r&d expenditure ecosystem - science policy forum

TRANSCRIPT

CURRENT STATUS & WAY FORWARD

R&D EXPENDITUREECOSYSTEM

JULY 2019

EAC-PM

FOREWORD

EAC-PM

Investments in Research & Development (R&D) are key inputs for economic growth. There is ample empirical evidence to support investment in R&D in view of its impact on productivity, exports, employment and capital formation. Many countries have therefore opted to earmark a certain portion of the national budget towards R&D. Various reports of World Bank, UNESCO and World Intellectual Property Organization (WIPO) reflect the progress in R&D expenditure country wise.

India’s investment in R&D has shown a consistently increasing trend over the years. However, as a fraction of GDP, public expenditure on R&D has been stagnant over the past two decades. It has remained constant at around 0.6% to 0.7% of GDP. This is well below that in major countries such as the US (2.8), China (2.1), Israel (4.3) and Korea (4.2). Public expenditure is not only dominant but also the driving force of R&D spend in the country. This is in sharp contrast to the pattern in most advanced countries where private sector is the dominant force. However, the share of public expenditure in total R&D spend has come down from three-fourths of all expenditures to about three-fifths over the last few years. Further, the Government is not only the primary source of R&D funding but also it is the primary user of these funds. Most strikingly, Government expenditure on R&D is undertaken almost entirely by the Central Government. There is a need for greater participation of State Government and Private Sector in overall R&D spending especially in application-oriented R&D.

With this background, this document has been prepared to give an insight into the various institutional elements of the R&D ecosystem in the country. The objective of this document is threefold. First objective is to address the data gaps in compiling R&D data so that international agencies receive up to date data on R&D in order to reflect India’s true rank globally. Second objective is to examine the expenditure trends in various sectors and their shortcomings. The third and final objective is to lay down the roadmap for achieving the desired target of R&D spend by the year 2022. It is pertinent to mention that the focus of this booklet is on R&D expenditure and not on other outputs of R&D which may be equally important.

The inputs for this document have been derived from various stakeholders including industry, academia and Government. I had chaired three meetings with these stakeholders to ascertain the status of R&D spend and invite suggestions on the way forward. Based on these discussions this document has proposed a host of measures for transforming the R&D ecosystem and increasing the share of R&D in GDP.

I would like to thank Mr B.N. Satpathy, Senior Consultant, EAC to PM and Mr Suneet Mohan, Assistant Consultant, EAC to PM for their vital support in coordinating the development of this document. I would also like to extend a special vote of thanks to Prof. K Vijay Raghavan, Principal Scientific Adviser to the Government of India, to Dr. Arabinda Mitra, Scientific Secretary, Office of PSA and to Shri. J B Mohapatra, Adviser to PSA for their immense support in finalization of this document. I hope this document will open a new chapter in economy-wide mainstreaming of Research and Development in the country.

Ratan P. WatalMember Secretary

Economic Advisory Council to the Prime Minister

I would like to congratulate the Economic Advisory Council to the Prime Minister, its Member- Secretary, Shri Ratan Watal (a former Finance Secretary and cheer-leader for science) and his team consisting of Shri B. N. Satpathy and Shri Suneet Mohan for their efforts in compiling this report on the ‘Research and Development Expenditure Ecosystem: The Way Forward’.

We all agree that the research and development investment leads to disproportionate positive rewards in today’s world. Meeting our sustainable development goals, mitigating the consequences of climate catastrophe, striving for a circular-economy, ensuring health and well- being for our people, conserving biodiversity, ensuring food security, and national security— all these are inalienable components of our ambition to be a US $ 5 trillion economy soon. Rarely has so much been expected and demanded of a large nation in so little time. India’s challenge is to grow economically, lift everyone out of poverty but do so by not exploiting the planet, by not polluting and by not exploiting people. This task is feasible only if science and technology are the fulcrum on which the levers of government and industry rest. When the fulcrum is strong, the levers can lift any weight.

The question, then, is how one can strengthen the fulcrum of science. Invest more in science, is the ready refrain. While total investment in science is a valuable metric, it often hides far more than it reveals. The correlation between percentage of GDP invested in science and economic growth is a correlation. The investment has to be broken up into parts to understand the causal components. This will lead to deciding how we should increase our investment. Where and how does the government invest? What are the components of each funding agency’s investment? By industry? By philanthropy? By state governments? This is the input-end. Next, there is the use of investment. What are the expectations, the responsibilities the accountabilities. Finally, what are the outcomes and impacts of the investments.

India will be 75 years young soon. In 1947, India was a very small country in terms of its science and its economy. Today our scientific enterprise is large and has been a major

PREFACE

Office of the Principal Scientific Adviser to the Government of India

contributor to a large economy. We can feed our people, hundreds of millions have health and well-being, and the consequences of natural disasters have been minimized due to the use of technology. Much, much more remains to be done.

Yet, if we introspect, we might conclude that the whole is less than the sum of the parts and wonderful things have happened despite not paying attention to synergy and collaboration. What if, just what if, the finance ministry, our industry and philanthropy worked together with our ecosystem to strengthen our foundations, enhance our institutions from good to great, impact positively in a focused way on our people and our economy? And, if our scientists and institutions see the government and industry as partners in the future of the country? Miracles can happen. We have seen some examples where such collaboration and synergy have worked well. The development and deployment of a rotavirus vaccine is one example. The nan-science mission is another. We need a thousand such efforts.

We have had over the years, had many small under- powered boats attempting to accomplish big voyages. Today we need more power to the boats, refurbish them and also need to facilitate their movement in the same direction, each in their own manner but together to a common goal. The Watal report charts the seas we are voyaging, tells us about our boats and suggest how we can have them reach our common destination. Kudos to the team. We now have the task to distil their thoughts and go forward.

Prof. K Vijay RaghavanPrincipal Scientific Adviser to the Government of India

BRICS Brazil, Russia, India, China and South Africa

CPSE Central Public Sector Enterprises

CSIR Council of Scientific & Industrial Research

CSO Central Statistics Office

CSR Corporate Social Responsibility

DAE Department of Atomic Energy

DBT Department of Bio Technology

DOS Department of Space

DPE Department of Public Expenditure

DRDO Defence Research and Development Organisation

DSIR Department for Scientific & Industrial Research

DST Department of Science and Technology

EAC to PM Economic Advisory Council to the Prime Minister

EMR Extra Mural Research

ERD Engineering, Research and Development

FDI Foreign Direct Investment

FM Frascati Manual

FY Financial Year

FYP Five Year Plan

GERD Gross Expenditure on Research and Development

GII Global Innovation Index

GST Goods and Service Tax

ICAI Institute of Chartered Accountants of India

ICAR Indian Council of Agricultural Research

ICMR Indian Council of Medical Research

ICT Information and Communications Technology

IISER Indian Institutes of Science Education and Research

IIT Indian Institute of Technology

INR Indian Rupee

2

INSEAD Institut Européen d'Administration des Affaires

IP Intellectual Property

IT Act Income Tax Act

MCA/MOCA Ministry of Corporate Affairs

MeitY Ministry of Electronics and Information Technology

MHRD Ministry of Human Resource Development

MNRE Ministry of New and Renewable Energy

MoEFCC Ministry of Environment, Forest and Climate Change

MoFPI Ministry of Food Processing Industries

MoSPI Ministry of Statistics and Programme Implementation

MoU Memorandum of Understanding

MSME Micro, Small and Medium Enterprises

NDCU Non-Departmental Commercial Undertakings

NIIT National Institute of Information Technology

NISER National Institute of Science Education and Research

NITI National Institution for Transforming India

NSF National Science Foundation

OECD Organization for Economic Cooperation and Development

PPP Purchasing Power Parity

PSA Principal Scientific Adviser

R&D Research and Development

RBI Reserve Bank of India

SAP Systems, Applications and Products

SNA System of National Accounts

SSTP State Science and Technology Programme

STI Science, Technology and Innovation

TDB Technology Development Board

UNESCO United Nations Educational, Scientific and Cultural Organization

WIPO World Intellectual Property Organization

XBRL Extensible Business Reporting Language

Y-o-Y Year on Year

List of Abbreviations and Acronyms

3

BRICS Brazil, Russia, India, China and South Africa

CPSE Central Public Sector Enterprises

CSIR Council of Scientific & Industrial Research

CSO Central Statistics Office

CSR Corporate Social Responsibility

DAE Department of Atomic Energy

DBT Department of Bio Technology

DOS Department of Space

DPE Department of Public Expenditure

DRDO Defence Research and Development Organisation

DSIR Department for Scientific & Industrial Research

DST Department of Science and Technology

EAC to PM Economic Advisory Council to the Prime Minister

EMR Extra Mural Research

ERD Engineering, Research and Development

FDI Foreign Direct Investment

FM Frascati Manual

FY Financial Year

FYP Five Year Plan

GERD Gross Expenditure on Research and Development

GII Global Innovation Index

GST Goods and Service Tax

ICAI Institute of Chartered Accountants of India

ICAR Indian Council of Agricultural Research

ICMR Indian Council of Medical Research

ICT Information and Communications Technology

IISER Indian Institutes of Science Education and Research

IIT Indian Institute of Technology

INR Indian Rupee

INSEAD Institut Européen d'Administration des Affaires

IP Intellectual Property

IT Act Income Tax Act

MCA/MOCA Ministry of Corporate Affairs

MeitY Ministry of Electronics and Information Technology

MHRD Ministry of Human Resource Development

MNRE Ministry of New and Renewable Energy

MoEFCC Ministry of Environment, Forest and Climate Change

MoFPI Ministry of Food Processing Industries

MoSPI Ministry of Statistics and Programme Implementation

MoU Memorandum of Understanding

MSME Micro, Small and Medium Enterprises

NDCU Non-Departmental Commercial Undertakings

NIIT National Institute of Information Technology

NISER National Institute of Science Education and Research

NITI National Institution for Transforming India

NSF National Science Foundation

OECD Organization for Economic Cooperation and Development

PPP Purchasing Power Parity

PSA Principal Scientific Adviser

R&D Research and Development

RBI Reserve Bank of India

SAP Systems, Applications and Products

SNA System of National Accounts

SSTP State Science and Technology Programme

STI Science, Technology and Innovation

TDB Technology Development Board

UNESCO United Nations Educational, Scientific and Cultural Organization

WIPO World Intellectual Property Organization

XBRL Extensible Business Reporting Language

Y-o-Y Year on Year

4

All the global sources of data are in public domain. Out of the six national sources of data, only four data sources i.e. DST, DPE, RBI and Economic Survey are in public domain. The data sources which are not in public domain however have been used for internal analysis. We briefly discuss the salient features of various data sources and the methodology used in data analysis:

1. World Bank: World Bank maintains an online databank of R&D expenditure as a percentage of GDP for each country.

2. United Nations Educational, Scientific and Cultural Organization (UNESCO): UNECSO published a technical paper in 2010 which serves as a guide for conducting R&D surveys for countries starting to measure research and experimental development. This guide provides R&D indicators for evidence-based policy. It maintains data on R&D spend in USD in PPP.

3. World Intellectual Property Organization (WIPO): World Intellectual Property Organization (WIPO), a specialized agency of the United Nations in collaboration with Cornell University, INSEAD publishes the Global Innovation Index (GII) which aims to capture the multi-dimensional facets of innovation by providing a rich database of detailed metrics for 126 economies, which represent 90.8% of the world’s population and 96.3% of global GDP. This is an annual publication. GII 2018 covers 80 indicators out of which five indicators relate to R&D Expenditure known as GERD. The indicators are: Gross expenditure on R&D (GERD), Global R&D companies, average expenditure top 3, GERD performed by business enterprise, GERD financed by business enterprise and GERD financed by abroad. Data on these indicators are included in computing India’s rank in GII.

4. Department of Science & Technology (DST): Aggregate data on R&D spend is disseminated by DST on an annual basis. DST compiles the data through an annual survey of R&D units and

Data used in this document has been sourced from the following sources:

GLOBAL SOURCES NATIONAL SOURCES• World Bank• UNESCO• WIPO

• DST• DPE• RBI• Economic Survey • MoSPI• MCA

NOTE ON DATA SOURCES & METHODOLOGY

5

gives breakup of the compiled data into five sub-segments, namely: Central Government, State Sector, Public Sector, Private Sector and Higher Education Sector. No other official source disseminates aggregate data on R&D spend other than DST.

5. Department of Public Enterprise (DPE): DPE brings out the R&D spend by Central Public Sector Enterprises (CPSEs) on an annual basis through its annual publication titled “Public Enterprise Survey”.

6. Reserve Bank of India (RBI): RBI publishes an annual document titled State Finances – A Study of Budgets. This publication inter-alia covers state wise expenditure incurred on Agricultural Research Education & S&T and Environment incurred by State Governments.

7. Economic Survey 2017-18: Economic Survey provides an analysis of the trends in R&D expenditure. It is covered in Volumes 1 & 2 of the Economic Survey 2017-18.

8. Ministry of Statistics and programme Implementation (MoSPI): MoSPI does not disseminate R&D expenditure data in public domain, nor its shares in GDP. However, for the purpose of this document MoSPI has provided relevant information regarding the methodology for calculation of R&D/GDP share. As per this, the Research and Development Expenditure comprise of expenditure incurred by the Public and Private Corporate Sector as no expenditure is incurred by the Household Sector on R&D. Data for these two sectors are obtained from the following sources:

Data Source:

(i) Public Sector: Data is obtained from analysis of the Budget Documents of the Central & State Governments and in respect of Non-Departmental Commercial Undertakings (NDCUs), it is obtained from their Annual Reports.

(ii) Private Corporate Sector: Data is received from Ministry of Corporate Affairs filed by the Companies under MCA 21. Annually National Accounts Division received the data in respect of approx. 7 lakh companies. Around 30,000 – 40,000 big companies file their return in XBRL format as per mandate and rest of the companies may file their return in non-XBRL format. Non-XBRL companies’ contribution in capital formation and GVA is very less compared to XBRL companies.

9. Ministry of Corporate Affairs (MCA): MCA does not disseminate R&D expenditure data in public domain. However, for the purpose of this report MCA has provided data on R&D spend by companies who file their annual returns in XBRL format.

This note on Data Sources concludes with the following observations:

Data Gaps: R&D Expenditure data on certain indicators of GERD as covered in GII are not available and hence are not included in the overall computation model of GII. Secondly, as indicated earlier R&D data by private companies are not available in public domain. Third, the R&D data relating to Universities and State Governments are not readily available. Fourth, there

6

is also a considerable time lag in collection and dissemination of data on R&D spend. These major data gaps need to be addressed.

