samba ar 2018 cover - financials.psx.com.pk

TRANSCRIPT

Vision & Mission 2

Core Values 3

Company Information 5

Branch Network 6

Board of Directors 8

Chairman's Message 9

The Executive Team 12

Performance Highlights 14

Samba Financial Group Awards 2018 15

Directors' Report 16

Six Years' Performance Highlights 28

Statement of Internal Controls 29

Complaint Handling Mechanism 30

Auditors' Review Report to the Members on

Code of Corporate Governance 31

Statement of Compliance with the

Code of Corporate Governance 32

Notice of Annual General Meeting 34

Financial Statements 37

Auditors' Report to the Members 38

Statement of Financial Position 42

Profit and Loss Account 43

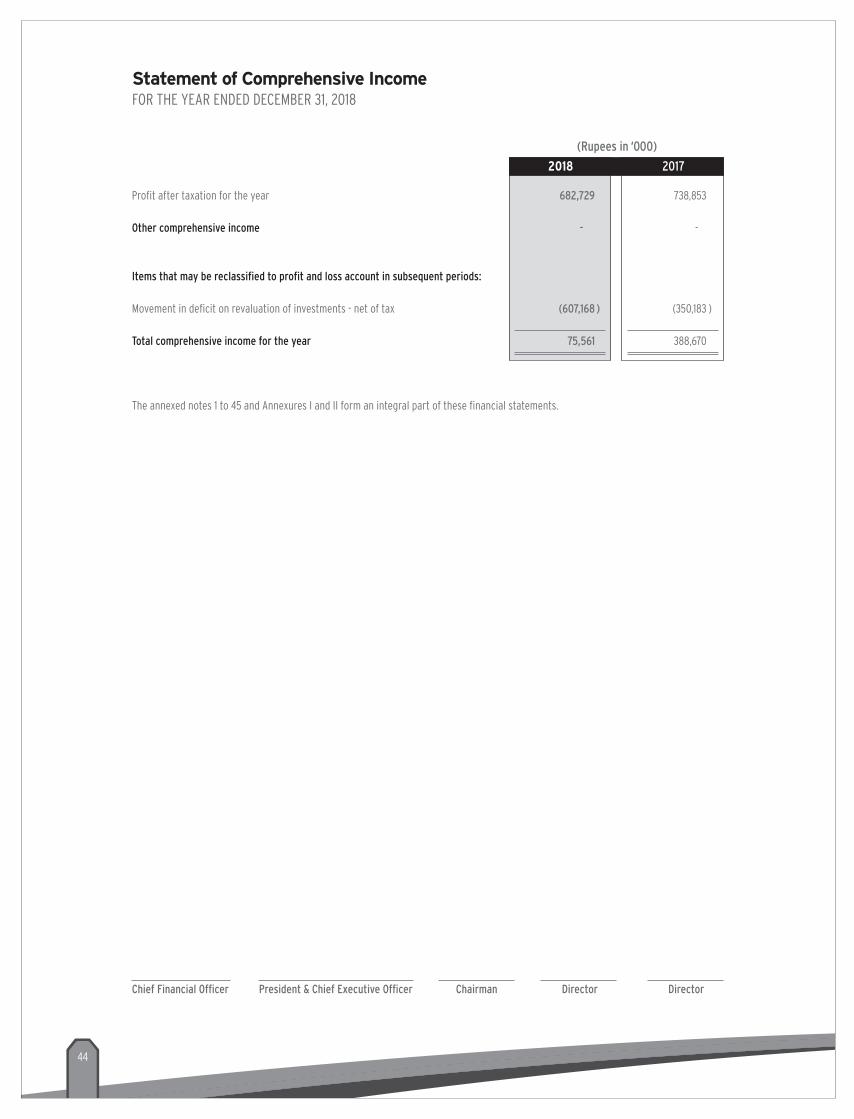

Statement of Comprehensive Income 44

Cash Flow Statement 45

Statement of Changes in Equity 46

Notes to the Financial Statements 47

Annexure - I 102

Annexure - II 103

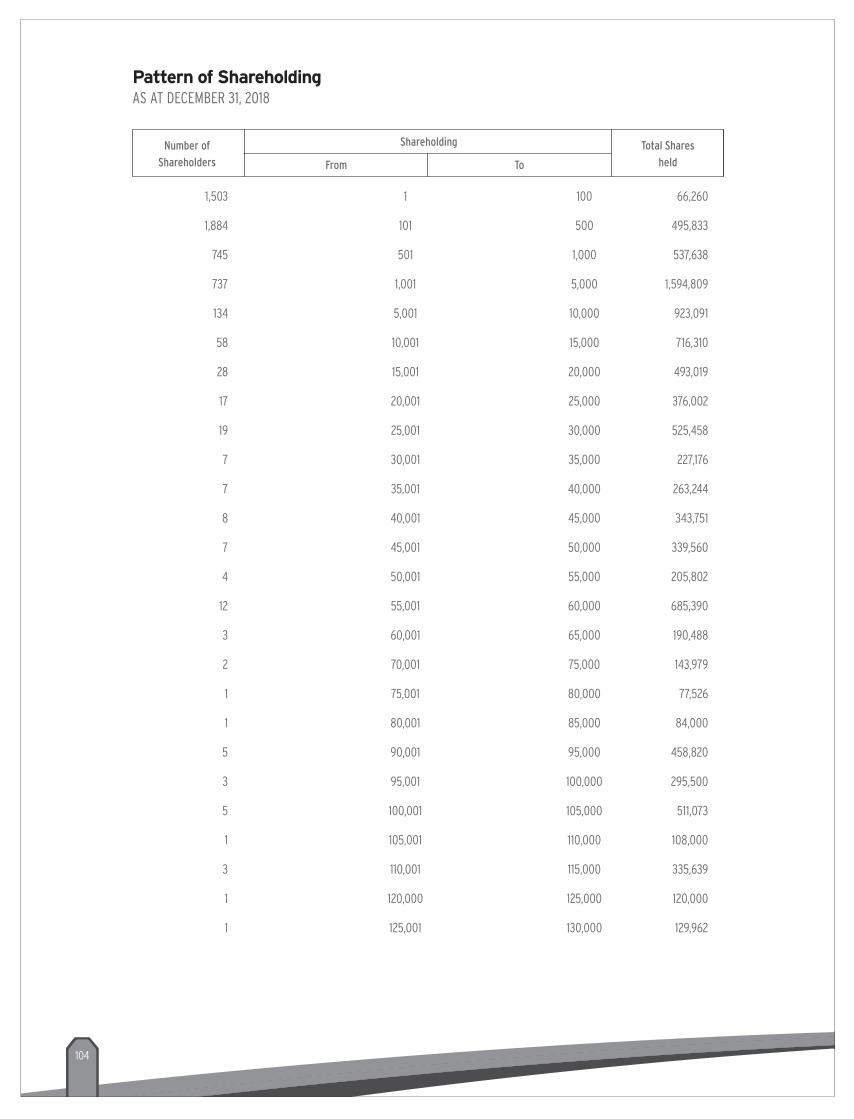

Pattern of Shareholding 104

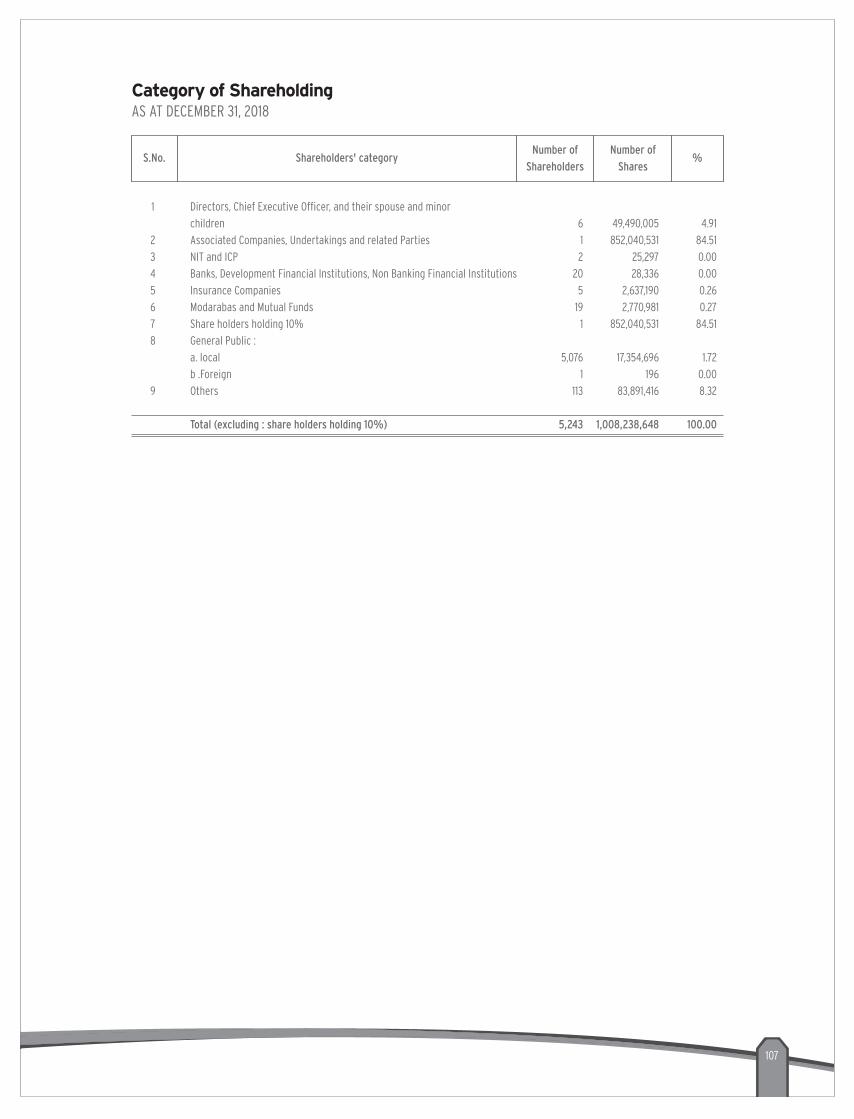

Category of Shareholding 107

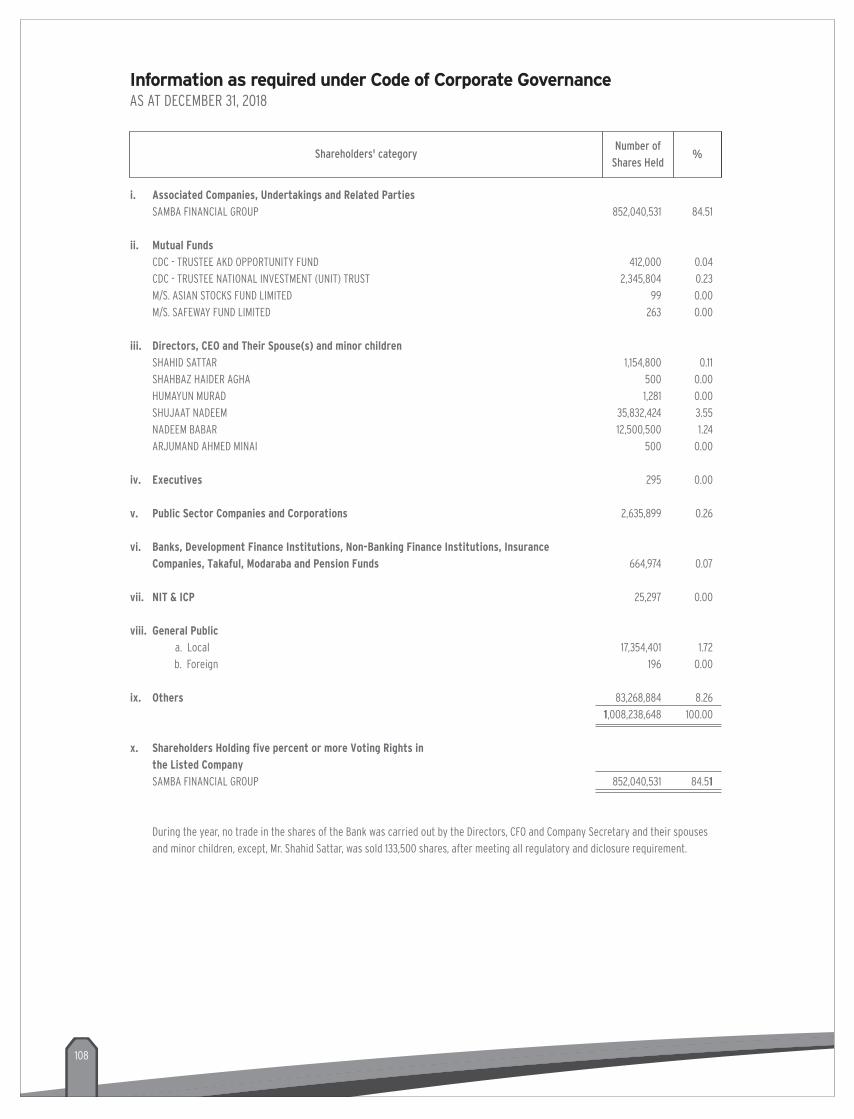

Information under Code of

Corporate Governance 108

Proxy Form 109

Admission Slip 113

CONTE

NTS

To be the most admired bank in Pakistan providing world class services and innovative solutions through its people and technology, yielding superior returns and demonstrating responsible corporate citizenship.

To become the most admired bank by:

• Providing world class solutions to our customers by exceeding their service expectations.

• Investing in people by hiring, motivating and retaining best talent.

• Creating sustainable value through growth and efficiency of all stakeholders.

• Delivering superior returns to our investors.

• Benefiting the communities in which we operate.

Vision

Mission

CoreValues

Meritocracy

We believe talent is brought to the fore by advancing individuals not for who they are, but for what they can produce. At Samba, we value the role of each employee from the highest to lowest levels.

Equal Opportunity

At Samba, we ensure all employees get equal opportunity to succeed. We value diversity and ensure fairness for all employees.

Respect & Dignity

At Samba, we respect every individual irrespective of their background and evaluate them on his/her potential and performance. Samba values such individual contributions and encourages employees to excel.

Integrity

At Samba, from top management to junior interns, we demand and maintain highest level of integrity. This is not just something we do, it is what we are.

Teamwork

Samba believes single units when joined with many like itself, combine into a powerful force that can achieve great things. We are encouraged to think as a group and to support each other.

0302

Auditors

Website

Mr. Rashid Jahangir

Chief Financial Officer

Auditors

A. F. Ferguson & Co. Chartered Accountants

Mohsin Tayebaly & Co. Advocates & Legal Consultants

Legal Advisors

Arif Habib Centre Plot No. 23, Ground floor,

M.T. Khan Road Karachi - Pakistan

Head Office

2nd Floor, Building # 13-T, F-7 Markaz, Near Post Mall,

Islamabad – Pakistan

Registered Office

Famco Associates (Pvt.) Limited

8-F, Next to Hotel Faran, Nursery, Block–6 P.E.C.H.S.,

Karachi – Pakistan

* Non-Executive Director w.e.f. Jan’ 24, 2019

** Appointed as Chairman of BNRC w.e.f. Feb’ 20, 2019

*** Resigned as Chairman of BNRC w.e.f. Jan’ 24, 2019

Share Registrar

www.samba.com.pk

(+92-21) 11 11 SAMBA (72622)

Help Line

Medium to Long Term AA (Double A)

Short Term Rating A-1 (A-One)

Credit Rating by JCR-VIS

Dr. Shujaat Nadeem Chairman/Non-Executive Director

Mr. Shahid Sattar President & CEO/Executive Director

Ms. Ranya Nashar Non-Executive Director

Mr. Antoine Mojabber Non-Executive Director

Mr. Beji Tak-Tak Non-Executive Director

Mr. Humayun Murad Independent Director

Mr. Nadeem Babar Independent Director*

Mr. Shahbaz Haider Agha Independent Director

Mr. Arjumand Ahmed Minai Independent Director

Mr. Humayun Murad Chairman

Ms. Ranya Nashar Member

Mr. Arjumand Ahmed Minai Member

Board Audit Committee

Mr. Beji Tak–Tak Chairman

Mr. Shahid Sattar Member

Mr. Antoine Mojabber Member

Mr. Shahbaz Haider Agha Member

Board Risk Committee

Mr. Shahbaz Haider Agha** Chairman

Ms. Ranya Nashar Member

Mr. Nadeem Babar*** Member

Mr. Humayun Murad Member

Board Nomination & Remuneration Committee

Dr. Shujaat Nadeem Chairman

Mr. Antoine Mojabber Member

Mr. Nadeem Babar Member

Board IT Committee

Board of Directors

Company Information

Website

Syed Zia-ul-Husnain Shamsi

Company Secretary

Mr. Shahid Sattar

President & Chief Executive Officer

0504

Currently, SBL has a network of 37 branches located in 10 major cities across the country.

Our Branch Network

KarachiFountain, SaddarRashid MinhasHyderiSMCHSBahria IDHA Phase VIShahra-e-FaisalGulshanCliftonBahadurabadIttehadSaba AvenueTauheed Commercial

LahoreGulbergMallAllama Iqbal Town

Johar TownDHA Phase IIINew Garden TownTufail Sarwar RoadCavalry GroundFaisal TownDHA Phase VBadami Bagh

IslamabadJinnah AvenueF-11F-7DHA Phase II

RawalpindiMurree RoadBahria TownWah Cantt.

GujranwalaG.T. Road

FaisalabadLiaquat Road

MultanNusrat Road

SialkotParis Road

PeshawarIslamia Road

Azad Jammu& KashmirBagh

0706

Chairman’sMessage

