seven point equity partners overview - september 2015

TRANSCRIPT

Introductory Materials

June 2015

Seven Point Overview

2

Private investment firm targe/ng long-‐term capital apprecia/on

Equity investments in lower middle market businesses with poten/al for excep/onal returns

Opera/onally focused, value-‐oriented “work boots” inves/ng strategy

North American focus, with global investment interest and capability

Founding principals are successfully execu/ng Seven Point strategy, building on strong investment track record

Talented Opera/ng Partners drive fundamental value crea/on

Lower Middle Market Opportunity

• North American lower middle market offers a large opportunity set, rich in targets ideally suited to Seven Point’s strategy

• There are an es/mated 146,000 companies in the middle market ($25M-‐$1B) space, represen/ng about $3 trillion in total revenues1.

• Size and scale of lower middle market companies favors investors like Seven Point, who can provide opera/onal capabili/es, not just capital

• Inefficient investment sector rela/ve to large buyout market, with greatest opportunity for proprietary sourcing

• Lower middle market is characterized by lower valua/ons and a\rac/ve risk/return profile

• Historically, investors focused on North American lower middle market have delivered higher returns than large buyout funds

3

1: The Market that Moves America: Insights, Perspec8ves, and Opportuni8es for Middle Market Companies, GE Capital and The Ohio State University Fisher College of Business, 2011.

Our Strategy: Value CreaBon

4

OperaBng Partner SelecBon

Macro and Sector Analysis

Sourcing and Due Diligence

Value CreaBon: ExecuBon

Exit

• Demonstrated career achievement in fundamental value crea/on

• Industry sector knowledge and network

• Demonstrated leadership ability

• Strong personal values and integrity

Achievement of excepBonal long-‐term returns for our investors

• Iden/fiable growth drivers: business cycle, demographics, product subs/tu/on, technological change

• Adequate universe of ac/onable, lower middle market opportuni/es

• Reasonable entry valua/ons

• Focus on proprietary opportuni/es and situa/ons where Opera/ng Partner involvement provides advantage

• Target “special situa/ons” and lower middle market deals in inefficient processes

• Deep company and industry research

• Improved revenue growth

• Cost reduc/on and margin enhancement

• Lean process implementa/on and con/nuous improvement

• Improved working capital management

• Capital spending discipline

• Add-‐on acquisi/ons

• Long-‐term posi/oning of business for strategic interest

• Dividend recapitaliza/ons as opera/ons improve

• Robust sale process if opportuni/es for improved future returns plateau

Our Strategy: Risk Management

5

Controllable Factors Uncontrollable Factors

Seven Point seeks to invest when the ability to drive value creaBon is weighted toward factors we can control

• Lower purchase price mul/ple at entry

• Tangible opportuni/es to improve sales and marke/ng to gain share

• Lean process transforma/on and con/nuous improvement

• Cost reduc/on opportuni/es • Improvements in working capital management

• Be\er capital spending discipline • More rigorous business processes • Company-‐wide alignment of incen/ves