Data Variation: It has been found that there is a lot of variation in official data. Data received from DST was cross checked with comparable data received from DPE and MoSPI. It was found that the data from these sources do not match. This variation between official data is due to lack of coordinated efforts to collect data on R&D spend on a composite platform. This variation in the data needs to be addressed.

Notwithstanding these data gaps and data variation, this document presents the aggregate data on R&D spend as received from DST as the underlying trend in R&D spend remains intact irrespective of the data source.

Since all the sources of data are official sources, all are relevant and important, the analysis presented in this document is therefore without prejudice to either of these data sources.

All data and graphs used in this document are provisional and subject to revision based on inputs from stakeholders.

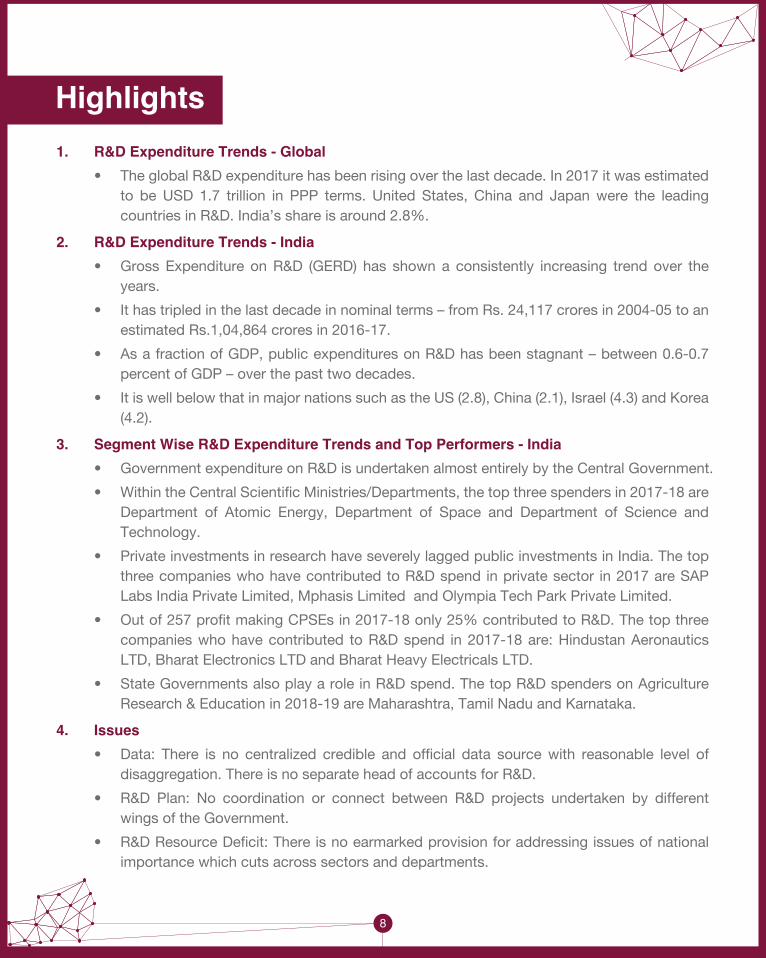

Highlights 1. R&D Expenditure Trends - Global • The global R&D expenditure has been rising over the last decade. In 2017 it was estimated

to be USD 1.7 trillion in PPP terms. United States, China and Japan were the leading countries in R&D. India’s share is around 2.8%.

2. R&D Expenditure Trends - India • Gross Expenditure on R&D (GERD) has shown a consistently increasing trend over the

years.

• It has tripled in the last decade in nominal terms – from Rs. 24,117 crores in 2004-05 to an estimated Rs.1,04,864 crores in 2016-17.

• As a fraction of GDP, public expenditures on R&D has been stagnant – between 0.6-0.7 percent of GDP – over the past two decades.

• It is well below that in major nations such as the US (2.8), China (2.1), Israel (4.3) and Korea (4.2).

3. Segment Wise R&D Expenditure Trends and Top Performers - India • Government expenditure on R&D is undertaken almost entirely by the Central Government.

• Within the Central Scientific Ministries/Departments, the top three spenders in 2017-18 are Department of Atomic Energy, Department of Space and Department of Science and Technology.

• Private investments in research have severely lagged public investments in India. The top three companies who have contributed to R&D spend in private sector in 2017 are SAP Labs India Private Limited, Mphasis Limited and Olympia Tech Park Private Limited.

• Out of 257 profit making CPSEs in 2017-18 only 25% contributed to R&D. The top three companies who have contributed to R&D spend in 2017-18 are: Hindustan Aeronautics LTD, Bharat Electronics LTD and Bharat Heavy Electricals LTD.

• State Governments also play a role in R&D spend. The top R&D spenders on Agriculture Research & Education in 2018-19 are Maharashtra, Tamil Nadu and Karnataka.

4. Issues • Data: There is no centralized credible and official data source with reasonable level of

disaggregation. There is no separate head of accounts for R&D.

• R&D Plan: No coordination or connect between R&D projects undertaken by different wings of the Government.

• R&D Resource Deficit: There is no earmarked provision for addressing issues of national importance which cuts across sectors and departments.

8

• R&D Incentives to Private Sector: The Private sector is playing a secondary role in the Indian R&D ecosystem compared to the Public sector. The reverse is the story in advanced countries.

• R&D Ecosystem in Public Sector: There is no connect between one PSU and another as regards to R&D investment. There is no institutional mechanism to connect PSU investment in R&D and academia.

• R&D in Universities: There is no systematic monitoring or evaluation of R&D projects by an independent unit.

• R&D by State Governments: There is no separate head of account for R&D and there is paucity of funds for research at the State level.

5. Opportunity • With growing globalization engineering R&D market in India is estimated to grow at a CAGR

of 14 per cent to reach US$ 42 billion by 2020.

6. Outcome and Targets • More than Double expenditure on R&D to ~ 2% of GDP by 2022

• India to target 50% of the Global R&D market

• Double R&D Exports by 2022

• Target FDI investment of USD 500 million by 2022

• Aspire to be one of the top ten Global R&D Institutions in emerging technologies

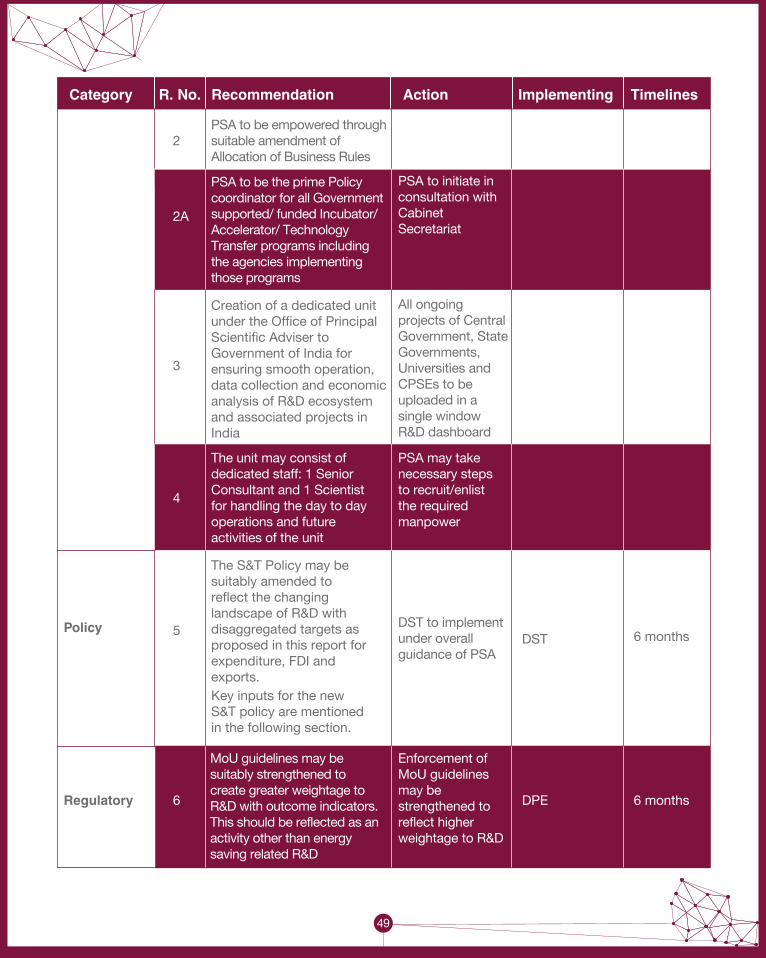

7. Recommendations • The document brings forward 14 recommendations under seven categories namely:

Institutional, Policy, Regulatory, Promotional, Monitoring & Evaluation, Data & Indicators and Tax Incentives with an empowered Office of Principal Scientific Adviser.

