seizing opportunities in the current secondaries market dr

TRANSCRIPT

RREEF Research

February 2009

Seizing Opportunities in the Current Secondaries Market

Introduction A synchronized global recession is now a reality, compounded by the on-going stress in financial markets. The downturn in the economy and massive risk aversion has impacted all asset classes and all regions of the world. Alternative investments have not been immune as conditions in the credit environment have forever changed such high-leverage business models. Economic recession has resulted in the dimming prospects for corporate profitability which is a key driver of underlying fundamentals across the private equity industry in particular. This combined with the dearth in available financing has raised doubts about the private equity model in the near term, especially for the mega-buyout sector.

Even though the private equity industry does face some near-term challenges, opportunities are emerging across different strategies including secondaries and distressed. The increased need for liquidity by investors and a slowdown in underlying cash flow has enhanced the profile of the secondaries market. In light of an overall decline in valuations and a significant reduction in anticipated distributions, many private equity investors are re-forecasting their pacing models and cash requirements for 2009. As a result, many are considering tapping into the secondary market as a liquidity option or exit. It is, thus, our expectation that this will be the year of the secondary market of private equity as investors need to rebalance their portfolios or liquidate positions in existing funds. Pricing trends are favorable to secondary buyers as compared to previous years, leading to potential opportunities for secondary investors.

In this report, we focus on the outlook and opportunities for the secondary market of private equity. Following the introduction, we review current market conditions in the private equity and secondary market. In each case, the impact of the credit crunch is highlighted with an assessment of risks and rewards. The review of market conditions for secondaries sets the backdrop for a discussion on pricing trends. In the pricing section, we analyze various metrics to highlight valuations of existing private equity positions across funds. An update of pricing in the listed private equity market also provides insight as to pricing implications for the secondary market. The ability to purchase existing private equity stakes at deep discounts in the secondary market has clear positive implications for returns. Following the pricing discussion, we focus on returns in the secondary market. Next, we provide an update of the market participants in secondaries. No longer viewed as a niche strategy, the secondary market is attracting a host of new buyers with a range of differentiated investment strategies. The report concludes with an assessment of different strategies being pursued by secondary funds. We also believe that generalist secondary funds are likely to direct more capital to real estate and in some cases infrastructure.

Market Conditions: Private Equity The economic and financial landscape of 2008 was challenging for the private equity industry. Tightening lending standards, limited availability of debt, lower corporate profitability, and weak exit opportunities have dealt serious blows to the traditional private equity model. A main feature of private equity is the reliance on leverage and the enhanced return that leverage provides investors.

Prepared By:

Asieh Mansour Chief Economist & Strategist RREEF San Francisco USA (415) 262-2044 [email protected]

Jaimala Patel Vice President RREEF New York USA (212) 454-1752 [email protected]

Table of Contents:

Introduction............................... 1

Market Conditions: Private Equity .......................... 1

Market Conditions: Secondaries............................. 6

Implications for Pricing ............. 8

A Look at Returns................... 10

Opportunities

in Secondaries....................... 11

Market Participants in Secondaries....................... 13

Conclusion.............................. 15

Appendix................................. 16

References ............................. 22

This report is intended for distribution only to accredited investors and their representatives. It is made available on the condition that it may not be reproduced, copied or otherwise distributed to any person without the express consent of RREEF America L.L.C.. Failure to comply with this requirement could result in the violation of applicable securities laws.

2 Alternative Investments

During the 2005 to 2007 period, many private equity backed transactions were structured with high leverage some times with as much as eight times EBITDA. In some cases , private equity firms were assuming that only the interest would have to be repaid by the company’s cash flow and that the principal of the debt could be refinanced at the time of the exit. But with too much debt and too little cash flow, some private equity deals structured during the recent vintage years are now running into trouble. It is now clear that the more recent vintage private equity transactions are likely to significantly under-perform given the abundance of liquidity, lax lending terms when they were executed, and high prices paid for assets.

Three key macro trends impacting the private equity industry are highlighted below:

1. Lesser Availability of Credit

Up until the credit crunch, private equity had been a fast-growing segment of the investment universe. Leveraged buyout activity drove high transaction volume through much of 2005 through 2007. The access to debt, the lower cost of debt, and healthy corporate balance sheets drove deal volume over these three years. (Please refer to Exhibit 1.) The limited scale of current private-equity backed M&A activity is being driven primarily by the lack of confidence in the short term growth prospects, the overall volatility in the capital markets, and the lack of debt.

Today’s lesser availability of credit has disproportionately impacted leveraged buyout activity (LBO). Transaction activity slowed significantly in the fourth quarter. (Please refer to Exhibit 2.) The liquidity crisis has deprived the mega-LBO deals the cheap and relatively abundant bank debt traditionally used to finance transactions.

Exhibit 1Private Equity Backed Global M&A Activity ($B)

$0

$100

$200

$300

$400

$500

2005 Q4 2006 Q2 2006 Q4 2007 Q2 2007 Q4 2008 Q2 2008 Q4

North America Europe Rest of WorldSource: Dealogic

Exhibit 2LBO Volume ($B)

$0

$50

$100

$150

$200

$250

$300

2005 Q4 2006 Q2 2006 Q4 2007 Q2 2007 Q4 2008 Q2 2008 Q4

North America Europe Rest of WorldSource: Dealogic

Alternative Investments 3

For 2009, we expect the limited availability of credit to further slow transaction volume and lower valuation multiples. This will also be excerbated by the ongoing consolidation in the financial services sector. Since financing will not be available, especially for mega deals, private equity firms need to put down more equity. In this environment of limited liquidity, we should see more “equity cures”, when private equity firms inject more capital into their investment in order to heal them. This will lead to lower returns. Heading into 2009 then, private equity general partners (GPs) will be required to focus more on adding value operationally and/or cutting costs in order to preserve or grow cash flow rather than through any financial engineering.

2. Weak Exit Markets

The global recession and on-going financial crisis have led to rising defaults and bankruptcy filings across many corporations. A number of private equity backed companies were also forced into bankruptcy. (Please refer to Exhibit 3.)

A large number of private equity funds are facing massive losses as more of the companies they used leverage to buy are defaulting on their debt obligations and in some instances filing for bankruptcy. In some cases, the current fragile environment is leading to a bust in a variety of deals. We report some examples for 2007 and 2008 in Exhibit 4. The economic slowdown is hurting underlying cash flows at the same time that banks are tightening lending terms. In this environment, the ability for the buyout firms to cash out of these deals and exit via an initial public offering (IPO) or trade sales have evaporated.

