scandinavian tobacco group powerpoint template

TRANSCRIPT

INVESTORPRESENTATION

FULL YEAR 2018

14 MARCH 2019

AGENDA

1. Highlights

2. Fuelling the Growth

3. Our categories

4. Financials

5. Financial ambitions and guidance 2019

6. Q&A

2

This presentation contains forward-looking statements. All statements other than statements of

historical fact included in the presentation are forward-looking statements. Forward-looking statements

give Scandinavian Tobacco Groups (“STG”) current expectations and projections relating to its financial

condition, results of operations, plans, objectives, future performance and business.

No representation, warranty or undertaking, express or implied, is made as to, and no reliance should

be placed on, the fairness, accuracy, completeness or correctness of the Information or the opinions

contained therein. The presentation has not been independently verified and will not be updated.

HIGHLIGHTS

3

Fuelling the Growth

~DKK 250 million in net

savings

FY2018

Delivered on Guidance

FY2019

>5% organic EBITDA

growth

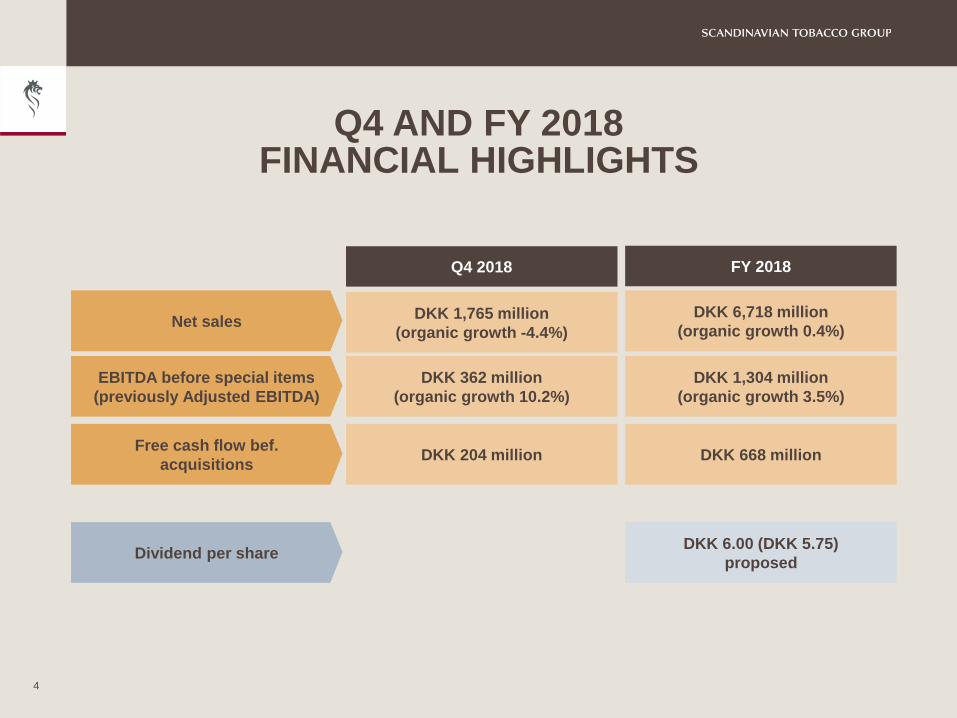

Q4 AND FY 2018FINANCIAL HIGHLIGHTS

4

Q4 2018

DKK 1,765 million

(organic growth -4.4%)

DKK 362 million

(organic growth 10.2%)

DKK 204 million

Net sales

EBITDA before special items

(previously Adjusted EBITDA)

Free cash flow bef.

acquisitions

DKK 6,718 million

(organic growth 0.4%)

FY 2018

DKK 1,304 million

(organic growth 3.5%)

DKK 668 million

Dividend per shareDKK 6.00 (DKK 5.75)

proposed

Simplified

organisation

and efficient

operating

model

Execution of

strategic

agenda and

drive internal

collaboration

Build strength

to cope with

changing

market

conditions

Prepare for

integration

of future

acquisitions

FUELLING THE GROWTH GROUP WIDE TRANSFORMATION

6

ORGANISATION

• FTE/net sales ratio

• Organisational layers from 10 to 7

• 100-120 white collar positions

GLOBAL LOGISTICS

• Manufacturing network

• Production allocation across factories

• Distribution efficiency and improve customer

service

OPERATIONAL COST EFFIENCY

• Product platforms

• SKU portfolio

• Capacity utilisation

FTG NET SAVINGS 250M

FULL-YEAR RUNRATE NET SAVINGS OF

~DKK 250 MILLION BY THE END OF 2021

SPECIAL COSTS 250M

SPECIAL COSTS OF UP TO DKK 250

MILLION. (DKK 182 MILLION IN 2018)

