real activities manipulation and auditors' client-retention decisions

TRANSCRIPT

Online Early — Preprint of Accepted ManuscriptThis is a PDF file of a manuscript that has been accepted for publication in an American Accounting Association journal. It is the final version that was uploaded and approved by the author(s). While the paper has been through the usual rigorous peer review process for AAA journals, it has not been copyedited, nor have the graphics and tables been modified for final publication. Also note that the paper may refer to online Appendices and/or Supplements that are not yet available. The manuscript will undergo copyediting, typesetting and review of page proofs before it is published in its final form, therefore the published version will look different from this version and may also have some differences in content.

We have posted this preliminary version of the manuscript as a service to our members and subscribers in the interest of making the information available for distribution and citation as quickly as possible following acceptance.

The DOI for this manuscript and the correct format for citing the paper are given at the top of the online (html) abstract.

Once the final published version of this paper is posted online, it will replace this preliminary version at the specified DOI.

The Accounting Review • Issues in Accounting Education • Accounting HorizonsAccounting and the Public Interest • Auditing: A Journal of Practice & Theory

Behavioral Research in Accounting • Current Issues in Auditing Journal of Emerging Technologies in Accounting • Journal of Information Systems

Journal of International Accounting Research Journal of Management Accounting Research • The ATA Journal of Legal Tax Research

The Journal of the American Taxation Association

preprint

accepted manuscript

Real Activities Manipulation and Auditors’ Client Retention Decisions

Yongtae Kim Santa Clara University

Myung Seok Park

Virginia Commonwealth University

Abstract: In this study, we examine the effect of clients’ real activities manipulation (RAM) on auditors’ client retention decisions. We find that, with the exception of RAM through overproduction, clients’ opportunistic operating decisions are positively associated with the likelihood of auditor resignations. We also provide evidence that auditors are especially sensitive to clients’ RAM to just meet or beat earnings benchmarks in their client retention decisions. In addition, we find that clients whose auditors resign from engagements tend to hire smaller auditors and these clients engage in RAM more aggressively. Our additional analysis shows that, with the exception of RAM through overproduction, clients’ abnormal operating decisions are significantly associated with litigation risk against auditors. Overall, our evidence suggests that auditors shed clients with aggressive RAM to avoid excessive risk. Keywords: Real activities manipulation, Auditors’ client retention decision, Auditor resignation Data Availability: Data used in this study are available from public sources identified in the

study.

Editor’s note: Accepted by John Harry Evans III. Submitted July 2011 Accepted August 2013

We are grateful for the helpful comments and suggestions of John Harry Evans III (Senior Editor), two anonymous reviewers, Michael Calegari, Carolyn Norman, Benson Wier, and workshop participants at the 2009 AAA annual meeting, the 2009 AAA Western Region Meeting, the 2009 International Risk Management Conference, University of Memphis, Singapore Management University, and Sungkyunkwan University. We also gratefully acknowledge funding from PwC INQuires grant program.

preprint

accepted manuscript

1

I. INTRODUCTION

Despite regulators' considerable attention to auditor changes motivated by clients’ opportunism

in financial reporting (e.g., Securities and Exchange Commission 1988), there is little evidence on the

impact of opportunism in financial reporting on auditors’ client retention decisions. Prior studies

provide some insights into the relation between opportunistic financial reporting and auditor changes

(e.g., Krishnan and Krishnan 1997; DeFond and Subramanyam 1998; Shu 2000; Heninger 2001).

Heninger (2001) finds that abnormal accruals are positively related to the probability of litigation

against auditors. Krishnan and Krishnan (1997) and Shu (2000) document that auditor litigation risk is

associated with auditor resignations. Nevertheless, the association between managerial opportunism

and auditor resignation is unclear. DeFond and Subramanyam (1998) find income-decreasing abnormal

accruals prior to auditor changes, suggesting that auditors restrict accrual-based earnings management

and that clients attempt to replace incumbent auditors with more lenient ones. Although evidence in

DeFond and Subramanyam (1998) has implications for the relation between auditor conservatism and

the client’s choice of its auditor, it provides little insight into the relation between managerial

opportunism and the auditor’s client portfolio management. In addition, a decrease in abnormal

accruals prior to auditor changes suggests that abnormal accruals reported in financial statements do not

fully capture the degree of managerial opportunism in financial reporting because they reflect auditors’

preference for conservative accounting choices for clients with greater audit risk.1

In this study, we examine the relation between the auditor’s client retention decision and

real activities manipulation (RAM), our proxy for managerial opportunism. Extant literature

(Healy and Wahlen 1999; Roychowdhury 2006; Cohen et al. 2008; Cohen and Zarowin 2010; Zang

2012) suggests that managers exercise discretion not only via their choice of accounting estimates

and methods (i.e., accrual-based earnings management), but also through operational decisions. As 1 That is, we may not fully capture the extent of managerial opportunism that exists before auditors exert their will in the auditing process.

preprint

accepted manuscript

2

an alternative tool of earnings management, RAM occurs through changing operating activities and

decisions (e.g., opportunistically reducing discretionary expenses, overproducing, and offering price

discounts to boost current-period sales).2 Unlike abnormal accruals, which reflect the realized level

of earnings management after auditors conduct financial statement audits, RAM is subject to less

auditor scrutiny because it is done through real operating decisions rather than accounting method

choices. As such, RAM better reflects managers’ behavior and attitudes toward financial

reporting because it is not filtered through the audit process.

Although managers rather than auditors typically control RAM, this does not necessarily

mean that auditors are unconcerned about clients’ aggressive RAM. In fact, according to our

conversations with several current and former BIG 4 audit partners and directors, auditors are

concerned about clients’ abnormal and aggressive operating decisions to meet or beat their earnings

benchmarks.3 Specifically, they recognize the negative consequences of such business practices.

They are especially concerned about long-term implications of such aggressive operating decisions,

because abnormal business practices may increase business risk to the client as well as to the

auditor.4 Although there are multiple reasons to terminate an engagement relationship with a client,

audit partners and directors that we interview agree that a client’s aggressive operating decisions that

sacrifice long-term value are an important factor in their client retention decisions.

In this study, we argue that auditors are concerned about clients' abnormal operating practices

for the following reasons. First, RAM has a negative impact on cash flows and future performance 2 Roychowdhury (2006) defines RAM as management actions that deviate from normal business practices, undertaken with the primary objective of meeting or beating certain earnings thresholds. 3 AU section 329.23 (PCAOB 2002) requires auditors to engage in analytical review procedures to evaluate significant unexpected differences in financial statement items. Audit analytical review is the diagnostic process of identifying and determining the cause of unexpected fluctuations in account balances. Prior literature (e.g., Wright and Ashton 1989; Koonce 1992) shows that analytical review is beneficial for detecting unexpected fluctuations and is an important part of auditing. By comparing the actual results with those expected for balance sheet and income statement items, auditors should consider that unexplained differences may indicate an increased audit risk (AU section 329.21, PCAOB 2002) 4 In our discussions, one audit partner suggests that auditors view clients’ abnormal operations (i.e., inventory and accounts receivable build-up, cuts in R&D, etc.) as a sign of business risk to the client as well as to the auditor.

preprint

accepted manuscript

3

(e.g., Ewert and Wagenhofer 2005; Graham et al. 2005; Cohen et al. 2008; Mizik and Jacobson

2008; Leggett et al. 2009; Cohen and Zarowin 2010; Mizik 2010; Francis et al. 2011; Zang 2012).

For instance, Ewert and Wagenhofer (2005) show that RAM is costly and directly reduces firm value

(Proposition 4). Deterioration of the client’s performance and financial health limits an auditor’s

future business opportunities with the client. Second, clients’ poor financial performance often leads

to auditors being held liable for clients’ stakeholder losses, even if the auditors are not directly

responsible (O’Malley 1993; Arthur Andersen & Co. et al. 1992). For instance, O’Malley (1993)

asserts that when a client experiences financial losses, the auditors may be sued by anyone who

allegedly suffered a financial loss. He claims, “The auditors need not have done anything to cause the

loss. They need only be perceived to have done nothing to prevent or minimize it, or indeed to

predict it, and well in advance of the event” (O’Malley 1993, 83). Prior studies also provide evidence

that investors see auditors as providing insurance coverage in the case of securities litigation

(Willenborg 1999; Mansi et al. 2004) and as a potential source for recovery of losses (Menon

and Williams 1994; Baber, Kumar, and Verghese 1995). Third, RAM can contribute to an increase

in audit risk. Overproduction leads to inventory build-up, and excessive credit sales result in an

increase in receivables, both of which increase audit risk (e.g., Simunic 1980; Stice 1991). Inventory

build-up increases the probability of inventory write-downs, while higher receivables increase the

risk of bad debt.5 Finally, aggressive RAM reflects the management’s opportunism in financial

reporting (e.g., Roychowdhury 2006; Cohen et al. 2008; Cohen and Zarowin 2010; Zang 2012). The

discovery of opportunistic operating decisions that dissipate firm value casts doubt on the integrity of

management and its financial statements.

