revenue, financial instruments and ifrs convergence - isca · revenue, financial instruments and...

TRANSCRIPT

Revenue, Financial Instruments and IFRS Convergence

Are you Ready for 2018 ?

Reinhard Klemmer

Chairman of ISCA Revenue Working Group, Partner & Technical Head, KPMG

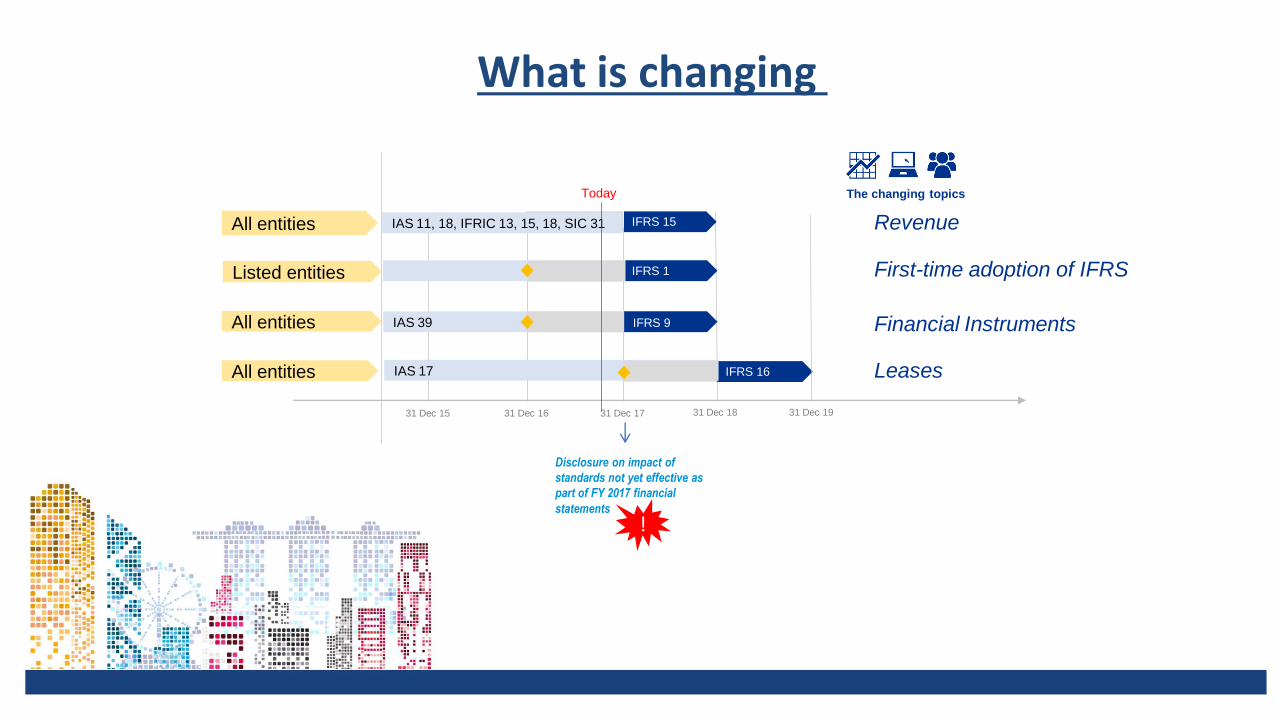

What is changing and where we are

Overview of the changes and timeline

Where we are – Survey Results

Root causes and the way forward

ISCA Guidance on Transition to IFRS

Revenue – ISCA Guidance on specific Real Estate issues

Financial Instruments

The changing topics

31 Dec 17 31 Dec 18 31 Dec 19

IFRS 16

31 Dec 15 31 Dec 16

First-time adoption of IFRS

Revenue

Financial Instruments

Leases

IFRS 15

IFRS 1

IAS 39 IFRS 9

IAS 17

Today

Disclosure on impact of

standards not yet effective as

part of FY 2017 financial

statements

!

IAS 11, 18, IFRIC 13, 15, 18, SIC 31

All entities

All entities

Listed entities

All entities

What is changing

IFRS 15 comparatives

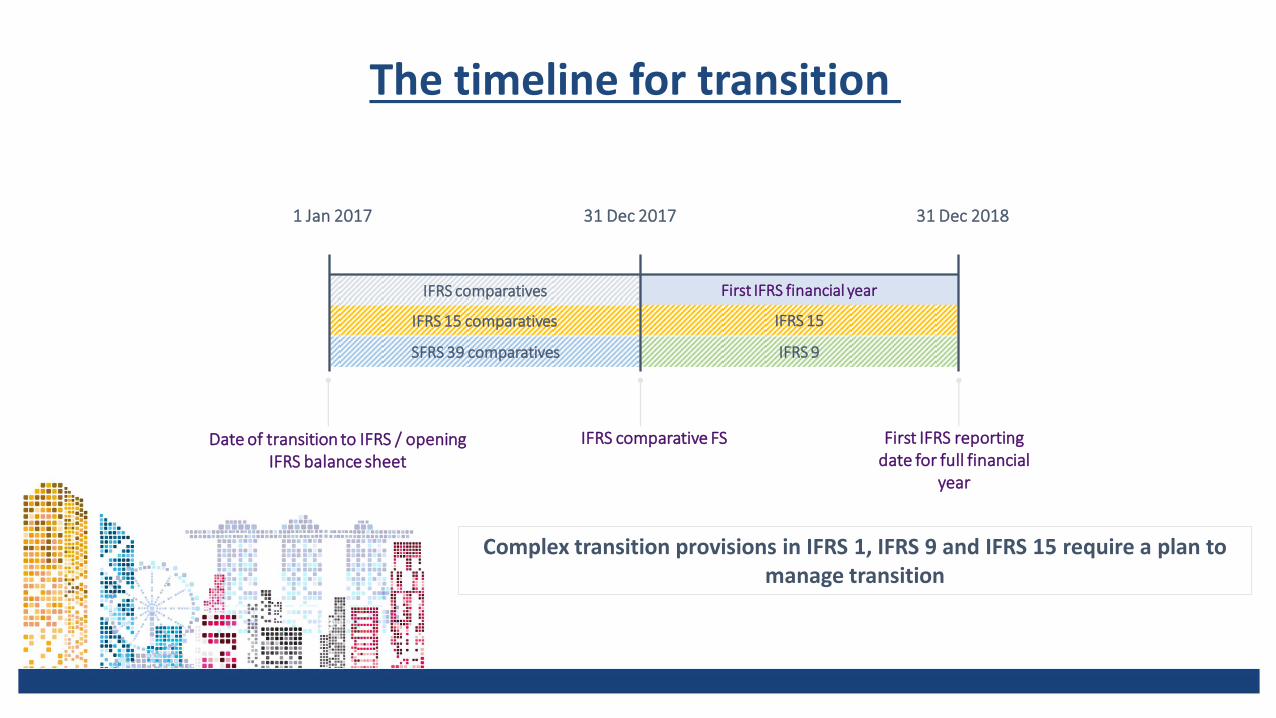

Complex transition provisions in IFRS 1, IFRS 9 and IFRS 15 require a plan to manage transition

IFRS comparatives First IFRS financial year

First IFRS reporting date for full financial

year

IFRS comparative FS

1 Jan 2017 31 Dec 2017 31 Dec 2018

Date of transition to IFRS / opening IFRS balance sheet

IFRS 15

SFRS 39 comparatives IFRS 9

The timeline for transition

IFRS 15 comparatives

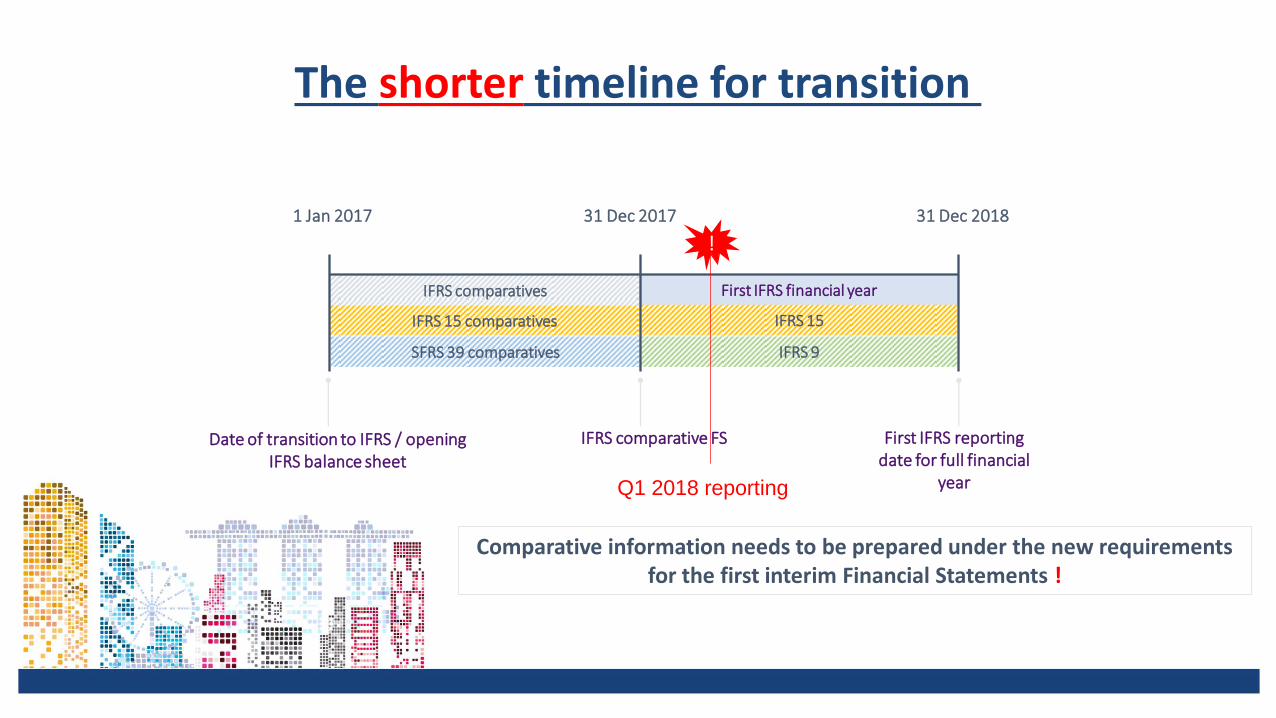

Comparative information needs to be prepared under the new requirements for the first interim Financial Statements !

