report institutional reforms of ipas rabat, january 2018 · report institutional reforms of ipas...

TRANSCRIPT

REPORT

Institutional reforms of IPAs Rabat, January 2018

This report contains the summary discussions, agendas, list of participants and presentations of the regional seminar on “Institutional Reforms of Investment Promotion Agencies” and the national workshop on “Transformation of the Moroccan Agency for Investment and Exports: Good Practices and International Perspective”, organised in Rabat on 30 January–1 February 2018, as well as the two background papers on the “Institutional reforms of investment promotion agencies in the OECD and the Southern Mediterranean region” and “The institutional transformation of investment promotion agencies and a case study”.

2

REPORT

In the framework of the EU-OECD Programme on Promoting Investment in the Mediterranean, which aims at supporting the implementation of sound investment policies and effective institutions in the Southern Mediterranean region, the OECD organised two events in Rabat, Morocco from 30th January to 1st February: 1. Regional seminar: Institutional reforms of investment promotion agencies The 1.5-day regional seminar provided a platform for MED and EU IPAs to exchange on their institutional frameworks for investment promotion (see agenda below). It allowed MED IPAs to:

Learn from emerging trends in IPA institutional settings –in the MED region but also in EU and OECD economies – and assess the different institutional options for investment promotion;

Discuss IPA governance and mandates with MED and EU peers. Exchange on the MED IPA survey to be filled in by MED countries, with a view to

provide comparative data allowing for a benchmarking of IPAs. The workshop was very well attended by 59 participants, representing seven beneficiary countries of the Programme (Algeria, Egypt, Jordan, Lebanon, Morocco, Palestinian Authority, and Tunisia). Libyan participants could not attend as they did not obtain their visa on time despite early mobilization. Egypt was represented by the Embassy in Rabat. Morocco sent a larger delegation of 8 persons. Representatives of the European Commission and the EU delegation in Rabat, Economic and Trade counsellors from several EU member countries (France, Germany and Spain) and ANIMA participated in most parts of the seminar (see list of participants below). Peer experts comprised representatives from five EU IPAs, namely Business France, CzechInvest, Enterprise Estonia, Enterprise Greece and Germany Trade and Investment. OECD experts also contributed to the seminar. The peer-learning format and exchanges with practitioners were highly appreciated by the participants. Two background papers were prepared for the seminar:

“The institutional transformation of investment promotion agencies and a case study” (prepared by Business France in coordination with OECD): While several Mediterranean and European countries have recently implemented important reforms of their investment promotion agencies, this document analyses the main developing trends at play and the challenges being faced in institutional transformation, including the integration of several mandates covering the development of trade, investment, SMEs, innovation, and/or specific sectors. This

3

report lays out a case study of Business France’s merger of investment and export mandates.

“Institutional reforms of investment promotion agencies in the OECD and the Southern Mediterranean region”: As various governments in the region have recently introduced changes in their institutional framework for investment promotion and facilitation, or are in the process of doing so, this note provides a brief overview of the main institutional choices and recent reforms of investment promotion agencies in the MED region and in OECD countries with a view to collectively reflect on the role, relevance and rationale of such reforms.

Discussions

The seminar was opened by H.E. Othman El Ferdaous, Secretary of State in charge of Investment in the Ministry of Industry, Investment, Trade and Digital Economy, Morocco; Michaela Dodini, Head of the Commercial Section at the EU Delegation in Morocco; and Marie-Estelle Rey, Senior Advisor, MENA-OECD Competitiveness Programme. During the first session, representatives of MED countries were invited to present their institutional framework for investment promotion, on-going and envisaged reforms of IPAs, and the challenges their agency is facing. The tour de table was very informative and confirmed timeliness of the workshop given the on-going institutional transformation or the reflection around the issue. Follow-up discussions focused on IPAs reporting lines (e.g. line ministry, head of government, etc.), the composition of the IPAs board, including private sector’s participation and its weight in the decision process, constraints and fears in merging different mandates (e.g. investment and export promotion), and IPA staff skills and competencies. Session 2 discussed the global trends in IPA institutional choices and organisational characteristics. Insights from a recent OECD survey on IPAs from OECD economies were presented, as well as the annual benchmark of Business France. These insights allowed to shed light on global trends in IPA institutional choices and organisational characteristics as well as on the main differences and similarities among MED IPAs and between MED and OECD IPAs. Participants also raised several questions regarding the scope of mandates and IPAs budget sources and financing options. They discussed the implications of charging fees for services, more common in export promotion agencies, in the context of a merger of the investment and export mandates. Session 3 was organised as a peer-learning session on streamlining IPAs institutional setting and governance. Presentations and discussions focused on IPAs’ legal status (i.e. whether the agency is governmental, public autonomous or with private sector participation), reporting lines (e.g. reporting to one single ministry, several ministries, head of government, etc.) and the role and composition of the IPA board. Various other issues were discussed, such as the policy advocacy role of IPAs, the potential role of an ombudsman in an IPA, the scope and role of IPA overseas offices, the status and reporting lines of trade attachés and the coordination of with regional investment promotion bodies and initiatives.

4

During session 4, the OCDE made an interactive presentation of the MED IPA survey (that was launched right after the workshop) presenting to participants the purpose, the scope and the content of the survey, and explaining how to fill in the questionnaire. The survey already covers 52 OECD and Latin American countries and will now be extended to the 8 MED countries covered by the Programme. Its aim is to benchmark MED IPAs with each other, with the OECD area and with other regions of the world, to help IPA practitioners and investment policymakers to better understand the existing approaches to investment promotion and undertake strategic decisions and reforms accordingly. MED IPAs were given the deadline of 31 March to complete the survey and the OECD will then treat and analyse the data, compile results and present the findings at the regional workshop on IPAs in fall 2018. Session 5 was also a peer-learning session and focused on the scope and diversity of mandates within an agency (i.e. combining inward foreign investment promotion with, for example, export promotion, innovation promotion, , SME development, management of SEZs, etc.). Business France which recently merged its investment and export promotion mandates insisted on the time needed for a successful transition and the importance of internal communication. Experts highlighted the strengths (new culture, better international visibility, coordination, cost efficiency) and weaknesses of a merger (notably in terms of management and performance indicators). Czech Invest also presented its structure and multi-mandate approach (in particular the double mandate of investment promotion and SME support), mentioning some specificities of the agency, including the participation of parliament members and private investors in the governance structure, cooperation with foreign chambers of commerce, FDI monitoring tools and their extensive suppliers database to promote business linkages between foreign affiliates and local SMEs. Germany Trade and Invest (GTAI) explained the complementarity of its trade and investment mandate, its cooperation with its partner network (in particular German chambers of commerce), the importance of information and intelligence gathering, the required level of sectoral expertise within the agency, and the promotion of investment in less developed regions (Eastern Germany). The session followed up with an interactive discussion on the merger of mandates with numerous questions from MED participants. Next steps

In conclusion, a tour de table allowed hearing the views and suggestions of country

representatives with regard to the workshop and future activities of the EU-OECD

Programme. Participants highlighted the usefulness and timeliness of the seminar, in

particular the theme of the merger of different mandates under a single agency. The peer-

learning approach was appreciated and “inspiring” as it triggered reflections of on-going and

future reforms.

Several themes were mentioned for follow-up, including revision of the investment legislation, policy advocacy, relationship between IPAs and the private sector, economic zones, impact of reforms at the territorial level.

5

In the evaluation forms, several other themes to further explore were also mentioned, including: IPA budget and management, client relationship management (CRM), policy advocacy and lobbying, connection with the diaspora, investment statistics, information systems and investment mapping, local investment attractiveness. Several countries also mentioned tax incentives and their role in attracting investment. 2. National workshop: Transformation of the Moroccan Agency for Investment and

Exports Development (AMDIE): good practices and international perspective The regional seminar was followed by a one-day national workshop organised at the request of Morocco, as a new agency was created on 15 December resulting from the merger of the investment and export promotion agencies (AMDI and Maroc Export). The agenda was tailored to the actual needs of the new agency and based on series of questions shared in advance by AMDIE staff and discussed with the experts. 25 representatives of AMDIE representing both agencies under the merger process participated in the workshop. Moderated by the OECD, the workshop benefitted from the contribution of four experts from EU members IPAs (Czech Republic, France and Greece). The meeting was opened by the OECD and the EU. After a presentation of Mr. Hicham Boudraa, the Director General ad interim of AMDIE who explained the strategy, rationale and organisation of the recent merger between the agencies, the experts presented their experience of integrating various mandates under one single entity. Then, discussions were framed around various topics: synergies of mandates in terms of organisation and rationale; human resource dimension and required skills and expertise; horizontal and vertical coordination; internal and institutional communication; implementation of the reforms at the regional level; overseas offices; billing of services; risks and difficulties of a merger; evaluation and performance indicators. In conclusion, M. Boudraa thanked its staff for the interactive and open discussions. He mentioned that based on other experiences and lessons learnt, each country has a model to conceive, and that the human factor is an essential criteria for the success of a merger, quoting the Greek representative: “with little resource, be resourceful”. M. Boudraa expressed its deep appreciation to the OECD for this successful peer-learning workshop, an opportunity for the staff of the two merged agencies to exchange and build confidence on the future endeavour of AMDIE. Communication

Communications efforts have been undertaken to inform key stakeholders ahead of the meeting. In particular, an invitation and the corresponding materials were extended to all OECD and MENA countries with diplomatic presence in Rabat, as well as to regional and international organisations.