Facing resource constraints, auditors may shed clients with limited future opportunities and

greater risk. Since auditors cannot effectively control the clients’ RAM, they attempt to adjust their 5 Furthermore, a significant growth in accounts receivables and inventory as consequences of RAM could provide greater opportunities for accrual-based earnings management in subsequent periods (e.g., Cohen et al. 2008).

preprint

accepted manuscript

4

client portfolios by resigning from risky engagements (Bockus and Gigler 1998). Therefore, we

predict that auditors are more likely to resign when clients engage in RAM aggressively.

Following prior literature (Roychowdhury 2006; Cohen et al. 2008; Cohen and Zarowin

2010), we estimate and examine three types of activities manipulation: 1) sales manipulation, 2)

overproduction, and 3) reduction of discretionary expenses. To mitigate the concern that clients’

financial performance may explain the relation between RAM and auditor resignation, we make

several research design choices. First, we construct our RAM measures after adjusting for the

client’s financial performance (see Kothari et al. 2005). We also explicitly control for the client’s

financial performance by including return on assets and other proxies for financial performance,

such as financial distress, and expected future performance in the regressions. In addition, we

utilize a performance-matched control sample.

Consistent with our prediction, we find that clients’ opportunistic operating decisions,

proxied by abnormal cash flows and abnormal discretionary expenses, are positively associated

with the likelihood of auditor resignations. We find little evidence, however, that abnormal

production costs are significantly associated with the likelihood of auditor resignations. Our

results are robust to three sets of control samples: client-initiated auditor changes, all continuing

audit clients, and performance-matched continuing audit clients. We also find that clients whose

auditors resign tend to engage in RAM more aggressively to meet or beat earnings benchmarks

prior to auditor changes, and that auditors are especially sensitive to clients’ RAM to just meet or

beat earnings benchmarks in their client retention decisions, with the exception of RAM through

overproduction. Furthermore, additional analysis reveals that clients whose auditors resign from

engagements tend to employ non-Big 4 auditors as successor auditors and that these clients

engage in RAM more actively than other clients whose incoming auditors are Big 4. We further

find that the association between RAM and the likelihood of auditor resignation is especially

preprint

accepted manuscript

5

prevalent for small clients and during the post- Sarbanes-Oxley Act of 2002 (SOX) period. In

addition, we find that client’s abnormal cash flows and abnormal discretionary expenses are

significantly associated with litigations against auditors.

Our study adds to the literature on auditor switches by highlighting the effect of

clients’ RAM on auditors’ client-portfolio management. Graham et al. (2005) report that

almost 80% of executives are willing to take real economic actions to maintain accounting

appearances. They admit to sacrificing long-term value for the sake of reporting desired

accounting numbers. Although earnings management through accounting choices is receiving

considerably more attention in the literature, survey results show that executives are more

willing to take real actions than accounting actions to meet earnings benchmarks. Despite the

pervasiveness of RAM and considerable attention to auditor switches, especially in the post-

SOX era, there is little evidence for the implication of RAM for auditors’ client retention

decisions. To the best of our knowledge, our study is the first to show an association between

clients’ opportunistic operating decisions and auditor resignations. In addition, we provide

evidence of a direct association between the auditor’s client retention decisions and

managerial opportunism, which is difficult to fully capture with abnormal accruals.

The remainder of this paper proceeds as follows. In Section II, we discuss related literature

and research issues. We describe our research design in Section III. We present empirical results in

Section IV, which is followed by additional analyses in Section V. We conclude in Section VI.

II. RESEARCH ISSUE

Heninger (2001) and Palmrose and Scholz (2004) report that clients’ aggressive financial

reporting is positively associated with auditor litigation risk. Stice (1991), Krishnan and

Krishnan (1997), and Shu (2000) provide empirical evidence of a positive association between

preprint

accepted manuscript

6

auditor litigation risk and auditor resignations. Stice (1991) reports a positive association

between the likelihood of litigation and the probability that the auditor will resign rather than be

dismissed from the engagement. By examining the role of litigation risk against auditors in

differentiating auditor resignations from dismissals, Krishnan and Krishnan (1997) also provide

empirical evidence that auditors tend to resign from engagements that are associated with high

litigation risk. Similarly, Shu (2000) presents evidence that clients whose auditors resign from

engagements possess greater litigation risk. Nonetheless, there is little evidence on the impact of

managerial opportunism in financial reporting on the auditor’s client retention decision.

DeFond and Subramanyam (1998) find income-decreasing abnormal accruals prior to the

auditor change, especially for clients with high litigation risk. This evidence suggests that when the

auditor restricts accrual-based earnings management, the client may attempt to replace the auditor with

a potentially more lenient one. DeFond and Subramanyam (1998) provide evidence on the client’s

response to the auditor’s preference for conservative accounting choices. This evidence, however,

provides little insight into the impact of managerial opportunism on the auditor’s client retention

decision. We shed light on this issue by examining the association between auditor resignations and

RAM, our proxy for managerial opportunism.

Recent studies (e.g., Roychowdhury 2006; Cohen et al. 2008; Cohen and Zarowin 2010;

Zang 2012) document that managers exercise discretion not only via their choice of accounting

estimates and methods (i.e., accrual-based earnings management), but also through operational

decisions. These studies suggest that managers engage in aggressive financial-reporting practices

using RAM. For instances, Roychowdhury (2006) provides evidence that managers tend to

manipulate operating activities to avoid reporting losses and to meet annual analyst forecasts.

Cohen et al. (2008) report that the level of RAM increases significantly after the passage of SOX,

preprint

accepted manuscript

7

while the level of accrual-based earnings management declines, indicating that firms shift from

using accrual-based earnings management to RAM after SOX.6

Unlike accrual-based earnings management, auditors may not be directly responsible for

clients’ RAM because it is not done through accounting method choices and managers typically

control it. Nonetheless, there are several reasons why clients’ aggressive RAM can be of

particular concern to auditors. First, RAM has a negative impact on the client’s cash flows and

future financial performance, which limits the auditor’s future business opportunities with the

client. Focusing on RAM to just meet earnings benchmarks, Gunny (2010) finds a positive

association between RAM and subsequent performance. An overwhelming majority of studies,

however, document RAM's negative impact on future financial performance and firm value (e.g.,

Ewert and Wagenhofer 2005; Graham et al. 2005; Cohen et al. 2008; Mizik and Jacobson 2008;

Leggett et al. 2009; Cohen and Zarowin 2010; Mizik 2010; Francis et al. 2011; Zang 2012). In

their analytical study, Ewert and Wagenhofer (2005) show that firm value directly depends on

the level of expected RAM, because of the costs associated with RAM (Proposition 4, 1112).

Zang (2012) argues that the main costs of RAM are the economic consequences of deviating

from optimal business operations and therefore jeopardizing the firm’s competitive advantage.

Graham et al. (2005) find that managers would rather take economic actions that could have

negative long-term consequences than make within-GAAP accounting choices to manage

earnings. Mizik and Jacobson (2008) and Mizik (2010) find that the myopic RAM has a negative

impact on future stock returns and financial performance. In a similar vein, Cohen and Zarowin

(2010) provide evidence that, for equity offering firms, a decline in post-offer performance

6 Earlier studies provide evidence on the opportunistic reduction of expenses, such as R&D expenses, to either increase earnings or meet earnings benchmarks (Dechow and Sloan 1991; Baber et al. 1991; Bushee 1998; Bens et al. 2002). Thomas and Zhang (2002) present evidence on RAM through overproduction. They find that firms tend to produce more than the quantity required to meet sales and normal target inventory levels to decrease the reported cost of goods sold, thereby increasing reported earnings.

preprint

accepted manuscript

8

because of RAM is more severe than that resulting from accrual-based earnings management.

Other studies report the negative (positive) association between RAM and accounting

performance (stock price crash) in the subsequent period (Leggett et al. 2009; Francis et al.

