introduction to financial analysis shyam sunder yale school of management september 12, 2012

TRANSCRIPT

Introduction to Financial Analysis

Shyam SunderYale School of Management

September 12, 2012

2

An Overview

• The opportunity sets • Business model

– Resource flows, technology, and strategy• How Far to look• Gathering Financial data• Financial manipulations, Shenanigans• Assessing and deciding• What to expect

3

Opportunity Set?

• What is the range of investment opportunities you wish to consider?– Corporate and government securities (e.g., stocks, bonds,

derivatives)– Commodities, currencies, their futures and derivatives– Land, housing, and other real estate (and related

securities)– Art, antiques, and collectibles– Other– Limit discussion today to equities

Business Model

• Independent of what you choose to analyze, you always have to identify, understand, and build the “business model” of the investment opportunity you wish to analyze

• What do we mean by business model?– Understand how the investment works

• Let us start with equity investment in a business firm

4

04/19/23 Sunder, Good Management 5

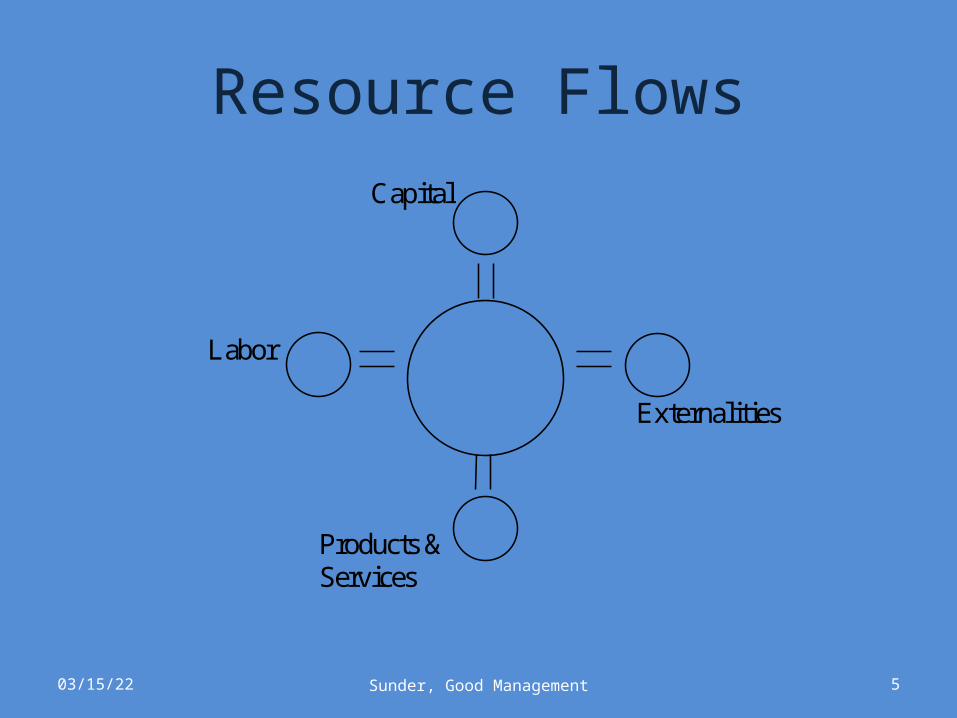

Resource Flows

Capital

Labor

Products & Services

Externalities

“Production Technology”• What is the “technology of producing” output from

inputs (include products and services)?• Plant investment, fixed and variable costs of plant• How does this “technology” compare with others?• What have been the changes in past? Prospective

changes? In the firm and in the industry?• Likely consequences of these changes for the

resource flows?

6

For Each Class of Resource Flows• Identify each significant resource• Estimate the volume or resource flows• Identify existing terms of exchange (price, volume,

elasticity)• Identify market conditions (competition, growth, new

technologies, price sensitivity, etc.)• Characterize the counterparties (the other side)• Identify potential changes, disruptions, innovations• Identify flexibility, substitutability, vulnerability• New ideas for improving terms of exchange, reducing

vulnerability by restructuring

7

Capital Flows• Common equity• Preferred equity• Bonds• Bank debt• Other borrowing (including private)• What combination of sources of financing?

– Domestic or foreign, currency denomination?

• At what cost and what risk?• New ideas?

