report of the statutory auditor to the council on the ... · on the consolidated financial...

TRANSCRIPT

The Lutheran World Federation Geneva

Report of the statutory auditor to the Council on the consolidated financial statements 2016

PricewaterhouseCoopers SA, avenue Giuseppe-Motta 50, case postale, CH-1211 Genève 2, Switzerland Téléphone: +41 58 792 91 00, Téléfax: +41 58 792 91 10, www.pwc.ch

PricewaterhouseCoopers SA is a member of the global PricewaterhouseCoopers network of firms, each of which is a separate and independent legal entity.

Report of the statutory auditor to the Council of The Lutheran World Federation

Geneva

Report of the statutory auditor on the consolidated financial statements

As statutory auditor, we have audited the accompanying consolidated financial statements of The Lutheran World Federation, which comprise the balance sheet, statement of comprehensive income, cash flow statement, statement of changes in reserves and notes, for the year ended 31 December 2016.

Board’s responsibility The Management is responsible for the preparation of the consolidated financial statements in accordance with the International Financial Reporting Standards (IFRS) and the requirements of Swiss law. This responsibility includes designing, implementing and maintaining an internal control system relevant to the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error. The Board is further responsible for selecting and applying appropriate accounting policies and making accounting estimates that are reasonable in the circumstances.

Auditor’s responsibility Our responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with Swiss law and Swiss Auditing Standards as well as the Inter-national Standards on Auditing. Those standards require that we plan and perform the audit to obtain reasonable assurance whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgment, includ-ing the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers the internal control system relevant to the entity’s preparation of the consolidated financial statements in order to design audit proce-dures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control system. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made, as well as evaluating the overall presentation of the consolidated financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion In our opinion, the consolidated financial statements for the year ended 31 December 2016 give a true and fair view of the financial position, the results of operations and the cash flows in accordance with the International Financial Reporting Standards (IFRS) and comply with Swiss law.

3

Report on other legal requirements

We confirm that we meet the legal requirements on licensing according to the Auditor Oversight Act (AOA) and independence (article 69b paragraph 3 CC in connection with article 728 CO) and that there are no circumstances incompatible with our independence.

In accordance with article 69b paragraph 3 CC in connection with article 728a paragraph 1 item 3 CO and Swiss Auditing Standard 890, we confirm that an internal control system exists which has been designed for the preparation of consolidated financial statements according to the instructions of the Association Board.

We recommend that the consolidated financial statements submitted to you be approved.

PricewaterhouseCoopers SA

Marc Secretan Charlotte Tavernier

Audit expert Auditor in charge

Audit expert

Geneva, 26 April 2017

Enclosure:

Consolidated financial statements (balance sheet, statement of comprehensive income, cash flowstatement, statement of changes in reserves and notes)

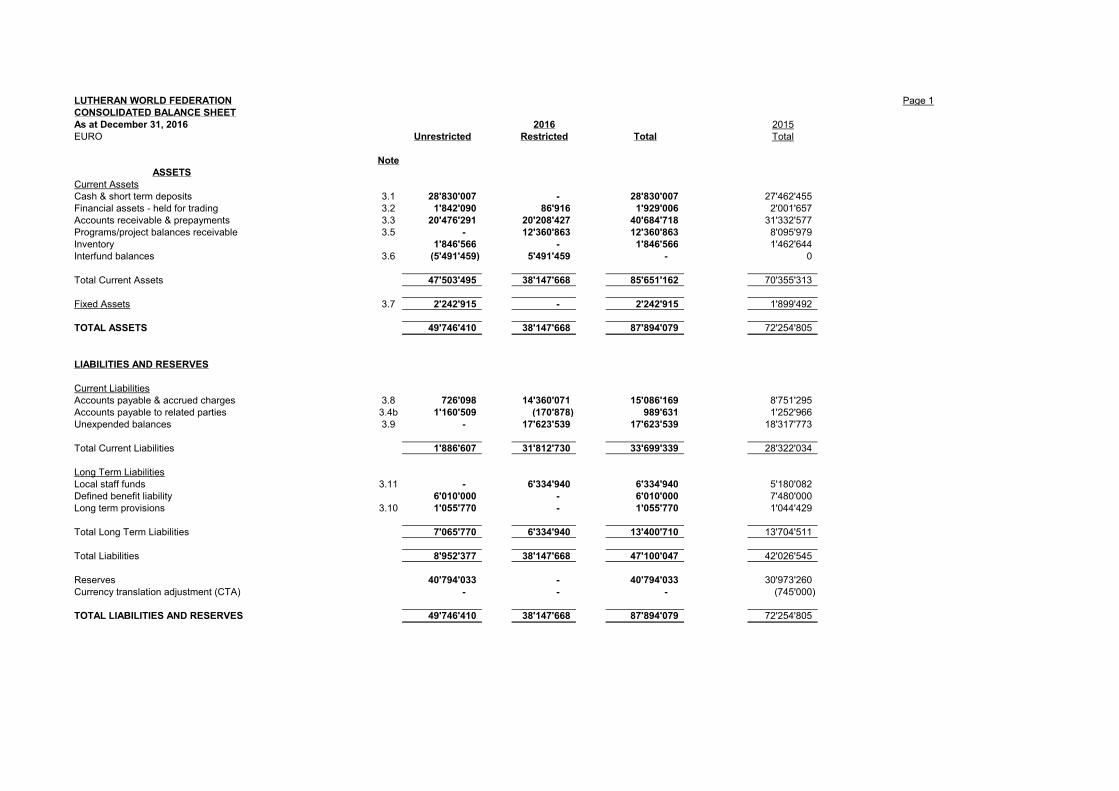

LUTHERAN WORLD FEDERATION Page 1

CONSOLIDATED BALANCE SHEET

As at December 31, 2016 2016 2015

EURO Unrestricted Restricted Total Total

Note

ASSETS

Current Assets

Cash & short term deposits 3.1 28'830'007 - 28'830'007 27'462'455

Financial assets - held for trading 3.2 1'842'090 86'916 1'929'006 2'001'657

Accounts receivable & prepayments 3.3 20'476'291 20'208'427 40'684'718 31'332'577

Programs/project balances receivable 3.5 - 12'360'863 12'360'863 8'095'979

Inventory 1'846'566 - 1'846'566 1'462'644

Interfund balances 3.6 (5'491'459) 5'491'459 - 0

Total Current Assets 47'503'495 38'147'668 85'651'162 70'355'313

Fixed Assets 3.7 2'242'915 - 2'242'915 1'899'492

TOTAL ASSETS 49'746'410 38'147'668 87'894'079 72'254'805

LIABILITIES AND RESERVES

Current Liabilities

Accounts payable & accrued charges 3.8 726'098 14'360'071 15'086'169 8'751'295

Accounts payable to related parties 3.4b 1'160'509 (170'878) 989'631 1'252'966

Unexpended balances 3.9 - 17'623'539 17'623'539 18'317'773

Total Current Liabilities 1'886'607 31'812'730 33'699'339 28'322'034

Long Term Liabilities

Local staff funds 3.11 - 6'334'940 6'334'940 5'180'082

Defined benefit liability 6'010'000 - 6'010'000 7'480'000

Long term provisions 3.10 1'055'770 - 1'055'770 1'044'429

Total Long Term Liabilities 7'065'770 6'334'940 13'400'710 13'704'511

Total Liabilities 8'952'377 38'147'668 47'100'047 42'026'545

Reserves 40'794'033 - 40'794'033 30'973'260

Currency translation adjustment (CTA) - - - (745'000)

TOTAL LIABILITIES AND RESERVES 49'746'410 38'147'668 87'894'079 72'254'805

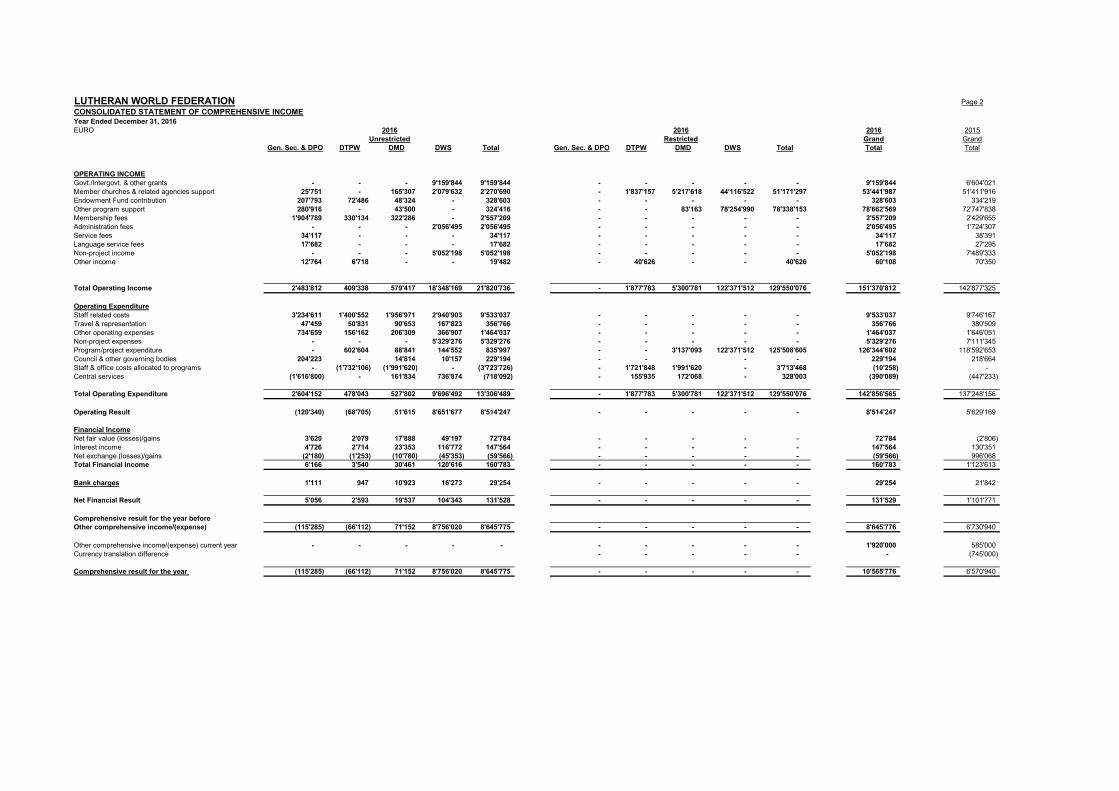

LUTHERAN WORLD FEDERATION Page 2

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

Year Ended December 31, 2016

EURO 2016 2015

Grand Grand

Gen. Sec. & DPO DTPW DMD DWS Total Gen. Sec. & DPO DTPW DMD DWS Total Total Total

