sensitivity analysis and density estimation using the

TRANSCRIPT

Sensitivity analysis and density estimation using the Malliavincalculus

Nicolas Privault

December 17, 2005

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Sensitivity analysis and Monte Carlo method

Consider (F ζ)ζ a family of random variables depending on a parameter ζ.

∂

∂ζE

hf

“F ζ

”i=

8>>><>>>:E

»f ′

`F ζ

´ ∂

∂ζF ζ

–

'E

ˆf

`F ζ+h

´˜− E

ˆf

`F ζ−h

´˜2h

Expectations can be computed by the Monte Carlo method:

E [F ] ' F1 + · · ·+ Fn

n,

where F1, . . . , Fn is a random sample of F .

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Application (1): sensitivity analysis in finance - Greeks

Price process:dSζ

t

Sζt

= r(Sζt )dt + σ(Sζ

t )dMt , Sζ0 = x .

F ζ = ST and ζ ∈ x , r , σ, T , ....

Payoff function:

f (x) = (x − K)+

0

0.5

1

1.5

2

2.5

3

1 1.5 2 2.5 3 3.5 4

x

f (x) = 1[K ,∞)(x).

0

0.5

1

1.5

2

1 1.5 2 2.5 3 3.5 4

x

Option price:

E [f (SζT )].

Greeks:

ζ = x : Delta

ζ = σ: Vega

ζ = r : Rho

ζ = T : Theta.

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Application (1): sensitivity analysis in finance - Greeks

Price process:dSζ

t

Sζt

= r(Sζt )dt + σ(Sζ

t )dMt , Sζ0 = x .

F ζ = ST and ζ ∈ x , r , σ, T , ....

Payoff function:

f (x) = (x − K)+

0

0.5

1

1.5

2

2.5

3

1 1.5 2 2.5 3 3.5 4

x

f (x) = 1[K ,∞)(x).

0

0.5

1

1.5

2

1 1.5 2 2.5 3 3.5 4

x

Option price:

E [f (SζT )].

Greeks:

ζ = x : Delta

ζ = σ: Vega

ζ = r : Rho

ζ = T : Theta.

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Application (1): sensitivity analysis in finance - Greeks

Price process:dSζ

t

Sζt

= r(Sζt )dt + σ(Sζ

t )dMt , Sζ0 = x .

F ζ = ST and ζ ∈ x , r , σ, T , ....

Payoff function:

f (x) = (x − K)+

0

0.5

1

1.5

2

2.5

3

1 1.5 2 2.5 3 3.5 4

x

f (x) = 1[K ,∞)(x).

0

0.5

1

1.5

2

1 1.5 2 2.5 3 3.5 4

x

Option price:

E [f (SζT )].

Greeks:

ζ = x : Delta

ζ = σ: Vega

ζ = r : Rho

ζ = T : Theta.

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Application (1): sensitivity analysis in finance - Greeks

Price process:dSζ

t

Sζt

= r(Sζt )dt + σ(Sζ

t )dMt , Sζ0 = x .

F ζ = ST and ζ ∈ x , r , σ, T , ....

Payoff function:

f (x) = (x − K)+

0

0.5

1

1.5

2

2.5

3

1 1.5 2 2.5 3 3.5 4

x

f (x) = 1[K ,∞)(x).

0

0.5

1

1.5

2

1 1.5 2 2.5 3 3.5 4

x

Option price:

E [f (SζT )].

Greeks:

ζ = x : Delta

ζ = σ: Vega

ζ = r : Rho

ζ = T : Theta.

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Application (1): sensitivity analysis in finance - Greeks

Price process:dSζ

t

Sζt

= r(Sζt )dt + σ(Sζ

t )dMt , Sζ0 = x .

F ζ = ST and ζ ∈ x , r , σ, T , ....

Payoff function:

f (x) = (x − K)+

0

0.5

1

1.5

2

2.5

3

1 1.5 2 2.5 3 3.5 4

x

f (x) = 1[K ,∞)(x).

