real estate investment risk management

TRANSCRIPT

Suite 5B Rivaan Center | P.O. Box 2384 – 00606 | Nairobi , Kenya | +254- 708 909 879 | www.iJenga.com

Real Estate Investment Risk ManagementUnderstanding Risk Management Strategies in Real Estate Investing with the

Goal to Mobilizing Local Institutional Capital in Real Estate & the Affordable

Housing Sector

Conference Presentation

October 29, 2020

Agenda

Copyright of iJenga Venture Limited2

1. Real Estate Investment Decisions

2. Risks in Real Estate Investing

3. Risk Management

Definitions

3

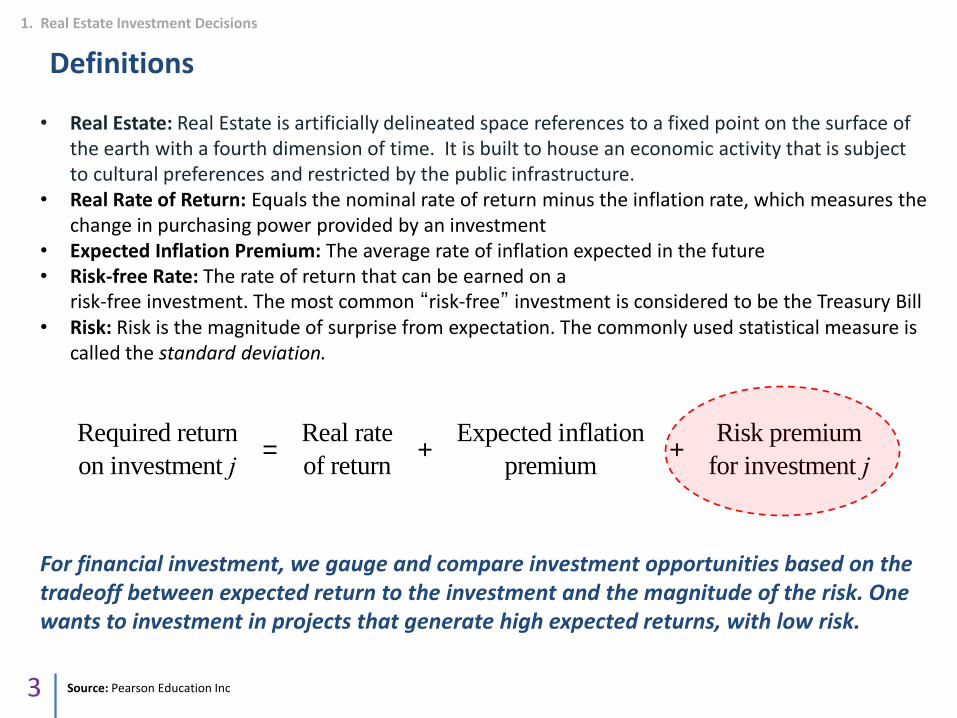

• Real Estate: Real Estate is artificially delineated space references to a fixed point on the surface of the earth with a fourth dimension of time. It is built to house an economic activity that is subject to cultural preferences and restricted by the public infrastructure.

• Real Rate of Return: Equals the nominal rate of return minus the inflation rate, which measures the change in purchasing power provided by an investment

• Expected Inflation Premium: The average rate of inflation expected in the future• Risk-free Rate: The rate of return that can be earned on a

risk-free investment. The most common “risk-free” investment is considered to be the Treasury Bill• Risk: Risk is the magnitude of surprise from expectation. The commonly used statistical measure is

called the standard deviation.

Required return

on investment j=

Real rate

of return+

Expected inflation

premium+

Risk premium

for investment j

Source: Pearson Education Inc

1. Real Estate Investment Decisions

For financial investment, we gauge and compare investment opportunities based on the tradeoff between expected return to the investment and the magnitude of the risk. One wants to investment in projects that generate high expected returns, with low risk.

Discussion on asset class allocation

4

1. Real Estate Investment Decisions

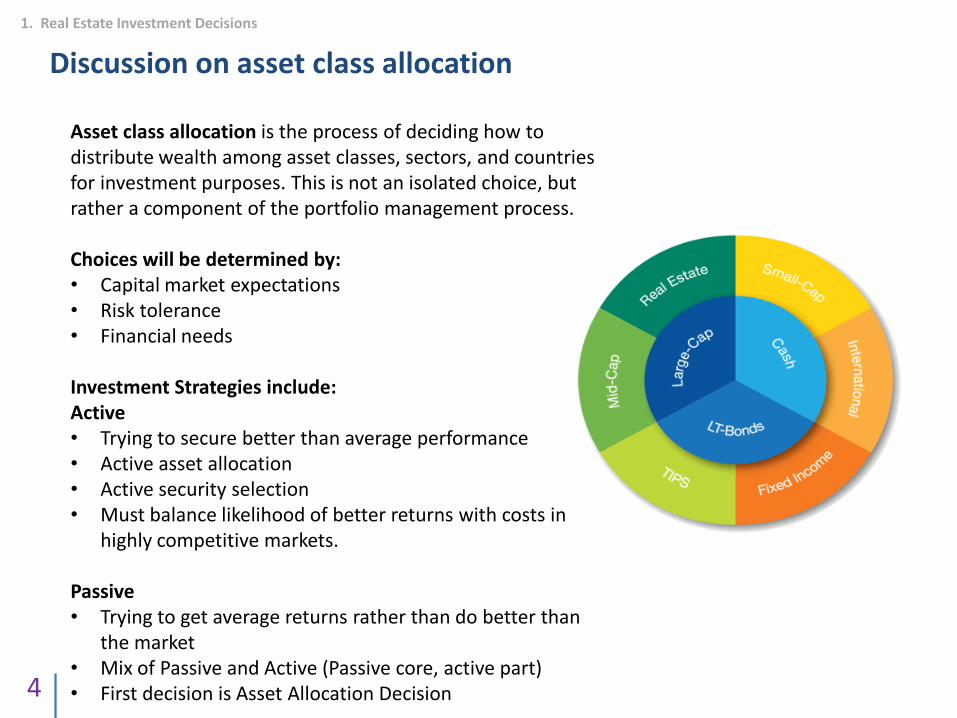

Asset class allocation is the process of deciding how to distribute wealth among asset classes, sectors, and countries for investment purposes. This is not an isolated choice, but rather a component of the portfolio management process.

Choices will be determined by:• Capital market expectations• Risk tolerance• Financial needs

Investment Strategies include:Active• Trying to secure better than average performance• Active asset allocation• Active security selection• Must balance likelihood of better returns with costs in

highly competitive markets.

Passive• Trying to get average returns rather than do better than

the market• Mix of Passive and Active (Passive core, active part)• First decision is Asset Allocation Decision

