rgnul-ipan working paper series 2012 · rgnul-ipan working paper series 2012 ......

TRANSCRIPT

RGNUL-IPAN Working Paper Series 2012

Call for Submissions (With Attached Concept Note)

FDI IN MULTI-BRAND RETAIL IN INDIA

International Policy Analysis Network, Asia‘s first youth-led public policy think tank has initiated an

Annual Working Paper Series in association with School of Agriculture Law and Economics (SALE),

Rajiv Gandhi National University of Law, India from the year 2012. The Research Theme for 2012

edition of this series is “FDI in Multi-Brand Retail in India”. Students, academicians and Ph.D

scholars are invited to submit papers to this Working Paper Series. Papers should address some

specific social, political, economic or cultural aspect of this policy.

Foreign contributors are especially encouraged to submit their contributions which discuss their

own country‘s experience in Organised Retail Sector. Even though the issue is essentially a policy

action by Govt. of India, the objective of this project is to stimulate and promote inter-disciplinary,

multi-jurisdictional and comparative public policy analysis.

This series for 2012-2013 will culminate with an international seminar or a book release by April,

2013. Next edition of the series with a new call for submissions will be issued in late October, 2013.

Contributions selected by a peer review panel will be notified about their prospective

presentation/publication by April, 2013.

The RGNUL-IPAN Working Paper Series is intended to:

Present high quality research and writing (including research in-progress) to a wide audience

of academics, policy-makers and commercial/media organizations.

Set the agenda in the broad field of public policy and sustainable development.

Stimulate and inform debate and policy, especially amongst youth.

Series Editor: Ms. Brindpreet Kaur

Coordinator, School of Agriculture Law and Economics (SALE)

Rajiv Gandhi National University of Law, Punjab, India

Series Asst. Editor: Mr. Kshitij Bansal

President, International Policy Analysis Network (IPAN)

Research Assistants:

1. Ms. Sonali Dhanker, IPAN Research Coordinator

2. Mr. Angshuman Hazarika, IPAN Research Coordinator

3. Mr. Nikhil Suresh Pareek, RGNUL Student of Law

4. Ms. Aparajita Paul, RGNUL Student of Law

5. Mr. Ankush Thakur, RGNUL Student of Law

The Editorial Board is comprised of RGNUL academics and IPAN experts with a wide range of

interests in public policy and economic research. They come from a variety of disciplinary

perspectives including economics, geography, law, politics, sociology, cultural, gender and

development studies.

Submission Guidelines

Contributors are encouraged to submit papers that address any specific social, political, economic or

cultural aspect of this retail policy, including its forms, institutions, audiences and experiences, and

its global, national, regional and local development. Specific and micro case studies are specifically

encouraged.

Contributors are highly encouraged to go through the detailed Concept Note attached with this call.

They should bear in mind when they are preparing their paper that it will be available online for

public reading.

The deadline for submissions is January 31, 2013.

Papers should conform to the following format:

3000-5000 words (excluding bibliography, including footnotes).

150-200 word abstract.

Headings and sub-headings are encouraged.

Chicago Manual of Citation should be strictly adhered to.

Papers should be prepared as a PC compatible Microsoft Word (2003 or 2007) file.

Graphs, pictures and tables should be included as appropriate in the same file as the paper.

The paper should be sent by email to:

(With the subject line as “SUBMISSION_RETAIL POLICY WORKING PAPER”)

Mr. Kshitij Bansal, Series Asst. Editor

For regular updates on this series and other IPAN initiatives:

www.facebook.com/IPANglobal

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

RGNUL-IPAN WORKING PAPER 2012

ON

FOREIGN DIRECT INVESTMENT IN MULTI BRAND RETAIL IN

INDIA

NOTE: This concept note is a part of RGNUL-IPAN Working Paper Series. IPAN and

RGNUL hold exclusive rights over its use and distribution. Unauthorised use of this

document in any form is strictly prohibited. The views expressed here are of the

Research Assistants involved in this project and don’t reflect those of International

Policy Analysis Network (IPAN) or of RGNUL.

PART 1: INTRODUCTION

Foreign Direct Investment in retail has a major significance in the present economic setup of Indian

economy. A major shift in the policy of Foreign Direct Investment (hereinafter referred to as FDI)

climate has provided an interesting future option to several international retailers' entry and

expansion plans for India. Foreign Direct Investment in multi-brand retail is an economic reform

which would allow global chains like Wal-Mart, Carrefour and Tesco etc. to own up to 51 percent of

joint retail ventures with Indian companies. The policy would let foreign retailers own up to 51

percent in multibrand retailing and 100 percent of single brand retailing.1

According to Deardoff’s Glossary of International Economics, FDI is defined as ―Acquisition or

construction of physical capital by a firm from one (source) country in another (host) country.‖2 FDI

is also stated as ―Investment that is made to acquire a lasting interest in an enterprise operating in an

1 Agencies, ―What‘s FDI in retail?‖ Hindustan Times, Nov. 29, 2012. Available at http://www.hindustantimes.com/India-

news/NewDelhi/What-s-FDI-in-retail/Article1-775543.aspx, Last accessed on 14 October, 2012.

2 Deardoff‟s Glossary of International Economics. Available at

http://www-personal.umich.edu/~alandear/glossary/f.html#fdi2, Last accessed on 12 October, 2012.

CONCEPT NOTE:

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

economy other than that of the investor, the investor‘s purpose being to have an effective voice in the

management of enterprise‖.3

It is the stated intent and objective of the Government of India to attract and promote foreign direct

investment in order to supplement domestic capital, technology and skills, for accelerated economic

growth. ―Foreign Direct Investment, as distinguished from portfolio investment, has the connotation

of establishing a lasting interest in an enterprise that is resident in an economy other than that of the

investor.‖4

Latest Policy Move:

The policy cleared by Union Cabinet stipulates that FDI in multi brand retail will be allowed up to

51% foreign equity through the government approval route, subject to adequate safeguards for

domestic stakeholders. The policy rollout will cover only cities with a population of more than 1

million5. It also specifies at least 30% of the procurement of manufactured/processed products must

be sourced from Indian ―small industries‖. 'Small industries' have been defined as industries which

have a total investment in plant & machinery not exceeding US $ 1.00 million.6

Organized retail penetration remains low, at 5 to 6 percent indicating room for growth.7 This provides

ample space for multi brand retailers to setup and explore the retail investment environment in India.

3 International Monetary Fund, Balance of Payments Manual, Washington, DC, 1977, pp.408

4 Circular 1 of 2012, Chapter 1, P. 6, Intent and Objective, Dept. Of Industrial Policy and Promotion, Ministry Of

Commerce And Industry (Circular On Consolidated FDI Policy),

Available At Http://Dipp.Nic.In/English/Policies/FDI_Circular_01_2012.Pdf, Last accessed on 14October, 2012.

5 Press Release Id 77725, Press Information Bureau, Government of India,

Available at http://pib.nic.in/newsite/erelease.aspx?relid=77725, Last accessed on 9 October, 2012.

6 Press Note No.4 (2012 Series), Ministry Of Commerce and Industry, Government of India.

Available at http://dipp.nic.in/English/acts_rules/Press_Notes/pn4_2012.pdf, Last accessed on 08October, 2012.

7 News release, 2012 Global Retail Development Index, June 11, 2012, AT Kearney, Global management consultancy

firm. Available at http://www.atkearney.com/consumer-products-retail/global-retail-development-index/news-release/-

/asset_publisher/56Fncka0K9JJ/content/brazil-tops-a-t-%C2%A0kearney-global-retail-development-index-for-the-

second-year/10192., Last accessed on 14October, 2012.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

What is Single Brand Retailing and Multibrand Retailing?

Single brand retailing: its meaning says own label brands or they can be described as those which are

created and owned by businesses that operate in the distribution channel. Single brand implies that

foreign companies would be allowed to sell goods sold internationally under a ‗single brand‘, viz.,

Reebok, Nokia and Adidas. FDI in ‗Single brand‘ retail implies that a retail store with foreign

investment can only sell one brand. For example, if ‗Nike‘ were to obtain permission to retail its

flagship brand in India, those retail outlets could only sell products under the ‗Nike‘ brand and not

the ‗Reebok‘ brand, for which separate permission is required.

Foreign direct investment in multi brand retail means that foreign players can sell multiple brands of

his parent company in another country under one roof. Multi Brand Retail allows foreign companies

to sell goods of more than one brand under one roof viz. Wal-Mart, Tesco etc. For example, in India,

Pantaloons is a multibrand retail shop where if talked about garments, one can sell Reebok, Nike and

Adidas under one roof only.

It is only after Press release of Ministry of Commerce and Industry, that Foreign Direct Investment in

multi brand retail is allowed8. Opening up FDI in multi-brand retail will mean that global retailers

will offer a range of daily use items which are directly related to consumers in same way as other

local ‗kirana‘ shops sell.

History of FDI in Retail in India:

The advent of FDI in general in India was witnessed during the end of 1990‘s when government

announced number of reforms which helped in the process of liberalisation and deregulation of the

economy. Since its inception there has been significant upsurge in the FDI flows in the country. But

when we talk about FDI in retail, it came quite late in 2006.

