property tax and school funding in...

TRANSCRIPT

Property Tax and School Funding in Utah

Prepared by the Office of Legislative Research and General Counsel for:

Bagels and Briefings

September 17, 2008

Presentation Outline

• Property tax background• Education funding and property tax

– Basic indicators of school funding needs– School funding sources– School property taxes

• Tax base• Tax rates• Tax revenues

Presentation Outline

• Property tax background• Education funding and property tax

– Basic indicators of school funding needs– School funding sources– School property taxes

• Tax base• Tax rates• Tax revenues

Why Discuss Property Taxes Today?

• Property tax is on the mind of many taxpayers– Preliminary property tax statements mailed in July– Truth in taxation hearings in August– Final 2008 property tax rates set by taxing entities after truth in taxation

hearings, then verified and finalized by Tax Commission– Property tax bills mailed to property owners

• Property tax is a major school funding source– Majority of all property tax statewide goes to fund schools– General implications for overall education funding, including state budget

implications– Implications when a new school district is created

• Taxable values have increased rapidly in recent years– Rapid value increases in existing property– Significant value growth from new property development

Three Major State & Local Revenue SourcesIncome, Property, and Sales Tax

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Bill

ions

of D

olla

rs

Property TaxIndividual Income TaxSales and Use Tax (State and Local)

FY 1982 to FY 2007

Data Source: Utah State Tax Commission, Property Tax Division & Economic and Statistical Unit

Property TaxA Major Component of

Utah’s State and Local Government Tax System

State individual income tax

State, local, and county sales and use tax

Local property tax

Other state taxes (severance, insurance,

cigarette, etc.)

Other local taxes (excise, franchise, and earmarked sales tax)

State corporate taxes (franchise/income, gross receipts)

State transportation taxes

Data Source: Utah State Tax Commission Annual Report, FY 2007

Presentation Outline

• Property tax background• Education funding and property tax

– Basic indicators of school funding needs– School funding sources– School property taxes

• Tax base• Tax rates• Tax revenues

Presentation Outline

• Property tax background• Education funding and property tax

– Basic indicators of school funding needs– School funding sources– School property taxes

• Tax base• Tax rates• Tax revenues

Why Do School Districts Impose Property Taxes?

• To understand property taxes, it is helpful to initially consider why school districts impose the property tax

• Basic answer is to provide revenue to meet school funding needs– However, different definitions of funding “needs”

exist– What are some basic measures of funding needs?

