resources, budget, and finance national association for court management resources, budget and...

TRANSCRIPT

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management

Resources, Budget and Finance Advanced Topics

Fundamentals and Foundations for Court Leaders

National Association For Court Management

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management

Exercise 1 - Optional warm-up exercise

How many of you have been asked in the last year to:

• Raise additional revenue?• Reduce your budget by some fixed amount or

percentage?• Close or cutback a program• Implement performance based budgeting?• Consider increased state funding?• Improve your budget advocacy skills?

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 3

• Court Revenue Analysis

• Strategic Planning

• Performance and Outcome Measures

• Strategies for Responding to Funding Reductions

• Increased State Funding

• Better Budget Advocacy

Topics

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management

Resources, Budget and Finance Fundamentals

Court Revenue Analysis

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 5

Learning ObjectivesAt the end of this session you should be able to:

• Identify the resources made available to your court

• Identify the sources of revenue for your court

• Identify nature of revenue sensitivity to economic conditions

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 6

Know your Resources

What types of resources are made available to your court to get its work done?

• Dollars

• Staff

• Information technology capabilities and functionality

• Equipment

• Facilities

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 7

What types of resources are made available to your court to get its work done?

• Reorganization of existing business practices; re-engineering

• Networking

• Allies

• Non-governmental organizations (NGO's)

Know your Resources

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 8

Sources of Court revenue

Typical sources of court revenue:• General Fund revenue – state or local

• Filing fees

• Surcharges on fees

• Fines

• Assessments on fines

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 9

Typical sources of court revenue: User fees Reimbursements for services State mandate payments Federal subsidies/reimbursements Grants and donations Other - Miscellaneous

Sources of Court revenue

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 10

Revenue Sources - General Fund

Where does GENERAL FUND revenue come from?

• Personal Income Tax

• Dividends and Capital Gains Tax

• Corporate Income Tax

• Sales tax

• Real Property tax

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 11

Where does GENERAL FUND revenue come from?

Personal property tax “Sin” taxes - Tobacco/alcohol Motor fuel taxes Gaming revenues User Fees and associated surcharges Reimbursements

Revenue Sources - General Fund

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 12

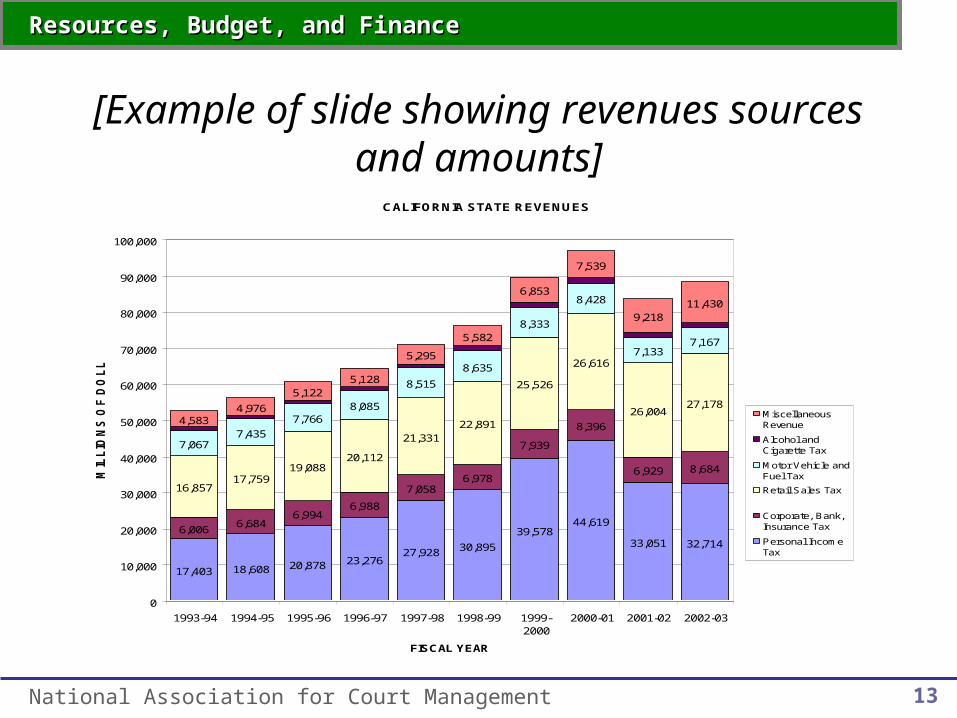

[Example of revenue amounts and proportions]