Prior to 2006, India prohibited FDI in both single brand and multi brand retail. In the second month

of 2006, government decided to open retail sector for FDI which was subject to certain conditions. At

8 Press Note No. 5 (2012 Series), Dept. Of Industrial Policy and Promotion, Ministry Of Commerce And Industry 14-09-

2012. Available At http://Dipp.Nic.In/English/Acts_Rules/Press_Notes/Pn4_2012.Pdf, Last accessed on 07 October,

2012.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

that time government provided 51 percent FDI in single brand retail.9 There have been

recommendations to further liberalize the Indian government‘s policy regarding FDI in retail trading,

including to increase the permissible level of FDI in single-brand retail operations and to open up the

multi-brand retail sector to FDI.

In November 2011, the Union Cabinet of Ministers, decided to permit up to 100 percent FDI in

single-brand retail trading and up to 51 percent FDI in multi-brand retail trading. Unfortunately for

foreign retailers, the Cabinet‘s November 2011 decision produced a considerable political backlash in

India. The political backlash was mainly focused on multi brand aspect of the FDI. Consequently, the

Indian government reversed course and indefinitely suspended plans to reform the retail sector. But

later government of India on January 12, 2012 allowed 100 percent FDI in single brand retail10

and

still there was no FDI in multi brand retail in the country.

Later amidst rising inflation, policy paralysis, risk of low grading by credit rating agencies and

surging deficits, Government of India decided to allow 51 percent FDI in multi brand retail.11

General Nature of Indian Retail Sector:

India is one of the most desirable retail destinations in the world due to a large middle class which

has a dispensable income. India‘s economic growth and demographic profile set it apart from others

Developing Nations and set up a case for global retailers to enter the market. Retailing is a significant

sector of the economy, both in terms of GDP contribution and share in public employment. Although

there is no set definition for retail but to opt for a reliable authority, the definition of retail was given

by the Delhi High Court in the case of Association of Traders of Maharashtra V. Union of

India12

defined ―retail as sale of final consumption or sale to ultimate consumer‖. A manufacturer

selling his own brand is not retailing. Retailing is the bridge between the manufacturer and the final

consumer and falls last in the distribution chain having interface with the end customer.

9 Press Note 3 (2006 Series), Issued On February 10, 2006, Issued By Dipp. Ministry Of Commerce And Industry.

Available At http://Www.Ksidc.Org/FDI_Policy_2006.Pdf, Last accessed on 06 October, 2012.

10 Press Note 1 (2012 Series), Issued On January 10, 2012, Issued By Ministry Of Commerce and Industry. Available At

http://Dipp.Nic.In/English/Acts_Rules/Press_Notes/Pn1_2012.Pdf, Last accessed on 07October, 2012.

11 Press Note 5 (2012 Series), Issued On January 10, 2012, Issued By Ministry Of Commerce And Industry. Available At

http://Rbidocs.Rbi.Org.In/Rdocs/Content/Pdfs/PRES210912_5.Pdf, Last accessed on 07October, 2012.

12 Federation Of Association Of Traders v. Union Of India, 2005 (79) DRJ 426.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

There is no definition of retail trade under the FDI policy. In layman‘s term it means selling of goods

to the consumer. So from local Kirana shops and mall based shopping formats, both form part of

retail sector. From street/cart retailers working on pavements/roadsides and small family run

businesses to international brands such as Rolex and Nike, the retail market in India is vibrant,

colourful and highly fragmented. In India, the retail industry is divided into organised and

unorganized sectors. Organised retailing refers to trading activities undertaken by licensed retailers,

that is, those who are registered for sales tax, income tax, etc. These include the corporate-backed

hypermarkets and retail chains, and also the privately owned large retail businesses.13

Unorganised

retailing, on the other hand, is dominated by large number of small retailers consisting of local kirana

shops, owner manned general stores, chemists, footwear shops, paan or beedi shops, pavement

vendors etc. which together make up the so called ―unorganised retail‖ or traditional retail14

.

At Kearney, a global management consulting firm, rates India as the most attractive nation for retail

investment. The study, presented in the Global Retail Development Index of 2012, is carried out

annually for 30 emerging markets, and has rated India fifth in all emerging markets. This report

expresses even more optimism, and estimates that suggests that India's retail market is expected to be

about US$535 billion by 2013, with around 10 per cent coming from organized retail.15

.

Indian retail is mainly dominant with small and medium enterprises in contradiction to the presence

of few giant corporate retailing outlets. Coming up of FDI in retail may see a significant shift in

Indian retail industry.

Key Features of the Policy:

Following are certain conditions which have been specified under the Press Note no. 5 of 201216

and

the foreign players have to comply with the same.

13

―Retailing, India In Business, Investment Technology Promotion Division, Ministry Of External Affairs, Govt. Of

India‖, Available at http://www.indiainbusiness.nic.in/industry-infrastructure/service-sectors/retailing.htm, Last accessed

on 09 October, 2012.

14 Ibid

15 ―Global Retail Expansion: Keeps On Moving 2012‘, Atkearny,

Available at http://www.atkearney.com/documents/10192/4799f4e6-b20b-4605-9aa8-3ef451098f8a, Last accessed on 14

October, 2012.

16 Press Note No. 5 of 2012, Govt. Of India,

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

As per paragraph 6.1 of the press note FDI is prohibited in :

(a) Lottery Business, including Government /private lottery, online lotteries, etc.

(b) Gambling and Betting, including casinos etc.

(c) Chit funds

(d) Nidhi company

(e) Trading in Transferable Development Rights (TDRs)

(f) Real Estate Business or Construction of Farm Houses

(g) Manufacturing of Cigars, cheroots, cigarillos and cigarettes, of tobacco or of tobacco

Substitutes.

(h) Activities / sectors not open to private sector investment e.g. Atomic Energy and Railway

Transport (other than Mass Rapid Transport Systems).

Foreign Technology Collaboration in any form, including licensing for franchise, trade

mark, brand name, management contract, is also prohibited for lottery business and Gambling

and Betting activities.

The above policy is an enabling policy only and the State Governments and Union

Territories would be free to take their own decisions in regard to implementation of the

policy. Therefore, retail sales outlets may be set up in those States & union Territories which

have agreed, or agree in future, to allow FDI in MBRT under this policy. The list of States

&Union Territories which have conveyed their agreement is annexed. Such agreement, in

future, to permit establishment of retail outlets under this policy, would be conveyed to the

Government of India through the Department of Industrial Policy & Promotion and additions

would be made to the annexed list accordingly. The establishment of the retail sales outlets

will be in compliance of applicable State &Union Territory laws/ regulations, such as the

Shops and Establishments Act etc.

FDI in retail is left to the discretion of state governments which will decide whether to allow

foreign supermarket chains like Wal-Mart, Carrefour etc.to enter their territory or not.

Available at http://Rbidocs.Rbi.Org.In/Rdocs/Content/Pdfs/PRES210912_5.Pdf, Last accessed on 08October, 2012.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

Minimum amount to be brought in, as FDI, by foreigner investor, would be US $ 100

million. Minimum investment to be made by foreign investor through any multinational is at

least of $1 million. At least half of the total FDI shall consist of ‗back-end infrastructure‘ such

as warehousing and cold storage facilities. This requirement has to be met within three years

of a retailer setting up shop.

At least 30% of the value of procurement of manufactured/ processed products

purchased shall be sourced from Indian 'small industries' which have a total investment in

plant & machinery not exceeding US $ 1.00 million. This valuation refers to the value at the

time of installation, without providing for depreciation. Further, if at any point in time, this

valuation is exceeded, the industry shall not qualify as a 'small industry' for this purpose. This

procurement requirement would have to be met, in the first instance, as an average of five

years' total value of the manufactured! Processed products purchased, beginning 1st April of

the year during which the first tranche of FDI is received. Thereafter, it would have to be met

on an annual basis. The multinational investing in the country will have to source almost one

third i.e. 30% of their manufactured and processed goods from industries with a total plant

and machinery investment of less than $1 million.

Retail sales outlets may be set up only in cities with a population of more than 10 lakh (1

million) as per 2011 Census and may also cover an area of 10 kms around the

municipal/urban agglomeration limits of such cities; retail locations will be restricted to

conforming areas as per the Master/Zonal Plans of the concerned cities and provision will be

made for requisite facilities such as transport connectivity and parking; In States/ Union

Territories not having cities with population of more than 10 lakh as per 2011 Census, retail

sales outlets may be set up in the cities of their choice, preferably the largest city and may

also cover an area of 10 kms around the municipal/urban agglomeration limits of such cities.

The locations of such outlets will be restricted to conforming areas, as per the Master/Zonal

Plans of the concerned cities and provision will be made for requisite facilities such as

transport connectivity and parking..

Retail trading, in any form, by means of e-commerce, would not be permissible, for

companies with FDI, engaged in the activity of multibrand retail trading. The Press Note

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

5 provides that retail trading, in any form, by means of e-commerce, would not be

permissible, for companies with FDI, engaged in the activity of multi-brand retail trading.