6

Tweets were also produced at the beginning of each event, reaching more than 2000 impressions in total. The event and its outcomes will also be shared internally at the OECD, as well as with OECD Member States Delegates.

7

8

9

Annex 1: Agenda

10

EU-OECD Programme on Promoting

Investment in the Mediterranean

REGIONAL SEMINAR

Institutional Reforms of Investment

Promotion Agencies

30-31 January 2018

Rabat, Morocco

Venue: Hotel Sofitel – Jardin des Roses

Agenda

11

Background

The EU-OECD Programme on Promoting Investment in the Mediterranean, launched in October

2016 in Tunis, aims at supporting Southern Mediterranean countries in implementing sound and

attractive investment policies and establishing effective institutions. Its end-goal is to help the region

attract quality investments, create job opportunities and foster local development, economic

diversification and stability.

The Programme is governed by an Advisory Group, co-chaired by the European Commission and the

OECD, with the participation of representatives of beneficiary countries, the Secretariat of the Union

for the Mediterranean and other regional partners.

Objectives of the seminar The seminar provides a platform for MED and EU Investment Promotion Agencies (IPAs) to

exchange on their institutional frameworks for investment promotion. Various recent practices in EU

and OECD countries’ IPAs will be presented and discussed among practitioners. The seminar will

focus on MED IPAs governance and core mandates and how they fit into the broader institutional

framework. The emerging trend of grouping together several mandates – such as investment and

trade promotion – under one single organisation will be explored. The discussions will allow

participants to better understand the possible underlying rationales, costs and benefits of these

different institutional settings, and learn about good practices for implementation.

Participants will include senior IPA representatives and investment policymakers from MED and EU

countries. Participants will benefit from a focused exchange of perspectives among practitioners and

hold an evidence-based and forward-looking discussion.

The seminar will allow MED IPAs to:

Debate about the different institutional choices for investment promotion;

Explore the different structures and mandates of IPAs based on EU and MED countries recent

experiences;

Provide a tutorial to the participants on how to fill the MED IPAs survey.

A background document will be shared ahead of the meeting on IPAs institutional setting in EU

countries and in the Mediterranean region.

12

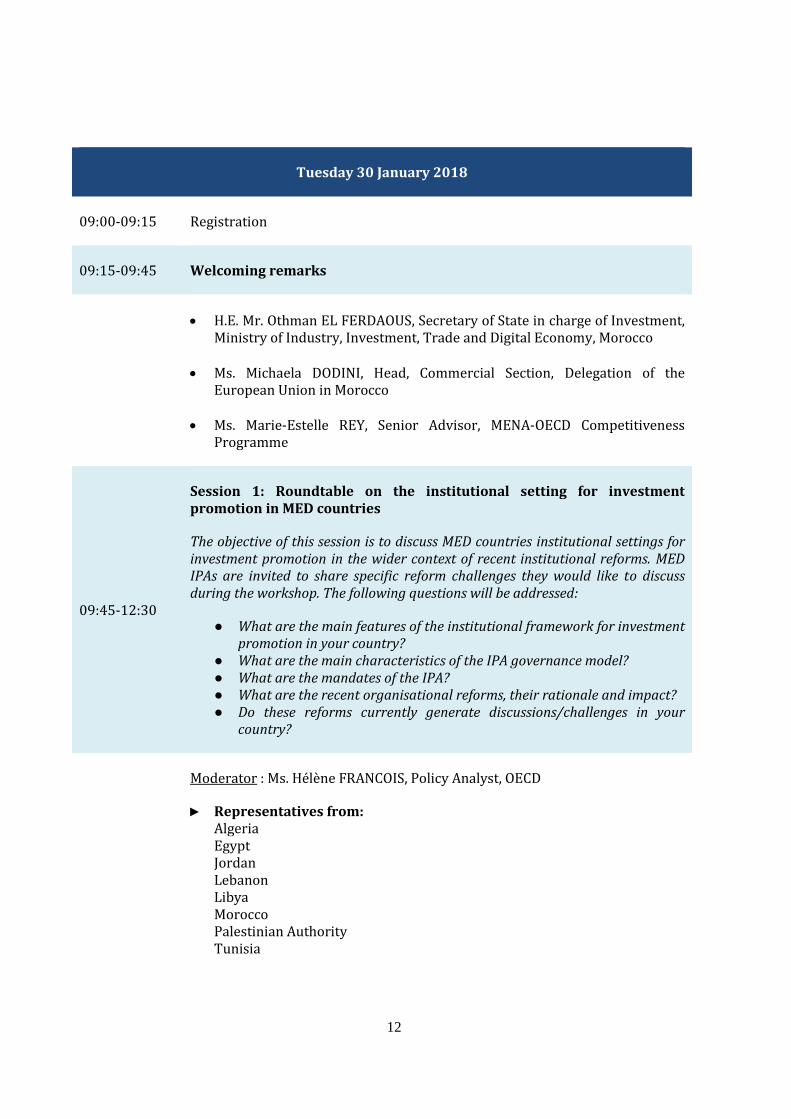

Tuesday 30 January 2018

09:00-09:15 Registration

09:15-09:45 Welcoming remarks

H.E. Mr. Othman EL FERDAOUS, Secretary of State in charge of Investment, Ministry of Industry, Investment, Trade and Digital Economy, Morocco

Ms. Michaela DODINI, Head, Commercial Section, Delegation of the European Union in Morocco

Ms. Marie-Estelle REY, Senior Advisor, MENA-OECD Competitiveness Programme

09:45-12:30

Session 1: Roundtable on the institutional setting for investment promotion in MED countries

The objective of this session is to discuss MED countries institutional settings for investment promotion in the wider context of recent institutional reforms. MED IPAs are invited to share specific reform challenges they would like to discuss during the workshop. The following questions will be addressed:

● What are the main features of the institutional framework for investment promotion in your country?

● What are the main characteristics of the IPA governance model? ● What are the mandates of the IPA? ● What are the recent organisational reforms, their rationale and impact? ● Do these reforms currently generate discussions/challenges in your

country?

Moderator : Ms. Hélène FRANCOIS, Policy Analyst, OECD

► Representatives from: Algeria Egypt Jordan Lebanon Libya Morocco Palestinian Authority Tunisia

13

11:00-11:30 Coffee break

Continued - Interactive discussions

12:30-14:00 Lunch break

14:00-15:00

Session 2: Global trends in IPAs institutional choices and organisational characteristics

IPAs evolve in their own historical and institutional contexts. Initially established to respond to specific policy objectives, they are governed in a way that is often dictated by their institutional contexts and broader political choices. This session will describe the latest global trends in IPAs institutional setting and organisational characteristics. The session will focus on IPAs legal status, governance models and formal mandates.

Moderator: Mr. Fares AL-HUSSAMI, Policy Analyst, OECD

► IPAs institutional choices and organisational characteristics in OECD countries: Insights from a recent OECD Survey Mr. Alexandre DE CROMBRUGGHE, Policy Analyst, OECD

► Worldwide and European trends in institutional reforms of IPAs: Findings from Business France Annual Benchmark Mr. Philippe YVERGNIAUX, Director of International Cooperation, and Ms. Véronique LEDRU, Mission International Cooperation, Business France

15:00-17:00

Session 3: EU-MED peer-learning session on streamlining IPAs institutional setting and governance

The governance of an IPA is related to the way it is supervised, guided, controlled and managed. An IPAs legal status also determines many organisational aspects of the agency, including how it fits into the broader institutional framework for investment promotion. In this session EU and MED IPAs will describe their current governance choices and recent or upcoming reforms to clarify:

IPAs’ legal status (e.g. governmental, autonomous, etc.); IPAs’ reporting lines (e.g. reporting to one single ministry, several

ministries, head of government, etc.); The role and composition of the IPA board.

The advantages and limitations of each option will be discussed.

14

► Mr. Christos SKOURAS, Communication, International & Institutional Affairs Directorate, Enterprise Greece

► Ms. Gerli PALGI, Business Development Manager, Product Owner Investment Agency, Enterprise Estonia

► Feedback on the experiences of MED and EU countries

Wednesday 31 January 2018

09:00-10:15

Session 4: Interactive tutorial on the MED IPA survey

This session will discuss the objectives and expected outcomes of the MED IPA survey, present the methodology and the timeframe, and familiarise the participants with the online platform used to fill the questionnaire. The survey aims to help IPAs and policymakers to better understand the existing approaches to investment promotion, benchmark their agencies against peers and undertake strategic decisions and reforms accordingly.

► Ms. Peline ATAMER, Policy Analyst, OECD

10:15-10:45 Coffee break

10:45-12:45

Session 5: EU-MED peer-learning session on multi-mandate agencies: Making it work and maximizing the benefits

The mandate of IPAs to promote and attract inward foreign investment is often combined with other mandates (e.g. promotion of innovation, SMEs, SEZs, trade, export, etc.). The case study will discuss, inter alia, the merging of investment and export promotion, which has become an increasingly adopted strategic choice by governments, including in the MED region. Participants will explain the rationale behind this decision, describe the merger process and present post-merger results, be they positive or negative.

