situation and prospects for forest conservation€¦ · · 2005-02-25situation and prospects for...

TRANSCRIPT

iii

Foreword

The State of the World’s Forests (SOFO) provides information on the current status of the world’sforests, as the name implies, but also discusses recent major policy and institutional

developments, future directions in forestry and external influences on the sector. The purpose is tomake current, reliable and policy-relevant information available to policy-makers, foresters andother natural-resource managers, academics, the forest industry and civil society. In doing so, it ishoped that SOFO will help facilitate informed discussion and decision-making.

SOFO was conceived in 1994 in response to a growing demand for reliable information on theworld’s forests and the absence of periodic reports giving a global and comprehensive view offorestry. The FAO Forestry Department consequently undertook to publish such a report every twoyears. The first SOFO was published in 1995. It was followed by a more comprehensive edition in1997, which attempted to provide an overall view of the forest sector and to put forestry into alonger-term perspective by examining trends from 1970 to the present and by looking ahead to 2010.SOFO 1997 serves as a benchmark document. SOFO 1999 takes a different approach: it concentrateson significant events and developments of the last two years and focuses on a limited number ofselected topical issues meriting a more in-depth look.

SOFO 1999 examines developments in the sector from the perspective of sustainable forestmanagement. It sheds light on policy reforms, institutional developments, international conventions,economic changes and other factors affecting forests, forest resources and their provision of socialand environmental services. SOFO 1999 addresses several questions: Are the changes taking place inforestry today bringing the world’s forests closer to being sustainably managed? Do these changesincrease forests’ contribution to sustainable development? Are international initiatives to supportthis process helping to move the sector in the right direction?

Information is a theme that runs through this issue of SOFO. Information and its analysis are thebasis for accurate planning and appropriate policy-making. SOFO 1999 takes a closer look at theneed for different types of forest information, the scope of databases, national and internationalcapabilities to collect and analyse information and international efforts to make it more accessible.Other topics addressed by SOFO 1999 include changing sources of wood supply, increased people’sparticipation in forest planning and management, and formal and informal instruments forachieving sustainable forest management.

The FAO Forestry Department hopes that SOFO will succeed in increasing awareness of key issuesfacing the forest sector today and in providing readers with valuable information. We hope that thiswill contribute to national, regional and international efforts to work towards sustainable forestmanagement, and thus towards sustainable human development.

As with the previous two reports, readers are encouraged to send FAO their comments on SOFO1999. Additional or updated information that may be incorporated into SOFO 2001 would be mostwelcomed.

M. Hosny El-LakanyAssistant Director-GeneralFAO Forestry Department

v

Contents

Foreword iiiAcknowledgements viiExecutive summary viii

PART ISITUATION AND PROSPECTS FOR FOREST CONSERVATION

AND DEVELOPMENT

The status of forest resources 1Status of forest resources and recent developments in forest condition 1Status of efforts to assess global forest resources 5

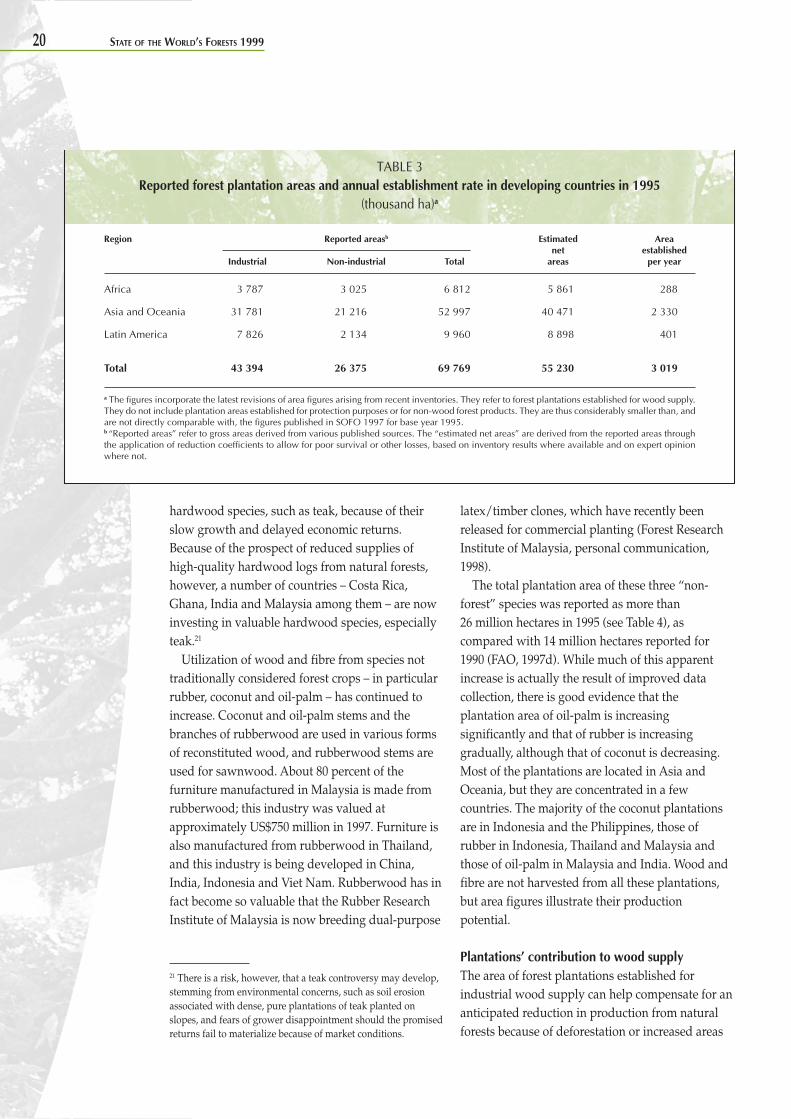

Status and trends in forest management 12Management of natural forests 12Forest plantations 19

Environmental and social services of forests 24The role of forest resources in fragile ecosystems 24Forests’ roles in mitigating global climate change 30

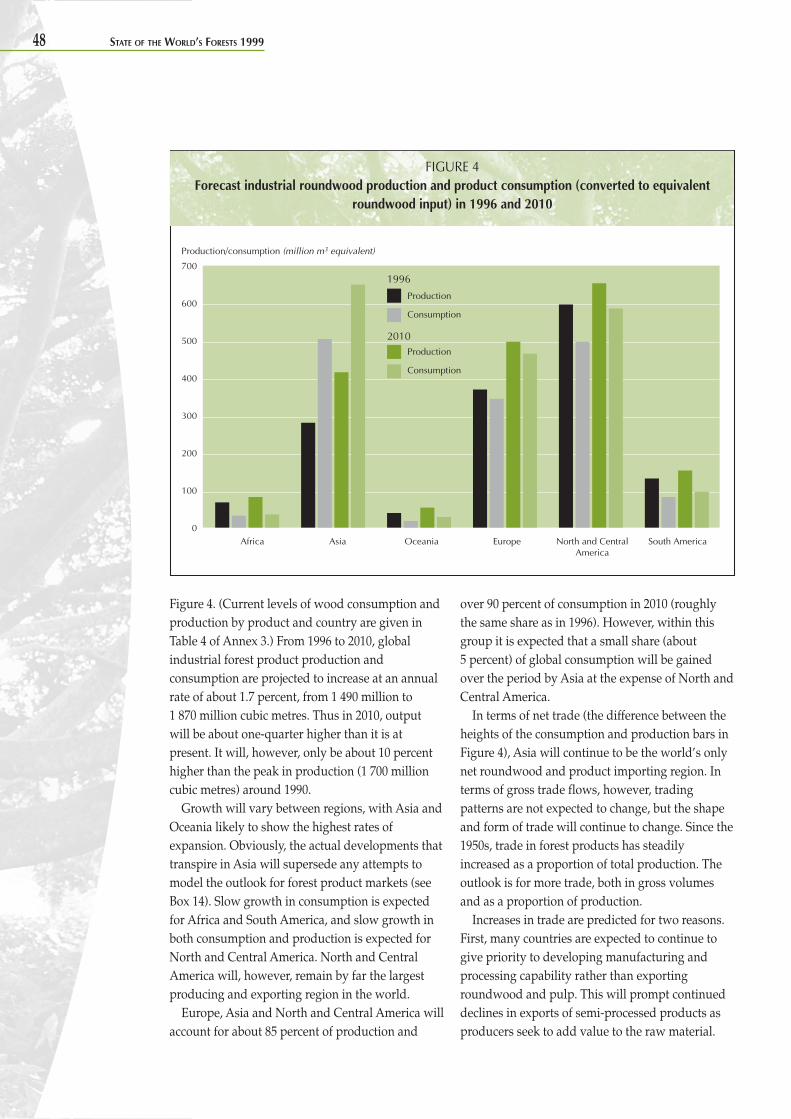

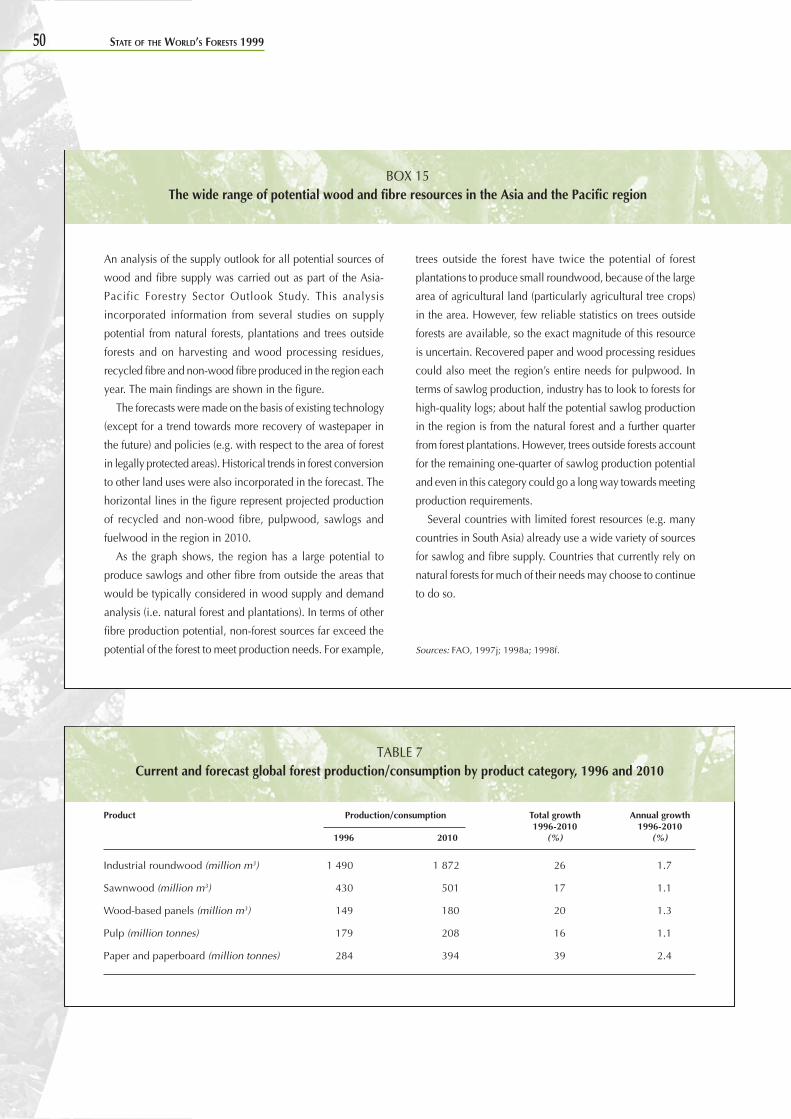

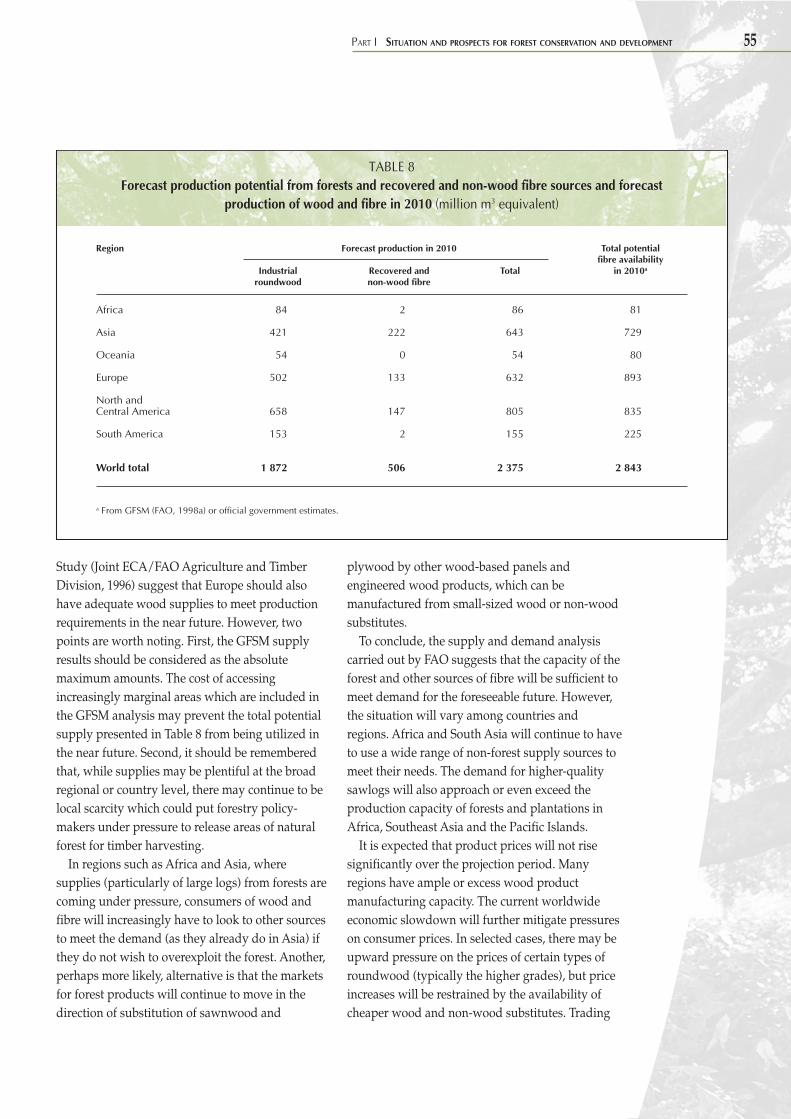

Global trends in forest products 34Non-wood forest products: a look at medicinal plants 35Contribution of woodfuels to the energy sector 37Trade in forest products: current issues and influences 40Future supply and demand for industrial roundwood and wood products 47

PART IIPOLICY, PLANNING AND INSTITUTIONAL ARRANGEMENTS

Issues in national forest planning, policy and legislation 61Developments related to national forest planning 61Recent policy issues 63Emerging trends in forest legislation 64

Evolving institutional framework 72New role and structure for forest administrations 72Effects of decentralization on forest management 73Trends in forestry research and technology transfer 76Preparing foresters for change: adapting education and training programmesto new demands 78

vi

PART IIITHE INTERNATIONAL DIALOGUE AND INITIATIVES ON FORESTS

UNCED follow-up: an update of the IPF/IFF process 81

Other global and regional initiatives in support of sustainableforest management 84Developments in international conventions and agreements 84Developments in criteria and indicators for sustainable forest management 86Other initiatives 88

Issues and options for international instruments to support sustainableforest management 92Background 92Analysis of the adequacy of legal instruments 93Identifying international forest issues 94Prerequisites for further progress 94Options for an international forest regime 95Some key questions for consideration 98