This would mean the web platforms carrying out enabling function shall not be impacted but

foreign firms that buy or sell any goods or services on online portals are prohibited under the

FDI policy17

.

Fresh agricultural produce, including fruits, vegetables, flowers, grains, pulses, fresh poultry,

fishery and meat products, may be unbranded.

Government will have the first right to procurement of agricultural products.

At least 50% of total FDI brought in shall be invested in 'backend infrastructure' within

three years of the first tranche of FDI, where 'back-end infrastructure' will include capital

expenditure on all activities, excluding that on front-end units; for instance, back-end

infrastructure will include investment made towards processing, manufacturing, distribution,

design improvement, quality control, packaging, logistics, storage, ware-house, agriculture

market produce infrastructure etc. Expenditure on land cost and rentals, if any, will not be

counted for purposes of back end infrastructure. At least half of the total FDI shall consist of

‗back-end infrastructure‘ such as warehousing and cold storage facilities. This requirement

has to be met within three years of a retailer setting up shop.

Applications would be processed in the Department of Industrial Policy & Promotion, to

determine whether the proposed investment satisfies the notified guidelines, before being

considered by the FIPB for Government approval.

There are few states and union territories which have agreed to allow FDI in multibrand

retail:: States: Andhra Pradesh, Assam, Delhi, Haryana, Jammu & Kashmir, Maharashtra,

Manipur, Rajasthan, Uttarakhand; Union territories: Daman & Diu and Dadra and Nagar

Haveli.

17

Nidhi Bothra, ―FDI in Retail Business: The Key Issues of New Policy”, Moneylife, Sep. 26, 2012. Available at

http://www.moneylife.in/article/fdi-in-retail-business-the-key-issues-of-the-new-policy/28689.html, Last accessed on

07October, 2012.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

There has been a sort of mixed response by policy analysts and corporate masters. Corporate

professionals like Akash Gupta (retail expert at consultancy firm PricewaterhouseCoopers India

Ltd.), estimates that opening up the retail sector will lead to significant improvement of supply-chain

infrastructure, which will help reduce food waste by 30% to 40%. Adi Godrej, president of

the Confederation of Indian Industry, a leading trade body, said coming up of FDI in retail

announcements have ―restarted the reform process‖18

.

18

WSJ Staff, ―FDI in retail: The End of Policy Paralysis‖, The Wall Street Journal. Available at

http://blogs.wsj.com/indiarealtime/2012/09/14/india-reacts-the-end-of-policy-paralysis/, Last accessed on 06October,

2012.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

PART 2: INDIAN RETAIL: WHAT MAKES IT UNIQUE?

It is considered that unorganized Retail is the second step after agriculture for those seeking to

climb the ladder of affluence and in search of higher income.19

The traditional Indian retail sector

is highly fragmented,20

mainly consisting of small, independent and family managed stores/ventures.

The domestic organized retail industry is also at a nascent stage. The factors which affect the sector

at the macro level are the growth of nuclear family structure and the rise of consumerism among the

youth.21

Over the last few years a number of business houses in India22

have started invested in the

field of retail either through the acquisition of existing businesses or through fresh investment. These

business houses include The Aditya Birla Group, Reliance and the Bharti Group.23

Organised Retail in India by Domestic Players:

The advent of the domestic business houses in the retail scenario has led to a huge change in the

domestic retail business scenario due to their deep pockets.24

The focus of the new entrants to the

field of retailing is to capture the eyeball of the customer by providing maximum value coupled with

modern business principles. The new retailers aim to bring in maximum number of repeat customers

and build a stable base.

Although the primary differentiator between the different businesses is price of the products,

however the retailers aim to build their own identity through the following main ways 25

:

(i) By improving sourcing and distribution efficiencies;

(ii) By expanding the product portfolio;

19

Kamaladevi Baskaran, ―The Fdi Permit for Multi Brand Retail Trading in India - Green Signal Or Red Signal‖,

Business Intelligence Journal - January, 2012 Vol.5 No.1, p. 176-186.

20 Natika Jain, ―Consumer Behaviour at Retail Outlet/ Shopping Mall”, Tirpude‟s National Journal of Business Research,

Vol. 2 Issue 1, p. 1

21 Mathew Joseph, Nirupama Soundararajan, Manisha Gupta, Sanghamitra Sahu, ―Working Paper No. 222 Impact of

organized Retailing on the Unorganized Sector‖, Indian Council For Research on International Economic Relations, 2008

22 Manju Smita Dash, ―Next-Generation Retailing In India: An Empirical Study Using Factor Analysis‖, International

Review of Management and Marketing ,Vol. 1, No. 2, 2011, p. 29

23 Retail Insights, Available at http://www.dnb.co.in/IndianRetailIndustry/insight.asp , Last accessed on 12October, 2012.

24 R.Y Naryanan, Temper Expectations from Retail Story, Available at http://www.thehindubusinessline.com/markets

/article3910762.ece , Last accessed on 11October, 2012.

25 Retail Advantage India, IBEF, November, 2010.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

(iii) Providing personalised customer services

(iv) Creating a unique store ambience.

The Indian Retailers who have established stores till date have tried to build a strong sourcing and

distribution network across the country to ensure that they can ensure consistent and stable supplies

of their products. The retailers however had a few teething problems which also resulted in a few

players falling out of the market. However, a few players have emerged strong and look to take

homegrown organised retailing into the coming years.

The Indian home grown organised retailers have also tried to consistently tried to widen their product

portfolio to bring in more variety for the customers. A few players such as Big Bazaar have

consistently ventured into new areas such as electronics and furniture to provide greater variety to the

customers across different product segments.

The growth of organised retail in India has also prompted the players to bring about changes to

ensure customer retention and loyalty. To ensure a steady footfall the businesses have started loyalty

programs and also promotion schemes including branded credit cards and point redemption schemes.

The organised retail sector has also seen constant modifications in the store designing and

maintenance strategies to keep up with the changing consumer preferences. The stores have

consistently tried to innovate with new product presentation and display strategies with an eye to

attract customers across age groups and spending capacities.

Growth in the Domestic Indian Retail Sector

The last decade has seen a sea change in the field of Indian retail. India's retail sector is estimated to touch

US$ 833 billion by 2013 and US$ 1.3 trillion by 2018.26

At present the retail sector contributes 10% to our

GDP and is the largest provider of employment after agriculture. The dynamics of the Indian retail sector

relating to political, social or economic environment has seen stark changes over time which has been

primarily led by the change in consumption patterns. The new millennium has seen a clear bifurcation of the

sector into organise and unorganised retail sectors.27

The fastest growing segments have been the wholesale

26

Tazyn Rahman, ―Organized Retail Industry In India – Opportunities And Challenges”, International Journal of

Research in Finance & Marketing, Volume 2, Issue 2 (February 2012) , p. 83

27 Sanjay Manocha and Anoop Pandey, ―Organized Retailing in India : Challenges and Opportunities‖, VSRD-IJBMR,

Vol. 2 (3), 2012, 79

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

cash and carry stores (150 per cent) followed by supermarkets (100 per cent) and hypermarkets (75-80

per cent). 28

Pattern of Retail Growth In India

The growth of the retail sector in India has been highly skewed to the urban sector and primarily

metropolitan cities due to the high population density and large populations. On comparison between

the different states across the country, it is found that the south Indian states of Tamil Nadu, Kerala,

Karnataka, Andhra Pradesh, lead the way followed by the prosperous West Indian states of

Maharashtra and Gujarat. The new wave of retail in India has now spread it to the peripheries of the

National Capital region and the prosperous states of Punjab and Haryana. The trend of modern retail

in the late 1990s29

started in the southern region as South India has clusters of metro cities and

tier-1 towns. Further, the licensing process in states such as Andhra Pradesh, where the licensing

process is now online, has greatly reduced the time lag.30

Mode Of Entry Into Retail Route

In India, the main players of organised retail have entered into the market through the following

modes:

(a) the acquisition route which gives a jump-start to take advantage of the already

experienced manpower, infrastructure, front-end property of the acquired firm;

Ex: Spencers acquired by RPG.31

(b) the JV partnerships, a preferred route for firms seeking foreign collaboration for

technical know-how and assistance in the back-end operations as well as future export

opportunities. Ex: Bharti Wal-mart India32

(c) New venture route for market entry. Ex: More Stores33

28

Ali Asgar Motiwala, Growth of Malls in India, US Commercial Service.

29 Rohit Bhasin and Bharti Ramola, Winning in India‟s Retails Sector, PwC, Mumbai, Unknown.

30 Available at http://www.indianexpress.com/news/retailers-want-single-window-clearance-for-setting-up-

outlets/205068/, Last accessed on 11October, 2012.

31 Available at http://www.spencersretail.com/cms.php?page=milestones , Last accessed on 10 October, 2012.

32 Available at http://ibnlive.in.com/news/bhartiwalmart-will-be-a-5050-pc-partnership-rajan-mittal/296496-7.html , Last

accessed on 11October, 2012.

33 Available at http://www.morestore.com/abt_retail.html , Last accessed on 12 October, 2012.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

(d) Mixture of Acquisition and JV routes for quick market access.