COMMERCIAL RESOURCES

• Four divisions anchored in Executive Board

• Customer service level

• Market shares in selected markets

• Number of active customers in online/catalogue business

FUELLING THE GROWTHOPERATIONAL INITIATIVES AND FINANCIAL IMPACT

GLOBAL PROCUREMENT

• A global procurement organisation

• Group purchases of DKK 4 billion

• The number of suppliers

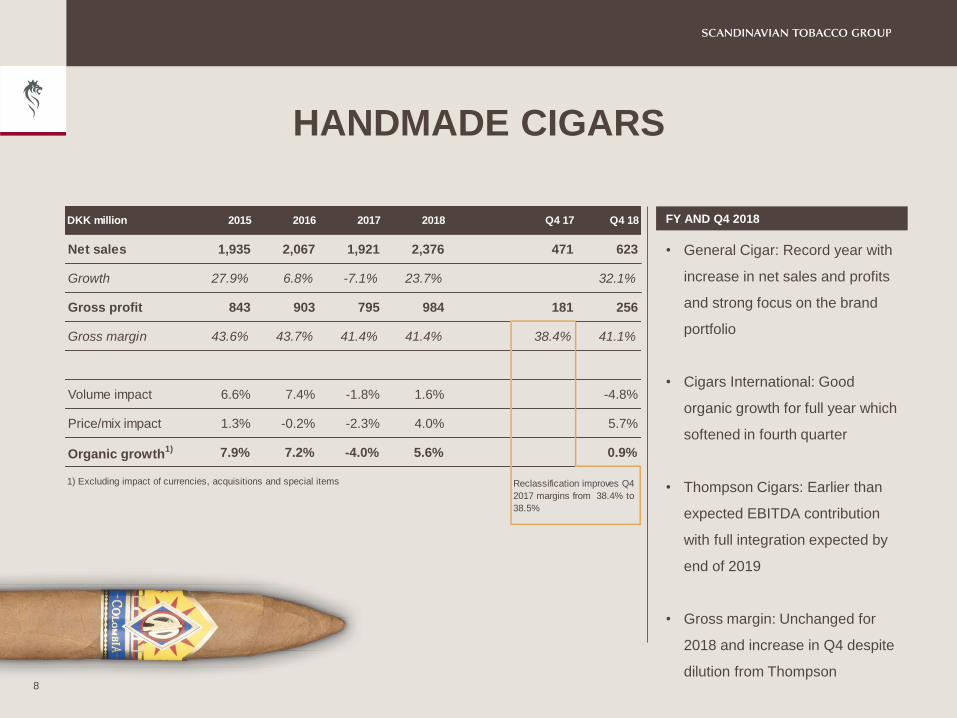

HANDMADE CIGARS

NO. 1 IN THE US

7

.