Discussion on asset class allocation continued

5

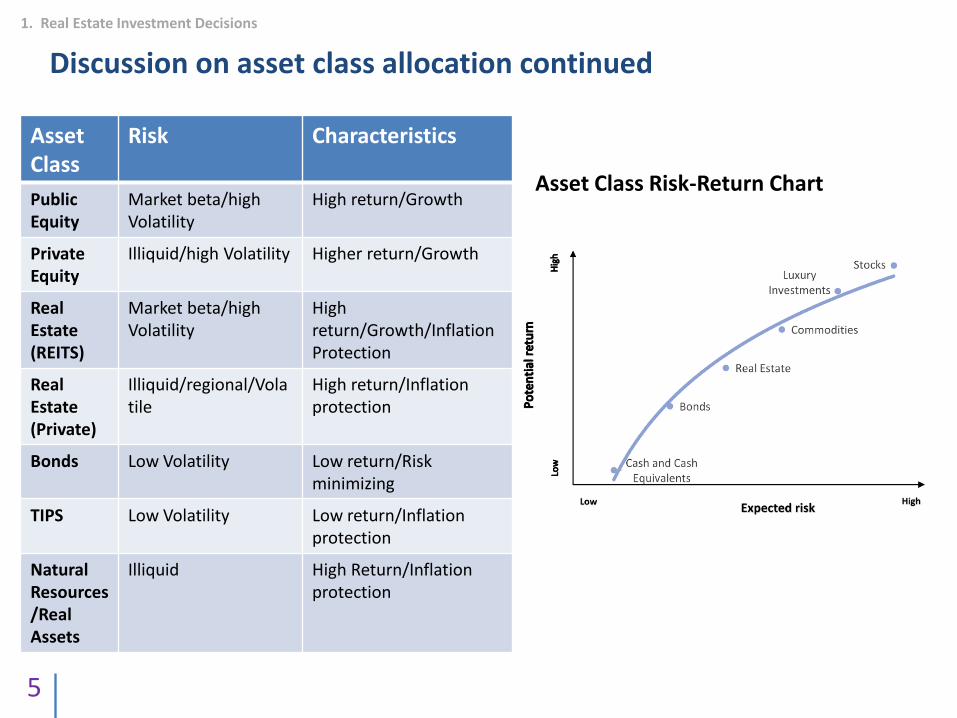

Asset Class

Risk Characteristics

Public Equity

Market beta/high Volatility

High return/Growth

Private Equity

Illiquid/high Volatility Higher return/Growth

Real Estate (REITS)

Market beta/high Volatility

High return/Growth/Inflation Protection

Real Estate (Private)

Illiquid/regional/Volatile

High return/Inflation protection

Bonds Low Volatility Low return/Risk minimizing

TIPS Low Volatility Low return/Inflation protection

NaturalResources/Real Assets

Illiquid High Return/Inflationprotection

Asset Class Risk-Return Chart

1. Real Estate Investment Decisions

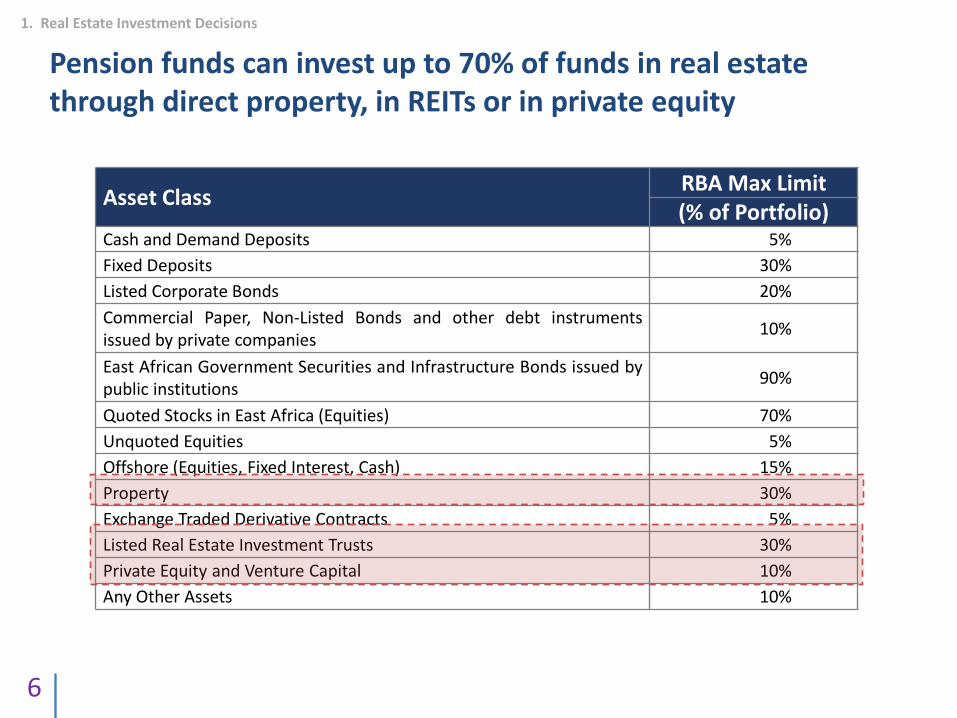

Pension funds can invest up to 70% of funds in real estate through direct property, in REITs or in private equity

6

Asset ClassRBA Max Limit(% of Portfolio)

Cash and Demand Deposits 5%

Fixed Deposits 30%

Listed Corporate Bonds 20%

Commercial Paper, Non-Listed Bonds and other debt instrumentsissued by private companies

10%

East African Government Securities and Infrastructure Bonds issued bypublic institutions

90%

Quoted Stocks in East Africa (Equities) 70%

Unquoted Equities 5%

Offshore (Equities, Fixed Interest, Cash) 15%

Property 30%

Exchange Traded Derivative Contracts 5%

Listed Real Estate Investment Trusts 30%

Private Equity and Venture Capital 10%

Any Other Assets 10%

1. Real Estate Investment Decisions

7

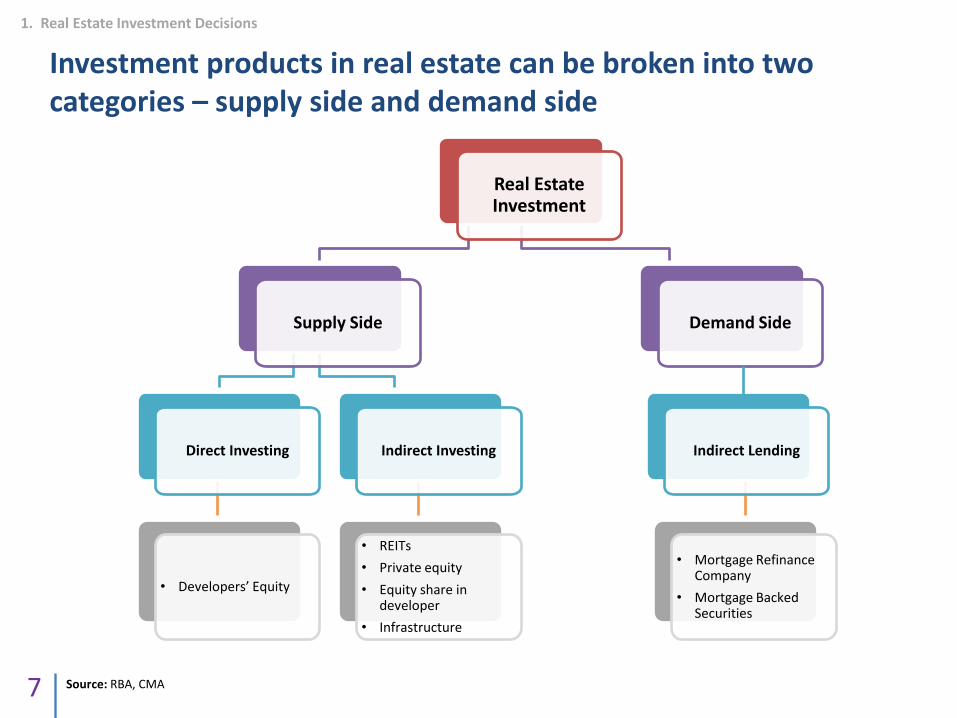

Investment products in real estate can be broken into two categories – supply side and demand side