IFRS comparatives First IFRS financial year

First IFRS reporting date for full financial

year

IFRS comparative FS

1 Jan 2017 31 Dec 2017 31 Dec 2018

Date of transition to IFRS / opening IFRS balance sheet

IFRS 15

SFRS 39 comparatives IFRS 9

The shorter timeline for transition

!

Q1 2018 reporting

Where we are – Survey Results

ISCA conducted a poll for listed companies on their preparedness for the coming change in the accounting framework from Singapore Financial Reporting Standards (SFRS) to the equivalent IFRS framework. For 235 listed companies the results are presented. For the survey the external auditors of the listed companies were asked for their assessment on their clients status of preparedness.

Survey Results – The Questions

The 7 questions were focusing on various stages of preparedness starting with awareness and ending with completion of the process and being ready to comply with IFRS:

Q1: Has work started or is interest being expressed in preparing?

Q2: Are the requirements understood, has knowledge been gained?

Q3: Has an implementation plan been drafted leading to the first publication of IFRS results (interim or

annual results)?

Q4: Has execution of the plan commenced with resources allocated?

Q5: Is the impact assessment substantially complete?

Q6: Is the quantification of the impact substantially complete?

Q7: Is the company ready to go – is the entire conversion plan substantially complete?

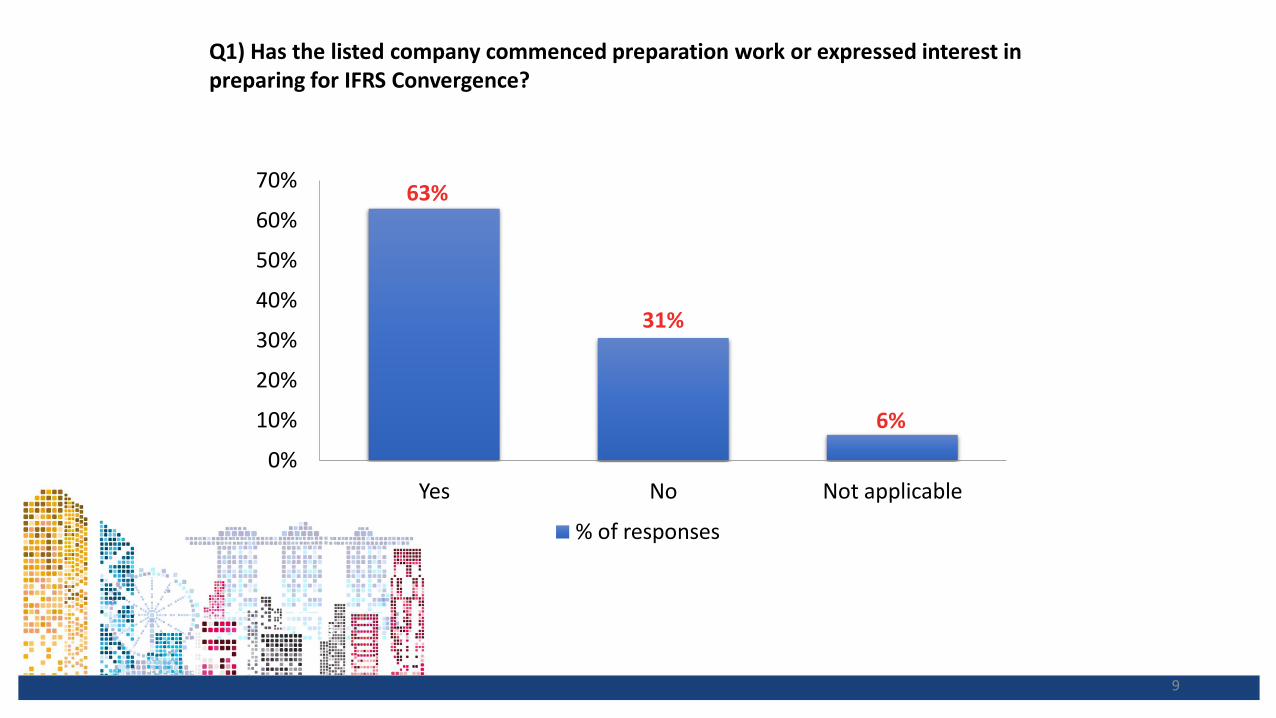

9

63%

31%

6%

Yes No Not applicable

0%

10%

20%

30%

40%

50%

60%

70%

% of responses

Q1) Has the listed company commenced preparation work or expressed interest in preparing for IFRS Convergence?

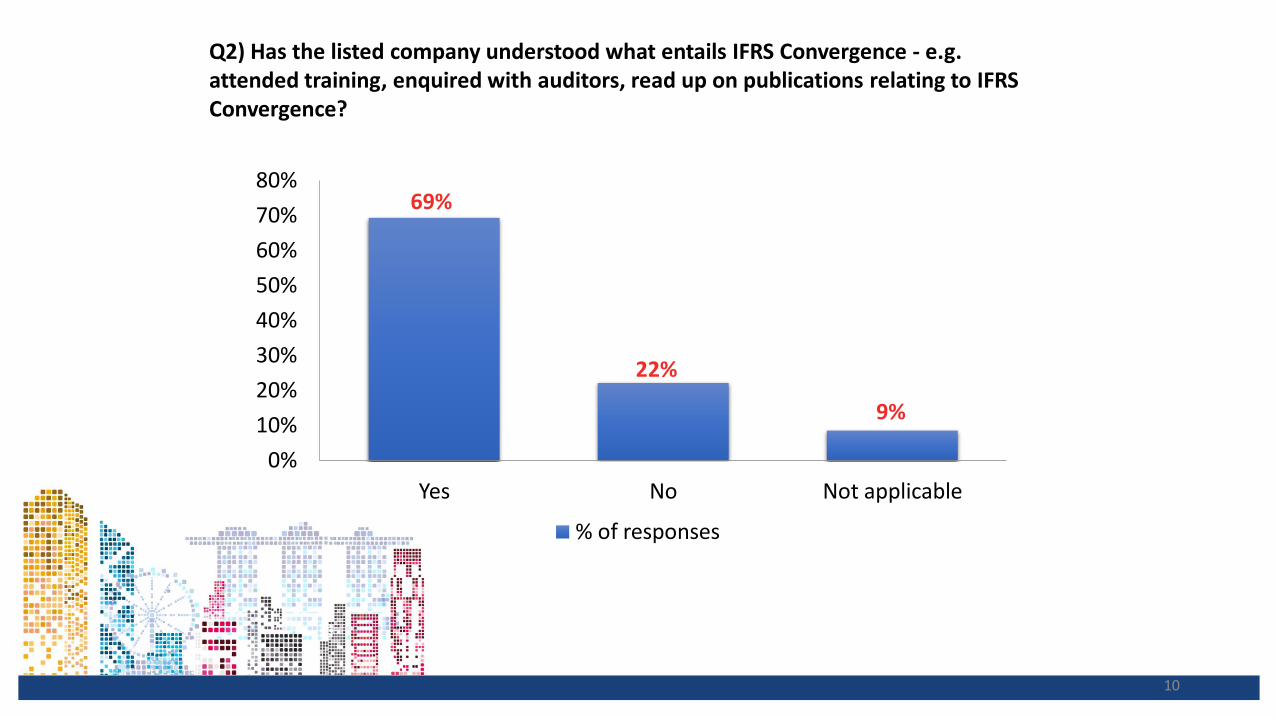

10

69%

22%

9%

Yes No Not applicable

0%

10%

20%

30%

40%

50%

60%

70%

80%

% of responses

Q2) Has the listed company understood what entails IFRS Convergence - e.g. attended training, enquired with auditors, read up on publications relating to IFRS Convergence?

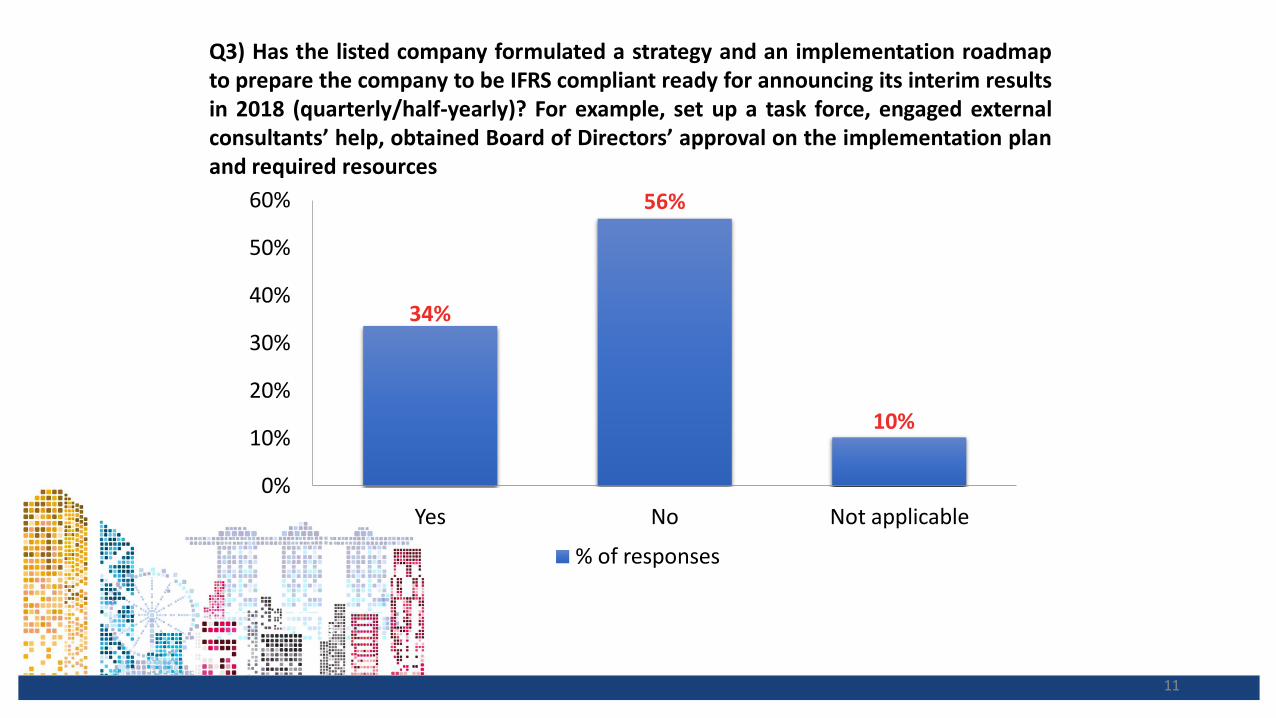

11

34%

56%

10%

Yes No Not applicable

0%

10%

20%

30%

40%

50%

60%

% of responses

Q3) Has the listed company formulated a strategy and an implementation roadmap to prepare the company to be IFRS compliant ready for announcing its interim results in 2018 (quarterly/half-yearly)? For example, set up a task force, engaged external consultants’ help, obtained Board of Directors’ approval on the implementation plan and required resources

