restructuring of china railways: implications for...

TRANSCRIPT

The World Bank

Restructuring of China Railways: Implications for India?

Louis S. ThompsonRailways AdviserThe World BankMarch 1, 2002New Delhi, India

2The World Bank

General railway restructuring trends and issuesCurrent thinking in China – implications for India?Restructuring in Indian Railways:? Is the Chinese experience useful?? Is Indian restructuring necessary?? Options and choices? Getting started

Restructuring of Ministry of Railways of China: Implications for India?

3The World Bank

General railway restructuring trends and issues (1)

Separation of “Government” from Enterprise: MOT, not MORSpinoff of non-core activitiesEncouragement of competitionShifting the public/private balance: the public plans, provides social resources, private sector operates, sometimes under contract with public

4The World Bank

General railway restructuring trends and issues (2)

Clear separation of rail commercial functions –accounting and/or institutional? US and Canada: formation of Amtrak/VIA,

deregulation, restructuring of Conrail? EU: separation of infrastructure from services,

separation of services (freight, intercity passenger, “social passenger”), required contracts for social services, competition for contracts, removal of old debts

? Japan: separation of JR freight, creation of 6 passenger companies

? Similar process nearly everywhere

5The World Bank

Directions of Railway ChangePrivate Involvement

Stru

ctur

al C

hang

e

Mixtures and partnerships are possible!

Public Ownership

Partnerships: Concessions or Franchises Awarded Private Ownership

Integral

China, Russia and India (ministries), MAV, SRT, MZ, others, (SOE's)

Argentina (13), Brazil (9), Mexico (5), Peru (3), Guatemala, Bolivia (2), Panama, Cote d'Ivoire/Burkina Faso, Cameroon, Congo (Brazzaville), Malawi, Madagascar, Jordan

New Zealand, Ferronor (Chile), CVRD (Brazil), A&B (Chile)

Dominant Integral, Separated Minority Operators

Amtrak, VIA, Japan Freight

Mexico City suburban, CONCOR (India)

US Class I, CN and CP, East/West/Central Japan Railways

SeparationE.U. and Chile passenger

Swedish suburban, FEPASA (Chile), LHS line (Poland)

U.K. franchises and EWS, Polish and Romanian freight

6The World Bank

Current railway thinking in China – implications for

India: MOR’s Problems

Confusion of government and enterprise rolesGeographic organization causes? fragmentation of traffic and decisions (but ~60 percent of freight

moves inter Administration)? bureaucratic decisions (revenue distribution, wagon allocation)

made at the center ? 14+ points of management ? no competition in rail transport (>70% of freight)

Organization for production, not market? no Lines Of Business, no costing information? “command and control” mentality? no price mechanism (flat tariff structure)

Non-core distractions (e.g. factories, restaurants)Imposed social role (e.g. schools, hospitals)

7The World Bank

Lanzhou

Beijing

Jinan

Shanghai

Nanchang

Guangzh

ou

Kunming

Liuzhou

Zhengzhou

Wulumuqi

Chen

gdu

Huhehaote

Shenyan

g

Haerbin

Today:14 Administrations19.7 million wagons interchanged276.4 million passengers interchanged

Lanzhou

Beijing

Jinan

Shanghai

Nanchang

Guangzh

ou

Kunming

Liuzhou

Zhengzhou

Wulumuqi

Chen

gdu

Huhehaote

Shenyan

g

Haerbin

Today:14 Administrations19.7 million wagons interchanged276.4 million passengers interchanged

Organization of MOR today

8The World Bank

Broad change themes in ChinaSeparate MOR’s enterprise functions from its Government functions – eventual creation of an MOTRestructure the enterprisesMake the enterprises commercialSpin off all non-rail activities (manufacturing as well as social) and make them independent