OPERATING INCOME

Govt./Intergovt. & other grants - - - 9'159'844 9'159'844 - - - - - 9'159'844 6'604'021

Member churches & related agencies support 25'751 - 165'307 2'079'632 2'270'690 - 1'837'157 5'217'618 44'116'522 51'171'297 53'441'987 51'411'916

Endowment Fund contribution 207'793 72'486 48'324 - 328'603 - - - - - 328'603 334'219

Other program support 280'916 - 43'500 - 324'416 - - 83'163 78'254'990 78'338'153 78'662'569 72'747'838

Membership fees 1'904'789 330'134 322'286 - 2'557'209 - - - - - 2'557'209 2'429'655

Administration fees - - - 2'056'495 2'056'495 - - - - - 2'056'495 1'724'307

Service fees 34'117 - - - 34'117 - - - - - 34'117 38'391

Language service fees 17'682 - - - 17'682 - - - - - 17'682 27'295

Non-project income - - - 5'052'198 5'052'198 - - - - - 5'052'198 7'489'333

Other income 12'764 6'718 - - 19'482 - 40'626 - - 40'626 60'108 70'350

Total Operating Income 2'483'812 409'338 579'417 18'348'169 21'820'736 - 1'877'783 5'300'781 122'371'512 129'550'076 151'370'812 142'877'325

Operating Expenditure

Staff related costs 3'234'611 1'400'552 1'956'971 2'940'903 9'533'037 - - - - - 9'533'037 9'746'167

Travel & representation 47'459 50'831 90'653 167'823 356'766 - - - - - 356'766 380'509

Other operating expenses 734'659 156'162 206'309 366'907 1'464'037 - - - - - 1'464'037 1'646'051

Non-project expenses - - - 5'329'276 5'329'276 - - - - - 5'329'276 7'111'345

Program/project expenditure - 602'604 88'841 144'552 835'997 - - 3'137'093 122'371'512 125'508'605 126'344'602 118'592'653

Council & other governing bodies 204'223 - 14'814 10'157 229'194 - - - - 229'194 218'664

Staff & office costs allocated to programs - (1'732'106) (1'991'620) - (3'723'726) - 1'721'848 1'991'620 - 3'713'468 (10'258) -

Central services (1'616'800) - 161'834 736'874 (718'092) - 155'935 172'068 - 328'003 (390'089) (447'233)

Total Operating Expenditure 2'604'152 478'043 527'802 9'696'492 13'306'489 - 1'877'783 5'300'781 122'371'512 129'550'076 142'856'565 137'248'156

Operating Result (120'340) (68'705) 51'615 8'651'677 8'514'247 - - - - - 8'514'247 5'629'169

Financial Income

Net fair value (losses)/gains 3'620 2'079 17'888 49'197 72'784 - - - - - 72'784 (2'806)

Interest income 4'726 2'714 23'353 116'772 147'564 - - - - - 147'564 130'351

Net exchange (losses)/gains (2'180) (1'253) (10'780) (45'353) (59'566) - - - - - (59'566) 996'068

Total Financial Income 6'166 3'540 30'461 120'616 160'783 - - - - - 160'783 1'123'613

Bank charges 1'111 947 10'923 16'273 29'254 - - - - - 29'254 21'842

Net Financial Result 5'056 2'593 19'537 104'343 131'528 - - - - - 131'529 1'101'771

Comprehensive result for the year before

Other comprehensive income/(expense) (115'285) (66'112) 71'152 8'756'020 8'645'775 - - - - - 8'645'776 6'730'940

Other comprehensive income/(expense) current year - - - - - - - - - - 1'920'000 585'000

Currency translation difference - - - - - - (745'000)

Comprehensive result for the year (115'285) (66'112) 71'152 8'756'020 8'645'775 - - - - - 10'565'776 6'570'940

Unrestricted

2016 2016

Restricted

LUTHERAN WORLD FEDERATION Page 3

Consolidated statement of changes in reserves

Year Ended December 31, 2016EUR

General General Scholarship Fd Comm Rev Fd Comm Enabl Fd Total General General Res.Admin. Inst.Cap. Dev. Prog.Op. Emergency Field desig Total

Balance at January 1, 2015 (1'720'479) (1'038'413) 399'637 490'600 93'070 (55'106) (422'852) 4'095'024 640'401 - - - 21'120'332 25'855'757 23'657'320

Surplus/(deficit) for the year 19'559 (201'977) (201'977) 36'349 - 585'000 6'982'009 7'567'009 7'420'940

Currency translation adjustment (CTA) (745'000)

IAS 19 adjustment (35'049) (22'356) (22'356) (15'854) (31'741) (31'741) (105'000)

Internal reserve transfers - -

Balance at December 31, 2015 (1'735'969) (1'262'746) 399'637 490'600 93'070 (279'439) (402'357) 4'063'283 640'401 585'000 - - 28'102'341 33'391'025 30'228'260

GS&DPO DTPW Grand Total

General General Scholarship Fd Comm Rev Fd Comm Enabl Fd Total General General Res.Admin. Inst.Cap. Dev. Prog.Op. Emergency Field desig Total

Balance at January 1, 2016 (1'735'969) (1'262'746) 399'637 490'600 93'070 (279'439) (402'357) 4'063'283 640'401 585'000 - - 28'102'341 33'391'025 30'973'260

Surplus/(deficit) for the year 37'402 163'530 163'530 - 12'075 8'882'766 8'894'841 9'095'773

Currency translation adjustment (CTA) (745'000)

IAS 19 adjustment (152'687) (66'112) (66'112) (92'377) (138'823) (138'823) (450'000)

Actuary result 1'920'000

Internal reserve transfers - -

Balance at December 31, 2016 (1'851'254) (1'165'328) 399'637 490'600 93'070 (182'021) (494'734) 3'936'535 640'401 585'000 - - 36'985'107 42'147'043 40'794'033

DMD DWS

LUTHERAN WORLD FEDERATION Page 4

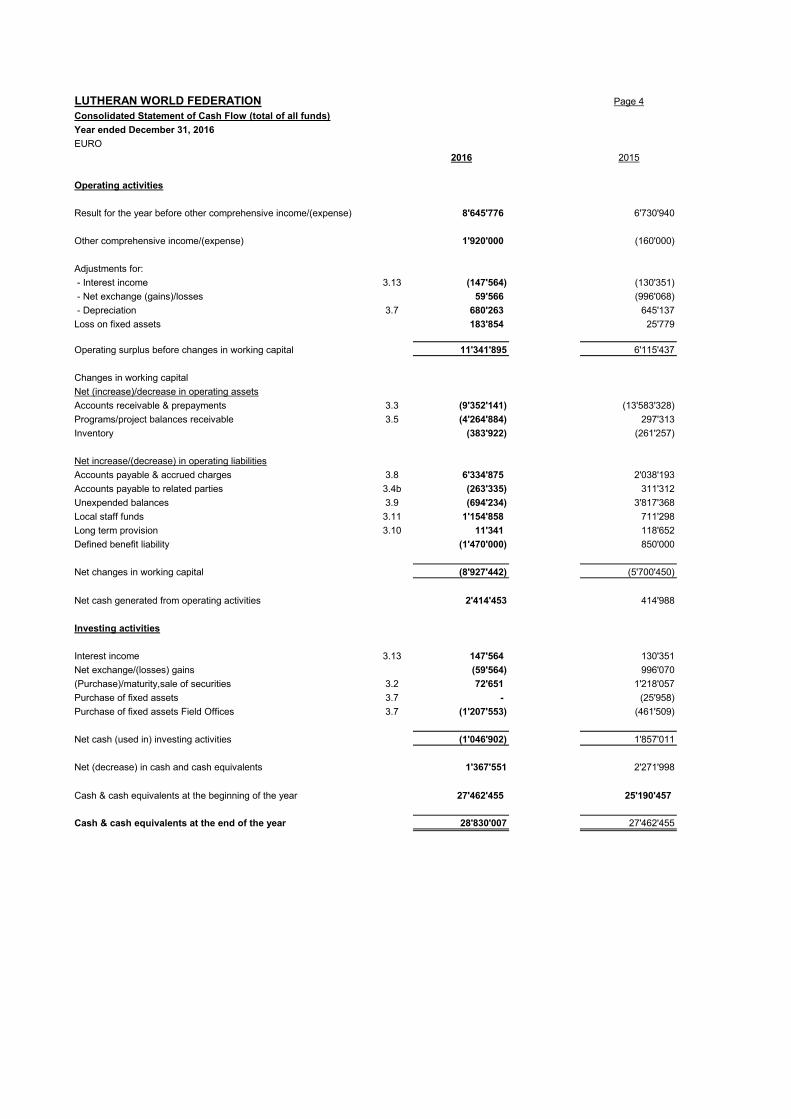

Consolidated Statement of Cash Flow (total of all funds)

Year ended December 31, 2016

EURO

2016 2015

Operating activities

Result for the year before other comprehensive income/(expense) 8'645'776 6'730'940

Other comprehensive income/(expense) 1'920'000 (160'000)

Adjustments for:

- Interest income 3.13 (147'564) (130'351)

- Net exchange (gains)/losses 59'566 (996'068)

- Depreciation 3.7 680'263 645'137

Loss on fixed assets 183'854 25'779

Operating surplus before changes in working capital 11'341'895 6'115'437

Changes in working capital

Net (increase)/decrease in operating assets

Accounts receivable & prepayments 3.3 (9'352'141) (13'583'328)

Programs/project balances receivable 3.5 (4'264'884) 297'313

Inventory (383'922) (261'257)

Net increase/(decrease) in operating liabilities

Accounts payable & accrued charges 3.8 6'334'875 2'038'193

Accounts payable to related parties 3.4b (263'335) 311'312

Unexpended balances 3.9 (694'234) 3'817'368

Local staff funds 3.11 1'154'858 711'298

Long term provision 3.10 11'341 118'652

Defined benefit liability (1'470'000) 850'000

Net changes in working capital (8'927'442) (5'700'450)

Net cash generated from operating activities 2'414'453 414'988

Investing activities

Interest income 3.13 147'564 130'351

Net exchange/(losses) gains (59'564) 996'070

(Purchase)/maturity,sale of securities 3.2 72'651 1'218'057

Purchase of fixed assets 3.7 - (25'958)

Purchase of fixed assets Field Offices 3.7 (1'207'553) (461'509)

Net cash (used in) investing activities (1'046'902) 1'857'011

Net (decrease) in cash and cash equivalents 1'367'551 2'271'998

Cash & cash equivalents at the beginning of the year 27'462'455 25'190'457

Cash & cash equivalents at the end of the year 28'830'007 27'462'455

Page 5 of 27

THE LUTHERAN WORLD FEDERATION

Geneva, Switzerland

Consolidated Financial Statements

Notes to the Financial Statements for the year ended December 31, 2016

1. Activities

The Lutheran World Federation (LWF) is a global communion of Christian churches in the

Lutheran tradition, founded in 1947. The LWF Secretariat is located in the Ecumenical

Centre, Rte de Ferney 150 in Geneva.