Our journey towards meeting our strategic objectives rests on a strong foundation of trust that Samba Bank has earned from its customers and other stakeholders. Our confidence, as we introduce high-quality digital strategies in pursuit of a differentiated customer experience, efficiency and quality earnings growth; is supported by the consistent record of accomplishment of Samba Bank that has always acted with responsibility, transparency and integrity. We are working to instill a culture of excellence across our bank and, at the same time, we are continuously investing in our businesses and people to offer high quality and differentiated service to our customers across all the business segments. We offer our staff and colleagues opportunities to learn and progress. We encourage them to improve, innovate, take ownership of their careers and succeed together.

Corporate and Investment Banking Group I am pleased to report that the Corporate and Investment Banking Group (CIBG) had an outstanding year, growing its customer base and loan book. The focus remains on improving margin with better cross-sell strategy and focus on deepening relationship with our customers. Multiple new cross sell initiatives were launched during the year including Samba Access (Cash Management System) and Call Deposit Receipts (CDRs). These initiatives stimulated the growth in deposits and a wider offering to our client base.

Retail Banking Group In the Retail Banking Group (RBG), we have successfully targeted Priority clients with improved wealth management products and a more focused service offering. As a result, the RBG’s deposit book saw healthy growth as well. More than 5,300 new relationships were added which helped the group to increase its Current Account book by 19% at the year-end with incremental deposit of PKR 4.9Bio. Personal Loan product (PIL), which was launched in 2017, was also a major success in 2018. The newly launched PIL portfolio closed over PKR 1Bio with a high quality portfolio. Considering the increased customer base and success of PIL initiative, the Auto Loan product was also launched in 2018. Both these products would help in further strengthening the RBG’s product offering to its retail clientele.

Global Markets

The Global Markets (GM) continued to support customer business groups’ liquidity requirements efficiently. During the year, the Pakistani Rupee underwent significant devaluation, core interest rate increased by 425bps and capital markets remained volatile. Global Markets capitalized on this volatility in the markets and delivered strong financial performance. The Margin Trading Product was amongst the new initiatives introduced by the business during the year and has already seen good traction and contribution to the bottom line of the bank

Commercial Banking Group and SME BankingThe Commercial Banking Group maintained its focus to grow its business and delivered positive results. The Commercial Banking Group was launched in late 2015 and its focus has been to serve commercial and medium-sized corporates.

In 2017, the SME banking proposition was launched to cater for financial needs of small & medium enterprises while complying with all regulatory requirements. Observing great potential in this segment, the Bank has developed a focused strategy to increase its standing in this market.

Information TechnologyFollowing the successful implementation of Temenos - T24 and allied systems, we have continued to make investments in the technology platform by launching the Samba-Smart Mobile Banking application, providing features beyond traditional functionalities to better respond to customers’ needs as they choose to manage their finances in new and different ways. We now have capability to deliver fast-to-market solutions and have a solid foundation for further development of customer experience and improving our solutions. This is an essential tool for the development of our digital services, anticipating the changing needs of customers in an increasingly connected world. The integration of Oracle Financials with core banking system (T-24) was another milestone for the bank.

Corporate Social ResponsibilityWe strive to operate as a responsible and sustainable company, collaborating with partners to promote social and economic development. Samba Bank manages business with its stakeholders in a manner that is ethically acceptable and beneficial for all. The bank holds an approved Corporate Social Responsibility (CSR) Policy to cover the core areas of focus on CSR. During 2018, the Bank continued to contribute towards education, health, environment, sports and awareness. Samba Bank in collaboration with World Wildlife Fund sponsored their plantation program named “Rung Do Pakistan”, and has donated 10,000 plants that will be planted across Pakistan covering different geographical locations.

Performance of the Board of DirectorsI take this opportunity to recognize the contribution of the Board of Directors to Samba Bank’s progress and continued success. During the year, the performance of Board of Directors exhibited high standards of business and professional conduct in managing and supervising the affairs of the Bank. The Board set the Bank’s strategic aims and provided the leadership to put them into effect, upholding the vision, mission and core values of the Bank. It also monitored the Bank’s financial and operational soundness, governance structure, the effectiveness of internal controls & audit functions and risk management framework.

AcknowledgementOn behalf of the Board of Directors, it is my pleasure to express my sincere appreciation to our customers and shareholders for their loyalty and continued support, the entire management team at Samba Bank for its continued dedication and service during the year, and to our staff for their wholehearted efforts. The achievements and the solid progress we have made in our journey could not have been realized without their dedication and loyalty. I look forward to a new year of challenges and opportunities, and hope you will join me in taking Samba Bank to even greater heights of success.