9The World Bank

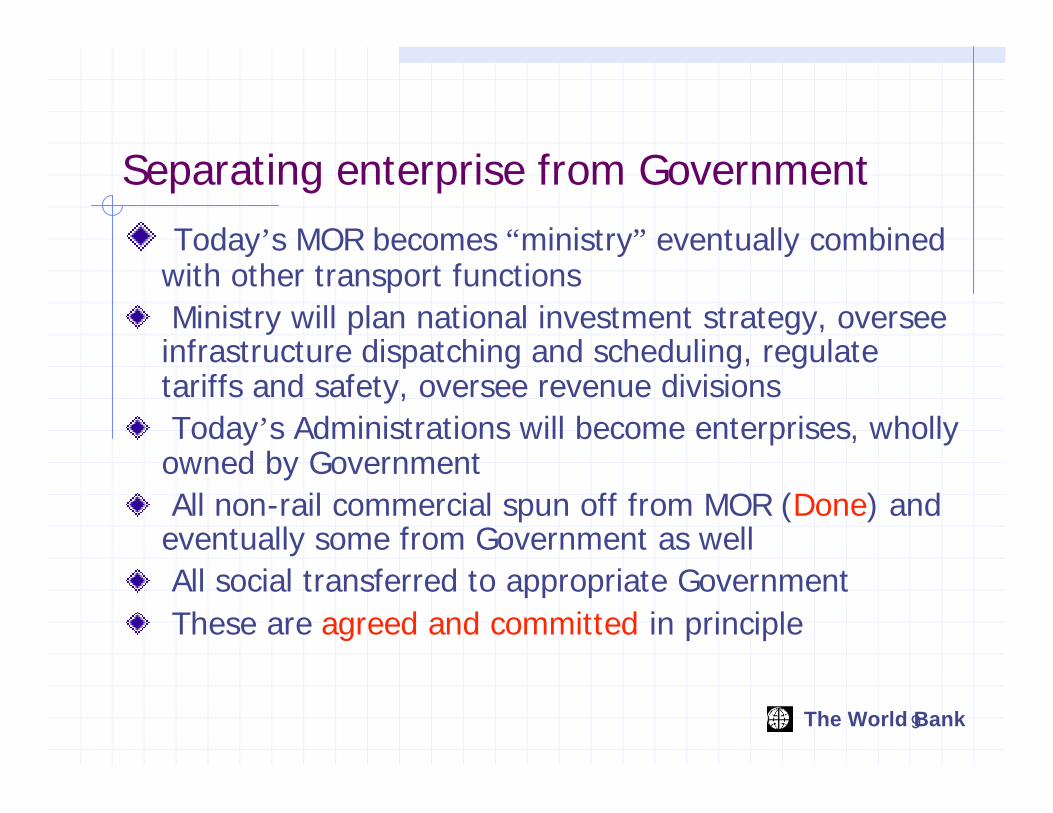

Separating enterprise from Government

Today’s MOR becomes “ministry” eventually combined with other transport functionsMinistry will plan national investment strategy, oversee infrastructure dispatching and scheduling, regulate tariffs and safety, oversee revenue divisionsToday’s Administrations will become enterprises, wholly owned by GovernmentAll non-rail commercial spun off from MOR (Done) and eventually some from Government as wellAll social transferred to appropriate GovernmentThese are agreed and committed in principle

10The World Bank

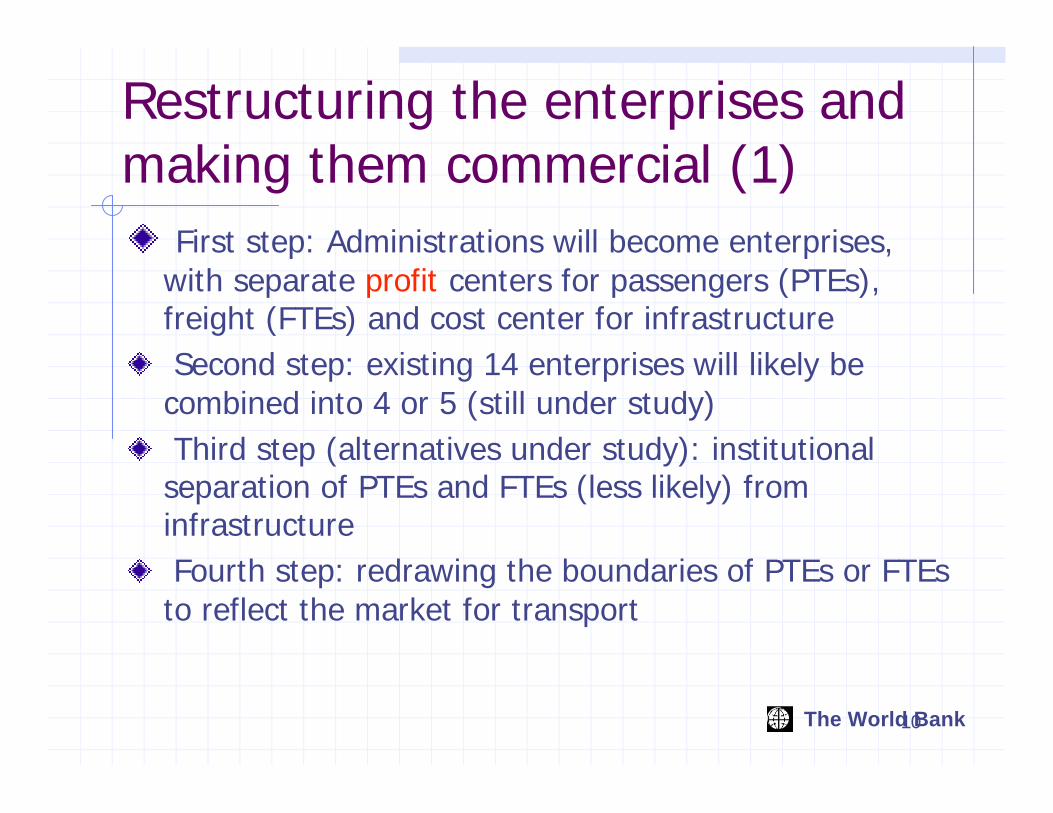

Restructuring the enterprises and making them commercial (1)

First step: Administrations will become enterprises, with separate profit centers for passengers (PTEs), freight (FTEs) and cost center for infrastructureSecond step: existing 14 enterprises will likely be combined into 4 or 5 (still under study)Third step (alternatives under study): institutional separation of PTEs and FTEs (less likely) from infrastructureFourth step: redrawing the boundaries of PTEs or FTEs to reflect the market for transport