Company Sponsor(s) Sector Reason CitedEOS Airlines Golden Gate Capital Airlines Unable to pass increasing fuel prices onto its customers

Maveron LLCSutter Hill Ventures

Global Motorsport Group Cerberus Capital Automotive Unable to service debtStonington Partners

Propex Inc. Genstar Capital Building Products Unable to service debtThe Sterling Group

Wellman Inc. Warburg Pincus Chemical Increased competition and commodities costs

Pierre Foods Inc. Madison Dearborn Partners LLC Consumer Products Soaring food costs

Sleep Innovations Inc. Catterton Partners Consumer Products Rising material costs, deterioration in the housing market and a generalslump in consumer spending

SemGroup LP Carlyle Group Energy Failed oil hedging startegy led to liquidity crisisRiverstone Holdings LLC

Hospital Partners of America Tailwind Capital Partners Healthcare/Medical Operating losses and liquidity concerns

Western Nonwovens Inc. Cerberus Capital Manufacturing Long-term liquidity problems, the rising cost of raw materials and decliningsales

Vertis Holdings Evercore Partners Media Recurring net losses and netative cash flow, unable to service debtThomas H. Lee Partners

CDX Gas LLC TCW Group Oil & Gas Exploration Inability to service debt payments

Linens 'N Things Inc. Apollo Management Retail Decline in profitability and liquidity

Mervyn's Holdings LLC Sun Capital Partners Retail Decline in profitability due to less consumer demand

Steve & Barry's LLC TA Associates Retail Liquidity, credit-market volatility and weak economy

Wickes Holdings LLC Sun Capital Partners Retail Slowing home sales and rising fuel prices led to a diminished demand

Hawaiian Telcom Communications Inc. Carlyle Group Telecommunications Debt levels and customer turnover

Jevic Holding Corp. Sun Capital Partners Transportation Housing and credit crisis led to lowered volume of motor vehicle shipments

Source: Thomson Reuters, Buyouts, peHUB and Bankruptcy Research Database

Exhibit 3Select LBO-Backed Companies That Filed For Bankruptcy Protection in 2008

4 Alternative Investments

In the US market, the sharp economic downturn and seizing up of credit markets has resulted in an upward trajectory in business bankruptcy filings. This is a trend we had not seen since the early 1990s. (Please refer to Exhibit 5.)

So far in this recession, retail and consumer-oriented investments have been hit the hardest.

Higher bankruptcies and busted deals have led to weaker exit markets. Private equity firms are now holding on to LBO-backed firms longer. The weak exit market will continue to delay the private equity sponsors’ ability to cash out of these companies by at least a couple of years. In some cases, private equity firms will actually be inclined to put more capital into those firms believed to stand a good chance of surviving the recession. The delay in cash outs will lower private equity returns and slow distributions back to limited partners (LPs).

Target Acquirer Announced Withdrawn Transaction Value

SLM Corp. J.C. Flowers, Friedman Fleischer & Lowe, Bank of America, JPMorgan 4/16/07 12/12/07 $24.63 billion

Cablevision Management Led Buyout 5/2/07 10/24/07 $8.23 billion

Harman International KKR, Goldman Sachs Capital Partners 4/26/07 10/23/07 $7.86 billion

ADS Blackstone 5/17/07 4/18/08 $6.43 billion

Penn National Centerbridge Partners, Fortress Investment Group 6/15/07 7/3/08 $5.73 billion

Triad Hospitals Goldman Sachs Capital Partners, CCMP Capital 2/5/07 3/19/07 $4.44 billion

United Rentals Cerberus 7/23/07 12/24/07 $2.82 billion

3Com Corporation Huawei, Bain Capital 9/28/07 3/20/08 $2.12 billion

Acxiom ValueAct, Silver Lake Partners 5/16/07 10/1/07 $1.83 billion

EGL The Woodbridge Company, Centerbridge Partners 1/2/07 5/24/07 $1.82 billion

PHH Corporation General Electric, Blackstone Group 3/15/07 1/1/08 $1.7 billion

Catalina Marketing ValueAct 2/21/07 4/17/07 $1.27 billion

Aeroflex General Atlantic LLC, Francisco Partners 3/2/07 5/25/07 $994.15 million

Myers Industries Goldman Sachs Capital Partners 4/24/07 4/4/08 $789.98 million

Reddy Ice GSO Capital Partners 7/2/07 1/31/08 $681.54 million

Cumulus Media Merrill Lynch Global Private Equity 7/23/07 5/12/08 $467.48 million

Source: FactSet MergerMetrics, WSJ

Exhibit 4Largest Busted LBOs, 2007-2008

Exhibit 5Total US Business Bankruptcy Filings, YE 1991-2009

0

5

10

15

20

25

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

(in th

ousa

nds)

Source: Office of U.S. District Courts, Moody's Economy.com

Alternative Investments 5

The listed market is under pressure as well, closing another exit option for private equity firms. As a result, the full impact of the credit crunch on private equity has yet to be seen, but a significant decline in performance is anticipated. A proxy for private equity performance is the S&P listed private equity index. As reflected in Exhibit 6, its performance has trailed that of the overall S&P 500 index and is a barometer of return expectations.

3. Denominator Effect

With rampant risk aversion in this credit environment, all asset classes have suffered. Public equity and other liquid parts of investor portfolios have declined in value as a result. By contrast illiquid asset classes, including private equity, have yet to fully re-price. This is exacerbated by a lag in reporting values by private equity firms as compared to daily valuations in the public equity markets. Falling public equity markets have left investors over-allocated to private equity as a proportion of their overall portfolio. We do expect, however, for private equity portfolios to be eventually marked down.

This so-called “denominator effect” has lowered near-term investor appetite for new allocations to private equity funds. Moreover, the collapse in M&A deal activity and debt and equity refinancings has meant that investors are not receiving their anticipated proceeds from exits, leaving them further exposed to private equity. This has been dubbed the “double-denominator effect”.

In some cases, investors in desperate need for liquidity are defaulting on their private equity commitments. More recently, some of the prominent private equity firms have released investors from a portion of their capital commitments.

Even though the private equity market faces some near-term challenges, we are optimistic about the long-term prospects for this asset class. The principal area of concern remains mega-buyouts during the vintage 2005 to 2007 years. On a risk-adjusted historic long term basis, however, private equity has outperformed traditional assets such as stocks and bonds. During the current downturn, there will be a more systematic differentiation between the experienced and successful GPs and the less skillful ones. Operational efficiency and value-add strategies at the firm level will replace financial engineering as the prime source of higher private equity returns for the current cycle.

Paradoxically, given the distress in economic fundamentals, many investors view 2009 as a great vintage year to invest in private equity. As a result, some investors are keen to deploy more capital to increased opportunities at the current price or are using the secondary market to diversify across vintage 2005-2007 funds at a lower attractive price.

Exhibit 6Listed Private Equity Performance

0

50

100

150

200

250

Dec-06 Mar-07 Jun-07 Sep-07 Dec-07 Mar-08 Jun-08 Sep-08 Dec-08020040060080010001200140016001800

S&P Listed Private Equity Index (L) S&P 500 (R)Source: Bloomberg

6 Alternative Investments

Market Conditions: Secondaries In the Fall of 2007, RREEF Research authored a paper entitled “The Secondary Private Equity Market in Perspective”. In it, the rationale for participating in the secondaries market was laid out. Amongst the benefits auctioning private equity commitments provides to sellers is liquidity for a traditionally illiquid asset class, the opportunity to lock-in returns early, the ability to rebalance investment portfolios and a tool to manage risk. While for buyers, the purchasing of secondaries provides access to older vintages of private equity funds, reduces the effects of the J-curve, eliminates blind-pool risk and provides for instant diversification. (For further information on the development of the secondaries market, please refer to the Appendix.)

Because of its attractiveness, in the past 18 months, the secondaries market has undergone a proliferation in terms of fundraising and deal volume. (Please refer to Exhibit 7.)

In 2008 alone, transaction activity was close to $20 billion—this in spite of the prolonged upheaval in the credit market. Furthermore, an excess of $34 billion in the current fundraising pipeline will provide additional dry powder for deals over the next few years. By comparison, both fundraising and deal volume in 2007 were around $14 billion. With a growing acceptance of secondaries as a viable exit and investment strategy as well as increasing sophistication of the market, this trend is anticipated to continue.