HANDMADE CIGARS

8

FY AND Q4 2018

• General Cigar: Record year with

increase in net sales and profits

and strong focus on the brand

portfolio

• Cigars International: Good

organic growth for full year which

softened in fourth quarter

• Thompson Cigars: Earlier than

expected EBITDA contribution

with full integration expected by

end of 2019

• Gross margin: Unchanged for

2018 and increase in Q4 despite

dilution from Thompson

DKK million 2015 2016 2017 2018 Q4 17 Q4 18

Net sales 1,935 2,067 1,921 2,376 471 623

Growth 27.9% 6.8% -7.1% 23.7% 32.1%

Gross profit 843 903 795 984 181 256

Gross margin 43.6% 43.7% 41.4% 41.4% 38.4% 41.1%

Volume impact 6.6% 7.4% -1.8% 1.6% -4.8%

Price/mix impact 1.3% -0.2% -2.3% 4.0% 5.7%

Organic growth1) 7.9% 7.2% -4.0% 5.6% 0.9%

1) Excluding impact of currencies, acquisitions and special items

Reclassification improves Q4

2017 margins from 38.4% to

38.5%

MACHINE-MADE CIGARSNO. 1 IN THE EU, AUSTRALIA AND CANADA

9

.avv

MACHINE-MADE CIGARS

FY AND Q4 2018

• Organic net sales improved

for most of the year but had a

disappointing finish in Q4

• The overall market share in

our key markets was down,

but good progress in UK,

Belgium and Spain

• Q4 was impacted by a weak

development in France

• Gross margin before special

items was down

10

DKK million 2015 2016 2017 2018 Q4 17 Q4 18

Net sales 2,702 2,593 2,491 2,367 668 616

Growth 4.2% -4.0% -3.9% -5.0% -7.9%

Gross profit 1,372 1,280 1,268 1,217 361 284

Gross margin 50.8% 49.3% 50.9% 51.4% 54.0% 46.0%

