review of management accounting research - springer978-0-230-35327-5/1.pdf · 13 management...

TRANSCRIPT

Review of Management Accounting Research

Also by Magdy G. Abdel-Kader

PERFORMANCE MEASUREMENT OF NEW PRODUCT DEVELOPMENTTEAMS IN HIGH TECHNOLOGY SECTOR (with E. Lin)

ENTERPRISE RESOURCE PLANNING (ERP) IMPLEMENTATION AND MANAGEMENT ACCOUNTING CHANGE IN A TRANSITIONALCOUNTRY (with A. Kholeif and M. Sherer)rr

NON-FINANCIAL PERFORMANCE MEASUREMENT AND MANAGEMENT PRACTICES IN MANUFACTURING FIRMS: A Comparative International Analysis (with A. Abdel-Maksoud)

BEHAVIOURAL ASPECTS OF AUDITORS’ EVIDENCEEVALUATION (with M. Abou-Seada)

INVESTMENT DECISIONS IN ADVANCED MANUFACTURING TECHNOLOGY: A Fuzzy Set Theory Approach (with D. Dugdale and P. Taylor)rr

Review of ManagementAccounting Research

Edited by

Magdy G. Abdel-KaderUniversity of Bedfordshire, UK

Editorial matter and selection © Magdy G. Abdel-Kader 2011 Individual chapters © respective authors 2011Foreword © Marc J. Epstein 2011

All rights reserved. No reproduction, copy or transmission of this publication may be made without written permission.

No portion of this publication may be reproduced, copied or transmitted save with written permission or in accordance with the provisions of the Copyright, Designs and Patents Act 1988, or under the terms of any licence permitting limited copying issued by the Copyright Licensing Agency, Saffron House, 6–10 Kirby Street, London EC1N 8TS.

Any person who does any unauthorized act in relation to this publication may be liable to criminal prosecution and civil claims for damages.

The authors have asserted their rights to be identified as the authors of this work in accordance with the Copyright, Designs and Patents Act 1988.

First published 2011 byPALGRAVE MACMILLAN

Palgrave Macmillan in the UK is an imprint of Macmillan Publishers Limited,registered in England, company number 785998, of Houndmills, Basingstoke, Hampshire RG21 6XS.

Palgrave Macmillan in the US is a division of St Martin’s Press LLC, 175 Fifth Avenue, New York, NY 10010.

Palgrave Macmillan is the global academic imprint of the above companies and has companies and representatives throughout the world.

Palgrave® and Macmillan® are registered trademarks in the United States,the United Kingdom, Europe and other countries.

This book is printed on paper suitable for recycling and made from fully managed and sustained forest sources. Logging, pulping and manufacturing processes are expected to conform to the environmental regulations of the country of origin.

A catalogue record for this book is available from the British Library.

A catalog record for this book is available from the Library of Congress.

10 9 8 7 6 5 4 3 2 120 19 18 17 16 15 14 13 12 11

ISBN 978-1-349-32197-1 ISBN 978-0-230-35327-5 (eBook)DOI 10.1057/9780230353275

To my sonMohamed

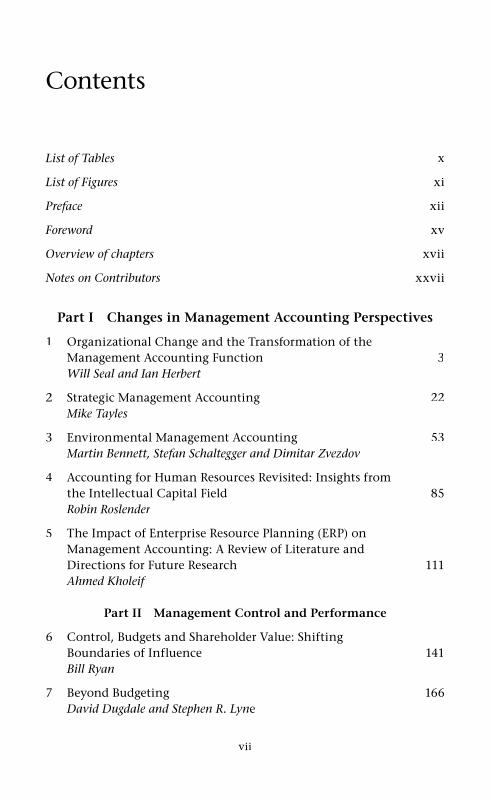

vii

Contents

List of Tables x

List of Figures xi

Preface xii

Foreword xv

Overview of chapters xvii

Notes on Contributors xxvii

Part I Changes in Management Accounting Perspectives

1 Organizational Change and the Transformation of theManagement Accounting Function 3

Will Seal and Ian Herbert

2 Strategic Management Accounting 22 Mike Tayles

3 Environmental Management Accounting 53Martin Bennett, Stefan Schaltegger and Dimitar Zvezdov

4 Accounting for Human Resources Revisited: Insights fromthe Intellectual Capital Field 85Robin Roslender

5 The Impact of Enterprise Resource Planning (ERP) onManagement Accounting: A Review of Literature and Directions for Future Research 111Ahmed Kholeif

Part II Management Control and Performance

6 Control, Budgets and Shareholder Value: Shifting Boundaries of Influence 141Bill Ryan

7 Beyond Budgeting 166David Dugdale and Stephen R. Lyne

viii Contents

8 Constructing Performance Measurement Packages 194Morten Jakobsen, Falconer Mitchell and Hanne Nørreklit

9 Balanced Scorecard Development: A Review of Literature and Directions for Future Research 214Magdy Abdel-Kader, Souad Moufty and Erkki K. Laitinen