► Mr. Philippe YVERGNIAUX, Director of International Cooperation, and Ms. Véronique LEDRU, Mission International Cooperation, Business France

► Mr. Vit SVAJCR, Senior Consultant, CzechInvest

► Dr. Marcus SCHMIDT, Director, Chemicals & Healthcare, Germany Trade and Invest

15

► Feedback on the experiences of MED and EU countries

12:45-13:00 Closing remarks and next steps of the Programme

Ms. Marie-Estelle REY, Senior Advisor, MENA-OECD Competitiveness Programme

Group picture

16

CONTACTS

Middle East and Africa Division, Global Relations Secretariat, OECD

Ms. Marie-Estelle Rey Senior Advisor Tel.: +33 1 45 24 81 46 Email: [email protected]

Mr. Arthur Pataud Policy Analyst Tel.: +33 1 45 24 15 83 Email: [email protected]

Investment Division, Directorate for Financial and Enterprise Affairs, OECD Ms. Hélène François Legal Advisor Tel.: +33 1 45 24 14 23 Email: [email protected]

Mr. Fares Al Hussami Policy Analyst Tel.: +33 1 45 24 74 25 Email: [email protected]

17

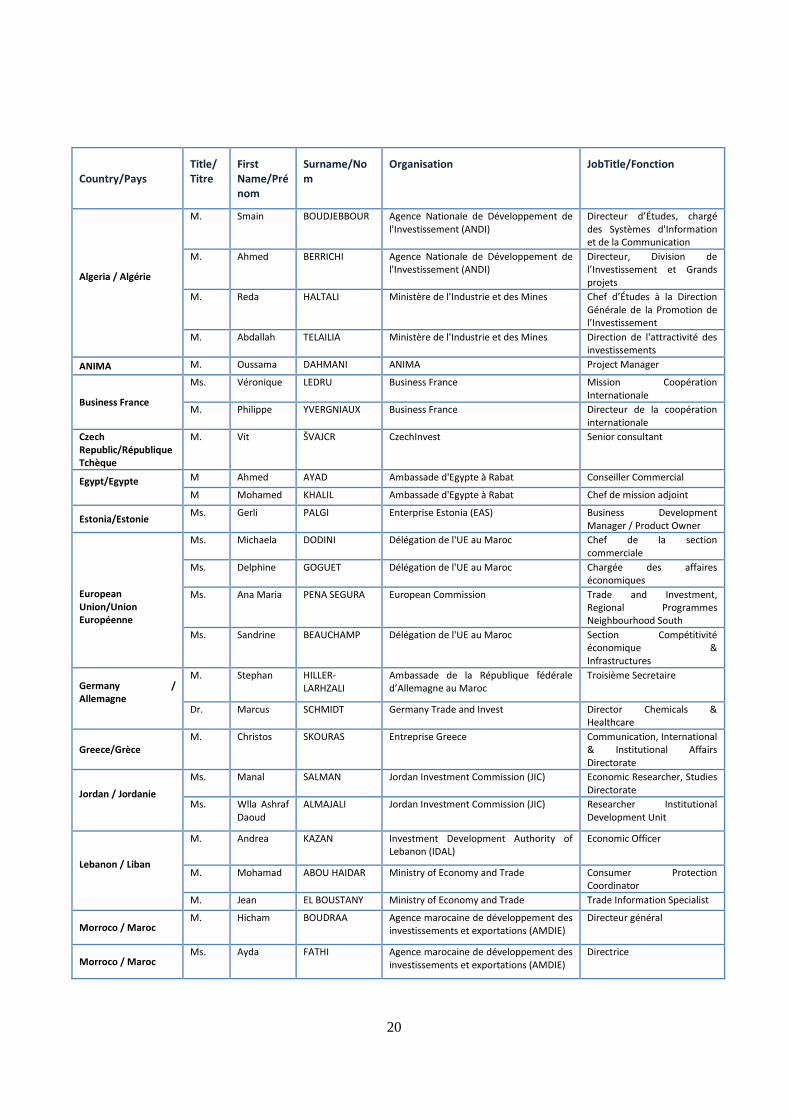

Annex 2 : Participants list

18

19

EU-OECD Programme on Promoting

Investment in the Mediterranean

Regional Seminar & National

Workshop

LIST OF PARTICIPANTS

30 January – 1st February 2018

Rabat, Morocco

Venue: Hotel Sofitel – Jardin des Roses

20

Country/Pays Title/Titre

First Name/Prénom

Surname/Nom

Organisation JobTitle/Fonction

Algeria / Algérie

M. Smain BOUDJEBBOUR Agence Nationale de Développement de l'Investissement (ANDI)

Directeur d’Études, chargé des Systèmes d'Information et de la Communication

M. Ahmed BERRICHI Agence Nationale de Développement de l'Investissement (ANDI)

Directeur, Division de l’Investissement et Grands projets

M. Reda HALTALI Ministère de l'Industrie et des Mines Chef d’Études à la Direction Générale de la Promotion de l’Investissement

M. Abdallah TELAILIA Ministère de l'Industrie et des Mines Direction de l'attractivité des investissements

ANIMA M. Oussama DAHMANI ANIMA Project Manager

Business France

Ms. Véronique LEDRU Business France Mission Coopération Internationale

M. Philippe YVERGNIAUX Business France Directeur de la coopération internationale

Czech Republic/République Tchèque

M. Vit ŠVAJCR CzechInvest Senior consultant

Egypt/Egypte

M Ahmed AYAD Ambassade d'Egypte à Rabat Conseiller Commercial

M Mohamed KHALIL Ambassade d'Egypte à Rabat Chef de mission adjoint

Estonia/Estonie Ms. Gerli PALGI Enterprise Estonia (EAS) Business Development

Manager / Product Owner

European Union/Union Européenne

Ms. Michaela DODINI Délégation de l'UE au Maroc Chef de la section commerciale

Ms. Delphine GOGUET Délégation de l'UE au Maroc Chargée des affaires économiques

Ms. Ana Maria PENA SEGURA European Commission Trade and Investment, Regional Programmes Neighbourhood South

Ms. Sandrine BEAUCHAMP Délégation de l'UE au Maroc Section Compétitivité économique & Infrastructures

Germany / Allemagne

M. Stephan HILLER-LARHZALI

Ambassade de la République fédérale d’Allemagne au Maroc

Troisième Secretaire

Dr. Marcus SCHMIDT Germany Trade and Invest Director Chemicals & Healthcare

Greece/Grèce M. Christos SKOURAS Entreprise Greece Communication, International

& Institutional Affairs Directorate

Jordan / Jordanie

Ms. Manal SALMAN Jordan Investment Commission (JIC) Economic Researcher, Studies Directorate

Ms. Wlla Ashraf Daoud

ALMAJALI Jordan Investment Commission (JIC) Researcher Institutional Development Unit

Lebanon / Liban

M. Andrea KAZAN Investment Development Authority of Lebanon (IDAL)

Economic Officer

M. Mohamad ABOU HAIDAR Ministry of Economy and Trade Consumer Protection Coordinator

M. Jean EL BOUSTANY Ministry of Economy and Trade Trade Information Specialist

Morroco / Maroc M. Hicham BOUDRAA Agence marocaine de développement des

investissements et exportations (AMDIE) Directeur général

Morroco / Maroc Ms. Ayda FATHI Agence marocaine de développement des

investissements et exportations (AMDIE) Directrice

21

Ms. Jihane LMIMOUNI Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de Service Organisations Internationales

Ms. Nejma EL HOUDA BOUAMAMA

Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de département

M. Ahmed BENNANI Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de service

Ms. Lamia BOUZBOUZ Agence marocaine de développement des investissements et exportations (AMDIE)

Chargée de Mission

M. Ali MEHREZ Agence marocaine de développement des investissements et exportations (AMDIE)

Chargé de mission

Ms. Nadia DRAFATE Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de département

Ms. Assia BENSAAD Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de département

M. Hicham BENLIMAN Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de département

M. Amine BELBACHIR Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de département

Ms. Ghita BADOUR Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de département

Ms. Fadoua BOUIMEZGANE Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de département

Ms. Ibtissam EL MRABET Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de service

Ms. Lamia RONDA Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de service

Ms. Maria BENMBAREK Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de service

Ms. Fadoua OUALLAL Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de Service

M. Youssef SALIOUI Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de Service

Ms. Zaynab MARCEL Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de Service

Ms. Hind KAICHOUCH Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de service

Ms. Yasmine SOUFIANI Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de Service

M. Ali IHABI Agence marocaine de développement des investissements et exportations (AMDIE)

Cadre

M. Khalid MIMOUNI Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de département

M. Kamal CHOUKRI Agence marocaine de développement des investissements et exportations (AMDIE)

Cadre

Morroco / Maroc

Ms. Mahassine EL RHERMOUL Agence marocaine de développement des investissements et exportations (AMDIE)

Chef de Service

M. Othman EL FERDAOUS Secrétariat d’Etat chargé de l’Investissement -Ministère de l’Industrie, de l’Investissement, du Commerce et de l’Economie Numérique