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

65,000

70,000

75,000

80,000

85,000

Dag

gett

Tint

icP

iute

Ric

hW

ayne

Gar

field

Nor

th S

umm

itK

ane

Sou

th S

umm

itG

rand

Bea

ver

Juab

Mor

gan

Em

ery

Nor

th S

anpe

teS

an J

uan

Milla

rdS

outh

San

pete

Car

bon

Duc

hesn

ePa

rk C

ityS

evie

rW

asat

chLo

gan

Uin

tah

Mur

ray

Iron

Box

Eld

erO

gden

Tooe

lePr

ovo

Cac

heC

harte

r Sch

ools

Sal

t Lak

eW

ashi

ngto

nN

ebo

Web

erJo

rdan

-Eas

tJo

rdan

-Wes

tA

lpin

eD

avis

Gra

nite

Jord

an

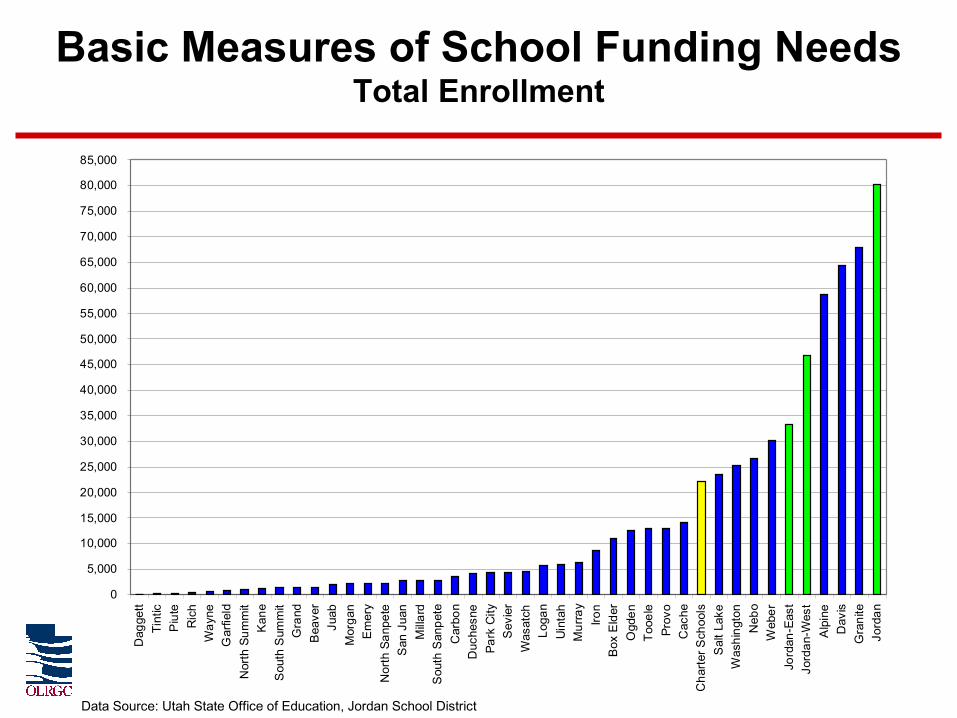

Basic Measures of School Funding NeedsTotal Enrollment

Data Source: Utah State Office of Education, Jordan School District

Basic Measures of School Funding NeedsEnrollment Growth

Data Source: Utah State Office of Education, Jordan School District

(1,000)

(500)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

Jord

an-E

ast

Gra

nite

Prov

oSa

n Ju

anM

illar

dE

mer

yO

gden

Loga

nM

urra

yS

alt L

ake

Piut

eTi

ntic

Kan

eG

arfie

ldD

agge

ttR

ich

Nor

th S

umm

itN

orth

San

pete

Way

neS

outh

Sum

mit

Bea

ver

Gra

ndC

arbo

nSe

vier

Sou

th S

anpe

teJu

abM

orga

nP

ark

City

Uin

tah

Duc

hesn

eB

ox E

lder

Was

atch

Cac

heIro

nW

eber

Neb

oTo

oele

Was

hing

ton

Dav

isJo

rdan

Jord

an-W

est

Alp

ine

Cha

rter

Sch

ools

1 Year Change in Enrollment3-year-average Change in Enrollment

Other Potential Measures of School Funding Needs

• Different types of students– Special education– English language learner– Gifted and talented– Low income

• Transportation / travel distance to school• Capital infrastructure

– Buildings (age, size, functionality, etc.)– Technology

• Other

Distribution of Needs and Tax Bases

• School needs, however defined, are very unlikely to perfectly match up with the tax base of any revenue source on a geographic basis (school-by-school or district-by-district)

• Examples:– Some states allow a local income tax. The distribution of

Utah’s income tax base does not align with the distribution of the student population (one basic measure of school need).

– Utah allows school districts to impose property tax. The distribution of the property tax base is not identical to the distribution of the student population (or of the income tax base).

Presentation Outline

• Property tax background• Education funding and property tax

– Basic indicators of school funding needs– School funding sources– School property taxes

