p.v. viswanath. p.v. viswanath 2 they provide information to the owners and creditors of the firm...

Post on 19-Dec-2015

219 views

TRANSCRIPT

Introduction to Financial Statement Analysis

P.V. VISWANATH

P.V. Viswanath

2

Functions of Financial Statements

They provide information to the owners and creditors of the firm about the company’s current status and past financial performance

Financial statements provide a convenient way for owners and creditors to set performance targets and to impose restrictions on the managers of the firm.

Financial statements provide convenient templates for financial planning.

P.V. Viswanath

3

The Balance Sheet

The balance sheet is a snapshot of the firm’s assets and liabilities at a given point in time

Assets are listed in order of liquidity, i.e. ease of conversion to cash without significant loss of value

Liabilities are listed in order of time to maturity

P.V. Viswanath

4

Assets

Assets are divided into current assets and long-term assets. Current assets are: Cash and marketable securities Accounts receivable Inventories Other current assets, such as prepaid expenses

Long-term assets include net property, plant and equipment (net PP&E). This consists of the original cost of PP&E reduced

each year by an amount called depreciation that is intended to account for wear-and-tear and obsolescence.

P.V. Viswanath

5

Assets

When a firm acquires another firm, it will acquire a set of assets that must be listed on its balance sheet. Often it will pay more for these assets than their book value on the acquired firm’s balance sheet.

The difference is listed as goodwill. Trade-marks, patents and other such assets,

along with goodwill are called intangible assets.If their value decreases over time, they will be

reduced by an amortization charge.Amortization, like depreciation is not a cash

expense.

P.V. Viswanath

6

Liabilities

Liabilities are divided into current and long-term liabilities.

Liabilities that will be satisfied in one year are known as current, and include: Accounts payable, Notes payable, short-term debt and all repayments of

debt that will occur within the year. Items such as salary or taxes that are owed but have

not yet been paid.The difference between current assets and

current liabilities is known as (net) working capital.

7

Long-term liabilities

Long-term debt is any loan or debt obligation with a maturity of more than one year.

Capital leases are long-term lease contracts that obligate the firm to make regular payments in exchange for the use of an asset.

Deferred taxes are taxes that are owed but not yet paid. Firms keep two sets of books – one for financial reporting and one for tax purposes. Deferred tax liabilities arise when the firm’s financial income exceeds its income for tax purposes. If a firm depreciates assets faster for tax purposes than for reporting purposes, its tax paid will be less than tax due according to reported income. Hence it will look as if the firm has not paid taxes that it owes.

Over time, the discrepancy will disappear and the tax due will be “paid.” Hence deferred tax is recorded as a liability.

P.V. Viswanath

P.V. Viswanath

8

Stockholder’s Equity

The sum of current liabilities and long-term liabilities is total liabilities. The difference between the firm’s asset and its liabilities is Stockholders’ Equity or the book value of equity.

This number often does not provide us with an accurate assessment of the firm’s equity because book values are based on historical quantities and not on market values.

The market price of a share times shares outstanding is called market capitalization; this reflects what investors expect the firms assets to produce in the future that can be distributed to shareholders.

P.V. Viswanath

9

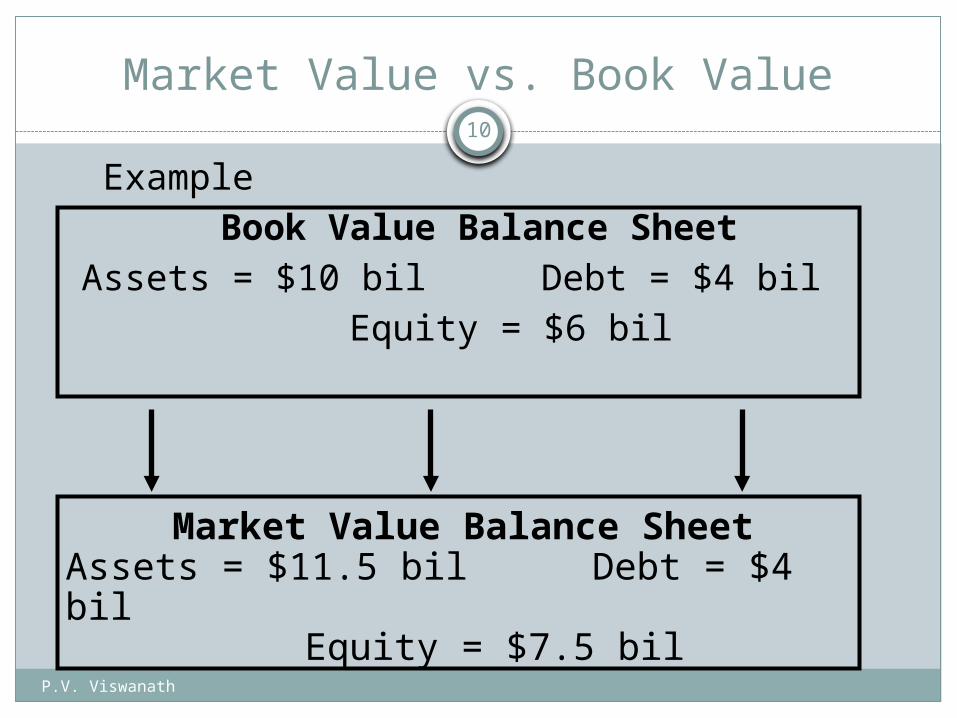

Market Value vs. Book Value

ExampleAccording to Generally Accepted Accounting

Principles (GAAP), your firm has equity worth $6 billion, debt worth $4 billion, assets worth $10 billion. The market values your firm’s 100 million shares at $75 per share and the debt at $4 billion.

