shared service centers & in-house banks: trends in ... · shared service centers & in-house...

TRANSCRIPT

The Financial Professionals Forum 2012

Shared Service Centers & In-House Banks: Trends in Treasury and Working Capital Management

Shared Service Centers & In-House Banks: Trends in Treasury and Working Capital Management

Moderated by Michael Guralnick & Ron Chakravarti Panelists:

Marco Sandoval, Americas Head of Treasury Operations, Pfizer Eduardo Cataldi, Chief Financial Officer, Ingenico

Oscar Ducoing, Financial Operations Manager, Pemex Maria Simmons, Treasurer, Copa Airlines

Cassio Moura, Chief Financial Officer, PromonLogicalls

The Financial Professionals Forum 2012

The Financial Professionals Forum 2012

Table of Contents

1. Trends and Key Drivers of SSCs

2. What’s Next for SSCs

3. In-House Banking and Implications

The Financial Professionals Forum 2012

Cost Management - With revenue slowdown, cost efficiency is a focus, as centralized procurement and processing hubs provide savings

Visibility - Access to quality bank information and accurate cash flow forecasts is critical for control

Liquidity Efficiency - Drive towards better usage / redeployment of internal cash, for more efficient internal liquidity management, less reliance on external funding

Credit Crunch - With customers and suppliers impacted, attention on optimization of working capital management – both processes (payables and receivables) and financing (supplier financing and distribution financing)

Efficiency – Focus on rationalization of bank relationships (improving cash efficiency), which also makes it easier to centrally manage end of day cash positions (improving counterparty risk management)

Automation - Leveraging technology for efficiency, better workflow control, and provider independence – deployment of ERP / TMS, XML ISO 200022, SWIFTNet

Working Capital Efficiency Supply Chain Stabilization Operational Excellence

Trends Driving Treasury and Shared Service Centers The environment is driving continued focus on organizational efficiency and operational excellence.

1

The Financial Professionals Forum 2012

Cost Savings

Improved Control

Efficiency Gains

Superior ERP integration

Process Standardization

Shorter Cycle Times

More Timely Information

Clearer Accountability

Centers of Excellence

Leaves Business Units to focus on core activities

Promotes ‘One Company’ Model

Shared Service Centers (SSCs): Defined

Hard Benefits

Regulatory / Market Changes Need for greater transparency

Control of processes and data

Compliance with regulations

Cost Reduction Consolidation to execute transactions with fewer resources

Move to lower cost zones

Increased efficiency and economies of scale

Standardized Business Processes High quality and scalable processes

Leverage technology systems and ERP investments

Transfer of best practices

Banking Needs Consistency of products and services

Fewer banking relationships and accounts

Outsourcing of activities

Drivers Benefits

– Centralization – Standardization – Automation – Globalization

Scalable operating model : Citi’s SSC Clients Report Financial Savings of 30% – 40%.

Soft Benefits

SSC Model

Organizations use SSCs to reduce cost, gain process harmonization and efficiencies, and increase visibility & control.

2

The Financial Professionals Forum 2012

Working Capital Strategy

(DPO, DSO, CCC, Payment terms)

Process Efficiency (SSC, ERP,

Automation)

Banking Interface

(Paper vs. Electronic, STP,

Connectivity)

Balancing Operational Excellence & Working Capital Efficiency

SSCs supporting standardization, centralization and automation

Working Capital Strategy: Best in class entities… Support Treasury through improved

visibility and cash forecasting Rely on Treasury to play an advisory role

in working capital initiatives and bank relationships

Process Efficiency: Best in class entities… Centralize back-office and

compliance functions in low cost, politically stable environments

Leverage economies of scale to reduce processing cost

Quickly react to changes in environment or polices

Take full advantage of automation and centralized processing

Banking Interface: Best in class entities… Centralize payment

processes to reduce transaction costs and risks

Automate processes to initiate through the most efficient channels, without compromising control

Benchmark processes regularly to drive down costs, reduce cycle times, and increase error-free straight through processing

Organizations are seeking to achieve success across three areas – working capital strategy, processing efficiency and managing their banking interfaces. Best in class companies find a balance across these three areas and use SSCs to deliver results.