Dr. Shujaat NadeemChairman

I am pleased to report that Samba Bank had another good year. Our key investment areas are growing well and we are encouraged by the results. Of course, we have a long way to go. We are working hard to establish income growth momentum across all our businesses. In this report, we describe our progress in realizing our goals and strategic objectives as we continue to strengthen our business proposition, and get closer to our customers. Our new business initiatives spanning commercial & SME banking, personal & auto loans, and Samba Gold are making positive contribution. Consequently, the bank has posted a record, all-time high, annual profit before tax (PBT) of PKR 1,110Mio which is 19.21% higher than previous year. At close of 2018, the total assets of the bank stood at PKR 122.8Bio; an increase of around 4% over last year.

09

Board of Directors

Mr. Shahid SattarMs. Ranya Nashar

Mr. Beji Tak-Tak

Mr. Nadeem BabarMr. Antoine Majobber

Dr. Shujaat Nadeem

Mr. Humayun Murad

Mr. Shahbaz Haider Agha

Mr. Arjumand Ahmed Minai

08

10 11

Our journey towards meeting our strategic objectives rests on a strong foundation of trust that Samba Bank has earned from its customers and other stakeholders. Our confidence, as we introduce high-quality digital strategies in pursuit of a differentiated customer experience, efficiency and quality earnings growth; is supported by the consistent record of accomplishment of Samba Bank that has always acted with responsibility, transparency and integrity. We are working to instill a culture of excellence across our bank and, at the same time, we are continuously investing in our businesses and people to offer high quality and differentiated service to our customers across all the business segments. We offer our staff and colleagues opportunities to learn and progress. We encourage them to improve, innovate, take ownership of their careers and succeed together.

Corporate and Investment Banking Group I am pleased to report that the Corporate and Investment Banking Group (CIBG) had an outstanding year, growing its customer base and loan book. The focus remains on improving margin with better cross-sell strategy and focus on deepening relationship with our customers. Multiple new cross sell initiatives were launched during the year including Samba Access (Cash Management System) and Call Deposit Receipts (CDRs). These initiatives stimulated the growth in deposits and a wider offering to our client base.

Retail Banking Group In the Retail Banking Group (RBG), we have successfully targeted Priority clients with improved wealth management products and a more focused service offering. As a result, the RBG’s deposit book saw healthy growth as well. More than 5,300 new relationships were added which helped the group to increase its Current Account book by 19% at the year-end with incremental deposit of PKR 4.9Bio. Personal Loan product (PIL), which was launched in 2017, was also a major success in 2018. The newly launched PIL portfolio closed over PKR 1Bio with a high quality portfolio. Considering the increased customer base and success of PIL initiative, the Auto Loan product was also launched in 2018. Both these products would help in further strengthening the RBG’s product offering to its retail clientele.

Global Markets

The Global Markets (GM) continued to support customer business groups’ liquidity requirements efficiently. During the year, the Pakistani Rupee underwent significant devaluation, core interest rate increased by 425bps and capital markets remained volatile. Global Markets capitalized on this volatility in the markets and delivered strong financial performance. The Margin Trading Product was amongst the new initiatives introduced by the business during the year and has already seen good traction and contribution to the bottom line of the bank

Commercial Banking Group and SME BankingThe Commercial Banking Group maintained its focus to grow its business and delivered positive results. The Commercial Banking Group was launched in late 2015 and its focus has been to serve commercial and medium-sized corporates.

In 2017, the SME banking proposition was launched to cater for financial needs of small & medium enterprises while complying with all regulatory requirements. Observing great potential in this segment, the Bank has developed a focused strategy to increase its standing in this market.

Information TechnologyFollowing the successful implementation of Temenos - T24 and allied systems, we have continued to make investments in the technology platform by launching the Samba-Smart Mobile Banking application, providing features beyond traditional functionalities to better respond to customers’ needs as they choose to manage their finances in new and different ways. We now have capability to deliver fast-to-market solutions and have a solid foundation for further development of customer experience and improving our solutions. This is an essential tool for the development of our digital services, anticipating the changing needs of customers in an increasingly connected world. The integration of Oracle Financials with core banking system (T-24) was another milestone for the bank.

Corporate Social ResponsibilityWe strive to operate as a responsible and sustainable company, collaborating with partners to promote social and economic development. Samba Bank manages business with its stakeholders in a manner that is ethically acceptable and beneficial for all. The bank holds an approved Corporate Social Responsibility (CSR) Policy to cover the core areas of focus on CSR. During 2018, the Bank continued to contribute towards education, health, environment, sports and awareness. Samba Bank in collaboration with World Wildlife Fund sponsored their plantation program named “Rung Do Pakistan”, and has donated 10,000 plants that will be planted across Pakistan covering different geographical locations.

Performance of the Board of DirectorsI take this opportunity to recognize the contribution of the Board of Directors to Samba Bank’s progress and continued success. During the year, the performance of Board of Directors exhibited high standards of business and professional conduct in managing and supervising the affairs of the Bank. The Board set the Bank’s strategic aims and provided the leadership to put them into effect, upholding the vision, mission and core values of the Bank. It also monitored the Bank’s financial and operational soundness, governance structure, the effectiveness of internal controls & audit functions and risk management framework.

AcknowledgementOn behalf of the Board of Directors, it is my pleasure to express my sincere appreciation to our customers and shareholders for their loyalty and continued support, the entire management team at Samba Bank for its continued dedication and service during the year, and to our staff for their wholehearted efforts. The achievements and the solid progress we have made in our journey could not have been realized without their dedication and loyalty. I look forward to a new year of challenges and opportunities, and hope you will join me in taking Samba Bank to even greater heights of success.

Dr. Shujaat NadeemChairman

I am pleased to report that Samba Bank had another good year. Our key investment areas are growing well and we are encouraged by the results. Of course, we have a long way to go. We are working hard to establish income growth momentum across all our businesses. In this report, we describe our progress in realizing our goals and strategic objectives as we continue to strengthen our business proposition, and get closer to our customers. Our new business initiatives spanning commercial & SME banking, personal & auto loans, and Samba Gold are making positive contribution. Consequently, the bank has posted a record, all-time high, annual profit before tax (PBT) of PKR 1,110Mio which is 19.21% higher than previous year. At close of 2018, the total assets of the bank stood at PKR 122.8Bio; an increase of around 4% over last year.

The Executive Team

Humayun M. BawkherZeeshan KayserSyed Zia ul Husnain Shamsi

Rashid JahangirAbid Husain

Chief Credit Officer

Chief Technology Officer

Group Head, Legal Affairs, IRMand Company Secretary

Chief Financial Officer

Group Head Operations

Down Left to Right

Muhammad Arshad MehmoodArif RazaTalal JavedShahid SattarSamina Hamid KhanSyed Ghazanfar Agha

Group Head Human Resources & Training

Group Head Global Market (Treasurer)

Group Head Consumer Banking

President & CEO

Chief Risk Officer

Group Head, Corporate & Investment Banking

Group Head Compliance

Group Head, Commercial Bankingand Administration

Chief Internal Auditor

Syed Amir Raza ZaidiAhmad Tariq Azam

Sitwat Rasool Qadri

Top Left to Right

14 15

Performance Highlights Samba Financial Group Awards 2018

Global Finance

• Best Foreign Exchange Provider in Saudi Arabia (10th year)

• Best Bank for Payments and Collections in the world for the first year and Best Bank for Payments and Collections in the Middle East (4th year in a row)

• Best Bank in Saudi Arabia (13th year in a row)• Best Online Cash Management in Saudi Arabia• Best Trade Finance Services in Saudi Arabia• Best Web Design in Saudi Arabia• Best Integrated consumer Banking Site in Saudi

Arabia• Best SMS/Text Banking in Saudi Arabia

Banker Middle East

• Best IT Risk Management KSA• Best IT Solutions KSA

The Banker Middle East (Top 100 Middle East Bank Rankings)

• Rank: 6th

Institute of Public Administration

• Best National Institution for Employment of Saudis Employees (10th year)

The Banker (Top 1000 World Bank Rankings)

• World Rank: 124 (119 Last Year) - Middle East Rank: 6th (6th Last Year)

World Union of Arab Bankers

• Best Arabian Bank for the year 2018.

The Asian Banker

• Strongest Bank in Saudi Arabia for the year 2018.• The Best Commercial Bank in Saudi Arabia

(The Global Wealth and Society awards)

MEED

• Best Bank/Financial Institution of the Year in the GCC

Total Number of Awards & Recognitions: 17

2008 2009 2010 201 1 201 2 201 3 201 4 201 7 201 8201 6201 5

Rupees in billion

2008 2009 2010 201 1 201 2 201 3 201 4 201 7 201 8201 5 201 6

54.9

40.240.2

28.850.3

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Advances Investments Placements Cash & bank balances Other assets

2013

2014

2015

2016

2017

2018

10%0%

2013

2014

2015

2016

2017

20% 30% 40% 50% 60% 70% 80% 90% 100%

Deposits Borrowings Bills payable Other liabilities Equity & Reserves

2018

65.2

21.0

� CA

GR

53.6

23

.2 � C

AG

R

2015 2016 201820142013

44%39% 8% 5% 4%

2017Assets: Advances 46% 43% 30% 28% 34% Investments 35% 39% 56% 56% 54%Placements 2% 4% 2% 5% 4%Cash & bank balances 7% 5% 5% 5% 3%Other assets 10% 9% 7% 6% 5%

53%32% 1% 3% 11%

Liabilities & Equity: Deposits 62% 63% 48% 49% 47%Borrowings 7% 12% 34% 35% 39%Bills payable 2% 1% 1% 1% 1% Other liabilities 3% 3% 2% 3% 2%Equity & Reserves 26% 21% 15% 12% 11%

16 17

Directors’ Report

On behalf of the Board of Directors, we are pleased to present the annual report of the Bank along with its audited

financial statements and auditors’ report for the year ended December 31, 2018.

Economic Highlights

Pakistan’s economy witnessed a decent growth in the last three years supported by the favorable global

economic environment, CPEC related investment activity, and expansionary fiscal and monetary policies.

However, the momentum was slowed down due to heightened external imbalances. PKR witnessed a 26%

devaluation in CY2018. With the objective to curtail domestic demand pressure, the central bank cumulatively

raised interest rates by 425bps in CY2018, with majority of increase happening in the latter half of the year.

Bank’s Operating Results and Financial Review

In terms of financial performance, 2018 has remained another successful year for the bank. The bank posted a

record annual profit before tax (PBT) of PKR 1,110mln which is 19.21% higher than previous year. At close of 2018,

the total assets of the bank stood at PKR 122.76bln with an increase of 4% over last year. Mark-up income of the

bank increased by 4% from last year and closed at PKR 7,556mln. The strong topline earnings were backed by

healthy increase in earning assets of the bank. Gross Loans & advances portfolio was increased by 33% from last

year and closed at PKR 53,592mln. Deposits were also increased by 19% from last year. During the year

management’s focus remained on attracting low and no cost deposits and improved the overall mix. The current

account portfolio of the bank increased by 32% during the year. The bank has also managed to book a healthy

non mark-up income of PKR 767mln which is higher by 7% from last year.

