revision of standards working group for revision of

TRANSCRIPT

Committee for the Registry of Auditors and Accountants 1 July 2014

CRAC BULLETIN No. 38 – July 2014 (Not for sale)

Working Group for Revision of Auditing Standards:

Initial Stage CompletedBetween April and May 2014, the working

group responsible for the revision of Auditing Standards has completed the corresponding research work with regard to the international standards, and has submitted revision proposals to the CRAC. These revision proposals are concerned primarily with the conflict between international standards and laws and regulations of Macao, where practical elements have also been considered.

The CRAC would then sort out and study the working group’s revision proposals before drafting a Formulation Plan for Macao Standards on Auditing. The committee plans to collect opinions and comments from the accounting industry with regard to the Plan. Meanwhile, the CRAC is actively seeking both Chinese and Portuguese translated versions of the Standards from the corresponding international institution.

CAPA Meeting at Sri Lanka: Asia Increases Discourse

Power Among Accounting Industry WorldwideA CRAC delegation attended, upon invitation,

the Confederation of Asian and Pacific Accountants’ (CAPA) Board Meeting held in Negombo, Sri Lanka on 22-23 May 2014. Participating in this meeting were a number of delegates representing different countries, including: Mr. Liang LiQun, Deputy Secretary General of the Chinese Institute of Certified Public Accountants (CICPA) and Ms. Liang Jing, CICPA’s representative on the CAPA Board, as well as members of the accounting industry representing Australia, UK, Canada, India, Korea and Japan among others.

As the host of the meeting, Mr. Arjuna Herath,

President of the Institute of Chartered Accountants of Sri Lanka (CA Sri Lanka), gave a brief introduction to Sri Lanka.

Sri Lanka has an area of 65,610 sq.km and a population of about 21 million, while Colombo is the capital of the country. With regard to Sri Lanka’s economy, the GDP in Sri Lanka is 60 thousand-millions US Dollars, GDP Growth is 7%, Per Capita Income is 2,800 US Dollars, and Unemployment Rate is 4.2%. Sri Lanka’s primary industries’ contribution to GDP include: agriculture 11.2%, industry 29.3% and services 59.5%, while there has seen a decline in the dependence on its traditional sector of agriculture. Sri Lanka’s exports are primarily comprised of tea leaves, textiles and

plastic products, while imports are primarily comprised of petroleum and other products.

The economic challenges faced by Sri Lanka at

present include: high inflation rate; reliance on the devaluation of currency to stimulate exports, which has led to a number of issues such as trade deficit and government debt.

The CA Sri Lanka was founded in 1959 and has a 55 year history and 4,300 members to this date. The CA Sri Lanka is responsible for establishing accounting standards, issuing practice licenses, and carrying out corresponding administrative work. Mr. Sujeewa Mudalige (CAPA President in 2014/2015) is from Colombo, Sri Lanka, where he is a partner of PricewaterhouseCoopers – Sri Lanka, and previously served as President of CA Sri Lanka.

A number of reporting items were passed during this CAPA meeting, Mr. Sujeewa Mudalige (President) and Mr. Brian Blood (Chief Executive) have respectively presented CAPA’s work report.

Mr. Mudalige stated that: for the accounting

profession, Asia has great growth potential when you look at its population or the scale of its economy. Because of globalization, the nature of

Revision of Standards

CAPA Meeting

Committee for the Registry of Auditors and Accountants 2 July 2014

many enterprises has changed over the years, and it can be foreseen that work related to the accounting profession in Asia will receive remarkable development. In order to move with the time, and to gain attention from the economic systems that are receiving service, industry people need to ensure that they draw support from the global accounting industry who would provide assistance and solutions, thereby allowing themselves to be ready to face challenges encountered in this region.

Mr. Blood talked about the post financial

tsunami economic development in Asia, of which he believes has already recorded obvious improvements; Mr. Blood anticipates that, with the continuing efforts from professionals, further development would still be possible. Hence, with great enthusiasm, he considers that: in order to achieve these objectives, we (accounting professionals) must fully equip ourselves, so that we could contribute effectively in the international scene. He hopes that each accounting representative contributes to the joint effort in helping accounting personnel of both the country as well as the region as a whole in making a big step forward.

