rush university medical center obligated group for … financial report and... · rush university...

TRANSCRIPT

TABLE OF CONTENTS (continued)

Page

This - i -

4832-1469-4177.4 4832-1469-4177.8

Rush University Medical Center Obligated Group Annual Report For Fiscal Year Ended June 30, 2016 Audited

TABLE OF CONTENTS

Page

- i -

CAUTIONARY STATEMENTS REGARDING FORWARD-LOOKING INFORMATION IN THIS ANNUAL REPORT .. 3

PURPOSE OF THE ANNUAL REPORT ................................................................................................................................... 3

OFFICER’S CERTIFICATE ....................................................................................................................................................... 4

OBLIGATED PERSONS ............................................................................................................................................................ 5 Selected Financial Results and Other Information ........................................................................................................ 6 Financial Ratios ............................................................................................................................................................. 7

OVERVIEW OF THE OBLIGATED GROUP ........................................................................................................................... 8 Obligated Group ............................................................................................................................................................ 8 Presentation of Financial Information ......................................................................................................................... 10

RUSH UNIVERSITY MEDICAL CENTER ............................................................................................................................ 11 Mission ........................................................................................................................................................................ 11 Changes in Management ............................................................................................................................................. 11 Service Area and Competition ..................................................................................................................................... 11 Rush University ........................................................................................................................................................... 11 Physician Alignment ................................................................................................................................................... 13

RUSH-COPLEY MEDICAL CENTER .................................................................................................................................... 14 Service Area and Competition ..................................................................................................................................... 15 Physician Alignment ................................................................................................................................................... 15 Awards ........................................................................................................................................................................ 15

RUSH OAK PARK HOSPITAL ............................................................................................................................................... 17 Service Area and Competition ..................................................................................................................................... 17 Physician Alignment ................................................................................................................................................... 17 Awards ........................................................................................................................................................................ 17

SUMMARY OF HISTORICAL UTILIZATION AND FINANCIAL INFORMATION ......................................................... 19 Historical Utilization of Services ................................................................................................................................ 19 Summary of Revenues and Expenses .......................................................................................................................... 19 Operating Results ........................................................................................................................................................ 20 Liquidity ...................................................................................................................................................................... 20 Capitalization ............................................................................................................................................................... 21 Sources of Revenue ..................................................................................................................................................... 21 Debt Service Coverage ................................................................................................................................................ 21 Recent Financial Performance – Fiscal Years Ended June 30, 2016 and 2015 .......................................................... 22 Capital Expenditures ................................................................................................................................................... 25

MISCELLANEOUS .................................................................................................................................................................. 25 Ratings ......................................................................................................................................................................... 25 Community Benefits .................................................................................................................................................... 26 Pension Plans ............................................................................................................................................................... 26 Contingencies .............................................................................................................................................................. 27 Investment Policies ...................................................................................................................................................... 27 Fair Value Measurements ............................................................................................................................................ 28 Endowment Investment and Spending Policies ........................................................................................................... 32 Interest Rate Swap Agreements ................................................................................................................................... 32 Affiliations, Merger, Acquisition and Divestiture ....................................................................................................... 33 Information Technology .............................................................................................................................................. 33 Campus Transformation .............................................................................................................................................. 34 Recent Transactions..................................................................................................................................................... 34 Subsequent Events ....................................................................................................................................................... 34

CONSOLIDATED FINANCIAL STATEMENTS ................................................................................................................... 35

TABLE OF CONTENTS (continued)

Page

- ii -

Consolidated Balance Sheets ....................................................................................................................................... 36 Consolidated Statements of Operations and Changes in Net Assets ........................................................................... 37 Consolidated Statements of Operations and Changes in Net Assets ........................................................................... 38 Consolidated Statements of Cash Flows...................................................................................................................... 39

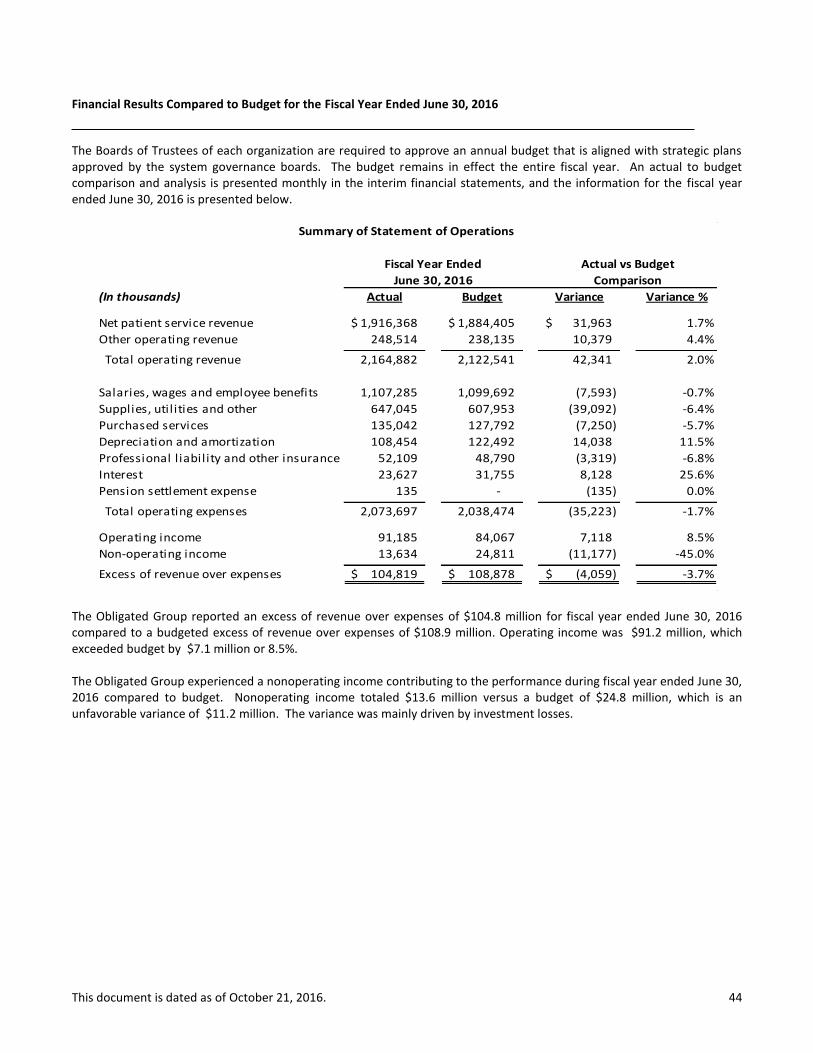

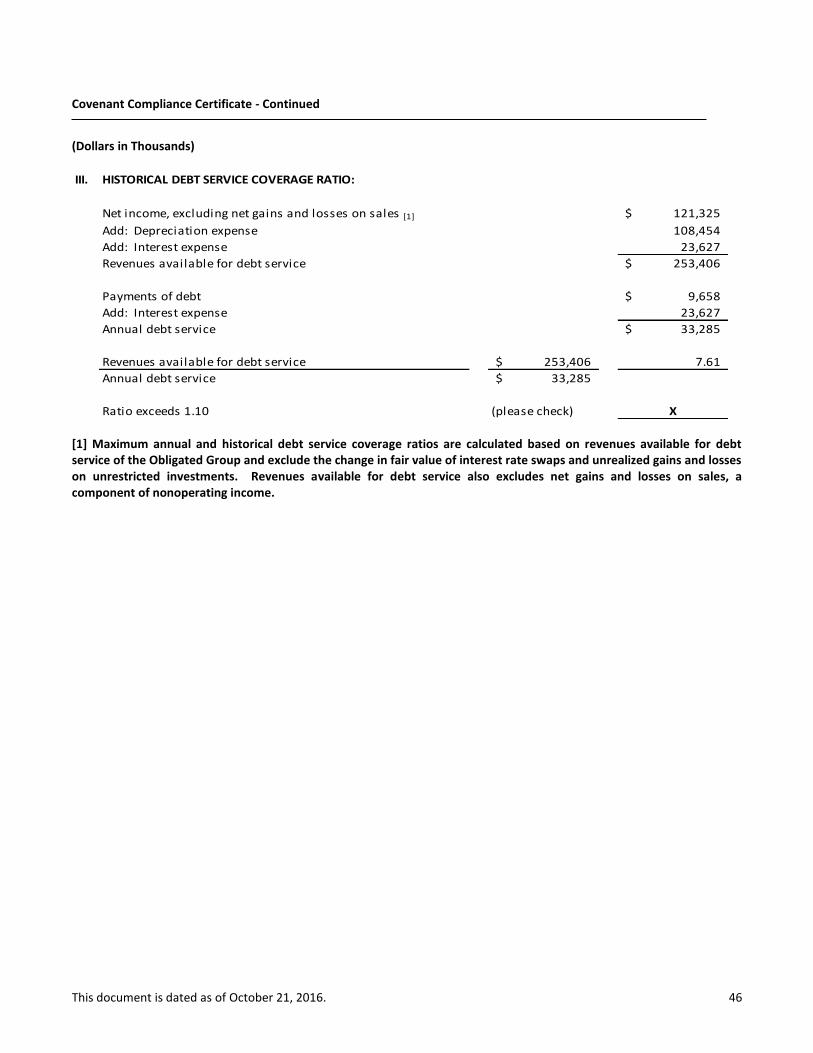

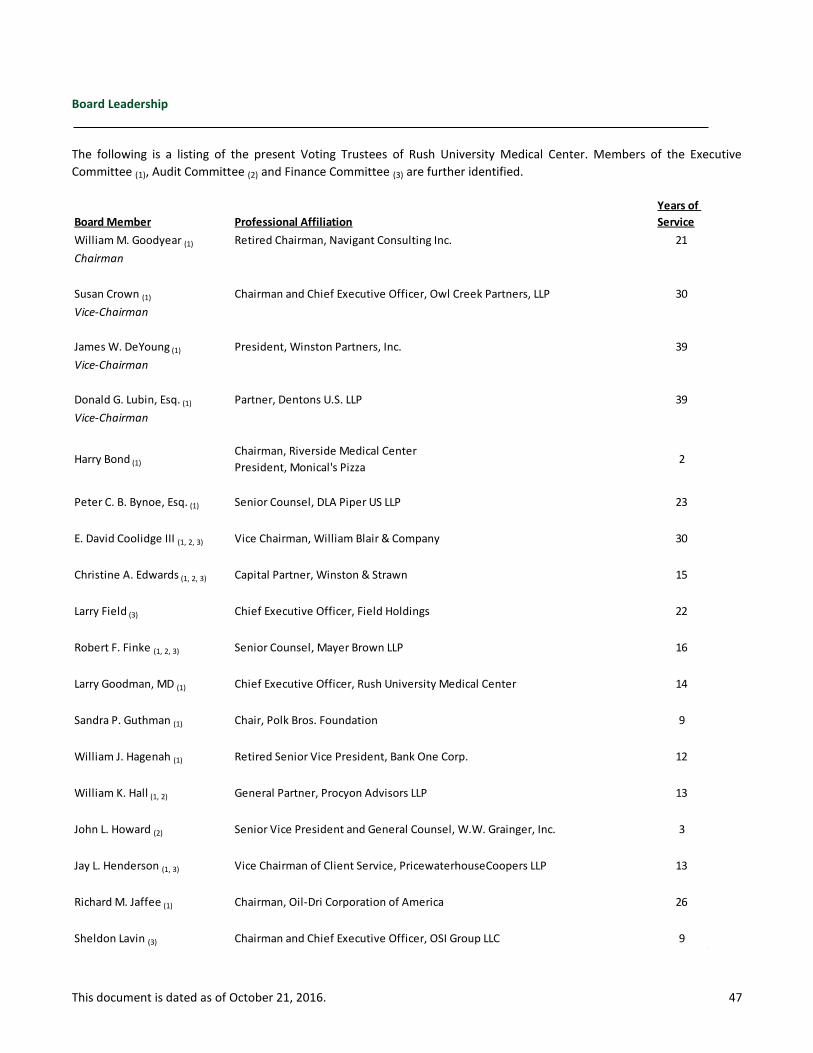

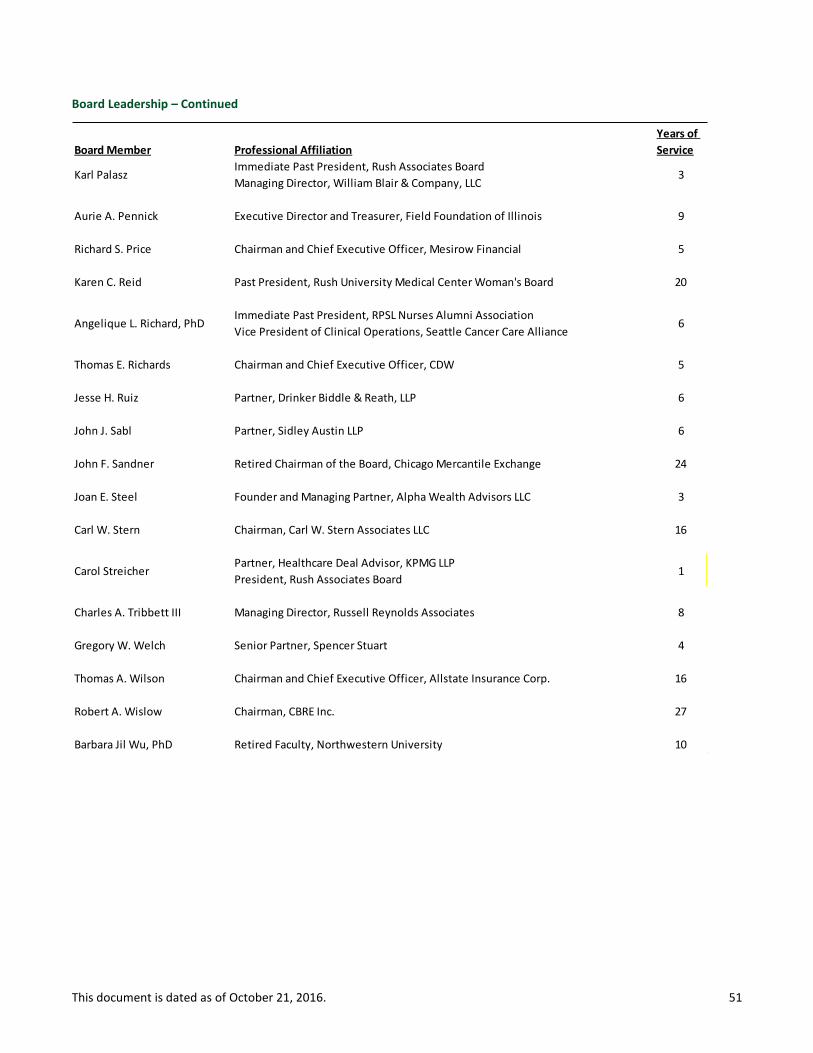

APPENDICES ........................................................................................................................................................................... 40 Consolidating Balance Sheet Information ................................................................................................................... 41 Consolidating Statement of Operations and Changes in Net Assets Information ....................................................... 42 Consolidating Statement of Operations and Changes in Net Assets Information ....................................................... 43 Financial Results Compared to Budget for the Fiscal Year Ended June 30, 2016 ...................................................... 44 Covenant Compliance Certificate ................................................................................................................................ 45 Board Leadership ........................................................................................................................................................ 47

This document is dated as of October 21, 2016. 3

CAUTIONARY STATEMENTS REGARDING FORWARD-LOOKING INFORMATION IN THIS ANNUAL REPORT

Certain statements included or incorporated by reference in this Annual Report constitute “forward-looking

statements.” Such statements are generally identifiable by the terminology used such as “plan,” “expect,” “estimate,” “budget,” or other similar words.

