seeing the bigger picture for digital print in a multi-media world

TRANSCRIPT

Seeing The Bigger Picture for Digital Print in a Multi-Media World Mark Lawn, Canon Europe

2

Industry trends Digital printing redefining the industry, but taking printers in very different directions

Emerging trends: - Renaissance of small (fewer than 20

staff), lean, entrepreneurial digital-only PSPs

- Consolidation in larger PSPs, who have offset heritage, although now also investing in digital

The result – a polarised industry: - Repeated mergers among larger printers

create industrial- scale factories - Smaller PSPs evolve into cross-media

providers of integrated marketing services

450

400

350

300

250

200

150

100

50

0

Bill

ion

Im

pre

ssio

ns (

A4

)

2011 2016

68.0

103.5

62.5

80.3

24.3

61.9

147.1

106.4

69.0

13.2 20.3

Consumer

Utility

Packaging

Transaction

Publishing

Promotional

General Office

Digital Print Industry Volume Growth by Applications

Source: InfoTrends – Western European Digital Production Printing Application Forecast 2011-2016

4

The Bigger Picture - ‘There’s More to Print than Printing’

87% - professional printing is ‘important’

One third NOT aware of capabilities of digital print – an opportunity!

71% - print is ‘equally’ or ‘more effective’ than other media in the comms mix

Not very

important 11% Not at all important 2% Critical

15%

Somewhat

important 25% Very important 47%

How important is professional-standard

printed communication to your

organisation?

Key findings Print is important

94% 94%

82%

64%

38% 35%

25%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Pri

nted m

ateria

ls

Webs

ites

Socia

l Netw

orking

TV an

d Radi

o

Mobil

e inte

rnet

OR co

des

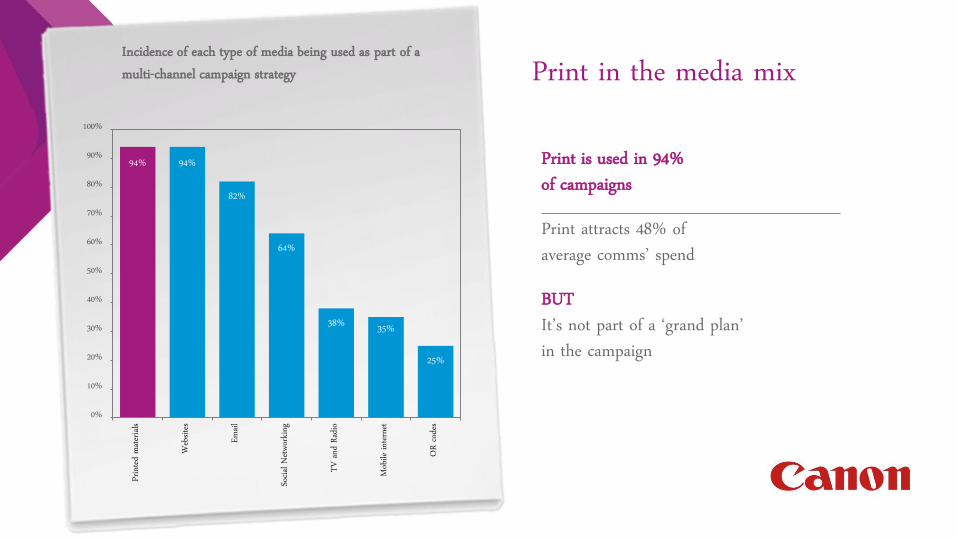

Incidence of each type of media being used as part of a multi-channel campaign strategy

Print is used in 94% of campaigns

Print attracts 48% of average comms’ spend

BUT It’s not part of a ‘grand plan’ in the campaign

Print in the media mix

7

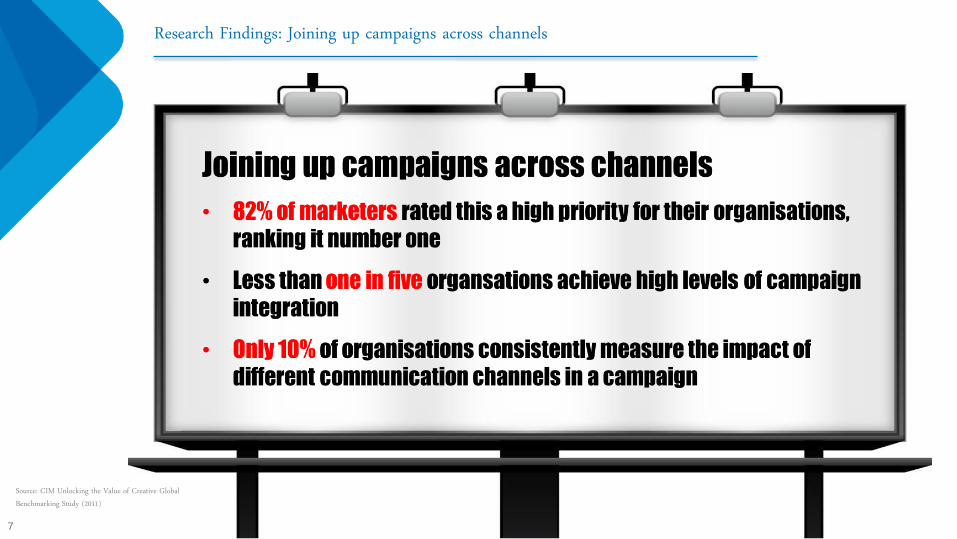

Research Findings: Joining up campaigns across channels

Source: CIM Unlocking the Value of Creative Global Benchmarking Study (2011)

