retail store audit sop1.xls

DESCRIPTION

Retail Store AuditTRANSCRIPT

Date Section Description

October 29, 2004 RRR Additional W/P's for cash handling

November 5, 2004 PPP

Add the following to the first comment box of the PPP audit

program:

"Clothing non-manager: $180/year includes PST and GST.

Safety shoes non-manager: $90/year plus taxes or $180 plus taxes

every two years.

Managers: $451/year including PST and GST. This allowance is

for clothing and safety shoes."

November 8, 2004 Inventory

Comment added to the extent of testing box for section 3.i),

"Indicate the total number of products counted, the total number of

SKU's in the store and calculate the % of total SKU's counted."

November 8, 2004

Manager

Questionnaire

More details relating to the gift certificates were added. See

Manager Interview-Draft unapproved November 8, 2004

November 8, 2004 Security and Safety Added section 5. to the audit program.

November 25, 2004 PPP Section 1.ii) added to PPP audit program

November 25, 2004 PPP Details added to the comment in 1.i) of PPP audit program

November 25, 2004 PPP Reasonability test developed for clothing allowance.

November 25, 2004

Manager

Questionnaire

Further details relating to the allocation of clothing and shoe

allowances.

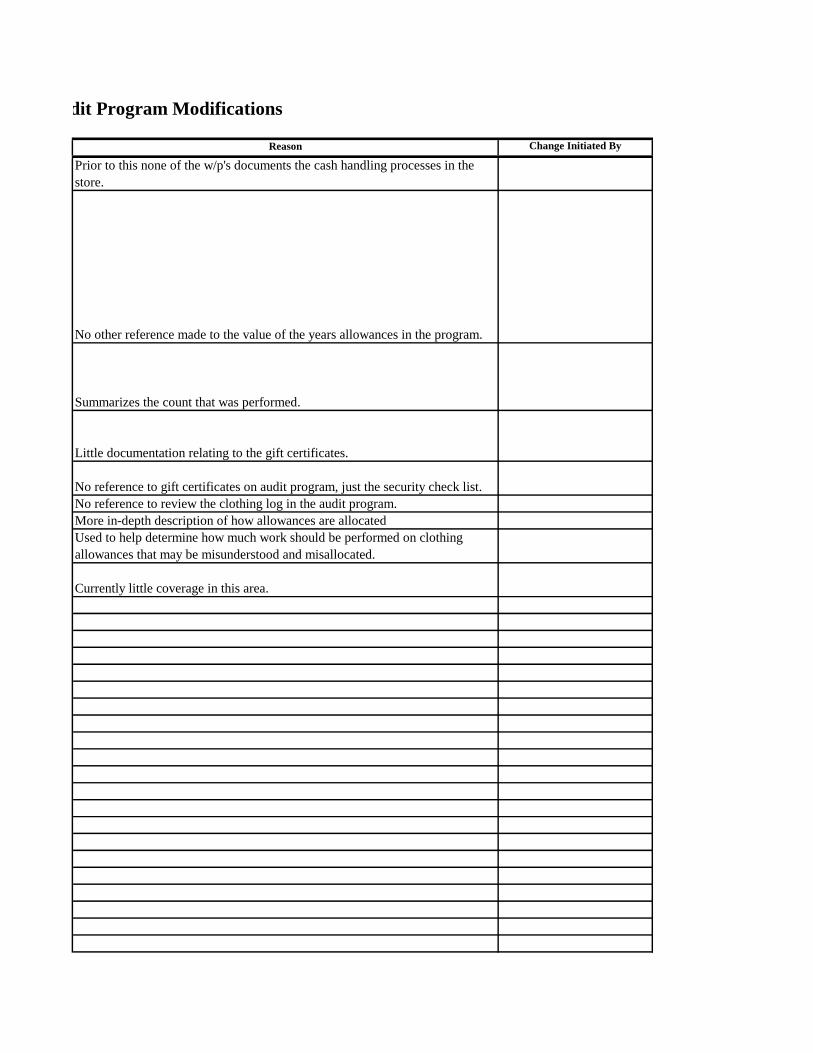

Store Audit Program Modifications

Reason Change Initiated By

Prior to this none of the w/p's documents the cash handling processes in the

store.

No other reference made to the value of the years allowances in the program.

Summarizes the count that was performed.

Little documentation relating to the gift certificates.

No reference to gift certificates on audit program, just the security check list.

No reference to review the clothing log in the audit program.

More in-depth description of how allowances are allocated

Used to help determine how much work should be performed on clothing

allowances that may be misunderstood and misallocated.

Currently little coverage in this area.

Store Audit Program Modifications

Change Approved By

Store Audit Program Modifications

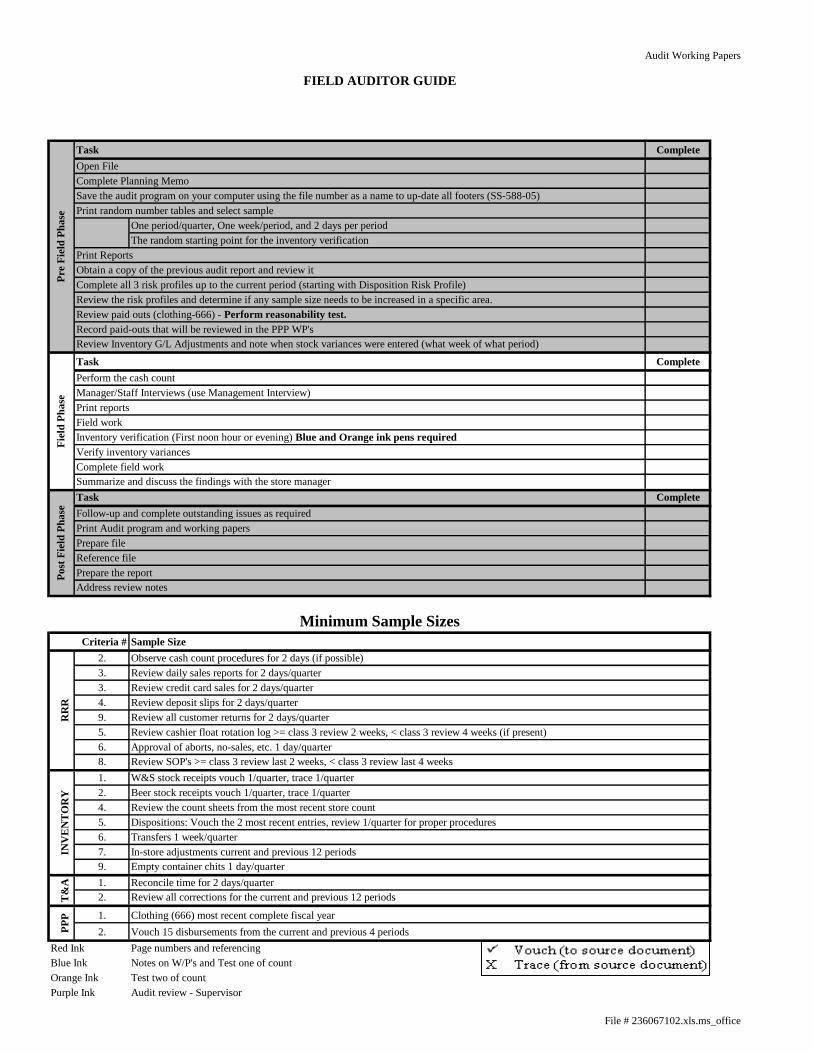

Obtain the "Index to Working Papers" from the "Store Audit Program" folder. For ease of formatting this document

has been maintained as a word document.

Obtain the "Index to Working Papers" from the "Store Audit Program" folder. For ease of formatting this document

has been maintained as a word document.

Audit Working Papers

Complete

Save the audit program on your computer using the file number as a name to up-date all footers (SS-588-05)

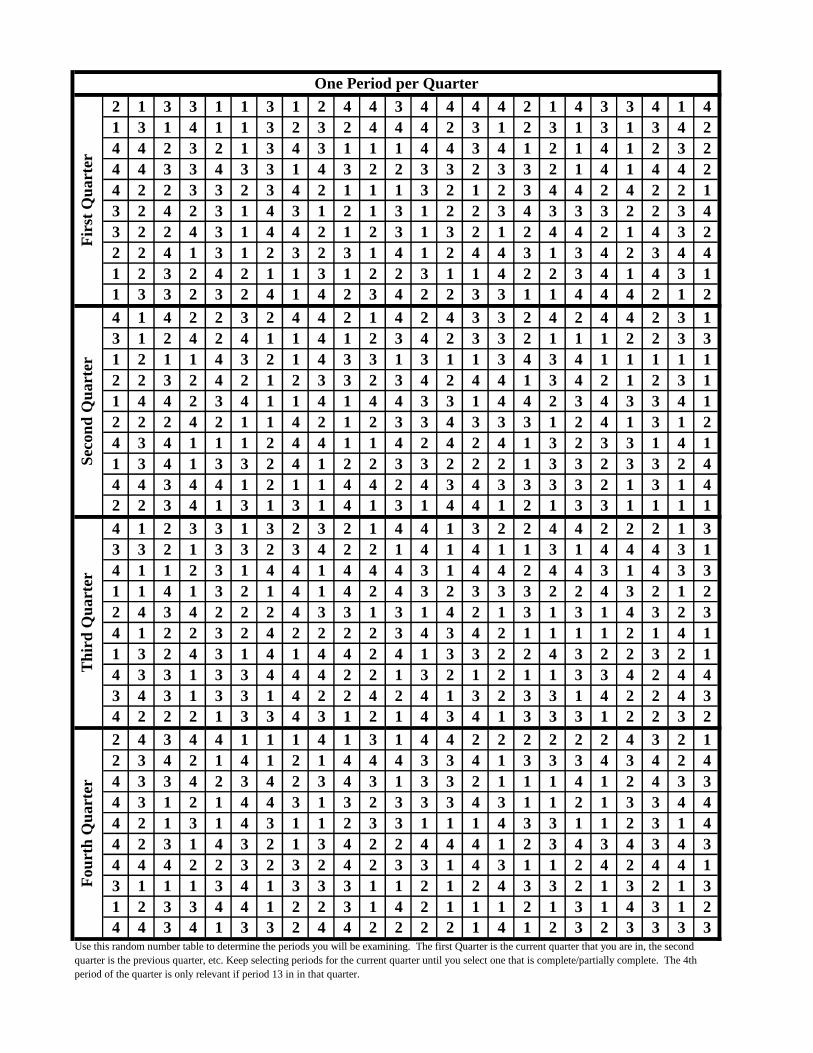

Print random number tables and select sample

One period/quarter, One week/period, and 2 days per period

The random starting point for the inventory verification

Complete

Complete

2.

3.

3.

4.

9.

5.

6.

8.

1.

2.

4.

5.

6.

7.

9.

1.

2.

1.

2.

Page numbers and referencing

Notes on W/P's and Test one of count

Test two of count

Audit review - Supervisor

Review deposit slips for 2 days/quarter

Review credit card sales for 2 days/quarter

Red Ink

Blue Ink

Orange Ink

Purple Ink

Beer stock receipts vouch 1/quarter, trace 1/quarter

W&S stock receipts vouch 1/quarter, trace 1/quarter

Observe cash count procedures for 2 days (if possible)

Review cashier float rotation log >= class 3 review 2 weeks, < class 3 review 4 weeks (if present)

Sample SizeCriteria #

RR

R

Review SOP's >= class 3 review last 2 weeks, < class 3 review last 4 weeks

Approval of aborts, no-sales, etc. 1 day/quarter

Review all customer returns for 2 days/quarter

T&

AP

PP Clothing (666) most recent complete fiscal year

Vouch 15 disbursements from the current and previous 4 periods

Review all corrections for the current and previous 12 periods

Empty container chits 1 day/quarter

Reconcile time for 2 days/quarter

Address review notes

Po

st F

ield

Ph

ase

Minimum Sample Sizes

Prepare file

Prepare the report

INV

EN

TO

RY

In-store adjustments current and previous 12 periods

Transfers 1 week/quarter

Dispositions: Vouch the 2 most recent entries, review 1/quarter for proper procedures

Review the count sheets from the most recent store count

Task

Task

Print reports

Review paid outs (clothing-666) - Perform reasonability test.

Review Inventory G/L Adjustments and note when stock variances were entered (what week of what period)

Print Reports

Complete all 3 risk profiles up to the current period (starting with Disposition Risk Profile)

Review the risk profiles and determine if any sample size needs to be increased in a specific area.

Record paid-outs that will be reviewed in the PPP WP's

Field work

Review daily sales reports for 2 days/quarter

Inventory verification (First noon hour or evening) Blue and Orange ink pens required

Verify inventory variances

Complete field work

Summarize and discuss the findings with the store manager

Task

Follow-up and complete outstanding issues as required

Print Audit program and working papers

Reference file

Fie

ld P

ha

se

Perform the cash count

Manager/Staff Interviews (use Management Interview)

FIELD AUDITOR GUIDE

Open File

Complete Planning Memo

Pre F

ield

Ph

ase

Obtain a copy of the previous audit report and review it

File # 236067102.xls.ms_office

Audit Working Papers

Audit review - DirectorGreen Ink

File # 236067102.xls.ms_office

Audit Working Papers

File # 236067102.xls.ms_office

Obtain the "Planning Memorandum" from the "Store Audit Program" folder. For ease of formatting this document

has been maintained as a word document.

Internal Audit Page 16 of 86 Confidential

Obtain the "Planning Memorandum" from the "Store Audit Program" folder. For ease of formatting this document

has been maintained as a word document.

Internal Audit Page 17 of 86 Confidential

NAME PERIODS ORIGIN

GL Fixed Asset Listing (also request serial #'s) - H.O. Financial Services

Copy of previous audit report - Previous audit file

Store inventory GL Adjustments current period + previous 12 office

SOS Dollar Sales by Retail Sales Code ending current period office

Paid Out (For Enquiry) - clothing (666) last complete fiscal year office

TAMS - Query Report for all part-time employees in the

store. Do not include TRC's that denote leave (I.e. EDO's,

leave, etc.).

Fiscal year prior to the last fiscal year (i.e. if you

are reviewing clothing for fiscal 2004, print the

part-time hours for fiscal 2003) office

TAMS - Query Report for all fulltime employees in the

store. last complete fiscal year office

Paid Out (For Enquiry) - all GL Accounts current period + previous 4 office or store

Inventory Reconciliation - Wine & Spirits

Print each of the four randomly selected periods

from the current and previous 3 quarters office or store

Inventory Reconciliation - Allied

Print each of the four randomly selected periods

from the current and previous 3 quarters office or store

Inventory Reconciliation - Beer

Print each of the four randomly selected periods

from the current and previous 3 quarters office or store

TAMS - Query Report 2 Days/quarter for 4 quarters office or store

Special Occasion Permit Report Most recent complete period store

Clerk Audaction Report (print by period) current period + previous 3 store

ISP employee master file - store

ISP security levels - store

POS security levels - store

DOCUMENT SUMMARY

File # 236067102.xls.ms_office

PRINTED

DOCUMENT SUMMARY

File # 236067102.xls.ms_office

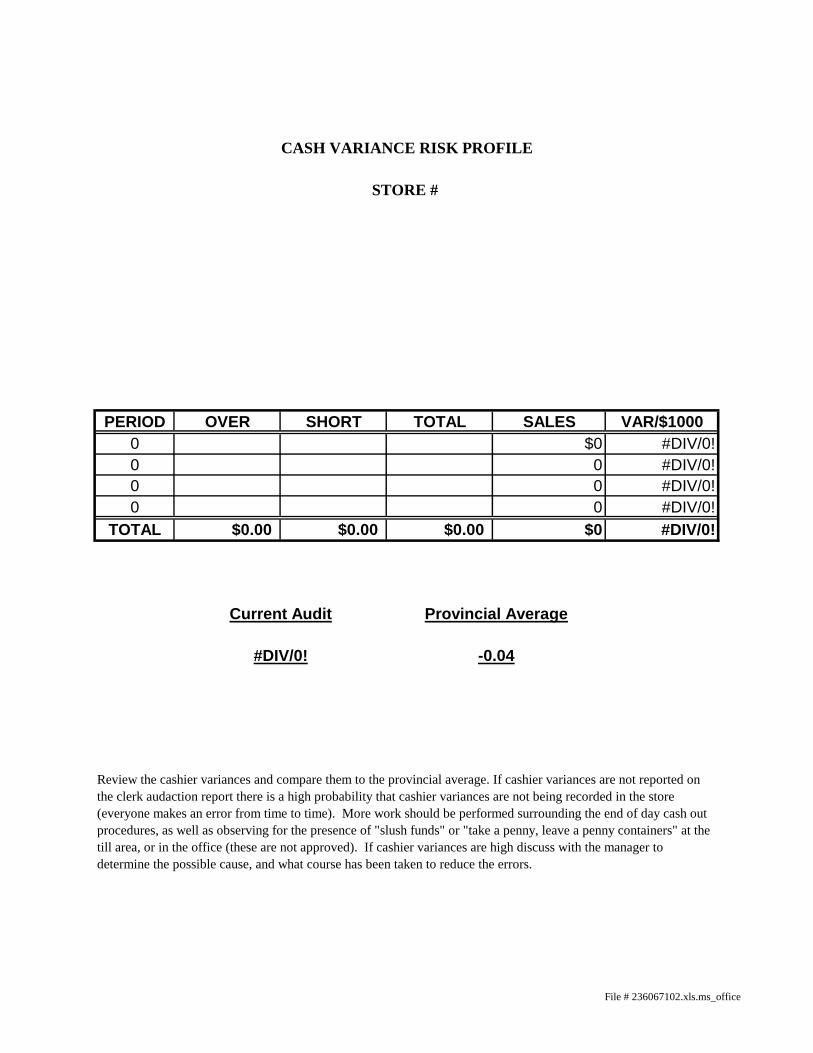

PERIOD OVER SHORT TOTAL SALES VAR/$1000

0 $0 #DIV/0!

0 0 #DIV/0!

0 0 #DIV/0!

0 0 #DIV/0!

TOTAL $0.00 $0.00 $0.00 $0 #DIV/0!

Review the cashier variances and compare them to the provincial average. If cashier variances are not reported on

the clerk audaction report there is a high probability that cashier variances are not being recorded in the store

(everyone makes an error from time to time). More work should be performed surrounding the end of day cash out

procedures, as well as observing for the presence of "slush funds" or "take a penny, leave a penny containers" at the

till area, or in the office (these are not approved). If cashier variances are high discuss with the manager to

determine the possible cause, and what course has been taken to reduce the errors.

#DIV/0! -0.04

CASH VARIANCE RISK PROFILE

STORE #

Current Audit Provincial Average

File # 236067102.xls.ms_office

PERIOD WINE & SPIRITS BEER

0

0

0

0

0

0

0

0

0

0

0

0

0

TOTAL $0.00 $0.00

Total Sales: $0

Total Variance: $0.00

Current Audit Provincial Average

#DIV/0! -0.72

STORE #

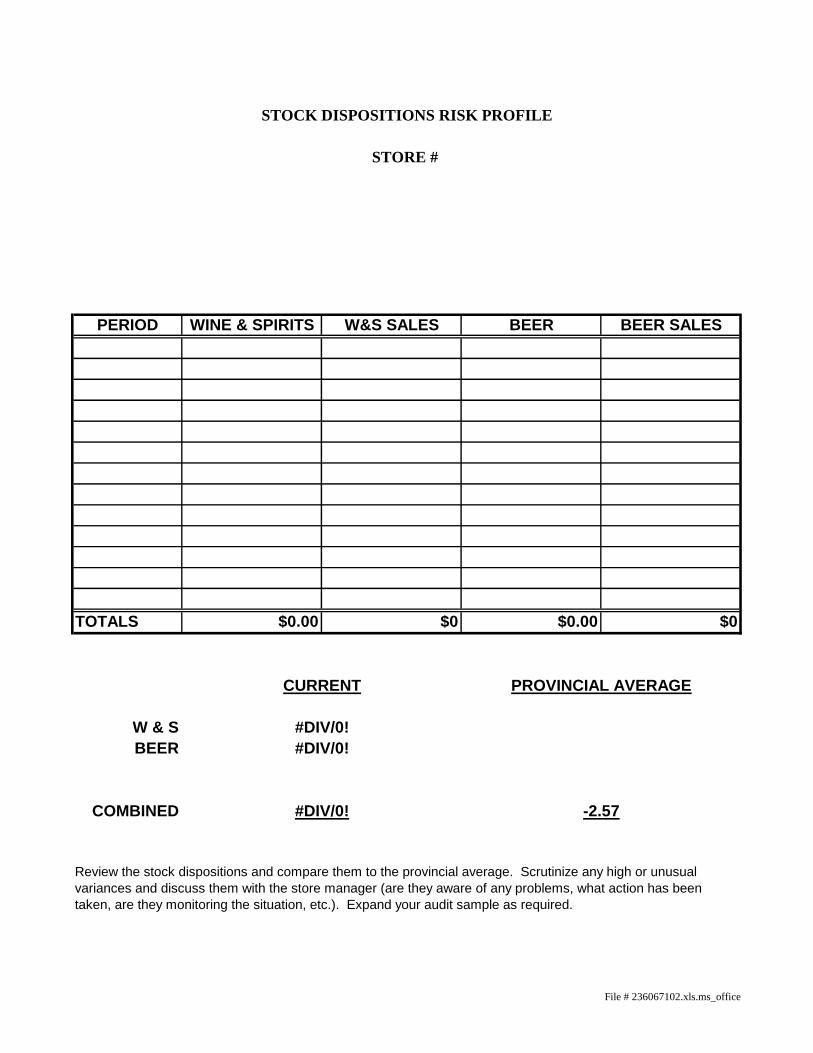

STOCK VARIANCE RISK PROFILE

Review the stock variances and compare them to the provincial

average. High variances may be an indication of customer losses,

shipping and receiving errors (case lots), poor count procedures

(units), poor organization in the warehouse (case lots), etc. Low

variances may be an indication that variances have not been

correctly adjusted, if this is the case the variances noted during the

audit count may be high (if unreported variances are material it could

be considered financial statement fraud). Discuss with the store

manager (are they aware of any problems, what action has been

taken, are they monitoring the situation, etc.). Expand your audit

sample as required.

File #236067102.xls.ms_office

PERIOD WINE & SPIRITS W&S SALES BEER BEER SALES

TOTALS $0.00 $0 $0.00 $0

W & S

BEER

COMBINED

STORE #

CURRENT PROVINCIAL AVERAGE

STOCK DISPOSITIONS RISK PROFILE

Review the stock dispositions and compare them to the provincial average. Scrutinize any high or unusual

variances and discuss them with the store manager (are they aware of any problems, what action has been

taken, are they monitoring the situation, etc.). Expand your audit sample as required.

#DIV/0!

#DIV/0!

#DIV/0! -2.57

File # 236067102.xls.ms_office

Revenue / Receivables / Receipts

Criteria Audit Procedures Initials Extent of testing W/P's

i) Cash counts to be performed upon arrival at the store. For 1 day

count total cash and credit card sales in class 1 and 2 stores and ensure

this agrees to the system.

· Observe for the presence of personal cheques, IOU's, petty cash

invoices indicating payment to employees (in the till but not processed

through the system), and that all credit card receipts are both present

and signed by the customer.

· For all other stores count the change fund.

When counting cash, be observant for counterfeit currency (see section

3.7.19 of new store policy manual).

· Reconcile the change fund and floats to cash withheld.

ii) Observe the location and security of the change fund/ unassigned

floats. Assess the accessibility of the funds.

iii) Discuss with the manager how/when the change fund is balanced.

· Review the documentation that substantiates the information provided

by the manager (adding machine tape, log, etc.) Review 2 days in class

3 and higher stores and 4 days in class 1 and 2 stores.

iv) Observe the purchase of change by employees. Note the amount of

segregation. The manager/supervisor s/b responsible for the change

purchase.

v) Review documentation relating to change purchases from the bank.

· Deposit slip itemizing change purchase must be present, if an

armoured car service is utilized documentation indicating the

acceptance the funds for the change purchase must be present.

vi) All coin advances to cashiers from the change fund must be verified

by a count of the cashiers cash tray. Tray must be over by amount of

advance from change fund.

Hours to complete RRR work.

1. The store change fund/floats are properly secured and accurate and an adequate level of segregation

of duties is present. All cash is present and accounted for in the store. (Section 3.7.1 and 3.7.2 Store

Policy and Procedure Manual)

· Manager/Supervisor balances the change fund at the beginning and end of each shift. If the person

starting the shift verified the fund at the end of the previous shift they do not have to re verify the

fund.

· Change fund is to be locked in a safe or deposited in the bank at night.

· A manager/supervisor must handle cashier coin requirements from the change fund.

· Change funds shall not be utilized for personal use.

· Change fund must be locked at all times.

· Access to the change fund shall be restricted to supervisory personnel.

· Responsibility of the change fund must be rotated among supervisory personnel, a log is to be

maintained for audit review.

Page 23 of 86 File # 236067102.xls.ms_office

Revenue / Receivables / Receipts

Criteria Audit Procedures Initials Extent of testing W/P's

Hours to complete RRR work.

1. The store change fund/floats are properly secured and accurate and an adequate level of segregation

of duties is present. All cash is present and accounted for in the store. (Section 3.7.1 and 3.7.2 Store

Policy and Procedure Manual)

· Manager/Supervisor balances the change fund at the beginning and end of each shift. If the person

starting the shift verified the fund at the end of the previous shift they do not have to re verify the

fund.

· Change fund is to be locked in a safe or deposited in the bank at night.

· A manager/supervisor must handle cashier coin requirements from the change fund.

· Change funds shall not be utilized for personal use.

· Change fund must be locked at all times.

· Access to the change fund shall be restricted to supervisory personnel.

· Responsibility of the change fund must be rotated among supervisory personnel, a log is to be

maintained for audit review.

i) For 2 days during the audit observe cashier(s) counting sales receipts

and supervisor confirming all receipts at the end of the day (document

procedures in the audit file, and include copy of cashier readings).

ii) Discuss with the cashier the procedure used to verify the float at the

beginning and end of their shift.

· For two days during the audit observe that the stated procedures are

followed.

iii) Verify that store cash/change funds are not used for personal use.

Observe for the presence of IOU's and personal cheques.

· If present COPY the IOU/personal cheque.

i) Review the daily sales/adjustment reports for 2 days per quarter to

ensure store manager has approved them.

ii) For the above sample review credit card slips to ensure they are

present, and correctly processed.

iii) For the above sample review the deposit slips to ensure:

· The bank stamp and teller initials are present.

· Observe for the store managers initials on the deposit slip

· Reconcile the deposit amount to the daily sales reports

· All credit card slips are present and signed, a hard copy of card is

required if reference number begins with an "M".

i) Interview the manager and staff regarding the procedures for handling

deposits.

· For two days during the audit observe and document the procedures.

ii) For the sample noted in 3. above review:

· Cashier reading to ensure they have been completed and signed by

both the employee and supervisor/manager.

· deposit slips to ensure they have been reviewed/approved by a

manager/supervisor.

iii) Observe bank deposit by accompanying manager to bank to ensure

security measures are in place.

· Observe the; lighting, accessibility, neighbourhood, location of drop-

box, manager should drive, etc.

2. Adequate segregation of duties is present when an employee cashes-out. (Section 3.1,3.7.1, 3.7.3,

3.7.16, and 3.7.20 Store Policy and Procedure Manual).

· Managers/supervisors/employees shall not use cash/change fund for personal use.

· Cashier must verify floats when they receive them and must report all variances to the manager.

· The amount of cash in the cash tray shall not be >$1500

· Cash is not counted in public view.

The following EOD procedures must be followed:

· Manager/Supervisor shall not show the cashier reading to the cashier until all funds have been

counted.

· After the cashier counts all cash the supervisor will complete the cash count form, recount the sales

receipts, and if they wish recount the float.

· The manager/supervisor must recount all floats if a variance >$1 exists.

· The manager/supervisor must enter the deposit amount into the ISP

· The manager/supervisor and cashier must sign the reading

· All sales receipts must be deposited (all variances must be recorded)

3. Store Manager reviews and approves the daily sales reports. All sales have been correctly recorded.

(Section 3.7.3, 3.7.4, and 3.7.20 Store Policy and Procedure Manual)

· The manager/supervisor shall monitor the transactions processed by all cashiers.

· Debit/credit slips, coupons, and redeemed gift certificates shall be retained in a secure location for

end of day reconciliation.

· All cash register detailed tape and transaction records must be retained.

· Manager/supervisor is responsible for the review and approval of daily sales reports.

4. Ensure adequate segregation of duties for deposits, and ensure all deposits are properly secured and

deposited. (Section 3.7.3, 3.7.15, and 3.7.20 Store Policy and Procedure Manual)

· The manager/supervisor is responsible for ensuring an adequate level of segregation of duties.

· Deposit envelopes are to be stored in a locked safe until pick-up by an authorized armoured car

service or delivered to the bank.

· All sales receipts are to be deposited in a night depository if the store does not have a safe.

· The following level of segregation of duties is required (in multi person stores):

· Cash count supervised by manager/supervisor

· Deposits verified by manager/supervisor

· Manager/supervisor deposits sales or authorizes pick-up by armoured car service.

· Manager/supervisor reviews and verifies returned deposit slips to dailies.

Page 24 of 86 File # 236067102.xls.ms_office

Revenue / Receivables / Receipts

Criteria Audit Procedures Initials Extent of testing W/P's

Hours to complete RRR work.

1. The store change fund/floats are properly secured and accurate and an adequate level of segregation

of duties is present. All cash is present and accounted for in the store. (Section 3.7.1 and 3.7.2 Store

Policy and Procedure Manual)

· Manager/Supervisor balances the change fund at the beginning and end of each shift. If the person

starting the shift verified the fund at the end of the previous shift they do not have to re verify the

fund.

· Change fund is to be locked in a safe or deposited in the bank at night.

· A manager/supervisor must handle cashier coin requirements from the change fund.

· Change funds shall not be utilized for personal use.

· Change fund must be locked at all times.

· Access to the change fund shall be restricted to supervisory personnel.

· Responsibility of the change fund must be rotated among supervisory personnel, a log is to be

maintained for audit review.

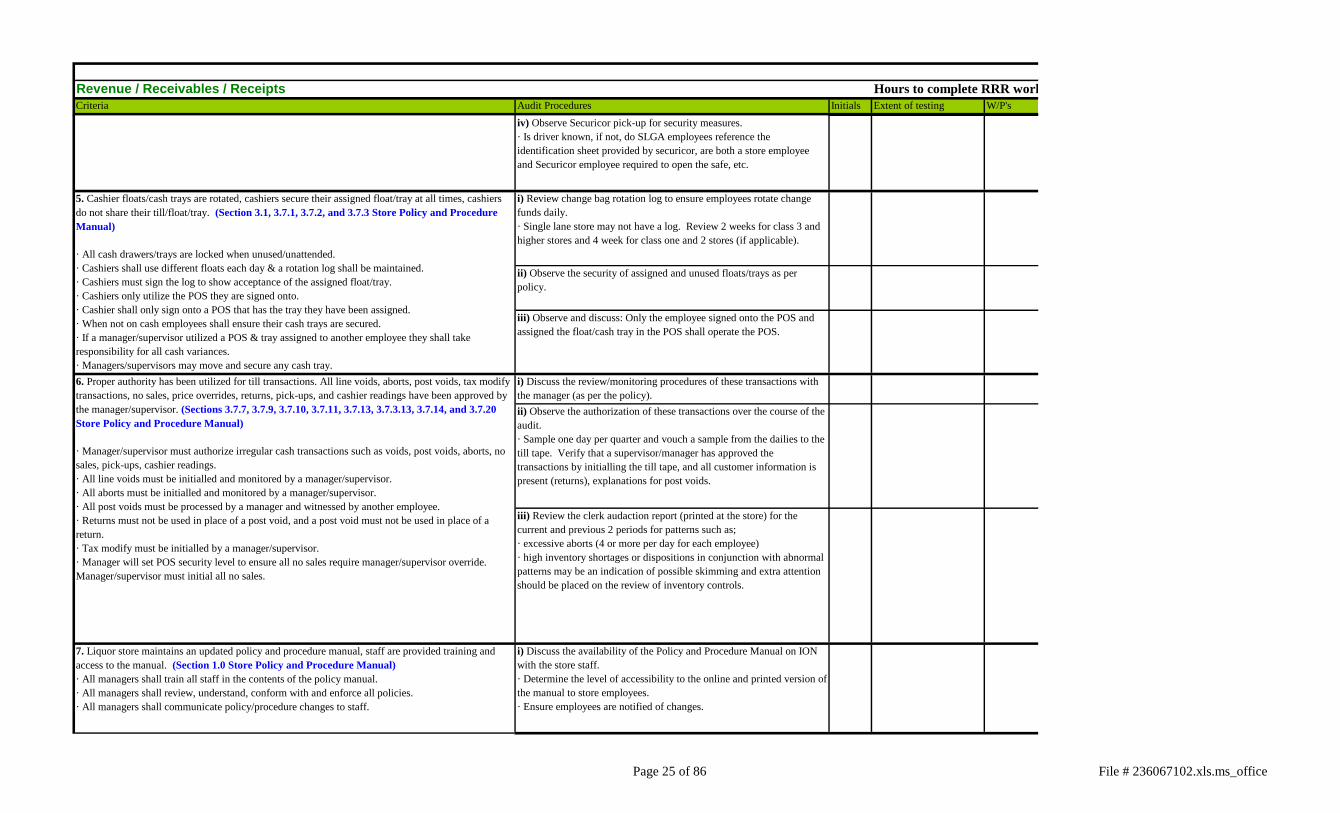

iv) Observe Securicor pick-up for security measures.

· Is driver known, if not, do SLGA employees reference the

identification sheet provided by securicor, are both a store employee

and Securicor employee required to open the safe, etc.

i) Review change bag rotation log to ensure employees rotate change

funds daily.

· Single lane store may not have a log. Review 2 weeks for class 3 and

higher stores and 4 week for class one and 2 stores (if applicable).

ii) Observe the security of assigned and unused floats/trays as per

policy.

iii) Observe and discuss: Only the employee signed onto the POS and

assigned the float/cash tray in the POS shall operate the POS.

i) Discuss the review/monitoring procedures of these transactions with

the manager (as per the policy).

ii) Observe the authorization of these transactions over the course of the

audit.

· Sample one day per quarter and vouch a sample from the dailies to the

till tape. Verify that a supervisor/manager has approved the

transactions by initialling the till tape, and all customer information is

present (returns), explanations for post voids.

iii) Review the clerk audaction report (printed at the store) for the

current and previous 2 periods for patterns such as;

· excessive aborts (4 or more per day for each employee)

· high inventory shortages or dispositions in conjunction with abnormal

patterns may be an indication of possible skimming and extra attention

should be placed on the review of inventory controls.

7. Liquor store maintains an updated policy and procedure manual, staff are provided training and

access to the manual. (Section 1.0 Store Policy and Procedure Manual)

· All managers shall train all staff in the contents of the policy manual.

· All managers shall review, understand, conform with and enforce all policies.

· All managers shall communicate policy/procedure changes to staff.

i) Discuss the availability of the Policy and Procedure Manual on ION

with the store staff.

· Determine the level of accessibility to the online and printed version of

the manual to store employees.

· Ensure employees are notified of changes.

5. Cashier floats/cash trays are rotated, cashiers secure their assigned float/tray at all times, cashiers

do not share their till/float/tray. (Section 3.1, 3.7.1, 3.7.2, and 3.7.3 Store Policy and Procedure

Manual)

· All cash drawers/trays are locked when unused/unattended.

· Cashiers shall use different floats each day & a rotation log shall be maintained.

· Cashiers must sign the log to show acceptance of the assigned float/tray.

· Cashiers only utilize the POS they are signed onto.

· Cashier shall only sign onto a POS that has the tray they have been assigned.

· When not on cash employees shall ensure their cash trays are secured.

· If a manager/supervisor utilized a POS & tray assigned to another employee they shall take

responsibility for all cash variances.

· Managers/supervisors may move and secure any cash tray.

6. Proper authority has been utilized for till transactions. All line voids, aborts, post voids, tax modify

transactions, no sales, price overrides, returns, pick-ups, and cashier readings have been approved by

the manager/supervisor. (Sections 3.7.7, 3.7.9, 3.7.10, 3.7.11, 3.7.13, 3.7.3.13, 3.7.14, and 3.7.20

Store Policy and Procedure Manual)

· Manager/supervisor must authorize irregular cash transactions such as voids, post voids, aborts, no

sales, pick-ups, cashier readings.

· All line voids must be initialled and monitored by a manager/supervisor.

· All aborts must be initialled and monitored by a manager/supervisor.

· All post voids must be processed by a manager and witnessed by another employee.

· Returns must not be used in place of a post void, and a post void must not be used in place of a

return.

· Tax modify must be initialled by a manager/supervisor.

· Manager will set POS security level to ensure all no sales require manager/supervisor override.

Manager/supervisor must initial all no sales.

4. Ensure adequate segregation of duties for deposits, and ensure all deposits are properly secured and

deposited. (Section 3.7.3, 3.7.15, and 3.7.20 Store Policy and Procedure Manual)

· The manager/supervisor is responsible for ensuring an adequate level of segregation of duties.

· Deposit envelopes are to be stored in a locked safe until pick-up by an authorized armoured car

service or delivered to the bank.

· All sales receipts are to be deposited in a night depository if the store does not have a safe.

· The following level of segregation of duties is required (in multi person stores):

· Cash count supervised by manager/supervisor

· Deposits verified by manager/supervisor

· Manager/supervisor deposits sales or authorizes pick-up by armoured car service.

· Manager/supervisor reviews and verifies returned deposit slips to dailies.

Page 25 of 86 File # 236067102.xls.ms_office

Revenue / Receivables / Receipts

Criteria Audit Procedures Initials Extent of testing W/P's

Hours to complete RRR work.

1. The store change fund/floats are properly secured and accurate and an adequate level of segregation

of duties is present. All cash is present and accounted for in the store. (Section 3.7.1 and 3.7.2 Store

Policy and Procedure Manual)

· Manager/Supervisor balances the change fund at the beginning and end of each shift. If the person

starting the shift verified the fund at the end of the previous shift they do not have to re verify the

fund.

· Change fund is to be locked in a safe or deposited in the bank at night.

· A manager/supervisor must handle cashier coin requirements from the change fund.

· Change funds shall not be utilized for personal use.

· Change fund must be locked at all times.

· Access to the change fund shall be restricted to supervisory personnel.

· Responsibility of the change fund must be rotated among supervisory personnel, a log is to be

maintained for audit review.

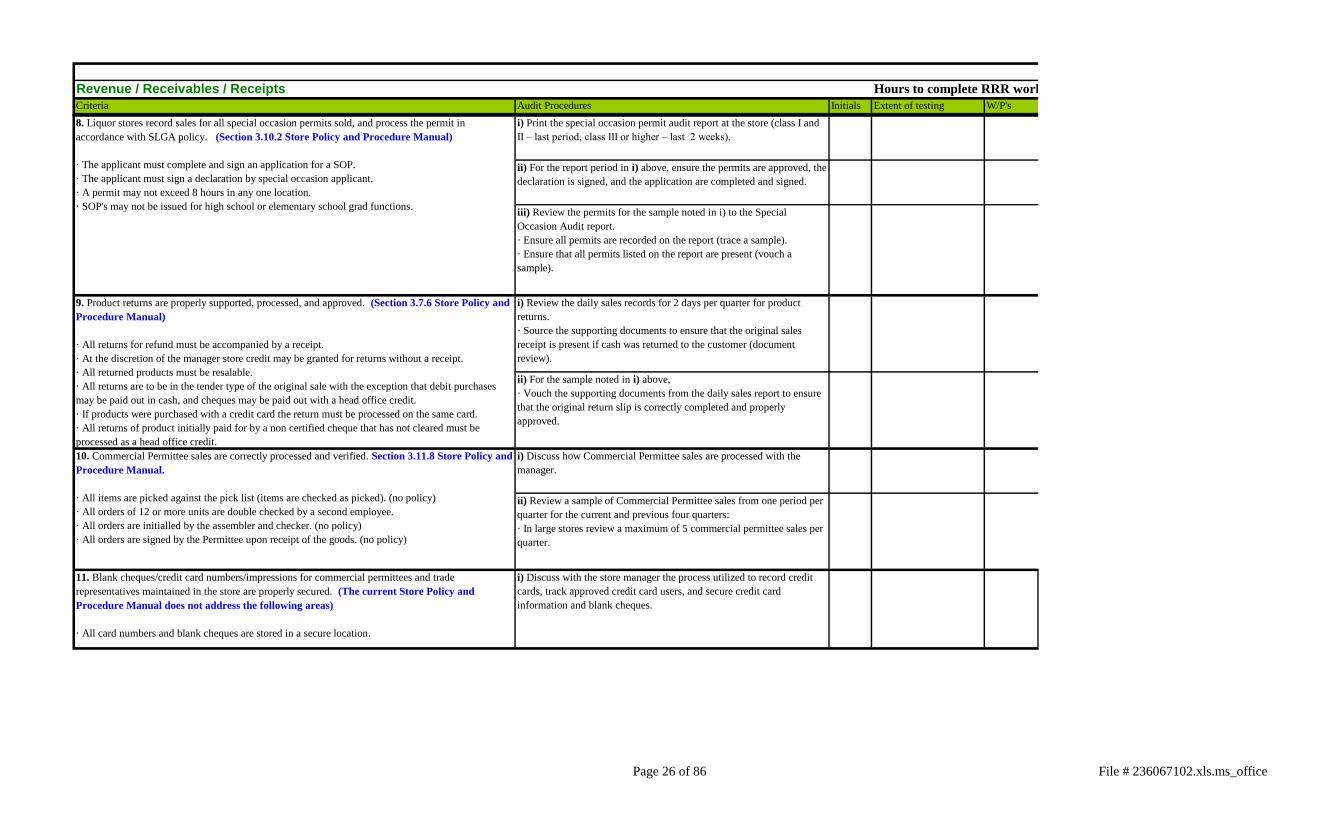

i) Print the special occasion permit audit report at the store (class I and

II – last period, class III or higher – last 2 weeks).

ii) For the report period in i) above, ensure the permits are approved, the

declaration is signed, and the application are completed and signed.

iii) Review the permits for the sample noted in i) to the Special

Occasion Audit report.

· Ensure all permits are recorded on the report (trace a sample).

· Ensure that all permits listed on the report are present (vouch a

sample).

i) Review the daily sales records for 2 days per quarter for product

returns.

· Source the supporting documents to ensure that the original sales

receipt is present if cash was returned to the customer (document

review).

ii) For the sample noted in i) above,

· Vouch the supporting documents from the daily sales report to ensure

that the original return slip is correctly completed and properly

approved.

i) Discuss how Commercial Permittee sales are processed with the

manager.

ii) Review a sample of Commercial Permittee sales from one period per

quarter for the current and previous four quarters:

· In large stores review a maximum of 5 commercial permittee sales per

quarter.

9. Product returns are properly supported, processed, and approved. (Section 3.7.6 Store Policy and

Procedure Manual)

· All returns for refund must be accompanied by a receipt.

· At the discretion of the manager store credit may be granted for returns without a receipt.

· All returned products must be resalable.

· All returns are to be in the tender type of the original sale with the exception that debit purchases

may be paid out in cash, and cheques may be paid out with a head office credit.

· If products were purchased with a credit card the return must be processed on the same card.

· All returns of product initially paid for by a non certified cheque that has not cleared must be

processed as a head office credit.

8. Liquor stores record sales for all special occasion permits sold, and process the permit in

accordance with SLGA policy. (Section 3.10.2 Store Policy and Procedure Manual)

· The applicant must complete and sign an application for a SOP.

· The applicant must sign a declaration by special occasion applicant.

· A permit may not exceed 8 hours in any one location.

· SOP's may not be issued for high school or elementary school grad functions.

i) Discuss with the store manager the process utilized to record credit

cards, track approved credit card users, and secure credit card

information and blank cheques.

10. Commercial Permittee sales are correctly processed and verified. Section 3.11.8 Store Policy and

Procedure Manual.

· All items are picked against the pick list (items are checked as picked). (no policy)

· All orders of 12 or more units are double checked by a second employee.

· All orders are initialled by the assembler and checker. (no policy)

· All orders are signed by the Permittee upon receipt of the goods. (no policy)

11. Blank cheques/credit card numbers/impressions for commercial permittees and trade

representatives maintained in the store are properly secured. (The current Store Policy and

Procedure Manual does not address the following areas)

· All card numbers and blank cheques are stored in a secure location.

Page 26 of 86 File # 236067102.xls.ms_office

Store Audit Program

Comments

Hours to complete RRR work.

Page 27 of 86 File # 236067102.xls.ms_office

Store Audit Program

Comments

Hours to complete RRR work.

Page 28 of 86 File # 236067102.xls.ms_office

Store Audit Program

Comments

Hours to complete RRR work.

Page 29 of 86 File # 236067102.xls.ms_office

Store Audit Program

Comments

Hours to complete RRR work.

Page 30 of 86 File # 236067102.xls.ms_office

Verified Y/N Tray # Float

Accoutability Total from

Reading Total Audit Count Audit Variance

$0.00 $0.00 $0.00

0.00 0.00 0.00

0.00 0.00 0.00

0.00 0.00 0.00

0.00 0.00 0.00

0.00 0.00 0.00

0.00 0.00 0.00

0.00 0.00 0.00

0.00 0.00 0.00

0.00 0.00 0.00

0.00 0.00 0.00

$0.00 $0.00 $0.00 $0.00 $0.00

$0.00

0.00

0.00

$0.00

0.00

$0.00Variance

Plus documented Change Orders

Plus Value of Change Fund

Total

Less Cash Withheld from Previous Day

Summary of all Cash Trays in the Store

Totals for all Trays

Total Assigned Floats from all Cash Trays

Reconciliation of Cash Withheld from Previous Days Daily Sales Reports

File # 236067102.xls.ms_office

Field Auditors Cash Count Form

Date: Time:

Denomination Quantity Value Total

Pennies 0 X $0.50 = $0.00

Nickels 0 X 2.00 = 0.00

Dimes 0 X 5.00 = 0.00

Quarters 0 X 10.00 = 0.00

Loonies 0 X 25.00 = 0.00

Toonies 0 X 50.00 = 0.00 $0.00

Denomination Quantity Value Total

Pennies 0 X $0.01 = $0.00

Nickels 0 X 0.05 = 0.00

Dimes 0 X 0.10 = 0.00

Quarters 0 X 0.25 = 0.00

Loonies 0 X 1.00 = 0.00

Toonies 0 X 2.00 = 0.00 $0.00

Denomination Quantity Value Total

$1 Dollar 0 X $1.00 = $0.00

$2 Dollar 0 X 2.00 = 0.00

$5 Dollar 0 X 5.00 = 0.00

$10 Dollar 0 X 10.00 = 0.00

$20 Dollar 0 X 20.00 = 0.00

$50 Dollar 0 X 50.00 = 0.00

$100 Dollar 0 X 100.00 = 0.00 $0.00

Value

$0.00

$0.00

0.00

0.00

$0.00

0.00

Cash Overage/(Shortage) 0

Notes:

Paper Currency

Cheques

Payee and Notes

CHANGE FUND

Rolled Coin

Change

Equals Total Cash receipts

Less Cash Withheld from Daily Sales Report

Auditor Cashier

Total Cash on Hand

Change Order

Plus 6 tray @ $200

Manager/Supervisor

I certify that the above record is a true and accurate representation of the change fund totalling $[Total

Cash on Hand].

File # 236067102.xls.ms_office

Field Auditor's Cash Count Form

Date: Time:

Denomination Quantity Value Total

Pennies 0 X $0.50 = $0.00

Nickels 0 X 2.00 = 0.00

Dimes 0 X 5.00 = 0.00

Quarters 0 X 10.00 = 0.00

Loonies 0 X 25.00 = 0.00

Toonies 0 X 50.00 = 0.00 $0.00

Denomination Quantity Value Total

Pennies 0 X $0.01 = $0.00

Nickels 0 X 0.05 = 0.00

Dimes 0 X 0.10 = 0.00

Quarters 0 X 0.25 = 0.00

Loonies 0 X 1.00 = 0.00

Toonies 0 X 2.00 = 0.00 $0.00

Denomination Quantity Value Total

$1 Dollar 0 X $1.00 = $0.00

$2 Dollar 0 X 2.00 = 0.00

$5 Dollar 0 X 5.00 = 0.00

$10 Dollar 0 X 10.00 = 0.00

$20 Dollar 0 X 20.00 = 0.00

$50 Dollar 0 X 50.00 = 0.00

$100 Dollar 0 X 100.00 = 0.00 $0.00

Value

$0.00

$0.00

0.00

$0.00

0.00

$0.00

Notes:

Less: Value of Authorized Float

Cash Overage/(Shortage)

Auditor Cashier Manager/Supervisor

I certify that the above record is a true and accurate representation of [tray# ] totalling $[Total Cash on

Hand].

Total Cash on Hand

Sales (Accountability Total on cashier reading)

Equals Total Cash receipts

TRAY # ________

Cheques

Payee and Notes

Rolled Coin

Change

Paper Currency

File # 236067102.xls.ms_office

Audit Working Papers

Period/Date Reviewed Approved Present

Correctly

Completed

Required

Hard Copies

Present Present Completed

Bank Stamp

Present # Reviewed

Original

Receipt

Present

Return Slip

Present

Return Slip

Complete Printed Completed

Signed by

Employee Approved

Notes:

Revenue / Receivables / Receipts

Daily Sales Reports Credit Card Slips Deposit Slips Retail Returns Cashier Readings

Page 34 of 86 File # 236067102.xls.ms_office

Audit Working Papers

Notes

Page 35 of 86 File # 236067102.xls.ms_office

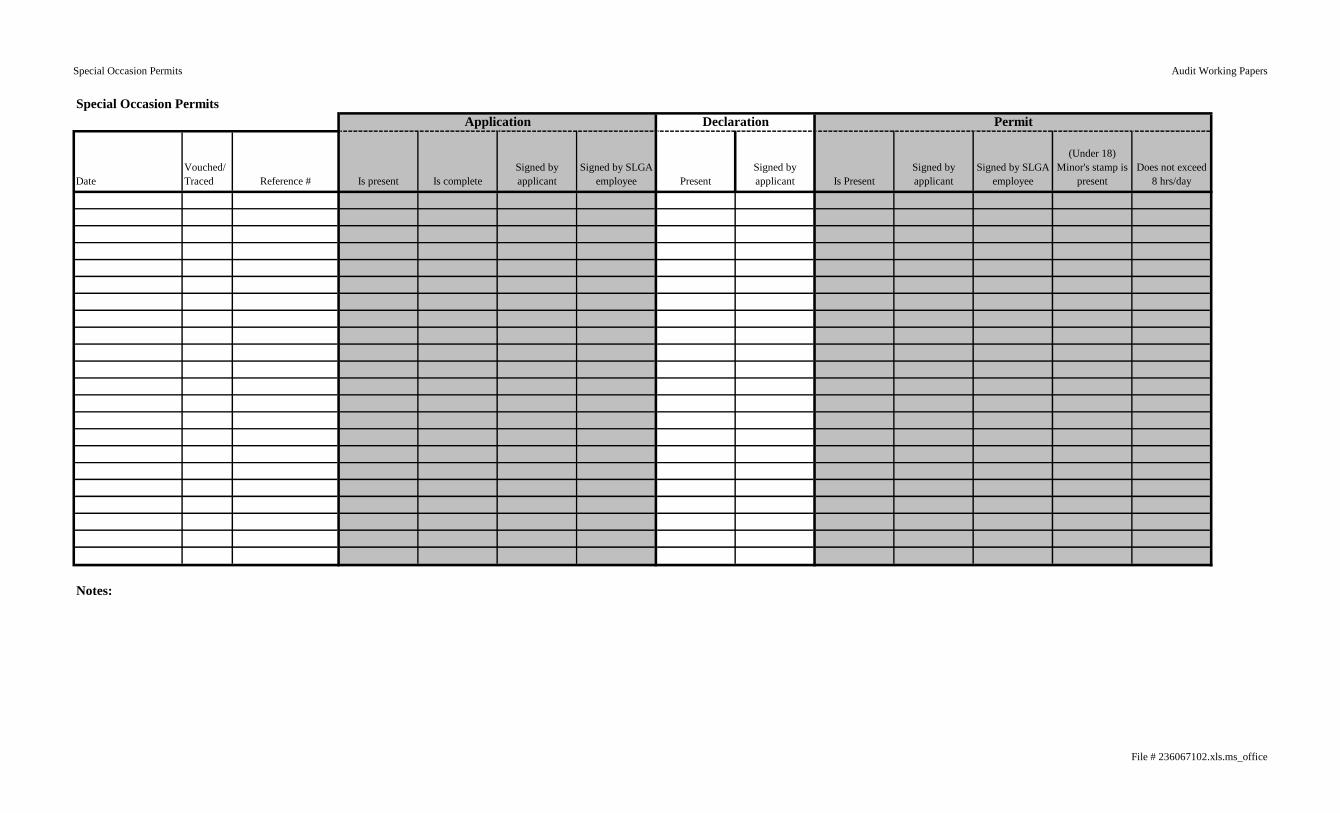

Special Occasion Permits Audit Working Papers

Date

Vouched/

Traced Reference # Is present Is complete

Signed by

applicant

Signed by SLGA

employee Present

Signed by

applicant Is Present

Signed by

applicant

Signed by SLGA

employee

(Under 18)

Minor's stamp is

present

Does not exceed

8 hrs/day

Notes:

Special Occasion Permits

Application Declaration Permit

File # 236067102.xls.ms_office

Special Occasion Permits Audit Working Papers

Notes

Special Occasion Permits

File # 236067102.xls.ms_office

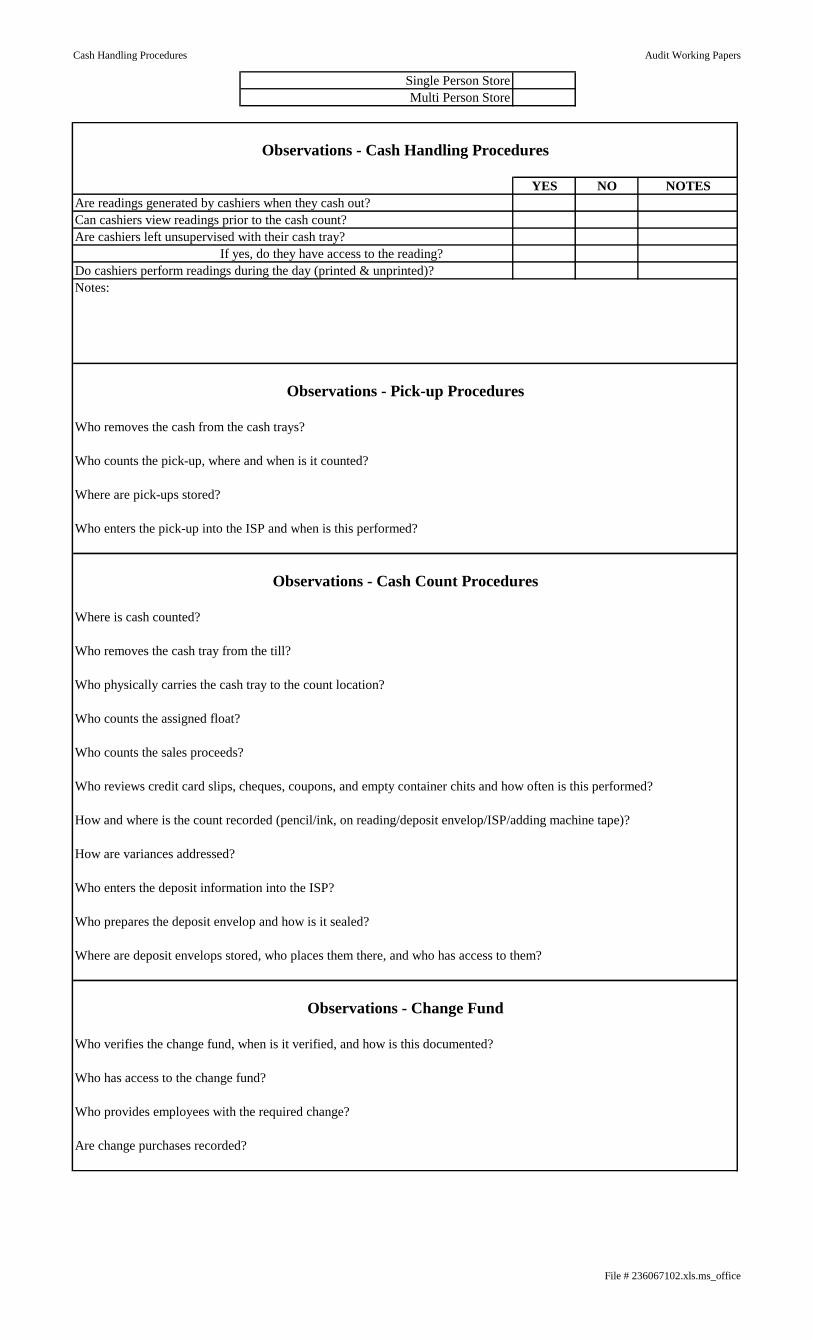

Cash Handling Procedures Audit Working Papers

Single Person Store

Multi Person Store

YES NO NOTES

Who removes the cash from the cash trays?

Who counts the pick-up, where and when is it counted?

Where are pick-ups stored?

Who enters the pick-up into the ISP and when is this performed?

Who counts the assigned float?

Who enters the deposit information into the ISP?

Who prepares the deposit envelop and how is it sealed?

Who counts the sales proceeds?

Where is cash counted?

Who removes the cash tray from the till?

Who physically carries the cash tray to the count location?

Who has access to the change fund?

Who verifies the change fund, when is it verified, and how is this documented?

Where are deposit envelops stored, who places them there, and who has access to them?

Observations - Change Fund

How and where is the count recorded (pencil/ink, on reading/deposit envelop/ISP/adding machine tape)?

Are change purchases recorded?

How are variances addressed?

Who provides employees with the required change?

Who reviews credit card slips, cheques, coupons, and empty container chits and how often is this performed?

Observations - Cash Count Procedures

Observations - Cash Handling Procedures

Notes:

Do cashiers perform readings during the day (printed & unprinted)?

Are readings generated by cashiers when they cash out?

Can cashiers view readings prior to the cash count?

Are cashiers left unsupervised with their cash tray?

If yes, do they have access to the reading?

Observations - Pick-up Procedures

File # 236067102.xls.ms_office

Commercial Permittees Audit Working Papers

Period/Date Reference #

Original customer

order retained

Inventory

checked off

Order checked

by 2nd

employee

Order initialled

by assembler

and checker

Order signed for

by permittee upon

receiving goods

Notes:

Commercial Permittees

File # 236067102.xls.ms_office

Commercial Permittees Audit Working Papers

Notes

Commercial Permittees

File # 236067102.xls.ms_office

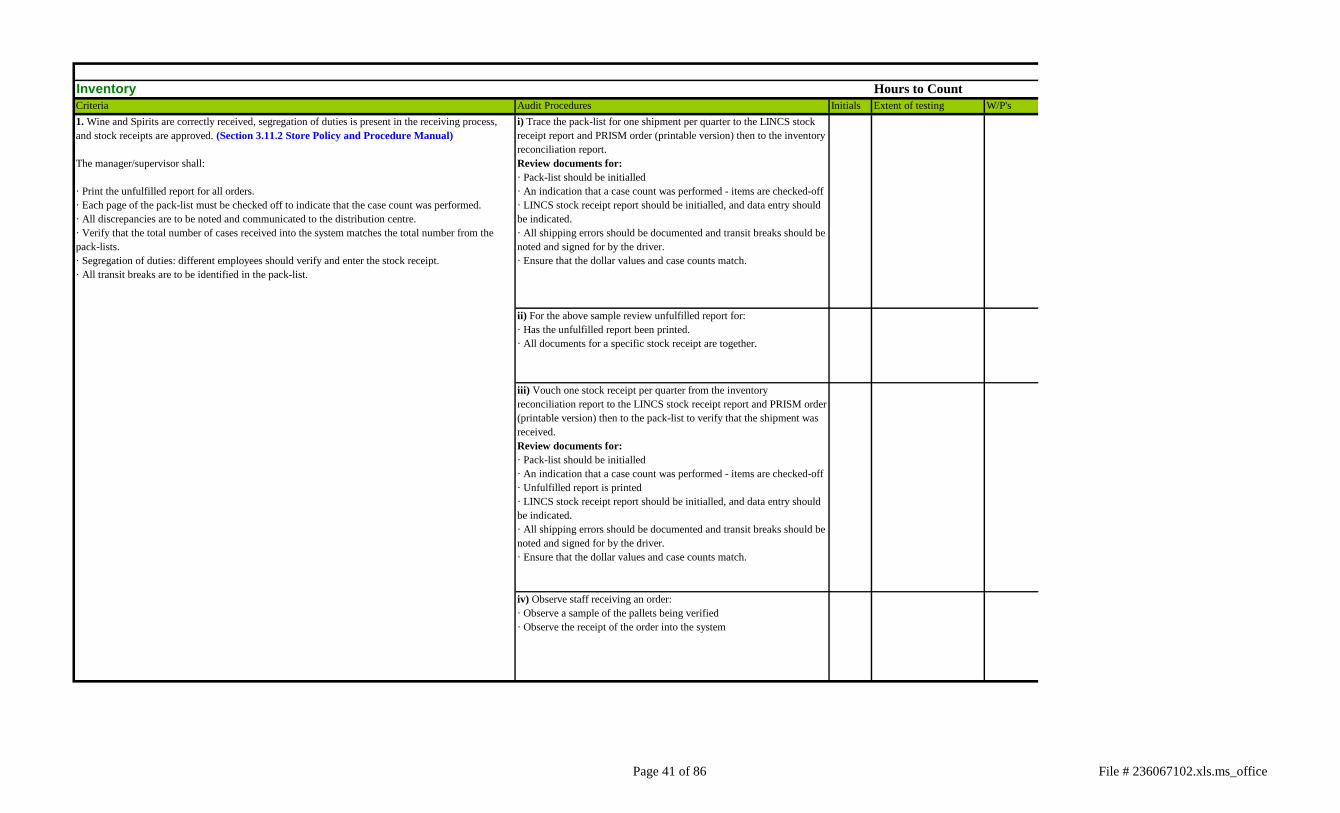

Inventory Hours to Count

Criteria Audit Procedures Initials Extent of testing W/P's

i) Trace the pack-list for one shipment per quarter to the LINCS stock

receipt report and PRISM order (printable version) then to the inventory

reconciliation report.

Review documents for:

· Pack-list should be initialled

· An indication that a case count was performed - items are checked-off

· LINCS stock receipt report should be initialled, and data entry should

be indicated.

· All shipping errors should be documented and transit breaks should be

noted and signed for by the driver.

· Ensure that the dollar values and case counts match.

ii) For the above sample review unfulfilled report for:

· Has the unfulfilled report been printed.

· All documents for a specific stock receipt are together.

iii) Vouch one stock receipt per quarter from the inventory

reconciliation report to the LINCS stock receipt report and PRISM order

(printable version) then to the pack-list to verify that the shipment was

received.

Review documents for:

· Pack-list should be initialled

· An indication that a case count was performed - items are checked-off

· Unfulfilled report is printed

· LINCS stock receipt report should be initialled, and data entry should

be indicated.

· All shipping errors should be documented and transit breaks should be

noted and signed for by the driver.

· Ensure that the dollar values and case counts match.

iv) Observe staff receiving an order:

· Observe a sample of the pallets being verified

· Observe the receipt of the order into the system

1. Wine and Spirits are correctly received, segregation of duties is present in the receiving process,

and stock receipts are approved. (Section 3.11.2 Store Policy and Procedure Manual)

The manager/supervisor shall:

· Print the unfulfilled report for all orders.

· Each page of the pack-list must be checked off to indicate that the case count was performed.

· All discrepancies are to be noted and communicated to the distribution centre.

· Verify that the total number of cases received into the system matches the total number from the

pack-lists.

· Segregation of duties: different employees should verify and enter the stock receipt.

· All transit breaks are to be identified in the pack-list.

Page 41 of 86 File # 236067102.xls.ms_office

Inventory Hours to Count

Criteria Audit Procedures Initials Extent of testing W/P's

1. Wine and Spirits are correctly received, segregation of duties is present in the receiving process,

and stock receipts are approved. (Section 3.11.2 Store Policy and Procedure Manual)

The manager/supervisor shall:

· Print the unfulfilled report for all orders.

· Each page of the pack-list must be checked off to indicate that the case count was performed.

· All discrepancies are to be noted and communicated to the distribution centre.

· Verify that the total number of cases received into the system matches the total number from the

pack-lists.

· Segregation of duties: different employees should verify and enter the stock receipt.

· All transit breaks are to be identified in the pack-list.

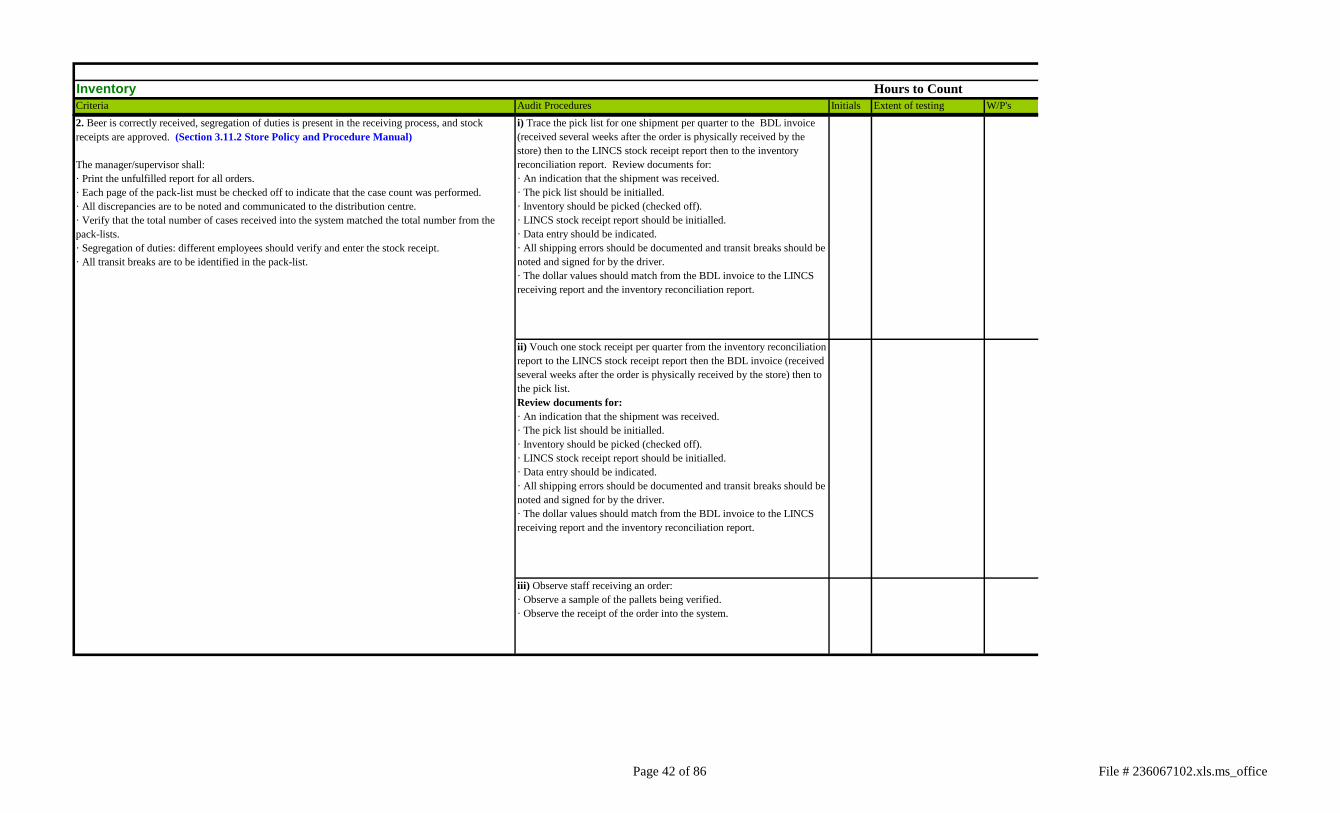

i) Trace the pick list for one shipment per quarter to the BDL invoice

(received several weeks after the order is physically received by the

store) then to the LINCS stock receipt report then to the inventory

reconciliation report. Review documents for:

· An indication that the shipment was received.

· The pick list should be initialled.

· Inventory should be picked (checked off).

· LINCS stock receipt report should be initialled.

· Data entry should be indicated.

· All shipping errors should be documented and transit breaks should be

noted and signed for by the driver.

· The dollar values should match from the BDL invoice to the LINCS

receiving report and the inventory reconciliation report.

ii) Vouch one stock receipt per quarter from the inventory reconciliation

report to the LINCS stock receipt report then the BDL invoice (received

several weeks after the order is physically received by the store) then to

the pick list.

Review documents for:

· An indication that the shipment was received.

· The pick list should be initialled.

· Inventory should be picked (checked off).

· LINCS stock receipt report should be initialled.

· Data entry should be indicated.

· All shipping errors should be documented and transit breaks should be

noted and signed for by the driver.

· The dollar values should match from the BDL invoice to the LINCS

receiving report and the inventory reconciliation report.

iii) Observe staff receiving an order:

· Observe a sample of the pallets being verified.

· Observe the receipt of the order into the system.

2. Beer is correctly received, segregation of duties is present in the receiving process, and stock

receipts are approved. (Section 3.11.2 Store Policy and Procedure Manual)

The manager/supervisor shall:

· Print the unfulfilled report for all orders.

· Each page of the pack-list must be checked off to indicate that the case count was performed.

· All discrepancies are to be noted and communicated to the distribution centre.

· Verify that the total number of cases received into the system matched the total number from the

pack-lists.

· Segregation of duties: different employees should verify and enter the stock receipt.

· All transit breaks are to be identified in the pack-list.

Page 42 of 86 File # 236067102.xls.ms_office

Inventory Hours to Count

Criteria Audit Procedures Initials Extent of testing W/P's

1. Wine and Spirits are correctly received, segregation of duties is present in the receiving process,

and stock receipts are approved. (Section 3.11.2 Store Policy and Procedure Manual)

The manager/supervisor shall:

· Print the unfulfilled report for all orders.

· Each page of the pack-list must be checked off to indicate that the case count was performed.

· All discrepancies are to be noted and communicated to the distribution centre.

· Verify that the total number of cases received into the system matches the total number from the

pack-lists.

· Segregation of duties: different employees should verify and enter the stock receipt.

· All transit breaks are to be identified in the pack-list.

i) Count 20% of the total store stock excluding allied products and

minitures, and 100% of the gift certificates. Utilize two tests to ensure

all physical stock is reported and all reported stock is physically present.

Count an additional 10% of the stock in any product category where

30% or more of the counted SKU's have a variance. Review the service

level report for negative inventory amounts (these are to be verified and

corrected). All variances are to be verified by an employee of the store

(preferably the manager).

ii) Summarize the count variances and have a store employee adjust the

perpetual inventory records (obtain a copy of the signed LINCS

adjustment report for the audit file).

iii) Observe the adjustment process ensuring:

· Adjustments are verified prior to being saved.

· The LINCS adjustment reports are initialled to indicate who

performed/approved the adjustment.

i) Review the Stock Over/Short information on the LINCS "Store

Inventory GL Adjustment" report for an indication of when the last four

inventory counts have been performed.

· Review count sheets of most recent count to determine when they were

printed.

· Discuss with manager to ensure they have been conducting inventory

counts quarterly.

ii) For the most recent count, review the count sheets for accuracy and

completion.

iii) For the sample same as ii) above, review the count sheets for an

indication that they were reviewed by a second employee (document in

the audit file).

iv) Review the count procedures with the store manager:

· Employees should be rotated (not count the same section every count,

and manager should determine who counts each section).

· A structured procedure should be followed to ensure inventory is not

missed during the count.

· Cases in the warehouse should be marked when they are counted.

· All counts are to be recorded using ink.

3. Verify Wine/Spirits, Beer inventory.

4. Quarterly inventory counts are conducted. (Section 3.11.7 Store Policy and Procedure Manual)

· Counts shall be completed in periods 3, 6, 9, and 13 (year end).

· All cases counted in the warehouse shall be marked.

· Have a structured process to ensure that inventory is not missed in the count.

· All variances must be verified by another employee.

· Counts must be recorded in ink.

· Corrections have a line drawn through the original count with the correction written above or to the

side.

· Extensions are to be rechecked by another employee.

· Count sheets must be signed by the counter and verifier.

· A different employee enters the variances.

· All documents must be retained.

Page 43 of 86 File # 236067102.xls.ms_office

Inventory Hours to Count

Criteria Audit Procedures Initials Extent of testing W/P's

1. Wine and Spirits are correctly received, segregation of duties is present in the receiving process,

and stock receipts are approved. (Section 3.11.2 Store Policy and Procedure Manual)

The manager/supervisor shall:

· Print the unfulfilled report for all orders.

· Each page of the pack-list must be checked off to indicate that the case count was performed.

· All discrepancies are to be noted and communicated to the distribution centre.

· Verify that the total number of cases received into the system matches the total number from the

pack-lists.

· Segregation of duties: different employees should verify and enter the stock receipt.

· All transit breaks are to be identified in the pack-list.

v) Trace the adjustments of the latest count from the count sheets to the

inventory adjustment report to ensure they have been completed

properly. Review adjustment report for approval, review the Store

Inventory GL Adjustment report to ensure the adjustment was saved

(adjustment report can be printed without saving/adjusting the

inventory).

i) Discuss the process with the manager and employees.

ii) Vouch the adjustments for the two most recent reports from the Store

Inventory GL Adjustment report to the original LINCS adjustment

report then to the original disposition report to ensure accuracy and

completion.

iii) For the sample noted above, review the disposition form for an

indication that the manager approved the disposition.

iv) For the sample noted above:

· Ensure the correct codes are utilized

· Customer complaint forms are present for returns

· Empty containers have been returned to inventory (beer) verify using

the clerk audaction report.

v) Review the original disposition reports for one period from each of

the previous three quarters (current quarter has been examined above).

Review the reports for:

· The presence of two signatures.

· Quantities are written alphabetically.

· Unused lines are crossed out to prevent additional items being added.

· Transit breaks are signed for by a representative of the transport

company.

· If possible an employee not involved in the disposition up-dates the

inventory.

5. Product dispositions are accurate, correctly documented and authorized. (Section 3.11.5 Store

Policy and Procedure Manual)

· Destruction of non-saleable stock is conducted in the presence of the store manager or designate and

one other employee of the store.

· Signature of 2 employees destroying the product.

· A different employee shall up-date the inventory system (signature required).

· Correct codes are utilized.

· Proper descriptions are utilized.

· Quantities are written alphabetically.

· Unused lines are struck through.

· Empty containers are returned to inventory (beer).

· Customer complaint forms are completed and attached.

· Drivers signature for transit breaks.

4. Quarterly inventory counts are conducted. (Section 3.11.7 Store Policy and Procedure Manual)

· Counts shall be completed in periods 3, 6, 9, and 13 (year end).

· All cases counted in the warehouse shall be marked.

· Have a structured process to ensure that inventory is not missed in the count.

· All variances must be verified by another employee.

· Counts must be recorded in ink.

· Corrections have a line drawn through the original count with the correction written above or to the

side.

· Extensions are to be rechecked by another employee.

· Count sheets must be signed by the counter and verifier.

· A different employee enters the variances.

· All documents must be retained.

Page 44 of 86 File # 236067102.xls.ms_office

Inventory Hours to Count

Criteria Audit Procedures Initials Extent of testing W/P's

1. Wine and Spirits are correctly received, segregation of duties is present in the receiving process,

and stock receipts are approved. (Section 3.11.2 Store Policy and Procedure Manual)

The manager/supervisor shall:

· Print the unfulfilled report for all orders.

· Each page of the pack-list must be checked off to indicate that the case count was performed.

· All discrepancies are to be noted and communicated to the distribution centre.

· Verify that the total number of cases received into the system matches the total number from the

pack-lists.

· Segregation of duties: different employees should verify and enter the stock receipt.

· All transit breaks are to be identified in the pack-list.

i) Review transfer in's for one week per quarter for a total of four weeks.

· Vouch transfer in's from the inventory reconciliation report to the

original transfer in document.

· Ensure there is a checkmark to indicate that all products were picked.

· Ensure the value matches that on the inventory reconciliation.

ii) For the above sample:

· Ensure that the transfer in is attached to the originating store's transfer

out and any associated shipping documentation.

· The receiving store signs for the goods received and documents any

damages/missing products.

iii) Review transfer out's for one week per quarter for a total of four

weeks.

· Vouch transfer out's from the inventory reconciliation report to the

original transfer out document. Review for an indication that:

· The product was verified by a second employee

· A completed bill of lading is attached to the transfer out

· The value matches that on the inventory reconciliation.

7. In-Store Adjustments are documented and correctly authorized. (Section 3.11.6 Store Policy and

Procedure Manual)

· Authorized and signed by the manager.

· A separate file is maintained for in-store adjustments (filed with period 13).

· A second employee shall verify all adjustments prior to updating.

· A detailed explanation must be provided.

i) Review all in-store adjustments for the current and previous 12 fiscal

periods.

· Vouch the adjustments from the Store Inventory GL Adjustment report

to the LINCS inventory adjustment report.

· Observe for manager approval, a detailed explanation, proper use, and

adequate filing.

i) Discuss these issues with the manager.

ii) During the course of the audit observe the doors and entrances of the

warehouse to ensure they are kept closed during business hours. Also

ensure that all persons in the warehouse are authorized SLGA employee

or are accompanied by SLGA staff.

iii) While observing the receipt of inventory observe if the inventory is

verified before it is signed for.

6. All transfers are verified, authorized, and correctly up-dated. (Section 3.11.3, and 3.11.4 Store

Policy and Procedure Manual)

· Inventory is picked off on the transfer in form.

· A second employee must enter the transfer into the system.

· Transfer in must be compared to the transfer out from the sending store (units and dollar value must

match).

· Employee verifying inventory must initial transfer in form.

· All transfer out's must be verified by a second employee prior to shipping.

· An employee not involved in the assembly or verification should enter the transfer into the system.

8. The Manager/Supervisor shall ensure adequate controls are implemented to protect inventory.

(Section 3.11.8 Store Policy and Procedure Manual)

Manager / Supervisor responsibilities include:

· ensuring that all inventory activities are segregated in multi staff stores

· all doors and entrances to the warehouse shall be kept closed during business hours

· access to the warehouse shall be restricted to authorized SLGA employees

· all orders greater than 12 units are checked by a second employee in multi staff stores

· ensure all merchandise is present prior to signing for it

· all partially filled cases in the warehouse are to be adequately identified

Page 45 of 86 File # 236067102.xls.ms_office

Inventory Hours to Count

Criteria Audit Procedures Initials Extent of testing W/P's

1. Wine and Spirits are correctly received, segregation of duties is present in the receiving process,

and stock receipts are approved. (Section 3.11.2 Store Policy and Procedure Manual)

The manager/supervisor shall:

· Print the unfulfilled report for all orders.

· Each page of the pack-list must be checked off to indicate that the case count was performed.

· All discrepancies are to be noted and communicated to the distribution centre.

· Verify that the total number of cases received into the system matches the total number from the

pack-lists.

· Segregation of duties: different employees should verify and enter the stock receipt.

· All transit breaks are to be identified in the pack-list.

i) Discuss with the manager the process used to reconcile the perpetual

inventory of empty containers. For two shipments per quarter review

the reconciliation records maintained by the store.

ii) Discuss with the manager the process utilized for the end of day

reconciliation of empty container slips, as well as the filing of empty

container slips.

iii) Discuss with the manager the process used to reconcile the empty

container slips to the dollar value paid out to customers. Review one

reconciliation per quarter.

iv) For one day per quarter review the empty container return slips for

an indication of employee and customer signatures.

9. Empty container inventory is verified and source documents are maintained. (Section 3.7.8 Store

Policy and Procedure Manual)

· A container return slip must be completed for each container return customer.

· Container returns are correctly and accurately recorded, and the perpetual inventory must be

reconciled after each shipment.

· The Manager or designate shall reconcile the total number of slips and total $ value paid out by each

cashier at least once every two weeks.

· Cashiers must maintain all container return slips presented to them for end of day reconciliation.

· All container return slips must be signed by the customer.

· Employee accepting the containers must initial the return slip.

Page 46 of 86 File # 236067102.xls.ms_office

Store Audit Program

Hours to complete Inventory Field Work

Comments

Page 47 of 86 File # 236067102.xls.ms_office

Store Audit Program

Hours to complete Inventory Field Work

Comments

Page 48 of 86 File # 236067102.xls.ms_office

Store Audit Program

Hours to complete Inventory Field Work

Comments

Page 49 of 86 File # 236067102.xls.ms_office

Store Audit Program

Hours to complete Inventory Field Work

Comments

Page 50 of 86 File # 236067102.xls.ms_office

Store Audit Program

Hours to complete Inventory Field Work

Comments

Page 51 of 86 File # 236067102.xls.ms_office

Store Audit Program

Hours to complete Inventory Field Work

Comments

Page 52 of 86 File # 236067102.xls.ms_office

Wine and Spirits Stock Receipts Audit Working Papers

LINCS

Period/Date

Vouched/Tra

ced Initialled

Items Checked-

Off*

Receiving Report

Initialled Documented Signed by Driver

Unfulfilled Report

is Printed

Prism Report

Printed

Data Entry

Stamp**

Shipping Errors

Documented

Case Count

Agrees***

Dollar Value

Agrees*** Notes

Notes:

*- It is no longer a requirement to pick each item, however this is meant to document this function if it is performed.

Pack List Transit Breaks

Unfulfilled report is not signed to indicate data entry as no other reports will match ($ and units) if it is not entered, and once you open the order you can tell if the unfulfilled items have been entered as it identifies ordered and shipped quantities which

eliminats the chance of double entry. An indication of data entry may save time.

***-Vouch from the LINCS Stock Receipt Report to the PRISM report to the Pack List (dollar value from Prism report to LINCS report).

** - This should be found on the top page of the order so it is in plain view to prevent the order from being entered twice.

***-Trace from the Pack List to the PRISM Report to the LINCS Stock Receipt Report (dollar value from Prism report to LINCS report).

File # 236067102.xls.ms_office

Wine and Spirits Stock Receipts Audit Working Papers

*- It is no longer a requirement to pick each item, however this is meant to document this function if it is performed.

***-Vouch from the LINCS Stock Receipt Report to the PRISM report to the Pack List (dollar value from Prism report to LINCS report).

** - This should be found on the top page of the order so it is in plain view to prevent the order from being entered twice.

***-Trace from the Pack List to the PRISM Report to the LINCS Stock Receipt Report (dollar value from Prism report to LINCS report).

File # 236067102.xls.ms_office

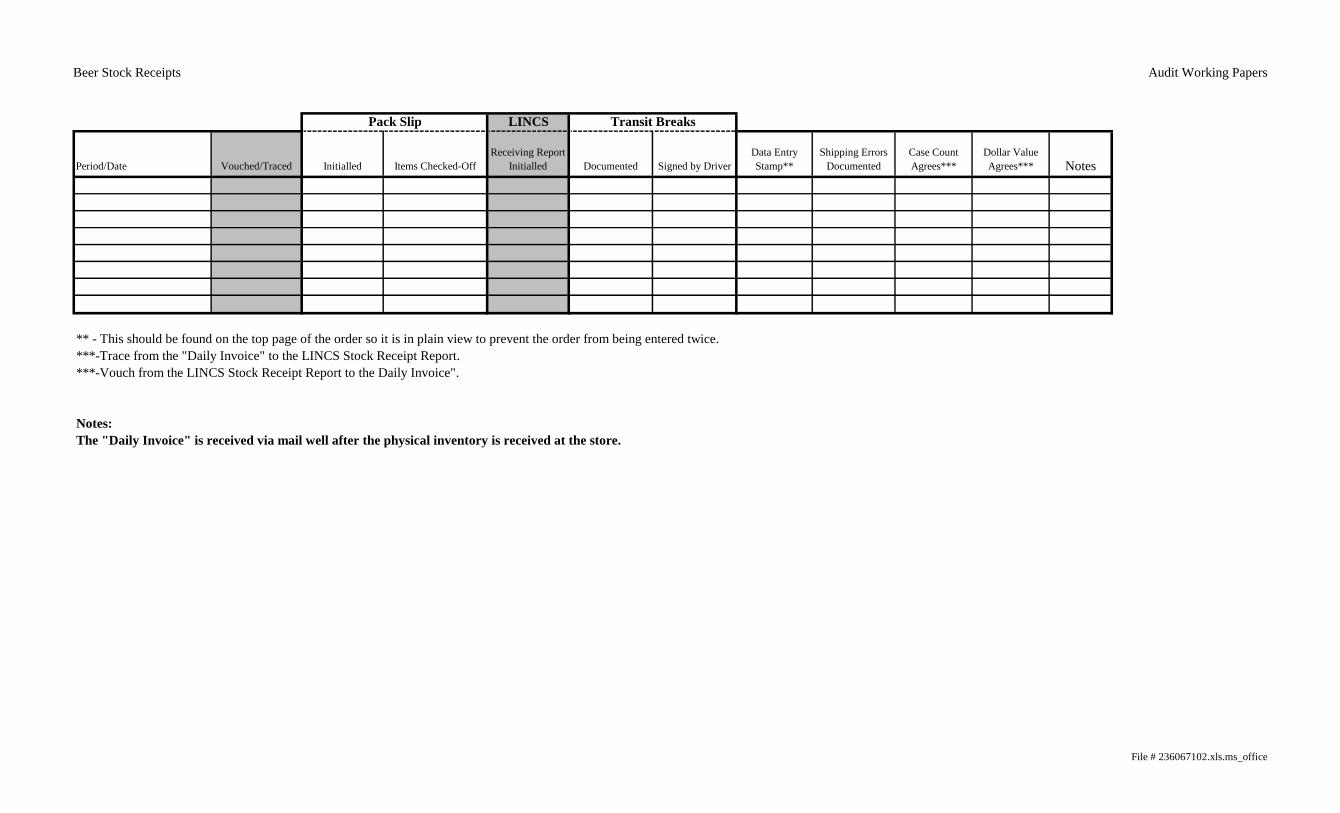

Beer Stock Receipts Audit Working Papers

LINCS

Period/Date Vouched/Traced Initialled Items Checked-Off

Receiving Report

Initialled Documented Signed by Driver

Data Entry

Stamp**

Shipping Errors

Documented

Case Count

Agrees***

Dollar Value

Agrees*** Notes

Notes:

***-Vouch from the LINCS Stock Receipt Report to the Daily Invoice".

Pack Slip Transit Breaks

** - This should be found on the top page of the order so it is in plain view to prevent the order from being entered twice.

***-Trace from the "Daily Invoice" to the LINCS Stock Receipt Report.

The "Daily Invoice" is received via mail well after the physical inventory is received at the store.

File # 236067102.xls.ms_office

Transfers Audit Working Papers

Period/Date Transfer In/Out

Source Doc.

Present

Inventory

Picked

Inventory

Signed for Documented Signed by Driver

Bill of Lading

Attached

Verified by

Second Emp. Notes

4/July 12, 2004

4/July 9, 2004

4/July 7, 2004

4/July 10, 2004

4/July 17, 2004

4/July 6, 2004

4/July 17, 2004

3/May 25, 2004

3/May 25, 2004

3/June 3, 2004

3/May 29, 2004

3/May 23, 2004

Notes:

T-Out's

Reference #

Transit Breaks

Dollar Values

match Inventory

Recon.

File # 236067102.xls.ms_office

Transfers Audit Working Papers

File # 236067102.xls.ms_office

Dispositions Audit Working Papers

Period/Date Reference # Correct codes Used

Complaint forms

attached

Empties returned to

inv. (beer)

2 Signatures for

destruction

Quantities recorded

alphabetically

Unused lines crossed

out

T-breaks signed by

Driver*

LINCS Inventory

adj report initialled

Molson

voucher

processed

correctly

Proper Segregation

of Duties Notes

* Driver required to sign shipping documents with damage outlined.

Notes:

Period/Date Reference #

2 Signatures for

destruction

Quantities

recorded

alphabetically

Unused lines

crossed out

T-breaks signed by

Driver*

LINCS Inventory adj

report initialled

Proper Segregation of

Duties Notes

* Driver required to sign shipping documents with damage outlined.

Notes:

Dispositions - One period for each of the previous 3 quarters

Dispositions - 2 most recent

File # 236067102.xls.ms_office

Count Sheets Audit Working Papers

Period/Date

Variances verified

by a second

employee

Counter signs all

sheets

Count recorded in

ink

Mistakes crossed out

with a line

Proper Segregation of

Duties

Accuracy of

extensions All products counted Notes

Notes:

File # 236067102.xls.ms_office

In-store Adjustments Audit Working Papers

Date Reference # Correctly Used

LINCS Adjustment report

present

LINCS report authorized

and signed by the MGR

Second person reviewed

the adjustment

Detailed explanation

provided

Stored in a separate file

and filed with period 13

records Notes

Notes:

Instore Adjustments - All from current and 12 previous fiscal periods2 most recent

File # 236067102.xls.ms_office

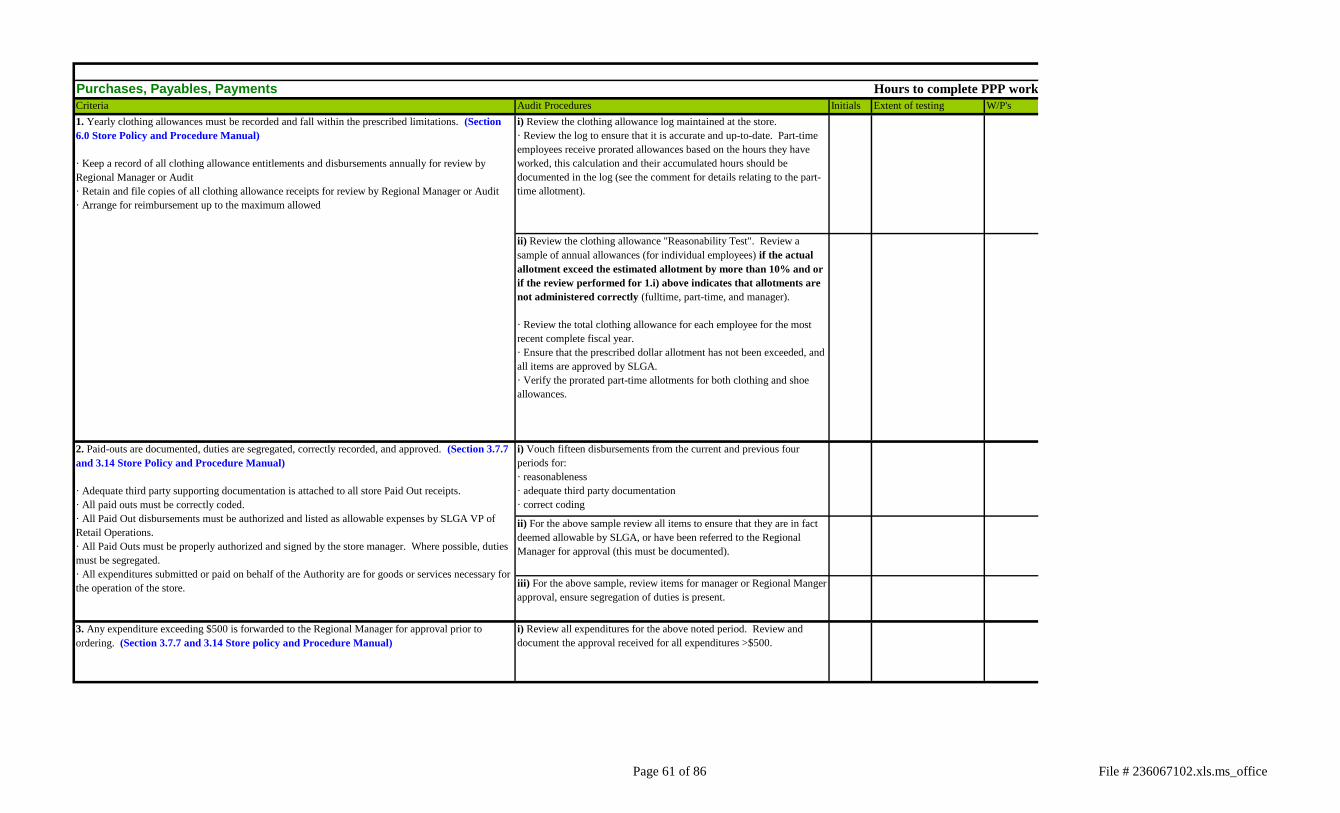

Purchases, Payables, Payments

Criteria Audit Procedures Initials Extent of testing W/P's

i) Review the clothing allowance log maintained at the store.

· Review the log to ensure that it is accurate and up-to-date. Part-time

employees receive prorated allowances based on the hours they have

worked, this calculation and their accumulated hours should be

documented in the log (see the comment for details relating to the part-

time allotment).

ii) Review the clothing allowance "Reasonability Test". Review a

sample of annual allowances (for individual employees) if the actual

allotment exceed the estimated allotment by more than 10% and or

if the review performed for 1.i) above indicates that allotments are

not administered correctly (fulltime, part-time, and manager).

· Review the total clothing allowance for each employee for the most

recent complete fiscal year.

· Ensure that the prescribed dollar allotment has not been exceeded, and

all items are approved by SLGA.

· Verify the prorated part-time allotments for both clothing and shoe

allowances.

i) Vouch fifteen disbursements from the current and previous four

periods for:

· reasonableness

· adequate third party documentation

· correct coding

ii) For the above sample review all items to ensure that they are in fact

deemed allowable by SLGA, or have been referred to the Regional

Manager for approval (this must be documented).

iii) For the above sample, review items for manager or Regional Manger

approval, ensure segregation of duties is present.

3. Any expenditure exceeding $500 is forwarded to the Regional Manager for approval prior to

ordering. (Section 3.7.7 and 3.14 Store policy and Procedure Manual)

i) Review all expenditures for the above noted period. Review and

document the approval received for all expenditures >$500.

2. Paid-outs are documented, duties are segregated, correctly recorded, and approved. (Section 3.7.7

and 3.14 Store Policy and Procedure Manual)

· Adequate third party supporting documentation is attached to all store Paid Out receipts.

· All paid outs must be correctly coded.

· All Paid Out disbursements must be authorized and listed as allowable expenses by SLGA VP of

Retail Operations.

· All Paid Outs must be properly authorized and signed by the store manager. Where possible, duties

must be segregated.

· All expenditures submitted or paid on behalf of the Authority are for goods or services necessary for

the operation of the store.

Hours to complete PPP work.

1. Yearly clothing allowances must be recorded and fall within the prescribed limitations. (Section

6.0 Store Policy and Procedure Manual)

· Keep a record of all clothing allowance entitlements and disbursements annually for review by

Regional Manager or Audit

· Retain and file copies of all clothing allowance receipts for review by Regional Manager or Audit

· Arrange for reimbursement up to the maximum allowed

Page 61 of 86 File # 236067102.xls.ms_office

4. Purchases are obtained at the best value for SLGA. (Section 3.14 Store policy and Procedure

Manual)

· Price comparisons must be done for goods or services >$50 and <$500.

· Bid comparisons must be attached to invoices for disbursements >$300.

· All required expenditures >$2,500 must be forwarded to SLGA Management Services for

Quotes/Tender/RFP.

i) Review all expenditures for the above noted period. Review and

document the presence of bid comparisons for disbursements >$300.

5. All cellular phones are authorized and correctly processed. (Section 3.14 Store policy and

Procedure Manual)

· All cellular phone purchases and contracts must be approved by the Regional Manager.

· All cellular phone bills are to be forwarded to the Regional Manager for approval and payment.

i) Review all expenditures for the above period for an indication of

disbursements relating to cellular phones. Ensure all cellular phone

invoices are forwarded to H.O. for payment.

6. Paid outs must be processed timely. (Section 3.14 Store policy and Procedure Manual)

· Paid outs must not be processed in advance.

i) For the sample noted in 2. compare the actual payment date on the

third party supporting documentation to the date the paid out was

processed at the store. All payments must be made prior to or on the

same day they have been processed at the store.

Page 62 of 86 File # 236067102.xls.ms_office

Store Audit Program

Comments

Hours to complete PPP work.

Page 63 of 86 File # 236067102.xls.ms_office

Page 64 of 86 File # 236067102.xls.ms_office

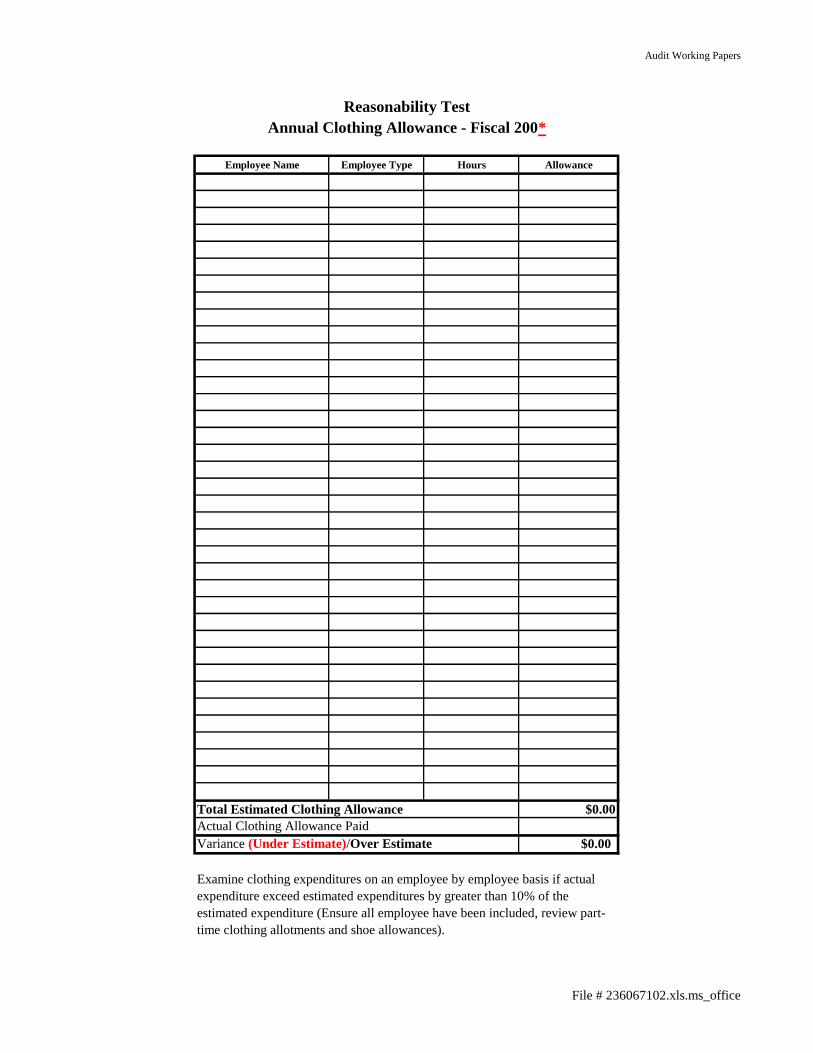

Audit Working Papers

Employee Name Employee Type Hours Allowance

$0.00

$0.00

Reasonability Test

Annual Clothing Allowance - Fiscal 200*

Examine clothing expenditures on an employee by employee basis if actual

expenditure exceed estimated expenditures by greater than 10% of the

estimated expenditure (Ensure all employee have been included, review part-

time clothing allotments and shoe allowances).

Total Estimated Clothing Allowance

Actual Clothing Allowance Paid

Variance (Under Estimate)/Over Estimate

File # 236067102.xls.ms_office

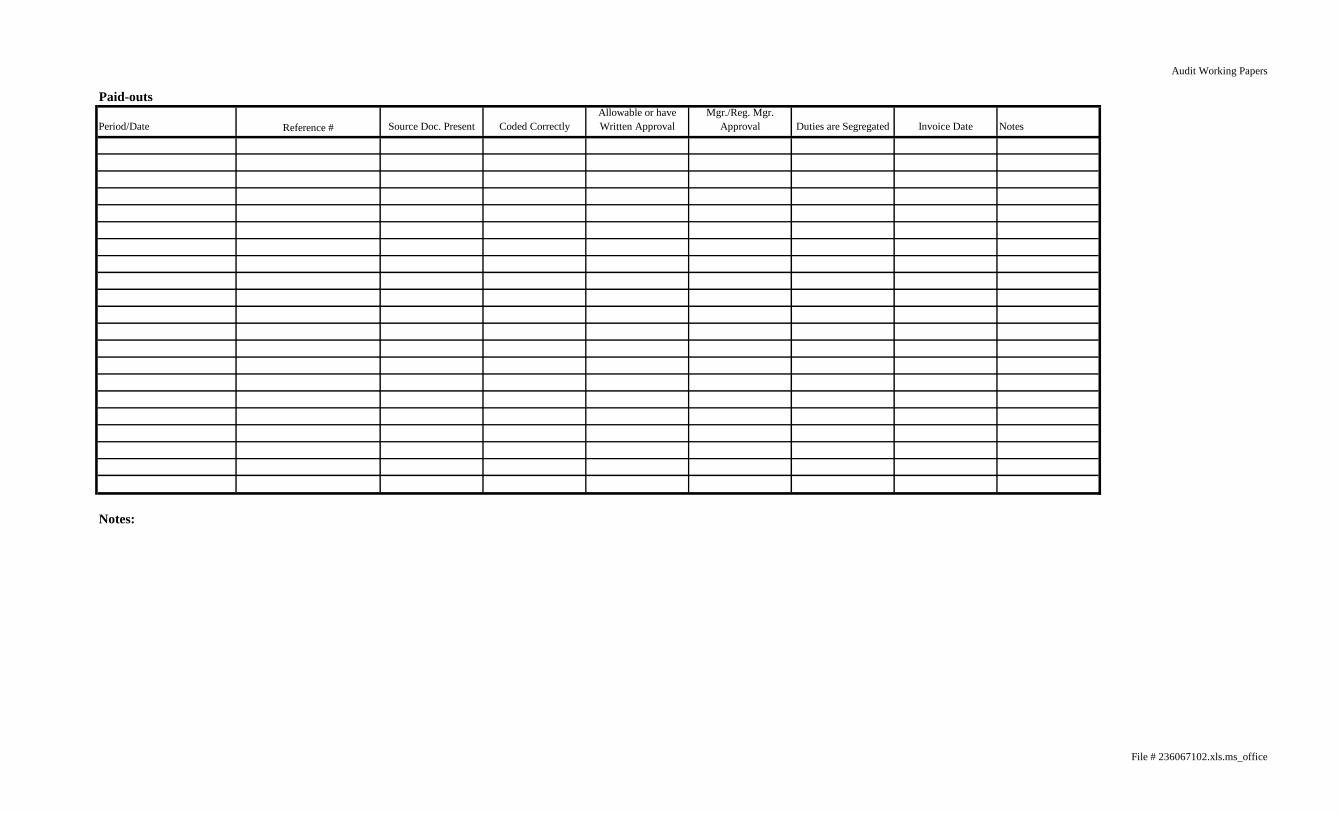

Audit Working Papers

Period/Date Source Doc. Present Coded Correctly

Allowable or have

Written Approval

Mgr./Reg. Mgr.

Approval Duties are Segregated Invoice Date Notes

Notes:

Paid-outs

Reference #

File # 236067102.xls.ms_office

Fixed Asset System

Criteria Audit Procedures Initials Extent of testing W/P's

i) Review the transfers and requisitions in the audit period to ensure

completeness and approval.

ii) Verify assets at the store to a printout of the Assets maintained on the

Head Office Fixed asset system.

· As with the alcohol inventory trace 1/2 of your sample from the floor

to the sheet, and the other half from the sheet to the floor.

i) Review the past four quarterly budget variance reports for:

· An indication that the manager reviewed and followed-up the reports.

· Include a copy of the most recent report in the audit file.

ii) Discuss this review with the manager - document what the manager

is looking for during the review.

1. Equipment Transfers and Requisitions are properly authorized. (Section 3.17 Store Policy

Manual)

2. Store Manager reviews the budget variance report for capital expenditures. (Section 3.17 Store

Policy Manual)

Hours to complete Fixed Asset work.

Page 67 of 86 File # 236067102.xls.ms_office

Store Audit Program

Comments

Hours to complete Fixed Asset work.

Page 68 of 86 File # 236067102.xls.ms_office

Payroll

Criteria Audit Procedures Initials Extent of testing W/P's

i) Discuss Time and attendance processing procedures with the store

manager.

ii) For one week per quarter:

· Ensure Time and Attendance worksheets are approved by the

manager.

iii) For the sample above ensure all employees have signed the work

sheet (when possible, review the information for 5 employees).

iv) For the above sample review the work sheets for use of the data

entry stamp or another indication of data entry.

v) For two days per quarter, reconcile the Time and Attendance

worksheet to the time and attendance information recorded in TAMS

(document in the audit file).

2. Time and attendance corrections are documented and approved. (Section 3.16 Store Policy and

Procedure Manual)

· A correction form must be submitted to H.O. to change data after it has been confirmed.

· Correction forma must be signed by the manager.

i) For the same sample as 1.v) above, vouch all time and attendance

corrections from TAMS (review the "last updated" field for an

indication than payroll staff last adjusted data) to the time and

attendance correction form. Review for accuracy and approval.

1. Time and attendance is correctly recorded, and authorized by the manager and employee. (Section

3.16 Store Policy and Procedure Manual)

· All hours work are recorded on the worksheet.

· All time entry must be performed by the manager/supervisor/designate.

· Worksheet is reconciled to the information on the system.

· Data entry stamp is utilized.

· Worksheet is signed by the manager/supervisor that reconciled it to the system.

· All employees must sign the worksheet.

Hours to complete Payroll work.

Page 69 of 86 File # 236067102.xls.ms_office

Store Audit Program

Comments

Hours to complete Payroll work.

Page 70 of 86 File # 236067102.xls.ms_office

Audit Working Papers

Payroll

Period/Week

Approved By

Manager

Signed By

Employees

Indication of Data

Entry Reconciled to TAMS # Reviewed Vouched Proper Approval

Correct Codes

Utilized Notes

Notes:

Worksheets Corrections

File # 236067102.xls.ms_office

Security and Safety

Criteria Audit Procedures Initials Extent of testing W/P's

i) Discuss with supervisors/managers – ensure they control access to the

keys/money.

· Complete security check-list.

ii) Identify "blind spots" in retail area.

· Observe the retail area for ‘blind spots’.

· Discuss with staff to determine if there are any retail areas they could

not monitor from the tills – document discussions in the audit file.

· Cash is not counted in public view.

· Alarm/system access codes are unique and confidential.

· Signs clearly identify areas not accessible to the public.

· Exterior doors not in use are locked at all times.

· Review POS security levels

· Review ISP security levels

i) Discuss with the manager.

ii) Observe and discuss the sale procedures and monitoring processes

for high risk products.

· High value products s/b in locked display cases or empty case/box s/b

on display and product s/b in the warehouse or office.

· Regular facings and counts s/b performed on high risk products during

the day.

· Shelf alarms and electronic tags can also be used.

i) Discuss with the manager.

ii) Print and review ISP and POS security levels, and ISP employee

master.

· No Sales must be restricted to manager/supervisor levels.

· Only managers/supervisors should be assigned the manager/supervisor

level of security.

i) Discuss with the manager.

ii) Complete safety check-list.

i) Discuss with the manager.

Hours to complete Security and Safety work.

3. Store manager designates the appropiate security levels on the ISP and POS. (Section 3.7.13 Store

Policy Manual, currently the Store Policy Manual does not address the ISP security levels)

· Manager will set POS security code to ensure that all No Sales require Manager/Supervisor

authorization.

· Only Managers/Supervisors should be assigned these levels of security

5. Gift certificates are secure and documented. (Currently not included in the Store Policy

Manual)

· Gift certificates are stored in a locked location.

· All gift certificates are recorded in a log.

· The gift certificate log is stored seperately from the gift certificates.

1. Store managers maintain at least the minimum standard of security requirements. (Section 3.1,

3.2, 3.4.1, 3.7.7, 3.13, 3.7.19, and 3.7.20 Store Policy Manual)

· Supervisors/managers control access to keys, money, store.

· Store manager maintains an unobstructed view of the retail area.

2. Store managers closely monitor the high value and high risk products. (Section 3.1 Store Policy

Manual)

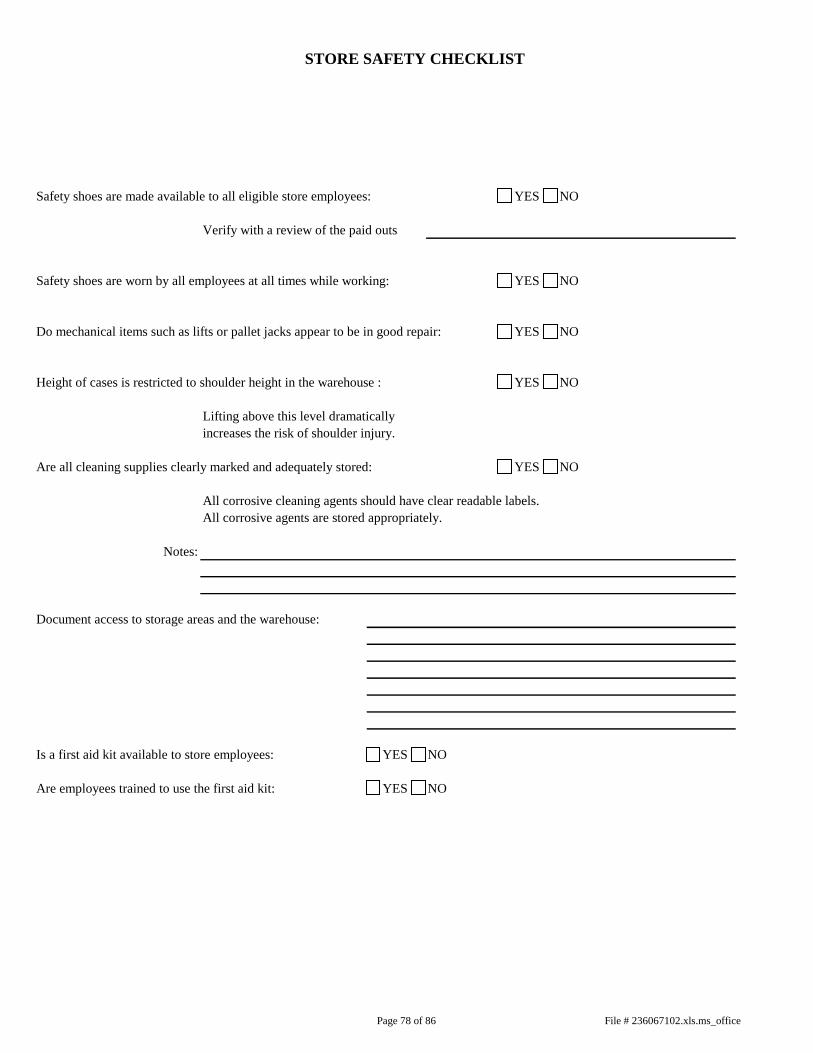

4. Store managers maintain at least the minimum standard of safety. (Section 3.3, and 6.0 Store

Policy Manual)

· Don't risk your safety during robberies.

· Don't pursue robbers.

· Wear CSA approved shoes at all times.

Page 72 of 86 File # 236067102.xls.ms_office

Security and Safety

Criteria Audit Procedures Initials Extent of testing W/P's

Hours to complete Security and Safety work.

1. Store managers maintain at least the minimum standard of security requirements. (Section 3.1,

3.2, 3.4.1, 3.7.7, 3.13, 3.7.19, and 3.7.20 Store Policy Manual)

· Supervisors/managers control access to keys, money, store.

· Store manager maintains an unobstructed view of the retail area.

ii) Over the course of the audit:

· Over the course of the audit, observe if the certificates are they

regularly left unlocked.

· Review the log to determine if it is up-to-date.

· Document the location of the log.

5. Gift certificates are secure and documented. (Currently not included in the Store Policy

Manual)

· Gift certificates are stored in a locked location.

· All gift certificates are recorded in a log.

· The gift certificate log is stored seperately from the gift certificates.

Page 73 of 86 File # 236067102.xls.ms_office

Store Audit Program

Comments

Hours to complete Security and Safety work.

Page 74 of 86 File # 236067102.xls.ms_office

Store Audit Program

Comments

Hours to complete Security and Safety work.

Page 75 of 86 File # 236067102.xls.ms_office

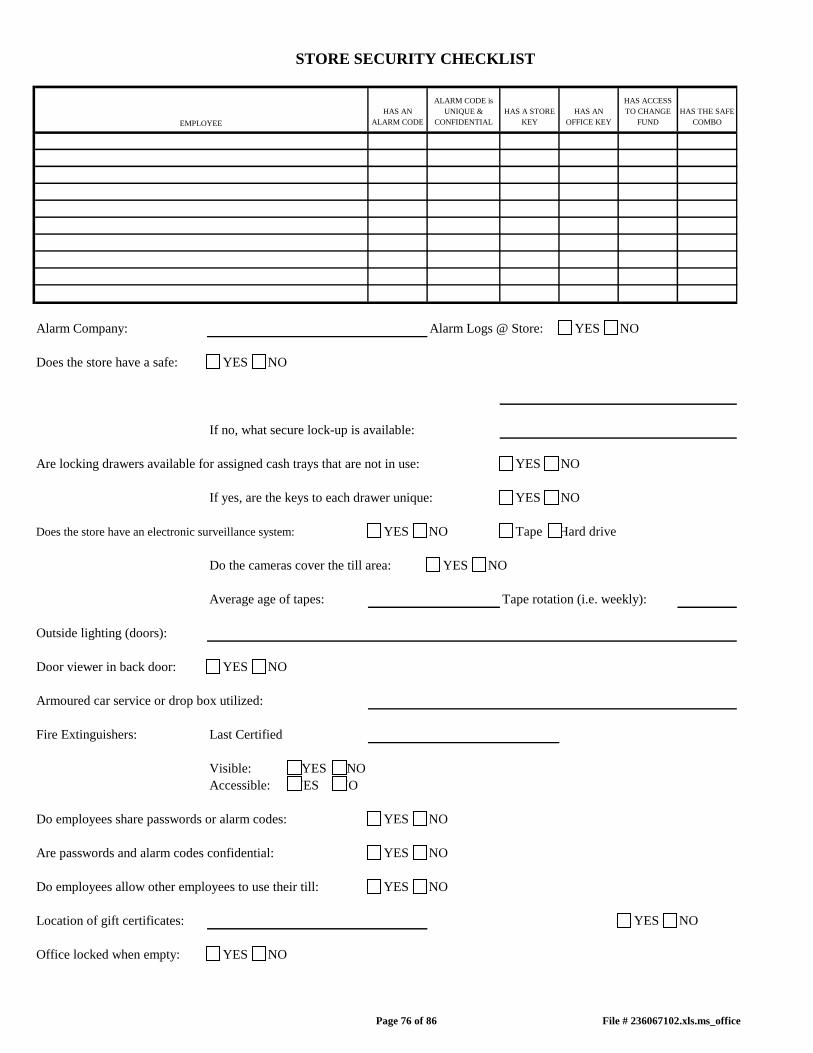

HAS AN

ALARM CODE

ALARM CODE is