recent trends & developments in ghana’s mining fiscal regime b.n.a. aryee advisor (mining)...

TRANSCRIPT

RECENT TRENDS & DEVELOPMENTS IN GHANA’S

MINING FISCAL REGIME

B.N.A. AryeeAdvisor (Mining)

Ministry of Lands & Natural Resources, Ghana

PRESENTATION OUTLINE

• Background & Introduction• Rationale for Recent Mining Fiscal Regime

Reform• Recent Trends in Ghana’s Mining Fiscal Regime• Other Developments• Guidance Questions & Answers

• Ghana is a significant gold producer in Africa (second after South Africa) and globally, being the 9th largest producer in the world.

• In 2013, Ghana produced about 4.3 million ounces of gold, only a marginal decline from the 2012 highest ever production in the history of the country,

BACKGROUND & INTRODUCTIONBACKGROUND & INTRODUCTION

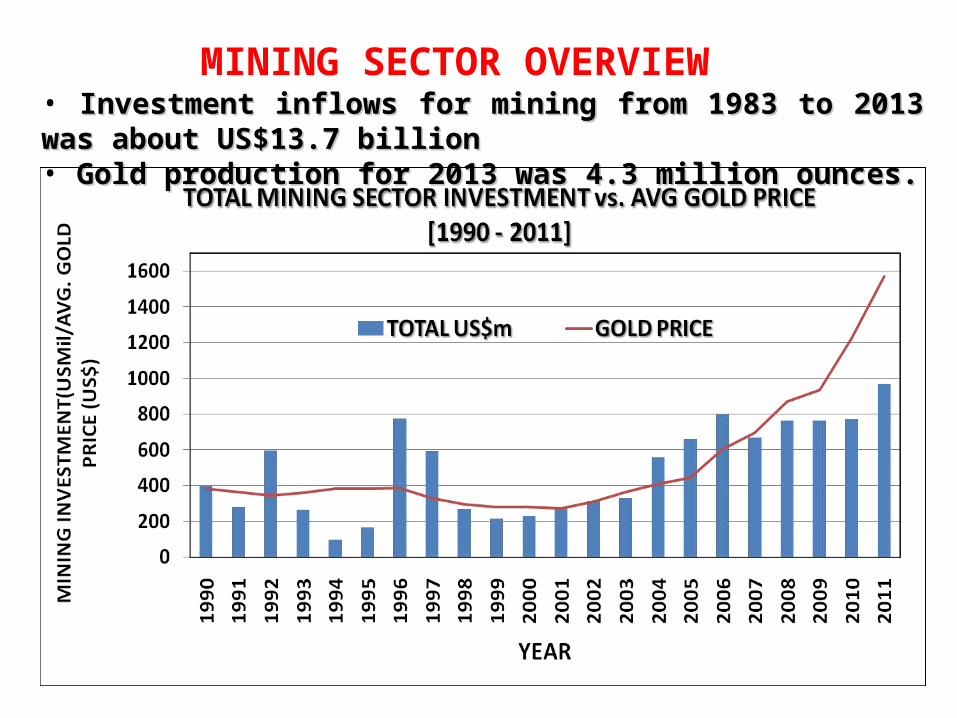

MINING SECTOR OVERVIEW• Investment inflows for mining from 1983 to 2013 was about US$13.7 billionInvestment inflows for mining from 1983 to 2013 was about US$13.7 billion• Gold production for 2013 was 4.3 million ounces.Gold production for 2013 was 4.3 million ounces.

OVERVIEW: MINERAL PRODUCTIONOVERVIEW: MINERAL PRODUCTION

OVERVIEW: MERCHANDISE EXPORTSOVERVIEW: MERCHANDISE EXPORTS

• The significant investment over the years and consequently mineral outputs led to an increased sector contribution to the economy of:

28% of Government revenue as collected by the

Ghana Revenue Authority in 2012

Export revenues from the mineral sector amounted

to US$5.1 billion in 2013 & accounted for 42% of total merchandise export in 2012

Employed 28,000 for large scale and estimated over 1

million people for small scale mining.

MINING SECTOR OVERVIEW

RATIONALE FOR THE RECENT REVIEW RATIONALE FOR THE RECENT REVIEW OF THE FISCAL REGIME 1OF THE FISCAL REGIME 1

Speaking at the recent World Economic Forum in Davos, Switzerland on challenges in the mining sector, President John Mahama explained that Ghana is having

•http://business.peacefmonline.com/pages/news/201401/186799.php

“issues with the big mining companies issues with the big mining companies that have stability agreements that that have stability agreements that locked in the level of royalties and taxes locked in the level of royalties and taxes for us. So when gold prices rose up to a for us. So when gold prices rose up to a record high we could not earn morerecord high we could not earn more.”