Q: What is the market value of your assets?

A: Since (Assets=Liabilities + Equity), your assets must have a market value of $11.5 billion.

P.V. Viswanath

10

Market Value vs. Book Value

ExampleBook Value Balance Sheet

Assets = $10 bil Debt = $4 bilEquity = $6 bil

Market Value Balance SheetAssets = $11.5 bil Debt = $4 bil

Equity = $7.5 bil

P.V. Viswanath

11

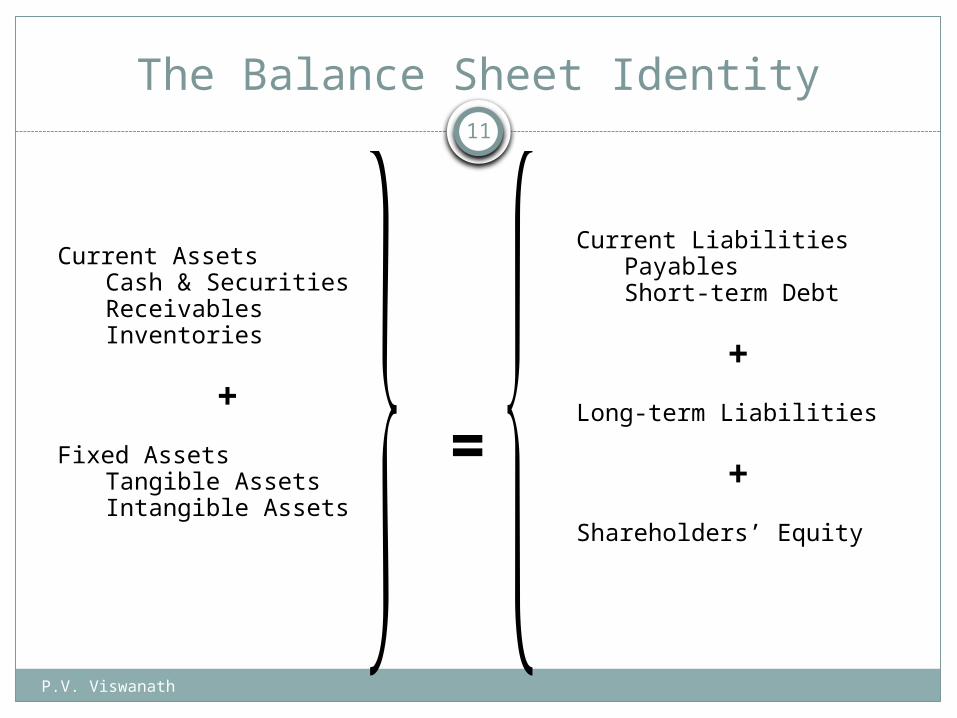

The Balance Sheet Identity

Current AssetsCash & SecuritiesReceivablesInventories

+Fixed Assets

Tangible AssetsIntangible Assets Current Liabilities

PayablesShort-term Debt

+Long-term Liabilities

+Shareholders’ Equity=

P.V. Viswanath

12

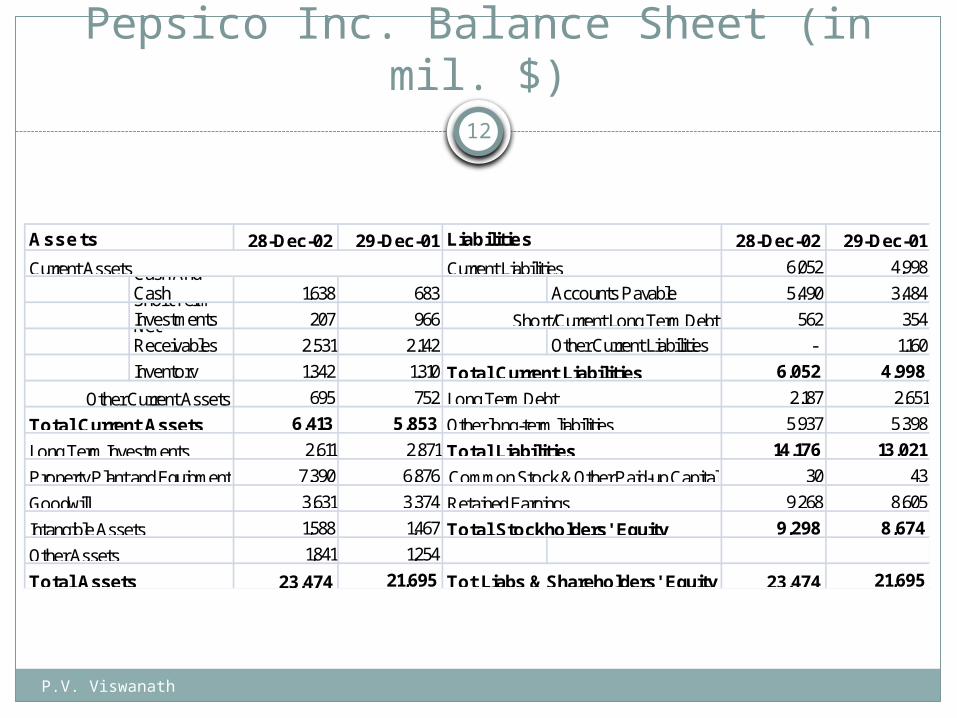

Pepsico Inc. Balance Sheet (in mil. $)

