

• Gesetz Grenelle II :

Genehmigungsverfahren für umweltgefährdende Anlagen (ICPE) fürWindenergieanlagen von über 50 m Höhe

1. Projektfinanzierung

VI. Generalunternehmervertrag (Turn key)

• Spezifikation der Leistungsinhalte, der Garantien, derAbnahmemodalitäten und des Eigentumsübergangs

• Verzugsstrafen

• WEA- Kaufvertrag und Wartungsvertrag, Garantie der technischen

14

• WEA- Kaufvertrag und Wartungsvertrag, Garantie der technischenVerfügbarkeit, Garantie des Schallleistungspegels, Garantie derLeistungskennlinie („power curve guarantee“)

• Möglichkeit der Übertragung des Vertrags zugunsten der Bank

1. Projektfinanzierung

2. Teil: Sicherheitenverträge:

I. Hypothek

II. Verpfändung der WEA

III. Cession Dailly

15

IV. Verpfändung der Geschäftsanteile / Aktien und der Bankkonten

1. Projektfinanzierung

I. Bestellung von erstrangigen Hypotheken auf den Er bpachtvertrag oder den Baupachtvertrag

• Höhe der Hypothek

• Notarielle Form und Eintragung ins Hypothekenregister

• Vorteil des Baupachtvertrags:

16

• Vorteil des Baupachtvertrags:

Aufrechterhaltung der Hypothek bei vorzeitiger Kündigung desPachtvertrags

1. Projektfinanzierung

II. Verpfändung der Windenergieanlage

• Verpfändung in Form eines « gage sans dépossession »

• Rechtliche Qualifizierung der Windenergieanlage als bewegliches Gut

• Wenn die Betreibergesellschaft zum Zeitpunkt der Gewährung der

17

• Wenn die Betreibergesellschaft zum Zeitpunkt der Gewährung derFinanzierung nicht Eigentümerin der Windenergieanlage ist:Verpfändungsversprechen

• Formalität im Rahmen der Verpfändung:

Hinterlegung beim Gerichtsschreiber des Handelsgerichts

1. Projektfinanzierung

III. Abtretung gewerblicher Forderungen als Sicherheit („ CessionDailly“)

Abtretung der Forderungen aus den wesentlichen Projektverträgen:

• aus dem Stromkaufvertrag mit EDF

• aus dem Netzanschlussvertrag mit ERDF

• aus dem WEA-Kaufvertrag

18

• aus dem WEA-Kaufvertrag

• aus dem Generalunternehmervertrag

• aus dem Wartungsvertrag

• aus den Versicherungsverträgen oder dem Versicherungsauftrag

• aus dem technischen Betriebsführungsvertrag

• aus den Ansprüchen auf Umsatzsteuererstattung

1. Projektfinanzierung

IV. Verpfändung der Geschäftsanteile / Aktien und der Bankk onten

• Verschiedene Mechanismen je nach Gesellschaftsform derBetreibergesellschaft

– SARL: Verpfändung der Geschäftsanteile

– SAS: Verpfändung des Aktienkontos Eintragung insHandelsregister des Gesellschaftssitzes

19

Handelsregister des Gesellschaftssitzes

• Verpfändung der Bankguthaben

Kontakte

Lefèvre Pelletier & associésLefèvre Pelletier & associés

Partner

Denis Chardigny

Tel.: +33 (0)1 53 93 30 04

Email: [email protected]

Pascaline Déchelette Tolot

Tel.: +33 (0)1 53 93 30 07

Email: [email protected]

Olivier Ortega

Tel.: +33 (0)1 53 93 39 96

Email: [email protected]

Olivia Michaud

Tel.: +33 (0)1 53 93 29 33

Email: [email protected]

21

Philippe Lefèvre

Tel.: +33 (0)1 53 93 30 01

Email: [email protected]

Philippe Pelletier

Tel.: +33 (0)1 53 93 30 05

Email: [email protected]

Marie-Odile Vaissié

Tel.: +33 (0)1 53 93 30 03

Email: [email protected]

Véronique Lagarde

Tel.: +33 (0)1 53 93 29 42

Email: [email protected] Antonia Raccat

Tel.: +33 (0)1 53 93 29 31

Email: [email protected]

Deutsch-Französisches Team (legal)

Silke Nadolni

Tel.: +33 (0)1 53 93 30 00

Email: [email protected]

Deutsch-Französisches Team (tax)

22

Jacques-Henry de Bourmont

Tel.: +33 (0)1 53 93 30 00

Email: [email protected]

Guillaume Rubechi

Tel.: +33 (0)1 53 93 30 00 / +49 (0) 69 71 04 56 230

Email: [email protected]

23