The LWF is a non-profit association incorporated and registered under Article 60 and

following of the Swiss Civil Code.

The LWF’s purpose is to:

- further the united witness to the Gospel of Jesus Christ and strengthen the member

churches in carrying out the missionary command and in their efforts towards Christian

unity worldwide

- further worldwide among member churches diaconic action, alleviation of human need,

promotion of peace and human rights, social and economic justice, care for God’s creation

and sharing of resources

- further through cooperative study the self-understanding and the communion of member

churches and help them to act jointly in common tasks

The Assembly, composed of representatives of the member churches of the Federation, is the

principal authority of the LWF. The Assembly is normally held every six years and is

responsible for the Constitution, electing the President and the members of the Council, and

giving general direction to the work of the Federation.

The Council is composed of the President, the Chairperson of the Finance Committee, and 48

persons elected by the Assembly. The term of office of the Council shall end at the close of the

next ordinary Assembly. The Council is responsible for the business of the Federation in the

interim between ordinary Assemblies. The Council elects the General Secretary and the

Chairperson of the Finance Committee. The Council elects the Vice-Presidents, decides on the

budgets of the Federation, and receives the audited accounts and approves them. The Council

also elects from among its members a “Meeting of Officers” Committee and Program

Committees as required and appoints their chairpersons.

The LWF Secretariat, headed by the General Secretary, carries out the tasks of the Federation.

The General Secretary is assisted in carrying out his duties by the Communion Office

Leadership Team composed of the heads of departments/units within the Communion Office.

The Council authorizes the structure and terms of reference of the Communion Office. The

General Secretary is responsible to the Council for conducting the business of the Federation

and carrying out the decisions of the Assembly and the Council.

Page 6 of 27

The financial statements of the LWF for the year ended 31 December 2016 are consolidated to

include:

General Secretariat & Department for Planning and Operations (Gen Sec)

Department for Theology and Public Witness (DTPW)

Department for Mission and Development (DMD)

Department for World Service (DWS)

Branch offices of the Department for World Service (Field Offices)

The consolidated financial statements presented do not include the results of the Department

for World Service associated programs. Each of these has its own legal status separate from

that of the LWF and the LWF exercises no control over them.

2. Summary of significant accounting policies

The financial statements will be put to the Members for approval at the Organization’s Annual

Meeting to be held in Windhoek, Namibia in May 2017.

These financial statements were authorized for issue on 25 April 2017 by the General Secretary

2.1 Statement of compliance

The consolidated financial statements have been prepared in accordance with International

Financial Reporting Standards.

2.2 Basis of preparation

The consolidated financial statements have been prepared under the historical cost convention,

except for securities which are stated at fair value. Fair value is the amount for which an asset

or a liability could be exchanged between knowledgeable and willing parties in an arm’s length

transaction.

Preparation of the consolidated financial statements requires the use of estimates and

assumptions that affect the reported amounts of assets and liabilities and disclosures of

contingent assets and liabilities at the date of the consolidated financial statements and the

reported amounts of revenues and expenses during the reporting period. Although these

estimates are based on management’s best knowledge of current events and actions, actual

results ultimately may differ from those estimates and the original estimates and assumptions

will be modified as appropriate in the year in which the circumstances change.

2.3 Adoption of new standards, amendments and interpretations effective in 2016

New and revised standards and interpretations, issued but not yet effective, have been

reviewed to identify the nature of the future changes in accounting policy and to estimate the

effect of any necessary changes in the consolidated income statement and financial position

upon their adoption.

Page 7 of 27

- The Federation has adopted the following new and amended IFRSs as of January 1,

2016:

- Amendments to IAS 1 – ‘Presentation of Financial Statements’ (effective for annual

periods beginning on or after 1 January 2016, prospective application)

- Amendment to IAS 16 and IAS 38 - 'Clarification of Acceptable Methods of

Depreciation and Amortisation' (effective for annual periods beginning on or after 1

January2016,prospectiveapplication)

- Annual Improvements to IFRSs 2012-2014 Cycle (effective for annual periods on or

after 1 January 2016):

This set of amendments impacts 4 standards:

- IFRS 5, 'Non-current assets held for sale and discontinued operations' regarding

methods of disposal.

- IFRS 7, 'Financial instruments: Disclosures', (with consequential amendments to IFRS

1) regarding servicing contracts.

- IAS 19,'Employee benefits' regarding discount rates.

- IAS 34, 'Interim financial reporting' regarding disclosure of information.

These amendments do not have a significant impact on the Federation’s consolidated financial

statements.

The following new or amended IFRS standards or interpretations have not yet been adopted

but need to be adopted in financial statements issued for period starting January 1, 2016 or

later:

- IFRS 15 Revenue from Contracts with Customers (effective for annual periods beginning

on or after January 1, 2018, retrospective application, earlier application permitted)

- IFRS 9 Financial Instruments (effective for annual periods beginning on or after January

1, 2018, retrospective application, earlier application permitted)

- IFRS 16 Leases (effective for annual periods beginning on or after January 1, 2019)

2.4 Basis of consolidation

The financial statements of the LWF are consolidated to include all departments of the Geneva

Communion Office and branch offices of the Department for World Service.

Transactions between departments and between departments and branch offices as well as

balances are eliminated.

a) Associated Programs

Former branch offices of the Department for World Service which have registered as legal

entities under local country statutory regulations and are not legally controlled by the LWF

have not been consolidated.

b) Related Parties

The Lutheran LWF Foundation for Inter-confessional Research with offices in Strasbourg, the

LWF Foundation (Endowment Fund), and the LWF Staff Welfare Plan have not been

consolidated in the financial statements. They are separate legal entities with their own boards.

LWF has representation on these boards but no controlling interest.

c) Assembly

The Assembly normally meets every six years. Up until the Assembly in Stuttgart in 2010,

separate books of account were maintained for the income and expenditure related to the

Page 8 of 27

Assembly and audited financial statements were prepared. The balance with the Assembly was

included in the financial statements. Henceforth, the Assembly will be included in the LWF

consolidated financial statements as a project.

The next Assembly will be held in Namibia in May 2017.

2.5 Restricted/unrestricted funds

The financial statements distinguish between Restricted and Unrestricted use funds. Restricted

use funds are those funds received from third parties who have imposed restrictions on the

purposes for which they may be used. Unrestricted use funds are those funds where there are

no externally imposed restrictions and include assets freely available or appropriated to

reserves for internally designated purposes.

2.6 Revenue and expenditure recognition

Restricted use funds are normally received as a result of a specific solicitation or with donor

imposed restrictions and are recognized as income over the duration of the program/project in

proportion to the achievement of the conditions attached to the contributions. Income for the

year is therefore equal to expenditure. Contributions received but not yet recognized are

included in Current Liabilities. Contributions not yet received relating to expenditure already

recognized are included in Current Assets.

In some instances, in-kind contributions are recognized in the financial statements and an

equal amount of expenditure is recorded. In-kind contributions are recorded at the value noted

in the accompanying shipping documents upon receipt.

Membership fees are fixed by the LWF Council and are recognized in the year they fall due.

The balances of memberships due at the end of the year are reviewed to reflect the probability

of the amount to be cashed. This does not invalidate the obligation on members to pay the

amounts owing.

Investment income is recognized on an accruals basis. The investment income together with

foreign exchange gains and losses and gains and losses on investments is allocated between the

various LWF departments according to the opening balance of reserves and net project/other

grant balances.

2.7 Area projects and general subsidies

Expenditure in respect of area projects in foreign countries is based upon remittances to

respective local churches or organizations. In accordance with established practice,

examination by the auditors has been made on the underlying documentation substantiating

such transfers in conformity with the agreed list of projects in the composite statement of

needs.

2.8 Foreign currency transactions

The consolidated financial statements are presented in EURO.

In 2011 the functional currency was changed from U.S. Dollar to Euro. The change in

functional currency was decided in order to better reflect the evolution of the activities. Indeed,

Page 9 of 27

most of the transactions now occur with counterparts in Europeans countries. Consequently

Euro provides a better image of the financial position and of the results of operations than U.S.

Dollar.

As of January 1, 2011, the presentation and functional currency of the LWF is the Euro. The

books of account are maintained in Euro. Assets and liabilities, excluding securities and fixed

assets, denominated in currencies other than the Euro have been translated at the December

31, 2016 rate of exchange per the European Commission “InforEuro” website. Foreign

exchange gains/losses are included within the Financial Income section of the Consolidated

Income and expenditure Statement.

Income and expenditure has been translated into Euro monthly using the previous month

exchange rate per the European Commission “InforEuro” website. Exchange gains/losses

resulting from the application of the accounting principles outlined above are credited/charged

to the Statement of Income and Expenditure.

2.9 Derivative financial instruments

The LWF may, at certain times, use derivative financial instruments, comprising forward

foreign exchange contracts to manage its exposure to foreign exchange risk. Derivative

financial instruments are stated at fair value. The fair value of forward exchange contracts is

determined using quoted forward rates at the balance sheet date. Derivatives are not

designated as effective accounting hedge instruments and as a result any gain or loss of fair

value is recognized in the Income and Expenditure Statement.

2.10 Cash and cash equivalents

The LWF considers cash on hand, amounts due from banks and short-term deposits with

banks to be cash and cash equivalents.

2.11 Financial assets

Financial assets are classified as financial assets at fair value through profit or loss, loans and

receivables, held-to maturity investments, or available-for-sale financial assets. The

classification depends on the purpose for which the financial assets were acquired.

Management determines the classification of its financial assets at initial recognition. All

regular way purchases and sales of financial assets are recognised at the settlement date i.e. the

date that the asset is delivered to or by the Federation. Financial assets are classified as current

assets, unless they are expected to be realised beyond twelve months of the balance sheet date.

Financial assets are derecognised when the rights to receive cash flows from the investments

have expired or have been transferred and the Federation has transferred substantially all

risks and rewards of ownership.