[Include one or two charts showing the level of revenue obtained from various sources, in gross amounts and percentages. Examples are provided on the next two slides.]

Revenue Sources - General Fund

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 13

CALIFORNIA STATE REVENUES

17,403 18,608 20,878 23,27627,928 30,895

39,57844,619

33,051 32,714

6,0066,684

6,9946,988

7,0586,978

7,939

8,396

6,929 8,684

16,85717,759

19,08820,112

21,33122,891

25,526

26,616

26,00427,178

7,0677,435

7,7668,085

8,515

8,635

8,333

8,428

7,1337,167

4,5834,976

5,1225,128

5,295

5,582

6,853

7,539

9,21811,430

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

1993-94 1994-95 1995-96 1996-97 1997-98 1998-99 1999-2000

2000-01 2001-02 2002-03

FISCAL YEAR

MIL

LIO

NS

OF

DO

LL

AR

S

MiscellaneousRevenue

Alcohol andCigarette Tax

Motor Vehicle andFuel Tax

Retail Sales Tax

Corporate, Bank,Insurance Tax

Personal IncomeTax

[Example of slide showing revenues sources and amounts]

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 14

[Example of slide showing revenues source proportions]

CALIFORNIA STATE REVENUES

32.9% 33.0% 34.3% 36.1%39.3% 40.5%

44.1% 46.0%39.5% 37.0%

11.4% 11.8% 11.5% 10.8%9.9% 9.2%

8.8%8.7%

8.3%9.8%

31.9% 31.5% 31.4% 31.2%30.0% 30.0%

28.4% 27.4%

31.1% 30.7%

13.4% 13.2% 12.8% 12.5% 12.0% 11.3% 9.3% 8.7%8.5% 8.1%

8.7% 8.8% 8.4% 7.9% 7.5% 7.3% 7.6% 7.8% 11.0% 12.9%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

1993-94 1994-95 1995-96 1996-97 1997-98 1998-99 1999-2000

2000-01 2001-02 2002-03

FISCAL YEAR

Per

cen

t o

f T

ota

l Rev

enu

es

MiscellaneousRevenue

Alcohol andCigarette Tax

Motor Vehicle andFuel Tax

Retail Sales Tax

Corporate, Bank,Insurance Tax

Personal IncomeTax

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 15

Revenue Sensitivities

• What is the historical trend of revenues?

• What economic conditions are revenue sources susceptible to?

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 16

• What is the near term prognosis regarding revenue levels?

• What affects the rebound of revenue and how soon?

• Is this a short-term problem, or long term?

• Is there a link between state and local funding cycles and revenues?

Revenue Sensitivities

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 17

[Example of slide addressing revenue sensitivity]

Findings of NGA/NASBO Survey

Economic conditions do not affect all tax sources equally:

• Sales tax 3.2% lower than projected

• Personal income tax 12.8% lower than projected

• Corporate income tax 21.5% lower than projected

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 18

[Example of slide addressing revenue sensitivity]

Revenue Sources Change Dramatically

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 19

Revenue Limitations• Special Funds - dedicated use(s)

• Special purpose revenues

• Reimbursements; Over-recovery

• Mandates

• Differences in state funded, vs. locally funded, court systems

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 20

Revenue Analysis Exercise [OPTION A]

Revenue Sources and Vulnerability• Identify all of the current revenue sources that fund the

program, function, or service• Assess the economic vulnerabilities of each of the funding

sources. • Where does the funding come from for each category of

program expense? • For each category of revenue funding the program, what

are the vulnerabilities of the revenues source? • If the program were to be cut, what would happen to the

revenue associated with or funding the program?