Source: RBA, CMA

Real Estate Investment

Supply Side

Direct Investing

• Developers’ Equity

Indirect Investing

• REITs

• Private equity

• Equity share in developer

• Infrastructure

Demand Side

Indirect Lending

• Mortgage Refinance Company

• Mortgage Backed Securities

1. Real Estate Investment Decisions

8

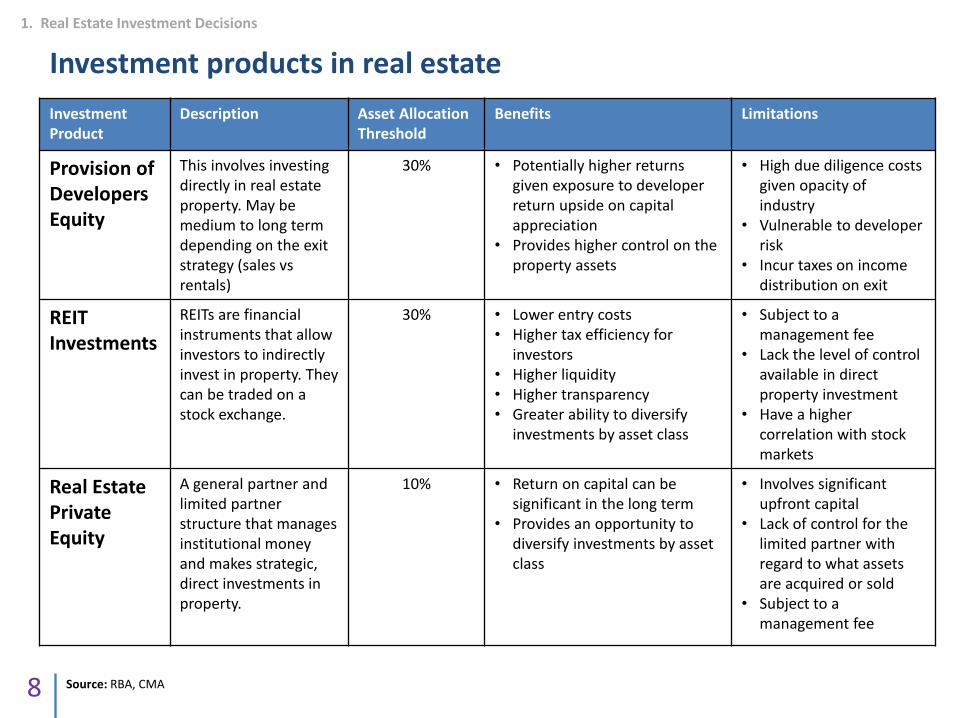

Investment products in real estate

Source: RBA, CMA

Investment Product

Description Asset Allocation Threshold

Benefits Limitations

Provision of Developers Equity

This involves investing directly in real estate property. May be medium to long term depending on the exit strategy (sales vs rentals)

30% • Potentially higher returns given exposure to developer return upside on capital appreciation

• Provides higher control on the property assets

• High due diligence costs given opacity of industry

• Vulnerable to developer risk

• Incur taxes on income distribution on exit

REIT Investments

REITs are financial instruments that allow investors to indirectly invest in property. They can be traded on a stock exchange.

30% • Lower entry costs• Higher tax efficiency for

investors• Higher liquidity• Higher transparency• Greater ability to diversify

investments by asset class

• Subject to a management fee

• Lack the level of control available in direct property investment

• Have a higher correlation with stockmarkets

Real Estate Private Equity

A general partner and limited partner structure that manages institutional money and makes strategic, direct investments in property.

10% • Return on capital can be significant in the long term

• Provides an opportunity to diversify investments by asset class

• Involves significant upfront capital

• Lack of control for the limited partner with regard to what assets are acquired or sold

• Subject to a management fee

1. Real Estate Investment Decisions

9

Investment products in real estate continued

Investment Product

Description Asset Allocation Threshold

Benefits Limitations

EquityInvestment in Developer

This refers to an equity investment in a real estate developer. (either public or private)

10 – 70% depending on

whether the firm is locally listed

• Provides exposure to a resilient industry while maintaining the benefits of a stock including liquidity and transparency where the stock is publicly traded

• Exposed to market risk on share prices

• Investors have no exposure to real assets and can’t take advantage of capital gains

InfrastructureDebt

Refers to investment in physical structures that are essential for operation of society

10 – 90% depending on the issuer (public vs

private)

• Provides diversification benefits from other assets

• Provides steady cashflows • Useful as an inflation hedge• Useful in showing commitment

to ESG principles• Potential tax benefits if issued

by government

• Limited returns compared to other alternative investments

MortgageBacked Securities (KMRC)

Pension funds could invest indirectly in real estate by buying assets backed by mortgage loans from banks. An example of this would be an investment in KMRC in a bid to provide long term capital

10% • Security has similar qualities to fixed income investments thus provides a guaranteed rate of return which is still higher than traditional corporate or government bonds