Ms. Jackie Poirier from the Professional Accountancy Organisations Development Committee (PAODC) also presented some of the committee’s work. The PAODC strives to: share the latest information with regard to issues that are happening at the moment as well as to provide technical training material; add or enhance information that are shared among Professional Accountancy Organizations (PAOs) in both volume and quantity and, in particular, information regarding corporate governance, operations, service and responsibility.

Prior to CAPA’s Board Meeting, the CAPA, together with the World Bank and the International Federation of Accountants (IFAC), jointly organized a high-level regional conference on Financial Reporting for Economic Development from 19-21 May. More than 200 delegates representing over 20 countries have participated in this conference hosted by the CA Sri Lanka.

The next CAPA Board Meeting is expected to

take place from 8-9 November 2014 at Rome, Italy. In addition, the World Congress of Accountants (WCOA), to be hosted by the IFAC, is also scheduled to take place in Rome from 10-13 November 2014.

Licensing Examinations: Round I Completed

Round I of the licensing examinations for first-time registration and reinstatement of registered auditors, registered accountants/accounting technicians 2014 has successfully taken place at the Cheng Feng Commercial Centre, Alameda Dr. Carlos d’Assumpção between May and June. A total of 64 candidates have sat this round of exams (13 candidates sat exam for registered auditors, 51 for registered accountants). Please refer to the table below for statistics for each subject.

The examination results are expected to be announced sometime between July and August, whereby registration for round II of the licensing examinations is expected to commence shortly after. Round II of the licensing examinations are scheduled to take place between November and December. Please visit the CRAC website regularly for up-to-date information. Alternatively, please call the CRAC office for enquiries.

Date Subject

Number of Candidates

Registered

Auditors

Registered

Accountants

24th

May 2014 General Accounting and Financial Accounting

/ General Accounting 4 32

25th

May 2014 Macao Taxation Law 11 27

31st May 2014 Cost Accounting 5 22

1st June 2014 Commercial Code 7 31

7th

June 2014 Auditing Standards 6 -

Examinations News

Committee for the Registry of Auditors and Accountants 3 July 2014

Official Announcement of the HengQin Corporate Income Tax Directory

The Ministry of Finance, together with the National Taxation Head Office, have announced the above-titled directory (No.26 [2014] of the Ministry of Finance) as well as various corporate income tax (CIT) related policies in March 2014. The directory and the policies are implemented from 1

st January

2014 to 31st December 2020.

According to the directory, corporations established in the new region of HengQin that fall within the category of encouraged industries will be charged a reduced rate of CIT at 15%. It should be noted that, corporations that fall within the category of encouraged industries refer to those corporations whose primary activity must be listed in the directory, and that the corporation’s income from that (primary) activity makes up at least 70% of the corporation’s total income; meanwhile, total income refers to the total income as stipulated in Article 6 of the Enterprise Income Tax Law of the People’s

Republic of China.

The directory of preference is categorized into 5

major industries that cover 72 items, including: 37 high and new technology items, 13 medical and health items, 10 scientific teaching and research items, 5 cultural and creative items, and 7 commercial trading and service items.

In addition, targeting those organizations that

have branches both within and outside the new HengQin zone, the policy has specified conditions for applying the preferred tax rates; the directory also provides corresponding provisions for enterprises that simultaneously enjoy conditions for other preferred tax rates. For more information, please visit the website below.

http://www.szds.gov.cn/portal/site/site/portal/szds/content.portal?contentId=E8B0BC4666D4B4A10CED2AF4A4B18545&categoryId=3099

Training Courses:

Overwhelming Registration for All 3 Courses In the second quarter of 2014, the CRAC has

collaborated with both local and foreign professional institutions in hosting 3 different topic-specific-training courses, ranging from investment in Mainland China, cost accounting to audit quality control. Application for these courses had been overwhelming, and 380 students had successfully registered to attend them. Amongst these students, 281 have attended and completed their respective courses, and would be awarded a certificate of attendance issued jointly by the CRAC and the institute in collaboration with very shortly.

