sector update, 11 september 2014 - osk188.co.th · sector update, 11 september 2014 regional...

TRANSCRIPT

See important disclosures at the end of this report Powered by EFATM

Platform 1

Sector Update, 11 September 2014

Regional Telecommunications

Staying Connected – Sept 2014

Macro

2

Risks

2

Growth

1

Value

2

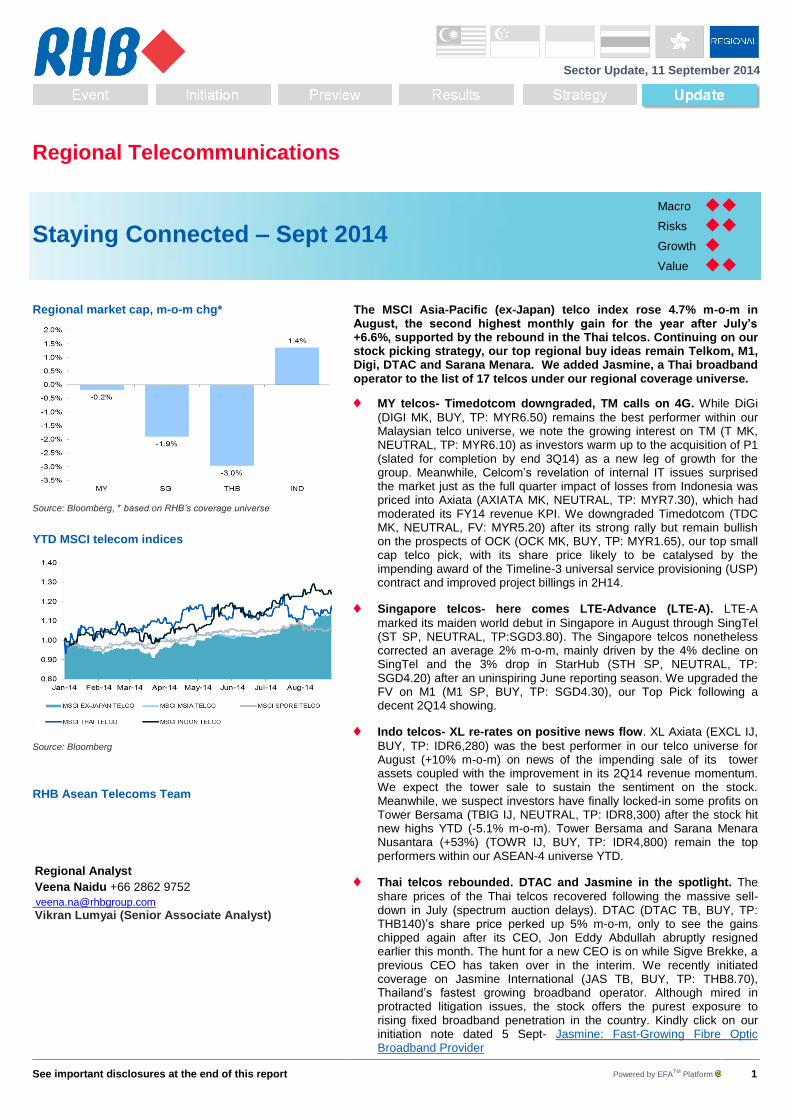

Regional market cap, m-o-m chg*

Source: Bloomberg, * based on RHB’s coverage universe

YTD MSCI telecom indices

Source: Bloomberg

RHB Asean Telecoms Team

Regional Analyst

Veena Naidu +66 2862 9752

[email protected] [email protected]

Vikran Lumyai (Senior Associate Analyst)

The MSCI Asia-Pacific (ex-Japan) telco index rose 4.7% m-o-m in August, the second highest monthly gain for the year after July’s +6.6%, supported by the rebound in the Thai telcos. Continuing on our stock picking strategy, our top regional buy ideas remain Telkom, M1, Digi, DTAC and Sarana Menara. We added Jasmine, a Thai broadband operator to the list of 17 telcos under our regional coverage universe.

MY telcos- Timedotcom downgraded, TM calls on 4G. While DiGi

(DIGI MK, BUY, TP: MYR6.50) remains the best performer within our Malaysian telco universe, we note the growing interest on TM (T MK, NEUTRAL, TP: MYR6.10) as investors warm up to the acquisition of P1 (slated for completion by end 3Q14) as a new leg of growth for the group. Meanwhile, Celcom’s revelation of internal IT issues surprised the market just as the full quarter impact of losses from Indonesia was priced into Axiata (AXIATA MK, NEUTRAL, TP: MYR7.30), which had moderated its FY14 revenue KPI. We downgraded Timedotcom (TDC MK, NEUTRAL, FV: MYR5.20) after its strong rally but remain bullish on the prospects of OCK (OCK MK, BUY, TP: MYR1.65), our top small cap telco pick, with its share price likely to be catalysed by the impending award of the Timeline-3 universal service provisioning (USP) contract and improved project billings in 2H14.

Singapore telcos- here comes LTE-Advance (LTE-A). LTE-A

marked its maiden world debut in Singapore in August through SingTel (ST SP, NEUTRAL, TP:SGD3.80). The Singapore telcos nonetheless corrected an average 2% m-o-m, mainly driven by the 4% decline on SingTel and the 3% drop in StarHub (STH SP, NEUTRAL, TP: SGD4.20) after an uninspiring June reporting season. We upgraded the FV on M1 (M1 SP, BUY, TP: SGD4.30), our Top Pick following a decent 2Q14 showing.

Indo telcos- XL re-rates on positive news flow. XL Axiata (EXCL IJ,

BUY, TP: IDR6,280) was the best performer in our telco universe for August (+10% m-o-m) on news of the impending sale of its tower assets coupled with the improvement in its 2Q14 revenue momentum. We expect the tower sale to sustain the sentiment on the stock. Meanwhile, we suspect investors have finally locked-in some profits on Tower Bersama (TBIG IJ, NEUTRAL, TP: IDR8,300) after the stock hit new highs YTD (-5.1% m-o-m). Tower Bersama and Sarana Menara Nusantara (+53%) (TOWR IJ, BUY, TP: IDR4,800) remain the top performers within our ASEAN-4 universe YTD.