9

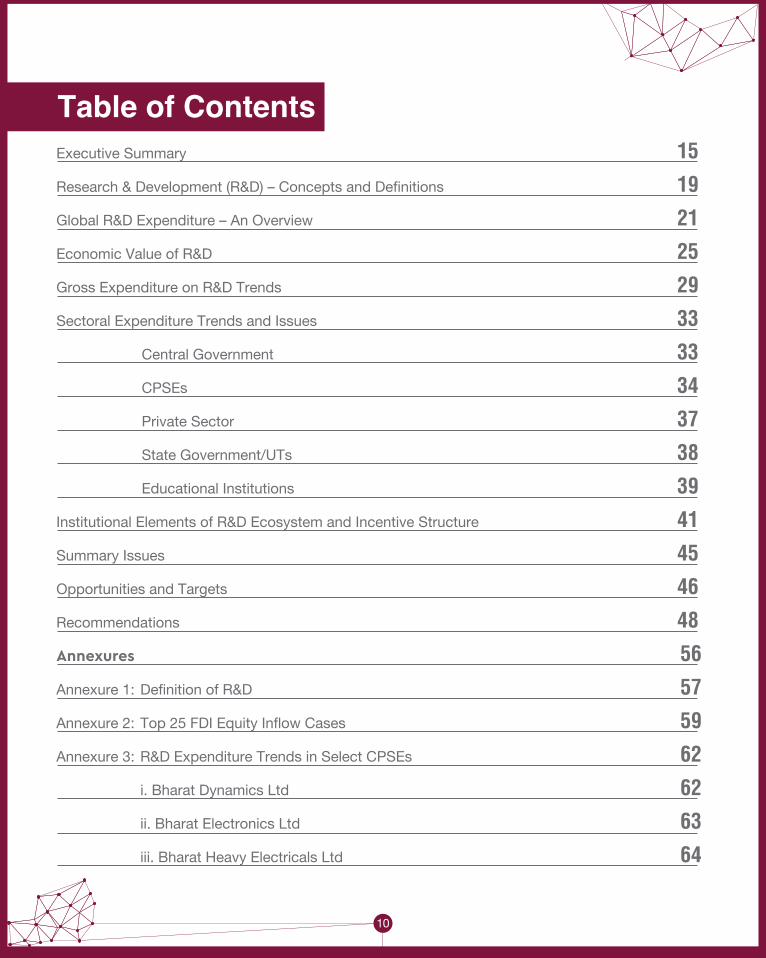

Executive Summary 15

Research & Development (R&D) – Concepts and Definitions 19

Global R&D Expenditure – An Overview 21

Economic Value of R&D 25

Gross Expenditure on R&D Trends 29

Sectoral Expenditure Trends and Issues 33

Central Government 33

CPSEs 34

Private Sector 37

State Government/UTs 38

Educational Institutions 39

Institutional Elements of R&D Ecosystem and Incentive Structure 41

Summary Issues 45

Opportunities and Targets 46

Recommendations 48

Annexures 56

Annexure 1: Definition of R&D 57

Annexure 2: Top 25 FDI Equity Inflow Cases 59

Annexure 3: R&D Expenditure Trends in Select CPSEs 62

i. Bharat Dynamics Ltd 62

ii. Bharat Electronics Ltd 63

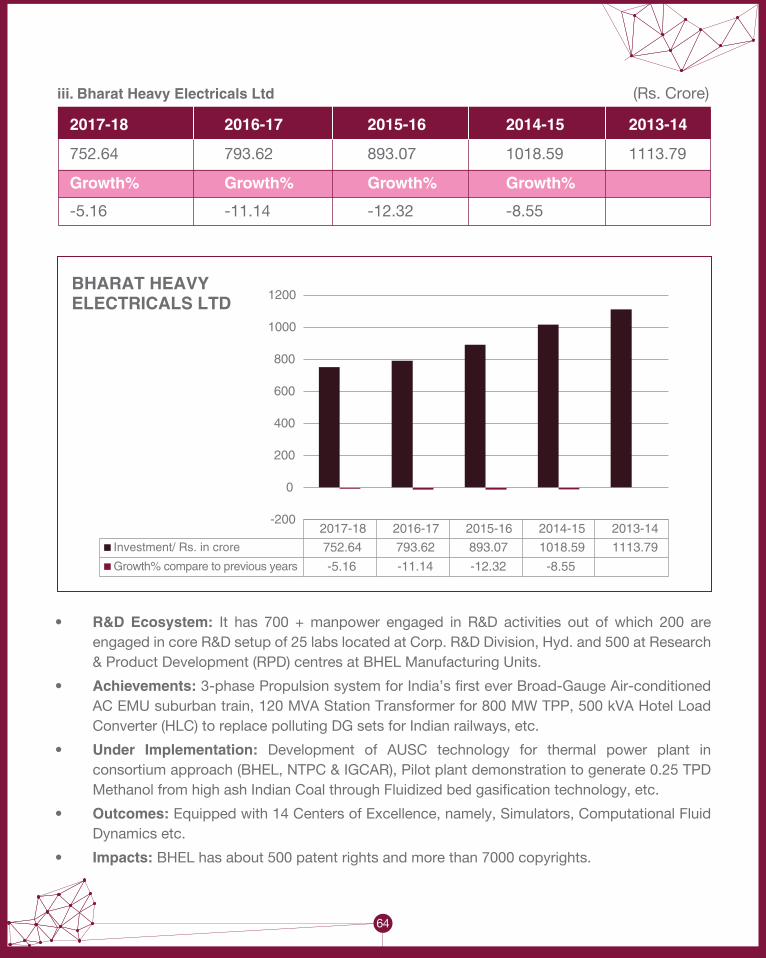

iii. Bharat Heavy Electricals Ltd 64

10

Table of Contents

iv. Electronics Corporation of India Ltd 65

v. ITI Ltd 66

vi. MAZAGON Dock & Shipbuilders Ltd 67

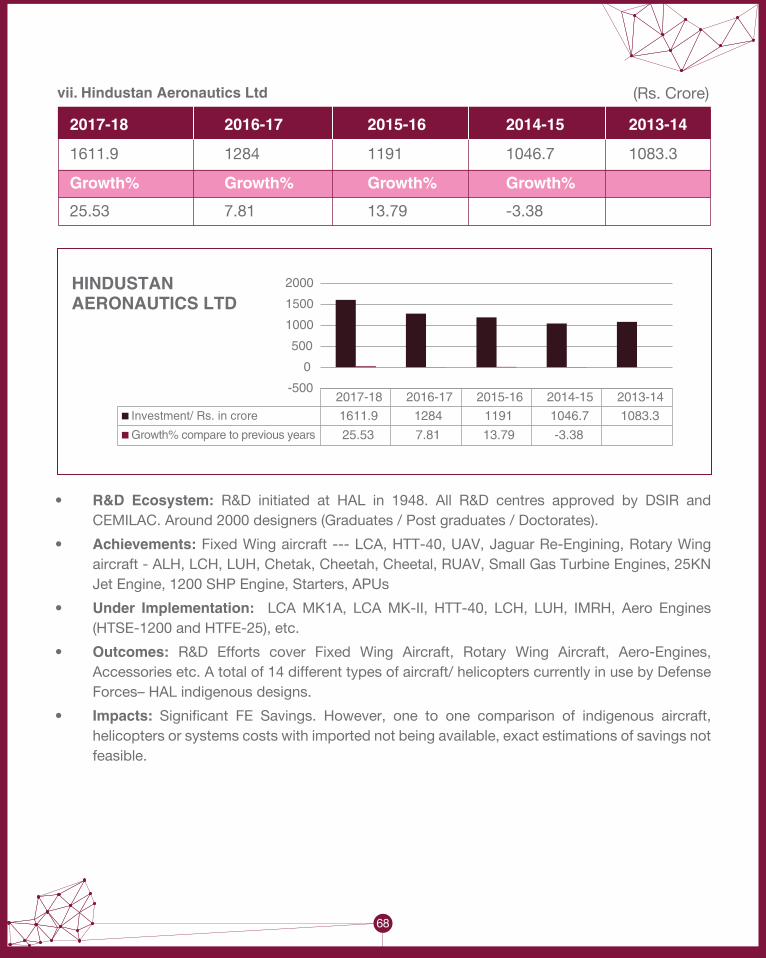

vii. Hindustan Aeronautics Ltd 68

viii. Hindustan Petroleum Corporation Ltd 69

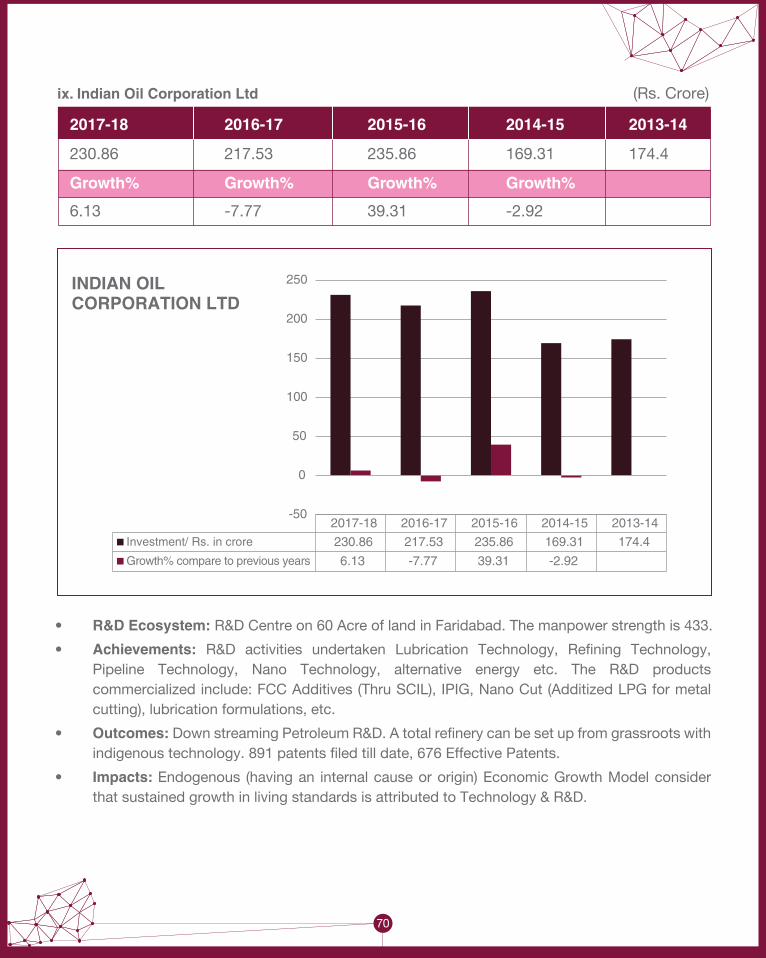

ix. Indian Oil Corporation Ltd 70

x. Bharat Petroleum Corporation Ltd 71

xi. NLC India LTD 72

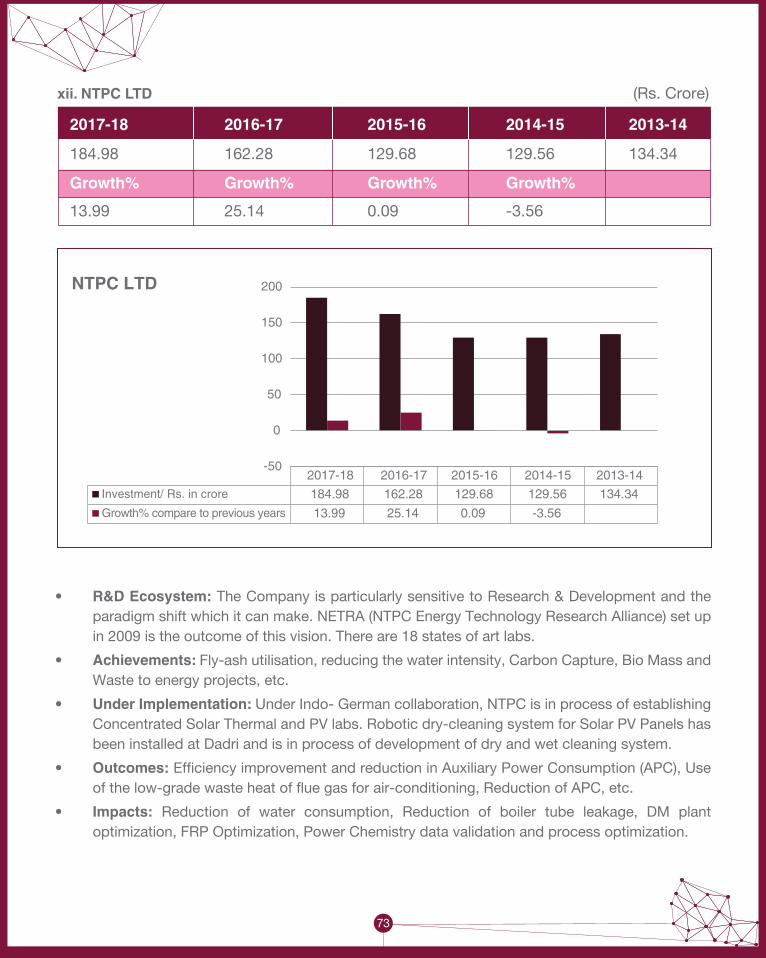

xii. NTPC LTD 73

xiii. Nuclear Power Corporation of India Ltd 74

xiv. Oil & Natural Gas Corporation Ltd 75

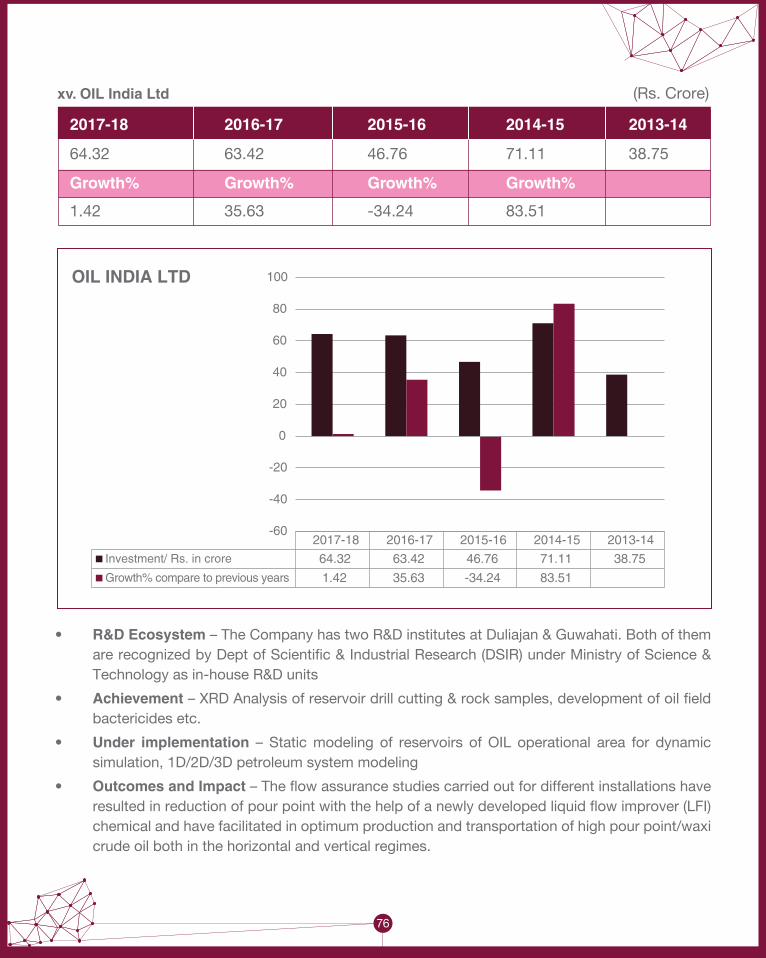

xv. OIL India Ltd 76

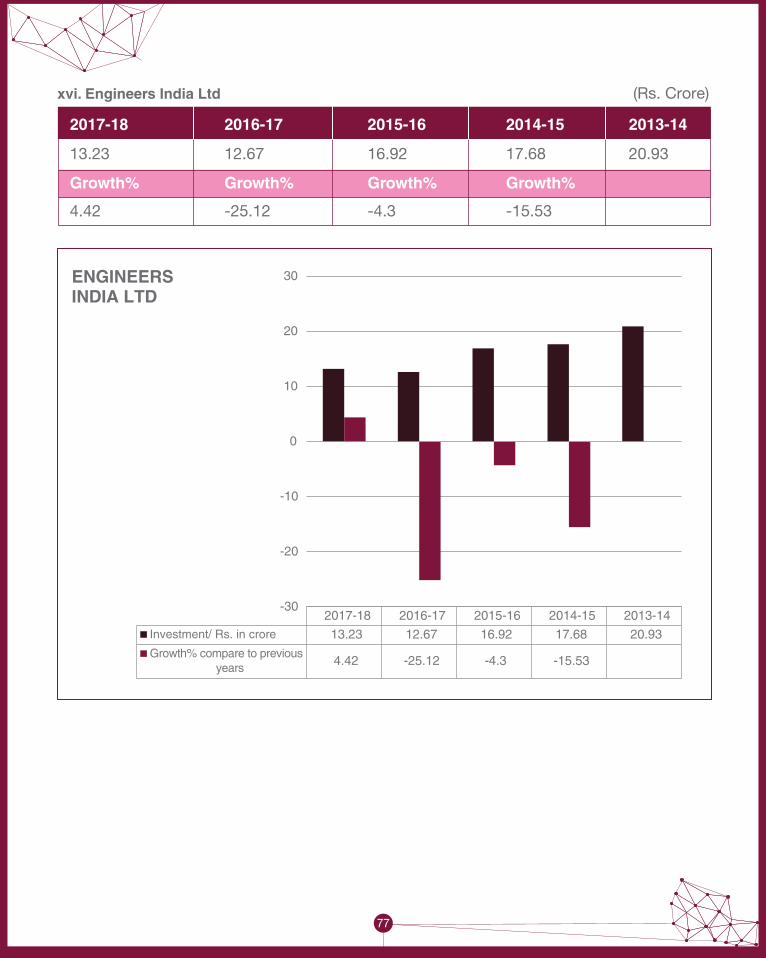

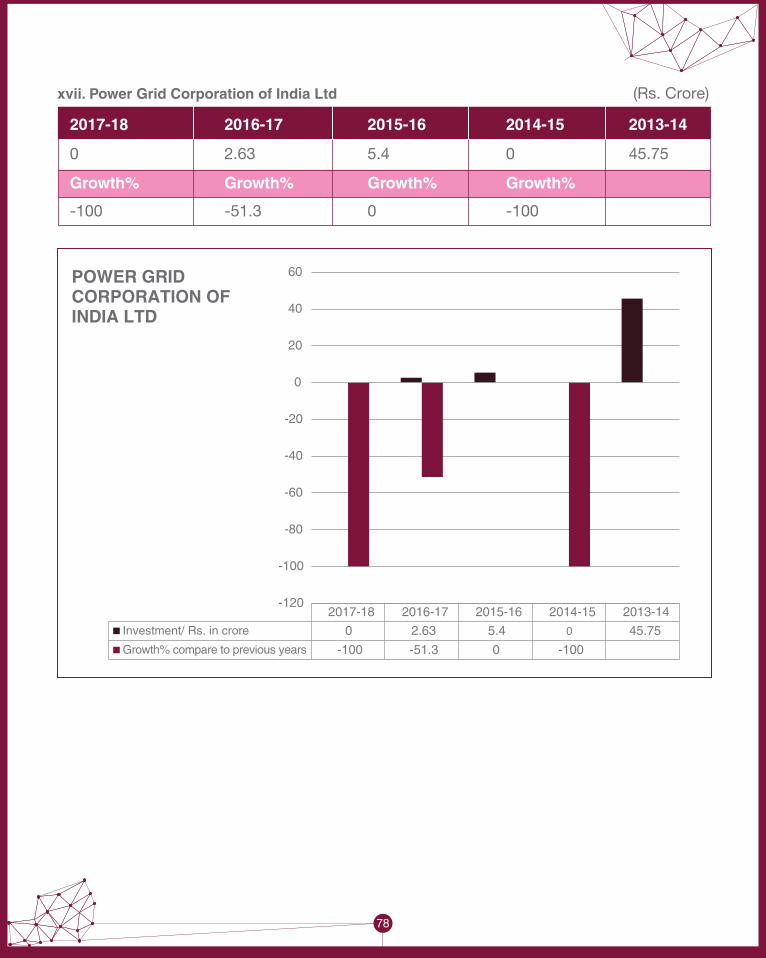

xvi. Engineers India Ltd 77 xvii. Power Grid Corporation of India Ltd 78

Annexure 4: CPSE Highlights 79

Annexure 5: Sectoral break up of R&D expenditure - last 5 year 80

Annexure 6: MCA Methodology for R&D Data Capturing 82

Annexure 7: State Governments/UTs expenditure on R&D 84

Annexure 8: Core Grants released to State S&T Councils 89

Annexure 9: Expenditures made under State S&T Programme 91

Annexure 10: DSIR Criteria for R&D Recognition 92

Annexure 11: Research Initiatives in MHRD 94

11

List of Figures and TablesFigure 1: India’s R&D Ecosystem - The Public and Private Sector 16