0

0.5

1

1.5

2

1 1.5 2 2.5 3 3.5 4

x

Option price:

E [f (SζT )].

Greeks:

ζ = x : Delta

ζ = σ: Vega

ζ = r : Rho

ζ = T : Theta.

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Application (2): density estimation

Let F ζ = F − ζ and f (x) = 1(−∞,0].

Density of F :

φF (ξ) : =∂

∂ζP(F ≤ ζ) =

∂

∂ζE

ˆ1(−∞,0](F − ζ)

˜=

∂

∂ζE

hf

“F ζ

”i' E [f (F − (ζ + h))]− E [f (F − (ζ − h))]

2h=

Eˆ1[ζ−h,ζ+h](F )

˜2h

.

Example: F =R T

0e−rtdNt .

0

0.2

0.4

0.6

0.8

1

1.2

1.5 2 2.5 3 3.5 4 4.5 5 5.5

Den

sity

y

h=1h=0.1

h=0.01

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Application (2): density estimation

Let F ζ = F − ζ and f (x) = 1(−∞,0].

Density of F :

φF (ξ) : =∂

∂ζP(F ≤ ζ) =

∂

∂ζE

ˆ1(−∞,0](F − ζ)

˜=

∂

∂ζE

hf

“F ζ

”i' E [f (F − (ζ + h))]− E [f (F − (ζ − h))]

2h=

Eˆ1[ζ−h,ζ+h](F )

˜2h

.

Example: F =R T

0e−rtdNt .

0

0.2

0.4

0.6

0.8

1

1.2

1.5 2 2.5 3 3.5 4 4.5 5 5.5

Den

sity

y

h=1h=0.1

h=0.01

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Application (2): density estimation

Let F ζ = F − ζ and f (x) = 1(−∞,0].

Density of F :

φF (ξ) : =∂

∂ζP(F ≤ ζ) =

∂

∂ζE

ˆ1(−∞,0](F − ζ)

˜=

∂

∂ζE

hf

“F ζ

”i' E [f (F − (ζ + h))]− E [f (F − (ζ − h))]

2h=

Eˆ1[ζ−h,ζ+h](F )

˜2h

.

Example: F =R T

0e−rtdNt .

0

0.2

0.4

0.6

0.8

1

1.2

1.5 2 2.5 3 3.5 4 4.5 5 5.5

Den

sity

y

h=1h=0.1

h=0.01

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Integration by parts

1 Dw a derivation operator acting on random variables:

f ′(F ζ) =Dw

ˆf (F ζ)

˜DwF ζ

.

2 D∗w the adjoint of Dw :

〈F , DwG〉 = E [FDwG ] = E [GD∗wF ] = 〈G , D∗

wF 〉.

3 Main argument:

∂

∂ζE

hf (F ζ)

i= E

hf ′

“F ζ

”∂ζF

ζi

= E

»Dw [f (F ζ)]

DwF ζ∂ζF

ζ

–= E

»f

“F ζ

”D∗

w

„∂ζF

ζ

DwF ζ

«–.

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Integration by parts

1 Dw a derivation operator acting on random variables:

f ′(F ζ) =Dw

ˆf (F ζ)

˜DwF ζ

.

2 D∗w the adjoint of Dw :

〈F , DwG〉 = E [FDwG ] = E [GD∗wF ] = 〈G , D∗

wF 〉.

3 Main argument:

∂

∂ζE

hf (F ζ)

i= E

hf ′

“F ζ

”∂ζF

ζi

= E

»Dw [f (F ζ)]

DwF ζ∂ζF

ζ

–= E

»f

“F ζ

”D∗

w

„∂ζF

ζ

DwF ζ

«–.

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Integration by parts

1 Dw a derivation operator acting on random variables:

f ′(F ζ) =Dw

ˆf (F ζ)

˜DwF ζ

.

2 D∗w the adjoint of Dw :

〈F , DwG〉 = E [FDwG ] = E [GD∗wF ] = 〈G , D∗

wF 〉.

