regulation and ratings agency update - airc.org.t regulation... · us rbc formula • beginning in...

TRANSCRIPT

Michael Owen, FCAS

Managing Director

Singapore

Regulation and Ratings Agency Update

Global RegulationInternational Association of Insurance Supervisors (IAIS)1

Rating AgenciesNew AM Best Credit Rating and SRQ

2 Country UpdateRegulatory Changes by Country

3

AGENDA

Section 1

Global RegulationInternational Association of Insurance Supervisors

Global Overview

• The International Association of Insurance Supervisors (IAIS) wasestablished in 1994 to promote cooperation among insurance supervisorsaround the globe and represents nearly 140 countries, including Taiwan.

• The IAIS develops Insurance Core Principals (ICPs) in order to:– promote a financially sound insurance sector– set out the fundamentals of effective insurance supervision– serve as a basic benchmark for insurance supervisors in all jurisdictions– foster convergence towards a globally consistent supervisory framework

• The ICPs are used in the evaluation of supervisory regimes under theFinancial Sector Assessment Program (FSAP) conducted jointly by theWorld Bank and the International Monetary Fund (IMF).

Global Overview

• For example, the 2015 FSAP for the US released on July 7, 2015concluded that the regulatory environment in US “observed” or “largelyobserved” 21 out of 26 ICPs.

• ICP 16 - Enterprise Risk Management for Solvency Purposes (adopted inOctober of 2010)– The supervisor establishes enterprise risk management requirements for

solvency purposes that require insurers to address all relevant andmaterial risks.

• ICP 17 - Capital Adequacy– The supervisor establishes capital adequacy requirements for solvency

purposes so that insurers can absorb significant unforeseen losses andto provide for degrees of supervisory intervention.

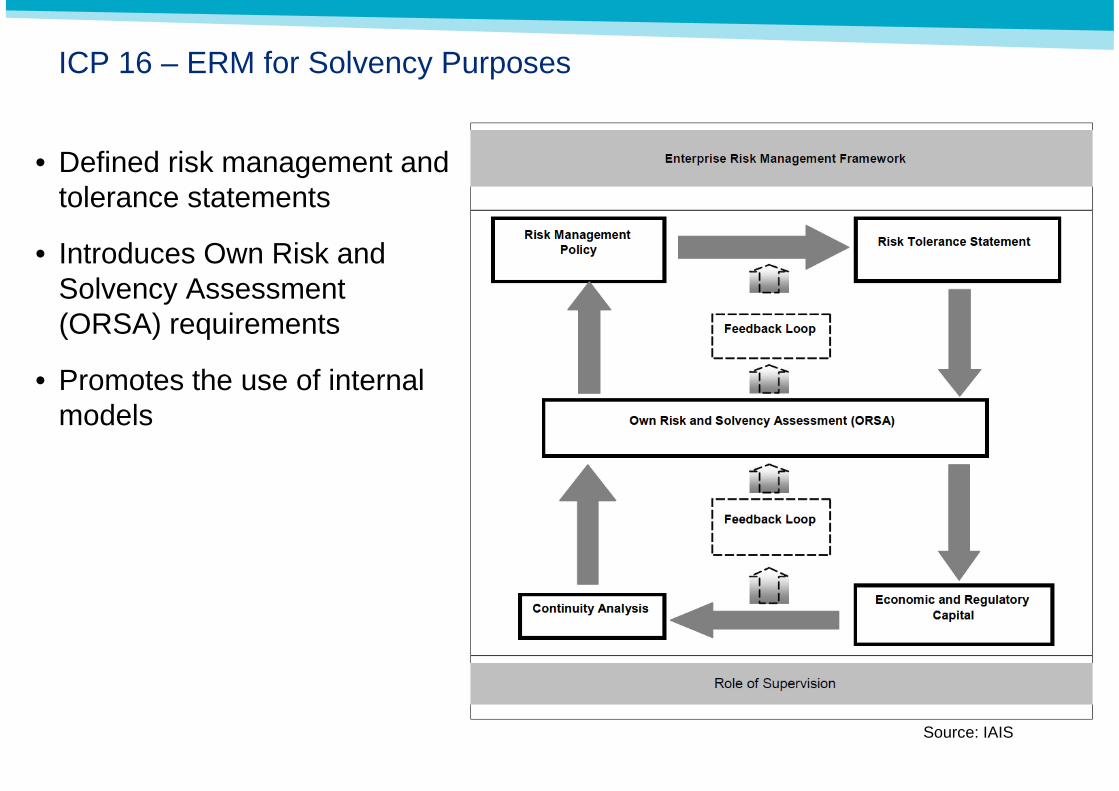

ICP 16 – ERM for Solvency Purposes

• Defined risk management and tolerance statements

• Introduces Own Risk and Solvency Assessment (ORSA) requirements

• Promotes the use of internal models

Source: IAIS

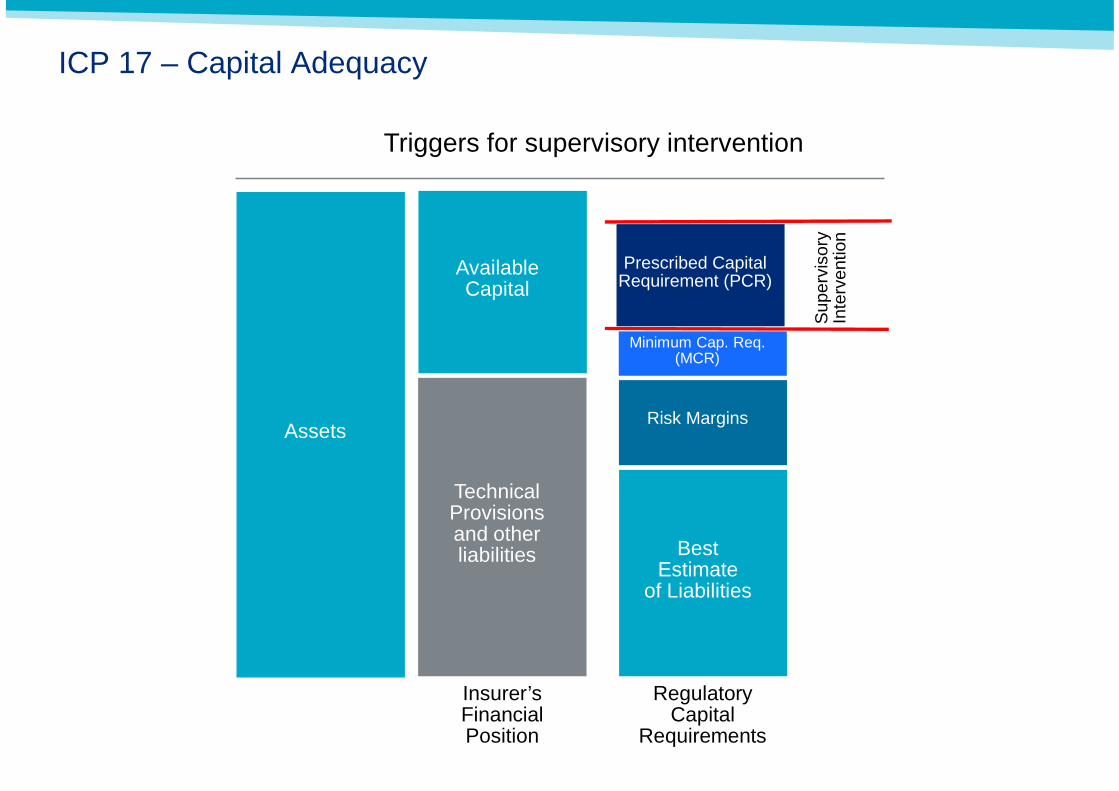

ICP 17 – Capital Adequacy

Technical Provisionsand other liabilities

AvailableCapital

Risk Margins

BestEstimate

of Liabilities

Prescribed Capital Requirement (PCR)

Sup

ervi

sory

Inte

rven

tion

Insurer’sFinancialPosition

RegulatoryCapital

Requirements

Triggers for supervisory intervention

Minimum Cap. Req. (MCR)

Assets

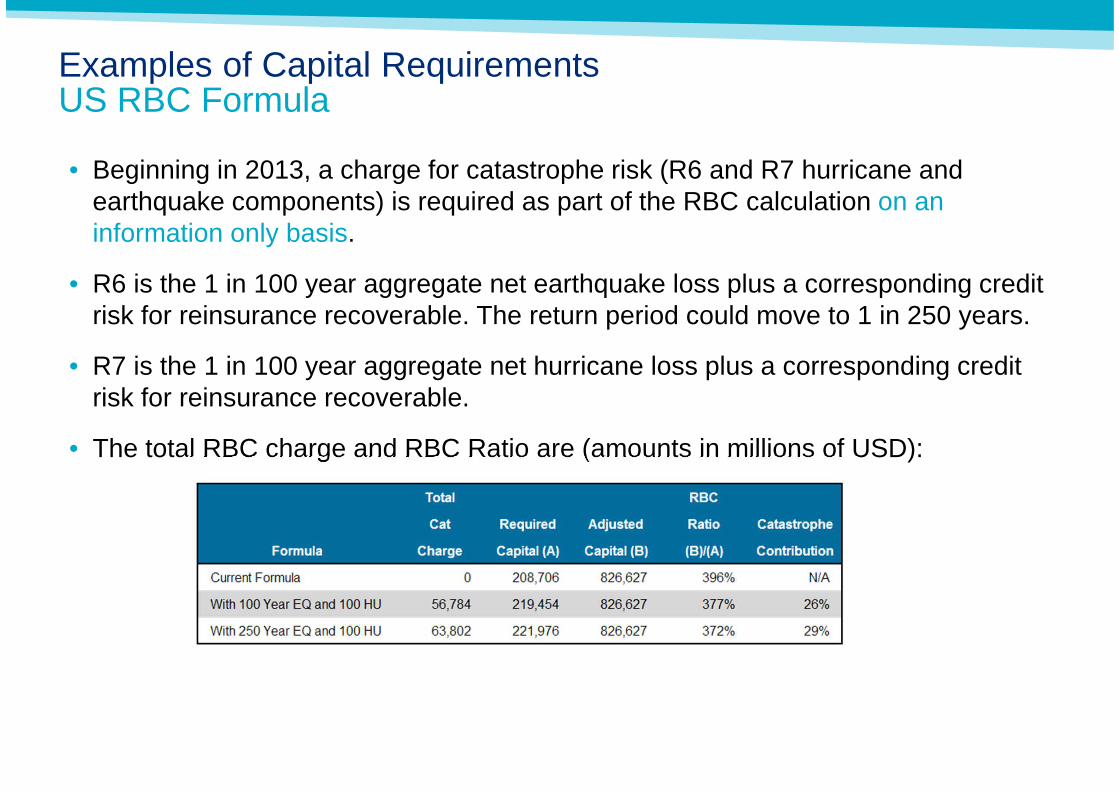

Examples of Capital RequirementsUS RBC Formula

• Beginning in 2013, a charge for catastrophe risk (R6 and R7 hurricane and earthquake components) is required as part of the RBC calculation on an information only basis.

• R6 is the 1 in 100 year aggregate net earthquake loss plus a corresponding credit risk for reinsurance recoverable. The return period could move to 1 in 250 years.

• R7 is the 1 in 100 year aggregate net hurricane loss plus a corresponding credit risk for reinsurance recoverable.