11The World Bank

Percent of Rail Passenger Traffic to Total Rail TrafficP-Km/(P-km+T-Km)

0102030405060708090

100

CA

N

USA

ES

RU

SLVE

SLK

C

HIN

AFIN

CZ

PL

S A TU

R

RO

B

HU

D F IN

D

E I P UK

KO

R

DK

IR

L

NL

EL

JPN

FREIGHTDOMINANT

PASSENGERDOMINANT

“Balanced”

12The World Bank

Lanzhou

Beijing

Jinan

Shanghai

Nanchang

Guangzh

ou

Kunming

Liuzhou

Zhengzhou

Wulumuqi

Chen

gdu

Huhehaote

Shenyan

g

Haerbin

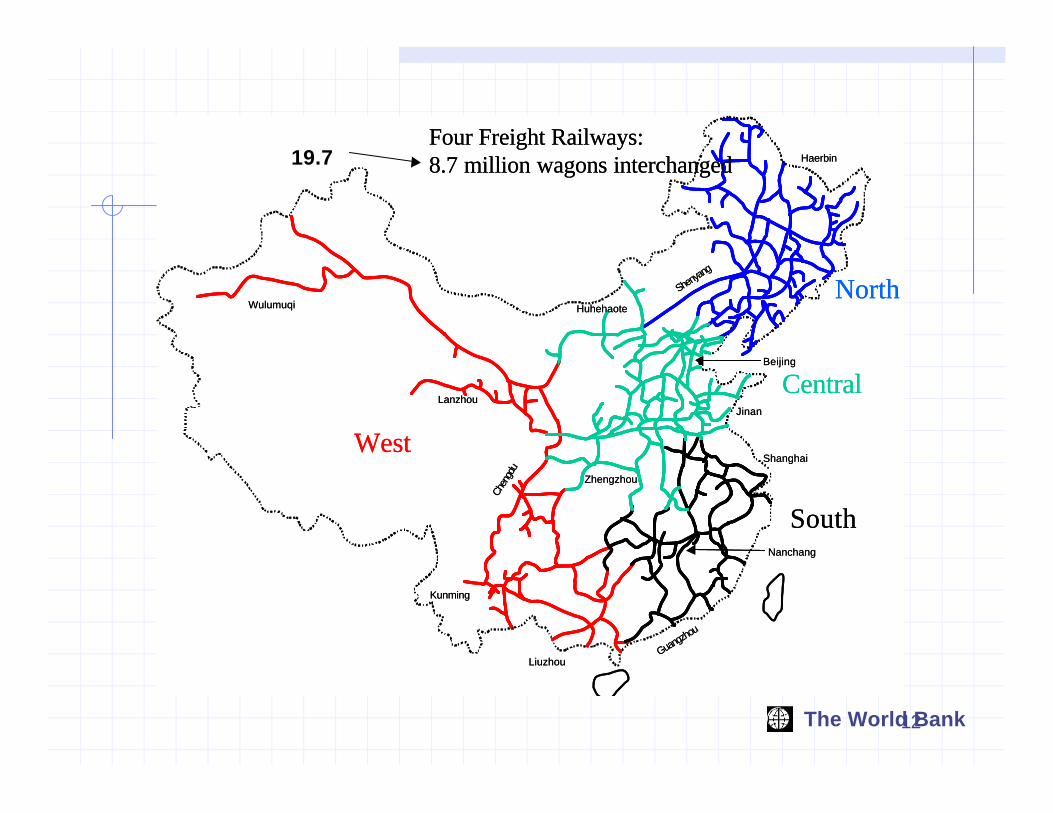

Four Freight Railways:8.7 million wagons interchanged

North

West

Central

South

Lanzhou

Beijing

Jinan

Shanghai

Nanchang

Guangzh

ou

Kunming

Liuzhou

Zhengzhou

Wulumuqi

Chen

gdu

Huhehaote

Shenyan

g

Haerbin

Four Freight Railways:8.7 million wagons interchanged

North

West

Central

South

19.7

13The World Bank

Restructuring the enterprises and making them commercial (2)

Create rail/rail competition by:? Trackage access rights? Redesign of service territory? Creating parallel tracks in selected markets? Creating source competition? There is debate on thisInvolve private sector by:(agreed measures)? Branch line ownership and operation (many)? Focused market operations (Guangshen) or

containers? Wagon ownership and leasing

14The World Bank

Jinan

Guangzh

ou

Lanzhou

Beijing

Shanghai

Nanchang

Kunming

Liuzhou

Zhengzhou

Wulumuqi

Chen

gdu

Huhehaote

Shenyan

g

Haerbin

Source Competition: 5 Administrations

Beijing jointly owned by the other four groups and operated as neutral connection

15The World Bank

MOR’s Restructuring:Issues and Approaches

Separation of enterprise and government -- establish an MOT, set up railways as enterprises, initially at Administration level