THE ACHIEVEMENT OF CERTAIN RESULTS OR OTHER EXPECTATIONS CONTAINED IN SUCH FORWARD-LOOKING STATEMENTS INVOLVES KNOWN AND UNKNOWN RISKS, UNCERTAINTIES AND OTHER FACTORS WHICH MAY CAUSE ACTUAL RESULTS, PERFORMANCE OR ACHIEVEMENTS DESCRIBED TO BE MATERIALLY DIFFERENT FROM ANY FUTURE RESULTS, PERFORMANCE OR ACHIEVEMENTS EXPRESSED OR IMPLIED BY SUCH FORWARD-LOOKING STATEMENTS. THE OBLIGATED GROUP DOES NOT PLAN TO ISSUE ANY UPDATES OR REVISIONS TO THOSE FORWARD-LOOKING STATEMENTS IF OR WHEN THE EXPECTATIONS, OR EVENTS, CONDITIONS OR CIRCUMSTANCES ON WHICH SUCH STATEMENTS ARE BASED OCCUR.

PURPOSE OF THE ANNUAL REPORT

The purpose of this Annual Report is to present the Rush University Medical Center Obligated Group’s (the Obligated Group consisting of Rush University Medical Center, Rush Oak Park Hospital, Copley Memorial Hospital, Rush-Copley Medical Center, Rush-Copley Foundation, Copley Ventures and Rush-Copley Medical Group) for fiscal years ended June 30, 2016 and 2015, and management’s discussion and analysis of the Obligated Group’s financial condition and results of operations for the fiscal year ended June 30, 2016. This report also provides insights on the quality of earnings reported, significant balance sheet assumptions used and any changes in assumptions used, risks to the balance sheet and statement of operations, and the impact of anticipated future events. This report includes the consolidated activities and results of Rush University Medical Center and Rush-Copley Medical Center, including all subsidiaries, collectively “Rush” or the “Obligated Group.” Rush University Medical Center also controls and operates Rush Oak Park Hospital. The primary activities and results of the Obligated Group include the hospitals, Rush University education and research activities, Rush University Medical Group (RUMG), RUMC’s faculty practice plans, and other physician practice activity as well as other operating activities.

This document is dated as of October 21, 2016. 4

OFFICER’S CERTIFICATE The undersigned duly appointed and acting Senior Vice President and Chief Financial Officer of Rush University Medical Center, as the Group Representative pursuant to the Master Continuing Disclosure Agreement dated as of February 1, 2015 (First Supplemental and Amended and Restated Master Trust Indenture) between the Group Representative and Digital Assurance Certification, L.L.C., as Dissemination Agent (Dissemination Agent), hereby certifies as follows:

1. Definitions. Capitalized terms used but not defined herein shall have the meanings ascribed thereto in the Master Continuing Disclosure Agreement.

2. Annual Report. Accompanying this Annual Report Certificate is the Annual Report for fiscal year ended June 30,

2016.

3. Compliance with Master Continuing Disclosure Agreement. The Annual Report is being delivered to the Dissemination Agent herewith not later than the sixtieth (120

th) day following the end of such fiscal year which is

the applicable Annual Report Date for purposes of such Annual Report. The Annual Report contains, or includes by reference, the Financial Information and Operating Data required by the Master Continuing Disclosure Agreement. The Financial Information and Operating Data include information with respect to the Obligated Persons identified in Schedule 1 hereto, and such Obligated Persons constitute all of the Obligated Persons with respect to the Related Bonds for the fiscal year covered by the Annual Report. To the extent any information is included in the Annual Report by reference, any document so referred to has been previously provided to the Repositories or filed with the SEC or, in the case of a reference to a Final Official Statement, has been filed with the MSRB.

Such Financial Information and Operating Data have been prepared on the same basis as the most recently prepared Audited Financial Statements.

IN WITNESS WHEREOF the undersigned has executed and delivered this Annual Report Certificate to the Dissemination Agent, which has received such certificate and the Annual Report, all as of the 21st day of October, 2016. RUSH UNIVERSITY MEDICAL CENTER

As Group Representative

By:

John P. Mordach

Its: Senior Vice President and Chief Financial Officer Acknowledgment of Receipt: Digital Assurance Certification (DAC) As Dissemination Agent

By: Shana Blanchard Its: Assistant Client Service Manager Director

This document is dated as of October 21, 2016. 5

OBLIGATED PERSONS

1. Rush University Medical Center (the Medical Center)

2. Rush Oak Park Hospital (ROPH)

3. Copley Memorial Hospital, Inc. (Copley or CMH)

4. Rush-Copley Medical Center, Inc. (Rush-Copley or RCMC)

5. Rush-Copley Foundation (Copley Foundation) 6. Copley Ventures, Inc. (Copley Ventures)

7. Rush-Copley Medical Group NFP (the Medical Group)

This document is dated as of October 21, 2016. 6

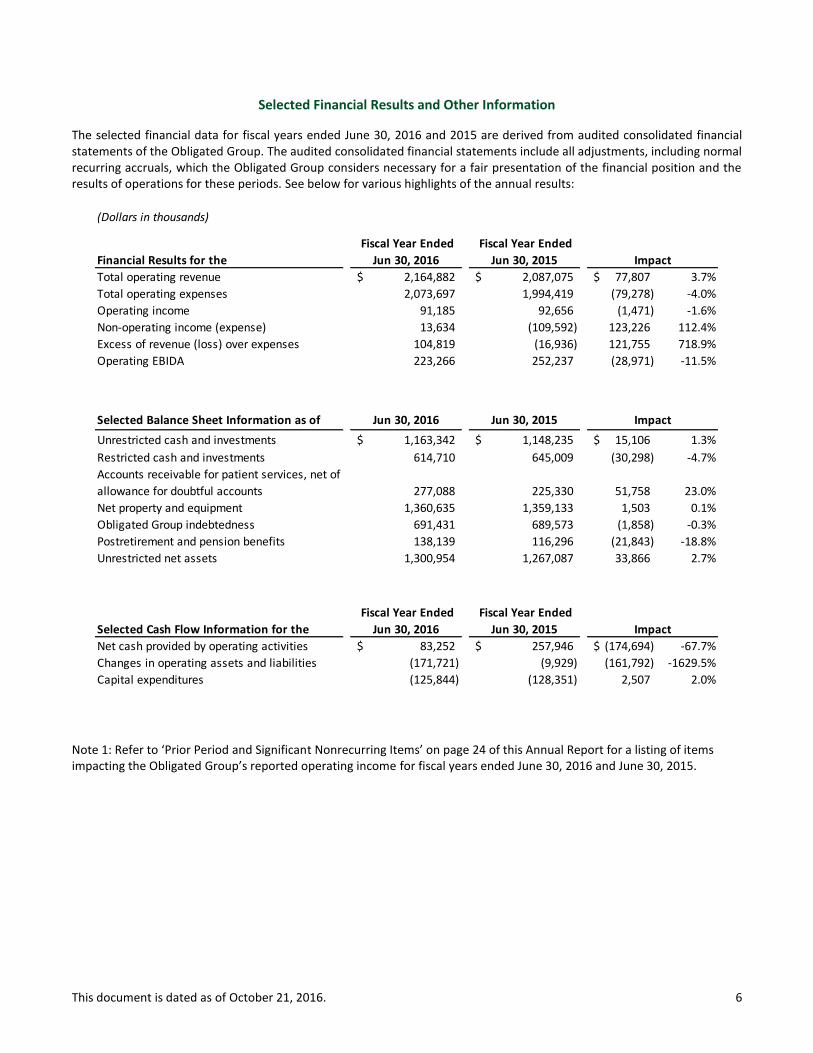

Selected Financial Results and Other Information

The selected financial data for fiscal years ended June 30, 2016 and 2015 are derived from audited consolidated financial statements of the Obligated Group. The audited consolidated financial statements include all adjustments, including normal recurring accruals, which the Obligated Group considers necessary for a fair presentation of the financial position and the results of operations for these periods. See below for various highlights of the annual results:

Note 1: Refer to ‘Prior Period and Significant Nonrecurring Items’ on page 24 of this Annual Report for a listing of items impacting the Obligated Group’s reported operating income for fiscal years ended June 30, 2016 and June 30, 2015.

(Dollars in thousands)

Financial Results for the

Fiscal Year Ended

Jun 30, 2016

Fiscal Year Ended

Jun 30, 2015

Total operating revenue 2,164,882$ 2,087,075$ 77,807$ 3.7%

Total operating expenses 2,073,697 1,994,419 (79,278) -4.0%

Operating income 91,185 92,656 (1,471) -1.6%

Non-operating income (expense) 13,634 (109,592) 123,226 112.4%

Excess of revenue (loss) over expenses 104,819 (16,936) 121,755 718.9%

Operating EBIDA 223,266 252,237 (28,971) -11.5%

Selected Balance Sheet Information as of Jun 30, 2016 Jun 30, 2015

Unrestricted cash and investments 1,163,342$ 1,148,235$ 15,106$ 1.3%

Restricted cash and investments 614,710 645,009 (30,298) -4.7%

Accounts receivable for patient services, net of

allowance for doubtful accounts 277,088 225,330 51,758 23.0%

Net property and equipment 1,360,635 1,359,133 1,503 0.1%

Obligated Group indebtedness 691,431 689,573 (1,858) -0.3%

Postretirement and pension benefits 138,139 116,296 (21,843) -18.8%

Unrestricted net assets 1,300,954 1,267,087 33,866 2.7%

Selected Cash Flow Information for the

Fiscal Year Ended

Jun 30, 2016

Fiscal Year Ended

Jun 30, 2015

Net cash provided by operating activities 83,252$ 257,946$ (174,694)$ -67.7%

Changes in operating assets and liabilities (171,721) (9,929) (161,792) -1629.5%

Capital expenditures (125,844) (128,351) 2,507 2.0%

Impact

Impact

Impact

This document is dated as of October 21, 2016. 7

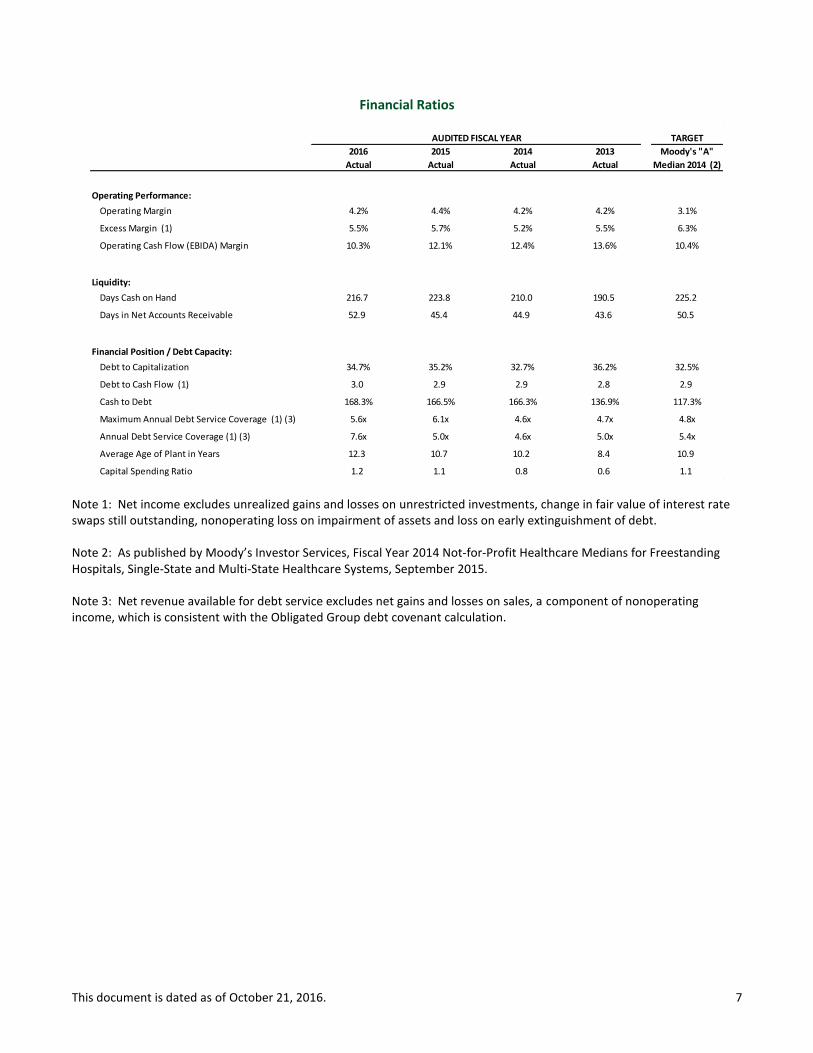

Financial Ratios

Note 1: Net income excludes unrealized gains and losses on unrestricted investments, change in fair value of interest rate swaps still outstanding, nonoperating loss on impairment of assets and loss on early extinguishment of debt.

Note 2: As published by Moody’s Investor Services, Fiscal Year 2014 Not-for-Profit Healthcare Medians for Freestanding Hospitals, Single-State and Multi-State Healthcare Systems, September 2015.

Note 3: Net revenue available for debt service excludes net gains and losses on sales, a component of nonoperating income, which is consistent with the Obligated Group debt covenant calculation.

TARGET

2016 2015 2014 2013 Moody's "A"

Actual Actual Actual Actual Median 2014 (2)

Operating Performance:

Operating Margin 4.2% 4.4% 4.2% 4.2% 3.1%

Excess Margin (1) 5.5% 5.7% 5.2% 5.5% 6.3%

Operating Cash Flow (EBIDA) Margin 10.3% 12.1% 12.4% 13.6% 10.4%

Liquidity:

Days Cash on Hand 216.7 223.8 210.0 190.5 225.2

Days in Net Accounts Receivable 52.9 45.4 44.9 43.6 50.5

Financial Position / Debt Capacity:

Debt to Capitalization 34.7% 35.2% 32.7% 36.2% 32.5%

Debt to Cash Flow (1) 3.0 2.9 2.9 2.8 2.9

Cash to Debt 168.3% 166.5% 166.3% 136.9% 117.3%

Maximum Annual Debt Service Coverage (1) (3) 5.6x 6.1x 4.6x 4.7x 4.8x

Annual Debt Service Coverage (1) (3) 7.6x 5.0x 4.6x 5.0x 5.4x

Average Age of Plant in Years 12.3 10.7 10.2 8.4 10.9

Capital Spending Ratio 1.2 1.1 0.8 0.6 1.1

AUDITED FISCAL YEAR

This document is dated as of October 21, 2016. 8

OVERVIEW OF THE OBLIGATED GROUP

This annual report contains information concerning the Rush University Medical Center Obligated Group, which is part of a multi-hospital system (the “System”) with operations that are linked by the common mission of patient care, education and research.

