re-boot – venture capital investing for the 21st century

DESCRIPTION

Healthcare venture capital fundraising and investment activity is at historical levels. While healthcare’s resurgence has been breathtaking, however, considerable challenges for those seeking to invest in venture funds still exist. What will it take to increase direct investing participation rates?TRANSCRIPT

“Re-Boot”Venture Capital Investing

in the 21st Century

S. Jordan AssociatesLife Sciences Business Development & Finance

2S. Jordan AssociatesLife Sciences Business Development & Finance

Introduction – Direct InvestingHealthcare venture capital fundraising and investment activity is at historical levels. Bolstered by robust Initial Public Off er-ings (IPOs), business development/licensing and Mergers and Acquisitions (M&A) activity, unprecedented amounts of capital are being raised/deployed into healthcare companies and distributed to General Partners (GPs) generating consis-tent, positive returns for investors.

While healthcare’s resurgence has been breathtaking, consider-able challenges for those seeking to invest in venture still exist including:

■ Access to top-decile performing funds■ Th e number of healthcare focused venture capital

fi rms (especially those funding early-stage compa-nies) rapidly declined following the “Great Reces-sion” and have only moderately recovered

■ Healthcare continues to compete for investment capital vis-a-vis sectors with perceived greater upside and lower risks (Technology)

In particular, the biotech and pharmaceutical market sectors dissuade many investors from participating given longer development timelines, and burdensome clinical, regulatory, and commercial hurdles. Th ough capital fl ows into the healthcare sector remain robust and forecasted to remain strong throughout 2015-2016, there is risk of a crowded private market without investors if the IPO window closes and non-venture capital (VC) investors (Crossover) pull back funding the sector.

Venture capital has oft entimes struggled returning “alpha” to Limited Partners (LPs) leading to constriction of active venture funds in the sector (inability of underperforming funds to raise capital and dissolve). However, recent market outperformance (more IPOs during 2013-2014 period than the cumulative total of the previous decade) has elevated distributions ($20 billion in 2014) and returns to record levels stimulating capital raising activity by leading venture funds. (Flagship Ventures raised $600 million, 3/15; SV Life Sciences, $400 million, 5/15, Clarus Ventures, $500 million, 6/15)

Source: Bruce Booth, “Venture-Backed Biotech Today, Refl ections on Exits, Funding, and Startup Formation,” Forbes 1/22/15

3S. Jordan AssociatesLife Sciences Business Development & Finance

In this market environment, management fees and carry are less of a concern to LPs but could change quickly with a reversal in capital fl ows and if lower returns ensues. Historically high fees detracted signifi cantly from returns render-ing most venture fund profi ts comparable to public market growth (Source: Kauff man Study). Th ese high fee structures (“2”/“20” model) further incentivize fund managers to raise larger funds making it more diffi cult to invest in early-stage deals (“can’t put enough capital to work”) which is the primary source of innovation in the healthcare sector (as evidenced by decreases in the number of Series A companies funded year-over-year, 2014-2015).

History has a tendency to repeat itself and venture investing is nor the exception exhibiting cyclical waves of outperfor-mance and underperformance. Periods of outperformance characterized by signifi cant infl ows of capital and plentiful exits/liquidity (IPOs) are followed by time periods (“Great Recession”) when investors (capital fl ows) fl ee the sector for safe havens. Not surprising then to note prior to recent outperformance, the high risk of venture coupled with meager returns led many to declare the “venture model broken.” Venture is far from dead, however, consider how answers to the questions below have the potential to smooth out capital fl ows into the healthcare sector throughout market cycles.

When venture fundraising/investment levels do subside, will alternative sources of capital become available to meet the growing capital needs of emerging growth companies in the healthcare sector?

Will LPs investing on a “direct” basis (co-investing vs. through traditional GP structures) be “that” source of alternative capital for emerging growth healthcare companies?