8

Maya Vik: ‘Image Capture to Output’

9

Customer Applications: mapro AG

“Eye-catching and well targeted personalised print can be the key that unlocks the value of online content”

Manfred Senn

6.6% Response (SAP Cross Media Campaign)

Customer Applications: Matthias Bernard

29% Response (EduBook Cross Media Campaign)

“We are no longer at the end of the supply chain. We are involved with client campaigns from conception to implementation and every step in between”

Matthias Bernard

Satisfaction with professional print service providers

1 = Does not meet needs at all

2

3

27%

18%

29%

13% 13%

4

5 = Fully meets needs

88% are happy with PSP meeting communications needs

BUT Only 47% think they are made aware of new developments or alternatives

50% of them don’t ask PSPs for innovation advice – they rely on tradeshows

Key findings Beyond print services

Awareness, consideration and usage of selected digital print applications

Aware and using

Aware and considering

Aware and not considering

Not aware

37% 33% 30%

11% 17% 13%

18% 24%

18%

32% 24% 36%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Short-run publications Targeted (customised) direct mail

Print-on-demand

Customers expect to be informed of new applications and services by PSPs

Want print to be more reactive and flexible in the mix

BUT 32% unaware of short run opportunities

24% unaware of DM applications

36% unaware of PoD

Key findings Need to communicate

“I’m not sure if we

measure ROI or how it

would be done…there

is no formal

measuring.” Managing Director Advertising agency, Germany

Very few buyers have an effective process for measuring ROI

Less than 1 in 10 have formal ROI measurement

Key findings Print ROI

14

Lessons to learn

Talk the customers' language Promote

new applications and print services

Be quicker and

more flexible

Demonstrate the value and ROI of print

Take a closer look at existing customer relationships

Canon Confidential

15

Drivers of anticipated future decline in print

Canon Confidential

Need to embrace web, email and social media

Virtual media faster and cheaper

Changing demographics Desire to be a greener, paper-free organisation

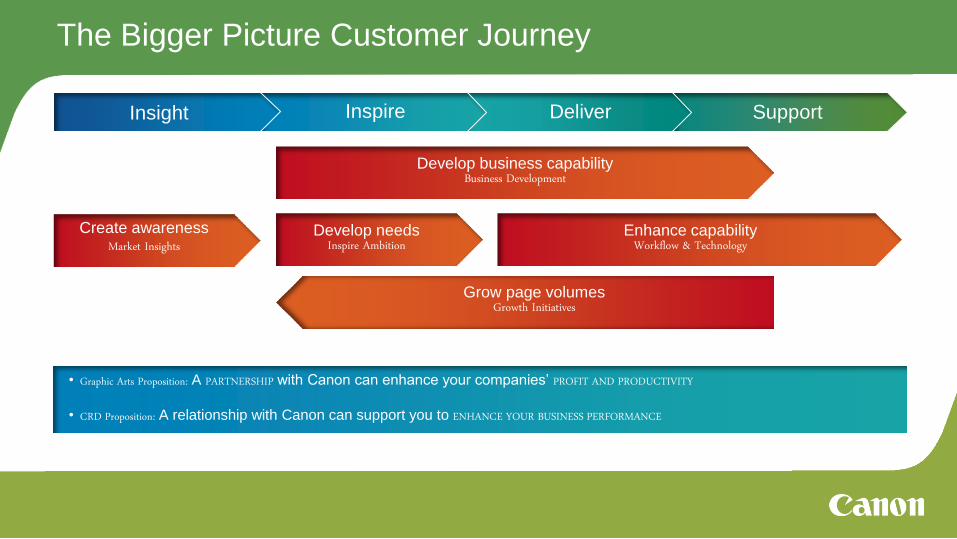

The Bigger Picture Customer Journey

Create awareness Market Insights

Develop needs Inspire Ambition

Develop business capability Business Development

Enhance capability Workflow & Technology

• Graphic Arts Proposition: A PARTNERSHIP with Canon can enhance your companies’ PROFIT AND PRODUCTIVITY

• CRD Proposition: A relationship with Canon can support you to ENHANCE YOUR BUSINESS PERFORMANCE

Insight Inspire Deliver Support

Grow page volumes Growth Initiatives

Canon Confidential

Thank You

18

Appendix - additional slides

20

Innovative Print Applications

Reactor Repro Lenticular Print Sample to be inserted

• Seeing The Bigger Picture for Digital Print in a Multi-Media World’ • • This presentation charts the continued growth and evolution of digital print with

examples of key applications and technologies, demonstrating the critical role that print continues to play in the modern communications landscape. Evidence from the most recent Insight report ‘The Bigger Picture’ is used to present the print buyer’s perspective of new market developments and the opportunities these create for print service providers. Practical examples are provided to convey how Canon is helping digital print service providers to evidence the ROI and value of print they produce and the expertise and skills that they can offer to build more consultative, collaborative and ultimately more effective relationships.