PART IVFORESTRY IN REGIONAL ECONOMIC GROUPS

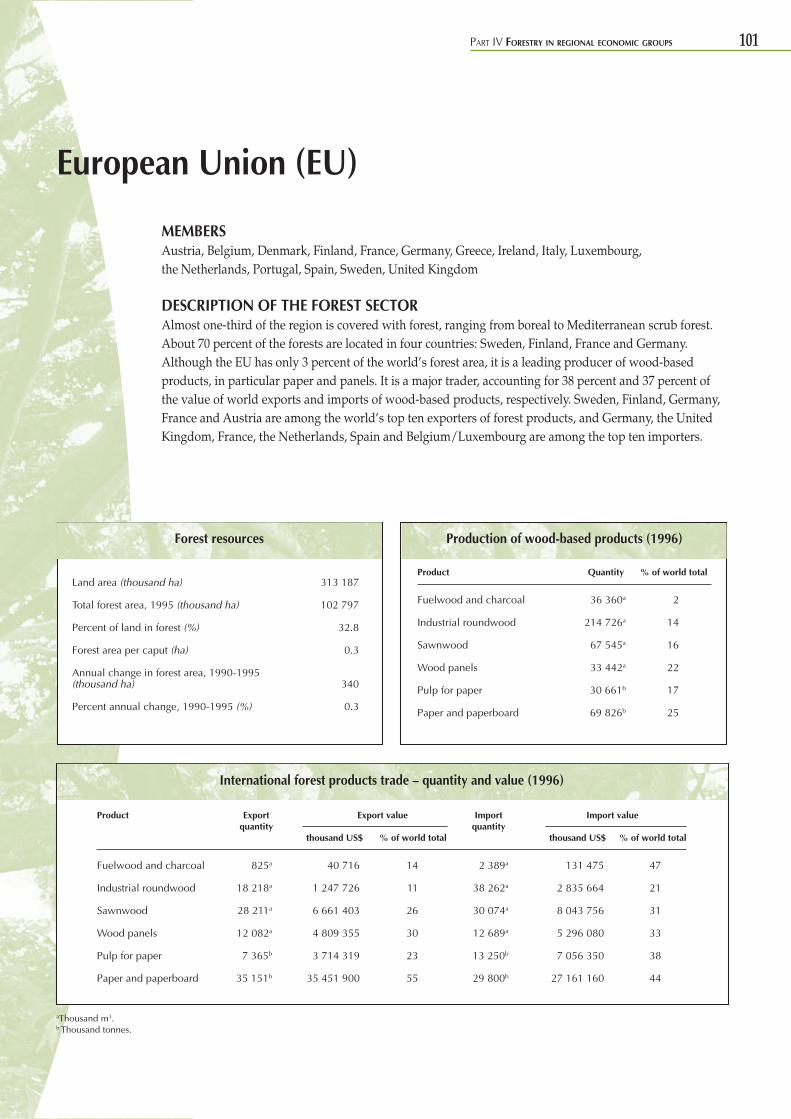

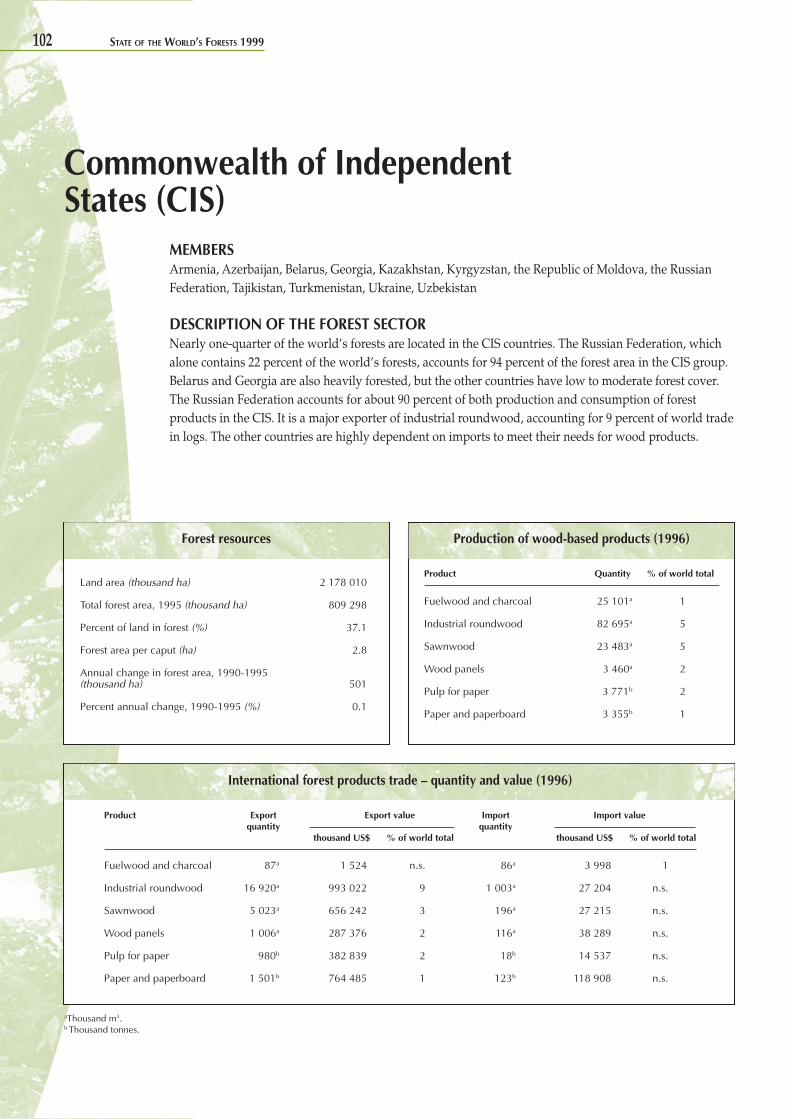

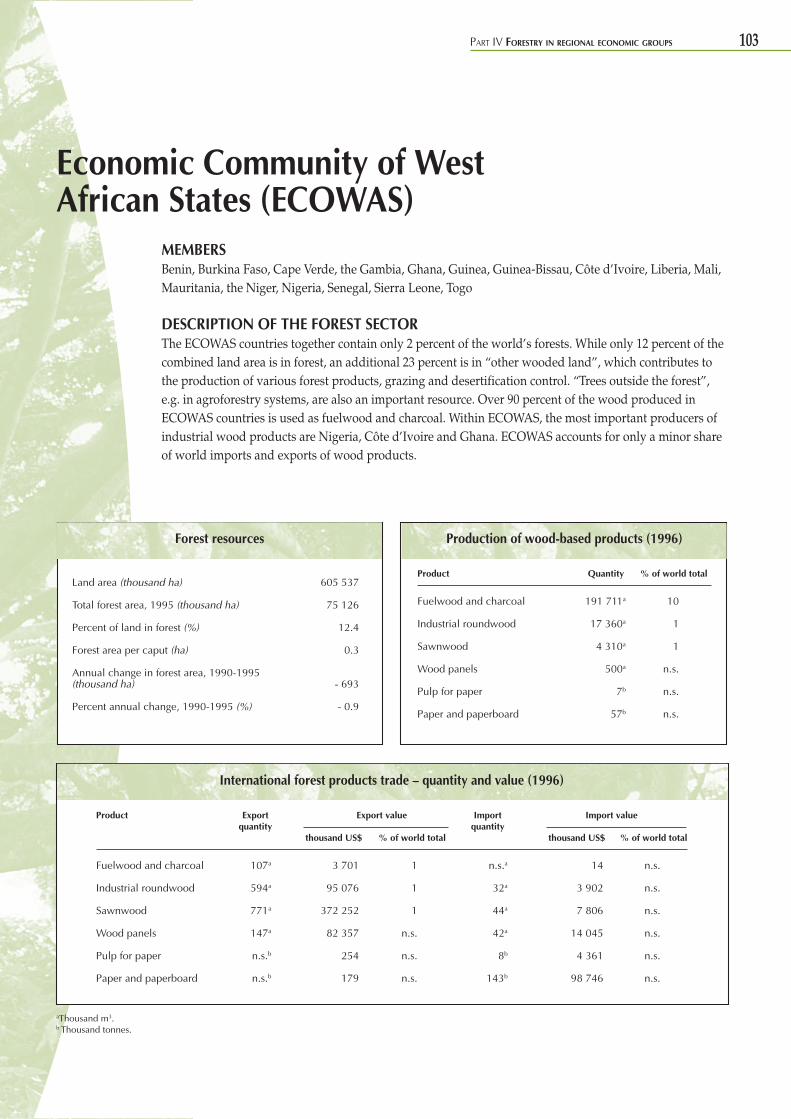

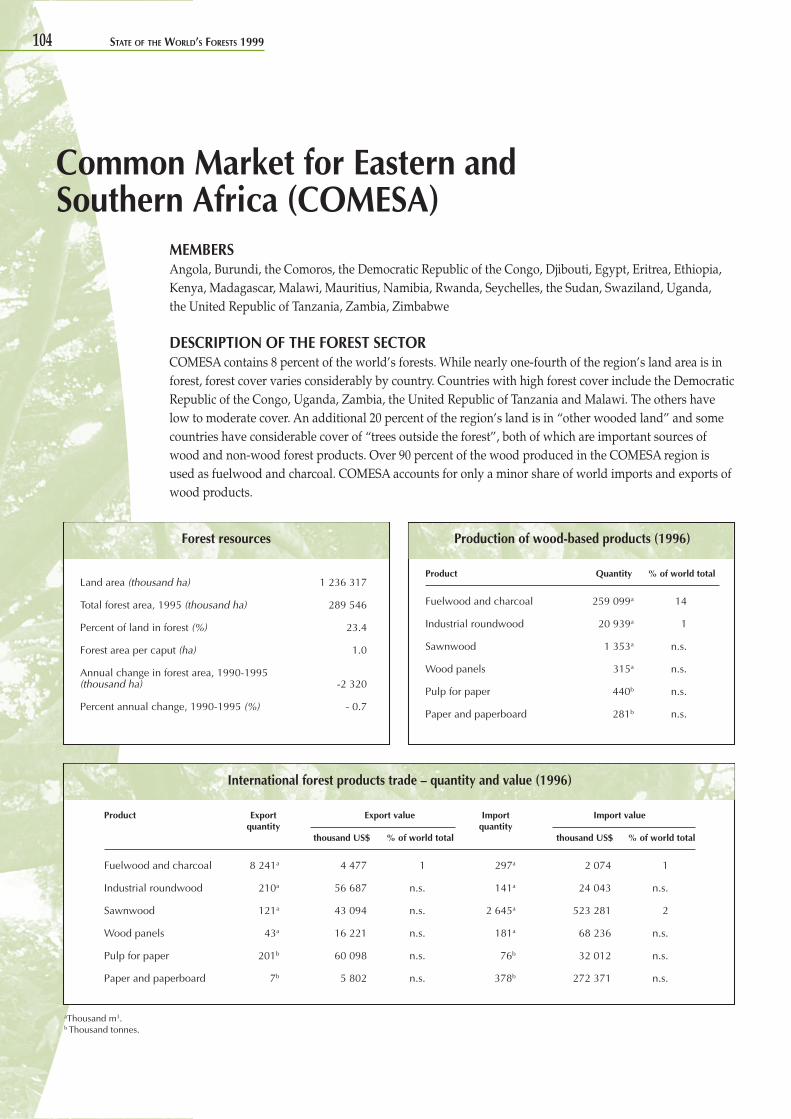

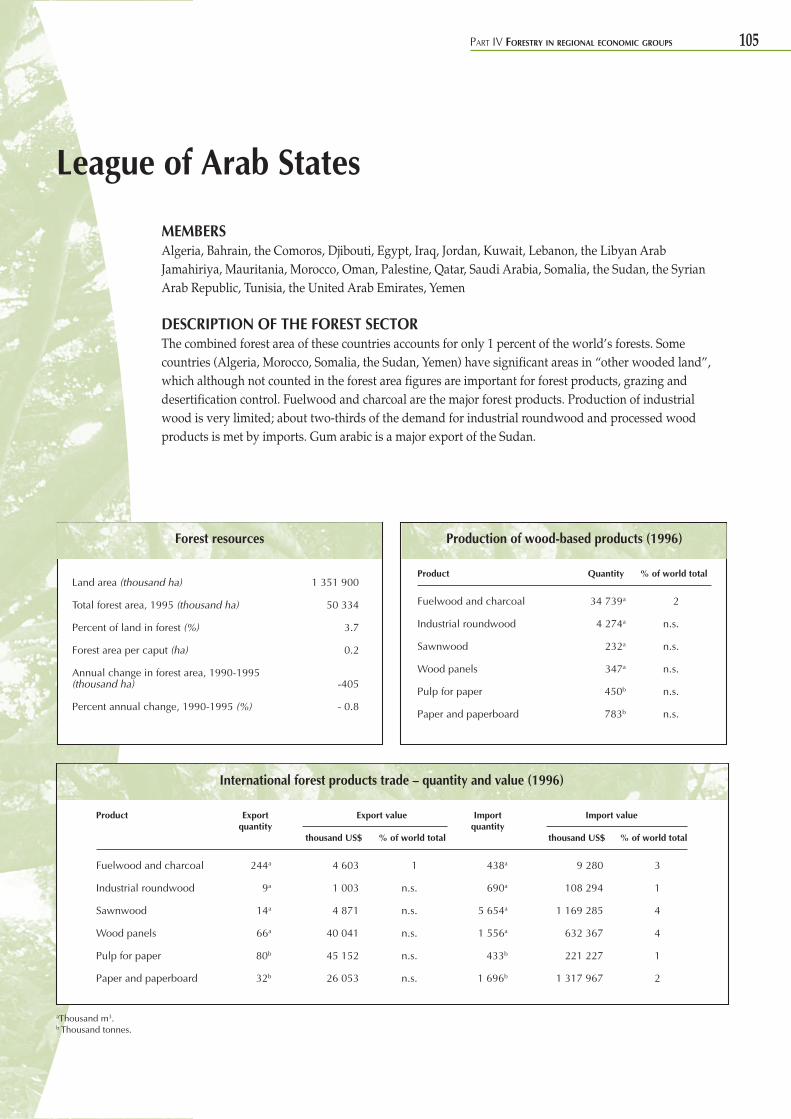

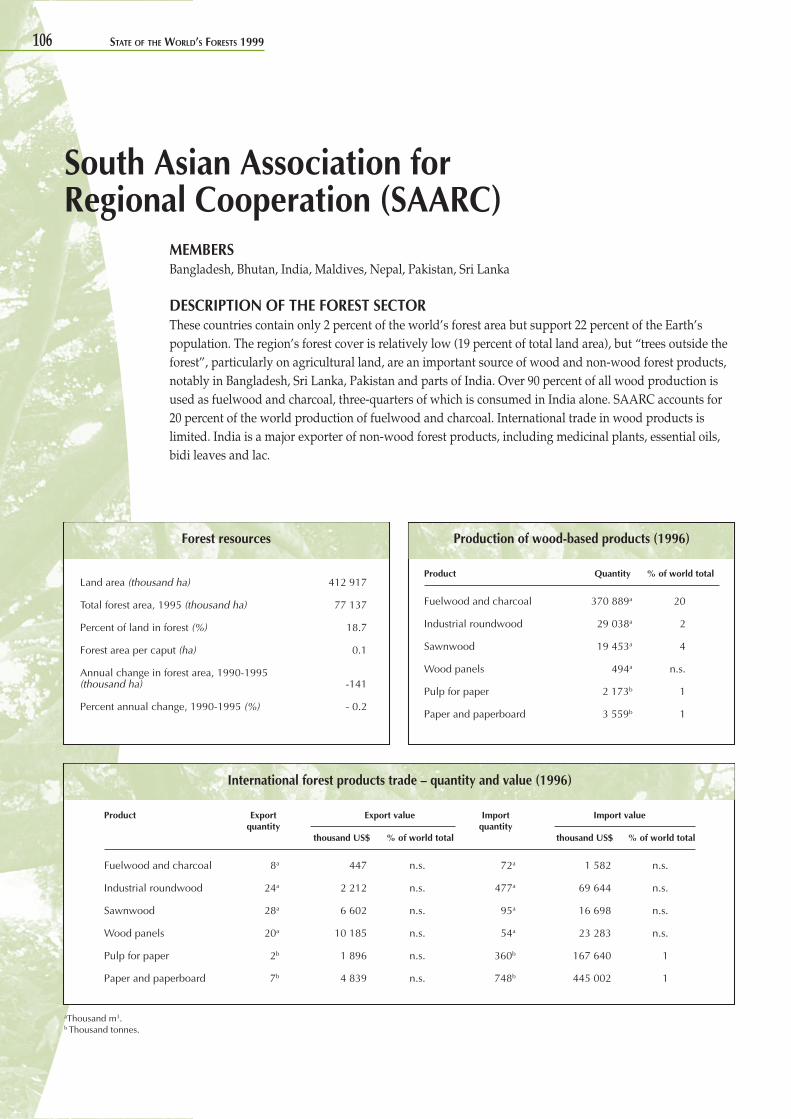

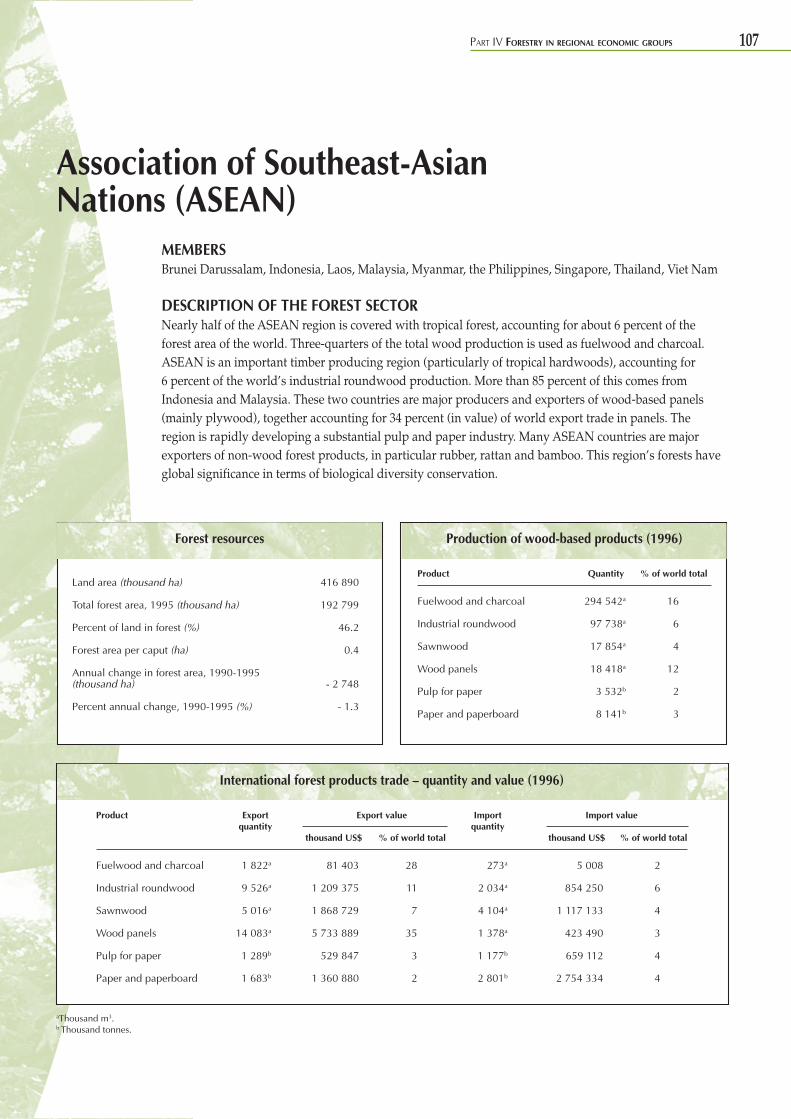

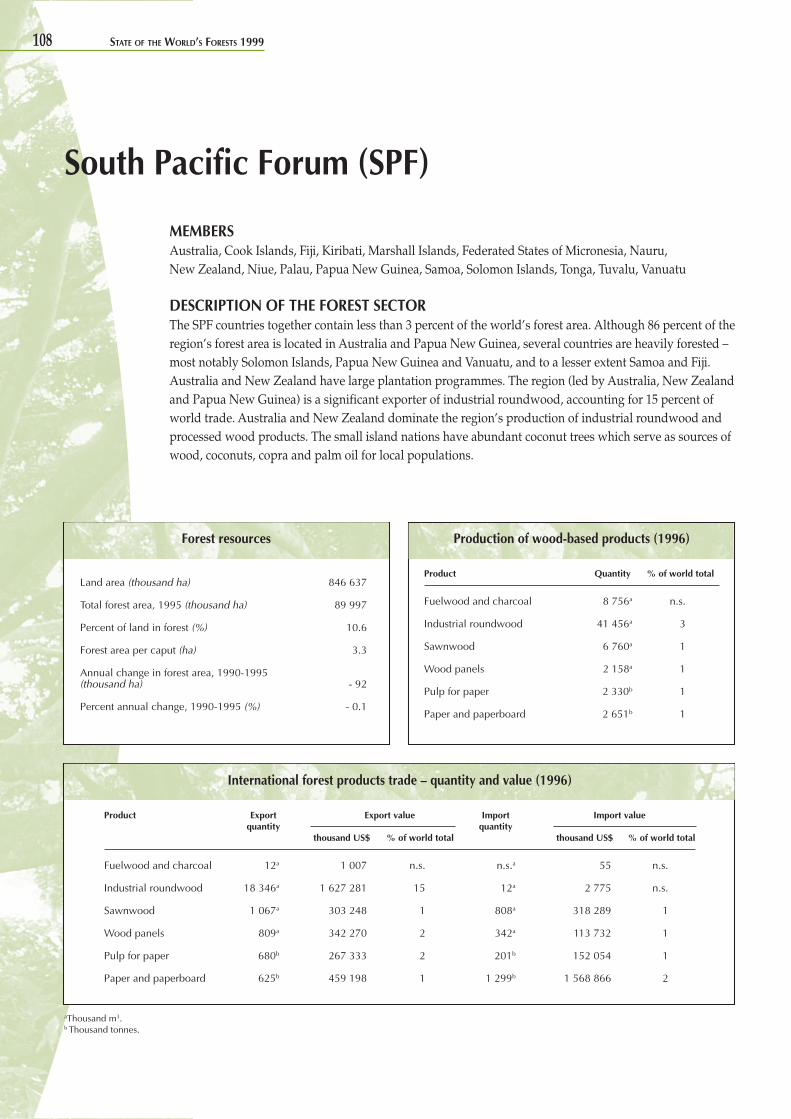

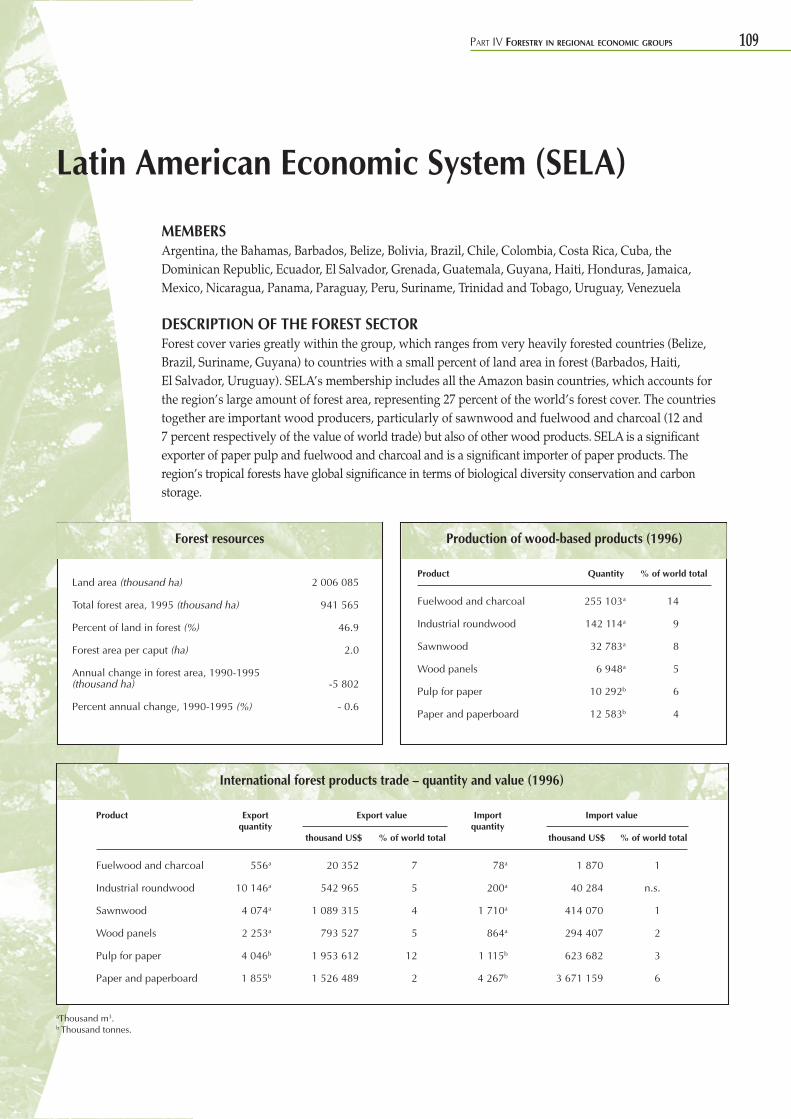

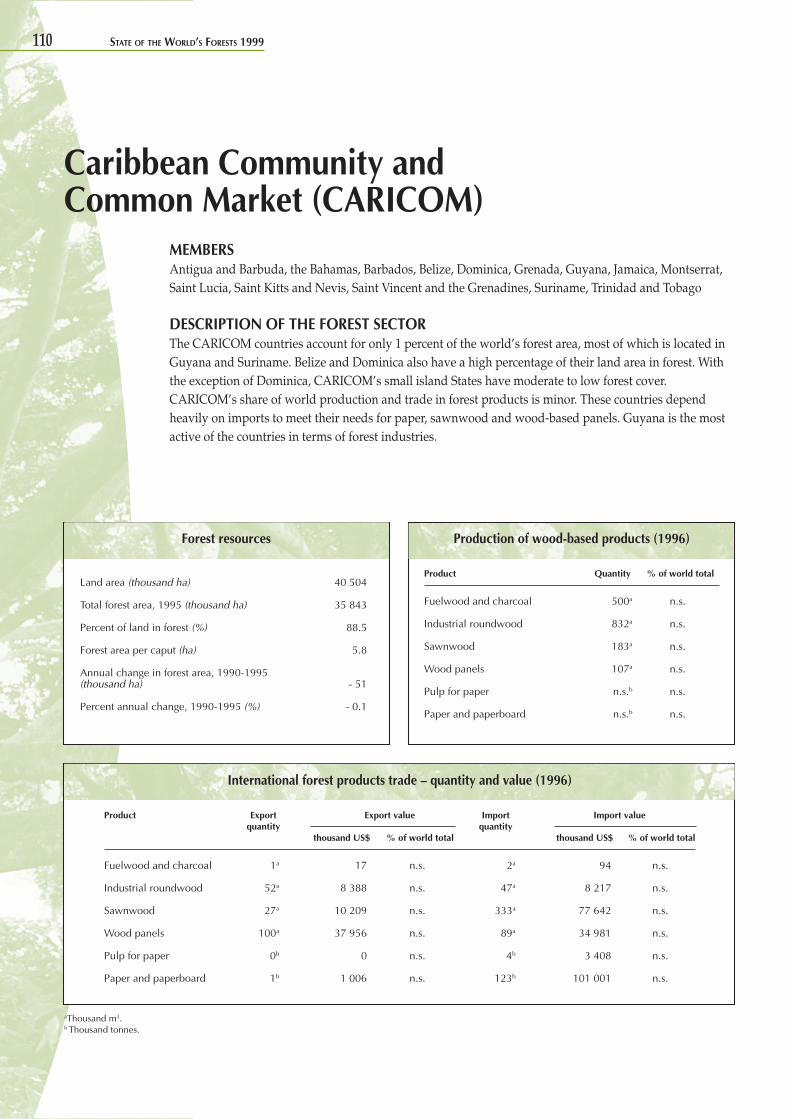

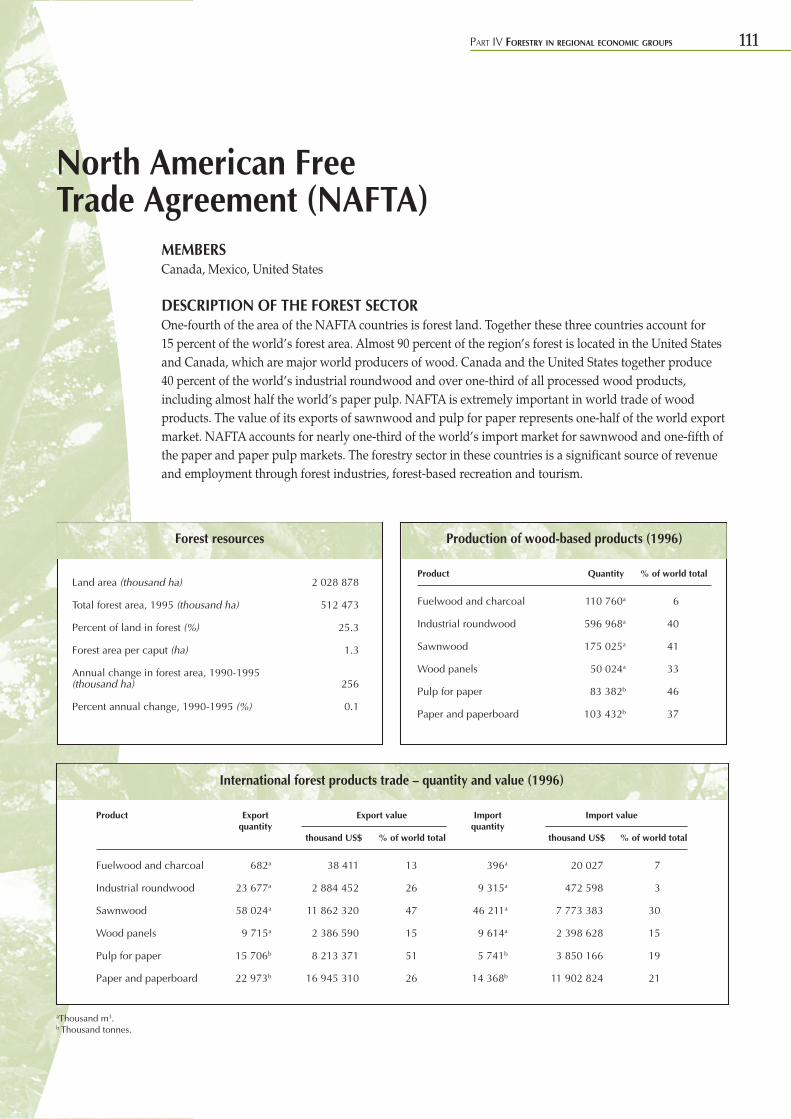

European Union (EU) 101Commonwealth of Independent States (CIS) 102Economic Community of West African States (ECOWAS) 103Common Market for Eastern and Southern Africa (COMESA) 104League of Arab States 105South Asian Association for Regional Cooperation (SAARC) 106Association of Southeast-Asian Nations (ASEAN) 107South Pacific Forum (SPF) 108Latin American Economic System (SELA) 109Caribbean Community and Common Market (CARICOM) 110North American Free Trade Agreement (NAFTA) 111

ANNEXESAnnex 1: Acronyms 114Annex 2: Definitions 116Annex 3: Data tables 119

BIBLIOGRAPHY 151

vii

SOFO 1999 owes its existence to the efforts of many individuals both within and outside FAO. Overall coordination and editing of the publication was carried out by S.M. Braatz. The

following FAO staff members and consultants were involved in collecting data, drafting sections orreviewing the document: G. Allard, J. Anderson, J. Ball, J. Balsiger, S. Bass, L.S. Botero, J. Bourke,S.M. Braatz, C. Brown, G. Bull, C.M. Carneiro, F. Castañeda, L. Christy, J. Clément, A. Contreras,R. Davis, P. Durst, C. Eckelmann, M. Hosny El-Lakany, L. Ferroukhi, T. Frisk, T. Hofer, M. Gauthier,S. Hald, R. Heinrich, H. Hilmi, V. Johnston, P. Koné, J. Lahaussois, M. Laverdière, J. Lindsay, L. Lintu,L. Ljungman, P. Lowe, G. Lund, Q. Ma, M. Malagnoux, M. Martin, D. McGuire, A. Mekouar,T. Michaelsen, M. Morell, H. Ortiz-Chour, F. Padovani, C. Palmberg-Lerche, M. Paveri, F. Pontecorvi,C. Prins, H. Qwist-Hoffmann, P. Qwist-Hoffmann, R. Romeo, L. Russo, K.H. Schmincke, E.H. Sène,O. Serrano, D. Shallon, A. Sherwood, P. Sigaud, H. Simons, O. Souvannavong, K. Thelen,M.A. Trossero, P. Vantomme, K. Warner, A. Whiteman, M.L. Wilkie and D. Williamson.

A number of outside collaborators contributed various pieces. H. Gillett (World ConservationMonitoring Centre, United Kingdom) prepared the piece on assessing biological diversity at thespecies and ecosystem level. B. Schlamadinger and G. Marland (Oak Ridge National Laboratory,United States) and C. Leining and B. Braatz (ICF Incorporated, United States) contributed the pieceon forests’ role in mitigating global climate change. D. Heuer (Precious Woods Ltd., Switzerland)prepared the box on certification of Precious Woods. D. Barron (Canadian Pulp and PaperAssociation) and H.S. Leng (Malaysia Timber Council) provided input for the piece on private-sectorinitiatives. N. Dudley (Equilibrium, United Kingdom) contributed the piece on NGOs for the sectionon initiatives in the international forestry debate.

The following members of the Internal Advisory Committee provided technical oversight inplanning and reviewing the document: J. Anderson, J. Ball, J. Bourke, S. Dembner, M. Paveri,P. Vantomme and K. Warner.

FAO wishes to acknowledge the extremely valuable guidance given by the members of SOFO’sExternal Review Committee: D. Barron, S. Bass, M. Dourojeanni, M. Goumandakoye, H. Gregersen,M. Hadley, J.P. Lanly, J. Maini, O. M’Hirit, C. Prins, M.N. Salleh and M. Simula. D. Kneeland alsoprovided helpful comments.

Many thanks are due to S. Dembner and to the staff of the Editorial Group, FAO Publishing andMedia Support Service for production and publication support. L. Ransom and E. Rubini providedessential secretarial assistance.

Acknowledgements

viii

The State of the World’s Forests (SOFO) isproduced by FAO every two years for the

purpose of making current, reliable and policy-relevant information available to policy-makers,foresters and other natural resource managers,academics, forest industry and the public. SOFO1999, the third in the series, examines the currentstatus of the world’s forests, recent policy andinstitutional developments and external impacts onthe sector. It concentrates on significant events anddevelopments of the 1997-1998 period and onselected topical issues.

This two-year period was marked by extremes:record high global temperatures; devastating floodsand severe droughts; widespread forest fires andheavy ice storms; and rapid global economicgrowth abruptly disrupted by the Asian economiccrisis. Forests have felt the impact of these climaticand economic phenomena.