4S. Jordan AssociatesLife Sciences Business Development & Finance

GENERAL PARTNERS:

Transition from Traditional GP Role to … “LEAD” INVESTOR

Reduce Financing Risk ■ Access to $11 billion in available co-invest capital

Enhanced Control ■ Direct investors are passive participants

Lower Investment Expense ■ Eliminate costs and complexity of syndication with other GPs

Rapid Decision Making ■ Direct investors depend upon diligence and track record of Lead

Greater Strategic Flexibility ■ Ability to fi nance to “Peak Value”

Higher Capital Effi ciency ■ Tighter reserves

Stronger Portfolio ■ More companies, broader diversifi cation

New LP Relationships ■ “Deal-by-Deal” leads to stronger relationships

LIMITED PARTNERS:

Transition from Traditional GP Role to … “DIRECT” INVESTOR

No Fee, No Carry ■ Gross IRR = Net IRR

Shortened Investment Horizons ■ Average “Hold” period for discrete healthcare invest-ment = 4.7 years

Accelerated Liquidity ■ Distributions made immediately upon “Exit” of each Company

Maximize MOIC ■ $100 to $150 million of annual investment potential in (12) to (15) deals

Participation with Top-Tier Managers ■ (8,300) Lead investors have made at least (1) invest-ment since 2012

Extensive Deal Flow ■ 900+ Direct healthcare co-investment opportunities, annually

Established “Exit” Pathway ■ Institutional leadership and strategic validation

Transparency ■ 8-week due diligence; Online portfolio management and reporting

Access To Management & Board ■ Opportunity evaluation, performance measurement, “exit” planning

Tailored Portfolio ■ Focus on sectors, stage of development, asset class, Lead investors

Favorable Valuation & Structure ■ “Pari Passu” investment directly alongside institutional Lead investor

‘Deal-By-Deal’ Discretion ■ Flexibility in decision-making, customizing portfolio

Sources of Potential Superior Outcomes in Direct Investing

Th e goals of this paper are to establish best practices for direct investing while providing managers (GPs), institutional managers (LPs), and early-stage/emerging growth companies with a greater understanding of the opportunities/chal-lenges associated with this unique funding mechanism. We believe successful implementation of these best practices will increase direct investing participation rates. Below is a summary overview of potential superior outcomes associated with direct investing:

5S. Jordan AssociatesLife Sciences Business Development & Finance

“State of the Union” – Venture Capital By any measure 2014 was a remarkable year for the venture capital industry. Fundraising “surged 56% over 2013 reaching its highest level since 2008 signaling confi dence in the industry is high due in part to increased distributions to investors over the past few years who then reinvested capital in new funds.” (Source: Jonathan Norris/Kristina Peralta, “Trends in Healthcare Investments and Exits 2015,” Silicon Valley Bank)

Investment levels soared to post-bubble heights! Healthcare venture investment grew signifi cantly, reaching $8.6 billion in 2014, a 30% increase over 2013. However, “only around 50% of the $6 billion invested in private biotechs came from ‘conventional’ venture investors.” (Source: Bruce Booth, “Venture-Backed Biotech Today, Refl ections on Exits, Funding, and Startup Formation,” Forbes, 1/22/15)

Th e IPO markets hit post-millennium highs in many key metrics, and the performance of the market has proven broad and resilient. Th e strong IPO markets continued to include a number of small-medium sized deals, and for the second year in a row and the second time ever, the majority of venture-backed IPOs were in the biotechnology/pharmaceutical industry.

