provisonal tax ib - without ba process - burns acutt

TRANSCRIPT

BURNS ACUTT

P R O V I S I O N A LT A X

I N FORMAT I ONBOOK LE T

A U G U S T 2 0 2 0

02

03

CONTENT S

01THE BAS I C S

BUS I N E S S

CATEGOR I E S &

S TRATEG I C

APPROACH

0 1

0 2

0 3

0 4

0 6

WHAT IS PROVISIONAL TAX?WHO IS A PROVISIONAL TAXPAYER?HOW ARE THE PROVISIONAL TAX PAYMENTS CALCULATED?

ESTIMATES OF TAXABLE INCOMEFAILURE TO SUBMIT A PROVISIONAL TAX RETURN (IRP6)

WHEN MUST PROVISIONAL TAX BE PAID?INTEREST AND PENALTIES

ABOUT GOVERNMENT CONCESSIONS - COVID-19 RELIEF

BUSINESS CATEGORIES & STRATEGIC APPROACH

August 2020www.burnsacutt.co.za

GOVERNMENT

CONCES S I ONS -

COV I D - 1 9 RE L I E F

MA I N S EC T I ONS

PAGES

WHAT I S PROV I S I ONA LTAX ?

Interest incomeCapital gainsRental income

Provisional tax is not separate from Income Tax – Itis the part payment (Provisional Estimate) ofIncome Tax.

Income earned in the tax year, which does nothave direct taxes levied against it, requires a taxpayment, which is essentially what Provisional Taxis.

Some basic examples would be:

On assessment the provisional tax payments willbe offset against the liability for normal tax for theapplicable year of assessment.

WHO I S A PROV I S I ONA LTAXPAY ER ?

Any person who receives income (or accruesincome) other than a salary, is a provisionaltaxpayer.

Most salary earners are therefore non-provisionaltaxpayers if they have no other sources of income.

It is important to note that receiving exemptincome does not make you a provisional taxpayer,e.g. receiving interest income below theexemption if you are under 65 of R23 800 (over 65:R34 500).

All Companies, Close Corporations and Trusts arerequired to be provisional taxpayers.

PAGE 1

B URNSACU T T . CO . ZA | 2 0 2 0

THE BASICS

HOW ARE THEPROV I S I ONA L T AXPAYMENT S CA L CU LA T ED ?

Less any allowable foreign tax credits for thisperiod (6 months).

The First Period (50%) of Estimated Taxable

Income for the year is payable

Less any allowable foreign tax credits for theyear and Less the amount paid for the firstprovisional period.

The Second Period (100%) of Estimated Taxable

Income for the year is payable

The Third Period (voluntary) to pay any shortfalls

in the provisional estimates before assessment

It excludes capital gains, lump sum withdrawalbenefits and any severance benefits.

COMPANY PROVISIONAL TAXPAYERS

Must submit a return of an estimate of the totaltaxable income expected. Even if the provisionaltax calculation results in a nil payment. The basicamount is the taxable income as last assessed lessany taxable capital gain.

The basic amount for all taxpayers must beincreased by 8% if the estimate is made more than18 months after the end of the latest precedingyear of assessment.

E S T IMA T E S OF T AXAB L EI N COME

The amount of the estimate submitted by aprovisional taxpayer shall not be less than thebasic amount unless the Commissioner agrees toan estimate that is lower than the basic amount.

The Commissioner may call upon a provisionaltaxpayer to justify any estimate or to furnishparticulars of the income and expenditure, or anyother particulars that may be required.

If the Commissioner is dissatisfied with theestimate, he or she may increase it to what he orshe considers reasonable; even if this is more thanthe basic amount. This increase is not subject toobjection and appeal.

The ‘basic amount’ is the taxpayer’s taxableincome assessed by the Commissioner for the lastyear assessed.

PAGE 2

BURNSACU T T . CO . ZA | 2 0 2 0

F A I L URE TO SUBM I T APROV I S I ONA L T AX RE TURN( I R P 6 )

The Commissioner may estimate the taxableincome and determine the amount payable if theprovisional taxpayer fails to submit an estimate.

The estimate made by the Commissioner iseffective for the relevant period within which theprovisional taxpayer is required to make thepayment.