• The total RBC charge and RBC Ratio are (amounts in millions of USD):

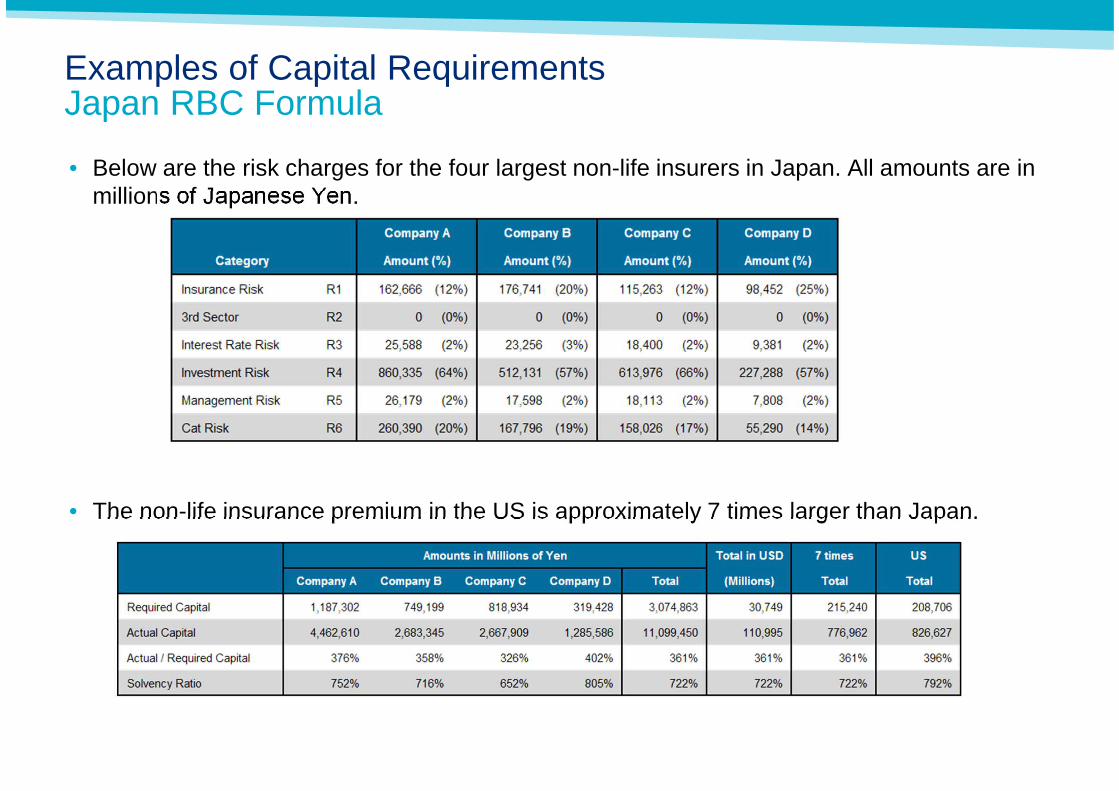

• Below are the risk charges for the four largest non-life insurers in Japan. All amounts are in millions of Japanese Yen.

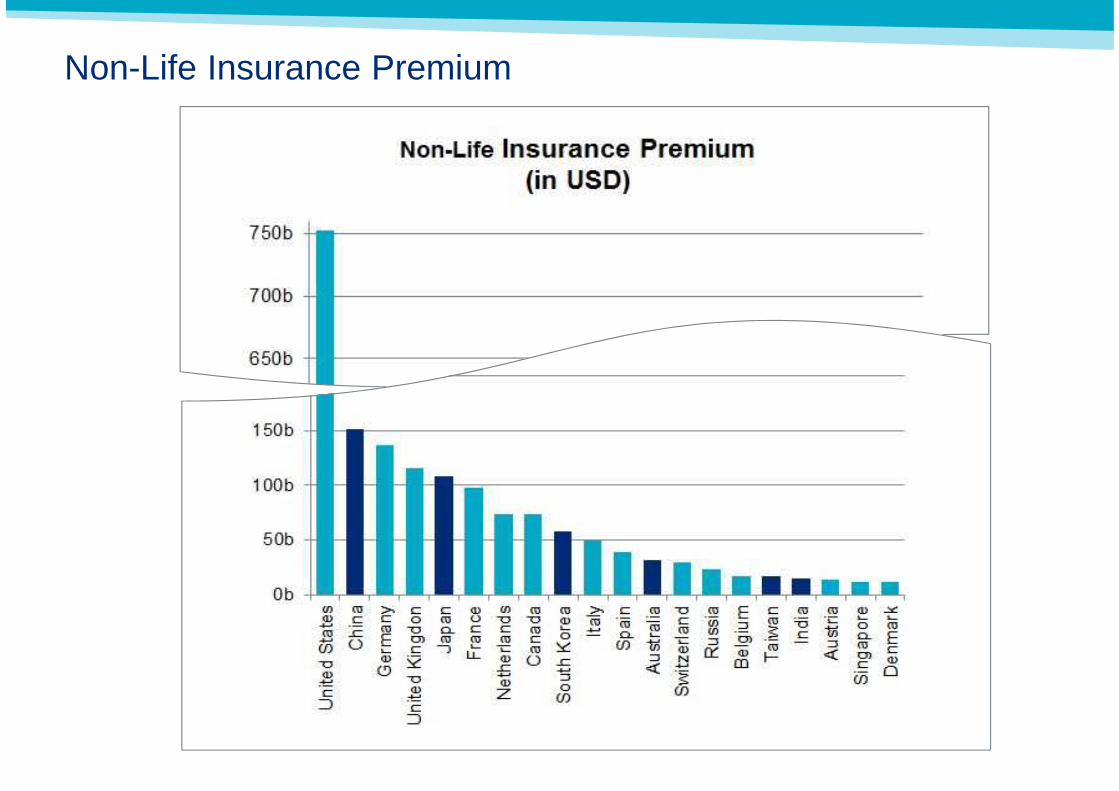

• The non-life insurance premium in the US is approximately 7 times larger than Japan.

Examples of Capital RequirementsJapan RBC Formula

Non-Life Insurance Premium

Section 2

Country UpdatesRegulatory Changes by Country

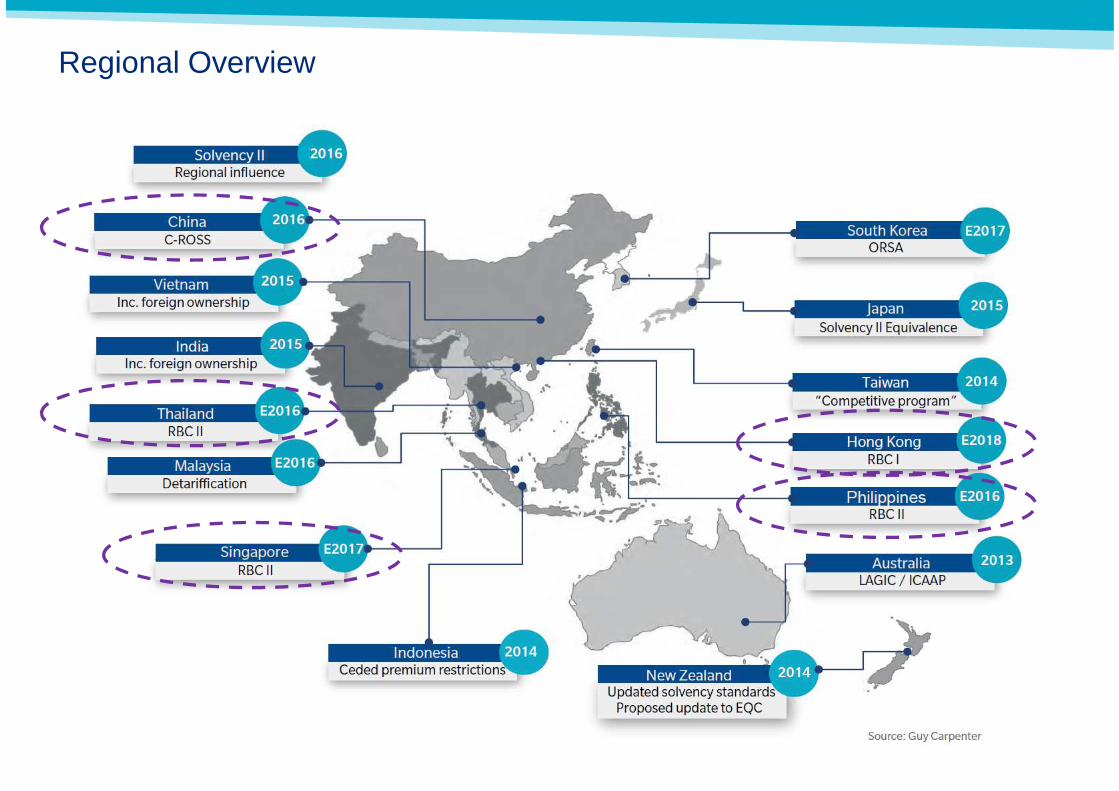

Solvency IIEffective January, 2016

Regional Overview

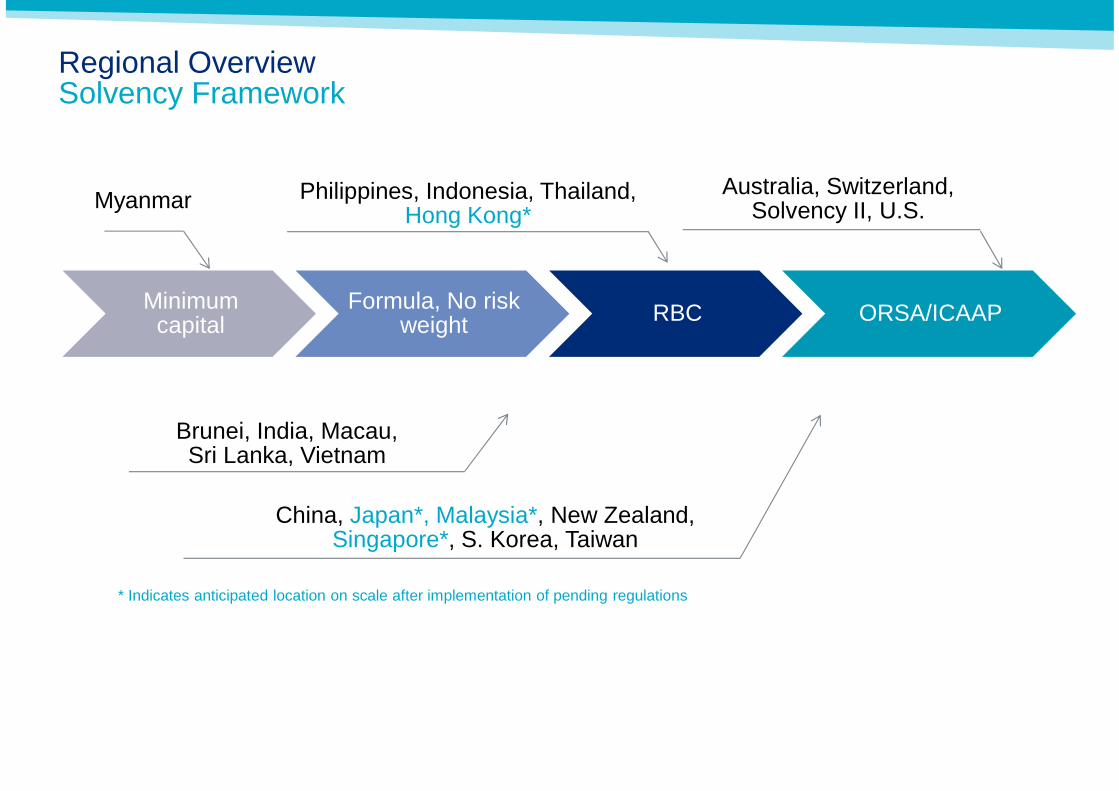

Regional OverviewSolvency Framework

Minimum capital

Formula, No risk weight RBC ORSA/ICAAP

Myanmar

Brunei, India, Macau, Sri Lanka, Vietnam

Philippines, Indonesia, Thailand, Hong Kong*

Australia, Switzerland, Solvency II, U.S.