28-Dec-02 29-Dec-01 28-Dec-02 29-Dec-01

6,052 4,998Cash And Cash 1,638 683 Accounts Payable 5,490 3,484Short Term Investments 207 966 Short/Current Long Term Debt 562 354Net Receivables 2,531 2,142 Other Current Liabilities - 1,160

Inventory 1,342 1,310 6,052 4,998

Other Current Assets 695 752 2,187 2,651

6,413 5,853 5,937 5,398

2,611 2,871 14,176 13,021

7,390 6,876 30 43

3,631 3,374 9,268 8,605

1,588 1,467 9,298 8,674

1,841 1,254

23,474 21,695 Tot Liabs & Shareholders' Equity 23,474 21,695

Assets

Current Assets

Total Assets

Goodwill

Intangible Assets

Other Assets

Total Current Assets

Long Term Investments

Property Plant and Equipment

Total Stockholders' Equity

Liabilities

Common Stock & Other Paid-up Capital

Retained Earnings

Total Liabilities

Long Term Debt

Other long-term liabilities

Current Liabilities

Total Current Liabilities

P.V. Viswanath

13

Income Statement

The income statement is like a video of the firm’s operations for a specified period of time.

You report revenues first and then deduct any expenses for the period.

Matching principle – GAAP requires the income statement to show revenue when it accrues and match the expenses required to generate the revenue.

14

Earnings Calculations

Gross Profit The difference between sales revenues and the costs incurred to

make and sell the products. Operating Expenses

Expenses in the ordinary course of running the business, but not directly related to producing the goods; includes administrative expenses, marketing expenses, R&D

Earnings before Interest and Taxes (EBIT) Includes other sources of income or expenses that arise from

activities that are not the central part of the business, e.g. investment income.

Pretax Income and Net Income (NI) From EBIT, we deduct interest paid and corporate taxes to determine

Net Income. EPS = NI/Shares Outstanding

P.V. Viswanath

P.V. Viswanath

15

Income Statement Pepsico Inc. (in mil. $)

As of year ending Dec 02 Dec 01

Revenue 25,112 26,935

Cost of Goods Sold 10,523 9,837

Gross Profit 14,589 17,098

SG&A Expense 8,523 11,608

Depreciation & Amortization 1,112 1,082

Operating Income 4,954 4,408

Nonoperating Income 316 227

EBIT 5046 4248

I nterest 178 219

I ncome Before Taxes 4,868 4,029

I ncome Taxes 1,555 1,367

P.V. Viswanath

16

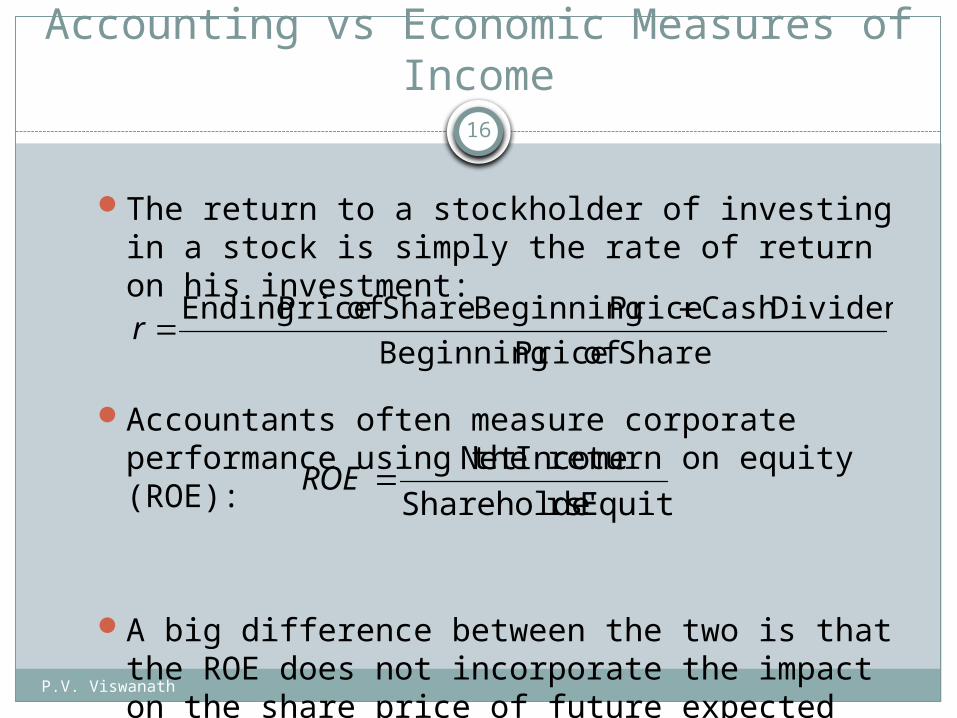

Accounting vs Economic Measures of Income

The return to a stockholder of investing in a stock is simply the rate of return on his investment:

Accountants often measure corporate performance using the return on equity (ROE):

A big difference between the two is that the ROE does not incorporate the impact on the share price of future expected superior (or inferior) returns

Share of Price Beginning

DividendCash Price Beginning - Share of Price Ending r

Equity rs'Shareholde

IncomeNet ROE

P.V. Viswanath

17

Ratio Analysis

Ratios also allow for better comparison through time or between companies

As we look at each ratio, ask yourself what the ratio is trying to measure and why is that information important