Secrétaire d'Etat

22

Palestinian Authority/Autorité Palestinienne

Ms Ibtesam ALSALAHAT Palestinian Investment Promotion Agency (PIPA)

Internal Audit Director

Ms Ola HAMOUDA Palestinian Investment Promotion Agency (PIPA)

Team Leader for Commercial Trade Representatives (CTRs)

M. Nael (Alan Hamed)

MOUSA (QARUOTY)

Office of Palestinian Council of ministers Lawyer

Spain/Espagne M. Luis Oscar MORENO

GARCIA-CANO Ambassade d'Espagne au Maroc Conseiller Economique et

Commercial

Tunisia/Tunisie

Ms. Nejia GHARBI Cabinet du Chef du Gouvernement Chargée de Mission au Cabinet du Chef du Gouvernement et Directeur général de l'Unité centrale d'Encadrement des Investisseurs

M. Zied LAHBIB Foreign Investment Promotion Agency (FIPA)

Directeur des études et coordinateur des bureaux de l’Agence à l’étranger

M. Samir BECHOUEL Agence de Promotion de l’Industrie et de l’Innovation (APII)

Directeur Général

M. Mondher BEN BRAHIM Instance Tunisienne de l’Investissement (TIA)

Directeur Central, Chef de pole

M. Nabil JEBALI Agence foncière industrielle (AFI)

M Taoukik TRABELSI Ambassade de Tunisie à Rabat

23

Annex 3: Presentations given at the Workshop and Pictures

Please click on this link : ftp://ftp.oecd.org/Rabat

24

Annex 4: Background note on “The institutional transformation

of investment promotion agencies and a case study”

25

This document was prepared as part of two separate events of the EU-OECD Programme for Investment Promotion in the Mediterranean: The regional seminar on “Institutional transformation of investment promotion agencies”, 30-31 January

2018, Rabat, Morocco, and The national workshop on the “Transformation of the Moroccan Agency for Investment and Export

Development (AMDIE): best practices and international perspective”, 1 February 2018, Rabat, Morocco. While several Mediterranean and European countries have recently implemented important reforms of their investment promotion agencies, this document analyses the main developing trends at play and the challenges being faced in institutional transformation, including the integration of several mandates covering the development of trade, investment, SMEs, innovation, and/or specific sectors. This report lays out a case study of Business France’s merger of investment and export mandates. This document has been prepared by Business France, in coordination with the OECD. It serves as a reference document to accompany the discussions and debates surrounding the events mentioned above. It is intended to be further enriched by the comments of the countries concerned, and is made available to participants for information purposes. It should not be used for excerpts and quotes, and does not necessarily reflect the views and opinions of the OECD or its member countries.

EU-OECD Programme for Investment Promotion in the

Mediterranean

Background document

The institutional transformation of investment promotion agencies and a case study

January 2018

26

Table of Contents

INTRODUCTION ........................................................................................ 27

1) GLOBAL AND EUROPEAN TRENDS IN INSTITUTIONAL REFORM OF INVESTMENT

PROMOTION AGENCIES .......................................................................... 27

1- Governance: the balance between control and efficiency .................... 30

2- Public service/business approach: a new client approach .................... 30

3- Reporting and measurement of economic impact ................................ 32

2) FOCUS ON INSTITUTIONAL MERGERS OF AGENCIES: GLOBAL TRENDS, METHODOLOGY,

AND CASE STUDY .................................................................................... 33

1- Why merge? .......................................................................................... 33

2- Recent developments ............................................................................ 34

3) CASE STUDY: THE MERGER OF INVESTMENT AND EXPORT ACTIVITIES THROUGH THE

EXAMPLE OF BUSINESS FRANCE ........................................................ 35

CONCLUSION ............................................................................................ 38

27

INTRODUCTION

The evolution of world trade over the last twenty years has dramatically changed the way public services are organised to stimulate the development of investment, as well as SMEs, innovation, and exports. The rise of global value chains is resulting in a stronger interlinking of trade, attraction of foreign investment, innovation, and SME development. While specialised sector-specific agencies have been created separately over time, they are now growing increasingly interconnected. Putting support behind SMEs, the local private sector, productive foreign direct investment (FDI), and transnational business partnerships is the best way to address the wealth and employment challenges facing all countries—especially Mediterranean countries. While this angle is not new in Europe, it is being increasingly applied in Africa, the Middle East and Eastern Europe through the “2025 or 2030 strategic visions”. This equates to modernising the organisation and function of the institutional environments in question in order to improve the efficiency of administrative action. This development involves either the creation of agencies for the promotion of exports, foreign investment, innovation, and SME development, or an adaptation of the operating methods of existing structures. As a result, governments are rethinking their strategies, and analysing how best to change their business models (against a backdrop of reduced State subsidies), as well as how to improve the measurement of economic impact stemming from their actions, and to improve efficiency through the use of digital tools. This document provides an analysis of the current trends and challenges faced by trade development, investment, SME development, and innovation agencies. A special effort has been made to shed light on issues arising from the institutional merger of agencies, and to present the case study of Business France. This specific example resulted from the 2015 merger of French investment and export agencies.

1) GLOBAL AND EUROPEAN TRENDS IN INSTITUTIONAL REFORM OF INVESTMENT

PROMOTION AGENCIES

The majority of countries around the world recognise the need for structured and proactive public action for economic development, through the following means:

Strong public support for the economic development of regional companies:

- Creation and development of SMEs;

- Support for innovation and creation of tech startups;

- Financing of SMEs;

- Export development.

The attraction of international income:

- Attraction of foreign direct investors;

- Attraction of international tourism (whether business or leisure).

28

While these different components are complementary in the context of a national economic development strategy, each requires specific methodological approaches, tools, and skills. How then does one identify the right balance between the specific character of each component of development (creation and development of SMEs, innovation, exports, FDI, tourism, etc.) and the need to create a sense of coherence to the action overall? Each country has a different response to this problem. Depending on their history, as well as their political and economic structure, States have equipped themselves with development structures (public agencies or State services) over the past forty years, taking charge of these different missions, both at a national and regional level, with the development of decentralisation policies. This development has often led to the fragmentation of the public support tool for economic development, with several dedicated national or regional agencies working more or less in a harmonious and complementary manner.

Reflecting on the rationalisation and simplification of public economic development schemes is not a novel concept. However, the notion has accelerated over the last decade in the context of the globalisation of the economy, with pressure mounting due to several factors:

Growing importance of internationalisation and innovation issues in the global economy, with

the development of global value chains (GVCs);

Increased competition between countries, both to attract foreign investors and to promote

their export businesses;

Increasing scarcity of public budget resources in a context of growing demands from

taxpayers to have public funds applied properly;

Global value chains and their impact on national economic development strategies

Today, large multinational companies are increasingly optimising their production value chain by situating

each element of the chain in the country which offers the best conditions for this element: product design,

component manufacturing, assembly, marketing, etc.

This revolution of how goods and services are produced and traded thus transforms the nature of global

trade. Global value chains (GVCs) of multinationals now account for 80% of world trade.

This growth of GVCs is reflected at a national level for many countries, by the growth of cross-border trade

and investment on the one hand, and an increase in the share of foreign content in the country's exports on

the other. According to the International Trade Centre (ITC), a 1% increase in foreign investment yields +

0.8% of exports; a 1% increase in export flows translates into a 1.2% increase in foreign investment. In

France, for example, the share of added value of foreign companies in French exports of goods and services

increased from 17% in 1995 to 25% in 2011 and 30% in 2016.

The rise of GVCs also highlights the interactions between large multinational companies and SMEs at the

heart of this dynamic. These SMEs—at times very local—are seeing growth in opportunities to join the

world economy by partnering up with multinational groups at all levels of the value chain, from product

development to component manufacturing and distribution.

• Out of 108 countries analysed by

Business France in 2016, 43%

have a merged export and

investment agency

• 80% have a public agency status,

and 10% have a State service

29

Increased demand for transparency and legibility of the effectiveness of public policies, both

by citizens and by parliaments and governments.

The combination of these factors has led to a professionalisation of business promotion agencies, with a growing demand for:

adapted individual skills in order to bring real specialised “experts” (in attractiveness,

promotion of exports, startups, innovation, financing of SMEs, etc.) into the mix

an increasingly sophisticated range of services provided to the client (SMEs, foreign

investors) to stand out from the competition;

economic efficiency in order to maintain a high level of benefits and results despite a

decrease in budgetary means.

These factors have also led to a new outlook beyond content (experts and services), for greater focus on the container—meaning the agencies. There has been a growing trend towards the restructuring of economic development agencies (national or regional) observed over the past ten years in developed countries (virtually all European countries, for example) and in developing or emerging countries. These restructurings—which most often result in mergers between public agencies, as well as the creation of new dedicated agencies or the de-merger of integrated agencies—are driven by attempts to achieve greater economic efficiency (in terms of the services provided and results obtained in the dedicated public budget), centred around three main factors:

Technical: coherence and complementary aspects of operations

Policy: governing coordination between different ministries, with or without other actors

involved (consular agencies, regional authorities, private sector, etc.)

Budget: business model and financing method.