Amongst them, the Quality Control for Audits

workshop, jointly hosted by the CRAC and the Union of Association of Professional Accountants of Macao on 17

th May, presented the different audit

requirements stipulated under the International Standards on Auditing (ISAs) to audit practitioners, and covered the following topics: the concepts of quality control for audits as well as audit cycle, common points of attention as well as common issues of and suggestions for audits. Meanwhile, the CRAC co-hosted a How Activity-Based Costing System Maximizes Organization’s Profit? seminar

with the Association of Chartered Certified Accountants (ACCA) on 22

nd May. Activity-based

costing (ABC) treats each activity as independent object for cost calculation, thereby improving the cost system. Because ABC focuses on each cost pool, gradually more enterprises have started to adopt this method for controlling cost. The seminar explored the implementation and application of ABC and the advantages it brings to entities. In this issue of CRAC Bulletin, we shall take a closer look at the third course (Investment in China and Holding Structures Seminar).

The CRAC and the ACCA jointly hosted the

above-titled seminar on 29th April to present the

precautions for investing in real estate properties and shares by understanding taxes in Mainland China as well as the objective of investment. By using both actual and illustrative case studies, the lecturer was able to enhance students’ concept and understandings towards the subject in the simplest and most vivid manner. A Q&A session also allowed the lecturer to answer many of the students’ queries, thereby enhancing teacher-students

CEPA Related News

Training News

Committee for the Registry of Auditors and Accountants 4 July 2014

interactions.

It is noted that, at the time of investing in real

estate properties or shares, the following types of taxes ought to be considered primarily: income-related taxes i.e. turnover tax such as value-added tax (VATs), sales tax and consumption tax; profit-related taxes such as corporate income tax and personal income tax; land and real estate related taxes such as deed tax, land-use tax of cities and towns, housing tax, and land appreciation tax; import-related taxes such as tariffs, import VATs, and consumption tax on imported goods; other taxes such as stamp duty and agricultural tax. In addition, attention must be paid to the effect of the Notice of the State Administration of Taxation on Strengthening the Management of Enterprise Income Tax Collection of Proceeds from Equity Transfers by Non-resident Enterprises (GuoShuiHan [2009] No.698) and, in particular, Article 6 with regard to indirect transfers of equity interests in a Chinese resident enterprise via abuse of organization forms.

The seminar also looked at the precautions of

investing in Mainland China from various aspects: 1. Objective: residential apartment, commercial apartment, or a company; 2. Purpose of ownership: owner-occupy, renting out, receiving share dividends, or to be transferred; 3. Equity structure: owned directly by individuals, owned through companies established outside Mainland China, owned through companies established outside Mainland China and representative office, or owned through foreign-invested enterprises.

Meanwhile, the seminar presented the pros and

cons or influential factors for each of the investment structures, including representative offices, domestic-funded enterprises, and foreign-invested enterprises (including individually-owned businesses). Meanwhile, the lecturer drew special attention to the importance of trademark registration, as well as the discrepancy between total investment and registered capital of foreign-invested enterprises as well its reasonable use.

Date Course Title

No. of Participants

Registered

Candidates

Certificates

Awarded

29th

April Investment in China and Holding Structures 174 123

17th

May Quality Control for Audits 41 37

22nd

May How Activity-Based Costing System Maximizes Organization’s Profit? 165 121

New Standard on Revenue Recognition

The new standard on revenue recognition, one that has received international attention among the accounting profession, has been issued in May 2014. Revenue recognition has always been a key accounting issue and, over the years, requirements of both the International Financial Reporting Standards (IFRS) and the US Generally Accepted Accounting Principles (US GAAP) were different in many levels, which hindered the comparability of financial statements from different parts of the world to a certain extent. In order to improve the comparability of financial statements, the International Accounting Standards Board (IASB) and the Financial Accounting Standard Board (FASB) (hereinafter referred to as the Boards) have jointly issued a discussion paper on revenue recognition as early as December 2008; subsequently, the Boards have issued the first exposure draft in June 2010 and later on, a re-exposure draft (after revisions were made to the original exposure draft) was issued in November

2011. Although it took 5 years to develop from the discussion paper to the new standard, but the issuance of the converged standard on revenue recognition from the Boards has undoubtedly created a milestone in the accounting profession globally. The new standard is expected to revolutionize the way enterprises deal with revenue recognition and, for certain industries such as telecommunications and real estate, the effect would be even more significant.