Ratios are used both internally and externally

P.V. Viswanath

18

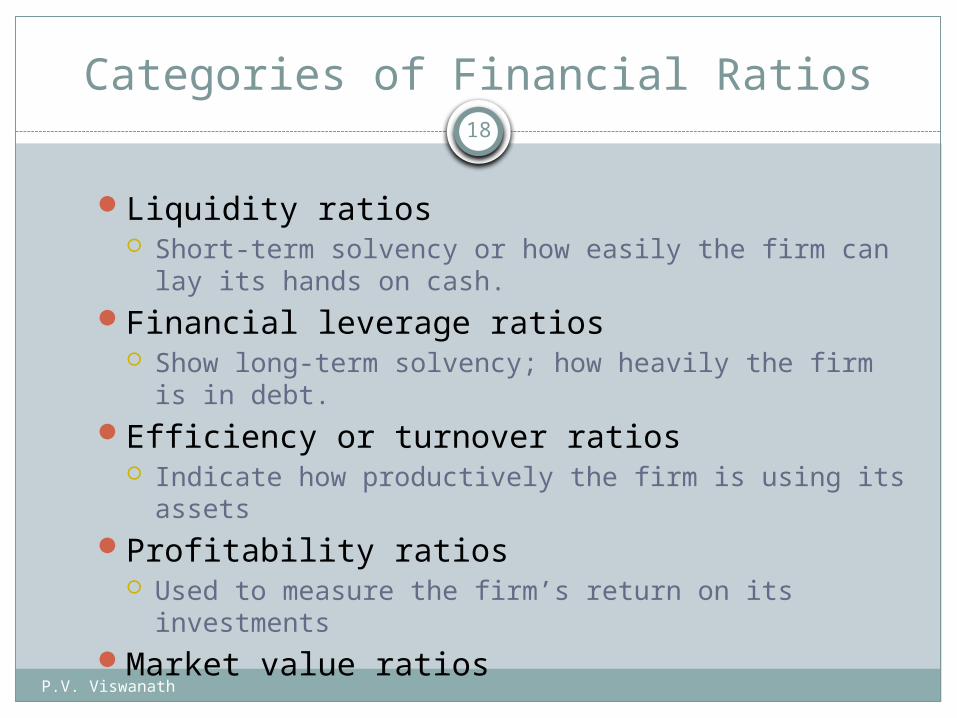

Categories of Financial Ratios

Liquidity ratios Short-term solvency or how easily the firm can lay its

hands on cash.Financial leverage ratios

Show long-term solvency; how heavily the firm is in debt.

Efficiency or turnover ratios Indicate how productively the firm is using its assets

Profitability ratios Used to measure the firm’s return on its investments

Market value ratios

P.V. Viswanath

19

Computing Profitability Measures

Profit Margin = Net Income / Sales 3313/ 25112 = 0.1319 times or 13.19%

Operating Profit Margin = (Operating Income) / Sales (4954) / 25112 = 0.1973 times or 19.73%

Return on Assets (ROA) = (Net Income) / Av TA (3313) / [(23474+21695)/2] = 0.1467 times or 14.67%

Return on Equity (ROE) = Net Income / Average Equity 3313 / [(9298+8674)/2] = 0.3687 times or 36.87%

P.V. Viswanath

20

Computing Leverage Ratios for 2002

Total Debt Ratio = (Total Debt) / TA Total debt, here, is usually interpreted to mean all

debt-like obligations, which is effectively total liabilities (14176) / 23,474 = .6039 times or 60.39% The firm finances almost 60% of their assets with debt.

Debt/Equity = Tot Debt / Tot Eq 14,176 / 9,298 = 1.5246 times

These numbers can also be computed for long-term debt (i.e. long-term liabilities):

Long Term Debt Ratio = LT Debt/ Total Assets = (2,187 + 5,937)/ 23,474 = 0.3461

Long Term Debt/Equity = (2,187 + 5,937)/9,298 = 0.87375

P.V. Viswanath

21

Computing Coverage Ratios

Determinants of the riskiness of a firm’s debt

Times Interest Earned = EBIT / Interest (4868 + 178) / 178 = 28.35 times

Cash Flow Coverage = (EBIT + Depreciation) / Interest (4868 + 178 + 1112) / 178 = 34.60 times