3 Main argument:

∂

∂ζE

hf (F ζ)

i= E

hf ′

“F ζ

”∂ζF

ζi

= E

»Dw [f (F ζ)]

DwF ζ∂ζF

ζ

–= E

»f

“F ζ

”D∗

w

„∂ζF

ζ

DwF ζ

«–.

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Integration by parts

Proposition

Assume that DwF ζ 6= 0, a.s. on ∂ζFζ 6= 0, ζ ∈ (a, b). We have

∂

∂ζE

hf

“F ζ

”i= E

»f

“F ζ

”D∗

w

„∂ζF

ζ

DwF ζ

«–, ζ ∈ (a, b). (1)

No differentiability assumption on f , compare with:

∂

∂ζE

hf

“F ζ

”i= E

hf ′

“F ζ

”∂ζF

ζi.

Independence on the bandwidth parameter h, compare with:

∂

∂ζE

hf

“F ζ

”i'

Eˆf

`F ζ+h

´˜− E

ˆf

`F ζ−h

´˜2h

.

The weight

W := D∗w

„∂ζF

ζ

DwF ζ

«is independent of f .

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Integration by parts

Proposition

Assume that DwF ζ 6= 0, a.s. on ∂ζFζ 6= 0, ζ ∈ (a, b). We have

∂

∂ζE

hf

“F ζ

”i= E

»f

“F ζ

”D∗

w

„∂ζF

ζ

DwF ζ

«–, ζ ∈ (a, b). (1)

No differentiability assumption on f , compare with:

∂

∂ζE

hf

“F ζ

”i= E

hf ′

“F ζ

”∂ζF

ζi.

Independence on the bandwidth parameter h, compare with:

∂

∂ζE

hf

“F ζ

”i'

Eˆf

`F ζ+h

´˜− E

ˆf

`F ζ−h

´˜2h

.

The weight

W := D∗w

„∂ζF

ζ

DwF ζ

«is independent of f .

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Integration by parts

Proposition

Assume that DwF ζ 6= 0, a.s. on ∂ζFζ 6= 0, ζ ∈ (a, b). We have

∂

∂ζE

hf

“F ζ

”i= E

»f

“F ζ

”D∗

w

„∂ζF

ζ

DwF ζ

«–, ζ ∈ (a, b). (1)

No differentiability assumption on f , compare with:

∂

∂ζE

hf

“F ζ

”i= E

hf ′

“F ζ

”∂ζF

ζi.

Independence on the bandwidth parameter h, compare with:

∂

∂ζE

hf

“F ζ

”i'

Eˆf

`F ζ+h

´˜− E

ˆf

`F ζ−h

´˜2h

.

The weight

W := D∗w

„∂ζF

ζ

DwF ζ

«is independent of f .

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Integration by parts

Proposition

Assume that DwF ζ 6= 0, a.s. on ∂ζFζ 6= 0, ζ ∈ (a, b). We have

∂

∂ζE

hf

“F ζ

”i= E

»f

“F ζ

”D∗

w

„∂ζF

ζ

DwF ζ

«–, ζ ∈ (a, b). (1)

No differentiability assumption on f , compare with:

∂

∂ζE

hf

“F ζ

”i= E

hf ′

“F ζ

”∂ζF

ζi.

Independence on the bandwidth parameter h, compare with:

∂

∂ζE

hf

“F ζ

”i'

Eˆf

`F ζ+h

´˜− E

ˆf

`F ζ−h

´˜2h

.

The weight

W := D∗w

„∂ζF

ζ

DwF ζ

«is independent of f .

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Wiener case [FLL+99], [FLLL01], [Ben02]

Mt = Bt is a Brownian motion:

-0.2

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

B(t)

t

dSζt

Sζt

= σ(Sζt )dBt + r(Sζ

t )dt, Sζ0 = x .

w ∈ L2(R+) and

Dw f (Bt1 , . . . , Btn ) =nX

i=1

Z ti

0

wsds∂f

∂xi(Bt1 , . . . , Btn ).

δ(wF ) := D∗wF , and δ coincides with the Ito stochastic with respect to w :

δ(w) =

Z ∞

0

wsdBs .