• General industry expansion • Na/onal and regional economic growth

• Capital markets condi/ons • New product or market development

• Acquisi/ons

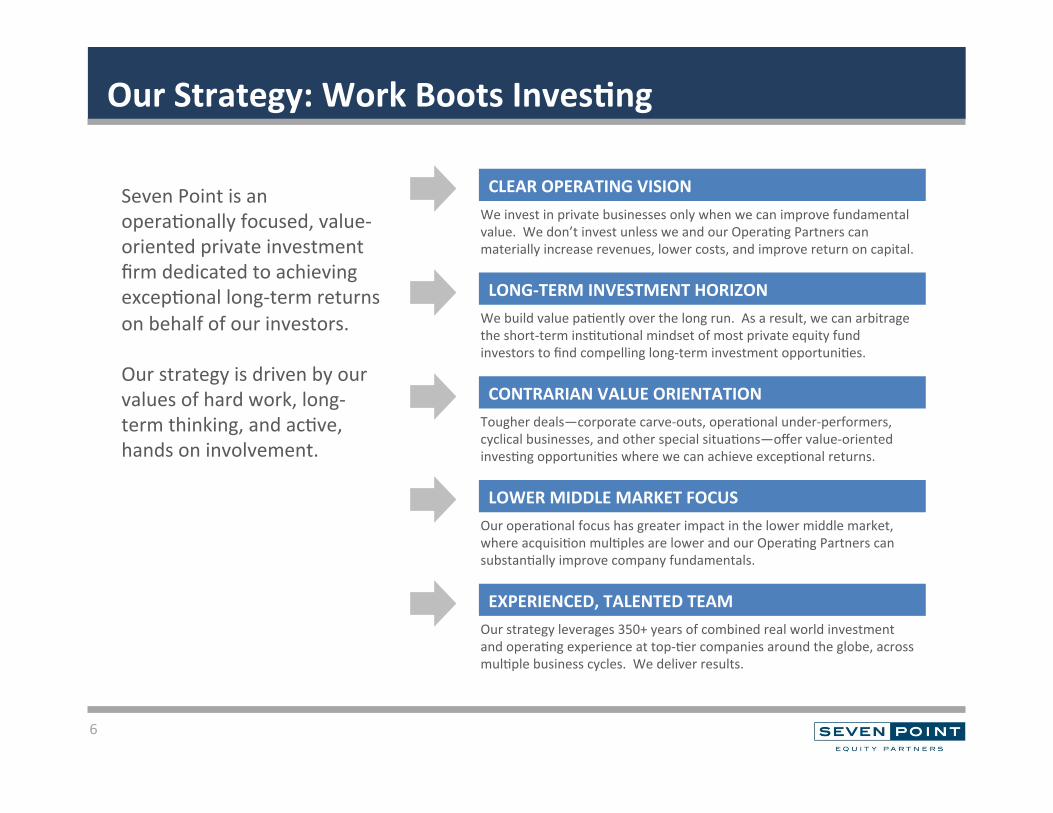

Our Strategy: Work Boots InvesBng

6

Seven Point is an opera/onally focused, value-‐oriented private investment firm dedicated to achieving excep/onal long-‐term returns on behalf of our investors. Our strategy is driven by our values of hard work, long-‐term thinking, and ac/ve, hands on involvement.

CLEAR OPERATING VISION We invest in private businesses only when we can improve fundamental value. We don’t invest unless we and our Opera/ng Partners can materially increase revenues, lower costs, and improve return on capital.

LONG-‐TERM INVESTMENT HORIZON We build value pa/ently over the long run. As a result, we can arbitrage the short-‐term ins/tu/onal mindset of most private equity fund investors to find compelling long-‐term investment opportuni/es.

CONTRARIAN VALUE ORIENTATION Tougher deals—corporate carve-‐outs, opera/onal under-‐performers, cyclical businesses, and other special situa/ons—offer value-‐oriented inves/ng opportuni/es where we can achieve excep/onal returns.

LOWER MIDDLE MARKET FOCUS Our opera/onal focus has greater impact in the lower middle market, where acquisi/on mul/ples are lower and our Opera/ng Partners can substan/ally improve company fundamentals.

EXPERIENCED, TALENTED TEAM Our strategy leverages 350+ years of combined real world investment and opera/ng experience at top-‐/er companies around the globe, across mul/ple business cycles. We deliver results.

Our Strategy: An ExcepBonal Team

7

SupporBve Senior Advisors Talented OperaBng Partners Experienced

Investment Team

• Tom Burchill Managing Partner

• Mark Kammert Partner

• Jen Oliva Vice President

• Randy Iles Building Products

• Steve Puccinelli Oak Hill Capital Partners

• Dean Nelson Sageview Capital

Eric Daliere

• John Keller Building Products

• Mike Laisure Industrial

• Alberto Sa/ne Industrial

• Scot Six Financial Services

• Mike Hadjinian Industrial

• John Stu\ard Trade shows

• Eric Daliere Industrial

Mike Hadjinian Randy Iles John Keller Mike Laisure Alberto SaBne Scot Six John StuZard

• Team track record of successfully execu/ng Seven Point investment strategy • Consistent, balanced historical investment performance across transac/ons and economic cycles

• Lower middle market track record aligned with Seven Point inves/ng strategy

8

Seven Point Team Overview

Strong Track Record

Deep Experience

Strong RelaBonships

• Significant transac/on and pormolio company experience across mul/ple industries, sectors, transac/on types and geographies

• Extensive experience implemen/ng value crea/on strategies in partnership with opera/ng execu/ves

• Broad network of deal sourcing, due diligence and post-‐investment resources, including opera/ng partners, consultants, and proprietary deal sources

• Strong rela/onships among key industry execu/ves, investment bankers, lenders and other deal intermediaries

• Seven Point investment and value crea/on strategies directly aligned with investment team’s past experience

• Seven Point principals Tom Burchill and Mark Kammert bring 26 and 28 years of experience in the industry, respec/vely

Credibility

Seven Point OperaBng Partners

• Opera/ng Partners drive opera/onal transforma/on, value crea/on, and risk management – Opera/ng Partners broaden universe of opportuni/es Seven Point can pursue – Results in incremental proprietary deal flow sourced by Opera/ng Partners – Resource-‐constrained lower middle market companies are matched with the capabili/es of world

class opera/ng execu/ves – Opera/ng Partners lead development and execu/on of detailed value crea/on roadmap – Opera/ng Partners use industry network to recruit addi/onal execu/ve talent for management

teams – Enhances due diligence through access to non-‐public industry informa/on – “Hands on” involvement reduces opera/onal risks post-‐acquisi/on

• Seven Point Opera/ng Partner backgrounds – Experience at large, mul/na/onal companies with strong management systems – Demonstrable value crea/on as CEOs or COOs of business units with revenues ranging from $100

million to $7 billion – Interna/onal management experience – Investment discipline developed through prior involvement in private equity-‐sponsored situa/ons – Entrepreneurial mindset that can handle challenges of lower middle market businesses – Desire to create significant personal wealth through equity incen/ves /ed to fundamental value

crea/on, not salary and bonus – High standards of integrity and fairness

9

Industry Sector Focus

• Seven Point industry focus:

– Industrial Manufacturing & Distribu/on – Financial Services – Business Services – Consumer Products