Th e total number of rounds and the number of fi rst funds remained relatively unchanged from prior years (meaning the average values per deal are steadily escalating accounting for increase in aggregate capital invested), while seed and early-stage companies continue to be the recipient of the majority of deals. (Source: Bruce Booth, “Where Does All Th at Biotech Venture Capital Go,” Forbes, 2/9/15 - Data Source: HBM)

6S. Jordan AssociatesLife Sciences Business Development & Finance

A healthy venture capital ecosystem requires its metrics to be in balance. And while the quality of new business opportu-nities (deal fl ow) remains very high and the best opportunities are getting funded, stresses remain. For instance, nearly the same number of private biotech companies received venture fi nancing in a lean year for the capital markets (2009) then in the IPO and M&A fueled year of 2014. (Source: Bruce Booth “Data Snapshot: Venture-Backed Biotech Financing Riding High,” Forbes, 4/21/15)

Given newly funded companies are the “lifeblood” of innovation in the healthcare ecosystem, this trend should be care-fully analyzed. From a venture capital perspective these fi nancing levels may refl ect the equilibrium level wherein compa-nies deserving of funding receive it. But from a company perspective, the costs of rejection and associated “opportunity costs” (another company selected by venture capitalists instead, fails) are high given capital’s infl uence on advancing pre/clinical milestones (“proof of concept”) in a timely fashion in light of competitive threats and limited patent lives.

And unlike the soft ware industry, exit demand far exceeds the pace of startup creation highlighting the disconnect between demand for innovation and formation of new startups. (Source: Bruce Booth “Startups, Exits, and Ecosystem Flux: Bullish for Biotech,” Forbes, 9/8/2014)

Source: Jonathan Norris, Kristina Peralta, “Trends in Healthcare Investments and Exits 2015,” Silicon Valley Bank

7S. Jordan AssociatesLife Sciences Business Development & Finance

In addition, despite the strong year for later-round deals, 2014 saw a drop in Series A funding (oft en involves a syndicate of venture fi rms backing a new approach to drug development funding early-stage companies). Series A round invest-ment dropped from $1.2 billion in 2013 to $0.9 billion in 2014. Th e number of fi rst-time Series A investments also dropped from 63 in 2013 to 62 in 2014. Not surprising, the biotech sector started fewer companies in the robust 4Q 2014 than in any quarter of 2009 and 2010. (Source: Bruce Booth “Data Snapshot: Venture-Backed Biotech Financing Riding High,” Forbes, 4/21/15)

8S. Jordan AssociatesLife Sciences Business Development & Finance

Investment Activity & Capital Commitments2014 was a great year for investment activity and capital commitments in healthcare! However, owing to the nature of venture capital as a long-term investment, the well-being of the asset class must always be considered from a historical perspective taking into account multiple market cycles.

In fact, the activity level of the US venture capital industry in 2014 was roughly half of what it was at the 2000-era peak. For example in 2000, 1,049 fi rms each invested $5 million or more during the year. In 2014, new fi rms and new play-ers increased that count from recent years but still only to 635 fi rms. Of those, 195 invested in fi rst fi nancings, and 197 invested in life sciences.

New commitments to venture capital funds in the United States (U.S.) by LPs increased to $30.0 billion in 2014 from $17.7 billion a year earlier, and this increase is not surprising. Th e strong IPO markets in 2012 (although it was selective), 2013, and 2014 returned long-deployed capital to the investors in venture capital funds which was then reinvested into new funds.

Investment levels in 2014 were remarkable; they were the highest amount since 2000, and the third-highest ever at $48 billion. Th is compares with $30.1 billion in 2013 which was more in line with the prior several years. “Healthcare venture investment in biopharma, device, and dx/tools companies accounted for 18% of all venture capital dollars invested in 2014 compared to 22% a year earlier. Th e dip resulted from the exponential growth in venture investment overall not from a decline of interest in the sector. In fact, healthcare venture investment rose 30% to $8.6B, the highest level in seven years.”

9S. Jordan AssociatesLife Sciences Business Development & Finance

And corporate venture capital played a major role in funding companies. Corporate venture investment dollars increased 69% in 2014 and deployed an estimated $5.3 billion into 766 venture rounds creating the highest investment total by far in the post-millennium period. Th is trend is refl ective of the high dependence by corporate partners on outside innovation to sustain their own growth objectives (“External R&D”). Interestingly companies receiving corporate venture invest-ments have a ~60% higher rate of licensing deals, M&A, and IPOs. (Source: Bruce Booth, “Want Better Odds? Get a Pharma Corporate VC to Invest,” Forbes, 5/22/12)

2014 is the seventh consecutive year — and the 12th in the past 14 years — in which more money was invested by the industry than raised in new commitments. Although this trend clearly illustrates the appeal among investors for venture capital investments, this imbalance is not sustainable. Over time, in order to sustain innovation and growth — along with superior investment returns which accompany them, either.