Commercial approach -- Line Of Business (LOB) organizations at all levels --freight, passenger companies,and related infrastructure

Rail enterprise structure -- full separation versus freight integral and passenger separation (US model) or fully integral models on 14 Administration or regrouped (5 Administration) basis

Market structure organization -- mergers of PTE’s and possibly FTE’s across Administration boundaries (infrastructure likely set up at Administration level, though other structures are possible)

Competition -- could have parallel/competitive infrastructure, but more likelywill be competitive trackage rights or source competition, if any

Private sector involvement -- non-core and local lines may be sold (Guangshen), private equipment ownership probable, specialized operators possible, generalized privatization not on the horizon (if ever)

Transition -- holding companies at the regrouped Administration level

Overall -- cautious, “experiment”-based approach, with many compromises and mixes (as always) – committed and unstoppable

16The World Bank

MOR Restructuring: AnalyticalTools for Evaluating Options

TMIS -- traffic, routing operating and revenue data (operational)Traffic costing models -- use basic data to estimate cost and “contribution” of traffic on shipment, commodity, line segment and area basis (operational)PC-based network models -- for traffic flow analysis (initial version operational)Next challenge: integrating TMIS data with costing and network models for rapid and accurate system analysisPC-based financial planning models -- to permit rapid analysis of cost and revenue scenarios

17The World Bank

Restructuring IR: is the Chinese approach relevant?

Similarities with China? Enterprise/Government role confusion -- politics? Regional monopoly structure, not market driven? Imposed social functions, large non-core activities

In other ways, India is different? Variations in Zonal characteristics ? Three gauges in India, one in China? Suburban operations (2000 trains daily)? Destructive freight-to-passenger cross subsidies? Much greater deferred maintenance, especially wagons

Clearly, India will need its own mix of ideas

18The World Bank

Is Indian Railway restructuring necessary? The Mohan Report

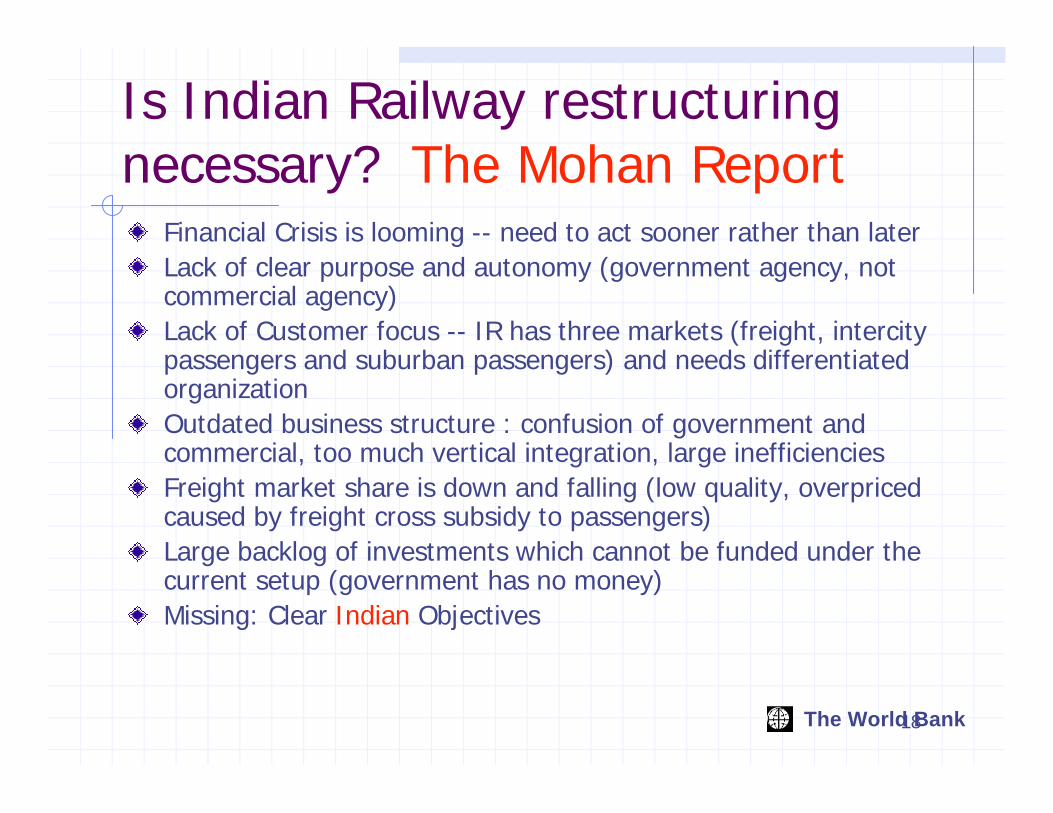

Financial Crisis is looming -- need to act sooner rather than laterLack of clear purpose and autonomy (government agency, not commercial agency)Lack of Customer focus -- IR has three markets (freight, intercity passengers and suburban passengers) and needs differentiated organizationOutdated business structure : confusion of government and commercial, too much vertical integration, large inefficienciesFreight market share is down and falling (low quality, overpriced caused by freight cross subsidy to passengers)Large backlog of investments which cannot be funded under the current setup (government has no money)Missing: Clear Indian Objectives