• Seven Point industry focus is developed through investment thesis with respect to sector growth drivers – Industry demand cycles – Macroeconomic trends in individual countries and regions – Technological change and product subs/tu/on – Structural evolu/on of industries and sub-‐segments – Barriers to entry and compe//ve advantages

• Opera/ng Partners are key advisors in determining investment strategy and industry focus – Long-‐term experience in industry cycles – Exper/se in par/cular countries and geographic regions – Access to decision-‐makers at key customers and suppliers – Knowledge of sector compe//ve dynamics – Understanding of industry value chain

10

• Over 500 investment opportuni/es reviewed each year • 20+ term sheets, represen/ng $735 million of poten/al equity

investments, over past three years • Two-‐thirds of transac/ons were proprietary opportuni/es or

limited sale processes • Average entry valua/on mul/ple of 4.7x EBITDA

Investment Sourcing & Criteria

11

Size

• Annual revenues: $25 million to $200 million • EBITDA: nega/ve to $20 million • Target equity investment: $10 million to $40

million

Seven Point Playbook – Opportunity Screening

12

BUSINESS CHARACTERISTICS TRANSACTION CHARACTERISTICS

• Large market, with strong industry fundamentals

• Established business model

• Strong demand dynamics for company’s products or services

• Passive or ineffectual ownership • Opera/onally challenged or under-‐performing

• EBITDA posi/ve or nega/ve • Major business risks are well understood and quan/fiable

• Controllable factors outweigh uncontrollable factors

• Clearly defined Seven Point plan to drive growth and profitability

• Value-‐oriented purchase price opportunity

• Seven Point controls board and decision making

• Low or moderate leverage, with expected returns driven principally by opera/onal value crea/on

• Seven Point investment through preferred equity to maximize upside, protect downside

• Require management to make significant personal investment

• Management incen/ve equity value aligned with Seven Point returns

Seven Point Playbook – Value CreaBon

13

Value CreaBon Assessment StabilizaBon Maximizing

Value CreaBon

• Assess value crea/on opportuni/es

• Perform market comparables valua/on

• Develop models / forecasts

• Develop 100-‐day plan

• Create first-‐year budget

• Complete background checks on management team

• Establish ini/al value crea/on roadmap

• Establish leadership team and clarify roles and responsibili/es for second /er management

• Begin implementa/on of value crea/on plan on closing date

• Begin to track key valua/on crea/on metrics and KPIs

• Invest in training and execu/on assistance, as needed

• Cri/cally review value crea/on roadmap

• Execute on value crea/on projects

• Supplement ini/al market research with empirical data

• Refine value crea/on metrics and KPIs

• Assess management accountability and success

• Focus annual budge/ng process on value crea/on plan

• Invest in training and execu/on assistance, as needed

Pre-‐Acquisi/on Post-‐Acquisi/on: First Six Months

Post-‐Acquisi/on: Six Months +

• Disciplined approach to value creaBon assessment and execuBon • SystemaBc program emphasizes accountability and metrics-‐based assessment

• Management compensaBon Bed to value creaBon

RiteScreen Overview

• In June 2014, Seven Point completed the acquisi/on of the leading independent supplier of window and pa/o door screens to the U.S. window and door manufacturing industry

• $56.2 million of revenues and $6.0 million in EBITDA on trailing twelve

month basis prior to closing – $5.0 million in pro forma EBITDA aqer adjustments for standalone costs

• A\rac/ve acquisi/on price equal to 4.9x TTM EBITDA – 5.8x trailing twelve month EBITDA adjusted for standalone costs

• Seven Point raised $15.9 million in equity from family offices and high net worth individuals

• Opera/ng Partner Randy Iles appointed CEO upon closing

14

OperaBng Partner – Randy Iles

15

T. Randall Iles OperaBng Partner Building Products

CEO, RiteScreen

þ Demonstrated career achievement in fundamental value creaBon • Extensive leadership experience as both restructuring

and growth-‐oriented CEO • As CEO of Andersen Corpora/on’s Silver Line subsidiary,

the largest vinyl window manufacturer in the U.S., Randy extensively restructured the company’s manufacturing, marke/ng, and distribu/on opera/ons to maintain profitability throughout the 2006-‐2009 industry downturn

Industry sector knowledge and network • 30 years of general management experience in the

building products industry • Leadership posi/ons at Silver Line, Pella, Armstrong

World Industries, and Kimball Interna/onal

Strong personal values and integrity • Execu/ve recruiter introduc/on and extensive

reference checks • Two years of interac/on with Seven Point principals

þ

þ

IdenBfiable growth drivers • Long-‐term demographic trends

in household forma/ons • Fed s/mulus and interest rates • Pent-‐up demand growing from

delayed “millennials” household forma/ons

• Reduced foreclosure inventory • Shiqing economics of rent vs. buy • Steady renova/on and remodeling

demand

Adequate universe of acBonable buyout opportuniBes • Many building products sectors remain rela/vely unconsolidated by global

compe//on as a result of local nature of U.S. markets • Fragmented universe of lower middle market suppliers

Reasonable entry valuaBons • Despite sharp run-‐up in public company mul/ples, lower middle market valua/ons

remain suppressed by cyclical concerns and lack of financing availability

Macro and Sector Analysis: Building Products

16

0

500

1,000

1,500

2,000

2,500

Starts in thousands

US Housing Starts, 1959-‐2014

55-‐Year Average

þ

þ

þ

Sourcing

17

þ Focus on proprietary opportuniBes and situaBons where OperaBng Partner involvement provides advantage