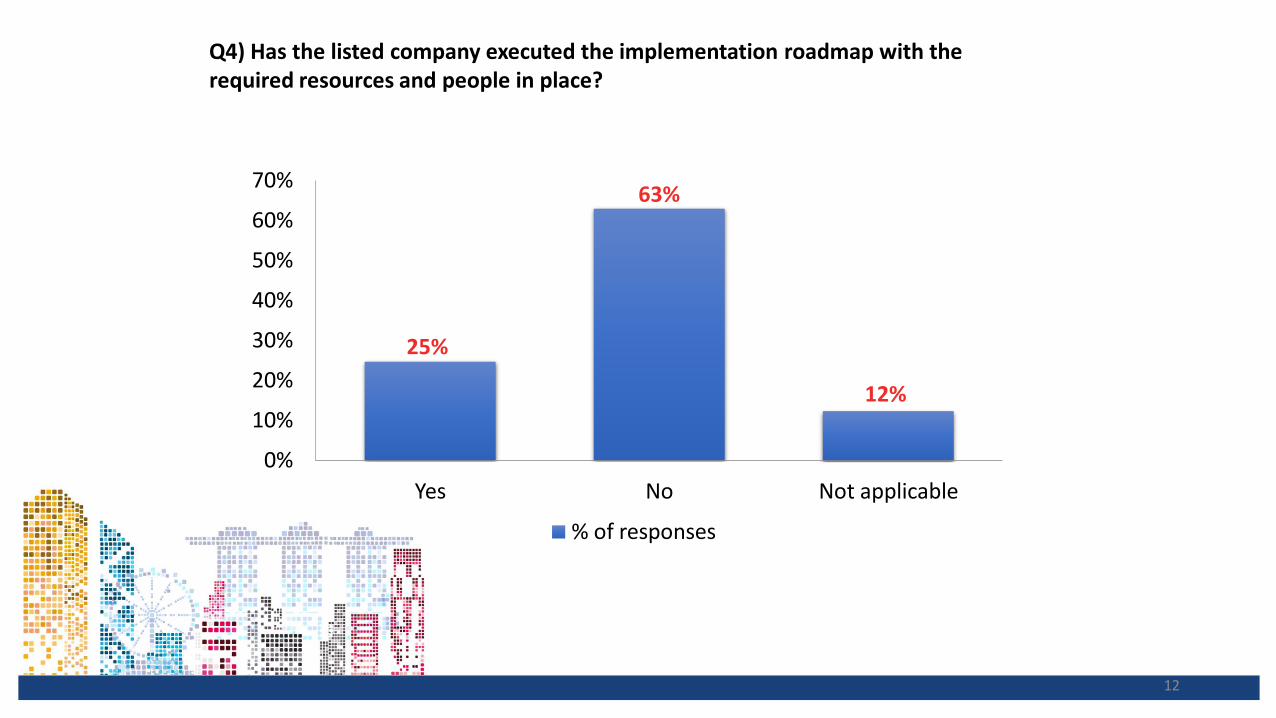

12

25%

63%

12%

Yes No Not applicable

0%

10%

20%

30%

40%

50%

60%

70%

% of responses

Q4) Has the listed company executed the implementation roadmap with the required resources and people in place?

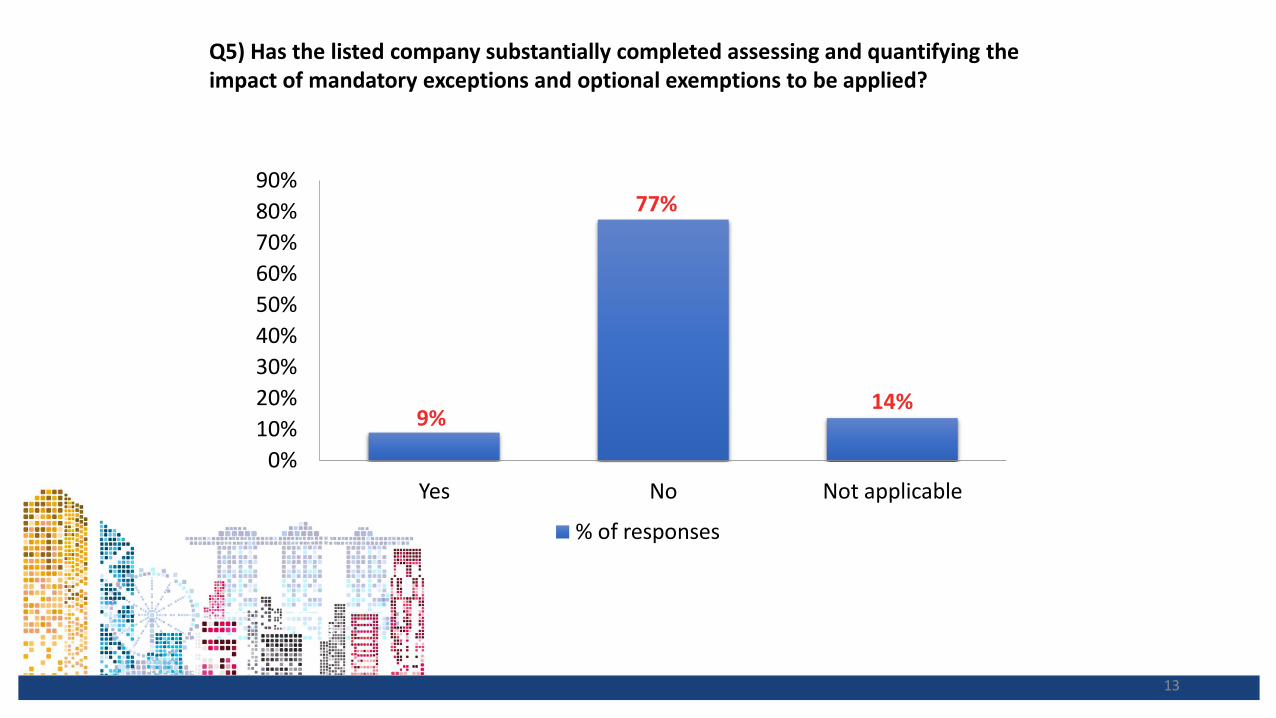

13

9%

77%

14%

Yes No Not applicable

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

% of responses

Q5) Has the listed company substantially completed assessing and quantifying the impact of mandatory exceptions and optional exemptions to be applied?