The largest member of the System is Rush University Medical Center (“RUMC” or the “Medical Center”). RUMC sees unique advantages in having a single management team and governing board that oversees inpatient and outpatient clinical operations, bench and clinical trials research, employed and affiliated physician oversight and university affairs. This integrated structure enhances the ability of RUMC to align these various functions in a patient-centered care model. The System is comprised of RUMC and its various subsidiaries and joint ventures; Rush Health, which is a physician hospital organization that includes each of the affiliated medical centers and hospitals along with many of their respective physicians; three community hospitals, including Rush Oak Park Hospital (“ROPH”), Rush-Copley Medical Center (“RCMC”) and Riverside Medical Center; and numerous physician relationships.

Obligated Group

RUMC and certain of its affiliates are Members of an Obligated Group created under the Master Indenture. The Members of the Obligated Group are:

Rush University Medical Center – RUMC owns and operates an academic medical center located in Chicago, Illinois. Major operations of RUMC include Rush University Hospital (“RUH”), Rush University and Rush University Medical Group (“RUMG”). The hospital operations of RUMC are licensed by the State of Illinois to operate 713 beds, of which 679 are currently staffed and include the Johnson R. Bowman Health Center for the Elderly, a rehabilitation and psychiatric facility, and Rush Children’s Hospital. According to COMPdata, RUMC is the third largest hospital provider in the eight county Chicago metropolitan area as measured by market share. RUMC is an Illinois not for profit corporation, which is exempt from federal income taxes under Section 501(c)(3) of the Internal Revenue Code of 1986, as amended (the “Code”).

Rush Oak Park Hospital – ROPH owns and operates a 296 licensed bed acute care, rehabilitation and skilled nursing hospital, of which 128 beds are currently staffed, located approximately eight miles west of RUMC in Oak Park, Illinois. RUMC is the sole corporate member of ROPH. Effective June 30, 2014, ROPH became a Member of the Obligated Group. ROPH is an Illinois not for profit corporation, which is exempt from federal income taxes under Section 501(c)(3) of the Code.

Rush-Copley Medical Center, Inc. – RCMC serves as the parent holding company for the Copley Members (as defined herein). RCMC supports the other Copley Members by providing administrative, management and related services. RCMC is an Illinois not for profit corporation, which is exempt from federal income taxes under Section 501(c)(3) of the Code.

Copley Memorial Hospital, Inc. (“Copley”) – Copley owns and operates an acute care hospital located approximately 35 miles west of RUMC in Aurora, Illinois. Copley is licensed by the State of Illinois to operate 210 beds, all of which are currently staffed. Copley is an Illinois not for profit corporation, which is exempt from federal income taxes under Section 501(c)(3) of the Code.

Rush-Copley Foundation (“Copley Foundation”) – Copley Foundation solicits contributions to support health care activities in RCMC’s service area, including, but not limited to, those of RCMC. Copley Foundation is an Illinois not for profit corporation, which is exempt from federal income taxes under Section 501(c)(3) of the Code.

Copley Ventures, Inc. (“Copley Ventures”) – Copley Ventures holds title to property for rental purposes. Copley Ventures is an Illinois not for profit corporation, which is exempt from federal income taxes under Section 501(c)(3) of the Code.

Rush-Copley Medical Group NFP (the “Medical Group”) – The Medical Group owns, operates, controls and otherwise coordinates the activities of physician practice health and medical services and provides certain physician billing and administrative services. The Medical Group is an Illinois not for profit taxable corporation.

This document is dated as of October 21, 2016. 9

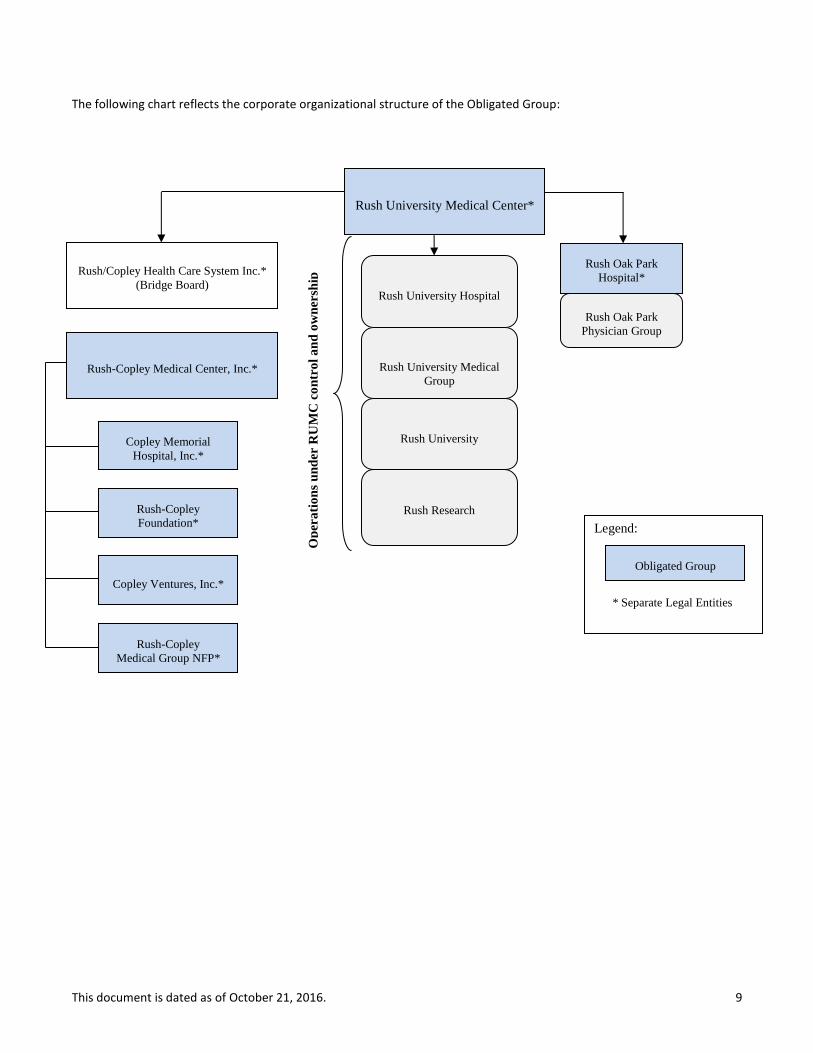

The following chart reflects the corporate organizational structure of the Obligated Group:

Rush Oak Park

Hospital*

Rush Oak Park

Physician Group

Rush/Copley Health Care System Inc.*

(Bridge Board)

Rush-Copley Medical Center, Inc.*

Copley Memorial

Hospital, Inc.*

Rush-Copley

Foundation*

Copley Ventures, Inc.*

Rush-Copley

Medical Group NFP*

Legend:

* Separate Legal Entities

Obligated Group

Rush University Hospital

Rush University Medical

Group

Rush University

Rush Research

Op

era

tio

ns

un

der

RU

MC

co

ntr

ol

an

d o

wn

ersh

ip

Rush University Medical Center*

This document is dated as of October 21, 2016. 10

Presentation of Financial Information

Although RUMC and the other corporations referenced above are currently the only Obligated Group Members under the Master Indenture, RUMC controls, directly or indirectly, a number of other non-member entities whose revenues and expenses and results of operations are included in the Obligated Group financial statements. Such non-member joint ventures and investment entities are accounted for in the Obligated Group audited consolidated financial statements and unaudited interim consolidated financial information using the equity method of accounting or are consolidated depending upon the control exercised by the applicable Obligated Group Member. Further, the information describing the financial condition of the Obligated Group contained in this annual report includes information with respect to these entities which are not Obligated Group Members. For fiscal year ended June 30, 2016, these non-member entities constituted approximately 1.2% of total revenue of the Obligated Group.

This document is dated as of October 21, 2016. 11

RUSH UNIVERSITY MEDICAL CENTER

Mission

The mission of RUMC is to provide the best health care for the individuals and diverse communities it serves through the integration of outstanding patient care, education, research and community partnerships.

Changes in Management

On October 26, 2015, K. Ranga Rama Krishnan, MD was appointed as dean of the Medical College of Rush University. Dr. Krishnan most recently served for seven years as the dean at the Duke-NUS Graduate Medical School in Singapore and previously as the school’s executive vice dean. Prior to and during his tenure in Singapore, Krishnan was professor in the Department of Psychiatry and Behavioral Sciences at Duke University Medical Center in North Carolina. He also served as chairman of psychiatry at Duke from 1998 to 2009. Dr. Krishnan earned his medical degree in 1978 and completed a rotating internship at Government General Hospital and Madras Medical College in Madras, India. Following this, he served as Senior House Officer at Queen Elizabeth Hospital, University of West Indies, Barbados.

Peter Butler retired from his role as president at the end of fiscal year 2016. Mr. Butler will continue to serve as professor and chairperson of the Department of Health Systems Management in the College of Health Sciences.

Michael Dandorph was promoted to president and chief operating officer, effective July 1, 2016. Mr. Dandorph is currently the executive vice president and chief operating officer for Rush.

Effective April 29, 2016, Anne Murphy is no longer serving as Senior Vice President of Legal Affairs and General Counsel. Carl Bergetz, Vice President of Legal Affairs, will be serving as Acting General Counsel.

Service Area and Competition

RUMC considers its service area to be the eight counties surrounding and including the City of Chicago. The eight county market area encompasses Cook, DuPage, Kane, Kankakee, Kendall, McHenry, Lake and Will counties. RUMC competes with four other academic medical centers in the Chicago metropolitan area as well as several large suburban hospitals with specialty and local strength. RUMC was the third largest hospital provider in the 8-county Chicago metropolitan area with a market share of 3.2% during the nine months ended March 31, 2016 and fiscal year ended June 30, 2015. In a highly fragmented market, RUMC focuses on building market share in its strategic programs: Neurosciences, Bone and Joint, Cancer Care, High Risk Infant and Mother, Transplant, and Heart and Vascular. RUMC was the market leader in Neurosciences and Bone & Joint, and third in Cancer Care and Transplant during the nine months ended March 31, 2016.

Rush University

Rush University currently offers more than 30 unique degree or certificate options in medicine, nursing, allied health and biomedical research. Rush University is known for its practitioner-teacher model, translational research, nurturing academic environment and focus on community and global health.

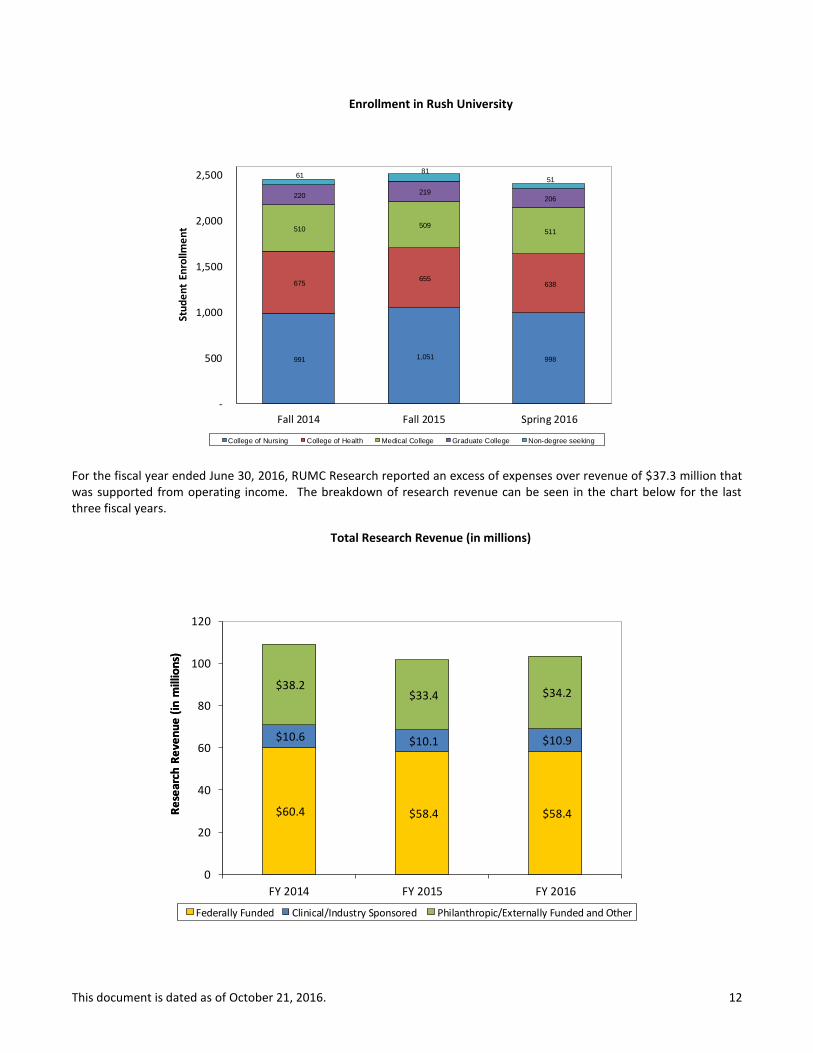

Revenue consists mainly of tuition revenue. Expenses are those instructional expenses required to educate the students. Enrollment continues to grow with 2,404 enrolled at the beginning of the Spring 2016 semester. Rush University’s teaching model is a teacher-practitioner model with practicing clinicians and other staff teaching students as part of the normal day to day responsibilities. Total enrollment in Rush University for the last three years is shown on the following chart:

This document is dated as of October 21, 2016. 12

Enrollment in Rush University

For the fiscal year ended June 30, 2016, RUMC Research reported an excess of expenses over revenue of $37.3 million that was supported from operating income. The breakdown of research revenue can be seen in the chart below for the last three fiscal years.

Total Research Revenue (in millions)

991 1,051 998

675 655

638

510 509

511

220 219

206

61 81

51

-

500

1,000

1,500

2,000

2,500

Fall 2014 Fall 2015 Spring 2016

College of Nursing College of Health Medical College Graduate College Non-degree seeking

Stu

de

nt

Enro

llme

nt

$60.4 $58.4 $58.4

$10.6 $10.1 $10.9

$38.2 $33.4 $34.2

0

20

40

60

80

100

120

FY 2014 FY 2015 FY 2016

Federally Funded Clinical/Industry Sponsored Philanthropic/Externally Funded and Other

Re

sear

ch R

eve

nu

e (

in m

illio

ns)

Re

sear

ch R

eve

nu

e (

in m

illio

ns)

This document is dated as of October 21, 2016. 13

Physician Alignment

RUMC builds relationships with employed and independent physicians through various means. RUMC employs approximately one-half of its medical staff, including those in its highly-ranked neurosurgery practice.

RUMC has also implemented various joint ventures with physicians to provide core services including the following:

Rush Surgicenter – Outpatient surgery operations at RUMC.

Circle Imaging – Outpatient imaging operations at RUMC.

Rush Radiosurgery – Outpatient stereotactic radiosurgery services at RUMC. In addition, RUMC has key strategic relationships with Midwest Orthopedics at Rush (“MOR”), a preeminent independent physician practice that is anchored in a building on the RUMC campus that was opened in 2009 by RUMC and MOR physicians. MOR provides a broad spectrum of orthopedics and sports medicine services, and utilizes the facilities at RUMC, the on-campus Rush Surgicenter, and ROPH. In 2011, RUMC entered into a broad umbrella clinical affiliation agreement, for an initial term of 10 years, with DuPage Medical Group (“DMG”), which is a multi-specialty and primary care group with over 425 physicians based in the western suburbs of Chicago. To date, the parties have implemented an affiliated outpatient cancer treatment program with infusion therapy at a newly-developed DMG building in Lisle, Illinois.