Thai telcos rebounded. DTAC and Jasmine in the spotlight. The

share prices of the Thai telcos recovered following the massive sell-down in July (spectrum auction delays). DTAC (DTAC TB, BUY, TP: THB140)’s share price perked up 5% m-o-m, only to see the gains chipped again after its CEO, Jon Eddy Abdullah abruptly resigned earlier this month. The hunt for a new CEO is on while Sigve Brekke, a previous CEO has taken over in the interim. We recently initiated coverage on Jasmine International (JAS TB, BUY, TP: THB8.70), Thailand’s fastest growing broadband operator. Although mired in protracted litigation issues, the stock offers the purest exposure to rising fixed broadband penetration in the country. Kindly click on our initiation note dated 5 Sept- Jasmine: Fast-Growing Fibre Optic Broadband Provider

Telecommunications 11 September 2014

See important disclosures at the end of this report 2

Malaysia (NEUTRAL) Telekom Malaysia enters R&D tie-up with Huawei

Fresh from signing an agreement to build a joint 5G research lab with LG U+, Huawei (002502 CH, NR) has entered a joint networking Research and Development (R&D) collaboration with Telekom Malaysia. Huawei and Telekom Malaysia said they have signed a memorandum of understanding covering the co-development of next-generation fixed and wireless access technologies. The companies plan to jointly research the most suitable copper and 4G networking technologies for the Malaysian broadband market. The collaboration covers the sharing of research facilities and the establishment of a joint lab within the TM Innovation Center. The joint R&D is aimed at allowing Telekom Malaysia to better manage its high speed broadband (HSBB) network, and to use it to launch additional services including internet protocol

television (IPTV) and high definition television (HDTV). The R&D project will cover

wireless broadband technologies and fixed-mobile convergence. (Telecom Asia, 13 Aug) Telekom Malaysia closer to P1 acquisition

Shareholders in Green Packet (GRPB MK, NR) have approved the planned joint investment in wireless broadband unit P1 by the company, Telekom Malaysia (TM) and SK Telecom (017670 KS, NR). Under the agreement, Telekom Malaysia will invest up to an initial MYR560m in Green Packet in exchange for a controlling 57% stake in P1. The three companies are also planning to invest a further MYR1.65bn towards P1's LTE rollout over the next few years. P1 plans to transition into a Time Division (TD)-LTE operator. Green Packet’s group managing director CC Puan said P1's direct entry into the mobile market will instantly grow the company's addressable market size fourfold to MYR34.5bn. (Telecom Asia, 11 Aug)

Comment: TM’s move into wireless broadband while negative for the mobile operators, is still a medium-term risk to the latter and not an immediate one. Thus far, TM has remained relatively tight-lipped on its wireless broadband ambitions. At this juncture, its wireless broadband service remains focused only on rural and underserved areas, but may reach 280 sites by year-end. While the mobile operators remain cautious of how aggressive TM may become, they are adopting a wait-and-see approach for now. Axiata denies offer from China Mobile

Axiata Group has denied reports that China Mobile (941 HK, NR) is seeking to purchase a stake in the operator group. Axiata Group CEO Datuk Seri Jamaludin Ibrahim told Malaysia's Daily Express that nobody at China Mobile has approached the company with an offer. Earlier this month, sources told Bloomberg that China Mobile is interested in buying up to 20% of Axiata Group, but that Axiata rebuffed the offer because it considered the bid to be too low. Based on market prices at the time, a 20% stake in Axiata would be worth around USD3.7bn, which would have been China Mobile's largest investment outside its home market. But besides not being approached, Jamaludin said that the company does not need any kind of investment or cash at the group level in any event. (Telecom Asia, 29 Aug) Comment: The statement by Axiata Group CEO would certainly put to rest earlier news that China Mobile wanted to buy a 20% stake in the group. In any case, we reiterate our view that Axiata has a healthy balance sheet and thus does not require any capital injection from the entry of a new shareholder. While China Mobile does offer Axiata Group some form of synergy by expanding the latter’s Asian mobile footprint, we think potential short-term benefits may not be significant since we understand that International Direct Dialing (IDD) traffic between China and Malaysia is not very material for Celcom Axiata.

.

YTD MSCI M’sia telecom index performance

Source: Bloomberg

Malaysia stock calls

Ticker TP (MYR) Rating

MAXIS MK 6.00 S

AXIATA MK 7.30 N

DIGI MK 6.50 B

T MK 6.10 N

TDC MK 5.20 B

OCK MK 1.65 B

Sector view

We remain NEUTRAL on the Malaysian telco sector due to: i) tepid industry revenue growth, ii) pronounced cannibalisation of SMS revenue by over-the-top (OTT) usage, and iii) valuations that do not look attractive. We are bullish on DiGi, which we think is monetising data most effectively. We also like Time dotCom (TdC) as a direct play to strong demand for international bandwidth.

Regional Analyst

Telecommunications 11 September 2014

See important disclosures at the end of this report 3

Singapore (NEUTRAL) SingTel revamps service layer for its enterprise services

SingTel has picked NetCracker and NEC APAC to transform the backend systems for its enterprise customers. The solution will automate and enhance SingTel’s end-to-end service fulfilment processes to enable its Group Enterprise to bring new products and services bundles to the market more swiftly.“NetCracker’s solutions will help (us) augment our operational efficiency, improve productivity and increase network configuration accuracy across our services,” said Lee Han Kheng, VP of global products at SingTel Group Enterprise. This new service fulfilment solution will establish a single, centralised network inventory database while bringing together SingTel’s service fulfilment, service assurance and network solution components into a seamless, automated process for resource checking, reservation and service activation. (Telecoms Asia, 28 Aug)

StarHub unveils cloud marketplace for SMEs

StarHub has unveiled a new cloud marketplace for the country’s SMEs. StarHub’s SmartBusiness brings together a range of cloud applications, and provides an easy experience for small and medium sized businesses (SMBs) to buy software and services. SmartBusiness also provides a gateway for partners such as Microsoft and McAfee as well as independent software vendors (ISVs) such as Deskera and Webnic to make available their applications rapidly to the local SMB base. “As applications are hosted in the cloud on SmartBusiness, SMB employees are empowered to access these applications and complete their work anywhere, anytime; this way, they do not have to work in the confines of their office,” noted StarHub. (Singapore Business Review, 21 Aug) Comment: We view this development positively to further strengthen its enterprise (fixed network services) business, which remains the fastest growing segment for the group albeit contribution is still modest at less than 20%. We keep our NEUTRAL rating on StarHub based on a DCF TP of SGD4.20. SingTel launches the world’s first LTE Advance (LTE-A) service for smartphones