Significant changes have also been driven bydevelopments within the forest sector. Policy-makers and forest managers have been respondingto changing national priorities and to internationalcommitments made at, and since, the UnitedNations Conference on Environment andDevelopment (UNCED) in 1992, aimed towardssustainable management of all types of forests. Abroader approach to forest management is beingsought, balancing social, economic andenvironmental objectives. The concerns of a widerrange of interest groups are being taken intoconsideration, and local communities areincreasingly becoming directly involved in forestplanning and management.

SOFO 1999 discusses the state and change offorests worldwide, new developments in forestmanagement and issues and trends related toforest goods and services. It also examines recentpolicy trends and institutional changes which arehaving an impact on how, for what purposes andby whom forests are being managed. This globalview of forestry today is augmented byinformation about the forest sector at the regionaland subregional levels.

Executive summary

CHANGES IN FOREST COVER ANDCONDITIONThe latest global figures on forest cover indicatethat in 1995 there were 3 454 million hectares offorest (including natural forests and forestplantations) worldwide. Between 1990 and 1995,the total area of forests decreased by 56.3 millionhectares – the result of a loss of 65.1 million hectaresin developing countries and an increase of8.8 million hectares in developed countries. Majorcauses of forest cover change include conversion offorests to agricultural land and large infrastructuraldevelopment in developing countries, and forestgrowth on abandoned agricultural land indeveloped countries.

The many causes of forest degradation includeoverharvesting of industrial wood and fuelwood,overgrazing, fire, insect pests and diseases, stormsand air pollution; of these, forest fires were the mostvisible in 1997-1998. These were the worst twoyears for wildfires and forest fires in recent times.Millions of hectares of forest burned. All regions ofthe world were affected and nearly all types offorests burned. National disasters were declared,and national and international resources weremobilized to fight the fires. Vast areas of forestburned in Brazil, Indonesia, Mexico and theRussian Federation. Although the exact areas arestill unknown, estimates are 2 million hectares inIndonesia in 1997 and perhaps more in 1998, and2 million hectares each in Brazil and the RussianFederation in 1998. While droughts associated withthe unusually strong El Niño weather patterncontributed to the increased number, size, intensityand duration of fires, land use practices, mainly inagriculture and forestry, were clearly major causesof many fires. The fires have catalysed national andinternational initiatives to encourage appropriatepolicy responses and operational measures forpreventing and controlling fires in the future.

TRENDS IN FOREST MANAGEMENTForest management objectives, managementpractices and the managers themselves have

ix

changed dramatically in the past decade in manycountries. Increased emphasis on environmentalvalues has resulted in significant expansion of theprotected area systems (including forest lands) ofsome countries over the past few years. Greateremphasis on management of natural forests formultiple purposes and increased attention toenvironmental factors have led, in some places, toreduced intensities of timber harvesting andchanges in management practices. Logging bans innatural forests have been announced in severalcountries. The increased emphasis on the use ofnatural forests for environmental protection,conservation of biological diversity and recreationhas increased the reliance on forest plantations andother sources of wood supply in some countries.

Efforts to improve the stewardship of forestsdesignated for wood production includesilvicultural improvements and the adoption ofenvironmentally sound timber harvesting practices.Operational guidelines and codes of practice forforest management have been adopted in Europeand North America. New silvicultural systems havebeen developed for temperate and boreal forests inNorth America and for tropical forests. Codes ofpractice and guidelines for forest harvesting haverecently been drafted for tropical forests, mostnotably in the Asia and the Pacific region.

Changing patterns of forest ownership, increasingsupport for locally based forest management andgreater participation of the private sector in forestmanagement have influenced how forests aremanaged and by whom. Changes leading toincreased local forest management in variouscountries include:

• a proliferation of new mechanisms for thedevolution of forest management to localcommunities or user groups;

• increased recognition of the historicalterritorial claims of local peoples;

• restoration of the lands (including forests) ofdispossessed communities and individuals.