• Tax base• Tax rates• Tax revenues

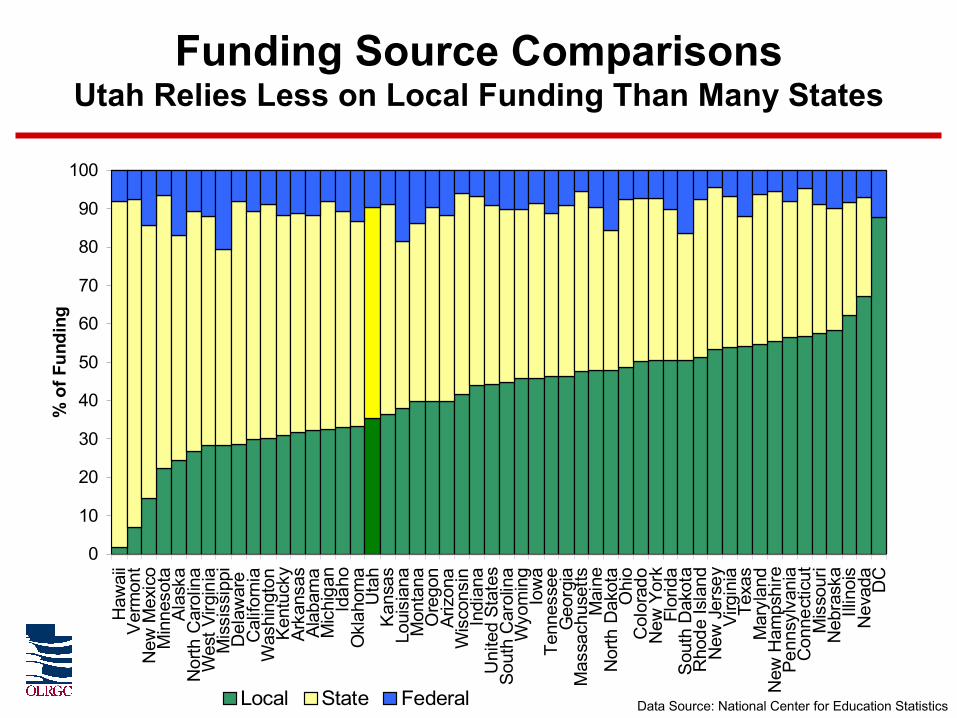

Funding Source ComparisonsUtah Relies Less on Local Funding Than Many States

Data Source: National Center for Education Statistics

0

10

20

30

40

50

60

70

80

90

100

Haw

aii

Ver

mon

tN

ew M

exic

oM

inne

sota

Alas

kaN

orth

Car

olin

aW

est V

irgin

iaM

issi

ssip

piD

elaw

are

Cal

iforn

iaW

ashi

ngto

nK

entu

cky

Arka

nsas

Alab

ama

Mic

higa

nId

aho

Okl

ahom

aU

tah

Kan

sas

Loui

sian

aM

onta

naO

rego

nAr

izon

aW

isco

nsin

Indi

ana

Uni

ted

Stat

esSo

uth

Car

olin

aW

yom

ing

Iow

aTe

nnes

see

Geo

rgia

Mas

sach

uset

tsM

aine

Nor

th D

akot

aO

hio

Col

orad

oN

ew Y

ork

Flor

ida

Sou

th D

akot

aR

hode

Isla

ndN

ew J

erse

yVi

rgin

iaTe

xas

Mar

ylan

dN

ew H

amps

hire

Penn

sylv

ania

Con

nect

icut

Mis

sour

iN

ebra

ska

Illin

ois

Nev

ada

DC

% o

f Fun

ding

Local State Federal

National ComparisonsMajor Education Revenue Sources by Region

Data Source: National Center for Education Statistics

Major Revenue Sources:– Income Taxes ($2.7 billion)– Property Taxes ($1.2 billion)– Federal Funds ($0.3 billion)– Dedicated Credits and Other ($0.06 billion)

Fiscal year 2008-09 estimates

Data source: Office of the Legislative Fiscal Analyst, Utah State Tax Commission

How is Utah Public Education Funded?

Property TaxA Major Component of Utah Public Education Funding

Data Source: Office of the Legislative Fiscal Analyst, State Office of Education

Income Tax

Other

Federal Funds

Property Tax Capital outlay,

debt service, other

Basic levy, voted leeway, board leeway

School Property Taxas a Percent of Total Property Tax

Special Districts 11%

Municipalities 15%

Counties18%

Schools 56%

Data Source: Utah State Tax Commission

School Property Tax Typesas a Percent of Total Property Tax

Special Districts

11%

Schools – Basic Levy (M&O)