In order to safeguard its assets against credit risk, the Bank has adopted a prudent approach and has charged

specific provision of PKR 239mln on both subjective and objective basis. In addition, the Bank has also charged a

general provision of PKR 33.45mln against its performing consumer loans. The Bank also managed to recover

PKR 289mln against the portfolio classified under non-performing status, demonstrating consistent and effective

remedial management.

With the introduction of new consumer products, performing various software upgrades & IT Infrastructure

security hardening and launching the Samba-Smart Mobile Banking application, the overall administrative cost of

the bank increased by only 12%.

New developments during the year

With the stabilization of Temenos-T24 and allied systems, SBL achieved another milestone in digital banking by

launching the Samba-Smart Mobile Banking application, providing features beyond traditional functionalities and

a few firsts for domestic market. Various software upgrades including integration of Oracle Financials with

Temenos-T24 and IT Infrastructure security hardening were performed in 2018. Samba Access and integrated

Cash Management solution was also introduced to facilitate banking needs of corporate and retail clients.

Projects for Digital Account on-boarding and ADC Switch & Cards System replacement through leveraging on new

technologies were also initiated during the year.

Considering the increased customer base and success of PIL initiative, the Auto Loan product was also launched

in 2018. Both these products would help in further strengthening the Retail Banking Group’s product offering to

its retail clientele.

Credit Rating

JCR-VIS, a premier credit rating agency, has reaffirmed SBL’s medium to long-term credit rating at AA (Double A)

and the short-term rating at A-1 (A-One). The outlook on the assigned ratings has also been regarded as ‘Stable’.

These short term and long term ratings of the Bank denote high credit quality with adequate protection factor

and strong capability for timely payments to all financial commitments owing to strong liquidity positions.

Statement of Internal Controls

The Board is pleased to endorse the management’s statement on the evaluation of internal controls which is

included in the annual report.

Risk Management Framework

Effective risk management is a prerequisite for achieving our business objectives and is thus a central part of the

Bank’s policies. To ensure that an effective risk management framework is implemented in the Bank, the Board of

Directors and senior management are actively involved in the formulation of policies, procedures and limits.

Accordingly, the Bank has a comprehensive risk management framework that establishes risk management

principles, guidelines and the governance structure. This framework defines the various committees established

Net mark-up / return / interest income after provisions 2,642 2,260

Non mark-up / interest income 767 715

Non mark-up / interest expenses 2,299 2,044

Profit before taxation 1,110 931

Taxation charge 427 192

Profit after taxation 683 739

Earnings per share – PKR 0.68 0.73

(Rupees in million)

20172018

18 19

to undertake effective risk monitoring by the Board of Directors and senior management, of the various types of