SOCIAL AND ENVIRONMENTAL SERVICESOF FORESTSRecognition of the social and environmentalservices of forests – such as mitigation of globalclimate change, conservation of soil and water

resources, enhancement of agricultural systems,conservation of biological diversity, improvementof urban and peri-urban living conditions,protection of natural and cultural heritage,generation of employment and provision ofrecreational opportunities – continues to grow.

As the emphasis on these important services oftrees and forests has increased, more attention hasbeen focused on forests in fragile ecosystems –including mountains, drylands and small islandStates – and in countries with low forest cover.Although these forests generally have relativelylow timber value, their important social andenvironmental functions have been increasinglyrecognized in management decisions. Forests’ rolein water conservation is expected to be given moreprominence as international attention increasinglyturns to freshwater resource issues.

The role of forests in mitigating global climatechange was given greater prominence with theadoption of the Kyoto Protocol of the FrameworkConvention on Climate Change in 1997 and thedeliberations of the fourth Conference of the Partiesin Buenos Aires, Argentina in November 1998. TheKyoto Protocol establishes legally bindingcommitments for reduced emissions of greenhousegases from industrialized countries and permits theuse of a limited list of activities in the land usechange and forest sector to meet thesecommitments. The protocol thus providesindustrialized countries incentives to invest, in boththeir own and other countries, in forestry activitieswhich increase carbon sequestration and/or reducecarbon emissions. While many details of the KyotoProtocol remain to be clarified, if ratified it shouldoffer possibilities for investment in forestry.

FOREST PRODUCTSMeeting the needs for wood and non-wood forestproducts while at the same time fulfilling demandsfor environmental and social services from forestsremains a major challenge.

While wood is the predominant commercialproduct from most forests, increased attention isbeing paid to non-wood forest products (NWFPs),whose main importance currently lies in theircontribution to household and local economies,particularly among the poor in developing

x

countries. Recent regional and international forahave addressed the needs to conserve non-woodresources while ensuring local peoples’ equitableaccess to and use of the resources, to improvemarket information and to develop appropriate andfair pricing mechanisms for NWFPs (includingroyalties on intellectual property rights). SOFO1999 focuses specifically on medicinal plants, whichas a group are among the most valuable NWFPsfrom forests. Most medicinal plants gathered fromthe wild come from forest lands.

Fuelwood and charcoal are expected to continue tobe important sources of household energy indeveloping countries. Moreover, recent policychanges and experiences with wood-basedbio-energy programmes in several countries indicatethat woodfuels may become increasingly attractive tosome countries as industrial energy sources.

Developed regions continue to dominate heavilyin production and consumption of industrial woodproducts. FAO has projected that demand forindustrial roundwood will increase by 1.7 percentannually between now and the year 2010, drivenboth by population increases and economic growth.While recent studies suggest that supplies aresufficient to meet this demand, the situation willvary among countries and will depend greatly onmarket conditions, government policies,technological improvements and human resourcedevelopment. Production of industrial roundwoodis expected to continue to exceed consumption inall regions except Asia, which will continue to relyon imports to make up the difference.

Recent trends which are expected to continue tohelp in meeting the increasing demand forprocessed wood products include:

• improved management of forests designatedfor wood production;

• increased production from plantations andfrom trees outside forests, particularly onagricultural land;

• new forest product technologies and gains inefficiency in wood processing;

• greater use of recovered paper and woodprocessing residues;

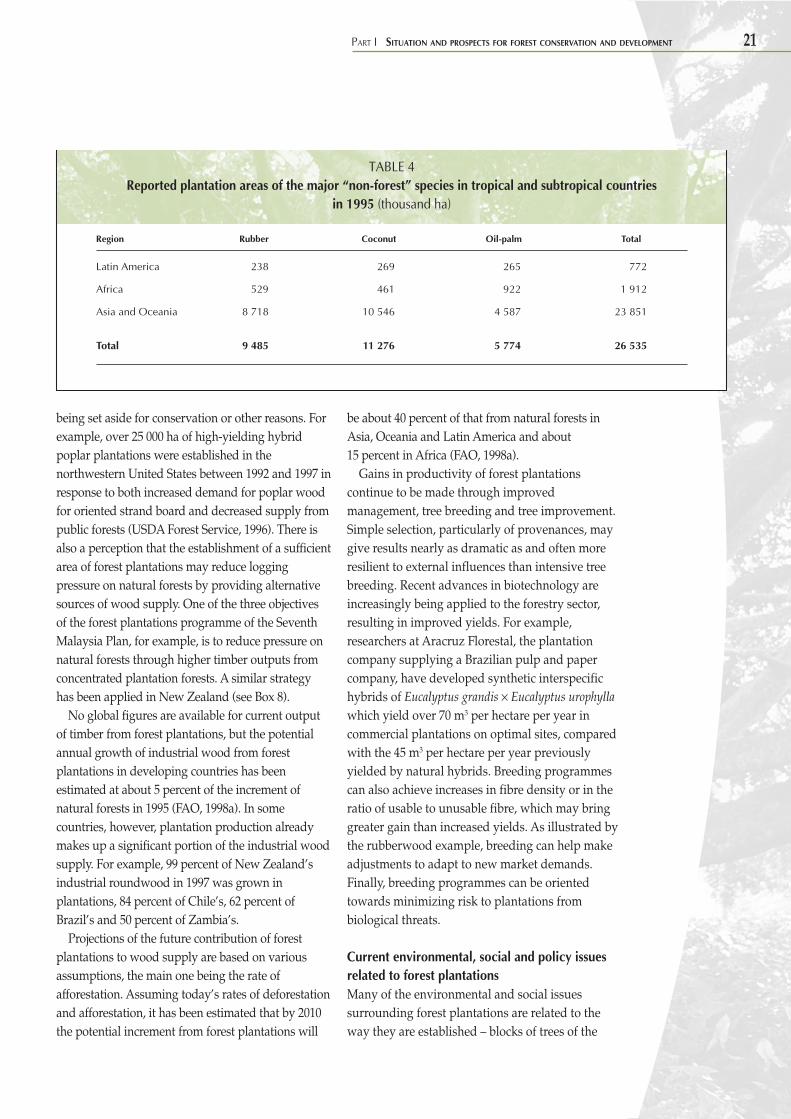

• increased use of wood and fibre from “non-forest” species (e.g. rubber, oil palm) in forestindustries.

Trade will help balance deficits of wood fibre inone place with surpluses elsewhere.

The Asian economic crisis, which began in mid-1997, has seriously disrupted forest products tradein the Asia and the Pacific region. The main impactson countries within the region have been:

• reduced demand for all forest products;• increased competitiveness of exporting

countries whose currencies have depreciated;• falling prices for forest products throughout

the region;• reduced earnings in the forest sector, resulting

in reduced harvests, mill closures andworkforce lay-offs.

While Asian wood markets have been the mostseverely affected, the effects have spread outsidethe region to countries that either depend heavilyon, or compete with, Asian markets. Woodexporters from Africa to New Zealand and fromNorth to South America have been affected.

Certification remains a high-profile but complexand often controversial issue. Various international,regional and national certification systems havebeen developed. The area of forests certified hasincreased considerably in the past two years,although significant volumes of certified productsapparently are not yet entering the market. It isunclear whether the demand for certified wood willincrease and whether certification will, in fact,significantly contribute to improved forestmanagement where deforestation is greatest, i.e. indeveloping countries.

RECENT CHANGES IN FOREST POLICY,LEGISLATION AND INSTITUTIONALFRAMEWORKEvident trends in forest policy reform includeattempts to privatize State forest resources andpublic forest-based companies, to decentralizecertain functions of central governmentadministrations and to eliminate some “perversesubsidies”, including the underpricing of forestconcessions.

Revision of forest-related laws around the worldhas accelerated significantly in recent years. Thelegal changes reflect commitments to:

• promote local forest management;• enhance the environmental functions of forests;

xi

• reinforce forest management planning,increasing consideration of environmental andsocial issues in management plans andsupporting public participation in the planningprocess;

• increase transparency in awarding forestconcessions.

Institutional changes in the forest sector –particularly privatization and the decentralizationand devolution of forest managementresponsibilities to the local level – have closelyparalleled these policy and legislative trends.Decentralization and privatization are also affectingforest research systems. Forest education andextension are responding to changing objectives forforest management, new forest owners and/ormanagers and the forest-related concerns of anincreased number of interest groups.

INTENSIFIED EFFORTS TO DEVELOPFOREST-RELATED INFORMATIONMany organizations have made substantial effortsover the past few years to collect and disseminateglobal forest-related information. Major initiativeshave been undertaken in forest cover assessmentand mapping, forest resources assessment, study ofwood supply and data collection on biologicaldiversity. Complementing these global efforts arevarious initiatives to collect and analyseinformation at the regional level and to strengthennational capacity in the collection, analysis and useof forest-related information.

INTERNATIONAL INITIATIVES ONFORESTSMany recent international initiatives are aimed atfostering sustainable forest management. More than150 countries are currently participating ininternational processes to develop and implementnational-level criteria and indicators for sustainableforest management. Various efforts at the forestmanagement unit level are being coordinated bythe Center for International Forestry Research(CIFOR), the International Tropical TimberOrganization (ITTO) and the African TimberOrganization (ATO). Other international initiativesinclude the establishment and management ofmodel and demonstration forests, ITTO’s “Year

2000 Objective” and the G8 countries’ actionprogramme on forests which was approved in May1998. Developments in the implementation of thethree international conventions arising fromUNCED (the Framework Convention on ClimateChange, the Convention on Biological Diversityand the Convention to Combat Desertification) andthe International Tropical Timber Agreementprovide additional support for certain elements offorest management. Non-governmentalorganizations and the private sector continue to beactive in the international forest debate and inefforts to improve forest management at the fieldlevel.

The post-UNCED international dialogue onforests led by the Intergovernmental Panel onForests (IPF) from 1995 to 1997 resulted in over 100negotiated proposals for action. Work continuesunder the Intergovernmental Forum on Forests(IFF), established in mid-1997. In 2000, IFF willpresent its final report to the United NationsCommission on Sustainable Development on itsthree major areas of work:

• the implementation of IPF’s proposals for action;• issues on which international consensus has

yet to be achieved;• the identification of possible elements of, and

work towards, consensus on internationalarrangements and mechanisms for themanagement, conservation and sustainabledevelopment of forests.

The issue of international instruments forsupport of forests first arose in 1990. Since then, anumber of such instruments, both legally and non-legally binding, have been developed. Consensuson whether additional international instruments areneeded, and if so, what they would cover, remainselusive. Discussion of whether to rely on existingmechanisms, to enhance them or to developadditional ones – such as a legally bindinginstrument on all types of forests – promises toremain high on the international forest agenda forat least the next few years. ◆

STATE OF THE WORLD’S FORESTS 1999

PART ISITUATION ANDPROSPECTS FORFOREST CONSERVATIONAND DEVELOPMENT

PART I SITUATION AND PROSPECTS FOR FOREST CONSERVATION AND DEVELOPMENT 1

The status of forestresources

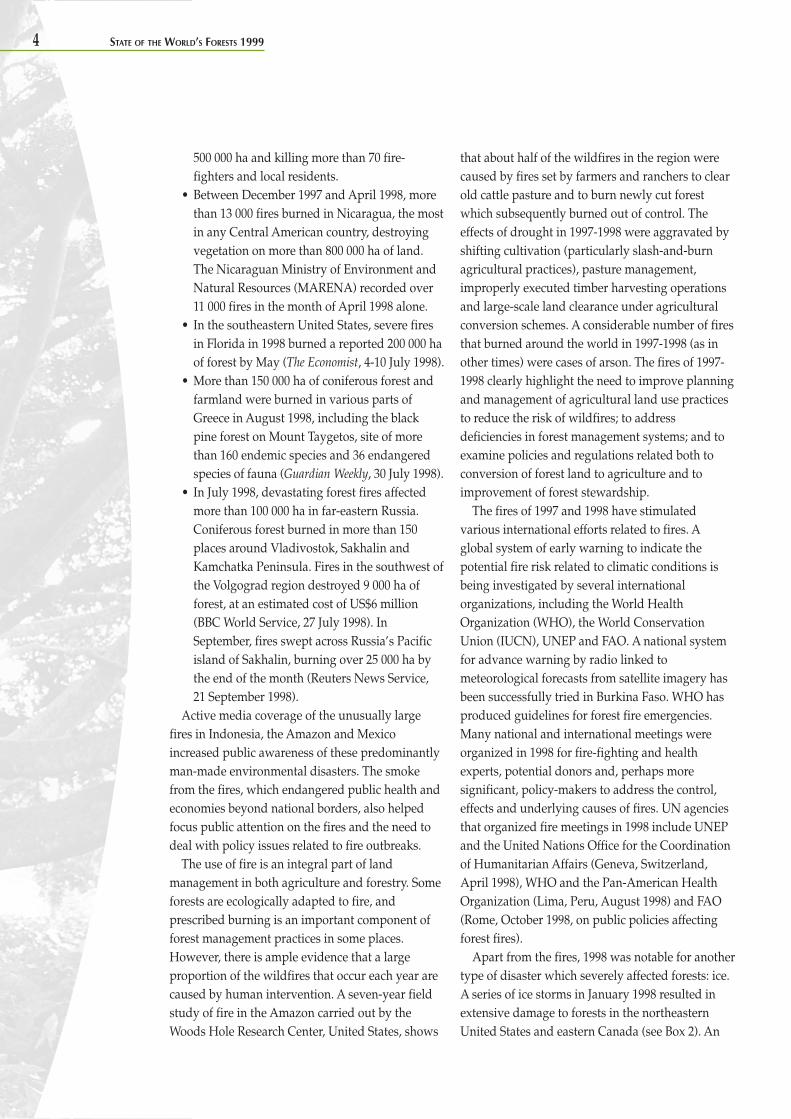

by region between 1980 and 1995 is shown inFigure 2.