RATIONALE FOR THE RECENT REVIEW RATIONALE FOR THE RECENT REVIEW OF THE FISCAL REGIME 2OF THE FISCAL REGIME 2

• “During the recent … prices of gold, … reached their peak levels ever. Yet the country did not benefit at all from the price hikes, particularly from gold,”

• economic and social benefits provided by the mining sector did not match government’s expectations, hence its decision to review the industry’s taxes -

• the issue with mining was … fair and transparent sharing of benefits and windfall gains from the exploitation of the country’s precious and irreplaceable natural resources.

Thus, government is taking a bold step to critically review the fiscal regimes and mining agreements, with the view of ensuring that the country benefited adequately and fairly from the gains in the mining sector.

- Dr Edward Larbi-Siaw, Tax Policy Advisor of the Ministry of Finance; (May 2013)

RECENT TRENDS IN GHANA’S FISCAL REGIMERECENT TRENDS IN GHANA’S FISCAL REGIMEITEMITEM SMCD 5, SMCD 5,

19751975PNDCL 153, PNDCL 153, 19861986

AMENDMENTS AMENDMENTS TO TO PNDCL 153PNDCL 153

ACT 703, ACT 703, 20062006

AMENDMENTS AMENDMENTS TO ACT 703TO ACT 703

Pre-prdn Cost Pre-prdn Cost Capitalization Capitalization & Capital & Capital AllowancesAllowances

20% 20% initial; initial; then then 15% 15% DBDB

75% initial; 75% initial; then 50% then 50% DBDB

75% initial; 75% initial; then 50% then 50% DBDB

20% SL20% SL

Investment Investment AllowanceAllowance

5%5% 5%5% 5%5%

Loss CFLoss CF Up to 5 YrsUp to 5 Yrs Up to 5 YrsUp to 5 Yrs

Forex Forex RetentionRetention

[25-80%] [25-80%] Offshore Offshore

[25-80% -[25-80% -20% 20% Onshore] Onshore]

Import DutiesImport Duties Exempt (*)Exempt (*) Exempt (*)Exempt (*)

RoyaltyRoyalty 6%6% 6-12%6-12% 3-6%3-6% 5% 5% {Act 794}{Act 794}

Corp Inc TaxCorp Inc Tax 50-55%50-55% 45%45% 35%35% 25%25% 35% [35% [mining]mining]

APT /WFPTAPT /WFPT 25% 25% on 35% IRRon 35% IRR {10% {10% proposedproposed))

* plant, machinery and equipment imported exclusively and specifically for Mining* plant, machinery and equipment imported exclusively and specifically for Mining

RECENT TRENDS IN GHANA’S FISCAL REGIMERECENT TRENDS IN GHANA’S FISCAL REGIMEITEM SMCD 5,

1975PNDCL 153, 1986 AMENDMENTS

TO PNDCL 153ACT 703, 2006

AMENDMENTS TO ACT 703

Withholding Tax

10% 10% 15%

Capital Gains Tax

10% 10% 15%

National Reconstruction Levy

2% of pretax profits(2001)

Equity Participation

10% free carried Interest ; + option of 20% shares at mkt price

10% free carried interest

Stabilization Deed of Warranty on Ltd Fiscal Terms

broad Stability & Devt Agree-ments

Revised Fiscal ProvisionsRevised Fiscal Provisions• During 2010 - 2012:

– royalty rate increased from a sliding 3-6 per cent to a fixed 5 per cent rate;

– corporate tax rate was increased from 25 to 35 per cent;

– Capital gains & Withholding taxes: 15%, up from 10%;

– 80%, then 50% Declining Balance Capital Allowance; replaced by uniform 20% for 5 years regime; and

– windfall profit tax at a rate of 10 percent for all mining companies was proposed, but shelved

Other Developments• Improving “Arms-length” Dealings Framework – Transfer Pricing

Regulations; L.I. 2188, 2012• Renegotiation of “Stability” Agreements, for simplification,

clarity, and equity;• Amendment of Minerals and Mining Act, Act 703 of 2006, under

way (& further Amendments being considered);• Formalization of Community Interests – MDF legislation almost

ready for Parliament;• Improved Stakeholder Engagement, for transparency and good

governance, e.g. EITI ;• Active Involvement in REC (ECOWAS) policy & legislation

harmonization drives; also Continental (AU/UNECA) Initiatives;• Ghana’s Application to AMDC to support its adoption of CMV

process.