12%

Schools – Other M&O

18%

Municipalities15%

Counties18% Schools – Capital Outlay /

Debt Service

24%Schools – Other

2%

Data Source: Utah State Tax Commission, State Office of Education

Property Tax Rates Vary by Location

Data Source: Utah State Tax Commission

-

0.002000

0.004000

0.006000

0.008000

0.010000

0.012000

0.014000

0.016000

0.018000

Kanab (Kane)

Woodruff(Rich)

Park City(Park City)

Circleville(Piute)

Salt Lake(Salt Lake)

Huntsville(Weber)

St. George(Washington)

Smithfield(Cache)

Bountiful(Davis)

Springville(Nebo)

Ogden(Ogden)

Tooele(Tooele)

Prop

erty

Tax

Rat

e

School District City County Special Districts

City (School District)

School Property Taxes as a Percent of Total Property Taxes

Data Source: Utah State Tax Commission

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Kanab (Kane)

Woodruff(Rich)

Park City(Park City)

Circleville(Piute)

Salt Lake(Salt Lake)

Huntsville(Weber)

St. George(Washington)

Smithfield(Cache)

Bountiful(Davis)

Springville(Nebo)

Ogden(Ogden)

Tooele(Tooele)

Scho

ol P

rope

rty

Tax

as %

of T

otal

Pro

pert

y Ta

x

School District City County Special Districts

City (School District)

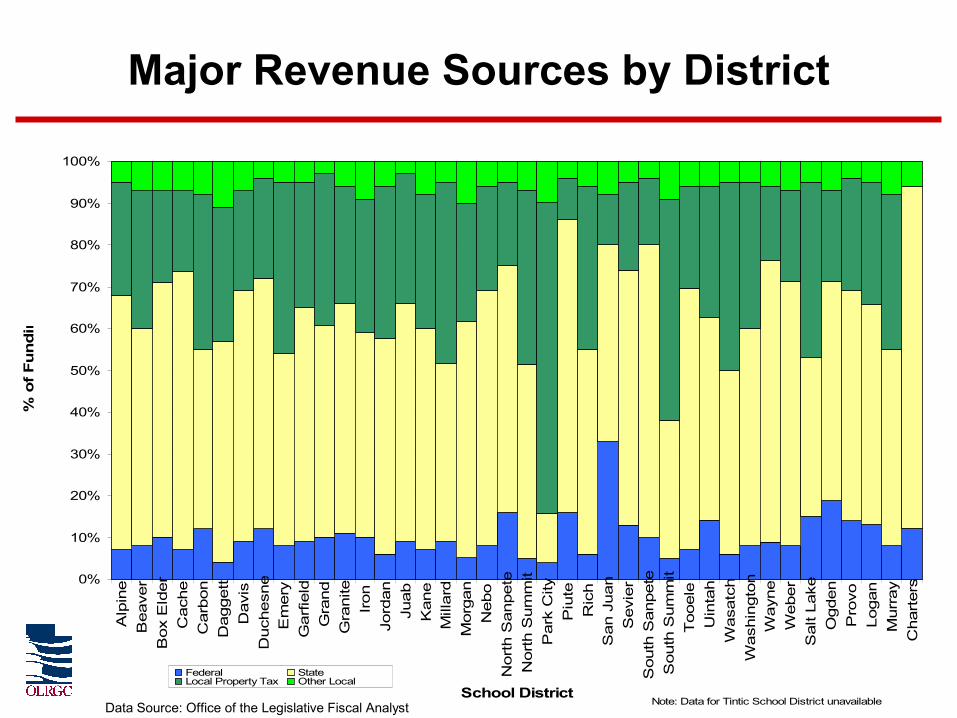

Major Revenue Sources by District

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Alp

ine

Bea

ver

Box

Eld

erC

ache

Car

bon

Dag

gett

Dav

isD

uche

sne

Em

ery

Gar

field

Gra

ndG

rani

teIr

onJo

rdan

Juab

Kan

eM

illar

dM

orga

nN

ebo

Nor

th S

anpe

teN

orth

Sum

mit

Par

k C

ityP

iute

Ric

hS

an J

uan

Sev

ier

Sou

th S

anpe

teS

outh

Sum

mit

Too

ele

Uin

tah

Was

atch

Was

hing

ton

Way

neW

eber

Sal

t Lak

eO

gden

Pro

voLo

gan

Mur

ray

Cha

rter

s

School District

% o

f F

un

din

g

Federal StateLocal Property Tax Other Local

Note: Data for Tintic School District unavailableData Source: Office of the Legislative Fiscal Analyst