SingTel has launched the first 300Mbps LTE-Advanced service for smartphones. The company started selling the Samsung Galaxy S5 4G+ - the first handset compatible with LTE-Advanced networks on 23 Aug. A second compatible smartphone, also from Samsung (005930 KS, NR), will be launched in September. SingTel soft-launched its 300Mbps LTE-A network in May, and introduced the first services over the network last month. But at the time, the only compatible device in its line-up was a Huawei mobile broadband dongle. As of today, the network covers more than 55% of Singapore, including the CBD, City Hall, Orchard and Shenton Way, SingTel said. The company aims to achieve nationwide outdoor coverage in the first quarter of 2015. SingTel will bundle the S5 for prices ranging from SGD688 (USD550) for its entry-level SGD27.90 per month Combo plan, to free for the most expensive SGD239.90 plan. (Telecoms Asia, 20 Aug)

YTD MSCI S’pore telecom index performance

Source: Bloomberg

Singapore stock calls

Ticker TP (SGD) Rating

ST SP 3.80 N

STH SP 4.20 N

M1 SP 4.30 B

Sector view

We are NEUTRAL on the sector due to: i) the competitive headwinds in the fixed broadband and pay-TV segments, and ii) unattractive sector valuations vs regional peers’. Our Top Pick, M1, is uniquely-positioned to capture a greater share of broadband/data revenue and is monetising data more effectively than its rivals.

Regional Analyst

Telecommunications 11 September 2014

See important disclosures at the end of this report 4

Indonesia (OVERWEIGHT)

XL completes sale of treasury shares

XL Axiata has successfully completed the entire sale of 231.1m treasury shares, representing 2.7% stake of the company as at 29 Aug. The shares were sold in the open market to a combination of both local and foreign institutional investors at an average price of IDR5,708 per share, above the minimum required price of IDR5,280. As a result of the sale of treasury shares, XL has improved its financial position. The sale of treasury shares which was announced on 25 June was related to the mandatory share buyback from dissenting shareholders arising from the merger between XL and Axis in Feb 2014 (Company Announcement). Comment : The sale netted XL some USD112m (IDR1.32tn), which would lower its net gearing position slightly to 2.03x from 2.1x at end 2Q14 and net debt/EBITDA, to 3.1x from 3.3x in addition to improving the liquidity of the stock. We maintain our BUY rating based on DCF FV of IDR6,280 (WACC: 8.5%, TG: 1.5%) with re-rating catalysts coming from: i) the impending sale of its tower assets with proceeds utilised to pare debt, and ii) further cost synergies from the merger with Axis Indonesia (Axis) in the months ahead, which should lower the anticipated earnings dilution from the merger in FY15. XL reports a 2Q14 loss following the merger with Axis

XL Axiata (XL) posted a net loss of IDR482.5bn in 1HFY14 vs a profit of IDR670.4bn in the previous corresponding period. The weaker performance was attributed to higher interest expense from additional debt undertaken to fund the acquisition of Axis Indonesia (Axis). XL’s overall revenue climbed 12% to IDR11.6tn in 1HFY14, driven mainly by data services while voice and text revenues rose 5%. The company’s non-voice services contributed 57% of its revenue, an increase from the 53% in 2Q13. (Indonesia Finance Today, 22 Aug) Comment : Kindly refer to our results review note dated 22 Aug - XL Axiata - Strong

Recovery Momentum

Telkom Sigma plans to float its ICT business in 2016-2017

Telekomunikasi Indonesia (TLKM IJ, BUY, TP: IDR3,200) plans to divest or sell some shares in Sigma Cipta Caraka (Telkom Sigma) by way of an IPO. According to Indra Utoyo, Telkom’s Director of Innovation & Strategic Portfolio, the corporate action is slated for 2016 or 2017. Telkom Sigma’s core businesses include system integration, data center and managed services. As of June 30, the company’s total assets amounted to IDR2tn (USD170.3 m), up from IDR1.89tn on 31 Dec 2013. Telkom Sigma is targeting a 48% share of Indonesia’s data center business or an equivalent of 73,000 sq m of floor space this year. For 2015, the company is eyeing a 60% share of the market or some 100,000 sq m of data centre. Telkom Sigma posted a revenue of IDR1tn in 1HFY14. Of the amount, the system integration business contributed 50% followed by data centre (40%) and managed services (10%). Telkom Sigma expects its revenue to reach IDR2tn in FY14, a 49% jump y-o-y. (Indonesia Finance Today, 22 Aug)

YTD MSCI Indon telecom index performance

Source: Bloomberg

Indonesia stock calls

Ticker TP (IDR) Rating

TLKM IJ 3,200 B

EXCL IJ 6,280 B

ISAT IJ 4,800 B

TBIG IJ 8,600 N

TOWR IJ 4,800 B

Sector view

We remain OVERWEIGHT on the sector due to: i) easing competitive risks, ii) the broad recovery in core sector earnings in 2015, and iii) our projection of peaking industry capex. Telkom remains our Top Pick for the mobile sector while Sarana Menara Nusantara is our preferred pick in the tower infrastructure sector.

Regional Analyst

Telecommunications 11 September 2014

See important disclosures at the end of this report 5

Thailand (NEUTRAL) TOT to embark on restructuring plan

The State Enterprise Policy Commission has instructed the Telephone Organisation of Thailand (TOT) to eliminate its non-core or unprofitable business units and focus on its core businesses: i) telecommunications infrastructure, ii) telecom towers, iii) wireless/ fixed-base broadband internet service, iv) cloud computing, v) international gateways, and vi) submarine cables in order to revive its financial status. TOT plans to submit the first part of its new business plan to the commission, with the second part due in two months. The first part comprises all the business details of TOT, a cost reduction strategy, operating efficiency plans as well as existing legal disputes with other companies. The second part is an evaluation of its assets and liabilities. (Bangkok Post, 29 Aug). Comment: The plans to restructure the business models and regularise the financial positions of TOT and Communications Authority of Thailand (CAT) are required as part of the review of the Frequency Allocation Act (FAA). We note that the National Council for Peace and Order (NCPO) had recently approved TOT’s submarine cable project worth THB5.98bn, which consists of three routes: Asia-Africa-Europe (AAE-1), South-East Asia-Japan (SJC Thailand) and South-East Asia-Middle East-Western Europe. On 20 Aug, the new TOT board approved AAE-1, which is worth THB1.4bn. Cellcos may be able to use expired concessions