8

Labor

• Managerial: skills, quality, work culture, price, mobility

• White collar: skills, quality, work culture, price, location

• Blue collar: Education and skills, quality, work culture, price, location, flexibility

• Fixed and variable components of labor costs

9

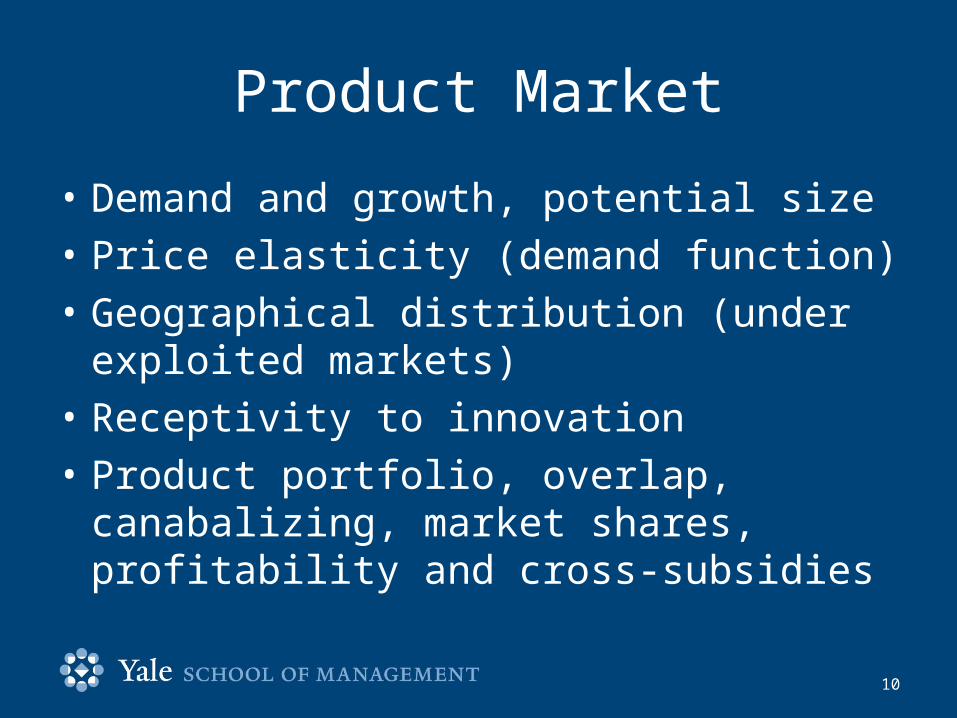

Product Market

• Demand and growth, potential size• Price elasticity (demand function)• Geographical distribution (under exploited

markets)• Receptivity to innovation• Product portfolio, overlap, canabalizing,

market shares, profitability and cross-subsidies

10

Vendors

• Supply chain (diversification, competition, vulnerability to disruption)

• Competitive conditions • Ownership and commitment• Geographic distribution• Potential for growth in volume• Pricing• New ideas: make-or-buy decisions

11

Externalities

• Resource flows which are not priced• Most difficult part of analysis of business

model• Difficult to price does not mean not important• Examples?

12

Strategy

• What is firm’s strategy with respect to – Technology– Products– Financiang– Labor– Supply chain– Generating profits and growth

13

14

How Far Do You Look?

• Do you know when you would want to exit (cash out) your investment?

• If not, how uncertain are you?• How much flexibility do you have in your time

horizon?

15

Gathering Financial Data• 10-K:

– auditor’s report: absence of opinion, qualified report, reputation of auditor, audit committee (independent directors act as intermediary with auditors)

– Footnotes: accounting policies / changes (in policies or estimates), review inventory valuation, (LIFO vs. FIFO / specific id) (except technology), revenue recognition (after sale vs. At sale with risk remaining), depreciation (accelerated vs. Straight line), estimate of warranty (high vs. Low), estimate of bad debts (high vs. Low), treatment of advertising (expense vs. Capitalize), loss contingencies (accrue loss vs. Footnote only), pending or imminent litigation (Item 3, better than footnote in annual), long term purchase commitments (at what price?)