To take advantage of the second wave of business now, the firms have moved into the formation of

subsidiaries or specialised stores targeting a particular population group. The firms are normally

present in one or both of the segments: lifestyle and value retailing under multiple retail formats

except for a few exceptions which target only one of the sectors. The leaders in the Indian Retail

sector are adopting a combination of formats including, mega (hyper and/or super), medium

(department and/or speciality), and small size (convenience and/or discount) for expansion. Rapid

expansion by the firms helps them to:

(i) Attain a large size increasing the bargaining power;

(ii) Economies of scope in sourcing by accruing costs across stores; and

(iii) Reach out to consumers at their doorsteps.

Understanding the way Indian Mega Retailers Run

Through this section we look into the important players of the organised retail market in India which

are run by the Indian business houses. The mega retailers follow an overall common strategy

irrespective of the type of product segment or market and a representative of each of the prevalent

models is taken for a case study. The main objective of these case studies is to understand how these

firms are planning to34

:

(i) Penetrate markets and build market share;

(ii) Introduce multiple product and format categories;

(iii) Operate the chain from sourcing to marketing;

(iv) Create product identities through prices

(v) Capture customer footfalls.

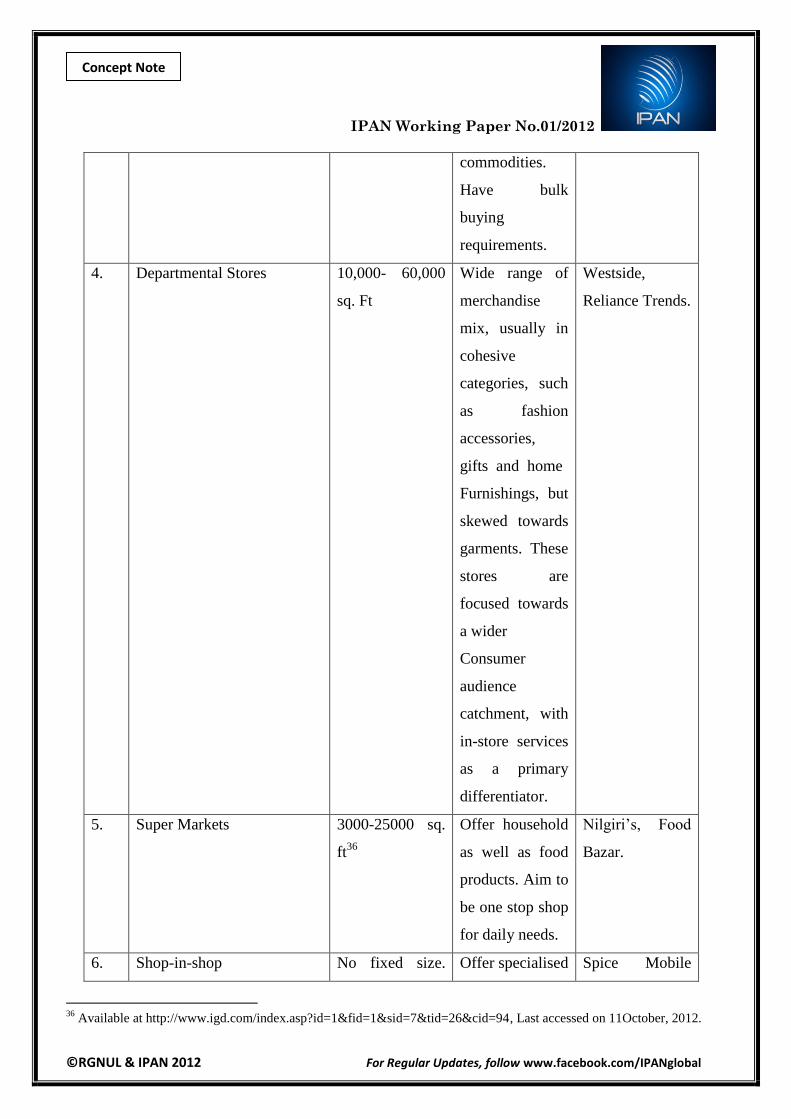

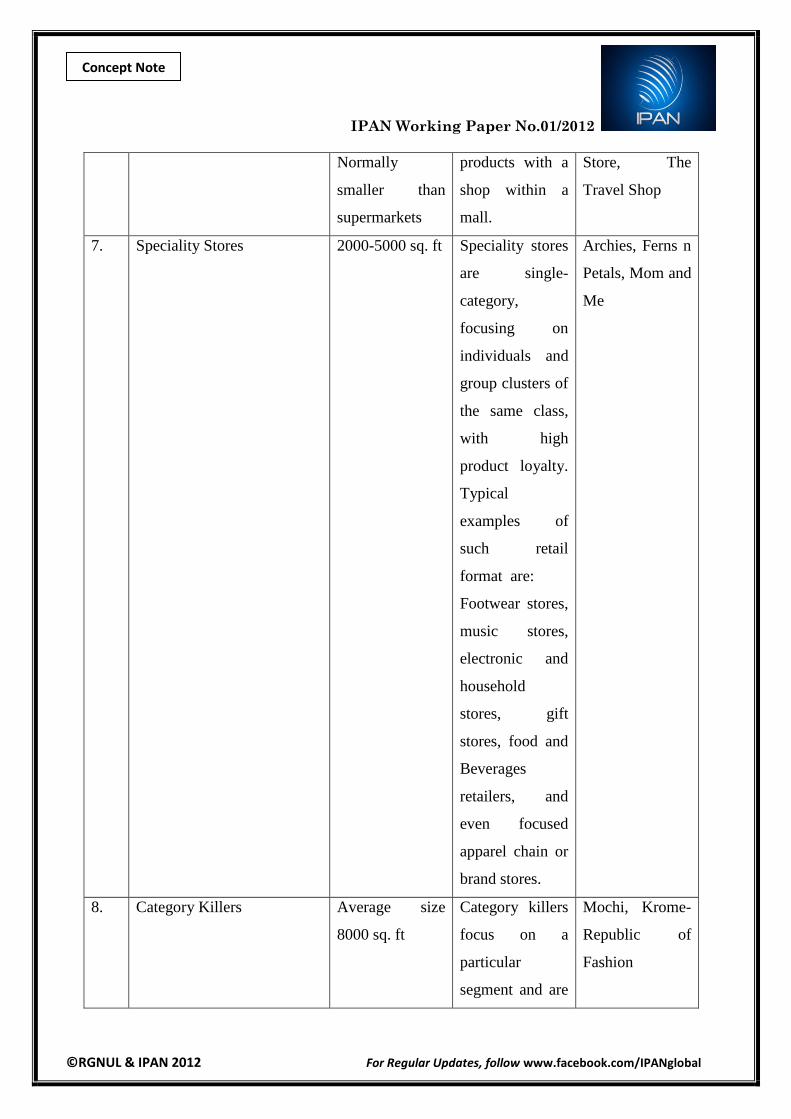

In India, the main formats prevalent among the retail stores are studied below in relation to store

sizes and their business identities.

The formats prevalent in retail sector are35

:-

34

Ibid

35 The IPAN SALE working group has taken these figures from (a) Working Paper No 222, Impact of Organized

Retailing on the Unorganised Sector, ICRIER, Indian Brand Equity Foundation, Retail, 2010. p. 8, (b) Rohit Bhasin and

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

Type of Store Store Size Description Examples

1. Restaurant Chains As required The restaurant

chains cater

mainly to a

particular

cuisine and

operate mainly

in the high-end

segment.

Sagar Ratna,

Mainland China,

O Calcutta

2. Hypermarket 50000- 100000

sq. Ft.

Offer a

large basket of

products,

ranging from

grocery, fresh

and processed

food, beauty and

household

products,

clothing and

appliances, etc.

Spencer, Big

Bazar, Easy Day

Market

3. Cash and Carry (B2B

format)

More than

75,000 sq. Ft

Focussed on

bulk buying and

selling of

Metro Cash and

Carry, Bharti-

Walmart

Bharti Ramola, Winning in India‟s Retails Sector, PwC, Mumbai , (c) Ms. Vidushi Handa And Mr. Navneet Grover,

―Retail Sector In India: Issues & Challenges‖, Zenith International Journal of Multidisciplinary Research, Vol. 2, Issue 5,

May 2012, p. 256, (d) Aditya P. Tripathi, ―Emerging Trends in Modern Retail Formats & Customer Shopping

Behavior in Indian Scenario: A Meta Analysis & Review‖, Unknown, p. 10 (e) Tazyn Rahman, ―Organized Retail

Industry In India – Opportunities And Challenges”, International Journal of Research in Finance & Marketing, Volume

2, Issue 2 (February 2012) , p. 85 and (f) Sanjay Manocha and Anoop Pandey, ―Organized Retailing in India : Challenges

and Opportunities‖, VSRD-IJBMR, Vol. 2 (3), 2012, p. 75 to design this table providing the division of different types of

retail formats. In addition to the existing concepts provided in the mentioned papers, a few formats have been added by

the research team itself.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

commodities.

Have bulk

buying

requirements.