The National Broadcasting and Telecommunications Commission (NBTC) will propose allowing cellular operators to use expired concessions so that the companies can seek new customers until the 1.8GHz spectra are auctioned. However, they would be required to pay annual revenue to the state, based on the 30% concession fee rate that they used to pay to Communications Authority of Thailand (CAT) Telecom. The 1,800MHz cellular concessions of True Move, the telco owned by True Corp (TRUE TB, NR) and Digital Phone Co (DPC), a wholly-owned subsidiary of Advanced Info Services (ADVANC TB, NEUTRAL, TP: THB235.00) expired in September while Advanced Info Services’ 900MHz concession will expire in Sept 2015. (The Nation, 1 Sept). Comment: The move is an interim measure to prevent potential service disruptions given that there are more than 4m customers remaining on the 1,800MHz networks of AIS (DPC) and True. The majority of these 2G subscribers are from the upcountry areas and are less compelled to switch to 3G. The extension would be a small reprieve for AIS as it owns less spectrum than its peers, which could affect subscriber experience on its network. Total Access Communications (DTAC) CEO resigns

Jon Eddy Abdullah, the chief executive officer of Total Access Communication (DTAC TB, BUY, TP: THB140.00), has resigned from his position after three and a half years at the helm. He said his resignation was due to a difference of opinion on how to take the company forward. Vice-chairman Sigve Brekke will serve as interim chief executive overseeing the overall management of the company until the board finds a permanent leader. He will continue serving as executive vice-president and head of Telenor Group's Asian operations. (Bangkok Post, 3 Sept). Comment: We are not overly concerned about the abrupt change in leadership. We note that Telenor also practices internal job rotations across its operating companies for key positions and such transitions are typically seamless. A check with DTAC’s investor relations unit also revealed that the company remains in good and capable hands, and the process to identify a new CEO is expected to be completed by year-end. Mr. Brekke served as DTAC’s CEO from 2005- 2008 and understands the social and political intricacies of running the business on the back of the shift in regulatory dynamics of the industry.

YTD MSCI Thai telecom index performance

Source: Bloomberg

Thailand stock calls

Ticker TP (THB) Rating

ADVANC TB 235 N

DTAC TB 140 B

JAS TB 8.70 B

Sector view

We downgrade the Thai telco sector to NEUTRAL from Overweight following the downgrade on Advanced Info Services to NEUTRAL from Buy post the 2Q14 results. Our Top Pick remains Total Access Communications (DTAC) as it has less spectrum risks and scope for capital management.

Regional Analyst

Veena Naidu +66 2862 9752

Vikran Lumyai (Senior Associate Analyst)

Telecommunications 11 September 2014

See important disclosures at the end of this report 6

Global

Video now makes up half of mobile traffic

Video now accounts for more than half of mobile network traffic worldwide, and LTE customers are more voracious consumers of video content, according to Citrix's latest mobile analytics report. Traffic associated with video made up 52% of worldwide mobile network traffic volumes in the second quarter, up from 45% a year earlier, the report states. LTE subscribers are 1.5 times more likely to watch video than 3G customers, and view videos for a longer period of time. Citrix senior product marketing manager Anna Yong said this proves that LTE drives increased demand for mobile video. “This sets the scene for greater urgency for mobile operators and publishers such as Twitter to reconcile an emerging conflict between user perception and reality, opening the door to more numerous and sophisticated sponsored data plans,” Yong said. (Telecom Asia, 4 Sept)

India targets 100% smartphone ownership by 2019

India's newest Government has announced initiatives aimed at ensuring that the entire population has a smartphone by 2019. The INR1.13trn (USD18.8bn) Digital India initiatives also aim to transform the nation into a connected economy, India's Economic Times said. India's smartphone penetration currently stands at around 74%, but the Government aims to increase this to 100% by 2019. The Government will also redouble efforts for the National Optic Fibre Network (NOFN) project, which has stalled for the past three years. The prime minister himself will monitor progress with the project to ensure it starts meeting its deadlines. (Telecom Asia, 25 Aug)

VoLTE superior to 3G, OTT voice

Voice over LTE technology (VoLTE) can provide a superior user experience to both 3G circuit switched (CS) voice and voice over Internet Protocol (VoIP) services such as Skype, finds a study by Signals Research Group (SRG). Real world tests in a commercially active VoLTE market found that the service can deliver superior call quality to both 3G CS voice and Skype's high definition (HD) voice service, said Alcatel-Lucent, which supplied the gear for the networks tested. VoLTE call setup time was also found to be nearly twice as fast as 3G circuit-switched fallback times, the study found. The standard also used fewer resources than Skype voice, contributing to a longer estimated battery life for users' devices and a less strained mobile network for the operator. VoLTE calls were also found to successfully hand over to 3G CS voice while leaving LTE coverage areas. (Telecom Asia, 15 Aug)

Mobile is driving growth in online shopping

More people than ever before are shopping online on their mobile devices, a new report from BuzzCity, commissioned by the Mobile Marketing Association (MMA), reveals. Nearly half of mobile user respondents (48%) made purchases online regularly and nearly one in five browse products online before buying in stores. Taken together, more than 70% of mobile consumers shop online. Mobile as a shopping channel is now on a par with PCs and a key to driving the change in consumer shopping behavior, the report noted. In some countries, mobile has even become the most dominant shopping channel. This is highly apparent in the Asia-Pacific region where mobile leads the way for shopping, as more of the population turn to mobile as their primary device. (Telecom Asia, 6 Aug)

Xiaomi becomes fifth-ranked smartphone vendor

China's Xiaomi rose to become the fifth largest smartphone vendor by market share during the second quarter, Strategy Analytics estimates. Xiaomi's share of the global market rose to 5% for the first time, the firm said. The strong growth is coming from China, where Xiaomi ships millions of smartphones every quarter, but the vendor has also been working hard to expand its presence internationally. Samsung's share of the global market, by contrast, slipped to 25% from 33% a year earlier. Apple's (AAPL US, NR) market share was 12%, while Huawei was in third place with a record 7% share. Strategy Analytics estimates that global smartphone shipments grew 27% year-on-year to 233 million units, thanks in part to healthy demand from Asia and Africa. (Telecom Asia, 4 Aug)