Target “special situaBons” and lower middle market deals in inefficient processes

þ

• RiteScreen’s aging management team wanted to re/re as part of sale, with no successors within the company

• Poten/al buyers needed an immediate management solu/on, which Seven Point’s Opera/ng Partner offered

• Seller needed to put RiteScreen in capable hands to maintain viable supplier to former sister window company

• Management challenges at RiteScreen discouraged many poten/al financial buyers

• Perceived complexity of corporate carve-‐out and required opera/onal restructuring reduced offer levels of compe/ng suitors

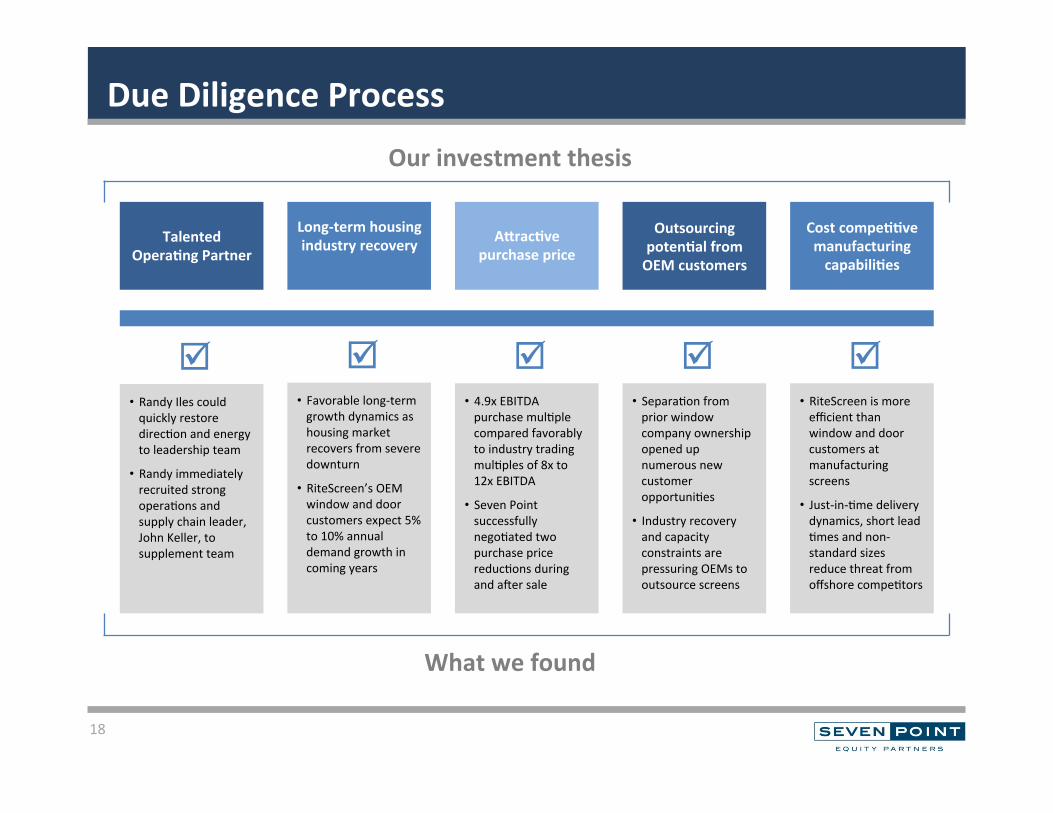

Due Diligence Process

18

Outsourcing potenBal from OEM customers

AZracBve purchase price

Long-‐term housing industry recovery Talented

OperaBng Partner

• Randy Iles could quickly restore direc/on and energy to leadership team

• Randy immediately recruited strong opera/ons and supply chain leader, John Keller, to supplement team

Our investment thesis

Cost compeBBve manufacturing capabiliBes

What we found

þ• Favorable long-‐term growth dynamics as housing market recovers from severe downturn

• RiteScreen’s OEM window and door customers expect 5% to 10% annual demand growth in coming years

þ• 4.9x EBITDA purchase mul/ple compared favorably to industry trading mul/ples of 8x to 12x EBITDA

• Seven Point successfully nego/ated two purchase price reduc/ons during and aqer sale

þ• Separa/on from prior window company ownership opened up numerous new customer opportuni/es

• Industry recovery and capacity constraints are pressuring OEMs to outsource screens

þ• RiteScreen is more efficient than window and door customers at manufacturing screens

• Just-‐in-‐/me delivery dynamics, short lead /mes and non-‐standard sizes reduce threat from offshore compe/tors

þ

Due Diligence Process (conBnued)

19

PotenBal market consolidaBon

New products and geographic markets

Favorable duopoly market structure

OperaBng improvement opportuniBes

• Seven Point and Opera/ng Partner confirmed numerous drivers for improved RiteScreen enterprise value

• Opportuni/es in selling process, lean manufacturing, purchasing, and working capital management

Our investment thesis

What we found

þ• RiteScreen shares na/onal leadership posi/on with diversified larger compe/tor that views screen product line as non-‐strategic