• The investment has lower prepayment risk compared to direct mortgages

• Investment is subject to credit risk

• Returns may be limited compared to other forms of real estate investment

Source: RBA, CMA

1. Real Estate Investment Decisions

10

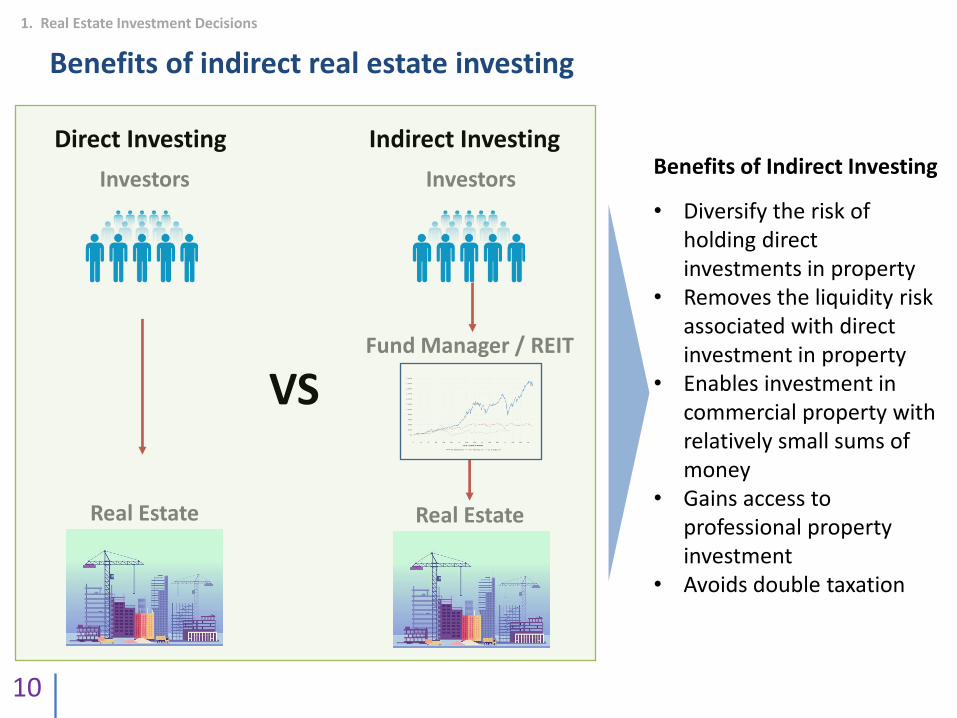

Benefits of indirect real estate investing

1. Real Estate Investment Decisions

Direct Investing

Real Estate

VS

Investors

Real Estate

Indirect Investing

Investors

Fund Manager / REIT

Benefits of Indirect Investing

• Diversify the risk of holding direct investments in property

• Removes the liquidity risk associated with direct investment in property

• Enables investment in commercial property with relatively small sums of money

• Gains access to professional property investment

• Avoids double taxation

11

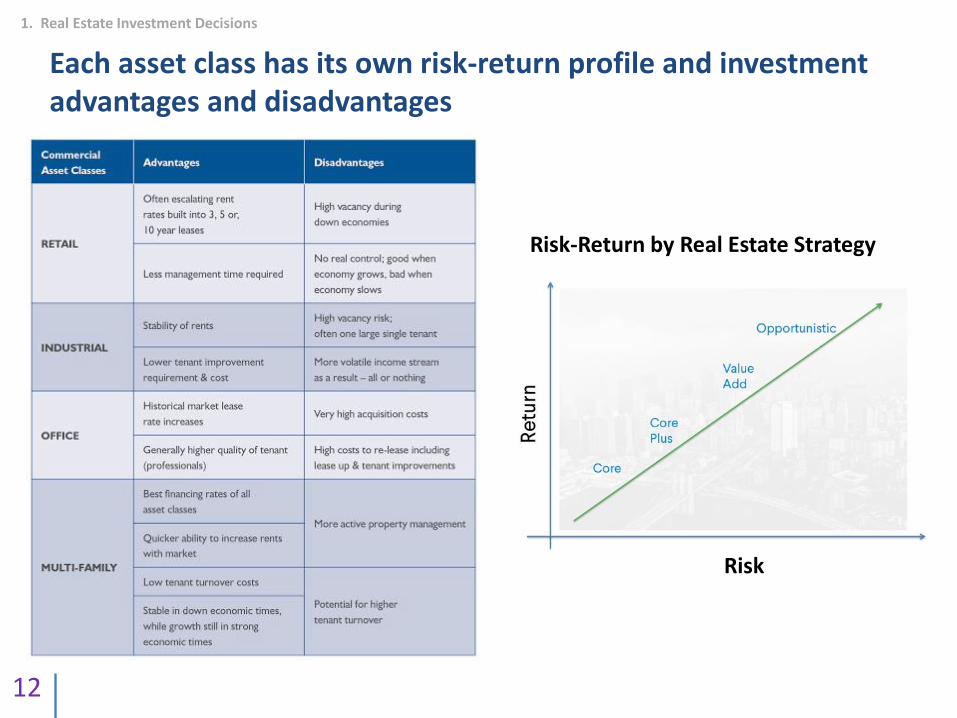

Real Estate has a number of property types or asset classes

1. Real Estate Investment Decisions

Various Property Types / Asset Classes

• Multifamily residential• Single Family Residential• Office• Industrial / Flex• Warehouse / Storage• Retail• Recreation• Land – potential uses• Education• Healthcare• Agricultural

12

Each asset class has its own risk-return profile and investment advantages and disadvantages

1. Real Estate Investment Decisions

Risk

Risk-Return by Real Estate Strategy

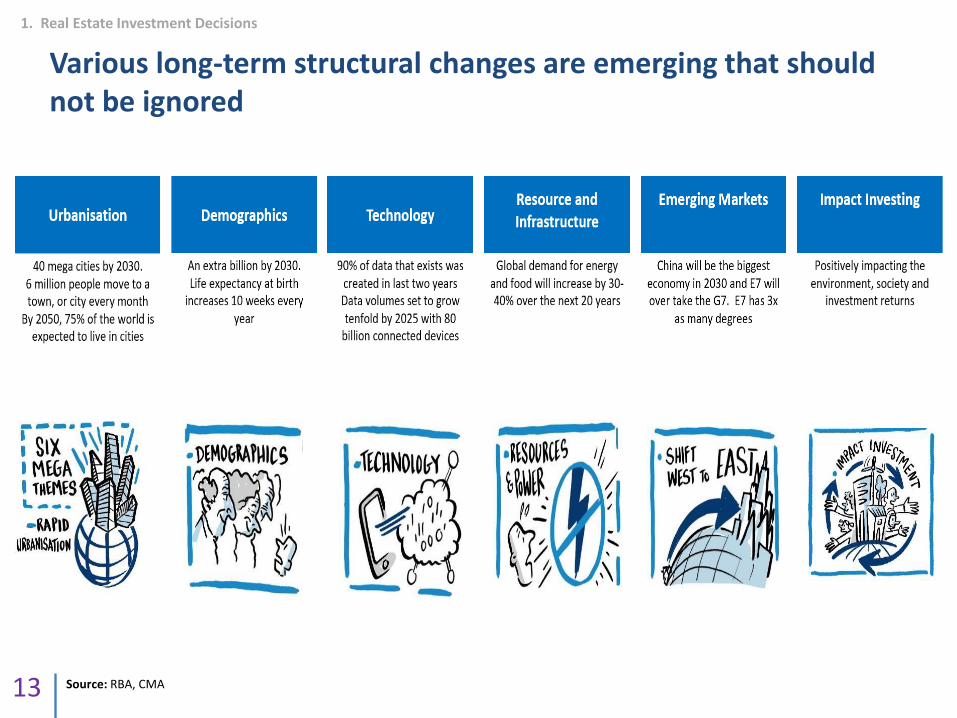

Various long-term structural changes are emerging that should not be ignored

13

1. Real Estate Investment Decisions

Source: RBA, CMA

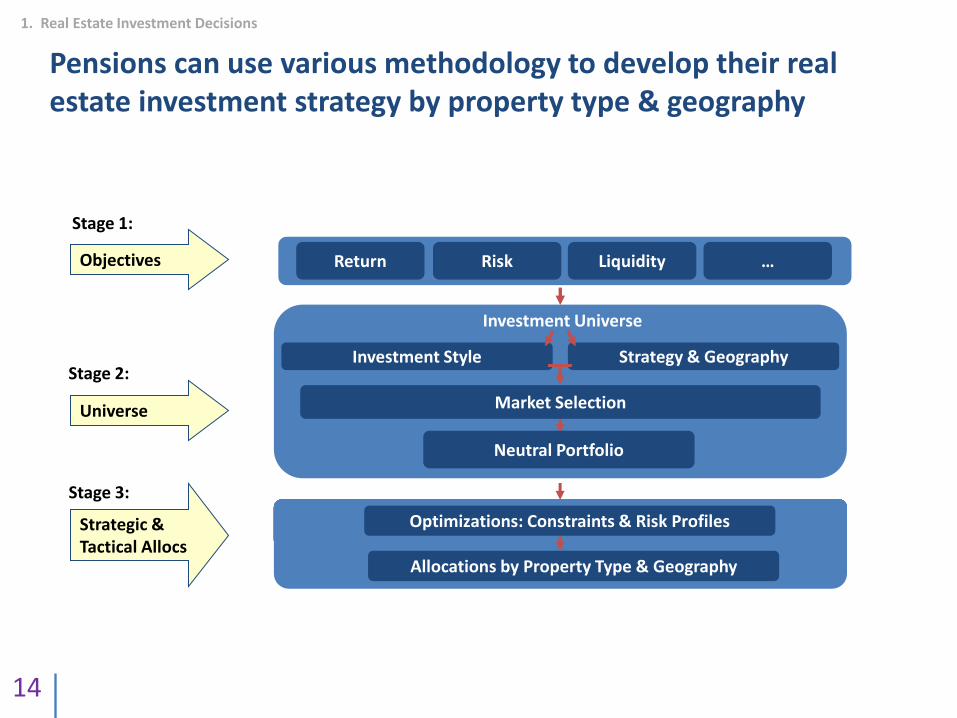

Pensions can use various methodology to develop their real estate investment strategy by property type & geography

14

1. Real Estate Investment Decisions

Stage 2:

Stage 3:

Stage 1:

Investment Style Strategy & Geography

Risk LiquidityReturn

Investment Universe

Objectives

Universe

Strategic & Tactical Allocs

Market Selection

Neutral Portfolio

Optimizations: Constraints & Risk Profiles

Allocations by Property Type & Geography

…

What distinguishes property from other asset classes?

15

Each individual property is unique – location, structure, size and design

It is subjective – individuals find different characteristics attractive and there is no central marketplace

Subject to complex legal considerations and transaction costs are high

Highly illiquid - it can take a considerable amount of time to buy or sell a property. The investor also has to sell the whole property or nothing at all.

Property can only be purchased in discrete and generally sizeable and relatively expensive units, making diversification difficult – only institutional investors can do this effectively

Supply of land is finite and its availability can be further restricted by legislation and local planning regulations. Price of property is heavily driven by changes in demand and not supply.