SOME GUIDANCE QUESTIONS

&

ANSWERSANSWERS

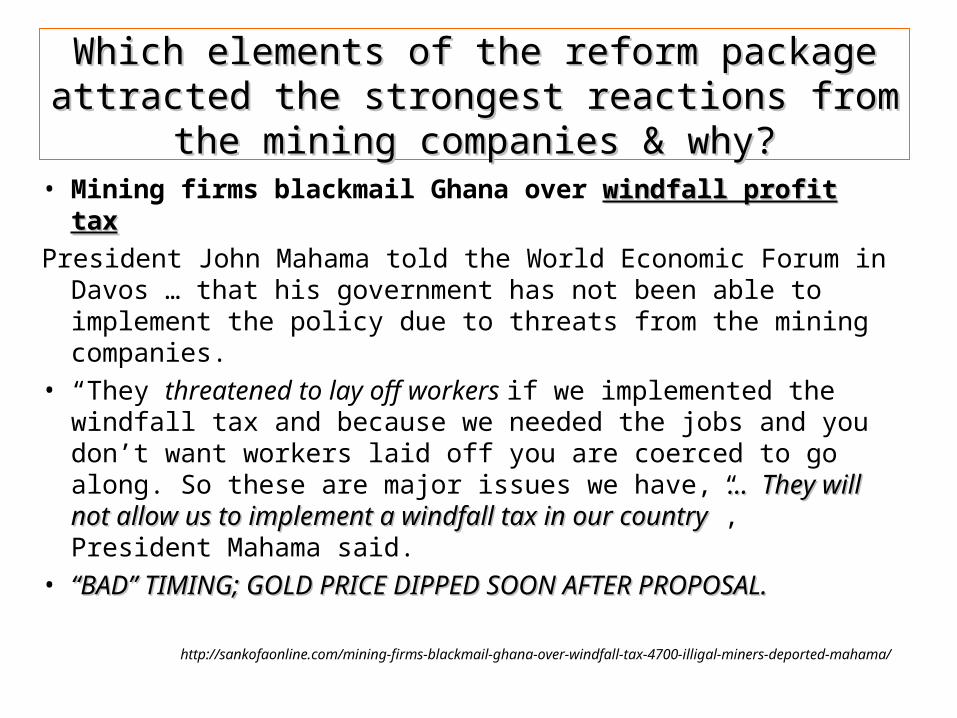

Which elements of the reform package attracted the Which elements of the reform package attracted the strongest reactions from the mining companies & why?strongest reactions from the mining companies & why?

• Mining firms blackmail Ghana over windfall profit taxwindfall profit taxPresident John Mahama told the World Economic Forum in Davos

… that his government has not been able to implement the policy due to threats from the mining companies.

• “They threatened to lay off workers if we implemented the windfall tax and because we needed the jobs and you don’t want workers laid off you are coerced to go along. So these are major issues we have, … They will not allow us to implement a … They will not allow us to implement a windfall tax in our countrywindfall tax in our country”, President Mahama said.

• ““BAD” TIMING; GOLD PRICE DIPPED SOON AFTER PROPOSAL.BAD” TIMING; GOLD PRICE DIPPED SOON AFTER PROPOSAL.

http://sankofaonline.com/mining-firms-blackmail-ghana-over-windfall-tax-4700-illigal-miners-deported-mahama/

Which elements of the fiscal reforms proved Which elements of the fiscal reforms proved most difficult to implement and why?most difficult to implement and why?

• Ring-fencing provision • Act 839 (2012) had a provision requiring mining

companies to match expenses from one Mining Area Mining Area to revenue from the same mining area; but Mining Area as defined by the Mineral and Mining Act, 2006 Act 703 was not for tax purposes & impeded implementation.

• INADEQUATE CONSULTATION AMONGST AGENCIESINADEQUATE CONSULTATION AMONGST AGENCIES

Would you regard the fiscal reform exercise as having Would you regard the fiscal reform exercise as having met its objectives? met its objectives?

YEAR MINERAL ROYALTY GHC

CORPORATE TAX GHC

20132013 364,673,038364,673,038 518,545,259518,545,259

20122012 359,392,853359,392,853 893,773,828893,773,828

20112011 222,027,706222,027,706 649,902,536649,902,536

20102010 144,697,345144,697,345 241,578,780241,578,780

Yes, as shown below, Royalty collections rose dramatically Yes, as shown below, Royalty collections rose dramatically between 2010 & 2012 due to the increase in rate, but between 2010 & 2012 due to the increase in rate, but impact was dampened in 2013 due to the fall in gold prices. impact was dampened in 2013 due to the fall in gold prices. Corporate taxes also improved due to the application of Corporate taxes also improved due to the application of new tax rates and capital allowance.new tax rates and capital allowance.

What are the main lessons that you draw from Ghana’s What are the main lessons that you draw from Ghana’s mining fiscal reforms? mining fiscal reforms?

To achieve and sustain the gains:• Need for adequate stakeholder consultations to have the Need for adequate stakeholder consultations to have the

desired impactdesired impact• Government should be more proactive and react quickly to Government should be more proactive and react quickly to

the changes in the mining industrythe changes in the mining industry, e.g. Government would have benefited more from gold price hikes if reforms were undertaken earlier, say btn 2008-09

• Fiscal reforms should also aim at maximising revenue without Fiscal reforms should also aim at maximising revenue without necessarily increasing taxes necessarily increasing taxes eg. By facilitating (i)Broadening tax base; (ii)Diversifying mineral resource base; (iii)Enhanced value addition, beneficiation and local content & linkages in general.

• Need to fashion suitable and sustainable tax system to meet Need to fashion suitable and sustainable tax system to meet the needs of small scale minersthe needs of small scale miners.

THANK YOUTHANK YOUFOR FOR

YOUR ATTENTIONYOUR ATTENTION

20