1. More capital must be raised, OR2. New investment models must be created

Source: Jonathan Norris/Kristina Peralta, “Trends in Healthcare Investments and Exits 2015” Silicon Valley Bank

10S. Jordan AssociatesLife Sciences Business Development & Finance

ExitsOnce successful portfolio companies mature, venture funds generally exit their positions in those companies by taking them public through an IPO or by selling them to presumably larger organizations (acquisition, trade sale or, increasingly, a fi nancial buyer). “Exits” are critical for generating investment returns for capital providers who oft entimes recycle capital back into more healthcare companies and in recent years this capital cycle has been robust.

In 2014, 83 venture-backed healthcare companies went public, the highest count since the post-2000 bubble. Add in the 37 IPOs in 2013 and these companies now account for $60 billion in aggregate market value. Interestingly, as was atypi-cally the case in 2013, many IPOs were early-stage biotechnology companies.

Despite the higher totals counts than recent years, the overall scope of the IPO market is considerably less than it was in the 1990s when 14% of fi rst fundings eventually went public.

Healthcare M&A still accounts for a large percentage of “exit” activity of any size. (Source: Bruce Booth, “Acquisitions As the Silent Partner in Biotech Liquidity: IPO Vs. M&A Exit Paths,” Forbes, 10/27/1014)

Source: Jonathan Norris/Kristina Peralta, “Trends in Healthcare Investments and Exits 2015,” Silicon Valley Bank

11S. Jordan AssociatesLife Sciences Business Development & Finance

ReturnsDuring the past 5 years, investment returns for the Venture Capital asset class have returned to the peak of the risk-reward scale. Th e Cambridge Associates U.S. Venture Capital Index® climbed 2.4% and 10.8%. For comparison, the S&P 500 was up 1.1% and 8.3% for the quarter and YTD, respectively. Q3 marked the ninth consecutive quarter of positive returns for the private equity benchmarks and the 12th consecutive quarter for venture capital.

12S. Jordan AssociatesLife Sciences Business Development & Finance

Investment Thesis: The Global Healthcare IndustryOver the last decade the healthcare industry has experienced signifi cant innovation, reform and expansion, which in turn has created a catalyst for continued business formation and growth. Venture capital investors thrive in such environments and healthcare, broadly speaking, is one of the most dynamic sectors in venture capital investing. Th ese circumstances will allow venture capital investors to help bring novel, innovative, and profi table healthcare technologies to market while generating superior returns for their stakeholders.

Healthcare Investment Environment

Th e healthcare venture capital industry can be classifi ed into several sub-sectors. Each of these sub-sectors is character-ized by unique strategic and investment dynamics and is aff ected diff erently by the macro-environment in ways that can be exploited by astute investors:

Th e demand characteristics for each sub-sector is driven by a unique combination of the aging U.S. demographics, advances in medical care and technology, and changes to the current regulatory environment. Th e profi tability of indi-vidual companies is largely dependent on their ability to create innovative and disruptive technologies while maintaining effi cient operations.