P.V. Viswanath

22

Computing Liquidity Ratios

Current Ratio = CA / CL 6413 /6052 = 1.06 times

Quick Ratio = (CA – Inventory) / CL (6413 – 1342) / 6052 = 0.838 times

Cash Ratio = Cash / CL 1,638 / 6,052 = .276 times

Net Working Capital to TA Ratio = NWC/TA (6413-6052)/ 23474 = 0.154

P.V. Viswanath

23

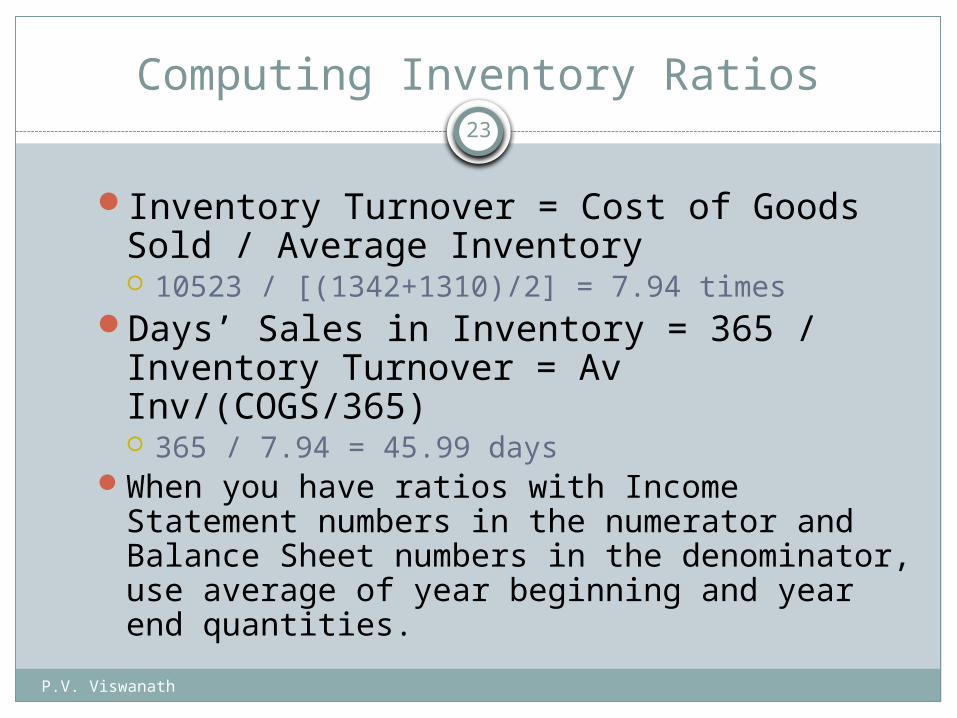

Computing Inventory Ratios

Inventory Turnover = Cost of Goods Sold / Average Inventory 10523 / [(1342+1310)/2] = 7.94 times

Days’ Sales in Inventory = 365 / Inventory Turnover = Av Inv/(COGS/365) 365 / 7.94 = 45.99 days

When you have ratios with Income Statement numbers in the numerator and Balance Sheet numbers in the denominator, use average of year beginning and year end quantities.

P.V. Viswanath

24

Computing Receivables Ratios

Receivables Turnover = Sales / Av Accounts Receivable 25112 / [(2531+2142)/2] = 10.75 times

Average Collection Period = Days’ Sales in Receivables = 365 / Receivables Turnover = Av Receiv/ (Av Sales) 365 / 10.75 = 33.96 days

P.V. Viswanath

25

Computing Total Asset Turnover

Total Asset Turnover = Sales / Av Total Assets 25112 / [(23474+21695)/2] = 1.11 times

Measure of asset use efficiencyNot unusual for TAT < 1, especially if a

firm has a large amount of fixed assets.What is a reasonable value for TAT will

depend on the industry in question

P.V. Viswanath

26

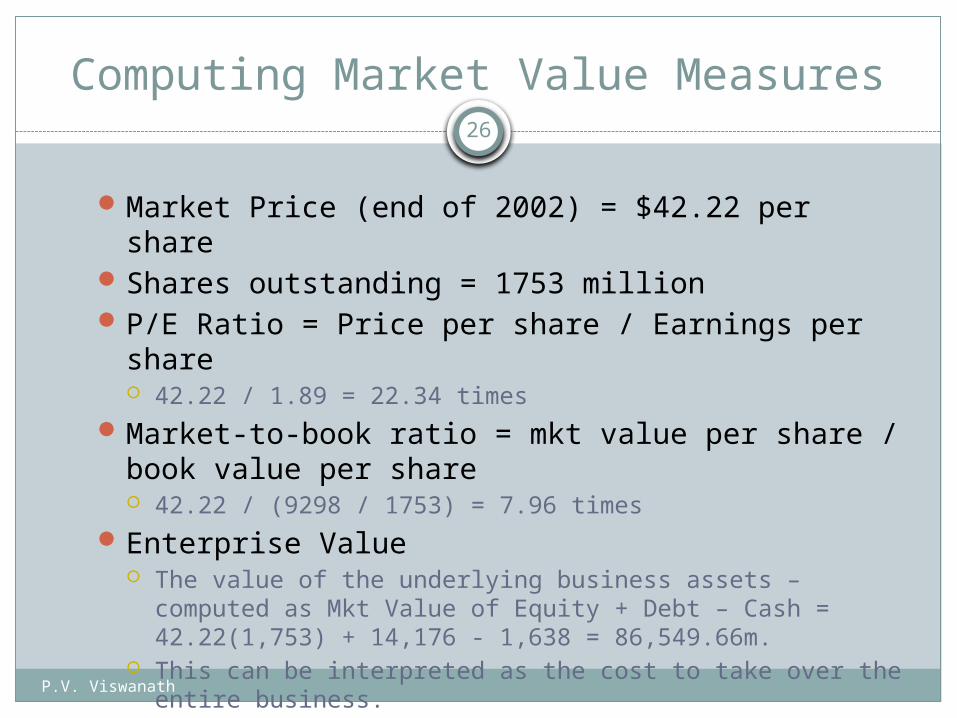

Computing Market Value Measures

Market Price (end of 2002) = $42.22 per shareShares outstanding = 1753 millionP/E Ratio = Price per share / Earnings per share

42.22 / 1.89 = 22.34 timesMarket-to-book ratio = mkt value per share / book

value per share 42.22 / (9298 / 1753) = 7.96 times

Enterprise Value The value of the underlying business assets – computed as

Mkt Value of Equity + Debt – Cash = 42.22(1,753) + 14,176 - 1,638 = 86,549.66m.