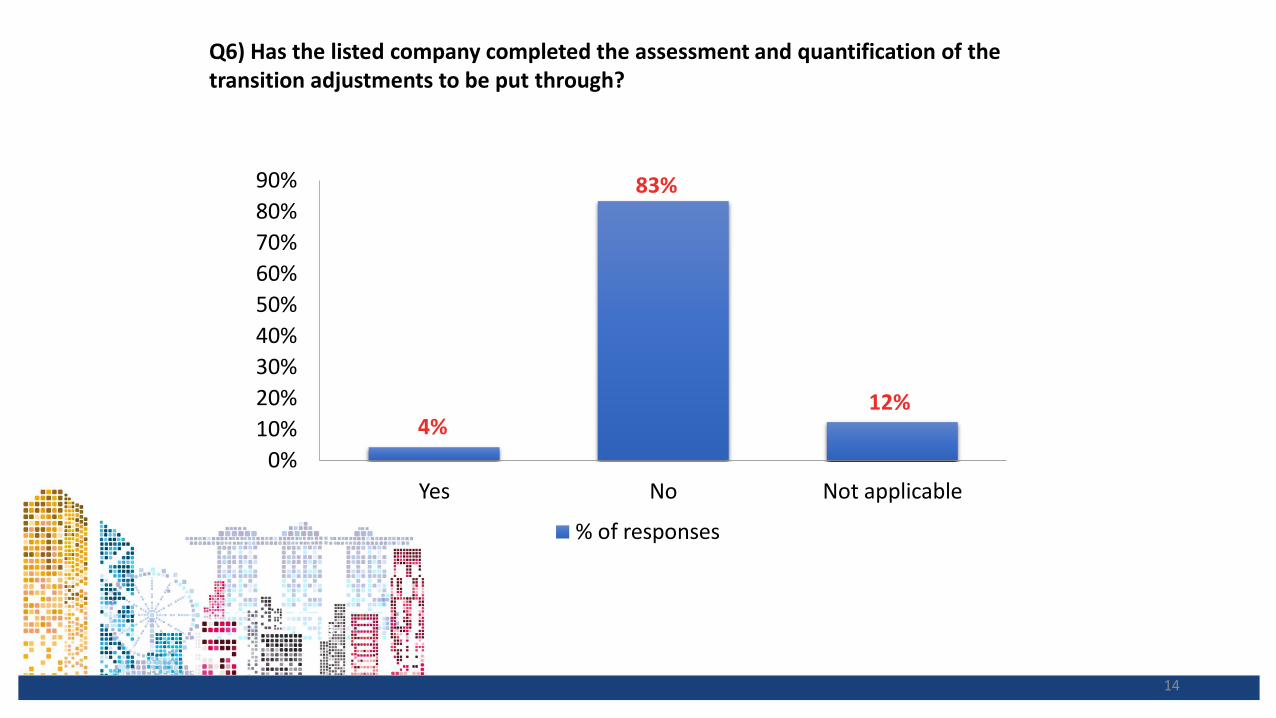

14

4%

83%

12%

Yes No Not applicable

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

% of responses

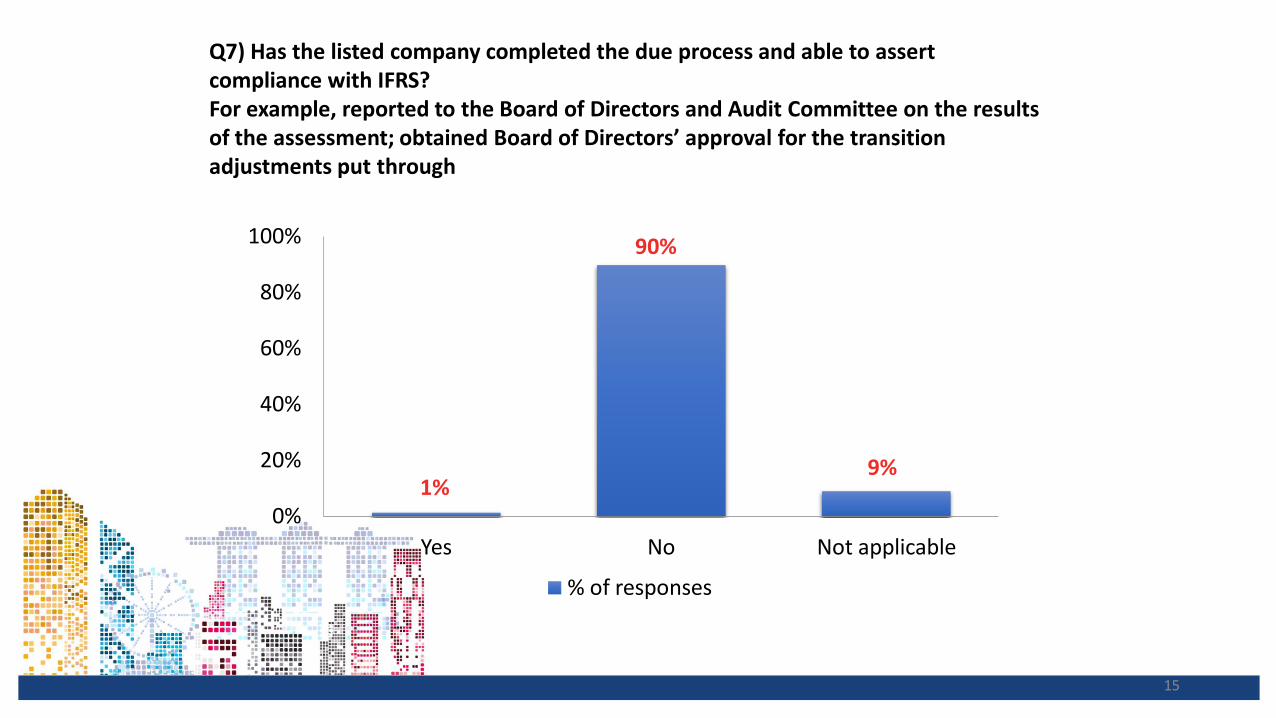

Q6) Has the listed company completed the assessment and quantification of the transition adjustments to be put through?

15

1%

90%

9%

Yes No Not applicable

0%

20%

40%

60%

80%

100%

% of responses

Q7) Has the listed company completed the due process and able to assert compliance with IFRS? For example, reported to the Board of Directors and Audit Committee on the results of the assessment; obtained Board of Directors’ approval for the transition adjustments put through

16

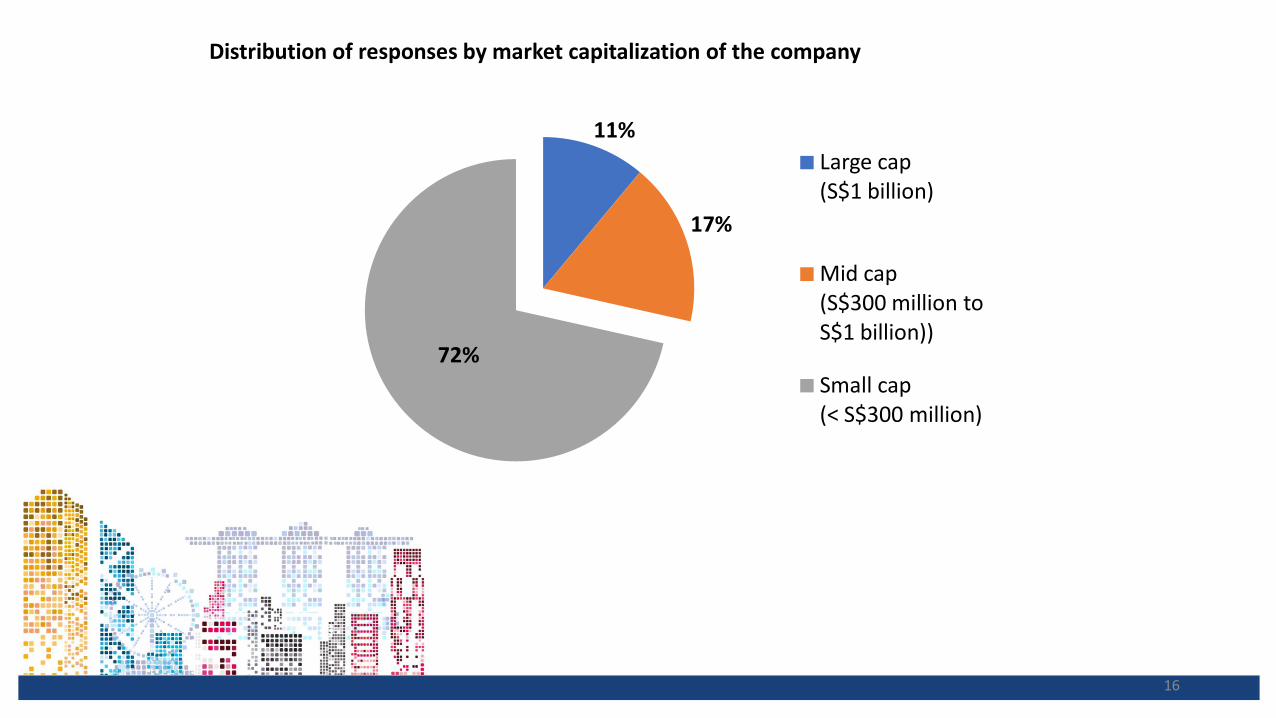

11%

17%

72%

Large cap (S$1 billion)

Mid cap (S$300 million to S$1 billion))

Small cap (< S$300 million)