19The World Bank

Mohan Report: Principles of Restructuring

Broad changes:? separate railway from government (create MOT and regulator),

Separate policy, regulatory, management? manage railway commercially (LOB organization)? Focus on core, spin off non-core (no mention of privatization)

businesses and social activities? Bring in some outside skills and management

Marketing:? Freight -- better quality of service, lower tariffs, competition? Passenger -- rebalance passenger tariffs

Improve efficiency (accelerated reduction in manpower (25 percent) with safety netFinancing including private sectorRecast accounts in structure and with Indian GAAP

20The World Bank

Places to start: where the World Bank could help

Overall policy framework is goodAccounting work to install GAAP, construct LOB accounts and define PSO paymentsInvestments in IT hardware and systems neededFormulation of Government and Regulatory functions and agenciesAnalytical assistance in structure of new organizations (traffic flow studies to analyze need to redraw zonal boundaries, set up specialized companies, establish competition, etc)? Separate suburban operations? Assess current Zonal and operating enterprise structure

Support in valuation and spin off of non-core (commercial and social)Labor analyses and safety net programsAssistance in spin off of branch linesAppropriate physical investments identified during restructuringanalyses

21The World Bank

What Has the World Bank Done?Restructuring analyses, analytical tools and TAAsset rehabilitation to support new structureLabor transitions and retrainingResettlementEnvironmental cleanupSupport changes in structure (suburban devolution, creation of management and accounting systems)Investment in appropriate private operators (Concor)

22The World Bank

Zonal Railways Are Different:Freight Ton-Km as Percent of Total Traffic

0

10

20

30

40

50

60

70

80

N. Eastern

Southern

Central

Western

N. Frontier

Northern

Eastern

S. Central

S. Eastern

IR Average

23The World Bank

The Gauge Effect:India’s Three Separate Railways

5.80 0.3

25.3

3.28.5

68.9

96.891.2

0

10

20

30

40

50

60

70

80

90

100

Narrow Gauge Meter Gauge Broad Gauge

% line-km% t-km% p-km

24The World Bank

IR’s Suburban Activities(Passenger-Km in 000,000)

