pt petrosea tbk expose 2009_en... · pt petrosea tbk –public expose –27 may 2009 overview pt...

TRANSCRIPT

PT Petrosea TbkPublic Expose27 May 2009

PT Petrosea Tbk – Public Expose – 27 May 2009

• This presentation will last for approximately 30 minutes, and will

be followed by a Q&A session for 30 minutes

• We will not distribute hard copy of this presentation. It can be

accessed at Petrosea’s website: www.petrosea.com

• Kindly refrain from using mobile phones during the presentation

• During the Q&A session, kindly limit your question to maximum

of two questions per person

Your kind attention please

Solid Management Team

Simon Sembiring – Independent Commissioner*

Simon Sembiring was appointed as Independent Commissioner of Petrosea on March 2009. He joined the Directorate

General of Mines and Energy as Director of Mining Industry Development in 1998 and became Head of Energy and Mineral

Resources Research & Development Agency at the Department of Energy and Mineral Resources in 2001. He was promoted

to Director General Geology and Mineral Resources in 2003 before holding his current position of Director General Mineral,

Coal and Geothermal since 2005.

Firdaus Siddik – President Commissioner

Firdaus Siddik was appointed President Commissioner of Petrosea in 2007 and was previously an Independent Commssioner

of the Company, a position he held starting November 2001. He is a prominent financial management professional with over

38 years experience in various fields of business ranging from oil & gas to mining, distribution, logistics and financial and

management services.

John Smith – Commissioner

John Smith was appointed Commissioner of Petrosea on January 2008. He is the CEO of Clough since August 2007. John is

a chartered Mechanical Engineer with a degree from Glasgow University and has almost 30 years of international oil & gas

experience from bases in Norway, the United Kingdom and Australia. John was CEO of Halliburton Subsea for the first two

years and served on the Board until June 2007.

* Appointed at EGM on 4 March 2009 (replacing John S. Karamoy)

Board of Commissioners:

Andrew Walsh – Commissioner

Andrew Walsh was appointed Commissioner of Petrosea on June 2004. He was appointed Chief Financial Officer for Clough

Limited and became a Director of the Clough Limited Board in November 2003. With over 20 years experience in the

international finance area, Andrew has held senior financial positions with GEC (now BAE Systems).

Solid Management Team

Micky Hehuwat – President Director

Micky Hehuwat was appointed as Director of Petrosea in early 2007, he was then later appointed to the role of President Director

on January 2008. Prior to this he was the long term Director and Indonesian representative of the major South African based

Group, Murray & Roberts, who later acquired a major shareholding in Clough Group, of which Petrosea forms a key element in

South East Asia.

Hendrick Ibrahim – Director External Affairs

Hendrick Ibrahim was appointed as Director of Petrosea in 1999 and has worked continuously with the Company since its

establishment in 1972. He was Manager of the strategic Balikpapan office for 7 years and Accounting Manager for the Company

at the Jakarta head office for over 18 years. He specializes in taxation and has been managing the Company’s Government

Relations portfolio since 1997.

Board of Directors:

Neil Whitaker – Director COO

Neil Whitaker was appointed as Chief Operating Officer of Petrosea in early 2008. He has a degree in Mining Engineering and

Geology from Leeds University in England and has 30 years experience in the Mining industry in positions from Supervisor to

General Management. He has worked with Contractors and Mine owners across Africa and Australia.

PT Petrosea Tbk – Public Expose – 27 May 2009

Overview

PT Petrosea Tbk is a multidisciplinary engineering, construction and mining company

with a track record of achievement in Indonesia since 1972. Today, Petrosea is

recognised as one of Indonesia's leading engineering and construction contractors.

Petrosea shall be an Indonesian mining house which will provide a complete mining

solution (from Pit to Port – PTP) delivering enhanced margin and return on assets

through integrated capability.