Nature

Value

Transfer & Settlements

Liquidity

Diversification

Effects on Price

1. Real Estate Investment Decisions

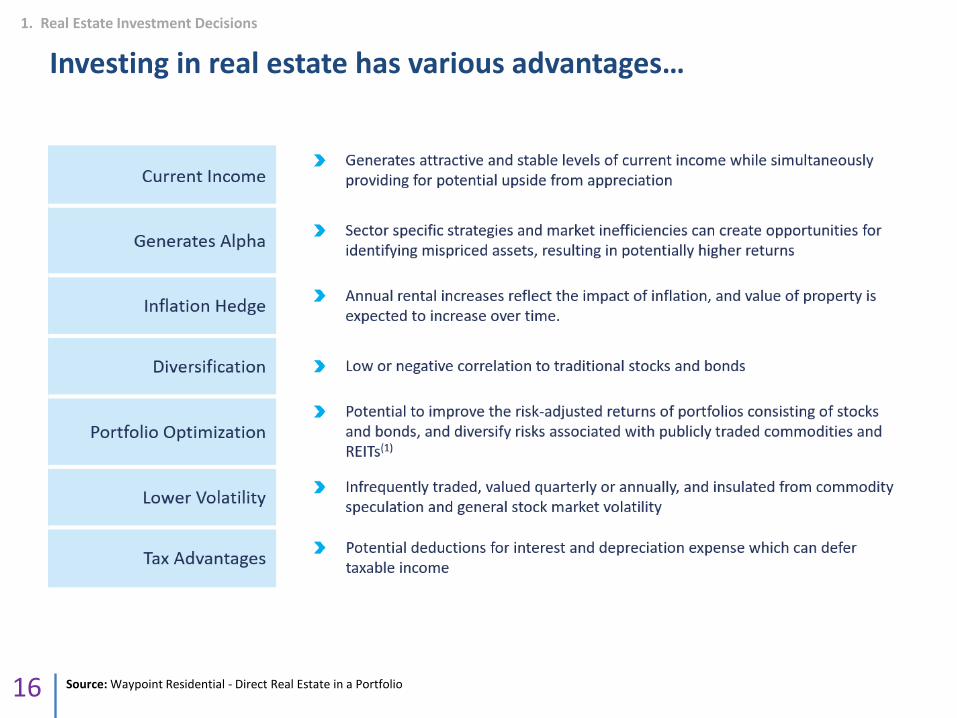

Investing in real estate has various advantages…

16

1. Real Estate Investment Decisions

Source: Waypoint Residential - Direct Real Estate in a Portfolio

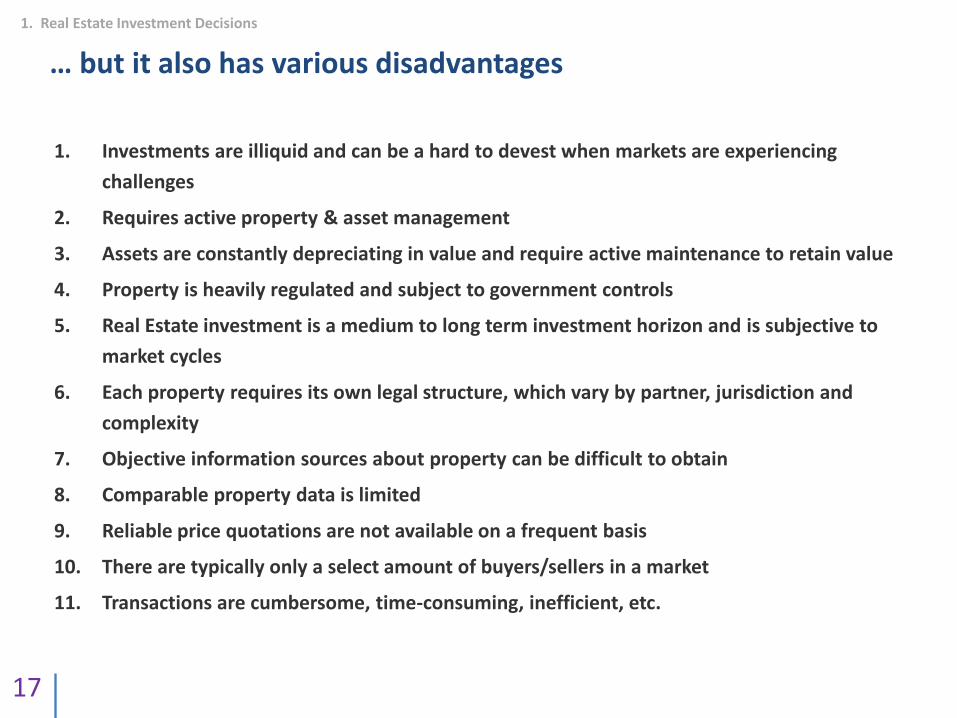

… but it also has various disadvantages

17

1. Real Estate Investment Decisions

1. Investments are illiquid and can be a hard to devest when markets are experiencing

challenges

2. Requires active property & asset management

3. Assets are constantly depreciating in value and require active maintenance to retain value

4. Property is heavily regulated and subject to government controls

5. Real Estate investment is a medium to long term investment horizon and is subjective to

market cycles

6. Each property requires its own legal structure, which vary by partner, jurisdiction and

complexity

7. Objective information sources about property can be difficult to obtain

8. Comparable property data is limited

9. Reliable price quotations are not available on a frequent basis

10. There are typically only a select amount of buyers/sellers in a market

11. Transactions are cumbersome, time-consuming, inefficient, etc.

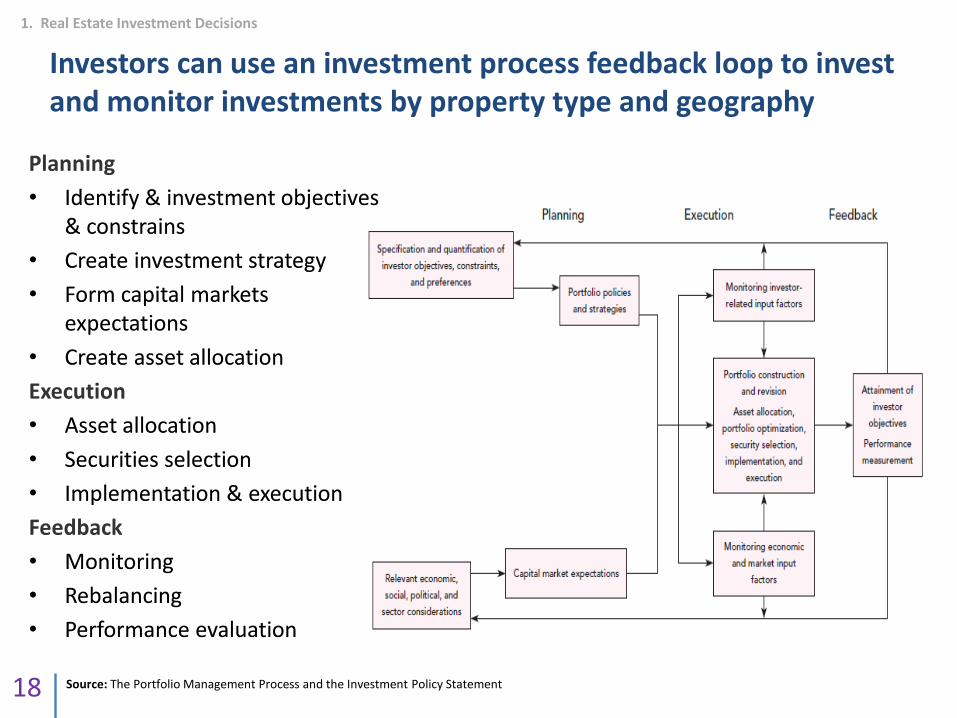

Investors can use an investment process feedback loop to invest and monitor investments by property type and geography