Presentation Outline

• Property tax background• Education funding and property tax

– Basic indicators of school funding needs– School funding sources– School property taxes

• Tax base• Tax rates• Tax revenues

• Some school districts have greater ability than others to generate revenue through property tax – Measures of school funding needs (such as student populations)

and property values do not align geographically • Why do school district property tax bases vary?

– Overall fair market value differences in different areas– Different mix of property types (commercial, residential, agricultural,

etc.)– Exemption / valuation differences among property types

• Primary residences receive 45% exemption, so 55% of value taxable• Greenbelt agricultural properties valued based on agricultural

production, not parcel fair market value

• Charter schools have no property tax base and cannot impose a property tax

Property Tax Bases Vary

School District Property Tax Base Composition

Data Source: Utah State Tax Commission

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Alp

ine

Bea

ver

Box

Eld

erC

ache

Car

bon

Dag

gett

Dav

isD

uche

sne

Emer

yG

arfie

ldG

rand

Gra

nite

Iron

Jord

anJu

abKa

neLo

gan

Mill

ard

Mor

gan

Mur

ray

Neb

oN

orth

.San

pete

Nor

th.S

umm

itO

gden

Par

k C

ityP

iute

Prov

oR

ich

Sal

t Lak

eSa

n Ju

anSe

vier

Sout

h.S

anpe

teS

outh

.Sum

mit

Tint

icTo

oele

Uin

tah

Was

atch

Was

hing

ton

Way

neW

eber

Primary Residential Secondary Residential Commercial / Industrial (includes centrally assessed) Agricultural Vacant Land (non-FAA) Motor Vehicle

District A District B District CTax Base $1,000,000,000 $2,000,000,000 $5,000,000,000

Needed Revenue $1,000,000 $1,000,000 $1,000,000Rate Required to Generate Revenue 0.001000 0.000500 0.000200

Tax impact on $250,000 primary residence $138 $69 $28

Total Enrollment 8,000 4,000 2,000 Tax Base per Enrolled Student $125,000 $500,000 $2,500,000

Suppose 3 school districts each need to raise $1 million per year. The districts each have a different tax base from which to generate the $1 million. To generate the same amount of total revenue, a taxpayer with an identically valued home in District A will pay five times the amount of tax the taxpayer in District C pays, because District C is able to generate the same revenue at a lower tax rate due to its larger tax base.

Because school districts have different sized tax bases and varying numbers of students to serve, it can be difficult to directly compare taxing capacity among school districts. One method of comparison is to compute the tax base per enrolled student.

Impact of Property Tax Baseon Property Tax Revenues

$0

$250,000

$500,000

$750,000

$1,000,000

$1,250,000

$1,500,000

$1,750,000

$2,000,000

$2,250,000

$2,500,000

Cha

rter S

choo

lsTi

ntic

Sout

h S

anpe

teTo

oele

Neb

oD

avis

Cac

heO

gden

San

Juan

Nor

th S

anpe

teW

eber

Sev

ier

Box

Eld

erA

lpin

eJo

rdan

- W

est

Piut

eLo

gan

Juab

Duc

hesn

eG

rani

teS

tate

wid

e Av

erag

eBe

aver

Prov

oJo

rdan

Mor

gan

Way

ne Iron

Was

hing

ton

Mur

ray

Jord

an -

Eas

tG

arfie

ldU

inta

hC

arbo

nM

illar

dW

asat

chEm

ery

Gra

ndSa

lt La

keN

orth

Sum

mit

Sou

th S

umm

itK

ane

Ric

hD

agge

ttPa

rk C

ity

Prop

erty

Tax

Bas

e pe

r Stu

dent

Taxable Property Tax Base per Student

Data Source: Utah State Office of Education

• Operations Levies– Basic levy– Voted leeway– Board leeway– K-3 reading

• 10% of basic levy– 10% of basic levy can be

used both for certain operations purposes (textbooks and supplies) and for capital outlay / certain debt service purposes