4. Departmental Stores 10,000- 60,000

sq. Ft

Wide range of

merchandise

mix, usually in

cohesive

categories, such

as fashion

accessories,

gifts and home

Furnishings, but

skewed towards

garments. These

stores are

focused towards

a wider

Consumer

audience

catchment, with

in-store services

as a primary

differentiator.

Westside,

Reliance Trends.

5. Super Markets 3000-25000 sq.

ft36

Offer household

as well as food

products. Aim to

be one stop shop

for daily needs.

Nilgiri‘s, Food

Bazar.

6. Shop-in-shop No fixed size. Offer specialised Spice Mobile

36

Available at http://www.igd.com/index.asp?id=1&fid=1&sid=7&tid=26&cid=94, Last accessed on 11October, 2012.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

Normally

smaller than

supermarkets

products with a

shop within a

mall.

Store, The

Travel Shop

7. Speciality Stores 2000-5000 sq. ft Speciality stores

are single-

category,

focusing on

individuals and

group clusters of

the same class,

with high

product loyalty.

Typical

examples of

such retail

format are:

Footwear stores,

music stores,

electronic and

household

stores, gift

stores, food and

Beverages

retailers, and

even focused

apparel chain or

brand stores.

Archies, Ferns n

Petals, Mom and

Me

8. Category Killers Average size

8000 sq. ft

Category killers

focus on a

particular

segment and are

Mochi, Krome-

Republic of

Fashion

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

able to provide a

wide range of

choice to the

consumer,

usually at

affordable

prices due to

the scale they

achieve. They

that offer less

variety but deep

assortment of

merchandise.

9. Discount Stores Average Size

1000 sq. Ft

Offers wide

range of

products,

mostly branded

at high rates of

discount.

Primarily

provide

discounts by

selling in bulk.

The Loot,

Koutons,

Liverpool

10. Convenience Stores37

400-2000 sq.ft Located near

Residential areas

in thickly

populated areas.

For easy access

and daily

Safal, 6ten,

Subhiksha,

Mother Diary

stores

37

Ms. Vidushi Handa And Mr. Navneet Grover, ―Retail Sector In India: Issues & Challenges‖, Zenith International

Journal of Multidisciplinary Research, Vol. 2, Issue 5, May 2012, p. 256

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

purchase.

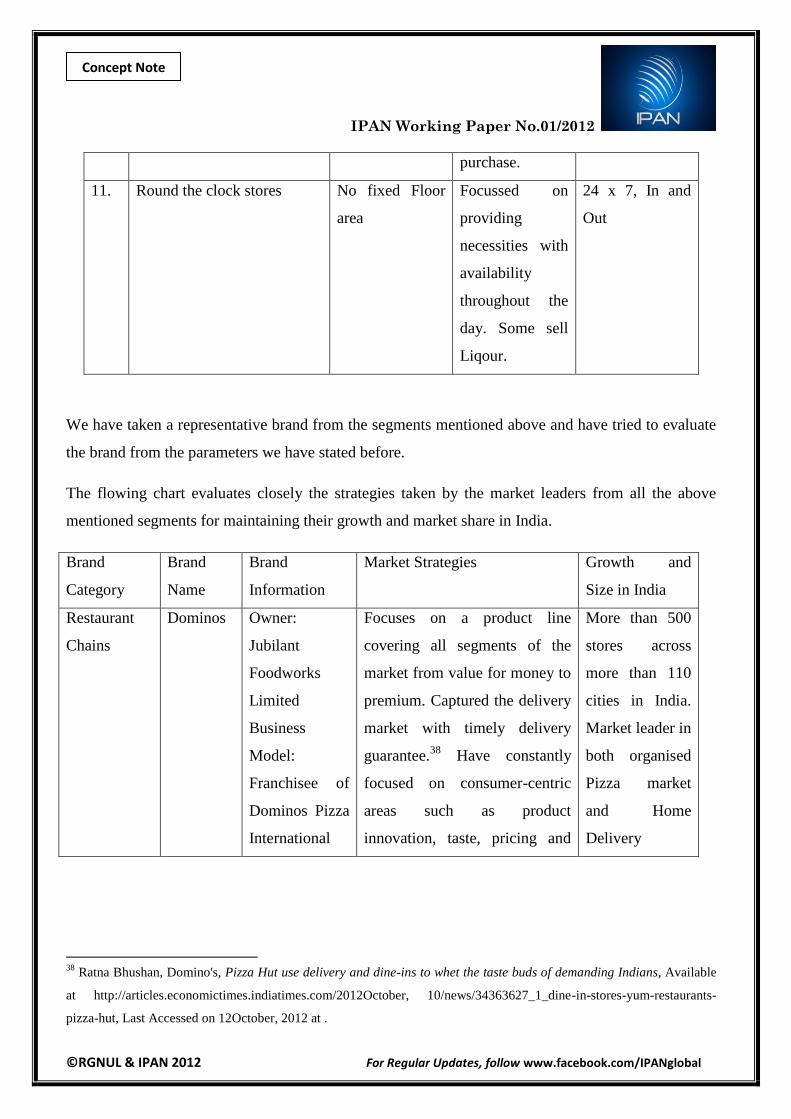

11. Round the clock stores No fixed Floor

area

Focussed on

providing

necessities with

availability

throughout the

day. Some sell

Liqour.

24 x 7, In and

Out

We have taken a representative brand from the segments mentioned above and have tried to evaluate

the brand from the parameters we have stated before.

The flowing chart evaluates closely the strategies taken by the market leaders from all the above

mentioned segments for maintaining their growth and market share in India.

Brand

Category

Brand

Name

Brand

Information

Market Strategies Growth and

Size in India

Restaurant

Chains

Dominos Owner:

Jubilant

Foodworks

Limited

Business

Model:

Franchisee of

Dominos Pizza

International

Focuses on a product line

covering all segments of the

market from value for money to

premium. Captured the delivery

market with timely delivery

guarantee.38

Have constantly

focused on consumer-centric

areas such as product

innovation, taste, pricing and

More than 500

stores across

more than 110

cities in India.

Market leader in

both organised

Pizza market

and Home

Delivery

38

Ratna Bhushan, Domino's, Pizza Hut use delivery and dine-ins to whet the taste buds of demanding Indians, Available

at http://articles.economictimes.indiatimes.com/2012October, 10/news/34363627_1_dine-in-stores-yum-restaurants-

pizza-hut, Last Accessed on 12October, 2012 at .

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

based in USA customer service.39

To increase

share in dine in market

Domino's is upgrading its dine-

in stores, allocating larger

spaces for them and foraying

into new cities. 40

Markets with

55% and 70 %

share

respectively.41

Income of Rs.

3145 million in

1st Quarter of

FY 2013.42

Hyper

Market

Big

Bazaar

Owner:

Pantaloon

Retail India

Limited

Business

Model:

Wholly Owned

Subsidiary

Coined the 3 C strategy:

Confidence, Change and

Consumption.43

Has succeeded

largely due to its emphasis on

consumer behaviour and

understanding the diversity of

Indian consumers. Further, it is

products driven where the focus

is on the front end to serve the

consumers well. Additionally,

the business model is based on

low margin and high turnover.

The shops offer products from

numerous categories spread

across multiple floors.44

More than 164

stores in India

in Big Bazaar

Format.45

Total income of

Rs. 7317 crores

in 2011-2012.46

39

Drypen, Domino's Marketing Strategies – Says, Affordability is the key to survival in India market,

http://drypen.in/branding/dominos-marketing-strategies-says-affordability-is-the-key-to-survival-in-india-market.html,

Last accessed on 09October, 2012

40 Id at 22.

41 Press Release, Jubilant Foodworks Limited, August 30, 2012.

42 Earnings Presentation, Jubilant Foodworks Limited, Q1 FY 13, July 25, 2012

43 Priya Kumar, The Story of Big Bazaar, Available at http://www.chillibreeze.com/articles_various/the-story-of-Big-

Bazaar-611.asp, Last accessed on 11October, 2012.

44 Ibid.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

Cash and

Carry

Best Price

Modern

Wholesale

Owner: Bharti

Wal-Mart India

Pvt. Ltd

Focussed on wholesale of more

than 5000 products.47

Primary

target are the retailers who sell

the products to the end

consumer.

More than 15

stores in India.

Sales of Rs.

1876 crores

with 143%

increase in

sales.48

Departmental

Stores

Westside

and Trent

Owner: Tata

Group

Retailing of clothes and

lifestyle products under one

roof.

More than 106

group stores.

Total operating

income

exceeding Rs.

19000 lakh.49

Super

Markets

Food

Bazar

Owner:

Pantaloon

Retail India

Limited

Business

Model:

Wholly Owned

Subsidiary

Sale of Food Product and

Groceries at affordable prices

and sale of product through

private brands to maximise

profits.

Sales revenue

not separately

available.

45

Raghavendra Kamath, Makeover at Big Bazaar, Available at http://www.business-standard.com/india /news/ makeover-

at-big-bazaar/483456/, Last accessed on 14October, 2012.

