privatization in lebanon middle east airlines; a case study faisal m. nsouli, ph.d. january 2007...

TRANSCRIPT

Privatization in Lebanon

Middle East Airlines; A Case Study

Privatization in Lebanon

Middle East Airlines; A Case Study

Faisal M. Nsouli, Ph.D.January 2007

L.E.A.

Special acknowledgements to my research assistants:

Mr. Joseph Reaidy, Mr. Ehab Salameh and Ms. Souad Daher

2

F.M. Nsouli, Ph.D.

Lebanese Economic Association

Table of contentsTable of contents I. Definition 5 Why To Privatize 6 Economic and financial effects of privatization

7-9

• Company performance 7• Fiscal Adjustments 8• Foreign Investment 8 • Capital Market Development 9• Employment 9

II. Privatization process 10-14

• Feasibility study 10• Preparation 11• Enterprise valuation 12• Privatization Techniques 13, 14

III. Current economic situation in Lebanon 15 - 19

Slide #

3

F.M. Nsouli, Ph.D.

Lebanese Economic Association

Table of contentsTable of contentsIV. The Need to privatize in Lebanon 20, 21V. MEA Background 22, 23

Restructuring 24 After Restructuring 25 MEA Potential for Growth 26, 27 Current/Future Status 28 - 30 MEA Fleet characteristics 31 - 33 Valuation 34 - 43 MEA Expected Value 44 MEA Share Price 45 Privatization Technique 46 Expected Results 47 - 50

• Lebanese Government 47• MEA’s Benefits from Strategic Partner 48• MEA 49• Consumer Satisfaction 50

VI. Conclusion 51 - 53

Slide #

4

F.M. Nsouli, Ph.D.

Lebanese Economic Association Abbreviations and

AcronymsAbbreviations and

AcronymsA319 Airbus 319 IPO Initial Public Offering

A321 Airbus 321 MASCO Mideast Aircraft Services Company

A330-200 Airbus 330-200 MEA Middle East Airlines

A310 Airbus 310 MEAG Middle East Airlines Ground Handling

A320 Airbus 320 MEAS Middle East Airports Services

B707 Boeing 707 M meter

B747 Boeing 747 Mil Million

BDL Banque Du Liban N.M Nautical miles

BOT Build operate transfer NPV Net Present Value

CCQ Cross Crew Qualification O TV Orange television

Disc Discounted Pax Passenger

ESOP Employee Stock Ownership Plan SOE State Owned Enterprise

GAAP Generally Accepted Accounting Principles UK United Kingdom

GDP Gross Domestic Product US United States

IFC International Finance Corporation Yr Year

IMF International Monetary Fund

5

F.M. Nsouli, Ph.D.

Lebanese Economic Association

I. DefinitionI. Definition "Privatization is defined as the transfer

of assets and service functions from the public to the private sector" (Manzetti 1999, 1).

While there are different forms of privatization, a widely accepted definition of privatization encompasses the privatization of management as well as the privatization of ownership.

6

F.M. Nsouli, Ph.D.

Lebanese Economic Association

Why To PrivatizeWhy To Privatize Privatization has been a growth business all

over the world in the past decade, there are many reasons behind governments’ will to privatize; which include:

Maximizing return. Increasing capital market. Restructuring debt position. breaking up monopolies. promoting investment. reducing public expenditure. ensuring continuity of service. improving efficiency. Reduce corruption.

7

F.M. Nsouli, Ph.D.

Lebanese Economic Association Economic and Financial

Effects of PrivatizationEconomic and Financial Effects of Privatization

Privatization usually leaves a positive impact on the country, which affects:

1. Company performance: There is near unanimity that Privatization had lead to improvement in company performance (both financial and operational). The impact can be measured by looking at the following firm’s positive performance indicators:

– Profitability– Labor productivity– Investment– Output– Financial leverage

Improved performance is primarily due to the fact that

once the private sector takes over a SOE, profitability becomes paramount.

8

F.M. Nsouli, Ph.D.