China, Japan*, Malaysia*, New Zealand, Singapore*, S. Korea, Taiwan

* Indicates anticipated location on scale after implementation of pending regulations

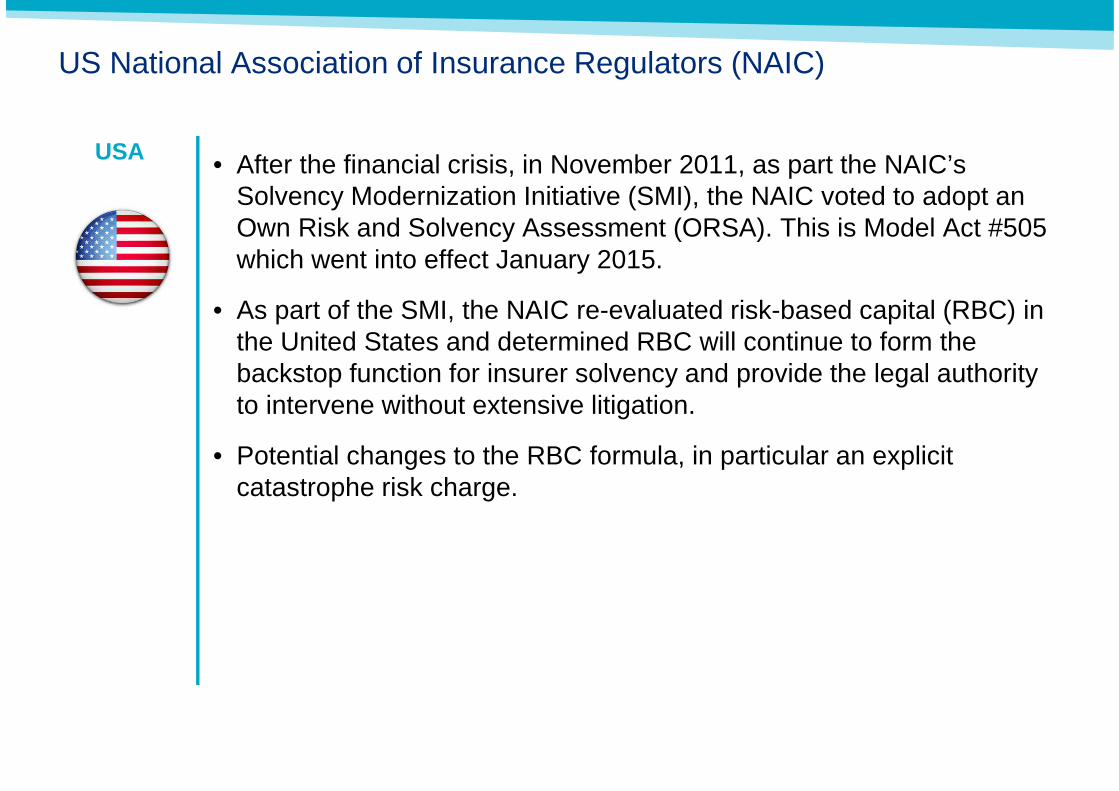

US National Association of Insurance Regulators (NAIC)

• After the financial crisis, in November 2011, as part the NAIC’s Solvency Modernization Initiative (SMI), the NAIC voted to adopt an Own Risk and Solvency Assessment (ORSA). This is Model Act #505 which went into effect January 2015.

• As part of the SMI, the NAIC re-evaluated risk-based capital (RBC) in the United States and determined RBC will continue to form the backstop function for insurer solvency and provide the legal authority to intervene without extensive litigation.

• Potential changes to the RBC formula, in particular an explicit catastrophe risk charge.

USA

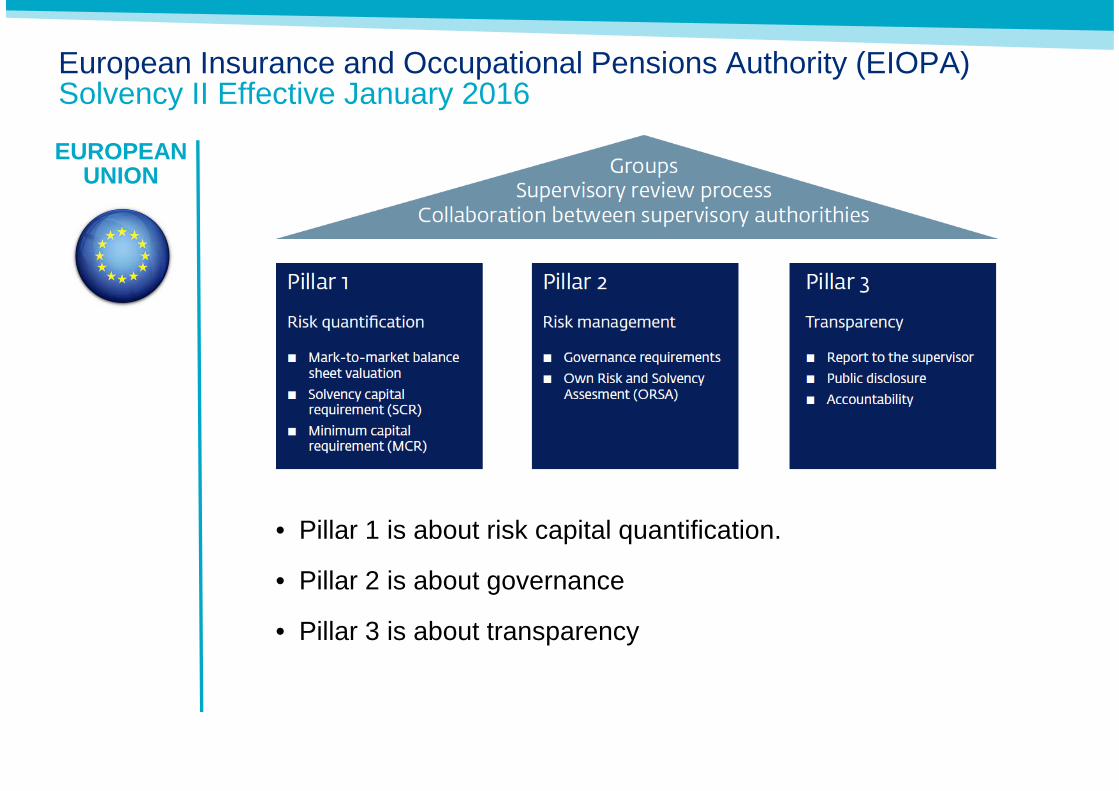

European Insurance and Occupational Pensions Authority (EIOPA)Solvency II Effective January 2016

• Pillar 1 is about risk capital quantification.

• Pillar 2 is about governance

• Pillar 3 is about transparency

EUROPEAN UNION

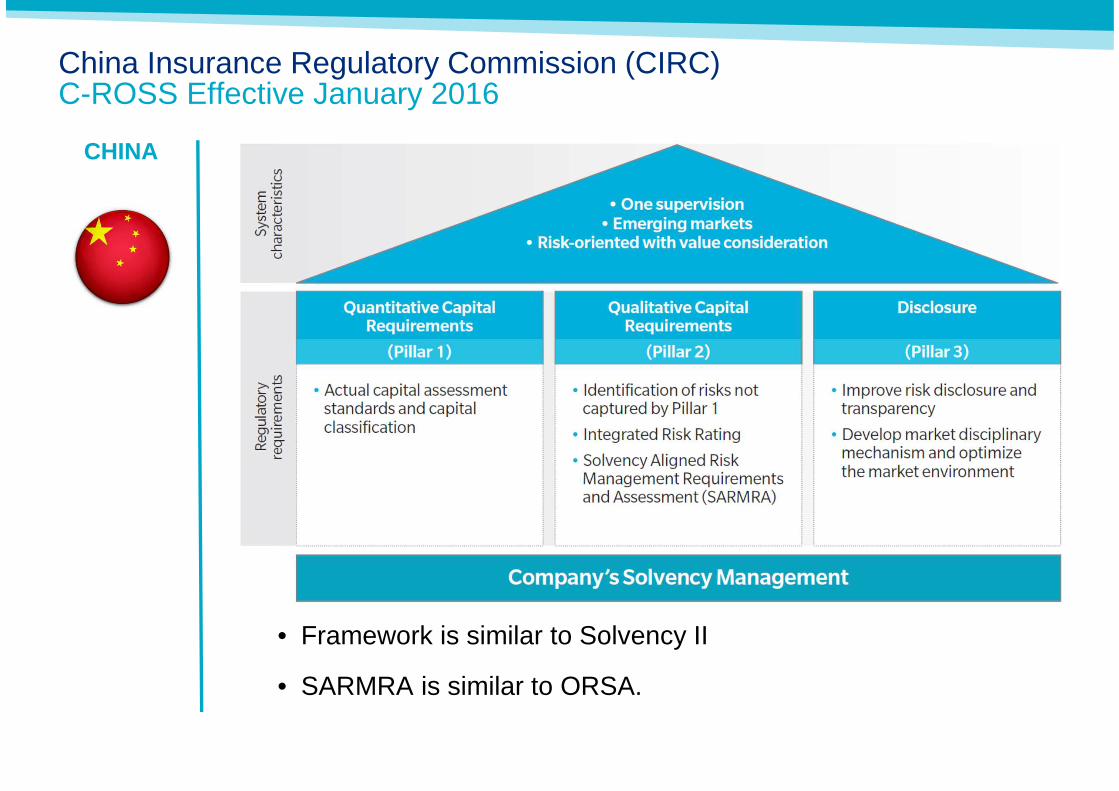

China Insurance Regulatory Commission (CIRC)C-ROSS Effective January 2016

CHINA

• Framework is similar to Solvency II

• SARMRA is similar to ORSA.