PT Petrosea Tbk – Public Expose – 27 May 2009

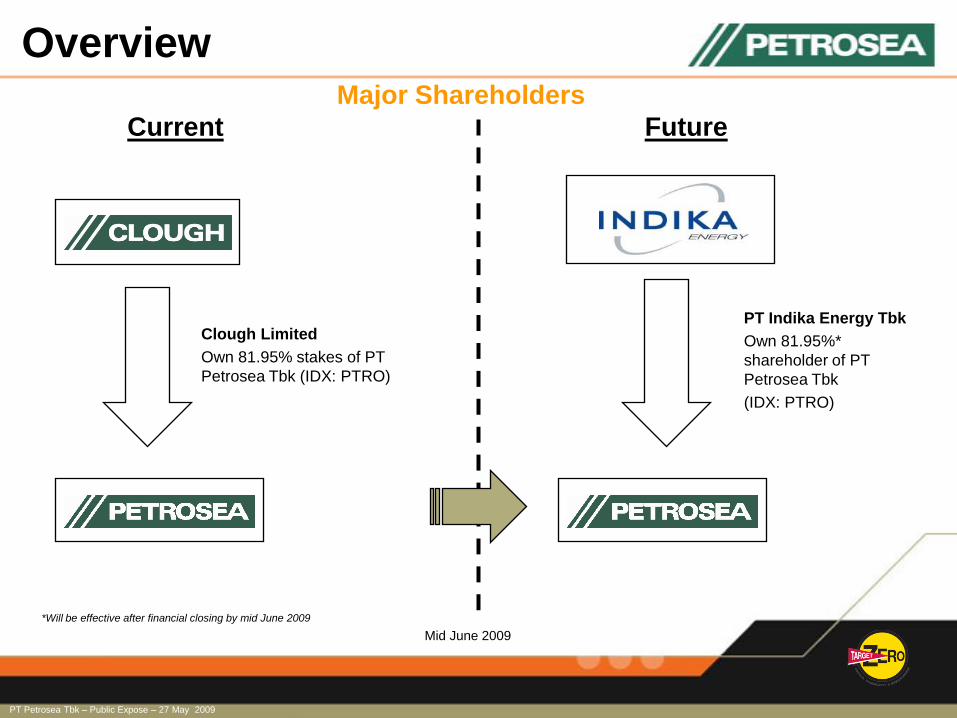

OverviewMajor Shareholders

*Will be effective after financial closing by mid June 2009

Clough Limited

Own 81.95% stakes of PT

Petrosea Tbk (IDX: PTRO)

PT Indika Energy Tbk

Own 81.95%*

shareholder of PT

Petrosea Tbk

(IDX: PTRO)

Mid June 2009

Current Future

PT Petrosea Tbk – Public Expose – 27 May 2009

Overview

• 1972 - Incorporated in Jakarta, Indonesia as PT Petrosea International

Indonesia

• 1984 - Acquired by Clough Limited

• 1990 - Listed on the Jakarta and Surabaya Stock Exchange

(now Indonesia Stock Exchange)

• The first publicly-listed Indonesian engineering and construction company

• The name was changed to PT Petrosea Tbk

• March 2009 – Clough agrees to sell its 81.95% stake in PT Petrosea

Tbk (“Petrosea”) to PT Indika Energy Tbk (“Indika”). Closing transaction

by mid-June 2009

History in Indonesia

PT Petrosea Tbk – Public Expose – 27 May 2009

Overview

How Indika Energy and Petrosea fit together

MINING RIGHTS

GENERAL GEOLOGICAL SURVEY

DETAILED EXPLORATION & DRILLING

BASELINE STUDIES

FEASIBILITY STUDIES

ENVIRONMENT IMPACT & ASSESSMENT

MINE DEVELOPMENT

MINE OPERATION

LOGISTICS SUPPORT

PORT OPERATIONS

BARGING

OFFSHORE LOADING TERMINALS

COAL SHIPPING

POWER GENERATION

PT Petrosea Tbk – Public Expose – 27 May 2009

Overview

• Average annual turnover over the last 5 years1 - US$133.8 million

• Total number of employees2 - 1,666 people

• Turnover per Business Operations3:

• Mining - 52%

• Engineering & Construction - 41%

• Services (incl. POSB, PT Tirta Kencana Cahaya Mandiri) - 7%

Current Business Operations

Petrosea

Offshore

Supply

Base

Engineering &

ConstructionMinerals & Infrastructure

Offshore Marine Construction

Oil & Gas Asset Support

Engineering

MiningContract Mining

Mine Services

PT Tirta

Kencana

Cahaya

Mandiri

PT Santan

Batubara

Business Lines Investment(Partnering)

1Based on PTP Annual Turnover for the Years Ended 31 December 2004-2008 2As of 31 April 20093Based on PTP Annual Turnover for the Year Ended 31 December 2008

