road to the euro

TRANSCRIPT

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 1/31

Euro formation and itscrisis

Financial risk management

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 2/31

Eurozone - Introduction

Eurozone is an Economic Monetary Union of 17 European

member states.

These states have adopted Euro as their sole tradingcurrency.

The Eurozone came into existence with the official launch of

the euro (alongside national currencies) on 1 January 1999.

Euro banknotes and coins were put into circulation for cash

payments on 1 January 2002.

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 3/31

Members of Eurozone

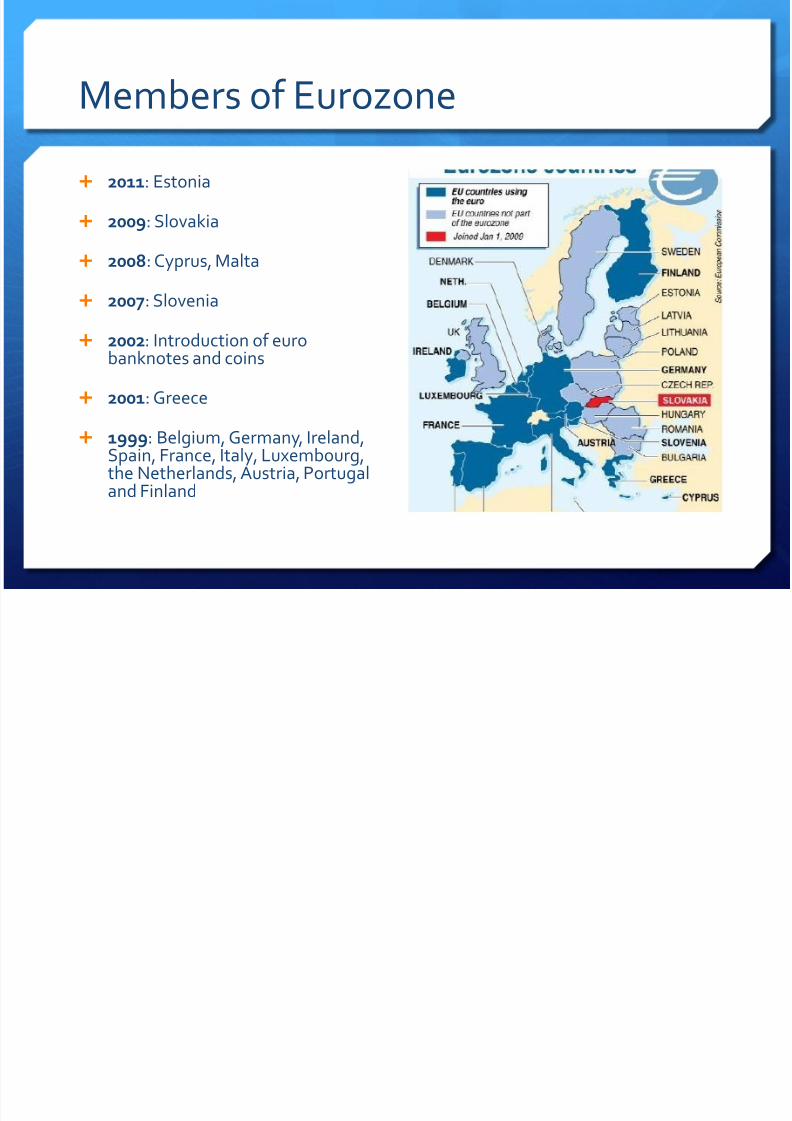

2011: Estonia

2009: Slovakia

2008: Cyprus, Malta

2007: Slovenia

2002: Introduction of eurobanknotes and coins

2001: Greece

1999: Belgium, Germany, Ireland,Spain, France, Italy, Luxembourg,the Netherlands, Austria, Portugaland Finland

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 4/31

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 5/31

Eurozone formation (Contd..)

One of the major turning points that led to the formation of

Euro was when the United States abandoned the gold

standard in 1971 .

Floating currencies raised the inevitability of currency

competition among the European states, the exact sort of

competition that contributed to the Great Depression 40

years earlier.

Thus there was a need of a single currency that would be

used for the whole of the European Union.

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 6/31

Advantages of a single currency

The single European currency stimulates trade activities and

free movement of capital, goods and people but these effects

should be subject to a profound academic research.

Obliteration of the existing exchange rate fluctuations

between a number of currencies and reduction of transaction

costs.