46 Kala Vijaya Raghavan & Sagar Malviya, Future Value to be merged with Pantaloon Retail to cut operating cost,

Available at http://articles.economictimes.indiatimes.com/2012-09-10/news/33737171_1_big-bazaar-pril-kb-s-fair-price,

Last accessed on 14October, 2012.

47 Available at http://www.bharti-walmart.in/Ourstores-Overview.aspx, Last accessed on 12October, 2012.

48 Sagar Malviya, New stores, rising sales fail to boost Bharti Walmart's net worth, Available at

http://articles.economictimes.indiatimes.com/2012-05-22/news/31814426_1_bharti-walmart-multinational-retailers-first-

cash-and-carry-store, Last accessed on 12October, 2012.

49 Audited Financial Results, Trent Limited, For the financial year ended 31

st March, 2012.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

Speciality

Stores

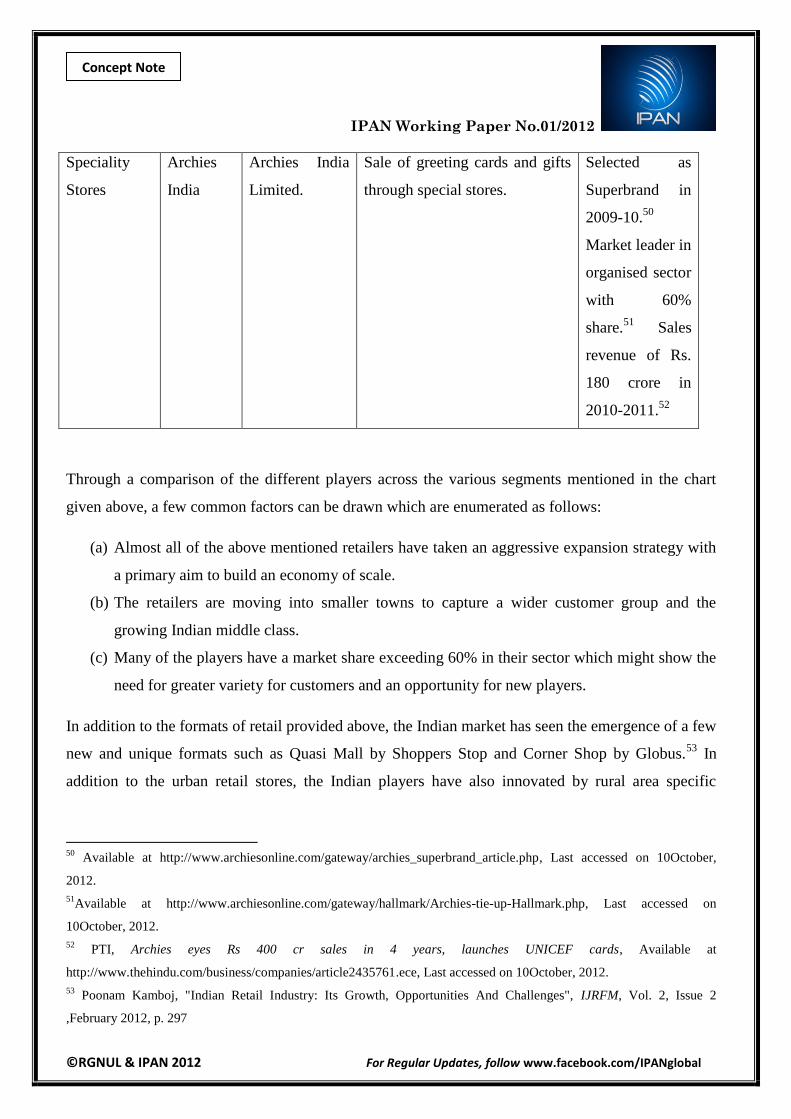

Archies

India

Archies India

Limited.

Sale of greeting cards and gifts

through special stores.

Selected as

Superbrand in

2009-10.50

Market leader in

organised sector

with 60%

share.51

Sales

revenue of Rs.

180 crore in

2010-2011.52

Through a comparison of the different players across the various segments mentioned in the chart

given above, a few common factors can be drawn which are enumerated as follows:

(a) Almost all of the above mentioned retailers have taken an aggressive expansion strategy with

a primary aim to build an economy of scale.

(b) The retailers are moving into smaller towns to capture a wider customer group and the

growing Indian middle class.

(c) Many of the players have a market share exceeding 60% in their sector which might show the

need for greater variety for customers and an opportunity for new players.

In addition to the formats of retail provided above, the Indian market has seen the emergence of a few

new and unique formats such as Quasi Mall by Shoppers Stop and Corner Shop by Globus.53

In

addition to the urban retail stores, the Indian players have also innovated by rural area specific

50

Available at http://www.archiesonline.com/gateway/archies_superbrand_article.php, Last accessed on 10October,

2012.

51Available at http://www.archiesonline.com/gateway/hallmark/Archies-tie-up-Hallmark.php, Last accessed on

10October, 2012.

52 PTI, Archies eyes Rs 400 cr sales in 4 years, launches UNICEF cards, Available at

http://www.thehindu.com/business/companies/article2435761.ece, Last accessed on 10October, 2012.

53 Poonam Kamboj, "Indian Retail Industry: Its Growth, Opportunities And Challenges", IJRFM, Vol. 2, Issue 2

,February 2012, p. 297

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

hypermarkets such as ITC‘s E- Choupal and HLL's project Shakthi and Mahamaza. This shows a

continuous process of innovation and experimentation by the Indian retailers.

Nature of Indian Consumerism

The Indian retail sector is frequently referred to as a gold mine which is ready to be tapped by the

most efficient businesses.54

The primary target of the marketers is an untapped consumer group with

growing spending power and India provides them that opportunity. The commonly attributed reasons

for the growth of the retail market in India have been: Rapidly increasing income level, Change in

lifestyle, Favourable pattern of geography, Retail offering one roof shopping experience, Increase in

the number of nuclear families, Improved purchasing power of Indian middle class, Presence

of domestic and foreign player, Effect of Liberalization, Privatization, and Globalization.55

In one of the few empirical research studies undertaken on the topic, conducted by Swati Kewlani and

Sandeep Singh among a random group of 150 people in Indore, India has revealed that consumers go

to shopping malls for the variety they get there and because ―they find shopping entertaining due

to good environment, and variety of products that they get there, reasonable price that are offered

along with the better quality of services rendered.‖ No doubt the big giants are giving tough

competition to small retail store, but consumers are still in favour of small retailers. 56

The study has

revealed that consumers prefer to buy consumer care and daily use products from shopping malls.

However, it has further revealed that they continue to buy from small retailers, and they spend

equally on buying from kiranas. The study listed a few benefits of local kiranas stated by the

surveyed people which are listed below:

(a) They are going to small retailers due to their long standing relations with them, the home

delivery services that the small retailers offer and because they find shopping less time

consuming while shopping with small retailers as compared to malls.

54

B.D. Singh & Sita Mishra, ―Indian Retail Sector- HR Challenges & Measures for Improvement‖, Indian Journal of

Industrial Relations, Volume 44 Issue 1, 2008.

55 Chandu. K. L , ―The New FDI policy in Retail in India: Promises, Problems and Perceptions”, Asian Journal Of

Management Research, Volume 3 Issue 1, 2012 , p.100-106

56 Swati Kewlani and Sandeep Singh, “Small Retailers Or Big Shopping Malls: Will Big Fishes Eat The Small?” Journal

of Radix International Educational and Research Consortium, Volume 1, Issue 2, February 2012.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

(b) When the respondents were asked whether they go to small retailers because of the

relationship they have developed over the period of time with them more than half (52%)

responded were with affirmation, thus clearly underlining the dictum that relationship

marketing hold the key to the survival of the minnows, which is emerging to be the U.S.P. of

these small retailers.

The authors also listed a few points why the kirana shop will be relevant even in the changed retail

landscape:

Firstly, the location of the shop at the neighbourhood allows for easy purchase of items at short

intervals without the need of detailed travel plans.

Secondly, there is a long friendly relationship with the neighbourhood kiranawalla based on mutual

trust.

Thirdly, the shopkeeper offers free home delivery under most circumstances.

Fourthly the small shopkeepers provide easy credit on the items of daily use and the amount is paid at

a fixed flexible interval by the customer enabling a lasting relationship.

Further, it is a commonly stated fact the Indian customer looks into the value for money aspect of a

product before a purchase decision which would make product differentiation on the basis of price a

key factor for any player coming into the market.

The main challenge before the Indian organised retail sector is to cope with the customer

expectations of the Indian customer who has till date been served at home by the Kirana shop. The

kirana shop provided convenient location, personalised location and easy credit. The Indian

organised retailer will have to come up with new and innovative platforms to tackle the kirana store

challenge and some factors such as instant credit will be a challenge for even the biggest players due

to the varied Indian conditions. Understanding the tastes and preferences to suit the local needs might

also need some time for the Indian organised retailer. A possible way to tackle the challenge might be

to include representatives of the local area in the business structure.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

Challenges Faced By the Organised Retail Sector In India

The challenges faced by a new and emerging business sector are many and new hurdles seem to

emerge with the expansion of the business. However, for the purpose of the study we have tried to

list a few of the major hurdles faced by the organised retail sector till date in its relatively short

journey in India:

Political Opposition

The Indian political scenario is crowded with varying opinions about organised retail and its

possible impact on the Indian customer. A number of views have been put forward regarding

organised retail contributing to unemployment in the country and its possible impact on the

small Kirana shop owner. Different states around the country have varied policies on

organised retail and investment by business houses in certain states have even been met with

violent opposition As such a uniform policy across the country is absent presenting a huge

hurdle to the major players in the country.