• Remaining compe/tors are small businesses that cannot serve na/onal OEMs

þ• Iden/fied licensing opportunity for new alterna/ve screen manufacturing technology

• Numerous expansion paths into new geographic regions to expand base of poten/al OEM customers

þ• Seven Point has already reviewed four ac/onable add-‐on acquisi/on candidates

• Opportuni/es to consolidate compe/tors and expand into adjacent products and services

þ

Value CreaBon Plan

20

Business process improvement

Revenue growth

Cost reducBon

Working capital improvement

ERP system implementaBon

• Be\er order flow • More accurate cos/ng and margin informa/on

• Inventory control

Improved selling process

• More aggressive new business focus • Restructured sales force • New agent representa/on

Support for value crea/on plan

Incremental market growth = $30 million revenues / $7.5 million EBITDA

Increased market share = $15-‐30 million revenues / $3.8-‐7.5 million EBITDA

Lean manufacturing implementaBon

$1-‐3 million EBITDA

Improved purchasing $1-‐2 million EBITDA

LogisBcs consolidaBon

$0.5-‐1.0 million EBITDA

• Direct labor and material efficiency • Reduced waste • One piece flow to reduced inventory stocks

• Consignment inventory management • Centraliza/on of purchasing • Vendor reviews

• Consolida/on of service providers • Route op/miza/on • Rate nego/a/on

VALUE CREATION POTENTIAL

Inventory reducBon $3-‐5 million reduc/on

Receivables management

• Implementa/on of perpetual inventory • Aging analysis • Op/miza/on of safety stocks and replenishment

$0.5-‐1.0 million reduc/on • Centralized credit management • Disciplined A/R tracking • Improved collec/on procedures

$0

$20

$40

$60

$80

$100

$120

Dollars in m

illions

RiteScreen Value CreaBon Analysis

21

Debt pay down

Working capital reduc/on

Cost reduc/ons

Increased market share

Organic market growth

Ini/al investment

Poten/al value crea/on

2.1x

2.3x

3.2x

3.7x

6.5x

Cumula/ve poten/al MOIC

Largely controllable

Not controllable

Closing Points

• The lower middle market is large, opportunity-‐rich, and ideally suited to Seven Point’s approach

• Seven Point’s differen/ated, opera/onally focused, value-‐oriented

investment strategy can deliver excep/onal returns

• An experienced Seven Point team is already successfully execu/ng the strategy

• Seven Point has developed significant momentum and credibility in the market and has a growing pipeline of aZracBve investment opportuniBes

22

Partners

23

Thomas F. Burchill Managing Partner Tom is the Managing Partner of Seven Point Equity Partners, LLC and brings over two decades of experience in inves/ng equity and debt capital to the Seven Point team. He has completed private equity transac/ons in North America, Europe and La/n America with aggregate invested capital of over $15 billion, and total corporate acquisi/on-‐related financings with an aggregate value of over $40 billion. Through this experience, he has developed exper/se in several industry sectors, including industrial products and services, energy, business services and financial services.

Un/l recently, Tom was also an Advisory Director of Investcorp Interna/onal, Inc., a global private equity and investment management firm.

Prior to forming Seven Point, Tom was the Senior Managing Partner and co-‐founder of SCIP Capital Management LLC, the principal inves/ng affiliate of The Silverfern Group, Inc. At SCIP, he invested over $250 million in equity capital and established a top-‐quar/le track record during the challenging 2006-‐2010 period. Tom implemented rigorous investment discipline, using limited leverage and working with talented opera/ng execu/ves to source and assess opportuni/es. Tom worked with a number of leading private equity investors, including Towerbrook, Oaktree, Cerberus and Stone Point, as deal partners.

Previously, Tom held senior posi/ons at Banc of America Securi/es LLC and Morgan Stanley & Co. Inc. in the Acquisi/on and Leveraged Finance groups opera/ng out of New York and London. Earlier in his career, at Chase Manha\an, Tom was an associate with Chemical/Chase Venture Partners and the Acquisi/on Finance Group, focused on private equity investments.

Tom earned his Masters in Management from the J.L. Kellogg Graduate School of Management at Northwestern University, and BA from The College of the Holy Cross.

Tom is a member of the board of directors of RS7 Holdings, LLC, the holding company for The RiteScreen Company, LLC.

Partners

24

Mark L. Kammert Partner Mark is a Partner at Seven Point Equity Partners, LLC and brings nearly 30 years of equity investment and investment banking experience to the firm. Prior to joining Seven Point, Mark was the Managing Partner and founder of Carbide Partners, LLC, a merchant banking firm focused on distressed equity investments in the automo/ve and building products sectors in partnership with turnaround CEOs.

Before forming Carbide Partners, Mark was a Managing Director and founding partner at Red Diamond Capital, Inc., a private equity buyout fund with $150 million of capital commi\ed by Mitsubishi Corpora/on, Japan’s largest trading company. At Red Diamond, he focused on equity investments in the automo/ve, building products, medical manufacturing and plas/cs and packaging sectors.