Distribution of responses by market capitalization of the company

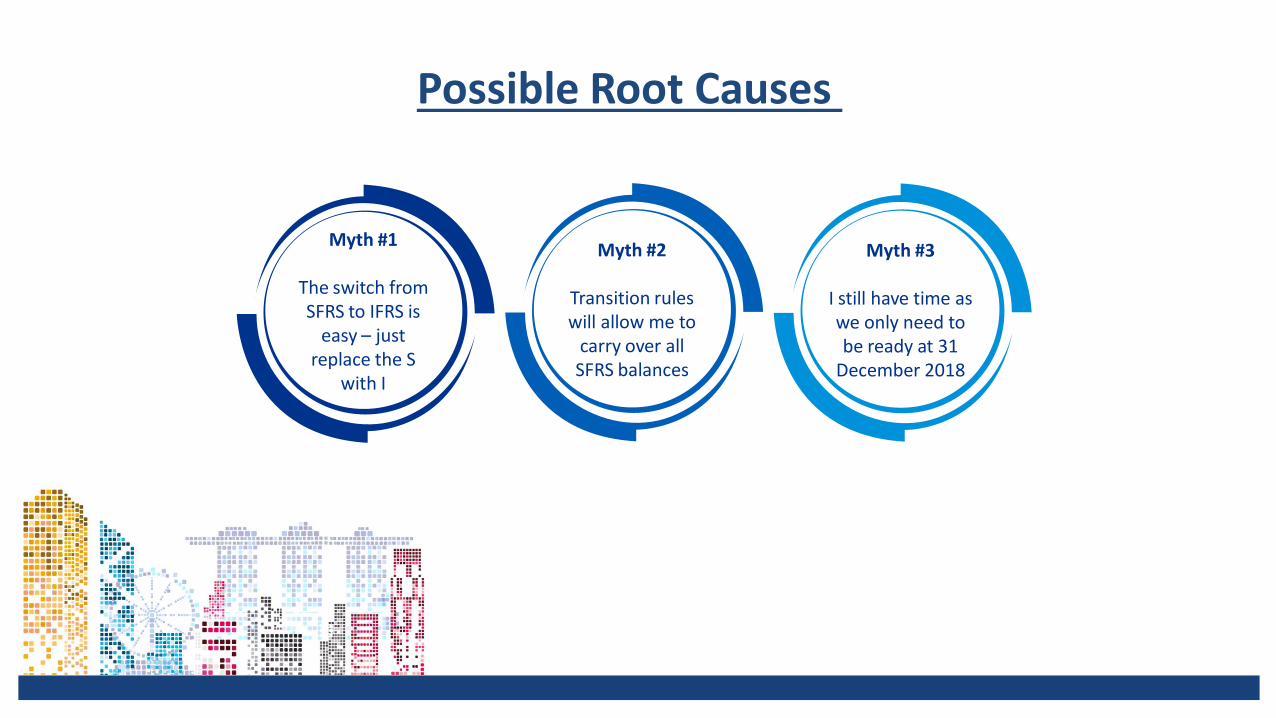

Myth #1

The switch from SFRS to IFRS is

easy – just replace the S

with I

Myth #2

Transition rules will allow me to

carry over all SFRS balances

Myth #3

I still have time as we only need to be ready at 31

December 2018

Possible Root Causes

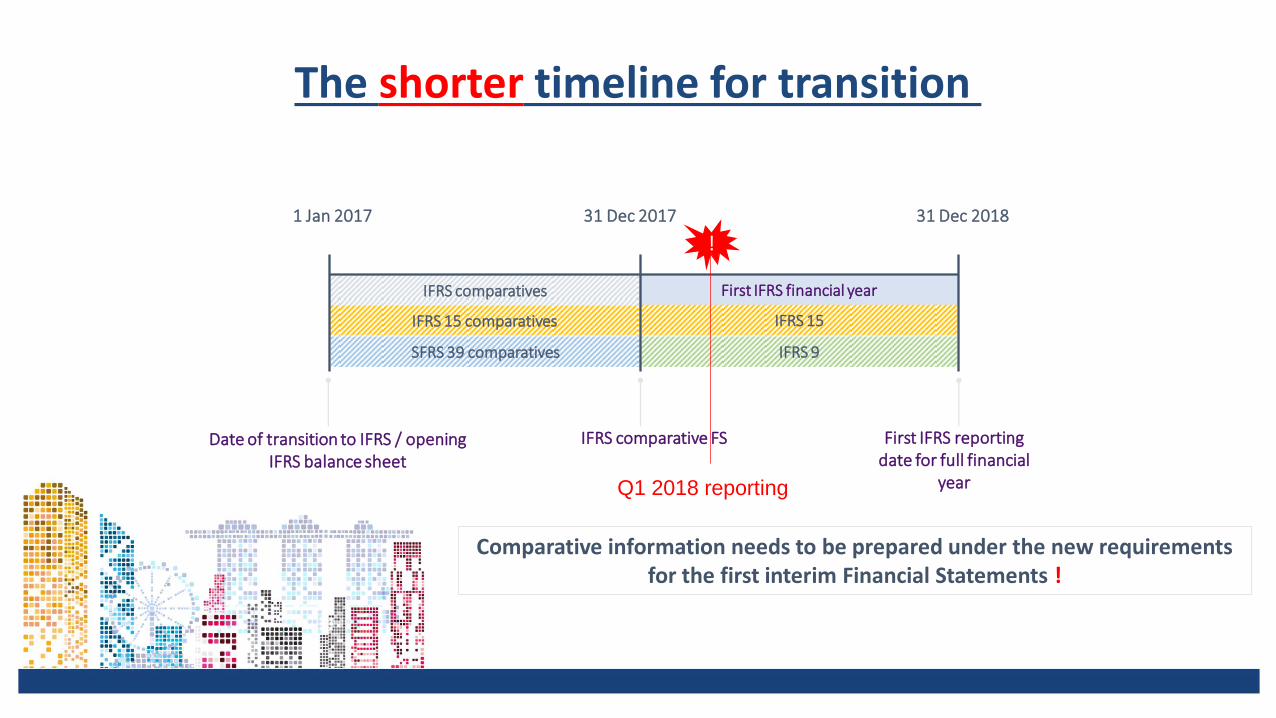

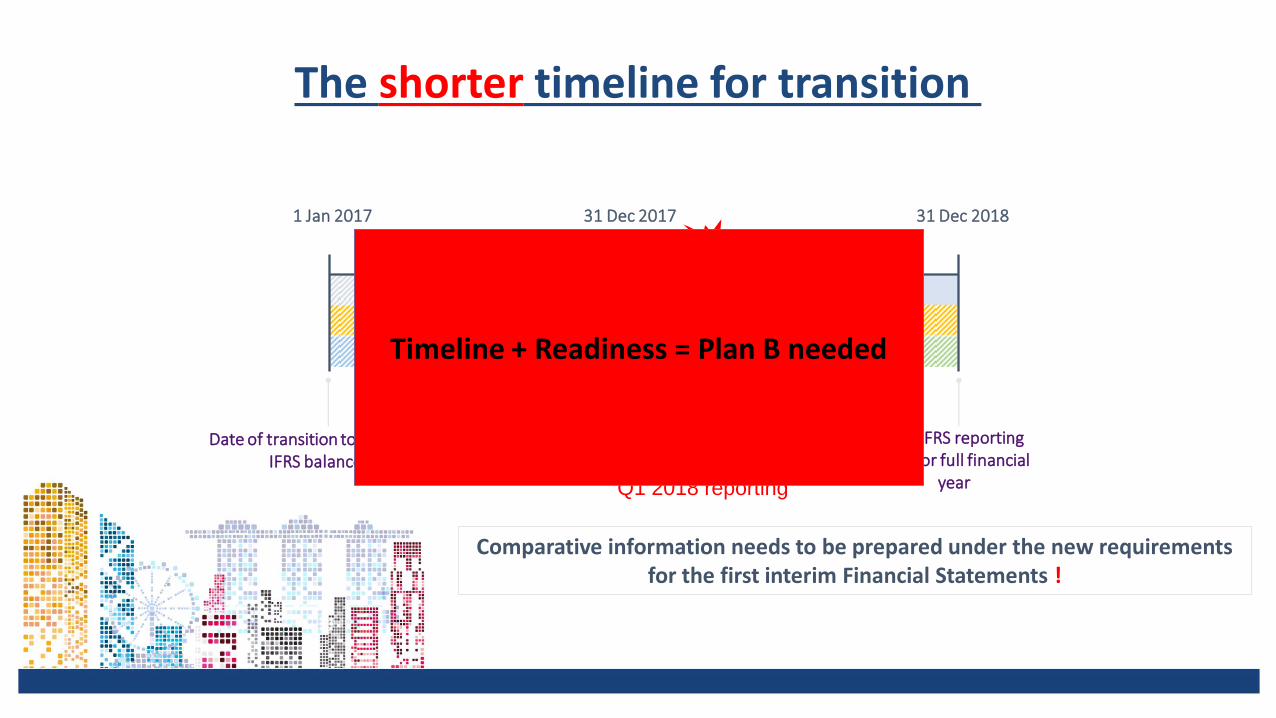

IFRS 15 comparatives

Comparative information needs to be prepared under the new requirements for the first interim Financial Statements !

IFRS comparatives First IFRS financial year

First IFRS reporting date for full financial

year

IFRS comparative FS

1 Jan 2017 31 Dec 2017 31 Dec 2018

Date of transition to IFRS / opening IFRS balance sheet

IFRS 15

SFRS 39 comparatives IFRS 9

The shorter timeline for transition

!

Q1 2018 reporting

IFRS 15 comparatives

Comparative information needs to be prepared under the new requirements for the first interim Financial Statements !

IFRS comparatives First IFRS financial year

First IFRS reporting date for full financial

year

IFRS comparative FS

1 Jan 2017 31 Dec 2017 31 Dec 2018

Date of transition to IFRS / opening IFRS balance sheet

IFRS 15

SFRS 39 comparatives IFRS 9

The shorter timeline for transition

!

Q1 2018 reporting

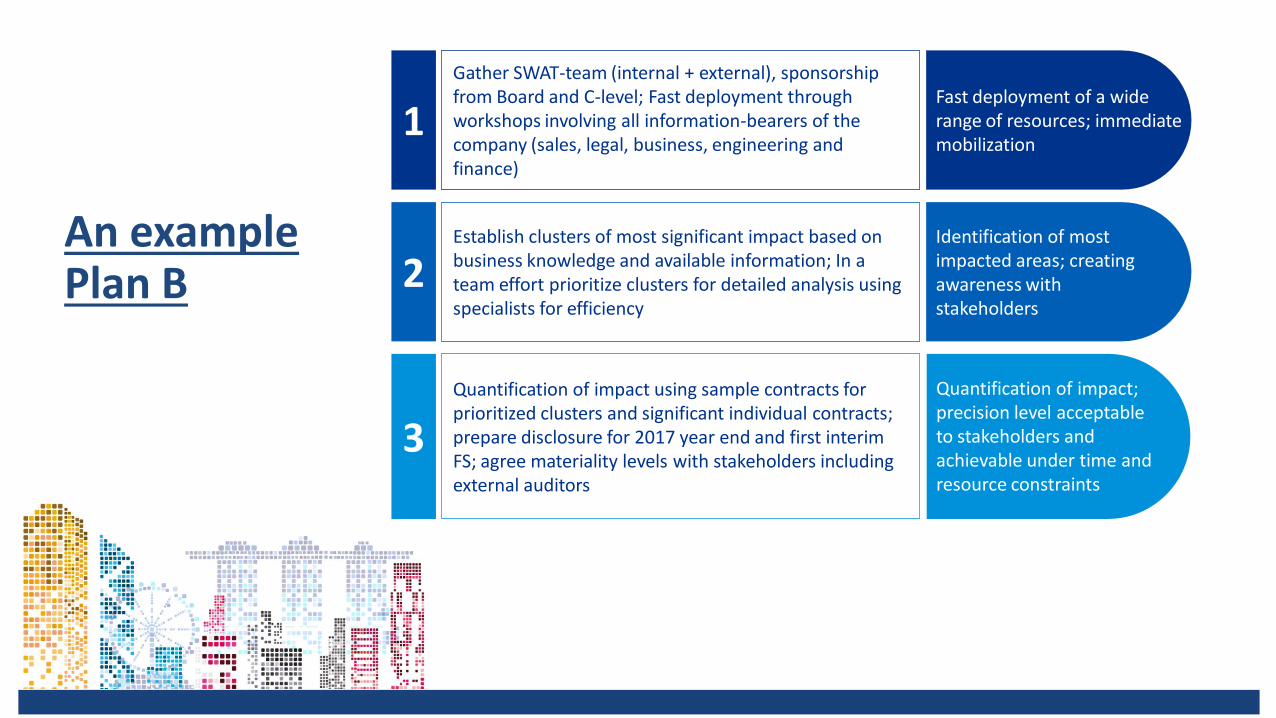

Timeline + Readiness = Plan B needed

1

2

3

Gather SWAT-team (internal + external), sponsorship from Board and C-level; Fast deployment through workshops involving all information-bearers of the company (sales, legal, business, engineering and finance)

Establish clusters of most significant impact based on business knowledge and available information; In a team effort prioritize clusters for detailed analysis using specialists for efficiency

Quantification of impact using sample contracts for prioritized clusters and significant individual contracts; prepare disclosure for 2017 year end and first interim FS; agree materiality levels with stakeholders including external auditors

Fast deployment of a wide range of resources; immediate mobilization

Identification of most impacted areas; creating awareness with stakeholders

Quantification of impact; precision level acceptable to stakeholders and achievable under time and resource constraints