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Wiener case [FLL+99], [FLLL01], [Ben02]

Mt = Bt is a Brownian motion:

-0.2

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

B(t)

t

dSζt

Sζt

= σ(Sζt )dBt + r(Sζ

t )dt, Sζ0 = x .

w ∈ L2(R+) and

Dw f (Bt1 , . . . , Btn ) =nX

i=1

Z ti

0

wsds∂f

∂xi(Bt1 , . . . , Btn ).

δ(wF ) := D∗wF , and δ coincides with the Ito stochastic with respect to w :

δ(w) =

Z ∞

0

wsdBs .

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Wiener case [FLL+99], [FLLL01], [Ben02]

Mt = Bt is a Brownian motion:

-0.2

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

B(t)

t

dSζt

Sζt

= σ(Sζt )dBt + r(Sζ

t )dt, Sζ0 = x .

w ∈ L2(R+) and

Dw f (Bt1 , . . . , Btn ) =nX

i=1

Z ti

0

wsds∂f

∂xi(Bt1 , . . . , Btn ).

δ(wF ) := D∗wF , and δ coincides with the Ito stochastic with respect to w :

δ(w) =

Z ∞

0

wsdBs .

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Wiener case [FLL+99], [FLLL01], [Ben02]

Mt = Bt is a Brownian motion:

-0.2

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

B(t)

t

dSζt

Sζt

= σ(Sζt )dBt + r(Sζ

t )dt, Sζ0 = x .

w ∈ L2(R+) and

Dw f (Bt1 , . . . , Btn ) =nX

i=1

Z ti

0

wsds∂f

∂xi(Bt1 , . . . , Btn ).

δ(wF ) := D∗wF , and δ coincides with the Ito stochastic with respect to w :

δ(w) =

Z ∞

0

wsdBs .

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Delta - first variation process

In [FLL+99] the relations

f ′(F ζ) =Dt

ˆf (F ζ)

˜DtF ζ

, 0 ≤ t ≤ T , a.s.,

and

DtSxT =

∂xSxT

∂xSxt

σ(Sxt ), 0 ≤ t ≤ T , a.s.,

are used, cf. [Nua95]. This gives

∂xSxT f ′(Sx

T ) =∂xS

xt

σ(Sxt )

Dt f (SxT ), 0 ≤ t ≤ T , a.s., (2)

which implies ifR T

0wsds = 1:

Delta =∂

∂xE [f (Sx

T )] = Eˆ∂xS

xT f ′ (Sx

T )˜

= E»Z T

0

wt∂xS

xt

σ(Sxt )

Dt f (SxT )dt

–= E

»f (Sx

T )δ

„1[0,T ]w

∂xSx

σ(Sx)

«–= E

»f (Sx

T )

Z T

0

wt∂xS

xt

σ(Sxt )

dBt

–= E

»f (Sx

T )BT

σxT

–.

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Poisson case

Mt = Nt is a Poisson process with jump times T1, T2, T3, . . .,

0

1

2

3

4

5

6

7

8

0 1 2 3 4 5 6 7 8 9 10

N(t)

t

w ∈ C1c ((0,∞)), and

DwF = −∞Xn=1

1NT =n

nXi=1

∂fn∂xi

(T1, . . . , Tn),

for F of the form

F = f01NT =0 +∞Xn=1

1NT =nfn(T1, . . . , Tn).

Recall that

E [F ] = f0e−λT + e−λT

∞Xn=1

1

n!

Z T

0

· · ·Z T

0

fn(t1, . . . , tn)dt1 · · · dtn.

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Poisson case

Mt = Nt is a Poisson process with jump times T1, T2, T3, . . .,

0

1

2

3

4

5

6

7

8

0 1 2 3 4 5 6 7 8 9 10

N(t)

t

w ∈ C1c ((0,∞)), and

DwF = −∞Xn=1

1NT =n

nXi=1

∂fn∂xi

(T1, . . . , Tn),

for F of the form

F = f01NT =0 +∞Xn=1

1NT =nfn(T1, . . . , Tn).