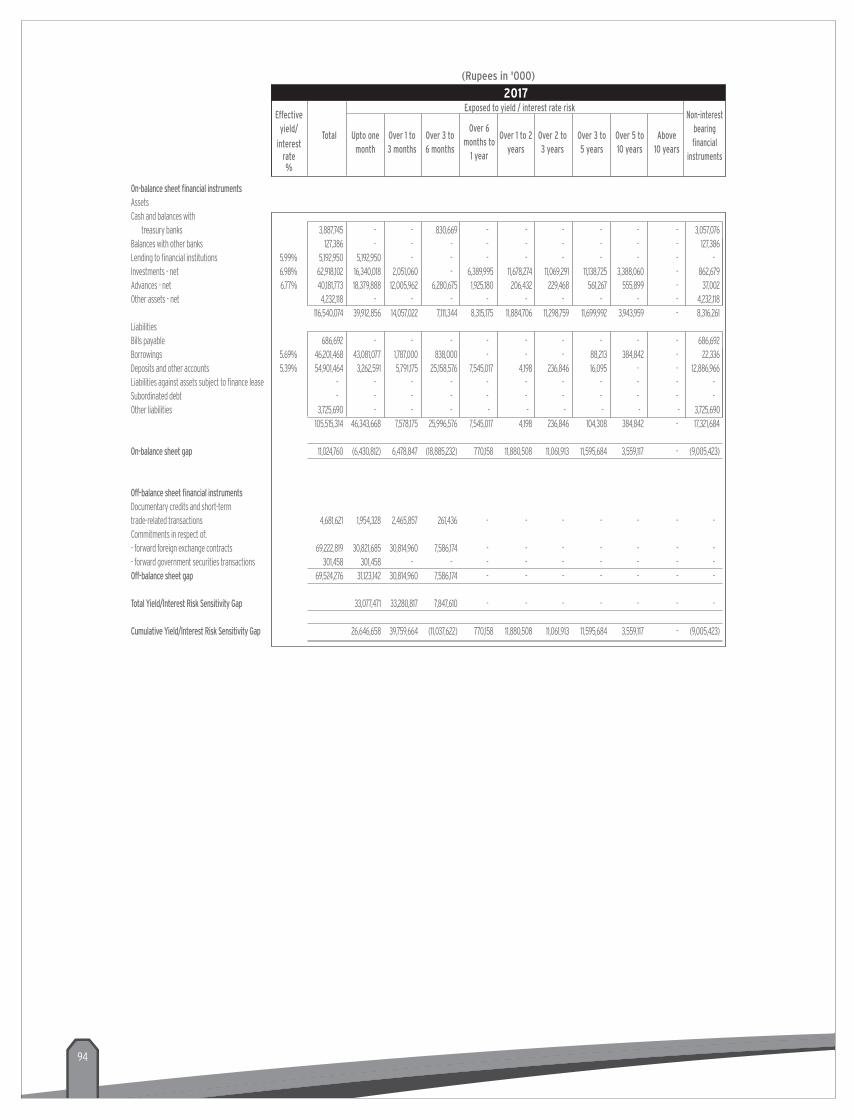

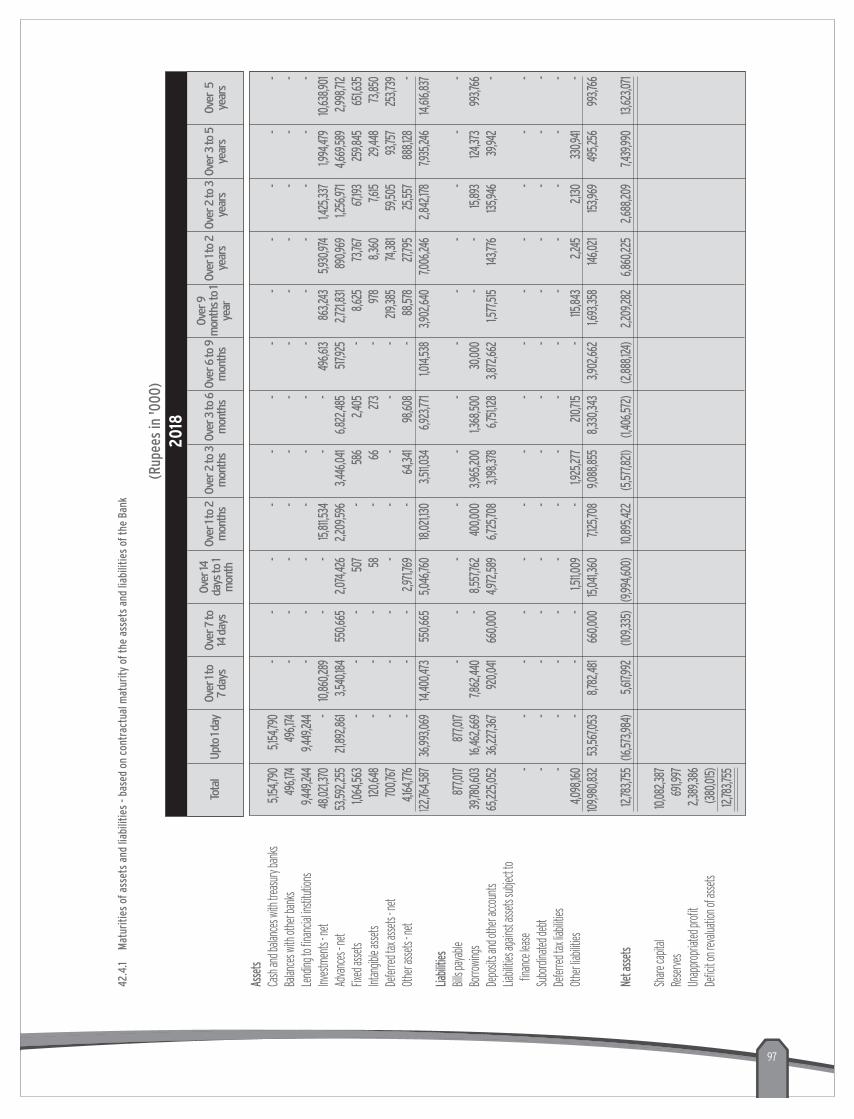

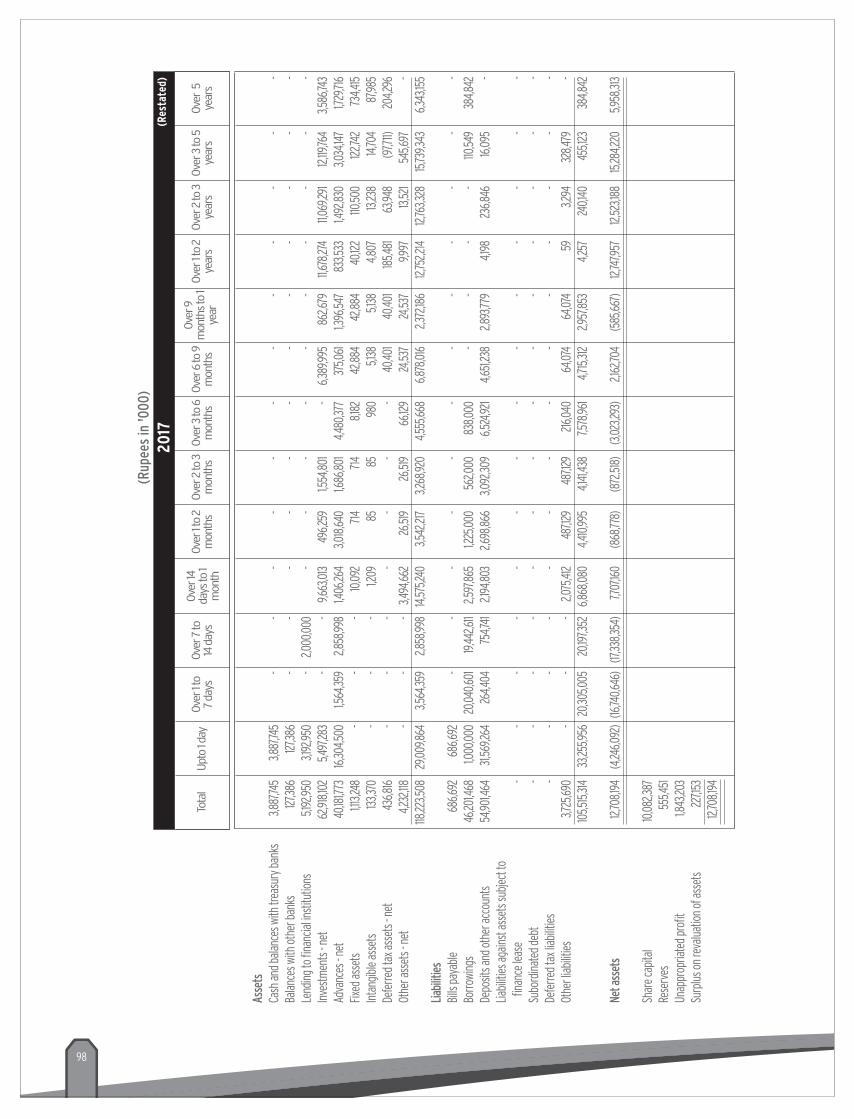

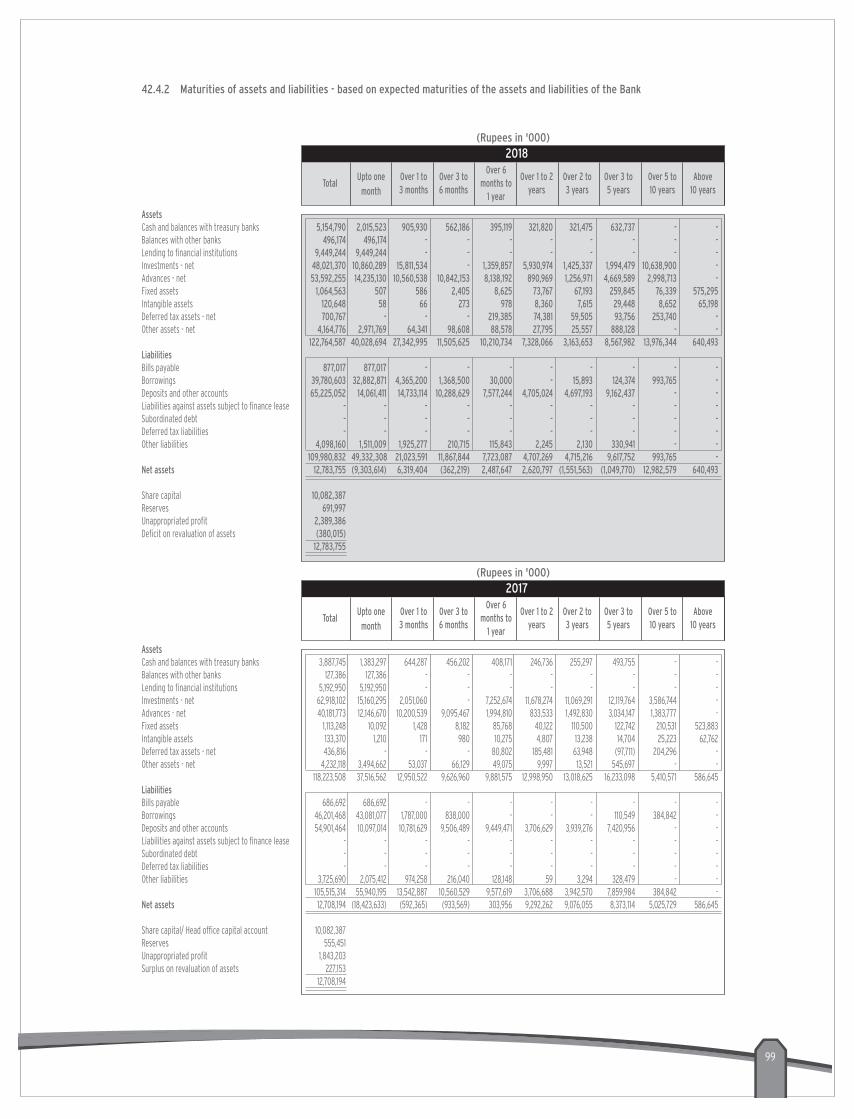

risks which include credit, market, operational and liquidity risks. These are discussed in more detail in note 42 to

the annexed financial statements.

Through the risk management framework, bank-wide risks are managed, with the objective of maximizing the

risk-adjusted returns while remaining within the risk parameters approved by the Board. The Bank’s risk

management framework is designed to balance corporate governance with well-defined independent risk

management principles. Refinements were continuously undertaken in the overall risk management governance

throughout 2018, based on the guiding principles established by the Board Risk Committee.

Statement under Code of Corporate Governance / Corporate and Financial Reporting Framework

The Board of Directors is aware of its responsibilities under the Code of Corporate Governance and is pleased to

report and certify that:

• The Bank is a subsidiary of SAMBA Financial Group of Saudi Arabia, which holds 84.51% shares of the Bank

as at December 31, 2018 (2017: 84.51%);

• Proper books of account of the Bank have been maintained;

• The financial statements prepared by the management of the Bank fairly present its state of affairs, result of

its operations, comprehensive income, cash flows, and changes in equity;

• Appropriate accounting policies have been consistently applied in the preparation of financial statements

except for changes in accounting policies disclosed in Note 5.1 of the annexed financial statements.

Accounting estimates are based on reasonable and prudent judgment;

• International Financial Reporting Standards, as applicable in Pakistan and adopted by the State Bank of

Pakistan, have been followed in preparation of the Bank’s financial statements, and departures, if any, have

been adequately disclosed;

• The system of internal controls is sound in design and has been effectively implemented and monitored on

best efforts basis;

• There are no doubts about the Bank’s ability to continue as a going concern;

• There has been no material departure from the best practices of corporate governance, as detailed in the

listing regulations;

• A summary of key operating & financial data for last 6 years is included in Annual Report;

• In order to strengthen the equity base for future expansion; the Bank has not declared dividend. Earnings Per

Share (EPS) for the year under review is PKR 0.68 (basic / diluted);

• A statement showing the Bank’s shareholding pattern as of December 31, 2018 is annexed;

• The book value of investments of Staff Provident Fund is PKR 238mln as per the audited financial statements for the period ended December 31, 2017;

• There are no statutory payments on account of taxes, duties, levies and charges which are outstanding as of December 31, 2018, except as disclosed in these financial statements;

• Statement of Compliance with Code of Corporate Governance is annexed;

• The financial statements of the Bank have been audited without qualification by auditors of the Bank, Messrs A.F. Ferguson & Company, Chartered Accountants;

• All the directors of the Bank, have completed their training program as per the requirements of the Code;

• Directors Fee is paid in line with Board & shareholders’ approval and the Bank is in the process of finalising a formal policy in this regard in accordance with the Companies Act, 2017 and the Code of Corporate Governance (CCG);

• In line with the requirements of the CCG, the Bank encourages representation of independent and non-executive directors, currently Board of Directors of the Bank comprise of four independent directors, four non-executive directors and one executive director. The Bank has eight males and one female director on its Board which evidence the gender diversity; and

• The Board evaluates its performance by the overall performance of the Bank. The Directors regularly attend the Board meetings and actively participate in the proceedings. The Board ensures that the Bank adopt the best practices of corporate governance in all areas of its operations and has a robust internal control system. The Board is fully cognizant of the Bank’s commitment to its sustainability strategy based on social, environmental factors and has issued appropriate policy guidelines to ensure continued performance in these areas.

Meetings of the Board

Four (4) Board meetings along with Eleven (11) Board Sub-Committee meetings were held during the period under review. The Board granted leave of absence to the Directors who did not attend the meetings. The number of meetings held and attended by each director is:

Number of meetings held 4 4 4 3 -

Number of meetings attended

Dr. Shujaat Nadeem 4 - - - -

Ms. Ranya Nashar 3 3 - 3 -

Mr. Antoine Mojabber 4 - 4 - -

Mr. Beji Tak-Tak 4 - 4 - -

Mr. Humayun Murad 4 4 - 3 -

Mr. Nadeem Babar 4 - - 3 -

Mr. Shahbaz Haider Agha 4 - 4 - -

Mr. Arjumand Ahmed Minai 4 4 - - -

Mr. Shahid Sattar 4 - 4 - -

BoardMeetings

Audit CommitteeMeetings

Risk CommitteeMeetings

Nomination &Remuneration

CommitteeMeetings

IT CommitteeMeetings

20 21

Share Acquisition by Directors and Executives

The Pattern of shareholding and additional information regarding pattern of shareholding is annexed separately.

During the year, no trade in the shares of the Bank was carried out by the Directors, CFO and Company Secretary

and their spouses and minor children, except, Mr. Shahid Sattar, who sold 133,500 shares, after meeting all

regulatory and disclosure requirements.

Corporate Social Responsibility

Corporate Social Responsibility (CSR) refers to a business practice that involves participating or taking initiatives

that benefits the social ecosystem in which an organization operates. When a business operates in an

environmentally, socially and economically responsible / transparent manner, it helps the organization succeed.

The Bank, being aware of its responsibilities toward the society as whole has taken initiatives to contribute

towards the society. A specific budget was allocated towards CSR and related activities in 2018 which was utilized

in form of contribution to some of the well-deserved organizations, engaged in philanthropic, education, health

and development activities for the betterment of the Pakistani Society at large. The details of donations /

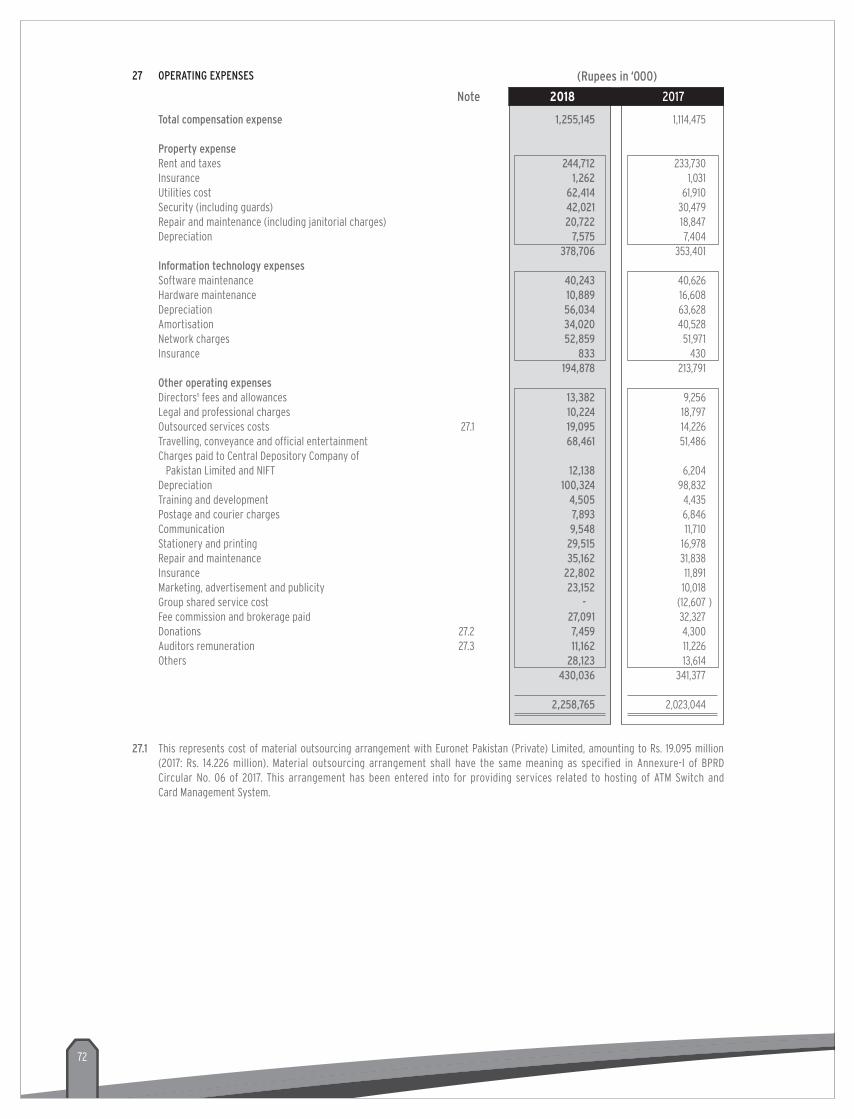

contributions made during the year have been disclosed in Note 27.2 of the annexed financial statements.

