rational expectations and the aggregation of diverse information in laboratory security markets...

TRANSCRIPT

Rational Expectations and the Aggregation of Diverse

Information in Laboratory Security Markets

Charles R. Plott, Shyam Sunder

• Information aggregation in the market when traders have divers information about an underlying state of nature – no trader knows the state of nature with certainty, but if they pool their information, traders can identify the state with certainty

• Rational expectations models suggest that markets might aggregate information even though traders are unable to communicate directly (and have no incentive to unilaterally reveal what they know)

• Three series of experiments to test the theory of rational expectations– Single asset market with diverse preferences and dividends

contingent on the state of nature– 3-asset market with state-contingent securities (Arrow-Debreu

securities)– Single asset market with identical preferences

Information structure

• Three possible states of nature: x, y and z• At the beginning of each period, the state

of nature was drawn from a publicly known distribution P(θ), θ in {x,y,z}

• If the state was, say, x, then half of the traders were told that the state was not y and the other half that the state was not z

• The number of informed traders and the type of information were both public

• Series A – diverse dividends (1,2,3,6,10,11, 4-S, 5-S)

• Series B – state-contingent claims (4-CC, 5-CC)• Series C – uniform dividends (7,8,9)• The differences in dividends and expectations

about the state of nature led to existence of gains from trade

• Trader i’s payoff

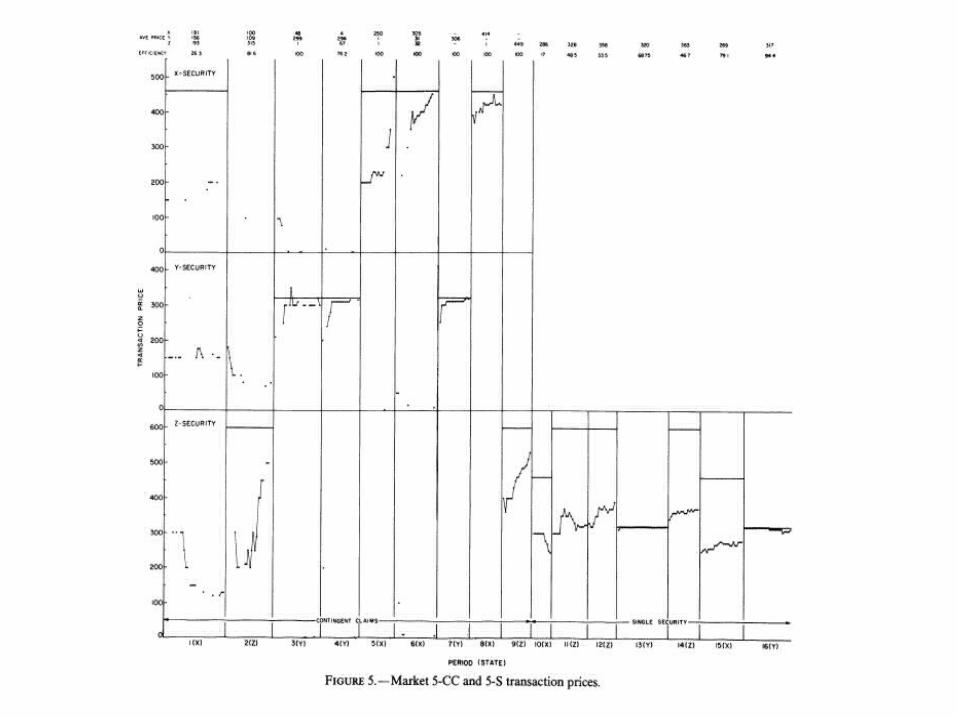

• The contingent claims market had three different securities, denoted, for convenience, also x,y and z

• θ-security yielded a positive dividend if the state θ occurred and zero otherwise

• Notice that a portfolio of one of each typo of security is equivalent to a portfolio of one security in the single security markets

Contingent securities

Competing models of security behavior

• The Rational expectations model (RE): all traders choose in equilibrium as if they are aware of the pooled information of all traders in the system