Telecommunications 11 September 2014

See important disclosures at the end of this report 7

Figure 1: Regional sector comparables Company Bloomberg Currency Ratings FV Price Mkt Cap PEG

Ticker (USDm) FY14^ FY15^ FY14^ FY15^ FY14^ FY15^ (x) FY14^ FY15^ FY14^ FY15^

Malaysia

Axiata AXIATA MK MYR Neutral 7.30 6.93 18,785.9 22.0 20.1 9.1 8.4 2.8 2.7 2.4 3.6 4.2 13.2 13.8

DiGi DIGI MK MYR Buy 6.50 5.73 14,087.2 22.4 21.2 15.2 14.4 nm nm 4.0 4.5 4.7 nm nm

Maxis MAXIS MK MYR Sell 6.00 6.55 15,546.3 23.5 22.3 13.7 12.7 10.0 10.4 4.5 6.1 4.9 38.4 45.8

TM T MK MYR Neutral 6.10 6.36 7,374.9 26.4 24.8 8.1 7.9 3.5 3.3 4.2 3.4 3.6 12.6 13.7

Time dotCom TDC MK MYR Neutral 5.20 4.88 884.3 23.1 21.4 10.6 13.1 0.9 0.8 2.9 0.8 1.2 4.9 5.0

OCK OCK MK MYR Buy 1.65 1.44 155.7 19.7 16.2 13.0 11.1 4.0 4.4 0.9 0.0 0.0 22.6 25.9

Singapore

SingTel ST SP SGD Neutral 3.82 3.89 49,660.1 17.2 16.1 13.4 13.4 2.6 2.5 2.5 4.3 4.3 15.1 15.8

StarHub STH SP SGD Neutral 4.20 4.15 5,729.6 19.0 16.6 10.3 9.9 nm nm 1.4 4.8 4.8 nm nm

M1 M1 SP SGD Buy 4.30 3.80 2,831.1 19.7 17.5 12.0 11.1 9.1 8.9 1.6 5.5 5.5 45.3 51.6

Indonesia

Telkom TLKM IJ IDR Buy 3,200 2,665 22,950.2 16.8 14.5 7.2 6.4 4.1 3.7 1.0 3.8 4.2 25.5 27.1

XL Axiata EXCL IJ IDR Buy 6,280 5,950 4,338.3 96.0 33.1 9.6 9.7 3.3 3.0 0.5 0.3 0.8 3.4 9.6

Indosat ISAT IJ IDR Buy 4,590 3,830 1,778.0 87.8 14.1 4.3 4.5 1.1 1.0 0.2 0.6 3.7 1.4 7.5

Tower Bersama TBIG IJ IDR Neutral 8,600 7,875 3,227.1 26.9 21.0 23.8 19.2 7.5 5.9 1.0 0.9 1.1 31.0 31.2

Sarana Menara TOWR IJ IDR Buy 4,800 4,195 3,656.7 47.4 38.5 18.4 15.6 9.7 7.7 2.1 0.0 0.0 26.3 23.3

Thailand

ADVANC ADVANC TB THB Neutral 235.00 209.00 19,450.2 17.4 15.3 10.1 10.2 13.3 12.7 1.3 5.8 6.5 77.5 85.1

DTAC DTAC TB THB Buy 140.00 109.00 8,078.7 20.6 17.4 8.9 8.0 8.5 8.0 1.1 4.6 5.5 38.4 47.2

Jasmine JAS TB THB Buy 8.70 6.70 1,429.8 13.1 11.0 9.1 7.9 3.6 3.1 0.7 3.7 4.2 27.8 28.8

Simple Avg. - Malaysia Telcos 23.5 22.0 11.3 11.3 4.3 4.3 3.6 3.7 3.7 17.3 19.6

Simple Avg. - Singapore Telcos 18.6 16.7 11.9 11.5 5.8 5.7 1.8 4.9 4.9 30.2 33.7

Simple Avg. - Indonesia Telcos 55.0 24.2 12.7 11.1 5.1 4.3 0.9 1.1 2.0 17.5 19.7

Simple Avg. - Thailand Telcos 19.0 16.3 9.5 9.1 10.9 10.3 1.2 5.2 6.0 57.9 66.2

Simple Avg. - Regional Telcos 31.6 20.6 11.7 11.0 5.7 5.4 2.0 3.1 3.4 25.4 28.8

^SingTel's FY14/15 refers to FY15/16

Note: Share prices as at 29 Aug 2014

P/E (x) EV/EBITDA (x) P/BV (x) DY (%) ROE (%)

Source: RHB

Telecommunications 11 September 2014

See important disclosures at the end of this report 8

Figure 2: Share price performance for the month (%) Figure 3: YTD share price performance (%)

-14.7

-6.5

-5.1

-4.5

-4.4

-3.1

-2.6

-0.4

0.5

0.6

0.7

1.3

1.9

5.3

5.7

6.3

10.2

-20 -15 -10 -5 0 5 10 15

Jasmine

OCK

Tower Bersama

Indosat

SingTel

Maxis

StarHub

Axiata

AIS

Telkom Indonesia

Digi

M1

Telekom Malaysia

DTAC

Sarana Menara Nusantara

TDC

XL Axiata

-9.9

-7.7

-4.5

-3.3

0.4

4.8

6.3

12.4

14.4

14.6

15.5

16.2

24.0

35.8

37.5

52.5

80.0

-20 0 20 40 60 80 100

Maxis

Indosat

Jasmine

StarHub

Axiata

AIS

SingTel

DTAC

XL Axiata

Telekom Malaysia

Digi

M1

Telkom Indonesia

Tower Bersama

TDC

Sarana Menara Nusantara

OCK

Source: Bloomberg Source: Bloomberg

Figure 4: FY15 P/E (x) Figure 5: FY15 EV/EBITDA (x)

0 10 20 30 40 50

Jasmine

Indosat

Telkom

Advanc

SingTel

OCK

StarHub

DTAC

M1

Axiata

Tower Bersama

DiGi

TDC

Maxis

TM

XL Axiata

PT Sarana

x

6.4

7.9

7.9

8.0

8.4

9.7

9.9

10.2

11.1

11.1

12.7

13.1

13.4

14.4

15.6

19.2

0 5 10 15 20 25

Telkom

Jasmine

TM

DTAC

Axiata

XL Axiata

StarHub

Advanc

M1

OCK

Maxis

TDC

SingTel

DiGi

PT Sarana

Tower Bersama

x

Source: Bloomberg, RHB Source: Bloomberg, RHB

Figure 6: FY15 dividend yield (%) Figure 7: FY15 ROE (%)