Detailed disclosures can be found in Note 3.2 to the consolidated financial statements.

Information on financial risk management is described in the Note 2.20

Dividends and interest earned are included in the line financial income.

a) Financial assets at fair value through profit or loss

Financial assets at fair value through profit or loss are financial assets held for trading. A

financial asset is classified in this category if acquired for the purpose of selling in the near

term. Derivatives are classified as held for trading unless they are designated and effective

Page 10 of 27

hedging instruments. When recognised initially, they are measured at fair value, and

transaction costs are expensed in the income statement. For held for trading investments, gains

or losses are recognised in the income statement.

b) Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinable payments

that are not quoted in an active market. They are carried at amortised cost using the effective

interest method. For loans and receivables, gains or losses are recognised in the income

statement when derecognised, impaired, or through the amortisation process. Loans and

receivables are classified as accounts receivable in the balance sheet (see Note 3.4).

c) Held-to-maturity investments

Debt securities with fixed or determinable payments and fixed maturity are classified as held-

to-maturity when the Federation has the positive intention and ability to hold to maturity.

These investments are measured at amortised cost using the effective interest method, less any

impairment losses. For held-to-maturity investments, gains or losses are recognised in the

income statement when derecognised, impaired, or through the amortisation process.

d) Available-for-sale financial assets

Available-for-sale financial assets are non-derivative financial assets that are designated as

such or not classified in any of the other categories. They are measured initially at fair value,

plus directly attributable transaction costs. At the end of each period, the book value is

adjusted to the fair value with a corresponding entry in a separate component of equity until

the investment is derecognised or determined to be impaired at which time the cumulative gain

or loss previously reported in equity is included in the income statement. When denominated in

a foreign currency, any monetary item is adjusted for the effect of any change in exchange

rates with unrealised gain or loss booked in the income statement.

For quoted equity instruments, the fair value is the market value being calculated by reference

to share exchange quoted selling prices at close of business on the balance sheet date. For non-

quoted financial assets, they are re-valued at fair value based on observable market

transactions and if not available based on prices given by reputable financial institutions or on

the price of the latest transaction.

An available-for-sale instrument is impaired when in management’s opinion there is objective

evidence that the estimated future recoverable amount is less than the carrying amount and

when its market value is 20% or more below its original cost for a sustained six-month period.

When an impairment loss has previously been recognised, further declines in value are

recorded as an impairment loss in the income statement. The charge is recorded within the

financial income line of the consolidated income statement. Impairment losses recognised on

equity instruments are not reversed in the income statement. Impairment losses recognised on

debt instruments shall be reversed through the income statement if the increase of the fair

value of available-for-sale debt instrument objectively relates to an event occurring after the

impairment charge.

The Lutheran World Federation has no financial assets which belong to categories c.) and d.).

2.12 Inventories

Inventories purchased from Restricted use Funds are expensed in the year of purchase. Rights

over inventories would not generate future economic benefit to the LWF due to the short term

nature of program contracts and the terms of contracts where rights over residual program

assets are vested with the grantors.

Page 11 of 27

The only material inventories purchased from Unrestricted use Funds are held at the DWS

program in Jerusalem. These inventories consist of medical supplies for the Augusta Victoria

Hospital (AVH) that the program runs. They are accounted for at cost which does not exceed

market value and recognized by the first-in, first-out method.

2.13 Fixed assets

a) Tangible

Tangible fixed assets purchased from Restricted use Funds are expensed in the year of

purchase. It is considered improbable that such expenditures will generate future economic

benefit to the LWF due to the short term nature of program contracts and the terms of

contracts where rights over residual program assets are vested with the grantors.

Tangible assets at the Secretariat in Geneva, comprising computer equipment and associated

software development costs, purchased from Unrestricted use Funds are capitalized and

amortized as detailed in 2.14. Assets of a capital nature with a cost lower than CHF 1,500

(laptops CHF 1,200) are not capitalized.

Tangible assets in the Department for World Service located outside of Geneva and purchased

from Unrestricted use Funds, comprising buildings and land improvements, vehicles and office

equipment are capitalized and amortized as detailed in 2.14. Assets of a capital nature with a

cost lower than USD 10,000 are not capitalized.

Gains and losses on disposals are determined by comparing proceeds with carrying amount

and are recognized in the Income and Expenditure Statement.

Repairs and maintenance costs are charged in the Income and Expenditure Statement during

the financial period in which they are incurred.

Subsequent expenditure is capitalized only when it increases the probable future economic

benefits of the asset.

b) Intangible

Acquired computer software at the Secretariat is capitalized on the basis of the costs incurred

to acquire and bring the specific software to use. Amortization is calculated on the straight-line

method as detailed in 2.14.

Costs associated with maintaining software are charged in the Income and Expenditure

Statement during the financial period in which they are incurred.

2.14 Fixed assets - depreciation

a) Secretariat

Based on the past experience the fixed assets located in Geneva are depreciated using the

straight-line method, over their estimated useful lives, as follow:

Office furniture & equipment 5 years

Computers equipment (except laptops) 4 years

Laptops 3 years

Page 12 of 27

Depreciation for a full year commences in the year of purchase.

The useful lives are reviewed and adjusted if appropriate at each balance sheet date.

b) Field

Based on the past experience of the useful life expectancy, the rate of depreciation is set by

each individual country program not to exceed the following rate per year by category:

Building 25 years

Plant & equipment 15 years

Vehicles 5 years

Office furniture & equipment 5 years

Computers 4 years

Depreciation for a full year commences in the year of purchase.

The useful lives are reviewed and adjusted if appropriate at each balance sheet date.

2.15 Impairment

The carrying amount of the LWF’s assets, other than financial assets (see Notes 2.10, 2.11) and

inventories (see Note 2.12), are reviewed at each balance sheet date to determine whether there

is any indication of impairment or, if earlier, whenever events or changes in circumstances

indicate that the carrying amount may not be recoverable.

An impairment loss is recognized whenever the carrying amount of an asset exceeds its

recoverable amount. Recoverable amount is the higher of the asset’s net selling price or its

value in use. Impairment losses are recognized in the Income and Expenditure Statement.

An impairment loss is reversed if there is an upward revision of the recoverable amount. An

impairment loss is only reversed to the extent that the asset’s carrying amount does not exceed

the carrying amount that would have been determined net of depreciation or amortization, if

no impairment loss had been recognized.

2.16 Provisions

Provisions are recognized when there is a legal or constructive obligation as a result of past

events, it is probable that an outflow of resources will be required to settle down that

obligation, and the amounts can be reliably estimated.

2.17 Reserves

Reserves are classified as either Unrestricted or Restricted reserves. Unrestricted reserves are

earmarked as detailed below:

a) General reserve

This reserve represents an unrestricted amount and is used to account for all resources over

which the department has discretionary control. It can be used to cover ongoing commitments

in case of emergencies.

Page 13 of 27

b) Scholarship Fund/DMD Program Fund

These funds are to be used for the Department for Mission and Development.

c) Field designated funds

These various funds are available exclusively for use in each field program according to the

definition of the fund.

2.18 Employee benefit costs

a) Employee termination/repatriation benefits/accrued vacation (ALT/ALTO)

These benefits are recognized proportionately as accrued over the employment period of

personnel. They exist to meet any termination and settling out expenses under present

contractual LWF working conditions for both Geneva (ALT – assignment, leave, termination

and accrued vacation monetary equivalent) and field (ALTO – assignment, leave, termination

for overseas staff) based staff.

b) Retirement benefit obligations

Until the end of December 2011, the LWF operated a single pension fund for expatriate field

staff and all headquarters staff. Pension obligations were covered by independent funds which

were held in a single, separate legal entity that is governed by Swiss law. On January 1, 2012

all the assets and liabilities of the fund were transferred to the Abendrot Foundation, Basel and

the pension obligations were taken over by Abendrot. The LWF pension fund was liquidated in

June 2014. For the purposes of these consolidated financial statements post–retirement pension

costs have been accounted for in accordance with IAS 19 (see note 3.20).

Staff employed locally by the LWF, receive social benefits in accordance with the legislation of

the countries concerned and the local collective staff agreements. The cost of such benefits is

recognized on an accruals basis in these consolidated financial statements.

c) Termination benefits

Termination benefits are payable whenever an employee’s employment is terminated before

the normal retirement date or contract completion date.

Termination benefits are recognized on the basis of a formal committed plan to terminate the

employment of current employees.

2.19 Leases

A lease is an agreement whereby the lessor conveys to the lessee in return for a payment or

series of payments the right to use an asset for an agreed period of time. An operating lease is a

lease that does not transfer substantially all the risks and rewards incidental to ownership.

The LWF had no operating or financial leases of a material nature.

Page 14 of 27

2.20 Financial risk management

The LWF is exposed to a variety of financial risks namely: market (including foreign currency

risk and pricing risk); credit risk; liquidity risk and interest rate risk. The LWF seeks to

actively minimize potential adverse effects arising from this exposure as detailed below.

a) Market risk

Foreign currency risk

Foreign currency risk arises primarily from contributions that are denominated in a currency

other than Euro. The main currencies giving rise to this risk are the U.S. Dollar , Swiss Franc

and Swedish Kroner. The LWF ensures that net exposure is kept to an acceptable level, by

selling foreign currencies at spot rates where necessary to address short-term needs.

Foreign currency risk arises from non-Euro securities held in the investment portfolio and for

which advice is given by professional investment managers.

Price risk

The LWF is exposed to securities price risk because of investments measured at fair value

through profit and loss. Unrealized gains/losses arising from fluctuations in prices are actively

monitored by professional investment managers. There is no exposure to commodity price risk.

b) Credit risk

The LWF’s principal receivables are with its member churches, governmental and

intergovernmental agencies where credit risk is considered to be low.

Securities transactions are held only with well-established banks and financial institutions. The

funds are invested either in short term deposits or in premium securities.

There is no significant concentration of credit risk. The maximum exposure to credit risk is

limited to the carrying amount of the monetary financial assets.