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 21

Roundtable Discussion Topics• What new sources of revenue has your state or court

implemented in the last few years?• What fluctuations in revenues have you experienced in the

last few years?• What is the level of assessments on criminal and traffic

fines in your jurisdictions? Have there been changes in the level of assessments recently? Have there been changes in what agencies or programs receive funding from the assessments?

• What pitfalls would you advise other states or courts to be aware of regarding particular revenue sources?

Revenue Analysis Exercise [OPTION B]

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management

Resources, Budget and Finance Fundamentals

Strategic Planning

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 23

Linking Spending to Priorities“Tell me where you spend your money

and I will tell you what your priorities are.”

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 24

Review of Fundamentals

• What is a strategic plan

• What are major steps in developing a strategic plan that are relevant to budgeting• stakeholder analysis and TOWS analysis

• Typical elements of a strategic plan

• Purpose of strategic plan and uses

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 25

Integrating the Strategic Plan Into the Budget Process

Link the strategic plan to resource acquisition and internal budget allocation

• Identify the priorities in the strategic plan

• Plan and build the budget request to support the priorities

• Respond to budget review questions in the context of the strategic plan

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 26

Monitoring Expenditures according to the strategic plan

• Develop spending plans which support the strategic plan goals

• Monitor actual spending patterns with respect to strategic plan priorities and goals

Integrating the Strategic Plan Into the Budget Process

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 27

Updating the Strategic PlanSteps in updating the strategic plan:

• Environmental Scanning for need to make changes

• Evaluation of accomplishment of strategic plan goals

• What would you do differently from the last time?

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 28

Strategic Planning Exercise [OPTION A]

Role, Vision, and Strategic PlanMake a list the goals and expected outcomes of the program, function, or service.

• Is the program consistent with the roles and purposes of the judiciary?

• Is the program consistent with the Court’s mission, values, and goals?

• Is the program consistent with the strategic plan?

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 29

Roundtable Discussion Topics

Strategic Planning Exercise [OPTION B]

• How many courts have strategic plans?• How did the existence of a strategic plan

help in:• Building a budget?• Defending the budget request?• Monitoring of budget expenditures?

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management

Resources, Budget and Finance Fundamentals

Performance and Outcome Measures

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 31

Linking Activities to Performance

“What you count affects how people behave.”

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 32

Review of Fundamentals

• Performance measures and outcome measures - what are they and what can they do

• Input, Output, and Outcome measures

• Trial Court Performance Standards

• CourTools

• Data collection supporting measures

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 33

Development of Outcome and Performance Measures

Create relevant and feasible measures:

• Consistent with Court’s mission and vision

• Base on goals and objectives in strategic plan

• Intuitive and understandable

• Relevant to the program or service

• Simple

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 34

Data collection in support of performance measures:

• Sources of data

• Accuracy of data entry

• Consistency of data entry

• Ease of calculating measures from raw data

• Presentation of measures

Development of Outcome and Performance Measures

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 35

Incorporating Performance Measures Into The Budget

ProcessUse of performance and outcome measures for:

• Cost benefit analysis

• Assessment of program effectiveness

• Resource allocation based on workload

• Bench-marking court operations

• Demonstrating responsible use of public funds

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 36

Performance Measures Exercise [OPTION A]

Performance and Outcome MeasuresIdentify several relevant performance measures and outcome measures for the program, function, or service

• How do they relate to the role of the judiciary and the court's mission and values?

• How do they measure the impact of the program?• How do they measure the effectiveness of the

program from a cost perspective?• How do they demonstrate the responsible use of

funds?

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 37

Roundtable Discussion Topics

Performance Measures Exercise [OPTION B]

• How many courts have performance or outcome measures?