Lebanese Economic Association Economic and Financial

Effects of PrivatizationEconomic and Financial Effects of Privatization

2. Fiscal Adjustments: governments often implement privatization to either reduce the burden of loss-making enterprises on public funds or to raise additional revenues to refill a financial gap. Governments have to accompany privatization with parallel measures to manage the public debt efficiently and to reduce the budget deficit.

3. Foreign Investment: Privatization and foreign investments are linked in ways: direct impact, indirect impact and catalytic impact.

• Direct impact: privatization attracts foreign investors by giving them the right to develop a new infrastructure facility or the right to deliver infrastructure services, but in both cases they should give in new investments.

• Indirect Impact: Privatization leads to the development of capital markets which with the proper regulatory framework attract foreign portfolio investments.

• Catalytic impact: is when privatization puts the developing country on the investor's radar screen and generates interest in it.

9

F.M. Nsouli, Ph.D.

Lebanese Economic Association Economic and Financial

Effects of PrivatizationEconomic and Financial Effects of Privatization

4. Capital Market Development: privatization has been the most important factor in the development of capital markets. It has led to growth and liquidity of the financial markets.

5. Employment: the impact of privatization on employment is not clear yet but it can be observed as neutral or positive. If the government couples privatization with adequate labor policy and social safety nets, the impact on employment will definitely be positive.

10

F.M. Nsouli, Ph.D.

Lebanese Economic Association II. Privatization

ProcessII. Privatization

Process1. Feasibility studyThe feasibility study should address the following aspects: Present financial viability and the need to minimize

costs and financial losses and to preserve asset values. The nature of the industry, the existing technology

involved and the need for new technology or market access.

The known or expected type and level of investor interest.

Consumer interests The constraints to privatization. The need, if any, to preserve part public ownership. The need, if any, to preserve the interests of

shareholders or managers. The short and longer term impact on employment. The need to maximize the proceeds of privatization. The need to maximize the eventual returns to Treasury.

11

F.M. Nsouli, Ph.D.

Lebanese Economic Association II. Privatization

ProcessII. Privatization

Process 2. Preparation: In a typical transaction, the Privatization

Commission, in consultation with the relevant ministry, submits a Summary of the proposed transaction to its Board. The Summary justifies the need for privatizing the property, the feasibility study, outlines the likely mode of privatization, and sometimes seeks guidance on issues relating to such matters as pricing, restructuring, legal considerations, and the regulatory framework. Once endorsed by the Board, it is submitted to the Cabinet for approval.

12

F.M. Nsouli, Ph.D.

Lebanese Economic Association

Privatization ProcessPrivatization Process

3.Property valuation : In order to obtain an independent assessment of

the value of the property being privatized, the Commission relies primarily on external firms. The Financial Advisor, where there is one, carries out the valuation to obtain a “reference price” for the property. In other cases, the Commission contracts with an external valuation firm or accounting firm as specified in the rules on the valuation of property. The methods used for the valuation vary with the type of business and often more than one method is used in determining the value. These include the discounted cash flow method, asset valuation at book or market value, and stock market valuation. The true value is dependent on many variables such as country risk, corporate strategy, and perceptions of future macroeconomic performance. Only the market can determine the true value.

13

F.M. Nsouli, Ph.D.

Lebanese Economic Association

Privatization ProcessPrivatization Process4.Privatization techniques Initial public offering (IPO) IPO is designed to achieve equity through widespread

public shares. It relies on sale of low priced public participation shares.

Build-Operate-Transfer (BOT) The private sector designs, finances, builds, and

operates the facility over the life of the contract. At the end of this period, ownership reverts to the government.

Contracting Out The government competitively contracts with a private

organization, for-profit or non-profit, to provide a service or part of a service.

Management ContractsThe operation of a facility is contracted out to a private company.

14

F.M. Nsouli, Ph.D.

Lebanese Economic Association

Privatization ProcessPrivatization Process Vouchers

Government pays for the service; however, individuals are given redeemable certificates to purchase the service on the open market.

Asset Sale or Long-Term Lease• Government sells the asset to a private sector

entity and then leases it back, thus turning physical capital into financial capital.

• Another asset sale technique is the employee buyout. Existing public managers and employees take the public unit private, typically purchasing the company through an Employee Stock Ownership Plan (ESOP).

15

F.M. Nsouli, Ph.D.