Recall that

E [F ] = f0e−λT + e−λT

∞Xn=1

1

n!

Z T

0

· · ·Z T

0

fn(t1, . . . , tn)dt1 · · · dtn.

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Poisson case

Mt = Nt is a Poisson process with jump times T1, T2, T3, . . .,

0

1

2

3

4

5

6

7

8

0 1 2 3 4 5 6 7 8 9 10

N(t)

t

w ∈ C1c ((0,∞)), and

DwF = −∞Xn=1

1NT =n

nXi=1

∂fn∂xi

(T1, . . . , Tn),

for F of the form

F = f01NT =0 +∞Xn=1

1NT =nfn(T1, . . . , Tn).

Recall that

E [F ] = f0e−λT + e−λT

∞Xn=1

1

n!

Z T

0

· · ·Z T

0

fn(t1, . . . , tn)dt1 · · · dtn.

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Integration by parts

By standard integration by parts we have, under the boundary conditionw(0) = w(T ) = 0:

E [DwF ] = −e−λTmX

n=1

λn

n!

Z T

0

· · ·Z T

0

nXk=1

w(tk)∂k fn(t1, . . . , tn)dt1 · · · dtn

= e−λTmX

n=1

λn

n!

Z T

0

· · ·Z T

0

fn(t1, . . . , tn)nX

k=1

w(tk)dt1 · · · dtn

= E

24F

k=N(T )Xk=1

w(Tk)

35 = E

»F

Z T

0

w(t)dN(t)

–.

Next, letting

D∗wG = G

Z T

0

w(t)dN(t)− DwG

we get

E [GDwF ] = E [Dw (FG)− FDwG ] = E

»F

„G

Z T

0

w(t)dN(t)− DwG

«–= E [FD∗

wG ].

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Asian options and reserve processes [KP04], [PW04]

Price process: Sζt = Sζ

0 ert(1 + σ)Nt .

Asian options: F ζ =1

T

Z T

0

Sζt dt.

W∆ =−1

xσ

0B@1−R T

0Sζ

t dtR T

0wtdNtR T

0wtS

ζ

t−dNt

+

R T

0Sζ

t dtR T

0wt (wt + rwt)Sζ

t−dNt“R T

0wtS

ζ

t−dNt

”2

1CA .

Density of reserve processes: F =

Z T

0

e(T−t)rdNt .

Wy =

R T

0w(t)dN(t) +

R T

0e−rtw(t)(rw(t)− w(t))dN(t)R T

0w(t)e−rtdN(t)

rR T

0w(t)er(T−t)dX (t)

.

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Asian options and reserve processes [KP04], [PW04]

Price process: Sζt = Sζ

0 ert(1 + σ)Nt .

Asian options: F ζ =1

T

Z T

0

Sζt dt.

W∆ =−1

xσ

0B@1−R T

0Sζ

t dtR T

0wtdNtR T

0wtS

ζ

t−dNt

+

R T

0Sζ

t dtR T

0wt (wt + rwt)Sζ

t−dNt“R T

0wtS

ζ

t−dNt

”2

1CA .

Density of reserve processes: F =

Z T

0

e(T−t)rdNt .

Wy =

R T

0w(t)dN(t) +

R T

0e−rtw(t)(rw(t)− w(t))dN(t)R T

0w(t)e−rtdN(t)

rR T

0w(t)er(T−t)dX (t)

.

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Asian options and reserve processes [KP04], [PW04]

Price process: Sζt = Sζ

0 ert(1 + σ)Nt .

Asian options: F ζ =1

T

Z T

0

Sζt dt.

W∆ =−1

xσ

0B@1−R T

0Sζ

t dtR T

0wtdNtR T

0wtS

ζ

t−dNt

+

R T

0Sζ

t dtR T

0wt (wt + rwt)Sζ

t−dNt“R T

0wtS

ζ

t−dNt

”2

1CA .

Density of reserve processes: F =

Z T

0

e(T−t)rdNt .