Part III Cost Management and Decision Making

10 The Activity-Based Approach 243John Innes and Reza Kouhy

11 Target Costing 275Il-woon Kim and Emily Berry

12 Throughput Accounting 295Tony Tollington and Venkateswara Pilla

13 Management Accounting in Pricing Decisions 311Erkki K. Laitinen

14 Capital Investment Appraisal 343Elaine Pamela Harris and Moataz El-Massri

Part IV Applications of Management Accounting inSpecific Sectors

15 Management Accounting and Control Research inPublic Organizations 381Raili Pollanen

16 Review of Management Control Change Research withSpecial Reference to the Public Sector and Less Developed Countries: A Critical Evaluation 415Junaid Ashraf and Shahzad Uddin

17 Performance Management in Non-Profit Organizations 450Billy Wadongo and Magdy Abdel-Kader

18 Inter-Organizational Performance Measurement Practicesbetween Supply Chain Partners: Issues for the Agri-FoodIndustry 479Lisa Jack

19 Management Accounting Research in the Hospitality Sector 497Will Seal and Ruth Mattimoe

Contents ix

Part V Methodological Issues in Management Accounting Research

20 The Positivistic Approach to Management Accounting:Recent Developments and Future Directions 523Ahmed Kholeif

21 Ontological Dependency on Epistemology Strategy:Interpretive Management Accounting Research Revisited 543Danture Wickramasinghe

Index 567

x

Tables

1.1 Outlooks on the management accounting function 1312.1 Limitations and advantages of throughput accounting 29712.2 Machine operations for the month 30012.3 Product-wise unit revenue and cost details for

the month 30012.4 Case calculations 30113.1 Examples of information provided by MAS on

customer behaviour for pricing 32013.2 Examples of information provided by MAS on

competition for pricing 32513.3 Examples of information provided by MAS on

product cost for pricing 32813.4 The effect of profit and sales targets on pricing decision 33113.5 Examples of information provided by MAS on

the effect of pricing targets 33213.6 Examples of information provided by MAS on

marketing mix decision 33514.1 Strategic studies 36014.2 Behavioural studies 36115.1 Journals, location of editors and editorial objectives 39115.2 Research topics 39315.3 Regions and countries 39815.4 Type of public sectors 40015.5 Main research methods 40215.6 Theoretical foundations 404

xi

Figures

1.1 A process versus a structural view of organization 5 1.2 Moving to a shared service centre model 8 3.1 EMA Framework 61 7.1 Limitations of traditional budgeting 169 7.2 More for less: the new model in a nutshell 173 7.3 Hope and Fraser’s critique of budgeting 176 7.4 Comparison of traditional criticisms of budgets

with those of Hope and Fraser 178 7.5 BBRT North America: company membership 180 7.6 Criticisms of budgeting 184 7.7 Structural analysis 189 8.1 Relationship between objectives, action variables and

action plans 201 8.2 The structure of causal, intervening and end

result model 203 8.3 The structure of the performance pyramid 204 8.4 The balanced scorecard structure 205 8.5 The structure of the performance prism 20611.1 The origin of target costing 27611.2 Target costing equation 27911.3 Target costing process and context 28511.4 Determining Target Cost 28711.5 Comparison of Western and Japanese approaches

to Target Costing 29113.1 Three hierarchic levels of pricing decision making 31213.2 The role of pricing in business decision-making process 31413.3 Purchasing process of a customer 31614.1 Investment appraisal process 34716.1 Literature review classificatory scheme 41720.1 Positivistic theory testing and development 535

xii

Preface

Over the past three decades, management accounting has seen a numberof innovative techniques, tools and philosophies. The most notable con-tributions include activity-based techniques, Balanced Scorecard, strate-gic management accounting, Beyond Budgeting, and sustainability and environmental management accounting. Arguably, these contributions are in response to criticisms that have been levelled at managementaccounting practices. Johnson and Kaplan’s argument of managementaccounting practice relevance lost has been cited as the main motive to call for changes in management accounting to keep up with the ‘revolu-tion’ in the information and manufacturing technologies as well as thenew competitive environment. Thus, there has been extensive researchin management accounting that aims to shift the traditional manage-ment accounting role of cost determination and financial control to amore ‘sophisticated’ role of creating value.

The accumulation of management accounting research over the yearshas created a challenge for new researchers. While textbooks of man-agement accounting normally place emphasis on established conceptsand practices, mainstream accounting academic journals are engaged in cutting-edge research of management accounting. Thus, this book aims to review management accounting research to bridge the gapbetween textbooks and mainstream academic journals. Contributionsto this book represent a variety in management accounting research in terms of topics, contexts, theories and research methods. In particular, this book is of interest to research students, academics and professional management accountants who want to gain a thorough understanding of the development of management accounting and its underpinningtheory and applications.

The book consists of 21 chapters. Each chapter reviews the extant research in a management accounting issue to explain its core concept, development, current criticisms and controversies and concludes by identifying gaps in the literature and suggestions for further research.Each chapter has been subject to a single-blind review process in which the reviewer was anonymous. The chapters are organized in five parts.Each part focuses on a particular theme, but there may be overlaps among contributions in different parts as this is the nature of manage-ment accounting research.