Awards RUMC provides care through a multidisciplinary approach that brings together a team of experts including physicians, scientists, nurses and other specialists to diagnose and treat patients in an integrated manner. This unique combination of teaching, research and patient care has earned RUMC national recognition for a number of its programs. Below is a list of certain awards which RUMC has received over the last two years.

Best Quality:

Ranked second in UHC 2015 Quality Leadership Awards, including orthopedics and neurosurgery, in an annual study of 101 academic medical centers. RUMC was the only medical center in Illinois listed in the top 10.

Chicago Tribune For the fourth consecutive time, RUMC has received Magnet designation, the highest national recognition given for nursing excellence in 2016. RUMC was the first hospital in Illinois treating both children and adults to achieve Magnet status. Named as 2015 recipient of the Access Living “Lead On!” Award for pioneering dedication to making healthcare accessible to all. In the spring 2016 survey, RUMC again received a top grade “A” for patient safety from the Leapfrog Group. RUMC has been named one of the 2016 “Most Wired” hospitals in the nation by Hospitals & Health Networks.

ANCC Magnet Status

Access Living

Accessibility

Leap Frog Patient Safety

H&H Networks Most Wired

UHC Quality

Leadership Awards

This document is dated as of October 21, 2016. 14

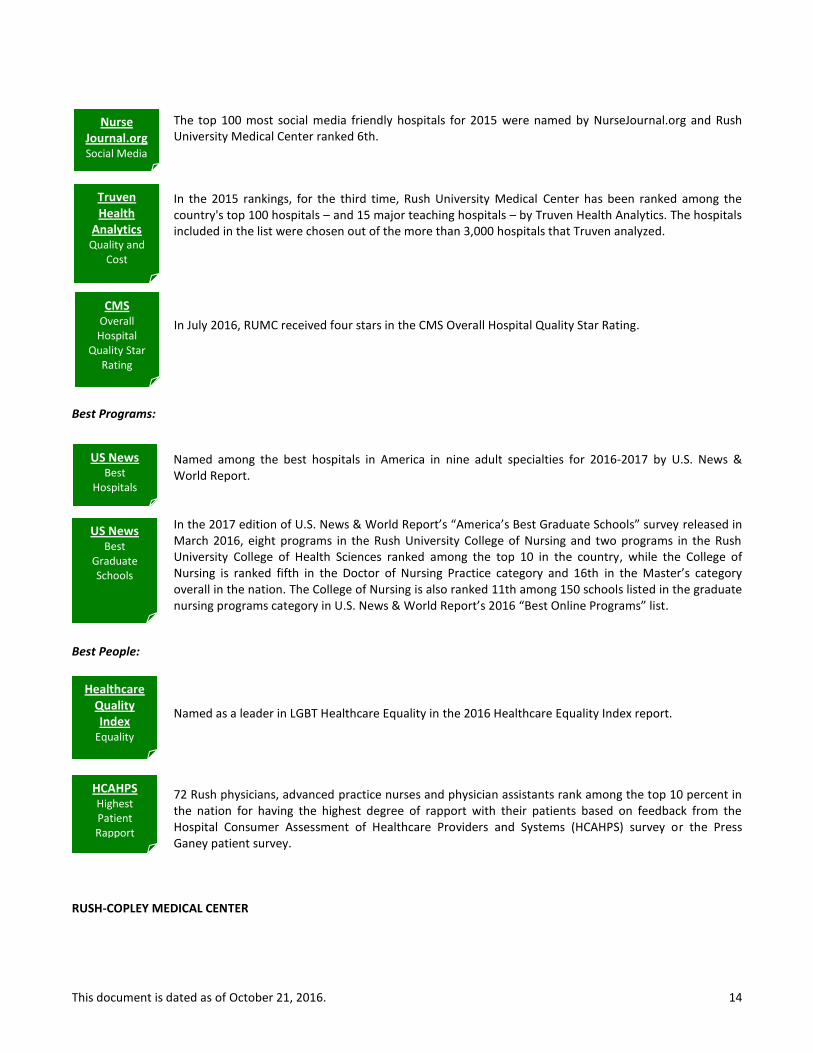

The top 100 most social media friendly hospitals for 2015 were named by NurseJournal.org and Rush University Medical Center ranked 6th.

In the 2015 rankings, for the third time, Rush University Medical Center has been ranked among the country's top 100 hospitals – and 15 major teaching hospitals – by Truven Health Analytics. The hospitals included in the list were chosen out of the more than 3,000 hospitals that Truven analyzed.

In July 2016, RUMC received four stars in the CMS Overall Hospital Quality Star Rating.

Best Programs:

Named among the best hospitals in America in nine adult specialties for 2016-2017 by U.S. News & World Report. In the 2017 edition of U.S. News & World Report’s “America’s Best Graduate Schools” survey released in March 2016, eight programs in the Rush University College of Nursing and two programs in the Rush University College of Health Sciences ranked among the top 10 in the country, while the College of Nursing is ranked fifth in the Doctor of Nursing Practice category and 16th in the Master’s category overall in the nation. The College of Nursing is also ranked 11th among 150 schools listed in the graduate nursing programs category in U.S. News & World Report’s 2016 “Best Online Programs” list.

Best People:

Named as a leader in LGBT Healthcare Equality in the 2016 Healthcare Equality Index report. 72 Rush physicians, advanced practice nurses and physician assistants rank among the top 10 percent in the nation for having the highest degree of rapport with their patients based on feedback from the Hospital Consumer Assessment of Healthcare Providers and Systems (HCAHPS) survey or the Press Ganey patient survey.

RUSH-COPLEY MEDICAL CENTER

Nurse Journal.org Social Media

US News Best

Hospitals

US News Best

Graduate Schools

Healthcare Quality Index

Equality

Truven Health

Analytics Quality and

Cost

HCAHPS Highest Patient Rapport

CMS Overall Hospital

Quality Star Rating

This document is dated as of October 21, 2016. 15

Service Area and Competition

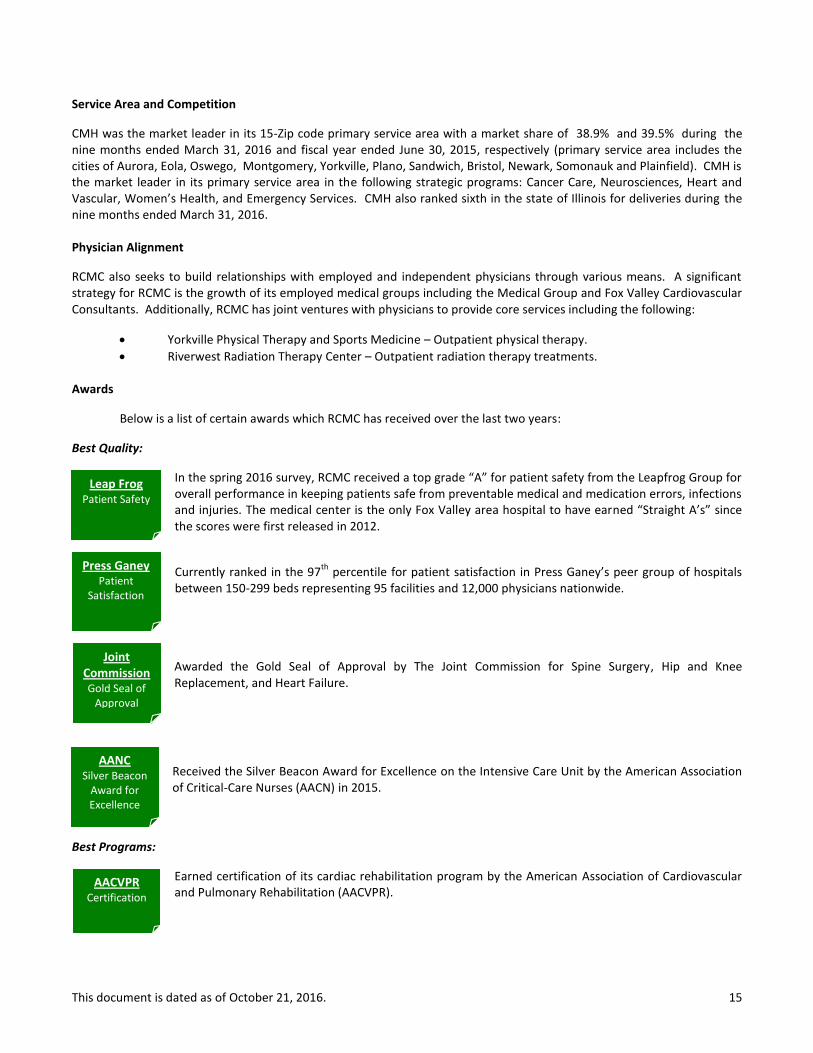

CMH was the market leader in its 15-Zip code primary service area with a market share of 38.9% and 39.5% during the nine months ended March 31, 2016 and fiscal year ended June 30, 2015, respectively (primary service area includes the cities of Aurora, Eola, Oswego, Montgomery, Yorkville, Plano, Sandwich, Bristol, Newark, Somonauk and Plainfield). CMH is the market leader in its primary service area in the following strategic programs: Cancer Care, Neurosciences, Heart and Vascular, Women’s Health, and Emergency Services. CMH also ranked sixth in the state of Illinois for deliveries during the nine months ended March 31, 2016. Physician Alignment

RCMC also seeks to build relationships with employed and independent physicians through various means. A significant strategy for RCMC is the growth of its employed medical groups including the Medical Group and Fox Valley Cardiovascular Consultants. Additionally, RCMC has joint ventures with physicians to provide core services including the following:

Yorkville Physical Therapy and Sports Medicine – Outpatient physical therapy.

Riverwest Radiation Therapy Center – Outpatient radiation therapy treatments. Awards

Below is a list of certain awards which RCMC has received over the last two years:

Best Quality:

In the spring 2016 survey, RCMC received a top grade “A” for patient safety from the Leapfrog Group for overall performance in keeping patients safe from preventable medical and medication errors, infections and injuries. The medical center is the only Fox Valley area hospital to have earned “Straight A’s” since the scores were first released in 2012.

Currently ranked in the 97

th percentile for patient satisfaction in Press Ganey’s peer group of hospitals

between 150-299 beds representing 95 facilities and 12,000 physicians nationwide.

Awarded the Gold Seal of Approval by The Joint Commission for Spine Surgery, Hip and Knee Replacement, and Heart Failure.

Received the Silver Beacon Award for Excellence on the Intensive Care Unit by the American Association of Critical-Care Nurses (AACN) in 2015.

Best Programs:

Earned certification of its cardiac rehabilitation program by the American Association of Cardiovascular and Pulmonary Rehabilitation (AACVPR).

Leap Frog Patient Safety

Press Ganey Patient

Satisfaction

Joint Commission Gold Seal of

Approval

AACVPR Certification

AANC Silver Beacon

Award for Excellence

This document is dated as of October 21, 2016. 16

Awarded the Joint Commission's Certificate of Distinction for Inpatient Diabetes Care in 2015.

In 2015, RCMC received the American Heart Association’s Heart-Check mark for Advanced Certification in Heart Failure. In 2016, RCMC has received the Get With The Guidelines® – Heart Failure Silver-Plus Quality Achievement Award.

In 2016, RCMC received the American Heart Association/American Stroke Association’s Get With The Guidelines® Stroke Gold Plus quality achievement award. The hospital also qualified to be recognized as a recipient of the American Heart Association/American Stroke Association’s Target: Stroke Honor Roll.

RCMC’s Wound Care Center was recognized with the Center of Distinction Award for Clinical Excellence in 2015, from Healogics, the nation’s largest provider of advanced wound care services.

RCMC was designated Blue Distinction® Center+ for Maternity Care and for Knee and Hip Replacement Surgeries by Blue Cross and Blue Shield.

Best People:

The Chicago Tribune selected RCMC as one of the 2015 “Chicago’s Top Workplaces.” RCMC ranked in the top ten of the large employer category. In addition, Rush-Copley was recognized as a top workplace for “communication” with the highest survey scores related to employees feeling well informed about important decisions.

Recognized as a Platinum-Level Fit-Friendly Worksite by the American Heart Association. Currently ranked in the 98

th percentile nationwide for employer engagement by IBM/Kenexa for health

care facilities with 100 or more respondents.

Chicago Tribune

Top Workplace

AHA Fit Friendly

IBM Employer

Engagement

Joint Commission

Inpatient Diabetes

American Heart

Association Heart Failure

Healogics Center of

Distinction Award

BCBS Blue

Distinction® Center+

American Stroke

Association Stroke Gold

Plus & Stroke Honor Roll

This document is dated as of October 21, 2016. 17

RUSH OAK PARK HOSPITAL

Service Area and Competition

Local competition is strong and represented by integrated delivery system hospitals and for-profit systems. Three of the strategic programs at RUMC are currently integrated at ROPH: Cancer Care, Heart and Vascular, and Bone and Joint. RUMC is the sole corporate member of ROPH. ROPH was the market leader in its 6-Zip code primary service area with a market share of 23.8% and 22.2% during the nine months ended March 31, 2016 and fiscal year ended June 30, 2015, respectively (primary service area includes the cities of Oak Park, Forest Park, and River Forest). ROPH focuses on building market share in its strategic programs: Neurosciences, Heart and Vascular, Cancer Care, and Bone & Joint. ROPH was first in Neurosciences and Heart and Vascular, and second in Bone & Joint in its primary service area during the nine months ended March 31, 2016.

Physician Alignment

ROPH has various relationships with employed and independent physicians. Rush Oak Park Physician Group (“ROPPG”) is comprised of seven physician groups that include 30 employed physicians with locations in Oak Park, Elmwood Park and North Riverside communities with Family Practice, Pediatrics and Internal Medicine physicians as well as other specialty services

Awards

Below is a list of certain awards which ROPH has received over the last two years:

Best Quality:

In 2016, ROPH achieved Magnet designation, the highest national recognition given for nursing excellence by the American Nurses Credentialing Center.

One of the 2016 “Most Wired” hospitals for the fourth year in a row.

Awarded the Gold Seal of Approval by The Joint Commission.

Recognized as a 2014 Top Performer on Key Quality Measures in heart attack, heart failure, pneumonia, surgical care, and stroke.

Awarded Press Ganey’s 2015 Guardian of Excellence Award for reaching the 95th percentile for clinical quality performance.

H&H Networks Most Wired

Joint Commission Gold Seal of

Approval

Press Ganey

Guardian of Excellence

Award

Joint Commission Top Performer on Key Quality

Measures

ANCC Magnet Status

This document is dated as of October 21, 2016. 18

In July of 2016, ROPH received four stars in the CMS Overall Hospital Quality Star Rating.

Best Programs:

Diabetes program recognized by the American Diabetes Association as meeting the National Standards for Diabetes Self-Management Education.

Recognized by the American College of Surgeons National Surgical Quality Improvement Program (ACS NSQIP) for achieving meritorious outcomes for surgical patient care in 2014.

Best People:

One of 10 hospitals in Illinois to have earned New York University College of Nursing’s Nurses Improving Care for Healthsystem Elders designation. In 2016, for the third consecutive year, ROPH was recognized as a “Leader in LGBT Healthcare Equality” by the Human Rights Campaign Foundation.