This can be interpreted as the cost to take over the entire business.

P.V. Viswanath

27

Payout and Retention Ratios

Dividend payout ratio = Cash dividends / Net income Cash dividend equals common dividend +

preferred divs 1041 / 3313 = .3142 or 31.42%

Plowback ratio = Retention ratio = 1 – payout ratio 1 – 0.3142 = 0.6858 = 68.58%

P.V. Viswanath

28

Benchmarking

Ratios are not very helpful by themselves; they need to be compared to something

Time-Trend Analysis Used to see how the firm’s performance is

changing through time Internal and external uses

Peer Group Analysis Compare to similar companies or within

industries SIC and NAICS codes

P.V. Viswanath

29

Standardized Financial Statements

Common-Size Balance Sheets Compute all accounts as a percent of total assets

Common-Size Income Statements Compute all line items as a percent of sales

Standardized statements make it easier to compare financial information, particularly as the company grows

They are also useful for comparing companies of different sizes, particularly within the same industry

P.V. Viswanath

30

Statement of Cashflows

A firm’s cashflows can be quite different from its net income. For example: The income statement does not recognize capital

expenditures as expenses in the year that the capital goods are paid for. Those expenses are spread over time as a deduction for depreciation.

The income statement recognizes revenues and expenses when sales are made, even though the money may not have been collected (revenues) or paid out (expenses).

P.V. Viswanath

31

The Statement of Cashflows

The statement of cashflows shows the firm’s cash inflows and outflows from Operations Investments and Financing

The form of this statement is determined by accounting standards.

P.V. Viswanath

32

Statement of Cash Flows:Operating Activities

Operating activities are earnings-related activities. Generally these relate to Income Statement activities, and items included in working capital. Included are: Sales and expenses necessary to obtain sales Related operating activities, such as extending credit to

customers investing in inventories obtaining credit from suppliers payment of taxes insurance payments Other activities that don't easily fit into the other two categories,

such as settlements in lawsuits.

P.V. Viswanath

33

Statement of Cash Flows:Investing and Financing Activities

Investing activities relate to the acquisition and disposal of noncash assets: assets which are expected to generate income for the company over a period of time. These include lending funds and collecting on these loans.

Financing activities relate to the contribution, withdrawing and servicing of funds to support business activities.

P.V. Viswanath

34

Pepsico Inc. (in mil. $)Statement of Cash Flows 2002

3,313

1,112

-390

-260

704

-53

201

4,627

-1,437

757

153

-527

-1,041

-1,734

-404

-3,179

34

$955

Depreciation

Adjustments To Net Income

Changes In Accounts Receivables

Changes In Liabilities

Net Income

Operating Activities, Cash Flows Provided By or Used In

Other Cashflows from Investing Activities

Total Cash Flows From Investing Activities

Investing Activities, Cash Flows Provided By or Used In

Capital Expenditures

Investments

Changes In Inventories

Changes In Other Operating Activities

Total Cash Flow From Operating Activities

Change In Cash and Cash Equivalents

Total Cash Flows From Financing Activities

Effect Of Exchange Rate Changes

Financing Activities, Cash Flows Provided By or Used In

Dividends P aid

Sale P urchase of Stock

Net Borrowings

P.V. Viswanath

35

Notes to Financial Statements

The Notes to the Financial Statements are frequently very useful in assessing the financial health of the firm. They often contain: An explanation of accounting methods used

Straight-line versus accelerated depreciation LIFO vs FIFO Restatement of results from prior years using the

new standards Greater details regarding certain assets and

liabilities Conditions and expiration dates of long- and short-

term debt, leases, etc.

P.V. Viswanath

36

Notes to Financial Statements

Information regarding the equity structure of the firm Conditions attached to the ownership of shares;

these can be particularly useful to assess the firm’s vulnerability to takeovers.

Documentation of changes in operations Acquisitions and Divestitures and their impact

Off-balance sheet items Forward contracts, swaps, options and other

derivative contracts, which do not appear in the balance sheet, but which can affect a firm greatly. A lot of Enron’s problems had to do with such off-balance sheet items.

P.V. Viswanath

37

Determinants of Growth

Profit margin – operating efficiencyTotal asset turnover – asset use efficiencyFinancial leverage – choice of optimal debt

ratioDividend policy – choice of how much to

pay to shareholders versus reinvesting in the firm

P.V. Viswanath

38

The Du Pont Identity

ROA = NI/ TA ROA = (NI/ Sales)*(Sales / TA) ROA = (Net Profit Margin)*(Asset Turnover)

ROE = NI / TE ROE = (NI/Sales)*(Sales/TA)*(TA/TE) = Net Profit Margin*Asset Turnover*Equity Multiplier

Net Profit margin is a measure of the firm’s operating efficiency – how well it controls costs

Total asset turnover is a measure of the firm’s asset use efficiency – how well it manages its assets

Equity multiplier is a measure of the firm’s financial leverage

P.V. Viswanath

39

Determinants of Earnings Growth Rate

Earnings in any period depends on the investment base, as well as the rate of return that the firm earns on that investment base:

Et+1 = (TEt)ROE = (TEt-1 + DTEt)(ROE), where DTEt is the increment in

total equity in period t over and above that in period t-1. = (TEt-1)ROE + (DTEt)(ROE) = Et + (DTEt)(ROE); Hence Et+1 - Et = (DTEt)(ROE)Dividing both sides by Et , we get gt = (DTEt/Et)(ROE)We have assumed that ROE does not change, i.e. that the

debt-equity ratio will be kept constant, as we can see from the DuPont identity.