•

Canon Confidential

‘Price is

important but not

critical, other

areas such as

reliability and

quality are more

important’ PR Manager Hospital, Germany

Customers generally loyal to PSPs – they trust suppliers

Approx. 90% buy on value for money

Just 10% cite lowest cost as buying criteria

BUT They may change to new suppliers with new services and innovation

Key findings Winning new customers

23

Increases Expectations on Print Service Providers

24

The Internet – Good or Bad for Printers

(need to generate more revenue from ‘web based’ software and services)

Source: ‘Insight Report – Digital Printing Directions’ by Professor Frank Romano

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Base year 1995 = 100%

2020

2010

2000

1995

Customer feedback:

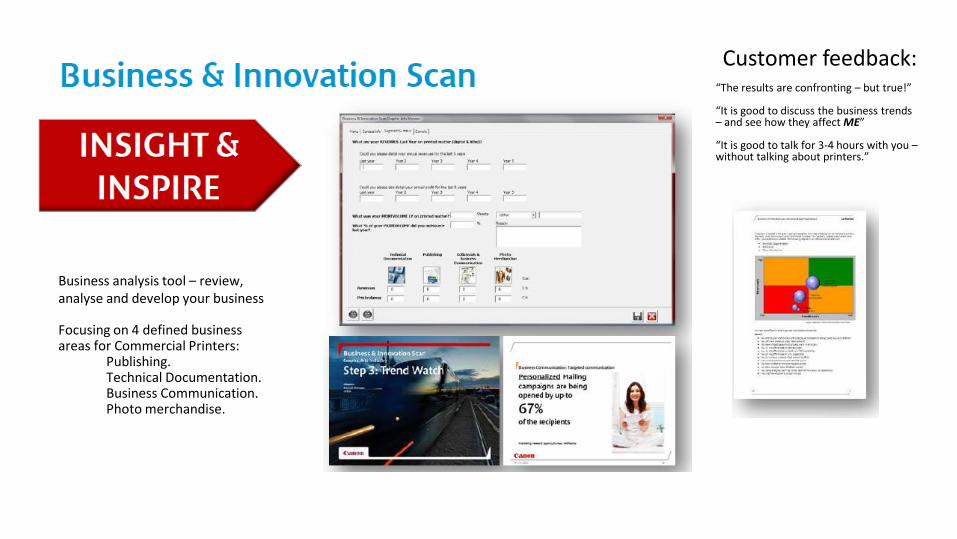

“The results are confronting – but true!” “It is good to discuss the business trends – and see how they affect ME” “It is good to talk for 3-4 hours with you – without talking about printers.”

Business analysis tool – review, analyse and develop your business Focusing on 4 defined business areas for Commercial Printers:

Publishing. Technical Documentation. Business Communication. Photo merchandise.

27

Most Growth / Investment Expected in Web to Print and Cross Media

28

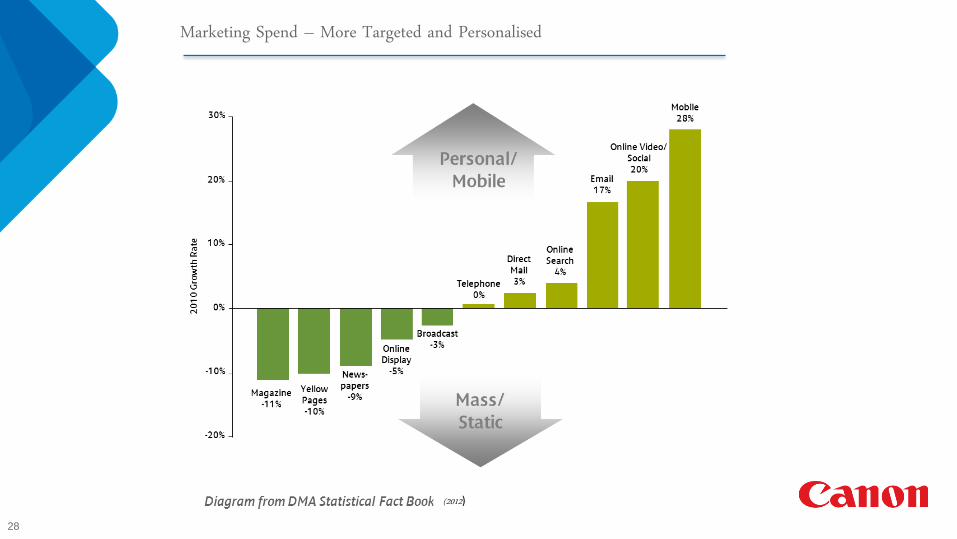

Marketing Spend – More Targeted and Personalised

(2012)