ADA Education

HRCF Equality

NYU Improving

Care

ACS NSQIP Top Surgical

Hospital

CMS Overall Hospital

Quality Star Rating

This document is dated as of October 21, 2016. 19

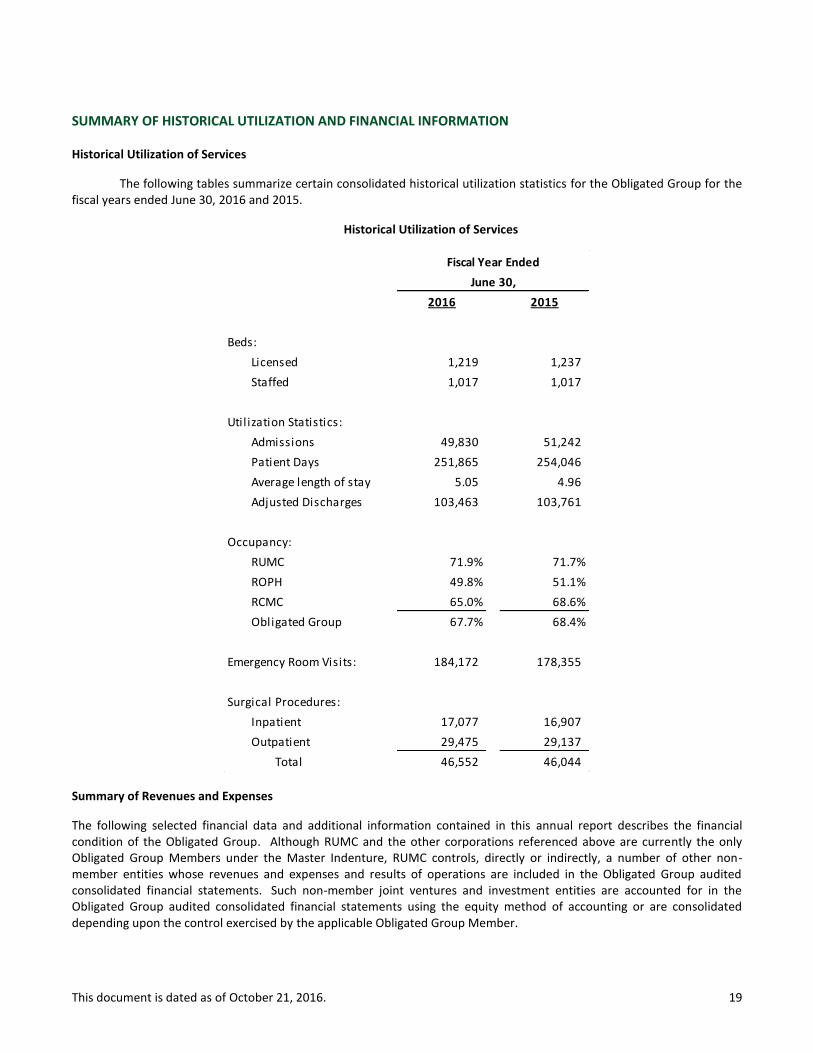

SUMMARY OF HISTORICAL UTILIZATION AND FINANCIAL INFORMATION

Historical Utilization of Services

The following tables summarize certain consolidated historical utilization statistics for the Obligated Group for the fiscal years ended June 30, 2016 and 2015.

Historical Utilization of Services

Summary of Revenues and Expenses

The following selected financial data and additional information contained in this annual report describes the financial condition of the Obligated Group. Although RUMC and the other corporations referenced above are currently the only Obligated Group Members under the Master Indenture, RUMC controls, directly or indirectly, a number of other non-member entities whose revenues and expenses and results of operations are included in the Obligated Group audited consolidated financial statements. Such non-member joint ventures and investment entities are accounted for in the Obligated Group audited consolidated financial statements using the equity method of accounting or are consolidated depending upon the control exercised by the applicable Obligated Group Member.

2016 2015

Beds:

Licensed 1,219 1,237

Staffed 1,017 1,017

Util ization Statistics:

Admissions 49,830 51,242

Patient Days 251,865 254,046

Average length of stay 5.05 4.96

Adjusted Discharges 103,463 103,761

Occupancy:

RUMC 71.9% 71.7%

ROPH 49.8% 51.1%

RCMC 65.0% 68.6%

Obligated Group 67.7% 68.4%

Emergency Room Visits: 184,172 178,355

Surgical Procedures:

Inpatient 17,077 16,907

Outpatient 29,475 29,137

Total 46,552 46,044

June 30,

Fiscal Year Ended

This document is dated as of October 21, 2016. 20

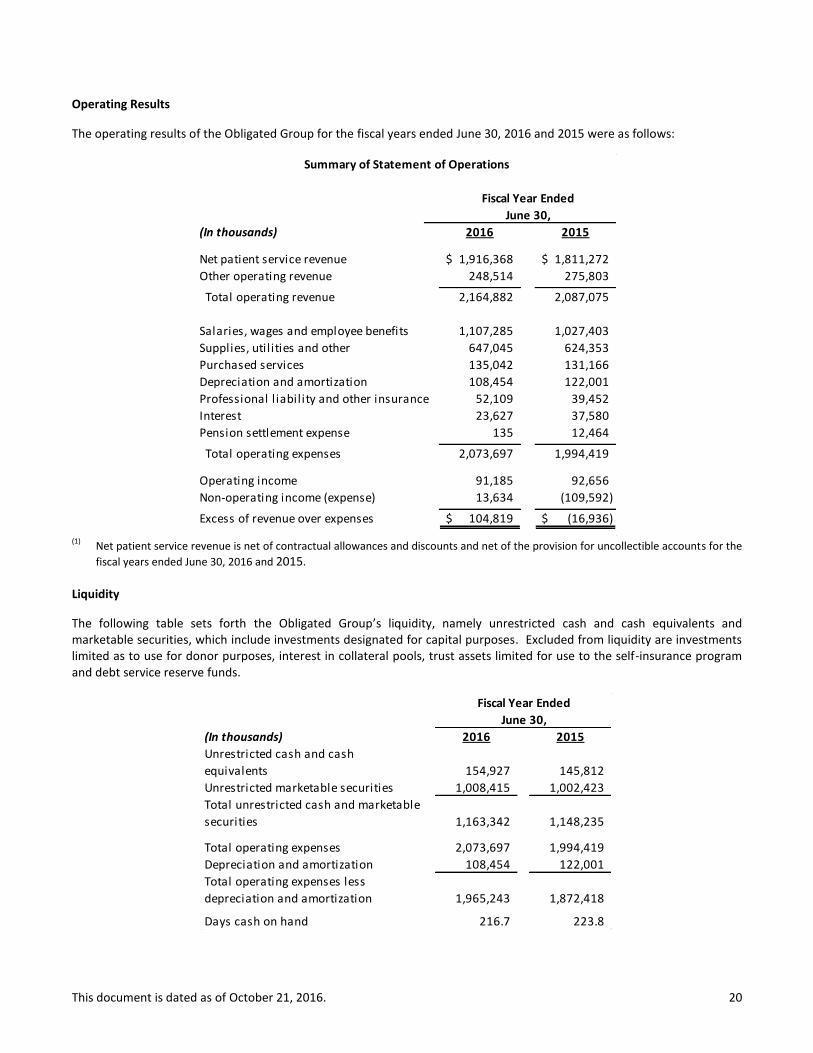

Operating Results

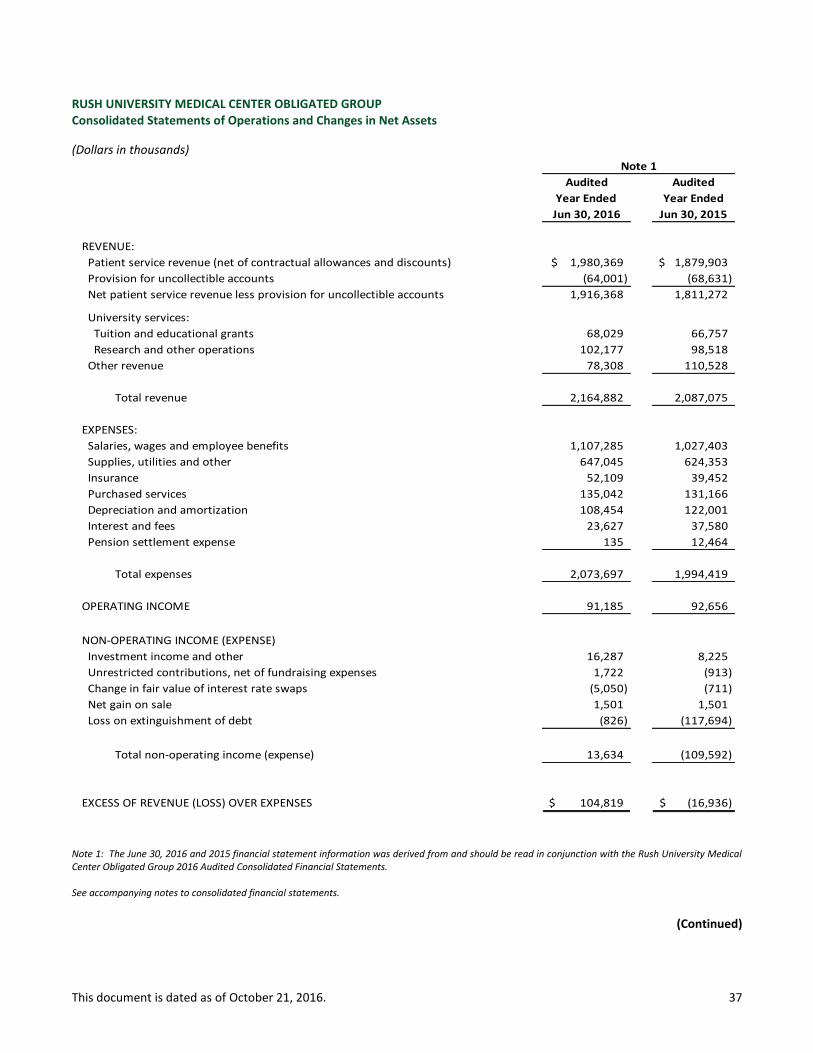

The operating results of the Obligated Group for the fiscal years ended June 30, 2016 and 2015 were as follows:

(1)

Net patient service revenue is net of contractual allowances and discounts and net of the provision for uncollectible accounts for the

fiscal years ended June 30, 2016 and 2015.

Liquidity

The following table sets forth the Obligated Group’s liquidity, namely unrestricted cash and cash equivalents and marketable securities, which include investments designated for capital purposes. Excluded from liquidity are investments limited as to use for donor purposes, interest in collateral pools, trust assets limited for use to the self-insurance program and debt service reserve funds.

(In thousands) 2016 2015

Net patient service revenue 1,916,368$ 1,811,272$

Other operating revenue 248,514 275,803

Total operating revenue 2,164,882 2,087,075

Salaries, wages and employee benefits 1,107,285 1,027,403

Supplies, util ities and other 647,045 624,353

Purchased services 135,042 131,166

Depreciation and amortization 108,454 122,001

Professional l iability and other insurance 52,109 39,452

Interest 23,627 37,580

Pension settlement expense 135 12,464

Total operating expenses 2,073,697 1,994,419

Operating income 91,185 92,656

Non-operating income (expense) 13,634 (109,592)

Excess of revenue over expenses 104,819$ (16,936)$

Summary of Statement of Operations

Fiscal Year Ended

June 30,

(In thousands) 2016 2015

Unrestricted cash and cash

equivalents 154,927 145,812

Unrestricted marketable securities 1,008,415 1,002,423

Total unrestricted cash and marketable

securities 1,163,342 1,148,235

Total operating expenses 2,073,697 1,994,419

Depreciation and amortization 108,454 122,001

Total operating expenses less

depreciation and amortization 1,965,243 1,872,418

Days cash on hand 216.7 223.8

June 30,

Fiscal Year Ended

This document is dated as of October 21, 2016. 21

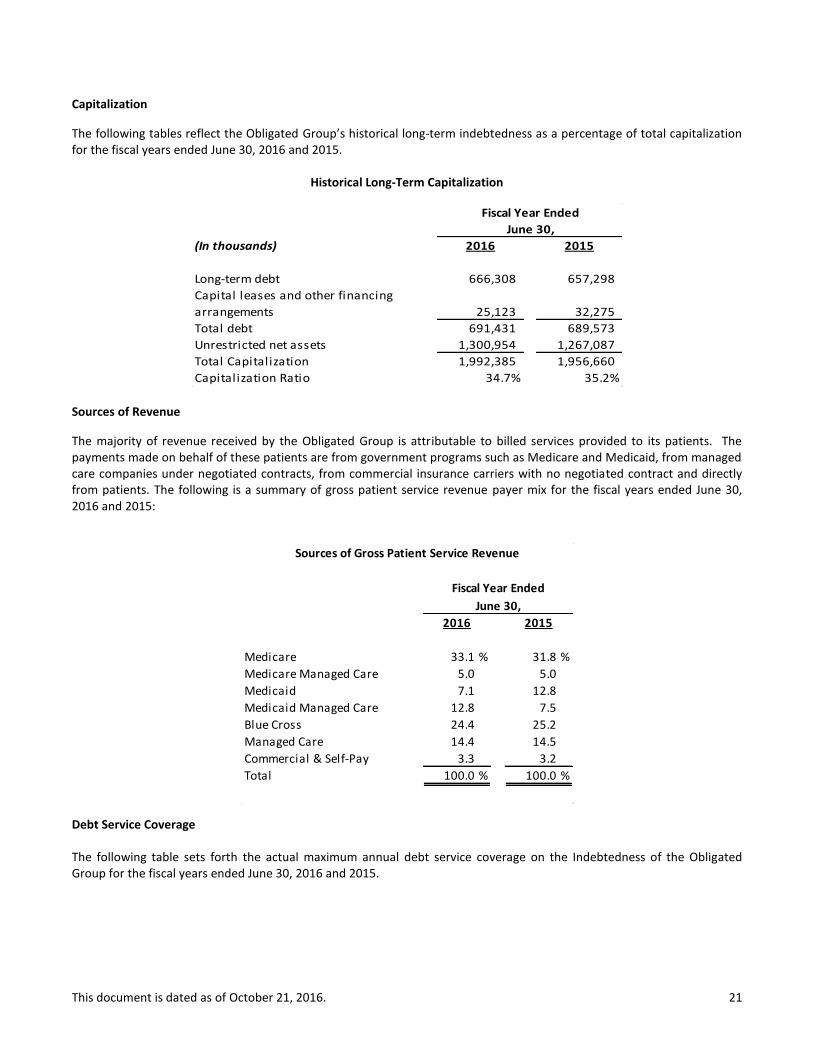

Capitalization

The following tables reflect the Obligated Group’s historical long-term indebtedness as a percentage of total capitalization for the fiscal years ended June 30, 2016 and 2015.