0

5

10

15

20

25

30

35

Mumbai Chennai Calcutta

Central

Western

Southern MGSouthern BG

Eastern

SouthEastern

2000 trains daily

25The World Bank

Suburban Rail Systems:Annual Passengers Per Km of Line

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

JohannesburgCape TownPretoriaRio:CBTU-RJSao Paulo:CPTMBA:M

itreBA:Sarm

ientoBA:RocaBA:San M

artinBA:Belgrano Sur

BA:Belgrano Norte

BA:UrquizaBA:SubteM

exico CityBangkok Skytrain

Mum

bai:CentralM

umbai:W

esternM

adras:SouthernNew York City:LIRR

Tokyo:JR EastTokyo:KeikyuTokyo:KeiseiCairo M

etro

26The World Bank

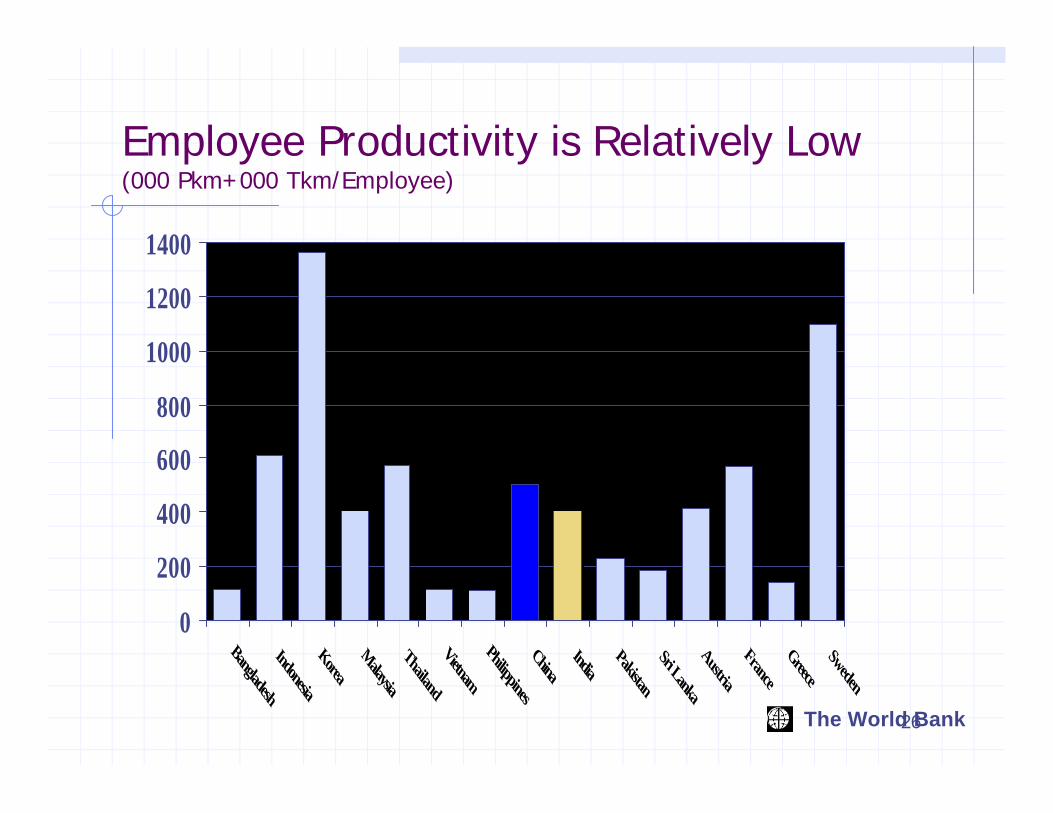

Employee Productivity is Relatively Low(000 Pkm+000 Tkm/Employee)

0

200

400

600

800

1000

1200

1400

Bangladesh

Indonesia

Korea

Malaysia

Thailand

Vietnam

Philippines

China India

Pakistan

Sri Lanka

Austria

France

Greece

Sweden

27The World Bank

Average Annual Output per Freight Wagon is Not High(000 Tkm per Wagon)

0

500

1000

1500

2000

2500

3000

Bangladesh

Indonesia

Korea Malaysia

Thailand

VietnamPhilippines

China India

Pakistan

Sri Lanka

Austria

France Greece

Sweden

28The World Bank

Ratio of Wage Costs to Revenues

0

10

20

30

40

50

60

1980 1985 1990 1995 2000

India China US Class I

%

29The World Bank

IR Ratio of Average Passenger Fareto Average Freight Tariff Is Very Low:

IR’s Destructive Linkage With High Passenger Share

4.1

BG Inter cityBG Sub’n

0

0.2

0.4

0.6

0.81

1.2

1.4

1.6

Bangladesh

Indonesia

Korea M

alaysia

Thailand

Vietnam

Philippines

China India

Pakistan

Sri Lanka

Austria

France

Greece

Sweden

MOR’s “escape”

Total

IR’s dilemma

30The World Bank

IR’s Program: Initial ActionsIR as enterprise separated from government --enterprise under commercial rules (profit motive, business Board with outside involvement and private sector personnel rules)Existing Zonal Railways adopt LOB organization on an accounting basisSeparate and localize suburban operations -- accounting first, then institutionalSpin off social, non-rail activitiesMake manufacturing activities independent and competitive, then privatize (if and when)

31The World Bank

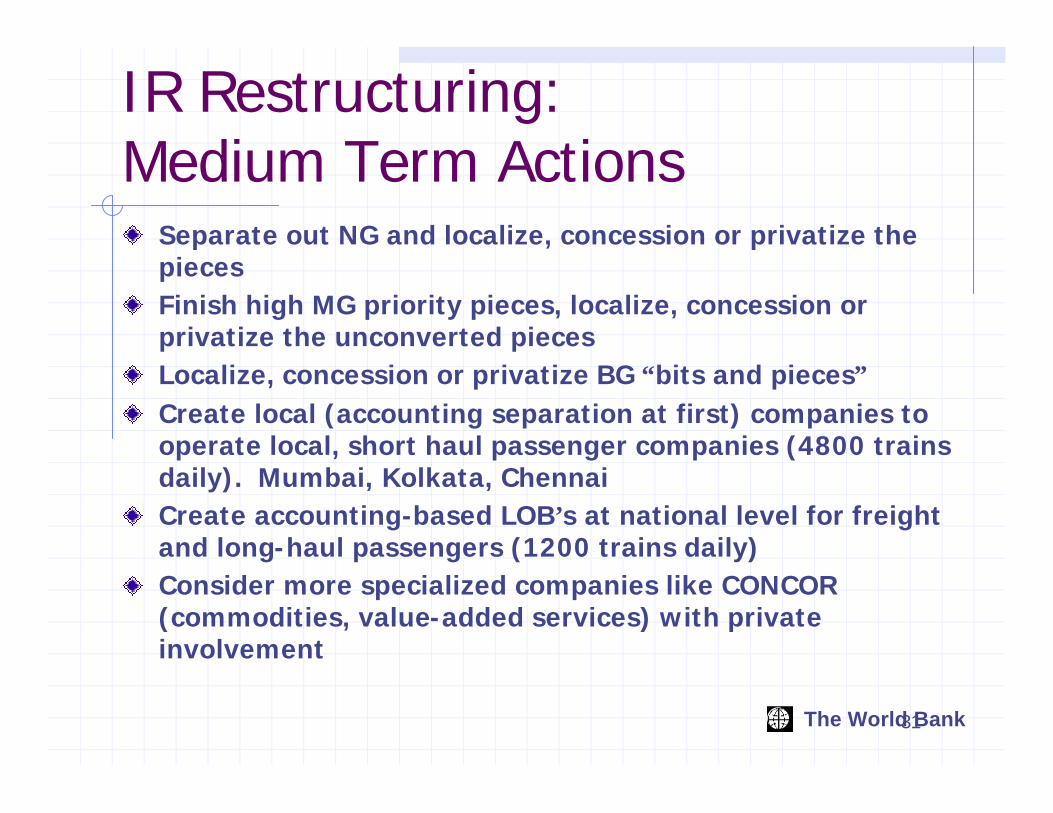

IR Restructuring:Medium Term Actions

Separate out NG and localize, concession or privatize the piecesFinish high MG priority pieces, localize, concession or privatize the unconverted piecesLocalize, concession or privatize BG “bits and pieces”Create local (accounting separation at first) companies to operate local, short haul passenger companies (4800 trains daily). Mumbai, Kolkata, ChennaiCreate accounting-based LOB’s at national level for freight and long-haul passengers (1200 trains daily)Consider more specialized companies like CONCOR (commodities, value-added services) with private involvement