Preface xiii

Part I includes five chapters that review research on changes in man-agement accounting perspectives. The first chapter (Seal and Herbert)reviews research on organizational change and the transformation of the management accounting function. This is followed by four chap-ters, each looking at management accounting from different but relatedperspectives (strategic management accounting by Tayles, in Chapter 2,environmental management accounting by Bennett, Schaltegger and Zvezdov, in Chapter 3, human resources by Roslender, in Chapter 4, and enterprise resource planning by Kholeif, in Chapter 5).

Part II reviews literature on issues related to management control andperformance. Ryan, in Chapter 6, uses the analogy of boundaries totrace changes in organizational control. In particular, issues of budgetand budgetary control and shareholder value are reviewed. Chapter 7(Dugdale and Lyne) reviews the Beyond Budgeting theme and tracesits origins, cases and impact. Chapters 8 and 9 review research on per-formance management. Jakobsen, Mitchell and Nørreklit (Chapter 8) focus on constructing performance measurement packages fromgeneric to firm-specific packages. In Chapter 9, Abdel-Kader, Moufty and Laitinen trace the development of balanced scorecard (BSC) andidentify three generations of its development. Further, they reviewresearch related to two themes: applications of BSC in practice and BSC assumptions.

Management accounting techniques of cost management and deci-sion making are reviewed in Part III. Innes and Kouhy (Chapter 10) give a brief history of activity-based approach and discuss research approaches such as surveys and case studies that have been used to study the application of activity-based approach in practice. Then fac-ets of activity-based approach, such as success factors, diffusion, power and politics and organizational culture and effect on performance arereviewed. Chapter 11 (Kim and Berry) explains target costing as a strate-gic weapon in controlling costs while producing high-quality products as desired by customers. In Chapter 12, Tollington and Pilla discuss the application of theory of constraints and throughput accounting to the management of production bottlenecks. Chapters 13 and 14 focus on management accounting research of pricing decisions (Laitinen) and of capital investment appraisal (Harris and El-Massri).

Part IV (Chapters 15–19) reviews applications of management accounting in specific sectors. The first three chapters focus on the pub-lic sector and non-governmental organizations. Pollanen, in Chapter 15,analyses literature of management accounting and control (MAC) prac-tices. The analysis shows the main research themes, methods, countries

xiv Preface

and regions, types of public sectors and theoretical foundation of MAC research published in 18 major accounting journals. Chapter 16 (Ashraf and Uddin) focuses on research of management control change in the public sector and less-developed countries. Based on the theoretical underpinning of the research, they classify the literature into main-stream (positivistic) research and alternative research. The alternativeresearch of MAC change has further been seen from three perspec-tives of agential, structural and third ways. Ashraf and Uddin argue that these three perspectives need to be incorporated to explain MAC change and the application of Habermasian theory, and labour process/cultural political economy provide a fuller picture of management con-trol change. Wadongo and Abdel-Kader, in Chapter 17, review literatureof performance management in non-profit organizations (NPO) and identify three streams of research that focus on the concept, determi-nants and frameworks of performance management within NPO. The remaining two chapters in this part focus on the application of man-agement accounting practices in two sectors that have received little attention until recently. Chapter 18 (Jack) reviews literature on inter-organizational performance measurement practices between supply chain partners within the agri-food industry, and Chapter 19 (Seal andMattimoe) discusses the management accounting research within thehospitality sector.

The final part of this book is devoted to two methodological issuesthat are commonly adopted in the management accounting research.Chapter 20, by Kholeif, critically reviews the mainstream positivistic approach to management accounting research, while Wickramasinghe, in Chapter 21, focuses on interpretive management accountingresearch.

Finally, I would like to thank all of the chapters’ authors for theircontributions and for their reviews of others’ contributions. Thanks are also due to Palgrave Macmillan and particularly to Lisa von Fircks and Gemma d’Arcy Hughes for their support.

MAGDY ABDEL-KADER

xv

Foreword

Management accounting and control looks very different today than it did just a few decades ago. Both in academic research and in managementpractice, the discussion of accounting for organizational costs and theuse of accounting information for management decision making havedramatically changed. Further, the development of systems to improveorganizational decision making has included new insights that rely on better tools to more broadly evaluate organizational performance.

The new analyses are increasingly sensitive to individual and organi-zational behavioral factors. Managing organizations has now been recognized to necessarily include concerns related to organizationalchange, environmental and social issues, corporate governance andmany others that were of little concern a few decades ago. Researchers in management accounting and control have turned more attention to the issues of identifying and measuring and including these issues into providing appropriate information for effective decisions.

With the expansion of the scope of the field, management account-ing and control researchers have expanded the list of problems they address and the research methods they use. The increased skills andtraining of management accounting researchers have also facilitated the broadening of the field and the contribution that they have made.

Magdy Abdel-Kader has provided a significant contribution with thisvolume. By carefully selecting topics that are essential elements of study and authors with significant expertise in their fields, the contributors to this volume provide an important overview for students of manage-ment accounting and control practice and research. This book can beused in courses in the field as an introduction to the many areas of important research. It can also be used for those who are beginning a new focus and want an easily accessible introduction to the state of the field in each area. For management accounting and control researchersto continue to make significant contributions to the advancement of both research and practice, this review of the state of the art in the fieldis critical.