Page 15 of 27

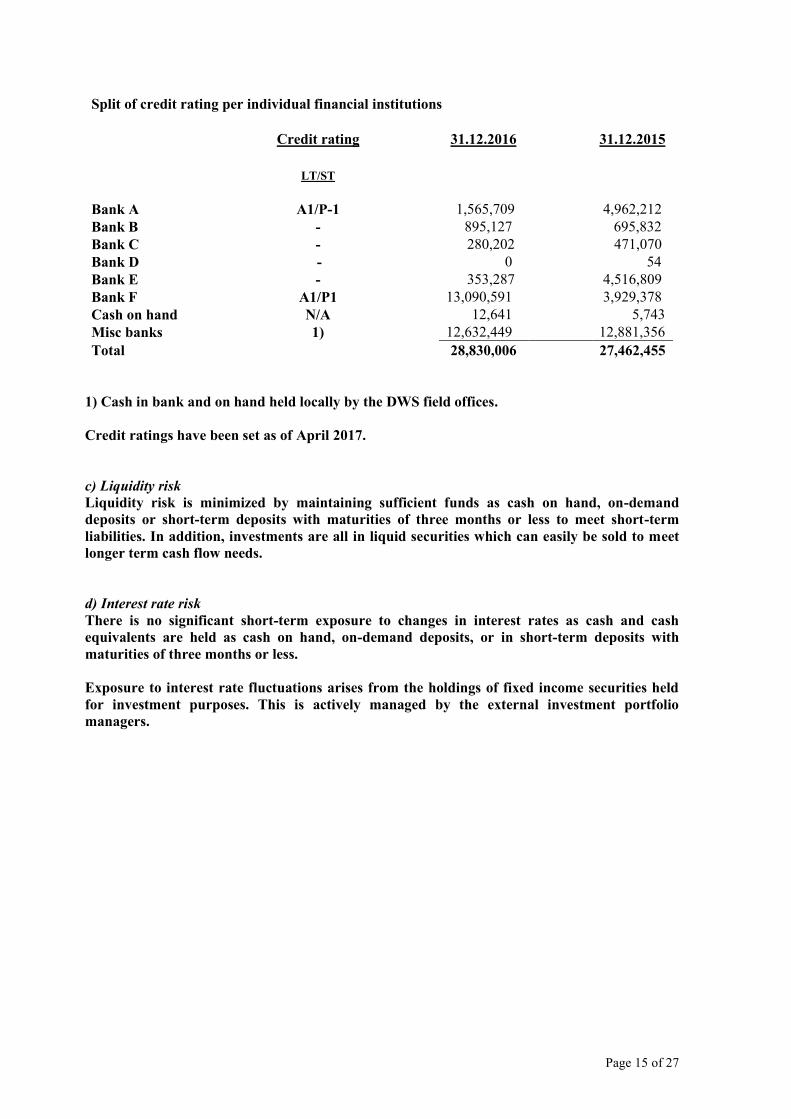

Split of credit rating per individual financial institutions

Credit rating 31.12.2016 31.12.2015

LT/ST

Bank A A1/P-1 1,565,709 4,962,212

Bank B - 895,127 695,832

Bank C - 280,202 471,070

Bank D - 0 54

Bank E - 353,287 4,516,809

Bank F A1/P1 13,090,591 3,929,378

Cash on hand N/A 12,641 5,743

Misc banks 1) 12,632,449 12,881,356

Total 28,830,006 27,462,455

1) Cash in bank and on hand held locally by the DWS field offices.

Credit ratings have been set as of April 2017.

c) Liquidity risk

Liquidity risk is minimized by maintaining sufficient funds as cash on hand, on-demand

deposits or short-term deposits with maturities of three months or less to meet short-term

liabilities. In addition, investments are all in liquid securities which can easily be sold to meet

longer term cash flow needs.

d) Interest rate risk

There is no significant short-term exposure to changes in interest rates as cash and cash

equivalents are held as cash on hand, on-demand deposits, or in short-term deposits with

maturities of three months or less.

Exposure to interest rate fluctuations arises from the holdings of fixed income securities held

for investment purposes. This is actively managed by the external investment portfolio

managers.

Page 16 of 27

e.) Financial instrument by category

December 31, 2015 Loans and

receivables

Assets at

fair value

through the

profit and

loss

Derivatives

used for

hedging

Available

for-sale Total

Assets as per balance sheet

Available-for-sale financial assets

Derivative financial instruments

Trade and other receivables 30,548,708 30,548,708

Other financial assets at fair value

through profit or loss 2,001,657 2,001,657

Cash and cash equivalents 27,462,455 27,462,455

Total 58,011,163 2,001,657 0 0 60,012,820

December 31, 2016 Loans and

receivables

Assets at

fair value

through the

profit and

loss

Derivatives

used for

hedging

Available

for-sale Total

Assets as per balance sheet

Available-for-sale financial assets 0

Derivative financial instruments 0

Trade and other receivables 39,068,612 39,068,612

Other financial assets at fair value

through profit or loss 1,929,006 1,929,006

Cash and cash equivalents 28,830,006 28,830,006

Total

67,898,618 1,929,006 0 0 69,827,624

Page 17 of 27

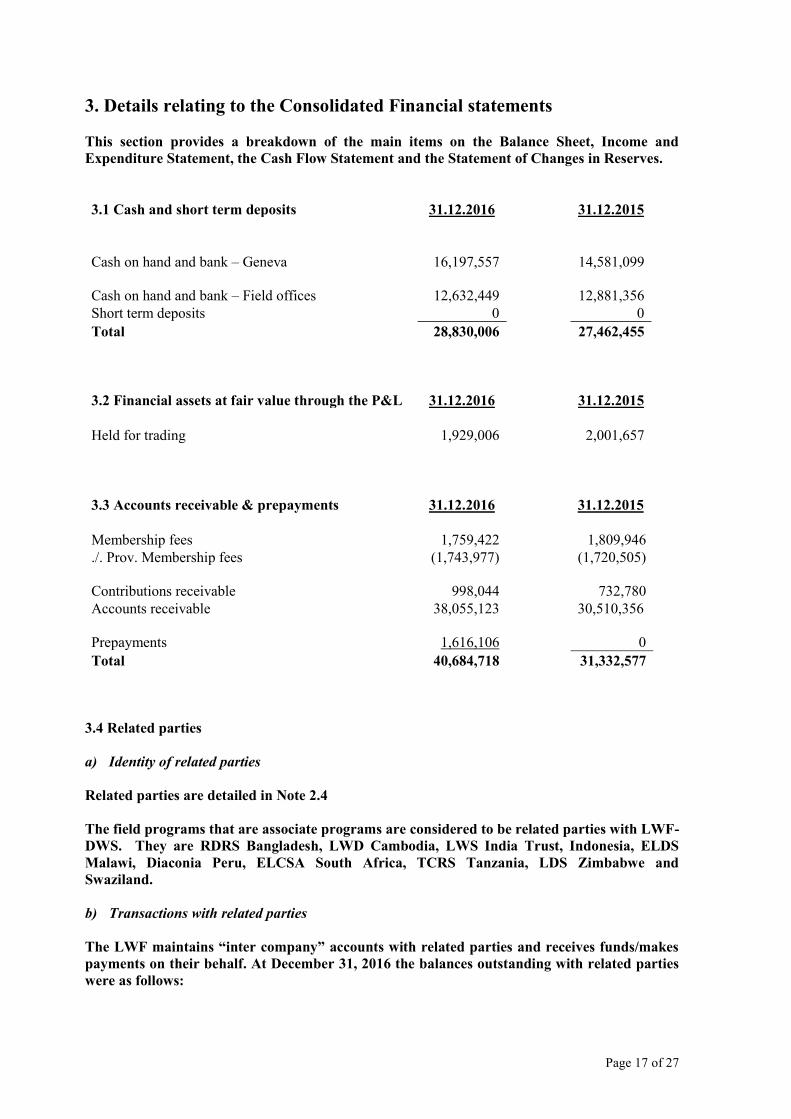

3. Details relating to the Consolidated Financial statements

This section provides a breakdown of the main items on the Balance Sheet, Income and

Expenditure Statement, the Cash Flow Statement and the Statement of Changes in Reserves.

3.1 Cash and short term deposits 31.12.2016 31.12.2015

Cash on hand and bank – Geneva 16,197,557 14,581,099

Cash on hand and bank – Field offices 12,632,449

12,881,356

Short term deposits 0 0

Total 28,830,006 27,462,455

3.2 Financial assets at fair value through the P&L 31.12.2016 31.12.2015

Held for trading 1,929,006 2,001,657

3.3 Accounts receivable & prepayments 31.12.2016 31.12.2015

Membership fees 1,759,422 1,809,946

./. Prov. Membership fees (1,743,977) (1,720,505)

Contributions receivable

998,044 732,780

Accounts receivable 38,055,123 30,510,356

Prepayments

1,616,106 0

Total 40,684,718 31,332,577

3.4 Related parties

a) Identity of related parties

Related parties are detailed in Note 2.4

The field programs that are associate programs are considered to be related parties with LWF-

DWS. They are RDRS Bangladesh, LWD Cambodia, LWS India Trust, Indonesia, ELDS

Malawi, Diaconia Peru, ELCSA South Africa, TCRS Tanzania, LDS Zimbabwe and

Swaziland.

b) Transactions with related parties

The LWF maintains “inter company” accounts with related parties and receives funds/makes

payments on their behalf. At December 31, 2016 the balances outstanding with related parties

were as follows:

Page 18 of 27

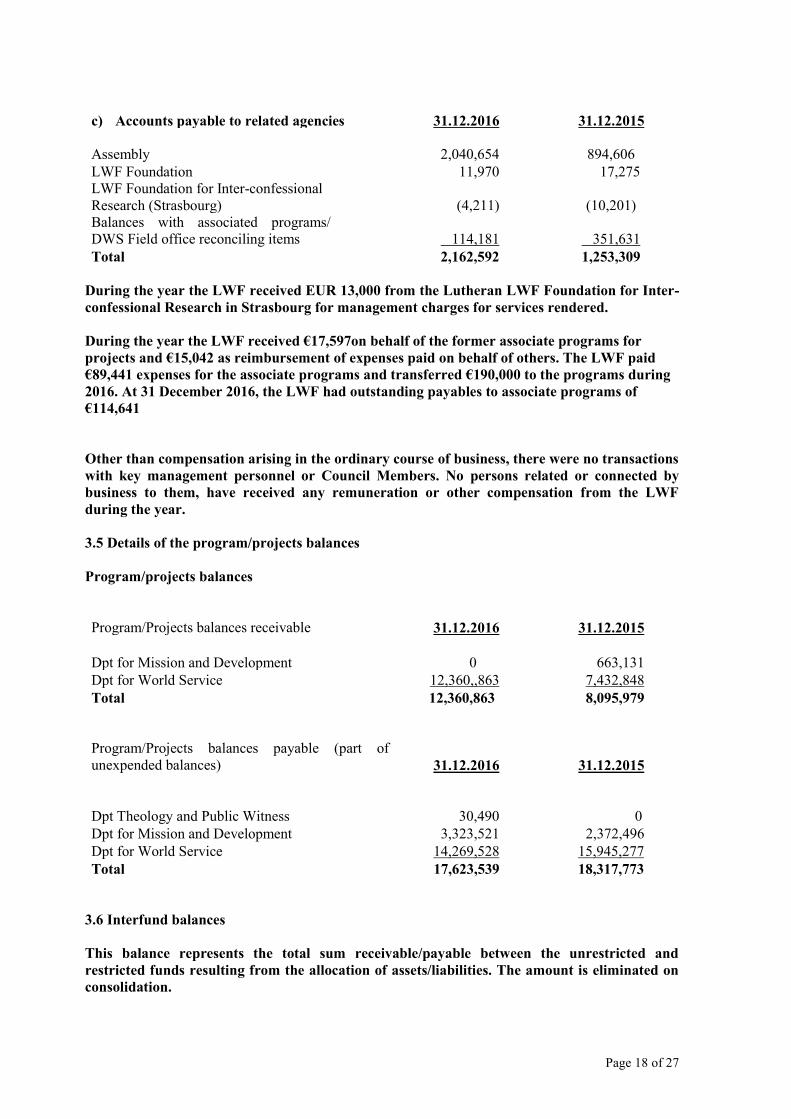

c) Accounts payable to related agencies 31.12.2016 31.12.2015

Assembly 2,040,654

894,606

LWF Foundation 11,970 17,275

LWF Foundation for Inter-confessional

Research (Strasbourg) (4,211) (10,201)