• In any given state the equilibrium price is the highest dividend in that state and the securities are held by the traders who have that high dividend potential

• The Prior Information model is based on 3 principles– traders apply Bayes law to update the

common prior on the state of nature using their private information

– the traders act on the probability so derived– traders are the expected utility maximizers

• Model’s prediction in our setting – the price of an asset will be equal to the expected value to the trader whose prior information about the state leads to the highest expected value across all traders

• The Maximin model assumes that traders act only on certainty

• The traders will not purchase a security unless the price is below the minimum they could possibly receive given their prior information

• The model’s prediction – the trader with the maximum (across all traders) of minimum (across all states) dividend will purchase the security and the price will be equal to this dividend

Results and conclusions

• In the single security markets with diverse preferences (Series A) the price predictions of the RE model do not perform well relative to the performance of the price predictions of the PI or MM models

• If the markets are complete (Series B) of if preferences are identical (Series C), the RE price predictions outperform the PI and MM models

• Allocation and profit predictions: In all markets, allocations aggregated over the final occurrence of each state and the distribution of profits are more accurately predict by the RE model than either the PI or MM models

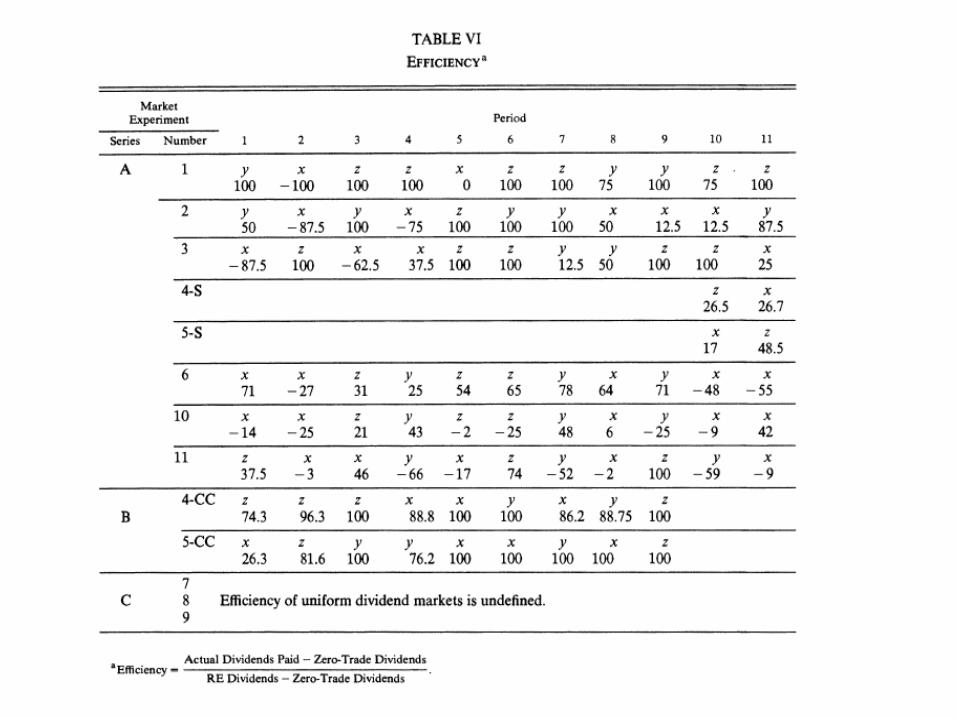

• Efficiency (defined for these experiments) is at 100% if and only if the total earnings of all traders are the maximum possible given the particular state that occurred (this just means that the traders that have the highest dividends should acquire the securities)

• The other reference point for efficiency is when dividend payments are the same as if no trades happened in the period (and then the efficiency is set to zero)

• Efficiency in the single security market are low relative to the contingent claims market

• The RE model is the least accurate predictor for the efficiency of Series A markets

• If information is perfectly aggregated, the markets should operate at 100% efficiency

• If information fails to be aggregated, then resources should be allocated according to the PI model in which each trader is risk neutral and acts on privately received information alone