Figure 2: % Share of Stakeholders 2016-17 16

Figure 3: Snapshot of Vision 17

Figure 4: Top 5 Priority Recommendations 18

Figure 5: Top 5 Countries Global share of R&D Spending (%) 21

Figure 6: Top 5 Countries R&D (as a % of GDP) 22

Figure 7: Top Five Companies with maximum R&D Spend 22

Figure 8: World Trade 2017 23

Figure 9: Top Exporters of R&D Services - Exported value in 2017 23

Figure 10: Top Importers of R&D Services - Imported value in 2017 24

Figure 11: R&D and Trade 26

Figure 12: Royalties, Copyright and License Fees 27

Figure 13: GERD on R&D by Performer Share 29

Figure 14: R&D Expenditure as a Percentage of GDP (Development Time) 31

Figure 15: Number of Operating CPSEs incurring Expenditure on R&D in last 5 years 35

Figure 16: Amount of R&D Expenditure of operating CPSEs in last 5 years (Rs in Crores) 35

Figure 17: % of R&D expenditure incurred by Operating CPSEs in last 5 years 35

Figure 18: Average Annual Growth Rate (%) (2017-18) 36

Figure 19: R&D Expenditure in XBRL_300500 37

Figure 20: Expenditure in Agricultural Research and Education 38

Figure 21: Expenditure in Science, Technology and Environment 39

Figure 22: Transformation of R&D Expenditure Ecosystem 44

12

Figure 23: National R&D Expenditure 47

Figure 24: Projected R&D Expenditure 47

Table 1: Top Five Countries in Global R&D Spend 21

Table 2: FDI inflow into R&D 27

Table 3: R&D Expenditure 30

Table 4: Expenditure of Principal Science Government Agencies 30

Table 5: Plan Outlays and Expenditure of Central Scientific Ministries/Departments 33

Table 6: Top Five CPSEs Incurring Maximum Expenditure on R&D 36

Table 7: Top Five Institutions & Amount Spend on R&D 40

Table 8: Recommendations, Actions, Implementing Agencies and Timelines 48

13

R&D Expenditure Ecosystem

This document has five objectives. First to examine the relevance of R&D in the context of economic growth and social wellbeing. Second to assess the level of R&D spend in India as compared to the global spend. Third to identify the major stakeholders in India’s R&D ecosystem and assess their relative contributions to total R&D spend. Fourth to examine the strength and weakness of the existing ecosystem in fostering R&D and lastly to prepare a roadmap for a smart efficient and effective R&D expenditure ecosystem by recommending suitable measures for reaching the desired level of R&D spend by 2022. These objectives have been addressed in the forthcoming chapters. A brief summary is given in the following paragraphs.

As India emerges as one of the world’s largest economies, it needs to gradually move from being a net consumer of knowledge to becoming a net producer. For this India needs to attract more productive investment in R&D. This would lay the foundation of a New India by 2022.

Investing in R&D is not only critical for maintaining growth momentum but also fundamental to India’s security: the human security of its populations; the resilience needed to address the multiple uncertainties stemming from climate change to global meltdown, the national security challenges stemming from cyberwarfare to autonomous military systems such as drones.

R&D has played a critical role in economic development of India and continues to do so. The economic contribution of R&D has been dealt in the second chapter of this document. The global R&D scenario has been dealt in the third chapter. In the subsequent chapters, India’s R&D expenditure trends have been dealt. Summary findings are as follows:

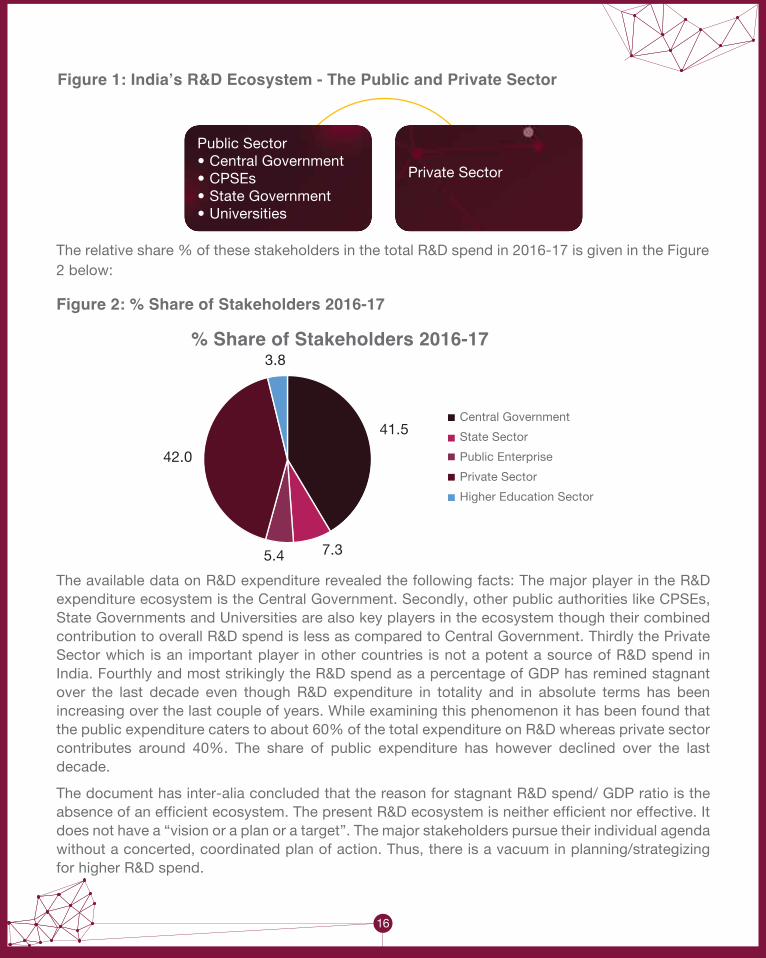

The major stakeholders in India’s R&D ecosystem can be divided into two categories. They are The Public and Private Sector:

15

1UNESCO

Towards a Smart, Efficient and Effective R&D Ecosystem

1. Executive Summary

Transform India’s R&D Expenditure Ecosystem by creating an institutional framework which fosters R&D spend in a coordinated, concerted and planned manner for achieving a target of GERD as 2% of GDP

16

Public Sector• Central Government• CPSEs• State Government• Universities

Private Sector

The relative share % of these stakeholders in the total R&D spend in 2016-17 is given in the Figure 2 below:

Figure 2: % Share of Stakeholders 2016-17

Figure 1: India’s R&D Ecosystem - The Public and Private Sector

The available data on R&D expenditure revealed the following facts: The major player in the R&D expenditure ecosystem is the Central Government. Secondly, other public authorities like CPSEs, State Governments and Universities are also key players in the ecosystem though their combined contribution to overall R&D spend is less as compared to Central Government. Thirdly the Private Sector which is an important player in other countries is not a potent a source of R&D spend in India. Fourthly and most strikingly the R&D spend as a percentage of GDP has remined stagnant over the last decade even though R&D expenditure in totality and in absolute terms has been increasing over the last couple of years. While examining this phenomenon it has been found that the public expenditure caters to about 60% of the total expenditure on R&D whereas private sector contributes around 40%. The share of public expenditure has however declined over the last decade.

The document has inter-alia concluded that the reason for stagnant R&D spend/ GDP ratio is the absence of an efficient ecosystem. The present R&D ecosystem is neither efficient nor effective. It does not have a “vision or a plan or a target”. The major stakeholders pursue their individual agenda without a concerted, coordinated plan of action. Thus, there is a vacuum in planning/strategizing for higher R&D spend.

% Share of Stakeholders 2016-17

Central Government

State Sector

Public Enterprise

Private Sector

Higher Education Sector

41.5

3.8

42.0

5.4 7.3

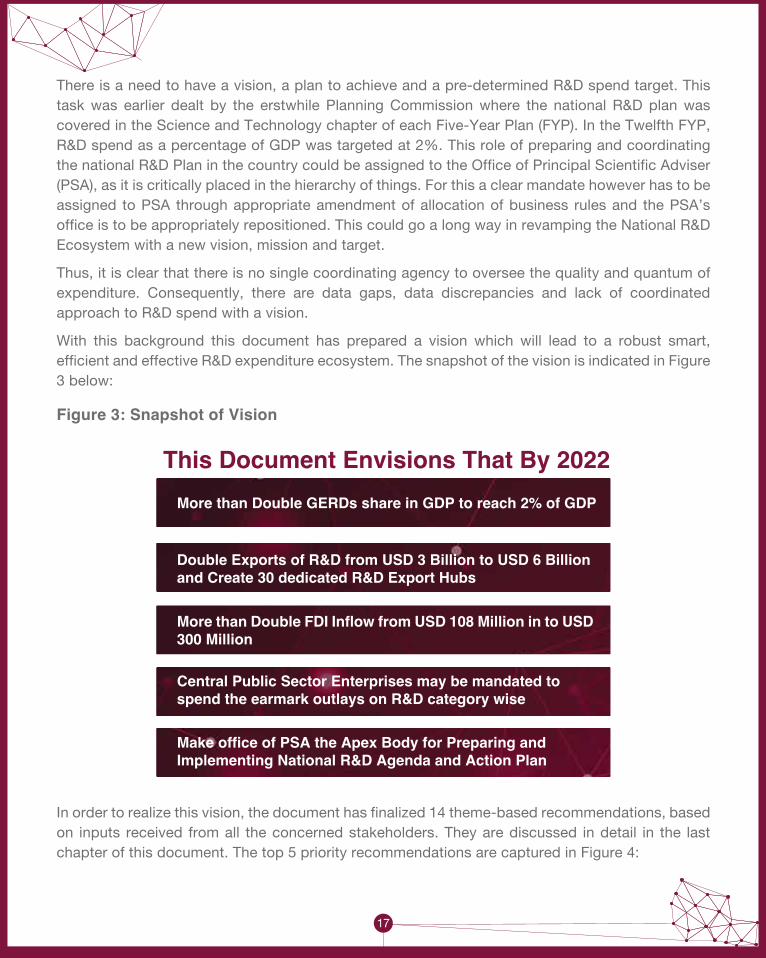

There is a need to have a vision, a plan to achieve and a pre-determined R&D spend target. This task was earlier dealt by the erstwhile Planning Commission where the national R&D plan was covered in the Science and Technology chapter of each Five-Year Plan (FYP). In the Twelfth FYP, R&D spend as a percentage of GDP was targeted at 2%. This role of preparing and coordinating the national R&D Plan in the country could be assigned to the Office of Principal Scientific Adviser (PSA), as it is critically placed in the hierarchy of things. For this a clear mandate however has to be assigned to PSA through appropriate amendment of allocation of business rules and the PSA’s office is to be appropriately repositioned. This could go a long way in revamping the National R&D Ecosystem with a new vision, mission and target.

Thus, it is clear that there is no single coordinating agency to oversee the quality and quantum of expenditure. Consequently, there are data gaps, data discrepancies and lack of coordinated approach to R&D spend with a vision.

With this background this document has prepared a vision which will lead to a robust smart, efficient and effective R&D expenditure ecosystem. The snapshot of the vision is indicated in Figure 3 below:

Figure 3: Snapshot of Vision

The available data on R&D expenditure revealed the following facts: The major player in the R&D expenditure ecosystem is the Central Government. Secondly, other public authorities like CPSEs, State Governments and Universities are also key players in the ecosystem though their combined contribution to overall R&D spend is less as compared to Central Government. Thirdly the Private Sector which is an important player in other countries is not a potent a source of R&D spend in India. Fourthly and most strikingly the R&D spend as a percentage of GDP has remined stagnant over the last decade even though R&D expenditure in totality and in absolute terms has been increasing over the last couple of years. While examining this phenomenon it has been found that the public expenditure caters to about 60% of the total expenditure on R&D whereas private sector contributes around 40%. The share of public expenditure has however declined over the last decade.

The document has inter-alia concluded that the reason for stagnant R&D spend/ GDP ratio is the absence of an efficient ecosystem. The present R&D ecosystem is neither efficient nor effective. It does not have a “vision or a plan or a target”. The major stakeholders pursue their individual agenda without a concerted, coordinated plan of action. Thus, there is a vacuum in planning/strategizing for higher R&D spend.

There is a need to have a vision, a plan to achieve and a pre-determined R&D spend target. This task was earlier dealt by the erstwhile Planning Commission where the national R&D plan was covered in the Science and Technology chapter of each Five-Year Plan (FYP). In the Twelfth FYP, R&D spend as a percentage of GDP was targeted at 2%. This role of preparing and coordinating the national R&D Plan in the country could be assigned to the Office of Principal Scientific Adviser (PSA), as it is critically placed in the hierarchy of things. For this a clear mandate however has to be assigned to PSA through appropriate amendment of allocation of business rules and the PSA’s office is to be appropriately repositioned. This could go a long way in revamping the National R&D Ecosystem with a new vision, mission and target.

Thus, it is clear that there is no single coordinating agency to oversee the quality and quantum of expenditure. Consequently, there are data gaps, data discrepancies and lack of coordinated approach to R&D spend with a vision.