2011). Facing resource constraints, auditors might be less willing to retain clients with potential

financial trouble that limits future possible business opportunities with the client.

Second, a client’s poor financial condition may also be costly for the auditor if the auditor

is held liable for the client’s stakeholder losses, even if the auditor is not directly responsible for

the losses (O’Malley 1993; Arthur Andersen & Co. et al. 1992).7 Stice (1991) contends that

clients’ poor financial conditions may provide plaintiffs with an incentive for recovering from

auditors, who are perceived to have “deep pockets.” Willenborg (1999) argues that larger,

prestigious auditors are perceived to provide an ex ante signal of increased insurance coverage in

the event of securities litigation. That is, investors view larger auditors as providing financial

statement users with a form of insurance. More recently, Mansi et al. (2004) find evidence that

investors value the insurance role of auditors in addition to their information role. Other studies

also suggest that investors rely on auditors as a potential source for recovery of losses (Menon

and Williams 1994; Baber, Kumar, and Verghese 1995).

Third, auditors of clients engaging in RAM could also be exposed to a greater audit risk going

forward. Overproduction to reduce the cost of goods sold in the current period leads to inventory

buildup. Excessive credit sales to boost current-period sales increase receivables in current and

subsequent periods. Prior studies (e.g., Simunic 1980; Stice 1991) report that both inventory build-up

and having more receivables increase audit risk because inventory build-up raises the probability of

7 To the extent that recent legislations (i.e., the Private Securities Litigation Reform Act of 1995 and the related Securities Litigation Uniform Standards Act of 1998) alter an audit firm’s liability from joint-and-several to proportional liability in an effort to reduce attempts to sue the “deep pockets” of the audit firm and its related insurance carriers, an auditor’s legal exposure to shareholder losses might have decreased in more recent years.

preprint

accepted manuscript

9

inventory write-downs and increases in receivables elevate the risk of bad debt. Cohen et al. (2008) find

that a significant growth in accounts receivables and inventory is associated with large magnitudes of

abnormal accruals.

Finally, RAM reflects the managements’ opportunistic attitude toward financial reporting

(e.g., Roychowdhury 2006; Cohen et al. 2008; Cohen and Zarowin 2010; Zang 2012). Managerial

opportunism in financial reporting is often considered as an outcome of poor managerial integrity

(AICPA 2007). The discovery of an irregularity, such as opportunistic operating decisions that

dissipate firm value, casts doubt on the integrity of management and its financial statements. A

lack of managerial integrity could lead to fraudulent reporting.8 Auditing standards require auditors

to explicitly consider management integrity in planning their audits and client retention decisions

(e.g., SAS No. 99, AU sec. 316.78, AICPA 2002 and PCAOB 2002). Johnstone and Bedard (2004)

find that auditors’ assessments of management integrity are highly significant in distinguishing

auditor resignations from continuing clients.

Research on the association between RAM and audit-related variables is limited. Cohen

and Zarowin (2010) find that clients audited by large audit firms and those with longer auditor

relationships are more likely to engage in RAM. A concurrent working paper by Sohn (2011) finds

a positive relation between audit fees and real earnings management. The enactment of SOX has

resulted in large increases in required audit work, SOX-induced resource constraints, and public

scrutiny. Facing resource constraints, auditors have incentives to shed from their portfolios riskier

clients and clients that offer limited future business opportunities. Bockus and Gigler (1998) show

that it may be more rational for an incumbent auditor to withdraw from a risky engagement than to

8 Kim et al. (2012) find that socially responsible firms engage in less RAM than firms that do not meet the same social criteria. In addition, they find that incidences of Accounting and Auditing Enforcement Releases (AAERs) against CEOs/CFOs are less frequent for socially responsible firms, indicating that traits of firm executives are important and closely related to opportunistic accounting decisions that may be subject to AAERs. Their findings suggest that RAM might be closely associated with managerial integrity.

preprint

accepted manuscript

10

demand higher fees for such an engagement. Therefore, to the extent that RAM is associated with

the client’s future financial trouble and opportunism in financial reporting, we predict that auditor

resignations are more likely when clients engage in RAM aggressively. Our empirical prediction

follows:

Empirical Prediction: Ceteris paribus, auditors are more likely to resign when clients aggressively engage in real activities manipulation prior to auditor switches.

III. RESEARCH DESIGN

Data and Sample Selection

We obtain a sample of auditor changes between January 2000 and December 2010 from the

Audit Analytics database. We exclude auditor changes associated with 2002 Andersen dismissals.

After merging with the COMPUSTAT and CRSP databases, we have an initial sample of 5,660

auditor changes. We obtain financial data from the COMPUSTAT database and stock price, trading

volume, and returns from the CRSP database. The sample is restricted to auditor changes of firms

that are in neither regulated industries nor financial institutions and have available data to calculate

RAM, abnormal accruals, and a proxy for auditor litigation risk, based on Shu’s (2000) model. After

applying these restrictions, we have 2,189 sample auditor changes, of which 589 are auditor

resignations and 1,600 are client-initiated dismissals. All continuous variables, including RAM

proxies, are winsorized at the top and bottom 1% of the distribution. Panel A of Table 1 reports the

sample distribution of auditor changes by two-digit Standard Industrial Classification (SIC) industry

code, and for comparison, that of all continuing audit clients.

[Insert Table 1 here.]

For the auditor resignation subsample, the most represented industry is Business Services,

which comprises 20.20 percent of the resignation sample. Electronic & Other Electric Equipment

preprint

accepted manuscript

11

comprises 15.62 percent, followed by Industrial Machinery & Computer Equipment at 9.68

percent. The same two industries make up the largest two shares of the auditor dismissal and

continuing client samples, whereas Instruments & Related Products is ranked fifth in auditor

resignations but third in the auditor dismissal and continuing client samples.

Panel B of Table 1 provides the sample distribution of auditor changes by year. The last

column shows that the relative proportion of auditor resignations as a percentage of all auditor

changes (resignation rate) generally increases over the sample period. Specifically, auditor

resignation rates average 21 percent over the 2000-2002 period versus 29 percent over the 2003-

2010 period. One possible reason for this increase is that Big 4 audit firms are shedding clients

who do not fit their risk profile; another reason may be that because they face compliance

challenges under SOX, Big 4 audit firms are reallocating resources and focusing on more

profitable clients.

Measurement of RAM

We follow prior studies (e.g., Roychowdhury 2006; Cohen et al. 2008; Cohen and

Zarowin 2010) in developing our proxies for RAM. Specifically, our three measures are (1)

abnormal levels of cash flow from operations (CFO), (2) abnormal production costs, and (3)

abnormal discretionary expenses. We measure the abnormal level of each activity as the residual

from the relevant estimation models by year and the two-digit SIC industry. Roychowdhury

(2006) defines sales manipulation as managers’ attempts to temporarily boost sales during the

year by offering price discounts or more lenient credit terms, which in turn lowers the cash

inflow. Hence, sales manipulation is expected to result in a lower current-period CFO. Following

prior studies (Roychowdhury 2006; Cohen et al. 2008; Cohen and Zarowin 2010), we estimate

the following model for firm i’s normal level of CFO:

CFOit /Ait-1 = α0 + α1(1/Ait-1) + β1(Sit /Ait-1) + β2( Δ Sit /Ait -1) + εit (1)

preprint

accepted manuscript

12

where CFOit is cash flow from operations in year t, Ait-1 is total assets at year t-1, Sit is net sales

in year t, and Δ Sit = Sit -Sit-1. For every firm-year, abnormal cash flow from operations is the

difference between the actual CFO and estimated “normal” CFO from equation (1).

The second measure of RAM is abnormal production costs. Managers of manufacturing

firms can manage earnings upward by producing more goods than necessary. With higher levels of

production, firms can spread fixed overhead costs over a larger number of units, thereby lowering

fixed costs per unit. Thus, overproduction results in a lower cost of goods sold (COGS) and better

operating margins. Prior studies (Roychowdhury 2006; Cohen et al. 2008; Cohen and Zarowin 2010)

define production costs as the sum of the COGS and the change in inventory during the year.