The reasons for this are multifold:

Fallout from the Credit Crunch

• Increased pressure is expected on distributions and returns which is prompting investors to unload commitments into the secondaries market.

• Investors are seeking to dilute their exposure to recent vintages of large- and mega-buyout funds which are expected to under-perform due to their reliance on highly leveraged companies, some of which are likely to default.

Distressed Situations

• In order to strengthen their balance sheets, some distressed investors are selling non-core assets and considering selling commitments.

• Other investors who are under severe financial duress and unable to meet their unfunded capital commitments must exit their obligations through secondaries.

Market Volatility

• In the wake of the declining stock market, investors who find themselves over-allocated to private equity are reducing their positions.

Exhibit 7Secondary Market Activity ($B)

$0

$5

$10

$15

$20

$25

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Secondary Fundraising Secondary Deal Volume

Source: Lexington Partners, Private Equity Analyst

Alternative Investments 7

• The spate of bad news and continued market volatility are seen as signals for some investors to “cut their losses” and sell fund interests early as they expect returns to continue to deteriorate.

Effective Portfolio Management

• Investors want to limit their number of managers and focus on core relationships.

• Investors are also looking to redirect resources to other asset classes which are seen as less risky and less volatile.

Immediate Need for Liquidity

• Time-constrained investors, like hedge funds, need to sell commitments in order to return capital to their investors in an expedient manner.

• The frequency of capital calls has overtaken the pace of distributions, creating a vacuum of capital for investors.

Last year, we witnessed a number of significant market events that have helped shape the current secondary private equity environment. Most recently, ABN-Amro sold a portfolio of private equity interests in 32 European companies to a consortium comprising of Goldman Sachs, AlpInvest and CPP for $1.5 billion. The University of Texas Investment Management Company sold $250 million in private equity fund interests on the secondary market to more than a half dozen buyers. And the California Public Employees’ Retirement System sold a portfolio of over 50 legacy private equity commitments for $3 billion to a syndicate of five investors—the second largest transaction of its kind. Over the next few years, deals of this size and profile are expected to become even more commonplace.

Market Risks Fuel Current Secondaries Interest

Sanguine market conditions preceding the latter half of 2007 had been all pointing towards a growing global economy, a robust financial environment and a burgeoning private equity sector. It was indeed a seller’s market for secondaries, as investors who might have been late to the private equity game were looking to make a quick entrance by purchasing commitments—often at a premium to net asset value (NAV). However, in the course of 2008, conditions changed drastically and the tide turned. (Please refer to Exhibit 8.)

Previous State of the Market Benefits to Secondaries Sellers Current State of the Market Benefits to Secondaries BuyersCheap and Plentiful Credit Investors want access to top-performing Credit Crunch Inability to finance deals with a low cost of

large buyout funds. Sellers are able to capital make large buyouts less attractive. sell these commitments at a premium. Reduced performance expectations have

buyers netting deep discounts for stakes.

Bullish Performance of An influx of capital and peaking private Decline in Public Equity Denominator effect forces sellers to Private Assets equity performance run up bids for Market reduce exposure to private equity.

secondary commitments. Buyers are Pension funds, endowments, etc. mustwilling to pay the price necessary to win sell commitments to cover liquiditydeals. requirements.

Record Number of Deals Private equity portfolios begin to take Deal Activity Comes to a With deal activity being moribund and the Being Completed shape quickly. Transparency and volume Standstill exit environment looking grim, some

of deals completed pique buyers interest. sellers are anxious to shed their private equity commitments. Opportunistic buyers are able to take advantage.

Global Economies are Investment opportunities are abundant in Widespread Recession "Golden Age" of private equity is over. Key Booming all geographies and industries. Strong private equity sectors, especially those

corporate balance sheets raise investor related to consumer goods, are suffering. confidence and risk-taking. Investors in distressed situations need to

recapitalize themselves by selling down commitments.

Source: RREEF Alternative Investments

First Half of 2007 First Half of 2009

Exhibit 8Changing Conditions have Shifted Secondaries from a Seller's Market to a Buyer's Market

8 Alternative Investments

The credit crunch, faltering equity markets, declining deal volumes and global recession have all introduced elements of downside risk and stress into the financial marketplace that need to be mitigated. As reviewed in an earlier section of this report, these adverse conditions have particularly taken a toll on the private equity market. The unavailability of credit has made private equity interests in leveraged companies particularly less attractive. Fewer deals are being executed and the use of leverage, which once bolstered returns, is nonexistent. The global recession is stalling growth for key private equity sectors.

In the initial stage of the private equity downturn, some institutional investors were first to anticipate market corrections and began preparing for portfolio sales in late 2007. Pension funds and endowments began to use secondaries as a way to rebalance their private equity portfolios; first, taking a top-down view as to how they fit within their overall investment portfolio and second, examining individual commitments and carving out non-core pieces. Since this rebalancing was done proactively, first-movers in the secondaries market were by and large price-setters. However, with the subsequent drop in the equity market in 2008, selling private equity commitments had become even more imperative. Institutional investors were hit hard by the denominator effect, often leaving them over-exposed to alternative investments and with a shortage of liquidity. These distressed sellers, facing a market where the supply of secondaries outstripped demand, had been forced to become price-takers.

Family offices and high net worth investors, whose actions typically trail those of institutional ones, are following suit by planning dispositions from the second half of 2008 to the first half of 2009. Distressed market conditions can often hit these smaller investors harder, making them more likely to execute deals out of necessity rather than for strategic reasons. In addition, some family offices and high net worth investors had relied on excessive use of leverage, sometimes financed through asset backed investments such as real estate, which have now also lost value.

Implications for Pricing In order to fully understand the effects of market risks on secondaries pricing, it is important to first consider what has been happening to private equity valuations. With the current economic and financial markets still in turmoil, it is not surprising that valuations for private equity funds have been plummeting. Not only is the short- to medium-term growth outlook for portfolio companies generally somber, but when compared to the high water mark valuations hit just a few years ago, the decline is startling. Moreover, funds that purchased at the top of the private equity cycle and paid over-inflated prices for deals look to suffer the most.

The decline in valuations is to be further exacerbated with new mark-to-market accounting rules (FAS 157) currently taking effect. GPs are now obligated to value their companies as if they were to sell them today instead of valuing them at cost. Furthermore, private equity valuations lag by one to two quarters so the fall-out from this past summer’s financial meltdown and economic contraction will not truly be captured until fourth quarter 2008 reports are released in March/April 2009.

The implication of falling valuations on secondaries pricing is two-fold. First, prospective secondaries sellers are anxious to shed private equity stakes as quickly as possible. They want to do so before the NAV of their portfolio falls any further, before the prices they can command for their commitments are driven down, before they are laden with more capital calls and before their liquidity dries up. Second, in anticipation of further portfolio write-downs, buyers are insisting on higher discounts to NAV to take over commitments in riskier funds. They believe that current valuations are outdated and that current market conditions have yet to be fully priced in. The combination of these two factors has culminated in a dramatic shift in pricing. After three years of being a seller’s market, pricing levels for secondaries has shifted in favor of buyers. According to Cogent Partner’s most recent secondary pricing survey, pricing

Alternative Investments 9

as a percentage of NAV has dropped to an average high bid of 61.0% of NAV as of the second half of 2008. (Please refer to Exhibit 9.)