But now, it is important to continue to build on the state of the artand develop new approaches to many of these areas. Environmental and sustainability accounting still requires the development of improved

xvi Foreword

systems and methods for identifying and measuring social and environ-mental impacts. It then needs testing of proposed and existing systems to determine which ones work and why, and how improved systems can be developed. Likewise, similar approaches are needed for otherperformance measurement and control systems. The relatively new concerns for the effectiveness of boards of directors and governance of both for profit and non-profit organizations need more attention from management control and performance measurement researchers to determine how accounting and control can be used to improve govern-ance, leadership and performance. With careful research of new meas-urement approaches and new systems for implementation, effectiveness can be increased.

Though some progress has been made, the studies of the effectiveness of various existing performance measurement systems are still in theirinfancy. Management accounting and control can make major contri-butions to organizational effectiveness if the increased rigour that has been developed over the past couple of decades is continued, but much work still needs to be done. This volume provides a start for researchers who want to understand the current state of the art, but building onthis work is even more important.

I am hopeful that this volume will provide an important buildingblock for future developments in both research and practice in manage-ment accounting, management control and performance measurement. I look forward to seeing a new volume in ten years with significantly new developments and contributions that change both the field and organizational effectiveness in general.

PROFESSOR MR ARC J. EPSTEIN

Rice University, USA

xvii

Overview of chapters

Chapter 1

The chapter critically reviews research that has focused on the way that the management accounting function has responded to the impact of organizational change. The latter has seen new variants of the divi-sionalized corporation with shared service centres as well as the out-sourcing of a range of business support services. There seems to be a mixture of ‘pure elements’, organizational hybrids and the hybridiza-tion of working practices. Some voices in the profession argue that the management accounting function is expected to complete its transfor-mation from a transaction-processing focus to a fully fledged ‘business partner’ with a high-decision support capability. Much of the mana-gerial discourse has been produced by management consultants andprofessional bodies.

Chapter 2

For almost three decades, some have seen Strategic Management Accounting (SMA) as the appropriate response to the problems emanat-ing from a changed competitive and technological environment. Some accounting researchers have seen SMA as implying a greater contribu-tion by accountants to strategy formulation and implementation. Somehave viewed it as suggesting accountants move away from purely finan-cial concerns to wider business issues. Others have seen it as an oppor-tunity to make accounting relevant again and to elevate its standing relative to other functions within organizations.

This chapter will first clarify the strategy concepts employed by SMAresearchers. It will then point to the interpretations of SMA (or similarterms such as Strategic Cost Management) that various authors have promoted. This has involved consideration of, for example, value chain,cost drivers and competitive advantage, but has also been extended to embrace a wider range of management accounting techniques whichhave a long-term, forward-looking and outward orientation. The rel-evance of these techniques to strategy is briefly outlined. The conclud-ing section will assess the extent to which these techniques support organizations in taking forward their strategy, how they relate to firms’

xviii Overview of chapters

market and economic performance and, finally, their implications for the management accountants’ role.

Chapter 3

In recent years, the natural environment and sustainability have become an increasingly significant variable in the strategic context in which business has to operate. This chapter examines how environ-mental issues, in particular, are influencing this context and can have an impact on business organizations. It then goes on to review recent literature on environmental management accounting (EMA), which itargues can be understood as the application of management account-ing to support business in responding to this challenge, ranging from relatively simple adaptations of conventional cost accounting practice to more complex and ambitious innovations. It concludes by suggest-ing some directions for further research, including the application of management accounting into the social aspects of sustainability and investigation into institutional differences between different organiza-tions and countries, and predicts that as EMA becomes more estab-lished, it is increasingly likely to become systematized and embeddedin accounting systems and to be managed by organizations’ account-ing functions.

Chapter 4

Absent from the rejuvenation of managerial accounting that has occurredduring the past 25 years has been any attempt to revisit accounting for human resources. This is despite the acknowledged growing impor-tance of employees within all organizations and the observation that human resource accounting itself was always envisaged as a managerial accounting development. Fortunately, a number of pertinent develop-ments that hold out the possibility of taking employees into account asa further element of the new management accounting have emerged inthe intellectual capital field. Of particular significance are advances in reporting, including the identification of a number of scoreboard frame-works together with narrative-based approaches. These are reviewed inthe course of the chapter, which concludes by identifying employeehealth and wellbeing as an important new issue that merits the atten-tion of those responsible for accounting to management.

Overview of chapters xix

Chapter 5

Extant management accounting research shows that there is a growing interest in the impact of Enterprise Resource Planning (ERP) on man-agement accounting. In order to advance research within this area, anunderstanding of what research has already done and what research is needed is of particular importance. The purpose of this chapter is to review the recent literature on the role of ERP systems in changing or stabilizing management accounting systems and practices and manage-ment accountants’ roles and relationships in order to identify gaps inthis literature and suggest future research opportunities. The outcome of this review is an identification of research gaps and a proposal of research opportunities classified into the following categories: (1) the role of ERP systems in changing and stabilizing management account-ing or management control techniques; (2) the implications of ERP systems for the management accounting profession; (3) ERP and man-agement accounting change and stability: less developed vs developedcountries; (4) ERP and management accounting change and stabilities:research methods and paradigms; (5) ERP and the future dominanceof management accounting over financial accounting; (6) ERP, misfit problem and management accounting change and stability; (7) ERP,other organizational change programs and management accounting change and stability; and (8) ERP vs Strategic Enterprise Management (SEM) and management accounting change and stability.