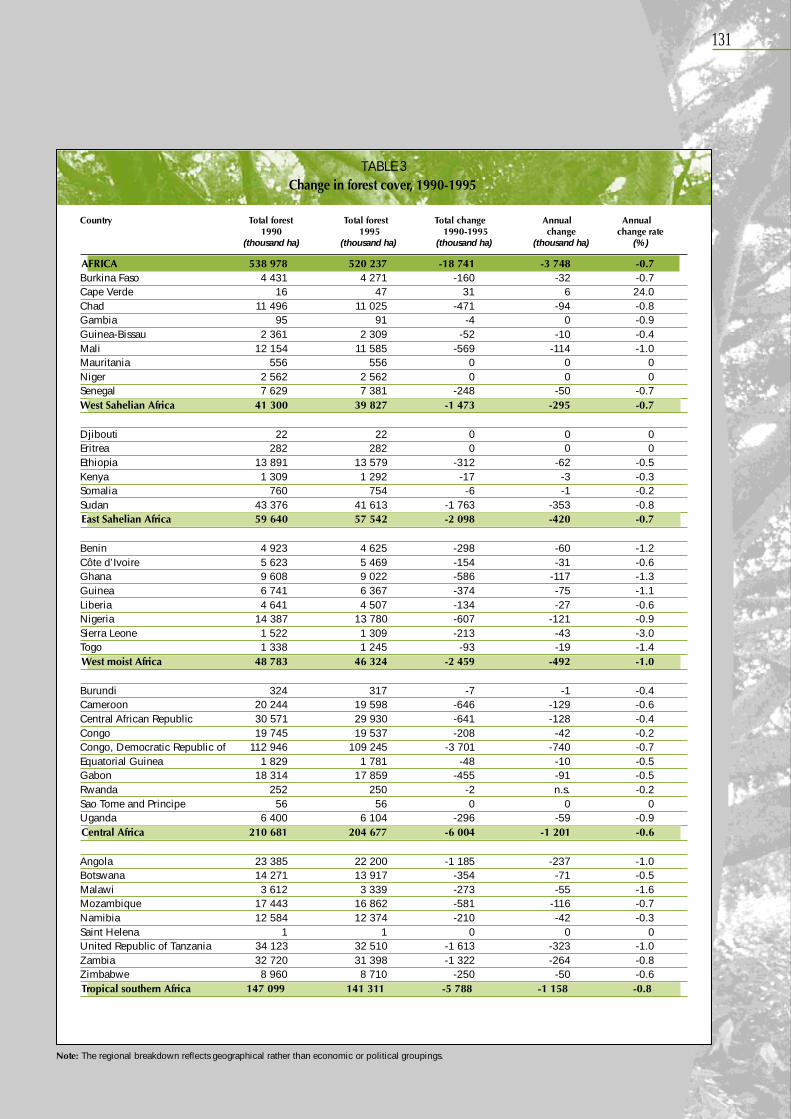

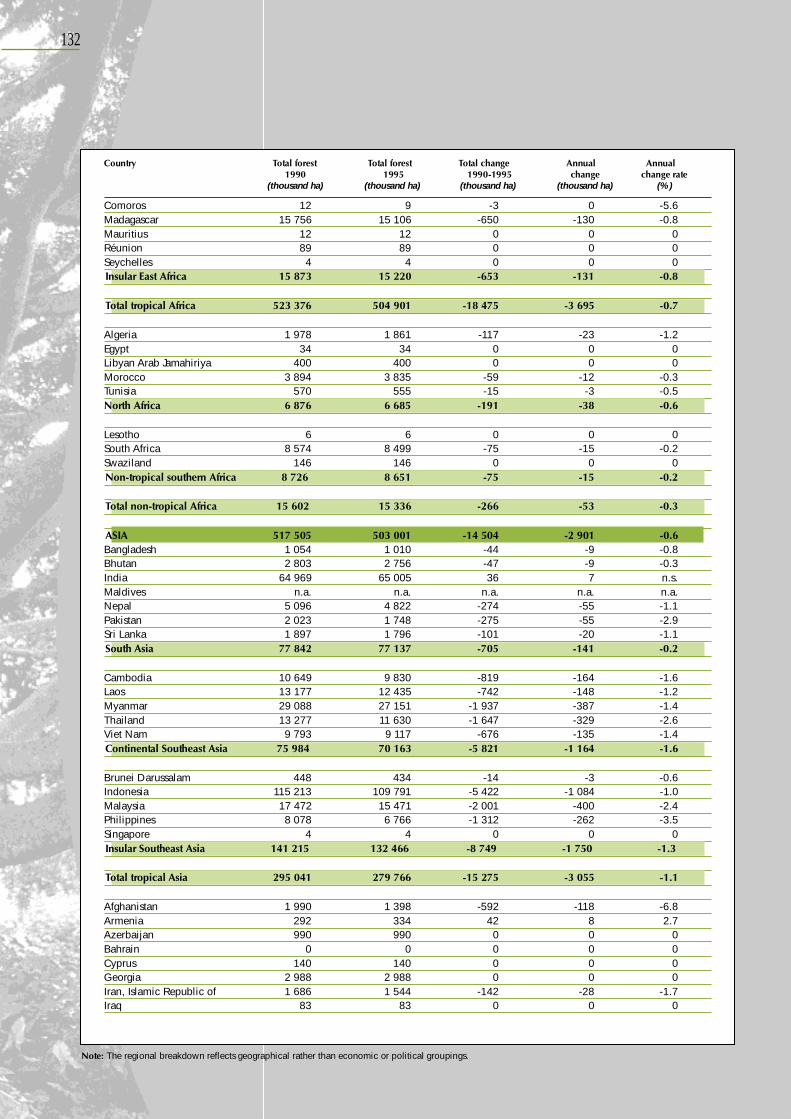

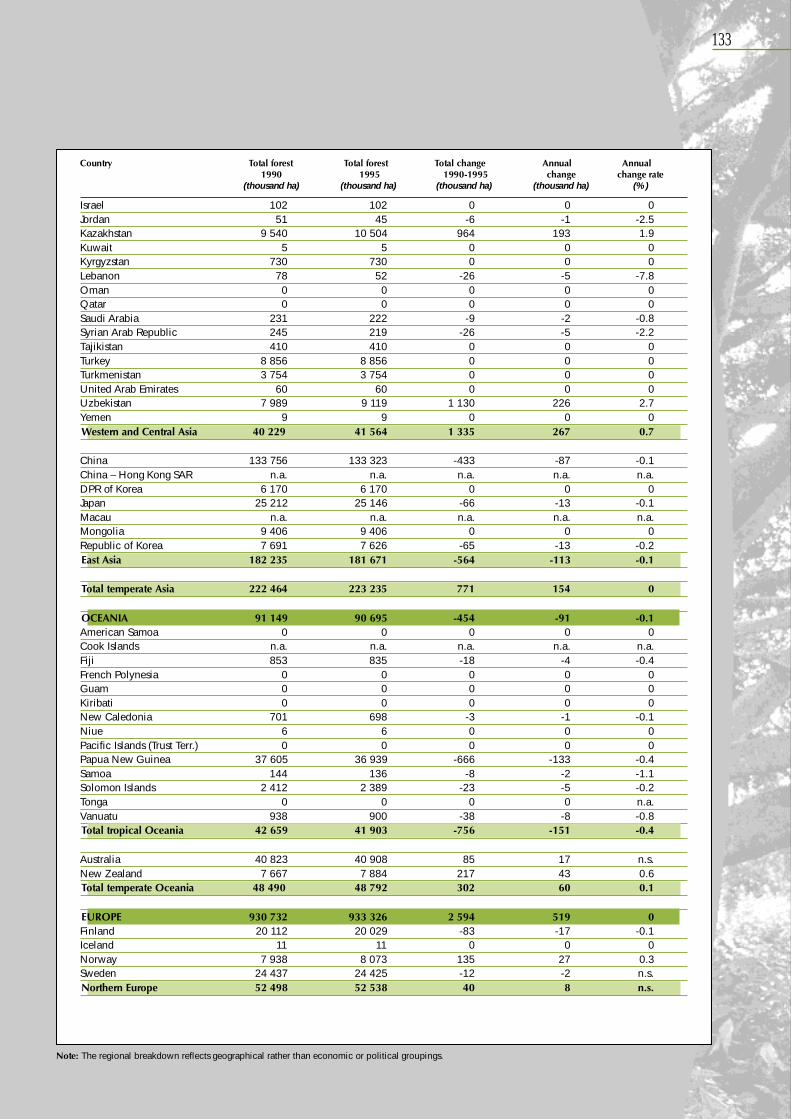

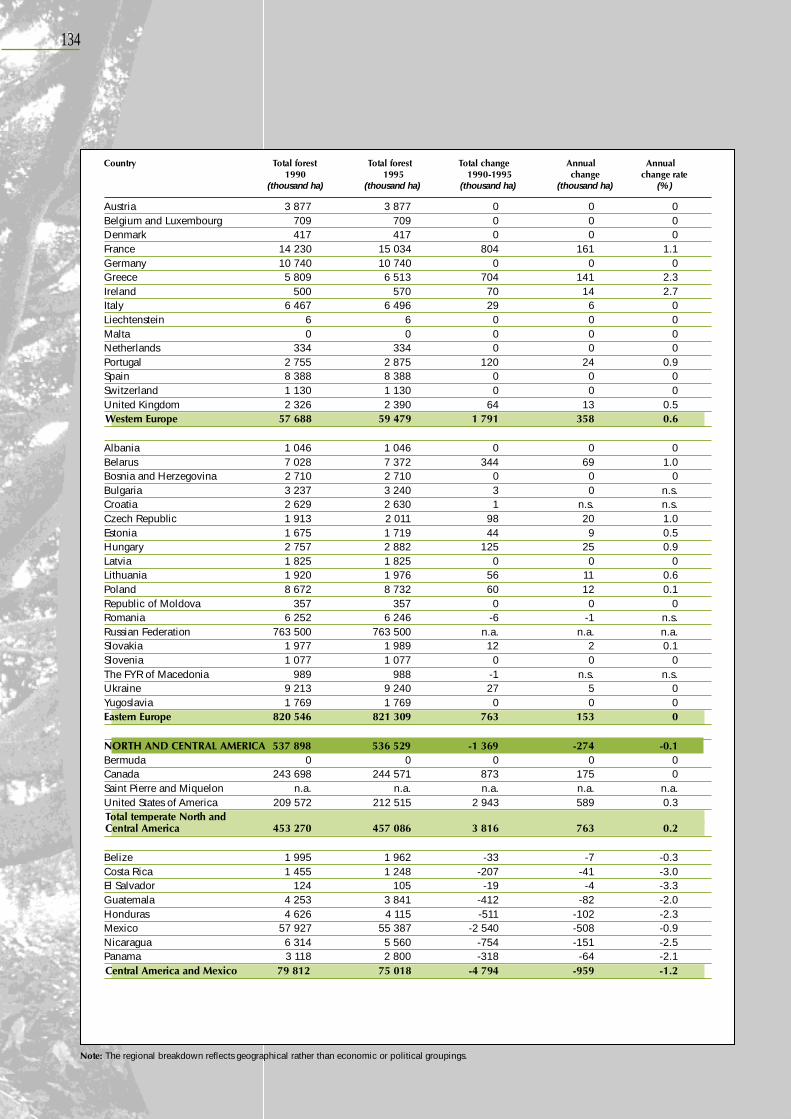

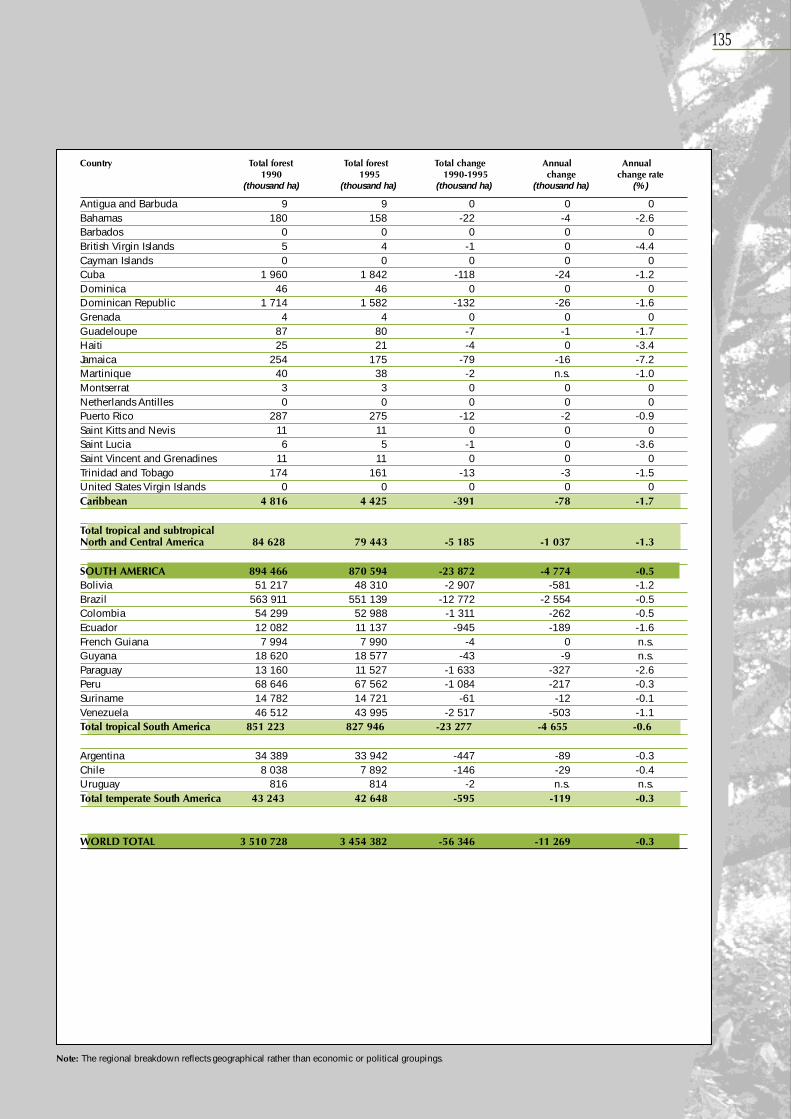

Between 1990 and 1995, there was an estimatednet loss of 56.3 million hectares of forestsworldwide. This represented a decrease of65.1 million hectares in developing countries andan increase of 8.8 million hectares in developedcountries. Although the global loss of forests wasstill very high, the figures suggest that the rate ofdeforestation might be slowing. The estimate offorest cover change in natural forests of developingcountries (which is where most deforestation istaking place) was an annual loss of 13.7 millionhectares between 1990 and 1995, compared with15.5 million hectares per year over the decade 1980-1990. It will be difficult to know if this is a trend,however, until a comparable global data set isavailable from the Global Forest ResourcesAssessment 2000 (see following discussion).

The major causes of change in forest cover in thetropics appear to be expansion of subsistenceagriculture in Africa and Asia and large economicdevelopment programmes involving resettlement,agriculture and infrastructure in Latin America andAsia (FAO, 1996a). The net increase in forest area indeveloped countries is largely a result ofafforestation and reforestation, including naturalregrowth on land abandoned by agriculture. Thisincrease has more than compensated for theclearing of some areas of forest in variousdeveloped countries, mainly for urban expansionand infrastructure development.

Forest condition: fire, ice and forest pestsThe causes of forest degradation vary from place toplace, and the magnitude and duration of the

Information on the status of the world’s forests –their extent, location, type and condition – is

important for efforts to improve forest managementworldwide and for assessments of forests’ ability toprovide the goods and services demanded of them.The following discussion focuses on two subjects:the area and condition of forest resourcesworldwide, and the status of the information baseon global forest resources, particularlyconcentrating on information on forest area andforest-based biological diversity.