Supply Chain

India is the seventh largest country in the world with varying climatic conditions and

consumer preferences across the country. The basic infrastructure of roads and availability of

storage facilities is not standard across the country which presents a huge challenge to the

investors. Infrastructure has been developed at priority in the last decade and it is hoped that a

planned expenditure of US$ 1 trillion in the 12th five year plan will help bridge the

infrastructure gap in the country. A strong supply chain is the immediate need of the hour and

any new player will have to build the supply chain to a large extent from the scratch.

Channel Conflicts

One of the primary modes by which the organised retails sector reduces costs worldwide is by

agreements with the producers and distributors of products. In India, however, the existing

supply model has been built with the small retailer in mind and a huge hurdle exists before the

organised retail sector to tackle the varied distribution system across the country.57

Further.

57

Indian Retail Market: Changing with the Changing Times, Deloitte, August, 2010.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

India also has varied taxation laws across the country with different rates of local taxes which

needs to be looked into by the retailers.

Location and Rental

Rent forms a large portion of the total expenditure of any organised retail business in India.58

Indian property rentals are sometimes exorbitant in the prime areas thus putting a strong

pressure on viability.59

The challenge for a retailer would be to find the right location for their

stores and select properties which do not impact their bottom-line. Certain retailers have taken

to developing their own properties keeping an eye on the savings in the long run.60

Understanding the unique Indian Customer

The Indian consumer has varied tastes and is primarily value oriented and pricing is critical in

the country.61

Further, the tastes vary across the country. Thus, a particular product may be a

best seller in one area while might not sell in the other state. The organised retailer has to

identify the tastes of the different areas and cater to the varied demands62

which might lead to

lesser volumes and lesser bargaining power. Further, the Indian customer also has a

preference for fresh products and the retailers would have to modify their strategies to suit

such preferences.63

Regulatory measures

As mentioned before, the Indian tax structure varies to a large extent among the different

states and Goods and Service Tax which is likely to be implemented in 201364

will replace a

58

Malls and Hyper Markets: Perspectives of Contemporary Shopping, School of Management Studies, Punjabi

University, Patiala, p. 40

59 Nargundkar Rajendra, Services Marketing: Text and Cases, Tata McGraw Hill, New Delhi, 2010, p. 348

60 Ratna Bhushan & Rasul Bailay, Tata, Reliance join retail rush, plan to build shopping malls across the country,

Available at http://articles.economictimes.indiatimes.com/2012-07-11/news/32632952_1_malls-retail-space-retail-

formats, Last accessed on 12 October, 2012.

61 Amisha Gupta, ―Foreign Direct Investment In Indian Retail Sector: Strategic Issues And Implications‖, IJMMR,

Volume 1, Issue 1 (December, 2010) , pp. 56

62 Ramaswamy VS, S Nakamuri, Marketing Management, Macmillan Publishers India Limited, New Delhi, 2009 p. 272

63 Unknown, The Great Indian Bazaar, McKinsey and Company, Mumbai 2008, p.22

64 GST rollout likely in 2013-14: Modi, Available at http://www.financialexpress.com/news/gst-rollout-likely-in-201314-

modi/938756/, Last accessed on 11October, 2012.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

host of levies like excise, sales tax, value-added tax, entertainment tax and luxury tax.

Further, starting a new business venture in India requires a number of licenses, which have to

be obtained from different government departments leading to considerable lead time in

opening up of the stores.65

Slow acceptance of private labels

Private labels enable retailers to offer products at better prices due to the removal of the high

cost brand names. Further, it lets the retailer package their own products middlemen and

enhances bargaining power with supplier. In-house brands account for 12-15% of sales and

more than 20-25% of profits for most Indian retailers which is very low compared to the

global mark of earning 55-60% of revenues from private labels. 66

The concept of private

labels has however not captured the desired attention in the Indian market which in certain

sectors shows a high brand loyalty thus reducing the options for the retailers.

Absence of trained labour force

Indian retailing faces the challenge of lack of trained manpower67

and the new employees

which are employed by the companies have to be trained in the sector, thus increasing the cost

for the companies which employ the workers. Further, lack of past experience reduces

efficiency. Further, the sector sees high attrition levels due to shortage of quality manpower.

65

Laxmikant S. Hurne, ―Proposed FDI in Multi-Brand Retailing: Will it heat the Indian unorganized Retail Sector?‖,

Review Of Research, Vol.1,Issue.VI, March, 2012, p.3

66 Sagar Malviya & Sarah Jacob, Private labels' euphoria subsides in retail, Available at

http://articles.economictimes.indiatimes.com/2011-06-13/news/29653341_1_private-labels-spencer-s-kampani-ceo-

thomas-varghese, Last accessed on 14 October, 2012.

67 Frost and Sullivan, Overview of The Indian Retail market, 2008 , p. 7

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

PART 3: EVOLUTION OF ORGANISED RETAIL WORLDWIDE

Retailing has come to be recognized as a discipline due to rapid growth in market coverage and

investments in this sector in India and the world. There are various factors responsible for retail

revolution across the globe, including in India. The demographic profile of the consumer has changed

and due to economic development and increased income level he has become affluent. Also it has

been observed that the powers have slowly started moving out of brands into retailer‘s hands due to

their proximity with customers and improvements in customer service. The emergence of private

labels will substantiate this fact. All the mass produced products are being served to mass consumers

through retail platforms allowing the customer to choose from wider assortments. There has been

revolution in retail industry. The India Retail Industry is the largest among all the industries,

accounting for over 10 per cent of the country‘s GDP and around 8 per cent of the employment. The

Retail Industry in India has come forth as one of the most dynamic and fast paced industries with

several players entering the market.

The industrial revolution necessitated dramatic changes on the retail front. The increase in

urbanization meant that consumers were now clustered .in small geographic areas. These led to the

emergence of shops to serve the needs of locals.68

The number of consumers increased and mass

transportation became a way of life. Mass manufacturing, longer distribution channels and mass

merchandisers evolved. Retail evolved in many ways over the 20th century. Self service, a concept

started in 1916 helped the retailer in reducing costs, as fewer workers were required to service the

customers.69

The emergence of the supermarkets during 1930s, discounted stores and hypermarket

like Carrefour in France in 1963 indicated retail boom. As the needs of consumers grew and changed,

one saw the emergence of commodity specialized mass merchandisers in 1970.70

The seventies also

witnessed the use of technology in the retail sector with the introduction of the barcode specialty

chains developed in the 80s as did large shopping malls. In 1995 the world of retail opened the doors

68

Andrew Edgecliffe Johnson, ―A Friendly Store from Arkansas‖, Financial Times, 19 June 1999.

69 Wal-Mart Associate Handbook, Available at http://walmart.3cdn.net/594f2e1e559832379c_k3m6bh9d8.pdf, Last

accessed on 16 October 2012.

70 Annual Report, Wal-Mart Stores, Inc. (1971-2001), Available at http://stock.walmart.com/annual-reports, Last

accessed on 16 October 2012.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

to global market on the web. With the growth of the World Wide Web, both the retailers and

consumers can find suppliers and products from anywhere in the world.71

Factors which Assisted the Growth of Global Organised Retail

In western states, rise of organised retail globally has been attributed towards urbanization, and

positive change brought in by post world war situation and some of the growth factors of organized

retail can be listed as72

:-

1. Increase in per capita income which in turn increases the household consumption

2. Demographical changes and improvements in the standard of living Change in patterns of

consumption and availability of low-cost consumer credit

3. Improvements in infrastructure and enhanced availability of retail space

4. Entry to various sources of financing

5. Advent of information technology

Lehman Brothers analysts have noted Wal-Mart‘s ―leading logistics and information

competencies‖.73

The Financial Times has called Wal-Mart ―an operation whose efficiency is the

envy of the world‘s storekeepers‖. Wal-Mart and other such ―big-box‖ retailer‘s competitive edge

is driven by a combination of conventional cost-cutting and sensitivity to demand conditions and

by superior logistics and distribution systems. The chain‘s most-cited advantages over small

retailers are economies of scale and access to capital markets, superior logistics, distribution, and

inventory control. These big retailer‘s cost-savings extend to its employment practices; many have

been accused of requiring employees to work off the clock and using illegal-immigrant labor

(through contractors).74

Such practices, if true, could reduce these retailers‘ measured employment

without reducing its actual labor inputs. Big retailer‘s low wages are also said to contribute to its

measured productivity. While Wal-Mart and such other companies‘ wage data are not publicly

71

Thomas L Friedman, The World Is Flat: The Globalized World in the Twenty-First Century, Penguin Books, 2007.