Following these studies, we estimate the following model for firm i’s normal COGS:

COGSit /Ait -1 = α0 + α1(1/Ait -1) + β(Sit /Ait -1) + εit (2)

where COGSit is the cost of goods sold in year t. Similarly, we estimate the model for firm i’s

normal inventory growth using the following equation:

Δ INVit /Ait -1 = α0 + α1 (1/Ait -1) + β1( Δ Sit /Ait -1) + β2( Δ Sit-1 /Ait -1) + εit (3)

where Δ INVit is the change in inventory in year t. Using equations (2) and (3), we estimate firm

i’s normal production costs from the following equation:

PRODit/Ait-1 = α0 + α1(1/Ait-1) + β1(Sit/Ait-1) + β2( Δ Sit/Ait-1) + β3( Δ Sit-1 /Ait-1) + εit (4)

The abnormal production cost is the difference between actual production costs and estimated “normal”

production costs. Unusually high production costs result in an increase in current period earnings.

The third measure of RAM is abnormal discretionary expenses. Prior studies

(Roychowdhury 2006; Cohen et al. 2008; Cohen and Zarowin 2010) express normal

discretionary expenses as a function of current sales. Following these studies, we estimate firm

i’s normal level of discretionary expenses using the following equation:

preprint

accepted manuscript

13

DISEXPit /Ait -1 = α0 + α1(1/Ait-1) + β (Sit -1 /Ait-1) + ε it (5)

where DISEXPit is discretionary expenses in year t, defined as the sum of research and development

(R&D), advertising, and selling, general, and administrative (SG&A) expenses. As Roychowdhury

(2006) and Cohen et al. (2008) note, modeling discretionary expenses as a function of current sales

creates a mechanical problem if firms manage sales upward to increase reported earnings in a certain

year, resulting in significantly lower residuals from a regression using current sales in that year. To

address this issue and estimate normal discretionary expenses, we express discretionary expenses as a

function of lagged sales. For every firm-year, the abnormal discretionary expenditure is the

difference between actual discretionary expenses and estimated “normal” discretionary expenses.

Unusually low discretionary expenses result in an increase in current period earnings.

An important concern in examining the relation between RAM and auditor resignation is the

confounding effect of clients’ performance. A client’s abnormal cash flows, production costs, and

discretionary expenses can be attributable to its poor performance. At the same time, auditors may

resign from poorly performing clients (Beneish et al. 2005). That is, clients’ financial performance may

explain the relation between RAM and auditor resignation. To mitigate this concern, we construct our

RAM measures after adjusting for financial performance. We follow the performance-matching

procedure that Kothari et al. (2005) propose in calculating performance-matched abnormal accruals.

We match each sample firm with all control firms from the same two-digit SIC industry, with ROA

(net income before extraordinary items divided by total assets) in the fiscal year greater than 50% but

less than 150% of the sample firms’ ROA.9 We measure the performance-adjusted abnormal cash flow

9 We restrict the range of comparable ROAs to ensure that the control firm's ROA is truly comparable to that of the sample firm. Without this restriction, even the ROA of the firm that has the closest ROA could be quite different from the ROA of the sample firm. We drop the sample observation if we cannot find a match within the 50% to 150% bound. We subtract the mean values of RAM measures of the matched control firms in the comparable performance range to mitigate the influence of measurement errors in RAM measures. We also attempt to apply a narrower cut-off of ROA greater than 80% but less than 120%. Although the number of usable observations is much smaller because of the limited availability of control firms, untabulated results are qualitatively similar. Throughout

preprint

accepted manuscript

14

from operations (AB_CFO), the performance-adjusted abnormal production costs (AB_PROD), and the

performance-adjusted abnormal discretionary expenses (AB_EXP) as the sample firm’s three individual

RAM proxies minus the mean values of corresponding measures for the matched control firms.

Cohen et al. (2008) contend that given sales levels, firms that manage earnings upward

experience some combination of unusually low cash flow from operations, unusually high production

costs, and unusually low discretionary expenses. Thus, they analyze the three individual RAM proxies

and also compute a single combined proxy by summing the three individual RAM variables. Similarly,

we use three individual proxies (AB_CFO, AB_PROD, and AB_EXP) and a combined proxy

(AB_COMBINED) in the analyses. Considering the expected directions of the three variables, we

calculate AB_COMBINED as (AB_PROD – AB_CFO – AB_EXP). Thus, our combined RAM proxy

increases as firms engage in more aggressive earnings management through real activities.

Empirical Model

To examine the relation between auditor resignation and RAM, we estimate the following

cross-sectional logistic regression model with an auditor resignation dummy (RESIGN) as a

dependent variable and real activities manipulation (RAM_PROXY) as an independent variable,

along with control variables:10

Pr (RESIGN =1) =F( α0 + α1 RAM_PROXY +∑=

9

2jjα OTHER AUDIT RISK CONTROL VARIABLES

+∑=

14

10kkα FINANCIAL PERFORMANCE CONTROL VARIABELS

+ ∑=

19

15llα OTHER CONTROL VARIABLES + INDUSTRY INDICATORS) (6)

RESIGN is an indicator variable that takes the value of one if the auditor resigns, and zero

otherwise. RAM_PROXY is one of our four proxies for RAM: performance-adjusted abnormal cash

the paper, we use the words “similar” or “consistent” to mean that the coefficients on variables of interest have the same signs and similar levels of statistical significances as those tabulated. 10 Industry indicators based on the client’s two-digit SIC are also included in model (6).

preprint

accepted manuscript

15

flows from operation (AB_CFO), performance-adjusted abnormal production costs (AB_PROD),

performance-adjusted abnormal discretionary expenses (AB_EXP), or a combined measure of

abnormal activities manipulation (AB_COMBINED). Control variables are defined in Appendix A.

In this study, we define unusually lower level of abnormal operating cash flows, unusually

lower level of discretionary expenses, and/or unusually high level of production costs as earnings

management through RAM. If clients with aggressive RAM are more likely to experience a high

probability of auditor resignation, we predict the coefficient estimates on AB_CFO and AB_EXP

(AB_PROD) to be negative (positive). We also expect the coefficient on AB_COMBINED to be

positive because the combined RAM proxy increases as firms engage in more aggressive earnings

management through real activities.

Johnstone and Bedard (2004) view the auditor’s portfolio management decisions as

functions of the client’s financial risk, audit risk, audit fees, and other client- and auditor-specific

variables. Thus, to isolate the incremental effect of RAM on auditor resignations, we include

other audit risk-related control variables that previous literature identifies as determinants of

audit risk and auditor changes, to minimize concerns about the correlated omitted variable

problem. To mitigate concerns about a potential endogeneity problem, especially one arising

from future financial performance, we include several control variables that are related to the

client’s financial performance. We also control for client size, auditor’s industry specialization,

resource constraints, and industry.

Prior research (Krishnan and Krishnan 1997; Shu 2000; Stice 1991) documents that

auditor litigation risk is positively associated with auditor resignations. To gauge the net effect of

RAM on auditor resignations after controlling for the effect of auditor litigation risk that can be

explained by factors other than RAM, we include the auditor litigation risk proxy,

AUDITOR_LIT, as a control variable. Note that we calculate the proxy for auditor litigation risk

preprint

accepted manuscript

16

based on Shu’s (2000) model, which does not incorporate RAM.11 We compute AUDITOR_LIT

at the end of the fiscal year prior to auditor changes, using the coefficients suggested in Shu

(2000).12 We also conduct additional analyses using an alternative version of Shu’s (2000) model,

as in Krishnan and Zhang (2005),13 and untabulated results are qualitatively similar.

To control for the potential substitution effect between accrual-based earnings management

and RAM (Cohen et al. 2008), we include abnormal accruals, AB_ACC, as an independent variable.

Ashbaugh-Skaife et al. (2008) find that internal control weakness affects the quality of accruals and

is positively associated with idiosyncratic risk and systematic risk, which in turn would increase audit

risk. Therefore we control for internal control deficiency (ICD). We also control for the variables that

represent the relationship between the auditor and the client, including an indicator for a going

concern opinion (OP_GC), an indicator for a long auditor tenure (LONG_TENURE), non-audit fee

(NON_AUDFEE), and audit fee (AUDFEE). Krishnan and Krishnan (1997) find that auditors are

more likely to resign from clients with going-concern opinions and less likely to resign from clients

with whom they have a long-term relationship, as evidenced by a long tenure. Cohen et al. (2010),

however, show that clients with longer auditor relationships are more likely to engage in RAM.

Following Johnson et al. (2002), we define auditor tenure as long if the predecessor auditor audited

the client for nine or more years. If an audit firm generates large non-audit and/or audit fees from the

client, it would be less likely to resign from the engagement. We also include a Big 4 indicator, BIG4,

as Cohen et al. (2010) find that clients of large audit firms are more likely to engage in RAM. At the

same time, Big 4 audit firms are more likely to resign from risky clients.