PT Petrosea Tbk – Public Expose – 27 May 2009

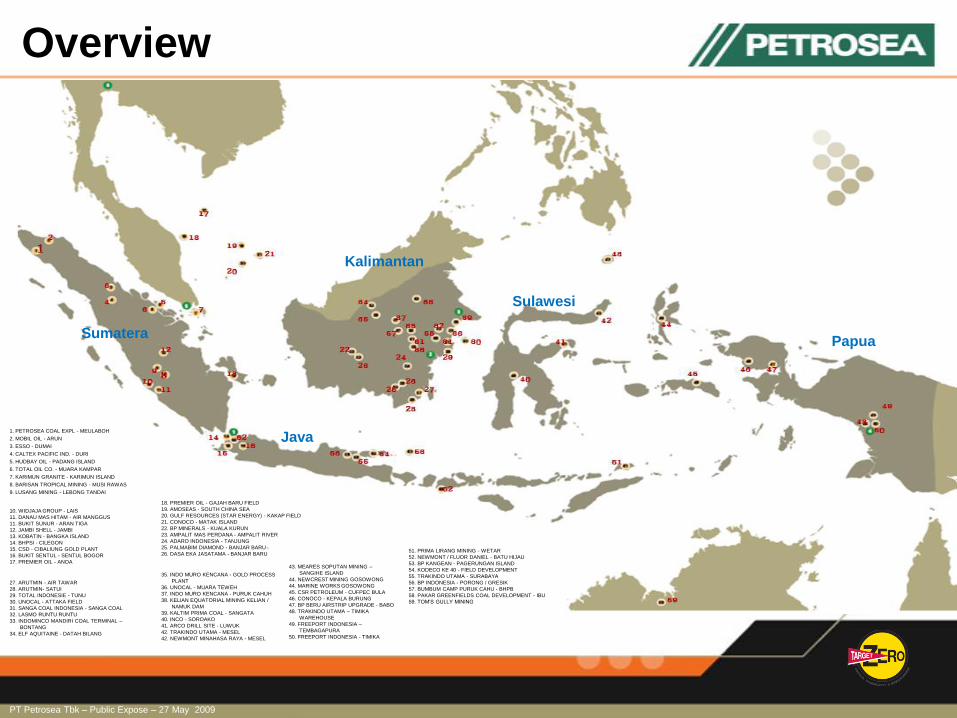

Overview

1. PETROSEA COAL EXPL - MEULABOH

2. MOBIL OIL - ARUN

3. ESSO - DUMAI

4. CALTEX PACIFIC IND. - DURI

5. HUDBAY OIL - PADANG ISLAND

6. TOTAL OIL CO. - MUARA KAMPAR

7. KARIMUN GRANITE - KARIMUN ISLAND

8. BARISAN TROPICAL MINING - MUSI RAWAS

9. LUSANG MINING - LEBONG TANDAI

10. WIDJAJA GROUP - LAIS

11. DANAU MAS HITAM - AIR MANGGUS

11. BUKIT SUNUR - ARAN TIGA

12. JAMBI SHELL - JAMBI

13. KOBATIN - BANGKA ISLAND

14. BHPSI - CILEGON

15. CSD - CIBALIUNG GOLD PLANT

16. BUKIT SENTUL - SENTUL BOGOR

17. PREMIER OIL - ANOA

18. PREMIER OIL - GAJAH BARU FIELD

19. AMOSEAS - SOUTH CHINA SEA

20. GULF RESOURCES (STAR ENERGY) - KAKAP FIELD

21. CONOCO - MATAK ISLAND

22. BP MINERALS - KUALA KURUN

23. AMPALIT MAS PERDANA - AMPALIT RIVER

24. ADARO INDONESIA - TANJUNG

25. PALMABIM DIAMOND - BANJAR BARU

26. DASA EKA JASATAMA - BANJAR BARU

27. ARUTMIN - AIR TAWAR

28. ARUTMIN- SATUI

29. TOTAL INDONESIE - TUNU

30. UNOCAL - ATTAKA FIELD

31. SANGA COAL INDONESIA - SANGA COAL

32. LASMO RUNTU RUNTU

33. INDOMINCO MANDIRI COAL TERMINAL –

BONTANG

34. ELF AQUITAINE - DATAH BILANG

35. INDO MURO KENCANA - GOLD PROCESS

PLANT

36. UNOCAL - MUARA TEWEH

37. INDO MURO KENCANA - PURUK CAHUH

38. KELIAN EQUATORIAL MINING KELIAN /

NAMUK DAM

39. KALTIM PRIMA COAL - SANGATA

40. INCO - SOROAKO

41. ARCO DRILL SITE - LUWUK

42. TRAKINDO UTAMA - MESEL

42. NEWMONT MINAHASA RAYA - MESEL

43. MEARES SOPUTAN MINING –

SANGIHE ISLAND

44. NEWCREST MINING GOSOWONG

44. MARINE WORKS GOSOWONG

45. CSR PETROLEUM - CUFPEC BULA

46. CONOCO - KEPALA BURUNG

47. BP BERU AIRSTRIP UPGRADE - BABO

48. TRAKINDO UTAMA – TIMIKA

WAREHOUSE

49. FREEPORT INDONESIA –

TEMBAGAPURA

50. FREEPORT INDONESIA - TIMIKA

51. PRIMA LIRANG MINING - WETAR

52. NEWMONT / FLUOR DANIEL - BATU HIJAU

53. BP KANGEAN - PAGERUNGAN ISLAND

54. KODECO KE 40 - FIELD DEVELOPMENT

55. TRAKINDO UTAMA - SURABAYA

56. BP INDONESIA - PORONG / GRESIK

57. BUMBUM CAMP PURUK CAHU - BHPB

58. PAKAR GREENFIELDS COAL DEVELOPMENT - IBU

59. TOM’S GULLY MINING

Kalimantan

Sulawesi