With this background this document has prepared a vision which will lead to a robust smart, efficient and effective R&D expenditure ecosystem. The snapshot of the vision is indicated in Figure 3 below:

Figure 3: Snapshot of Vision

17

In order to realize this vision, the document has finalized 14 theme-based recommendations, based on inputs received from all the concerned stakeholders. They are discussed in detail in the last chapter of this document. The top 5 priority recommendations are captured in Figure 4:

This Document Envisions That By 2022More than Double GERDs share in GDP to reach 2% of GDP

Double Exports of R&D from USD 3 Billion to USD 6 Billion and Create 30 dedicated R&D Export Hubs

More than Double FDI Inflow from USD 108 Million in to USD 300 Million

Central Public Sector Enterprises may be mandated to spend the earmark outlays on R&D category wise

Make office of PSA the Apex Body for Preparing and Implementing National R&D Agenda and Action Plan

Figure 4: Top 5 Priority Recommendations

Top 5 Priority RecommendationsThe STI Policy may be suitably amended to reflect the changing landscape of R&D with disaggregated targets as proposed in this report for expenditure, FDI and exports

Create new R&D Export Hubs which could leverage the existing Science Parks with Software Technology Parks. 30 such parks may be created which will be inline with special economic zones for R&D

MoU guidelines may be suitably strengthened to create greater weightage to R&D with outcome indicators. This should be reflected as an activity other than energy saving related R&D

A corpus of INR 5000 Crore may be created for funding of mega projects with cross cutting themes which are of national interest

PSA to be the top national coordinator for R&D in the Country and appropriately positioned. This office will connect with all R&D Spending stakeholders including CPSEs, Universities, domestic and international R&D institutions and State Governments

18

By acceptance of these recommendations it is estimated that overall R&D spend will increase by more than four times in 2021-2022 with private sector playing a major role and contributing 60% of the total spend instead of 40% as observed in the present scenario. This will relieve the public exchequer of fiscal stress arising out of need to achieve a 2% ratio with GDP. This will also lead to doubling of R&D exports and FDI coming into the R&D sector.

19

2. Research & Development (R&D) – Concepts and Definitions

Research & Development (R&D) has many connotations. It is used in various forums for various objectives. In this document we make a distinction between R&D as an activity which is unique and R&D Expenditure which is recognized under the prevailing law as expenditure attributable to R&D.

R&D activities can be defined as any systematic and creative work undertaken in order to increase the stock of knowledge and use of this knowledge to devise new applications. R&D activities include one or more of the categories of research such as basic research, applied research and experimental development. (Source: UNESCO manual 1984 and frascati manual, OECD, 2015). The term R&D thus covers three activities: basic research, applied research and experimental development (FM §64). The basic criterion for distinguishing R&D from related activities is the presence in R&D of an appreciable element of novelty and the resolution of scientific and/or technological uncertainty, i.e. when the solution to a problem is not readily apparent to someone familiar with the basic stock of common knowledge and techniques for the area concerned (FM §84).

As regards R&D expenditure, the global practice is to term it as Gross Domestic Expenditure on R&D (GERD). The nomenclature of GERD is derived from OECD manual “The Measurement of Scientific and Technical Activities: Proposed Standard Practice for Surveys of Research and Development, Paris”. In line with the System of National Accounts (SNA), and following the National Science Foundation (NSF), the manual recommended classifying R&D according to three main economic sectors: business, government and private. To these three sectors, the OECD, following the NSF again, added a fourth one: higher education. The rationale for including Higher Education was as follows: The definitions of the first three sectors are basically the same as in national accounts, but higher education is included as a separate main sector here because of the concentration of a large part of fundamental research activity in the universities and the crucial importance of these institutions in the formulation of an adequate national policy for R&D. For linking R&D and Economic Growth, OECD has used GERD as a percentage of Gross National Product as an indicator for international comparisons. The generalized use of this indicator has been reflected in many global

R&D as an activity has three distinguishing features. It involves Basic Research, Applied Research and Experimental Development. The concept of GERD has been derived from OECD and is known as Gross Domestic Expenditure on R&D. It is the sum of R&D Expenditure of four economic sectors namely, Business, Government, Private Sector and Higher Education. This section discusses the various definitions of R&D as an activity and the criterion for identifying R&D Expenditure.

publications like the Global Innovation Index which uses five indicators of GERD. The indicators used are: Gross expenditure on R&D (GERD) as a proportion of GDP. Global R&D companies, average expenditure top 3, GERD performed by business enterprise, GERD financed by business enterprise and GERD financed by abroad.

In India, the Department of Scientific & Industrial Research (DSIR) is operating a scheme for granting recognition & registration to in-house R&D units established by corporate industry. This is the only scheme of the Government which is set-up for benchmarking the industrial R&D. Government of India has announced a number of fiscal incentives for research and development by industry from time to time and many of these incentives are implemented through DSIR. In-house R&D units recognized by DSIR are not only eligible for these incentives (wherever applicable) but also for receiving funds for R&D from other government departments and agencies such as DST, DBT, Deity, MoEFCC, MNRE, MoFPI, CSIR, ICMR, ICAR, TDB where recognition to the in-house R&D centre by DSIR is a requirement. As regards the Accounting Standard of ICAI, an enterprise is required to disclose the aggregate amount of R&D expenditure as an expense during the period under the financial statements. The Accounting standard prescribes the recognition criteria of the Intangible Asset which may be generated from the R&D activities undertaken by the company, rules for measurement, and disclosure requirements in the financial statements. The expenditure incurred by the enterprise can broadly be categorised into Research expenditure and Development expenditure. Expenditure incurred on research is to be recognized as an expense and charged off at the point of incurrence. The other definitions of R&D used in India are mentioned in Annexure 1.

20

Research & Development (R&D) has many connotations. It is used in various forums for various objectives. In this document we make a distinction between R&D as an activity which is unique and R&D Expenditure which is recognized under the prevailing law as expenditure attributable to R&D.

R&D activities can be defined as any systematic and creative work undertaken in order to increase the stock of knowledge and use of this knowledge to devise new applications. R&D activities include one or more of the categories of research such as basic research, applied research and experimental development. (Source: UNESCO manual 1984 and frascati manual, OECD, 2015). The term R&D thus covers three activities: basic research, applied research and experimental development (FM §64). The basic criterion for distinguishing R&D from related activities is the presence in R&D of an appreciable element of novelty and the resolution of scientific and/or technological uncertainty, i.e. when the solution to a problem is not readily apparent to someone familiar with the basic stock of common knowledge and techniques for the area concerned (FM §84).

As regards R&D expenditure, the global practice is to term it as Gross Domestic Expenditure on R&D (GERD). The nomenclature of GERD is derived from OECD manual “The Measurement of Scientific and Technical Activities: Proposed Standard Practice for Surveys of Research and Development, Paris”. In line with the System of National Accounts (SNA), and following the National Science Foundation (NSF), the manual recommended classifying R&D according to three main economic sectors: business, government and private. To these three sectors, the OECD, following the NSF again, added a fourth one: higher education. The rationale for including Higher Education was as follows: The definitions of the first three sectors are basically the same as in national accounts, but higher education is included as a separate main sector here because of the concentration of a large part of fundamental research activity in the universities and the crucial importance of these institutions in the formulation of an adequate national policy for R&D. For linking R&D and Economic Growth, OECD has used GERD as a percentage of Gross National Product as an indicator for international comparisons. The generalized use of this indicator has been reflected in many global

publications like the Global Innovation Index which uses five indicators of GERD. The indicators used are: Gross expenditure on R&D (GERD) as a proportion of GDP. Global R&D companies, average expenditure top 3, GERD performed by business enterprise, GERD financed by business enterprise and GERD financed by abroad.

In India, the Department of Scientific & Industrial Research (DSIR) is operating a scheme for granting recognition & registration to in-house R&D units established by corporate industry. This is the only scheme of the Government which is set-up for benchmarking the industrial R&D. Government of India has announced a number of fiscal incentives for research and development by industry from time to time and many of these incentives are implemented through DSIR. In-house R&D units recognized by DSIR are not only eligible for these incentives (wherever applicable) but also for receiving funds for R&D from other government departments and agencies such as DST, DBT, Deity, MoEFCC, MNRE, MoFPI, CSIR, ICMR, ICAR, TDB where recognition to the in-house R&D centre by DSIR is a requirement. As regards the Accounting Standard of ICAI, an enterprise is required to disclose the aggregate amount of R&D expenditure as an expense during the period under the financial statements. The Accounting standard prescribes the recognition criteria of the Intangible Asset which may be generated from the R&D activities undertaken by the company, rules for measurement, and disclosure requirements in the financial statements. The expenditure incurred by the enterprise can broadly be categorised into Research expenditure and Development expenditure. Expenditure incurred on research is to be recognized as an expense and charged off at the point of incurrence. The other definitions of R&D used in India are mentioned in Annexure 1.

21

In 2017 the global R&D spend amounted to USD 1.7 trillion in PPP terms. The top five countries in global R&D spend are indicated in Table 1:

Table 1: Top Five Countries in Global R&D Spend1

The global share percentage of the countries listed above is indicated in Figure 5:

Figure 5: Top 5 Countries Global share of R&D Spending (%)

3. Global R&D Expenditure – An Overview

Globally R&D expenditure is led by five countries, they are: USA, China, Japan, Germany and South Korea. Asia is emerging as a global destination for R&D investment. India’s share is not only low but as compared to GDP is negligible. This is in addition to the fact that the R&D companies who have a global stature in R&D are not from India. This is not only a challenge but also an opportunity for India. In this section we have indicated the emerging trends in global R&D spend.

Rank Country R&D Spending in Billion PPP $#1 United States 543.2

#2 China 496.0

#3 Japan 175.8

#4 Germany 127.1

#5 South Korea 89.8

1UNESCO

United States

China

Japan

Germany

South Korea

Rest of the World

31.9

29.1

10.3

7.5

5.3

15.9

22

In terms of spend, United States is the largest of the global spenders on R&D followed by China and Japan. The major spenders within Europe are Germany, France, and the UK. The industries that lead in the total R&D spending are auto, health care, computing and electronics and defence. Measuring R&D in absolute terms shows where most of the world’s research happens, but it fails to capture the countries that are spending more in relative terms.

The top five countries which allocate the highest percentage of their GDP to R&D in 2017 is indicated in Figure 6:

Figure 6: Top 5 Countries R&D (as a % of GDP)

The top five companies that have the maximum spend on R&D is as under3:

Figure 7: Top Five Companies with maximum R&D Spend

3

Top 5 Countries R&D (as a % of GDP

South Korea

4.3% 4.2%

3.4%3.2% 3.2%

Israel Japan Switzerland Finland

R&D (in billion U.S. dollars)

Amazon Alphabet Volkswagen Samsung Intel Co.

22.6

16.2 15.8 15.313.1

2UNESCO3www.statista.com

While the United States and Japan remain leaders in R&D spend, there is an increasing shift of R&D spend to the Asian markets. The Asian economies such as China, India, Japan and South Korea are likely to drive R&D growth in years to come, especially in the fields of energy, pharmaceuticals and space technologies. Growth of technological capabilities in this region is the prime contributing factor. Another factor which influences the move of R&D towards the Asian countries is the demographic factor. The growing population base in Asia, primarily China and India will continue to drive market opportunities. R&D for consumer related products and technologies, such as consumer electronics, foods, and transportation, is likely to increase in direct relation to the population growth trends. With globalization, outsourcing, and increased investments in R&D in the area of ICT (information and communications technologies) there has been a spread of R & D to new geographies. Technology organizations can now outsource the development of new technology-based products to various countries that have many of the technology resources once limited to advanced economies. Countries such as China, India, Korea, Brazil, and Eastern Europe are now able to attract FDI into R&D sector.4

R&D also contributes to world trade in commercial services. In terms of classification trade in R&D is covered under “other commercial services”. It has got two categories i.e. Work undertaken on a systematic basis to increase the stock of knowledge and Other than work undertaken on a systematic basis to increase the stock of knowledge. In 2017 the share of Other Commercial Services exports and imports in total global commercial services exports and imports were 54% and 50% respectively. India is a leading exporter of other commercial services with a share of 4.9% in global trade of commercial services in 2017.

Figure 8: World Trade 2017

23

6WTO – World Trade Statistics 2017

World Trade 2017• Merchandise: USD 17.73 Trillion• Commercial Services: USD 5.28 Trillion

The top 5 countries importing and exporting R&D services are as under:

Figure 9: Top Exporters of R&D Services - Exported value in 2017

4,27,65,150

2,48,41,407

64,94,925 54,17,839 49,50,819

United States ofAmerica

Germany Japan Belgium Ireland

Top Exporters of R&D Services - Exported value in 2017 in USD Thousand

6

24

7WTO – World Trade Statistics 2017

Figure 10: Top Importers of R&D Services - Imported value in 2017

3,49,22,000

3,05,80,517

2,22,02,899

1,73,11,081

1,32,94,129

United States ofAmerica

Ireland Germany Japan Switzerland

Top Importers of R&D Services - Imported value in 2017 in USD Thousand

India’s share in Global R&D Expenditure is 2.8% amounting to USD 48.1 billion in PPP terms. In terms of R&Ds share in GDP, it is around 0.6% which is one of the lowest amongst the BRICS Countries.

7

There is ample global evidence of the fact that R&D is a key driver of productivity and economic growth. It has been observed that two-thirds of economic growth in Europe from 1995 to 2007 was attributed to R&D. R&D accounted for 15% of all productivity gains in Europe for this period. An increase of 10% in R&D investment is associated with gains in productivity ranging from 1.1% to 1.4% (Donselaar and Koopmans, 2016).

Conceptually, R&D contributes to economic growth in multiple ways. It leads to capital formation which in turn results in economic growth. It is a source for trade in services and FDI. The evidence with respect to India is given in the following paras.

As per the data received from Ministry of Statistics, R&D expenditure increased from Rs. 57,908 crore in 2015-16 to Rs. 73,720 crore in 2017-18. However, as a percentage of GDP, R&D has remained virtually stagnant at around 0.6%. It may be noted here that this data is not in public domain and does not tally with data published by Department of Science and Technology (DST) and other international organizations like World Bank. This is due to the fact that the coverage of data and their sources are different. This has been explained in the note on data sources.

Notwithstanding this data variation it is worth emphasizing that the trend of a stagnant R&D, GDP ratio in the last one decade remains unchanged.

R&D is a service activity. As per CSO’s new method, it is now a part of the professional scientific & technical activities. Export and Import revenue arising out of this activity are captured under the invisibles category of balance of payments published by RBI.

As per data received from RBI, R&D exports have grown from USD 1,486 million in 2015-16 to USD 3,603 million in 2017-18 and R&D imports have grown from USD 339 million in 2015-16 to USD 464 million in 2017-18. It is noteworthy that India enjoys a positive balance of trade in R&D sector which means that India is a net exporter of R&D to rest of the world. This is graphed in Figure 11.