3

Panel Discussion on Trends and Key Drivers of SSCs

The Financial Professionals Forum 2012

The Financial Professionals Forum 2012

What’s Next For Shared Service Centers? Mature SSCs have delivered their promise of cost savings…So what’s next?

Off-shoring and Outsourcing Location, Location, Location SSC Hotspots Location Evolution Captive or Outsourced?

Finding More Savings Additional Cost Reduction Search for Incremental Savings Banking Solutions to Drive Further

Automation

Creating New Value Rising to the Economic Challenge New Customers, New Services Focus on Function -Supplier

Management From Cost Cutters to Strategic

Enablers The Strategic Value of SSC Data A New Culture for SSCs

New Perceptions of SSCs In Search of Best Practice From Support to Service Mechanisms to Keep SSCs Connected

to Their Customers Talent – a Challenge...

…or an Opportunity?

4

The Financial Professionals Forum 2012

According to Citi Treasury Diagnostics research, 67% of firms manage WC through shared service centers

However, according to recent research from Deliotte, only 8% of SSCs cover 4 or more continents, with 43% covering only a single country

Expanding the geographical coverage of an SSC to service more countries can be a logical way to increase the value of the SSC and deliver more cost savings and efficiencies

Many SSCs have experienced demand from new geographies due to macro-economic conditions – as business has scaled back in certain locations, an on-the-ground presence is no longer viable/necessary

Citi’s experience – based on capabilities in over 190 countries and 135 currencies, and SSC clients across every region – is that scalable solutions to expand your SSC’s reach is entirely feasible with minimal disruption

More Geographies – Expanding the Scope of Your SSC Expanding geographical coverage can be a powerful way to increase the value of existing SSCs and deliver further cost savings.