Thus, regardless of the form they may take, recent or ongoing restructurings all appear to result from a triple concern for simplification and increased efficiency for client companies, as well as better use of public money provided by taxpayers. The Business France case study (presented below)—resulting from the merger in 2015 of French investment and export agencies—illustrates the various issues at play. This includes the point of view of the decision-making mechanisms of the public authorities that led to the restructuring of the agencies, as well as the main challenges and opportunities faced by the merged agencies. In particular, we seek to focus on three themes that are present in most agency mergers:

Governance;

The balance between public service and the business approach: the business model of the

agencies;

Reporting and measurement of the economic impact.

Examples of recent restructurings:

Export+investment : GTAI (Germany),

Enterprise Greece, Business Sweden,

ICEX (Spain), AMDIE (Morocco),

Business France, Business Finland

(merger of FINPRO [export/invest] and

TEKES [innovation agency]).

30

1 - Governance: the balance between control and efficiency

A vast majority of agencies have the status of a public agency with their own legal identity under the supervisory authority of the State: Ministries of Economy, Foreign Trade, SMEs, Investment, or Foreign Affairs. For example, Business France is a public industrial and commercial establishment (EPIC) under the supervisory authority of the Ministries of Economy, Foreign Affairs and Territorial Cohesion, while JETRO (Japan), is a non-profit State agency under the supervision of the Ministry of Economy, Trade, and Industry. 80% of agencies in the MENA region have the status of a public agency. In this configuration, the State generally partners with other entities in the governance of the agency: regional authorities, consular agencies, or trade associations and employers. Around 12%1 of IPAs are services integrated into the State administration, such as the International Trade and Invest (ITI) in the United Kingdom. This is one of the three arms of the Department for International Trade. 8% of IPAs have a private status and are wholly or partly financed by the private sector. One example of this is Business Sweden, a semi-public agency under the supervisory authority of the Ministry of Foreign Affairs and the Industrial Trade Association. Improving agency governance is often one of the primary objectives, and even one of the key decision-making factors, for agency merger projects. This objective is legitimate when it comes to improving the way the chain of command operates and the reporting between the supervisory authorities and the agency (or agencies, if prior to the merger):

to set goals and action plans;

to track and report Key Performance Indicators (KPIs) and evaluate the results;

to set the budgetary means and human resources required for the direction of operations.

Experience has proven that this legitimate issue of efficiency can at times be distorted by other issues of influence between different administrations. In light of these issues, the priorities for efficiency are thus often invoked as pretexts (for one purpose or another). This may even be harmful in both directions, either by preventing the development of synergies between business lines that could be useful for improving efficiency, or by forcing partnerships into place that ultimately don’t bear significant benefits for the quality of the different investment and export services concerned. 2- Public service/business approach: a new client approach

Foreign investment promotion is generally considered a “State mission” and a public service par excellence. Without concerns over charging the companies served, it is essentially motivated by the public good; it seeks to create jobs and bring additional wealth to the country. Following this logic, the client of the investment promotion agency is not the foreign company, but the State itself.

1 Source: Business France

31

In contrast, export promotion activities (or related SME financing angles) are often considered as “business services”. The government export promotion agency is seen as serving corporate clients, often hailing from abroad, which puts public services in competition with private consultants offering the same export development services. This view of the market is reinforced when these services are charged, even partially, to the client companies. The merger of export and investment agencies thus causes a clash of cultures between the public service mentality and an outlook favouring commercial activity. Yet, are these two visions really contradictory. In reality, they are far less at odds than they seem. The HR analyses from the Business France merger provide some insight into the subject. The investment teams on the “public service” side also claimed to be employing a “business” approach (selling a location to a foreign client company for example). Meanwhile, export teams, the wielders of the business approach (and, in this case, charging clients), also laid claim to a mission of public service, for the benefit of the country, the balance of trade, and the prosperity of home-grown companies. While we mustn’t underestimate the impact of this clash of cultures, it’s important to move past it and to seize the opportunity of the merger to reconcile the two visions. From both sides, the client is and must be perceived by all to be the company (exporting SME or foreign investor). The services (export or implementation) of the agency are centred around the company, whether or not the company is being charged. In both cases, unlike a private consultant, the services provided to the corporate client mean more for the agency than simply generating profit or turnover; they contribute to the economic prosperity of the country. The business model of the agencies has therefore evolved. Business promotion agencies—

which came to be during the second half of the last century on a model of public service or

administrative service—have long favoured a financing model based almost exclusively on State

subsidies, whether they be linked to the promotion of investment, exports, innovation, or tourism

activities.

The concept of charging for services, especially for export, developed in Europe starting in the

2000s, for three reasons:

Limits on State subsidies against a backdrop of reduced public spending, leading many

agencies to adapt their work plan each year to perform higher (in results) with less (in terms

of budget);

Pressure from private consultants offering similar export support services, in opposition

against services by public bodies deemed as unfair competition;

Lastly, many agencies have pointed out that having even partial charges for services

provided to SMEs makes it possible to reinforce both the level of quality requirements and the

motivation of the companies concerned. This ultimately results in more efficient services and

higher satisfaction rates for SMEs.

Business France and Business Sweden are two European agencies that have pushed the charging concept to the next level, with private financing representing 48% (Business France) and 46% (Business Sweden) of their annual budget.

32

For Business France, the guiding principle is not charging to make a profit, but rather partial participation in the full costs of producing the services and services provided. Beyond this, the charging principle has a twofold virtue. The first is the company’s commitment to the costs associated with its prospecting approach, which are inherently high. The second is the effect on the BF teams, whose quality and efficiency were strengthened when all or part of the cost of the service was charged to the company and shown as being valuable.

The experience of agencies that adopted partial private financing of their export services and recently returned to 100% State-funded service models is worth exploring further. Enterprise Ireland, for example, charged for export consultancy services and has returned to services fully funded by the State. Another similar example is Finnish agency FINPRO (now Business Finland following its merger with innovation agency TEKES), which relinquished its fee-charging advisory business to the private sector in 2014 and has now shifted focus to export management. On the other hand, no agency charges for support services when dealing with foreign investors. The only exception is countries in which investors have to pay a company registration fee, which is sometimes handled by investment promotion agencies or “one-stop shops”. Yet several agencies are starting to charge for services offered (at market or subsidised prices), as well as assistance provided to their partners at regional or local level. Business France has a regional support trial scenario underway at the moment. 3- Reporting and measurement of economic impact

As observed in the past, agency mergers are often motivated by attempts to achieve greater efficiency through the development of synergies, including budget efficiency or other ways of optimising spending on a lower budget. The impression that efficiency must be improved, present in both public opinion and supervisory authorities, is often fuelled by poor measurement and communication of the real impact of

Example of pricing system by level of service

Source: Business France

33

agencies in question on economic development. Moreover, it’s worth noting that the issue of measuring the impact of business promotion agencies is at the heart of many considerations and efforts, in particular those of the OECD, UNCTAD, or ITC. Thus, it is important during a merger to not simply juxtapose key performance indicators (KPIs) and pre-existing reporting procedures from the agencies before the merger. In particular, the merger enables:

Comparison and sharing of methods and approaches (which mostly differ before the merger)

of the two agencies: the nature of performance indicators, the mode of result validation (by

questionnaire, independent survey), long-term tracking of the impact of results (number of

new investors, number of export flows, for example) conveyed through surveys and academic

studies;

An overhaul of the system, above all else, which uses the merger as an opportunity to apply

new practices and benchmarks for reporting and impact measurement: developing a set of

consistent performance indicators between the two businesses, setting up an economic

studies service in partnership with the academic field to carry out reliable impact studies.

Such an approach, beyond its direct effectiveness in measuring impact and reporting results, can have the additional benefit of reinforcing the emergence of a shared corporate culture built around a common frame of reference for indicators. 2) FOCUS ON INSTITUTIONAL MERGERS OF AGENCIES: GLOBAL TRENDS,

METHODOLOGY, AND CASE STUDY

At the same time that international organisations (OECD, UNCTAD, ITC, etc.) are developing an increasing number of studies on synergies between international trade and investment, as well as developing programmes on the link between promotion of foreign investment, exports, and the development of SMEs, more and more countries are merging their Investment and Export agencies.

1- Why merge?

Among the reasons driving the decision to merge, particular factors stand out:

Strong synergies between SME

development, innovation, export

promotion, and attraction of

foreign investment;

Willingness that stretches to

the highest political level

(usually the head of state) to

mobilise action and awareness

Five good reasons to merge - To create improved coherence of public policies and

simplification of the system;

- To help pinpoint synergies to create added value: 1+1 does not

equal 2 but 3;

- To bolster efficiency that leads to joint operations, shared tools

(in both directions), and sharing of international networks;

- To increase the agency's advocacy power through enhanced

visibility;

- To encourage the development of new skills and offer new

perspective for employees.

34

on foreign trade and foreign investment as a potent source of growth;

Creating added value through the development of synergies;

Establishment of greater interdepartmental coordination;

Greater control of public finances.

However, as experience has shown, organisations that integrate both foreign investment and trade also face obstacles, and their efforts do not necessarily translate into cost savings and synergies. Hungary, Malta, and Lithuania are examples of countries which have ultimately de-merged agencies and recreated two separate entities. A merger is a complex process with results measured over time (three to five years depending on the case). It’s a carefully-prepared undertaking that requires a risk-benefit analysis at the institutional and operational levels prior to the merger. The central challenge lies in creating a new corporate culture in light of different core activities and goals. The prospecting of foreign companies as potential investors or buyers of exports from a nation requires a variety of strategies, employee profiles, and performance measurement indicators. Experience shows that an umbrella structure is generally put in place by investment promotion agencies that merge investment, export promotion, and support for SMEs and innovation. This structure not only brings together transversal services (human resources, administrative management, IT services, and management of international subsidiaries), but also operates export and investment promotion missions separately for different operational teams. 2- Recent developments

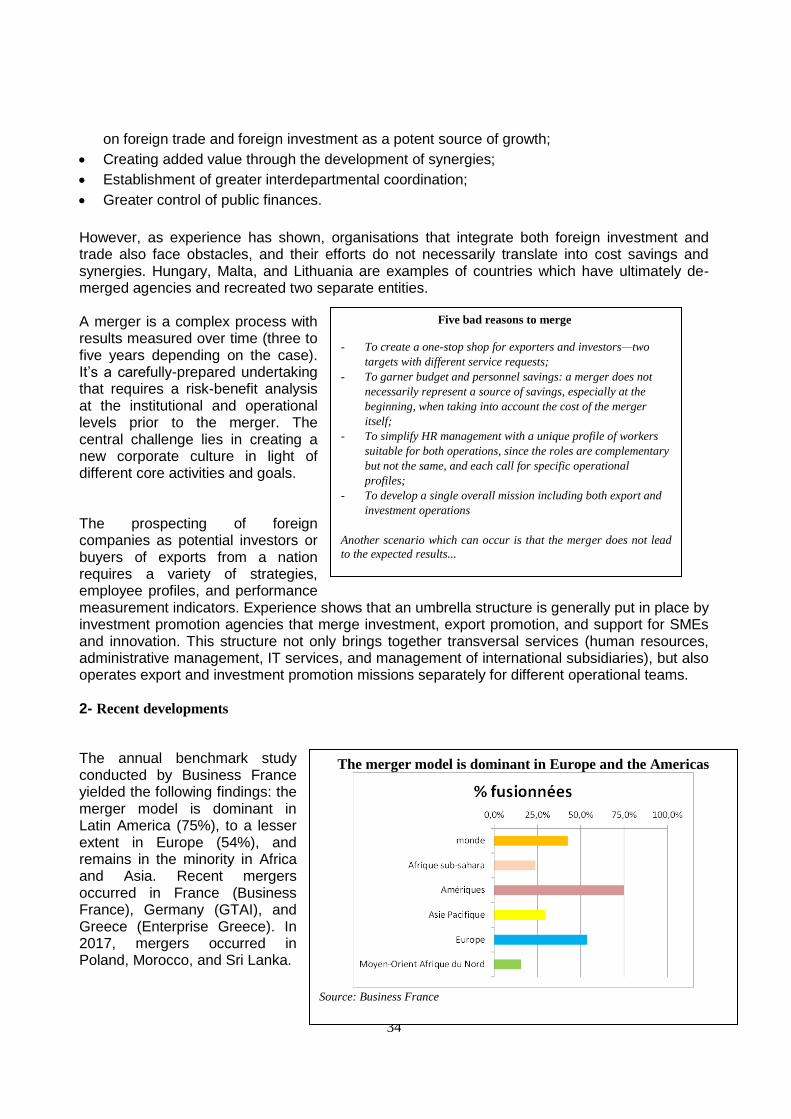

The annual benchmark study conducted by Business France yielded the following findings: the merger model is dominant in Latin America (75%), to a lesser extent in Europe (54%), and remains in the minority in Africa and Asia. Recent mergers occurred in France (Business France), Germany (GTAI), and Greece (Enterprise Greece). In 2017, mergers occurred in Poland, Morocco, and Sri Lanka.

Five bad reasons to merge

- To create a one-stop shop for exporters and investors—two

targets with different service requests;

- To garner budget and personnel savings: a merger does not

necessarily represent a source of savings, especially at the

beginning, when taking into account the cost of the merger

itself;

- To simplify HR management with a unique profile of workers

suitable for both operations, since the roles are complementary

but not the same, and each call for specific operational

profiles;

- To develop a single overall mission including both export and

investment operations

Another scenario which can occur is that the merger does not lead

to the expected results...

The merger model is dominant in Europe and the Americas

Source: Business France

35

Through merger or rapprochement, about a quarter of the agencies also integrate operations that are complementary to both export and investment, mainly: SME development (Cameroon, Congo, Croatia, Luxembourg, the Netherlands, Ireland, Georgia, etc.); support for innovation (Slovakia, Slovenia, Norway, Ireland, Luxembourg, Albania); promotion of tourism (Norway, Iceland, Estonia, Chile, Colombia, Australia), etc. Recent developments are reflected worldwide via the following means:

The recent creation of dual-purpose Export-Investment agencies in several emerging

countries, where the Export promotion operation is entrusted to the existing Investment

promotion agency, such as Pronicaragua or APIEX Angola.

Two-thirds of the Export/Investment merged agencies have offices abroad, compared with

40% for Export-only agencies, and 33% for Investment-only agencies.

A small number of countries have decided to reverse the process by “de-merging” the

Export/Investment agency into two individual and specialised agencies. This has occurred in

Hungary, Malta, and Lithuania, generally for governance issues with an abundance of

exchanges between several Ministries.

Meanwhile, the trend towards mergers has been on the rise in Europe in recent years. Most

European countries have reconsidered the relevance of their public systems by merging

investment and export agencies, which also helped to assess the innovation and

development of SMEs.

3) CASE STUDY: THE MERGER OF INVESTMENT AND EXPORT ACTIVITIES THROUGH

THE EXAMPLE OF BUSINESS FRANCE

The merger of Ubifrance and the Invest in France Agency (IFA) brought together two public institutions

with similar legal structures. From a technical point of view, the merger was carried out through the

absorption of the IFA by Ubifrance, for reasons of size ratio. The merger took place in three successive

phases: preparation, implementation, and stabilisation.

36

Source: Business France

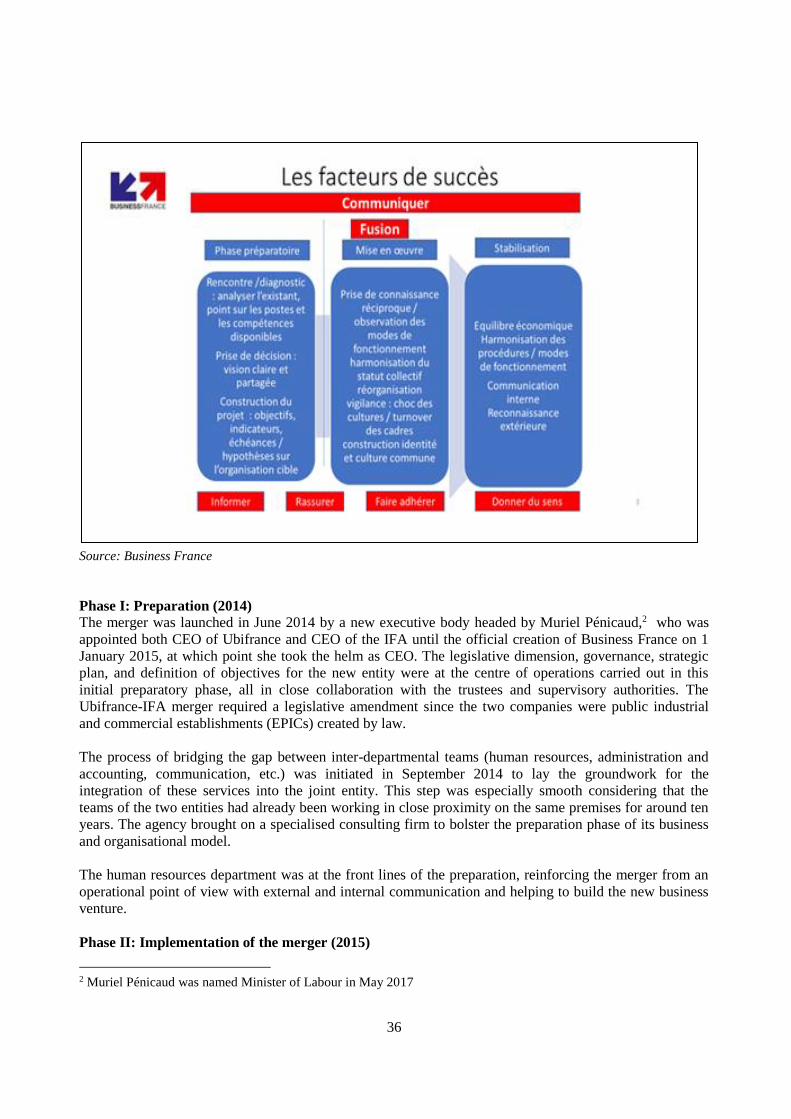

Phase I: Preparation (2014)

The merger was launched in June 2014 by a new executive body headed by Muriel Pénicaud,2 who was

appointed both CEO of Ubifrance and CEO of the IFA until the official creation of Business France on 1

January 2015, at which point she took the helm as CEO. The legislative dimension, governance, strategic

plan, and definition of objectives for the new entity were at the centre of operations carried out in this

initial preparatory phase, all in close collaboration with the trustees and supervisory authorities. The

Ubifrance-IFA merger required a legislative amendment since the two companies were public industrial

and commercial establishments (EPICs) created by law.

The process of bridging the gap between inter-departmental teams (human resources, administration and

accounting, communication, etc.) was initiated in September 2014 to lay the groundwork for the

integration of these services into the joint entity. This step was especially smooth considering that the

teams of the two entities had already been working in close proximity on the same premises for around ten

years. The agency brought on a specialised consulting firm to bolster the preparation phase of its business

and organisational model.

The human resources department was at the front lines of the preparation, reinforcing the merger from an

operational point of view with external and internal communication and helping to build the new business

venture.

Phase II: Implementation of the merger (2015)

2 Muriel Pénicaud was named Minister of Labour in May 2017

37

This phase was devoted to building a shared corporate culture by bringing together various teams to work

on the transformation and to bring new ideas from the bottom up. The involvement of management and the

implementation of transparent and intensive channels of communication were essential in carrying out this

phase of transformation, which required several projects at the same time, in order to:

Provide the support that managers needed to meet their objectives and help ease in the merger

alongside their teams. Help organise team-building exercises, an effective tool for teams to get to know

each other better and work in close cooperation;

Rebuild the human resources policies: agreement on adaptation, harmonisation of the salary and

position grid, professional training, new contracts, etc.;

Implement an internal communication strategy, including intranet, to ensure a strong grasp of the

issues and objectives, as well as encouraging team members get better acquainted with each other;

Create a new corporate mission statement by working with employees through running theme-based

team meetings led by cross-departmental managers;

Experiment with new business services, particularly for the investment wing, by taking advantage of

the synergies generated by the creation of collaborative spaces between business lines.

Business France brought on a specialised company to assist the agency over a one-year period in

establishing a human impact analysis, detecting misunderstandings, and providing feedback on synergies

with potential to be developed further.

Phase III: Stabilisation (2016-2017)

The new business plan incorporates new strategic directions to be applied in early 2018, such as:

Governance with strengthened and streamlined interdepartmental coordination, a strengthening of

partnerships (particularly with regional partners), and stronger involvement with ambassadors abroad

vis a vis attractiveness;

A strengthened business model which

accounts for the fact that 50% of the agency’s

budget comes from services invoiced to

support activities tailored to exporters;

An expanded and more targeted range of

services based on all the agency’s skills and

new business lines, such as prospecting of

financial investors to invest in innovative

companies or in existing projects;

While the operations remain very different—

as do the business profiles and operational procedures—they are nonetheless complementary;

The integration of information systems had to be entirely redesigned. Pending the implementation of a

new platform, the two systems continue to coexist.

Key Achievements New identity with outside awareness

New corporate culture, shared by all team

members

Overall priority management and annual

action plan

Simplified relationship with supervisory

Ministries

Expanded export/investment services offer

38

CONCLUSION

Institutional mergers are one mode of reorganisation of business activity used to answer the needs of

legibility and coherence in a context of greater control over public expenditures. The trend of mergers has

grown and accelerated over the last decade due to globalisation. Other agencies favour different

approaches (rapprochement, creation of separate entities, or sometimes de-merging). For agencies that

have chosen to merge two or more operations, here are some recommendations in terms of operational

strategy:

Before making the final decision to merge, launch a strategic planning initiative, which can vary in

scope between short and long term, to obtain a very clear vision of the objectives to meet for each

business line. If the merger concerns more than two entities, analysis must be carried out to ascertain if

the different entities should merge at the same time or in successive phases.

Define the hierarchy of the new agency with the supervisory authorities (roles, direction, and

governance) and position the agency with partners in the same ecosystem to avoid tension among

actors who may have significant blocking capacity if their project membership is not achieved.

Anticipate and prepare for the cost of the merger. One of the objectives of a merger is to ultimately

achieve greater control of budget costs. However, the agency has to face additional expenses in the

beginning which stem directly from the merger: construction of a new identity, the cost of outside

consultation, integration of personnel of varying statuses, moving costs, etc.;

Redesign the functions of human resources. One merger in two is delayed due to a lack of

consideration when it comes to human, social, cultural, or communication problems. In this sense, it is

important to prepare the relationship with the employee representative bodies from the start, and to

take the necessary time to explain the meaning of the merger and the way employees stand to benefit.

At the same time, organise internal communication throughout the merger process to avoid losing a

sense of purpose—and therefore efficiency—and encourage the different teams to support the new

business venture.

Mergers remain complex, with changes that will only take effect after three to five years, depending on the

individual circumstances. The most successful mergers ensure that issues of power balance between the

various supervisory authorities are well-identified and respected within the new governance mode. This

new framework should be concentrated on achieving greater efficiency in objective validation methods and

action plans, in the reporting and evaluation of results, and in the allocation of budgetary and human

resources. This represents a significant and fundamental challenge.

39

Annex 5: Background note on “Institutional reforms of investment promotion agencies in the OECD and the

Southern Mediterranean region”

40

EU-OECD Programme on Promoting

Investment in the Mediterranean

Background note

Institutional reforms of investment promotion agencies in the OECD and the Southern Mediterranean region

January 2018

This background note has been prepared for the regional workshop “Institutional Reforms of Investment Promotion Agencies” taking place on 30-31 January in Rabat, Morocco. This workshop is part of EU-OECD Programme on Promoting Investment in the Mediterranean launched in October 2016, which aims at supporting the implementation of sound investment policies and effective institutions in the Southern Mediterranean region (MED region).

As various governments in the region have recently introduced changes in their institutional framework for investment promotion and facilitation, or are in the process of doing so, it is timely to collectively reflect on the role, relevance and rationale of such reforms. This is the focus of the second pillar of the EU-OECD Programme on Promoting Investment in the Mediterranean and the purpose of the present workshop.

This note was elaborated to support the dialogue on these issues. It provides a brief overview of the main institutional choices and recent reforms of investment promotion agencies in the MED region and in OECD countries.

This background note is a draft document. Please do not quote or cite. Comments are welcome.

Contacts: Fares Al-Hussami ([email protected]) and Hélène Francois ([email protected]), Policy

Analysts, OECD Investment Division

41

Introduction

Most countries have established investment promotion agencies (IPA) to attract foreign direct investment

(FDI) in the hope to generate jobs and sustained economic growth. According to a recent survey in OECD

countries, the number of IPAs has increased substantially over the past two decades. As it is currently the

case in MED countries, existing IPAs in the OECD area have undergone major institutional reforms and

restructuring. Indeed, most OECD IPAs underwent at least one major organisational reform in recent years,

often leading to the acquisition of new mandates or a merger with another agency.

This points to common trends across countries and highlights investment promotion as a dynamic policy

area, in which a lot of institutional learning, experimentation, and adjustments are taking place. In addition,

one size does not fit all and different approaches are suitable for different countries. Even in similar

geographic and development contexts, large differences exist among IPAs in terms of institutional choices,

strategic priorities, functions, activities, techniques and instruments. Evidence reveals that these

characteristics can have a strong impact on the effectiveness of investment promotion and facilitation.3

This diversity in the institutional approaches and the dynamism of changes stresses the importance of

accurate up-to-date information on the current institutional landscape for investment promotion and peer-

learning opportunities among IPA professionals and policy-makers in different countries.

This background note focusses on the institutional environment and governance of IPAs. It provides a brief

overview of the type of choices made by OECD member states with respect to IPAs legal status,

governance models and formal mandates, based on preliminary results from the OECD-IDB survey of

Investment Promotion Agencies undertaken in 2017. The note also offers a short and preliminary snapshot

of recent reforms of MED IPAs institutional framework, with a focus on IPAs reporting lines and

mandates.

Institutional choices and organisational characteristics: An overview of concepts and recent trends

When established, investment promotion agencies (IPAs) can be created as part of a ministry, as an

autonomous public agency, as a joint public-private body or as a fully privately-owned organisation. They

can have very different mandates, governance mechanisms and organisational cultures. An increasing

number of IPAs are merging their investment and trade promotion functions while others decide to become

(or remain) more specialised. Some have an extensive presence abroad while others rely on partner

organisations to represent them overseas. Governments have also pushed through reforms to decentralise

investment promotion and facilitation by delegating some functions of IPAs to the sub-national level.

Legal status and reporting line

The governance of an IPA is related to the way it is supervised, guided, controlled and managed. When

IPAs are established, their legal status – often formalised by law – will determine many organisational and

functional aspects of the agency. The legal status will have a particular incidence on the level of autonomy

of the IPA vis-à-vis the government, particularly in terms of financial and human resources management.

From the least to the most autonomous forms of IPA, the most common types of legal status are either:

governmental (often as a department or a unit within a ministry);

autonomous public agency;

joint public-private body; or

fully privately-owned organisation.

3 Harding, T. and B.S. Javorcik (2007), “Developing Economies and International Investors: Do Investment

Promotion Agencies Bring Them”, World Bank Policy Research Working Paper, No. 4339, August.