STATUS OF FOREST RESOURCES ANDRECENT DEVELOPMENTS IN FORESTCONDITIONForest cover1

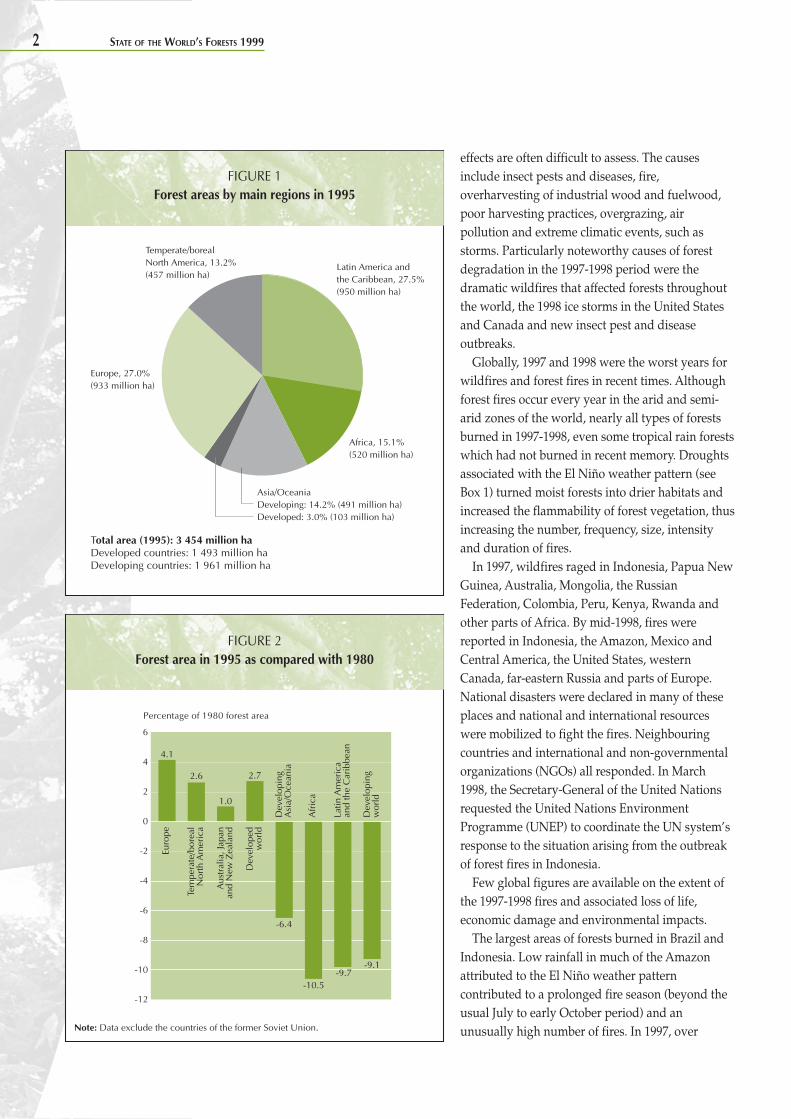

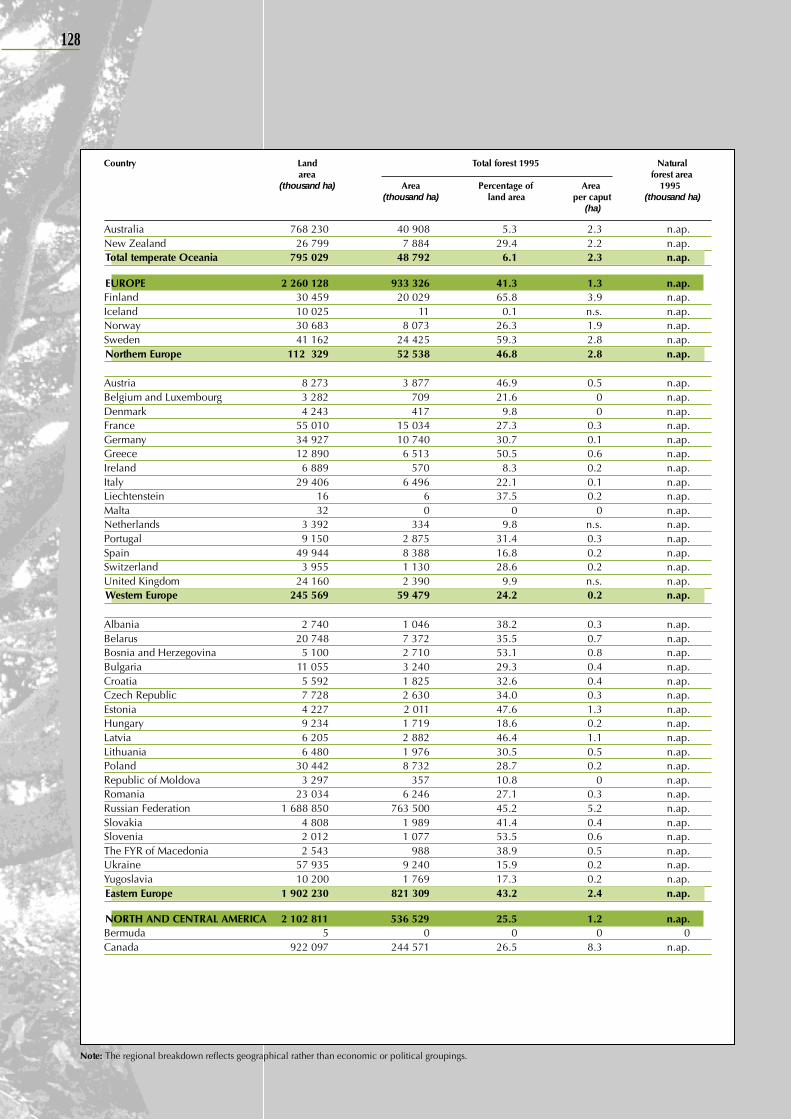

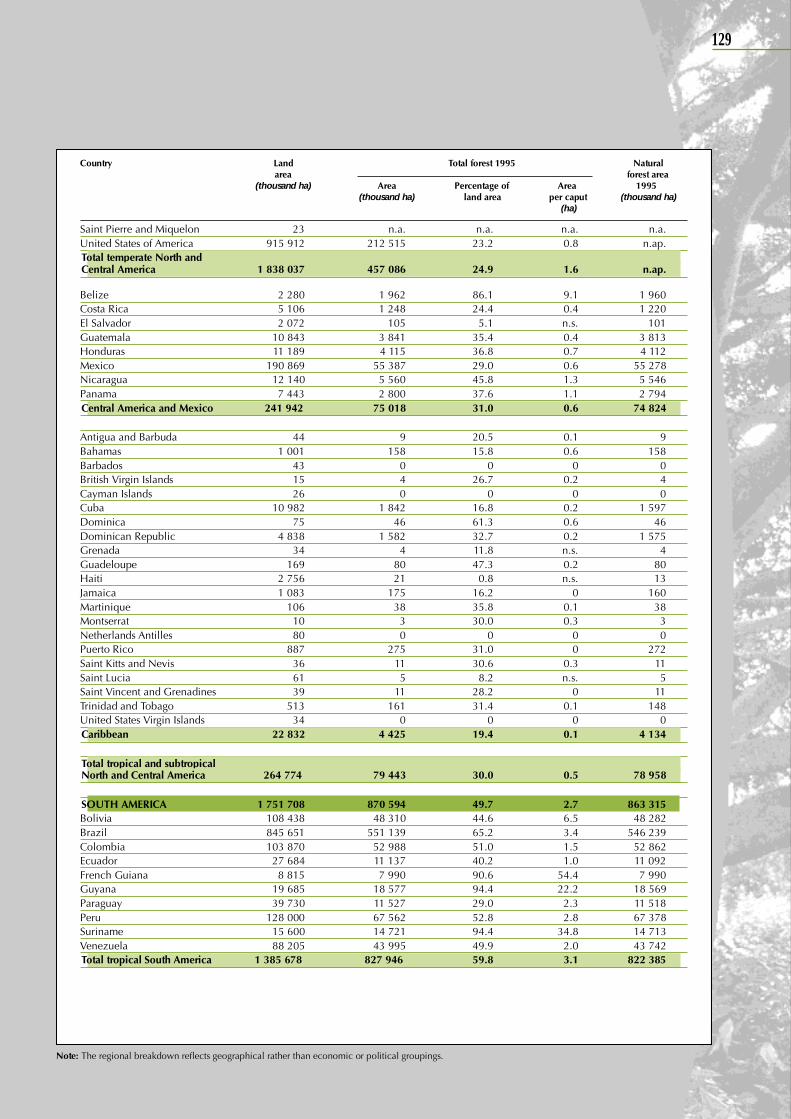

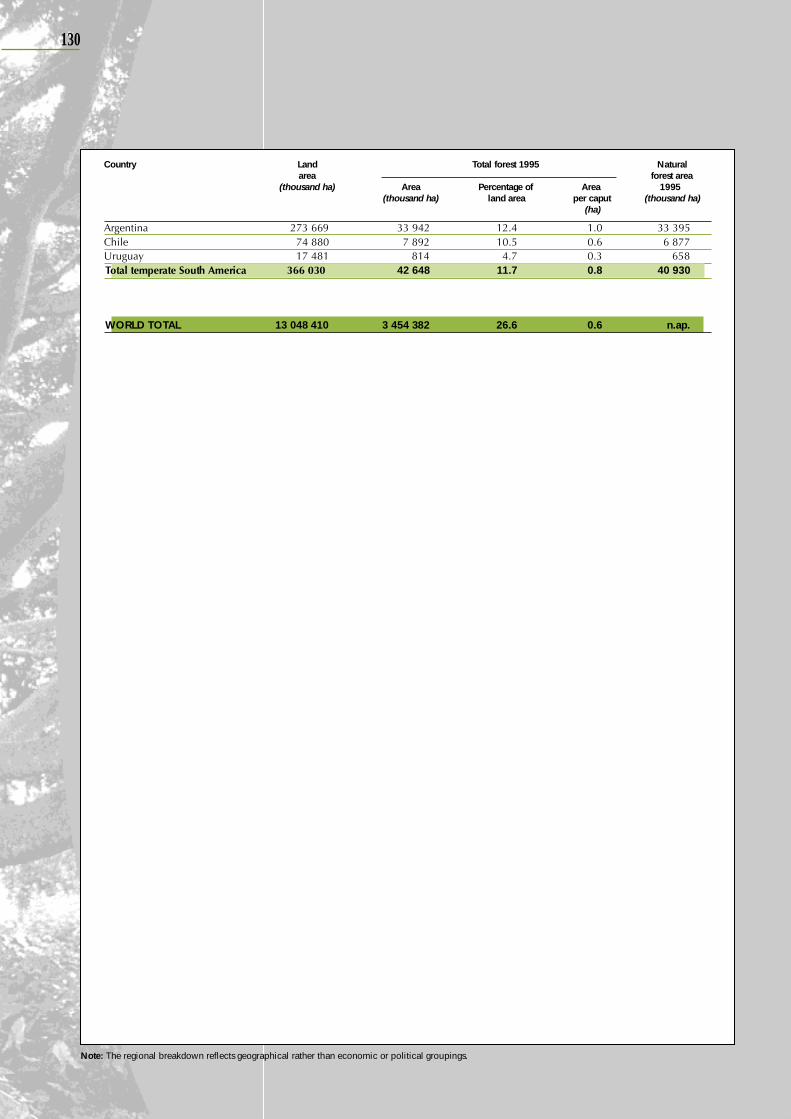

The area of the world’s forests, including naturalforests and forest plantations, was estimated to be3 454 million hectares in 1995, or about one-fourthof the land area of the Earth. About 55 percent ofthe world’s forests are located in developingcountries, with the remaining 45 percent indeveloped countries (Figure 1) (see Table 2 ofAnnex 3 for country data). The world’s forests arealmost equally divided between tropical/subtropical forests and temperate/boreal forests.Only about 3 percent of the world’s forests areforest plantations. The remaining 97 percent arenatural or semi-natural forests.

Change in forest coverData published in the State of the World’s Forests1997 (FAO, 1997d) provide a picture of the trendsin forest cover over a 15-year interval (1980-1995)and allow a comparison between the 1980-1990and 1990-1995 periods. Between 1980 and 1995,the extent of the world’s forests (including bothnatural forests and forest plantations) decreasedby some 180 million hectares. There was a netincrease of 20 million hectares in developedcountries, but a net loss of 200 million hectaresin developing nations. The change in forest area

1 The State of the World’s Forests 1997 provided the most recentdata available on global forest cover. As no new global data seton forest resources will be available until the results of the ForestResources Assessment 2000 study are published, a summary ofthe 1995 figures published in SOFO 1997 is provided in thissection.

2 STATE OF THE WORLD’S FORESTS 1999

FIGURE 1Forest areas by main regions in 1995

Note: Data exclude the countries of the former Soviet Union.

effects are often difficult to assess. The causesinclude insect pests and diseases, fire,overharvesting of industrial wood and fuelwood,poor harvesting practices, overgrazing, airpollution and extreme climatic events, such asstorms. Particularly noteworthy causes of forestdegradation in the 1997-1998 period were thedramatic wildfires that affected forests throughoutthe world, the 1998 ice storms in the United Statesand Canada and new insect pest and diseaseoutbreaks.

Globally, 1997 and 1998 were the worst years forwildfires and forest fires in recent times. Althoughforest fires occur every year in the arid and semi-arid zones of the world, nearly all types of forestsburned in 1997-1998, even some tropical rain forestswhich had not burned in recent memory. Droughtsassociated with the El Niño weather pattern (seeBox 1) turned moist forests into drier habitats andincreased the flammability of forest vegetation, thusincreasing the number, frequency, size, intensityand duration of fires.

In 1997, wildfires raged in Indonesia, Papua NewGuinea, Australia, Mongolia, the RussianFederation, Colombia, Peru, Kenya, Rwanda andother parts of Africa. By mid-1998, fires werereported in Indonesia, the Amazon, Mexico andCentral America, the United States, westernCanada, far-eastern Russia and parts of Europe.National disasters were declared in many of theseplaces and national and international resourceswere mobilized to fight the fires. Neighbouringcountries and international and non-governmentalorganizations (NGOs) all responded. In March1998, the Secretary-General of the United Nationsrequested the United Nations EnvironmentProgramme (UNEP) to coordinate the UN system’sresponse to the situation arising from the outbreakof forest fires in Indonesia.

Few global figures are available on the extent ofthe 1997-1998 fires and associated loss of life,economic damage and environmental impacts.

The largest areas of forests burned in Brazil andIndonesia. Low rainfall in much of the Amazonattributed to the El Niño weather patterncontributed to a prolonged fire season (beyond theusual July to early October period) and anunusually high number of fires. In 1997, over

FIGURE 2Forest area in 1995 as compared with 1980

Temperate/borealNorth America, 13.2%(457 million ha)

Europe, 27.0%(933 million ha)

Africa, 15.1%(520 million ha)

Latin America andthe Caribbean, 27.5%(950 million ha)

Total area (1995): 3 454 million haDeveloped countries: 1 493 million haDeveloping countries: 1 961 million ha

Asia/OceaniaDeveloping: 14.2% (491 million ha)Developed: 3.0% (103 million ha)

Percentage of 1980 forest area

Latin

Am

eric

aan

d th

e C

arib

bean

Dev

elop

ing

wor

ld

Afr

ica

Dev

elop

ing

Asi

a/O

cean

ia

Aus

tral

ia, J

apan

and

New

Zea

land

Dev

elop

edw

orld

Tem

pera

te/b

orea

lN

orth

Am

eric

a

Euro

pe

6

4

2

0

-2

-4

-6

-8

-10

-12

4.1

2.6

1.0

2.7

-6.4

-10.5-9.7

-9.1

PART I SITUATION AND PROSPECTS FOR FOREST CONSERVATION AND DEVELOPMENT 3

2 million hectares of rain forest in Brazil burned(Schemo, 1998). Analysis of satellite data from theUnited States National Oceanic and AtmosphericAdministration showed an increase of over50 percent in the number of fires from July toNovember 1997 compared with the same periodin 1996, and an 86 percent increase in a 100-dayperiod (June to early September) in 1998 comparedwith the same period in 1997 (Schwartzman, 1998).Most of the fires occurred in Mato Grosso andPará states.

Some Brazilian forests of particular ecological orcultural significance were affected. In March 1998,fires burned over 600 000 ha of rain forest inRoraima, including parts of the Yanomami Indianreserve, near the border with Venezuela (Schemo,1998). In late September 1998, raging fires destroyeda large area of Brasilia National Park – a sanctuaryfor rare species from Brazil’s central savannahregion – killing wildlife and smothering theBrazilian capital with smoke. Earlier in the month,fire in the state of Mato Grosso threatened to moveinto Xingu National Park, home to 17 indigenousgroups, until rains extinguished the fire.

In Indonesia the fires of 1997-1998 burned millions

of hectares in Sumatra and Kalimantan. The exactarea is still unknown. One estimate is that about2 million hectares (including savannah withgrassland) burned in 1997 alone. Severalorganizations have begun the lengthy and complextask of interpreting satellite images to determinethe total area burned (Schweithelm, 1998). Largequantities of smoke generated by ground fires fedby slow burning fuels affected neighbouringcountries, influencing human health, interferingwith transportation systems and disrupting themulti-million-dollar tourist industry, all of whichcontributed significantly to the economic and socialcost of the fires. Many underground fires continuedto burn into mid-1998 in natural peat and coal beds,threatening new outbreaks of fire.

A representative sample of forest fires elsewherein the world includes the following:

• Fires in Mexico and Central America burned areported 1.5 million hectares. These generatedlarge quantities of smoke which blanketed theregion and spread into the United States as faras Chicago.

• From January to June 1998, about 13 000 firesburned in Mexico alone, consuming nearly

and the Philippines in both seasons and in southeastern Africa

and northern Brazil during the northern winter season, and

Indian monsoon rainfall was lower in the northern summer

season. The record-high global temperatures in 1998 were

also believed to be linked to El Niño. La Niña started to develop

in mid-1998. Climatic anomalies in 1998 which may be

associated with La Niña include dry conditions in parts of

South America; wetter than normal conditions in northern

Australia and the Philippines; above-normal rainfall during

the southwest monsoon in India; increased hurricane activity

in the Caribbean and Central America; dry spells in parts of

Argentina and Chile; above-normal rainfall in southern Africa,

with the exception of Zimbabwe; and possibly drier than

normal conditions in the Horn of Africa.

The El Niño Southern Oscillation (ENSO) is a periodically

occurring oceanic-atmospheric phenomenon. It consists of

El Niño, a “warm phase” or a large-scale warming in the

equatorial Pacific Ocean, and La Niña, a “cool phase” in which

surface waters of the central Pacific Ocean are colder than

normal. These phases are closely associated with changes in

atmospheric conditions (Southern Oscillation). ENSO events

occur on average every four years and typically last 14 to

22 months. They exhibit certain characteristic rainfall and

temperature anomalies. The El Niño that began in March 1997

and continued until mid-1998 is believed to have been one

of the most severe in recorded history. It had a pronounced

impact on weather and climate around the globe. While some

parts of the world received more rain than normal, abnormally

dry conditions occurred across northern Australia, Indonesia

BOX 1The 1997-1998 El Niño southern oscillation: El Niño and La Niña

4 STATE OF THE WORLD’S FORESTS 1999

500 000 ha and killing more than 70 fire-fighters and local residents.

• Between December 1997 and April 1998, morethan 13 000 fires burned in Nicaragua, the mostin any Central American country, destroyingvegetation on more than 800 000 ha of land.The Nicaraguan Ministry of Environment andNatural Resources (MARENA) recorded over11 000 fires in the month of April 1998 alone.

• In the southeastern United States, severe firesin Florida in 1998 burned a reported 200 000 haof forest by May (The Economist, 4-10 July 1998).

• More than 150 000 ha of coniferous forest andfarmland were burned in various parts ofGreece in August 1998, including the blackpine forest on Mount Taygetos, site of morethan 160 endemic species and 36 endangeredspecies of fauna (Guardian Weekly, 30 July 1998).

• In July 1998, devastating forest fires affectedmore than 100 000 ha in far-eastern Russia.Coniferous forest burned in more than 150places around Vladivostok, Sakhalin andKamchatka Peninsula. Fires in the southwest ofthe Volgograd region destroyed 9 000 ha offorest, at an estimated cost of US$6 million(BBC World Service, 27 July 1998). InSeptember, fires swept across Russia’s Pacificisland of Sakhalin, burning over 25 000 ha bythe end of the month (Reuters News Service,21 September 1998).

Active media coverage of the unusually largefires in Indonesia, the Amazon and Mexicoincreased public awareness of these predominantlyman-made environmental disasters. The smokefrom the fires, which endangered public health andeconomies beyond national borders, also helpedfocus public attention on the fires and the need todeal with policy issues related to fire outbreaks.

The use of fire is an integral part of landmanagement in both agriculture and forestry. Someforests are ecologically adapted to fire, andprescribed burning is an important component offorest management practices in some places.However, there is ample evidence that a largeproportion of the wildfires that occur each year arecaused by human intervention. A seven-year fieldstudy of fire in the Amazon carried out by theWoods Hole Research Center, United States, shows

that about half of the wildfires in the region werecaused by fires set by farmers and ranchers to clearold cattle pasture and to burn newly cut forestwhich subsequently burned out of control. Theeffects of drought in 1997-1998 were aggravated byshifting cultivation (particularly slash-and-burnagricultural practices), pasture management,improperly executed timber harvesting operationsand large-scale land clearance under agriculturalconversion schemes. A considerable number of firesthat burned around the world in 1997-1998 (as inother times) were cases of arson. The fires of 1997-1998 clearly highlight the need to improve planningand management of agricultural land use practicesto reduce the risk of wildfires; to addressdeficiencies in forest management systems; and toexamine policies and regulations related both toconversion of forest land to agriculture and toimprovement of forest stewardship.

The fires of 1997 and 1998 have stimulatedvarious international efforts related to fires. Aglobal system of early warning to indicate thepotential fire risk related to climatic conditions isbeing investigated by several internationalorganizations, including the World HealthOrganization (WHO), the World ConservationUnion (IUCN), UNEP and FAO. A national systemfor advance warning by radio linked tometeorological forecasts from satellite imagery hasbeen successfully tried in Burkina Faso. WHO hasproduced guidelines for forest fire emergencies.Many national and international meetings wereorganized in 1998 for fire-fighting and healthexperts, potential donors and, perhaps moresignificant, policy-makers to address the control,effects and underlying causes of fires. UN agenciesthat organized fire meetings in 1998 include UNEPand the United Nations Office for the Coordinationof Humanitarian Affairs (Geneva, Switzerland,April 1998), WHO and the Pan-American HealthOrganization (Lima, Peru, August 1998) and FAO(Rome, October 1998, on public policies affectingforest fires).

Apart from the fires, 1998 was notable for anothertype of disaster which severely affected forests: ice.A series of ice storms in January 1998 resulted inextensive damage to forests in the northeasternUnited States and eastern Canada (see Box 2). An

PART I SITUATION AND PROSPECTS FOR FOREST CONSERVATION AND DEVELOPMENT 5

estimated 10 million hectares of forests and treeswere affected, extending from Ontario to Quebecand New Brunswick in Canada and across northernNew England in the United States (Irland, 1998).

While less visible than the wildfires and icestorms within the last two years, recent outbreaksof insect pests and diseases in forests may result insubstantial economic loss and environmentaldamage. Although insect pests and diseases areoften integral components of forest dynamics,severe outbreaks can be damaging and requirecostly control efforts. Their incidence and economicimpact may be highest on plantations establishedfor the purpose of wood production. Some newpest outbreaks reported in the last few years arenoted in Box 3.

Climatic extremes associated with El Niño in1997-1998 (see Box 1) are thought to be linked tosome of the current severe pest outbreaks affectingforests and trees. For example, a serious outbreak ofgypsy moth (Lymantria dispar) which is posing arisk to northern European forests is believed tohave been exacerbated by increased temperaturesand prolonged drought conditions over the last twoyears. The outbreak, which started in 1996 and wasstill ongoing in mid-1998, is affecting thousands ofhectares of valuable hardwoods (particularly oaks)in Bulgaria, Croatia, Romania and Serbia.

STATUS OF EFFORTS TO ASSESS GLOBALFOREST RESOURCESForest resources assessmentForest resources assessments generally provideinformation on forest extent and location, types,condition, wood volume, and/or biomass. Theymay be done on a subnational, national, regional orglobal level. Global assessments are done in one oftwo ways: using a bottom-up approach whichharmonizes and sums national statistics, or using atop-down approach in which data are generated atthe regional, continental or global level. Nationalforest inventories are fundamental to bottom-upapproaches to forest resources assessment(see Box 4).

The major global forest cover assessment effortsare being carried out by FAO, the InternationalGeosphere-Biosphere Programme (IGBP), theEuropean Commission’s Joint Research Centre

BOX 2Effects of the ice storm in the northeastern

United States in January 1998

In January 1998, in what meteorologists called a “100-year

event”, a series of ice storms blanketed northern New England

and New York with up to 7.5 cm of ice. Nearly 7 million

hectares of rural forests and urban trees across the states of

Maine, New Hampshire, Vermont and New York were affected.