13S. Jordan AssociatesLife Sciences Business Development & Finance

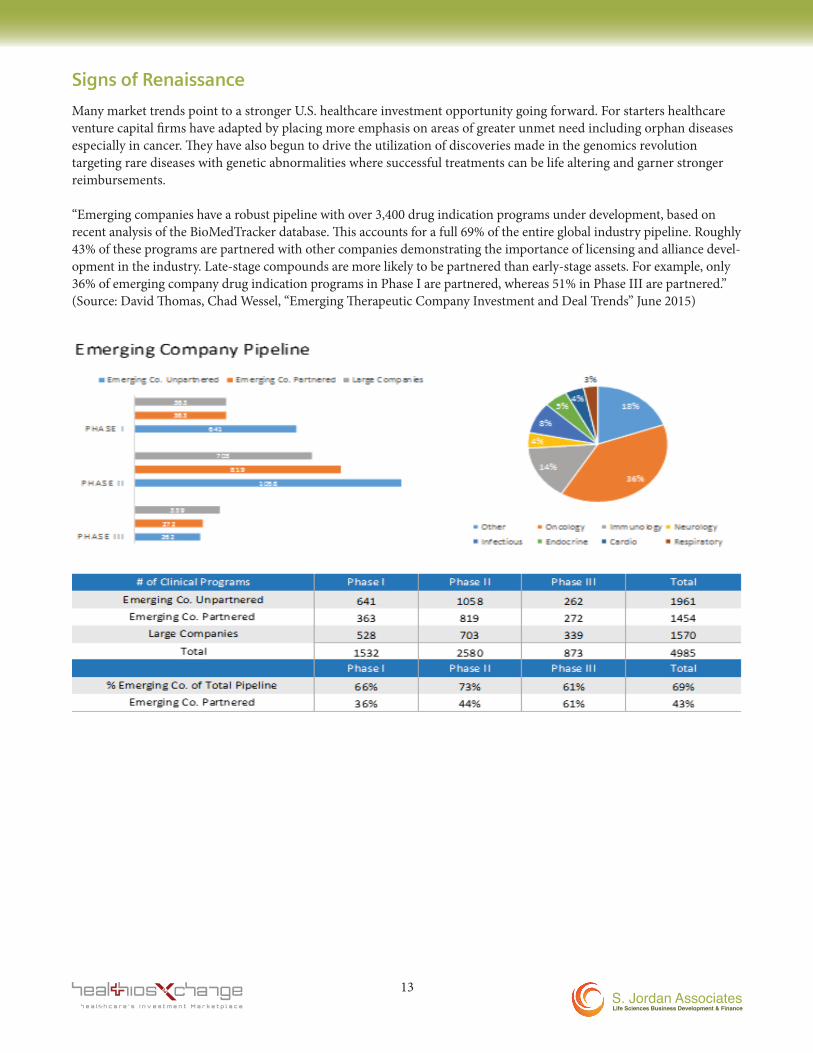

Signs of Renaissance

Many market trends point to a stronger U.S. healthcare investment opportunity going forward. For starters healthcare venture capital fi rms have adapted by placing more emphasis on areas of greater unmet need including orphan diseases especially in cancer. Th ey have also begun to drive the utilization of discoveries made in the genomics revolution targeting rare diseases with genetic abnormalities where successful treatments can be life altering and garner stronger reimbursements.

“Emerging companies have a robust pipeline with over 3,400 drug indication programs under development, based on recent analysis of the BioMedTracker database. Th is accounts for a full 69% of the entire global industry pipeline. Roughly 43% of these programs are partnered with other companies demonstrating the importance of licensing and alliance devel-opment in the industry. Late-stage compounds are more likely to be partnered than early-stage assets. For example, only 36% of emerging company drug indication programs in Phase I are partnered, whereas 51% in Phase III are partnered.” (Source: David Th omas, Chad Wessel, “Emerging Th erapeutic Company Investment and Deal Trends” June 2015)

14S. Jordan AssociatesLife Sciences Business Development & Finance

Th is is not surprising as many large pharmaceutical companies have signifi cantly pruned their research and development staff and expenses and seem to view smaller biotechnology companies, many VC-backed, as “outsourced R&D.” With the predicted patent cliff of Big Pharma now a current reality, and with many of the larger biotechnology companies aggres-sively participating in acquisitions, we expect this favorable M&A environment to continue.