Lebanese Economic Association III. Current Economic

Situation in LebanonIII. Current Economic Situation in Lebanon

The direct and indirect costs of the July 2006 war far exceed the capacity of any middle-income country to bear, let alone a country that has been saddled with a very large public debt and a country that had just come out of a major setback associated with the assassination of Prime Minister Hariri, which has left deep scars on the economic and political landscape. As a result, the burden of Lebanon’s public debt has become even heavier.

Based on assessments carried out by

independent consultants retained by the Prime Minister’s Office, the total direct cost of early recovery and reconstruction is now estimated at around US$2.8 billion.

16

F.M. Nsouli, Ph.D.

Lebanese Economic Association Current Economic

Situation in LebanonCurrent Economic

Situation in Lebanon In the early 1990s, the government

undertook the task of reconstruction of public infrastructure, and of investing in social peace.

With eroded revenue base, the government relied heavily on borrowing domestically, in addition to some external loans.

The gross public debt started rising sharply from $2 billion in 1990 to $15.3 billion in 1997 and to $25 billion by the year 2000 equivalent to 150% of GDP. Then increasing at a rough $3 billion per year and reaching $36 billion in 2004 and $38 billion in 2005 equal to 175% of GDP.

17

F.M. Nsouli, Ph.D.

Lebanese Economic Association Current Economic

Situation in LebanonCurrent Economic

Situation in LebanonSaddled with such a large public debt,

and just coming out of a major setback associated with the assassination of Prime Minister Hariri (2005), which has left deep scars on the economic and political landscape, Lebanon further took another shock represented in the July war; and the burden of Lebanon’s public debt has become even heavier.

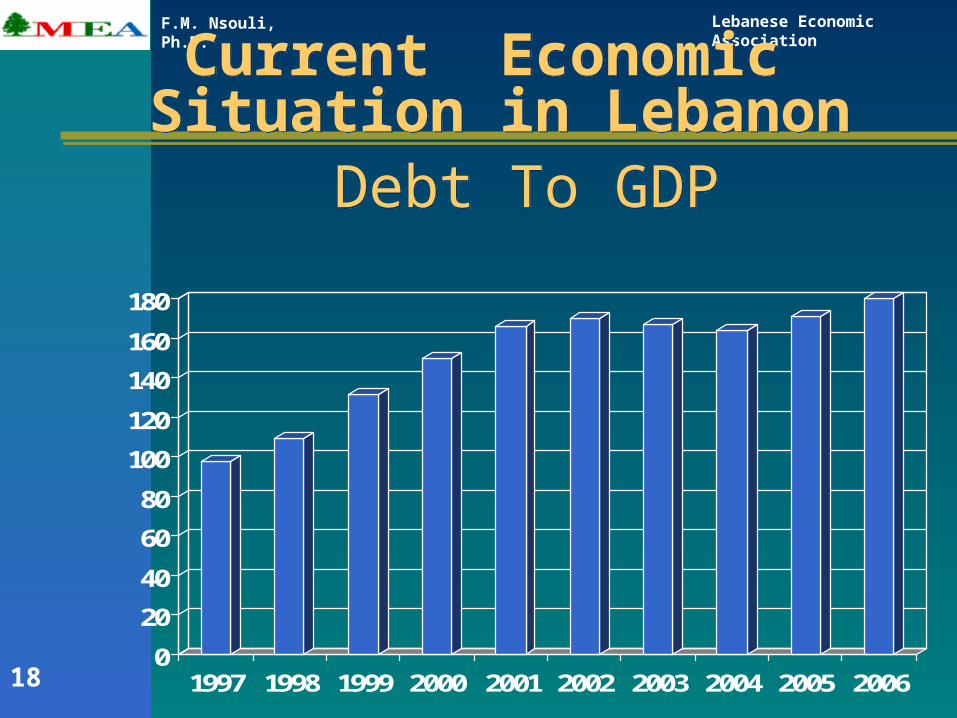

As a result, total gross public debt reached US$40.5 billion end of 2006—equivalent to 180% of estimated post war 2006 GDP.

18

F.M. Nsouli, Ph.D.