Auditors

The retiring external auditors Messrs A.F. Ferguson & Company, Chartered Accountants, being eligible, have

offered themselves for re-appointment. The Board of Directors, on the suggestion of the Audit Committee,

recommends Messrs A.F. Ferguson & Company, Chartered Accountants (a member firm of

PricewaterhouseCoopers) to be appointed for the next year.

Events after the Balance Sheet Date

There have been no material events that occurred subsequent to the date of the Balance Sheet that require

adjustments to the financial statements. Details of non-adjusting events after the reporting date have been

disclosed in Note 44 of the annexed financial statements.

Future Outlook

The stabilization measures taken during the last few months have put economy on the track of recovery. Monthly

indicators are showing visible signs of deceleration in domestic demand. The current account deficit is narrowing

gradually along with increase in financial inflows from friendly countries. Drop in crude oil prices in the last two

months is a major positive for the economy as it will lower the import bill in the coming quarters. Low oil prices

are not only positive from the external account perspective, but this will also help limit the impact on inflation and

interest rates. It is expected that government will capitalize on the opportunity provided by the low oil prices

environment to undertake long due key structural reforms. If done successfully, this would result in high &

self-sustaining economic growth and durable financial stability.

The economic conditions particularly for the banking industry will remain challenging during 2019 in Pakistan.

However, the management’s focus shall continue to rightly position itself in the market and will live up to maintain

the brand image of SAMBA as a symbol of customer confidence, loyalty and enhanced service quality.

With a view to the above forecasts, the Bank continues to foresee effective measures for its growth keeping its

core focus to leverage on the building blocks put into place; steadily build up its earning assets; effectively

manage the associated risks; and reduce its cost of funds through continued improvement in its deposit mix. This

would be facilitated by delivery of world class banking services to the Bank’s valued customers.

Acknowledgement

We wish to express sincere gratitude to our customers, business partners and shareholders for their patronage

and trust. The Board of Directors and the management would like to thank the State Bank of Pakistan and other

regulatory bodies for their guidance and support. We also sincerely appreciate the dedication, commitment and

team work of all employees of the Bank who worked very hard to transform the Bank into a successful franchise.

On behalf of the Board of Directors,

Shahid Sattar

President and Chief Executive Officer

February 20, 2019

Karachi

Arjumand Ahmed Minai

Director

22 23

24 25

26 27

28 29

2018 2017 2016 2015 2014 2013

Statement of Financial Position

Assets

Advances - gross 55,892 42,503 30,988 26,260 23,916 20,561

Investments - gross 48,139 62,936 57,272 44,828 20,055 14,104

Lending to financial institutions 9,449 5,193 5,277 2,000 1,900 791

Cash and balances with treasury and other banks 5,651 4,015 5,540 4,330 2,605 2,913

Fixed assets 1,065 1,113 1,290 1,269 759 839

Intangible assets 121 133 169 54 42 23

Deferred tax asset - net 701 437 410 658 1,058 1,484

Other assets - gross 4,338 4,406 4,562 3,118 2,567 1,810

Total assets - gross of provisions 125,355 120,736 105,507 82,517 52,903 42,525

Provision against advances - specific and general (2,300) (2,321) (2,198) (2,073) (2,104) (2,292)

Provision for diminution in the value of investments (118) (18) (35) (102) (102) (113)

Provision held against bad and doubtful other assets (173) (173) (175) (176) (115) (119)

Total assets - net of provisions 122,765 118,224 103,100 80,166 50,581 40,001

Liabilities

Customer deposits and other accounts 65,225 54,901 50,307 38,844 31,642 24,633

Borrowings 39,781 46,201 35,847 27,326 5,965 2,987

Bills payable 877 687 915 492 309 919

Other liabilities 4,098 3,726 3,711 1,660 1,411 1,331

Total liabilities 109,981 105,515 90,780 68,322 39,326 29,870

Net assets 12,784 12,708 12,320 11,844 11,255 10,131

Share capital 10,082 10,082 10,082 10,082 10,082 8,082

Advance against proposed issue of shares - - - - - 1,614

Reserves 692 555 408 299 213 167

Unappropriated profit / (accumulated losses) 2,389 1,843 1,252 816 472 291

Equity 13,164 12,481 11,743 11,198 10,767 10,154

(Deficit)/ surplus on revaluation of assets - net of tax (380) 227 577 647 488 (23)

12,784 12,708 12,320 11,844 11,255 10,131

Profit & Loss Account

Mark-up / return / interest earned 7,556 7,256 5,682 5,468 4,619 3,207

Mark-up / rerurn / interest expensed (4,847) (4,897) (3,576) (3,326) (2,806) (1,823)

Net mark-up / interest income 2,708 2,359 2,106 2,143 1,813 1,384

Fee, commission, brokerage and Income from dealing in foreign currencies 503 349 317 201 153 152

Dividend income and (loss) / gain on sales of securities - net 258 139 739 507 41 -

Other income and unrealised (loss) / gain on revaluation of investments 5 227 23 98 24 8

Non mark-up / interest income 767 715 1,079 805 217 160

Revenue 3,475 3,074 3,185 2,948 2,030 1,544

Non mark-up / interest expenses (2,297) (2,042) (1,993) (2,111) (1,646) (1,551)

(Charge) / reversal / recovery of provision / against write-offs (68) (101) (265) (22) 41 88

Profit / (Loss) before taxation 1,110 931 926 815 425 81

Taxation (427) (192) (382) (385) (199) 3

Profit / (Loss) after taxation 683 739 545 431 226 84

Other Information

Return on equity (RoE)* 5.4% 5.9% 4.4% 3.7% 2.1% 0.9%

Return on assets (RoA)* 0.6% 0.6% 0.6% 0.6% 0.5% 0.2%

Profit before tax to revenue ratio 31.9% 30.3% 29.1% 27.7% 20.9% 5.2%

Advances to deposits ratio (ADR) 82.2% 73.2% 57.2% 62.3% 68.9% 74.2%

Efficiency ratio (cost to revenue) 66.1% 66.5% 62.6% 71.6% 81.1% 100.4%

Earning Per Share (EPS) 0.68 0.73 0.54 0.43 0.24 0.10

Market value per share - rupees 8.04 6.96 7.26 6.00 7.00 4.72

Number of employees 837 747 680 657 602 614

Number of branches 37 37 37 34 28 28

* These ratios are based on average volume of respective years.

Six Years' Performance HighlightsRs. in Millions

Statement of Internal Controls

Management is responsible for establishing and maintaining adequate controls for providing reasonable

assurance on effective and efficient operations, internal financial controls and compliance with laws and

regulations. Furthermore, development of internal control systems is an ongoing process. Internal controls are

designed to manage, rather than eliminate, the risk of failure to achieve business objectives, and can only provide

reasonable, and not absolute, assurance against material misstatement or loss.

The responsibility for adherence to controls mainly lies with the business from where the risk arises. For

monitoring the effectiveness of internal control systems, the Bank has set roles for certain functions such as

Audit & Risk Review (ARR), Compliance and the Operations Risk Management Department (ORMD). ARR

periodically carries out audits of branches and departments to monitor compliance with the Bank's control and

processing standards, and regulatory requirements. Likewise, Compliance department is responsible for assisting

the senior management in managing effectively the regulatory compliance and Money Laundering & Terrorist

Financing risks faced by the Bank. Also, the ORMD function within the Risk Management Group carries out quality

assurance reviews of processes and transactions of branch banking operations, to ensure compliance of policies

and fulfillment of regulatory requirements. In order to institutionalize a robust control and risk management

culture, Key Risk Indicators (KRIs) for respective control areas have been identified along with tolerance limits.

Further, the Bank's KRI inventory is regularly updated to reflect latest trends with breaches being promptly

reported to senior management. Also, a Risk and Controls Self-Assessment (RCSA) regime has been implemented

throughout the Bank. An accountability process is in place to ensure effectiveness of the overall control

environment. Further, management gives due consideration to recommendations made by internal and external

auditors and regulators, especially for improvements in internal control systems and processes, and takes timely

action to implement their recommendations.

To implement Internal Control Guidelines, as required by State Bank of Pakistan, Internal Audit Department

reviewed the detailed exercise of documenting and benchmarking existing internal processes and controls,

relating to financial reporting on the basis of international standards. This project assists in further improving

internal controls across the Bank and ensures compliance with the SBP requirements. As per the SBP roadmap,

the Bank had completed all stages and is in compliance with SBP instructions and obtained exemption from the

State Bank of Pakistan for submission of Long Form Report (LFR) certified by external auditors. Bank has made

efforts to comply with the prerequisites of ICFR through submission of Internal Audit Annual Assessment Report

of 2017 to SBP after sign off from Board’s Audit Committee.

The Board of Directors is ultimately responsible for the internal control system and endorses the above evaluation

by management.

Shahid Sattar

President and Chief Executive Officer

February 20, 2019

Karachi

(Restated) (Restated)

30 31

Complaint Handling Mechanism

Samba Bank Limited (SBL) continued to place primary focus on providing its customers with world class banking

solutions with the objective of making its customer experience synonymous with “ease and convenience”.

As part of this effort, the Bank launched Samba Smart Application in 2018. This is a mobile banking application

which allows customers to transfer funds, pay bills and handle many other banking services from the comfort of

their mobile phones. Samba Smart Application can be used by both customers and non-customers and also

includes a Financial ChatBot which users can interact with to perform account related transactions.

The Bank also connected with Keenu network as part of its efforts to strengthen its digital payments solutions,

thus connecting us with its 50+ merchant network.

Samba Bank Limited updated its Financial Consumer Protection Framework in order to build the customer’s

confidence in our products and services. We aim to treat our customers fairly and equitably without any

discrimination in provision of banking services. The framework strives to create awareness about consumer rights

and obligations while using the banks product and services.

Complaint Summary

In 2017, the total complaints received were 1240 where the average resolution time was 4 working days.

Encouragingly, the year 2018 saw the Bank’s average complaints’ resolution turnaround fall to 3 working days

with 1632 complaints being logged.