Historical Long-Term Capitalization

Sources of Revenue

The majority of revenue received by the Obligated Group is attributable to billed services provided to its patients. The payments made on behalf of these patients are from government programs such as Medicare and Medicaid, from managed care companies under negotiated contracts, from commercial insurance carriers with no negotiated contract and directly from patients. The following is a summary of gross patient service revenue payer mix for the fiscal years ended June 30, 2016 and 2015:

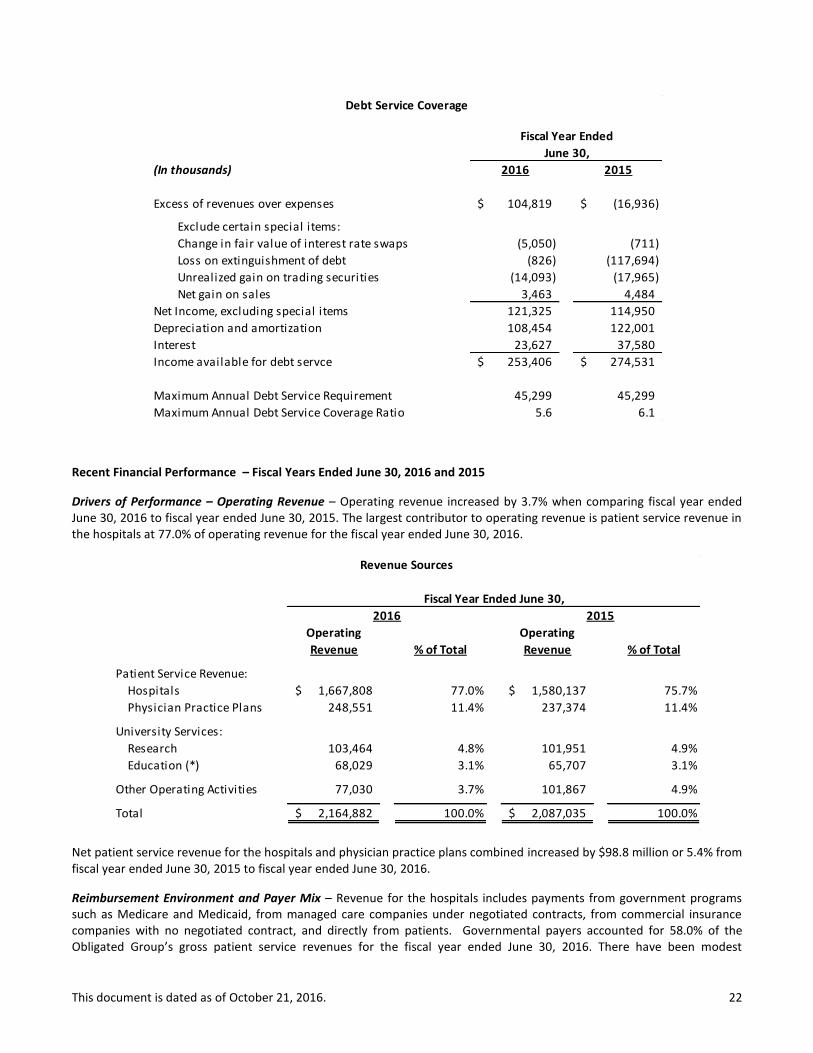

Debt Service Coverage

The following table sets forth the actual maximum annual debt service coverage on the Indebtedness of the Obligated Group for the fiscal years ended June 30, 2016 and 2015.

(In thousands) 2016 2015

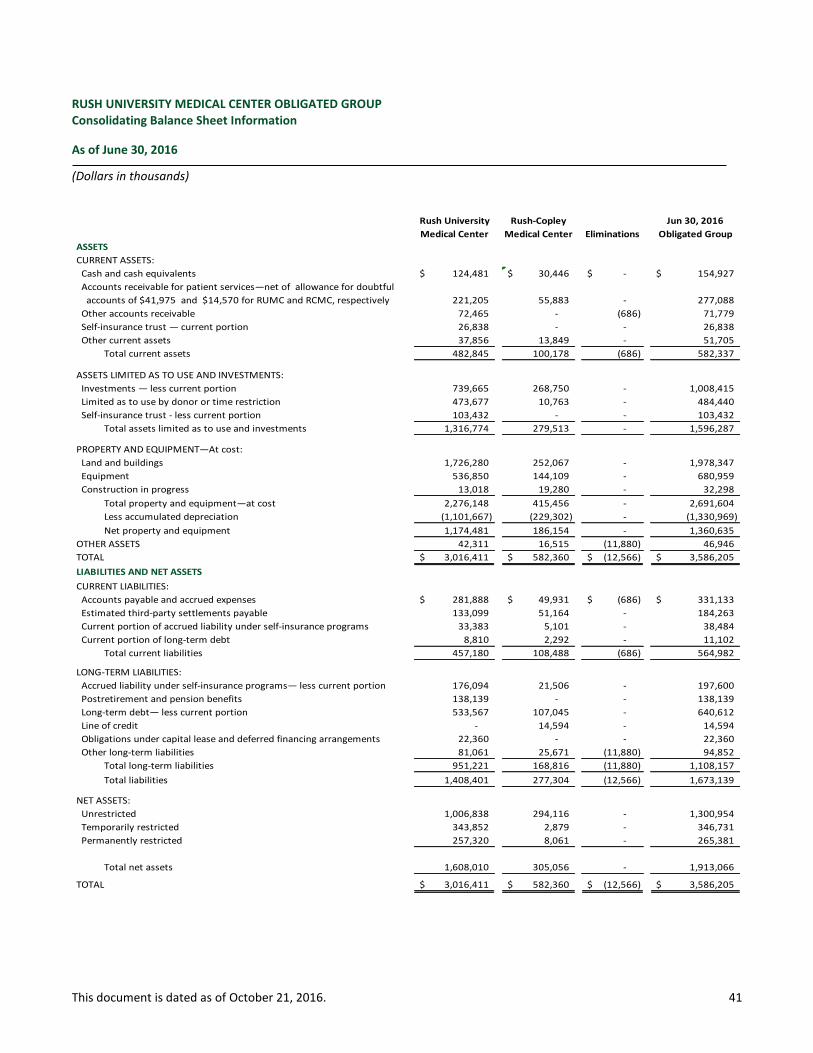

Long-term debt 666,308 657,298

Capital leases and other financing

arrangements 25,123 32,275

Total debt 691,431 689,573

Unrestricted net assets 1,300,954 1,267,087

Total Capitalization 1,992,385 1,956,660

Capitalization Ratio 34.7% 35.2%

June 30,

Fiscal Year Ended

2016 2015

Medicare 33.1 % 31.8 %

Medicare Managed Care 5.0 5.0

Medicaid 7.1 12.8

Medicaid Managed Care 12.8 7.5

Blue Cross 24.4 25.2

Managed Care 14.4 14.5

Commercial & Self-Pay 3.3 3.2

Total 100.0 % 100.0 %

Sources of Gross Patient Service Revenue

Fiscal Year Ended

June 30,

This document is dated as of October 21, 2016. 22

Recent Financial Performance – Fiscal Years Ended June 30, 2016 and 2015

Drivers of Performance – Operating Revenue – Operating revenue increased by 3.7% when comparing fiscal year ended June 30, 2016 to fiscal year ended June 30, 2015. The largest contributor to operating revenue is patient service revenue in the hospitals at 77.0% of operating revenue for the fiscal year ended June 30, 2016.

Net patient service revenue for the hospitals and physician practice plans combined increased by $98.8 million or 5.4% from fiscal year ended June 30, 2015 to fiscal year ended June 30, 2016.

Reimbursement Environment and Payer Mix – Revenue for the hospitals includes payments from government programs such as Medicare and Medicaid, from managed care companies under negotiated contracts, from commercial insurance companies with no negotiated contract, and directly from patients. Governmental payers accounted for 58.0% of the Obligated Group’s gross patient service revenues for the fiscal year ended June 30, 2016. There have been modest

(In thousands) 2016 2015

Excess of revenues over expenses 104,819$ (16,936)$

Exclude certain special items:

Change in fair value of interest rate swaps (5,050) (711)

Loss on extinguishment of debt (826) (117,694)

Unrealized gain on trading securities (14,093) (17,965)

Net gain on sales 3,463 4,484

Net Income, excluding special items 121,325 114,950

Depreciation and amortization 108,454 122,001

Interest 23,627 37,580

Income available for debt servce 253,406$ 274,531$

Maximum Annual Debt Service Requirement 45,299 45,299

Maximum Annual Debt Service Coverage Ratio 5.6 6.1

Debt Service Coverage

June 30,

Fiscal Year Ended

Operating Operating

Revenue % of Total Revenue % of Total

Patient Service Revenue:

Hospitals 1,667,808$ 77.0% 1,580,137$ 75.7%

Physician Practice Plans 248,551 11.4% 237,374 11.4%

University Services:

Research 103,464 4.8% 101,951 4.9%

Education (*) 68,029 3.1% 65,707 3.1%

Other Operating Activities 77,030 3.7% 101,867 4.9%

Total 2,164,882$ 100.0% 2,087,035$ 100.0%

Fiscal Year Ended June 30,

2016 2015

Revenue Sources

This document is dated as of October 21, 2016. 23

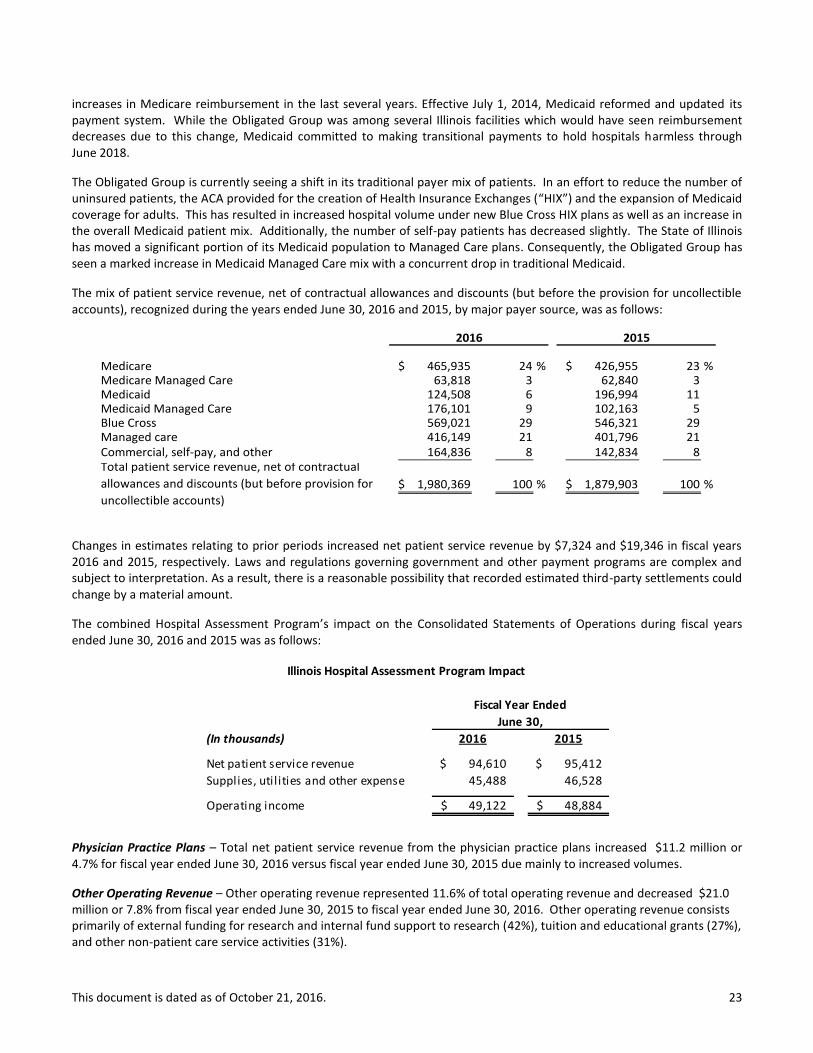

increases in Medicare reimbursement in the last several years. Effective July 1, 2014, Medicaid reformed and updated its payment system. While the Obligated Group was among several Illinois facilities which would have seen reimbursement decreases due to this change, Medicaid committed to making transitional payments to hold hospitals harmless through June 2018.

The Obligated Group is currently seeing a shift in its traditional payer mix of patients. In an effort to reduce the number of uninsured patients, the ACA provided for the creation of Health Insurance Exchanges (“HIX”) and the expansion of Medicaid coverage for adults. This has resulted in increased hospital volume under new Blue Cross HIX plans as well as an increase in the overall Medicaid patient mix. Additionally, the number of self-pay patients has decreased slightly. The State of Illinois has moved a significant portion of its Medicaid population to Managed Care plans. Consequently, the Obligated Group has seen a marked increase in Medicaid Managed Care mix with a concurrent drop in traditional Medicaid.

The mix of patient service revenue, net of contractual allowances and discounts (but before the provision for uncollectible accounts), recognized during the years ended June 30, 2016 and 2015, by major payer source, was as follows:

Medicare 465,935$ 24 % 426,955$ 23 % Medicare Managed Care 63,818 3 62,840 3 Medicaid 124,508 6 196,994 11 Medicaid Managed Care 176,101 9 102,163 5 Blue Cross 569,021 29 546,321 29 Managed care 416,149 21 401,796 21 Commercial, self-pay, and other 164,836 8 142,834 8 Total patient service revenue, net of contractual

allowances and discounts (but before provision for

uncollectible accounts)

1,980,369$ 100 % 1,879,903$ 100 %

2016 2015

Changes in estimates relating to prior periods increased net patient service revenue by $7,324 and $19,346 in fiscal years 2016 and 2015, respectively. Laws and regulations governing government and other payment programs are complex and subject to interpretation. As a result, there is a reasonable possibility that recorded estimated third-party settlements could change by a material amount.

The combined Hospital Assessment Program’s impact on the Consolidated Statements of Operations during fiscal years ended June 30, 2016 and 2015 was as follows:

Physician Practice Plans – Total net patient service revenue from the physician practice plans increased $11.2 million or 4.7% for fiscal year ended June 30, 2016 versus fiscal year ended June 30, 2015 due mainly to increased volumes.

Other Operating Revenue – Other operating revenue represented 11.6% of total operating revenue and decreased $21.0 million or 7.8% from fiscal year ended June 30, 2015 to fiscal year ended June 30, 2016. Other operating revenue consists primarily of external funding for research and internal fund support to research (42%), tuition and educational grants (27%), and other non-patient care service activities (31%).

(In thousands) 2016 2015

Net patient service revenue 94,610$ 95,412$

Supplies, util ities and other expense 45,488 46,528

Operating income 49,122$ 48,884$

Fiscal Year Ended

June 30,

Illinois Hospital Assessment Program Impact

This document is dated as of October 21, 2016. 24

The decrease in other operating revenue is mainly the result of asset monetization revenue recognized during fiscal year ended June 30, 2015. In July 2014, Rush sold its royalties of Ampyra and recognized $34.7 million of revenue within other operating revenue.

Drivers of Performance – Operating Expense – Operating expenses increased by $79.3 million or 4.0% from fiscal year ended June 30, 2015 to fiscal year ended June 30, 2016. Operating costs as a percentage of operating revenue for the fiscal years ended June 30, 2016 and 2015, were as follows:

Salaries, Wages and Employee Benefits – Salaries, wages and employee benefits increased by $79.9 million or 7.8% when comparing fiscal year ended June 30, 2015 to fiscal year ended June 30, 2016.

The table below shows the employed FTEs and employed physicians for the Obligated Group as of June 30, 2016 as compared to June 30, 2015:

Note: Of the 10,969 FTE’s, approximately 8.1% of non-clinical employees are represented by a union. On Tuesday, August 16, 2016, RUMC received the decision from the three member panel of the U.S. Court of Appeals for the District of Columbia unanimously affirming the order of the National Labor Relations Board that the Medical Center engage in collective bargaining with Local 743, Teamsters concerning its representation of Patient Care Technicians. In conjunction with our legal department and our outside labor relations law firm, we are considering whether RUMC would request further review. Depreciation and Amortization – Depreciation and amortization expense decreased $13.5 million or 11.1% for fiscal year ended June 30, 2016 versus fiscal year ended June 30, 2015. In December 2015 RUMC received a settlement of $9 million related to a breach of contract over the design of the Tower, as discussed on pages 27 and 29 of this report. In fiscal year 2013, RUMC recorded $10 million of additional depreciation expense to write-off the impaired asset.