Chapter 6

This chapter contributes to the current debate and studies around devel-opments in organizational control. The analogy of boundaries is used in order to trace out change aspects in the area of organizational per-formance control. For example, budgets and budgetary control are partof organizational control and are concerned with controlling or guid-ing the behaviour of organizational members for some organizationalgoals to be achieved (Tannenbaum, 1962; Anthony, 1965; Anthony and Deardon, 1980). Budgets have gone through various iterations over thepast few decades, from being seen as a rational utopian type answerto control in organizations to the more recent work where budgets areseen as almost obsolete and something to be avoided (Hope and Fraser,2003). Of particular concern are the ideological and pragmatic changes in the business context as to the manner and influence of budgets. The

xx Overview of chapters

context also shows major changes in other aspects of business perform-ance control, such as the development of Shareholder Value particularly with regard to the notion of influence and control of the firm.

Chapter 7

Budgeting in private companies has been well understood for almosta century. Although criticized for encouraging gaming, constraining management and both(!) slack and over-ambitious targeting, budgetingwas considered necessary until the late 1990s, when Hope and Fraser mounted their ‘Beyond Budgeting’ attack. They went much furtherthan the traditional critiques and called for the abandonment of budg-eting systems.

In this chapter, the ‘Beyond Budgeting’ movement is traced from an initial interest in ‘advanced budgeting’ to the recommendation to aban-don budgeting. Development of the Beyond Budgeting Round Table (BBRT) is described, and the early cases that shaped Beyond Budgetingare reviewed. The chapter includes a comparison of the traditional cri-tique of budgeting with the contemporary Beyond Budgeting critique, noting that, although the criticisms seem similar, the Beyond Budgetingposition is much more radical and espouses changes to organizational structure and culture, not just budgeting systems.

The limited independent research into the impact of Beyond Budgeting is reviewed, and it is concluded that, as yet, the movement has made little impact on practice or managerial attitudes. The chapter concludes with an attempt to reconcile the Beyond Budgeting case with practice. It may be possible to abandon budgets at corporate headquar-ters so long as business units have sufficient autonomy. However, it is suggested that, within business units, where significant coordinationissues might exist, budgeting might continue to be important.

Chapter 8

This chapter covers the area of constructing performance-measurementpackages from generic packages to firm-specific packages grounded in the practice of managerial decision making. The chapter begins with an outline of the purposes of performance measurement, followed by a section that discusses the six most common generic performance-measurement packages. Thereafter follows a discussion of the design of performance packages for the specific firm and the managerial chal-lenges the package is intended to solve. The chapter does not provide a

Overview of chapters xxi

standard solution to this task but raises a number of issues to consider in order to ensure successful design of firm-specific performance-meas-urement packages that can form both a reliable and valid foundationfor decision making throughout the organization.

Chapter 9

This chapter reviews the increasing literature concerning Balanced Scorecard (BSC) to gain an understanding of how this technique hasemerged and developed. BSC has become a popular tool, especially in the US and in European countries such as the UK, Germany, Sweden andFinland. However, in some countries, such as France and Japan, it has notbeen popular. The literature shows a positive correlation between firms’size and BSC’s usage and a high rate of failure in its adoption. However,there is little agreement on the effect of BSC on organizational perform-ance, the number, contents and weights of BSC perspectives and meas-ures, or the cause-and-effect relationships between the perspectives.

Chapter 10

The activity-based (AB) approach concentrates on overhead costs andhas been used in both private- and public-sector organizations. In the 1980s, Cooper and Kaplan promoted the AB approach with conceptssuch as cost pools and cost drivers. The AB approach includes prod-uct costing, customer costing (and profitability), costing of distributionchannels, budgeting, cost management, performance management and decision making. AB case studies and surveys have been conducted in many countries – particularly in the 1990s and 2000s. Researchers have explored several topics relating to the AB approach, including meas-ures of success, factors associated with success, diffusion (including demand and supply factors), power and politics and organizational cul-ture, effects on financial performance, changing role of management accountants and managers’ views. The development (in the 2000s) of time-driven AB costing requires further research, as do many aspects of the ‘traditional’ AB approach.

Chapter 11

Target costing, the methodology of determining the allowable amount of cost that can be incurred on a product and still earn the requiredprofit from that product, has been used in Japan for almost 40 years. It

xxii Overview of chapters

is a strategic weapon in controlling costs while producing high-quality products containing features and functionality desired by customers.Initially started by Toyota in the late 1960s, target costing evolved not from a vision but from the need to respond to changes in the externalenvironment (Kim et al., 2004).

The aim of this chapter is to provide a comprehensive and practicalview on target costing by presenting its history, methodology, imple-mentation and successes within the United States. The chapter willbe useful for the target costing manager to balance the managementaspects of implementing target costing along with the technical tasksto be accomplished. It will be useful for both academicians and prac-titioners in their efforts to enhance target costing in both theory and practice.

Chapter 12

There is no practical use of knowing an accurate product cost if the product fails on other grounds, such as poor quality, delayed delivery to the marketplace or lack of innovation in a rapidly changing busi-ness environment. In this short chapter, we focus upon accounting forthroughput; that is, the speed of response of a business entity to the mar-ket place and that too from a manufacturing perspective. The Goldratt’s Theory of Constraints (TOC) and the Throughput Accounting ratio (TA ratio) developed by Galloway and Waldron are critically discussed and then applied to the management of production bottlenecks in an illus-trative case. In addition, literature review is carried out to look into thecurrent state of use of throughput accounting and its evolution from the 1980s. In view of the positive contribution of throughput account-ing in taking complex decisions in a continuously changing businessenvironment, further research is suggested.