18

Planning

• Identify & investment objectives & constrains

• Create investment strategy

• Form capital markets expectations

• Create asset allocation

Execution

• Asset allocation

• Securities selection

• Implementation & execution

Feedback

• Monitoring

• Rebalancing

• Performance evaluation

Source: The Portfolio Management Process and the Investment Policy Statement

1. Real Estate Investment Decisions

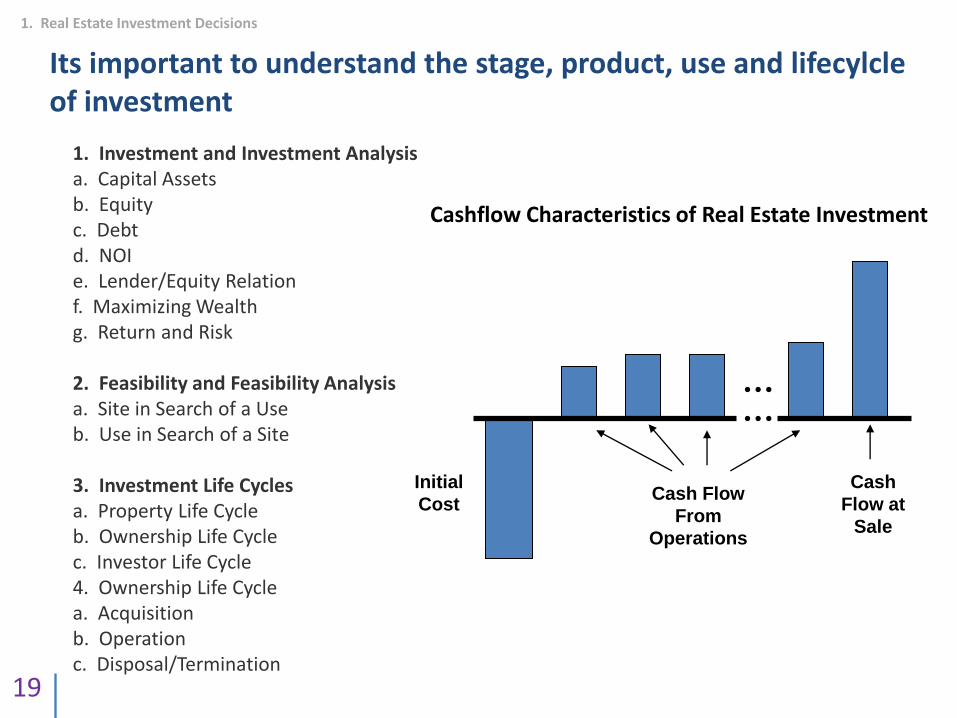

Its important to understand the stage, product, use and lifecylcleof investment

19

Cash

Flow at

Sale

Cash Flow

From

Operations

Initial

Cost

Cashflow Characteristics of Real Estate Investment

1. Investment and Investment Analysisa. Capital Assetsb. Equityc. Debtd. NOIe. Lender/Equity Relationf. Maximizing Wealthg. Return and Risk

2. Feasibility and Feasibility Analysisa. Site in Search of a Useb. Use in Search of a Site

3. Investment Life Cyclesa. Property Life Cycleb. Ownership Life Cyclec. Investor Life Cycle4. Ownership Life Cyclea. Acquisitionb. Operationc. Disposal/Termination

1. Real Estate Investment Decisions

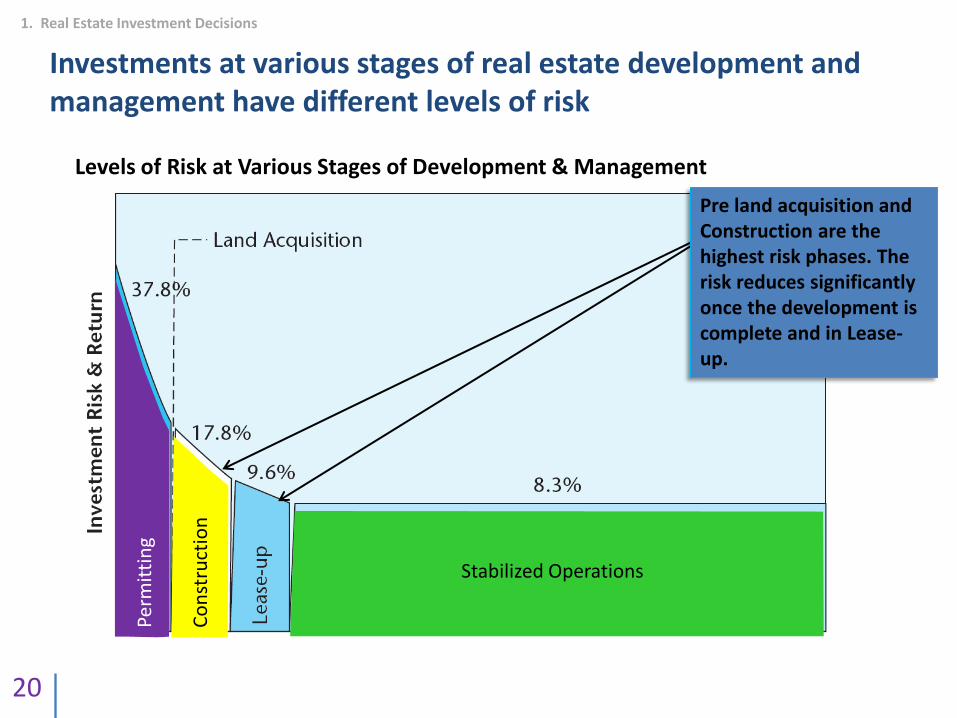

Investments at various stages of real estate development and management have different levels of risk

20

Perm

itti

ng

Co

nst

ruct

ion

Stabilized Operations

Pre land acquisition and Construction are the highest risk phases. The risk reduces significantly once the development is complete and in Lease-up.

1. Real Estate Investment Decisions

Levels of Risk at Various Stages of Development & Management

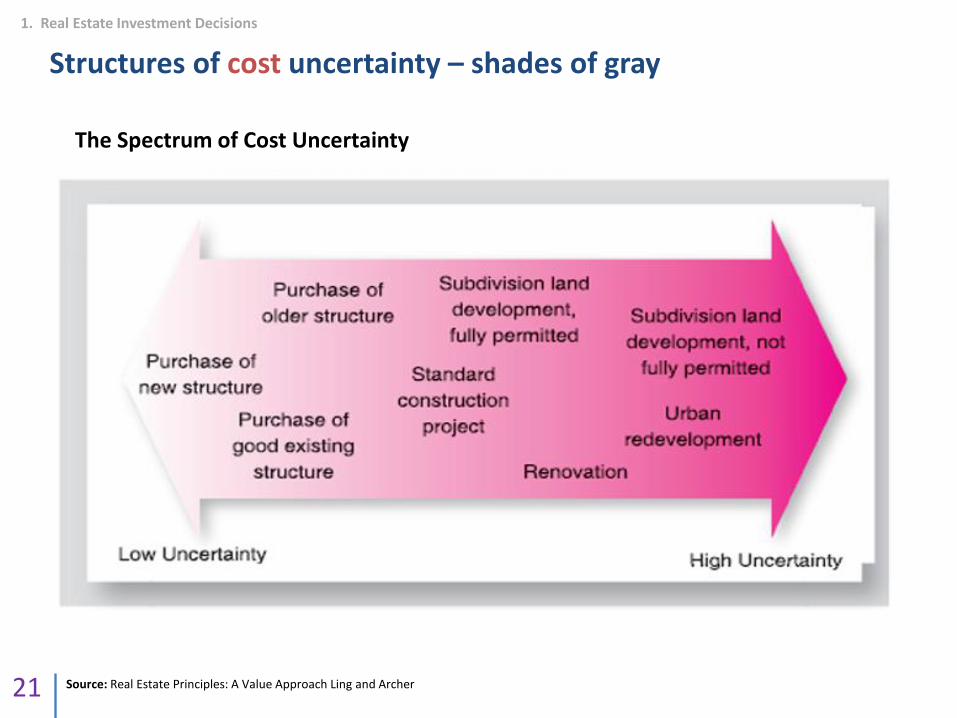

Structures of cost uncertainty – shades of gray

21

1. Real Estate Investment Decisions

The Spectrum of Cost Uncertainty

Source: Real Estate Principles: A Value Approach Ling and Archer

Structures of cash flow uncertainty – shades of gray

22

1. Real Estate Investment Decisions

The Spectrum of Cash Flow Uncertainty

Source: Real Estate Principles: A Value Approach Ling and Archer

Agenda

Copyright of iJenga Venture Limited23

1. Real Estate Investment Decisions

2. Risks in Real Estate Investing

3. Risk Management

Market Risks

24

2. Risks in Real Estate Investing

Background

All markets have ups and downs tied to the economy, interest rates, inflation or other market trends.