Comparatively, the average winning bid was 108.2% of NAV in 2006, 104.1% of NAV in 2007 and 84.7% of NAV in the first half of last year. (Please refer to Exhibit 10.)

Separately, venture funds achieved an average high bid of only 55.0% since many of them are fully invested and face a tough exit environment. Buyouts fared only slightly better, with the average high bid being 64.7%. Investors are essentially purchasing risk when taking on large unfunded commitments in buyout funds with precarious deal prospects.

The current discount to NAV for secondaries parallels what we have been witnessing in the public market. Most listed private equity funds are currently trading at between -40% to -75% of NAV. (Please refer to Exhibit 11.)

Exhibit 9Secondary Pricing as % of NAV

50%

60%

70%

80%

90%

100%

110%

2003 2004 2005 2006 2007 1H2008 2H2008

Buyout Venture All Private Equity

Source: Cogent Partners Secondary Market Pricing and Outlook

Exhibit 10Secondary Bid Spreads by Fund Type

40%

50%

60%

70%

80%

90%

100%

110%

All All All Buyout Buyout Buyout Venture Venture Venture

2007 1H2008 2H2008 2007 1H2008 2H2008 2007 1H2008 2H2008

High Low AverageSource: Cogent Partners Secondary Market Pricing and Outlook

10 Alternative Investments

This is due, in part, to lower confidence in the private equity sector, as well as contagion from the broader equity market. Although we do not anticipate secondaries to be discounted as sharply, the public market is a fair indicator of how long we can expect discounting to continue and when valuations should begin to rise again.

Going forward, secondaries will continue to be priced at a significant discount to NAV. Valuation concerns aside, buyers are entering into deals knowing that they will need to ride out a tough market before their investment pays off. Some private equity-backed companies are likely to go bankrupt or require significant restructuring. Holding periods of the remaining portfolio companies will be long, the exit environment will be difficult, and distributions will be slower. However, if priced correctly, we believe that secondary stakes can still produce solid returns.

A Look at Returns What are the return profiles for funds vested in secondary commitments like? Data is scant and as the market continues to mature, the past may be a tepid indicator as what we can expect from future performance. Historically, transactions have shown little correlation between the purchase price of secondaries as a percentage of NAV and their future performance. Asset value appreciation has typically been responsible for a large share of value-creation in secondary transactions as opposed to just buying-in at a significant discount. Secondary performance has also been influenced by strong historical returns of the primary private equity market and favorable track records of selected managers.

The performance of secondaries in the current cycle may hinge on a different set of factors, however. Given the widespread dour outlook of many private equity sectors, returns this time around may be driven more by the purchase price of commitments rather than increasing valuations. Given the steep discounts to NAV that buyers are currently able to command, a portfolio that is able to hold its current NAV through the remaining life of the fund can outperform a portfolio that was purchased near NAV yet unable to increase its valuation. To the buyer’s benefit, having knowledge of the underlying assets of a portfolio makes it easier to model future valuations, price-in the appropriate amount of risk and offer bids that should clear a minimum equity multiple or IRR hurdle. If the return scenarios of a potential deal do not measure up, prudent investors often abandon it rather than incur a hit to their portfolio.

Exhibit 11Listed Private Equity Premium/Discount to NAV

-100

-80

-60

-40

-20

0

20

40

Mar-06 Sep-06 Mar-07 Sep-07 Mar-08 Sep-08

3i Group AIG Private EquityBear Stearns Private Equity Castle Private Equity Conversus Capital Lehman Brothers Private Equity Partners Pantheon International Participations Partners Group Global Opportunities

Source: Bloomberg

Alternative Investments 11

According to Cogent Partners, implied return rates have been underwritten to extend from 10% to 25% over the past three years, with an emphasis on the higher end of the range for the current market scenario.

The data that we do have available on secondary funds shows that, on average, they have generated an equity multiple between 1.2x and 2.8x over a 15-year period. (Please refer to Exhibit 12.)

In the five-year period beginning in 2000, secondary funds have achieved an equity multiple that is greater than most venture funds yet less than the average buyout fund. The last year we have meaningful return data is for 2005. We expect that as private equity continues to weather through the down-cycle, equity multiples for buyout funds and venture capital will decrease while secondaries performance should hold steady. Secondaries should also present a lower risk strategy due to their semi-transparent nature vis-à-vis other private equity strategies. Finally, since their investment duration is shorter, secondaries should achieve higher overall IRRs.

Opportunities in Secondaries With the maturation of the secondary market of private equity, the range of products being transacted is expanding. Traditionally, much of the focus of secondary acquisitions has been the purchase of LP interests in buyout, growth capital and venture portfolios. As the market has grown and evolved, secondary transactions have involved increasingly complex strategies and new industry sectors.

The different vehicles and niche strategies in the secondary market are listed below:

• Specialized Secondary Funds: These funds have traditionally been focused on limited partnership interests. They came out of the dot.com boom and until recently have been much more focused on the technology sector. The root of the secondary market is with the bust in the technology sector earlier this decade. Many private equity investments in venture capital funds were illiquid and the secondary market provided an option for liquefying these stakes. Targeted industries have included software, telecom and healthcare.

• Direct Secondaries: An increasing number of secondary funds are more directly focused on purchasing positions in a portfolio of individual companies rather than an existing fund interest in a large number of companies. This type of secondary investment is expected to increase over the next several years with activity generated by both venture capital and

Exhibit 12Weighted Average Equity Multiple

0

1

2

3

4

5

6

7

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

Secondaries All Private Equity

Buyouts Venture

Source: Preqin, RREEF Research calculations

12 Alternative Investments

buyout general partners who are trying to sell-off the remaining assets in mature funds. In both the specialized funds and the direct secondaries, the key buyers in the market are sophisticated secondaries specialists that can appropriately price the interests whether on a direct or portfolio level.

• Real Estate Secondary Funds: Secondary buyers have set their sights increasingly on the private equity real estate market. The driving factors leading real estate investors to tap into the secondary market are very similar to the factors that have driven private equity LPs recently. The real estate market structured through LP funds has significantly grown over the last decade. The availability of leverage during 2005 through 2007 has also led to a rapid pace of real estate acquisitions activity among LPs. Reportedly, over the past five years, about $3 billion in capital has been raised and invested by secondary real estate fund managers. As market dynamics have changed and investors have liquidity needs, real estate investors are also rebalancing their real estate portfolios. Much more real estate interests are expected to come on the market in 2009 as many investors are over allocated to this asset class as a result of the denominator effect. Many investors are looking at the secondary market as a more efficient way of gaining exposure to other geographies and sectors as well. We expect the real estate secondary market to grow with new supply and increasing amount of interest among investors.

Exhibit 13 summarized key trends in the secondary market. We break down fund activity across mega funds, midsize funds, and new entrants. In terms of the availability of dry powder, mega funds continue to dominate. In the following section, we will also summarize the key secondary market participants going forward.

Exhibit 13Secondary Market Dynamics

Active SecondaryFunds in 2009-10(1)Fund Size

($ MM)

Megafunds:8-10 active managers

~$25 bn

Midsize Funds:6-8 active managers

~$6 bn

Small Funds / New Entrants:

15+ active managers~$3 bn

Smaller pool of secondary buyers

• Opportunistic participants retreated

• Few new entrants

New larger funds• Established players have

scaled up to Mega Secondary funds ($2bn+)

Human resource constrained• Need for larger teams /

some movement of people

Attractive mid-marketAble to participate in larger deals (via syndication) and smaller transactionsFewer direct competitors

Est. Dry PowderTo be spent in 2009-2011(2)

100

10,000

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Closed

Fundraising / to launch

100

10,000

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Closed

Fundraising / to launch

2,000

500

Less efficient and less competitive market segment

~$34 bn

Secondary Funds: How Big They Will Get?