• How did the existence of performance or outcome measures help in:

• Building a budget;• Defending the budget request, and• Monitoring of budget expenditures?

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management

Resources, Budget and Finance Fundamentals

Strategies for Responding to Budget Reductions

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 39

Strategies for Responding to Budget Reductions

Two Approaches to Responding to Budget Cuts:

• Increase Revenues to offset spending cut

• Reduce Expenditures

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 40

Increase Revenue – Short Term/One Time:

• Redirect resources

• Redirect expenses

• Use reserve funds

• Borrow

Strategies for Responding to Budget Reductions

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 41

Increase Revenue – Long Term:

• Enhanced Revenue Collection

• New Revenue Sources

• Leverage Resources

• Rally Support with Funding Body

Strategies for Responding to Budget Reductions

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 42

Three categories of responses

• "Nick and Cut

• “Rearranging the Deck Chairs“

• "Rational Deconstruction"

Strategies for Responding to Budget Reductions

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 43

What strategies are available that are short term in nature and impact?

• Minimal impact on programs, services, and service levels

• Expectation of return to ‘normal’ funding levels before impact on services is irreversible

"Nick and Cut“Short Term or One Time Responses

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 44

Examples of Typical First Cuts:

• Across the board percentage cuts

• Reduce training and travel

• Cut management analysis capability

• Reduce hours or close on some days

"Nick and Cut“Short Term or One Time Responses

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 45

Examples of Personnel Related Cuts: • Hiring Freeze• Reduce Work Hours• Wage Freeze or Reduction• Reduction in overtime usage• Reduction in on-call staff coverage• Furlough• Layoffs

"Nick and Cut“Short Term or One Time Responses

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 46

Examples of Personnel Related Cuts: • Renegotiate labor contracts

• Reduce Benefits – “take backs”

• Postpone salary increases or raises

• Reduce employer contribution toward benefit costs

• Freeze vacation or comp time payouts

"Nick and Cut“Short Term or One Time Responses

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 47

Examples of Non-personnel Cuts:

• Supplies – stop or postpone purchasing

• Equipment – stop or postpone improvements, upgrades or purchasing

• Services - reduce service levels or defer services

"Nick and Cut“Short Term or One Time Responses

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 48

“Rearranging the Deck Chairs"

Changing the Way Courts Do Business

What strategies are available that make more effective use of resources given to the court?

• Concept is to:• Do the right thing, and • Do it in a more effective manner

• Expectation of ‘permanent’ savings

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 49

Strategies:• Performance management and evaluation

• Redesigning court work flows

• Changing business practices

• Greater use of IT

• Close high cost facilities

• Business process outsourcing

“Rearranging the Deck Chairs"

Changing the Way Courts Do Business

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 50

"Rational Deconstruction" Long Term, Fundamental Responses

What strategies are available that are long term in nature and impact?

• Concept is rational reduction or rational deconstruction

• Expectation is permanent reduction of costs

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 51

Strategies:

• Strategic planning

• Eliminate a practice – “Seize the Time”

• Eliminate or reduce services

• Eliminate programs

"Rational Deconstruction" Long Term, Fundamental Responses

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 52

What is basis for making these decisions?• Identify role of court and core functions• Is the court required to do this in the first

place? • Is the court required to do it in this way?• Can another agency do this?• What level of service is required, if any?

"Rational Deconstruction" Long Term, Fundamental Responses

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 53

Budget Reduction Exercise [OPTION A]

Responding to Budget ReductionsIdentify possible alternative responses to the proposed budget reduction:

• Revenue options - existing revenues or new revenues

• Operational changes that would allow the program to continue to meet its objectives, but at a lower cost

• Rational Deconstruction – what could the court stop doing, or do differently

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 54

Roundtable Discussion Topics

Budget Reduction Exercise [OPTION B]

• What types of budget reductions have courts faced?