- bef. special items 52.2% 52.6% 52.4% 52.2% 53.4% 49.1%

Volume impact -5.7% -6.0% -3.7% -5.2% -9.4%

Price/mix impact 3.4% 2.2% 1.3% 1.8% 0.5%

Organic growth1) -2.3% -3.9% -2.4% -3.4% -9.0%

1) Excluding impact of currencies, acquisitions and special items

Reclassif ication improves

Q4 2017 margins from

53.4% to 55.3%

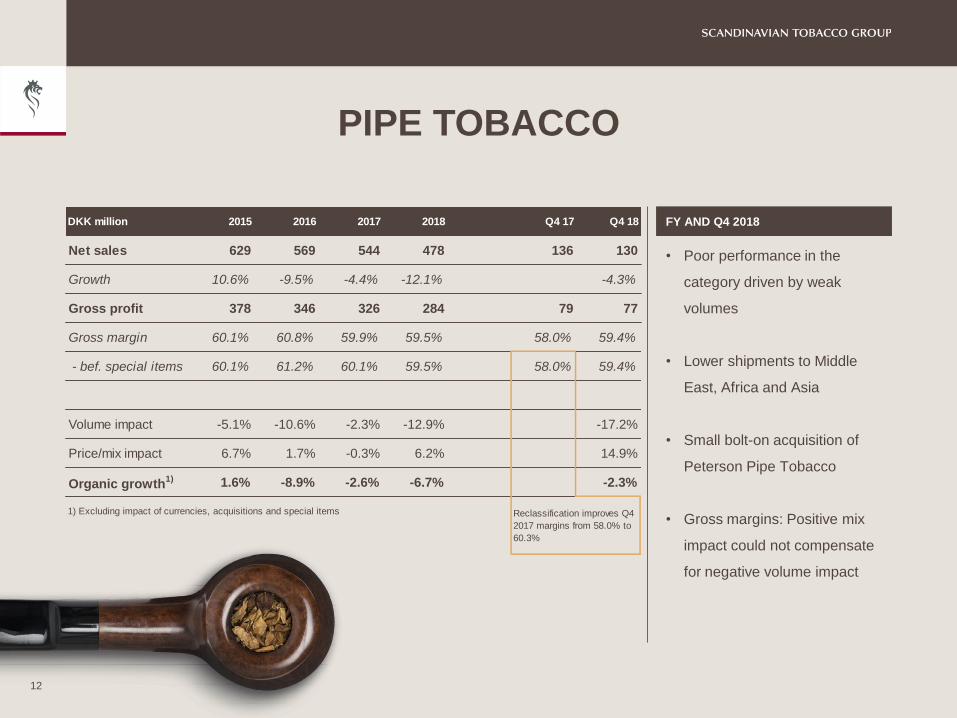

PIPE TOBACCO

NO. 1 GLOBALLY

11

.

PIPE TOBACCO

12

FY AND Q4 2018

• Poor performance in the

category driven by weak

volumes

• Lower shipments to Middle

East, Africa and Asia

• Small bolt-on acquisition of

Peterson Pipe Tobacco

• Gross margins: Positive mix

impact could not compensate

for negative volume impact

DKK million 2015 2016 2017 2018 Q4 17 Q4 18

Net sales 629 569 544 478 136 130

Growth 10.6% -9.5% -4.4% -12.1% -4.3%

Gross profit 378 346 326 284 79 77

Gross margin 60.1% 60.8% 59.9% 59.5% 58.0% 59.4%

- bef. special items 60.1% 61.2% 60.1% 59.5% 58.0% 59.4%

Volume impact -5.1% -10.6% -2.3% -12.9% -17.2%

Price/mix impact 6.7% 1.7% -0.3% 6.2% 14.9%

Organic growth1) 1.6% -8.9% -2.6% -6.7% -2.3%

1) Excluding impact of currencies, acquisitions and special items Reclassification improves Q4

2017 margins from 58.0% to

60.3%

FINE-CUT TOBACCONO. 1 IN THE US AND DENMARK

13

.

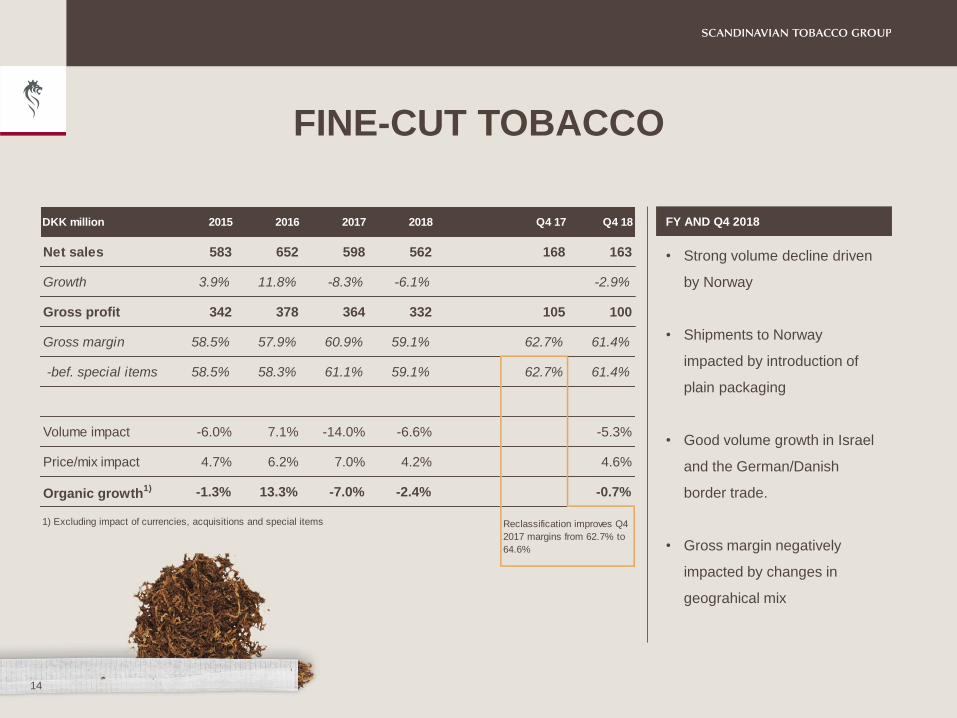

FINE-CUT TOBACCO

14

FY AND Q4 2018

• Strong volume decline driven

by Norway

• Shipments to Norway

impacted by introduction of

plain packaging

• Good volume growth in Israel

and the German/Danish

border trade.