Previously, Mark was a Managing Director and co-‐founder of Pedersen Kammert & Co. LLC, an investment banking firm focused on complex middle market M&A, restructuring and financing assignments for large mul/na/onal corpora/ons, including Union Pacific, Invensys, Saint-‐Gobain and Thales Group, as well as private business owners and financial sponsors. Mark worked for over a decade at Dillon, Read & Co. Inc., where he gained extensive experience in corporate buyouts, mergers and acquisi/ons, and public and private financings for clients such as Honeywell, Rockwell Interna/onal, General Mills, and Quantum Chemical in the firm’s Corporate Finance, Mergers & Acquisi/ons, Corporate Buyout and Private Placement Groups.

Mark earned his MBA from the Stanford University Graduate School of Business and his BA from Yale University.

Mark is a member of the board of directors of RS7 Holdings, LLC, the holding company for The RiteScreen Company, LLC.

Senior Advisors

25

Steven G. Puccinelli, Senior Advisor Steve joined Seven Point Equity Partners, LLC as a Senior Advisor in 2013. He is currently a Partner at Oak Hill Capital Management, where he focuses on investments in the services sector. Steve was previously a Managing Director and member of the Investment Commi\ee for the Private Equity Group of Investcorp Interna/onal, Inc. Prior to this, Steve was Head of Private Equity in North America and Europe and chaired their Investment Commi\ee. During his tenure, Investcorp invested in 36 companies in North America and Europe, with total equity commitments of over $5 billion.

Prior to joining Investcorp, Steve was a member of the Investment Banking group of Donaldson, Luvin & Jenre\e (DLJ), Inc., where he served as Managing Director and Head of the Consumer and Retail Industry Groups. Prior to DLJ, he was a Cer/fied Public Accountant and worked for Peat Marwick Mitchell & Co.

Steve received a BS from the University of California, Berkeley and an MBA from Harvard Business School. He is currently a board member of Berlin Packaging, Inc., an Oak Hill Capital pormolio company, and RS7 Holdings, LLC, the holding company for The RiteScreen Company, LLC.

Dean Nelson, Senior Advisor Dean Nelson also joined Seven Point Equity Partners, LLC as a Senior Advisor in 2014. Currently, Dean is partner of Sageview Capital, a private equity firm that provides growth capital to small-‐ to mid-‐sized companies in the business services, financial services, and technology sectors. Prior to joining Sageview Capital, Dean was a founder and head of KKR Capstone, an opera/ng team focused on improving performance in KKR’s pormolio companies, and providing late-‐stage due diligence support to KKR’s investment teams. Dean also served as CEO and President of Primedia, Inc., and as Head of Worldwide Opera/ons and Technology at First Data Corp.

Dean has served on several boards of directors including Del Monte Corpora/on, Dollar General Corpora/on, Primedia, Inc., Sealy Corpora/on, Toys “R” Us Inc. and Yellow Pages Group. Before joining KKR, Dean was a management consultant with The Boston Consul/ng Group for 15 years, serving as a partner and head of the firm’s Chicago office. Dean received a BS with honors from Purdue University and an MBA with high honors from the University of Chicago.

OperaBng Partners

26

Eric Daliere, OperaBng Partner — Industrial Eric is an opera/onally focused CEO and strategic leader who has led businesses in a variety of industries, including building products, specialty chemicals, aircraq MRO services, medical device manufacturing, consumer goods, and business services, to improved performance.

Since 2009, Eric has been the President and CEO of Tarke\ Sports, the worldwide leader in sports flooring surfaces, based in Montreal, Quebec. Eric was appointed by the company’s board to lead a turnaround of Tarke\, where he has increased EBITDA by $25 million and improved opera/ng cash flow by $35 million through produc/vity improvements and reduc/ons in overhead spending. By jumpstar/ng innova/on and introducing new commercial strategies, Eric has also improved Tarke\’s annual revenues by over $40 million.

Before joining Tarke\, Eric was a Director and founding member of KKR Capstone, a group within KKR dedicated to improving the opera/ng performance of the firm’s pormolio companies. At KKR Capstone, Eric led opera/ng turnarounds and strengthened the func/onal capabili/es at several pormolio companies, including AVEOS, Masonite Interna/onal, Accellent, Van Hoffman, and Rockwood Special/es.

Eric had prior experience as a Principal of The Boston Consul/ng Group, where he worked in Europe with a number of leading global companies to improve opera/onal performance, and as an Associate at Zell-‐Chilmark Fund, LP, a leading distressed debt investor.

Eric received a BA in Economics with honors from Northwestern University and an MBA from the J.L. Kellogg Graduate School of Management.

Michael Hadjinian, OperaBng Partner — Industrial Mike is an experienced leader of industrial and manufacturing businesses and has been the CEO of six companies, with revenues ranging from $3 million to $200 million, in the past 25 years. He has specialized in tackling turnarounds and challenging management assignments.

Mike is currently an Entrepreneur-‐in-‐Residence at Accelerant Venture Capital in Dayton, Ohio, a seed-‐stage fund that invests in technology businesses, where he helps manage the fund’s pormolio companies, focusing on making new investments in technology based businesses and increasing returns from under-‐performing investments. Mike previously held CEO posi/ons with Ven/lex USA, W.C. Wood Corpora/on, JK North America, TPI Composites, Accutec, and Rexworks, where he recorded a variety of accomplishments, including drama/c sales growth, implementa/on of lean manufacturing, opera/onal restructurings, and successful M&A transac/ons and business sales. As a result of his diverse assignments, Mike has broad experience in the industrial manufacturing, capital equipment, consumer durables, advanced materials, and specialty machinery sectors.