• Capital Outlay & Debt Service Levies– Debt service– Capital outlay– Voted capital outlay (not

currently imposed)

• Other Levies– Special transportation– Recreation– Judgment– Tort Liability– Public Law 874 - Federal

impact aid / Title VII (not currently imposed)

School District Property Tax Levies

0.000000

0.001000

0.002000

0.003000

0.004000

0.005000

0.006000

0.007000

0.008000

0.009000

0.010000

Tin

ticT

ooel

eS

outh

San

pete

Ogd

enN

ebo

San

Jua

nD

uche

sne

Juab

Loga

nD

avis

Alp

ine

Bea

ver

Jord

anS

evie

rG

arfie

ldW

asat

chS

outh

Sum

mit

Cac

heN

orth

San

pete

Uin

tah

Box

Eld

erC

arbo

nM

illar

dW

ashi

ngto

nW

eber

Em

ery

Gra

nite

Nor

th S

umm

itIr

onM

orga

nP

rovo

Mur

ray

Sal

t Lak

eP

iute

Par

k C

ityG

rand

Dag

gett

Way

neR

ich

Kan

e

Tota

l Tax

Rat

e

Total Other Tax RatesTotal Capital Outlay & Debt Service Tax RatesTotal Maintenance & Operations Tax Rates

Utah School District Property Tax RatesTax Year 2007

Data Source: Utah State Office of Education

Property Tax Base per Student and Total Tax Rate

Data Source: Utah State Office of Education

Current School Funding Equalization

• Basic Program – Utah’s basic program (WPU) in the operations portion of the public education

budget is often seen nationally as a model of an equitable education funding system

– Similar students meeting qualifying characteristics are funded similarly• Districts with different property tax base receive same funding level

– Different student characteristics yield different funding amounts• Kindergarten student generates less funding than other grades (0.55 WPU)• Special education student generates more funding

– Each school district imposes the basic levy – an identical tax rate statewide– Because of the equalized basic program, a large portion of the maintenance and

operations budget for schools is equalized• Other Funding

– Schools can generate additional revenue by imposing certain property tax levies authorized by statute

• Some state funding minimally equalizes certain other property tax levies (voted leeway / board leeway guarantee) but not equalized near the extent of the basic program equalization

– School Building Program• Foundation Program• Enrollment Growth Program

– Non-WPU driven programs (“below-the-line”) funded with income taxes collected on an equal basis statewide

Basic Program (WPUs),

$1,840,119,735

Voted and Board Leeway,

$359,913,204

Related to Basic Program,

$857,278,121

One-time programs and Other,

$62,820,000

Components of the Minimum School Program

Data source: Office of the Legislative Fiscal Analyst, Public Education Budget Guide

Basic Levy History

$0

$50,000,000

$100,000,000

$150,000,000

$200,000,000

$250,000,000

$300,000,000

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

e

Year

Basi

c Le

vy R

even

ue

0.000000

0.000500

0.001000

0.001500

0.002000

0.002500

0.003000

0.003500

0.004000

0.004500

0.005000

Basi

c Le

vy R

ate

Basic Levy RevenueBasic Levy Rate

Data source: Utah State Office of Education

The Weighted Pupil Unit (WPU)

• The WPU is not total per-pupil spending• The WPU is used to determine the cost of the basic

school program on a uniform basis for each student– 1 WPU = 1 student in average daily membership (ADM)– Students in Kindergarten receive 0.55 WPUs– Specific programs generate additional WPUs, generally based

on student qualifications (special education, technology education, etc.)

• The Legislature establishes the WPU value annually– FY 2009 WPU Value = $2,577– Districts and charter schools receive basic program funding

based on their total number of WPUs• Hypothetical example:

1,000 WPUs x $2,577 = $2,577,000 (total basic program funding)

How is the Basic Program Equalized?