Chapter 13

A pricing decision is one of the most important decisions made by the management. It is, however, very scarcely considered in managementaccounting (MA) research and textbooks. This chapter responds to thelack of consideration describing the role of MA and MA systems (MAS) in pricing decisions. Its purpose is to discuss the different perspectives of pricing decisions and their connections to MAS. First, the complexity of pricing decisions is emphasized. This complexity leads to the need for a broad scope of MA information. Second, the role of MAS in customer

Overview of chapters xxiii

analysis within pricing decisions is recognized as an impulse for new product development, established product improvement and demandquantity analysis. Third, this role is however considered different indifferent competitive environments (perfect competition, monopoly, monopolistic competition). Fourth, traditional product costing is regarded as playing both planning (ex ante) and control (ex post) rolesin pricing decisions. Fifth, it is showed that different pricing targets are crucial for pricing. Sixth, it is emphasized that MAS plays an importantrole in marketing mix decisions. Pricing is only one but integral part of these decisions.

Chapter 14

This chapter traces the development of the theory and practice of capi-tal investment appraisal from its origins through to recent case studiesand field work, with a particular emphasis on the behavioural aspects of the capital investment decision (CID) making process. It highlightsthe need for researchers in this area to understand the psychology of decision making as well as the socio-political context of organizational management in order to develop theory in this area. It also identifiespotentially fruitful avenues for further research to address the needsof different types of organization at different stages of developmentacross the world. Cases are drawn from publicly owned organizationsand small- to medium-sized enterprises as well as multi-national corpo-rations. Indeed, there is significant scope for new investment appraisalmodels and techniques to be developed closely with potential users toensure that management accounting for strategic control remains rel-evant for the majority of organizations, not just those with a primary profit motive.

Chapter 15

This chapter reviews academic literature on management accountingand control (MAC) practices in the public sector in the 2000s. Publicorganizations have increasingly adopted MAC techniques that havebeen traditionally developed and used in the private sector, for exampleactivity-based costing and balanced scorecards. Such techniques havecommonly been adopted in response to widespread pressures on public organizations to improve the efficiency and effectiveness of their opera-tions and services, as well as accountability to regulators, the public and other stakeholders. The review reveals a trend towards MAC techniques

xxiv Overview of chapters

being considered within their broader organizational, regulatory and social context. The regulatory and political environment and multipleaccountability relationships are particularly important contextual con-straints affecting public organizations. However, research in general is limited by some gaps in the topical coverage and by most studies being conducted only in a few regions and countries and published only in afew specialty journals.

Chapter 16

This chapter critically evaluates ‘management control change research’in general, with special emphasis on the public sector and less-developedcountries in particular. Recent trends in researching the public sector in less-developed countries, focusing on management control change,are identified and discussed in the chapter. The extant accounting lit-erature on management control change is broadly divided into two the-oretical camps, that is ‘mainstream’ and ‘alternative’. The alternativecamp is further subdivided into three perspectives, namely ‘agential’,‘structural’ and ‘third ways perspectives’. After a review of the litera-ture on management control change in general, research carried out in public-sector organizations and in less-developed countries is alsoreviewed. The chapter argues that, in order to make robust explana-tions of management control change, structural, ‘ideational’ and agen-tial perspectives need to be incorporated in a theoretical framework.Without denying the contributions from other perspectives, the chap-ter points out that the Habermasian theory and labour process/cultural political economy do seem to provide some acknowledgements of all three aspects of our social and organizational life.

Chapter 17

Non-profit organizations have become major players in internationaldevelopment, particularly in developing countries. Consequently, thereis an increasing demand for developing a comprehensive performance management system in such organizations. While there has been someresearch that focuses on design, adoption and use of performance meas-urement and management systems in for-profit organizations, there is limited research focused on performance management practices inthe voluntary sector. In particular, only few studies have investigated determinants of performance measurement practices and their effectswithin non-profit organizations. Therefore, this chapter aims to review

Overview of chapters xxv

the literature of performance management systems to identify gaps forfuture research in non-governmental organizations.

Chapter 18

Inter-organizational performance measurement (IOPM) is an emerging area of study for researchers. The current position of IOPM research is reviewed in this chapter, in the context of the agri-food industry, with its complex and fragmentary supply chains. The fundamental issues of identifying the key performance indicators and information flows, the need for good communications and trust and integration with computer-based technologies form the platform for ongoing research. However, whether these approaches should be functional and pre-scriptive, or interpretative, is also a matter of concern for management accounting researchers, and the path is open for innovative interdisci-plinary research in this field.

Chapter 19

The chapter reviews management accounting research in the hospitality sector. The sector has generated a rich literature on the links betweenmanagement accounting concepts and practice. Although some of the work is industry-specific and based largely on contingency approaches, there are examples of how research in the area has contributed to more general innovations based on institutional and practice theories. Future research, particularly in pricing and room stock management, is prompted by continuing improvements in IT and Internet-based dis-tribution with immense possibilities for gathering, analysing and inte-grating market intelligence.