Source: RREEF Estimates based on Preqin Private Equity, DJ Private Equity Analyst, and market research

(1) Funds raising and not closed yet / funds announced to raise(2) Aggregate estimated amounts available for 2009-2011 secondary transactions

Alternative Investments 13

Market Participants in Secondaries Active participation in the secondary market of private equity is becoming widely accepted among both limited partners and general partners. The change in perception towards secondaries has broadened the diverse set of players in this market. As compared to a decade ago, there is no longer a stigma attached to participation in the secondary market and indeed investors often operate in both the primary market and secondary market of private equity.

There are two main groups of players in private equity’s secondary market.

Sellers: A large number of private equity investors are currently also secondaries sellers. Commensurate with the tremendous growth in the private equity asset class, the seller base of the secondary market has increased significantly. There are numerous reasons for investors coming to the secondary market to sell a private equity interest, especially in this credit environment. These include the need for liquidity in distressed situations, active portfolio management, the need to mitigate the denominator effect of over allocation to private equity, diversification across vintage years, and consolidation across the stronger managers. For a complete review of seller considerations in the secondary market, please refer to the Appendix following this report. The sale of private equity interests on the secondary market is being driven by different types of sellers as highlighted below:

• Limited Partners familiar with the secondary market including large public pension plans and endowments/foundations. A couple of active participants in recent transactions include CALPERS and the University of Texas Investment Management.

• Limited Partners unfamiliar with the secondary market.

• Corporate owners of non-public assets.

• Distressed sellers needing liquidity including insurance companies (AIG), investment banks (Lehman), and General Partners/Managers (Citigroup).

• Banks who want to get out of the private equity sector. For example, Bank of America sold its North America venture capital division to a group of secondary investors.

• General Partners who are not in distress have also been more willing to transact in the secondary market. The motivation is largely to strengthen their returns by selling tail-end funds. Moreover, the limited exit alternatives are leading to increased sales of tail-end portfolio sales among GPs.

• Hedge Funds have been tapping the secondary market to satisfy redemption queues.

• Publicly-traded funds (KKR Private Equity Investors LP, SVG Capital etc.) which have overcommitted to certain private equity deals or need to raise capital due to a slower distribution environment.

14 Alternative Investments

Buyers: The secondaries market is attracting new buyers including more than just the secondary specialists. In many cases, investors are looking for ways to augment their private equity exposure and are using secondary commitments to complement those in the primary market. The enhanced liquidity has attracted a variety of new buyers. There are many advantages in buying existing private equity interests. Investors get immediate exposure to private equity interests, the required lock-in period is shorter and the J-curve effect is effectively avoided. There is also much a greater degree of transparency when purchasing secondary interests. The underlying companies have had several years of performance history under their belt. The list of secondary buyers includes more than just secondary specialists who have been the established players.1 The participants include:

• Secondary Funds

• Fund of Funds

• Sovereign Wealth Funds

• Insurance Companies and Banks

• Endowments/Foundations

• Family offices and high net worth investors

1 We are getting nascent indications that the pool of secondary buyers is altering. There is growing evidence that opportunistic participants have exited or have become active sellers and the number of new entrants has shrunk.

Exhibit 15Expanding Secondary Buyer Universe

Consultant2%

Hybrid25%

Corporate Pension 1%

Fund of Funds35%

Insurance Company8%

Sovereign Wealth

2%Bank2%

Family Office

5%

Secondary Fund16%

Endowment/ Foundation1%

Public Pension3%

Source: Probitas Partners

Reasons for Selling

Recycle Capital/ Create Capacity

40%

Exiting Non-Core Relationships

27%Opportunistic

Seller13%

Portfolio Rebalancing

13%

Reduce Exposure to

Mega Buyouts7%

What is Being Sold

Early-Stage VC29%

Small-Mid Buyout26%

Real Estate16%

Late-Stage VC10%

Mega Buyout10%

Credit Strategies6%

Mezzanine3%

Seller Profiles

Pension Fund25%

Fund of Funds15%

Insurance Company

18%

Bank21%

Endowment/ Foundation

21%

Exhibit 14The Private Equity Seller Market

Source: Probitas Partners

Alternative Investments 15

In the current environment, the supply of investors’ partnership interests is greater than demand. We estimate that sellers have between $50 billion - $150 billion for sale. This is over 5% of the $1.2 trillion private equity market. The supply estimate refers to the sum of both NAV and the unfunded commitment. Applying current market discounts, the amount for sale is $30 billion to $75 billion. By contrast, the capital available for transactions in 2009-2011 is estimated at $34 billion.2 This mismatch between supply and demand of secondhand private equity fund commitments should place further downward pressure on pricing.

Conclusion Increasing economic and financial stress is impacting the performance of all asset classes. Investors who find themselves overstretched with their private equity commitments, are increasingly tapping into the secondaries market. The favorable pricing that secondary buyers command in this environment underpins our sanguine outlook for this sector of the private equity investment universe. Indeed, 2009 should be a key year for opportunities in the secondary market. Investors, however, should seek GPs that have experience in pricing secondary stakes and experienced management teams.

2 This figure includes unallocated capital in 2006-2008, active secondary funds and the estimated fundraising of secondary funds in the market or announced to be in the market in 2009-2010.

16 Alternative Investments

Appendix Introduction to Secondaries

Secondary private equity can apply to either the sale of privately managed companies amongst managers or the sale of interests in existing private equity funds between investors. A traditional private equity fund, comprised of both a GP and a collection of LPs, typically seeks to invest in emerging or existing firms that exhibit potential for value creation through private control. As the life of the fund winds down, managers must decide how to relinquish control of their fund’s portfolio companies in order to return capital back to investors. Common exit strategies include initial public offerings and company buy-backs. Another option is to sell the company to another private equity firm, which is often referred to as a secondary buy-out, or sell an entire portfolio of companies to a secondary fund, which is commonly known as a direct secondary. Both of these tail-end fund transactions are fairly widespread and represent a means by which multiple private equity firms can realize value from the same investment.

Likewise, the secondary market provides an exit strategy for LPs who, for a number of different reasons, may want to withdraw from a private equity fund prior to maturity. The selling of an LP’s commitments to another party, whether it is a direct investor or a fund of funds manager, represents the other facet of the secondary private equity market. Historically about 3% of equity commitments change hands over the life of a fund but this figure is expected to double over the next few years as this strategy becomes increasingly desirable to LPs and investors. Secondaries function as a revolving-door to the world of private equity, mutually beneficial to those entering and exiting the market. From a seller’s vantage, secondaries allow for greater liquidity, provide the ability to lock-in returns early and serve as an effective portfolio management tool. Buyers have equally been drawn to secondaries as they help build mature private equity portfolios quickly, require a shorter investment period, involve greater transparency and diversification and offer attractive entry strategies and valuations.

Development of the Market

The secondary private equity market has become much more efficient and well-developed since its beginnings 20 years ago. Although the inherent structure of private equity excludes any formal trading of interests, informal trading mechanisms have developed recently allowing transactions to take place. This is evidenced by the secondary market deal volume expanding exponentially over the past five years from an estimated $7.0 billion in 2003 to $19.9 billion in 2008.