Hypothetical District 1,000 WPUs x $2,500 per WPU = $2,500,000 basic program amount Property tax base = $1,500,000,000 x basic levy (.001500) = $2,250,000 property tax revenue $250,000 Income Tax (Uniform School Fund)

$250,000

$2,250,000 $2,500,000

Property Tax

Income Tax $250,000

Basic ProgramTwo Hypothetical School Districts

District A District BValue of WPU $2,500 $2,500WPUs 1,000 1,000 Basic program statutory entitlement $2,500,000 $2,500,000

Net Taxable Value (Property Tax Base) $1,500,000,000 $500,000,000Basic levy (Tax Rate) 0.001500 0.001500 Basic Levy Yield (Property Tax Revenue) $2,250,000 $750,000

Allocation from Uniform School Fund $250,000 $1,750,000

Income Tax

Income Tax

Property Tax

Property Tax

Basic Levy (Property Tax)

$260 Million

Statewide Basic Program Funding Sources

Uniform School Fund (Income Tax)

$1.580 Billion

Data source: Office of the Legislative Fiscal Analyst, Public Education Budget Guide

Basic Program Amounts

Data source: Utah State Office of Education

$0

$25

$50

$75

$100

$125

$150

$175

$200

$225

$250

$275

$300Al

pine

Bea

ver

Box

Eld

erC

ache

Car

bon

Dag

gett

Dav

isD

uche

sne

Em

ery

Gar

field

Gra

ndG

rani

teIro

nJo

rdan

Juab

Kan

eLo

gan

Mill

ard

Mor

gan

Mur

ray

Neb

oN

orth

San

pete

Nor

th S

umm

itO

gden

Park

City

Piut

ePr

ovo

Ric

hS

alt L

ake

San

Jua

nS

evie

rS

outh

San

pete

Sou

th S

umm

itTi

ntic

Tooe

leU

inta

hW

asat

chW

ashi

ngto

nW

ayne

Web

erC

harte

r Sch

ools

Mill

ions

Estim

ated

Bas

ic P

rogr

am F

undi

ng A

mou

nt Uniform School FundProperty Tax

Basic Program Funding Source

Data source: Utah State Office of Education

Property Tax

$484M

Capital Outlay Foundation Program

$24.4M ongoing

Capital Outlay Enrollment

Growth Program

$2.9M ongoing

FY 2007-08

Statewide School District Capital Outlay Funding Sources

Data source: Utah State Office of Education

School Funding SystemRelies on Accurate Property Valuation

• Failure to accurately and uniformly assess properties at fair market value distorts the allocation of school funds– With the truth-in-taxation certified rate process,

undervaluation of properties in one area causes higher taxes statewide through an increase in the certified rate for the basic levy

– In addition to basic program funding, other state funds are also tied to property tax values per student, including voted/board leeway guarantees and capital outlay foundation program

• So assessment practices by the Tax Commission and assessors in each county impact taxpayers statewide

Property Tax Revenue per Student

2008 General Session School Property Tax Equalization Bills

• HB 1 – Basic Program– Establishes the tax year 2008 basic levy rate (estimated)

• SB 2 – Basic Program and Property Tax Allocations for Charter Schools– Increases the value of the WPU to $2,577– Requires school districts to provide a portion of revenue from certain

property tax levies for charter school students residing within the district boundaries

• SB 48 – School District Capital Outlay – Requires a partial equalization of the capital outlay property tax levy

within Salt Lake County

Theoretical Equalization Continuum

User Fee

Only parents of children in

schools

Secondary school fees

Impact Fee

Owners of new homes

and new businesses

Currently prohibited by

statute

District-wide Equalization

All property owners within school district

Discretionary school property tax levies

(voted leeway, board leeway, debt service levy, capital outlay

levy, etc.)

County-wide Equalization

All property owners within a county

(same as district in all but 7 counties)

Partial capital outlay equalization in county of

the first class

Statewide Equalization

Taxpayers statewide

Basic levy / basic program, educator salary adjustments, state pupil

transportation funds

Who should pay for school costs?

Please feel free to contact staff with any questions:

Office of Legislative Research and General Counsel

(801) 538-1032