WHEN MUS T PROV I S I ONA LTAX BE PA I D ?

Personal Income Tax Runs from 1 March – 28/29February.

Company Income Tax is as per the company's yearend.

First period: This payment must be made withinsix months from the commencement of the yearof assessment in question. (August if your financialyear end is February).

Second period: This payment must be made nolater than the last day of the year of assessment inquestion. (Financial year end - Usually February).

I N T ER E S T AND P ENA L T I E S

Taxable income > R1 000 000 - estimate is lessthan 80% of the actual taxable income.Taxable income < R1 000 000 - estimate is lessthan 90% of the actual taxable income.

Interest is either levied on an underpayment ofprovisional tax or paid to the taxpayer on anoverpayment of provisional tax.

A penalty will be levied on the shortfall where ithas been determined that the actual taxableincome is more than the taxable incomeestimated on the second provisional tax return if:

At Burns Acutt we apply 90% and 95% of taxableincome to be prudent unless instructed otherwise.

PAGE 3

BURNSACU T T . CO . ZA | 2 0 2 0

PAGE 2 4

POP S T ARMAG . COM | 2 0 2 1

The COVID-19 tax relief is governed according tothe Draft Disaster Tax Administration Relief Bill - 1April 2020.

A qualifying taxpayer is a company, trust, andindividual that: i) Conducts trade; ii) The grossincome does not exceed R100 million during theyear of assessment starting on or after 1 April 2020to 31 March 2021; iii) The gross income for the yearof assessment must not include more than 10percent of income derived from interest,dividends, foreign dividends, rental from lettingfixed property and any remuneration receivedfrom an employer.

A micro business for the purpose of this process, isa micro business as defined in the Sixth Scheduleto the Income Tax Act.

That is tax compliant: this means that the taxpayermust be fully tax compliant qualifying for a taxclearance.

The taxpayer must be registered for all applicabletaxes.

All tax returns across all tax types must have beensubmitted.

No outstanding tax debts, unless there is a validpayment agreement, approved suspension ofpayment pending an objection or appeal, or taxdebt less than R100.

The deferral of the provisional tax payment appliesto qualifying taxpayers who are required to submitprovisional tax returns for the period starting from1 April 2020 to 31 March 2021.

The first provisional tax payment due from 1 April2020 to 30 September 2020 will be based on 15 %of the estimated total tax liability.

The second provisional tax payment from 1 April2020 to 31 March 2021 will be based on 65% theestimated total tax liability (payment will be 65%less the 15% already paid).

Table showing the difference between the Covid-19 relief measure and normal provisional taxsubmission:

First Provisional

C O V I D - 1 9R E L I E F

Second Provisional

Third Provisional

50% (65 - 15%)

35%

15% 50%

N O R M A L

50%

Optional top-up

ABOUT

PAGE 4

BURNSACU T T . CO . ZA | 2 0 2 0

GOVERNMENT CONCESSIONS -COVID-19 RELIEF

WHEN MUS T PROV I S I ONA LTAX BE PA I D

I N T ERE S T AND P ENA L T I E S

PAGE 5

BURNSACU T T . CO . ZA | 2 0 2 0

The tax compliance test.The gross income threshold.To pay the 15% or the 65% by the relevant duedates.

The remaining 35% of the provisional tax liabilitywill be deferred and payable when making thethird provisional tax payment. This must be paidby the due date applicable to the relevanttaxpayer. Administrative penalties and interest willnot be levied on the deferred provisional taxliability for the first and second period.

COVID-19 tax relief will not apply to provisionaltaxpayers failing:

Where it is discovered that the provisionaltaxpayer did not qualify for the COVID-19 tax relief,the relevant relief will be withdrawn, and normalpenalties and interest will apply.

The deferral is exactly that, a deferral and all taxeswill have to be paid in the end.

You are not required to opt for the provisional taxrelief measures and can choose to declare and payprovisional tax as normal (50% first provisional and50% second provisional with third provisionaloptional top-up payment).