0.8

1.1

1.2

3.6

3.7

4.2

4.2

4.2

4.3

4.7

4.8

4.9

5.5

5.5

6.5

0 2 4 6 8

XL Axiata

Tower Bersama

TDC

TM

Indosat

Telkom

Axiata

Jasmine

SingTel

DiGi

StarHub

Maxis

DTAC

M1

Advanc

%

5.0

7.5

9.6

13.7

13.8

15.8

23.3

25.9

27.1

28.8

31.2

45.8

47.2

51.6

85.1

0 20 40 60 80 100

TDC

Indosat

XL Axiata

TM

Axiata

SingTel

PT Sarana

OCK

Telkom

Jasmine

Tower Bersama

Maxis

DTAC

M1

Advanc

%

Source: Bloomberg, RHB

Source: Bloomberg, RHB

Telecommunications 11 September 2014

See important disclosures at the end of this report 9

Kindly click on the links below for our recent reports on the sector

Regional Telecoms - 1H2014 Results Takeaways (8 Sep) Axiata Group - IT Issues Cap Celcom’s Growth (28 Aug) Axiata Group - Short-Term Drag By XL (27 Aug) Digi.com : Keeping Up The Good Work (26 Aug) Time dotCom - A More Cautious Tone (25 Aug)

XL Axiata - Strong Recovery Momentum (22 Aug) Tower Bersama Infrastructure - Steady Growth(21 Aug)

Sarana Menara Nusantara - Regains Growth Momentum (20 Aug) SingTel - Bumpy Enterprise Road (15 Aug) SingTel - 1QFY15 Results In Line (14 Aug) Axiata Group - China Mobile Reportedly Eyeing 20% Stake (7 Aug) StarHub - Missing The Grant (7 Aug) Regional Telecommunications - Staying Connected – Aug 2014 (6 Aug) ID_Telkom 1HFY14 Results Review_20140725_RHB (25 July) Telecommunications - Time To Redial (23 July) Telecommunications Infrastructure - M&A Opportunities Abound (23 July) Maxis - Initial Signs Of Bottoming Out (23 July) M1 - On a Roll (22 July) DTAC - A Boost From Mobile Data (21 July) Digi.com - Leading The Way (18 July) Regional Telecommunications - Staying Connected – July 2014 (9 July) OCK Group - Towering Growth (4 July 2014) Advanced Info Services - Asean Corporate Day (ACD) Takeaways (4 July 2014) Regional Telecommunications - 1Q2014 Results Takeaways (June 12) Telecommunications - Quiet 1QCY14 For Cellcos (June 12) Regional Telecommunications - Staying Connected – June 2014 (5 Jun)

10

RHB Guide to Investment Ratings Buy: Share price may exceed 10% over the next 12 months Trading Buy: Share price may exceed 15% over the next 3 months, however longer-term outlook remains uncertain Neutral: Share price may fall within the range of +/- 10% over the next 12 months Take Profit: Target price has been attained. Look to accumulate at lower levels Sell: Share price may fall by more than 10% over the next 12 months Not Rated: Stock is not within regular research coverage Disclosure & Disclaimer All research is based on material compiled from data considered to be reliable at the time of writing, but RHB does not make any representation or warranty, express or implied, as to its accuracy, completeness or correctness. No part of this report is to be construed as an offer or solicitation of an offer to transact any securities or financial instruments whether referred to herein or otherwise. This report is general in nature and has been prepared for information purposes only. It is intended for circulation to the clients of RHB and its related companies. Any recommendation contained in this report does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. This report is for the information of addressees only and is not to be taken in substitution for the exercise of judgment by addressees, who should obtain separate legal or financial advice to independently evaluate the particular investments and strategies. This report may further consist of, whether in whole or in part, summaries, research, compilations, extracts or analysis that has been prepared by RHB’s strategic, joint venture and/or business partners. No representation or warranty (express or implied) is given as to the accuracy or completeness of such information and accordingly investors should make their own informed decisions before relying on the same. RHB, its affiliates and related companies, their respective directors, associates, connected parties and/or employees may own or have positions in securities of the company(ies) covered in this research report or any securities related thereto, and may from time to time add to, or dispose off, or may be materially interested in any such securities. Further, RHB, its affiliates and related companies do and seek to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities of such company(ies), may sell them or buy them from customers on a principal basis and may also perform or seek to perform significant investment banking, advisory or underwriting services for or relating to such company(ies), as well as solicit such investment, advisory or other services from any entity mentioned in this research report. RHB and its employees and/or agents do not accept any liability, be it directly, indirectly or consequential losses, loss of profits or damages that may arise from any reliance based on this report or further communication given in relation to this report, including where such losses, loss of profits or damages are alleged to have arisen due to the contents of such report or communication being perceived as defamatory in nature. The term “RHB” shall denote where applicable, the relevant entity distributing the report in the particular jurisdiction ment ioned specifically herein below and shall refer to RHB Research Institute Sdn Bhd, its holding company, affiliates, subsidiaries and related companies. All Rights Reserved. This report is for the use of intended recipients only and may not be reproduced, distributed or published for any purpose without prior consent of RHB and RHB accepts no liability whatsoever for the actions of third parties in this respect. Malaysia This report is published and distributed in Malaysia by RHB Research Institute Sdn Bhd (233327-M), Level 11, Tower One, RHB Centre, Jalan Tun Razak, 50400 Kuala Lumpur, a wholly-owned subsidiary of RHB Investment Bank Berhad (RHBIB), which in turn is a wholly-owned subsidiary of RHB Capital Berhad. Singapore This report is published and distributed in Singapore by DMG & Partners Research Pte Ltd (Reg. No. 200808705N), a wholly-owned subsidiary of DMG & Partners Securities Pte Ltd, a joint venture between Deutsche Asia Pacific Holdings Pte Ltd (a subsidiary of Deutsche Bank Group) and OSK Investment Bank Berhad, Malaysia which have since merged into RHB Investment Bank Berhad (the merged entity is referred to as “RHBIB”, which in turn is a wholly-owned subsidiary of RHB Capital Berhad). DMG & Partners Securities Pte Ltd is a Member of the Singapore Exchange Securities Trading Limited. DMG & Partners Securities Pte Ltd may have received compensation from the company covered in this report for its corporate finance or its dealing activities; this report is therefore classified as a non-independent report. As of 11 September 2014, DMG & Partners Securities Pte Ltd and its subsidiaries, including DMG & Partners Research Pte Ltd do not have proprietary positions in the securities covered in this report, except for: a) - As of 11 September 2014, none of the analysts who covered the securities in this report has an interest in such securities, except for: a) - Special Distribution by RHB Where the research report is produced by an RHB entity (excluding DMG & Partners Research Pte Ltd) and distributed in Singapore, it is only distributed to "Institutional Investors", "Expert Investors" or "Accredited Investors" as defined in the Securities and Futures Act, CAP. 289 of Singapore. If you are not an "Institutional Investor", "Expert Investor" or "Accredited Investor", this research report is not intended for you and you should disregard this research report in its entirety. In respect of any matters arising from, or in connection with this research report, you are to contact our Singapore Office, DMG & Partners Securities Pte Ltd Hong Kong This report is published and distributed in Hong Kong by RHB OSK Securities Hong Kong Limited (“RHBSHK”) (formerly known as OSK Securities Hong Kong Limited), a subsidiary of OSK Investment Bank Berhad, Malaysia which have since merged into RHB Investment Bank Berhad (the merged entity is referred to as “RHBIB”), which in turn is a wholly-owned subsidiary of RHB Capital Berhad.

