q3 report 2013€¦ · • project office in kista for agile development close to a client ......

TRANSCRIPT

2013-10-25 Q3 report 1

Q3 Report 2013

• Quiet but stable business period • Improved profit • Strong development in International and Finland • Mixed market signals • High potential in new contracts in public

sector and good development in industry segment • Project office in Kista for agile development close to a client • Cybercom was named the best IT workplace 2013 in Poland

Highlights Q3

2013-10-25 Q3 report 2

• OH cost -7 MSEK • 18% lower administrative staff • Good development International and Finland • Sales reduction in the Swedish operations is

still negatively affecting profitability

Q3 2013

2013-10-25 Q3 report 3

SEK million Q3 2013 Q3 2012 Sales 249.3 273.9 Employees 1,243 1,365 EBIT 8.6 -2.9 EBIT % 3.4% -1.1% Profit after tax 4.8 -4.3 Cash flow 3.9 -85.4 EPS, SEK 0.03 -0.08 Equity/assets ratio % 69.8% 56.6%

• Sales decrease by 9% • Currency effects on sales + SEK 1.5

million • Calendar effect of +1 day • 122 fewer employees

Rolling Twelve Months

2013-10-25 Q3 report 4

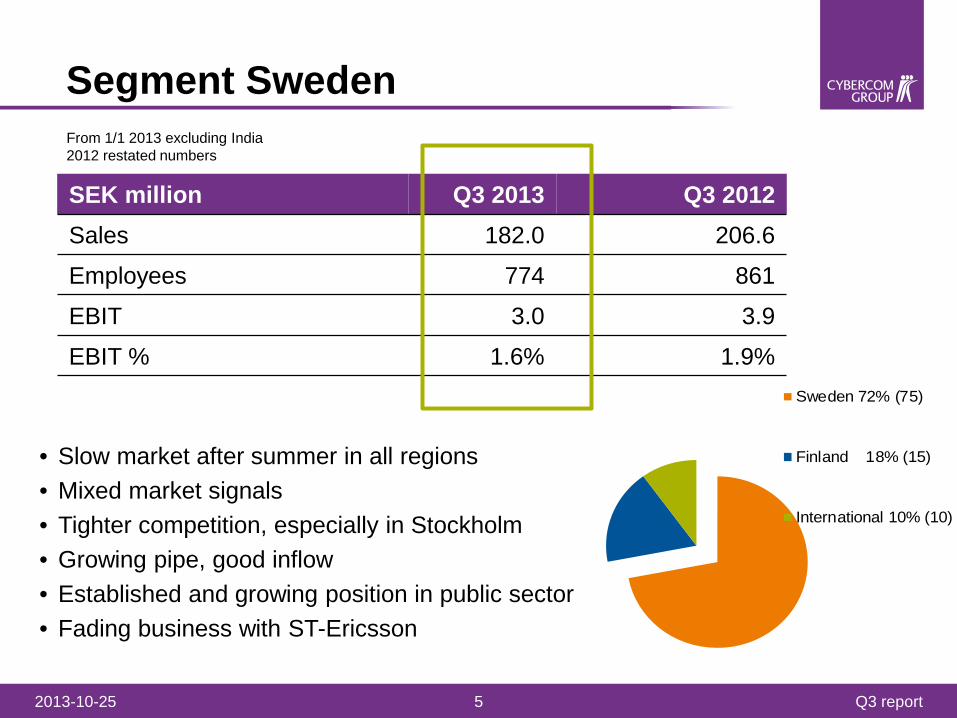

Segment Sweden

2013-10-25 Q3 report 5

• Slow market after summer in all regions • Mixed market signals • Tighter competition, especially in Stockholm • Growing pipe, good inflow • Established and growing position in public sector • Fading business with ST-Ericsson

SEK million Q3 2013 Q3 2012 Sales 182.0 206.6

Employees 774 861

EBIT 3.0 3.9

EBIT % 1.6% 1.9% Sweden 72% (75)

Finland 18% (15)

International 10% (10)

From 1/1 2013 excluding India 2012 restated numbers

SEK million Q3 2013 Q3 2012 Sales 44.7 43.3

Employees 246 264

EBIT 1.0 -2.2

EBIT % 2.2% -5.1%

Segment Finland

2013-10-25 Q3 report 6

Sweden 72% (75)

Finland 18%(15)

International 10% (10)

• Continued recovery top line and profit • Increasing sales per employee • Successful development in Public and Industry • Mixed market, tough competition

Segment International

2013-10-25 Q3 report 7

Sweden 72% (75)

Finland 18% (15)

International10% (10)

• Good turnaround in profit • Good contribution from the Connectivity management

assignments in Africa • Satisfied development in Denmark • New clients in local market Poland, establishing

Connectivity management

SEK million Q3 2013 Q3 2012 Sales 32.1 33.7

Employees 207 217

EBIT 2.9 -0.3

EBIT % 9.0% -0.9%

From 1/1 2013 including India 2012 restated numbers

Stable Cash Flow

2013-10-25 Q3 report 8

• Activities to improve tied-up capital having positive effect on working capital • Factoring in Sweden ended • Loan amortisation started according to plan

Cybercom Group, SEK millionQ3

2013Q3

2012Jan - Sep

2013Jan - Sep

2012 2012 RTM

Cash f low before changes in w orking capital 3.5 0.2 9.5 -4.3 16.8 30.6Changes in w orking capital 0.4 -85.6 60.3 -71.9 -117.5 14.7Cash flow from operating activities 3.9 -85.4 69.8 -76.2 -100.7 45.3Investments in tangible and intangible f ixed assets -1.1 -8.0 -7.0 -15.1 -15.2 -7.1Acquisition in subsidiaries/net assets - - -0.7 -4.5 -4.5 -0.7Divestment of subsidiaries - -1.7 - -7.1 -7.4 -0.3Other items 0.1 0.2 0.1 0.2 0.1 0.1Cash flow from investing activities -1.0 -9.5 -7.6 -26.5 -27.0 -8.0New share issue -0.1 -0.1 -0.1 -0.1 115.8 115.8Change in factoring and overdraft facilities - 55.4 -43.4 94.0 43.4 -94.0Change in other f inancial liabilities 1.4 5.2 -11.1 -21.0 -70.4 -60.5Cash flow from financing activities 1.3 60.5 -54.6 72.9 88.8 -38.7Period's cash flow 4.2 -34.4 7.6 -29.8 -38.9 -1.4Cash and cash equivalents at period's start 23.2 65.2 20.3 62.4 62.4 29.1Exchange differences in cash and cash equivalents -0.8 -1.7 -1.3 -3.5 -3.2 -1.1

Cash and cash equivalents at period's end 26.6 29.1 26.6 29.1 20.3 26.6

ICT market growth as a whole is forecasted 2,2%, where services is forecasted to grow 3,0% (Gartner)

Connectivity, mobility and the cloud – main trends driving

ICT market Public e-services increases i.e. eHealth, eMed, eEducation Connected industry are taking form – M2M,smart home,

smart plants, monitoring, analyse, decrease waste • Mixed market signals in the Nordics short term demand • Good inflow, but long decision times • A highly competitive landscape

– Gigants has entered the market – Brokers are here to stay – Niche companies are growing – Pricing is more volatile

The Market

2013-10-25 Q3 report 9

Sales highlights

2013-10-25 Q3 report 10

• The ten largest clients 45% (48) of sales • The largest single client 14% (11) of sales • Framework agreement clients 64% (59)

– New agreements with the Swedish Tax Agency and Saab

• Turnkey assignments 38% (39) • Major clients

– Alma Media, Ericsson, Millicom, MTV Media, Outotec, SAAB, Sony Mobile, TeliaSonera, the Swedish Transport Administration and Volvo

Cybercom’s business domains

2013-10-25 Q3 report 11

• Assuring the end to end security, reducing business risk • 5% of sales • High potential for growth • Swedish Tax Agency, SL, EIdentification Board

• Designing and adding needed intelligence to clients’ products/devices

• 45% of sales • Strong future market • Wireless Maingate, Ericsson,

Helsingin Energia Saab, QlikTech, Verisure, Kone, Outotec,

• Assuring the connectivity, making networks efficient and manageable

• 8% of sales • International market • Millicom , Emtel Mauritius,

Celcom Malaysia

• Providing the future connected world solutions, for people and devices

• 42% of sales • Broad market but intensified

competition • eGovernment Delegation

Finland’s Board of Education, MTV Media

References

2013-10-25 Q3 report 12

M2M

2013-10-25 Q3 report 13

eHealth

2013-10-25 Q3 report 14

Market & Stakeholders

2013-10-25 Q3 report 15

• Connectivity – our strong position – M2M – eHealth – Cloud

• The Nordics is main market • Continuous improvement • Balanced focus on Public, Industry

and Telecom • Broader footprint with key clients • Prime Brand in Connectivity for talents and clients

Going forward

2013-10-25 Q3 report 16

Main shareholders

2013-10-25 Q3 report 17

Shareholder Holding %JCE GROUP AB 38.70 %Swedbank Robur funds 8.20 %Didner & Gerge Fonder Aktiebolag 4.64 %SEB LIFE INTERNATIONAL ASSURANCE 3.88 %FÖRSÄKRINGSAKTIEBOLAGET, AVANZA PENSION 3.86 %JCE SECURITIES AB 2.62 %NORDNET PENSIONSFÖRSÄKRING AB 2.27 %HASSBJER DEVELOPMENT AB 1.97 %GRANIT SMÅBOLAG 1.16 %SUNDMAN, DAG OLOFSSON 1.15 %HANSSON, LARS ERIK 0.84 %CONSAFE SECURITIES AB 0.83 %TEQUITY AB 0.82 %THURESSON, MARCUS 0.62 %METZLER INTL INVESTMENTS PLC /, METZLER EUROPEAN 0.57 %

2013-10-25 Q3 report 18