5

Single Country – 43%

Single Continent – 31%

2 Continents -12%

3 Continents – 6%

4+ Continents – 8% * Source: 2009 Global Shared Services Survey,

Deloitte Consulting

Panel Discussion on What’s Next for SSCs

The Financial Professionals Forum 2012

The Financial Professionals Forum 2012

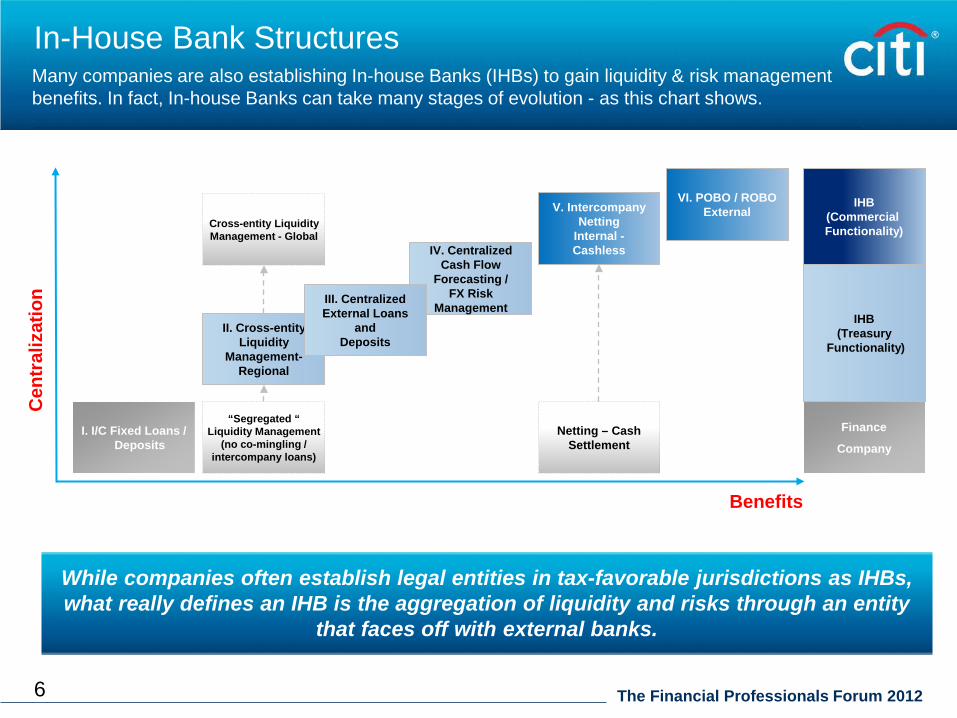

In-House Bank Structures Many companies are also establishing In-house Banks (IHBs) to gain liquidity & risk management benefits. In fact, In-house Banks can take many stages of evolution - as this chart shows.

6

I. I/C Fixed Loans / Deposits

II. Cross-entity Liquidity

Management- Regional

V. Intercompany Netting

Internal - Cashless

VI. POBO / ROBO External

Finance

Company

IHB (Treasury

Functionality)

IHB (Commercial Functionality)

Netting – Cash Settlement

Cen

tral

izat

ion

Benefits

“Segregated “ Liquidity Management

(no co-mingling / intercompany loans)

Cross-entity Liquidity Management - Global

IV. Centralized Cash Flow

Forecasting / FX Risk

Management

While companies often establish legal entities in tax-favorable jurisdictions as IHBs, what really defines an IHB is the aggregation of liquidity and risks through an entity

that faces off with external banks.

III. Centralized External Loans

and Deposits

The Financial Professionals Forum 2012

Model Business Units hold their operating

cash in pseudo-bank accounts within IHB

BUs transact with IHB to conduct internal Treasury deals - FX and investments/deposits

All BU / IHB transactions are done at “arms length”

External liquidity is concentrated at IHB through automated daily sweeps by bank

Only IHB deals with banks - owns all credit lines, does all external FX and Investment/Deposit deals

Commercial Transactions between BUs and IHB include Intercompany Netting, Payments on Behalf of, and Receipts on Behalf of

A “Highly Evolved” In House Bank IHBs are managed by Treasury to aggregate and net risks arising from the Trading Model - internally and with external counterparties. It minimizes banking transaction volume and costs. It also becomes the hub for information for working capital / commercial flows.

7

Legend 1. Interco txns

aggregated and settled to G/L (cash-less, wherever possible)

2. Liquidity aggregated, intercompany loans recorded on G/L

3. Net transactions with banks

I/C Trade Flows

Global or Regional Treasury Center

IHB

BU

BU

BU

BU

JV

Bank(s)

Liquidity Structure

Stand alone

accounts

Netting Center

Net MM & FX Trades

3

I/C trxns 1 Liquidity 2

3 Third party payments

POBO &ROBO

The Financial Professionals Forum 2012

SSC and Treasury Both centralized functions can work together to create greater efficiencies and benefits to each other and the firm as a whole.

8

SSC

Controllers / Working Capital Function

Payment Factory Netting Center Regional Treasury Center

In-house Bank

Treasury Function

SSC helps Treasury Supports bank consolidation and rationalization

processes

Centralized processing improves predictability and accuracy of cash forecasts, FX exposure forecasts

Potentially takes over Treasury back office functions such as FX settlements

Treasury system (TMS) links to SSC ERP for automated G/L entry of Treasury deals

Treasury helps SSC Establishes bank account structure to complement

SSC

Co-ordinates bank relationships for AR and AP

Serve as expert on policies for working capital (e.g.. payment terms) and banking aspects of SSC processing

Integrates processes with SSC as In-house Bank is implemented for greater W/C benefits