Java

SumateraPapua

PT Petrosea Tbk – Public Expose – 27 May 2009

(in US$ Thousand) 2008 2007

Operating Revenue 205,794 125,962

Operating Income 10,869 12,622

Net Income 1,775 7,097

Earning Per Share (US$) 0.0176 0.0704

Dividend Per Share (US$) - 0.0297

Cash 9,068 21,582

Working Capital 16,698 37,607

Capital Expenditure 45,080 25,684

Total Assets 178,268 148,638

Debt 43,691 24,226

Total Equity 70,657 76,411

Operating Income / Operating Revenue (%) 5.28% 10.02%

Net Income / Operating Revenue (%) 0.86% 5.64%

Net Income / Total Assets (%) 1.00% 4.78%

Net Income / Equity (%) 2.51% 9.29%

Debt / Equity Ratio 0.62 0.32

Current Ratio 1.22 1.71

*Audited, Years Ended 31 December

Financial Performance

PT Petrosea Tbk – Public Expose – 27 May 2009

*Audited, Years Ended 31 December

Financial Performance

106

126

206

0

50

100

150

200

250

2006 2007 2008

Mill

ion U

S$

Operating Revenue

Operating revenue (LHS)

76

32

18

106

82

17

0

10

20

30

40

50

60

70

80

90

100

110

120

Mining Engineering and Construction

Services

Mill

ion U

S$

Operating Revenue by Business Segment

2007 2008

Strong Revenue Growth

• Strong Operating Revenue growth 63% to

US$205.79m

• E&C 160% to US$82m

• Mining 41% to US$106m

• Services 7% to US$17m

• In 2008, from total operating revenue,

Mining contributed 52%, E&C 41%, and

Services 7% consecutively

*Audited, Years Ended 31 December

PT Petrosea Tbk – Public Expose – 27 May 2009

Financial Performance*

6.44

7.10

1.77

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

2006 2007 2008

Mill

ion U

S$

Net Income

Net income (LHS)

1.40 1.29

8.18

3.20

-2.52

5.76

-3.00

-2.00

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

Mining Engineering and Construction

Services

mill

ion

US

$

Net Income by Business Segment

2007 2008

*Audited, Years Ended 31 December

• Net Income 75% to US$1.77m

• Mining 129% to US$ 3.2m

• E&C 295% to US$2.52m

• Services 30% to US$5.76m

Reduction in Net Income due to provision for

Impairment (Pakar Coal mine infrastructure), increased

interest expenses & finance charges, and overhead.