• Gross margin negatively

impacted by changes in

geograhical mix

DKK million 2015 2016 2017 2018 Q4 17 Q4 18

Net sales 583 652 598 562 168 163

Growth 3.9% 11.8% -8.3% -6.1% -2.9%

Gross profit 342 378 364 332 105 100

Gross margin 58.5% 57.9% 60.9% 59.1% 62.7% 61.4%

-bef. special items 58.5% 58.3% 61.1% 59.1% 62.7% 61.4%

Volume impact -6.0% 7.1% -14.0% -6.6% -5.3%

Price/mix impact 4.7% 6.2% 7.0% 4.2% 4.6%

Organic growth1) -1.3% 13.3% -7.0% -2.4% -0.7%

1) Excluding impact of currencies, acquisitions and special items Reclassification improves Q4

2017 margins from 62.7% to

64.6%

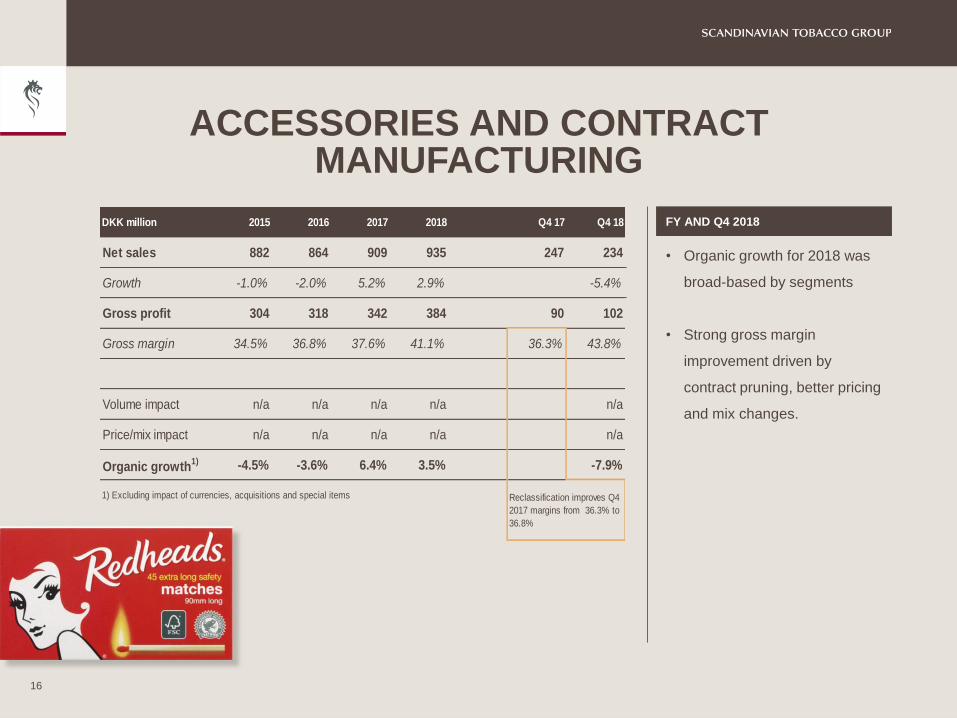

ACCESSORIES AND CONTRACTMANUFACTURING

POSITIVE GROWTH

15

.

ACCESSORIES AND CONTRACTMANUFACTURING

16

FY AND Q4 2018

• Organic growth for 2018 was

broad-based by segments

• Strong gross margin

improvement driven by

contract pruning, better pricing

and mix changes.

DKK million 2015 2016 2017 2018 Q4 17 Q4 18

Net sales 882 864 909 935 247 234

Growth -1.0% -2.0% 5.2% 2.9% -5.4%

Gross profit 304 318 342 384 90 102

Gross margin 34.5% 36.8% 37.6% 41.1% 36.3% 43.8%

Volume impact n/a n/a n/a n/a n/a

Price/mix impact n/a n/a n/a n/a n/a

Organic growth1) -4.5% -3.6% 6.4% 3.5% -7.9%

1) Excluding impact of currencies, acquisitions and special items Reclassification improves Q4

2017 margins from 36.3% to

36.8%

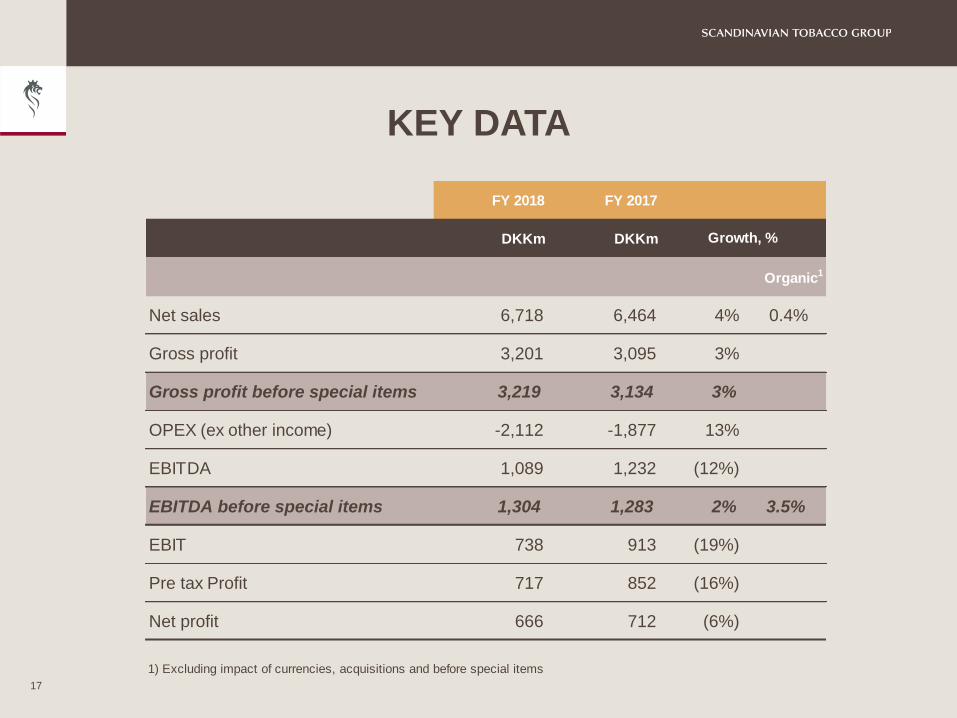

KEY DATA

17

FY 2018 FY 2017

DKKm DKKm

Organic1

Net sales 6,718 6,464 4% 0.4%

Gross profit 3,201 3,095 3%

Gross profit before special items 3,219 3,134 3%

OPEX (ex other income) -2,112 -1,877 13%

EBITDA 1,089 1,232 (12%)