11 The untabulated results for the logistic model excluding the auditor litigation proxy, AUDITOR_LIT, are qualitatively similar. 12 AUDITOR_LIT = 0.276(SIZE) + 1.153(INV) + 2.075(REC) + 1.251(ROA) – 0.088(CURRENT RATIO) + 1.501(LEVERAGE) + 0.301(GROWTH) - 0.371(RETURN) – 2.309 (STOCK VOLATILITY) + 0.235(BETA) + 1.464(TURNOVER) + 1.060(DELIST) + 0.928(TECH) + 0.463(OPINION) - 10.049. Variables are defined in Appendix A. 13 To reduce noise in the computed measure, Krishnan and Zhang (2005) use only the significant variables in Shu’s (2000) model.

preprint

accepted manuscript

17

Auditors may resign from clients that experience declining profit or revenue (Beneish

et al. 2005). Poor financial performance may also trigger clients to engage in RAM. To control

for the client’s financial performance, we include several performance proxies, including ROA

(Johnstone and Bedard 2004), a loss indicator (LOSS), changes in sales (ΔSALES), a proxy for

financial distress (DISTRESS) (Krishnan and Krishnan 1997; Shu 2000), and a proxy for

expected future performance (F_PERF).

We also include other client- and auditor-specific variables, such as client’s leverage

(LEVERAGE), client’s sales growth (GROWTH), client’s size (SIZE), auditor’s industry market

share (MSHARE), and an indicator for a busy season audit (BUSY_FYE) as well as industry fixed

effects. Because auditors are more likely to resign from riskier clients, we expect a positive relation

between leverage and propensity for auditor resignations. If GROWTH proxies for risk, it would be

positively related to auditor resignation. Alternatively, auditors may prefer clients with high growth,

thus predicting a negative relation between GROWTH and auditor resignation. Krishnan and

Krishnan (1997) predict that client size is positively related to auditor resignations because it is

positively related to litigation risk, but find an insignificant relation. Auditors may want to retain

bigger clients, however. Thus, a priori, it is difficult to predict the sign of the relation between the

client’s size and auditor resignation propensity.

IV. EMPIRICAL RESULTS

To examine the association between RAM and auditor resignations, we use three

different control samples. The first control sample consists of client-initiated auditor changes

(i.e., auditor dismissals). Several prior studies use this approach to examine auditor resignations

(e.g., Krishnan and Krishnan 1997; Shu 2000). As the second control sample, we use continuing

audit clients, as in Johnstone and Bedard (2004). Finally, to further control for the effect of

preprint

accepted manuscript

18

clients’ performance on the relation between RAM and auditor resignations, we use

performance-matched continuing audit clients as the third control sample. Table 2, Panel A

reports descriptive statistics by auditor change and continuing audits.

[Insert Table 2 here.]

The mean and median values of the AB_CFO and AB_EXP (AB_COMBINED) for the

sample of auditor resignations are significantly lower (higher) than those for the samples of client-

initiated auditor dismissals and continuing audits. Note that our combined RAM proxy,

AB_COMBINED, increases as firms engage in more aggressive earnings management through real

activities. The results show that the differences in mean and median values between resignation

and dismissal samples are statistically significant at conventional levels. We observe similar results

between resignation and continuing audit samples. For AB_PROD, we find no significant

difference between auditor resignation and dismissal samples and between auditor resignation and

continuing audit samples. In sum, the descriptive statistics suggest that clients tend to have

unusually low cash flows and discretionary expenses prior to auditor resignations. We find no

evidence, however, that production costs are unusually high for clients with auditor resignations.

Panel A of Table 2 also provides evidence that the auditor resignation sample has

significantly higher litigation risk based on Shu’s (2000) model,14 and higher audit-related fees but

lower non-audit fees than the auditor dismissal sample. The descriptive statistics show that the

auditor resignation sample has relatively less effective internal controls, a higher probability of

going-concern opinion, and shorter auditor tenure. It is noted that approximately half of auditor

resignations are initiated by Big 4 auditors, while about 72 percent of dismissals are related to Big 4

14 Auditor litigation is a rare event. The mean auditor litigation score from the Shu model, AUDITOR_LIT, for the resignation sample is -5.6836, which corresponds to the 34 basis points of the auditor litigation probability (exp(-5.6836)/(1+exp(-5.6836)). In contrast, the mean value of the auditor litigation score is –6.0677 for the dismissal sample, which is equivalent to the 23 basis points of the litigation probability.

preprint

accepted manuscript

19

auditors. The results also show that the auditor resignation sample has, on average, a higher

likelihood of reporting a loss, lower ROA, greater financial distress, and worse future earnings,

compared to both dismissal and continuing audit samples. Furthermore, we observe that auditor

resignation sample features both a smaller client size and a smaller auditor’s market share than the

two control samples.

Panel B of Table 2 presents Pearson correlation coefficients for selected variables. As

shown, RESIGN is significantly and negatively (positively) correlated with AB_CFO and

AB_EXP (AB_COMBINED). Note that unusually low cash flows, unusually high production

costs, and unusually low discretionary expenses represent more aggressive RAM to manage

earnings upward. Our combined RAM proxy increases as firms engage in more aggressive

earnings management through real activities. Thus, bivariate correlations suggest that auditors

are more likely to resign from clients engaging in RAM, except overproduction. We also observe

that RESIGN is positively (negatively) correlated with auditor litigation, internal control

weakness, going-concern opinion, audit fee, loss, and financial distress (auditor tenure, non-audit

fee, Big 4 auditor indicator, ROA, a proxy for future performance, client size, and auditor market

share). Consistent with the findings of Cohen et al. (2008), AB_CFO and AB_EXP are negatively

correlated. Furthermore, the results show that while AB_CFO is positively (negatively)

correlated with change in sales and financial distress (ROA), AB_EXP is positively (negatively)

correlated to ROA (financial distress). We find little evidence, however, of correlations between

COMBINED_RAM and the financial performance variables, except change in sales.

Analysis with Auditor Dismissals as a Control Sample

Table 3 presents the results of the cross-sectional logistic regression analyses using a

control sample of auditor dismissals. In this table and all subsequent tables, we report test

statistics and significance levels based on standard errors adjusted for firm clustering.

preprint

accepted manuscript

20

[Insert Table 3 here.]

The coefficients on AB_CFO and AB_EXP are negative and significant at the p<0.01 or

p<0.05 level in models 1 and 3. The coefficient on the combined proxy, AB_COMBINED, is

positive and significant at the p<0.01 level in model 4, indicating that client firms that experience

auditor resignations are more likely to make opportunistic operating decisions that deviate from

normal business practices prior to the auditor change than are client firms which dismiss their

auditors. In contrast, the coefficient on AB_PROD is not statistically significant in model 2. Note

that we obtain these results after controlling for abnormal accruals. The coefficient on

AUDITOR_LIT is positive and significant at the five-percent level in all models, indicating that

auditors are more likely to resign from engagements when the auditor litigation risk increases,

which is consistent with Shu (2000).

Our results also show that the likelihood of auditor resignation is significantly higher for

clients having internal control deficiencies, auditors’ going-concern opinions, and financial

distress. Auditor tenure, audit fee, Big 4 auditor indicator, expected future performance, and

client size are significantly negatively associated with the probability of auditor resignation.15 In

sum, the results reported in Table 3 suggest that although auditor resignation is driven by several

factors, auditors seem to view a client's aggressive RAM, with the exception of that through

overproduction, as an important factor in their client portfolio management decisions.

Analysis with Continuing Audit Clients as a Control Sample

This section provides evidence of the effect of RAM on auditor resignations, using

continuing clients as an alternative control sample. This approach enables us to examine the

effect of RAM on audit firms’ client portfolio-management decisions more directly by

comparing RAM for clients with auditor resignations versus clients without auditor changes. 15 Big 4 auditors may be more likely to resign from risky clients, but they are not necessarily more likely to resign from all clients. See Table 7 and related discussions for analyses by incoming and outgoing auditor types.

preprint

accepted manuscript

21

Table 4 presents the logistic regression results of auditor resignation on RAM and control

variables. The coefficients on AB_CFO and AB_EXP (AB_COMBINED) are again negative

(positive) and significant at the p<0.05 or p<0.01 level. These results are consistent with those

reported in Table 3. Overall, the results presented in Table 4 show that clients with auditor

resignations tend to make more opportunistic operating decisions, except those for

overproduction, than do clients with continuing auditors.