Hence debt must be increased and equity decreased in such a way as to keep the debt ratio constant, assuming that the assets side of the business maintains a constant profitability.

P.V. Viswanath

40

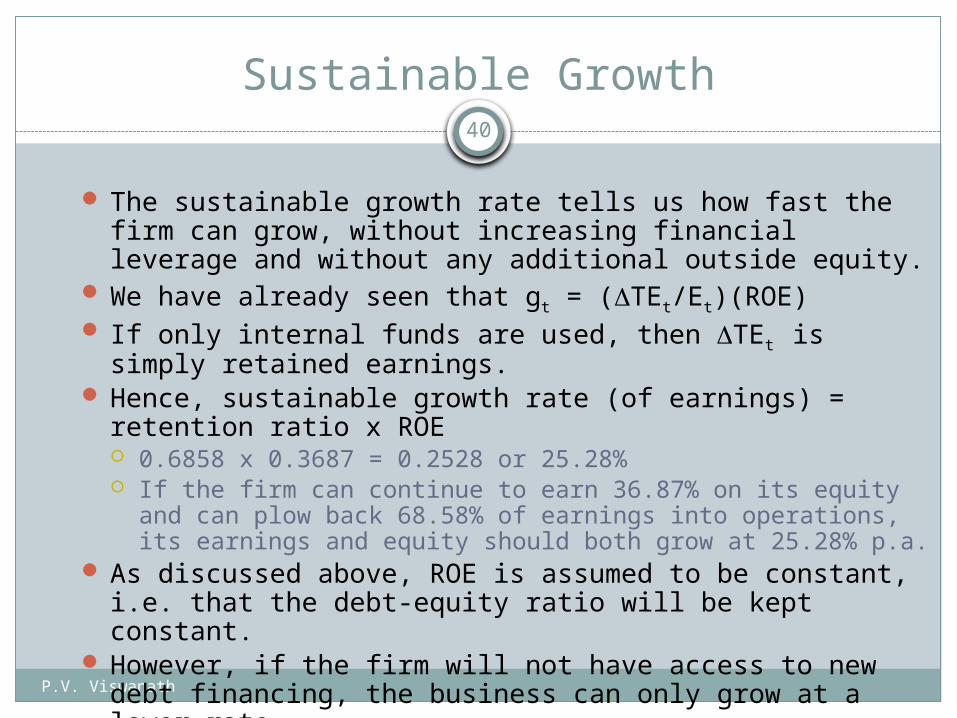

Sustainable Growth

The sustainable growth rate tells us how fast the firm can grow, without increasing financial leverage and without any additional outside equity.

We have already seen that gt = (DTEt/Et)(ROE) If only internal funds are used, then DTEt is simply retained

earnings. Hence, sustainable growth rate (of earnings) = retention

ratio x ROE 0.6858 x 0.3687 = 0.2528 or 25.28% If the firm can continue to earn 36.87% on its equity and can

plow back 68.58% of earnings into operations, its earnings and equity should both grow at 25.28% p.a.

As discussed above, ROE is assumed to be constant, i.e. that the debt-equity ratio will be kept constant.

However, if the firm will not have access to new debt financing, the business can only grow at a lower rate.

P.V. Viswanath

41

Internal Growth Rate

0.2169 x (9298+8674) /(23474+21695) = 0.2528 x 0.3979 = 0.1006 or 10.06%

assets total

equityx

equity

incomenet x

incomenet

earnings retained

assets total

earnings retained

rategrowth

Internal

assets total

equityx

RateGrowth

eSustainabl

rategrowth

Internal

The rate at which the business as a whole, i.e. the total assets of the firm can grow without additional external financing is called the internal growth rate.

P.V. Viswanath

42

Desirable Modifications to Income Statement

There are a few expenses that are consistently mis-categorized in financial statements. In particular, Operating leases are considered as operating expenses

by accountants but they are really, partly, financial expenses. For example, CAKE classifies leases of its restaurant locations as operating leases and does not report them in its balance sheet.

R&D expenses are considered as operating expenses by accountants but they are really capital expenses.

The degree of discretion granted to firms on revenue recognition and extraordinary items is used to manage earnings and provide misleading pictures of profitability.

P.V. Viswanath

43

Dealing with Operating Leases

A Lease is a long-term rental agreement Leases can either be capital leases or operating leases

A capital lease is often for as long as the life of the equipment, or there may be an option for the lessee to buy the equipment at the end of the contract period. Capital leases have to be capitalized and shown on the balance sheet.

In an operating lease, typically, the contract period is shorter than the life of the equipment, and the lessor pays all maintenance and servicing costs. Operating leases do not have to be shown on the balance sheet.

However, operating leases also represent expected fixed periodic payments, and thus function similar to debt. As such, a financial analyst would want to see operating leases capitalized as well

P.V. Viswanath

44

Dealing with Operating Lease Expenses

How do we do this?

First, we compute the “debt” value of the operating lease as the PV of the operating lease expenses, using the pre-tax cost of debt as the discount rate.

This now creates an asset - the value of which is equal to the debt value of operating leases. This asset now has to be depreciated over time.

Second, the operating income has to be adjusted to reflect these changes.