Earlier in his career, Mike was the Division General Manager of FMC Corpora/on’s Sweeper Division and was Director of Business Development and Strategic Planning for their Specialized Machinery Group. He held a variety of management posi/ons with Pillar Industries, Applied Power and Harnischfeger Corpora/on, where he gained early career experience in engineering, manufacturing, sales, and interna/onal business.

Mike has BS in Electrical Engineering from Marque\e University and an MBA from the University of Wisconsin.

OperaBng Partners

27

T. Randall Iles, OperaBng Partner — Building Products Randy is currently the CEO of The RiteScreen Company, LLC. Randy has extensive leadership experience as both a restructuring and growth-‐oriented execu/ve in the building products manufacturing industry. He was most recently CEO of Andersen Corpora/on’s Silver Line Building Products subsidiary, the country’s largest manufacturer of vinyl windows. Recruited as CEO of this 7,000-‐employee business in 2006, prior to the most severe downturn in the history of the building products industry, Randy extensively restructured Silver Line’s manufacturing opera/ons, distribu/on strategy, marke/ng efforts and business culture. Despite a 50% decline in window industry volumes, Silver Line maintained profitability and gained substan/al market share during Randy’s tenure.

Before Silver Line, Randy was Corporate Vice President and General Manager of Kimball Interna/onal’s $300 million office furniture business. He led a major business turnaround and cost reduc/on program, revitalizing the company’s top line growth and leading the business to record profitability.

Previously, Randy was President of Pella Corpora/on’s Entry Systems Division, where he completed the acquisi/on of a family-‐owned door company and successfully integrated the new unit into Pella’s exis/ng window and pa/o door businesses. Prior to this, Randy was Pella Corpora/on’s Senior Vice President, Marke/ng & Sales, responsible for all of this $1 billion company’s brand marke/ng, distribu/on and channel strategies.

Randy began his career at Armstrong World Industries, where he played a variety of senior general management, sales, marke/ng and opera/onal leadership roles in the company’s commercial and residen/al building materials businesses. Randy received his BS in business administra/on from Penn State University.

John Keller, OperaBng Partner — Building Products John is the Senior VP of Opera/ons & Supply Chain at The RiteScreen Company, LLC. He has extensive experience as an manufacturing and supply chain execu/ve in the building products and distribu/on sectors. Before joining RiteScreen, John was the Vice President of Opera/ons & Supply Chain for Silver Line Building Products, a $500 million division of Andersen Windows, where he was responsible for four plants and nearly 3,500 employees. He worked with Silver Line for 11 years in various execu/ve posi/ons. John’s aggressive efforts to improve opera/ng efficiencies and reduce costs helped Silver Line maintain profitability every year during the recent building products industry downturn. John led Silver Line’s lean manufacturing transforma/on, crea/ng a culture of con/nuous improvement throughout the organiza/on.

Prior to Silver Line, John spent 11 years in the office supply distribu/on business with Corporate Express, which was later acquired by Staples. At Corporate Express, John was a Divisional President, where he assumed P&L responsibility for an $85 million division that was losing money and was able to improve profitability from a 2% loss to a 5% net profit within 18 months. John accomplished this turnaround by increasing sales (both organically and through an acquisi/on) and significantly improving the unit’s cost structure.

Early in his career, John spent five years as a management consultant with RCG Interna/onal, leading various consul/ng assignments in logis/cs, opera/ons and supply chain.

John has two undergraduate degrees from Rutgers University, a BS in Industrial Engineering and a BA in Economics/Finance, and completed graduate studies at Rutgers Graduate School of Management.

OperaBng Partners

28

James M. (Mike) Laisure, OperaBng Partner — Industrial Mike is a 40-‐year veteran in the industrial manufacturing sector, with global experience in the industrial, automo/ve OEM and aqermarket, heavy truck OEM and aqermarket, recrea/onal vehicle, agricultural and mining equipment, and engine markets. Mike is currently the CEO of Fluid Rou/ng Solu/ons, a Tier 1 and Tier 2 automo/ve supplier that designs and manufactures fluid and fuel handling systems. Mike acquired FRS in partnership with Sun Capital Partners in June 2007 and subsequently led a corporate restructuring and opera/ng turnaround that increased EBITDA from a nega/ve level to $32 million by 2012. FRS was sold to a strategic buyer, Park-‐Ohio Holdings Corp., in 2012 for an 8x cash-‐on-‐cash return to the company’s equity investors.

Mike is a director at American Railcar Industries, Inc. and Federal-‐Mogul Corpora/on. Previously, he was President and COO of Remy Interna/onal, a supplier of rota/ng electrical motors to automo/ve, commercial truck and off-‐highway OEMs and aqermarket customers. Before joining Remy, Mike served as President of Dana Corpora/on, where he worked in posi/ons of increasing responsibility for almost 30 years. As President, Mike was responsible for the Automo/ve Systems Group, the largest of Dana’s two Strategic Business Units (SBUs). His SBU included 34,000 people in 176 facili/es and 32 countries and accounted for $7 billion of Dana’s $9 billion in revenue. Dana is a supplier of axle, driveshaq, engine, frame, chassis, and transmission technologies, employing 46,000 people and serving OEM customers that include Ford, DaimlerChrysler, BMW, General Motors, and Toyota.