Balances with associated programs/

DWS Field office reconciling items 114,181 351,631

Total 2,162,592 1,253,309

During the year the LWF received EUR 13,000 from the Lutheran LWF Foundation for Inter-

confessional Research in Strasbourg for management charges for services rendered.

During the year the LWF received €17,597on behalf of the former associate programs for

projects and €15,042 as reimbursement of expenses paid on behalf of others. The LWF paid

€89,441 expenses for the associate programs and transferred €190,000 to the programs during

2016. At 31 December 2016, the LWF had outstanding payables to associate programs of

€114,641

Other than compensation arising in the ordinary course of business, there were no transactions

with key management personnel or Council Members. No persons related or connected by

business to them, have received any remuneration or other compensation from the LWF

during the year.

3.5 Details of the program/projects balances

Program/projects balances

Program/Projects balances receivable 31.12.2016 31.12.2015

Dpt for Mission and Development 0 663,131

Dpt for World Service 12,360,,863 7,432,848

Total 12,360,863 8,095,979

Program/Projects balances payable (part of

unexpended balances) 31.12.2016 31.12.2015

Dpt Theology and Public Witness

30,490 0

Dpt for Mission and Development 3,323,521 2,372,496

Dpt for World Service 14,269,528 15,945,277

Total 17,623,539 18,317,773

3.6 Interfund balances

This balance represents the total sum receivable/payable between the unrestricted and

restricted funds resulting from the allocation of assets/liabilities. The amount is eliminated on

consolidation.

Page 19 of 27

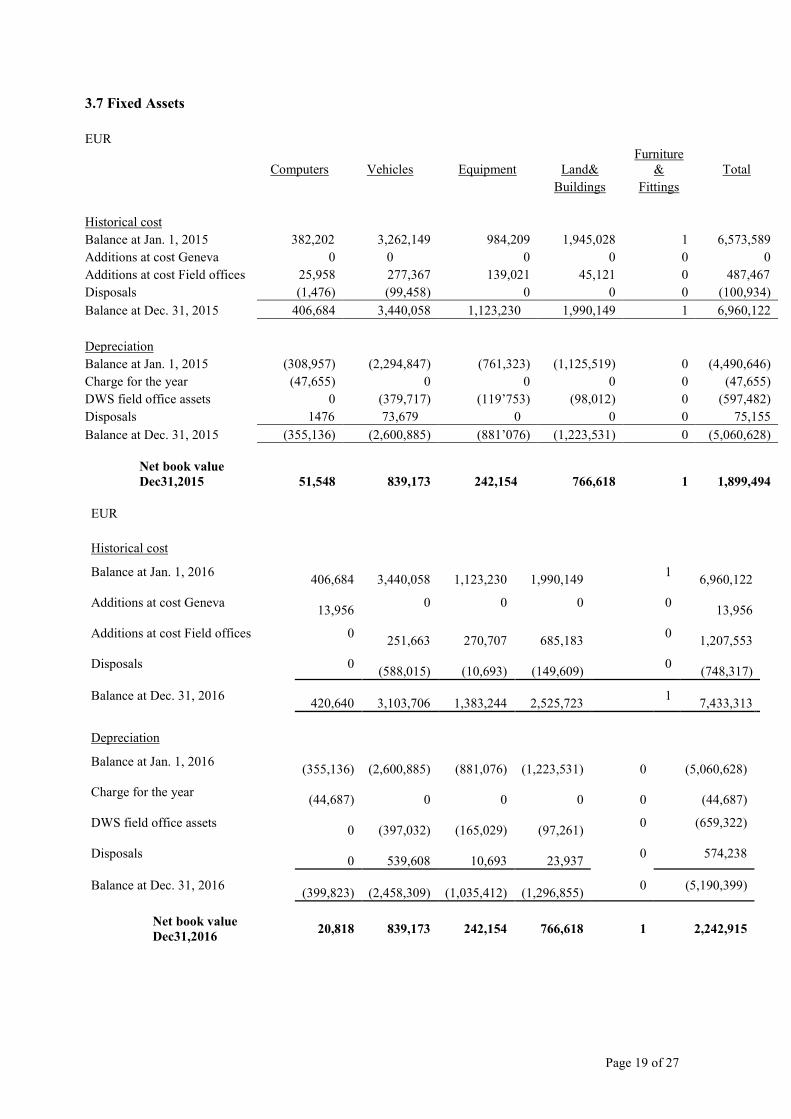

3.7 Fixed Assets

EUR

Computers Vehicles Equipment Land&

Furniture

& Total

Buildings Fittings

Historical cost

Balance at Jan. 1, 2015 382,202 3,262,149 984,209 1,945,028 1 6,573,589

Additions at cost Geneva 0 0 0 0 0 0

Additions at cost Field offices 25,958 277,367 139,021 45,121 0 487,467

Disposals (1,476) (99,458) 0 0 0 (100,934)

Balance at Dec. 31, 2015 406,684 3,440,058 1,123,230 1,990,149 1 6,960,122

Depreciation

Balance at Jan. 1, 2015 (308,957) (2,294,847) (761,323) (1,125,519) 0 (4,490,646)

Charge for the year (47,655) 0 0 0 0 (47,655)

DWS field office assets 0 (379,717) (119’753) (98,012) 0 (597,482)

Disposals 1476 73,679 0 0 0 75,155

Balance at Dec. 31, 2015 (355,136) (2,600,885) (881’076) (1,223,531) 0 (5,060,628)

Net book value

Dec31,2015

51,548 839,173 242,154 766,618 1 1,899,494

EUR

Historical cost

Balance at Jan. 1, 2016

406,684

3,440,058

1,123,230

1,990,149 1

6,960,122

Additions at cost Geneva

13,956 0 0 0 0

13,956

Additions at cost Field offices 0

251,663

270,707

685,183 0

1,207,553

Disposals

0

(588,015)

(10,693)

(149,609) 0

(748,317)

Balance at Dec. 31, 2016

420,640

3,103,706

1,383,244

2,525,723 1

7,433,313

Depreciation

Balance at Jan. 1, 2016

(355,136)

(2,600,885)

(881,076)

(1,223,531)

0

(5,060,628)

Charge for the year

(44,687)

0

0

0

0

(44,687)

DWS field office assets

0

(397,032)

(165,029)

(97,261) 0 (659,322)

Disposals

0

539,608

10,693

23,937 0 574,238

Balance at Dec. 31, 2016

(399,823)

(2,458,309)

(1,035,412)

(1,296,855) 0 (5,190,399)

Net book value

Dec31,2016

839,173 242,154 766,618 1 2,242,915 20,818

Page 20 of 27

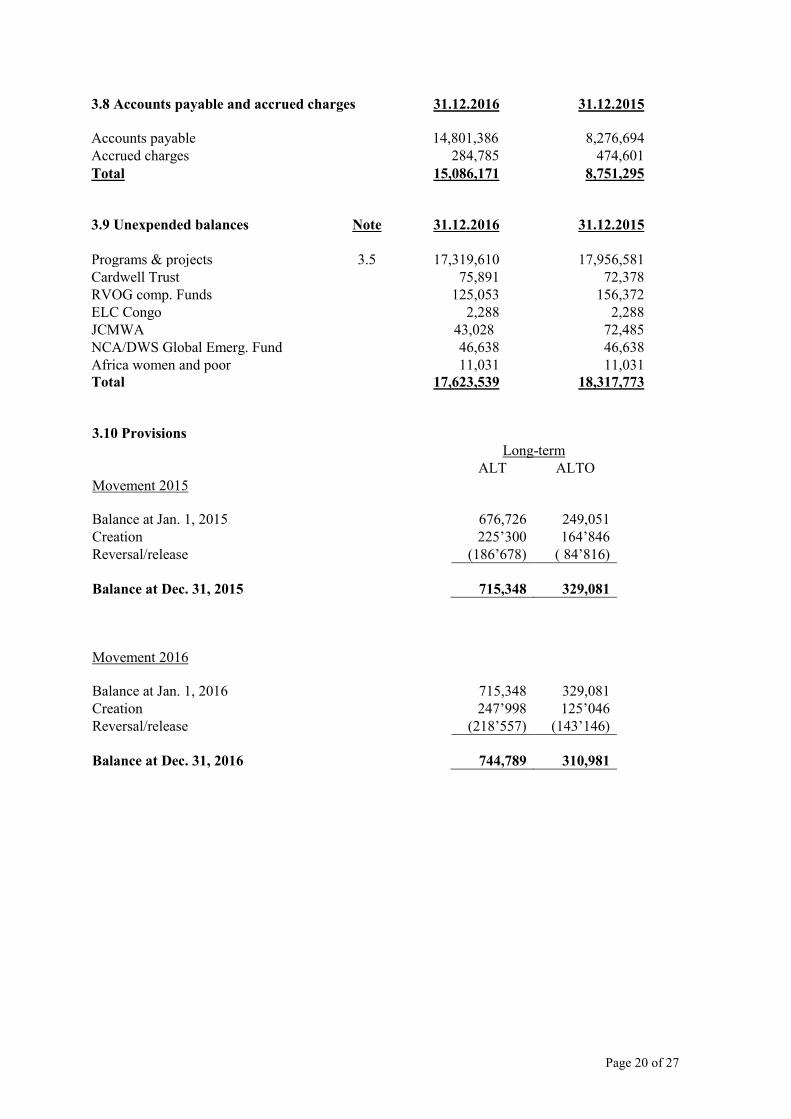

3.8 Accounts payable and accrued charges 31.12.2016 31.12.2015

Accounts payable 14,801,386 8,276,694

Accrued charges 284,785 474,601

Total 15,086,171 8,751,295

3.9 Unexpended balances Note 31.12.2016 31.12.2015

Programs & projects 3.5 17,319,610 17,956,581

Cardwell Trust 75,891 72,378

RVOG comp. Funds 125,053 156,372

ELC Congo 2,288 2,288

JCMWA 43,028 72,485

NCA/DWS Global Emerg. Fund 46,638 46,638

Africa women and poor 11,031 11,031

Total 17,623,539 18,317,773

3.10 Provisions

Long-term

ALT ALTO

Movement 2015

Balance at Jan. 1, 2015

676,726 249,051

Creation 225’300 164’846

Reversal/release (186’678) ( 84’816)