Independent Auditor’s Review Report to The members on The Statement of Compliance with The Code of Corporate Governance

We have reviewed the enclosed Statement of Compliance with the Listed Companies (Code of Corporate

Governance) Regulations, 2017 (the Regulations) prepared by the Board of Directors of Samba Bank Limited (the

Bank) for the year ended December 31, 2018 in accordance with the requirements of regulation 40 of the

Regulations.

The responsibility for compliance with the Regulations is that of the Board of Directors of the Bank. Our

responsibility is to review whether the Statement of Compliance reflects the status of the Bank’s compliance with

the provisions of the Regulations and report if it does not and to highlight any non-compliance with the

requirements of the Regulations. A review is limited primarily to inquiries of the Bank’s personnel and review of

various documents prepared by the Bank to comply with the Regulations.

As a part of our audit of the financial statements we are required to obtain an understanding of the accounting

and internal control systems sufficient to plan the audit and develop an effective audit approach. We are not

required to consider whether the Board of Directors’ statement on internal control covers all risks and controls or

to form an opinion on the effectiveness of such internal controls, the Bank’s corporate governance procedures

and risks.

The Regulations require the Bank to place before the Audit Committee, and upon recommendation of the Audit

Committee, place before the Board of Directors for their review and approval, its related party transactions and

also ensure compliance with the requirements of section 208 of the Companies Act, 2017. We are only required

and have ensured compliance of this requirement to the extent of the approval of the related party transactions

by the Board of Directors upon recommendation of the Audit Committee. We have not carried out procedures to

assess and determine the Bank’s process for identification of related parties and that whether the related party

transactions were undertaken at arm’s length price or not.

Based on our review, nothing has come to our attention which causes us to believe that the Statement of

Compliance does not appropriately reflect the Bank's compliance, in all material respects, with the requirements

contained in the Regulations as applicable to the Bank for the year ended December 31, 2018.

A. F. Ferguson & Co.

Chartered Accountants

Dated: February 28, 2019

Karachi

32 33

Statement of Compliance with the Code of Corporate Governance For the Year Ended December 31, 2018Samba Bank Limited (the Bank) has complied with the requirements of the Listed Companies (Code of Corporate Governance) Regulations, 2017 (the Regulations) in the following manner:

1. The total number of directors are 9 as per the following:a. Male: 8b. Female: 1

2. The Composition of Board is as follows:

Category Names

Independent Directors Mr. Humayun Murad Mr. Nadeem Babar Mr. Shahbaz Haider Agha Mr. Arjumand Ahmed Minai

Executive Director Mr. Shahid Sattar [President and Chief Executive Officer (CEO)] Non-Executive Directors Dr. Shujaat Nadeem (Chairman) Mr. Antoine Mojabber Mr. Beji Tak-Tak Ms. Ranya Nashar

3. The directors have confirmed that none of them is serving as a director on more than five listed companies, including this Bank (excluding the listed subsidiaries of listed holding companies, where applicable).

4. The Bank has prepared a Code of Conduct and has ensured that appropriate steps have been taken to disseminate it throughout the Bank along with its supporting policies and procedures.

5. The Board has developed a vision / mission statement, overall corporate strategy and significant policies of the Bank. A complete record of particulars of significant policies along with the dates on which they were approved or amended has been maintained.

6. All the powers of the Board have been duly exercised and decisions on relevant matters have been taken by the Board / shareholders as empowered by the relevant provisions of the Companies Act, 2017 (the Act) and these Regulations.

7. The meetings of the Board were presided over by the Chairman and, in his absence, by a director elected by the Board for this purpose. The Board has complied with the requirements of the Act and the Regulations with respect to frequency, recording and circulating minutes of meeting of the Board.

8. The Board of directors have a formal policy and transparent procedures for remuneration of directors in accordance with the Act and these Regulations.

9. The Board has arranged Director’s training program for the following:

a. Dr. Shujaat Nadeemb. Mr. Antoine Mojabberc. Mr. Beji Tak-Takd. Ms. Ranya Nashare. Mr. Humayun Muradf. Mr. Nadeem Babar

g. Mr. Shahbaz Haider Aghah. Mr. Shahid Sattar

10. The Board has approved appointment of Chief Financial Officer (CFO), Company Secretary and Head of Internal Audit, including their remuneration and terms and conditions of employment and complied with relevant requirements of the Regulations.

11. CFO and CEO duly endorsed the financial statements before approval of the Board.

12. The Board has formed committees comprising of members given below:

a. Audit Committee(i) Mr. Humayun Murad (Chairman)(ii) Ms. Ranya Nashar (Member) (iii) Mr. Arjumand Ahmed Minai (Member)

b. Board Nomination and Remuneration Committee(i) Mr. Nadeem Babar (Chairman)(ii) Ms. Ranya Nashar (Member) (iii) Mr. Humayun Murad (Member)

c. Board Risk Management Committee(i) Mr. Beji Tak-Tak (Chairman)(ii) Mr. Shahid Sattar (Member)(iii) Mr. Antoine Mojabber (Member)(iv) Mr. Shahbaz Haider Agha (Member)

13. The terms of reference of the aforesaid committees have been formed, documented and advised to the committee for compliance.

14. The frequency of meetings of the aforesaid committees were as per following:

a. Audit Committee: 4 meetings were held during the financial year ended December 31, 2018

b. Board Nomination and Remuneration Committee: 3 meetings were held during the financial year ended December 31, 2018

c. Board Risk Management Committee: 4 meetings were held during the financial year ended December 31, 2018

15. The Board has set up an effective internal audit function within the Bank. The staff is suitably qualified and experienced for the purpose and is conversant with the policies and procedures of the Bank.

16. The statutory auditors of the Bank have confirmed that they have been given a satisfactory rating under the quality control review program of the Institute of Chartered Accountants of Pakistan (ICAP) and registered with Audit Oversight Board of Pakistan, that they or any of the partners of the firm, their spouses and minor children do not hold shares of the Bank and that the firm and all its Partners are in compliance with International Federation of Accountants (IFAC) guidelines on code of ethics as adopted by the ICAP.

17. The statutory auditors or the persons associated with them have not been appointed to provide other services except in accordance with the Act, these regulations or any other regulatory requirement and the auditors have confirmed that they have observed IFAC guidelines in this regard.

18. We confirm that all other requirements of the Regulations have been complied with.

Dr. Shujaat NadeemChairman

Dated: February 20, 2019

34 35

Notice of the Sixteenth Annual General MeetingNotice is hereby given that the Sixteenth Annual General Meeting of Samba Bank limited (“the Bank”) will be held at 10:00 a.m. on Wednesday, the March 27, 2019, at Hotel Serena, Islamabad, to transact the following business:

Ordinary Business

1. To confirm the minutes of the 15th Annual General Meeting held on March 27, 2018.

2. To receive, consider and adopt the Audited Annual Accounts of the Bank for the year ended December 31, 2018, together with the Reports of the Directors and Auditors thereon.

3. To appoint Auditors’ and to fix their remuneration. M/s A. F. Ferguson & Company, Chartered Accountants have offered themselves for a term ending at the conclusion of the next Annual General Meeting. The retiring Auditors, being eligible for reappointment.

4. To elect eight Directors of the Bank, as fixed by the Board under the provisions of section 159 of the Companies Act, 2017 for a period of 3 years commencing from March 27, 2019.

The names of the retiring Directors are:

I. Mr. Antoine Mojabber II. Mr. Arjumand Ahmed Minai III. Mr. Beji Tak-Tak IV. Mr. Humayun Murad V. Mr. Nadeem Babar VI. Ms. Ranya Nashar VII. Mr. Shahbaz Haider Agha VIII. Dr. Shujaat Nadeem

Any Other Business

To transact any other business of the Bank with the approval of the Chair.

By Order of the Board

March 06, 2019 Zia-ul-Husnain ShamsiKarachi Company Secretary

1. Share Transfer Books of the Bank will remain closed from 21-03-2019 to 27-03-2019 (both days inclusive). Transfer received in order at Bank’s Registrar, M/s. Famco Associates (Pvt.) Ltd., 8-F, Next to Hotel Faran, Nursery, Block-6, P.E.C.H.S., Shahra-e-Faisal, Karachi, upto close of business on 20-03-2019 will be considered in time for the purpose of Annual General Meeting.

2. Copies of the minutes of the Annual General Meeting dated March 27, 2018 are available for inspection by Members as required under section 152 of the Companies Act, 2017.

3. Any member desirous to contest the Election of Directors shall file the following with the Company Secretary of the Bank not later than fourteen days before the day of the above said meeting;

a) His/her intention to offer himself/herself for the election in terms of section 159 (3) of the Companies Act 2017, he/she should confirm that;

• He/she is not ineligible to become a director of the Bank under any applicable laws and regulations (including Listing Regulations of Pakistan Stock Exchange).

• Neither he/she nor his/her spouse is engaged in the business of brokerage or is a sponsor, director or officer of a corporate brokerage house.

• He/she is not serving as a director in more than five listed companies simultaneously. Provided that this l imit shall not include the directorships in the listed subsidiaries of a listed holding company.

b) Consent to act as director in Form 28 under Section 167 of the Companies Act 2017.

c) Affidavits, Annexure and Questionnaire in terms of State Bank of Pakistan's BPRD Circular No. 04 dated April 23, 2007, BPRD Circular No. 05 dated March 12, 2015, and BPRD Circular No. 09 dated October 18, 2018.

A copy of the relevant documents may be downloaded from the websites of the Securities & Exchange Commission of Pakistan and State Bank of Pakistan or may be obtained from the office of the Company Secretary of the Bank.

4. A Member entitled to attend and vote at the Annual General Meeting may appoint another Member as his/her proxy to attend and vote for him/her provided that a corporation may appoint as its proxy a person who is not a Member but is duly authorized by the corporation. Proxies must be received at the Registered Office of the Bank not less than 48 hours before the time of the holding of the Annual General Meeting.

5. CDC account holders will be required to follow the under mentioned guidelines as laid down in Circular No. 01 dated January 26, 2000, of the Securities and Exchange Commission of Pakistan for attending the meeting.

6. CDC shareholders, the account holder or sub-account holder whose registration details are uploaded as per the Central Depository Company of Pakistan Limited Regulations, shall authenticate his/her identity by showing his/her original Computerised National Identity Card (CNIC) or original passport at the time of attending the Annual General Meeting.

7. In the case of a corporate entity, the Board of Directors' resolution/power of attorney with specimen signature of the nominee shall be produced at the time of the Annual General Meeting (unless it has been provided earlier), to the Bank along with the proxy form.

8. Shareholders are requested to notify any change in their addresses to the Bank’s Shares Registrar, M/s. Famco Associates (Pvt.) Ltd., 8-F, Next to Hotel Faran, Nursery, Block-6, P.E.C.H.S., Shahra-e-Faisal, Karachi, immediately.

Circulation of Annual Audited Accounts via Email/CD/USB/DVD or Any Other Media

Pursuant to the directions given by the Securities and Exchange Commission of Pakistan through its SRO 787(1)/2014 dated September 8, 2014 and SRO 470(1)/2016 dated May 31, 2016 that have allowed the companies to circulate its Annual Audited Accounts (i.e. Annual Balance Sheet and Profit and Loss Accounts, Statements of Comprehensive Income, Cash Flow Statement, Notes to the Financial, Statements Auditor's and Director's Report) to its members through CD / DVD / USB / or any other Electronic Media at their registered Addresses.