Wy =

R T

0w(t)dN(t) +

R T

0e−rtw(t)(rw(t)− w(t))dN(t)R T

0w(t)e−rtdN(t)

rR T

0w(t)er(T−t)dX (t)

.

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Density estimation - finite differences

φF (y) =∂

∂yE

ˆ1(−∞,0](F − y)

˜'

Eˆ1[y−h,y+h](F )

˜2h

.

0

0.2

0.4

0.6

0.8

1

1.2

1.5 2 2.5 3 3.5 4 4.5 5 5.5

Den

sity

y

h=1h=0.1

h=0.01

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Density estimation - Malliavin method

φF (y) =∂

∂yE

ˆ1(−∞,0](F − y)

˜= −E

»1(−∞,0](F − y)D∗

w

„1

DwF

«–.

0

0.2

0.4

0.6

0.8

1

1.2

1.5 2 2.5 3 3.5 4 4.5 5 5.5

Den

sity

y

Malliavin methodExact value

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Localization [FLL+99], [KHP02]

Consider the decomposition

1[0,∞) = f + g ,

where g is C1:

0

0.2

0.4

0.6

0.8

1

1.2

-2 -1.5 -1 -0.5 0 0.5 1 1.5 2

x

f(x)g(x)

We have

d

dyE [1[0,∞)(F − y)] =

d

dyE

»f

„F − y

h

«–+

d

dyE

»g

„F − y

h

«–= E

»D∗

w

„1

DwF

«f

„F − y

h

«–+

1

hE

»1F>yf

′„

F − y

h

«–.

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Density estimation - localized Malliavin method

φF (y) = −E

»f

„F − y

h

«D∗

w

„1

DwF

«–− 1

hE

»1F>yf

′„

F − y

h

«–.

0

0.2

0.4

0.6

0.8

1

1.2

1.5 2 2.5 3 3.5 4 4.5 5 5.5

Den

sity

y

h=1h=0.2

h=0.01

Optimization: f (x) = e−x , x ≥ 0, h = ‖W ‖−1L2(Ω)

.

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Density estimation - finite differences

F =

Z T

0

e−rtdNt .

0.2

0.3

0.4

r

2.5 3 3.5 4 4.5 5 5.5

y

0

0.5

1

1.5

2

0.2

0.3

0.4

r

2.5 3 3.5 4 4.5 5 5.5

y

0

0.5

1

1.5

2

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

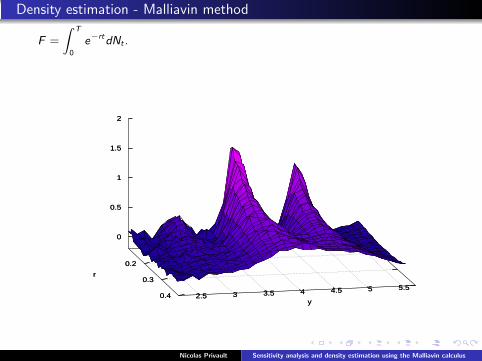

Density estimation - Malliavin method

F =

Z T

0

e−rtdNt .

0.2

0.3

0.4

r

2.5 3 3.5 4 4.5 5 5.5

y

0

0.5

1

1.5

2

0.2

0.3

0.4

r

2.5 3 3.5 4 4.5 5 5.5

y

0

0.5

1

1.5

2

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Density estimation - localized Malliavin method

F =

Z T

0

e−rtdNt .

0.2

0.3

0.4

r

2.5 3 3.5 4 4.5 5 5.5

y

0

0.5

1

1.5

2

0.2

0.3

0.4

r

2.5 3 3.5 4 4.5 5 5.5

y

0

0.5

1

1.5

2

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Jump diffusion model [DJ], [DP04], [BMM]

(Bt)t∈R+ a standard Brownian motion,

(Nt)t∈R+ is a Poisson process with intensity λ > 0,

(Zk)k≥1 an i.i.d. sequence of random variables with probability distributionν(dx),

(Xt)t∈R+ a compound Poisson process with Levy measureµ(dy) = λν(dx). and finite intensity λ:

Xt =

NtXk=1

Zk , t ∈ R+, (3)

(Sxt )t∈R+ a jump-diffusion price process:8>><>>:

dSxt

Sxt

= r(Sxt )dt + σ1(S

xt )dBt + σ2(S

xt−)dXt ,

Sx0 = x .