An example Plan B

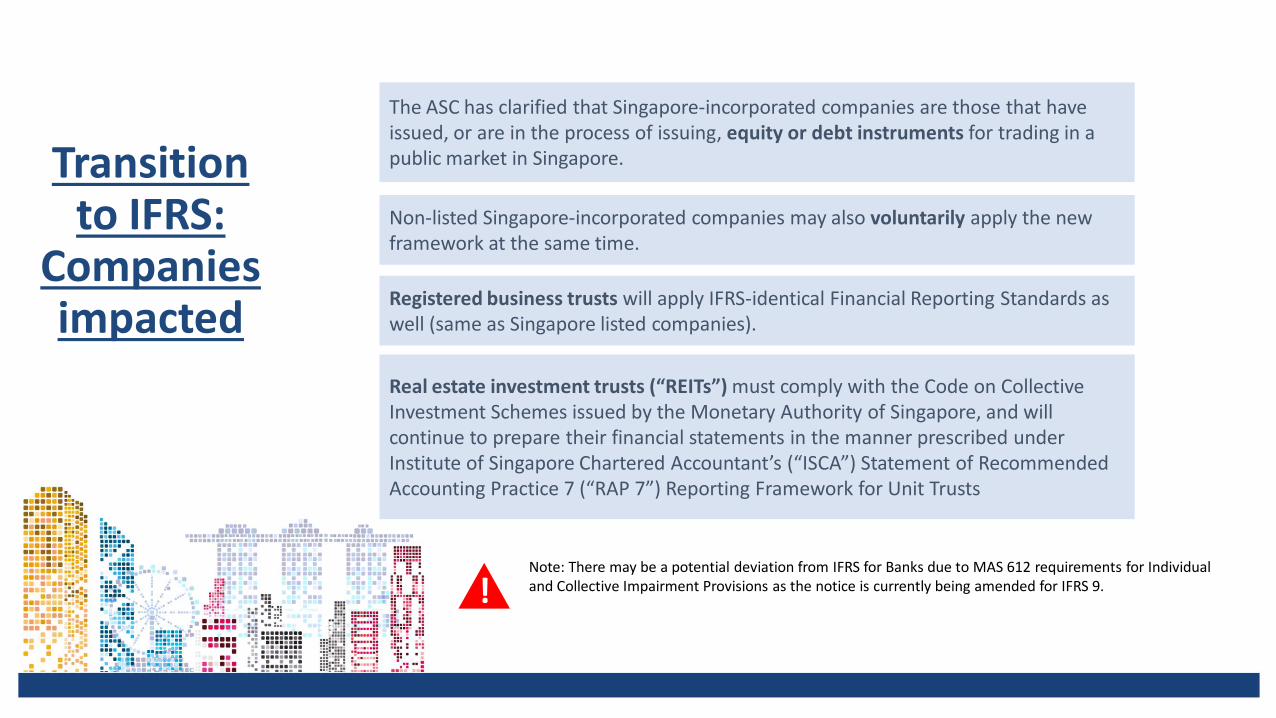

Real estate investment trusts (“REITs”) must comply with the Code on Collective Investment Schemes issued by the Monetary Authority of Singapore, and will continue to prepare their financial statements in the manner prescribed under Institute of Singapore Chartered Accountant’s (“ISCA”) Statement of Recommended Accounting Practice 7 (“RAP 7”) Reporting Framework for Unit Trusts

Registered business trusts will apply IFRS-identical Financial Reporting Standards as well (same as Singapore listed companies).

Non-listed Singapore-incorporated companies may also voluntarily apply the new framework at the same time.

The ASC has clarified that Singapore-incorporated companies are those that have issued, or are in the process of issuing, equity or debt instruments for trading in a public market in Singapore.

Note: There may be a potential deviation from IFRS for Banks due to MAS 612 requirements for Individual and Collective Impairment Provisions as the notice is currently being amended for IFRS 9. !

Transition to IFRS:

Companies impacted

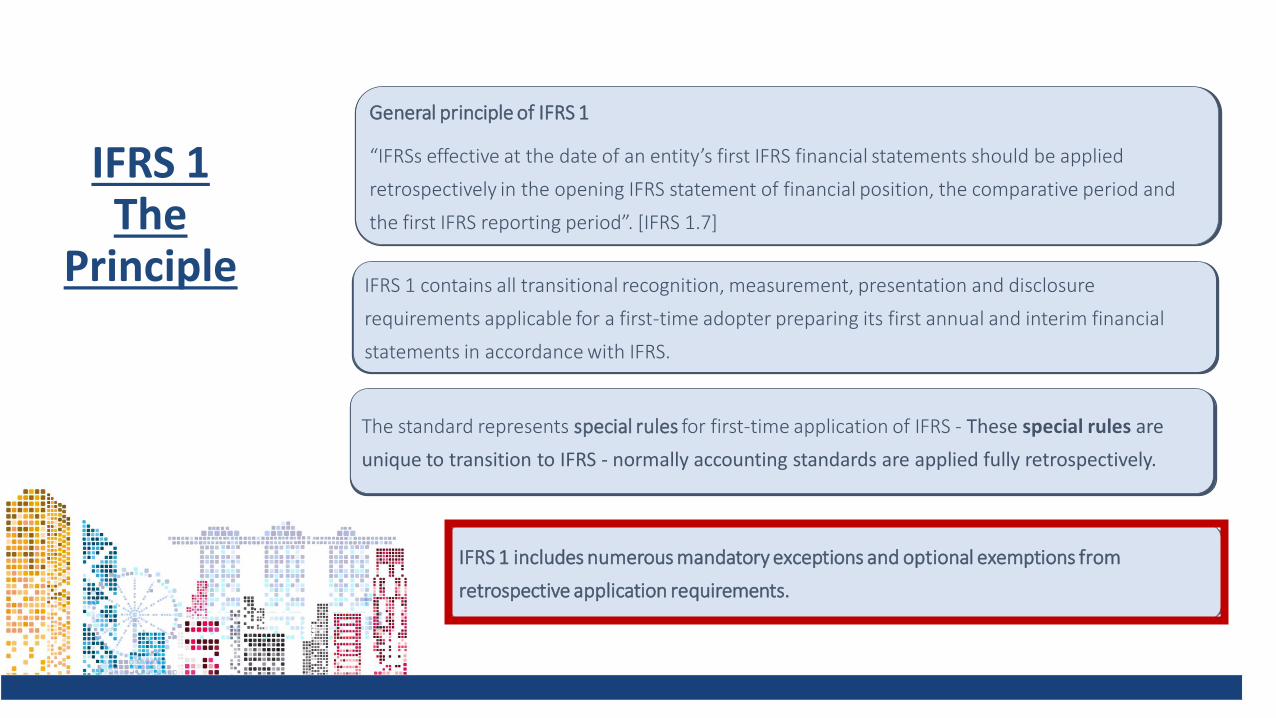

IFRS 1 contains all transitional recognition, measurement, presentation and disclosure

requirements applicable for a first-time adopter preparing its first annual and interim financial

statements in accordance with IFRS.

The standard represents special rules for first-time application of IFRS - These special rules are

unique to transition to IFRS - normally accounting standards are applied fully retrospectively.

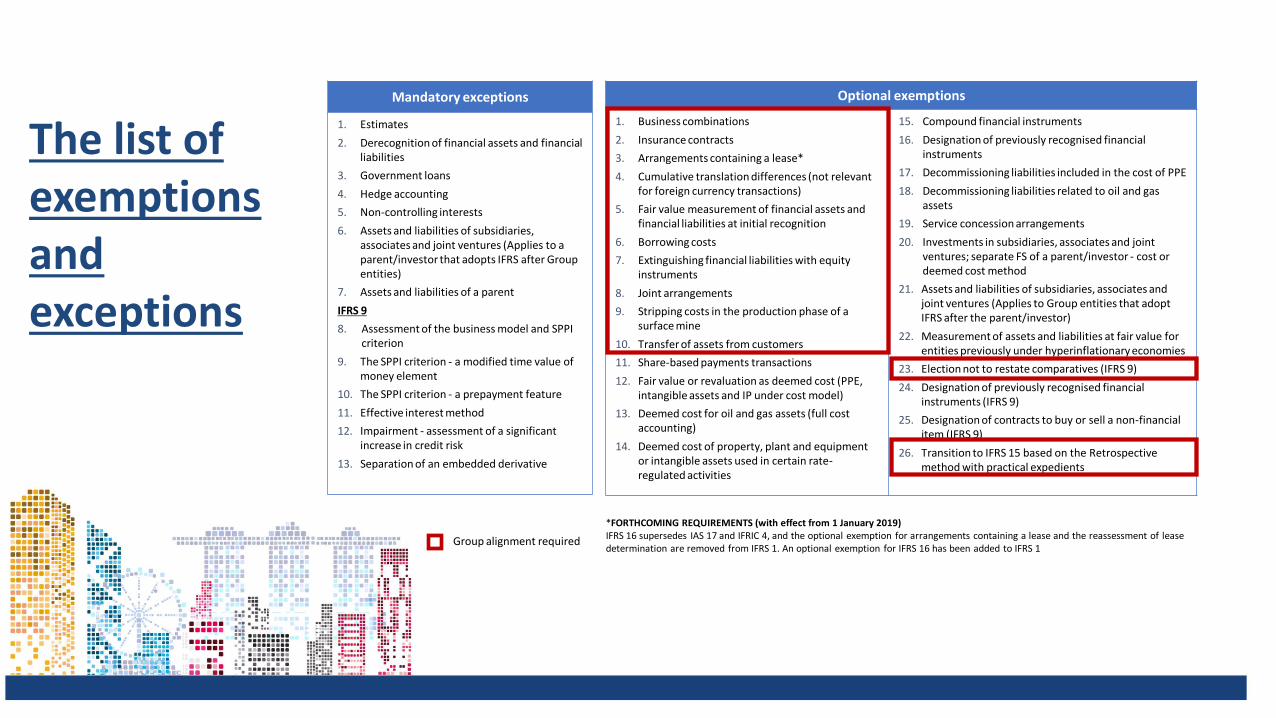

IFRS 1 includes numerous mandatory exceptions and optional exemptions from

retrospective application requirements.

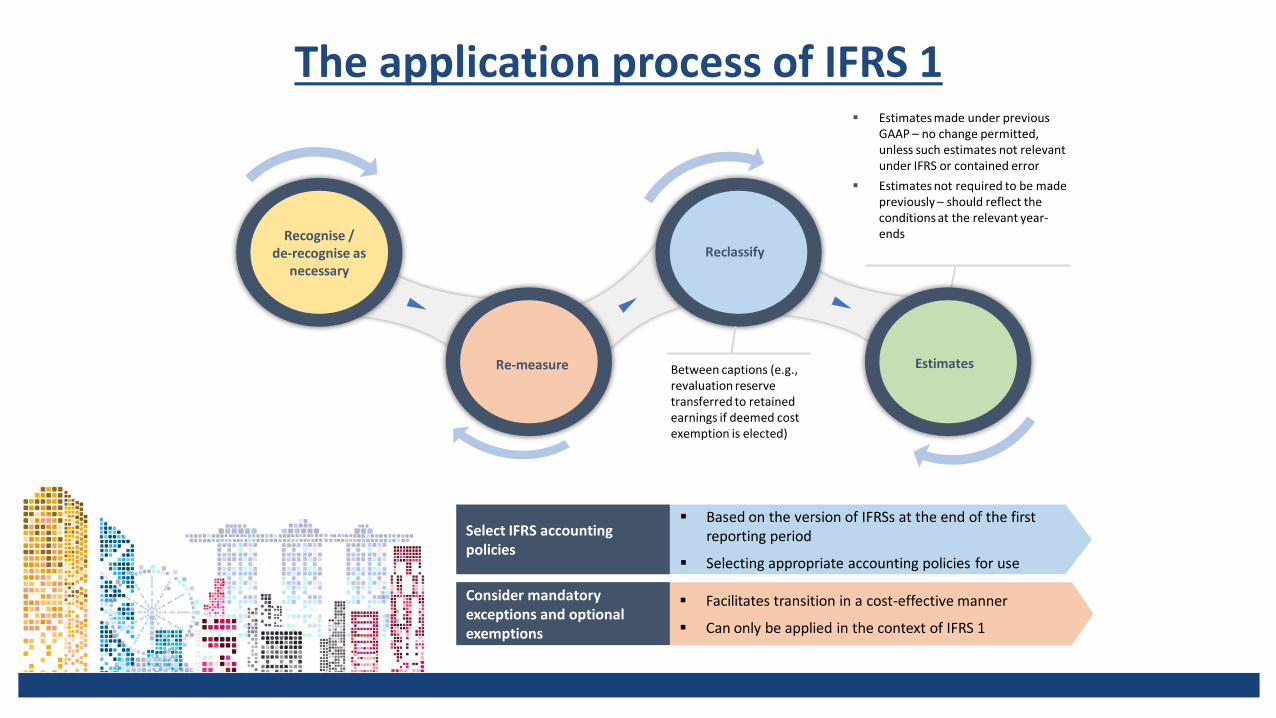

General principle of IFRS 1

“IFRSs effective at the date of an entity’s first IFRS financial statements should be applied

retrospectively in the opening IFRS statement of financial position, the comparative period and

the first IFRS reporting period”. [IFRS 1.7]