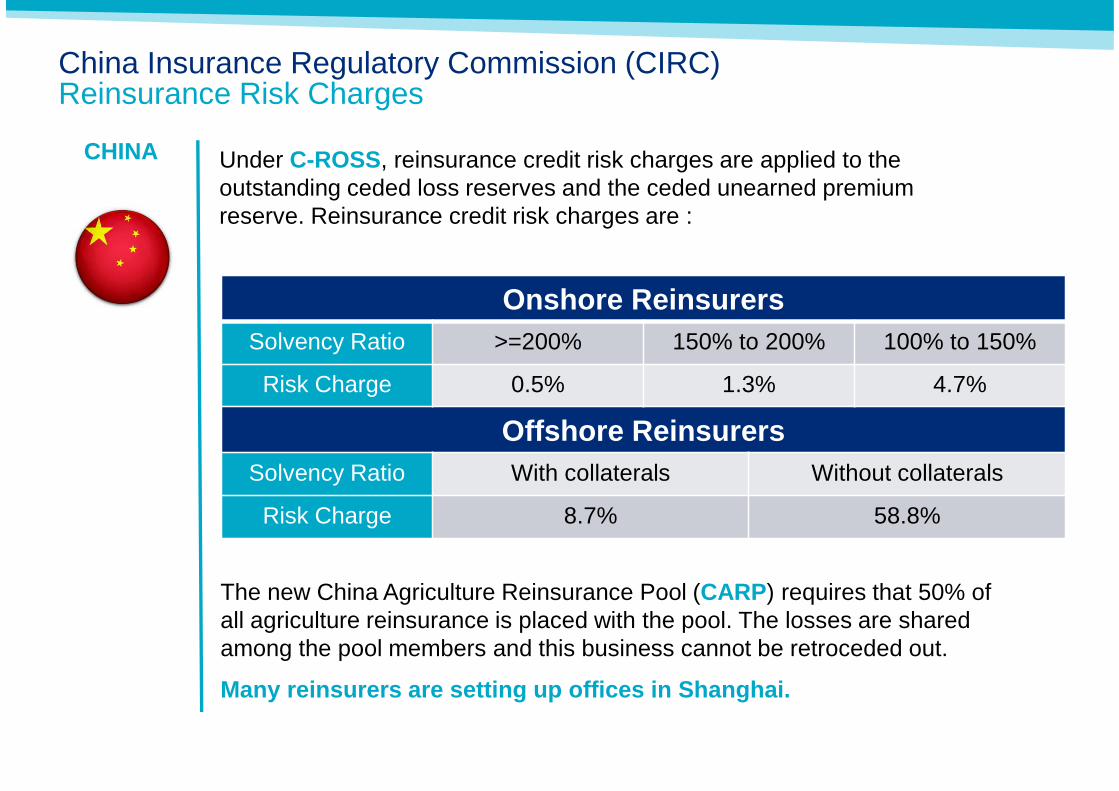

China Insurance Regulatory Commission (CIRC)Reinsurance Risk Charges

CHINA Under C-ROSS, reinsurance credit risk charges are applied to the outstanding ceded loss reserves and the ceded unearned premium reserve. Reinsurance credit risk charges are :

Onshore ReinsurersSolvency Ratio >=200% 150% to 200% 100% to 150%

Risk Charge 0.5% 1.3% 4.7%

Offshore ReinsurersSolvency Ratio With collaterals Without collaterals

Risk Charge 8.7% 58.8%

The new China Agriculture Reinsurance Pool (CARP) requires that 50% of all agriculture reinsurance is placed with the pool. The losses are shared among the pool members and this business cannot be retroceded out.

Many reinsurers are setting up offices in Shanghai.

Australian Prudential Regulation Authority (APRA)

• New capital standards introduced in 2013

• Requires each company to perform an Internal Capital Adequacy Assessment Process (ICAAP). This must be produced annually and include– What is an appropriate level of capital– How and why the capital requirements changed for prior

assessment– Options available to re-capitalize.

AUSTRALIA

Bank Negara Malaysia (BNM)

• Adopted many of the guidelines developed by Australia’s APRA.

• RBC was updated in 2013

• Takaful companies included in 2014.

• BNM also require an ICAAP.

• Current issue is the detariffication of motor and fire rates scheduled for 2016.

MALAYSIA

Financial Services Authority (FSA) in Japan

• In 2014 the FSA required companies to perform an ORSA.

• Applying for equivalency with Solvency II for domestic reinsurance companies writing business in Europe.– This allow Japan domiciled reinsurers to assume business in

Europe without collateral requirements. (Treated the same as European reinsurers).

• Expected to apply for equivalency with Solvency II for insurers in the future.

JAPAN

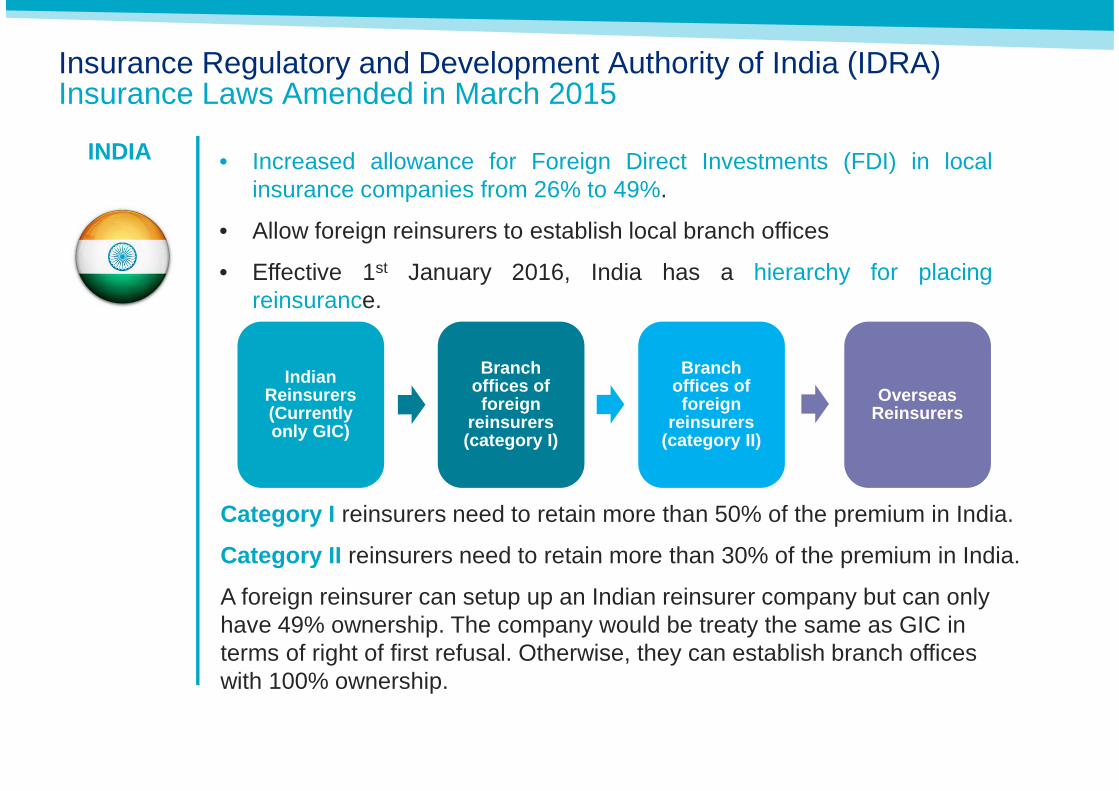

Insurance Regulatory and Development Authority of India (IDRA)Insurance Laws Amended in March 2015

INDIA • Increased allowance for Foreign Direct Investments (FDI) in localinsurance companies from 26% to 49%.

• Allow foreign reinsurers to establish local branch offices

• Effective 1st January 2016, India has a hierarchy for placingreinsurance.

IndianReinsurers(Currently only GIC)

Branch offices of foreign

reinsurers(category I)

Branch offices of foreign

reinsurers(category II)

Overseas Reinsurers

Category I reinsurers need to retain more than 50% of the premium in India.

Category II reinsurers need to retain more than 30% of the premium in India.

A foreign reinsurer can setup up an Indian reinsurer company but can only have 49% ownership. The company would be treaty the same as GIC in terms of right of first refusal. Otherwise, they can establish branch offices with 100% ownership.

Financial Services Authority (OJK)

INDONESIARestrictions on cession to foreign reinsurers. Mandatory cession of 25% to domestic reinsurers. Right of first refusal.

Mandatory 100% cession to domestic reinsurers for motor, PA, surety, credit, and cargo.

Assumes the local reinsurers have the expertise. For example, structure motor solutions could be ceded overseas.