11

RHBSHK, RHBIB and/or other affiliates may beneficially own a total of 1% or more of any class of common equity securities of the subject company. RHBSHK, RHBIB and/or other affiliates may, within the past 12 months, have received compensation and/or within the next 3 months seek to obtain compensation for investment banking services from the subject company. Risk Disclosure Statements The prices of securities fluctuate, sometimes dramatically. The price of a security may move up or down, and may become valueless. It is as likely that losses will be incurred rather than profit made as a result of buying and selling securities. Past performance is not a guide to future performance. RHBSHK does not maintain a predetermined schedule for publication of research and will not necessarily update this report Indonesia This report is published and distributed in Indonesia by PT RHB OSK Securities Indonesia (formerly known as PT OSK Nusadana Securities Indonesia), a subsidiary of OSK Investment Bank Berhad, Malaysia, which have since merged into RHB Investment Bank Berhad, which in turn is a wholly-owned subsidiary of RHB Capital Berhad. Thailand This report is published and distributed in Thailand by RHB OSK Securities (Thailand) PCL (formerly known as OSK Securities (Thailand) PCL), a subsidiary of OSK Investment Bank Berhad, Malaysia, which have since merged into RHB Investment Bank Berhad, which in turn is a wholly-owned subsidiary of RHB Capital Berhad. Other Jurisdictions In any other jurisdictions, this report is intended to be distributed to qualified, accredited and professional investors, in compliance with the law and regulations of the jurisdictions. DMG & Partners Research Guide to Investment Ratings Buy: Share price may exceed 10% over the next 12 months Trading Buy: Share price may exceed 15% over the next 3 months, however longer-term outlook remains uncertain Neutral: Share price may fall within the range of +/- 10% over the next 12 months Take Profit: Target price has been attained. Look to accumulate at lower levels Sell: Share price may fall by more than 10% over the next 12 months Not Rated: Stock is not within regular research coverage DISCLAIMERS This research is issued by DMG & Partners Research Pte Ltd and it is for general distribution only. It does not have any regard to the specific investment objectives, financial situation and particular needs of any specific recipient of this research report. You should independently evaluate particular investments and consult an independent financial adviser before making any investments or entering into any transaction in relation to any securities or investment instruments mentioned in this report. The information contained herein has been obtained from sources we believed to be reliable but we do not make any representation or warranty nor accept any responsibility or liability as to its accuracy, completeness or correctness. Opinions and views expressed in this report are subject to change without notice. This report does not constitute or form part of any offer or solicitation of any offer to buy or sell any securities. DMG & Partners Research Pte Ltd is a wholly-owned subsidiary of DMG & Partners Securities Pte Ltd, a joint venture between OSK Investment Bank Berhad, Malaysia which have since merged into RHB Investment Bank Berhad (the merged entity is referred to as “RHBIB” which in turn is a wholly-owned subsidiary of RHB Capital Berhad) and Deutsche Asia Pacific Holdings Pte Ltd (a subsidiary of Deutsche Bank Group). DMG & Partners Securities Pte Ltd is a Member of the Singapore Exchange Securities Trading Limited. DMG & Partners Securities Pte Ltd and their associates, directors, and/or employees may have positions in, and may effect transactions in the securities covered in the report, and may also perform or seek to perform broking and other corporate finance related services for the corporations whose securities are covered in the report. This report is therefore classified as a non-independent report. As of Error! Bookmark not defined., DMG & Partners Securities Pte Ltd and its subsidiaries, including DMG & Partners Research Pte Ltd, do not have proprietary positions in the subject companies, except for: a) - As of Error! Bookmark not defined., none of the analysts who covered the stock in this report has an interest in the subject companies covered in this report, except for: a) Error! Bookmark not defined. DMG & Partners Research Pte. Ltd. (Reg. No. 200808705N)

Kuala Lumpur Hong Kong Singapore

Malaysia Research Office

RHB Research Institute Sdn Bhd Level 11, Tower One, RHB Centre

Jalan Tun Razak Kuala Lumpur

Malaysia Tel : +(60) 3 9280 2185 Fax : +(60) 3 9284 8693

RHB OSK Securities Hong Kong Ltd.

(formerly known as OSK Securities Hong Kong Ltd.) 12th Floor

World-Wide House 19 Des Voeux Road Central, Hong Kong

Tel : +(852) 2525 1118 Fax : +(852) 2810 0908

DMG & Partners

Securities Pte. Ltd. 10 Collyer Quay

#09-08 Ocean Financial Centre Singapore 049315

Tel : +(65) 6533 1818 Fax : +(65) 6532 6211

Jakarta Shanghai Phnom Penh

PT RHB OSK Securities Indonesia

(formerly known as PT OSK Nusadana Securities Indonesia)

Plaza CIMB Niaga 14th Floor

Jl. Jend. Sudirman Kav.25 Jakarta Selatan 12920, Indonesia

Tel : +(6221) 2598 6888 Fax : +(6221) 2598 6777

RHB OSK (China) Investment Advisory Co. Ltd.