42

In OECD economies, more than half of surveyed IPAs are organised as autonomous public agencies and

less than a third are embedded in the government (as a department in a ministry, for example). Only a

small fraction of OECD IPAs are private or joint public-private organisations.4

IPAs can have different reporting lines, depending on their legal status and broader institutional

environment. They can report to one specific minister or to several ministers, or to an inter-ministerial

taskforce. They also often report to a Board of Directors. In some cases, IPAs report directly to the head of

government. According to the OECD-IDB survey, the majority of IPAs report to a ministry. Some of their

strategic documents and financial reports are available to the public and are approved by government

bodies.

An important part of the governance of IPAs is the existence and role of a board. When an IPA is

established, decision-makers may decide to place it under the authority of a board, which allows for an

external entity to supervise the work of the agency. Boards can vary greatly from an organisation to

another; they can be of advisory nature or with a high degree of decision power. They can be composed of

public or private representatives, or both, and sometimes include representatives from research and

academia, civil society or other parts of society.

Scope and diversity of mandates

All IPAs have been created with the core mandate to promote and attract inward foreign investment.

Institutional environments differ from a country to another, however, and IPAs can thus be either fully

dedicated to investment promotion or be part of a broader agency that includes additional mandates (box

1). In the OECD area, large variations exist with respect to the number of IPA mandates, but all of them

perform at least another mandate than inward investment promotion.5 OECD IPAs often combine several

mandates, in particular related to innovation and trade promotion. The role of IPAs in promoting

investment that support economic development in the host country is also important, as half of OECD

agencies have as a mandate to promote regional development.

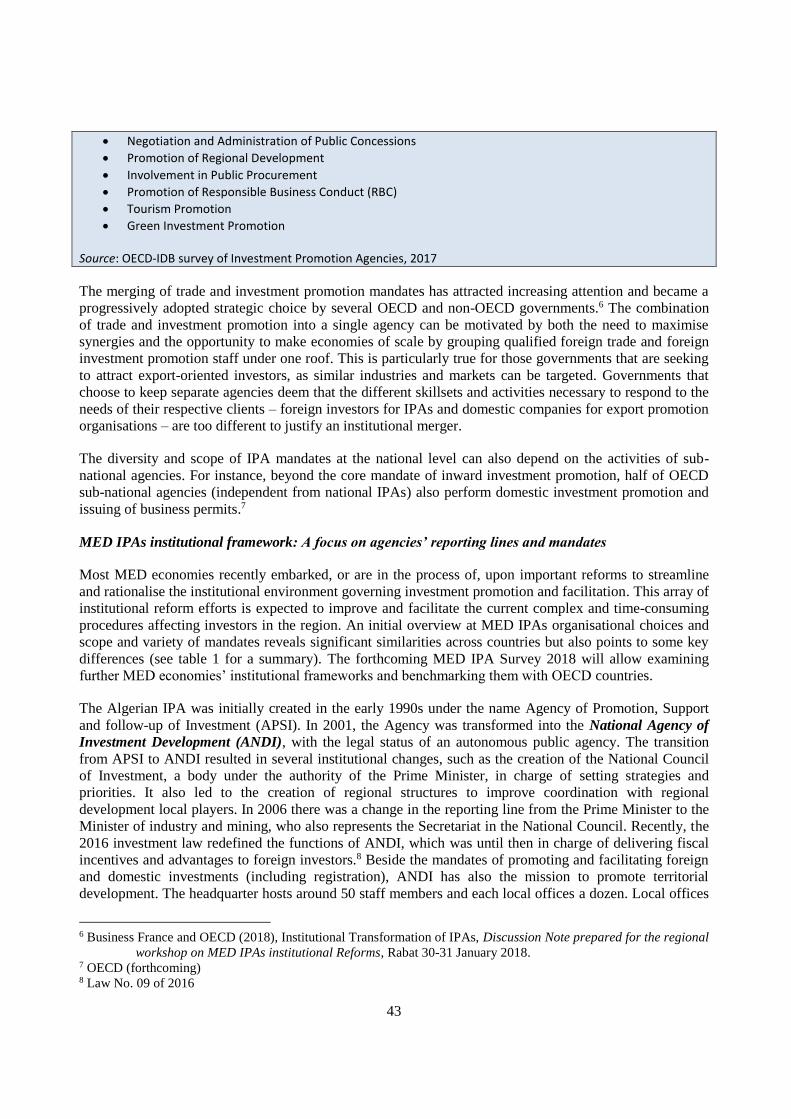

Box 1. IPAs list of potential formal mandates

Inward Foreign Investment Promotion

Outward Investment Promotion

Domestic Investment Promotion

Operation of One-Stop Shop (OSS) (e.g. Business Registration, Permits, Licenses)

Screening and Prior Approval of Investment Projects with Foreign Participation (e.g. economic needs test) or Investor Registration

Issuing of Relevant Business Permits

Negotiation of International Trade, Investment or Other Agreements

Export Promotion

Trade Facilitation (e.g. Single Window for Trade, Assistance in Custom Matters)

Innovation Promotion

Management of Free Trade- or Special Economic Zones (SEZs) or Industrial Parks

Granting Fiscal Incentives

Granting Financial or other Incentives (e.g. land)

Management of Privatizations

Management of Public-Private Partnerships (PPPs)

4 OECD (forthcoming) 5 OECD (forthcoming)

43

Negotiation and Administration of Public Concessions

Promotion of Regional Development

Involvement in Public Procurement

Promotion of Responsible Business Conduct (RBC)

Tourism Promotion

Green Investment Promotion

Source: OECD-IDB survey of Investment Promotion Agencies, 2017

The merging of trade and investment promotion mandates has attracted increasing attention and became a

progressively adopted strategic choice by several OECD and non-OECD governments.6 The combination

of trade and investment promotion into a single agency can be motivated by both the need to maximise

synergies and the opportunity to make economies of scale by grouping qualified foreign trade and foreign

investment promotion staff under one roof. This is particularly true for those governments that are seeking

to attract export-oriented investors, as similar industries and markets can be targeted. Governments that

choose to keep separate agencies deem that the different skillsets and activities necessary to respond to the

needs of their respective clients – foreign investors for IPAs and domestic companies for export promotion

organisations – are too different to justify an institutional merger.

The diversity and scope of IPA mandates at the national level can also depend on the activities of sub-

national agencies. For instance, beyond the core mandate of inward investment promotion, half of OECD

sub-national agencies (independent from national IPAs) also perform domestic investment promotion and

issuing of business permits.7

MED IPAs institutional framework: A focus on agencies’ reporting lines and mandates

Most MED economies recently embarked, or are in the process of, upon important reforms to streamline

and rationalise the institutional environment governing investment promotion and facilitation. This array of

institutional reform efforts is expected to improve and facilitate the current complex and time-consuming

procedures affecting investors in the region. An initial overview at MED IPAs organisational choices and

scope and variety of mandates reveals significant similarities across countries but also points to some key

differences (see table 1 for a summary). The forthcoming MED IPA Survey 2018 will allow examining

further MED economies’ institutional frameworks and benchmarking them with OECD countries.

The Algerian IPA was initially created in the early 1990s under the name Agency of Promotion, Support

and follow-up of Investment (APSI). In 2001, the Agency was transformed into the National Agency of

Investment Development (ANDI), with the legal status of an autonomous public agency. The transition

from APSI to ANDI resulted in several institutional changes, such as the creation of the National Council

of Investment, a body under the authority of the Prime Minister, in charge of setting strategies and

priorities. It also led to the creation of regional structures to improve coordination with regional

development local players. In 2006 there was a change in the reporting line from the Prime Minister to the

Minister of industry and mining, who also represents the Secretariat in the National Council. Recently, the

2016 investment law redefined the functions of ANDI, which was until then in charge of delivering fiscal

incentives and advantages to foreign investors.8 Beside the mandates of promoting and facilitating foreign

and domestic investments (including registration), ANDI has also the mission to promote territorial

development. The headquarter hosts around 50 staff members and each local offices a dozen. Local offices

6 Business France and OECD (2018), Institutional Transformation of IPAs, Discussion Note prepared for the regional

workshop on MED IPAs institutional Reforms, Rabat 30-31 January 2018. 7 OECD (forthcoming) 8 Law No. 09 of 2016

44

are spread in all the 48 governorates and are dedicated to business facilitation, including business

registration, and territorial promotion.

The Egyptian IPA, the General Authority for Investment and Free Zones (GAFI), created in 1971, is a

governmental agency operating under the umbrella of the Ministry of Investment and International

Cooperation. In 2016, a decree established the Supreme Council for Investment, an inter-ministerial body

chaired by the President. The role of the Council is to take measures to improve the investment climate,

develop the framework for legislative and administrative reforms and approve the Investment Plan and

major economic projects.9 Beside its mandates of promoting and facilitating foreign and domestic

investment, GAFI is also the principal government body in charge of regulating investment, including of

special investment regimes (e.g. Free Zones, Development Zones and Investment Zones). In addition,

GAFI is also mandated with the granting of state-owned lands to investors and of supporting

entrepreneurship and innovation.10 At the sub-national level, GAFI established five one-stop shops (OSS)