Professional Liability and Other Insurance – Professional liability and other insurance cost the Obligated Group $52.1 million for fiscal year ended June 30, 2016, which is an increase of $12.7 million or 32.1% from fiscal year ended June 30, 2015. The increase is due to RUMC recording additional professional liability expense during fiscal year 2016 in accordance with internal reserving policies.

2016 2015

Salaries, wages and employee benefits 53.1% 49.2%

Supplies, util ities and other (including purchased services) 37.5% 36.8%

Depreciation and amortization 5.2% 5.8%

Professional l iability and other insurance 2.5% 1.9%

Interest 1.1% 1.8%

Operating Costs as a Percentage of Operating Revenue

Fiscal Year Ended

June 30,

Percent

2016 2015 Change

Number of Full-time Equivalents 10,969 10,647 3.0%

Number of Employed Physicians 629 603 4.3%

As of Jun 30,

This document is dated as of October 21, 2016. 25

Interest Expense – Interest expense was $23.6 million for fiscal year ended June 30, 2016, which is a decrease of $14.0 million or 37.1% from fiscal year ended June 30, 2015. The significant decrease is the result of the debt refinancing completed in February 2015.

Significant Nonrecurring Items – During the fiscal years ended June 30, 2016 and 2015 significant nonrecurring items impacted the Obligated Group’s reported operating income as follows:

Non-operating Income/Expense – Total non-operating income increased by $123.2 million from fiscal year ended June 30, 2015 to fiscal year ended June 30, 2016. Non-operating income consists of investment income, unrestricted contributions, loss on extinguishment of debt, and interest rate swaps. The significant increase is due to the $117.7 million loss on extinguishment of debt recognized in fiscal year 2015.

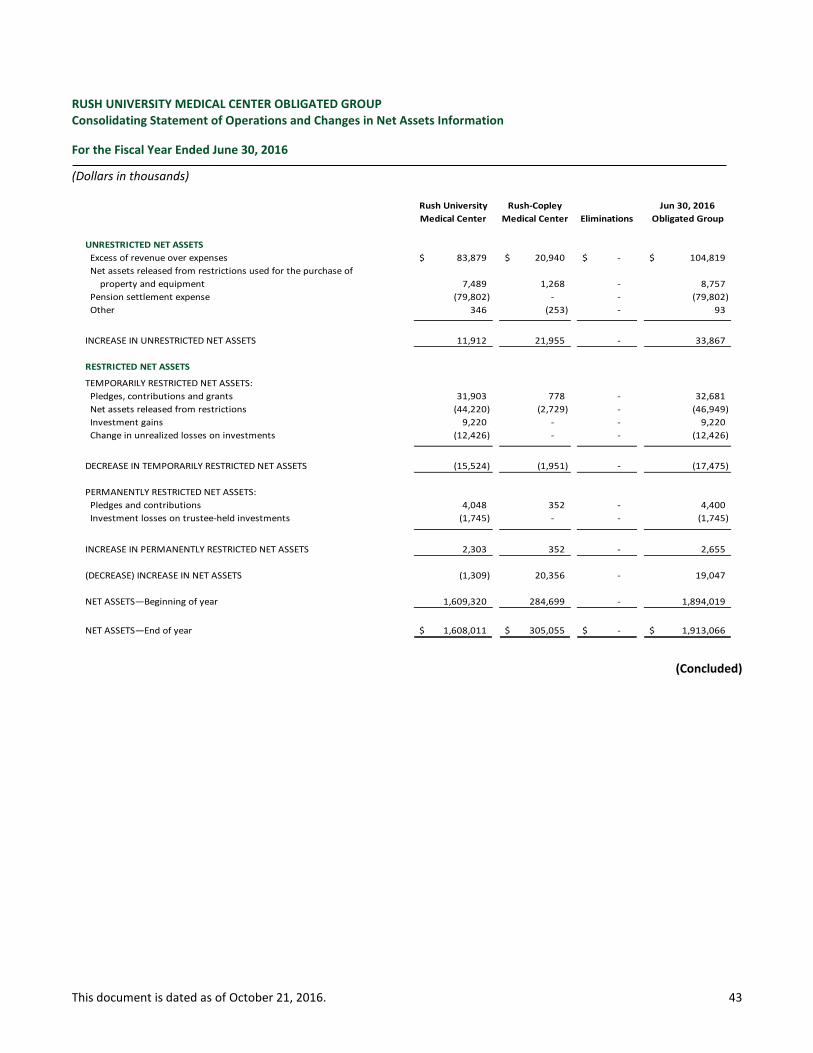

Liquidity and Capital Resources – The Obligated Group’s unrestricted cash and investments at market value increased by $15.1 million or 1.3% from June 30, 2015 to June 30, 2016, 216.7 days cash on hand at June 30, 2016. Included in unrestricted cash and investments was $81.9 million and $72.0 million of Specific Purpose Fund balances as of June 30, 2016 and June 30, 2015, respectively, and $48.1 million and $51.2 million of appreciation on the unrestricted portion of RUMC’s endowment as of June 30, 2016 and June 30, 2015, respectively.

Excluded from unrestricted cash and investments were the following temporarily restricted assets:

Appreciation on the restricted portion of RUMC’s endowment fund of $193.7 million and $208.3 million as of June 30, 2016 and June 30, 2015, respectively. These temporarily restricted funds are used to support specific purposes such as research and education.

The Obligated Group as well as other Illinois hospitals have experienced significant delays in payments by the State of Illinois for amounts due under Medicaid and other state funded programs. Periodically the State catches up with the payments and the delays experienced by the Obligated Group improve, however these delays have increased through the fourth quarter of this fiscal year. Days in accounts receivable ended at 52.9 as of June 30, 2016. Collections of non-Medicaid receivables during the year have been strong to help offset any continuing payment delays on Medicaid receivables.

Capital Expenditures

Since completion of the Tower, spending has normalized to levels consistent with fiscal year 2006 and earlier. Total capital expenditures for the Obligated Group amounted to $124.0 million for fiscal year ended June 30, 2016, a $4.3 million decrease from fiscal year ended June 30, 2015. The Obligated Group’s construction commitments outstanding as of June 30, 2016 were $61.8 million.

MISCELLANEOUS

Ratings

Moody’s, S&P and Fitch have assigned municipal bond ratings of “A1”, “A+” and “A+,” respectively, to the long-term debt of the Obligated Group. As of January 7, 2015, Fitch affirmed the Obligated Group’s A+ rating and revised the outlook to

Fiscal Year Ended Jun-16 Fiscal Year Ended Jun-15

June 30, Operating June 30, Operating

(In millions) 2016 Margin 2015 Margin

Operating income reported $91.2 4.2% $92.7 4.4%

Items impacting operating revenue (12.4) -0.6 (49.8) -2.4

Items impacting operating expenses (13.7) -0.6 30.8 1.5

Total adjustments (26.1) -1.2 (19.1) -0.9

Adjusted operating income $65.1 3.0% $73.6 3.5%

This document is dated as of October 21, 2016. 26

“Positive.” As of January 9, 2015, Moody’s upgraded the Obligated Group’s rating to A1 rating and revised the outlook to “Stable.” As of May 5, 2016, S&P affirmed the Obligated Group’s A+ rating and the “Stable” outlook.

Any explanation of the significance of such ratings may only be obtained from Moody’s, S&P and Fitch. Certain information and materials not included in this Annual Report may have been furnished to Moody’s, S&P and Fitch concerning the Obligated Group. Generally, rating agencies base their ratings on such information and materials and on investigations, studies and assumptions by the rating agencies. Such ratings reflect only the views of such organizations, and an explanation of the significance of such ratings may be obtained only from the rating agencies furnishing the same. There is no assurance that such ratings will remain in effect for any given period of time or that such ratings will not be revised downward or upward or withdrawn entirely by any of such rating agencies if, in the judgment of such rating agency, circumstances warrant. Any such downward revision or withdrawal of such rating may have an adverse effect on the market price or marketability of the Obligated Group’s outstanding bonds.

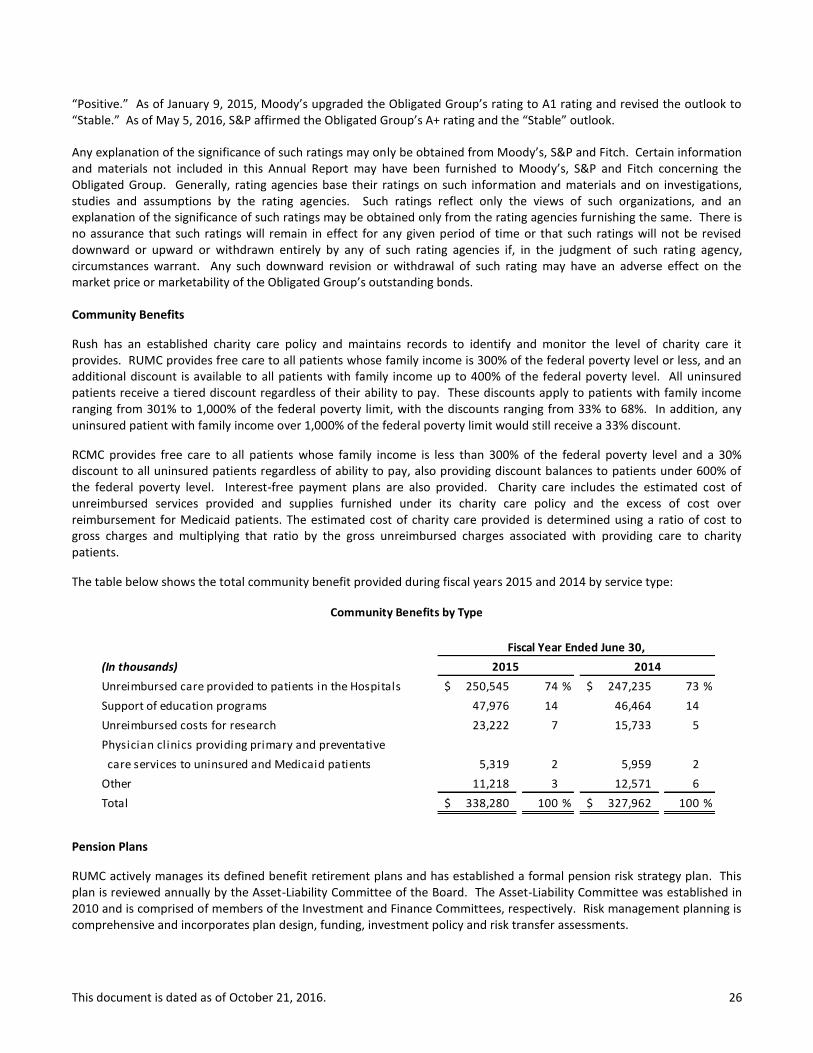

Community Benefits

Rush has an established charity care policy and maintains records to identify and monitor the level of charity care it provides. RUMC provides free care to all patients whose family income is 300% of the federal poverty level or less, and an additional discount is available to all patients with family income up to 400% of the federal poverty level. All uninsured patients receive a tiered discount regardless of their ability to pay. These discounts apply to patients with family income ranging from 301% to 1,000% of the federal poverty limit, with the discounts ranging from 33% to 68%. In addition, any uninsured patient with family income over 1,000% of the federal poverty limit would still receive a 33% discount.

RCMC provides free care to all patients whose family income is less than 300% of the federal poverty level and a 30% discount to all uninsured patients regardless of ability to pay, also providing discount balances to patients under 600% of the federal poverty level. Interest-free payment plans are also provided. Charity care includes the estimated cost of unreimbursed services provided and supplies furnished under its charity care policy and the excess of cost over reimbursement for Medicaid patients. The estimated cost of charity care provided is determined using a ratio of cost to gross charges and multiplying that ratio by the gross unreimbursed charges associated with providing care to charity patients.

The table below shows the total community benefit provided during fiscal years 2015 and 2014 by service type:

Pension Plans

RUMC actively manages its defined benefit retirement plans and has established a formal pension risk strategy plan. This plan is reviewed annually by the Asset-Liability Committee of the Board. The Asset-Liability Committee was established in 2010 and is comprised of members of the Investment and Finance Committees, respectively. Risk management planning is comprehensive and incorporates plan design, funding, investment policy and risk transfer assessments.

(In thousands)

Unreimbursed care provided to patients in the Hospitals 250,545$ 74 % 247,235$ 73 %

Support of education programs 47,976 14 46,464 14

Unreimbursed costs for research 23,222 7 15,733 5

Physician clinics providing primary and preventative

care services to uninsured and Medicaid patients 5,319 2 5,959 2

Other 11,218 3 12,571 6

Total 338,280$ 100 % 327,962$ 100 %

2015 2014

Fiscal Year Ended June 30,

Community Benefits by Type

This document is dated as of October 21, 2016. 27

Funded Status – RUMC regularly measures its plans’ funded status on a PPA Funded Ratio, FAS Funded Ratio and Economic Funded Ratio. These measurements utilize different time periods and discount rates to measure the liability and different smoothing methods for the assets held in the Master Retirement Trust. The FAS Funded Ratio found in the footnotes to the financial statements as of June 30, 2016, reflects a funded ratio of 87%.

Funding – For the past seven consecutive calendar years, RUMC contributed more than the minimum required by Employee Retirement Income Security Act and the Code funding rules. During the fiscal year ended June 30, 2016, RUMC contributed $66.0 million to the plan.

Investment Policy – The portfolio’s investment objective is to achieve a total return that meets or exceeds the plan’s obligations over a full market cycle. This cycle is generally defined as rolling five year periods.

Plan Design – During June 2015, Rush offered a voluntary lump sum cash out to certain eligible terminated vested participants, resulting in a total settlement amount of $46.0 million. In addition, the de-risking initiative triggered a one-time non-cash charge of $12.5 million as a result of the total payments exceeding the plan’s interest cost and service cost components in fiscal year 2015.