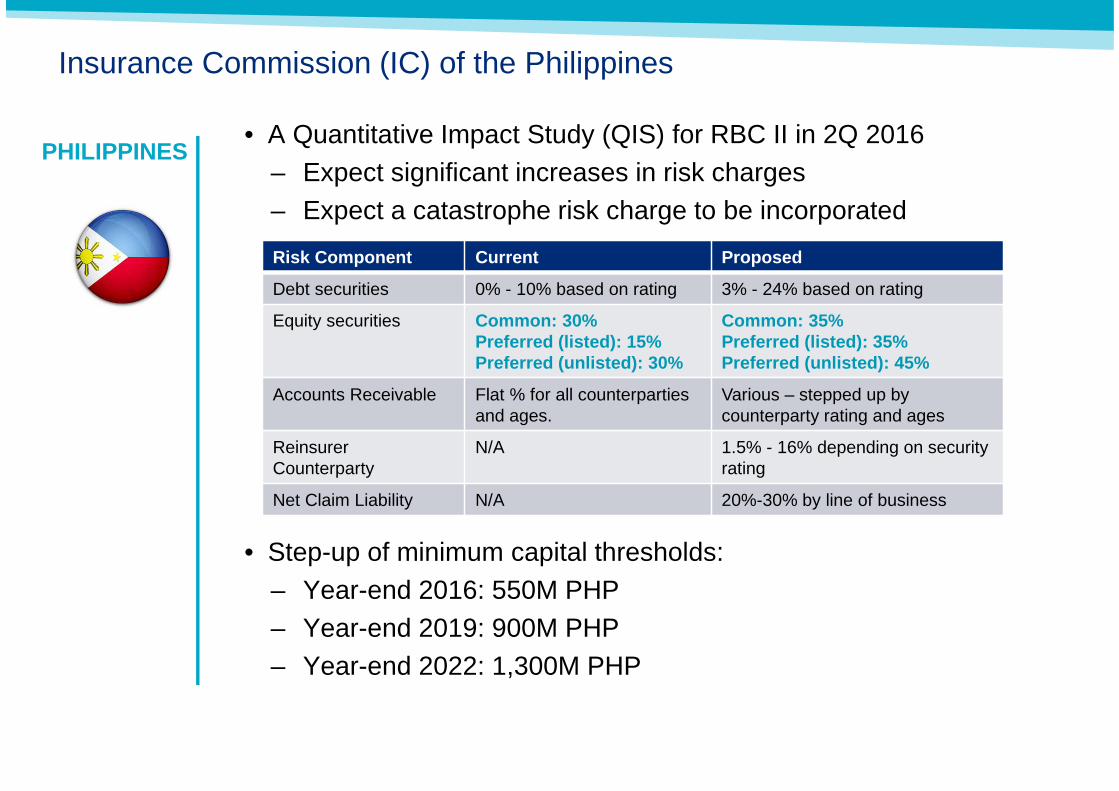

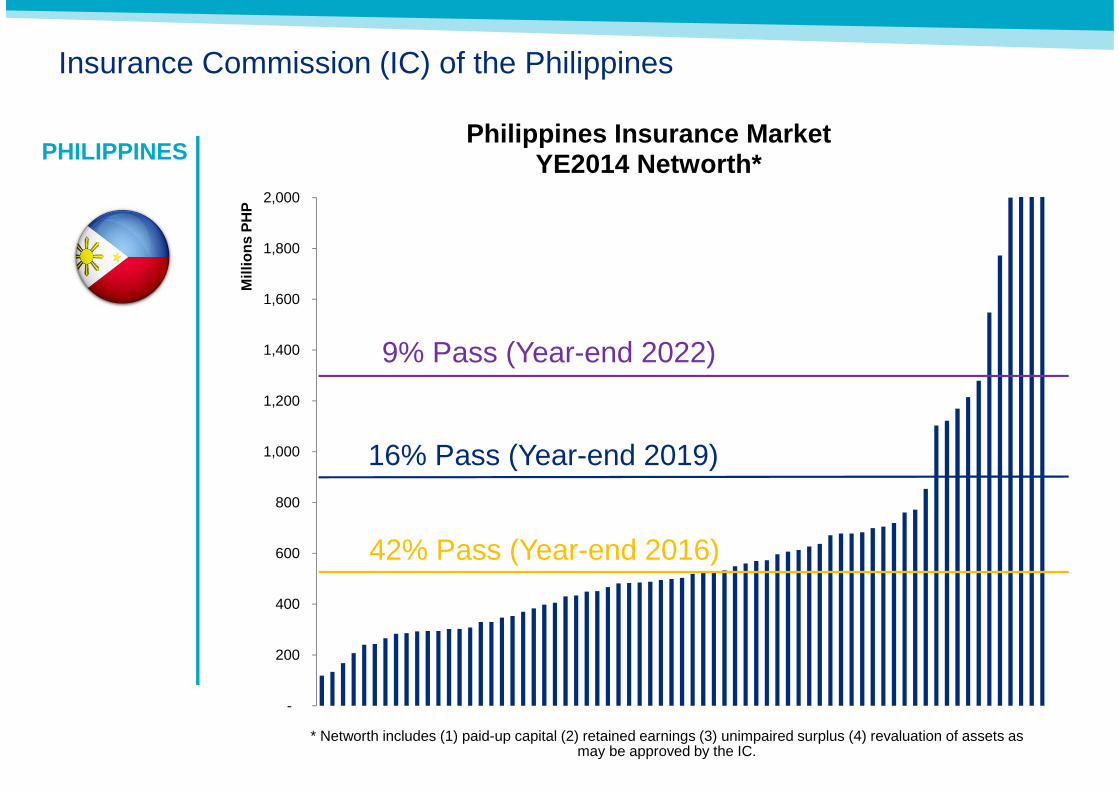

Insurance Commission (IC) of the Philippines

• A Quantitative Impact Study (QIS) for RBC II in 2Q 2016– Expect significant increases in risk charges– Expect a catastrophe risk charge to be incorporated

• Step-up of minimum capital thresholds:– Year-end 2016: 550M PHP– Year-end 2019: 900M PHP– Year-end 2022: 1,300M PHP

Risk Component Current Proposed

Debt securities 0% - 10% based on rating 3% - 24% based on rating

Equity securities Common: 30% Preferred (listed): 15%Preferred (unlisted): 30%

Common: 35% Preferred (listed): 35%Preferred (unlisted): 45%

Accounts Receivable Flat % for all counterparties and ages.

Various – stepped up by counterparty rating and ages

Reinsurer Counterparty

N/A 1.5% - 16% depending on security rating

Net Claim Liability N/A 20%-30% by line of business

PHILIPPINES

Insurance Commission (IC) of the Philippines

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Mill

ions

PH

P

Philippines Insurance Market YE2014 Networth*

* Networth includes (1) paid-up capital (2) retained earnings (3) unimpaired surplus (4) revaluation of assets as may be approved by the IC.

42% Pass (Year-end 2016)

16% Pass (Year-end 2019)

9% Pass (Year-end 2022)

PHILIPPINES

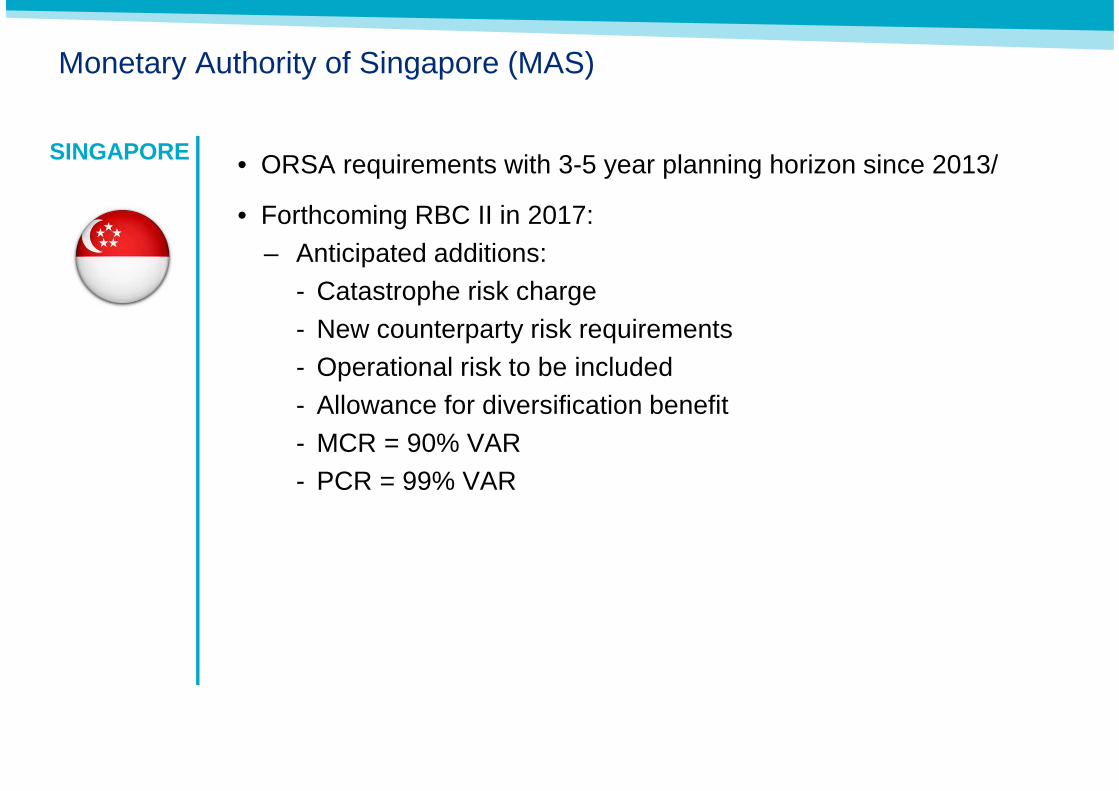

Monetary Authority of Singapore (MAS)

• ORSA requirements with 3-5 year planning horizon since 2013/

• Forthcoming RBC II in 2017: – Anticipated additions:

- Catastrophe risk charge- New counterparty risk requirements- Operational risk to be included- Allowance for diversification benefit- MCR = 90% VAR - PCR = 99% VAR

SINGAPORE

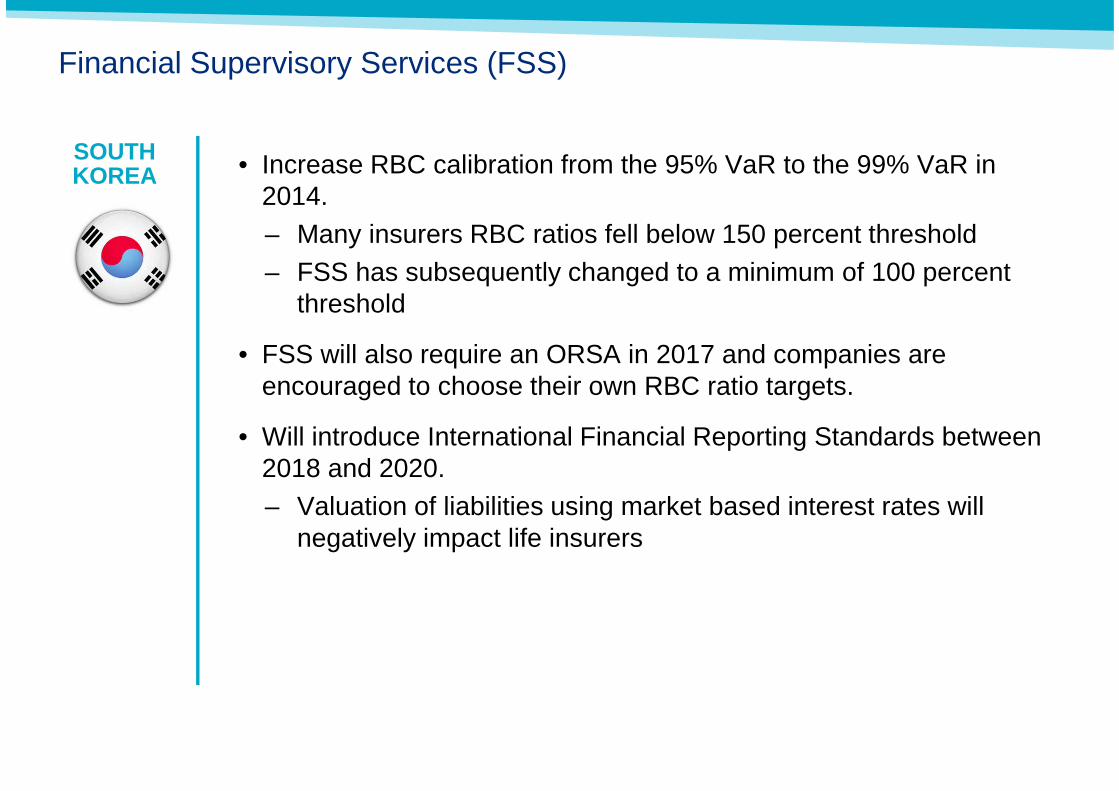

Financial Supervisory Services (FSS)

• Increase RBC calibration from the 95% VaR to the 99% VaR in 2014.– Many insurers RBC ratios fell below 150 percent threshold– FSS has subsequently changed to a minimum of 100 percent

threshold

• FSS will also require an ORSA in 2017 and companies are encouraged to choose their own RBC ratio targets.

• Will introduce International Financial Reporting Standards between 2018 and 2020. – Valuation of liabilities using market based interest rates will

negatively impact life insurers

SOUTH KOREA

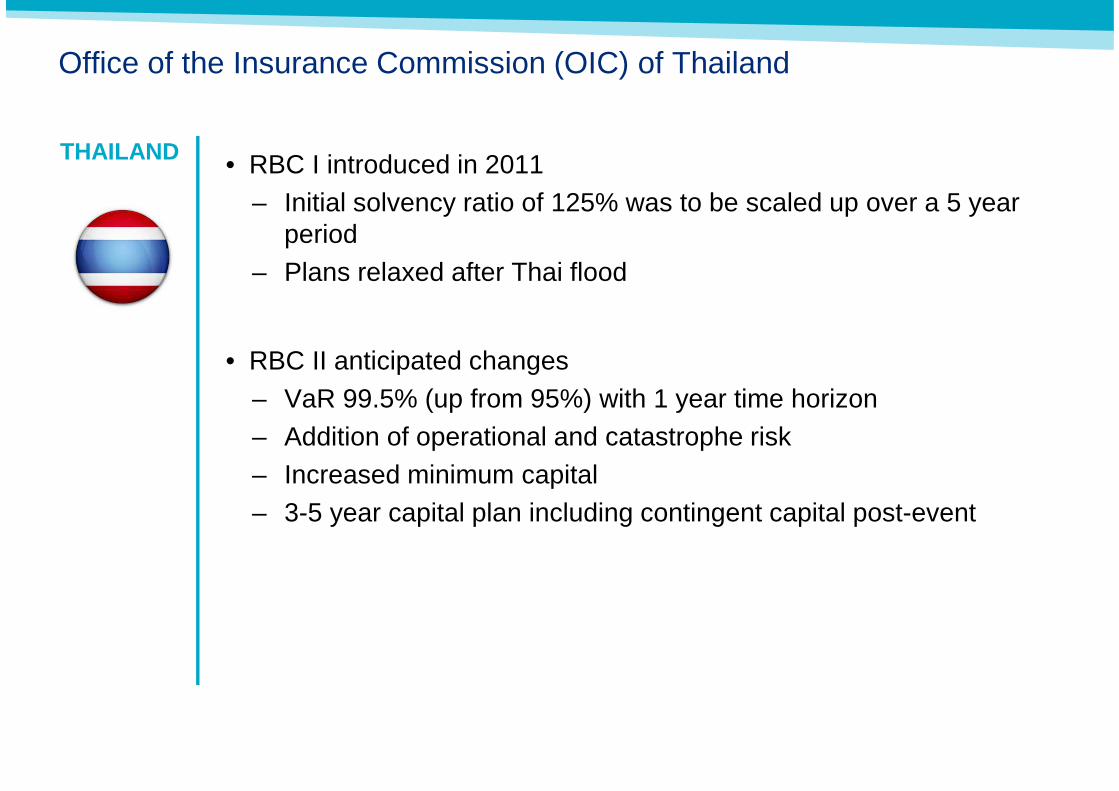

Office of the Insurance Commission (OIC) of Thailand

• RBC I introduced in 2011– Initial solvency ratio of 125% was to be scaled up over a 5 year

period– Plans relaxed after Thai flood

• RBC II anticipated changes– VaR 99.5% (up from 95%) with 1 year time horizon– Addition of operational and catastrophe risk– Increased minimum capital– 3-5 year capital plan including contingent capital post-event

THAILAND

27July 18, 2016

Section 3

Rating AgenciesNew AM Best Credit Rating and SRQ

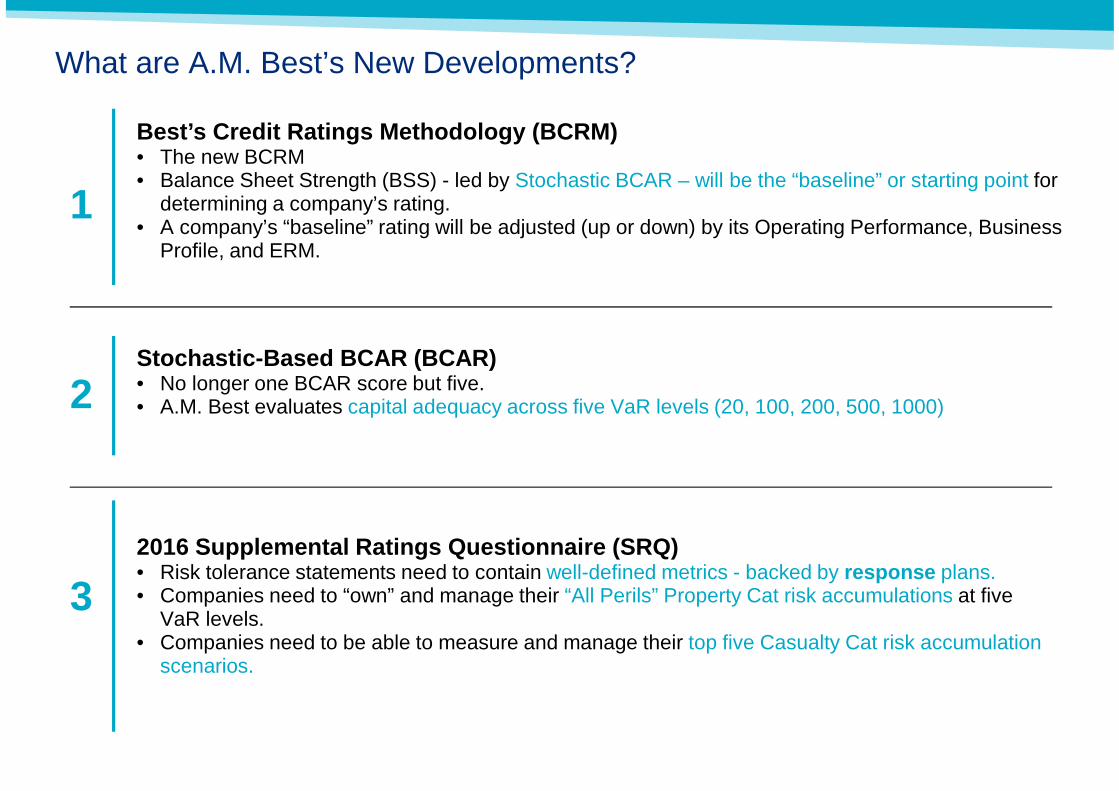

What are A.M. Best’s New Developments?

Best’s Credit Ratings Methodology (BCRM)• The new BCRM • Balance Sheet Strength (BSS) - led by Stochastic BCAR – will be the “baseline” or starting point for

determining a company’s rating.• A company’s “baseline” rating will be adjusted (up or down) by its Operating Performance, Business

Profile, and ERM.

3

2

1

Stochastic-Based BCAR (BCAR)• No longer one BCAR score but five.• A.M. Best evaluates capital adequacy across five VaR levels (20, 100, 200, 500, 1000)

2016 Supplemental Ratings Questionnaire (SRQ)• Risk tolerance statements need to contain well-defined metrics - backed by response plans.• Companies need to “own” and manage their “All Perils” Property Cat risk accumulations at five

VaR levels.• Companies need to be able to measure and manage their top five Casualty Cat risk accumulation

scenarios.

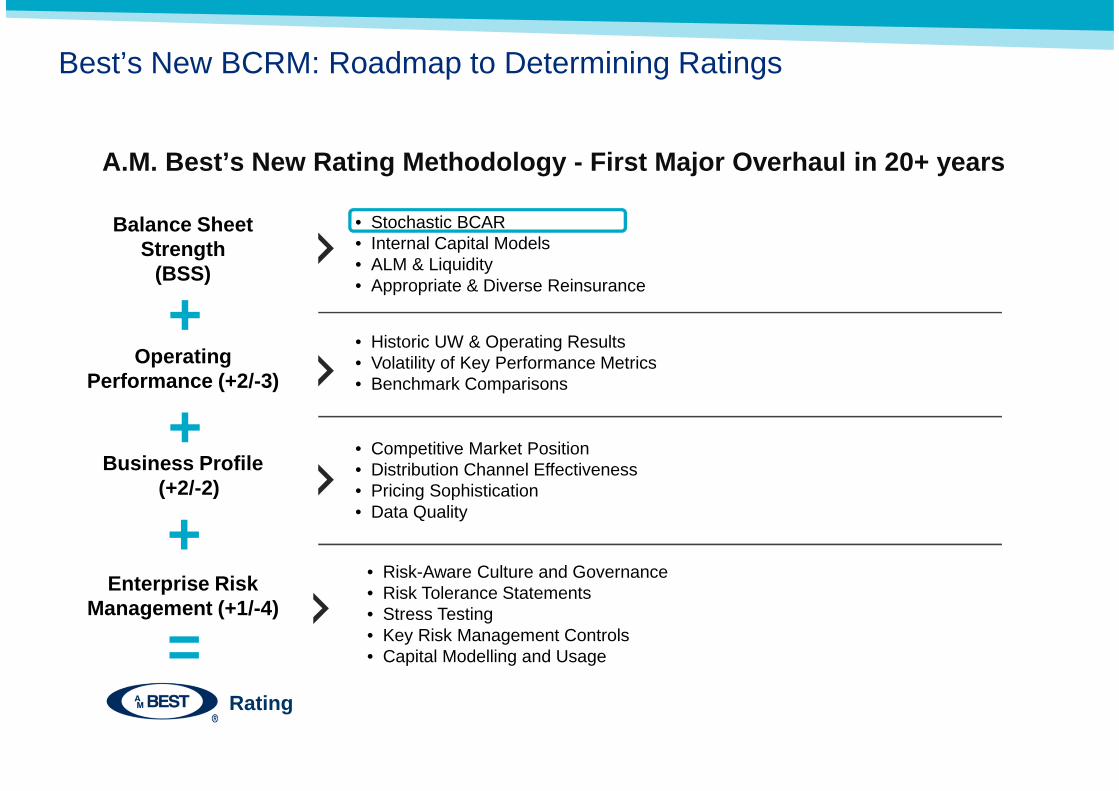

Business Profile(+2/-2)

Balance Sheet Strength

(BSS)

Operating Performance (+2/-3)

Enterprise Risk Management (+1/-4)

• Stochastic BCAR • Internal Capital Models• ALM & Liquidity• Appropriate & Diverse Reinsurance

• Historic UW & Operating Results• Volatility of Key Performance Metrics• Benchmark Comparisons

Rating

• Competitive Market Position• Distribution Channel Effectiveness• Pricing Sophistication• Data Quality

• Risk-Aware Culture and Governance• Risk Tolerance Statements• Stress Testing• Key Risk Management Controls• Capital Modelling and Usage

Best’s New BCRM: Roadmap to Determining Ratings

A.M. Best’s New Rating Methodology - First Major Ove rhaul in 20+ years

+

+

+

=

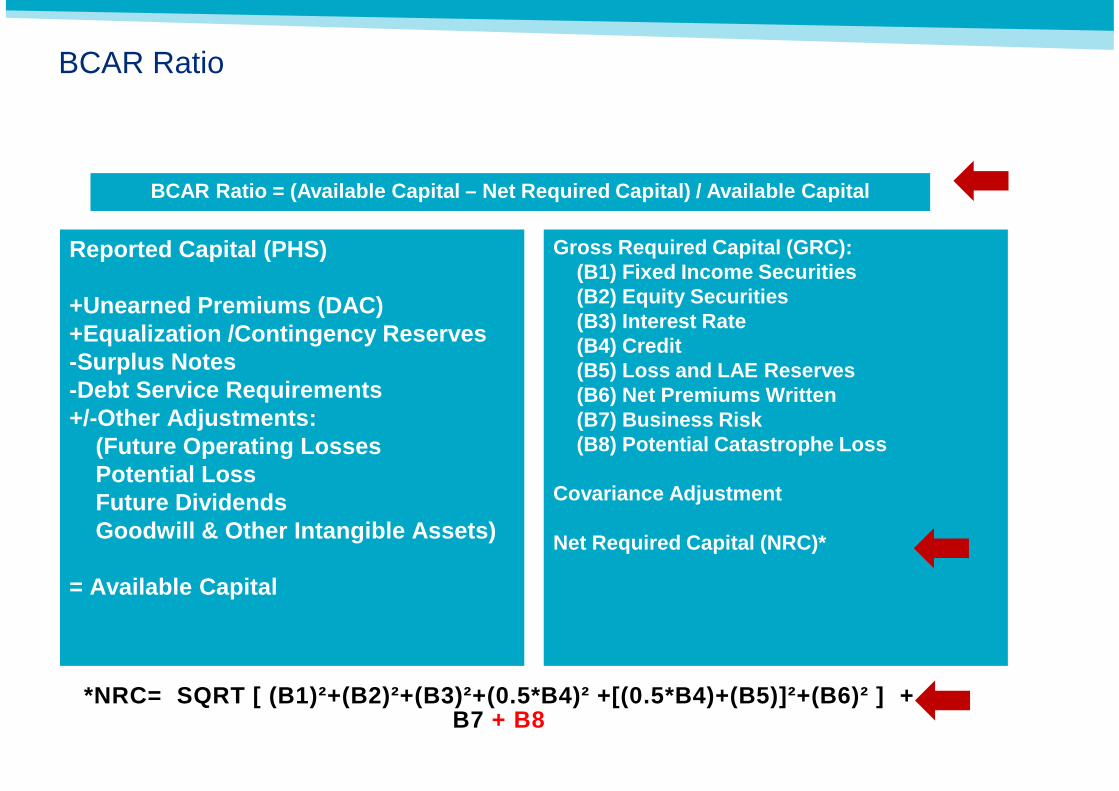

BCAR Ratio

Reported Capital (PHS)

+Unearned Premiums (DAC)+Equalization /Contingency Reserves-Surplus Notes-Debt Service Requirements+/-Other Adjustments:

(Future Operating LossesPotential LossFuture DividendsGoodwill & Other Intangible Assets)

= Available Capital

Gross Required Capital (GRC):(B1) Fixed Income Securities(B2) Equity Securities(B3) Interest Rate(B4) Credit(B5) Loss and LAE Reserves(B6) Net Premiums Written(B7) Business Risk(B8) Potential Catastrophe Loss

Covariance Adjustment

Net Required Capital (NRC)*

BCAR Ratio = (Available Capital – Net Required Capit al) / Available Capital

*NRC= SQRT [ (B1)²+(B2)²+(B3)²+(0.5*B4)² +[(0.5*B4 )+(B5)]²+(B6)² ] + B7 + B8

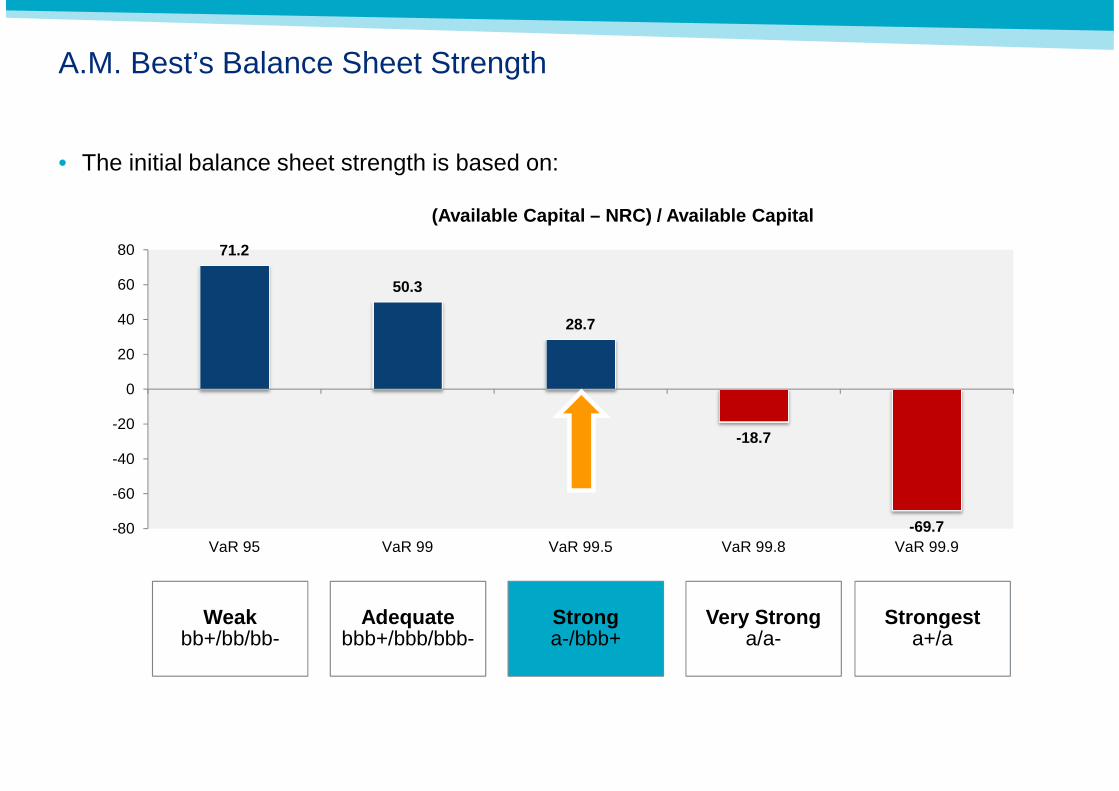

A.M. Best’s Balance Sheet Strength

71.2

50.3

28.7

-18.7

-69.7-80

-60

-40

-20

0

20

40

60

80

VaR 95 VaR 99 VaR 99.5 VaR 99.8 VaR 99.9

(Available Capital – NRC) / Available Capital

Weakbb+/bb/bb-

Adequatebbb+/bbb/bbb-

Stronga-/bbb+

Very Stronga/a-

Strongesta+/a

• The initial balance sheet strength is based on:

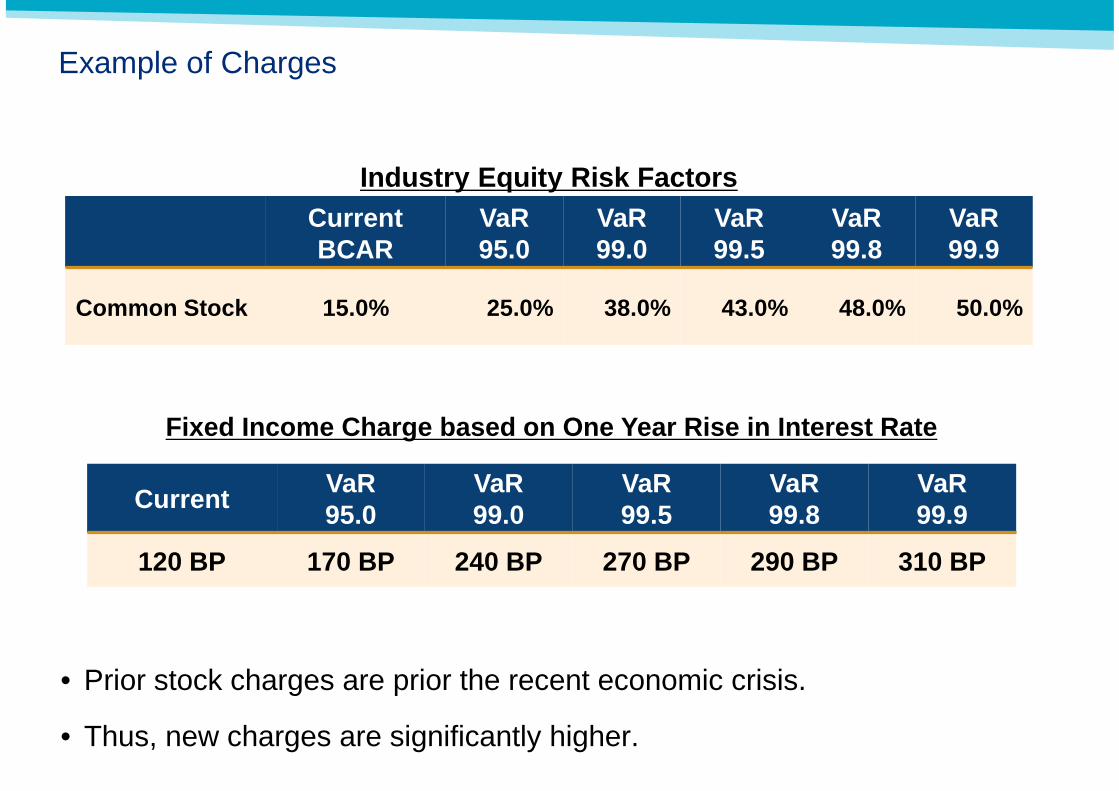

Example of Charges

• Prior stock charges are prior the recent economic crisis.

• Thus, new charges are significantly higher.

Industry Equity Risk FactorsCurrentBCAR

VaR95.0

VaR99.0

VaR 99.5

VaR 99.8

VaR 99.9

Common Stock 15.0% 25.0% 38.0% 43.0% 48.0% 50.0%

Fixed Income Charge based on One Year Rise in Intere st Rate

CurrentVaR95.0

VaR99.0

VaR99.5

VaR99.8

VaR99.9

120 BP 170 BP 240 BP 270 BP 290 BP 310 BP

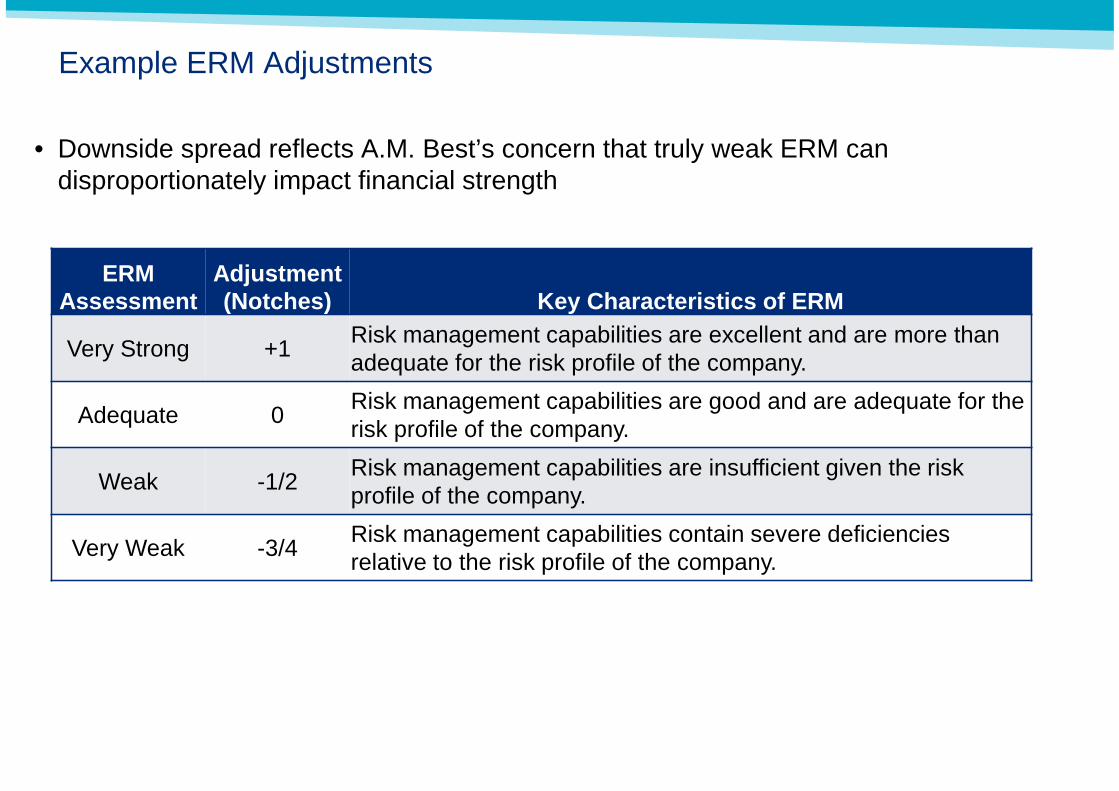

Example ERM Adjustments

• Downside spread reflects A.M. Best’s concern that truly weak ERM can disproportionately impact financial strength

ERM Assessment

Adjustment (Notches) Key Characteristics of ERM

Very Strong +1Risk management capabilities are excellent and are more than adequate for the risk profile of the company.

Adequate 0Risk management capabilities are good and are adequate for the risk profile of the company.

Weak -1/2Risk management capabilities are insufficient given the risk profile of the company.

Very Weak -3/4Risk management capabilities contain severe deficiencies relative to the risk profile of the company.

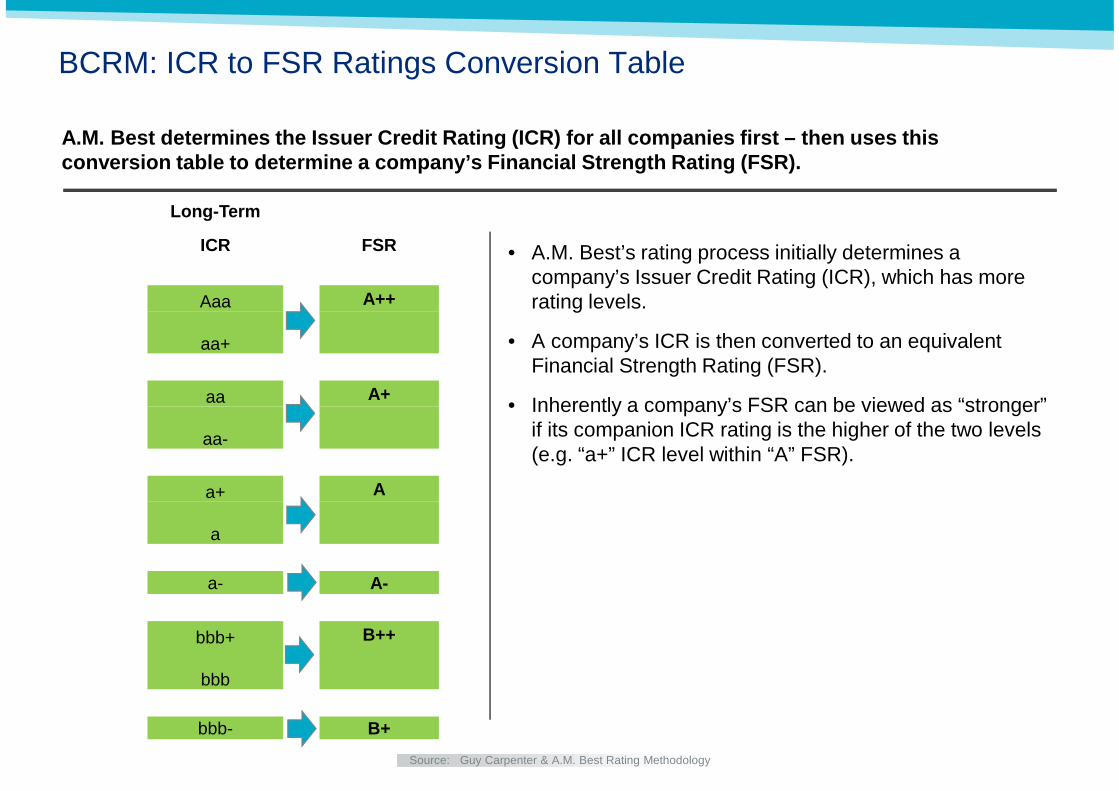

• A.M. Best’s rating process initially determines a company’s Issuer Credit Rating (ICR), which has more rating levels.

• A company’s ICR is then converted to an equivalent Financial Strength Rating (FSR).

• Inherently a company’s FSR can be viewed as “stronger” if its companion ICR rating is the higher of the two levels (e.g. “a+” ICR level within “A” FSR).

Long-Term

ICR FSR

Aaa A++

aa+

aa A+

aa-

a+ A

a

a- A-

bbb+ B++

bbb

bbb- B+

BCRM: ICR to FSR Ratings Conversion Table

A.M. Best determines the Issuer Credit Rating (ICR) for all companies first – then uses this conversion table to determine a company’s Financial Strength Rating (FSR).

Source: Guy Carpenter & A.M. Best Rating Methodology

• AM Best’s SRQ has 28 ERM.

• Question I10 - Please state any overall risk appetite and risk tolerancestatement(s) that have been established or approved by a board or seniormanagement.

• Question I4 - How often does the board review whether its risk tolerances are acceptable? (reporting)

• Question I11 - Who is most responsible for monitoring whether risk tolerances are exceeded? (governance)

• Question I14 - Does management have detailed procedures in place in the event risk tolerances are exceeded? (contingency plans)

• Question I15 - What are the company's largest net accumulated exposure at a single location and for a single account based on all exposures combined?

A.M. Best’s 2015 Supplemental Rating Questionnaire (SRQ)Enterprise Risk Management Questions

• AM Best’s SRQ has 14 Catastrophe Risk Questions

• They ask for windstorm, earthquake, other, and combined OEP and AEP results, gross and net of reinsurance, at the 20, 50, 100, 200, 250, 500, and 1000 year basis (VaR basis) (Question F1)

• Question F4 - Please provide your company's tail value at risk (TVAR) or Tail Conditional Expectation (TCE) above the loss return thresholds of 20, 50, 100, 200, 250, 500 and 1,000 years on a per occurrence basis.

• Question F5 asks which vendor models where used, the version, who ran the analysis and question F6 asks what options have been used. The options mentioned are demand surge, storm surge, fire following, secondary uncertainty, mid-term view for Atlantic Multidecadal Oscilation (AMO).

• Question F7 - Has the default weighting between the attenuation functions/relationships been changed with respect to the earthquake model?

A.M. Best’s 2015 Supplemental Rating Questionnaire (SRQ)Catastrophe Risk Management Questions

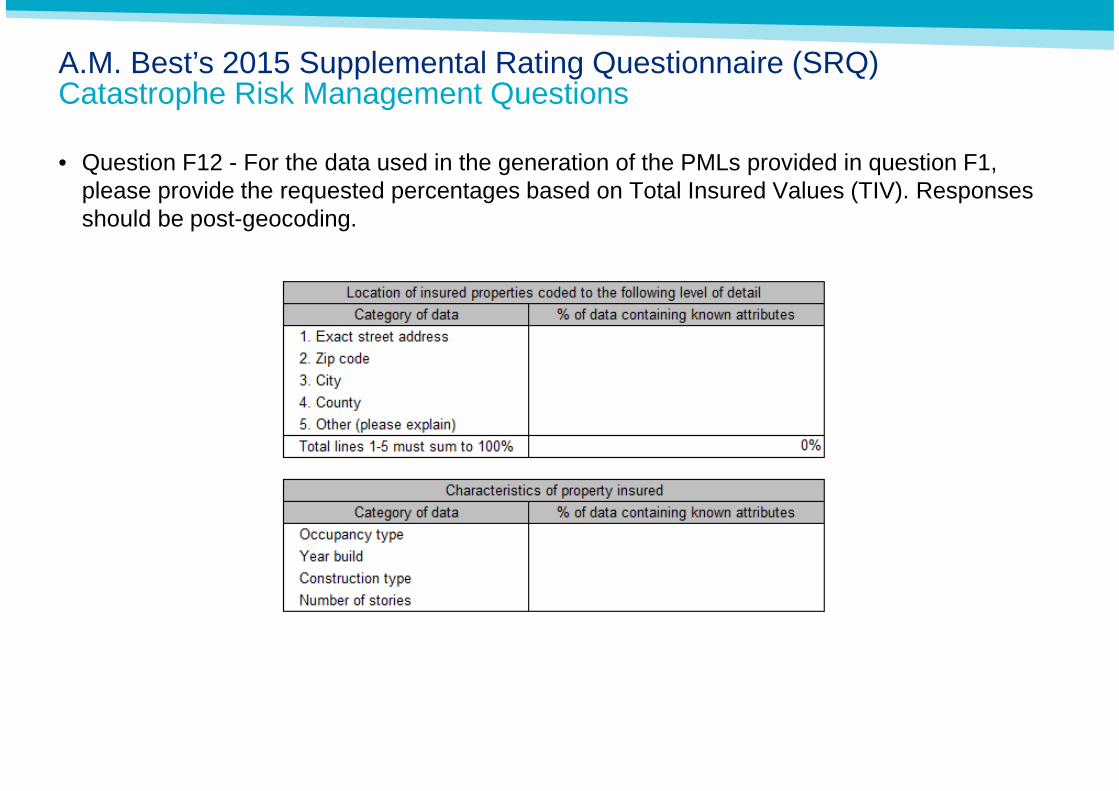

• Question F12 - For the data used in the generation of the PMLs provided in question F1, please provide the requested percentages based on Total Insured Values (TIV). Responses should be post-geocoding.

A.M. Best’s 2015 Supplemental Rating Questionnaire (SRQ)Catastrophe Risk Management Questions

About Guy Carpenter

Guy Carpenter & Company, LLC is a leading global risk and reinsurance specialist. Since 1922, the company has delivered integrated reinsurance andcapital market solutions to clients across the globe. As a most trusted and valuable reinsurance broker and strategic advisor, Guy Carpenter leverages itsintellectual capital to anticipate and solve for a range of business challenges and opportunities on behalf of its clients. With over 2,300 professionals in morethan 60 offices around the world, Guy Carpenter delivers a powerful combination of broking expertise, strategic advisory services and industry-leadinganalytics to help clients achieve profitable growth. For more information on Guy Carpenter’s complete line-of-business expertise and range of business units,including GC Specialties, GC Analytics®, GC Fac®, Global Strategic Advisory, GC Securities*, Client Services and GC Micro Risk Solutions®, please visitwww.guycarp.com and follow Guy Carpenter on LinkedIn and Twitter @GuyCarpenter.

Guy Carpenter is a wholly owned subsidiary of Marsh & McLennan Companies (NYSE: MMC), a global professional services firm offering clients advice andsolutions in the areas of risk, strategy, and people. With annual revenue of $13 billion and 60,000 colleagues worldwide, Marsh & McLennan Companiesprovides analysis, advice, and transactional capabilities to clients in more than 130 countries through: Marsh, a leader in insurance broking and riskmanagement; Mercer, a leader in talent, health, retirement, and investment consulting; and Oliver Wyman, a leader in management consulting. Marsh &McLennan is committed to being a responsible corporate citizen and making a positive impact in the communities in which it operates. Visit www.mmc.comfor more information and follow us on LinkedIn and Twitter @MMC_Global.

*Securities or investments, as applicable, are offered in the United States through GC Securities, a division of MMC Securities LLC, a US registered broker-dealer andmember FINRA/NFA/SIPC. Main Office: 1166 Avenue of the Americas, New York, NY 10036. Phone: (212) 345-5000. Securities or investments, as applicable, are offered inthe European Union by GC Securities, a division of MMC Securities (Europe) Ltd. (MMCSEL), which is authorized and regulated by the Financial Conduct Authority, mainoffice 25 The North Colonnade, Canary Wharf, London E14 5HS. Reinsurance products are placed through qualified affiliates of Guy Carpenter & Company, LLC. MMCSecurities LLC, MMC Securities (Europe) Ltd. and Guy Carpenter & Company, LLC are affiliates owned by Marsh & McLennan Companies. This communication is notintended as an offer to sell or a solicitation of any offer to buy any security, financial instrument, reinsurance or insurance product.

Disclaimer

Guy Carpenter & Company, LLC provides this presentation for general information only. The information contained herein is based on sources we believereliable, but we do not guarantee its accuracy, and it should be understood to be general insurance/reinsurance information only. Guy Carpenter & Company,LLC makes no representations or warranties, express or implied. The information is not intended to be taken as advice with respect to any individual situationand cannot be relied upon as such.

Statements concerning tax, accounting, legal or regulatory matters should be understood to be general observations based solely on our experience asreinsurance brokers and risk consultants, and may not be relied upon as tax, accounting, legal or regulatory advice, which we are not authorized to provide.All such matters should be reviewed with your own qualified advisors in these areas.

Readers are cautioned not to place undue reliance on any historical, current or forward-looking statements. Guy Carpenter & Company, LLC undertakes noobligation to update or revise publicly any historical, current or forward-looking statements, whether as a result of new information, research, future events orotherwise.

The trademarks and service marks contained herein are the property of their respective owners.

© 2016 Guy Carpenter & Company, LLC

All rights reserved.