The euro exchange rate does not offer shelter from currencyfluctuations in general but provides predictability and unifies

the means of exchange in all countries in the Eurozone.

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 7/31

Convergence criteria

To join the eurozone, a country must abide by rigorous “convergencecriteria”.

The criteria include:

1. A budget deficit of less than 3 percent of gross domestic product(GDP);

2. Government debt levels of less than 60 percent of GDP;

3. Annual inflation no higher than 1.5 percentage points above the

average of the lowest three members’ annual inflation;

4. A two-year trial period during which the acceding country’s nationalcurrency must float within a plus-or-minus 15 percent currency bandagainst the euro.

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 8/31

European Central Bank

The European Central Bank and the national central banks

together constitute the Eurosystem, the central banking

system of the euro area.

The main objective of the Eurosystem is to maintain price

stability: safeguarding the value of the euro.

Furthermore, it has the exclusive right to authorize the

issuance of euro banknotes.

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 9/31

Role of ECB

The Bank achieves its objectives by, among other means,controlling the supply of money in the Eurozone and determiningkey interest rates.

The ECB also has the task of controlling the Eurozone’s foreigncurrency reserves and of buying and selling individual currencies asrequired to keep exchange rates within reasonable limits.

Setting key interest rates is an important tool in the ECB arsenal.

The ECB works closely with the central banks in all 27 EU membercountries. Collectively, the ECB and these member central banksform the European System of Central Banks (ESCB).

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 10/31

ROAD TO THE EURO

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 11/31

On May 9,1950 France and Germany decided to pool their coal andsteel production.

This coal and steel community gradually evolved to a customs

union for free trade of goods.

After the fall of communism , democracy spread through Europeand Greece, Spain , Portugal were brought into the union.

Soon borders were opened , freedom of personal movement was

guaranteed paving the way to full economic integration.

Hence creation of the euro was next logical step to complete thesense of European unity.

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 12/31

THE (UNEASY) CASE FOR MONETARY

UNION

Euro was introduced to make inter-country trades lessunpredictable. However trade among euro nations were uponly 10-15% , not a transformative figure.

Assuming the euro would be as successful as the dollar was awrong notion from start because –

Europe is not fiscally integrated. German taxpayers do notpay for Irish bank bailouts or Greek pension funds.

Lack of a common language makes workers lessgeographically mobile in times of high unemployment ascompared to their American counterparts.

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 13/31

Also by giving up on one’s own currency, a country givesup its economic flexibility.

In times of economic recession, effecting a wage cut isextremely difficult.

But with one’s own currency a country can simpledevalue it to effect a de-facto wage cut.

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 14/31

EUPHORIA EUROCRISIS

The euro officially came into existence on Jan 1, 1999.However the final transition to European money happenedafter 3 years.

The creation of the euro instilled a new confidence especiallyin those European countries which had historically beenconsidered risky investments.

An example of this was Greece, with a long history of highinflation and debt defaults.

The risk premium on Greece bonds melted away becauseinvestors thought incase of bankruptcy the European CentralBank(ECB) would bail it out.

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 15/31

Country-specific fiscal woes had vanished. Greek bonds, Spanishbonds, Irish bonds and Portuguese bonds traded as if they were assafe as German bonds.

The traditionally high interest rate countries went on a borrowingspree which was largely financed by banks in Germany.

There was a huge real estate boom and prices rose 180%.

Germany too recovered from a depression fuelled by the export

boom driven by it’s European neighbor's spending sprees.

Then the bubble burst.

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 16/31

The financial crisis spread to Europe causing the real estate bubble toburst and employment to crash since real estate accounted for 13%employment in Spain and Ireland.

Employment rates fell to 10% in Spain and 14% in Ireland.

These governments ran into huge deficits since tax receipts thatdepended on real estate transactions declined and cost of unemployment benefits soared.

Greece government ran into huge debts leading to flight of investors.

Deflation is the only way to pull the European continent out of thiscrisis. However apart from the obvious problem of driving down wagesthere is another problem.

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 17/31

Collision between deflating incomes and unchangeddebt causes debtors to meet the same obligations withlower income.

This is done by further cutting down expenditurethereby further pushing the economy into deeperrecession in a vicious cycle.

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 18/31

FOUR WAYS OUT

Willingness to endure fiscal austerity and slashing of wages to restore investor confidence.

Debt restructuring

Combination of default and devaluation

Revived Europeanism- convincing German taxpayers to

bear the brunt of bailouts.