72 J.R. Graham, ―Marketing Strategies for Businesses that are more ‗Bricks‘ than ‗Clicks‘‖, The American Salesman, Vol.

45 No. 9, 2000, pp. 19-25.

73 Emek Basker, ―Selling a Cheaper Mousetrap: Entry and Competition in the Retail Sector‖, Draft report University of

Missouri, January 2004.

74 Steven Greenhouse, ―Suits Say Wal-Mart Forces Workers to Toil off the Clock‖, New York Times, 25 June 2002.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

available, several sources estimate the current typical hourly wage of a Walmart ―associate‖ to be

$7-$8/hour.75

These wages are on par with wages paid by other large discount chains (like K-Mart

and Target), but are typically below union rates.

To look into the explicit reasons behind the growth of organized retail, it would be convenient for us

to look into the growth of specific model, Wal-Mart is frequently referred as ―King of Inventory

Management‖, as the company keeps lesser inventory in comparison to it peers, reason attributed not

only to economy of scales that it has over other competitors but also scientifically advanced supply

chain management which gives corporation an edge over its competitors, forget small traders (mom

& pop store keepers). Many case studies have been conducted to decode the same, one of the most

cited one was published by Harvard Business Review, in which the whole supply chain management

was referred as Rocket Science.76

Specific departments in these corporations work to reduce per/piece

cost so as to contain the cost at such a low level which cannot be met by small retailers, thus

eventually driving them out of competition. In short, Business analysts explain Wal-Mart's success as

a function of four major factors: a big box format,77

everyday low pricing, efficiency in logistics,78

and competitive intensity.79

75

Virginia Postrel, ―Lessons in keeping Business Humming, Courtesy of Wal-Mart U‖, New York Times, 28 Feb. 2002,

At C2.

76 Marshall L Fischer, Ananth Raman and Anna Sheen Mcclelland, ―Rocket Science Retailing Is Almost Here, Are You

Ready?‖, Harvard Business Review, July-August, 2000.

77 The "Big Box Format" is the principle of how "Larger stores increase sales per square foot by encouraging customers

to buy additional goods, often on impulse. Big-Box Stores also let retailers spread fixed labor costs like store

management and cleaning crews across more sales.".

78 One of Wal-Mart's greatest achievement is its use and development of it applications:

It is widely regarded as the leader in the use of it in retail and pioneered a number of it applications including, for

example: Early adoption of computers to track inventory in distribution centers (1969),Use of computer terminals in

stores to facilitate communication (1977),Scanning using UPC codes (1980),Ground-breaking use of electronic data

interchange (1985), Satellite communications network (1987),Use of radio frequency (rf) guns (late 1980s), Expansion of

the edi system to include an extranet, which became an early form of escm (beginning in 1991), Development of 'retail

link,' a micro-merchandising and supply chain management tool (beginning in 1991), As with its managerial innovations,

these innovative uses of it improved Wal-Mart's productivity (both capital and labor) and cost position. They also resulted

in continued market share gain due to their contribution to lower prices, lower out of stocks, and more effective

merchandising.

Mckinsey & Co., US Productivity Growth, 1995-2000 1, 2001, Available at

http://www.mckinsey.com/mgi/reports/pdfs/productivity/retail.pdf, Last accessed on 07 October, 2012.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

Comparison of these Factors with Indian Context

Most of the retail sector in India is unorganised, which are popularly referred as mom-pop stores.

The biggest advantage in this sector is the consumer familiarity that passes on from one generation to

the next. The transformation stage of the retail sector started in late 1990‘s. The emergence of pure

retailer has started at this stage as it is been perceived as a beginner and the organised retailing is

getting more attractive. In India, the retail business contributes around 14 percent of GDP in 2011.80

Of this, the organized retail sector accounts only for about five to six percent share, and the

remaining share is contributed by the unorganised sector. The main challenge faced by the organised

sector is the competition from unorganized sector. An important aspect of the current economic

scenario in India is the emergence of organized retail. There has been considerable growth in

organized retailing business in recent years and it is poised for much faster growth in the future.

Major industrial houses have entered this area and have announced very ambitious future expansion

plans.81

Transnational corporations are also seeking to come to India and set up retail chains in

collaboration with big Indian companies. However, opinions are divided on the impact of the

growth of organised retail in the country. Factors responsible for the growth of organised sector do

have applicability in Indian context also, as the growth factors of organized retail are:-

Increase in per capita income which in turn increases the household consumption

Increasing per capita income is one of the reason that has enabled foreign and domestic

investors to invest in organised retail, as with the rise in income there is bound to be rise in

living standard of people, and India has witnessed unprecedented growth post liberalization

thereby realization of higher income by households.82

79

Ibid.

80 ‗Global Retail Expansion: Keeps On Moving 2012‘, Atkearny, Available at

http://www.atkearney.com/documents/10192/4799f4e6-b20b-4605-9aa8-3ef451098f8a, Last accessed on 14 October,

2012.

81 RIL, RPG, Videcon, Bharti-Airtel, Aditya Vikram Birla Group, etc., to name a few.

82 C. K. Prahalad, The Fortune at the Bottom of the Pyramid: Eradicating Poverty Through Profits, Pearson Prentice Hall,

2006.

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

Demographical changes and improvements in the standard of living

With the impetus provided to industrial activity by measures initiated in 1991 budget,

employment opportunities increased on exponential fold in urban centers resulting in rural-

urban migration, which had a significant effect in bringing about demographic change in the

country.83

Change in patterns of consumption and availability of low-cost consumer credit

With the objective of providing injections in the financial system, and to reduce leakages so as

to provide impetus to private investment in the country, interest rates were decontrolled in a

specific band, which resulted in easy access of credit to consumers, which in turn has led to

spur growth in the financial system.84

Improvements in infrastructure and enhanced availability of retail space

Infrastructure was government‘s first priority, as in pre-liberalisation period there was dearth

of investment in the same, so various initiatives were taken such as providing tax exemptions

on infra-bonds, various models were developed like public private partnership (PPP Model),

Build Operate Transfer (BOT Model), etc., to involve private sector in developing

infrastructure of the country. Some of the prominent projects include Golden Quadrilateral

(road sector), Ultra Mega Power Plant (Electricity generation), etc., were taken on the same

lines and has resulted in spurring investment by retail players.

Entry to various sources of financing

Post liberalization there was huge influx of capital in the economy, so to regulate the same

various legislations were passed and amended like Securities Exchange Board of India (SEBI,

1992) came into existence and since then there have been various financing models have been

allowed like mutual funds, fund of funds, relaxation in external commercial borrowings

83

National Council Of Applied Economic Research, Delhi (NCAER), report on ‗The India Market Demographic Report

2002‘.

84 Shivam Shirdhonkar, ―Analysis of Rural Retail Market for Aadhar‖, Available at

http://www.scribd.com/doc/50797888/20600169-godrej-Aadhar-Report, Last accessed on 14 October, 2012. .

IPAN Working Paper No.01/2012

©RGNUL & IPAN 2012 For Regular Updates, follow www.facebook.com/IPANglobal

Concept Note

(ECBs), Indian Depository Receipt (IDR), etc., to enable private individuals to raise money in

a proper legal framework. Various guidelines have been amended and have brought in

transparency such as ICDR 2009 regulations, etc., which regulates the conduct of companies

having securities listed in the capital market.85

Advent of information technology

Post 1990s, globe has witnessed astonishing development in the field of information technology

due to heavy investment made in the sector during dot com bubble regime, resulting in advance

technology being available at cheaper prices which has further come to as an aid to retail sector.

Big corporations like Wal-Mart uses satellites, Radio Frequency Identification (RFID) system

which has further increase the efficiency of the corporations, there by resulting in minimising

costs.86

Impact of Organised Retail Worldwide on Macro Economy

During recent decades, FDI has increased exponentially: the yearly global flows of FDI increased

from 55 billion US $ in 1980 to 1,306 billion US $ in 2006. FDI inflows increased continuously

during the 1980s and 1990s - with the sharpest growth in the late 1990s - to reach a peak in 2000.

Between 2001 and 2003 the developed economies experienced a sharp decline in FDI inflows,

associated with a general global economic recession. Developing countries were affected only to a

small extent. FDI flows started to recover in 2004 and were back at their 2000 level in 2006.87

When a firm wants to invest in a foreign country, there are two possible entry modes, greenfield

investment or M&A (mergers and acquisitions). Greenfield FDI refers to the establishment of new

production facilities such as offices, buildings, plants, factories and the movement of intangible

capital (mainly services) to a foreign country, one of the preliminary conditions laid down in DIPP

notification. Greenfield FDI thus directly adds to production capacity in the host country and, other

things remaining the same, contributes to capital formation and employment generation in the host

85

M.Y. Khan, Indian Financial System, Tata Mcgraw-Hill Education, New Delhi, 2011.

86 Miguel Bustillo, ―Wal-Mart Radio Tags to Track Clothing‖, Wall Street Journal, 23 July 2010.

http://online.wsj.com/Article/Sb10001424052748704421304575383213061198090.html, Last accessed on 16 Oct. 2012.

87 UNCTAD Report on ‗Trade and Development 2007‘,