Investors can’t eliminate market shocks, but they can hedge their bets against booms and busts with a

diversified portfolio and strategy based on general market conditions.

The risk associated with real estate investments is primarily determined by the uncertainty of the value of the

property involved. Property and property-related assets are inherently difficult to appraise due to the

individual nature of each property and due to the fact that there is not necessarily a clear price mechanism.

As a result, valuations may be subject to substantial uncertainties. There is a risk that the estimates resulting

from the valuation process will not reflect the actual sales price. As such, a property market recession could

materially adversely affect the value of the property.

Mitigation Strategies

• Active research on economic cycles

• Strategic investment and disposition of assets

• Cash reserves for ‘rainy days’

• Sensitivity analysis on investment to model downside risk and returns

Asset-Level Risks

25

2. Risks in Real Estate Investing

Background

Asset-level or business risk involves changes in the occupancy rates, level of new construction, and zoning

and permit regulation, as well as additions to the competitive supply. Oher risks include labor problems and

moratoria on types of utilities like gas, sewers, water and electricity.

Differences among customers and building practices may result in losses due to construction delays, the

failure to obtain permits, and behavior of labor and supervisory personnel.

Some risks are shared by every investment in an asset class. In real estate investing, there’s always demand

for apartments in good and bad economies, so multifamily real estate is considered low-risk and therefore

often yields lower returns. Office buildings are less sensitive to consumer demand than shopping malls, while

hotels, with their short, seasonal stays and reliance on business and tourism travel, pose far more risk than

either apartments or office.

Mitigation Strategies

• Active portfolio management and economic / sector research

• Strategic investment and disposition of assets

• Experienced consultant and contractor teams and strong contracts

• Diverse portfolio of cyclical and recession resistant assets

Idiosyncratic Risk

26

2. Risks in Real Estate Investing

Background

Idiosyncratic risk is specific to a particular property. The more risk, the more return.

Construction, for example, will add risk to a project because it limits the capacity for collecting

rents during this time. And when developing a parcel from the ground up, investors take on

more types of risk than just the construction risk. There’s also entitlement risk – the chance that

government agencies with jurisdiction over a project won’t issue the required approvals to

allow the project to proceed; environmental risks that range from soil contamination to

pollution; budget overruns and more, such as political and workforce risks. Location is another

idiosyncratic risk factor.

Mitigation Strategies

• Robust feasibility study with in-depth understanding of neighborhood market

• Experienced consultant and contractor teams and strong contracts

• Diverse portfolio of cyclical and recession resistant assets

Liquidity Risk

27

2. Risks in Real Estate Investing

Background

Liquidity risk reflect the amount of time required to liquidate an investment. Real estate has a

relatively high degree of liquidity risk given the size of investment and the number of investors,

depending on the local market conditions. Even normally liquid markets can become illiquid

when they experience extraordinary events, such as events like market crashes, pandemics, or

market cycles.

Mitigation Strategies

• Robust feasibility study with in-depth understanding of neighborhood market

• Strategic investment and disposition of assets

• Good quality brokers and consultants to help facilitate a professional disposition of asset

• Diverse portfolio of cyclical and recession resistant assets

Leverage Risk

28

2. Risks in Real Estate Investing

Background

The more debt on an investment, the more risky it is and the more investors should demand in return.

Leverage is a force multiplier: It can move a project along quickly and increase returns if things are going well,

but if a project’s loans are under stress – typically when its return on assets isn’t enough to cover interest

payments – investors tend to lose quickly and a lot. As a rule, leverage should not exceed 75%, including

mezzanine and preferred equity, because both of these types of debt sit ahead of common equity in payment

order. Returns should be generated primarily from the performance of the real estate – not through excessive

use of leverage – and it’s critical that investors understand this point.

Similarly, structural risk is to be noted. A senior secured loan gives a lender a structural advantage over

“mezzanine” or subordinated debt because senior debt is the first to be paid; it has top place in the event of

liquidation. Equity is the last payout in the capital structure, so equity holders face the highest risk. Structural

risk also exists in joint ventures. In these types of deals, the investor has to be aware of their rights relative to

their position in the LLC, which is either a majority or minority holding.

Mitigation Strategies

• Conservative leverage ratios and cost efficient capital structure

• Robust feasibility study with in-depth understanding of neighborhood market

• Robust sensitivity analysis to understand downside risk in poor market conditions

Credit Risk

29

2. Risks in Real Estate Investing

Background

The length and stability of the property’s income stream is what drives value. A property leased

to a Grade A company for 30 years will command a much higher price than a multi-tenant office

building with similar rents. However, keep in mind that even the most creditworthy tenants can

go bankrupt, as history has shown us time and time again. The more stability in a property’s

income stream, the more investors are willing to pay because it behaves more like a bond with

predictable income streams. However, the triple-net lease landlord is taking a risk that the

tenant will stay in business for the length of the lease, and that there will be a waiting buyer.

Mitigation Strategies

• Conservative leverage ratios and cost efficient capital structure

• Active tenant, property and asset management

• Robust feasibility study with in-depth understanding of neighborhood market

• Robust sensitivity analysis to understand downside risk in poor market conditions

Regulation Risk

30

2. Risks in Real Estate Investing

Background

Regulatory amendments may affect prospects for the future lease of the premises, or prospects for the future

sale of the property. New technical or other requirements (including health and environmental requirements)

pertaining to the property may also impose costs on the company or individual that cannot be recouped from

the tenants. Time to time, relevant tax rules, or the application of rules may change. Amendments to tax

rules may result in investors being faced with new and different investment conditions, including reduced

profitability of the project.

Also, delays in the planning approval process increase the above mentioned time risk. At a time like this when

government parastatals such as land registries remain closed due to the ongoing novel coronavirus pandemic,

projects are set to be delayed indefinitely prolonging set project timelines and ultimately leading to increased

development costs as debt costs continue to accumulate. Additionally, all development is subject to planning,

and while developers, in general, apply for permissions that are in line with official planning rules and

development plans, the multitude of affected stakeholder interests can lead to specific conditions that affect

the cost and feasibility of a project. The approval process should be project managed professionally to

minimize this risk.

Mitigation Strategies

• Experienced consultant and contractor teams and strong contracts

• Conservative workplan with contingency planning incorporated

• Robust sensitivity analysis to understand downside risk in poor market conditions

Time Risk

31

2. Risks in Real Estate Investing

Background

Exceeding the planned project timeline leads to two main risks: cost of capital such as interest

increases with delays reducing project returns, and market conditions may change over time for

the worse. This is especially relevant as usually, top of the market conditions trigger developers

to pursue marginal opportunities. As markets turn and consolidate, delays in the completion of

such projects aggravate losses. The time risk can be addressed by professional best practice

project management including, selection of experienced and qualified project management

teams, clear documentation, coordination, and communication between project parties, and

timely commencement of marketing. An overall understanding of market forces and dynamics is

also critical.