PT Petrosea Tbk – Public Expose – 27 May 2009

Increase in Work in Hand

• Work in Hand by 26.8% to US$582*

million as a result of:

• Securing additional mining services

contracts of US$250 million with PT

Santan Batubara

• US$315 million with Gunung Bayan

Pratamacoal (GBP) extension contract

• Additional clients in oil & gas supply

services at the Petrosea Offshore Supply

Base (POSB)

Financial Performance

192

459

582*

0

100

200

300

400

500

600

2006 2007 2008

mill

ion U

S$

Work in Hand

*As at April 2009

PT Petrosea Tbk – Public Expose – 27 May 2009

Financial Performance

5.7

-11.2

-7.1

-12.5

9.1

21.6

-3.7

-10.6

7.3

21.6

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

Operating Activities

Investing Activities

Financing Activities

Net Increase Ending Balance

mill

ion U

S$

Cash Flow Position

2008 2007

42.1

37.6

16.7

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

2006 2007 2008

Mill

ion U

S$

Net Working Capital

Net working capital (RHS)

*Audited, Years Ended 31 December

Cash flow deteriorated:

Cash Ending Balance 58% to

US$9.1m

• Operating: 74%

• Investing: 199%

• Financing: 33%

Working Capital 56% to

US$16.7m

• Current Assets 0.56%

to US$91m

• Current Liabilities

40.5% to US$74.3 m

1.71

1.22

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2007 2008

Curr

ent R

atio

Current Ratio

PT Petrosea Tbk – Public Expose – 27 May 2009

Financial Performance

• Debt to Equity Ratio from 0.32 to 0.62 as

a result of large fleet acquisition program

on the back of securing additional long

term mining contracts

• Debt (Finance leases) 80% to

US$43.7m

• Equity 7.5% to US$76.4m

24.23

43.69

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

50.00

2007 2008

mill

ion U

S$

Debt - Finance Leases

0.32

0.62

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

2007 2008

Debt to

Equity R

atio

Debt to Equity Ratio

*Audited, Years Ended 31 December

PT Petrosea Tbk – Public Expose – 27 May 2009

Financial Performance

*Audited, Years Ended 31 December

• Capital Expenditure 75% to US$45.1m

• Mining 45% to US$35.4m

• Services to US$9m

• Capital Expenditure primarily relates to

acquisition of mining fleet to execute the

GBP extension contract worth US$315m

and the Santan mining contract worth

US$250m

16.6

25.7

45.1

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

2006 2007 2008

Mill

ion U

S$

CAPEX

Capex (LHS)

24.3

0.01.0

35.4

0.0

9.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Mining Engineering and Construction