Lebanese Economic Association Current Economic

Situation in LebanonCurrent Economic

Situation in Lebanon

0

20

40

60

80

100

120

140

160

180

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Debt To GDPDebt To GDP

19

F.M. Nsouli, Ph.D.

Lebanese Economic Association Current Economic

Situation in LebanonCurrent Economic

Situation in Lebanon 65% of the public debt outstanding matures between

2007 & 2010, in addition to most of the new borrowing during and subsequent to the July war. Close to US$16 billion of the debt outstanding as of mid-2006 matures in 2007and 2008.

Debt (as of June 30, 2006) maturing in the years

2007-2010 (US$ billion)

Total

2007-08

2009-10

2007-10

Foreign Currency Debt 4.5 5.5 10.0

Local Currency Debt 11.4 3.4 14.8

Total Public Debt excluding interest

15.9 8.9 24.8

20

F.M. Nsouli, Ph.D.

Lebanese Economic Association IV. Need to Privatize

in LebanonIV. Need to Privatize

in Lebanon The IMF has long maintained that privatization

is not an end in itself, but a means to achieving an end.

In Lebanon, the end should not be seen solely in terms of getting the highest return from privatization to reduce the public debt. Indeed, the total valuation of enterprises with the potential for privatization is quite small in relation to the total debt (around 10-15 percent).

Rather, the end should be to reduce the cost and enhance the quality of service in key industries such as power, telecommunications, and transportation, with the ultimate aim of spurring economic growth.

21

F.M. Nsouli, Ph.D.

Lebanese Economic Association IV. Need to Privatize

in LebanonIV. Need to Privatize

in Lebanon A Public-Private Partnership Strategy

needs to be developed which conceives of the full scope of private participation options, from service contracts all the way to full privatization, and is applied differently to SOEs that are very different in nature (water, electricity, telecommunications, tobacco, ports, casinos, MEA).

MEA is one of many promising SOES , following is a study of MEA privatization.

22

F.M. Nsouli, Ph.D.

Lebanese Economic Association

V. MEA BackgroundV. MEA Background MEA was established in 1945.The Lebanon

based airline lunched its first service routes to Syria, Cyprus and Egypt; it then establish regular passenger service to the gulf region.

By the early 1970’s MEA was going through its golden age earning a total revenue in 1974 approximately equal to $140 million.

From 1975 till 1990 MEA suffered losses as a direct result of the civil war.

23

F.M. Nsouli, Ph.D.

Lebanese Economic Association

MEA BackgroundMEA Background After the return to normality in 1990 till

1998,MEA started to become a burden for the Lebanese government especially with its continuous losses due to many reasons; mainly:

-The direct consequences of the war. -The overstaffed employees. -The relatively old fleet (unable to

compete). -Corruption/heavy expenses.

As a result, restructuring was a must to solve these problems (it also served as a first step towards privatization).

24

F.M. Nsouli, Ph.D.

Lebanese Economic Association

RestructuringRestructuring Due to the study conducted by the

International Funding Corporation (IFC), the following steps were imposed:

1. Laying off around 1500 employees; this was accompanied by the Union’s opposition, but with Government’s support.

2. Down sizing destination/Fleet where many destinations were closed, all old Aircraft were sold (B707, B747) and replaced by leased Airbus A310 & A320.

3. Reorganization into affiliated companies: MEA, MEAS, MEAG, MASCO.

25

F.M. Nsouli, Ph.D.

Lebanese Economic Association

After RestructuringAfter Restructuring As a result, MEA income statement

changed from suffering great losses to breaking even in 2002, and earning profits in 2003.

2004: $ 50 m net profit were declared.

2005: $46 m were declared despite the political instability (Hariri assassination ).

2006: $10 m are expected despite the latest destructive war on Lebanon.

26

F.M. Nsouli, Ph.D.

Lebanese Economic Association MEA Potential for

GrowthMEA Potential for

Growth MEA may increase its market share

due to the presence of many potential destinations like: Berlin, Copenhagen, Brussels, Doha, Bahrain, Dhahran, Tehran, Montreal, New York, Sao Paolo, Singapore, Sydney, Beijing…(Most of them were old destinations).