The Boards have formed the Joint Transition

Resource Group for Revenue Recogntion (TRG) in June 2014. Members of the TRG include financial statement preparers, auditors and users representing a wide spectrum of industries. The TRG will inform the Boards about potential implementation issues that could arise when companies and organizations implement the new Standard. The TRG will also provide stakeholders with an opportunity to learn

International Development of Accounting Standards

Committee for the Registry of Auditors and Accountants 5 July 2014

about the new Standard from others involved with implementation. However, the Boards have stressed that the TRG will not issue guidance. Any stakeholder can submit a potential implementation issue for discussion at TRG meetings (at present scheduled for 2014 and 2015).

In this issue of the CRAC Bulletin, we shall take a brief look at the content of the IASB’s new Standard (please visit www.ifrs.org for the complete Standard).

The IASB latest revenue Standard will be

included in the IFRS as IFRS 15 Revenue from Contracts with Customers. IFRS 15 establishes principles for reporting useful information to users of financial statements about the nature, amount, timing and uncertainty of revenue and cash flows

arising from an entity’s contracts with customers. IFRS 15 is effective for annual periods beginning on or after 1

st January 2017, while earlier

application is permitted. IFRS 15 replaces IAS 11 Construction Contracts, IAS 18 Revenue and related interpretations.

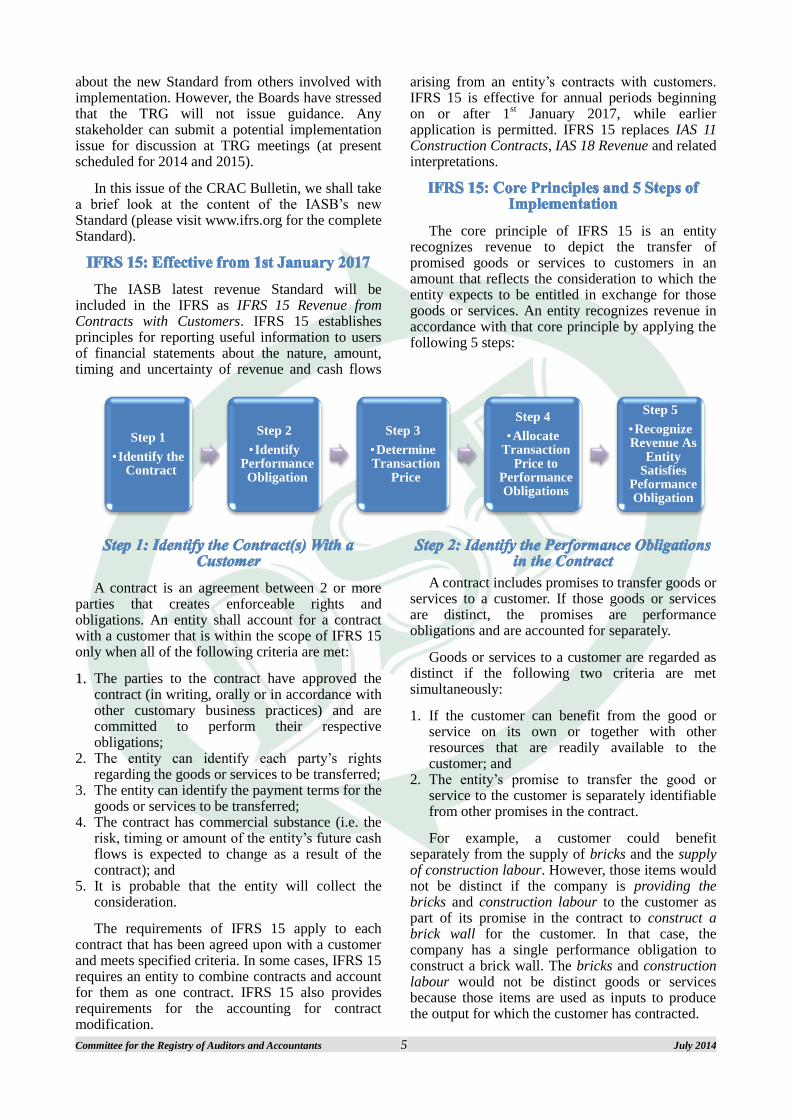

The core principle of IFRS 15 is an entity

recognizes revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. An entity recognizes revenue in accordance with that core principle by applying the following 5 steps:

A contract is an agreement between 2 or more

parties that creates enforceable rights and obligations. An entity shall account for a contract with a customer that is within the scope of IFRS 15 only when all of the following criteria are met:

The parties to the contract have approved the 1. contract (in writing, orally or in accordance with other customary business practices) and are committed to perform their respective obligations;

2. The entity can identify each party’s rights regarding the goods or services to be transferred;

3. The entity can identify the payment terms for the goods or services to be transferred;

4. The contract has commercial substance (i.e. the risk, timing or amount of the entity’s future cash flows is expected to change as a result of the contract); and

5. It is probable that the entity will collect the consideration.

The requirements of IFRS 15 apply to each

contract that has been agreed upon with a customer and meets specified criteria. In some cases, IFRS 15 requires an entity to combine contracts and account for them as one contract. IFRS 15 also provides requirements for the accounting for contract modification.

A contract includes promises to transfer goods or

services to a customer. If those goods or services are distinct, the promises are performance obligations and are accounted for separately.

Goods or services to a customer are regarded as

distinct if the following two criteria are met simultaneously: 1. If the customer can benefit from the good or

service on its own or together with other resources that are readily available to the customer; and

2. The entity’s promise to transfer the good or service to the customer is separately identifiable from other promises in the contract.

For example, a customer could benefit

separately from the supply of bricks and the supply of construction labour. However, those items would not be distinct if the company is providing the bricks and construction labour to the customer as part of its promise in the contract to construct a brick wall for the customer. In that case, the company has a single performance obligation to construct a brick wall. The bricks and construction labour would not be distinct goods or services because those items are used as inputs to produce the output for which the customer has contracted.

Step 1

•Identify the Contract

Step 2

•Identify Performance Obligation

Step 3

•Determine Transaction

Price

Step 4

•Allocate Transaction

Price to Performance Obligations

Step 5

•Recognize Revenue As

Entity Satisfies

Peformance Obligation

Committee for the Registry of Auditors and Accountants 6 July 2014

Statistics As of 30

th June 2014, the number of registered auditors, registered accountants, audit firms, and

accounting firms registered with the Committee for the Registry of Auditors and Accountants is as follows:

Registered Auditors 113

Registered Accountants 170

Registered Audit Firms 13

Registered Accounting Firms 1

The transaction price is the amount of

consideration in a contract to which an entity express to be entitled in exchange for transferring promised goods or services to a customer. In determining the transaction price, the following may be considered:

1. The transaction price can be a fixed amount of

customer consideration, but it may sometimes include variable consideration or consideration in a form other than cash;

2. The transaction price is also adjusted for the effects of the time value of money if the contract includes a significant financing component and for any consideration payable to the customer;

3. If the consideration is variable, an entity estimates the amount of consideration to which it will be entitled in exchange for the promised goods or services. The estimated amount of variable consideration will be included in the transaction price only to the extent that it is highly probable that a significant reversal in the amount of cumulative revenue recognized will not occur when the uncertainty associated with the variable consideration is subsequently resolved.

An entity typically allocates the transaction

price to each performance obligation on the basis of the relative stand-alone selling prices of each distinct good or service promised in the contract. If a stand-alone selling price is not observable, an entity estimates it. Sometimes, the transaction price includes a discount or a variable amount of consideration that relates entirely to a part of the contract. The requirements specify when an entity allocates the discount or variable consideration to one or more, but not all, performance obligations in the contract.

An entity recognizes revenue when (or as) it

satisfies a performance obligation by transferring a promised good or service to a customer (which is when the customer obtains control of the good or service). The amount of revenue recognized is the amount allocated to the satisfied performance obligation.

A performance obligation may be satisfied: 1. At

a point in time (typically for promises to transfer goods to a customer); or 2. Over time (typically for promises to transfer services to a customer). For performance obligation satisfied over time, an entity recognizes revenue over time by selecting an appropriate method for measuring the entity’s progress towards complete satisfaction of that performance obligation.

Committee for the Registry of Auditors and Accountants

Address : 1/F, Centro de Recursos da Direcção dos Serviços de Finanças No. 30, Rua da Sé, Macau

Tel : (853) 8599 5343, 8599 5344 Fax : (853) 2838 9177 E-mail : [email protected] Website : http://www.dsf.gov.mo

Accounting Standards Hotline

(853) 8599 5300

Editorial Contributions are Welcome!