The view that yesterday’s primaries are today’s secondaries explains the supply-driven growth of the market. Secondary private equity interests descend from the reselling of primary commitments with a lag time of two to five years. Given this scenario, it is fairly easy to foresee the potential size of the secondary market and to prepare to take advantage of the opportunities it presents. Stemming from $500 billion of primary commitments recorded in 2007, secondary deal volume could grow by an additional $15 billion to $30 billion over the next few years. Today, there is an estimated $25 billion of dry powder available for secondary private equity transactions.

Alternative Investments 17

Similarly, demand-driven growth of secondaries has been perpetuated by changing needs and perceptions towards private equity on the part of investors. Investors are constantly increasing their allocations towards private equity and feel ever-more comfortable and confident dealing in the secondary space. Much of this growth is attributable to secondary fund activity. Specialized secondary funds are dedicated to buying secondary commitments from willing sellers while funds of funds tend to have a mix of both primary and secondary commitments. Both these types of investors purchase secondary interests from LPs in order to create a portfolio of investments and generally target funds that are 50% to 80% invested. Secondary fund managers require strong transaction and deal-sourcing skills, ability to price underlying portfolio companies and agility in pulling together a significant amount of resources in a short amount of time. Between 2000 and 2007, secondary fundraising tripled from $4.7 billion to $14.2 billion. This growth is expected to continue over the long-term, especially given the size of the current primary market and the increasing supply of investors looking to take down their private equity interests.

Exhibit APrivate Equity Fundraising ($B)

$0

$100

$200

$300

$400

$500

$600

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Buyout Real Estate Venture Fund of Funds Other

Source: Preqin

Exhibit BSecondary Market Activity ($B)

$0

$5

$10

$15

$20

$25

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Secondary Fundraising Secondary Deal Volume

Source: Lexington Partners, Private Equity Analyst

18 Alternative Investments

The Benefits of Secondaries

From a Buyer’s Perspective

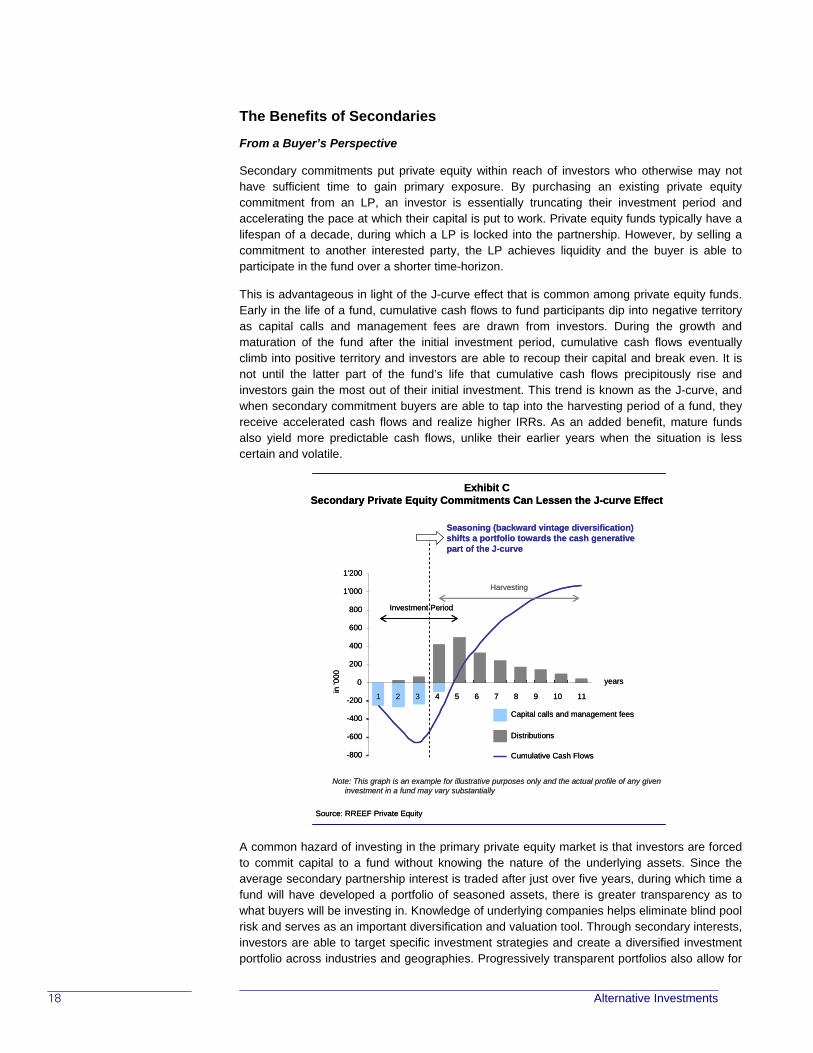

Secondary commitments put private equity within reach of investors who otherwise may not have sufficient time to gain primary exposure. By purchasing an existing private equity commitment from an LP, an investor is essentially truncating their investment period and accelerating the pace at which their capital is put to work. Private equity funds typically have a lifespan of a decade, during which a LP is locked into the partnership. However, by selling a commitment to another interested party, the LP achieves liquidity and the buyer is able to participate in the fund over a shorter time-horizon.

This is advantageous in light of the J-curve effect that is common among private equity funds. Early in the life of a fund, cumulative cash flows to fund participants dip into negative territory as capital calls and management fees are drawn from investors. During the growth and maturation of the fund after the initial investment period, cumulative cash flows eventually climb into positive territory and investors are able to recoup their capital and break even. It is not until the latter part of the fund’s life that cumulative cash flows precipitously rise and investors gain the most out of their initial investment. This trend is known as the J-curve, and when secondary commitment buyers are able to tap into the harvesting period of a fund, they receive accelerated cash flows and realize higher IRRs. As an added benefit, mature funds also yield more predictable cash flows, unlike their earlier years when the situation is less certain and volatile.

A common hazard of investing in the primary private equity market is that investors are forced to commit capital to a fund without knowing the nature of the underlying assets. Since the average secondary partnership interest is traded after just over five years, during which time a fund will have developed a portfolio of seasoned assets, there is greater transparency as to what buyers will be investing in. Knowledge of underlying companies helps eliminate blind pool risk and serves as an important diversification and valuation tool. Through secondary interests, investors are able to target specific investment strategies and create a diversified investment portfolio across industries and geographies. Progressively transparent portfolios also allow for

Note: This graph is an example for illustrative purposes only and the actual profile of any given investment in a fund may vary substantially

Seasoning (backward vintage diversification) shifts a portfolio towards the cash generative part of the J-curve

-800

-600

-400

-200

0

200

400

600

800

1'000

1'200

in '0

00

Capital calls and management fees

Distributions

Cumulative Cash Flows

Investment Period

Harvesting

years

1 2 3 4 6 7 8 9 105 11

Exhibit CSecondary Private Equity Commitments Can Lessen the J-curve Effect

Source: RREEF Private Equity

Note: This graph is an example for illustrative purposes only and the actual profile of any given investment in a fund may vary substantially

Seasoning (backward vintage diversification) shifts a portfolio towards the cash generative part of the J-curve

-800

-600

-400

-200

0

200

400

600

800

1'000

1'200

in '0

00

Capital calls and management fees

Distributions

Cumulative Cash Flows

Investment Period

Harvesting

years

1 2 3 4 6 7 8 9 105 11

Exhibit CSecondary Private Equity Commitments Can Lessen the J-curve Effect

Source: RREEF Private Equity

Alternative Investments 19

thorough due diligence of assets which ultimately aids in the valuation process and helps generate higher risk-adjusted returns.