Potential to increase flights’ frequency of some of the demanding destinations namely to: Dubai, Riyadh, Paris, and London (especially during summer season).

27

F.M. Nsouli, Ph.D.

Lebanese Economic Association MEA Potential for

GrowthMEA Potential for

Growth Potential to reduce costs by adding

more airplanes to the Fleet, which will lead to:

– Reduce costs of leasing.

– Benefit from some economies of scale (crew/employees/operating fees).

28

F.M. Nsouli, Ph.D.

Lebanese Economic Association

Current/Future StatusCurrent/Future Status MEA currently owns 6 Airbus A321

fully equipped, capacity: 31J/118Y. In addition MEA leases 3 Airbus A330-200 capacity 42J/208Y.

In mid December 2006 MEA signed a contract to purchase 4 additional Airbus A319, proposed capacity 24J/80Y and 4 additional Airbus A330 to replace the current leased ones.

Delivery of these Aircrafts is expected to be in 2008 and 2009.

29

F.M. Nsouli, Ph.D.

Lebanese Economic Association

Current/Future StatusCurrent/Future Status This new purchase is expected to open

new horizons for MEA where:– New routes/destinations will be added.– Frequency flights on current routes

will be increased .– Potential to add more Aircrafts in the

future.– Better cross utilization of the Fleet.

The company is also studying an option to add another 5 Aircrafts in 2010 and 2011

30

F.M. Nsouli, Ph.D.

Lebanese Economic Association

Current/Future StatusCurrent/Future Status

Current Situation

By 2010

Aircrafts owned

6 Airbus A3213 Airbus A330 leased

6 Airbus A3214 Airbus A3194 Airbus A330

Flights and destinations

20 destinations*108 flights/week

34 destinations170 flights/week

* Additional destinations during special holidays and seasons e.g. Sharm El Sheikh

31

F.M. Nsouli, Ph.D.

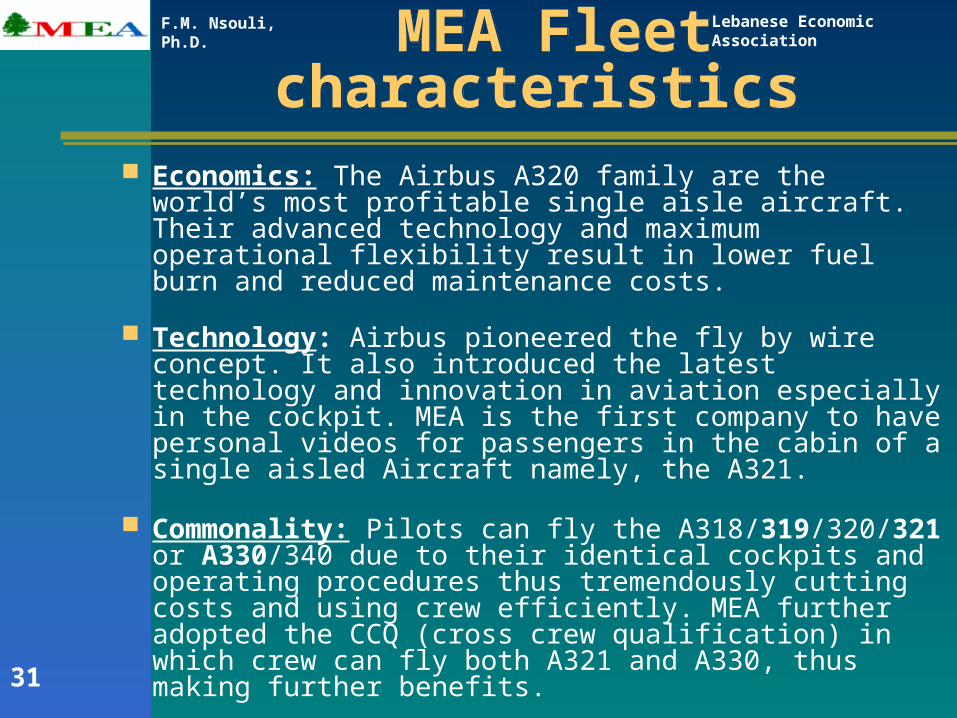

Lebanese Economic Association MEA Fleet

characteristics MEA Fleet

characteristics Economics: The Airbus A320 family are the world’s

most profitable single aisle aircraft. Their advanced technology and maximum operational flexibility result in lower fuel burn and reduced maintenance costs.