[Insert Table 4 here.]

Analysis with Performance-Matched Continuing Audit Clients as a Control Sample

This section presents results based on performance-matched continuing audit clients as an

alternative control sample. We match each auditor resignation with the firm from the same two-

digit SIC industry that retains its auditor and has the closest ROA to the auditor resignation firm.

Through this one-to-one matching, we further control for the potential effect of clients’ financial

performance on the relation between RAM and auditor resignations.

Panel A of Table 5 reports descriptive statistics of RAM proxies for the auditor

resignation sample and the matching sample of continuing audit clients. The mean values of

AB_CFO and AB_EXP (AB_COMBINED) are significantly lower (higher) for the resignation

subsample than for the matching sample.

[Insert Table 5 here.]

Panel B of Table 5 reports the logistic regression results of auditor resignation on RAM and

control variables. Consistent with the results reported in Tables 3 and 4, the coefficients on

AB_CFO and AB_EXP (AB_COMBINED) are negative (positive) and significant at conventional

levels. The coefficient on AB_PROD is insignificant, however. In sum, the evidence based on one-

to-one matching is consistent with our prediction that auditors are more likely to resign from

engagements when their clients actively engage in RAM, except for RAM through overproduction.

preprint

accepted manuscript

22

Analysis with “Suspect” Clients

Prior studies (e.g., Roychowdhury 2006; Cohen et al. 2008) conduct additional analyses

using “suspect” firms (SUSPECT) that are particularly likely to manage earnings based on the

three benchmarks of zero earnings, non-negative changes in earnings, and analysts’ forecasts.

Graham et al. (2005) also conclude that managers choose real actions over accounting actions to

meet earnings benchmarks. This suggests that RAM is more likely to occur if the firm would

otherwise miss its earnings targets. Examining the “suspect” sample of “meet or beat” clients

also mitigates concerns about possible measurement errors in RAM proxies.

Following prior studies, we examine whether clients whose auditors resign from engagements

more aggressively engage in earnings management through RAM to meet these benchmarks prior to

auditor changes. First, we identify SUSPECT firm-years as those observations with net income before

extraordinary items, scaled by total assets that fall in the interval [0, 0.01).16 In the upper section of

Panel A of Table 6, we report mean and median values of RAM proxies for clients in the auditor

resignation sample and the auditor dismissal and continuing audit samples where the client firms

manage earnings to “just” avoid reporting a loss (i.e., fall within the interval).

Next, the middle section of Panel A of Table 6 reports results using a second measure of

SUSPECT firm-years, in which the change in net income before extraordinary items scaled by total

assets falls in the interval [0, 0.01). The mean and median values of RAM proxies for clients “just”

meeting or beating last year’s earnings are reported. Finally, the lower section of Panel A of Table 6

reports results for clients that manage earnings to “just” meet or beat the existing analysts’ consensus

forecasts prior to the earnings announcement. We define the analyst forecast error (AFE) as the

16 Roychowdhury (2006) and Cohen et al. (2008) identify and use firm-year observations with net income or change in net income before extraordinary items scaled by total assets that fall in the interval [0, 0.005) as SUSPECT firm-years. In this study, we use the broader interval [0, 0.01) as SUSPECT firm-years, because the number of firm-year observations is too small when we use the interval [0, 0.005). We also replicate our analyses using the interval [0, 0.005) as SUSPECT firm-years, however, and find the results qualitatively similar to those reported using the broader interval [0, 0.01).

preprint

accepted manuscript

23

difference between actual earnings per share (EPS) as reported by the Institutional Brokers’ Estimate

System (I/B/E/S) less the last consensus EPS forecast prior to the earnings announcement. We focus

on firm-year observations in which the AFE is one cent per share or less.

[Insert Table 6 here]

We find little evidence from the first benchmark, RAM to “just” avoid reporting losses,

potentially because of the small sample size. As shown for the last two benchmarks (i.e., RAM to “just”

meet or beat last year’s net income, and RAM to “just” meet or beat analyst forecasts by one cent per

share), the suspect clients with auditor resignation have significantly lower (higher) mean and median

values of AB_CFO and AB_EXP (COMBINED_RAM) than suspect clients with auditor dismissals,

except for the median difference in AB_EXP. This is also the case when we compare clients whose

auditors resign to continuing audit clients. Overall, these results suggest that clients whose auditors

resign tend to make more opportunistic operating decisions, except for overproduction, than those with

auditor dismissals or continuing audits when facing potential benchmark incentives.

We also re-estimate the logistic regressions by including the indicator for suspect clients,

SUSPECT, which takes the value of one if the firm-year observation belongs to any suspect firm

categories discussed above and zero otherwise, and the interaction of this indicator and RAM proxies.

Panel B of Table 6 presents the results with auditor dismissals as a control sample. Consistent with the

previously reported results, AB_CFO and AB_EXP (COMBINED_RAM) are significantly and

negatively (positively) associated with the likelihood of auditor resignation. More importantly, the

coefficients on the interactions of the suspect client indicator and RAM proxies, AB_CFO*SUSPECT

and AB_EXP*SUSPECT (AB_COMBINED*SUSPECT), are negative (positive) and significant at

conventional levels, indicating that auditors are even more likely to resign from suspect clients. The

sum of coefficients on RAM proxies and the interaction term, (α1+α3), are negative (positive) for

AB_CFO and AB_EXP (COMBINED_RAM) and significant at the p<0.05 or p<0.01 level.

preprint

accepted manuscript

24

Powers (2005) points out that an inference based on the coefficient of interaction term in logit

and probit models can be misleading. More generally, Ai and Norton (2003) argue that the

magnitude of the interaction effects (marginal effect of changes in two variables) in nonlinear models

does not equal the marginal effect of the interaction term, and that the statistical significance of the

former is not easily calculated. They present a consistent estimator of the interaction effect for

nonlinear models by taking cross-derivative and cross-difference into account. Following prior

studies (Ai and Norton 2003; Norton, Wang, and Ai 2004), we calculate the consistent estimators

and standard errors of the interaction effects in our logit models. We report the interaction effect and

Z-statistics, as well as statistical significance, for each logit model at the bottom of Panel B of Table

6. Consistent with the results reported earlier, interaction effects are significantly negative (positive)

for AB_CFO and AB_EXP (AB_COMBINED). Taken together, the results reported in Table 6

suggest that, with the exception of overproduction, the association between the likelihood of auditor

resignations and real operating decisions tends to be more pronounced for the suspect clients.17

V. ADDITIONAL ANALYSES

Auditor Resignations and RAM by Types of Incoming and Outgoing Auditors

For every auditor resignation, there is another auditor willing to pick up the same client. That

is, in an environment in which audits of all publicly traded companies are required, auditors cannot

collectively resign from riskier clients en masse — some audit firms must audit these risky clients.

Bockus and Gigler (1998) establish conditions under which an incumbent auditor prefers to resign

from the client and a different audit firm agrees to audit the client firm. Therefore, the direction of

auditor change is not necessarily from big to small auditors.

17 Untabulated results with the control sample of continuing audits are qualitatively similar to those reported in Panel B of Table 6.

preprint

accepted manuscript

25

Shu (2000) reports that compared to clients who dismiss auditors, clients whose auditors

resign are more likely to switch to small auditors. A recent report by the Government Accountability

Office (GAO, 2006) suggests that smaller firms move to smaller auditors because of concerns related

to audit and other costs, and because large auditor resignations are related to client profitability and

risk concerns. In this section, we investigate how RAM is associated with the allocation of clients

among different auditors surrounding auditor resignations.

SOX expands auditors’ responsibilities to include providing opinions on the effectiveness

of the clients’ internal controls and increased regulatory scrutiny of audit firms’ practices. Big 4

auditors may shed some low-quality clients when they make their client portfolio decisions

because of an increase in compliance challenges associated with SOX. By examining incoming

and outgoing auditors’ characteristics, we provide more insight into the association between RAM

and auditor-client realignments.

[Insert Table 7 here.]