EBITDA before special items 1,304 1,283 2% 3.5%

EBIT 738 913 (19%)

Pre tax Profit 717 852 (16%)

Net profit 666 712 (6%)

1) Excluding impact of currencies, acquisitions and before special items

Growth, %

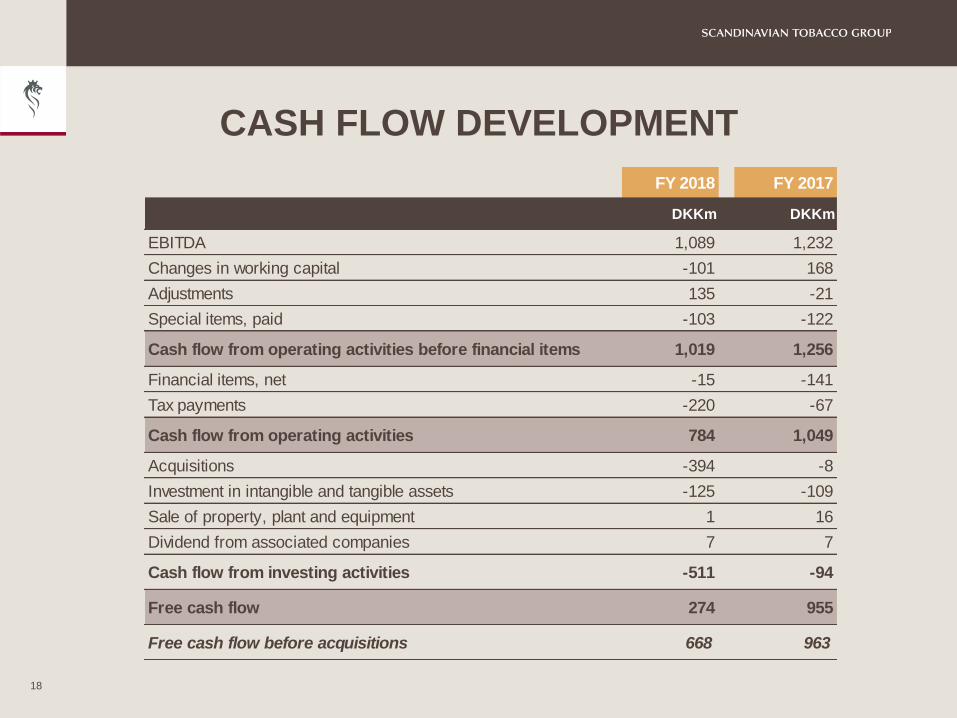

CASH FLOW DEVELOPMENT

18

FY 2018 FY 2017

DKKm DKKm

EBITDA 1,089 1,232

Changes in working capital -101 168

Adjustments 135 -21

Special items, paid -103 -122

Cash flow from operating activities before financial items 1,019 1,256

Financial items, net -15 -141

Tax payments -220 -67

Cash flow from operating activities 784 1,049

Acquisitions -394 -8

Investment in intangible and tangible assets -125 -109

Sale of property, plant and equipment 1 16

Dividend from associated companies 7 7

Cash flow from investing activities -511 -94

Free cash flow 274 955

Free cash flow before acquisitions 668 963

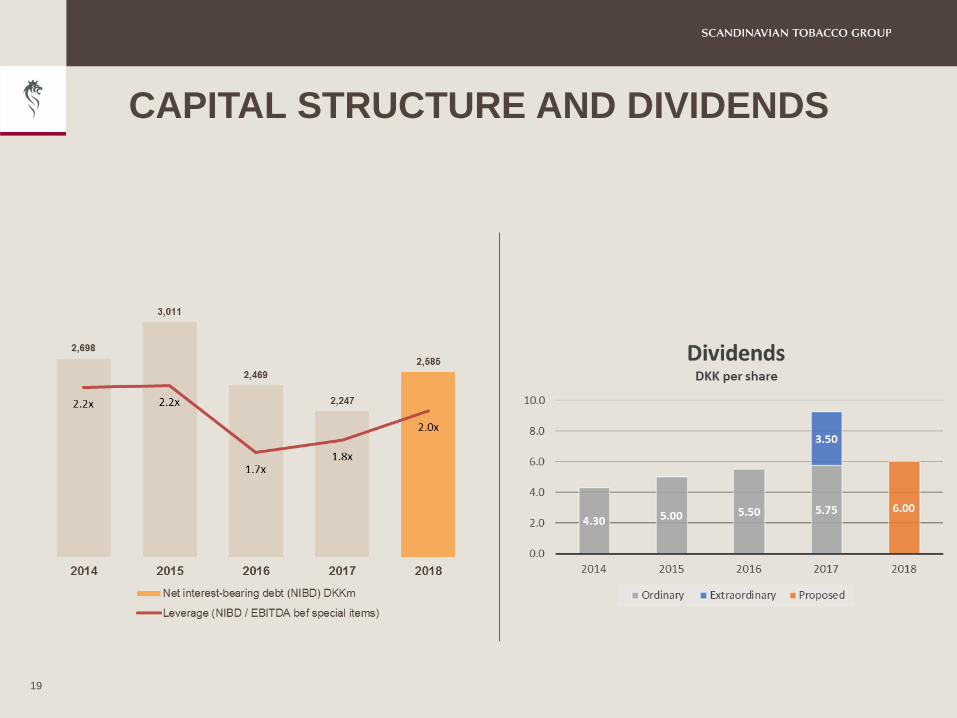

CAPITAL STRUCTURE AND DIVIDENDS

19

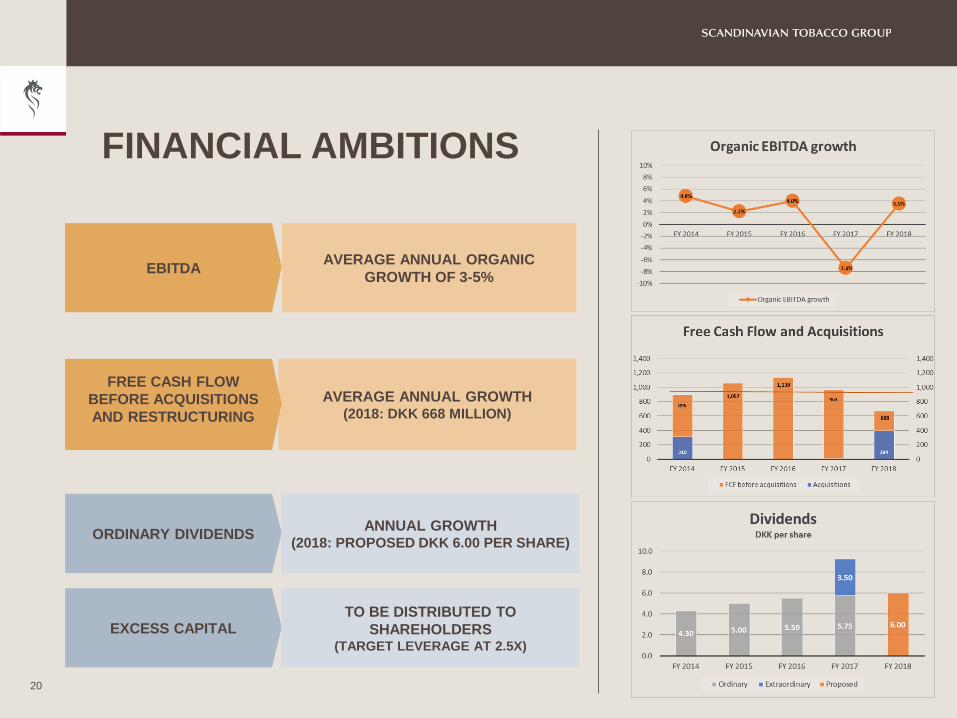

FINANCIAL AMBITIONS

20

AVERAGE ANNUAL ORGANIC

GROWTH OF 3-5%

AVERAGE ANNUAL GROWTH (2018: DKK 668 MILLION)

EBITDA

FREE CASH FLOW

BEFORE ACQUISITIONS

AND RESTRUCTURING

ORDINARY DIVIDENDS

EXCESS CAPITAL

ANNUAL GROWTH(2018: PROPOSED DKK 6.00 PER SHARE)

TO BE DISTRIBUTED TO

SHAREHOLDERS(TARGET LEVERAGE AT 2.5X)