32The World Bank

IR Narrow Gauge Lines Compared With Smaller Operating Concessions(gold = line-km, blue = traffic density in TU/km)

0

500

1000

1500

2000

2500

CH: Arica-La Paz

BO: Andina

CH: FERRONOR

PE: Southern

PE: Southeastern

BO: Oriental

PE: Central

BO: Chiapas

BR: Novoeste

BR: TCJordan

N. Frontier

Western

Central

Eastern

S. Eastern

Northern

IR NG Lines

33The World Bank

IR Meter Gauge Lines Comparedwith Middle-Sized Operating Concessions(gold = line-km, blue = traffic density in TU/km)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

AR: Belgrano

AR: Roca

AR: FEPSA

AR: Mesop.

AR: BAP

AR: NCA

C'I/BFBR: Novoeste

BR: FCA

BR: FSA

ME: Sudeste

BR: FEPASA

ME: Nordeste

N. Frontier

Northern

S. Central

Western

Southern

N. Eastern

IR MG Lines

34The World Bank

Three IR Markets: the Impact of LOB Focus and Private InvolvementTraffic Volume Index: 1994=100

80

100

120

140

160

180

200

90 91 92 93 94 95 96 97 98

CONCORPassengerFreight

35The World Bank

Km of Line: MOR Administrations Compared with IR Zones

0

2000

4000

6000

8000

10000

12000

Wulum

uqiHuhehaoteKunm

ingLiuzhouJinanGuangzhouNanchangLanzhouChengduShanghaiHarbinZhengzhouBeijingShenyangN. FrontierEasternN. EasternSouthernCentralS. CentralS. EasternW

esternNorthern

Total BG

36The World Bank

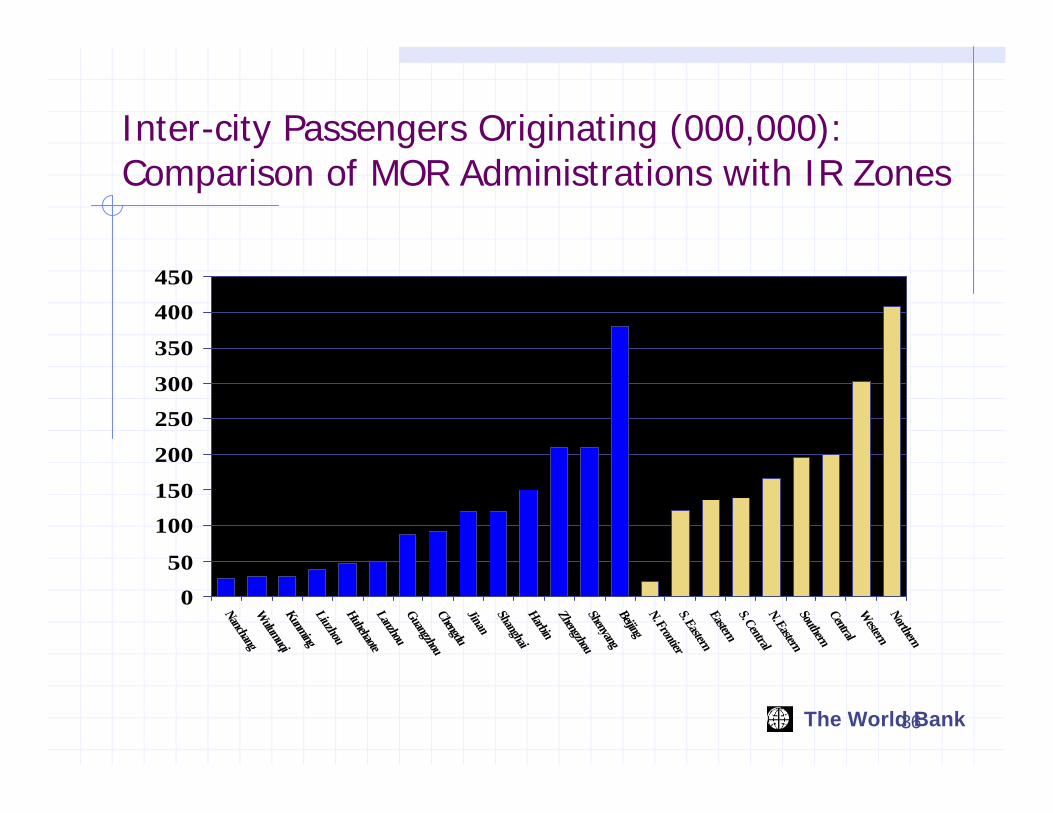

Inter-city Passengers Originating (000,000): Comparison of MOR Administrations with IR Zones