Balance at Dec. 31, 2015

715,348

329,081

Movement 2016

Balance at Jan. 1, 2016

715,348 329,081

Creation 247’998 125’046

Reversal/release (218’557) (143’146)

Balance at Dec. 31, 2016

744,789

310,981

Page 21 of 27

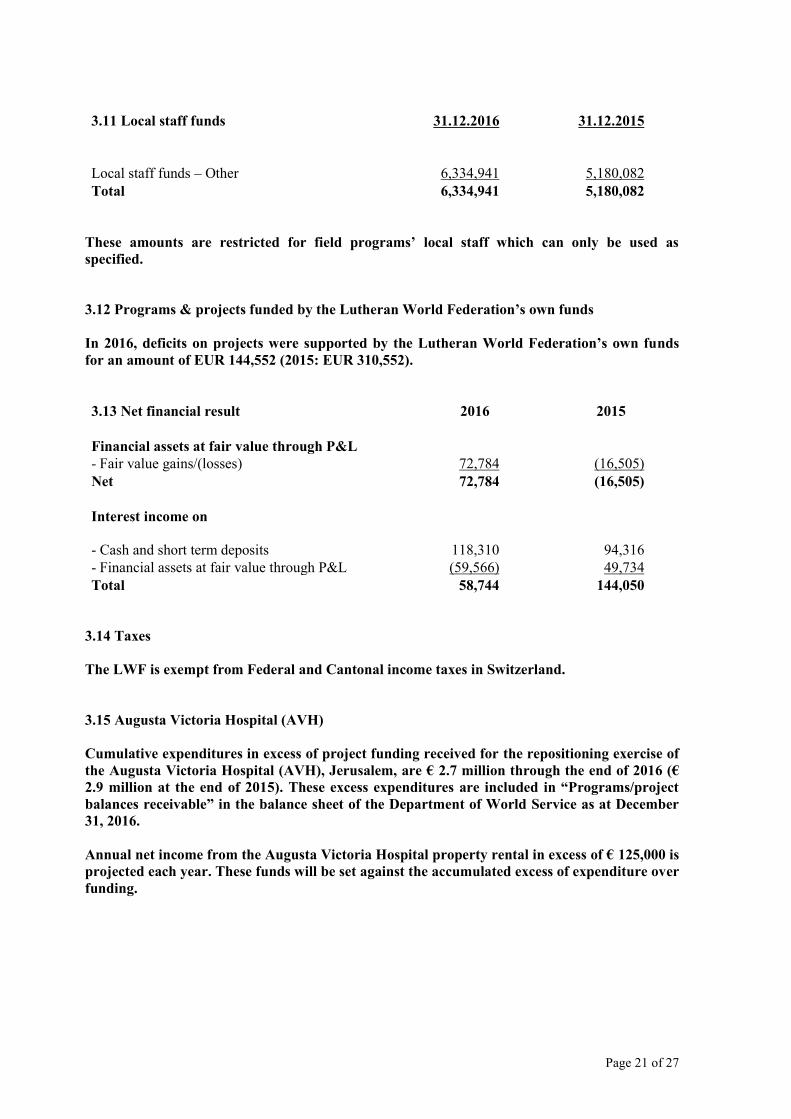

3.11 Local staff funds 31.12.2016 31.12.2015

Local staff funds – Other 6,334,941 5,180,082

Total 6,334,941 5,180,082

These amounts are restricted for field programs’ local staff which can only be used as

specified.

3.12 Programs & projects funded by the Lutheran World Federation’s own funds

In 2016, deficits on projects were supported by the Lutheran World Federation’s own funds

for an amount of EUR 144,552 (2015: EUR 310,552).

3.13 Net financial result 2016 2015

Financial assets at fair value through P&L

- Fair value gains/(losses) 72,784 (16,505)

Net 72,784 (16,505)

Interest income on

- Cash and short term deposits 118,310

94,316

- Financial assets at fair value through P&L (59,566) 49,734

Total 58,744 144,050

3.14 Taxes

The LWF is exempt from Federal and Cantonal income taxes in Switzerland.

3.15 Augusta Victoria Hospital (AVH)

Cumulative expenditures in excess of project funding received for the repositioning exercise of

the Augusta Victoria Hospital (AVH), Jerusalem, are € 2.7 million through the end of 2016 (€

2.9 million at the end of 2015). These excess expenditures are included in “Programs/project

balances receivable” in the balance sheet of the Department of World Service as at December

31, 2016.

Annual net income from the Augusta Victoria Hospital property rental in excess of € 125,000 is

projected each year. These funds will be set against the accumulated excess of expenditure over

funding.

Page 22 of 27

3.16 Contingent Liabilities

Medical Malpractice claims – Jerusalem Program:

The Hospital purchases professional and general liability insurance policies to cover medical

Malpractice claims. In 2016, the limit of coverage amounted to USD 2,500,000 equivalent to €

2,391,658 for each single claim. According to the estimates by the insurers concerning these

claims, the maximum liability of the Hospital in the medical malpractice claims outstanding at

December 31, 2016, in the form of the excess (deductible) amounts the Hospital is required to

settle in accordance with the terms of the insurance policies, was € 679,231.

3.17 Donations in kind

In some instances, in-kind contributions are recognized in the financial statements and

an equal amount of expenditure is recorded. In 2016 and 2015, respectively, the

amount included in revenue and expenditure related to in-kind contributions is EUR

1,459,333 and EUR 571,504. In-kind contributions are recorded at the value noted in

the accompanying shipping documents upon receipt.

3.18 Capital commitments

There were no capital expenditure commitments at 31 December 2016.

3.19 Retirement benefit obligations

Headquarters and expatriate field staff (see note 2.18b) above)