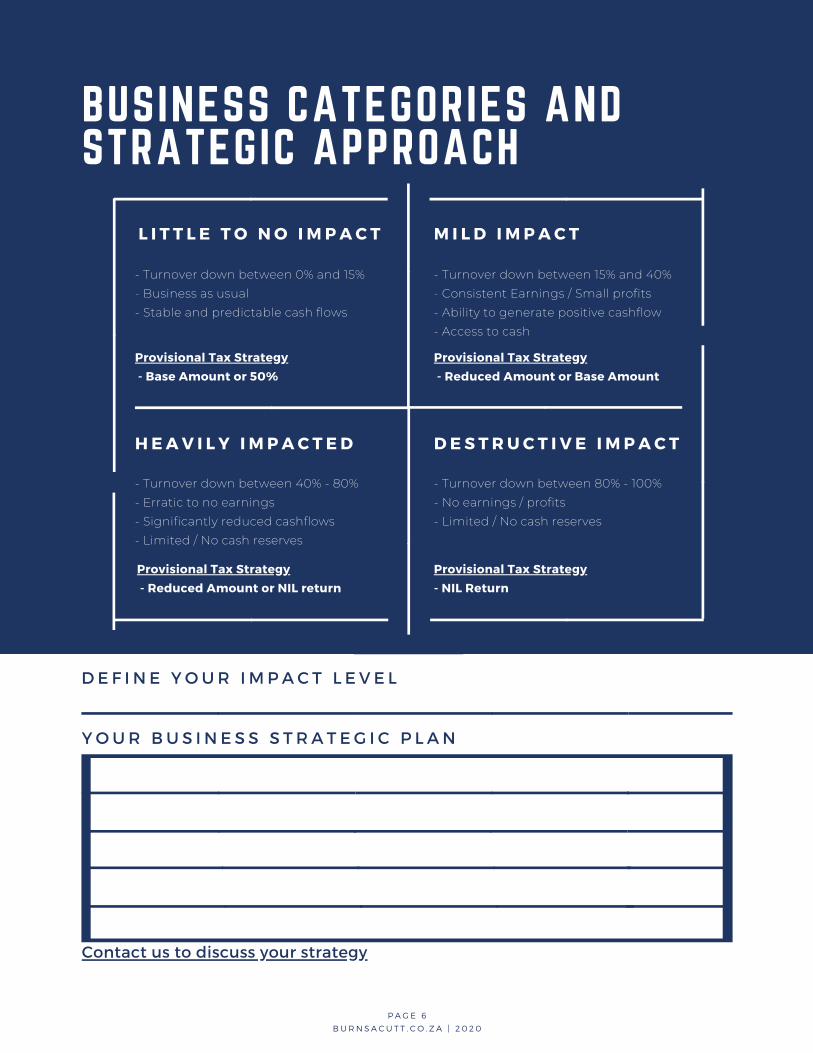

- Turnover down between 0% and 15% - Business as usual - Stable and predictable cash flows

L I T T L E TO NO I M PAC T M I L D I M PAC T

HEAV I L Y I M PAC T ED DES TRUC T I V E I M PAC T

- Turnover down between 15% and 40%- Consistent Earnings / Small profits- Ability to generate positive cashflow- Access to cash

- Turnover down between 40% - 80% - Erratic to no earnings - Significantly reduced cashflows - Limited / No cash reserves

- Turnover down between 80% - 100% - No earnings / profits - Limited / No cash reserves

Provisional Tax Strategy

- Base Amount or 50%

Provisional Tax Strategy

- Reduced Amount or Base Amount

Provisional Tax Strategy

- Reduced Amount or NIL return

Provisional Tax Strategy

- NIL Return

PAGE 6

BURNSACU T T . CO . ZA | 2 0 2 0

BUSINESS CATEGORIES ANDSTRATEGIC APPROACH

YOUR BUS I N E S S S T RA T EG I C P LAN

Contact us to discuss your strategy

DE F I N E YOUR I M PAC T L E V E L

Tel: (031) 563 8237

Fax: (031) 564 8736

Email: [email protected]

Website: www.burnsacutt.co.za

27 Canford Park

53 Anthony Road

Durban North, 4051

PO Box 35084

Northway, 4065

PAGE 7

BURNSACU T T . CO . ZA | 2 0 2 0