A Great Time to Be a Healthcare Investor

Several underlying factors lead us to believe that the recent positive trends in healthcare are sustainable. One major trend is demographics. Research by the Centers for Medicare and Medicaid Services shows that healthcare spending is projected to grow at an average rate of 5.8 percent from 2012-2022, 1.0 percentage point faster than expected average annual growth in the GDP. It also states that at a projected sum of $5 trillion dollars, healthcare spending will be 19.9 percent of the GDP by 2022. A large part of this anticipated growth is driven by population growth and the aging of America. Furthermore, the advancement in medical innovations, especially the fruits from deciphering the human genome, is only in its early chapters. According to the National Human Genome Research Institute, it cost $100 million to sequence a genome in 2000. Th at cost has been cut exponentially in just the last fi ve years and is now below $10,000.

As gene-based drugs, testing and services have gained traction, investors have taken note. In a report issued by venture capital database Pitch Book, it is stated that capital invested in genomics-related companies roughly tripled from 2008 to 2012, expanding from $269 million to $760 million. We are optimistic that over the next few years several diseases, including certain cancers and inherited genetic diseases, will be treated by manipulation of genomic material in-vivo or ex-vivo causing a paradigm shift in the annals of therapeutics akin to the introduction of penicillin to treat infections.

2014 was also the best exit year for VC-backed biopharma companies over the past decade… “the value both in terms of up fronts and full “biobuck” potential have reached new highs topping over $5 and $8 billion, respectively.” (Source: “HBM Pharma/Biotech Report 2014,” and Bruce Booth, “Data Snapshot: VC-Backed BioPharma M&A 2014”)

15S. Jordan AssociatesLife Sciences Business Development & Finance

Finally, the potential eff ects of the landmark regulatory overhaul known as the Aff ordable Care Act (ACA) have only begun to surface. Th e changes in the regulatory environment brought by the ACA will likely create opportunity for services that reduce costs or manage resources more effi ciently; on the other hand, it may adversely impact the pricing power of pharmaceutical companies given the streamlining of care and the increased power of the counterparties they negotiate with as more providers bear risk for costs through accountable care organizations and other integrated health-care delivery models. According to the Centers for Medicare and Medicaid Services, by 2022 the ACA is projected to reduce the number of uninsured people by 30 million, add approximately 0.1 percentage-point to average annual health spending growth over the full projection period, and increase cumulative health spending by roughly $621 billion. Th e revolution in healthcare delivery from this Act will provide opportunities (as well as challenges) for all areas of health-care investing.

Out of the Ashes: Re-Inventing VCNotwithstanding recent resurgence in performance and the accompanying growth in both capital commitments and the number of funds, fundamental questions persist as to the durability — and integrity — of Venture Capital.

In fact, it was not long ago that the entire viability of the VC asset class was being questioned:

■ A Tsunami Rips Th rough the Venture Industry■ Why Venture Capital is Broken■ Th e Death of Venture Capital As We Know It■ Venture Must Re-Invent■ VC Is Too Fat, and Returns are Too Th in■ Honey, I Shrunk the VC’s

Th e ills which plague VC cannot be cured by a single “Bull” market. As illustrated by a landmark study published in 2012 by the Kauff man Institute which evaluated the performance of 100 VC funds over a 20-year period — including several “boom” and “bust” cycles — the entire process of growth capital investing must still be re-aligned in order to succeed.

Among the key fi ndings of the Kauff man report are the following:

■ Only twenty of 100 venture funds generated returns that beat a public-market equivalent by more than 3 percent annually, and half of those began investing prior to 1995

■ Th e majority of funds—sixty-two out of 100—failed to exceed returns available from the public markets, aft er fees and carry were paid

■ Only four of thirty venture capital funds with committed capital of more than $400 million delivered returns better than those available from a publicly traded small cap common stock index

■ Of eighty-eight venture funds in our sample, sixty-six failed to deliver expected venture rates of return in the fi rst twenty-seven months (prior to serial fundraises). Th e cumulative eff ect of fees, carry, and the uneven nature of venture investing ultimately left us with sixty-nine funds (78%) that did not achieve returns suffi cient to reward us for patient, expensive, long-term investing.