Mitigation Strategies

• Experienced consultant and contractor teams and strong contracts

• Conservative workplan with contingency planning incorporated

• Robust feasibility study with in-depth understanding of neighborhood market

• Robust sensitivity analysis to understand downside risk in poor market conditions

Agenda

Copyright of iJenga Venture Limited32

1. Real Estate Investment Decisions

2. Risks in Real Estate Investing

3. Risk Management

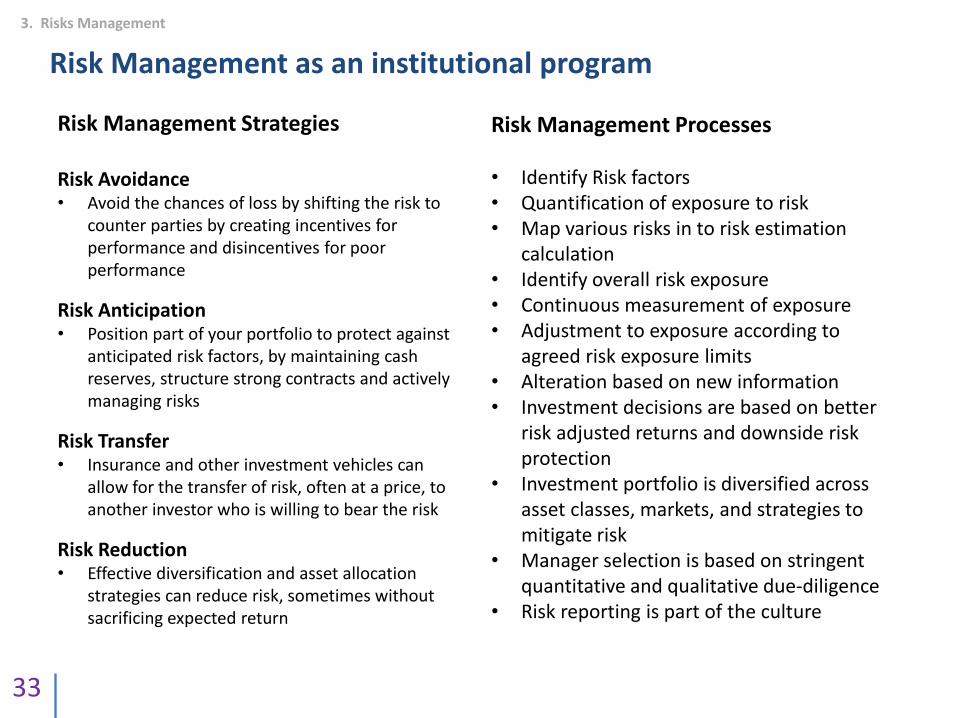

Risk Management as an institutional program

33

Risk Management Strategies

Risk Avoidance• Avoid the chances of loss by shifting the risk to

counter parties by creating incentives for performance and disincentives for poor performance

Risk Anticipation• Position part of your portfolio to protect against

anticipated risk factors, by maintaining cash reserves, structure strong contracts and actively managing risks

Risk Transfer• Insurance and other investment vehicles can

allow for the transfer of risk, often at a price, to another investor who is willing to bear the risk

Risk Reduction• Effective diversification and asset allocation

strategies can reduce risk, sometimes without sacrificing expected return

Risk Management Processes

• Identify Risk factors• Quantification of exposure to risk• Map various risks in to risk estimation

calculation• Identify overall risk exposure• Continuous measurement of exposure• Adjustment to exposure according to

agreed risk exposure limits• Alteration based on new information• Investment decisions are based on better

risk adjusted returns and downside risk protection

• Investment portfolio is diversified across asset classes, markets, and strategies to mitigate risk

• Manager selection is based on stringent quantitative and qualitative due-diligence

• Risk reporting is part of the culture

3. Risks Management

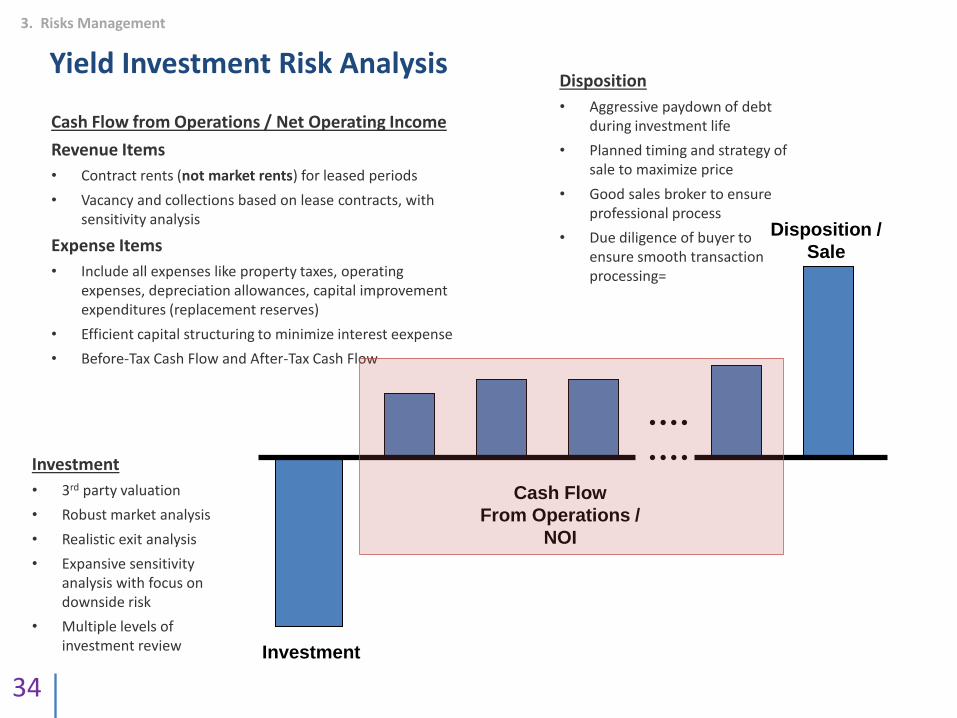

Yield Investment Risk Analysis

34

Disposition /

Sale

Cash Flow

From Operations /

NOI

Investment

Cash Flow from Operations / Net Operating Income

Revenue Items

• Contract rents (not market rents) for leased periods

• Vacancy and collections based on lease contracts, with sensitivity analysis

Expense Items

• Include all expenses like property taxes, operating expenses, depreciation allowances, capital improvement expenditures (replacement reserves)

• Efficient capital structuring to minimize interest eexpense

• Before-Tax Cash Flow and After-Tax Cash Flow

Investment

• 3rd party valuation

• Robust market analysis

• Realistic exit analysis

• Expansive sensitivity analysis with focus on downside risk

• Multiple levels of investment review

Disposition

• Aggressive paydown of debt during investment life

• Planned timing and strategy of sale to maximize price

• Good sales broker to ensure professional process

• Due diligence of buyer to ensure smooth transaction processing=

3. Risks Management

Development Risk Analysis

35

Project Feasibility

FinancingAsset

Management Design & Approvals

Construction & Delivery

Offtake Management

Using iJenga’s proprietary integrated development methodology we can highlight key areas of risk and various risk management strategies, like stage gates, quality team, cost effect finance, robust contracts, threshold offtake, and good construction and project management (CM & PM)

Stag

e G

ages

& R

isk

Mgt

A robust feasibility study should define in detail the strategy, including market, offtake, financials, team, timelines, implementation, and risk management.

An experienced team can save a development a lot of rework, time and energy

Front loading developers equity will ensure the developer is invested in the project

Good construction contract terms and strong CM & PM can manage site risk

Threshold presales / offtake before construction start can manage construction risk

Active dialog with govt can manage regulatory risk

Well structured finance and capital management can keep interest cost down

3. Risks Management