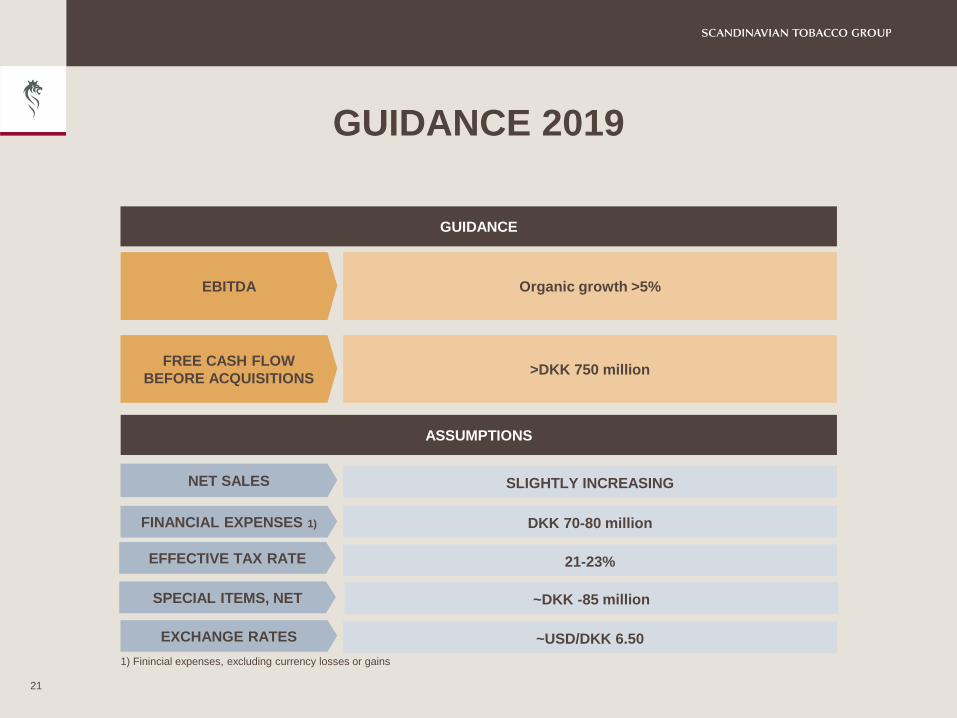

GUIDANCE 2019

21

GUIDANCE

Organic growth >5%

>DKK 750 million

EBITDA

FREE CASH FLOW

BEFORE ACQUISITIONS

NET SALES

1) Finincial expenses, excluding currency losses or gains

SLIGHTLY INCREASING

ASSUMPTIONS

FINANCIAL EXPENSES 1) DKK 70-80 million

21-23%

~DKK -85 million

~USD/DKK 6.50

EFFECTIVE TAX RATE

SPECIAL ITEMS, NET

EXCHANGE RATES

Q&A

22

23

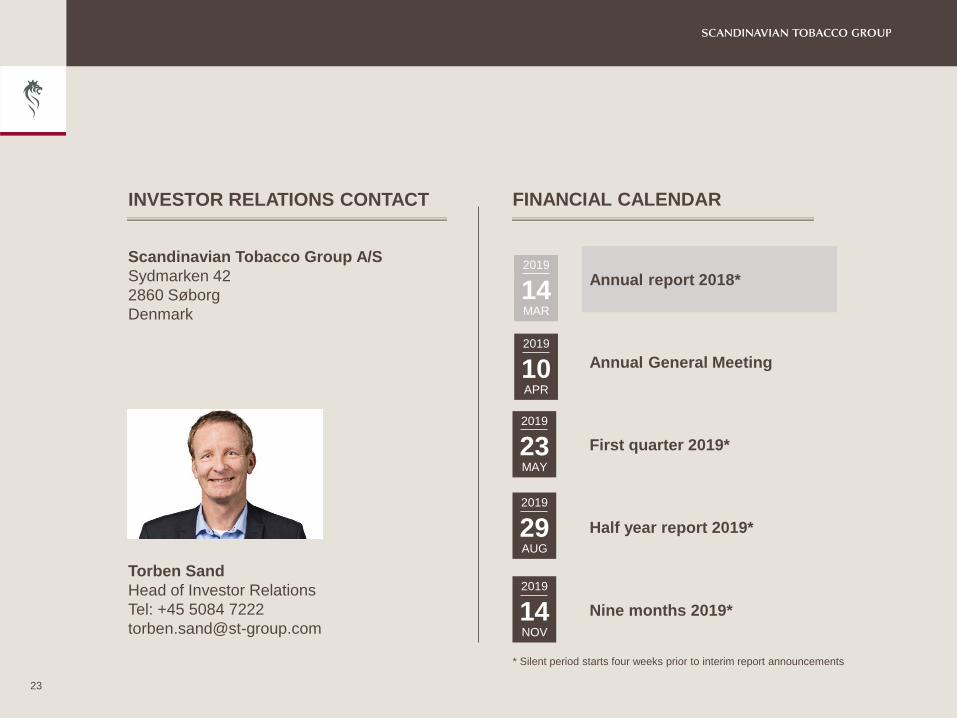

INVESTOR RELATIONS CONTACT FINANCIAL CALENDAR

Scandinavian Tobacco Group A/S

Sydmarken 42

2860 Søborg

Denmark

Torben Sand

Head of Investor Relations

Tel: +45 5084 7222

2019

14NOV

Annual report 2018*

Annual General Meeting

First quarter 2019*

Half year report 2019*

Nine months 2019*

* Silent period starts four weeks prior to interim report announcements

2019

14MAR

2019

10APR

2019

23MAY

2019

29AUG

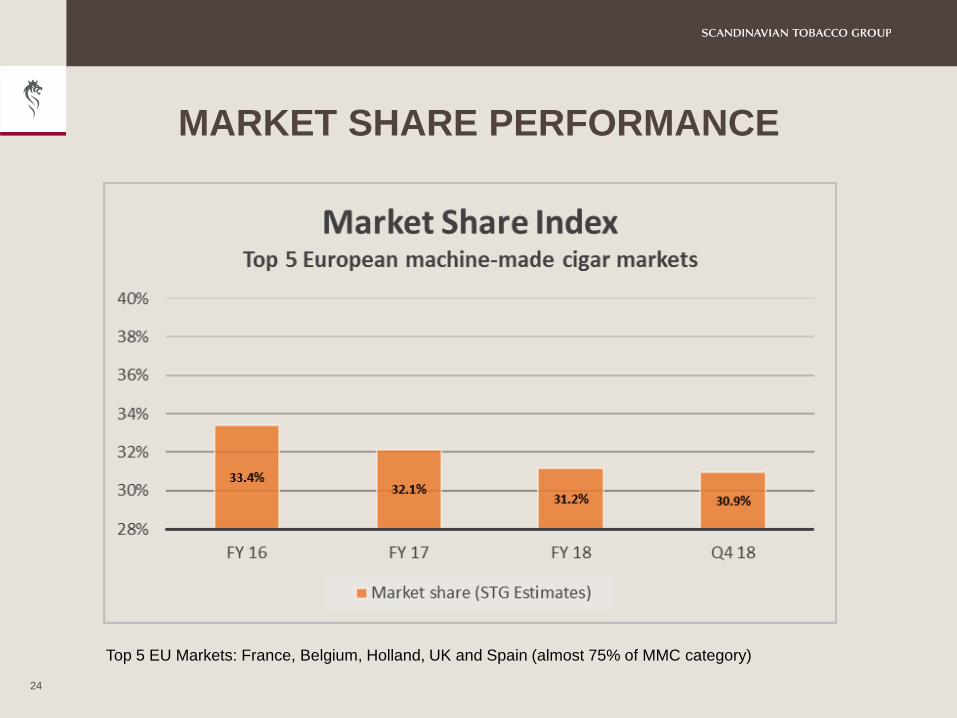

MARKET SHARE PERFORMANCE

24

Top 5 EU Markets: France, Belgium, Holland, UK and Spain (almost 75% of MMC category)