• What types of short-term fixes have courts used?• What examples are there of court’s changing

procedures and business practices? • What examples are there of reassessment of what

court’s did or elimination of programs?

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management

Resources, Budget and Finance Fundamentals

A Shift to Greater State Funding

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 56

Greater State FundingDrivers

Why Are States Considering Greater State Funding?

• Bad Economic Times

• Initiatives Limiting Tax Rates or Expenditure Growth

• Local Government Pressure from Restricted Local Revenues

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 57

Greater State FundingConcurrent Changes

What Else is Happening?• Court restructuring, coordination,

consolidation, or unification

• Performance Based Budgeting and Strategic Planning Requirements

• Initiatives – “Three Strikes,” Determinate Sentencing, Problem Solving Courts

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 58

Greater State FundingExpectations and Reality

Anticipated Benefits• Higher Levels of Court Funding

• Greater Equity of Funding Across Courts

• Greater Stability of Funding Levels

• Standardization of Programs and Services

• Economies of Scale

• Improved Practices

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 59

Greater State Funding Expectations and Reality

Concerns• Winners and Losers

• Centralization – Loss of Local Control

• Change in Status of Court Employees

• More ‘Red Tape”

• Inability to Respond to Local Priorities

• Weakened Collaboration with Local Agencies

• Stifle Innovation

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 60

Underlying Issues• Adequacy – How Much is Enough?

• Equity – Equal Access to Justice

• Stability and Predictability

• Accountability for Court Expenditures

• What are Core Judicial Functions?

• Budgeting Mechanisms and Governance

Greater State Funding Expectations and Reality

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 61

Roundtable Discussion Topics

Shifting to Greater State Funding Exercise

• What increases in state funding have courts experienced?

• What caused the shift to occur?• What were the expectations about the shift?• What were the realities associated with the shift?• What were the unexpected impacts and

consequences?

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management

Resources, Budget and Finance Fundamentals

Better Budget Advocacy

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 63

Better Budget AdvocacyThe Context

• Know Your Audience• Know Your ‘Competitors’• Know the Fiscal Condition• Know Collaboration and Partnership

Opportunities• Know Your Ability to Make Your Case

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 64

Better Budget Advocacy Strategies

Internal Capabilities• Know Your Mission, Vision, Values, Goals, and

Objectives• Think and Act Strategically• Constantly Examine Existing Practices• Pursue Collaboration and Partnership Opportunities• Identify and Measure Meaningful Outcomes• Maintain a High Quality Data System

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 65

Get Your Court's Story Told Role of the court – what does the court do? Identify impact of a reduction in funding on:

Public safety Public services

Demonstrate cost effectiveness Demonstrate accountability

Better Budget Advocacy Strategies

Internal Capabilities

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 66

• Get to Know Funders and Regularly Meet with Them

• Build Personal Relationships

• Submit Realistic Requests

• Provide Valid Supporting Documentation

• Establish and maintain credibility

Better Budget Advocacy Strategies

External Capabilities

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 67

Roundtable Discussion Topics

Improved Budget Advocacy Exercise

• What have you done that improved your success in budget advocacy?

• What mistakes have you and your court made?• What have you done to improve your internal

budget capacity?• What have you done to improve external

relations?

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 68

Wrap-up Exercise

Preparing and Defending Your ProgramHow would your group respond to the proposed budget reduction?

• Highlights of approach taken and analysis made

• Best arguments to sustain program and funding

• Discussion and feedback from the larger group

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 69

Discussion and Feedback

Based on what you have heard:

• What is one thing you will do differently when you get to work tomorrow?

• What is one thing you need to learn how to do, or do better?

• What is one relationship you need to build, or repair?

Resources, Budget, and FinanceResources, Budget, and Finance

National Association for Court Management 70

Concluding Remarks

• [Revenue analysis]

• [Strategic Planning]

• [Performance and Outcome measures]

• [Responding to Funding Reductions]

• [Shifting to Greater State Funding]

• [Better Budget Advocacy]