25

4. Economic Value of R&D

R&D as an activity is measurable and has economic value. It contributes to GDP, Exports – Imports and FDI. The Intellectual Property generated from R&D also brings in revenue to the economy in the form of copy rights and patents. This section discusses the economic contribution of R&D to Indian Economy.

Figure 11: R&D and Trade

R&D and Trade (USD Million)

2015-16 2016-17 2017-18Exports 1486 2075 3603

Imports 339 397 464

Net 1147 1678 3139

1486

2075

3603

339397

464

1147

1678

3139

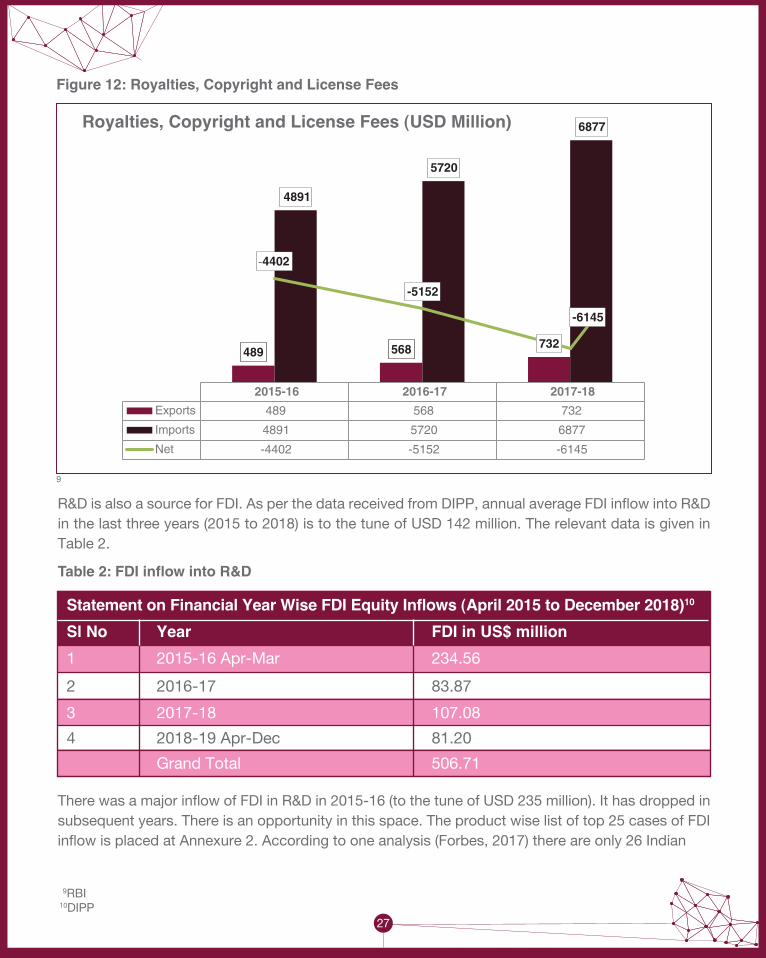

R&D leads to Intellectual Property which in turn generates revenue to the researcher in the form of Royalties, copyright and license fees. Export and Import of Royalties, copyright and license fees are important reflectors of innovation in the country.

As per the data received from RBI, export revenue on these accounts have grown from USD 489 million in 2015-16 to USD 732 million in 2017-18, whereas import revenue has grown from USD 4891 million in 2015-16 to USD 6877 million in 2017-18. The Figure 12 indicates that India is a net importer of IP and there is immense opportunity in this area to grow.

26

8

8RBI

Figure 12: Royalties, Copyright and License Fees

Royalties, Copyright and License Fees (USD Million)

2015-16 2016-17 2017-18

Exports 489 568 732

Imports 4891 5720 6877

Net -4402 -5152 -6145

489 568 732

4891

5720

6877

-4402

-5152

-6145

0

R&D is also a source for FDI. As per the data received from DIPP, annual average FDI inflow into R&D in the last three years (2015 to 2018) is to the tune of USD 142 million. The relevant data is given in Table 2.

Table 2: FDI inflow into R&D

There was a major inflow of FDI in R&D in 2015-16 (to the tune of USD 235 million). It has dropped in subsequent years. There is an opportunity in this space. The product wise list of top 25 cases of FDI inflow is placed at Annexure 2. According to one analysis (Forbes, 2017) there are only 26 Indian

9RBI10DIPP

9

Statement on Financial Year Wise FDI Equity Inflows (April 2015 to December 2018)10 Sl No Year FDI in US$ million1 2015-16 Apr-Mar 234.56

2 2016-17 83.87

3 2017-18 107.08

4 2018-19 Apr-Dec 81.20

Grand Total 506.71

27

companies in the list of the top 2,500 global R&D spenders compared to 301 Chinese companies. 19 (of these 26) firms are in just three sectors: pharmaceuticals, automobiles and software. India has no firms in five of the top ten R&D sectors as opposed to China that has a presence in each of them.

To sum up, R&D has contributed to capital formation, export of services and FDI. This is in addition to the fact that the contribution of R&D to social wellbeing is also phenomenal. Our societies face multiple, complex and urgent challenges that affect the quality of life of our citizens: from energy efficiency to security, climate change or an ageing population. R&D has played a crucial role to anticipate and respond to these needs. There is little data to support these aspects of R&D though their impact is felt all across the society.

Investing in R&D is fundamental to India’s national security: the security of its populations; the resilience needed to address the multiple uncertainties stemming from climate change and global meltdown.

28

29

The first trend observed is that the investments in Indian science, measured in terms of Gross Expenditure on R&D (GERD), have shown a consistently increasing trend over the years. GERD has tripled in the last decade in nominal terms – from Rs. 24,117 crores in 2004-05 to Rs. 85,326 crores in 2014-15 and an estimated Rs.1,04,864 crores in 2016-17 – and double in real terms (Table 3).

The second trend is that as a fraction of GDP, R&D spend has been stagnant – between 0.6 - 0.7 percent of GDP – over the past two decades. India’s spending on R&D (about 0.6 percent of GDP) is well below that in major nations such as the US (2.8), China (2.1), Israel (4.3) and Korea (4.2). It is also unique in how dominant government is in carrying out R&D (Figure 13).

Figure 13: GERD on R&D by Performer Share

5. Gross Expenditure on R&D Trends11

Gross Expenditure on R&D is a relevant indicator for measuring the amount of resources allocated in the economy to R&D activities. The overall trends of R&D expenditure in India are not satisfactory. In this section we discuss the various contributors to aggregate R&D expenditure and their relative roles. This is a macro picture followed by segment wise analysis in the succeeding sections.

India China

Per

cent

age

of G

ER

D

Germany

Government Business Unversity Private Non-Profit

Korea USA Japan Israel

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

GERD on R&D by Performer Share in 2015

11Economic Survey.

30

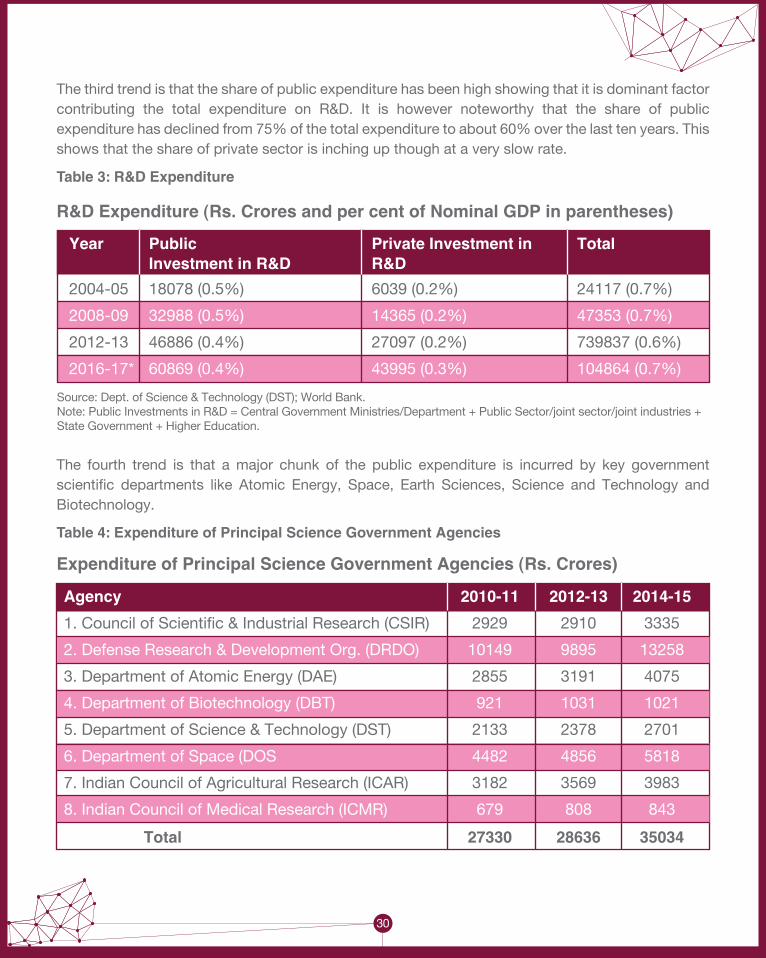

The third trend is that the share of public expenditure has been high showing that it is dominant factor contributing the total expenditure on R&D. It is however noteworthy that the share of public expenditure has declined from 75% of the total expenditure to about 60% over the last ten years. This shows that the share of private sector is inching up though at a very slow rate.

Table 3: R&D Expenditure

Year Public Private Investment in Total Investment in R&D R&D2004-05 18078 (0.5%) 6039 (0.2%) 24117 (0.7%)

2008-09 32988 (0.5%) 14365 (0.2%) 47353 (0.7%)

2012-13 46886 (0.4%) 27097 (0.2%) 739837 (0.6%)

2016-17* 60869 (0.4%) 43995 (0.3%) 104864 (0.7%)

R&D Expenditure (Rs. Crores and per cent of Nominal GDP in parentheses)

The fourth trend is that a major chunk of the public expenditure is incurred by key government scientific departments like Atomic Energy, Space, Earth Sciences, Science and Technology and Biotechnology.

Table 4: Expenditure of Principal Science Government Agencies

Expenditure of Principal Science Government Agencies (Rs. Crores)

Source: Dept. of Science & Technology (DST); World Bank.Note: Public Investments in R&D = Central Government Ministries/Department + Public Sector/joint sector/joint industries +State Government + Higher Education.

Agency 2010-11 2012-13 2014-151. Council of Scientific & Industrial Research (CSIR) 2929 2910 3335

2. Defense Research & Development Org. (DRDO) 10149 9895 13258

3. Department of Atomic Energy (DAE) 2855 3191 4075

4. Department of Biotechnology (DBT) 921 1031 1021

5. Department of Science & Technology (DST) 2133 2378 2701

6. Department of Space (DOS 4482 4856 5818

7. Indian Council of Agricultural Research (ICAR) 3182 3569 3983

8. Indian Council of Medical Research (ICMR) 679 808 843

Total 27330 28636 35034

The fifth trend is that in contrast to the trend observed in advanced countries where the private sector carries out the bulk of research and development. In India, the government is not just the primary source of R&D funding but also its the primary user of these funds.

Government expenditure on R&D is undertaken almost entirely by the central government with state government playing a secondary role.

The sixth trend is that universities play a relatively small role in the research activities of the country. This is in contrast to the scenario in advanced countries where universities play a critical role in creating the talent pool for research and generating high quality research. In India, publicly funded research is concentrated in specialized research institutes under different government departments. This leaves universities to largely play a teaching role – a decision that goes back to the 1950s. It is now widely acknowledged that whatever the merits of the decision at the time, this disconnect has severely impaired both teaching as well as the research enterprise in the country.

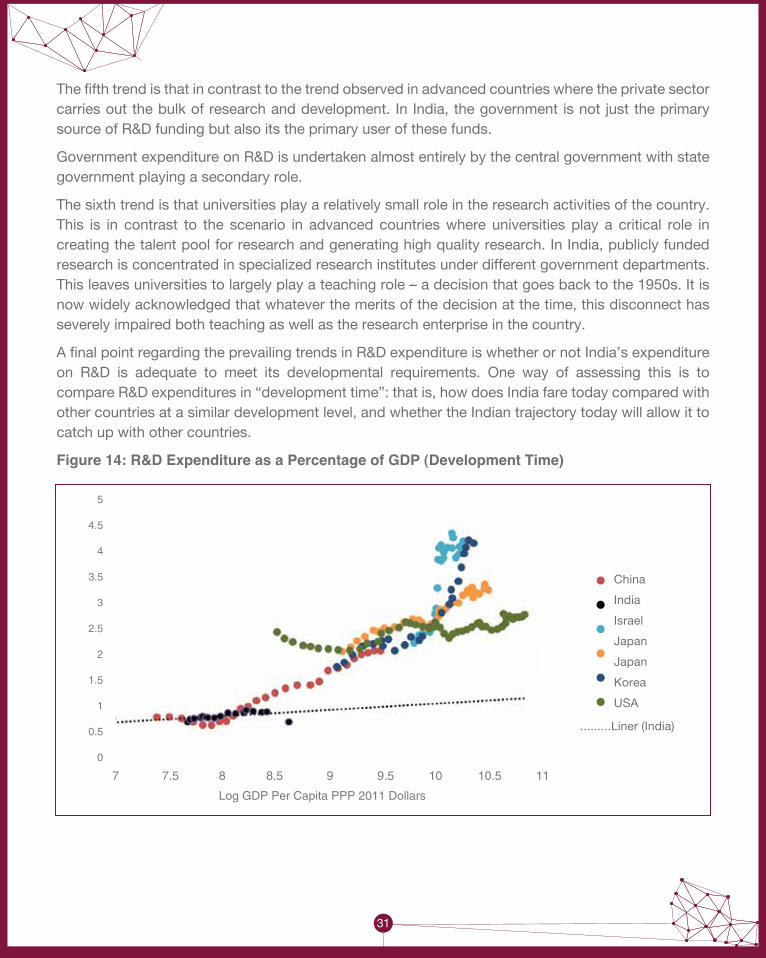

A final point regarding the prevailing trends in R&D expenditure is whether or not India’s expenditure on R&D is adequate to meet its developmental requirements. One way of assessing this is to compare R&D expenditures in “development time”: that is, how does India fare today compared with other countries at a similar development level, and whether the Indian trajectory today will allow it to catch up with other countries.

Figure 14: R&D Expenditure as a Percentage of GDP (Development Time)

31

China

India

Israel

Japan

Japan

Korea

USA

.........Liner (India)

Log GDP Per Capita PPP 2011 Dollars

5

4.5

4

3.5

3

2.5

2

1.5

1

0.5

0

7 7.5 8 8.5 9 9.5 10 10.5 11

32

The Figure 14 plots R&D as a share of GDP against per capita GDP for a set of comparable countries. It shows that India was, at one point, spending more on R&D as percentage of GDP than countries like China at the same level of GDP per capita. As a lower middle-income country, it is not surprising that India’s spending on R&D lags upper-middle income and high-income countries such as China, Israel, and the U.S. However, it currently underspends even relative to its income level. In addition, most other countries, especially East Asian countries like China, Japan, and Korea, have seen dramatic increases in R&D as a percentage of GDP as they have become richer. India, on the other hand, has only seen a slight increase. In fact, in 2015, there was a sizeable decline in R&D spending even as GDP per capita continued to rise.

33

Gross Expenditure on R&D (GERD) is mainly driven by Government sector comprising of Central Government 45.1%, State Governments 7.4%, Higher Education 3.9% and Public Sector Industries 5.5% with Private Sector Industries contributing 38.1% during 2014-15. In totality, there are five tiers under which the R&D expenditure has been categorised.

Central Government: The first tier is the Central Government. In India Central Government dominates and drives R&D. Major share of R&D spend is accounted for by the Central Government. Given the importance of the growth in R & D, the government had proposed an increased allocation for scientific departments in the 12th Five Year Plan. It had earmarked 3% of planned outlay which was higher than agriculture, irrigation and communications. It had proposed an allocation of Rs 1.30 lakh crore for science, technology and environment as against a total allocation of 43.3 lakh crore. It had also offered various incentives for promoting R&D in the country.

The Science & Technology departments who have the highest spend in R&D are as follows:

Table 5: Plan Outlays and Expenditure of Central Scientific Ministries/Departments

6. Sectoral Expenditure Trends and Issues

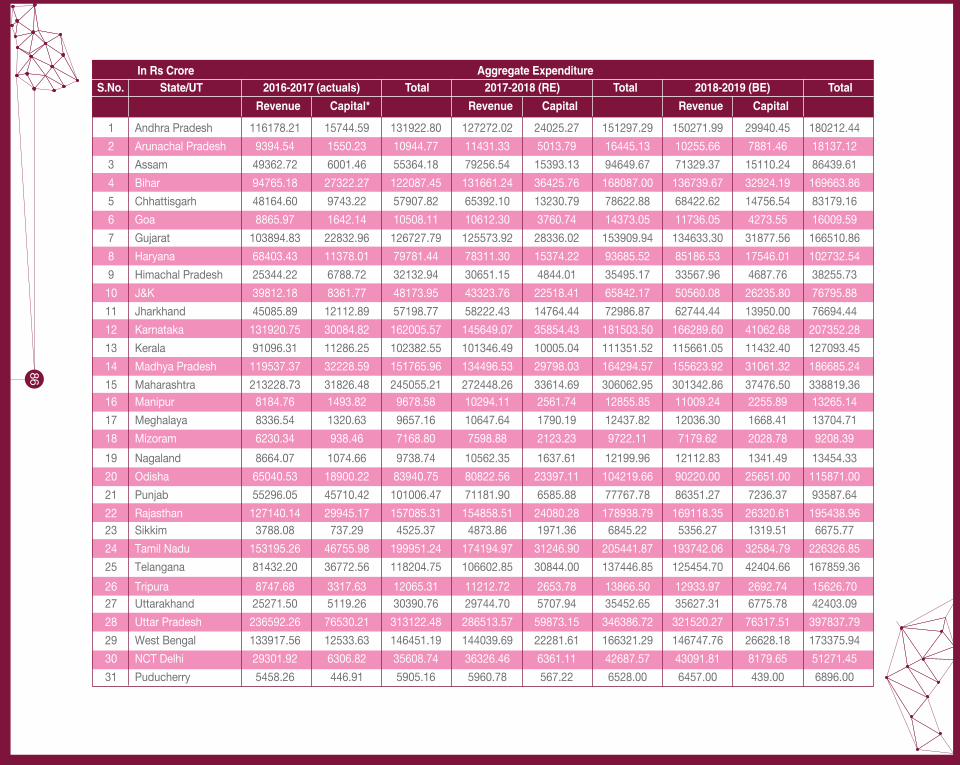

This section deals with R&D expenditure trends segment wise. The major segments covered are Central Government, CPSEs, Private Sector, State Governments and Educational Institutes. It is pertinent to mention here that the data for these segment wise trends have been received from relevant stakeholders. They do not tally with the data published by DST but the underlying trends and conclusions remain intact, that is Central Government is the major contributor to R&D spend in India, which is against Global Trends.

Plan Outlays and Expenditure of Central Scientific Ministries/Departments (in Rs Crore)S&T Department/Agencies Twelfth Plan (2012–17) Outlay Union Budget 2019-20

DAE (R&D sector) 19878 16725

MoES 9506 1901

DST 21596 5321

DBT 11804 2580

DSIR including CSIR 17896 4895

DOS 39750 11538Interim budget

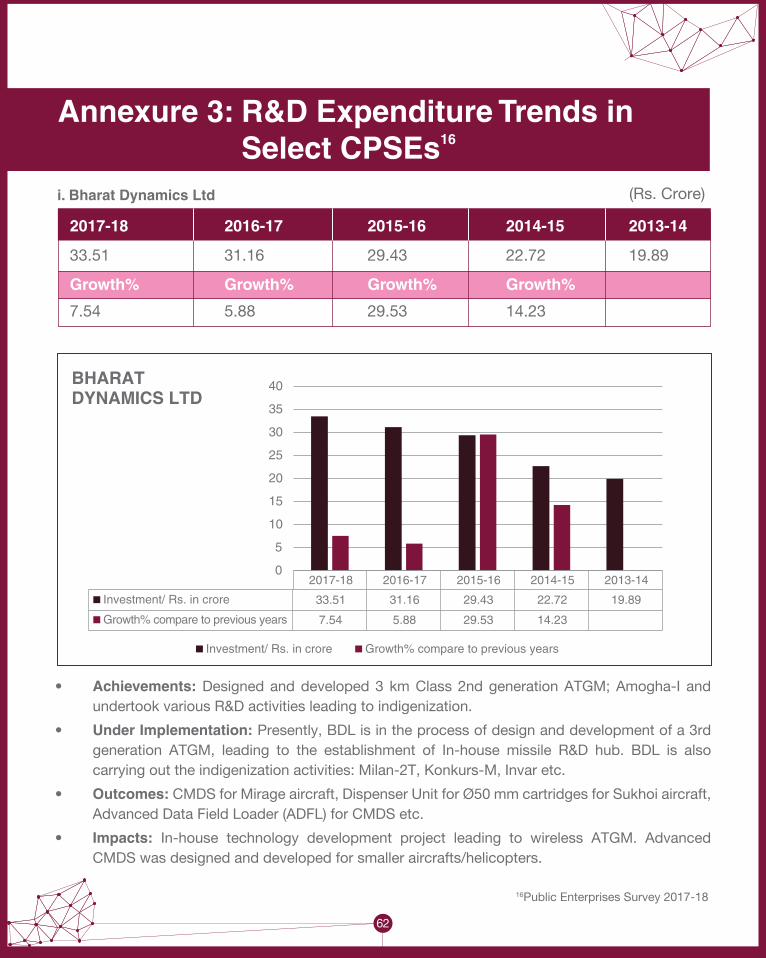

CPSEs12 : The second tier of this ecosystem are the CPSEs. They also contribute to the overall R&D spend in the country. The official source for data pertaining to R&D spend by CPSEs is DPE. This data does not tally with the data captured by DST. However, the variation is not very large. In the following tables and graphs, the major highlights of the R&D expenditure incurred by CPSEs are discussed. The R&D expenditure trends in select CPSEs are placed at Annexure 3. The brief CPSE highlights are placed at Annexure 4.

Out of 257 operating CPSEs in 2017-18, only 65 CPSEs are incurring expenditure on R&D, though the guidelines stipulate that profit making CPSEs may earmark certain portion of their profit for R&D. All profit making CPSEs do not adhere to these guidelines. The total number of CPSEs incurring expenditure on R&D has been declining over the years. Notwithstanding this in absolute terms the total expenditure on R&D incurred by CPSEs on R&D has increased from Rs. 3360 crore in 2013-14 to Rs. 5612 crore in 2017-18. The percentage of R&D expenditure incurred by CPSEs as a proportion of Profit After Tax (PAT) and Total revenue has increased from 2.26 in 2013-14 to 4.38 in 2017-18 and from 0.16 in 2013-14 to 0.26 in 2017-18 respectively.

Issues:

• It is noteworthy that many Departments in Government of India other than scientific departments spend on R&D.

• In the absence of a separate accounting head it is difficult to capture the expenditure on R&D in the entire central government sector.

• Secondly, many scientific departments incur expenditure on commercialization of R&D without any clear outcome and impact.

• In the absence of a clear-cut guidance on commercialization, many R&D expenditures could end up as wasteful expenditure.

34

12DPE

35

65

81

6772 69

2013-14 2014-15 2015-16 2016-17 2017-18

No. of CPSEs

Figure 16: Amount of R&D Expenditure of operating CPSEs in last 5 years (Rs in Crores)

Figure 15: Number of Operating CPSEs incurring Expenditure on R&D in last 5 years

Figure 17: % of R&D expenditure incurred by Operating CPSEs in last 5 years

3360.66

2591.29

3611.46

5016.985612.3

2013-14 2014-15 2015-16 2016-17 2017-18

R&D Expenditure incurred by Operating CPSEs

2.62

0.16 0.13 0.2 0.260.26

2.52

3.16

44.38

2013-14 2014-15 2015-16 2016-17 2017-18

R&D as% PAT R&D as% of Total Revenue

The Sectoral break of R&D expenditure in CPSEs for last 5 years is given in Annexure 5. The Figure 18 shows the average annual growth rate in R&D expenditure sector wise. It can be seen that the petroleum sector has registered the highest growth rate in R&D expenditure during 2017-18 (an increase of ~12%) compared to the greatest dip in the growth rate of R&D expenditure in power generation sector which saw a decline of about 14% during this period.

Figure 18: Average Annual Growth Rate (%) (2017-18)

Table 6: Top Five CPSEs Incurring Maximum Expenditure on R&D

S. No. Expenditure on Research & Development (`in Crores) 2017-18

1 Hindustan Aeronautics LTD. 1611.86

2 Bharat Electronics LTD. 938.51

3 Bharat Heavy Electricals LTD. 752.64

4 Oil & Natural Gas Corporation LTD. 586.23

5 Steel Authority of India LTD. 335.5

36

Average Annual Growth Rate (%) (2017-18)

Heavy & MediumEngineering

Petroleum (Refinery& Marketing

Crude Oil Contract &Construction and

Tech. Consultancy Services

6.14

11.62

0.16

-14.08

4.42

PowerGeneration

Issues: • The major issue is that notwithstanding the detailed guidelines on R&D, the CPSEs are

not incurring R&D expenditure as it is not being monitored closely.• The second issue is that the MoU guidelines which require specific target setting are

also not closely watched. • The third issue is that the outcome of expenditure on R&D is not clearly visible nor is

there any structured collaboration with academia.

Private Sector13: The third tier in the ecosystem is the private sector. The data pertaining to the expenditure trends in the private sector is captured by both DST and MCA. It is however pertinent to mention that while DST data is in public domain, MCA data is not in public domain. Notwithstanding this it was found that there is a huge discrepancy in the data published by DST and the data received from MCA. The extent of discrepancy is as follows: As per data received from MCA, on 31.03.2017, the total number of registered companies were 1641333 out of which total number of registered and active companies was 1169303. The total number of companies which filed annual financial statements was 713088 out of which 46567 companies filed their financial statements in XBRL format. The total number of registered and active companies incurring expenditure on R&D were only 6104 and the total expenditure on R&D incurred by them was INR 3918.3 crore. These R&D data figures are completely at variance with the data reported by DST, as per which private investment in R&D in 2016-17 is INR 43995 crore. Since MCA is the official primary source of all data relating to companies registered under the Companies Act, data furnished by MCA has been quoted in this document in order to reflect the extent of discrepancy with DST data. This could be due to different methodologies adopted in collecting relevant data from companies. The methodology of data capturing as adopted by MCA for R&D expenditure is given in Annexure 6. The summary point is that this huge discrepancy needs to be addressed by examining the financial statements of each R&D incurring company.