– Industry specific notes– Segment information (showing unhealthy segment)– Management discussion and analysis– Specific concise disclosures liquidity, capital expenditures, candor– consistent with footnotes

16

More Financial Data• Annual Report: president’s letter, forthright vs. Always upbeat• Proxy (for annual meeting): litigation, executive

compensation• Turnover of management• Related party transactions• 10-Q: unaudited, consistency with 10-K• 8-K (special events): auditor changes, disagreements over

accounting policies (opinion shopping), change in control of the company, acquisitions, dispositions, resignation of directors, bankruptcy

• Prospectus• Past performance• Quality of management and directors• Conference calls, market history, industry reports, personal

experience with products and services of the firm

17

Things to Watch for

• Executive incentives which encourage managing financial statements

• Poor internal controls• Quarterly financial statements (they are not audited)• Companies with weak control environment (board of

directors is not independent; auditors not independent)• Management facing extreme competitive pressure• Management with questionable character• Fast growth companies whose real growth is beginning to

slow• Basket case companies struggling to survive• Newly public companies• private companies (especially those which aren’t audited)

18

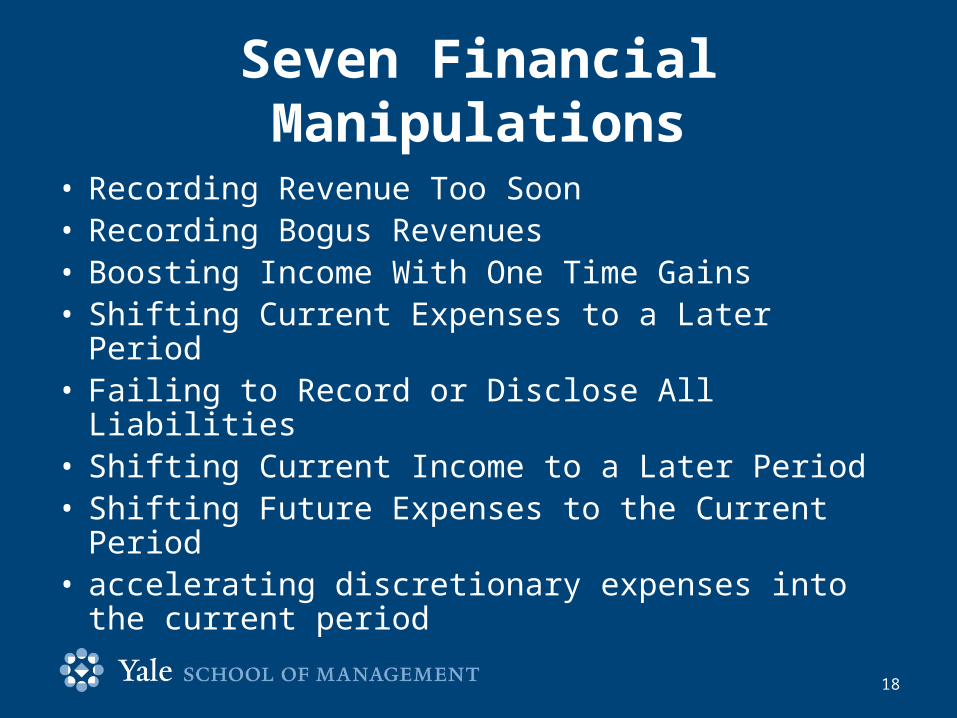

Seven Financial Manipulations

• Recording Revenue Too Soon• Recording Bogus Revenues• Boosting Income With One Time Gains• Shifting Current Expenses to a Later Period• Failing to Record or Disclose All Liabilities• Shifting Current Income to a Later Period• Shifting Future Expenses to the Current Period• accelerating discretionary expenses into the current

period

19

Assessing What You Find

• Valuation models: choices, triangulation• When you find an over or under-valued

security, ask yourself– Did others miss something that I know?– Did I miss something that other know?

• Is the market efficient? If so, how efficient?

20

Deciding on investment

• Have I found something which is mis-priced?• Do I understand why it is mispriced?• Does investment in this opportunity fit my

goals, investment horizon, and constraints?• What is the worst that can happen with this

investment? Can I live with that?

21

Was that a good investment or bad?

• Learning from post mortems• Why did that investment work, or did not

work?• What did I learn from this experience?

22

What should You Expect?• You are competing with a lot of other smart people• Most of us cannot expect to be the winners all the

time• If your winning average is slightly more than 50/50,

you are doing fine• But it takes a long time to find out• Markets makes it tough for the wise to make a lot of

money, and for fools to lose a great deal (index funds will earn you the average anyway)

• So, you better do the hard work of research and understanding before jumping into the investment game

Thank You!