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 19/31

Impact and Recovery

Measures Of Euro Crisis

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 20/31

Recovery Measures

There are a wide range of recovery measures implementedby the EU,ECB, and IMF .

1. The ECB Attempted to Stimulate Economic Activity byEasing Collateral Requirements and Lending More Money.

2. The ECB Began a Controversial Bond Buying Program in anEffort to Keep Borrowing Costs Down for StrugglingMember States

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 21/31

Recovery Measures(Cont…)

The ECB Offered Unlimited Dollar Loans to Further StimulateEconomic Growth and Encourage Market Activity.

The EU, European Central Banks, and the IMF Unveiled a € 750Rescue Plan.

Formation of organisations like EFSF: (European FinancialStability Facility),EFSM(European Financial StabilisationMechanism) to provide financial assistance.

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 22/31

Recovery Measures EFSF

EFSF: EUROEAN FINANCIAL STABILITY FACILITY:

In May 2010, the 27 EU member states agreed to create the EFSF, a legalinstrument aiming at preserving financial stability in Europe by providing financialassistance to Eurozone states in difficulty through issue of bonds.

It has financed the following eurozone countries

€17.7 billion of the total €67.5 billion rescue package for Ireland (the rest was loaned fromindividual European countries, the European Commission and the IMF).

It contributed one-third of the €78 billion package for Portugal.

As part of the second bailout for Greece, the loan was shifted to the EFSF, amountingto €164 billion .

On 20 July 2012, European finance ministers sanctioned the first tranche of a partial bail-out worth up to €100 billion for Spanish banks.[

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 23/31

Recovery Measures EFSM

European Financial Stabilisation Mechanism (EFSM):

On 5 January 2011, the European Union created theEFSM, an emergency funding programme reliant uponfunds raised on the financial markets and guaranteed bythe European Commission using the budget of theEuropean Union as collateral.

Under the EFSM, the EU successfully placed in thecapital markets a €5 billion issue of bonds as part of thefinancial support package agreed for Ireland, at aborrowing cost for the EFSM of 2.59%

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 24/31

Impact of Euro Crisis On

European Countries

US Economy

Indian Economy

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 25/31

Impact On US Economy

The Euro Crisis affected the US economy in thefollowing ways:

1. Trade:

Euro had depreciated against Euro by almost 15%. This

devaluation of the Euro that was triggered by the crisismade American exports more expensive.

2. Decline in American manufacturing Sector:

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 26/31

Impact On US Economy (Cont…)

3. Banking Sector:

The second concern related to the banking sector as the

banks across the Atlantic were highly integrated witheach other, they were widely affected.

4. Unemployment was seen on a rise

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 27/31

Impact On Indian Economy

1. Impact on Indian Financial markets:

The debt crisis had negatively impacted the Indian Stock Marketas the Europeans had pulled out their funds from the Indian stock

markets, further leading to lower foreign currency reserves.

2. Trade:

27% of India’s trade was with European countries, (with 20% of exports and 13% of imports approx) and the euro crisis hadimpacted India’s exports to the region by a complete 1% decline.

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 28/31

Impact On IndianEconomy (Cont..)

3.Tourism:

Europe accounts for more than one-third of total tourist arrivals inIndia. Travel receipts have also suffered.

4.Depreciated of the rupee:

Slow growth in Europe has coaxed the investors to invest in US

dollar. This has enabled the US dollar to appreciate as compared toother currencies in the world. Dropping exports coupled with risingcrude oil prices has created immense pressure on Indian rupee,which in turn has depreciated with respect to US dollar.

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 29/31

Impact On Indian Economy (Cont..)

5. Slowdown in the manufacturing and the service sectors:

Due to the contraction in European and American

markets, the demand of goods and services fromcountries like India and China have slowed down .

6. No significant Impact on FDI flows in India

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 30/31

Current Scenario

The European Fiscal Compact that has come into force in 2013 is amove towards a complete economic integration of eurozonecountries, under the 3% “grail” – this number marking the limit fornational budget deficits.

To finance their expenses, states rely on their fiscal revenues andon loans they take out on the financial markets .

Countries of Southern Europe have chosen to reach this goalthrough violent cuts in public spending and a considerable raise of

taxes.

Various other austerity measures are also taken to reduce spendingand cut more borrowing at various levels.

7/27/2019 Road to the Euro

http://slidepdf.com/reader/full/road-to-the-euro 31/31

THANK YOU-SUSHMITA BHATACHARYA

-NISHIT HATHI-PRIYANKA JAIDEEP-RISHIKA PODDAR