Mike a\ended the Advanced Management Program at Harvard Business School, received his MBA from Miami University, and his BS from Ball State University.

Alberto L. SaBne, OperaBng Partner — Industrial Alberto is currently the Senior Vice President of the Driveline Business Unit at American Axle & Manufacturing, Inc., where he has been a senior corporate officer since 2001. He was previously American Axle’s Group Vice President, Global Sales and Business Development. Alberto has more than 27 years of interna/onal automo/ve supplier experience. Alberto is a director of two of American Axle’s key interna/onal joint ventures—AAM Sona Axle in India and AAM Hefie Axle Co. in China.

Alberto is a Managing Partner and co-‐founder of Interna/onal Steel Solu/ons Holdings LLC, a private investment and opera/ng company that acquired the Gabriel OEM light vehicle shock absorber business in Tennessee from ArvinMeritor in 2006. Following the acquisi/on, Alberto and his partners successfully turned around the business, diversifying the customer base, reducing the opera/on’s breakeven point, and improving plant systems and quality. ISS sold the business to Magne/ Marelli, a unit of the Fiat Group, for a large gain on investment in 2010.

Prior to joining American Axle, Alberto worked at Dana Corpora/on, where he held various senior execu/ve posi/ons. Alberto holds three MS degrees in industrial and opera/ons research engineering, mechanical engineering and metallurgical engineering from the University of Michigan and a BS in mechanical engineering from Universidad Simon Bolivar, Caracas, Venezuela.

OperaBng Partners

29

Scot O. Six, OperaBng Partner — Financial Services Scot has over 20 years of experience in senior management posi/ons in asset management and investment banking. Scot has led growth related ini/a/ves through investment in exis/ng business lines or pursued new business ventures organically and via acquisi/on. He has also led major reorganiza/ons, restructurings, and post-‐acquisi/on integra/on efforts for Morgan Stanley & Co. and Deutsche Bank Group.

Scot most recently served as Global Head of Marke/ng for Deutsche Asset Management (DeAM), the $750 billion asset management division of Deutsche Bank, where he served on the Global Execu/ve Commi\ee. Scot’s responsibili/es included oversight of the generalist salesforce, marke/ng, strategy, M&A, and business development ac/vi/es globally. During his /me at DeAM, Scot led efforts to develop a mul/-‐asset class alterna/ves firm in Brazil; extend DeAM’s Private Equity, Infrastructure, and Real Estate businesses in China and India; and build a global solu/ons business through the acquisi/on of Outsourced CIO, Hedge Fund Fund-‐of-‐Fund, Pormolio Hedging, and Private Equity Fund-‐of-‐Fund businesses.

Previously at Deutsche Bank, Scot served as Deputy Global Head of the 800-‐person Equity Research Department and was a member of the four-‐person Execu/ve Commi\ee running the $2 billion (revenues) Global Cash Equity Division. Prior to his /me at Deutsche Asset Management, Scot was a Founder and Partner of Green Partners LLC, a renewable energy private investment fund, which invested over $800 million of capital in the development of distributed power facili/es throughout Europe and the United States.

Earlier in Scot’s career, he led the Corporate Strategy Team at Morgan Stanley. Scot began his career at Andersen Consul/ng, where he focused on strategic planning and business transforma/on. Scot holds BS in Opera/ons Research and Industrial Engineering from Cornell University.

John StuZard, OperaBng Partner — Trade Shows John is a talented marke/ng services industry leader with more than 18 years of experience in the trade show sector. With a varied background in strategic business development, customer focus, sales and marke/ng, logis/cs management, and finance, John has managed trade show and marke/ng services businesses for global companies in North America, Europe, Asia and Central America.

John was most recently a Managing Director at UBM plc, where he led the company’s North American M&A efforts and managed a pormolio of trade shows in the US and Mexico in the construc/on, hotel and restaurant, fine chemicals, beauty and cosme/cs, online security, and cruise industries with over $50 million in revenues.

Before joining UBM, John was a senior execu/ve at Reed Exhibi/ons in Europe and North America, where he managed a number of trade shows in the industrial, pharmaceu/cal, jewelry, books, communica/ons and interior design sectors. John established a strong record of turning around under-‐performing businesses and leading the interna/onal expansion efforts of several of Reed’s largest shows in China, India and South America. Prior to his work with Reed, John was the European Director for Advanstar Communica/ons’ trade show and magazine business in the technology and communica/ons industries.

John has had addi/onal career experience in the resort management, consumer packaged goods, and management consul/ng industries. John received a BA with honors in English Literature from London University and an MBA from Cranfield University.

Contact InformaBon

30

Mark L. Kammert Partner

Office (direct): 203-‐604-‐0323 Mobile: 203-‐984-‐5901

Thomas F. Burchill Managing Partner

Office (direct): 203-‐293-‐4058 Mobile: 203-‐253-‐2020

1175 Post Road East Westport, CT 06880