IFRS 1 The

Principle

Recognise / de-recognise as

necessary

Re-measure

Reclassify

Estimates

Estimates made under previous GAAP – no change permitted, unless such estimates not relevant under IFRS or contained error

Estimates not required to be made previously – should reflect the conditions at the relevant year-ends

Between captions (e.g., revaluation reserve transferred to retained earnings if deemed cost exemption is elected)

Based on the version of IFRSs at the end of the first reporting period

Selecting appropriate accounting policies for use

Facilitates transition in a cost-effective manner

Can only be applied in the context of IFRS 1

Select IFRS accounting policies

Consider mandatory exceptions and optional exemptions

The application process of IFRS 1

The list of exemptions and exceptions

Mandatory exceptions

1. Estimates

2. Derecognition of financial assets and financial liabilities

3. Government loans

4. Hedge accounting

5. Non-controlling interests

6. Assets and liabilities of subsidiaries, associates and joint ventures (Applies to a parent/investor that adopts IFRS after Group entities)

7. Assets and liabilities of a parent

IFRS 9

8. Assessment of the business model and SPPI criterion

9. The SPPI criterion - a modified time value of money element

10. The SPPI criterion - a prepayment feature

11. Effective interest method

12. Impairment - assessment of a significant increase in credit risk

13. Separation of an embedded derivative

Optional exemptions

1. Business combinations

2. Insurance contracts

3. Arrangements containing a lease*

4. Cumulative translation differences (not relevant for foreign currency transactions)

5. Fair value measurement of financial assets and financial liabilities at initial recognition

6. Borrowing costs

7. Extinguishing financial liabilities with equity instruments

8. Joint arrangements

9. Stripping costs in the production phase of a surface mine

10. Transfer of assets from customers

11. Share-based payments transactions

12. Fair value or revaluation as deemed cost (PPE, intangible assets and IP under cost model)

13. Deemed cost for oil and gas assets (full cost accounting)

14. Deemed cost of property, plant and equipment or intangible assets used in certain rate-regulated activities

15. Compound financial instruments

16. Designation of previously recognised financial instruments

17. Decommissioning liabilities included in the cost of PPE

18. Decommissioning liabilities related to oil and gas assets

19. Service concession arrangements

20. Investments in subsidiaries, associates and joint ventures; separate FS of a parent/investor - cost or deemed cost method

21. Assets and liabilities of subsidiaries, associates and joint ventures (Applies to Group entities that adopt IFRS after the parent/investor)

22. Measurement of assets and liabilities at fair value for entities previously under hyperinflationary economies

23. Election not to restate comparatives (IFRS 9)

24. Designation of previously recognised financial instruments (IFRS 9)

25. Designation of contracts to buy or sell a non-financial item (IFRS 9)

26. Transition to IFRS 15 based on the Retrospective method with practical expedients

*FORTHCOMING REQUIREMENTS (with effect from 1 January 2019) IFRS 16 supersedes IAS 17 and IFRIC 4, and the optional exemption for arrangements containing a lease and the reassessment of lease determination are removed from IFRS 1. An optional exemption for IFRS 16 has been added to IFRS 1

Group alignment required

Preserve SFRS accounting and achieve minimal-impact transition

Optimize transition by evaluating transition options

The key decision

The ISCA “IFRS Convergence 2018 Implementation Roadmap”

ISCA published a Guide to help with the Convergence to IFRS. Some parts are focused on Directors and Management as readers, but all the details necessary to prepare for Convergence are also provided to help companies in their switch to IFRS.

Director oversight of IFRS Conversion Management Actions to implement IFRS Bird’s eye view of IFRS Convergence Step-by-Step Application Guide of SG-IFRS 1 Transitional Provisions in SG-IFRS 1 Various Appendices

ISCA Guidance on “Revenue Recognition for Sale of

Uncompleted Residential Properties in Singapore”

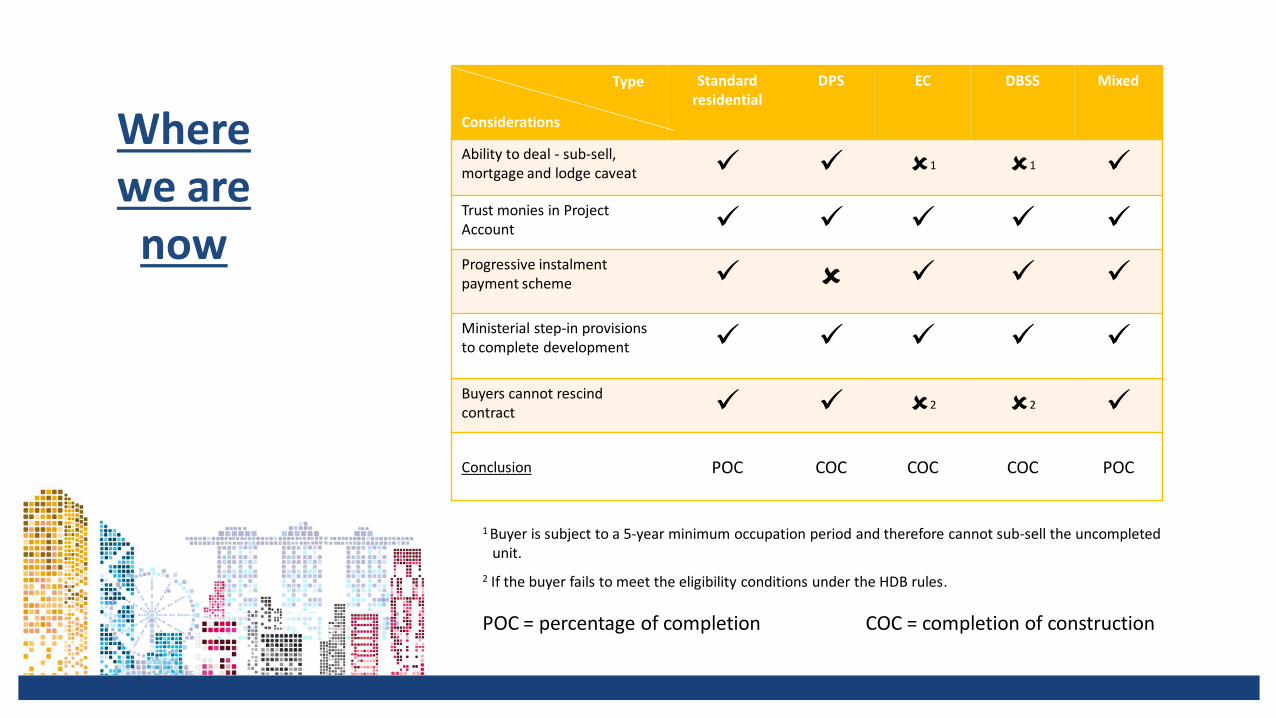

Where we are

now

Considerations

Standard residential

DPS EC DBSS Mixed

Ability to deal - sub-sell, mortgage and lodge caveat 1 1

Trust monies in Project Account Progressive instalment payment scheme

Ministerial step-in provisions to complete development

Buyers cannot rescind contract 2 2

Conclusion POC COC COC COC POC

Type

1 Buyer is subject to a 5-year minimum occupation period and therefore cannot sub-sell the uncompleted unit.

2 If the buyer fails to meet the eligibility conditions under the HDB rules.

POC = percentage of completion COC = completion of construction

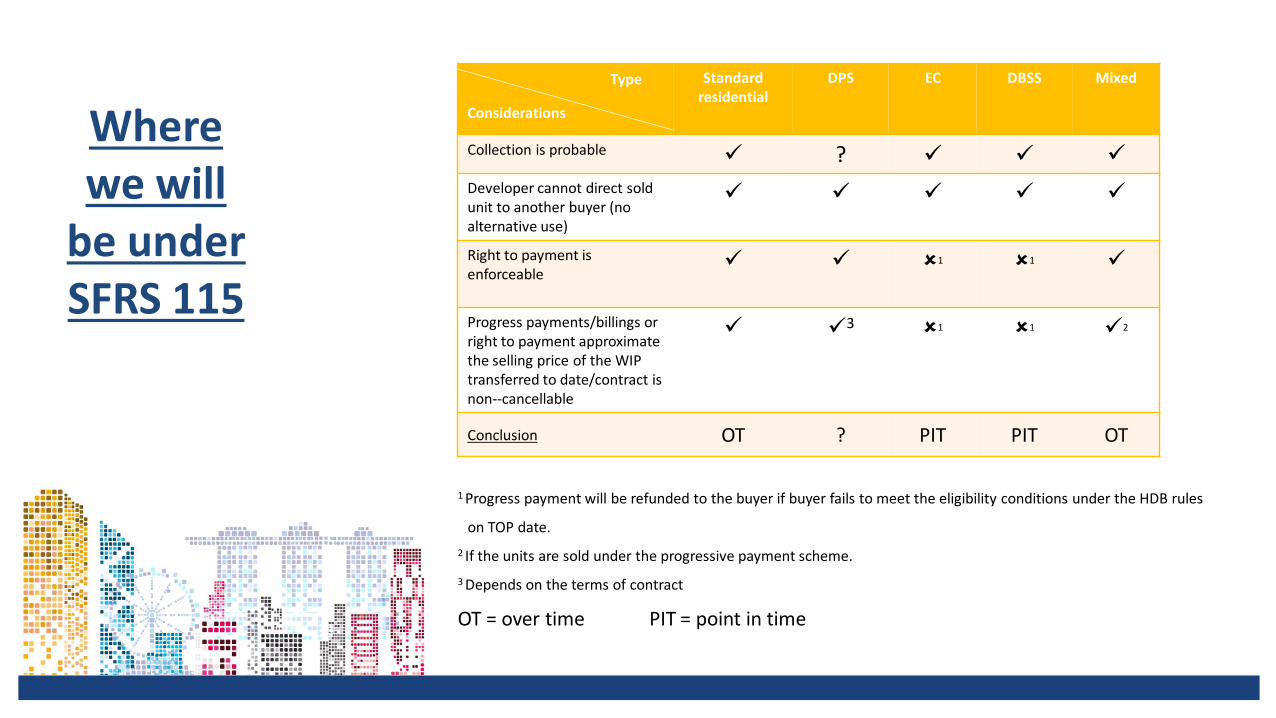

Where we will

be under SFRS 115

Type Type

Considerations

Standard residential

DPS EC DBSS Mixed

Collection is probable ?

Developer cannot direct sold unit to another buyer (no alternative use)

Right to payment is enforceable

1 1

Progress payments/billings or right to payment approximate the selling price of the WIP transferred to date/contract is non--cancellable

3

1 1 2

Conclusion OT ? PIT PIT OT

Type

1 Progress payment will be refunded to the buyer if buyer fails to meet the eligibility conditions under the HDB rules

on TOP date.

2 If the units are sold under the progressive payment scheme.

3 Depends on the terms of contract

OT = over time PIT = point in time

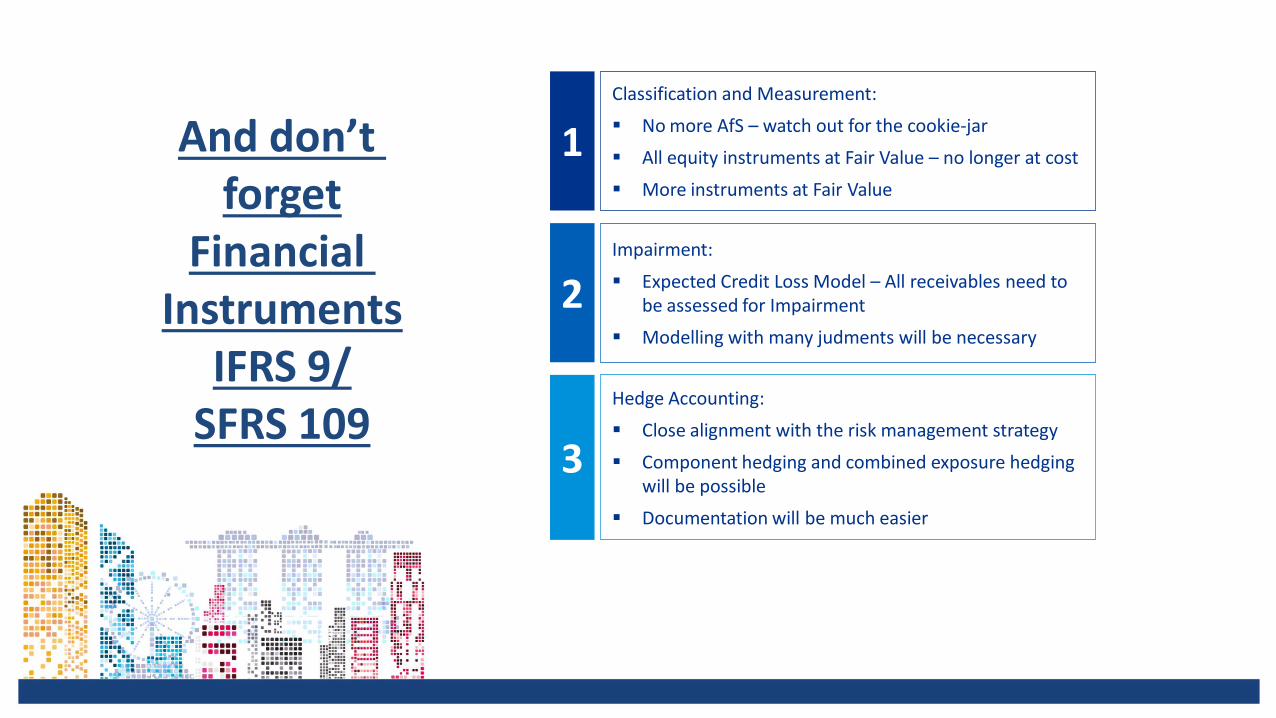

And don’t forget

Financial Instruments

IFRS 9/ SFRS 109

1

2

3

Classification and Measurement:

No more AfS – watch out for the cookie-jar

All equity instruments at Fair Value – no longer at cost

More instruments at Fair Value

Impairment:

Expected Credit Loss Model – All receivables need to be assessed for Impairment

Modelling with many judments will be necessary

Hedge Accounting:

Close alignment with the risk management strategy

Component hedging and combined exposure hedging will be possible

Documentation will be much easier

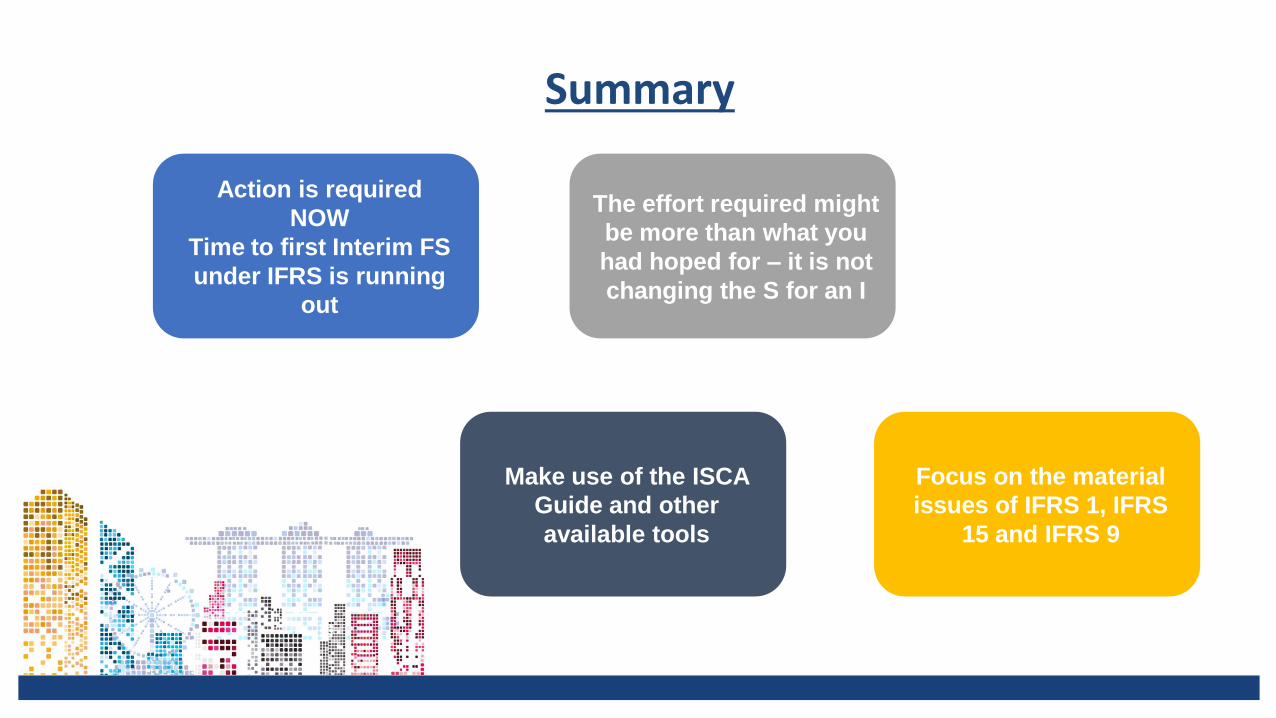

Summary

Focus on the material

issues of IFRS 1, IFRS

15 and IFRS 9

The effort required might

be more than what you

had hoped for – it is not

changing the S for an I

Action is required

NOW

Time to first Interim FS

under IFRS is running

out

Make use of the ISCA

Guide and other

available tools

Important disclaimer This Presentation (the Presentation) has been prepared by ISCA for the exclusive use of the recipients to whom it is addressed. Each recipient agrees that it will not permit any third party to, copy, reproduce or distribute to others this Presentation, in whole or in part, at any time without the prior written consent of ISCA, and that it will keep confidential all information contained herein not already in the public domain. The Preparers expressly disclaim any and all liability for representations or warranties, expressed or implied, contained in, or for omissions from, this Presentation or any other written or oral communication transmitted to any interested party in connection with this Presentation so far as is permitted by law. In particular, but without limitation, no representation or warranty is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, estimates, forecasts, analyses or forward looking statements contained in this Presentation which involve by their nature a number of risks, uncertainties or assumptions that could cause actual results or events to differ materially from those expressed or implied in this Presentation. In furnishing this Presentation, the Preparers reserve the right to amend or replace this Presentation at any time and undertake no obligation to update any of the information contained in the Presentation or to correct any inaccuracies that may become apparent. This Presentation shall remain the property of ISCA.

To download the guidance, please go to: IFRS Convergence 2018 Implementation Roadmap https://isca.org.sg/media/2238610/ifrs-convergence-2018-implementation-roadmap.pdf Report Findings: Poll on Readiness Level of Listed Companies to issue IFRS compliant interim results in 2018 https://isca.org.sg/media/2238611/ifrs-convergence-poll-report-final.pdf For more information on IFRS Convergence 2018, please visit: https://isca.org.sg/tkc/fr/current-issues/ifrs-convergence/

For any enquiries, please contact ISCA’s Corporate Reporting & Ethics (CoRE) Division @ [email protected].

To download the guidance, please go to: Revenue Recognition on Sale of Uncompleted Residential Properties in Singapore: Application of FRS 115 Revenue from Contracts with Customers https://isca.org.sg/media/2238612/isca_frs-115-revenue-recognition.pdf

For any enquiries, please contact ISCA’s Corporate Reporting & Ethics (CoRE) Division @ [email protected].