Chapter 20

The mainstream positivistic approach to management accounting research seeks to provide essentially rational explanations to socialphenomena. Reviewing the recent developments in this approach to provide some directions for future research is the main aim of this chapter. Various recent issues surrounding the use of this approach inmanagement accounting research have been reviewed in this chapter,including the recent debate around empirical positivistic research inmanagement accounting, the sound definition of management account-ing constructs, the closure of the gap between surveys and case studies

xxvi Overview of chapters

in management accounting research, the appropriate use of statistical methods for testing hypotheses in management accounting and the use of graphics to map theory-consistent empirical research. Based on this review, some guidelines and recommendations are offered.

Chapter 21

This chapter reviews emerging ontologies and their epistemological roles manifested in interpretive management accounting research. It defines the notions of ontology, epistemology, methodology and interpretive management accounting research and their philosophical interdepend-encies and shows how ontological assumptions influence the research-er’s epistemological stance, which, in turn, influences methodologicalchoices and scientific knowledge production. It then provides a critique of mainstream management accounting research. Having shown howcritiques led to the promotion of the case study approach, the chapterproceeds to illustrate how social and organizational theories are used toprovide plausible explanations for case study stories and how scientific knowledge is thereby produced. Finally, it explores the validity of sci-entific knowledge and the implications of these validity claims for the interpretive research in management accounting.

xxvii

Contributors

Magdy G. Abdel-Kader is Professor in Management Accountingrat the University of Bedfordshire, UK and the Editor-in-Chief of the International Journal of Management Accounting Research. His mainresearch interests include management accounting, performance man-agement and capital investment decisions. He is the co-author of books on investment decision in AMT, enterprise resources planning (ERP) and performance measurement of new product development teams and is co-editor of a book on performance evaluation of shop floor [email protected]

Muhammad J. Ashraf is Assistant Professor in Accounting at Suleman fDawood School of Business, Lahore University of Management Sciences, Pakistan. His current research focus is on studying management con-trol changes in public-sector organizations operating in less-developedcountries. [email protected]

Martin Bennett is Emeritus Reader in Sustainability Accounting at the University of Gloucestershire, UK and a Fellow of the Institute of Chartered Accountants in England and Wales and has served on its Sustainability Committee since its inception, as well as on several reviewgroups on sustainability issues. He is a founder member and past Chair of the Environmental and Sustainability Management Accounting Network (EMAN). [email protected]

Emily Berry is a graduate assistant with the George W. Daverio Schoolof Accountancy at the University of Akron, USA. [email protected]

David Dugdale is Professor Emeritus in Management Accounting at the University of Bristol, UK. His research interests include costing systems and performance management. He has served on the RAE panel for accounting and finance and several CIMA committees and as AssociateEditor of the British Accounting Review. [email protected]

Moataz Elmassri is Assistant Lecturer in the Department of Accountingat Zagazig University, Zagazig, Egypt. He gained his M.Sc. in Accounting and Finance at De Montfort University, Leicester, UK. He teaches

xxviii Notes on Contributors

management accounting at undergraduate and professional [email protected]

Elaine Harris is Professor in Accounting and Management and Directorof Roehampton University Business School in London. She is the authorof Gower Publishing’s Strategic Project Risk Appraisal and Managementand Managing Editor of Emerald’s Journal of Applied Accounting Research(JAAR). She chairs the Management Control Association (MCA) and is a member of ACCA’s Research Committee and CIMA’s Lifelong LearningPolicy Committee. [email protected]

Ian Herbert is Senior Lecturer at the School of Business and Economics,Loughborough University, UK. He teaches courses in managementaccounting at undergraduate and post-graduate levels. His researchinterests are the evolving role of the finance function and the impactof shared services on the design of the multidivisional company andprofessional work. [email protected]

John Innes is Emeritus Professor at the University of Dundee, UK. His research interests include the activity-based approach, Japanese cost man-agement and the role of management accountants. [email protected]

Lisa Jack is Professor in Accounting at the University of Portsmouth, UK.She qualified as an accountant and worked as an auditor before movinginto teaching and research. She was a lecturer at University of Essex before becoming Professor in Accounting at University of Portsmouthin 2009. Her main areas of research are performance measurement and the agri-food industry. [email protected]

Morten Jakobsen is Associate Professor in Management Accountingat Aarhus School of Business and Social Science, Aarhus University, Denmark. His research areas are management accounting and gov-ernmentality, management accounting and inter-organizational rela-tions and managerial practices concerning performance measures. [email protected]

Ahmed Kholeif is Senior Lecturer in Accounting at Edge Hill University,fUK. He has lectured at Alexandria University, Egypt; University of Essex, UK; and King Faisal University, Saudi Arabia. His research inter-ests include ERP systems, management accounting change, structura-tion theory and institutional theory. [email protected]

Il-woon Kim is Professor in Accounting and International Businessand Associate Director of Institute for Global Business at University of

Notes on Contributors xxix

Akron, USA. He has published numerous articles on target costing andother topics, and through CAM-I, he has worked on many target costingprojects with large companies around the world. [email protected]

Reza Kouhy is Professor in Accounting at the University of Abertay Dundee, UK. His research interests include human resource account-ing, energy accounting and performance management. [email protected]

Erkki K. Laitinen is Professor in Accounting and Finance at the University of Vaasa, Finland. His main research interests are manage-ment accounting and control systems, failure prediction and financialstatement analysis. He has published a large number of scientific [email protected]