Some 2 million hectares were severely damaged. Hardwood

species suffered most. Estimates for natural resource losses

exceeded US$1 000 million. The effects of the storm remain:

thousands of kilometres of forest roads and trails are littered

with debris; many rural landowners will lose forest income;

management plans may be obsolete and need costly revision;

and debris increases the risk of insect pest outbreaks and fire.

Source: USDA Forest Service, 1998.

BOX 3Recent insect pest and disease outbreaks

In the Philippines, new insect pest outbreaks include the moths

Nyctalemon spp. on Endospermum peltatum and Xyleutes spp.

on Gmelina arborea, which are affecting plantations, and the

scolytid beetle Dryocoetiops laevis on Dipterocarpus

grandiflorus in secondary forests. The giant wood moth

(Endoxyla spp.) and the cerambycid beetle (Phoracantha spp.)

are becoming significant new threats to eucalyptus plantations

in Queensland, Australia. The Asian long-horned beetle,

Anoplophora glabripennis, is affecting urban hardwoods in

New York and Chicago, United States. The gypsy moth

(Lymantria dispar) is affecting thousands of hectares in eastern

Europe and Turkey. New disease problems include

Phythopthora spp. on Elmerrillia seedlings in Indonesia and

root rot of Acacia mangium in the Philippines caused by

Phellinus noxius.

(JRC) and the World Conservation MonitoringCentre (WCMC). FAO and WCMC mainly use abottom-up approach, which provides the most

6 STATE OF THE WORLD’S FORESTS 1999

detail at the country level. IGBP and JRC use a top-down method, which provides spatial informationon forest cover over broad areas. The FAO, JRC andIGBP assessments are ongoing, long-termprogrammes.

Currently available information. FAO, incollaboration with other partners, has beenconducting global forest resources assessmentsabout every ten years since 1947. The latest ForestResources Assessment (FRA), which was done for1990, was carried out jointly by FAO, the UnitedNations Economic Commission for Europe (ECE)and their member countries (FAO, 1995).2 FRA 1990was divided into two parts: one for theindustrialized countries (the temperate and borealforests) and the other for developing countries(mainly tropical and subtropical, but also sometemperate forests). ECE and FAO conducted thetemperate/boreal forest resources assessment(TBFRA) through the use of a questionnaire. Thetropical assessment was based on existing reliable

information and a remote-sensing-based samplingdesign for study of land cover changes. Theassessment for developing countries producedinformation primarily about the area of forest in1990 and the change since 1980, with data fromdifferent years adjusted to these reference points.This information is available by country and byecofloristic zone. TBFRA includes data on state andchange of forest area (which have not been adjustedto a given reference year) and gives additionalinformation on ownership and management status,growing stock, annual growth and fellings. FRA1990 is currently the most comprehensive source ofglobal-, regional- and national-level information onforest state and change available. It does not,however, show the spatial distribution of forests.

Since FRA 1990, new information requirementshave emerged, including location-specific or spatialdata which support efforts in sustainable forestmanagement and assessment of forests’environmental functions (e.g. conservation ofbiological diversity, mitigation of global climatechange). As a consequence, several groups,including IGBP, JRC and WCMC, have embarkedupon additional global assessments of forest coverand deforestation. All are assessing various aspectsof the spatial distribution of forest cover, althoughnone are as comprehensive as the FRA programmeor present the same information.

IGBP, an international consortium of scientificorganizations, developed a global low-resolutionsatellite image-mapping project. The work is basedon interpretation and classification of advancedvery-high-resolution radiometer (AVHRR) satelliteimagery which has a 1-km resolution. The IGBPland cover data set and maps and a related GlobalLand Cover Characterization database are beingvalidated. While the main objective of these projectsis not to provide information on forest area per se,estimates of forest area may be generated from thedatabase and biomass estimates may be derivedfrom modelling.

The JRC TREES (Tropical Resources andEnvironment monitoring by Satellites) project,

2 A partial, interim assessment using modelling was done forforest cover and forest cover change for the reference year 1995;the results were published in SOFO 1997.

BOX 4Importance of forest inventories as a basis

for sustainable forest management

Forest inventories and statistical systems serve as the foundation

of sound policies to support sustainable forest management.

Integrating social, economic and environmental concerns into

forest-sector planning requires a great deal of information on

forests, across the landscape and through time. Studies

repeatedly come to the same conclusion: much better

information is needed on the quantity, quality and use of forests.

Despite growing demands for better information, investments

in even basic forest inventories are declining. Many countries

have not conducted a comprehensive and statistically sound

forest inventory since the 1970s or early 1980s. In other

countries, physical inventories are declining in frequency and

intensity and are being replaced by modelling. New methods,

such as remote sensing, are expanding the ability to observe

large changes in land cover. Still, without reasonably current

forest inventories, it is increasingly difficult to assess change

in forest quality and function and to draw useful conclusions

about the sustainability of use.

PART I SITUATION AND PROSPECTS FOR FOREST CONSERVATION AND DEVELOPMENT 7

established in 1991, develops forest coverassessment techniques for the tropical belt. Theproject includes:

• a baseline inventory of forest area (using amultispectral 1-km AVHRR data set);

• continuous monitoring which would directattention to the areas undergoing the mostactive land cover change (i.e. deforestation);

• analysis of the derived information in terms ofspatio-temporal patterns of deforestationthrough the comprehensive Tropical ForestInformation System (TFIS).

A multiyear set of AVHRR data was acquiredover the whole tropical belt during the period 1991-1994. This global assessment has been furthercalibrated using high-resolution image maps forselected sites. The main outputs of this effortinclude a global tropical forest cover base map at1-km resolution (the first such forest map at thisresolution) and related figures at the regional tonational levels.

The second phase (1996-1999) of the TREESproject is directed at developing a prototype thatcan regularly produce relevant and accurateinformation on the state of tropical forestecosystems. A panel of international experts hasidentified “hot spots” where deforestation is themost active. JRC is developing more automaticmethods of forest monitoring using a range ofremote-sensing and other spatial data and hasdeveloped a new sampling scheme to measurechanges using different types of high-resolutionsatellite imagery.

TFIS organizes the data (remote-sensing orcartographic) and current knowledge (reports, fieldobservations, etc.) in a systematic manner. Work isbeing done to allow an interface between TFIS andinformation systems of the European Commissionand other regional and international organizations.

In 1996, WCMC, in collaboration with the WorldWide Fund for Nature (WWF), compiled a WorldForest Map showing forest extent and protectedareas with forested land. The map is the product ofa global geographic information system (GIS)containing more detailed maps and digital filesfrom the best available national and internationalsources, compiled mainly between the early 1980sand early 1990s by WCMC in collaboration with

IUCN. WCMC used a nominal scale of 1:1 million,adjusting input data of varying scales (rangingfrom 1:100 000 to 1:5 million).

The digital information was used to estimate thearea of each major forest type in the world underprotection and to provide a baseline for futuremonitoring of forests. The spatial data have formedthe basis for a major statistical analysis of forestprotection in the world, carried out by WCMC inconjunction with the Center for InternationalForestry Research (CIFOR), and have beenpublished on CD-ROM. The digital map ismaintained at WCMC.

WCMC recently produced a new set of national-level forest statistics derived from the land covermaps overlaid with the political boundaries ofcountries. This could provide area estimates at thenational level.

WCMC has also developed a GIS databaseshowing an estimate of forest cover some8 000 years ago for the World Resources Institute(WRI) and WWF. Using the data from WCMC,WRI, under its Frontier Forests Initiative,3

developed another global map comparing the largetracts of forest lands remaining today with thoseexisting 8 000 years ago. The Frontier ForestsInitiative assessed three attributes: historic forestlost, forest condition (the amount of the world’scurrent forest cover remaining in large tracts ofintact natural forest) and threats to frontier areas.The WRI/WCMC map may be considered a globalassessment of natural forest change over a largetime span.

As a follow-up, WRI has launched the majorGlobal Forest Watch project to monitor forestdevelopment globally. Currently WRI is workingwith some 20 NGO partners in Cameroon, Gabon,Canada and Indonesia to map concessions, roadsand other developments. The goal is to carry out asimilar effort in all major forested countries withinthe next five years.

Each of the above-mentioned efforts usesdifferent definitions, sources and methods forclassifying the vegetation. Their estimates of forest

3 The Frontier Forests Initiative is a five-year, multidisciplinaryeffort to promote stewardship in and around the world’s lastmajor frontier forests by investment, policy and public opinion.

8 STATE OF THE WORLD’S FORESTS 1999

cover are thus not directly comparable. The qualityof information from any assessment dependslargely on the quality of the basic input data. Themaps from WCMC and WRI were compiled fromexisting data sources, which could reflect landcover, land use and/or land potential.Consequently, they suffer from the same problems ofharmonization as do most bottom-up approaches.

The Global Observation of Forest Cover (GOFC),a new effort of an international partnership ofinstitutions including FAO, will build on previousglobal forest assessments using earth satellites.GOFC has a goal of stimulating the production ofglobally consistent products derived from satellitedata, supplemented by in situ data, by 2002. Thiswill be achieved by facilitating the provision offorestry information and satellite data toorganizations such as FAO and UNEP, the GlobalClimate Observing System (GCOS) and the GlobalTerrestrial Observing System (GTOS), NGOs andnational forest ministries through partnershiparrangements with space agencies.

Information to be available through FRA 2000. TheFAO Global Forest Resources Assessment 2000(FRA 2000) will be the most comprehensive andcomplete assessment yet. As envisioned, FRA 2000will consist of:

• a common set of definitions and standards forboth tropical and temperate/boreal forests;

• a common set of parameters to be assessed,including not only the traditional timberinformation, but also information, whereavailable, on non-wood forest products,naturalness, biological diversity, protectedareas, carbon sequestration functions, forestcondition and socio-economic functions;

• a remote-sensing-based “wall-to-wall” globalforest map keyed to forest classes used in theassessment, an ecoregion map and a databaseat 1-km resolution;

• a global sample of satellite data to measurechanges in forest cover over the past 20 years.

As the data will be spatially registered,researchers may be able to measure changes in landcover over time; thus a base may be established forimproved comparisons for beyond 2010.

FRA 2000 will make further improvements on the

data-gathering techniques used in 1990 and willalso make use of the data and technologies of otherorganizations. FAO will use some of the imageryand GIS data sets of IGBP, JRC, the Earth ResourcesObservation Systems (EROS) Data Center of theUnited States Geological Survey and others todevelop the global forest cover map and databasefor FRA 2000.

EROS Data Center, FAO and WCMC aredeveloping the Global Forest Map, which will bethe first globally consistent small-scale mapshowing forest cover distribution. The map is beinggenerated through refinement and modelling ofIGBP’s Global Land Cover Characterizationdatabase using advanced image processing and GIStechniques, combined with validation by nationalexperts and existing reliable information.

In the past, an update on global forest resourceswas possible only every ten years. Institutionaldevelopment and communication technologies mayeventually make it possible to have much morefrequent updates and much better quality of data.While technological gains have improved theprecision of the estimates and the range ofinformation that can be collected, many countriesstill need assistance in the planning, execution andfinancing of their own national forest inventories.

These assessment efforts will continue to providevital information on the location and extent offorests at the global level. Even more valuable willbe the information on net change in extent andcondition of forests over time, which addresses theheart of the problem – what is happening to theworld’s forests and consequently to forests’ abilityto provide the range of goods and servicesdemanded of them.

Assessments of forest-based biological diversityNatural forests are arguably the single mostimportant repository of terrestrial biologicaldiversity (diversity of ecosystems, species andgenetic resources). Diversity is an essential factor inmaintaining forest function. Conservation andmanagement of biological diversity are, therefore,important issues in forest planning. Global,regional and national planning, priority-setting anddecision-making related to the conservation ofbiological diversity all depend on an understanding

PART I SITUATION AND PROSPECTS FOR FOREST CONSERVATION AND DEVELOPMENT 9

of the distribution of species and ecosystems, theirprotection status and the threats to them, and oninformation on the status of the conservation anduse of forest genetic resources.

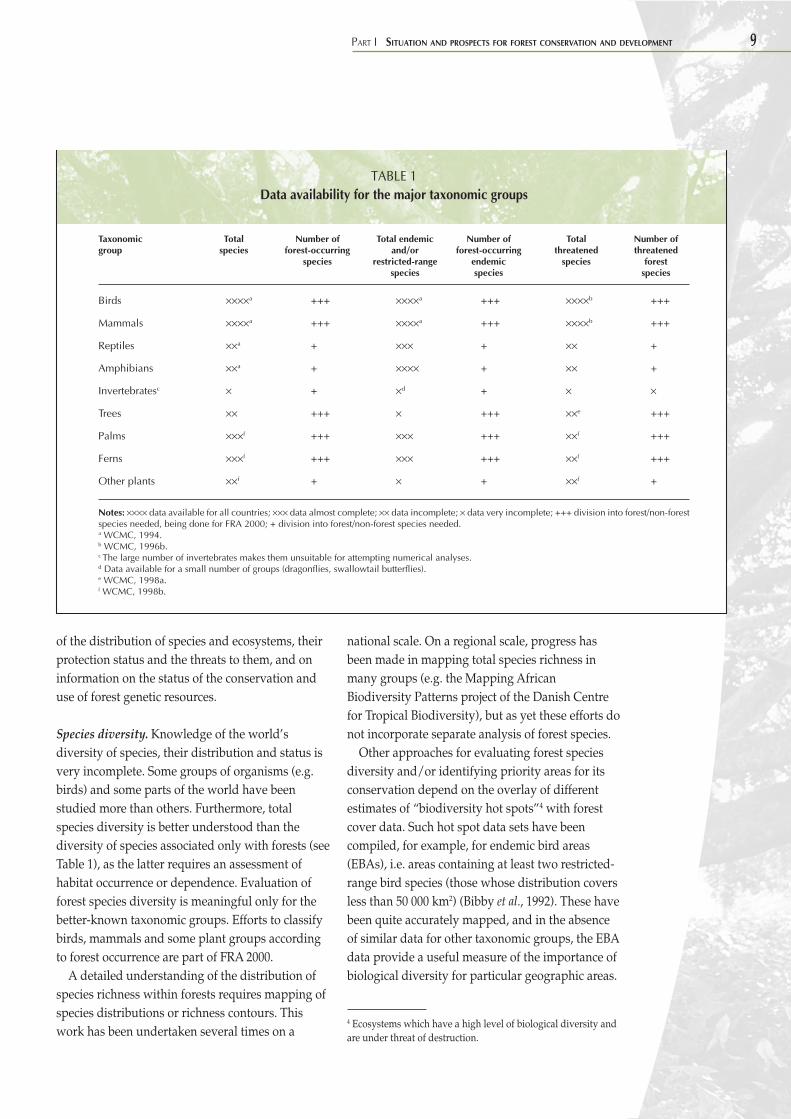

Species diversity. Knowledge of the world’sdiversity of species, their distribution and status isvery incomplete. Some groups of organisms (e.g.birds) and some parts of the world have beenstudied more than others. Furthermore, totalspecies diversity is better understood than thediversity of species associated only with forests (seeTable 1), as the latter requires an assessment ofhabitat occurrence or dependence. Evaluation offorest species diversity is meaningful only for thebetter-known taxonomic groups. Efforts to classifybirds, mammals and some plant groups accordingto forest occurrence are part of FRA 2000.

A detailed understanding of the distribution ofspecies richness within forests requires mapping ofspecies distributions or richness contours. Thiswork has been undertaken several times on a

national scale. On a regional scale, progress hasbeen made in mapping total species richness inmany groups (e.g. the Mapping AfricanBiodiversity Patterns project of the Danish Centrefor Tropical Biodiversity), but as yet these efforts donot incorporate separate analysis of forest species.

Other approaches for evaluating forest speciesdiversity and/or identifying priority areas for itsconservation depend on the overlay of differentestimates of “biodiversity hot spots”4 with forestcover data. Such hot spot data sets have beencompiled, for example, for endemic bird areas(EBAs), i.e. areas containing at least two restricted-range bird species (those whose distribution coversless than 50 000 km2) (Bibby et al., 1992). These havebeen quite accurately mapped, and in the absenceof similar data for other taxonomic groups, the EBAdata provide a useful measure of the importance ofbiological diversity for particular geographic areas.

4 Ecosystems which have a high level of biological diversity andare under threat of destruction.

TABLE 1Data availability for the major taxonomic groups

Taxonomic Total Number of Total endemic Number of Total Number ofgroup species forest-occurring and/or forest-occurring threatened threatened

species restricted-range endemic species forestspecies species species

Birds ××××a +++ ××××a +++ ××××b +++

Mammals ××××a +++ ××××a +++ ××××b +++

Reptiles ××a + ××× + ×× +

Amphibians ××a + ×××× + ×× +

Invertebratesc × + ×d + × ×

Trees ×× +++ × +++ ××e +++

Palms ×××f +++ ××× +++ ××f +++

Ferns ×××f +++ ××× +++ ××f +++

Other plants ××f + × + ××f +

Notes: ×××× data available for all countries; ××× data almost complete; ×× data incomplete; × data very incomplete; +++ division into forest/non-forestspecies needed, being done for FRA 2000; + division into forest/non-forest species needed.a WCMC, 1994.b WCMC, 1996b.c The large number of invertebrates makes them unsuitable for attempting numerical analyses.d Data available for a small number of groups (dragonflies, swallowtail butterflies).e WCMC, 1998a.f WCMC, 1998b.

10 STATE OF THE WORLD’S FORESTS 1999

Other hot spot data sets include WCMC andIUCN’s Centres of plant diversity (WWF/IUCN,1994), WWF-US’s Global 200 ecoregions5 andConservation International’s Hotspots.6

Mapping could also be used to identify areaswhere threatened and endangered forest species areconcentrated. This would require categorization ofspecies according to their forest occurrence and,ideally, relatively detailed data on theirdistributions. Nonetheless, some advances could begained simply from addressing presence/absencedata at the national or provincial level.

A country may have high forest species diversityeither because it has a wide range of different foresttypes each with its own distinct biota (e.g. theUnited States) or because individual forest typesare highly diverse in species (e.g. some lowlandtropical moist forest). The former characteristic isgenerally related to the size of the country, the latternot necessarily so. Countries with very high forestdiversity usually combine the two characteristics.