16S. Jordan AssociatesLife Sciences Business Development & Finance

Based on the conclusions on their report, the Kauff man Foundation made the following recommendations for investors regarding the future of growth capital investing:

■ Invest directly in a small portfolio of new companies, without being saddled by high fees and carry■ Co-invest in later-round deals side-by-side with seasoned investors■ Invest in VC funds of less than $400 million with a history of consistently high public market equivalent

(PME) performance, and in which GPs commit at least 5% of capital■ Move a portion of capital invested in VC into the public markets. Th ere are not enough strong VC investors

with above-market returns to absorb even our limited investment capital

As the pace of global innovation accelerates and economies around the world depend increasingly on growth, a vibrant venture capital industry will be vital to securing the future. Th is sentiment is the subject of a recent study by PWC, which predicts global alternative assets will increase to US$15.3 trillion by 2020. Among the fi ndings of the PWC study are:

■ Rapid developments in the global economic environment have pushed asset management to the forefront of social and economic change

■ An important part of this change – the need for increased and sustainable long-term investment returns – has propelled the alternative asset classes to a more prominent role in the investment management industry.

■ Th e global alternative asset management industry is expected to experience a transformation as alternative asset managers transform their business and operations and make technology a top investment priority

Th e impending transformation in alternative asset management will have far-reaching eff ects on medical innovation and the global healthcare capital markets. For each of the participants, the impact of these transformations will change the manner in which they do business.

17S. Jordan AssociatesLife Sciences Business Development & Finance

(source: Preqin)

■ 92% of investors expect to either “Increase” or “Maintain” their allocations to Venture Capital and Private Equity over the long term

■ 55% of Limited Partners with fund investments in healthcare identifi ed management fees as the principal motivation for a shift in investment strategies. In addition, investors cited better control of investments, greater transparency, and an opportunity to increase diversifi cation.

■ 77% of Limited Partners are “Actively” or “Opportunistically” engaging in Direct Investments■ 24% of LPs allocate more than 10% of AUM to Direct investment. By 2016, Direct investments will increase by

50% to 15% of AUM■ 86% of Limited Partners assert that Direct Investing yields either “Signifi cantly Better” or “Slightly

Better” returns■ 87% of Limited Partners intend to “Increase” or “Maintain” their Direct investment activity during the

next fi ve years

Going DIRECT: A New Paradigm in Healthcare Venture Capital Investing

Th e recent Preqin Private Equity Survey was completed in June 2014. It studied 1,176 Limited Partners (“LPs”) world-wide with principal investment focus in a range of alternative asset classes.

Following is a summary of the principal fi ndings from the Preqin survey:

18S. Jordan AssociatesLife Sciences Business Development & Finance

Confronting Risks – Direct Investing Venture Capital investing provides LPs with the potential benefi t of outsized returns that beat public markets and the ability to fund novel ideas, but it does not come without risk. From illiquidity to improper valuation, being able to successfully navigate and manage these risks is key to generating positive returns. Investing directly can help strategic LPs mitigate and temper these risks. (Source: “Making Waves: Th e Cresting Co-Investment Opportunity,” 2015, Cambridge Associates, 2015) Inherent risks include:

DIRECT CO-INVESTING REQUIRES THE RIGHT SKILLSET

“Investors considering direct co-investments should determine whether they have or would like to add the appropriate skills in-house, work with advisor, or would prefer to outsource the activity entirely to an advisor or fund manager.”

ONE MUST FIND ONE’S OWN CO-INVESTMENTS

“Direct co-investors must regularly remind target GPs of their interest to see suffi cient and attractive deal fl ow. Even then, access can be challenging when many others are competing for the same opportunities.”

TIMING IS UNPREDICTABLE

“GPs are likely to syndicate co-investments to their investors when capital accessible via their main funds is low.”

APPROVAL IN “30 MINUTES OR LESS”

“Once a GP decides to pursue an investment, interested co-investors may have as little as two weeks to review available information, conduct their own assessment of the opportunities, decide whether to participate, and then secure internal approval.”