Services

mill

ion U

S$

CAPEX by Business Segment

2007 2008

PT Petrosea Tbk – Public Expose – 27 May 2009

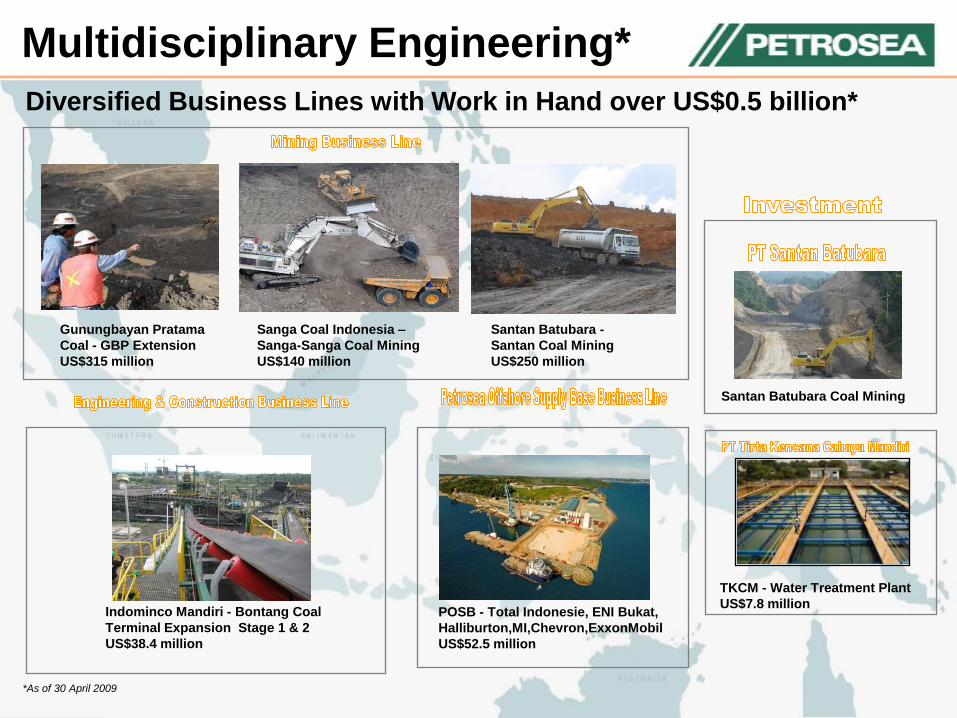

Indominco Mandiri - Bontang Coal

Terminal Expansion Stage 1 & 2

US$38.4 million

TKCM - Water Treatment Plant

US$7.8 million

Santan Batubara Coal Mining

Multidisciplinary Engineering*

*As of 30 April 2009

Sanga Coal Indonesia –

Sanga-Sanga Coal Mining

US$140 million

Gunungbayan Pratama

Coal - GBP Extension

US$315 million

Santan Batubara -

Santan Coal Mining

US$250 million

POSB - Total Indonesie, ENI Bukat,

Halliburton,MI,Chevron,ExxonMobil

US$52.5 million

Diversified Business Lines with Work in Hand over US$0.5 billion*

PT Petrosea Tbk – Public Expose – 27 May 2009

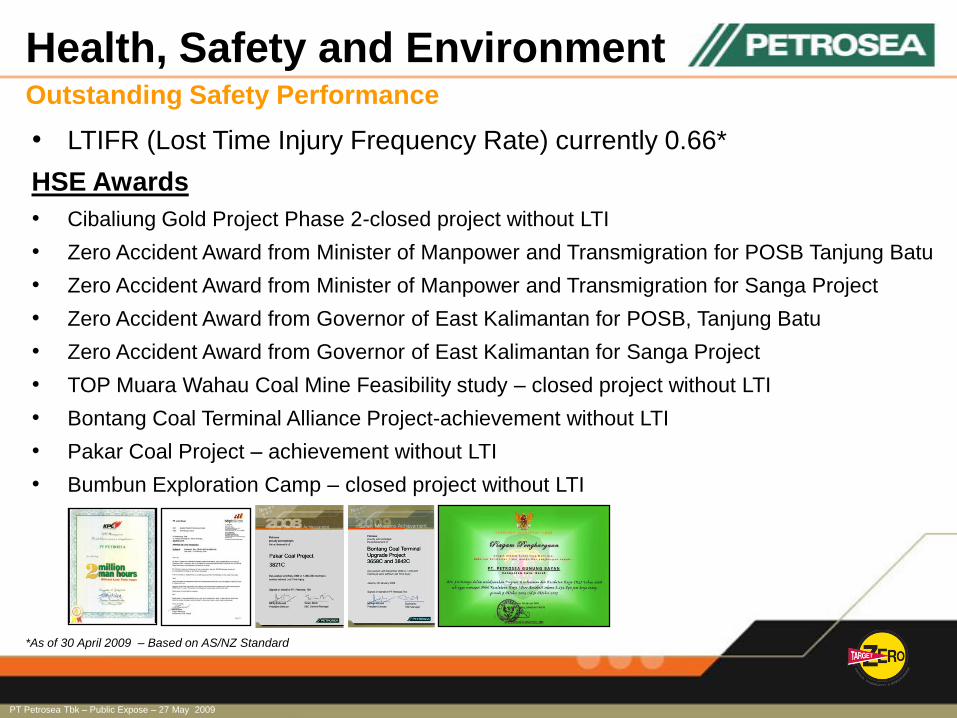

Health, Safety and EnvironmentOutstanding Safety Performance

• LTIFR (Lost Time Injury Frequency Rate) currently 0.66*

HSE Awards

• Cibaliung Gold Project Phase 2-closed project without LTI

• Zero Accident Award from Minister of Manpower and Transmigration for POSB Tanjung Batu

• Zero Accident Award from Minister of Manpower and Transmigration for Sanga Project

• Zero Accident Award from Governor of East Kalimantan for POSB, Tanjung Batu

• Zero Accident Award from Governor of East Kalimantan for Sanga Project

• TOP Muara Wahau Coal Mine Feasibility study – closed project without LTI

• Bontang Coal Terminal Alliance Project-achievement without LTI

• Pakar Coal Project – achievement without LTI

• Bumbun Exploration Camp – closed project without LTI

*As of 30 April 2009 – Based on AS/NZ Standard

PT Petrosea Tbk – Public Expose – 27 May 2009

Quality Assurance

• Petrosea Management System has been certified to ISO 9001 since 2000

• Up-graded to ISO 9001:2008 version in April 2009

• Petrosea Management System is an integrated system of process documents,

tools and technologies designed to meet the needs of Operations, Quality,

Health, Safety and Environment within which reside the fundamental business

processes of:

• Mining Operations

• Engineering & Construction Projects

• Offshore Supply Base Operations

ISO 9001:2008

PT Petrosea Tbk – Public Expose – 27 May 2009

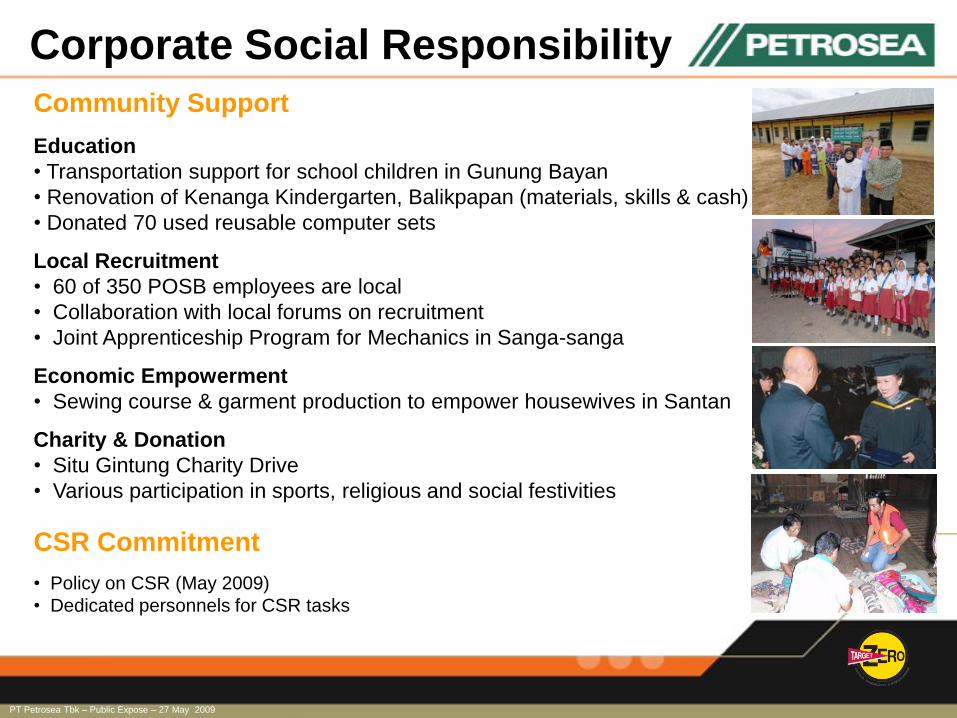

Corporate Social Responsibility

Community Support

Education

• Transportation support for school children in Gunung Bayan

• Renovation of Kenanga Kindergarten, Balikpapan (materials, skills & cash)

• Donated 70 used reusable computer sets

Local Recruitment

• 60 of 350 POSB employees are local

• Collaboration with local forums on recruitment

• Joint Apprenticeship Program for Mechanics in Sanga-sanga

Economic Empowerment

• Sewing course & garment production to empower housewives in Santan

Charity & Donation

• Situ Gintung Charity Drive

• Various participation in sports, religious and social festivities

CSR Commitment

• Policy on CSR (May 2009)

• Dedicated personnels for CSR tasks

PT Petrosea Tbk – Public Expose – 27 May 2009

Market Outlook

• Mining and mineral market has driven the company growth during the year but with the current

commodity plunge, we expect this market to consolidate in the medium term

• Strong demand throughout Asia and supply disruptions in major coal producing countries have

tightened the coal supply in the global market

• Indonesia is currently the world’s largest exporter of thermal coal

• Domestic demand is projected to drive Indonesian thermal coal production in the medium term as the

government rapidly builds coal-fired power plants

• World prices for most of mineral commodities have been trending-down to new equilibrium levels

• The outlook for the Indonesian mineral market is still positive following the recent production increase

Mining & Mineral*

*Source: Barlow Jonker, Indonesia Coal Mining Association, Mitrais Mining News Report, Minister of Energy and Mineral Resources