Forest ecosystem diversity. Ecosystem diversity inforests is important not only in its own right butalso as a predictor of species diversity. However,assessing ecosystem diversity requires meaningfulsystems of classification of forests, and these areincreasingly difficult to generate as thegeographical scale increases. Scientists may developschemes that are useful in local or national contextsfor expressing differences between forestecosystems, based on combinations ofphysiognomy, phenology and floristics. However,harmonizing several different schemes to produceoverviews on a continental or global scale is adifficult task which may entail so muchsimplification as to eliminate any real utility inexpressing ecosystem diversity.

For example, the harmonization of forest coverdata from 70 different sources to produce the firstglobal map of closed forest distribution, The WWFworld forest map (WCMC, 1996a), resulted in asimplistic classification with only five classes(temperate needleleaf, temperate broadleaf andmixed, tropical moist, tropical dry and mangroveforests), reflecting the difficulty of combining themany much more detailed classification systemsused throughout the world. A more detailed

classification involving 25 classes which was usedby WCMC and CIFOR in the production of asubsequent digital data set on global forest cover(Iremonger, Ravilious and Quinton, 1997) is moremeaningful in biodiversity terms but is still verysimplistic.

Remote sensing data are potentially a powerfulsource of information on forest ecosystemdistribution and diversity. However, manyregionally focused programmes, such as TREES andPathfinder,7 have been forced to use simplifiedclassification schemes because of the analyticalcomplexity of extracting more detail from satellitedata. Global satellite-derived land cover data areavailable from the EROS Data Center inpreliminary form. This data set helps to provide aconsistent global view of forests’ location andinformation about their diversity according to anumber of classification schemes ranging from thesimple to the complex, based on phenology as wellas spectral response. The greatest advance inexamining forest ecosystem diversity on a broadgeographic scale is likely to come through thecombination of remote sensing data withecoregional classifications as envisaged in FRA 2000.

Forest genetic resources. FAO, the InternationalPlant Genetic Resources Institute (IPGRI) and theInternational Centre for Research in Agroforestry(ICRAF) are facilitating regional initiatives to assessthe status of genetic resources of forest trees atspecies and provenance levels; to identify gaps oroverlaps in protection and development efforts; andto elaborate action plans for the conservation,management, sustainable utilization andenhancement of genetic resources of priorityspecies. Regional syntheses will be prepared fromdata provided by the countries.

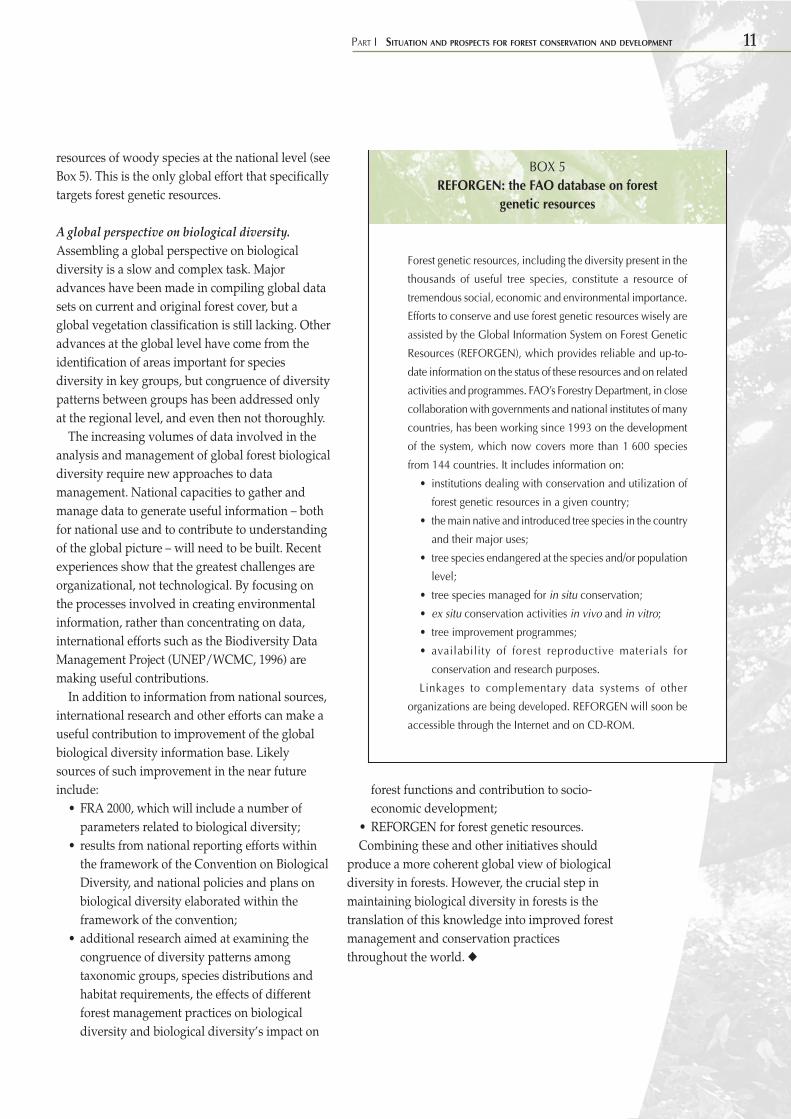

At the global level, FAO is developing the GlobalInformation System on Forest Genetic Resources(REFORGEN) for monitoring the status of genetic

5 See WWF-US’s Web site: http://www.worldwildlife.org.6 For more information, see Conservation International’s Website: http://www.conservation.org.7 Pathfinder is the Humid Tropical Forest Inventory Project, acollaborative research effort of the University of NewHampshire, the University of Maryland and the NationalAeronautics and Space Administration, United States.

PART I SITUATION AND PROSPECTS FOR FOREST CONSERVATION AND DEVELOPMENT 11

resources of woody species at the national level (seeBox 5). This is the only global effort that specificallytargets forest genetic resources.

A global perspective on biological diversity.Assembling a global perspective on biologicaldiversity is a slow and complex task. Majoradvances have been made in compiling global datasets on current and original forest cover, but aglobal vegetation classification is still lacking. Otheradvances at the global level have come from theidentification of areas important for speciesdiversity in key groups, but congruence of diversitypatterns between groups has been addressed onlyat the regional level, and even then not thoroughly.

The increasing volumes of data involved in theanalysis and management of global forest biologicaldiversity require new approaches to datamanagement. National capacities to gather andmanage data to generate useful information – bothfor national use and to contribute to understandingof the global picture – will need to be built. Recentexperiences show that the greatest challenges areorganizational, not technological. By focusing onthe processes involved in creating environmentalinformation, rather than concentrating on data,international efforts such as the Biodiversity DataManagement Project (UNEP/WCMC, 1996) aremaking useful contributions.

In addition to information from national sources,international research and other efforts can make auseful contribution to improvement of the globalbiological diversity information base. Likelysources of such improvement in the near futureinclude:

• FRA 2000, which will include a number ofparameters related to biological diversity;

• results from national reporting efforts withinthe framework of the Convention on BiologicalDiversity, and national policies and plans onbiological diversity elaborated within theframework of the convention;

• additional research aimed at examining thecongruence of diversity patterns amongtaxonomic groups, species distributions andhabitat requirements, the effects of differentforest management practices on biologicaldiversity and biological diversity’s impact on

forest functions and contribution to socio-economic development;

• REFORGEN for forest genetic resources.Combining these and other initiatives should

produce a more coherent global view of biologicaldiversity in forests. However, the crucial step inmaintaining biological diversity in forests is thetranslation of this knowledge into improved forestmanagement and conservation practicesthroughout the world. ◆

BOX 5REFORGEN: the FAO database on forest

genetic resources

Forest genetic resources, including the diversity present in the

thousands of useful tree species, constitute a resource of

tremendous social, economic and environmental importance.

Efforts to conserve and use forest genetic resources wisely are

assisted by the Global Information System on Forest Genetic

Resources (REFORGEN), which provides reliable and up-to-

date information on the status of these resources and on related

activities and programmes. FAO’s Forestry Department, in close

collaboration with governments and national institutes of many

countries, has been working since 1993 on the development

of the system, which now covers more than 1 600 species

from 144 countries. It includes information on:

• institutions dealing with conservation and utilization of

forest genetic resources in a given country;

• the main native and introduced tree species in the country

and their major uses;

• tree species endangered at the species and/or population

level;

• tree species managed for in situ conservation;

• ex situ conservation activities in vivo and in vitro;

• tree improvement programmes;

• availability of forest reproductive materials for

conservation and research purposes.

Linkages to complementary data systems of other

organizations are being developed. REFORGEN will soon be

accessible through the Internet and on CD-ROM.

12 STATE OF THE WORLD’S FORESTS 1999

Sustainable forest management entails thebalancing of the economic, environmental and

social functions and values of forests for the benefitof present and future generations – a complex andchallenging task in the face of the Earth’s rapidlyexpanding population and increasing demands forforest products and services. However, a number ofpositive developments give cause for cautiousoptimism. Among these is the unprecedented levelof attention, energy and commitment fromthousands of formal and informal, global to local,governmental and non-governmental organizationsaround the world (see Part III for discussion ofinternational initiatives).

While frequent reference is made in the literatureto areas where forests are not being managed in asustainable manner, the magnitude of the problemglobally is not known at present. A previous studyby FAO (1982) estimated that less than 5 percent ofthe world’s tropical forest classified as productivewas under intensive management in 1980.8 FRA2000 will assess both quantitative and qualitativedata pertaining to sustainable forest managementworldwide. Recent figures indicate that almost allEuropean forests are managed,9 i.e. have a formal orinformal management plan for one or acombination of objectives (e.g. wood production,conservation of biological diversity, soil and waterconservation, recreation) (Third MinisterialConference on the Protection of Forests in Europe/Ministry of Agriculture, Rural Development andFisheries of Portugal, 1998a).

Sustainable management of forests implies theprovision of a range of goods and services. Whileall forests, by their nature, are multipurpose, andwhile more emphasis is given to management formultiple functions, most managed forests have aprimary management objective: production (ofwood and/or non-wood products), protection(mainly for soil and water conservation) orconservation (of biological diversity, culturalheritage sites, etc.). The following discussions of

natural forests and forest plantations focus onmanagement where wood production is theprimary objective, as issues related to timberharvesting are among the more contentious in theforest debate today. Social and environmentalfunctions of forests are treated in a subsequentsection.

MANAGEMENT OF NATURAL FORESTSThere is a global commitment to improve themanagement of forests. This improvement entails arebalancing of forest management objectives, whichis bringing about changes in the way forests aremanaged and, in some places, a reallocation offorest areas between different uses. This may resultin reduced timber harvests in natural forests, butincreased production of other goods and services.Implementing sustainable forest management maylead to reduced volumes harvested in the shortterm, yet there is an expectation that it will increasewood supply over the long term.

Natural forest management is currently beingaffected by changes in resource availability,developments in management objectives andpractices, and institutional changes which have ledto a more diverse set of forest managers.

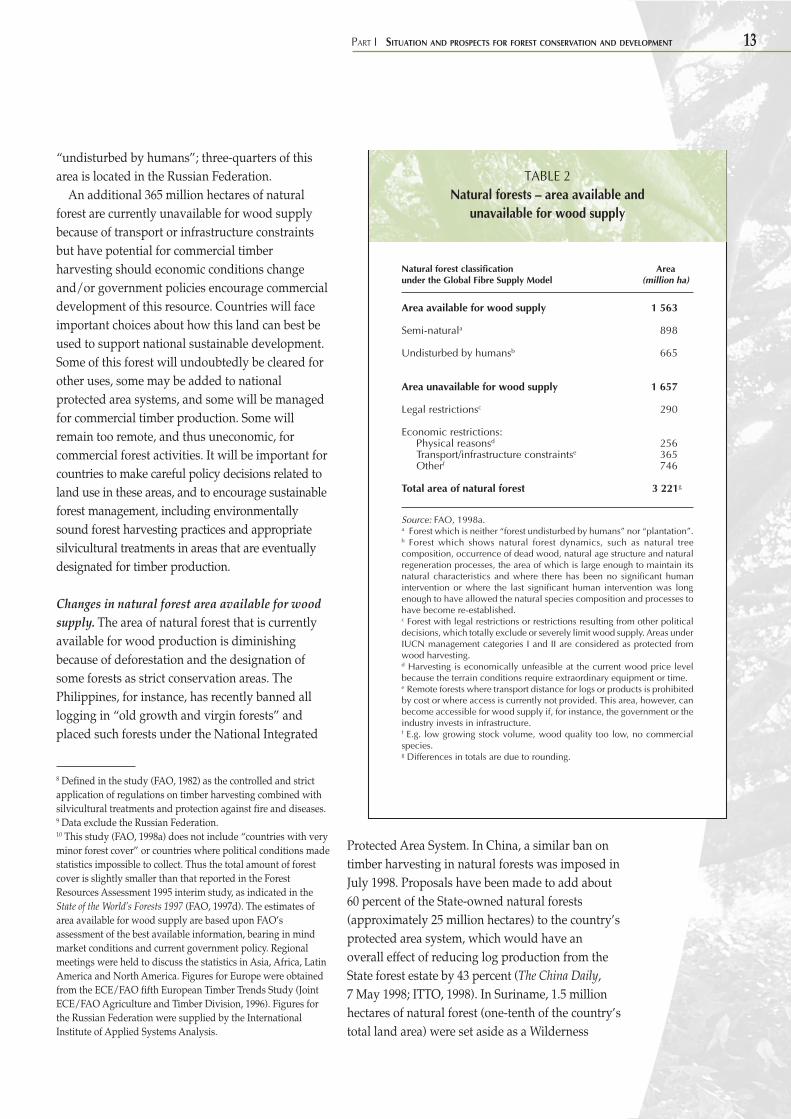

Trends in resource availability and in woodsupplyArea of natural forest available for wood supply.Nearly one-half (1 563 million hectares) of the areaof natural forests worldwide (an estimated3 221 million hectares) is considered to be availablefor wood supply under current legal and marketconditions (i.e. there are no legal restrictions andforest cover is both economically and physicallyaccessible) (FAO, 1998a)10 (see Table 2). Concernsrelated to timber harvesting and the need toencourage the use of environmentally sound forestharvesting practices apply to this area. At least42 percent (665 million hectares) of the areaavailable for wood supply is estimated to be

Status and trends in forestmanagement

PART I SITUATION AND PROSPECTS FOR FOREST CONSERVATION AND DEVELOPMENT 13

8 Defined in the study (FAO, 1982) as the controlled and strictapplication of regulations on timber harvesting combined withsilvicultural treatments and protection against fire and diseases.9 Data exclude the Russian Federation.10 This study (FAO, 1998a) does not include “countries with veryminor forest cover” or countries where political conditions madestatistics impossible to collect. Thus the total amount of forestcover is slightly smaller than that reported in the ForestResources Assessment 1995 interim study, as indicated in theState of the World’s Forests 1997 (FAO, 1997d). The estimates ofarea available for wood supply are based upon FAO’sassessment of the best available information, bearing in mindmarket conditions and current government policy. Regionalmeetings were held to discuss the statistics in Asia, Africa, LatinAmerica and North America. Figures for Europe were obtainedfrom the ECE/FAO fifth European Timber Trends Study (JointECE/FAO Agriculture and Timber Division, 1996). Figures forthe Russian Federation were supplied by the InternationalInstitute of Applied Systems Analysis.

TABLE 2Natural forests – area available and

unavailable for wood supply

Natural forest classification Areaunder the Global Fibre Supply Model (million ha)

Area available for wood supply 1 563

Semi-naturala 898

Undisturbed by humansb 665

Area unavailable for wood supply 1 657

Legal restrictionsc 290

Economic restrictions: Physical reasonsd 256 Transport/infrastructure constraintse 365 Otherf 746

Total area of natural forest 3 221g

Source: FAO, 1998a.a Forest which is neither “forest undisturbed by humans” nor “plantation”.b Forest which shows natural forest dynamics, such as natural treecomposition, occurrence of dead wood, natural age structure and naturalregeneration processes, the area of which is large enough to maintain itsnatural characteristics and where there has been no significant humanintervention or where the last significant human intervention was longenough to have allowed the natural species composition and processes tohave become re-established.c Forest with legal restrictions or restrictions resulting from other politicaldecisions, which totally exclude or severely limit wood supply. Areas underIUCN management categories I and II are considered as protected fromwood harvesting.d Harvesting is economically unfeasible at the current wood price levelbecause the terrain conditions require extraordinary equipment or time.e Remote forests where transport distance for logs or products is prohibitedby cost or where access is currently not provided. This area, however, canbecome accessible for wood supply if, for instance, the government or theindustry invests in infrastructure.f E.g. low growing stock volume, wood quality too low, no commercialspecies.g Differences in totals are due to rounding.

“undisturbed by humans”; three-quarters of thisarea is located in the Russian Federation.

An additional 365 million hectares of naturalforest are currently unavailable for wood supplybecause of transport or infrastructure constraintsbut have potential for commercial timberharvesting should economic conditions changeand/or government policies encourage commercialdevelopment of this resource. Countries will faceimportant choices about how this land can best beused to support national sustainable development.Some of this forest will undoubtedly be cleared forother uses, some may be added to nationalprotected area systems, and some will be managedfor commercial timber production. Some willremain too remote, and thus uneconomic, forcommercial forest activities. It will be important forcountries to make careful policy decisions related toland use in these areas, and to encourage sustainableforest management, including environmentallysound forest harvesting practices and appropriatesilvicultural treatments in areas that are eventuallydesignated for timber production.

Changes in natural forest area available for woodsupply. The area of natural forest that is currentlyavailable for wood production is diminishingbecause of deforestation and the designation ofsome forests as strict conservation areas. ThePhilippines, for instance, has recently banned alllogging in “old growth and virgin forests” andplaced such forests under the National Integrated

Protected Area System. In China, a similar ban ontimber harvesting in natural forests was imposed inJuly 1998. Proposals have been made to add about60 percent of the State-owned natural forests(approximately 25 million hectares) to the country’sprotected area system, which would have anoverall effect of reducing log production from theState forest estate by 43 percent (The China Daily,7 May 1998; ITTO, 1998). In Suriname, 1.5 millionhectares of natural forest (one-tenth of the country’stotal land area) were set aside as a Wilderness

14 STATE OF THE WORLD’S FORESTS 1999