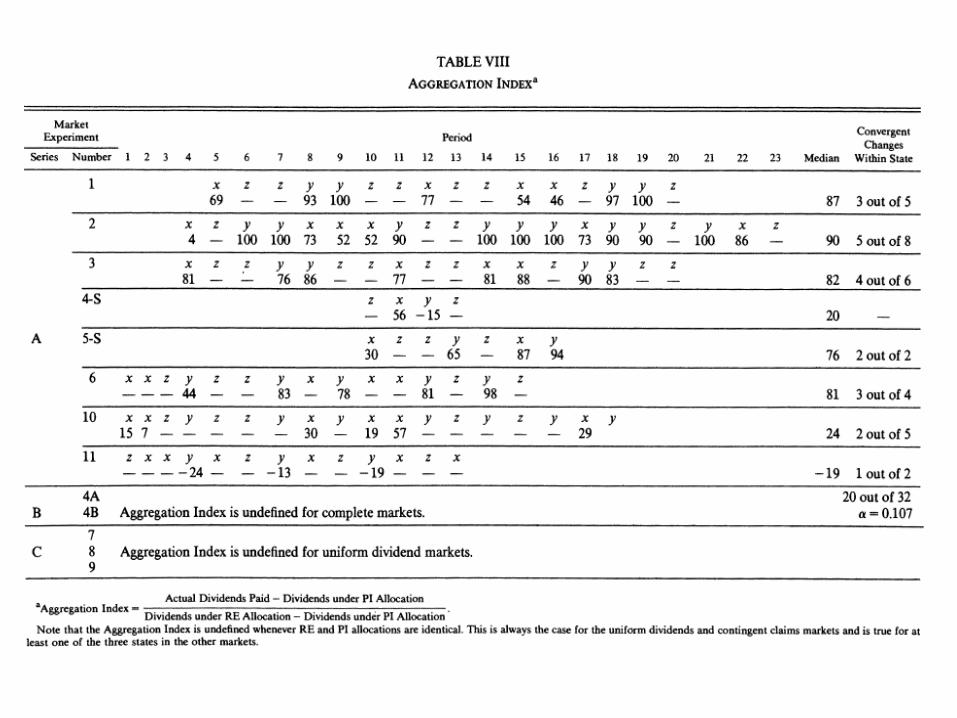

• Information aggregation is measured in the same way as efficiency, except that the lower benchmark is not the no-trade case, but rather the PI model prediction

• Information aggregation occurred in all markets, except one. Aggregation improved in later periods

The role of bids in Contingent Claims markets

• Hypothesis 1. The opening action in a market period is an offer to sell a contingent claim corresponding to one of the two states that has not occurred and is made by a trader who has prior information that the corresponding state has not occurred

• Under the null hypothesis that the opening action could happen in any of the three markets, the probability of the event described in Hypothesis 1 would be 1/5

• It’s observed in 12 out of 18 cases, so the null is rejected

• Hypothesis 2: The first action in the "state" market is a bid (to buy)

• Because the first action can either be a bid or an offer, under the null hypothesis that the opening action in the true state market is purely random, the probability of the event described in Hypothesis 2 would be 0.5. The null is again rejected at the α=0.001 level

• Conjecture: Prior experience of traders with the RE phenomenon is not a sufficient condition for the single security market to arrive at the RE equilibrium

• Conjecture: The increase in the number of trader types does not improve the RE formation process

• Conjecture: Volume increases do not facilitate RE price formation

Other variables

Why do contingent claims markets aggregate information better?

• The first possible explanation: the single security markets are slow to adjust and that, given more time, these markets too will behave as predicted by the RE model

• The second explanation: the message space is larger in the contingent claims markets, in the sense that three sets of bids/offers/prices are available to traders

• The third explanation: the type of information implicit in the structure of the contingent claims - a security paid a positive dividend only if a state occurred and paid zero otherwise, so the purchase or sale of a security could be directly interpreted as a belief about the occurrence of a particular state