0

50

100

150

200

250

300

350

400

450

NanchangW

ulumuqiKunmingLiuzhouHuhehaoteLanzhouGuangzhouChengduJinanShanghaiHarbinZhengzhouShenyangBeijingN. FrontierS. EasternEasternS. CentralN. EasternSouthernCentralW

esternNorthern

37The World Bank

Freight Tons Originating (000,000): Comparison of MOR Administrations with IR Zones

0

50000

100000

150000

200000

250000

LiuzhouHuhehaoteKunmingW

ulumuqiLanzhouNanchangHarbinJinanChengduShenyangZhengzhouGuangzhouShanghaiBeijingN. EasternN. FrontierSouthernW

esternNorthernCentralS. CentralEasternS. Eastern

38The World Bank

MOR’s Freight Orientation:Percent Passenger TrafficP-km/(P-km+T-km) in %

01020304050

6070

80 82 84 86 88 90 92 94 96 98 0

India China

39The World Bank

Freight Traffic(billions of ton-km)

0

200

400

600

800

1000

1200

1400

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 0

Year

India China Conrail

40The World Bank

Passenger Traffic(000,000 p-km)

050

100150200250300350400450500

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 0

India China

Russia Japan

41The World Bank

Point to Point Rail Passenger Flows in China(1997 data excludes intra-zonal flows)

42The World Bank

1997 Passenger Flow Density(excludes intrazonal traffic)

43The World Bank

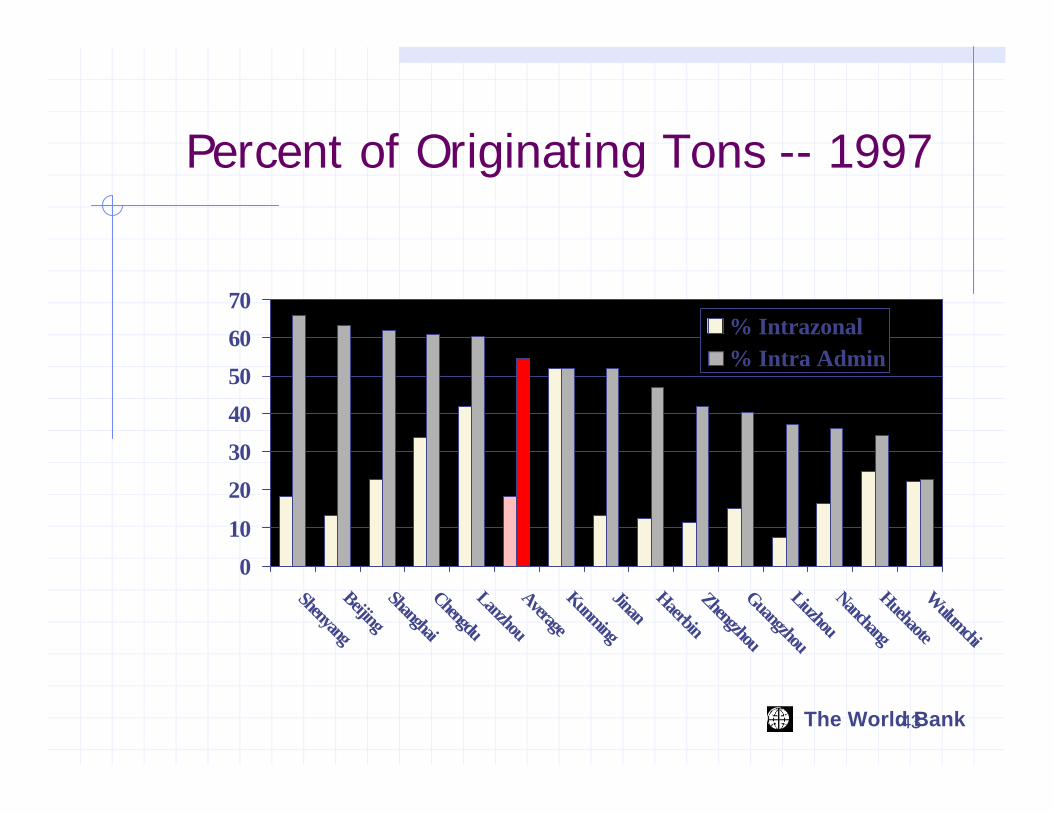

Percent of Originating Tons -- 1997

0

10

20

30

40

50

60

70

Shenyang

Beijing

Shanghai

Chengdu

Lanzhou

Average

Kunming

JinanHaerbin

Zhengzhou

Guangzhou

Liuzhou

Nanchang

Huehaote

Wulumchi

% Intrazonal% Intra Admin

44The World Bank

Point to Point Rail Freight Flows in China(1997 data excludes intra-zonal flows)

45The World Bank

1997 Freight Flow Density (Tons)(excludes intrazonal traffic)