Indonesia Macro Economic Outlook

Key Macro Economic Indicator 2008 2009E* 2010E*

Real GDP (% y-o-y) 6.1 4.3 5.3

GDP (US$ billion)- nominal 450 453 520

Currency/US$ (Year-end) 11,120 10,200 10,000

Currency/US$ (Average) 9,767 10,650 10,100

BI Policy Rate (% year end) 9.25 7.00 7.50

Consumeer Price (% year end) 11.20 5.00 6.50

Source: CEIC, *Danamon Estimates

PT Petrosea Tbk – Public Expose – 27 May 2009

Market OutlookMining & Mineral*

*Source: Minister of Energy and Mineral Resources

131.00

154.00

193.00

217.00 225.00

250.00

17.56%

25.32%

12.44%

3.69%

11.11%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

0.00

50.00

100.00

150.00

200.00

250.00

300.00

2004 2005 2006 2007 2008 2009F

Mill

ion

US

$

Coal Production

Coal Production (million ton), LHS Growth (%), RHS

No. Commodity 2007 2008 2009F

Unit

1 Copper 797.40 580.95 826.37 Thousand Ton

2 Gold 117.73 57.94 99.34 Ton

3 Silver 269.38 209.06 238.61 Ton

4 Tin 91.28 79.21 105.00 Thousand Ton

5 Bauxite 15,406.04 14,986.52 14,439.32 Thousand Ton

6 Nickel in Mate 77.93 74.40 88.18 Thousand Ton

7 Nickel in Ore 6,623.02 14,902.26 14,166.14 Thousand Ton

8 Ferronickel 18.53 18.70 22.42 Thousand Ton

9 Granite 1.88 2.05 2.50 Million m3

10 Diamond 22,980.68 20,359.20 96,000.00 Carrat

11 Iron Ore 1,894,757.98 4,609,540.54 4,609,540.54 Ton

12 Coal 217.00 225.00 250.00 Million Ton

Source: EMR Department 2009

MINERAL and COAL PRODUCTION

Bumi Resources, PT31.16%

Adaro Indonesia, PT23.20%

Kideco Jaya Agung, PT14.14%

Berau Coal, PT7.80%

Indominco Mandiri, PT6.49%

Tambang Batubara Bukit Asam, PT

5.92%

Bayan Resources, PT3.65%

Baramarta, PD2.73%

Trubaindo Coal Mining, PT

2.72%Bahari Cakrawal Sebuku,

PT2.18%

TOP TEN INDONESIAN COAL PRODUCERS (2008)

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

50.00

55.00

60.00

Bumi Resources, PT

Adaro Indonesia, PT

Kideco Jaya Agung, PT

Berau Coal, PT

Indominco Mandiri, PT

Tambang Batubara Bukit Asam, PT

Bayan Resources, PT

Baramarta, PD

Trubaindo Coal Mining, PT

Bahari Cakrawal Sebuku, PT

52.12

38.80

23.64

13.0510.86 9.90

6.10 4.57 4.55 3.65

Milli

on To

ns

TOP TEN INDONESIAN COAL PRODUCERS (2008)

PT Petrosea Tbk – Public Expose – 27 May 2009

Market Outlook

• Oil and gas market has been a difficult market for the company during theyear, but we anticipate improving activity in this area in the medium term forboth onshore and offshore project opportunities. Focus still in the mining forshort term horizon

• Decline rates of the Indonesian oil production and proven oil reserves havetapered off as a result of increased development activities in existingproducing oil company and new field development projects

• Recent increases in exploration drilling and licensing activities should alsorestore Indonesian oil production growth in the coming years

• The outlook for the Indonesian gas market is positive as Indonesian gasproduction is expected to continue its historical growth trend and projectionsof sustained growth

• Indonesian gas reserves have also increased as a result of numerousdiscoveries by both producing and exploration oil companies

Oil and Gas*

*Source: Indonesia Petroleum Association

PT Petrosea Tbk – Public Expose – 19 June 2008 25

Profit Outlook

• Strong EBIT growth - Mining Business Line.

• Three contract mining projects in operation and one project forecast to

start in the near term

• PT Santan Batubara has commenced production stage. Will contribute

to EBIT growth in upcoming years

• Steady EBIT growth – POSB and E&C

• POSB to service multiple major oil and gas operators

• One construction project under E&C and potential 2-3 projects in the

pipeline

PT Petrosea Tbk – Public Expose – 27 May 2009

Petrosea – Grow with Us

• Strong operating performance through underlying Revenue

• Focus to improve the EBIT before growth in 2010

• Work in Hand over US$0.5 billion*

• Maintain outstanding safety performance

• Indonesia mining and mineral market consolidated

• Future earning growth - driven by Mining Business Line and POSB.

• Synergy with the new shareholder, seize the opportunities to support company growth

*April 2009

PT Petrosea Tbk – Public Expose – 27 May 2009

Thank You

Questions?

• Please state your name

• Kindly limit your question to max. 2 questions per person