FINDING A PEARL….OR JUST AN OYSTER

“Direct co-investors off ers investors the potential — by no means guaranteed — to try their hand at selecting which of a GPs co-investment opportunities will outperform, and to add exposure there.”

TOO GOOD TO BE TRUE

“Even with fund dynamics making co-investments available, investors should be cognizant of adverse selection risk, including the possibility that managers may, knowingly or not, be sharing their less attractive opportunities.”

Th ough inherent risks remain, “the strategy’s popularity has grown as institutional investor increasingly seek ways to invest more private capital with select GPs at a reduced cost, oft en at more than half-off the prevailing cost of access. (Source: “Making Waves: Th e Cresting Investment Opportunity, Cambridge Associates, 2015) Increasingly, GPs are off ering more co-invest diff erentiating themselves from the LP community, deepening relationships with key investors, managing their own risk, and maintaining greater fl exibility for themselves.

19S. Jordan AssociatesLife Sciences Business Development & Finance

Summary of the advantages associated with “Direct” investing vs. through venture capital (GP) funds.

RISKS OF VENTURE Summary Description The DIRECT Investment Solution

Illiquidity Capital Velocity / Access to Cash■ Reduce investment horizon ■ Create “Evergreen” fund mechanism

Adverse Selection

“Investors should be cognizant of the possibility that managers may be sharing their less attractive opportunities.”

– Cambridge Associates

■ Establish stringent investment criteria – “Rule Set” – stipulating that every Direct investment be subject to leadership from new, third-party institutional investor

Diversifi cation Achieving a Portfolio Effect ■ Invest at same rate as top-decile GPs

Correlation Targeting pure “Alpha” ■ # of General Partners, multiplied by the # of

institutionally-backed portfolio companies, equals the potential for non-correlated IRR.

VolatilityExtreme dispersion of returns on company-by-company basis

■ Eliminate “J-Curve” ■ Mitigate “downside” through deal selection

based on “Rule Set”■ 65.3% of Standard Deviation of Returns in

VC due to “upside” events

Performance Generating superior IRR / MOIC■ No Fee, No Carry. ■ Gross Return = Net Return

Scalability of Venture Capital

“At fund sizes greater than $200 million, performance suffers”

– Kaufmann Foundation

■ (900) direct transactions■ $11 billion opportunity

Access to Best Managers / GPs

“Increasingly challenging to get into top tier funds since VC funds are getting smaller and access is limited.”

– National Venture Capital Association

■ Broad exposure to top-tier funds■ ‘Dating Prior to a Marriage’■ Eliminating the effect of fees and carried

interest enables greater universe of GPs to achieve top-decile Gross IRR

Valuation

“As early-stage investors seek to preserve their positions in compa-nies in early rounds of fi nancing, venture co-investments are more often offered at late-stage rounds when they may also be subject to high valuations.”

– Cambridge Associates

■ Every direct investment made on “pari passu” basis, subject to discrete, independent pricing as established by new institutional “Lead” investor with like-minded return expectations

“Zeros”High loss ratios associated with write-offs

■ Single Purpose Investment Vehicle (“SPV”) permits diversifi cation, attenuates impact of losses, preserves return profi le of portfolio

Inconsistent Cash Flows

“Cash fl ows from venture capital are lumpy.”

– Preqin

■ Continuous distributions upon “exit” of each discrete portfolio company

■ Continuous liquidity following investment period of initial portfolio companies

Relationship with GPs

“GPs assume signifi cant reputa-tional risk with their investors when offering co-investment opportuni-ties. Poor interactions with LPs and poor results could cost future fund commitments.”

– Coller & Company

■ Third-party, “Arms-Length” structure ■ Deal-by-Deal decision making

S. Jordan AssociatesLife Sciences Business Development & Finance

S. Jordan AssociatesLife Sciences Business Development & Finance

Scott Jordan312.451.6210

For more information, contact: