q3 2012 investor relation presentation

TRANSCRIPT

November 2012

Q3 2012

INVESTOR PRESENTATION

This document does not constitute or form part of and should not be construed as, an offer to sell or issue or the solicitation of an offer to buy or acquire securities of AFI Development Plc (the "Company") or any of its subsidiaries in any jurisdiction or an inducement to enter into investment activity. No part of this document, nor the fact of its distribution, should form the basis of, or be relied on in connection with, any contract or commitment or investment decision whatsoever. No representation, warranty or undertaking, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or the opinions contained herein. None of the Company or any of its affiliates, advisors or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with the document.

This communication is only being distributed to and is only directed at (1) qualified institutional buyers (within the meaning of Rule 144A of the United States Securities Act of 1933, as amended (the "Securities Act") or (2) accredited investors (as defined in Rule 501(a) of Regulation D adopted pursuant to the Securities Act). Any person who is not a "qualified institutional buyer" or "accredited investor" should not act or rely on this document or any of its contents.

This document contains "forward-looking statements", which include all statements other than statements of historical facts, including, without limitation, any statements preceded by, followed by or that include the words "targets", "believes", "expects", "aims", "intends", "will", "may", "anticipates", "would", "could" or similar expressions or the negative thereof. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors beyond the Company's control that could cause the actual results, performance or achievements of the Company to be materially different from future results, performance or achievements expressed or implied by such forward-looking, including, among others, the achievement of anticipated levels of profitability, growth, cost and synergy of recent acquisitions, the impact of competitive pricing, the ability to obtain necessary regulatory approvals and licenses, the impact of developments in the Russian economic, political and legal environment, volatility in stock markets or in the price of our shares or GDRs, financial risk management and the impact of general business and global economic conditions.

Such forward-looking statements are based on numerous assumptions regarding the Company's present and future business strategies and the environment in which the Company will operate in the future. By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. These forward-looking statements speak only as at the date as of which they are made, and the Company expressly disclaims any obligation or undertaking to disseminate any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company's expectations with regard thereto or any change in events, conditions or circumstances on which any such statements are based.

Neither the Company, nor any of its agents, employees or advisors intends or has any duty or obligation to supplement, amend, update or revise any of the forward-looking statements contained in this document.

The information contained in this document is provided as at the date of this document and is subject to change without notice.

2

Disclaimer

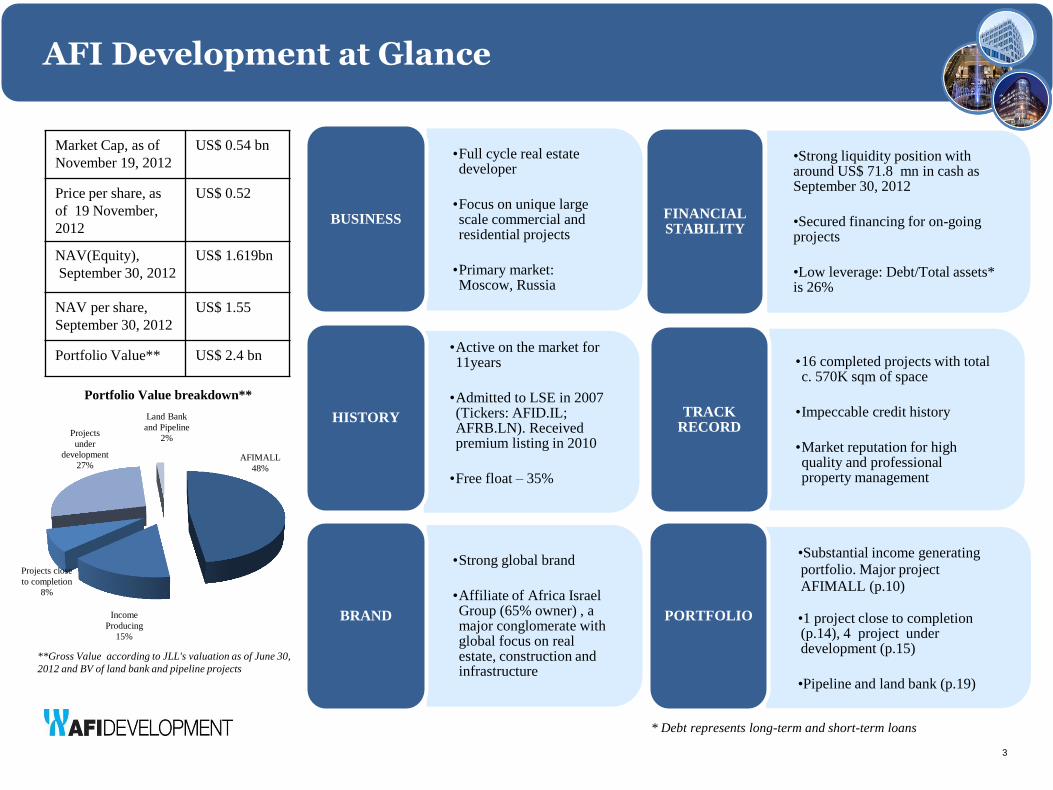

Portfolio Value breakdown**

•Full cycle real estate developer

•Focus on unique large scale commercial and residential projects

•Primary market: Moscow, Russia

BUSINESS

•Active on the market for 11years

•Admitted to LSE in 2007 (Tickers: AFID.IL; AFRB.LN). Received premium listing in 2010

•Free float – 35%

HISTORY

•Strong global brand

•Affiliate of Africa Israel Group (65% owner) , a major conglomerate with global focus on real estate, construction and infrastructure

BRAND

•Strong liquidity position with around US$ 71.8 mn in cash as September 30, 2012

•Secured financing for on-going projects

•Low leverage: Debt/Total assets* is 26%

FINANCIAL STABILITY

•16 completed projects with total c. 570K sqm of space

•Impeccable credit history

•Market reputation for high quality and professional property management

TRACK RECORD

•Substantial income generating

portfolio. Major project

AFIMALL (p.10)

•1 project close to completion (p.14), 4 project under development (p.15)

•Pipeline and land bank (p.19)

PORTFOLIO

3

Market Cap, as of

November 19, 2012

US$ 0.54 bn

Price per share, as

of 19 November,

2012

US$ 0.52

NAV(Equity),

September 30, 2012

US$ 1.619bn

NAV per share,

September 30, 2012

US$ 1.55

Portfolio Value** US$ 2.4 bn

* Debt represents long-term and short-term loans

AFI Development at Glance

**Gross Value according to JLL's valuation as of June 30,

2012 and BV of land bank and pipeline projects

AFIMALL

48%

Income

Producing

15%

Projects close

to completion

8%

Projects

under

development

27%

Land Bank

and Pipeline

2%

Current Portfolio

4 Note: the NOI projections are “forward looking statements” based on JLL valuation assumptions and Company estimations and they can be realized or not realized due to factors beyond the Company's control including, among

others, the impact of competitive pricing, the ability to obtain necessary regulatory approvals and licenses, the impact of developments in the Russian economic, political and legal environment, volatility in stock markets or in the price

of our shares or GDRs, financial risk management and the impact of general business and global economic conditions

Key Projects in Moscow

Yielding Assets / Trading Stock

Projects close to completion

Development Projects

Pipeline and Land Bank

Value (JLL): US$ 1.5 bn

GLA: 174.5K sqm (excl. hotels)

NOI stab.: US$ 196.7 mn (AFID share)

GSA: 1.4K sqm Price psqm: 13K – 15K

Number of keys: 568 keys

Value(JLL): US$ 193.7 mn

GLA: 51K sqm

NOI stab.

(AFID share): US$ 21 mn

Value(JLL): US$ 668.6 mn

GLA: 227 K sqm

NOI stab. US$ 145 mn

(AFID share):

GSA: 501.2K sqm

CF from sale: US$ 1.9bn

Value(JLL): US$ 211 mn

BV:

(as of 30.06.12): US$ US$ 37 mn

Ownership:50%

AFIMALL City Berezkovskaya Aquamarine II

H2O Four Winds

Aquamarine

Hotel Paveletskaya, 1

Aquamarine III

Kosinskaya

Otradnoe Pochtovaya

Plaza SPA*

Other

projects

Plaza Spa*

*Outside of

Moscow

Other

Tverskaya

Plazas

Tverskaya

Plazas Ib&II

Others

Portfolio Overview

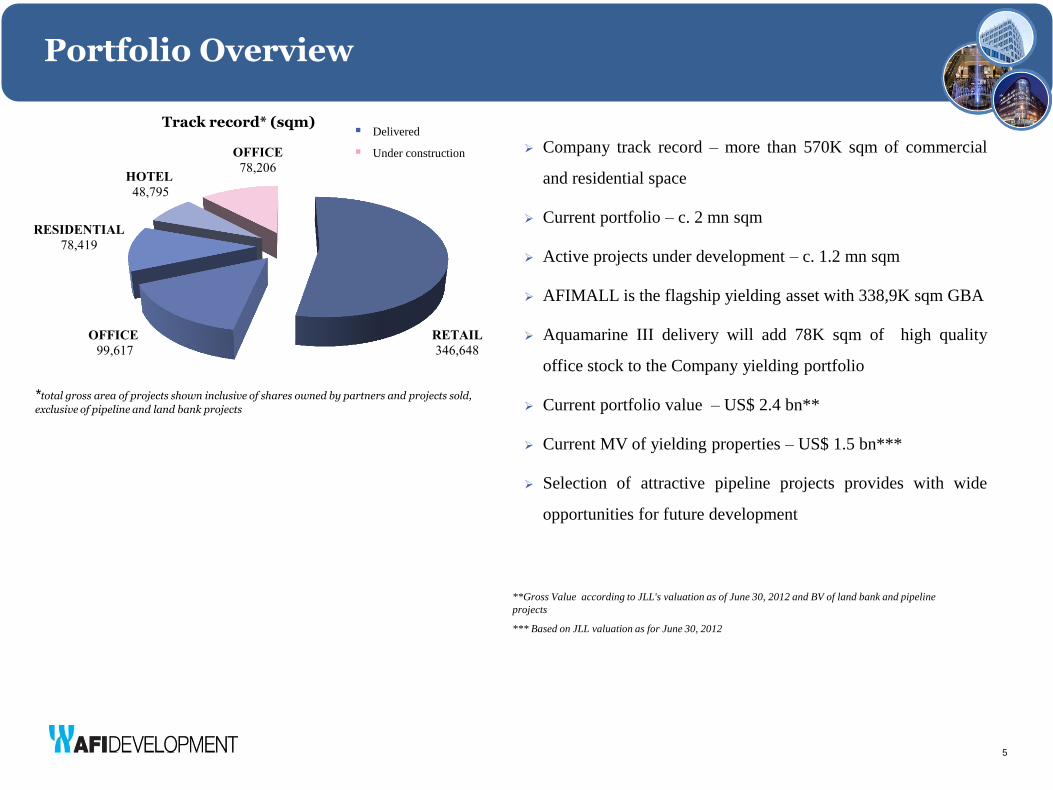

Track record* (sqm)

*total gross area of projects shown inclusive of shares owned by partners and projects sold,

exclusive of pipeline and land bank projects

Company track record – more than 570K sqm of commercial

and residential space

Current portfolio – c. 2 mn sqm

Active projects under development – c. 1.2 mn sqm

AFIMALL is the flagship yielding asset with 338,9K sqm GBA

Aquamarine III delivery will add 78K sqm of high quality

office stock to the Company yielding portfolio

Current portfolio value – US$ 2.4 bn**

Current MV of yielding properties – US$ 1.5 bn***

Selection of attractive pipeline projects provides with wide

opportunities for future development

5

Delivered

Under construction

RETAIL

346,648

OFFICE

99,617

RESIDENTIAL

78,419

HOTEL

48,795

OFFICE

78,206

**Gross Value according to JLL's valuation as of June 30, 2012 and BV of land bank and pipeline

projects

*** Based on JLL valuation as for June 30, 2012

SECTION 1

Company Update

Projects Update in Q2 2012

7

OP

ER

AT

ION

AL

UP

DA

TE

:

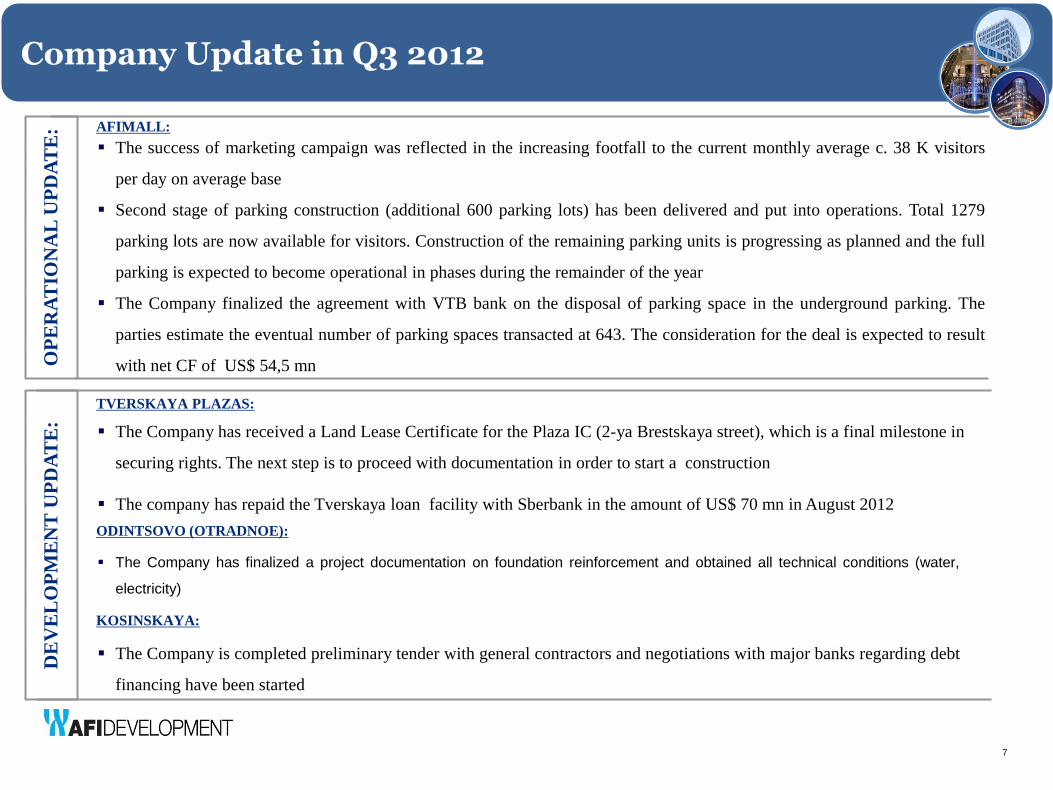

The success of marketing campaign was reflected in the increasing footfall to the current monthly average c. 38 K visitors

per day on average base

Second stage of parking construction (additional 600 parking lots) has been delivered and put into operations. Total 1279

parking lots are now available for visitors. Construction of the remaining parking units is progressing as planned and the full

parking is expected to become operational in phases during the remainder of the year

The Company finalized the agreement with VTB bank on the disposal of parking space in the underground parking. The

parties estimate the eventual number of parking spaces transacted at 643. The consideration for the deal is expected to result

with net CF of US$ 54,5 mn

The Company is completed preliminary tender with general contractors and negotiations with major banks regarding debt

financing have been started

The Company has finalized a project documentation on foundation reinforcement and obtained all technical conditions (water,

electricity)

AFIMALL:

DE

VE

LO

PM

EN

T U

PD

AT

E:

TVERSKAYA PLAZAS:

The Company has received a Land Lease Certificate for the Plaza IC (2-ya Brestskaya street), which is a final milestone in

securing rights. The next step is to proceed with documentation in order to start a construction

The company has repaid the Tverskaya loan facility with Sberbank in the amount of US$ 70 mn in August 2012

ODINTSOVO (OTRADNOE):

KOSINSKAYA:

Company Update in Q3 2012

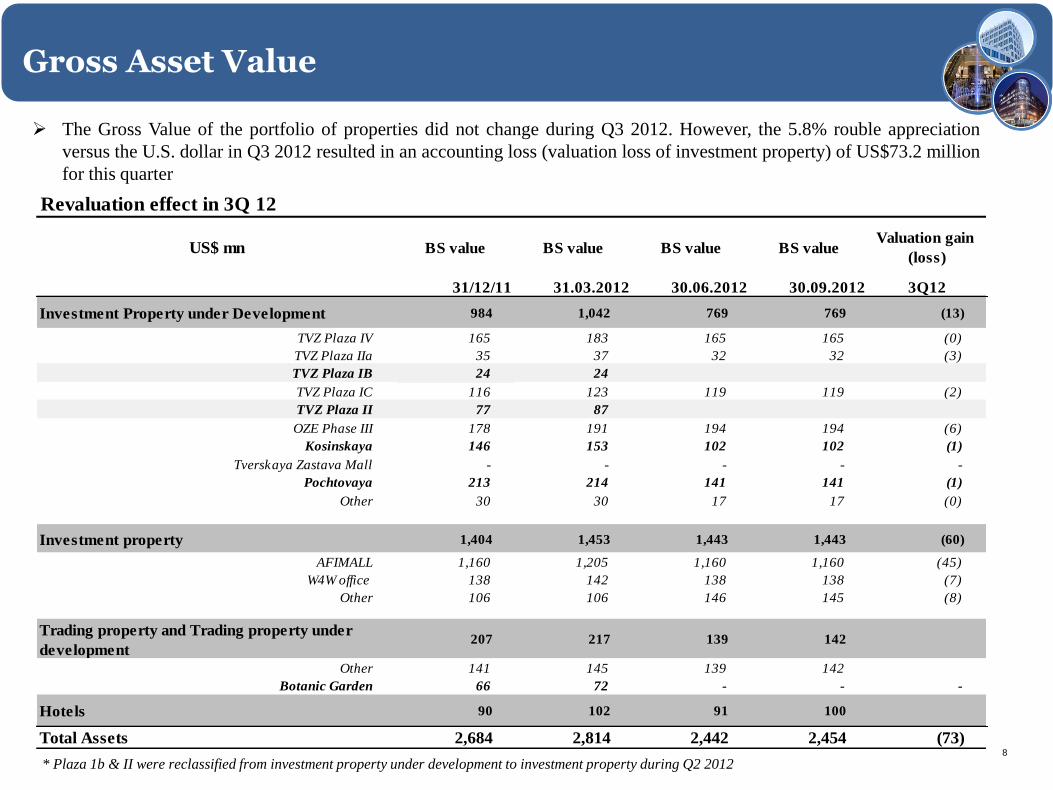

Revaluation effect in 3Q 12

US$ mn BS value BS value BS value BS value Valuation gain

(loss)

31/12/11 31.03.2012 30.06.2012 30.09.2012 3Q12

Investment Property under Development 984 1,042 769 769 (13)

TVZ Plaza IV 165 183 165 165 (0)

TVZ Plaza IIa 35 37 32 32 (3)

TVZ Plaza IB 24 24

TVZ Plaza IC 116 123 119 119 (2)

TVZ Plaza II 77 87

OZE Phase III 178 191 194 194 (6)

Kosinskaya 146 153 102 102 (1)

Tverskaya Zastava Mall - - - - -

Pochtovaya 213 214 141 141 (1)

Other 30 30 17 17 (0)

Investment property 1,404 1,453 1,443 1,443 (60)

AFIMALL 1,160 1,205 1,160 1,160 (45)

W4W office 138 142 138 138 (7)

Other 106 106 146 145 (8)

Trading property and Trading property under

development207 217 139 142

Other 141 145 139 142

Botanic Garden 66 72 - - -

Hotels 90 102 91 100

Total Assets 2,684 2,814 2,442 2,454 (73)

8

Gross Asset Value

8

Gross Asset Value

The Gross Value of the portfolio of properties did not change during Q3 2012. However, the 5.8% rouble appreciation

versus the U.S. dollar in Q3 2012 resulted in an accounting loss (valuation loss of investment property) of US$73.2 million

for this quarter

* Plaza 1b & II were reclassified from investment property under development to investment property during Q2 2012

Projects Update

SECTION 2

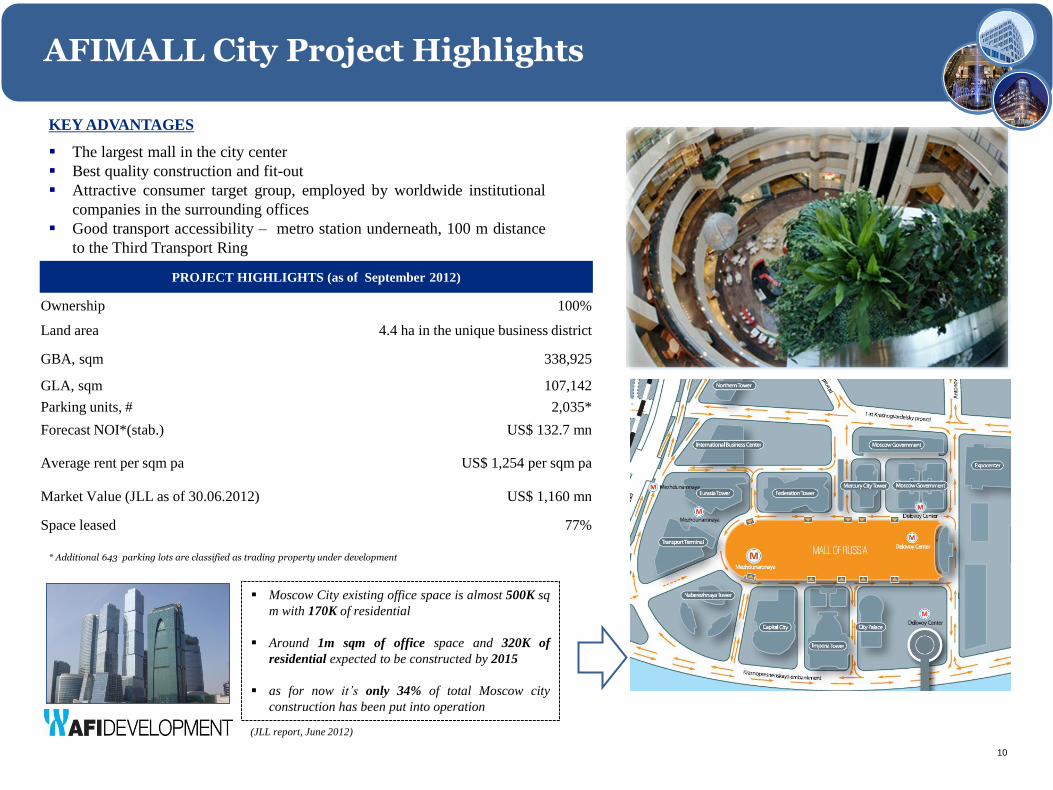

AFIMALL City Project Highlights

* Additional 643 parking lots are classified as trading property under development

KEY ADVANTAGES

The largest mall in the city center

Best quality construction and fit-out

Attractive consumer target group, employed by worldwide institutional

companies in the surrounding offices

Good transport accessibility – metro station underneath, 100 m distance

to the Third Transport Ring

10

PROJECT HIGHLIGHTS (as of September 2012)

Ownership 100%

Land area 4.4 ha in the unique business district

GBA, sqm 338,925

GLA, sqm 107,142

Parking units, # 2,035*

Forecast NOI*(stab.) US$ 132.7 mn

Average rent per sqm pa US$ 1,254 per sqm pa

Market Value (JLL as of 30.06.2012) US$ 1,160 mn

Space leased 77%

Moscow City existing office space is almost 500K sq

m with 170K of residential

Around 1m sqm of office space and 320K of

residential expected to be constructed by 2015

as for now it’s only 34% of total Moscow city

construction has been put into operation

(JLL report, June 2012)

AFIMALL City Operational Summary

NEXT STEPS ON TRACK TO PROJECT PROMOTION

Improve operations at AFIMALL

get permission documents for the whole underground parking by the end of 2012

Increase occupancy level and number of visitors

Stabilize tenant mix through reduction of tenants rotation

11

OPERATION:

The footfall has increased in Q3 compare to Q2 and reached c. 38 K visitors per day on average

Average base rental rate - US$ 1,254* psm pa

The Company is testing various tariff schemes in order to increase the amount of visitors that use AFIMALL’s parking. One of the schemes is free parking in the evening during the working days

Availability of the parking is actively promoted through various media channels

The marketing campaign is in progress

AFIMALL PARKING:

Second stage of parking construction (additional 600 parking lots) has been delivered and put into operation. Total 1279 parking lots are now available for visitors

The Company finalized the agreement with VTB bank on the disposal of parking space in the underground parking. The parties estimate the eventual number of parking spaces transacted at 643. The consideration for the deal is expected to result with net CF of US$ 54,5 mn

Daily average footfall in AFIMALL (‘000 visitors)

2012

38К

0

5

10

15

20

25

30

35

40

45

*(after indexation and before discounts provided)

Building Kalinina TOTAL

Ownership 100% 50% 74% 99.1% 100% 50% 100% 100% 100% 50% 100%

Moscow Moscow Moscow Moscow Moscow Moscow Moscow Moscow Moscow Kavkaz Kavkaz

GBA, sqm 338,925 31,000 11,612 16,512 10,698 4,925 5,700 2,095 11,130 25,000 9,526 462K

GLA, sqm 21,950 10,250 14,085 8,996 4,726 5,510 1,913 159 keys 274 keys 134 keys 174K

Parking lots (total), # 2,035 142 300 126 72 78 - - 15 - 15

Ocupancy rate, % 99% 98% 72%

Average rent, $/sq m 1,245 1,428 549 251 254 540 1,403 1,036 ADR 192 ADR 105 -

Market rent, US$, (JLL) 1,152 1,279 550 286 320 540 2,000 2,500 ADR 244 ADR 120 ADR 121

Class Retail Office B Office B Office B Street retail Street Hotel Hotel Hotel

12 months Forward E,

US$ mn**72.5 30.7 3.3 3.6 2.5 1.5 2.8 0.9 3.0 4.3 2.1 127

MV(AFID share),US$

mn**1,160 138 29.4 28.9 19 18 32 9 45 23 1,531

CAP Rate 30.6.12 - JLL 10% 10% 12% 13% 13.75% 9% 9%,13% 9%, 12.5% 9.5% 13% 13%

AFIMALL Four Winds BerezkovskayaPaveletskaya, bld.

1H2O

Location

77% 100% 94% 100%

107,142

31

Plaza Spa

92%

Aquamarine

Hotel

Four Winds

Fitness and RetailTvesrkaya Plaza II

Tverskaya Plaza

Ib

Street retail Office A

Yielding Properties

12

12

* Including parking area

** Based on JLL valuation as of 30.06.2012

*** Additional 643 parking lots are classified as trading property under development

*

***

Property under Construction

Ozerkovskaya III

14

KEY ADVANTAGES

Located in Zamoskvorechye, Moscow’s prestigious business

area within the Garden Ring

3-rd phase of Ozerkovskaya Embankment development site

4 Class A office buildings comprising one complex

ACTUAL PLAN:

The Company has delivered the project in Q2 2012; received

commissioning certificate in August 2012

The company works on refinancing construction loan facility

with lower interest rate payments and more favorable terms

TARGETS:

To get a ownership certificate in Q4 2012

To reduce current interest rate for the loan facility

Proceed with lease up/sale

PROJECT HIGHLIGHT 100 % of share

Year of construction 2012

Ownership 50%

Location Moscow

GBA 78.6K

GLA 51.1K

Parking units 557

MV (JLL valuation, as for 30.06.2012)

UD$ 387.3 mn

MV, AFID share only (JLL valuation, as for 30.06.2012)

US$ 193.7 mn

Loan Balance (30.06.2012)

US$ 24.2 mn

Projects under Development

Projects under Development

16

PARAMETERS DATA

Type Residential

Land plot, Ha 31.8

GBA, sqm 703.3K

GSA/GLA, sqm 436K/37K

Phase I:

GSA/GLA, sqm 142K/7,5K

Parking units, # 2,053

Outstanding investment

(Based on JLL, 30.06.12)

US$ 871 mn

Expected CF from Sales

(Based on JLL, 30.06.12)

US$ 1.3 bn

MV(JLL as f 30.06.2012) US$ 108.5 mn

PARAMETERS DATA

Type Retail

Land plot, Ha 8ha

GBA, sqm 111.7K

GLA, sqm 89.7K

Outstanding investment costs US$ 56mn

Stab. NOI (JLL est.) US$ 22.7K

MV(JLL as f 30.06.2012) US$ 102.3 mn

DESCRIPTION:

• Convenient access to the main motorways, close

proximity to nearest metro station

• Unique concept for accommodation of small

shops, offices, warehouses and retails

CURRENT PLAN:

• Project documentation on foundation

reinforcement issued

• The company obtained all technical conditions

(water, radio, electricity)

• Negotiations with potential anchor tenants are in

process

TARGETS:

• Finalize negotiation regarding bank financing

• Finalize construction

DESCRIPTION:

• Located on 32 ha site in the town of Odintsovo, one

of the newest and most environmentally clean areas

bordering Moscow

• Project includes multifunctional infrastructure with

schools, kindergardens and sports facilities for

children

• Construction permit received; tender for main

constructor has been issued

CURRENT PLAN:

• Construction site is fully mobilized. Renovation can be

start shortly in Q1 2013

• The Company is providing tender with general

contractors

• Negotiations with major banks concerning debt

financing have been started

TARGETS:

• Start renovation in Q1 2013

Projects under Development (1/2) K

OS

INS

KA

YA

O

TR

AD

NO

E

Projects next for Development

17

DESCRIPTION:

The project is located in the Moscow Central District

on the Yauza river bank; total site area is 5.65 ha

Attractive neighborhood which benefits from the

developed social infrastructure; transport, shops and

cultural amenities

CURRENT PLAN:

Based on the best-use concept the Company plans to

develop the project as a residential complex with

total GBA of 170K sqm. GZK is on place

TARGETS:

Finish design in 2013

PARAMETERS DATA

Type Residential

Land plot, Ha 5.65ha

GBA, sqm 170.3K

GSA/GLA, sqm 57.6K/37.2K

# of parking spaces 1,8K

Outstanding investment costs US$ 288 mn

Average price US$ 6K

MV (JLL as f 30.06.2012) US$ 140.0 mn

PARAMETERS DATA

Type Office

Land plot(total), Ha 1.95

GBA, sqm 169.7K

GLA, sqm 107.2K

Plaza Ic: 24.2K/7.0K

Plaza IIa 7.6K

Plaza IV: 68.4K

Parking Units, # 1.8K

Outstanding investment costs US$ 357 mn

MV(JLL as f 30.06.2012) US$ 315.5 mn

DESCRIPTION:

• Located in one of Moscow’s most central

neighborhoods near Belorussky rail terminal, on the

intersection with Tverskaya Street

• Excellent access both by public and private transport

CURRENT STATUS:

• Design stage

• The Company has received the land Lease

Certificates for the Plaza IC (2-ya Brestskaya)

• The negotiations with City on developments rights

for other two Plazas (IV and IIa) are in process

Projects under Development (2/2) T

VE

RS

KA

YA

P

LA

ZA

S

PO

CH

TO

VA

YA

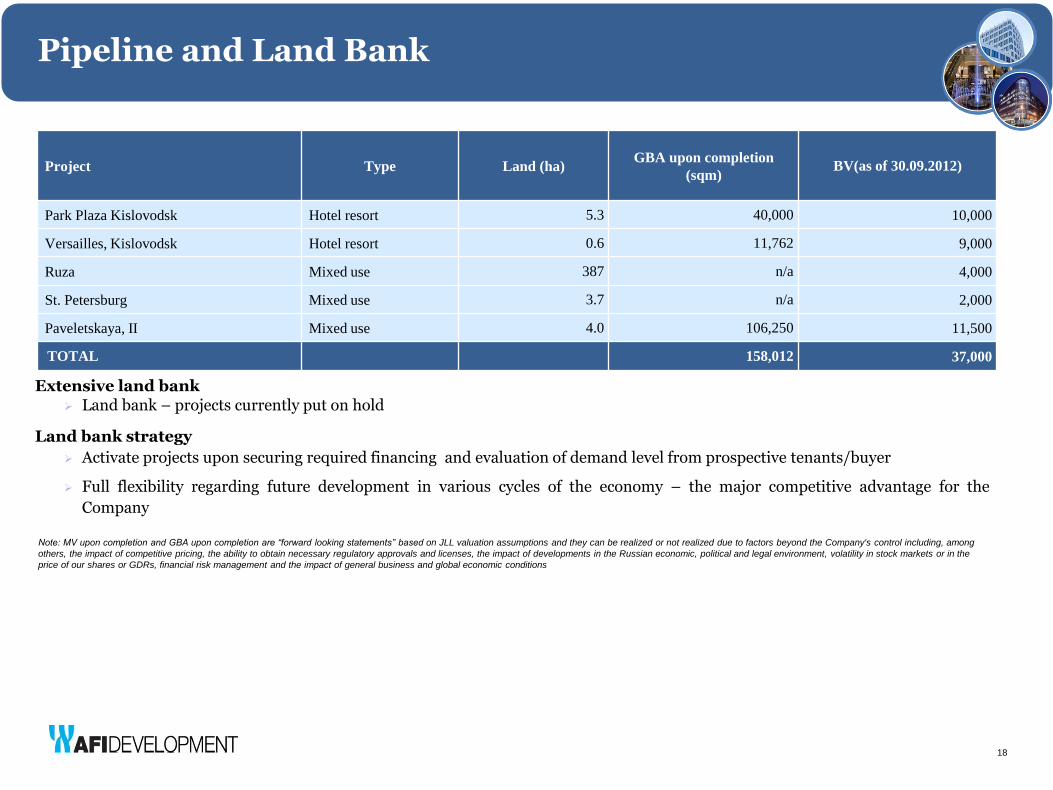

Extensive land bank Land bank – projects currently put on hold

Land bank strategy

Activate projects upon securing required financing and evaluation of demand level from prospective tenants/buyer

Full flexibility regarding future development in various cycles of the economy – the major competitive advantage for the

Company

Pipeline and Land Bank

Project Type Land (ha) GBA upon completion

(sqm) BV(as of 30.09.2012)

Park Plaza Kislovodsk Hotel resort 5.3 40,000 10,000

Versailles, Kislovodsk Hotel resort 0.6 11,762 9,000

Ruza Mixed use 387 n/a 4,000

St. Petersburg Mixed use 3.7 n/a 2,000

Paveletskaya, II Mixed use 4.0 106,250 11,500

TOTAL 158,012 37,000

18

Note: MV upon completion and GBA upon completion are “forward looking statements” based on JLL valuation assumptions and they can be realized or not realized due to factors beyond the Company's control including, among

others, the impact of competitive pricing, the ability to obtain necessary regulatory approvals and licenses, the impact of developments in the Russian economic, political and legal environment, volatility in stock markets or in the

price of our shares or GDRs, financial risk management and the impact of general business and global economic conditions

Q3 2012 Financial Results

SECTION 3

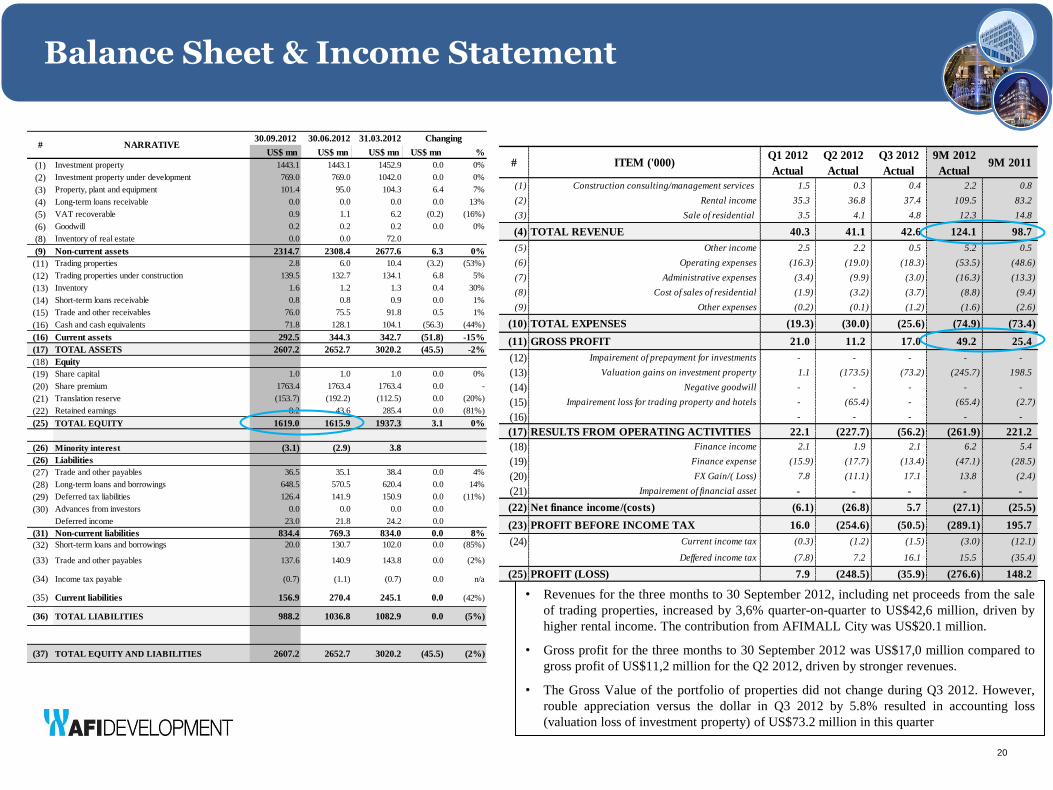

Balance Sheet & Income Statement

20

20

• Revenues for the three months to 30 September 2012, including net proceeds from the sale

of trading properties, increased by 3,6% quarter-on-quarter to US$42,6 million, driven by

higher rental income. The contribution from AFIMALL City was US$20.1 million.

• Gross profit for the three months to 30 September 2012 was US$17,0 million compared to

gross profit of US$11,2 million for the Q2 2012, driven by stronger revenues.

• The Gross Value of the portfolio of properties did not change during Q3 2012. However,

rouble appreciation versus the dollar in Q3 2012 by 5.8% resulted in accounting loss

(valuation loss of investment property) of US$73.2 million in this quarter

30.09.2012 30.06.2012 31.03.2012

US$ mn US$ mn US$ mn US$ mn %

(1) Investment property 1443.1 1443.1 1452.9 0.0 0%

(2) Investment property under development 769.0 769.0 1042.0 0.0 0%

(3) Property, plant and equipment 101.4 95.0 104.3 6.4 7%

(4) Long-term loans receivable 0.0 0.0 0.0 0.0 13%

(5) VAT recoverable 0.9 1.1 6.2 (0.2) (16%)

(6) Goodwill 0.2 0.2 0.2 0.0 0%

(8) Inventory of real estate 0.0 0.0 72.0

(9) Non-current assets 2314.7 2308.4 2677.6 6.3 0%

(11) Trading properties 2.8 6.0 10.4 (3.2) (53%)

(12) Trading properties under construction 139.5 132.7 134.1 6.8 5%

(13) Inventory 1.6 1.2 1.3 0.4 30%

(14) Short-term loans receivable 0.8 0.8 0.9 0.0 1%

(15) Trade and other receivables 76.0 75.5 91.8 0.5 1%

(16) Cash and cash equivalents 71.8 128.1 104.1 (56.3) (44%)

(16) Current assets 292.5 344.3 342.7 (51.8) -15%

(17) TOTAL ASSETS 2607.2 2652.7 3020.2 (45.5) -2%

(18) Equity

(19) Share capital 1.0 1.0 1.0 0.0 0%

(20) Share premium 1763.4 1763.4 1763.4 0.0 -

(21) Translation reserve (153.7) (192.2) (112.5) 0.0 (20%)

(22) Retained earnings 8.2 43.6 285.4 0.0 (81%)

(25) TOTAL EQUITY 1619.0 1615.9 1937.3 3.1 0%

(26) Minority interest (3.1) (2.9) 3.8

(26) Liabilities

(27) Trade and other payables 36.5 35.1 38.4 0.0 4%

(28) Long-term loans and borrowings 648.5 570.5 620.4 0.0 14%

(29) Deferred tax liabilities 126.4 141.9 150.9 0.0 (11%)

(30) Advances from investors 0.0 0.0 0.0 0.0

Deferred income 23.0 21.8 24.2 0.0

(31) Non-current liabilities 834.4 769.3 834.0 0.0 8%

(32) Short-term loans and borrowings 20.0 130.7 102.0 0.0 (85%)

(33) Trade and other payables 137.6 140.9 143.8 0.0 (2%)

(34) Income tax payable (0.7) (1.1) (0.7) 0.0 n/a

(35) Current liabilities 156.9 270.4 245.1 0.0 (42%)

(36) TOTAL LIABILITIES 988.2 1036.8 1082.9 0.0 (5%)

(37) TOTAL EQUITY AND LIABILITIES 2607.2 2652.7 3020.2 (45.5) (2%)

NARRATIVE # Changing

Actual Actual Actual Actual

(1) Construction consulting/management services 1.5 0.3 0.4 2.2 0.8

(2) Rental income 35.3 36.8 37.4 109.5 83.2

(3) Sale of residential 3.5 4.1 4.8 12.3 14.8

(4) TOTAL REVENUE 40.3 41.1 42.6 124.1 98.7

(5) Other income 2.5 2.2 0.5 5.2 0.5

(6) Operating expenses (16.3) (19.0) (18.3) (53.5) (48.6)

(7) Administrative expenses (3.4) (9.9) (3.0) (16.3) (13.3)

(8) Cost of sales of residential (1.9) (3.2) (3.7) (8.8) (9.4)

(9) Other expenses (0.2) (0.1) (1.2) (1.6) (2.6)

(10) TOTAL EXPENSES (19.3) (30.0) (25.6) (74.9) (73.4)

(11) GROSS PROFIT 21.0 11.2 17.0 49.2 25.4

(12) Impairement of prepayment for investments - - - - -

(13) Valuation gains on investment property 1.1 (173.5) (73.2) (245.7) 198.5

(14) Negative goodwill - - - - -

(15) Impairement loss for trading property and hotels - (65.4) - (65.4) (2.7)

(16) - - - - -

(17) RESULTS FROM OPERATING ACTIVITIES 22.1 (227.7) (56.2) (261.9) 221.2

(18) Finance income 2.1 1.9 2.1 6.2 5.4

(19) Finance expense (15.9) (17.7) (13.4) (47.1) (28.5)

(20) FX Gain/( Loss) 7.8 (11.1) 17.1 13.8 (2.4)

(21) Impairement of financial asset - - - - -

(22) Net finance income/(costs) (6.1) (26.8) 5.7 (27.1) (25.5)

(23) PROFIT BEFORE INCOME TAX 16.0 (254.6) (50.5) (289.1) 195.7

(24) Current income tax (0.3) (1.2) (1.5) (3.0) (12.1)

Deffered income tax (7.8) 7.2 16.1 15.5 (35.4)

(25) PROFIT (LOSS) 7.9 (248.5) (35.9) (276.6) 148.2

# ITEM ('000)Q1 2012 9M 2012Q2 2012 Q3 2012

9M 2011

Loans and Cash Position as of Sep 30, 2012

21

Balance as of Sep-

30, 2012

(US$ mn)

RCB $309 - 3-month LIBOR +

6,7%- USD

RCB $222 $128 9.5% - RUB

Total AFIMALL $532

Ozerkovskaya III (50%) Sberbank $21 - 13.0% $4,4 RUB

Kalinina Hotel Sberbank $20 - 6.75% $0,03 RUB

Four Winds (50%) Nordea Bank $81 -3-month LIBOR +

4,5%$1 USD

Total/Blind interest rate 653 7.8%

Currency

AFIMALL (Refinance)

Project Lending bankAvailable

(US$ mn)Nominal Interest rate

Principal

amortization until

31/12/12 (US$ mn)

Contact Information

Registered office AFI DEVELOPMENT PLC 25 Olympion St., Omiros & Araouzos Tower, 3035 , Limassol, Cyprus. Tel: +357 25 340 058 Principal office of operating subsidiary AFI RUS 16 A Berezhkovskaya Embankment, building 5, Moscow, 121059, Russian Federation. Tel: +7 495 796 99 88 http://investors.afi-development.ru

22