Shareholders who wish to receive the hardcopy of Financial Statements shall have

to fill the standard request form (also available on the company's website www.samba.com.pk) and send us to the Company address.

Submission of CNIC (mandatory)

Pursuant to the directives of the SECP, CNIC/SNIC numbers of shareholder is MANDATORILY to be mentioned on dividend warrants. Shareholders are therefore, requested to submit a copy of their valid CNIC/SNIC (if not already provided) to the company’s Share Registrar, M/s. Famco Associates (Pvt.) Ltd., 8-F, Next to Hotel Faran, Nursery, Block-6, P.E.C.H.S., Shahra-e-Faisal, Karachi. In the absence of a member’s valid CNIC/SNIC, the Company will be constrained to withhold dispatch of dividend warrant to such members.

Notes:

Standard Request Form

38

Independent Auditor’s Report To The Members Of Samba Bank Limited

Report on the Audit of the Financial Statements

Opinion

We have audited the annexed financial statements of Samba Bank Limited (the Bank), which comprise the statement of financial position as at December 31, 2018, and the profit and loss account, the statement of comprehensive income, the statement of changes in equity and the cash flow statement for the year then ended, along with unaudited certified returns received from the branches except for 10 branches which have been audited by us and notes to the financial statements, including a summary of significant accounting policies and other explanatory information and we state that we have obtained all the information and explanations which, to the best of our knowledge and belief, were necessary for the purposes of the audit.

In our opinion and to the best of our information and according to the explanations given to us, the statement of financial position, profitand loss account, the statement of comprehensive income, statement of changes in equity and cash flow statement together with the notes forming part thereof conform with the accounting and reporting standards as applicable in Pakistan, and, give the information required by the Banking Companies Ordinance, 1962 and the Companies Act, 2017 (XIX of 2017), in the manner so required and respectively give a true and fair view of the state of the Bank’s affairs as at December 31, 2018 and of the profit and other comprehensive loss, the changes in equity and its cash flows for the year then ended.

Basis for Opinion

We conducted our audit in accordance with International Standards on Auditing (ISAs) as applicable in Pakistan. Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Bank in accordance with the International Ethics Standards Board for Accountants’ Code of Ethics for Professional Accountants as adopted by the Institute of Chartered Accountants of Pakistan (the Code) and we have fulfilled our other ethical responsibilities in accordance with the Code. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis forour opinion.

Key Audit Matters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the financial statements of the current period. These matters were addressed in the context of our audit of the financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

Following are the Key Audit Matters:

Provision against advances(Refer note 10 to the financial statements) The Bank makes provision against advances on a time based criteria that involves ensuring all non-performing loans and advances are classified in accordance with the ageing criteria specified in the Prudential Regulations (PRs) issued by the State Bank of Pakistan (SBP).

In addition to the above time based criteria the PRs require a subjective evaluation of the credit worthiness of borrowers to determine the classification of advances.

The PRs also require the creation of general provision for theconsumer portfolio.

The Bank has recognized a net reversal of provision against advances amounting to Rs. 17.408 million in the profit and loss account in the current year. As at December 31, 2018, the Bank holds a provision of Rs 2,299.525 million against advances.

The determination of provision against advances based on the above criteria remains a significant area of judgement and estimation. Because of the significance of the impact of these judgements / estimations and the materiality of advances relative to the overall statement of financial position of the Bank, we

Our audit procedures to verify provision against advances, amongst others, included the following:

We reviewed the design and tested the operating effectiveness of key controls established by the Bank to identify loss events and for determining the extent of provisioning required against non-performing loans.

The testing of controls included testing of:

• controls over monitoring of advances with higher risk of default and correct classification of non-performing advances on subjective criteria;

• controls over accurate computation and recording of provisions; and

• controls over the governance and approval process related to provisions, including continuous reassessment by the management.

In accordance with the regulatory requirement, we sampled and tested at least sixty percent of the total advances portfolio and

1

S.No. Key Audit Matters How the matter was addressed in our audit

39

Information Other than the Financial Statements and Auditor’s Report Thereon

Management is responsible for the other information. The other information comprises the information included in the Annual Report, but does not include the financial statements and our auditor’s report thereon.

Our opinion on the financial statements does not cover the other information and we do not express any form of assuranceconclusion thereon.

In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

considered the area of provision against advances as a key audit matter.

Change in format of the financial statements(Refer note 5.1.1 to the financial statements)

The State Bank of Pakistan (SBP) has amended the format of annual financial statements of banks. All banks are directed to prepare their annual financial statements on the revised format effective from the accounting year ending December 31, 2018. Accordingly, the Bank has prepared these financial statements on the new format prescribed by the SBP.

As part of this transition to the new requirements, the management performed a gap analysis to identify differences between the previous and current format. The adoption of new format required certain recognition requirements, reclassification of comparative information and also introduced additional disclosure requirements.

In view of the significant impact of the first time adoption of the revised format on these financial statements, we considered this as a key audit matter.

performed the following substantive procedures for sample loan accounts:

• verified repayments of loan / mark-up installments and checked that non-performing loans have been correctly classified and categorized based on the number of days overdue.

• examined watch list accounts and, based on review of the individual facts and circumstances, discussions with management and our assessment of financial conditions of the borrowers, formed a judgement as to whether classification of these accounts as performing was appropriate.

We checked the accuracy of specific provision made against non-performing advances and of general provision made against consumer finance by recomputing the provision amount in accordance with the criteria prescribed under the PRs.

We reviewed and understood the requirements of the SBP’s amended format of annual financial statements for banks. Our audit procedures included the following:

• considered the management’s process to identify the changes required in the financial statements to comply with the new format; and

• obtained relevant underlying supports relating to changes required in the financial statements consequent to the adoption of the new format to assess their appropriateness and verified them on a test basis.

2

S.No. Key Audit Matters How the matter was addressed in our audit

Responsibilities of Management and the Board of Directors for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with accounting and reporting standards as applicable in Pakistan, the requirements of Banking Companies Ordinance, 1962 and the Companies Act, 2017 (XIX of 2017) and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Bank’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Bank or to cease operations, or has no realistic alternative but to do so.

The Board of directors is responsible for overseeing the Bank’s financial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs as applicable in Pakistan will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with ISAs as applicable in Pakistan, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Bank’s internal control. • Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management. • Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Bank’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Bank to cease to continue as a going concern.

• Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

We communicate with the Board of Directors regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

We also provide to the Board of Directors with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

From the matters communicated with the Board of Directors, we determine those matters that were of most significance in the audit of the financial statements of the current period and are therefore the key audit matters. We describe these matters in our auditor’s report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication.

40

41

Report on Other Legal and Regulatory Requirements

Based on our audit, we further report that in our opinion:

a) proper books of account have been kept by the Bank as required by the Companies Act, 2017 (XIX of 2017) and the returns referred above from the branches have been found adequate for the purpose of our audit;

b) the statement of financial position, the profit and loss account, the statement of comprehensive income, statement of changes in equity and cash flow statement together with the notes thereon have been drawn up in conformity with the Banking Companies Ordinance, 1962 and the Companies Act, 2017 (XIX of 2017) and are in agreement with the books of account and returns;

c) investments made, expenditure incurred and guarantees extended during the year were in accordance with the objects and powers of the Bank and the transactions of the Bank which have come to our notice have been within the powers of the Bank; and

d) zakat deductible at source under the Zakat and Ushr Ordinance, 1980 (XVIII of 1980), was deducted by the Bank and deposited in the Central Zakat Fund established under section 7 of that Ordinance.

2. We confirm that for the purpose of our audit we have covered more than sixty per cent of the total loans and advances of the Bank.

The engagement partner on the audit resulting in this independent auditor’s report is Shahbaz Akbar.

A. F. Ferguson & Co.Chartered AccountantsDated: February 28, 2019Karachi

42

Statement of Financial PositionAS AT DECEMBER 31, 2018

(Rupees in ‘000)

(Restated) (Restated)

2017 20162018Note

ASSETS

Cash and balances with treasury banks 6 5,154,790 3,887,745

Balances with other banks 7 496,174 127,386

Lendings to financial institutions 8 9,449,244 5,192,950

Investments - net 9 48,021,370 62,918,102

Advances - net 10 53,592,255 40,181,773

Fixed assets 11 1,064,563 1,113,248

Intangible assets 12 120,648 133,370

Deferred tax assets - net 13 700,767 436,816

Other assets - net 14 4,164,776 4,232,118

122,764,587 118,223,508

LIABILITIES

Bills payable 15 877,017 686,692

Borrowings 16 39,780,603 46,201,468

Deposits and other accounts 17 65,225,052 54,901,464

Liabilities against assets subject to finance lease - - - -

Subordinated debt - - - -

Deferred tax liabilities - - - -

Other liabilities 18 4,098,160 3,725,690

109,980,832 105,515,314

NET ASSETS 12,783,755 12,708,194

REPRESENTED BY:

Share capital 19 10,082,387 10,082,387

Reserves 691,997 555,451

(Deficit) / surplus on revaluation of assets 20 (380,015 ) 227,153

Unappropriated profit 2,389,386 1,843,203

12,783,755 12,708,194

CONTINGENCIES AND COMMITMENTS 21

The annexed notes 1 to 45 and Annexures I and II form an integral part of these financial statements.

Chief Financial Officer President & Chief Executive Officer Chairman Director Director

4,723,664

816,421

5,277,254

57,237,456

28,789,980

1,290,007

168,708

409,641

4,386,604

103,099,735

915,076

35,847,072

50,306,804

- -

- -

- -

3,711,259

90,780,211

12,319,524

10,082,387

407,680

577,336

1,252,121

12,319,524

43

Profit and Loss AccountFOR THE YEAR ENDED DECEMBER 31, 2018

(Rupees in ‘000)

20172018Note

Mark-up / return / interest earned 22 7,555,595 7,256,121 Mark-up / return / interest expensed 23 4,847,164 4,896,833 Net mark-up / return / interest income 2,708,431 2,359,288

Non mark-up / interest income Fee and commission income 24 265,594 210,616 Dividend income 45,332 44,661 Foreign exchange income 237,464 138,260 Gain on securities 25 214,586 94,258 Other income 26 3,743 227,351 Total non mark-up / interest income 766,719 715,146 Total income 3,475,150 3,074,434

Non mark-up / interest expenses Operating expenses 27 2,258,765 2,023,044 Workers' Welfare Fund 28 23,024 19,014 Other charges 29 15,278 36 Total non mark-up / interest expenses 2,297,067 2,042,094 Profit before provisions 1,178,083 1,032,340 Provisions and write offs - net 30 (68,364 ) (101,412 )Extra ordinary / unusual items - - -

Profit before taxation 1,109,719 930,928 Taxation 31 (426,990 ) (192,075)

Profit after taxation 682,729 738,853 (Rupees)

Earnings per share - basic and diluted 32 0.68 0.73

The annexed notes 1 to 45 and Annexures I and II form an integral part of these financial statements.

Chief Financial Officer President & Chief Executive Officer Chairman Director Director

(Restated)

44