Technology: Airbus pioneered the fly by wire concept. It also introduced the latest technology and innovation in aviation especially in the cockpit. MEA is the first company to have personal videos for passengers in the cabin of a single aisled Aircraft namely, the A321.

Commonality: Pilots can fly the A318/319/320/321 or A330/340 due to their identical cockpits and operating procedures thus tremendously cutting costs and using crew efficiently. MEA further adopted the CCQ (cross crew qualification) in which crew can fly both A321 and A330, thus making further benefits.

32

F.M. Nsouli, Ph.D.

Lebanese Economic Association MEA Fleet

characteristicsMEA Fleet

characteristics Route Optimization: the different capacity and

range of the different Airbus family enables companies to better optimize their routes:

• The A321 can be used for most of the demanded routes of the MEA network.

• The A330 can best be utilized on long routes like: New York, Montreal, Sao Paolo, London, Paris … it could also be used to cover highly demanded short and medium routes (Dubai, Riyadh, Cairo, Kuwait)

• The A319 with its lowest passenger capacity can be used for the less demanded routes (Istanbul, Athens, Geneva …) and thus benefit from savings on fuel, over flying fees, and landing fees.

33

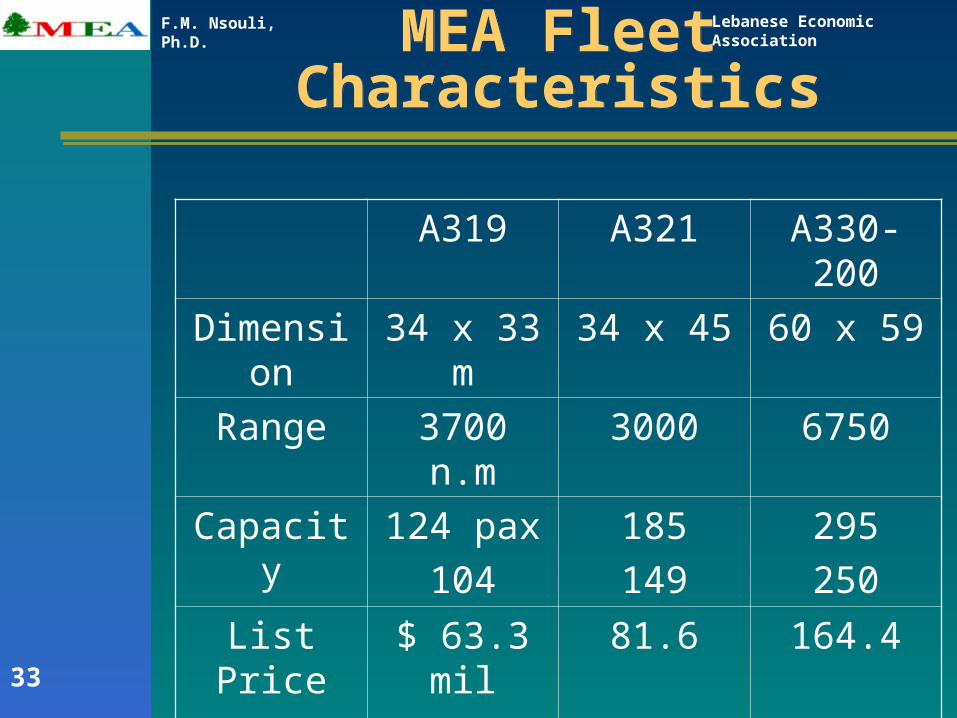

F.M. Nsouli, Ph.D.

Lebanese Economic Association MEA Fleet

CharacteristicsMEA Fleet

Characteristics

A319 A321 A330-200

Dimension

34 x 33 m

34 x 45 60 x 59

Range 3700 n.m

3000 6750

Capacity 124 pax104

185149

295250

List Price2006

$ 63.3 mil

81.6 164.4

34

F.M. Nsouli, Ph.D.