Historical transactions have shown little correlation between the purchase price of secondaries and their future performance, which is reassuring news to investors who may view second-hand assets as potentially inferior. Asset appreciation is responsible for a large share of value-creation in secondary transactions as opposed to just buying-in at a significant discount. Secondary performance is also influenced by strong historical returns of the primary private equity market and favorable track records of selected managers.

Finally, secondary private equity lets buyers retroactively invest in funds that are no longer open to subscription, gain exposure to vintage years that have since passed and rapidly build a portfolio of interests. With the benefits of hindsight, investors who missed their chance to partner with certain managers first time around may be able to assume the commitments of existing investors and enter into funds mid-cycle. Furthermore, some GPs will not allow LPs into a fund without a prior commitment or relationship, therefore entering selective funds after they have closed can serve as a gateway to an exclusive set of managers. The same goes for buying into particular vintage years which may show their merits down the line after sufficient time has passed. Vintage year diversification is particularly helpful in reducing the J-curve effect as previously discussed.

Note: This graph is an example for illustrative purposes only and the actual profile of any given investment in a fund may vary substantially

Exhibit DValue Appreciation

Source: RREEF Private Equity

Value appreciation responsible for larger share of value creation in a secondary transaction

100

Portfolio Cost

1.0x cost

Realized Cash proceeds

1.7x cost

0.1x cost

10

0.6x cost

60

170

NAV Discount at Purchase

Appreciation of Assets

RealizedValue Creation

70100 170

Note: This graph is an example for illustrative purposes only and the actual profile of any given investment in a fund may vary substantially

Exhibit DValue Appreciation

Source: RREEF Private Equity

Value appreciation responsible for larger share of value creation in a secondary transaction

100

Portfolio Cost

1.0x cost

Realized Cash proceeds

1.7x cost

0.1x cost

10

0.6x cost

60

170

NAV Discount at Purchase

Appreciation of Assets

RealizedValue Creation

70100 170

Exhibit ECurrent Profile of Secondaries Buyers

Other11%

Family Office5%

Insurance Company

8%

Secondary Fund16%

Hybrid25%

Fund of Funds35%

Source: Probitas

20 Alternative Investments

From a Seller’s Perspective

The underlying liquidity of the secondary market serves as an effective portfolio and risk management tool for investors. Similar to a buyer’s situation where secondary interests help shorten the time commitment to private equity, proactive sellers can use secondaries to exit funds early with the purpose of locking-in returns and redeploying capital elsewhere. Moreover, this exit strategy allows investors to quickly rebalance their portfolio in the event of an asset over-allocation problem or from a diversification standpoint. Secondaries help alleviate the “denominator effect” when investors, who must adhere to a fixed upper-bound percentage of assets in private equity, find that they need to reduce their holdings if the value of their other assets such as stocks and bonds diminish. This scenario is especially true for institutional investors who may have more stringent investment parameters. Nearly a quarter of all investors acknowledge using secondaries to restructure their private equity portfolios.

Situations specific to a fund or an investor can also prompt a sell-off in private equity commitments. Fund governance issues involve changes in management, strategy, or ownership while fund performance concerns can include deflation or dilution of investment value and earnings volatility. From the investor’s side, mergers or acquisitions, redirection of strategy, changes in organizational structure, capital adequacy requirements, financial restructuring and manager consolidation are oft-cited reasons for exiting private equity partnerships prematurely.

Exhibit FSellers’ Disposal Motivations

Early’90s

Mid-Late’90s

Early’00s Today

Risk Management

Active Portfolio Management

Manager Consolidation

Portfolio Rebalancing

Lock in returns

Earnings volatility

M&A

Restructuring

Liquidity needs

Distressed situation

Regulatory pressure

Source: RREEF Private Equity estimates

Exhibit FSellers’ Disposal Motivations

Early’90s

Mid-Late’90s

Early’00s Today

Risk ManagementRisk Management

Active Portfolio Management

Manager ConsolidationManager Consolidation

Portfolio RebalancingPortfolio Rebalancing

Lock in returnsLock in returns

Earnings volatilityEarnings volatility

M&AM&A

RestructuringRestructuring

Liquidity needsLiquidity needs

Distressed situationDistressed situation

Regulatory pressureRegulatory pressure

Source: RREEF Private Equity estimates

Alternative Investments 21

Investment Considerations and Challenges

Investing in secondary interests can be a complex process for all parties involved in a transaction. The intrinsic qualities that make secondaries a sought-after investment, such as their relative transparency and amenable pricing structure, are also the ones that require the most attention from buyers. Ultimately, buyers must possess a certain set of resources and skills in order to navigate through these obstacles. One of the best ways to source deals is to cultivate deep relationships with LPs and GPs. LPs usually have commitments spread across different funds while GPs are often the first aware of a possible commitment for sale. By working through both partnership tracks, investors can quickly uncover potential secondary opportunities.

As soon as a buyer successfully pairs up with a seller, the process of intensive and extensive due diligence begins. It is often not enough to rely solely on a GP’s valuation of an asset portfolio to price a secondary interest; their estimates can be biased, inaccurate or outdated. Independent valuations need to be conducted in order to arrive at a fair market value and to avoid paying a premium for commitments. In most other industries, investors use a standard set of metrics and comparable sales to help value assets, but for private equity, the process is not as straightforward. Venture capital investments may be too immature to value and distressed assets may not have fully turned-around yet. In these instances, a buyer must apply shrewd judgment as to how a portfolio should price. Once this price is determined, negotiations begin between the buyer and seller which can be a drawn-out process if there are multiple offers being considered or if both parties cannot come to terms on the sales price. Alternatively, if the pool of buyers is small and the seller is under pressure to dispose of their commitments, negotiations and due diligence will need to take place quickly. Either way, given the difficulty in executing a transaction and the level of dedication the process requires, secondary investing is best done via a specialist fund that has the appropriate knowledge and resources to undertake the process.

Exhibit GLP Profiles

Pension Fund25%

Fund of Funds15%

Insurance Company

18%

Bank21%

Endow ment/ Foundation

21%Source: Probitas

22 Alternative Investments

References Coller Capital. “Global Private Equity Barometer.” Winter 2008-09.

Dow Jones. “Guide to the Secondary Market.” March 2007.

Dow Jones. “Guide to the Secondary Market.” June 2008.

Dow Jones. “Private Equity Analyst”. December 2008

Dow Jones. “Dow Jones Private Equity Analyst: 2008 Review & 2009 Outlook”. December 2008.

Lee, A. S. W. “Private Equity Secondary Funds and their Competitive Strategies.” July 2003.

McGrady, C and B. Heffern. “Secondary Market Pricing and Outlook, 2007.” Cogent Partners. February 2008.

McGrady, C and B. Heffern. “Mid-Year 2008 Secondary Market Pricing and Outlook.” Cogent Partners. September 2008.

McGrady, C and B. Heffern. “Secondary Pricing Analysis Interim Update, Winter 2008.” Cogent Partners. January 2009.

Preqin, Private Equity Spotlight. “Preqin’s Predictions for 2009.” January 2009/Volume 5-Issue 1.

Preqin, Private Equity Spotlight. “Credit Crunch Special Issue.” October 2008/Volume 4-Issue 10.