Table 7 presents the results from the logistic regression including an indicator for non-Big 4

incoming auditor and its interaction with RAM proxies. The coefficients on four RAM proxies are all

insignificant, while the coefficients on AB_CFO*IN_NON-BIG4 and AB_EXP*IN_NON-BIG4

(AB_COMBINED*IN_NON-BIG4) are negative (positive) and significant at conventional levels. As

shown at the bottom of Table 7, the interaction effects are also statistically significant. The combined

coefficient estimates (α1+α3) for RAM proxies, AB_CFO and AB_EXP (AB_COMBINED), are

negative (positive) and significant at the p<0.01 level, suggesting that our results are driven primarily

by auditor changes with non-Big 4 incoming auditors.

Untabulated results from the logistic regression including an indicator for Big 4 outgoing

auditor and its interaction with RAM proxies show that while the coefficients on AB_CFO and

AB_EXP (AB_COMBINED) are negative (positive) and significant at conventional levels, those on

preprint

accepted manuscript

26

the interaction terms are insignificant. The interaction effects are also insignificant. Taken together,

we interpret these results to mean that while both Big 4 and non-Big 4 auditors shed risky clients

with aggressive RAM, smaller auditors generally acquire these clients.

Effect of the Sarbanes-Oxley Act of 2002

Cohen et al. (2008) report that the level of RAM increases significantly after the passage

of SOX. To investigate whether an increase in RAM around SOX explains our evidences

reported earlier, we conduct additional analyses by partitioning our sample into two sub-periods:

pre- and post-SOX. We classify years 2000 and 2001 as the pre-SOX period and 2002 through

2010 as the post-SOX period.18 Table 8 presents the results from the logistic regression including

a post-SOX indicator, POST, and its interaction with RAM proxies.

[Insert Table 8 here]

The coefficients on AB_CFO, AB_PROD, AB_EXP, and AB_COMBINED are all

insignificant. 19 In contrast, the coefficients on interaction terms, AB_CFO*POST and

AB_EXP*POST (AB_COMBINED*POST), are negative (positive) and significant at conventional

levels. The interaction effects are consistent with this result. The combined coefficients are

negative (positive) and statistically significant for AB_CFO and AB_EXP (AB_COMBINED). Thus,

our findings reported earlier appear to be driven mainly by abnormal operating decisions that

become more prevalent in the post-SOX period, which is consistent with Cohen et al. (2008).

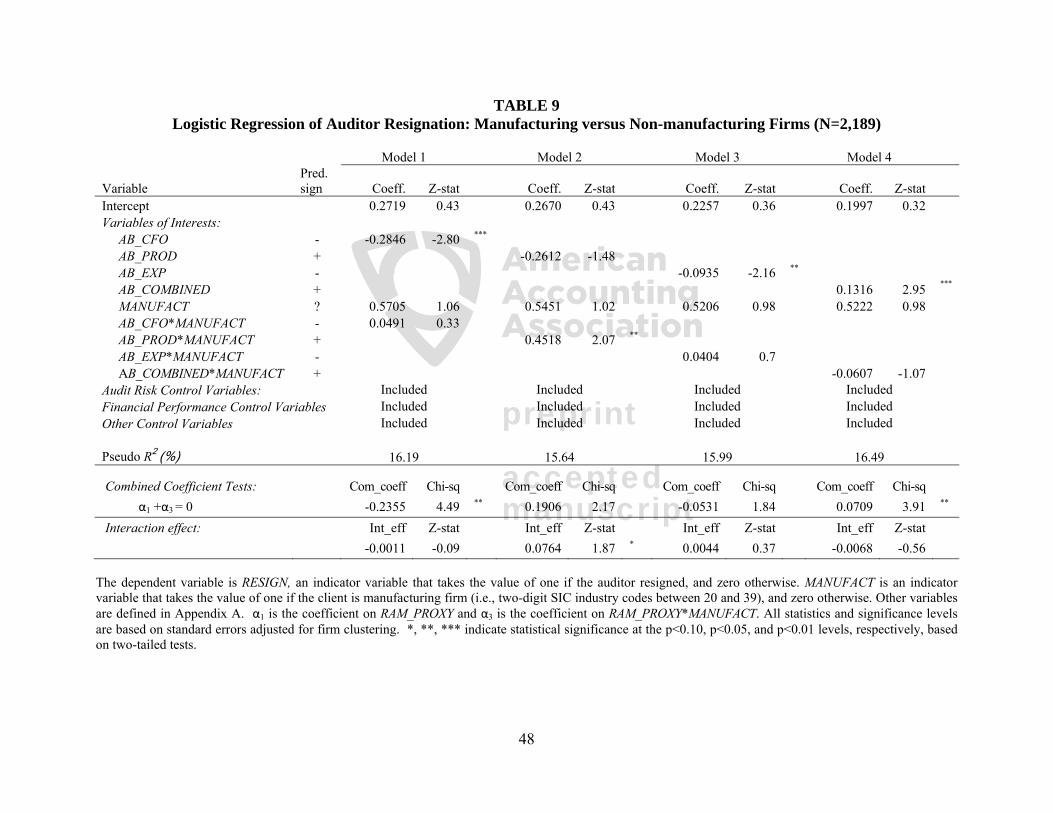

Analysis by Manufacturing versus Non-manufacturing Clients

As RAM through overproduction is applicable only to manufacturing firms, the insignificant

coefficient on AB_PROD in our logistic regressions may result from including non-manufacturing

firms in the sample. Following Cohen et al. (2008), who provide an additional analysis only for

18 Untabulated results excluding year 2002 (the transition year) from the post SOX period are qualitatively similar. 19 Low power because of the small pre-SOX sample may be preventing significance in the pre-SOX period.

preprint

accepted manuscript

27

manufacturing firms, we estimate the logistic regression analysis including an indicator for

manufacturing firms, MANUFACT, and the interaction of this indicator and RAM proxies. Table 9

summarizes the results where we define a firm as a manufacturing firm if its two-digit SIC falls

between 20 and 39 (Cohen et al., 2008). Consistent with the results reported in Table 3, we continue

to find significantly negative (positive) coefficients on AB_CFO and AB_EXP (AB_COMBINED) at

the p<0.05 or p<0.01 level. For AB_PROD, the interaction effect is significantly positive, but the

combined coefficient is statistically insignificant. Overall, the results in Table 9 suggest that our

results are similar between manufacturing clients and other clients.20

[Insert Table 9 here]

Analysis of the Effect of Clients’ Size

Larger clients typically provide more business opportunities to audit firms, and thus even if

such clients are risky, audit firms might be reluctant to resign from the engagements. To see if the

relation between auditor resignation and real operating decisions differs across client’s size, we

conduct an additional analysis. We partition our sample into big and small clients based on the

median value of the client size in our sample. Untabulated results show that our results are largely

driven by auditor changes from small clients.

Association between RAM and Litigations against Auditors

To corroborate our main analyses and provide evidence that RAM exposes auditors to an

increased litigation risk, we examine the association between clients’ abnormal operating

decisions and the incidence of auditor litigations. We obtain a sample of litigations against

auditors from the Audit Analytics Litigation database between 2000 and 2010. Several recent

studies (e.g., Arena and Julio 2011; Crane 2011; Hackenbrack et al. 2011; DeFond et al. 2012)

20 Cohen et al. (2008) also find that the results for non-manufacturing firms are consistent with those for manufacturing firms.

preprint

accepted manuscript

28

also rely on the Audit Analytics Litigation database to identify auditor litigations. The Audit

Analytics Litigation database includes legal cases against auditors as well as other parties. We

carefully screen legal cases against auditors by examining auditors in the legal exposure periods.

We merge the sample with the COMPUSTAT and CRSP and restrict sample observations to

those having the necessary data to calculate variables for RAM, abnormal accruals, and other

variables to be included in the logit model. If there are multiple auditor litigations for a client, we

retain only the first litigation in the sample. Because auditor litigation is a rare event, we do not

limit this analysis to the clients with auditor changes. Our final sample consists of 174 auditor

litigations. We construct the control sample based on the fiscal year and four-digit SIC industry

code. We identify 6,003 control firm years not subject to auditor litigation.

By incorporating RAM proxies and abnormal accruals after controlling for variables in

Shu’s (2000) model, we estimate the following logistic regression model:

Pr(LIT = 1) = F(α0 + α1 RAM_PROXY + α2 AB_ACC + α3 SIZE + α4 INV + α5 REC + α6 ROA + α7 CURRENT RATIO + α8 LEVERAGE + α9 GROWTH + α10 RETURN + α11 STOCK VOLATILITY + α12 BETA + α13 TURNOVER + α14 DELIST + α15 TECH + α16 OPINION) (7) where LIT = an indicator variable that takes the value of one if the client’s auditor is named in a lawsuit, and zero otherwise. Other variables are defined in Appendix A.21 If aggressive RAM is positively associated with auditor litigation risk, the coefficients on

AB_CFO and AB_EXP (AB_PROD) will be negative (positive). If RAM and auditor litigation risk

are positively associated, the coefficient on AB_COMBINED, which increases in aggressive RAM,

will be positive. Table 10 presents the results of the logistic regression model.