Stephen Lyne is Head of the School of Economics, Finance and Management at the University of Bristol, UK. His main research inter-ests are in organizational management accounting, particularly the useof activity-based techniques, budgeting techniques, balanced scorecardsand performance management. [email protected]

Ruth Mattimoe is Lecturer in Management Accounting and FinancialStatement Analysis at DCU Business School, Dublin, Ireland. She quali-fied as a Chartered Accountant winning second place in the CAP1 examination. Her PhD at the Manchester School of Accounting andFinance on room rate pricing in the Irish hotel industry won a CIMAResearch Foundation grant. She is keenly interested in the applicationof accounting techniques to service industries, especially tourism. [email protected]

Falconer Mitchell is Professor in Management Accounting at the University of Edinburgh, UK. His research interests are in manage-ment accounting development and change, cost management and per-formance measurement. He is Chairman of CIMA’s Research Board. [email protected]

Souad Moufty is Assistant Lecturer at Damascus University, Syria, and a doctoral student in Management Accounting at Brunel University, UK. Her main research interests include balanced scorecard and per-formance management. [email protected]

Hanne Nørreklit is Professor at Aarhus University, Denmark. Her teach-ing and research area covers performance measurements, internationalmanagement control, management fashion, management rhetoric and

xxx Notes on Contributors

validity issues in management control. She has published in journals such as Accounting, Organizations and Society,yy Contemporary Accounting Research and Management Accounting Research. [email protected]

Venkateswara Pilla is Lecturer in Accounting and Finance at BrunelUniversity, UK. He is a qualified Chartered and Management Accountant. His work experience includes accounting, finance, taxation and man-agement consulting functions and systems integration. His researchinterests include accounting and sustainability. [email protected]

Raili Pollanen is Associate Professor in Accounting at Sprott Schoolof Business, Carleton University, Canada. Her research focuses on per-formance measurement, management control and accounting regula-tion, and her papers have been published in several journals, booksand proceedings. She has served on several professional committees,including a taskforce on Canadian public performance reporting. [email protected]

Robin Roslender is Professor in Accounting and Finance at theUniversity of Dundee, UK. He has made contributions to the litera-ture on accounting for people since 1992 and is currently editor of the Journal of Human Resource Costing and Accounting. [email protected]

Bill Ryan is Professor in Accounting at Hult International Business School in London. His research is in the general area of Management Control spanning Accounting and Business Strategy, and he has pub-lished papers across these areas. Before entering academic life, he held a number of senior management positions in accounting and strate-gic change management in companies such as Chrysler and the 3M Corporation, where he completed assignments in the UK, Europe andthe US. [email protected]

Stefan Schaltegger is Professor in Management and Head of the Centrerfor Sustainability Management and the MBA Sustainability Management at Leuphana University in Luneburg, Germany. His research areas includecorporate sustainability management, sustainability accounting and reporting and sustainable entrepreneurship. He is the chairman of the Steering Committee of the Environmental and Sustainability Management Accounting Network (EMAN). [email protected]

Will Seal is Professor in Accounting at the University of SouthamptonSchool of Management, UK. Before joining Southampton Management School in 2011, he has held Chairs at the Universities of Essex, Birmingham

Notes on Contributors xxxi

and Loughborough. His current research interests include accounting for hotels and hospitality, shared service organizations, supply chains and relational contracting and management accounting in local [email protected]

Mike Tayles is Emeritus Professor in Accounting and Finance at the University of Hull and a chartered management accountant. Hisresearch interests include management accounting practices, cost sys-tem design and activity-based cost management and developments instrategic management accounting including accounting for intellectual capital. Various aspects of this work have been financially supportedand subsequently published by UK accounting bodies. He has published papers in professional and international academic journals and research reports. [email protected]

Tony Tollington is Reader in Accounting at Brunel University, UK and a former chief accountant. His research interest is directed towards intan-gible assets. [email protected]

Shahzad Uddin is Professor in Accounting and the Director of Essex Accounting Centre at the University of Essex, UK. He is the co-editorof Journal of Accounting in Emerging Economies and the founding chair of the BAA SIG Accounting in Emerging Economies. He is a member of the executive committee of Professors of Accounting and [email protected]

Billy Wadongo is a doctoral student in Management Accounting at theUniversity of Bedfordshire, UK. He has published several peer-reviewed articles on performance measurement and management in internationaljournals and has co-authored a book on ‘hospitality organisationalbehaviour’. He has previously worked as a lecturer, an M&E consult-ant and a training facilitator for NGOs in Kenya and the USA. Morerecently, he worked as the Executive Director, Sustainable Development for All-Kenya (SDFA-Kenya). [email protected]

Danture Wickramasinghe is Professor in Management Accounting at Hull University Business School, UK. His publications appear in inter-national journals, including Accountability, Auditing, and Accountability Journal and Critical Perspectives on Accounting. He is the co-author of ggManagement Accounting Change: Approaches and Perspectives and Handbookof Accounting and Development. [email protected]

Dimitar Zvezdov is Research Assistant at the Centre for SustainabilityManagement at the Leuphana University in Luneburg, Germany. His

xxxii Notes on Contributors

core research area is corporate sustainability accounting. Between 2008 and 2010, he was engaged in the research project ‘Accounting infor-mation and the accounting function in sustainability management’,funded by the Institute of Chartered Accountants in England and Wales. [email protected]