Probitas Partners. “Private Equity Market Review and Institutional Investor Survey.” January 2009

Probitas Partners. “Secondary Market Update.” September 2008.

Tegler, D. and K. Caplic. “Secondary Considerations: An Introduction to Secondary Funds.” Testa, Hurwitz & Thibeault, LLP. May 2002.

Watson Wyatt. “Private Equity Explained.” June 2007.

Alternative Investments 23

Important disclosure © 2009. All rights reserved. No further distribution is allowed without prior written consent of the Issuer. RREEF is the brand name of the real estate, infrastructure and private equity division for the asset management activities of Deutsche Bank AG. In the US this relates to the asset management activities of RREEF America L.L.C.; in Germany: RREEF Investment GmbH, RREEF Management GmbH, and RREEF Spezial Invest GmbH; in Australia: Deutsche Asset Management (Australia) Limited (ABN 63 116 232 154) Australian financial services license holder; in Hong Kong: Deutsche Asset Management (Hong Kong) Limited (“DeAMHK”); in Japan: Deutsche Securities Inc. (*); in Singapore, Deutsche Asset Management (Asia) Limited (Company Reg. No. 198701485N) and in the United Kingdom, RREEF Limited, RREEF Global Advisers Limited, and Deutsche Asset Management (UK) Limited; in addition to other regional entities in the Deutsche Bank Group. (*) For DSI, financial advisory (not investment advisory) and distribution services only. Key RREEF research personnel, including Asieh Mansour, Chief Economist and Strategist and Peter Hobbs, Head of Real Estate Research are voting members of the investment committee of certain of the RREEF Alternative Investment Funds. Members of the investment committees vote with respect to underlying investments and/or transactions and certain other matters subjected to a vote of such investment committee. Additionally, research personnel receive, and may in the future receive incentive compensation based on the performance of a certain investment accounts and investment vehicles managed by RREEF and its affiliates. This material is intended for informational purposes only and it is not intended that it be relied on to make any investment decision. It does not constitute investment advice or a recommendation or an offer or solicitation and is not the basis for any contract to purchase or sell any security or other instrument, or for Deutsche Bank AG and its affiliates to enter into or arrange any type of transaction as a consequence of any information contained herein. Neither Deutsche Bank AG nor any of its affiliates, gives any warranty as to the accuracy, reliability or completeness of information which is contained in this document. Except insofar as liability under any statute cannot be excluded, no member of the Deutsche Bank Group, the Issuer or any officer, employee or associate of them accepts any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this document or for any resulting loss or damage whether direct, indirect, consequential or otherwise suffered by the recipient of this document or any other person. The views expressed in this document constitute Deutsche Bank AG or its affiliates’ judgment at the time of issue and are subject to change. This document is only for professional investors. This document was prepared without regard to the specific objectives, financial situation or needs of any particular person who may receive it. No further distribution is allowed without prior written consent of the Issuer. The forecasts provided are based upon our opinion of the market as at this date and are subject to change, dependent on future changes in the market. Any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance. For Investors in the United Kingdom: Issued in the United Kingdom by RREEF Limited or RREEF Global Advisers Limited of One Appold Street, London, EC2A 2UU. Authorised and regulated by the Financial Services Authority. This document is a “non-retail communication” within the meaning of the FSA’s Rules and is directed only at persons satisfying the FSA’s client categorisation criteria for an eligible counterparty or a professional client. This document is not intended for and should not be relied upon by a retail client. When making an investment decision, potential investors should rely solely on the final documentation relating to the investment or service and not the information contained herein. The investments or services mentioned herein may not be appropriate for all investors and before entering into any transaction you should take steps to ensure that you fully understand the transaction and have made an independent assessment of the appropriateness of the transaction in the light of your own objectives and circumstances, including the possible risks and benefits of entering into such transaction. You should also consider seeking advice from your own advisers in making this assessment. If you decide to enter into a transaction with us you do so in reliance on your own judgment. For Investors in Australia: In Australia, Issued by Deutsche Asset Management (Australia) Limited (ABN 63 116 232 154), holder of an Australian Financial Services License. An investment with Deutsche Asset Management is not a deposit with or any other type of liability of Deutsche Bank AG ARBN 064 165 162, Deutsche Asset Management (Australia) Limited or any other member of the Deutsche Bank AG Group. The capital value of and performance of an investment with Deutsche Asset Management is not guaranteed by Deutsche Bank AG, Deutsche Asset Management (Australia) Limited or any other member of the Deutsche Bank Group. Investments are subject to investment risk, including possible delays in repayment and loss of income and principal invested. For Investors in Hong Kong: Interests in the funds may not be offered or sold in Hong Kong or other jurisdictions, by means of an advertisement, invitation or any other document, other than to Professional Investors or in circumstances that do not constitute an offering to the public. This document is therefore for the use of Professional Investors only and as such, is not approved under the Securities and Futures Ordinance (SFO) or the Companies Ordinance and shall not be distributed to non-Professional Investors in Hong Kong or to anyone in any other jurisdiction in which such distribution is not authorised. For the purposes of this statement, a Professional investor is defined under the SFO. For investors in MENA region: This information has been provided to you by Deutsche Bank AG Dubai branch, an Authorised Firm regulated by the Dubai Financial Services Authority. It is solely directed at wholesale clients of Deutsche Bank AG Dubai branch, who Deutsche Bank AG Dubai branch is satisfied meet the regulatory criteria as established by the Dubai Financial Services Authority.

RREEF Research

Main Offices

Frankfurt

Mergenthalerallee 73-75 65760 Eschborn Germany Tel: +49 69 71704 906

Hong Kong

48/F Cheung Kong Centre 2 Queen’s Road Central Hong Kong Tel: +852 2203 8888 London

1 Appold Street Broadgate London EC2A 2UU United Kingdom Tel: +44 20 7545 8000 New York

280 Park Avenue 23W Floor New York NY10017-1270 United States Tel:+1 212 454 3900 San Francisco

101 California Street 26th Floor San Francisco CA 94111 United States Tel:+1 415 781 3300 Tokyo Floor 17 Sanno Park Tower 2-11-1 Nagata-cho Chiyoda-Ku Japan Tel:+81 3 5156 6000

RREEF Research

Publication Address: RREEF 101 California Street 26th Floor San Francisco, CA 94111 USA Website: www.rreef.com Additional information is available upon request

Europe Brenna O’Roarty Director +44 20 7545 6099 Lonneke Löwik Vice President +44 20 7545 6328 Maren Väth Vice President +49 69 717 04 204 Ermina Topintzi Assistant Vice President+30 210 7256 153

Asia Pacific Tan Yen Keng Vice President +852 2203 8062 Koichiro Obu Vice President +81 3 5156 6512 Henry (Wei) Chin Vice President +852 2203 7908

Peter HobbsHead, Global Real Estate Research +44 20 7547 4855

Asieh Mansour Chief Economist and Strategist +1 415 262 2044

North America Alan Billingsley Director +1 415 262 2017 Brooks Wells Director +1 212 454 6437 Hope Nadji Director +1 415 262 2022 Andrew J. Nelson Vice President +1 415 262 7735 Bill Hersler Vice President +1 415 262 2075 Ross Adams Vice President +1 415 262 2097 Jaimala Patel Vice President +1 212 454 1752 Stella Yun Xu Assistant Vice President +1 415 262 7715

I-009776-1.1