The top 5 private companies that have the maximum R&D expenditure in FY 2017 are shown in Figure 19:

Figure 19: R&D Expenditure in XBRL_300500

37

13MCA

453.2414.4

162.57 145.86

SAP Labs IndiaPrivate Limited

Mphasis Limited Olympia Tech Park (Chennai) Private Limited

Nuevosol EnergyPrivate Limited

Sun PharmaAdvanced Research

Company Limited

230.3

R&D Expenditure in (In Rs. Crore) XBRL_300500

14RBI

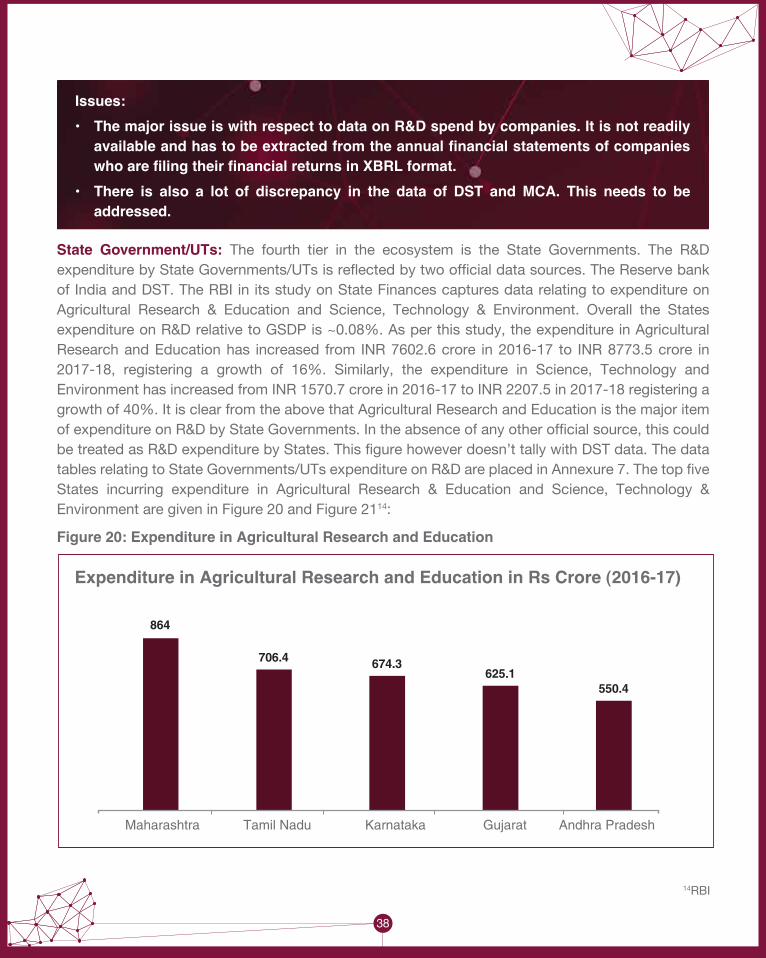

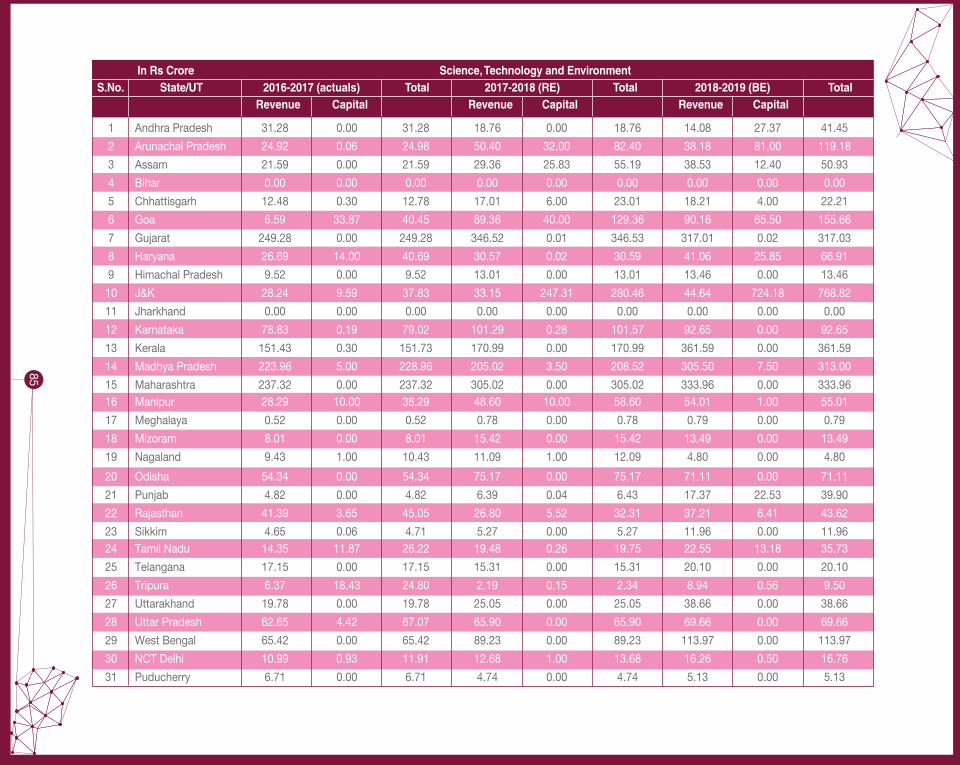

State Government/UTs: The fourth tier in the ecosystem is the State Governments. The R&D expenditure by State Governments/UTs is reflected by two official data sources. The Reserve bank of India and DST. The RBI in its study on State Finances captures data relating to expenditure on Agricultural Research & Education and Science, Technology & Environment. Overall the States expenditure on R&D relative to GSDP is ~0.08%. As per this study, the expenditure in Agricultural Research and Education has increased from INR 7602.6 crore in 2016-17 to INR 8773.5 crore in 2017-18, registering a growth of 16%. Similarly, the expenditure in Science, Technology and Environment has increased from INR 1570.7 crore in 2016-17 to INR 2207.5 in 2017-18 registering a growth of 40%. It is clear from the above that Agricultural Research and Education is the major item of expenditure on R&D by State Governments. In the absence of any other official source, this could be treated as R&D expenditure by States. This figure however doesn’t tally with DST data. The data tables relating to State Governments/UTs expenditure on R&D are placed in Annexure 7. The top five States incurring expenditure in Agricultural Research & Education and Science, Technology & Environment are given in Figure 20 and Figure 2114:

Figure 20: Expenditure in Agricultural Research and Education

38

Issues: • The major issue is with respect to data on R&D spend by companies. It is not readily

available and has to be extracted from the annual financial statements of companies who are filing their financial returns in XBRL format.

• There is also a lot of discrepancy in the data of DST and MCA. This needs to be addressed.

Expenditure in Agricultural Research and Education in Rs Crore (2016-17)

864

706.4 674.3625.1

550.4

Maharashtra Tamil Nadu Karnataka Gujarat Andhra Pradesh

39

Figure 21: Expenditure in Science, Technology and Environment

249.3237.3 229

151.7

79

Gujarat Maharashtra Madhya Pradesh Kerala Karnataka

Expenditure in Science, Technology and Environment in RS Crore (2016-17)

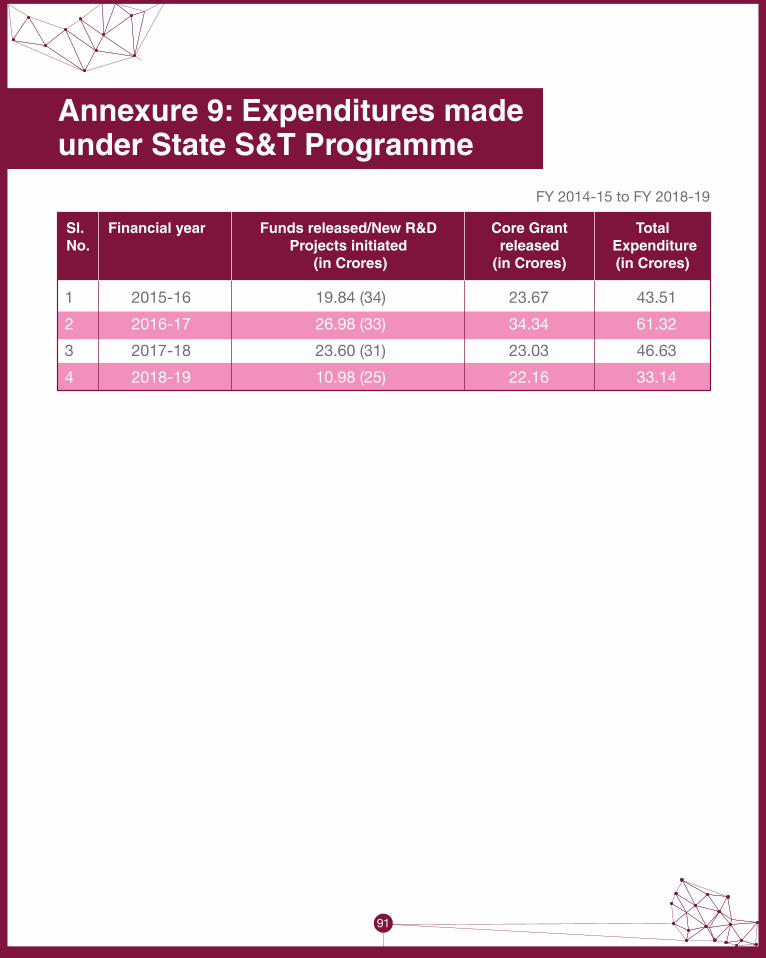

DST has initiated a State S&T Programme (SSTP) and has facilitated establishment of State S&T Councils under State S&T Programme (SSTP) with specific objectives of spreading awareness, building capacity, promoting innovation, and boosting up India’s indigenous capabilities to solve various location specific challenges. The Core support to S&T Councils and the details of expenditures made under the State S&T Programme from FY 2014-15 to current year by DST are given in Annexures 8 and 9 respectively.

Issues: • The state budgets do not reflect R&D spend directly. It is merged in agricultural

research or with science, technology and environment heads. It therefore useful to have a separate accounting head for R&D in states.

Educational Institutions: The fifth tier in the ecosystem is the educational institution. Higher education is critical for developing a modern economy, a just society and a vibrant polity. It equips young people with skills relevant for the labour market and the opportunity for social mobility. It provides people already in employment with skills to negotiate rapidly evolving career requirements. It is estimated that developed economies and even China will face a shortage of about 40 million highly skilled workers by 2020, while, based on current projections of higher education, India is likely to see some surplus of graduates in 2020. Thus, India could capture a higher share of global knowledge-based work, by increasing its exports of knowledge-intensive goods and R&D services, if there is adequate focus on higher education and its research quality is globally benchmarked.

The data for R&D spends in higher educational institutions is not readily available in Ministry of Human Resource Development. However as per the information provided by MHRD, the top five institutions and the amount spend by them on R&D is indicated in Table 7:

Table 7: Top Five Institutions & Amount Spend on R&D

Educational Institutions: The fifth tier in the ecosystem is the educational institution. Higher education is critical for developing a modern economy, a just society and a vibrant polity. It equips young people with skills relevant for the labour market and the opportunity for social mobility. It provides people already in employment with skills to negotiate rapidly evolving career requirements. It is estimated that developed economies and even China will face a shortage of about 40 million highly skilled workers by 2020, while, based on current projections of higher education, India is likely to see some surplus of graduates in 2020. Thus, India could capture a higher share of global knowledge-based work, by increasing its exports of knowledge-intensive goods and R&D services, if there is adequate focus on higher education and its research quality is globally benchmarked.

The data for R&D spends in higher educational institutions is not readily available in Ministry of Human Resource Development. However as per the information provided by MHRD, the top five institutions and the amount spend by them on R&D is indicated in Table 7:

Table 7: Top Five Institutions & Amount Spend on R&D

S.No. Name of IIT Research Grant Received from GoI (Rupees in crore) 2016-17 2017-18 2018-19 Total1 IIT Madras 188.87 277.24 536.55 1002.66

2 IIT Bombay 282.34 282.02 250.93 815.29

3 IIT Kharagpur 161.65 222.14 138.76 522.55

4 IIT Delhi 97.03 236.85 154.24 488.12

5 IIT Kanpur 87.03 110.59 119.28 316.90

The only available data in public domain is maintained by DST, as per which the higher educational institutions play a secondary role in national R&D spend. 12th FYP had therefore observed that India must develop world class research universities as well as have sophisticated teaching institutions to impart key vocational and generic skills in a timely manner to cope with the rapidly changing market needs. This would create an ecosystem to foster R&D in educational institutions. The resources for this could be garnered by earmarking a certain proportion of education cess toward research.

Issues: • There is no consolidated information available on R&D spend by higher education

institutions. • The list of R&D projects being undertaken is not also available in public domain

though they are incurred from public sources. • There is no institutional mechanism for industry and academia collaboration on

research. • The quality of research and its outcome is not available in public domain.

40

41

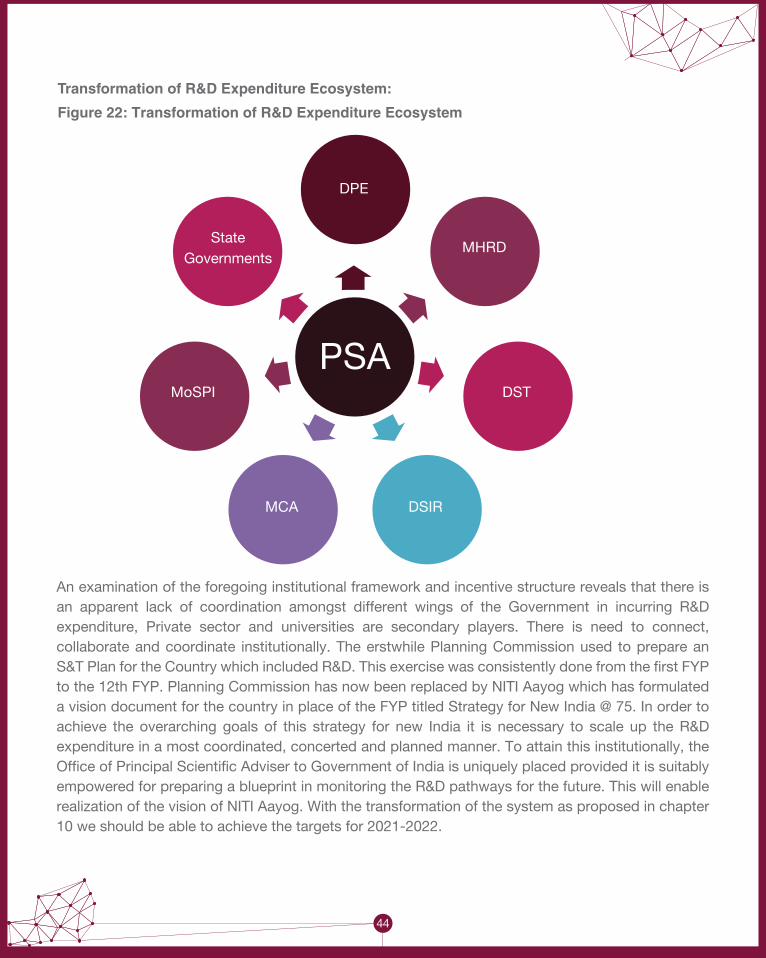

The institutional elements of R&D ecosystem revolve around six stakeholders. They are DST, DSIR, DPE, MHRD State Governments and MCA.

Department of Science & Technology:

DST is a major stakeholder in the R&D ecosystem. As per allocation of business rules of Government of India, DST is responsible for science & technology policy and also data compilation on R&D. Accordingly, it has a significant role to play.

The S&TI policy of the Government of India as formulated by DST was published in 2013. As per this, India's R&D investment is currently under 1% of the GDP. Increasing Gross Expenditure in Research and Development (GERD) to 2% of the GDP has been a national goal for some time. Achieving this in the next five years (2018) is realizable if the private sector raises its R&D investment to at least match the public sector R&D investment from the current ratio of around 1:1.4 which is as per DST data. The implementation of policy has however not resulted in achieving the target of 2% of GDP. Secondly, the data compiled by DST comes with a long-time lag and does not tally with data disseminated by other stakeholders.