realignment 101. the road to realignment 1978 proposition 13 1% property tax rate (average was...

TRANSCRIPT

REALIGNMENT 101

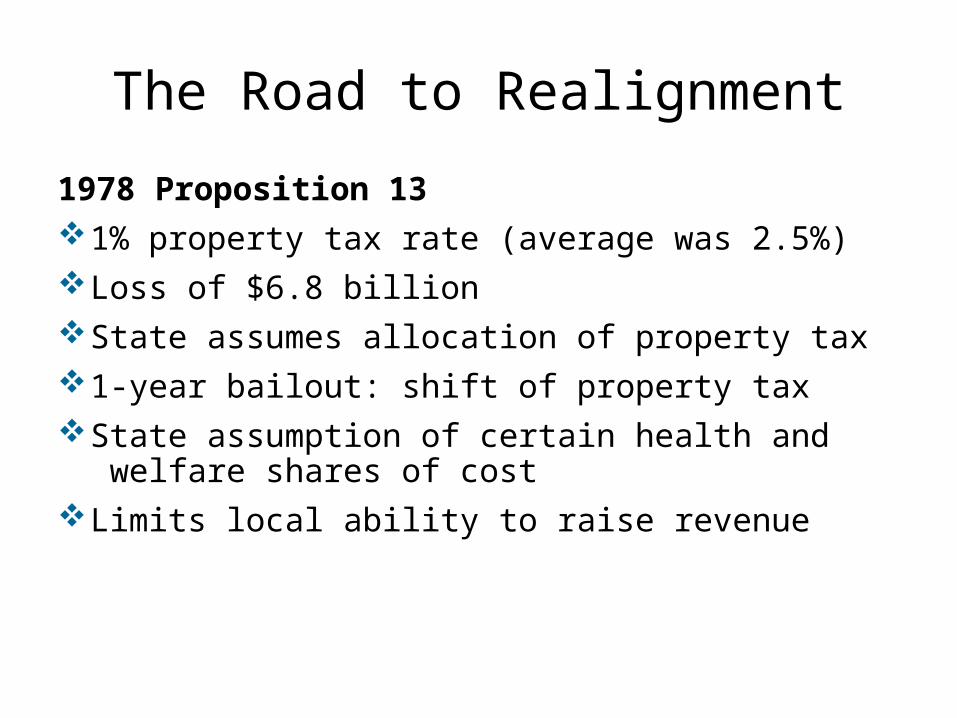

The Road to Realignment

1978 Proposition 131% property tax rate (average was 2.5%)Loss of $6.8 billionState assumes allocation of property tax 1-year bailout: shift of property taxState assumption of certain health and

welfare shares of costLimits local ability to raise revenue

1979 AB 8 Long Term Fiscal Relief

Same formula as the 1978 1-year bailout State created AB 8 health program – block grant State assumed county shares of Medi-Cal and

SSI/SSP Other shares of cost changed Included a Deflator – activated if state General

Fund revenues insufficient to maintain funding

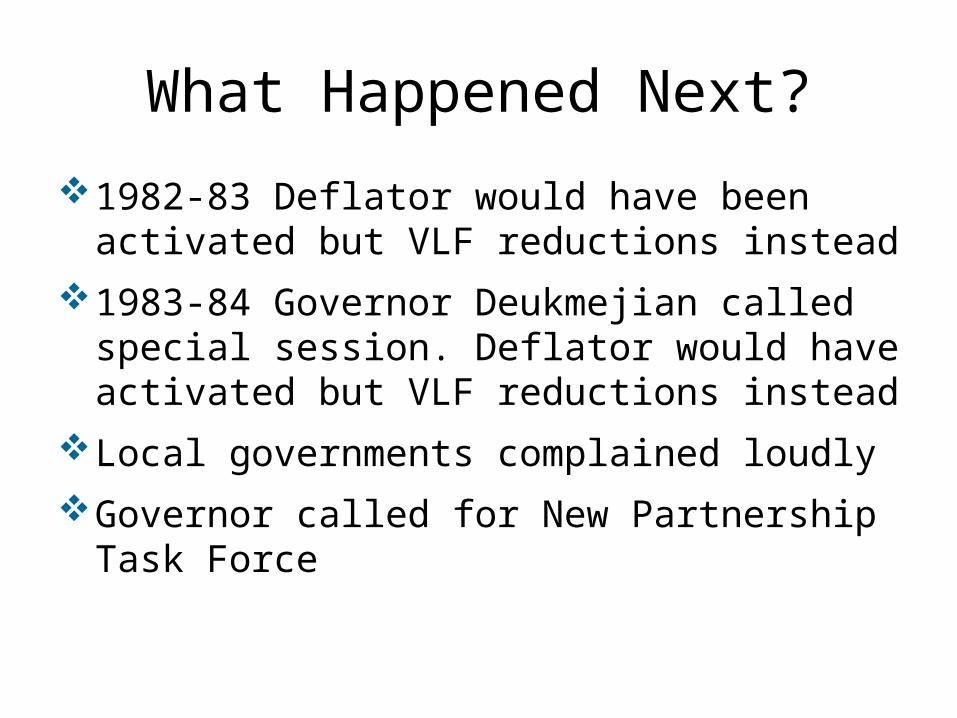

What Happened Next?

1982-83 Deflator would have been activated but VLF reductions instead

1983-84 Governor Deukmejian called special session. Deflator would have activated but VLF reductions instead

Local governments complained loudlyGovernor called for New Partnership Task

Force

Task Force Recommendations

Constitutional protection of VLFRepeal AB 8 DeflatorShift a portion of existing state sales tax to

locals to replace subventionsRealign programs shared by state and

counties Capitated health and welfare programs Shift a portion of state sales tax to fund Entitlement programs stay as they are

The 80’s. What ? No Realignment?