Panel Discussion on In-House Banking and Implications for SSCs

The Financial Professionals Forum 2012

efficiency, renewable energy & mitigation

In January 2007, Citi released a Climate Change Position Statement, the first US financial institution to do so. As a sustainability leader in the financial sector, Citi has taken concrete steps to address this important issue of climate change by: (a) targeting $50 billion over 10 years to address global climate change: includes significant increases in investment and financing of alternative energy, clean technology, and other carbon-emission reduction activities; (b) committing to reduce GHG emissions of all Citi owned and leased properties around the world by 10% by 2011; (c) purchasing more than 52,000 MWh of green (carbon neutral) power for our operations in 2006; (d) creating Sustainable Development Investments (SDI) that makes private equity investments in renewable energy and clean technologies; (e) providing lending and investing services to clients for renewable energy development and projects; (f) producing equity research related to climate issues that helps to inform investors on risks and opportunities associated with the issue; and (g) engaging with a broad range of stakeholders on the issue of climate change to help advance understanding and solutions.

Citi works with its clients in greenhouse gas intensive industries to evaluate emerging risks from climate change and, where appropriate, to mitigate those risks.

© 2012 Citibank, N.A. All rights reserved. Citi and Arc Design is a registered service mark of Citigroup Inc..

IRS Circular 230 Disclosure: Citigroup Inc. and its affiliates do not provide tax or legal advice. Any discussion of tax matters in these materials (i) is not intended or written to be used, and cannot be used or relied upon, by you for the purpose of avoiding any tax penalties and (ii) may have been written in connection with the "promotion or marketing" of any transaction contemplated hereby ("Transaction"). Accordingly, you should seek advice based on your particular circumstances from an independent tax advisor.Any terms set forth herein are intended for discussion purposes only and are subject to the final terms as set forth in separate definitive written agreements. This presentation is not a commitment to lend, syndicate a financing, underwrite or purchase securities, or commit capital nor does it obligate us to enter into such a commitment, nor are we acting as a fiduciary to you. By accepting this presentation, subject to applicable law or regulation, you agree to keep confidential the information contained herein and the existence of and proposed terms for any Transaction.Prior to entering into any Transaction, you should determine, without reliance upon us or our affiliates, the economic risks and merits (and independently determine that you are able to assume these risks) as well as the legal, tax and accounting characterizations and consequences of any such Transaction. In this regard, by accepting this presentation, you acknowledge that (a) we are not in the business of providing (and you are not relying on us for) legal, tax or accounting advice, (b) there may be legal, tax or accounting risks associated with any Transaction, (c) you should receive (and rely on) separate and qualified legal, tax and accounting advice and (d) you should apprise senior management in your organization as to such legal, tax and accounting advice (and any risks associated with any Transaction) and our disclaimer as to these matters. By acceptance of these materials, you and we hereby agree that from the commencement of discussions with respect to any Transaction, and notwithstanding any other provision in this presentation, we hereby confirm that no participant in any Transaction shall be limited from disclosing the U.S. tax treatment or U.S. tax structure of such Transaction. We are required to obtain, verify and record certain information that identifies each entity that enters into a formal business relationship with us. We will ask for your complete name, street address, and taxpayer ID number. We may also request corporate formation documents, or other forms of identification, to verify information provided.Any prices or levels contained herein are preliminary and indicative only and do not represent bids or offers. These indications are provided solely for your information and consideration, are subject to change at any time without notice and are not intended as a solicitation with respect to the purchase or sale of any instrument. The information contained in this presentation may include results of analyses from a quantitative model which represent potential future events that may or may not be realized, and is not a complete analysis of every material fact representing any product. Any estimates included herein constitute our judgment as of the date hereof and are subject to change without any notice. We and/or our affiliates may make a market in these instruments for our customers and for our own account. Accordingly, we may have a position in any such instrument at any time.Although this material may contain publicly available information about Citi corporate bond research, fixed income strategy or economic and market analysis, Citi policy (i) prohibits employees from offering, directly or indirectly, a favorable or negative research opinion or offering to change an opinion as consideration or inducement for the receipt of business or for compensation; and (ii) prohibits analysts from being compensated for specific recommendations or views contained in research reports. So as to reduce the potential for conflicts of interest, as well as to reduce any appearance of conflicts of interest, Citi has enacted policies and procedures designed to limit communications between its investment banking and research personnel to specifically prescribed circumstances.