Effective January 1, 2015, a new defined benefit plan was established. This new plan (the “Pre-2015 Separations Plan” or the “Pre-2015 Plan”), is a spinoff of the current Retirement Plan. The Retirement Plan’s benefit obligation and assets attributable to participants who terminated employment prior to January 1, 2015 with a vested benefit were transferred to the Pre-2015 Plan as of the effective date. In addition to the pension programs, Rush also provides postretirement health care benefits for certain employees. Further benefits under the postretirement healthcare plans have been curtailed. Contingencies

RUMC has settled its breach of contract claim against architect Perkins+Will, Inc. and its mechanical design subcontractor, Environmental Systems Design, Inc. (ESD), relating to alleged errors and omissions by the defendants in the design of the Tower. A $9 million settlement was recorded as an offset to depreciation expense in December 2015. RUMC also settled its case against ASI, Ohio Farmers’ Insurance, and Illinois National Insurance for construction and design defects in the Tower. Under the settlement agreement, RUMC will receive $8 million from the parties on August 25, 2016. In addition, in the ordinary course of business, Rush receives new lawsuits containing allegations of professional liability and/or general liability. Investment Policies

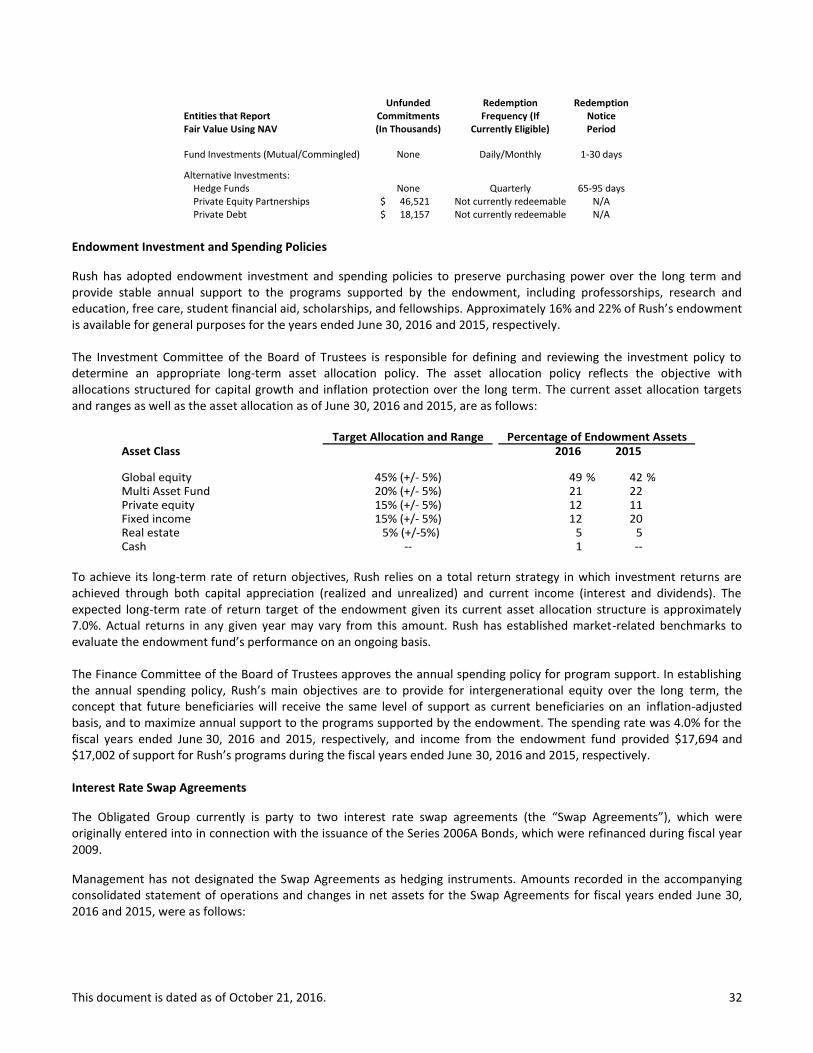

The Obligated Group’s investment program consists of unrestricted cash and investments, an endowment at RUMC and RCMC and investment trusts maintained for the specific purpose of funding RUMC’s self-insured general and professional liability claims, and RUMC’s defined benefit plan. The Investment Committee of the Board of Trustees at RUMC has the primary purpose of assisting the Board of Trustees in the oversight of RUMC’s asset pools, and specifically, assets in the self-insurance trust, endowment fund, and Master Retirement Trust and investment offerings in the defined contribution plans. The Finance Committee of the Board of Trustees at RUMC has similar responsibilities for unrestricted cash and investments. The Finance Committee of the Board of Directors at RCMC is responsible for determining and implementing all investment policies, selecting and terminating investment managers and reviewing investment performance.

The Obligated Group’s unrestricted cash and investments consisted of the following as of June 30, 2016 and 2015:

This document is dated as of October 21, 2016. 28

The objective of the RUMC self-insurance trust is to fund the self-insurance obligations of RUMC. As of June 30, 2016 the self-insurance trust assets had a market value of $130.3 million versus a market value of $138.0 million as of June 30, 2015. The decrease in the self-insurance trust assets related to the investment income of approximately $1.1 million and $54.6 million payout of claims and related fees during fiscal year ended June 30, 2016. The following table shows the current asset allocation targets and ranges as well as the asset allocation as of June 30, 2016, and for June 30, 2015 for the self-insurance trust:

RUMC uses the total return concept to record returns on investments in its self-insurance trust. RCMC does not maintain a self-insurance trust to fund its self-insurance obligations. As of June 30, 2016, approximately $18.8 million of RCMC’s unrestricted cash and investments is estimated to be required to fund self-insurance obligations.

Fair Value Measurements

As of June 30, 2016 and 2015, Rush held certain assets and liabilities that are required to be measured at fair value on a recurring basis, including marketable securities and short-term investments, certain restricted, trusteed and other investments, derivative instruments, and beneficial interests in trusts. Certain alternative investments measured using either the cost or equity method of accounting are excluded from the fair value disclosure provided herein.

Valuation Principles

Under FASB guidance on fair value measurements, fair value is defined as an exit price, representing the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The valuation techniques used to measure fair value are based upon observable and unobservable inputs. Observable inputs generally reflect market data from independent sources and are supported by market activity, while unobservable inputs are generally unsupported by market activity. The three-level valuation hierarchy, which prioritizes the inputs used in measuring fair value of an asset or liability at the measurement date, includes:

Level 1 inputs — Quoted prices (unadjusted) for identical assets or liabilities in active markets. Securities typically priced using Level 1 inputs include listed equities and exchange-traded mutual funds.

Level 2 inputs — Quoted prices for similar assets or liabilities in active markets, quoted prices for identical or similar assets and liabilities in nonactive markets, and model-driven valuations whose inputs are observable for the asset or liability, either directly or indirectly. Securities typically priced using Level 2 inputs include government bonds (including US treasuries and agencies), corporate and municipal bonds, collateralized obligations, interest rate swaps, commercial paper and currency options.

Asset Summary

(In millions)

2016 2015

Cash and Cash Equivalents 156$ 146$

Fixed Income Securities 488 523

Public Equity 298 260

Multi-Asset 174 168

Other 47 51

Total 1,163$ 1,148$

Total Unrestricted Cash & Investments

Fiscal Year Ended June 30,

Asset Class Jun 30, 2016 Jun 30, 2015

Fixed Income 75% (+/-5%) 67% 74%

Domestic Equity 25% (+/-5%) 27% 26%

Cash/Money Market -- -- 6% --

Percentage Trust Assets as of

Target Allocation and Range

This document is dated as of October 21, 2016. 29

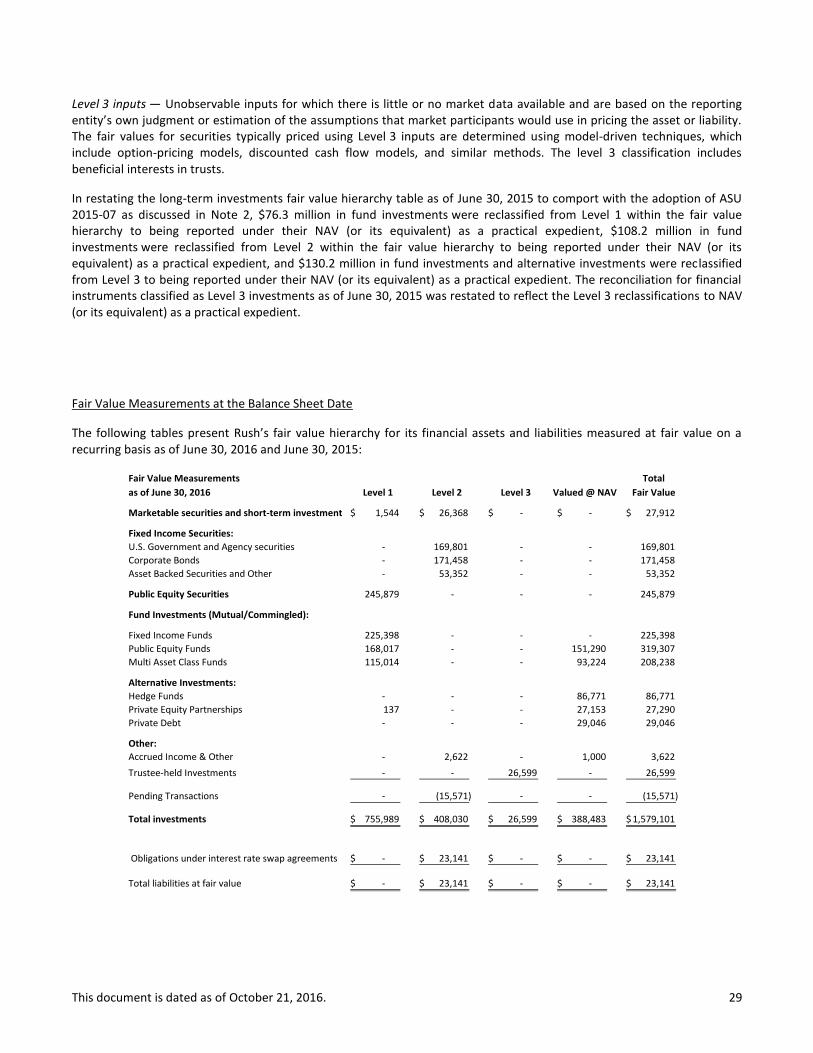

Level 3 inputs — Unobservable inputs for which there is little or no market data available and are based on the reporting entity’s own judgment or estimation of the assumptions that market participants would use in pricing the asset or liability. The fair values for securities typically priced using Level 3 inputs are determined using model-driven techniques, which include option-pricing models, discounted cash flow models, and similar methods. The level 3 classification includes beneficial interests in trusts.

In restating the long-term investments fair value hierarchy table as of June 30, 2015 to comport with the adoption of ASU 2015-07 as discussed in Note 2, $76.3 million in fund investments were reclassified from Level 1 within the fair value hierarchy to being reported under their NAV (or its equivalent) as a practical expedient, $108.2 million in fund investments were reclassified from Level 2 within the fair value hierarchy to being reported under their NAV (or its equivalent) as a practical expedient, and $130.2 million in fund investments and alternative investments were reclassified from Level 3 to being reported under their NAV (or its equivalent) as a practical expedient. The reconciliation for financial instruments classified as Level 3 investments as of June 30, 2015 was restated to reflect the Level 3 reclassifications to NAV (or its equivalent) as a practical expedient.

Fair Value Measurements at the Balance Sheet Date

The following tables present Rush’s fair value hierarchy for its financial assets and liabilities measured at fair value on a recurring basis as of June 30, 2016 and June 30, 2015:

Fair Value Measurements Total

as of June 30, 2016 Level 1 Level 2 Level 3 Valued @ NAV Fair Value

Marketable securities and short-term investments 1,544$ 26,368$ - $ - $ 27,912$

Fixed Income Securities:

U.S. Government and Agency securities - 169,801 - - 169,801

Corporate Bonds - 171,458 - - 171,458

Asset Backed Securities and Other - 53,352 - - 53,352

Public Equity Securities 245,879 - - - 245,879

Fund Investments (Mutual/Commingled):

Fixed Income Funds 225,398 - - - 225,398

Public Equity Funds 168,017 - - 151,290 319,307

Multi Asset Class Funds 115,014 - - 93,224 208,238

Alternative Investments:

Hedge Funds - - - 86,771 86,771

Private Equity Partnerships 137 - - 27,153 27,290

Private Debt - - - 29,046 29,046

Other:

Accrued Income & Other - 2,622 - 1,000 3,622

Trustee-held Investments - - 26,599 - 26,599

Pending Transactions - (15,571) - - (15,571)

Total investments 755,989$ 408,030$ 26,599$ 388,483$ 1,579,101$

Obligations under interest rate swap agreements - $ 23,141$ - $ - $ 23,141$

Total liabilities at fair value - $ 23,141$ - $ - $ 23,141$

This document is dated as of October 21, 2016. 30

Fair Value Measurements Total

as of June 30, 2015 Level 1 Level 2 Level 3 Valued @ NAV Fair Value

Marketable securities and short-term investments 2,299$ 31,299$ - $ - $ 33,598$

Fixed Income Securities:

U.S. Government and Agency securities - 186,629 - - 186,629

Corporate Bonds - 155,853 - - 155,853

Asset Backed Securities and Other - 65,351 - - 65,351

Public Equity Securities 233,447 - - - 233,447

Fund Investments (Mutual/Commingled):

Fixed Income Funds 300,848 - - - 300,848

Public Equity Funds 154,771 - - 93,981 248,752

Multi Asset Class Funds 114,515 166 - 97,726 212,407

Alternative Investments:

Hedge Funds - - - 89,726 89,726

Private Equity Partnerships - - - 17,337 17,337

Private Debt - - - 15,729 15,729

Other:

Accrued Income & Other - 2,770 - - 2,770

Trustee-held Investments - - 28,344 - 28,344

Pending Transactions - (219) - - (219)

Total investments 805,880$ 441,848$ 28,344$ 314,500$ 1,590,572$

Obligations under interest rate swap agreements - $ 18,092$ - $ - $ 18,092$

Total liabilities at fair value - $ 18,092$ - $ - $ 18,092$

During fiscal year ended June 30, 2015, there were security transfers of $4.3 million from Levels 1 to Level 2 due to a reclassification of an underlying holding.

Valuation Techniques and Inputs for Level 2 and Level 3 Instruments

The Level 2 and Level 3 instruments listed in the preceding fair value tables use the following valuation techniques and inputs as of the valuation date:

Marketable Securities and Short-term Investments – Marketable securities classified as Level 2 are invested in a short-term collective fund that serves as an investment vehicle for cash reserves. Fair value was determined using the calculated NAV as of the valuation date, based on a constant price. These funds are invested in high-grade and short-term money market instruments with daily liquidity.

Fixed Income Securities – Fixed income securities consists primarily of U.S. Government and agency securities, corporate bonds, and asset backed securities, all of which are classified as Level 2. The fair value of investments in U.S. government and agency securities and corporate bonds was primarily determined using techniques consistent with the market approach, including matrix pricing and significant observable inputs of institutional bids, trade data, broker and dealer quotes, discount rates, issues spreads, and benchmark yield curves. The asset backed securities encompasses collateralized bond obligations, collateralized loan and mortgage obligations any other asset backed securities. The fair value of these securities was determined using techniques consistent with the market and income approach, such as discounted cash flows and matrix pricing.

Fund Investments – Investments in this category classified as Level 2 are held in a commingled fund that invests primarily in global equity and bond mutual funds. The fair value of this commingled fund is based upon the calculated NAV at the valuation date under a market approach. Investments in this category classified as NAV, which are invested in a multistrategy hedge fund, are priced on the last business day of each calendar month. The values of the underlying investments are estimated based on many factors, including operating performance,

This document is dated as of October 21, 2016. 31

balance sheet indicators, growth, and other market and business fundamentals. The underlying investment strategies can include long-short, global macro, fixed-income and currency hedges, and other tactical opportunity-related strategies.

Beneficial Interest in Trusts – The fair value of beneficial interests in perpetual and charitable trusts classified as Level 3 was determined using an income approach based on the present value of expected future cash flows to be received from the trust or based on Rush’s beneficial interest in the investments held in the trust measured at fair value. Since Rush is unable to liquidate the funds held and benefits only from the distributions generated off of such investments, the interest in such trusts are all shown in Level 3.