(formerly known as OSK (China) Investment Advisory Co. Ltd.)

Suite 4005, CITIC Square 1168 Nanjing West Road

Shanghai 20041 China

Tel : +(8621) 6288 9611 Fax : +(8621) 6288 9633

RHB OSK Indochina Securities Limited

(formerly known as OSK Indochina Securities Limited) No. 1-3, Street 271

Sangkat Toeuk Thla, Khan Sen Sok Phnom Penh

Cambodia Tel: +(855) 23 969 161 Fax: +(855) 23 969 171

Bangkok

RHB OSK Securities (Thailand) PCL

(formerly known as OSK Securities (Thailand) PCL) 10th Floor, Sathorn Square Office Tower

98, North Sathorn Road, Silom Bangrak, Bangkok 10500

Thailand Tel: +(66) 862 9999 Fax : +(66) 108 0999

Thai Institute of Directors Association (IOD) – Corporate Governance Report Rating 2013

ADVANC BCP CPF ERW IVL NKI PS ROBINS SCB SNC TCAP TMB UV AOT BECL CPN GRAMMY KBANK NOBLE PSL RS SCC SPALI THAI TNITY VGI ASIMAR BKI CSL HANA KKP PAP PTT S&J SCSMG SPI THCOM TOP WACOAL BAFS BROOK DRT HEMRAJ KTB PG PTTEP SAMART SE-ED SSI THRE TRC BANPU BTS DTAC ICC LPN PHOL PTTGC SAMTEL SIM SSSC TIP TRUE BAY CIMB EASTW INTUCH MCOT PR QH SAT SIS SVI TASCO TTW BBL CK EGCO IRPC MINT PRANDA RATCH SC SITHAI SYMC TKT TVO

2S AYUD CNT GL KKC MBK OISHI SABINA STANLY TK TTCL zZMICO ACAP BEC CPALL GLOW KSL MBKET PB SAMCO STEC TLUXE TUF AF BFIT CSC GOLD KWC MFC PDI SCCC SUC TMILL TWFP AHC BH DCC GSTEL L&E MFEC PE SCG SUSCO TMT TYM AIT BIGC DELTA GUNKUL LANNA MODERN PF SEAFCO SYNTEC TNL UAC AKP BJC DTC HMPRO LH MTI PJW SFP TASCO TOG UMI AMANAH BLA ECL HTC LHBANK NBC PM SIAM TCP TPC UMS AMARIN BMCL EE IFEC LHK NCH PPM SINGER TF TPCORP UP AMATA BWG EIC INET LIVE NINE PPP SIRI TFD TPIPL UPOIC AP CCET ESSO ITD LOXLEY NMG PREB SKR TFI TRT UT APCO CENTEL FE JAS LRH NSI PRG SMT THANA TRU VIBHA APCS CFRESH FORTH JUBILE LST NWR PT SNP THANI TSC VIH ASIA CGS GBX KBS MACO OCC PYLON SPCG THIP TSTE VNG ASK CHOW GC KCE MAJOR OFM QTC SPPT TICON TSTH VNT ASP CM GFPT KGI MAKRO OGC RASA SSF TIPCO TTA YUASA *** PHATRA was voluntarily delisted from the Stock Exchange of Thailand effectively on September 25,2012

A BCH CRANE FPI IT MBAX PICO SGP TBSP TPP WIN AAV BEAUTY CSP FSS JMART MDX PL SIMAT TCCC TR WORK AEC BGI CSR GENCO JMT PRINC POST SLC TEAM TTI AEONTS BLAND CTW GFM JTS MJD PRECHA SMIT TGCI TVD AFC BOL DEMCO GJS JUTHA MK PRIN SMK TIC TVI AGE BROCK DNA GLOBAL KASET MOONG Q-CON SOLAR TIES TWZ AH BSBM DRACO HFT KC MPIC QLT SPC TIW UBIS AI CHARAN EA HTECH KCAR MSC RCI SPG TKS UEC AJ CHUO EARTH HYDRO KDH NC RCL SRICHA TMC UOBKH AKR CI EASON IFS KTC NIPPON ROJNA SSC TMD UPF ALUCON CIG EMC IHL KWH NNCL RPC STA TMI UWC ANAN CITY EPCO ILINK LALIN NTV SCBLIF SUPER TNDT VARO ARIP CMR F&D INOX LEE OSK SCP SVOA TNPC VTE AS CNS FNS IRC MATCH PAE SENA SWC TOPP WAVE BAT-3K CPL FOCUS IRPC MATI PATO SF SYNEX TPA WG *** CIMBI was voluntarily delisted from the Stock Exchange of Thailand effectively on September 25, 2012.

IOD (IOD Disclaimer)

การเปิดเผลผลการส ารวจของสมาคมส่งเสริมสถาบันกรรมการบรษิัทไทย (IOD) ในเรื่องการก ากับดูแลกิจการ (Corporate Governance) นี้เป็นการด าเนินการตามนโยบายของส านักงานคณะกรรมการก ากับหลักทรัพย์และตลาดหลักทรัพย์ โดยการส ารวจของ IOD เป็นการส ารวจและประเมินจากข้อมูลของบรษัทจดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทยและตลาดหลกัทรัพย์เอ็มเอไอ ที่มีการเปิดเผยต่อสาธารณะและเป็นข้อมูลที่ผูล้งทุนทั่วไปสามารถเข้าถงึได้ ดังนั้นผลส ารวจดังกล่าวจึงเป็นการน าเสนอในมุมมองของบุคคลภายนอกโดยไม่ได้เป็นการประเมินการปฏิบัติและมิได้มีการใช้ข้อมูลภายในในการประเมิน

อนึ่ง ผลการส ารวจดังกล่าว เป็นผลการส ารวจ ณ วนัที่ปรากฎในรายงานการก ากับดแูละกิจการบริษัทจดทะเบียนไทยเท่านั้น ดังนั้นผลการส ารวจจึงอาจเปลี่ยนแปลงได้ภายหลังวันดังกล่าว ทัง้นี้บริษัทหลักทรัพย์ อาร์เอสบี โอเอส เค จ ากัด (มหาชน) มิได้ยืนยันหรือรับรองถึงความถูกต้องของผลการส ารวจดงักล่าวแต่อย่างใด