[Insert Table 10 here.]

As predicted, the coefficients on AB_CFO and AB_EXP are negative and significant at 21 All variables are measured in the year associated with litigation. To reduce the effect of outliers, all continuous variables are winsorized at the top and bottom 1% of the distribution.

preprint

accepted manuscript

29

conventional levels. The combined proxy, AB_COMBINED, shows a positive and significant

relation to the incidence of auditor litigation at the p<0.01 level. In contrast, the coefficient on

AB_PROD is insignificant. Coefficients on the control variables are in the predicted directions,

and their magnitudes are comparable to those in Shu (2000). In sum, these results are consistent

with clients’ aggressive abnormal operating decisions, except those for overproduction, being

positively associated with auditor litigation risk. This evidence suggests that aggressive RAM

may lead to increased legal exposure for auditors.

VI. SUMMARY AND CONCLUSION

It is well known that auditors have become more conservative in their clients' portfolio

management in the post-SOX era. Extant literature reports that RAM is an alternative tool of earnings

management (e.g., Roychowdhury 2006; Cohen et al. 2008; Cohen and Zarowin 2010) and that

managers tend to trade off RAM and accrual-based management as substitutes, a phenomenon that is

more prevalent in post-SOX periods (e.g., Cohen et al. 2008). In this study, we examine the relation

between the auditor’s client retention decision and RAM. We predict that auditors are more likely to

resign when clients engage in RAM aggressively prior to auditor switches.

Consistent with our prediction, we find that, with the exception of RAM through

overproduction, clients’ opportunistic operating decisions are positively associated with the

likelihood of auditor resignations. Our results are robust to three sets of control samples: client-

initiated auditor changes, all continuing audit clients, and performance-matched continuing audit

clients. We also find that clients with auditor resignations tend to engage in RAM, except for

RAM through overproduction, more aggressively to meet or beat their earnings benchmarks

prior to auditor changes compared to those with auditor dismissals or continuing audits. In

preprint

accepted manuscript

30

addition, we find that, except for overproduction, auditors are especially sensitive to clients’

RAM to just meet or beat earnings benchmarks in their clients' retention decisions.

Additional analysis shows that clients whose auditors resign from the engagement tend to

hire non-Big 4 auditors as successor auditors and that these clients engage in RAM more actively

than other clients whose incoming auditors are Big 4. We further find that the association between

RAM and the likelihood of auditor resignation is particularly pronounced for small clients and

during the post-SOX period. Finally, we find that client’s RAM, specifically abnormal cash flows

and abnormal discretionary expenses, is significantly associated with litigations against auditors.

Our findings should be of interest to auditors, investors, clients’ audit committees, and

regulators. Disclosure about auditor resignations may reveal useful information about clients’

financial-reporting practices. Since auditor resignations potentially signal risk arising from clients’

opportunistic financial reporting behavior, investors can make more informed decisions when they

understand the linkage between RAM and auditor resignations. Our study also has an implication

for clients’ audit committees, because these committees can help avoid potential negative

consequences associated with RAM and auditor resignations by overseeing management reporting

practices. Further, our study has an implication for regulators, because they are concerned about

auditor changes that are triggered by management opportunism (see Securities and Exchange

Commission, 1988).

preprint

accepted manuscript

31

REFERENCES

Ai, C. and E. C. Norton. 2003. Interaction terms in logit and probit models. Economic Letters 80: 123-129.

American Institute of Certified Public Accountants (AICPA). 2002. Consideration of Fraud in a Financial Statement Audit. Statement on Auditing Standards No. 99. New York, NY: AICPA.

American Institute of Certified Public Accountants (AICPA). 2007. A Firm’s System of Quality Control. Statements on Quality Control Standards No. 7 (QC sec. 10). New York, NY: AICPA.

Arena, M., and B. Julio. 2011. Litigation risk, cash holdings, and corporate investment. Working paper, Marquette University and London Business School.

Arthur Andersen & Co., Coopers & Lybrand, Deloitte & Touche, Ernst & Young, KPMG Peat Marwick, & Price Waterhouse. 1992. The Liability Crises in the United States: Impact on the Accounting Profession.

Ashbaugh-Skaife, H., D. Collins, W. Kinney, and R. LaFond. 2008. The effect of SOX internal control deficiencies and their remediation on accrual quality. The Accounting Review 83 (1): 217-50.

Baber, W., P. Fairfield, and J. Haggard. 1991. The effect of concern about reported income on discretionary spending decisions: the case of research and development. The Accounting Review 66: 818–829.

__________., K. Kumar, and T. Verghese. 1995. Client security price reactions to the Laventhol and Horwath bankruptcy. Journal of Accounting Research 33 (Autumn): 385-95.

Beneish, M. D., P. E. Hopkins, I. P. Jansen, and R. Martin. 2005. Do auditor resignations reduce uncertainty about the quality of firms’ financial reporting? Journal of Accounting and Public Policy 5: 357-390.

Bens, D., V. Nagar, and M. Wong. 2002. Real investment implications of employee stock option exercises. Journal of Accounting Research 40: 359–393.

Bockus, K., and F. Gigler. 1998. A theory of auditor resignation. Journal of Accounting Research 36:191-208.

Bushee, B. 1998. The influence of institutional investors on myopic R&D investment behavior. The Accounting Review 73: 305–333.

Cohen, D., A. Dey, and T. Lys. 2008. Real and accrual-based earnings management in the pre- and post-Sarbanes-Oxley periods. The Accounting Review 83: 757–787.

_________., and P. Zarowin. 2010. Accrual-based and real earnings management activities around seasoned equity offerings. Journal of Accounting and Economics 50: 2-19.

Crane, A. D. 2011. The litigation environment of a firm and its impact on financial policy. Working paper, Rice University.

Dechow, P., and R. Sloan. 1991. Executive incentives and the horizon problem: an empirical investigation. Journal of Accounting and Economics 14: 51–89.

DeFond, M. L., C. Y. Lim, and Y. Zhang. 2012. Do auditors value client conservatism? Working paper, University of Southern California and Singapore Management University.

_________., and K. Subramanyam. 1998. Auditor changes and discretionary accruals. Journal of Accounting & Economics 25 (February): 35–67.

Ewert, R., and A. Wagenhofer. 2005. Economic effect of tightening accounting standards to restrict earnings management. The Accounting Review 80: 1101-1124.

Francis, B., I. Hasan, and L. Li. 2011. Firms’ real earnings management and subsequent stock price crash risk. Working Paper. Rensselaer Polytechnic Institute.

Government Accountability Office (GAO). 2006. Sarbanes-Oxley Act: Consideration of key principles needed in addressing implementation for smaller public companies. (GAO-06-361).

preprint

accepted manuscript

32

Graham, J., C. Harvey, and S. Rajgopal. 2005. The economics implications of corporate financial reporting. Journal of Accounting and Economics 40: 3-73.

Gunny K. 2010. The relation between earnings management using real activities manipulation and future performance: Evidence from meeting earnings benchmarks. Contemporary Accounting Research 27(3): 855-888.

Hackenbrack, K., N. T. Jenkins, and M. Pevzner. 2011. Relevant but delayed information in negotiated audit fees. Working paper, Vanderbilt University and George Mason University.

Healy, P, and J. Wahlen. 1999. A review of the earnings management literature and its implications for standard setting. Accounting Horizons 13: 365–383.

Heninger, W. 2001. The association between auditor litigation and abnormal accruals. The Accounting Review 76: 111-126.

Johnson, V. E., I. K. Khurana, and J.K. Reynolds. 2002. Audit-firm tenure and the quality of financial reports. Contemporary Accounting Research 19 (4): 637-660.

Johnstone, K. M., and J. Bedard. 2004. Audit firm portfolio management decisions. Journal of Accounting Research 42 (4): 659-690.

Jones, J. 1991. Earnings management during import relief investigations. Journal of Accounting Research 29: 193–228.

Kim, Y., M. Park, and B. Wier. 2012. Is earnings quality associated with corporate social responsibility?. The Accounting Review 87 (3): 761-796.