Page 23 of 27

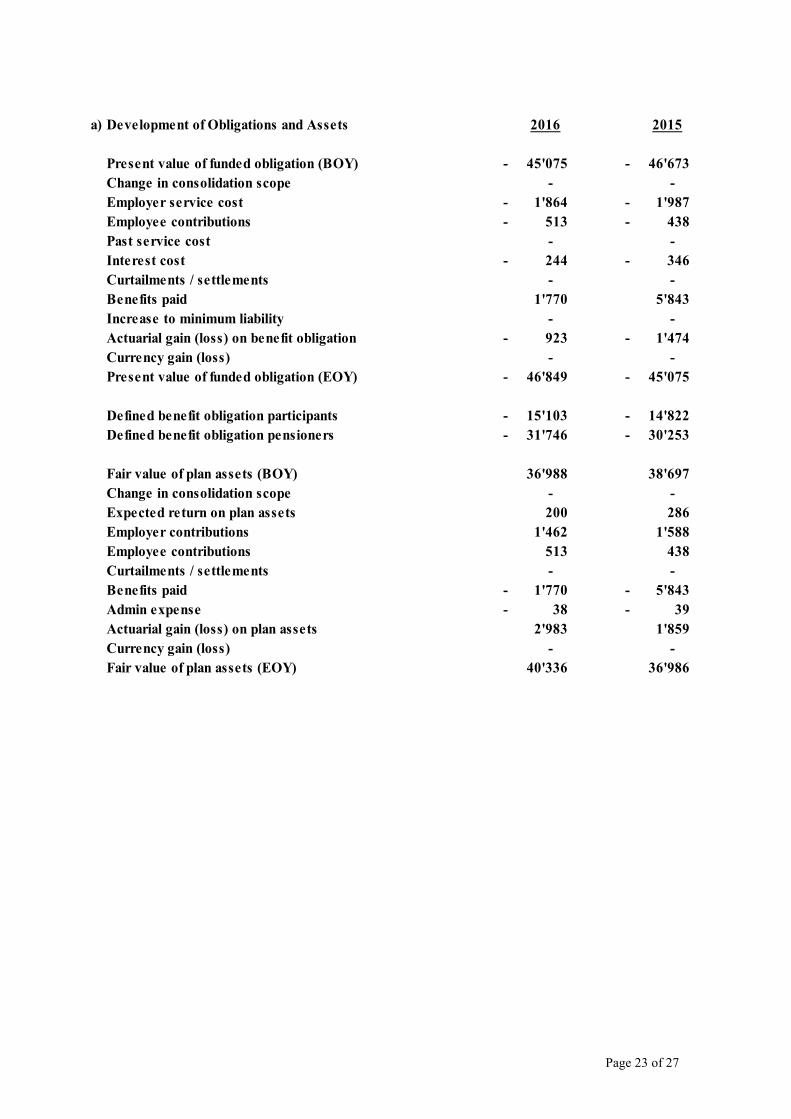

a) Development of Obligations and Assets 2016 2015

Present value of funded obligation (BOY) 45'075 - 46'673 -

Change in consolidation scope - -

Employer service cost 1'864 - 1'987 -

Employee contributions 513 - 438 -

Past service cost - -

Interest cost 244 - 346 -

Curtailments / settlements - -

Benefits paid 1'770 5'843

Increase to minimum liability - -

Actuarial gain (loss) on benefit obligation 923 - 1'474 -

Currency gain (loss) - -

Present value of funded obligation (EOY) 46'849 - 45'075 -

Defined benefit obligation participants 15'103 - 14'822 -

Defined benefit obligation pensioners 31'746 - 30'253 -

Fair value of plan assets (BOY) 36'988 38'697

Change in consolidation scope - -

Expected return on plan assets 200 286

Employer contributions 1'462 1'588

Employee contributions 513 438

Curtailments / settlements - -

Benefits paid 1'770 - 5'843 -

Admin expense 38 - 39 -

Actuarial gain (loss) on plan assets 2'983 1'859

Currency gain (loss) - -

Fair value of plan assets (EOY) 40'336 36'986

Page 24 of 27

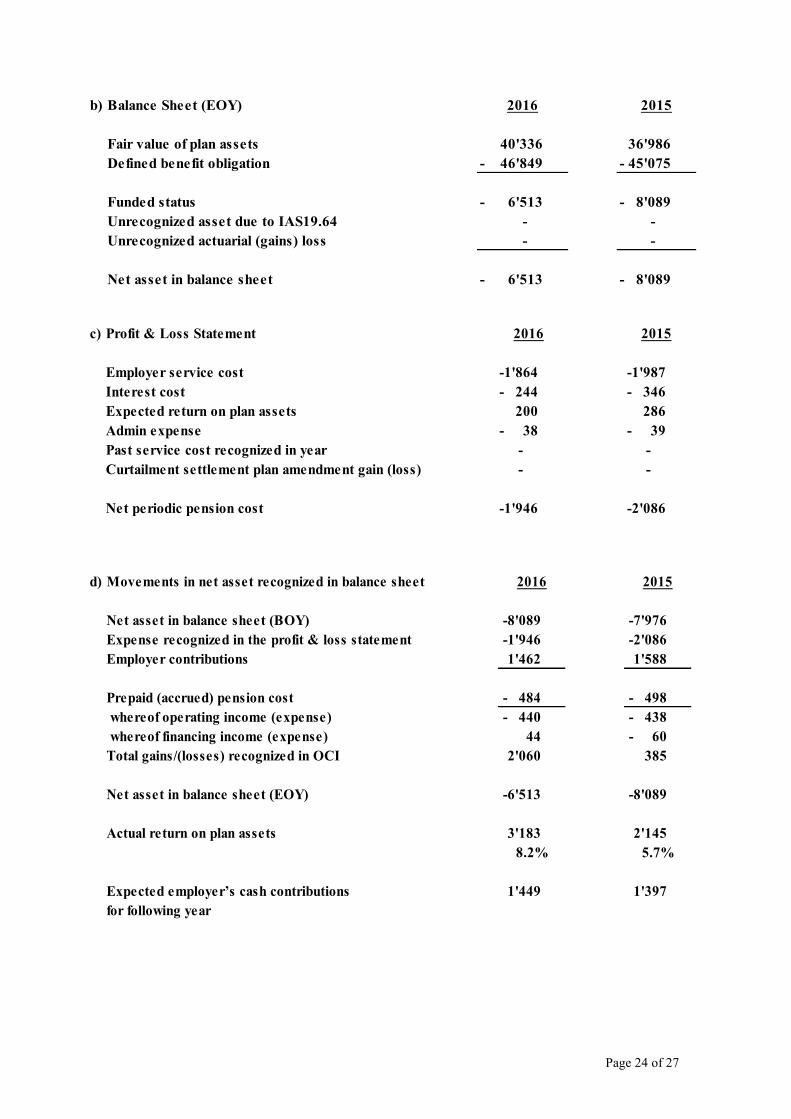

b) Balance Sheet (EOY) 2016 2015

Fair value of plan assets 40'336 36'986

Defined benefit obligation 46'849 - 45'075 -

Funded status 6'513 - 8'089 -

Unrecognized asset due to IAS19.64 - -

Unrecognized actuarial (gains) loss - -

Net asset in balance sheet 6'513 - 8'089 -

c) Profit & Loss Statement 2016 2015

Employer service cost 1'864 - 1'987 -

Interest cost 244 - 346 -

Expected return on plan assets 200 286

Admin expense 38 - 39 -

Past service cost recognized in year - -

Curtailment settlement plan amendment gain (loss) - -

Net periodic pension cost 1'946 - 2'086 -

d) Movements in net asset recognized in balance sheet 2016 2015

Net asset in balance sheet (BOY) 8'089 - 7'976 -

Expense recognized in the profit & loss statement 1'946 - 2'086 -

Employer contributions 1'462 1'588

Prepaid (accrued) pension cost 484 - 498 -

whereof operating income (expense) 440 - 438 -

whereof financing income (expense) 44 60 -

Total gains/(losses) recognized in OCI 2'060 385

Net asset in balance sheet (EOY) 6'513 - 8'089 -

Actual return on plan assets 3'183 2'145

8.2% 5.7%

Expected employer’s cash contributions 1'449 1'397

for following year

Page 25 of 27

e) Principal actuarial assumptions (BOY) 31.12.2016 31.12.2015

Discount rate 0.45% 0.55%

Expected net return on plan assets

Average future salary increases 1.50% 1.50%

Future pension increases 0.00% 0.00%

Credit rate on savings capital 0.45% 0.55%

Mortality tables used BVG2015GT BVG2010GT

Average retirement age 64/64 64/64

Average life expectancy of a pensioner at retirement

- Women 25.42 24.98

- Men 23.32 22.46

f) Asset allocation 31.12.2016 31.12.2015

Cash 4.4% 4.2%

Bonds 29.1% 36.8%

Equities 26.2% 26.8%

Property 27.0% 24.8%

Other 13.3% 7.4%

Total 100% 100%

To our knowledge, all assets are quoted or traded with the exception of property (main part direct hold

property), of Private Equity of 7.2% in other and mortgage of 8% in bonds.

Page 26 of 27

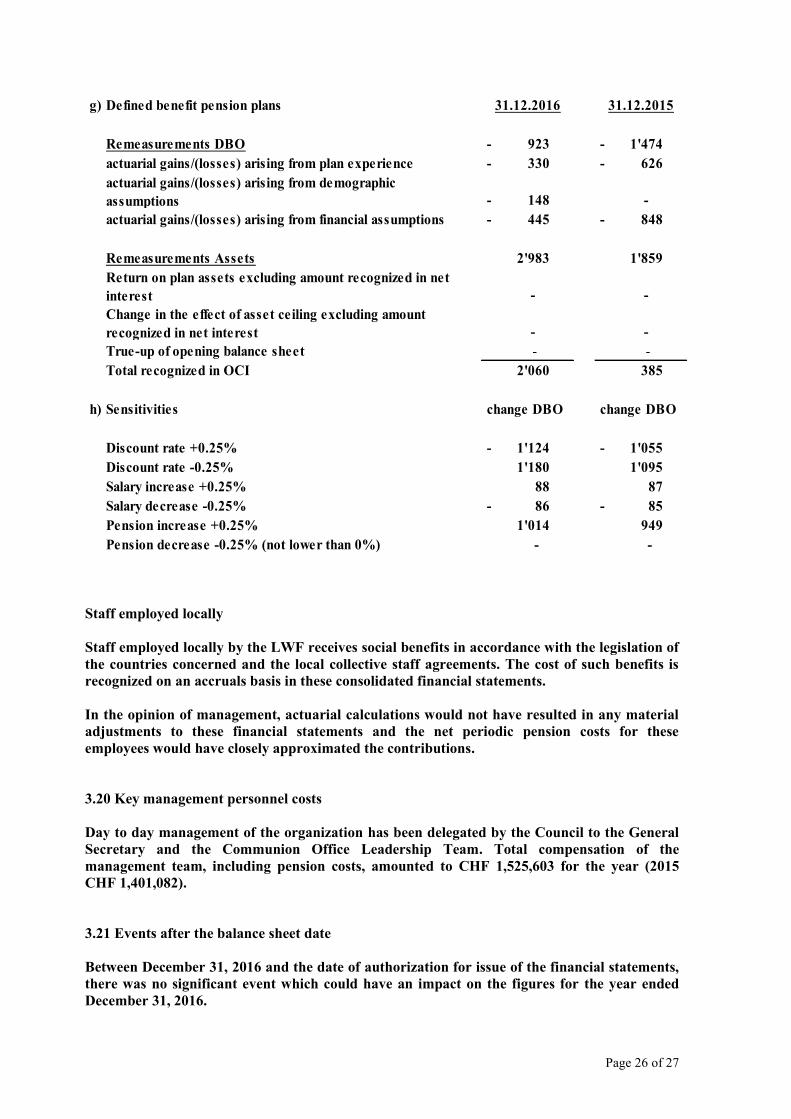

g) Defined benefit pension plans 31.12.2016 31.12.2015

Remeasurements DBO 923 - 1'474 -

actuarial gains/(losses) arising from plan experience 330 - 626 -

actuarial gains/(losses) arising from demographic

assumptions 148 - -

actuarial gains/(losses) arising from financial assumptions 445 - 848 -

Remeasurements Assets 2'983 1'859

Return on plan assets excluding amount recognized in net

interest - -

Change in the effect of asset ceiling excluding amount

recognized in net interest - -

True-up of opening balance sheet - -

Total recognized in OCI 2'060 385

h) Sensitivities change DBO change DBO

Discount rate +0.25% 1'124 - 1'055 -

Discount rate -0.25% 1'180 1'095

Salary increase +0.25% 88 87

Salary decrease -0.25% 86 - 85 -

Pension increase +0.25% 1'014 949

Pension decrease -0.25% (not lower than 0%) - -

Staff employed locally

Staff employed locally by the LWF receives social benefits in accordance with the legislation of

the countries concerned and the local collective staff agreements. The cost of such benefits is

recognized on an accruals basis in these consolidated financial statements.

In the opinion of management, actuarial calculations would not have resulted in any material

adjustments to these financial statements and the net periodic pension costs for these

employees would have closely approximated the contributions.

3.20 Key management personnel costs

Day to day management of the organization has been delegated by the Council to the General

Secretary and the Communion Office Leadership Team. Total compensation of the

management team, including pension costs, amounted to CHF 1,525,603 for the year (2015

CHF 1,401,082).

3.21 Events after the balance sheet date

Between December 31, 2016 and the date of authorization for issue of the financial statements,

there was no significant event which could have an impact on the figures for the year ended

December 31, 2016.

Page 27 of 27

3.22 LWF Staff Statics (FTE)

In 2016 LWF Employed total 2,607 regular staff, 71 staff in Geneva head quarter and 2,536

staff in LWF field offices.

3.23 Pension Liability

On 31th December 2016, the liability to the pension scheme amounted to CHF 8,260.

3.24 Audit Fees

The total audit fees paid in 2016 was CHF 85,000 for audit of the LWF Geneva Head quarter

including the consolidated reports and CHF 21’000 paid for other projects audits/ services.

For Country program audits and services LWF paid EUR 395,347 in 2016.