If at first you don’t succeed ……..

Realignment

Restructuring

Disengagement

Attempt to swap AFDC and Trial Courts but little interest and hard to accomplish

1991 – The Stars Are Aligned

1989 and 1990 significant budget reductions to county programs including AB 8 Health and Mental Health

Governor Wilson elected January $7 billion budget gap Discretionary programs: AB 8 Health, Indigent

Health and Mental Health proposed for elimination

Willing to tax? Could “realign” programs

1991 January Budget Proposal

Transfer responsibility for AB 8, Indigent Health, Community Mental Health and Local Health Services to counties ($942 million)

Increase the alcoholic beverage tax to national average; change the VLF depreciation schedule and allocate revenues to counties for programs ($942 million)

Provide local agencies authority to increase sales tax ½% for drug enforcement and crime prevention

Reactions

LAO Report: The County-State Partnership plus principles

Legislature: Realignment Task Force – 7 Members plus principles reporting to the Budget Conference Committee

CSAC: Work groups plus principles

How Did Realignment Change?

Grew to $2.2 billionSwapped taxes to VLF depreciation

increase and ½ cent sales taxAdded changing shares of cost in

primarily social services programsGot much more complicatedChapters 87, 89 and 91, Statutes of 1991

Complications

Other calls on the money? How many accounts are needed?Shares of cost = mandate?VLF constitutionally protected – specify use?Potential loss of federal fundsAllocation and structure of the fundsFlexibilityPending lawsuits and legal challenges

What Was Realigned (in millions)

Community Mental Health $452

State Hospitals/County Clients 210

IMDs 88

AB 8 Health Care 503

Local Health Services 3

Indigent Health 435

Local Block Grants 52

Stabilization 15

Juvenile Justice Grants 37

TOTAL $1,795

State/County Shares of Cost ($s in m)

CCS 75/25 50/50 $30

Foster Care 95/5 40/60 363

CWS 76/24 70/30 42

IHSS 97/3 65/35 235

CSBG 84/16 70/30 13

Adoptions 100/0 75/25 12

GAIN 100/0 70/30 26

AFDC 89/11 95/5 -155

County Adm 50/50 70/30 -95

$549

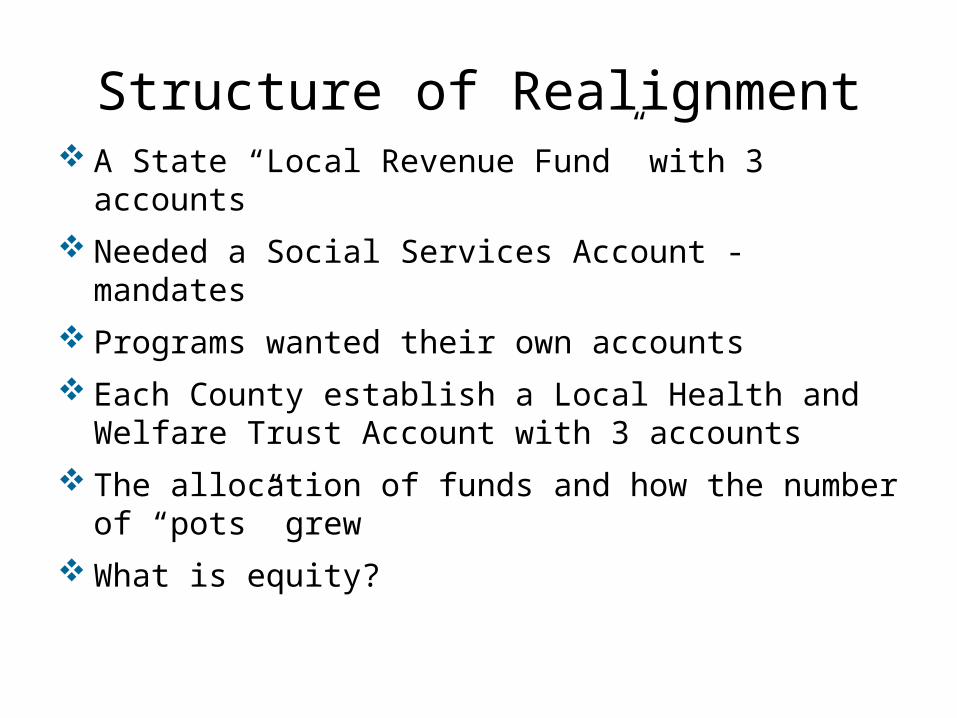

Structure of Realignment A State “Local Revenue Fund” with 3 accounts Needed a Social Services Account - mandates Programs wanted their own accounts Each County establish a Local Health and Welfare

Trust Account with 3 accounts The allocation of funds and how the number of

“pots” grew What is equity?

Lawsuits/Challenges/Poison Pills

Medically Indigent Adult transfer of 1982 – if mandate, Poison Pill to repeal VLF increase

Proposition 98 – share in the sales tax? Poison Pill to repeal new ½ cent sales tax

If any provision determined to be a reimbursable state mandate, Poison Pill to render Realignment inoperative

Other Issues

First year estimates short – had to redefine the base

MOEsWhat happens when a formula changes – IHSS to

PCSP with federal fundsMIA mandate case decisionPolicy changes imposed by the StateDoes Realignment affect Net County Costs Transfers between accounts

Issues For Consideration

Lessons Learned What program level being realigned What authority over the program What might the State require in the future Are there new “equity” issues Data and reviews

What Does the Future Hold

Governor’s May Revision Proposal – move money from “discretionary” mental health to shares of cost in Social Services Account

Federal Health Care Reform The Unknown