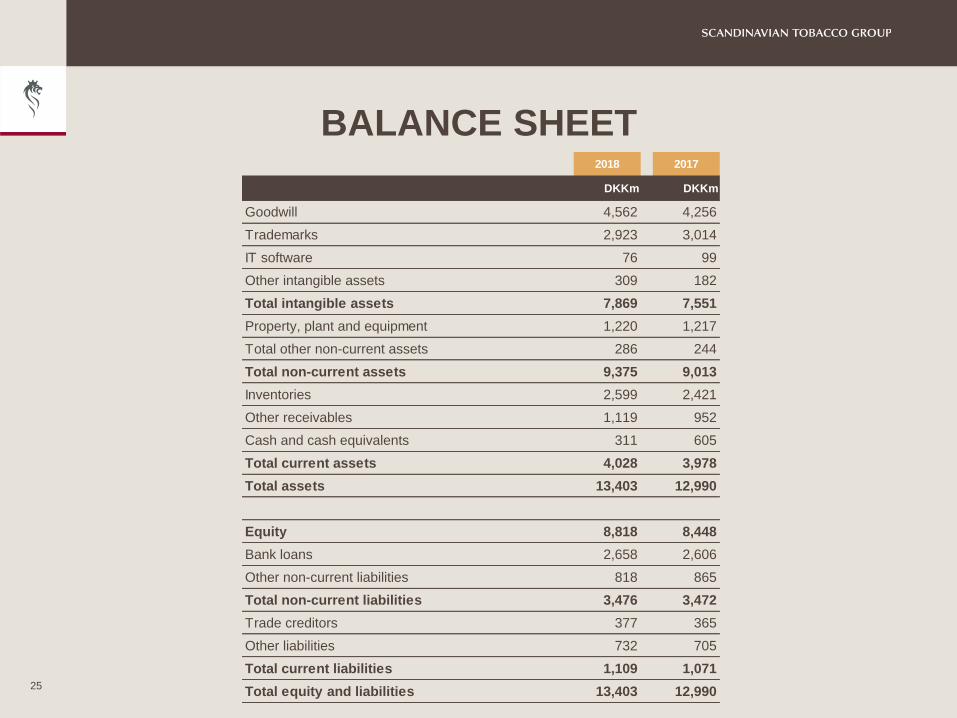

BALANCE SHEET

25

2018 2017

DKKm DKKm

Goodwill 4,562 4,256

Trademarks 2,923 3,014

IT software 76 99

Other intangible assets 309 182

Total intangible assets 7,869 7,551

Property, plant and equipment 1,220 1,217

Total other non-current assets 286 244

Total non-current assets 9,375 9,013

Inventories 2,599 2,421

Other receivables 1,119 952

Cash and cash equivalents 311 605

Total current assets 4,028 3,978

Total assets 13,403 12,990

Equity 8,818 8,448

Bank loans 2,658 2,606

Other non-current liabilities 818 865

Total non-current liabilities 3,476 3,472

Trade creditors 377 365

Other liabilities 732 705

Total current liabilities 1,109 1,071

Total equity and liabilities 13,403 12,990

FORWARD LOOKING STATEMENTS

This presentation contains forward-looking statements. All statements other than statements of historical fact included in

the presentation are forward-looking statements. Forward-looking statements give Scandinavian Tobacco Groups (“STG”)

current expectations and projections relating to its financial condition, results of operations, plans, objectives, future

performance and business. These statements may include, without limitation, any statements preceded by, followed by or

including words such as “target,” “believe,” “expect,” “aim,” “intend,” “may,” “anticipate,” “estimate,” “plan,” “project,” “will,”

“can have,” “likely,” “should,” “would,” “could” and other words and terms of similar meaning or the negative thereof. Such

forward-looking statements involve known and unknown risks, uncertainties and other important factors beyond STG’s

control that could cause STG’s actual results, performance or achievements to be materially different from the expected

results, performance or achievements expressed or implied by such forward-looking statements. Such forward-looking

statements are based on numerous assumptions regarding STG’s present and future business strategies and the

environment in which it will operate in the future.

No representation, warranty or undertaking, express or implied, is made as to, and no reliance should be placed on, the

fairness, accuracy, completeness or correctness of the Information or the opinions contained therein. The presentation

has not been independently verified and will not be updated. The Information, including but not limited to forward-looking

statements, applies only as of the date of this document and is not intended to give any assurances as to future results.

STG expressly disclaims any obligation or undertaking to disseminate any updates or revisions to the Information,

including any financial data or forward-looking statements, and will not publicly release any revisions it may make to the

Information that may result from any change in STG’s expectations, any change in events, conditions or circumstances on

which these forward-looking statements are based, or other events or circumstances arising after the date of this

document. Market data used in the Information not attributed to a specific source are estimates of STG and have not been

independently verified.

26