P.V. Viswanath

45

Operating Leases: Adjusting Operating Income

Note that the operating lease expense has two components an operating expense component, i.e. the reduction in the

value of the asset being used, represented by the depreciation, and

a financing component, i.e. the cost of financing the asset.

Using this model, we assume that Interest expense on the debt created by converting operating leases = Operating lease expense - Depreciation on asset created by operating lease. Then,

Adjusted Operating Income = Operating Income - Depreciation on operating lease asset + operating lease expenses = Operating Income + Imputed Interest expense on operating leases. = Operating Income + Debt value of Operating leases x Cost of debt

P.V. Viswanath

46

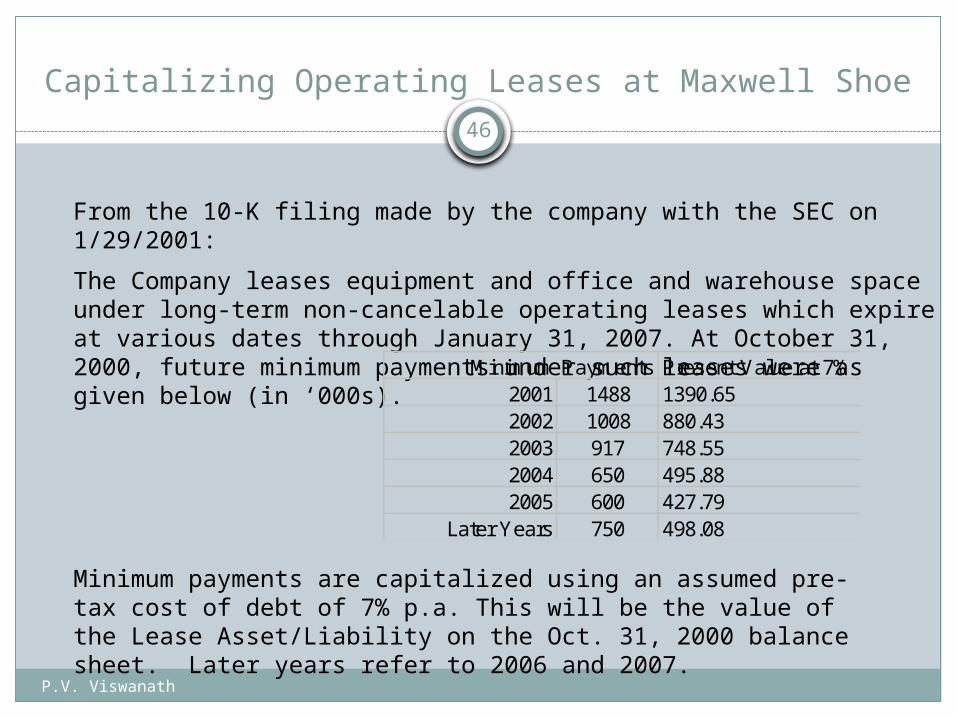

Capitalizing Operating Leases at Maxwell Shoe

From the 10-K filing made by the company with the SEC on 1/29/2001:

The Company leases equipment and office and warehouse space under long-term non-cancelable operating leases which expire at various dates through January 31, 2007. At October 31, 2000, future minimum payments under such leases were as given below (in ‘000s).

Minimum payments are capitalized using an assumed pre-tax cost of debt of 7% p.a. This will be the value of the Lease Asset/Liability on the Oct. 31, 2000 balance sheet. Later years refer to 2006 and 2007.

Minimum Payments Present Value at 7%2001 1488 1390.652002 1008 880.432003 917 748.552004 650 495.882005 600 427.79

Later Years 750 498.08

P.V. Viswanath

47

Capitalizing Operating Leases at Maxwell Shoe

I assume that payments are made at the end of the fiscal year, ending in October.

Since the figure for "Later Years," $750, is larger than the declining sequence of amounts for previous years, I assume that this reflects the amounts for both 2006 and 2007.

Since the leases expire in January 2007, which is 3 months past the fiscal year end, I have prorated the amounts for 2006 and 2007, viz. $600 for 2006 (payable at the end of October 2006) and $150 for 2007 (payable at the end of January 2007).

Hence the $498.08 computed as the present value for the row “Later Years” equals 600/(1.07)6 + 150/(1.07)6.25.

The present value of the minimum payments (as of Oct. 31, 2000) works out to $4441.38.

P.V. Viswanath

48

Imputed Interest Expenses on Operating Leases

Adjusted Operating Income = Operating Income + Imputed Interest Payment

= $13,489 + $357.55 = $13,846.55

Net Income is not affected because the imputed interest expense will be subtracted from Operating Income, just as any other interest expense would be.

Lease payments in 2000 were $1024. Hence the PV of operating leases as of end 1999 would be (PV of Op. Leases as of end 2000 + Lease expenses for 2000)/1.07 = (4441.38+1024)/1.07 = $5107.83.

The imputed interest expense is the Debt Value of Operating Leases x Interest rate.

PV(Operating Leases) as of Oct. 31, 1999 5107.83Interest rate on debt 7%

Imputed Interest expense on PV of operating leases 357.55

P.V. Viswanath

49

Effects of Capitalizing Operating Leases

Debt: will increase, leading to an increase in debt ratios used in the cost of capital and levered beta calculation

Operating income: will increase, since operating income will now be before the imputed interest on the operating lease expense

Net income: will be unaffected since it is after both operating and financial expenses anyway

Return on Capital will generally decrease since the increase in operating income will be proportionately lower than the increase in book capital invested