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Jump diffusion model [DJ], [DP04], [BMM]

(Bt)t∈R+ a standard Brownian motion,

(Nt)t∈R+ is a Poisson process with intensity λ > 0,

(Zk)k≥1 an i.i.d. sequence of random variables with probability distributionν(dx),

(Xt)t∈R+ a compound Poisson process with Levy measureµ(dy) = λν(dx). and finite intensity λ:

Xt =

NtXk=1

Zk , t ∈ R+, (3)

(Sxt )t∈R+ a jump-diffusion price process:8>><>>:

dSxt

Sxt

= r(Sxt )dt + σ1(S

xt )dBt + σ2(S

xt−)dXt ,

Sx0 = x .

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Jump diffusion model [DJ], [DP04], [BMM]

(Bt)t∈R+ a standard Brownian motion,

(Nt)t∈R+ is a Poisson process with intensity λ > 0,

(Zk)k≥1 an i.i.d. sequence of random variables with probability distributionν(dx),

(Xt)t∈R+ a compound Poisson process with Levy measureµ(dy) = λν(dx). and finite intensity λ:

Xt =

NtXk=1

Zk , t ∈ R+, (3)

(Sxt )t∈R+ a jump-diffusion price process:8>><>>:

dSxt

Sxt

= r(Sxt )dt + σ1(S

xt )dBt + σ2(S

xt−)dXt ,

Sx0 = x .

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Jump diffusion model [DJ], [DP04], [BMM]

(Bt)t∈R+ a standard Brownian motion,

(Nt)t∈R+ is a Poisson process with intensity λ > 0,

(Zk)k≥1 an i.i.d. sequence of random variables with probability distributionν(dx),

(Xt)t∈R+ a compound Poisson process with Levy measureµ(dy) = λν(dx). and finite intensity λ:

Xt =

NtXk=1

Zk , t ∈ R+, (3)

(Sxt )t∈R+ a jump-diffusion price process:8>><>>:

dSxt

Sxt

= r(Sxt )dt + σ1(S

xt )dBt + σ2(S

xt−)dXt ,

Sx0 = x .

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Jump diffusion model [DJ], [DP04], [BMM]

(Bt)t∈R+ a standard Brownian motion,

(Nt)t∈R+ is a Poisson process with intensity λ > 0,

(Zk)k≥1 an i.i.d. sequence of random variables with probability distributionν(dx),

(Xt)t∈R+ a compound Poisson process with Levy measureµ(dy) = λν(dx). and finite intensity λ:

Xt =

NtXk=1

Zk , t ∈ R+, (3)

(Sxt )t∈R+ a jump-diffusion price process:8>><>>:

dSxt

Sxt

= r(Sxt )dt + σ1(S

xt )dBt + σ2(S

xt−)dXt ,

Sx0 = x .

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Jump diffusion model [DJ], [DP04], [BMM]

Price process:

dSζt

Sζt

= rdt + σ1dBt + σ2(dNt − λdt), Sζ0 = x .

w ∈ L2(R+) and

Dw f (Bt1 , . . . , Btn , T1, . . . , Tn) =nX

i=1

Z ti

0

wsds∂f

∂xi(Bt1 , . . . , Btn , T1, . . . , Tn).

Vega2, European options:

∂

∂σ2E [f (Sσ2

T )] = E

»f (Sσ2

T )BT

σ1T

„NT

1 + σ2− λT

«–.

Derivation with respect to absolutely continuous jump amplitudes [BMM].

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Jump diffusion model [DJ], [DP04], [BMM]

Price process:

dSζt

Sζt

= rdt + σ1dBt + σ2(dNt − λdt), Sζ0 = x .

w ∈ L2(R+) and

Dw f (Bt1 , . . . , Btn , T1, . . . , Tn) =nX

i=1

Z ti

0

wsds∂f

∂xi(Bt1 , . . . , Btn , T1, . . . , Tn).

Vega2, European options:

∂

∂σ2E [f (Sσ2

T )] = E

»f (Sσ2

T )BT

σ1T

„NT

1 + σ2− λT

«–.

Derivation with respect to absolutely continuous jump amplitudes [BMM].

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Jump diffusion model [DJ], [DP04], [BMM]

Price process:

dSζt

Sζt

= rdt + σ1dBt + σ2(dNt − λdt), Sζ0 = x .

w ∈ L2(R+) and

Dw f (Bt1 , . . . , Btn , T1, . . . , Tn) =nX

i=1

Z ti

0

wsds∂f

∂xi(Bt1 , . . . , Btn , T1, . . . , Tn).

Vega2, European options:

∂

∂σ2E [f (Sσ2

T )] = E

»f (Sσ2

T )BT

σ1T

„NT

1 + σ2− λT

«–.

Derivation with respect to absolutely continuous jump amplitudes [BMM].

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Jump diffusion model [DJ], [DP04], [BMM]

Price process:

dSζt

Sζt

= rdt + σ1dBt + σ2(dNt − λdt), Sζ0 = x .

w ∈ L2(R+) and

Dw f (Bt1 , . . . , Btn , T1, . . . , Tn) =nX

i=1

Z ti

0

wsds∂f

∂xi(Bt1 , . . . , Btn , T1, . . . , Tn).

Vega2, European options:

∂

∂σ2E [f (Sσ2

T )] = E

»f (Sσ2

T )BT

σ1T

„NT

1 + σ2− λT

«–.

Derivation with respect to absolutely continuous jump amplitudes [BMM].

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Vega2 as a function of K and T (finite differences, 10e4 samples, h=0.01)

0.4 0.8

1.2 1.6

2

T

40 60 80 100 120 140 160 180 200K

0

2

4

6

8

10

0.4 0.8

1.2 1.6

2

T

40 60 80 100 120 140 160 180 200K

0

2

4

6

8

10

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

Vega2 as a function of K and T (Malliavin method, 10e4 samples, h=0.01)

0.4 0.8

1.2 1.6

2

T

40 60 80 100 120 140 160 180 200K

0

2

4

6

8

10

0.4 0.8

1.2 1.6

2

T

40 60 80 100 120 140 160 180 200K

0

2

4

6

8

10

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus

E. Benhamou.

Smart Monte Carlo: various tricks using Malliavin calculus.Quant. Finance, 2(5):329–336, 2002.

M.-P. Bavouzet-Morel and M. Messaoud.

Computation of Greeks using Malliavin’s calculus in jump type market models.Preprint, 2004.

M.H.A. Davis and M.P. Johansson.

Malliavin Monte Carlo Greeks for jump diffusions.Stochastic Processes and their Applications.

V. Debelley and N. Privault.

Sensitivity analysis of European options in jump diffusion models via the Malliavin calculus on Wiener space.Preprint, 2004.

E. Fournie, J.M. Lasry, J. Lebuchoux, P.L. Lions, and N. Touzi.

Applications of Malliavin calculus to Monte Carlo methods in finance.Finance and Stochastics, 3(4):391–412, 1999.

E. Fournie, J.M. Lasry, J. Lebuchoux, and P.L. Lions.

Applications of Malliavin calculus to Monte-Carlo methods in finance. II.Finance and Stochastics, 5(2):201–236, 2001.

A. Kohatsu-Higa and R. Pettersson.

Variance reduction methods for simulation of densities on Wiener space.SIAM J. Numer. Anal., 40(2):431–450, 2002.

Y. El Khatib and N. Privault.

Computations of Greeks in markets with jumps via the Malliavin calculus.Finance and Stochastics, 4(2):161–179, 2004.

N. Privault and X. Wei.

A Malliavin calculus approach to sensitivity analysis in insurance.Insurance Math. Econom., 35(3):679–690, 2004.

Nicolas Privault Sensitivity analysis and density estimation using the Malliavin calculus