Lebanese Economic Association

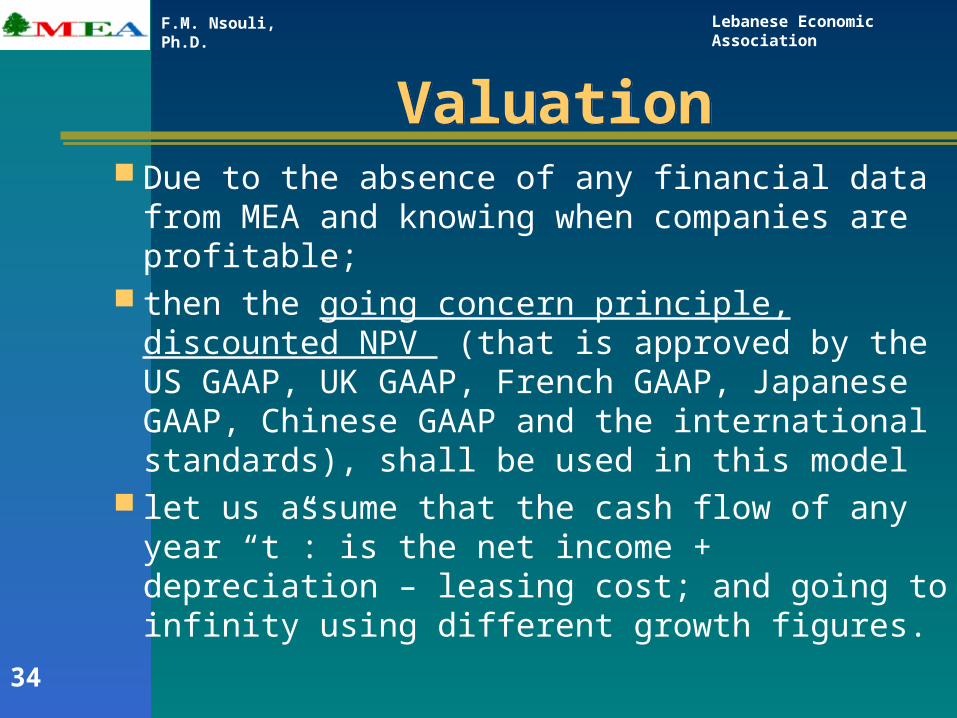

ValuationValuation Due to the absence of any financial data

from MEA and knowing when companies are profitable;

then the going concern principle, discounted NPV (that is approved by the US GAAP, UK GAAP, French GAAP, Japanese GAAP, Chinese GAAP and the international standards), shall be used in this model

let us assume that the cash flow of any year “t”: is the net income + depreciation – leasing cost; and going to infinity using different growth figures.

35

F.M. Nsouli, Ph.D.

Lebanese Economic Association

ValuationValuation Different growth rates are used for the first six years,

constant growth for the next 6 years, and zero growth thereafter.

Five scenarios of expected net Incomes are estimated:Upper-bound optimisticOptimisticRecessionWorstLower-bound worst

Each scenario is given an estimated probability taking into account historical data.

36

F.M. Nsouli, Ph.D.

Lebanese Economic Association

ValuationValuation Leasing costs are deducted from the average

net income, depreciation is then added to the average net income to get average cash flow.

Three different discounted rates are estimated each with an approximate probability.

The value of the Company is equal to:Net present value of the first 6 years plus NPV of the next 6 years plus NPV of the perpetuity thereafter, using the weighted average discounted rate.

37

F.M. Nsouli, Ph.D.

Lebanese Economic Association

ValuationValuation Growth Rate estimation:

– Part of the growth is related to the country’s expected economic situation and the general demographic growth.

– A second part is related to adding new Aircrafts, this effect is realized between 2008 and 2011. Each A319 attributes to approx 9% growth and the A330 attributes to approx 16% growth through out the three year period.

– A final part is due to what is called the “after effect” of adding new aircrafts, it will be realized by years 2011 and 2012.

Year 2007

2008

2009 2010

2011

2012 2013 till 201

8

2019onwar

d

Growth

8% 13 16 19 22 13 4 0

38

F.M. Nsouli, Ph.D.

Lebanese Economic Association

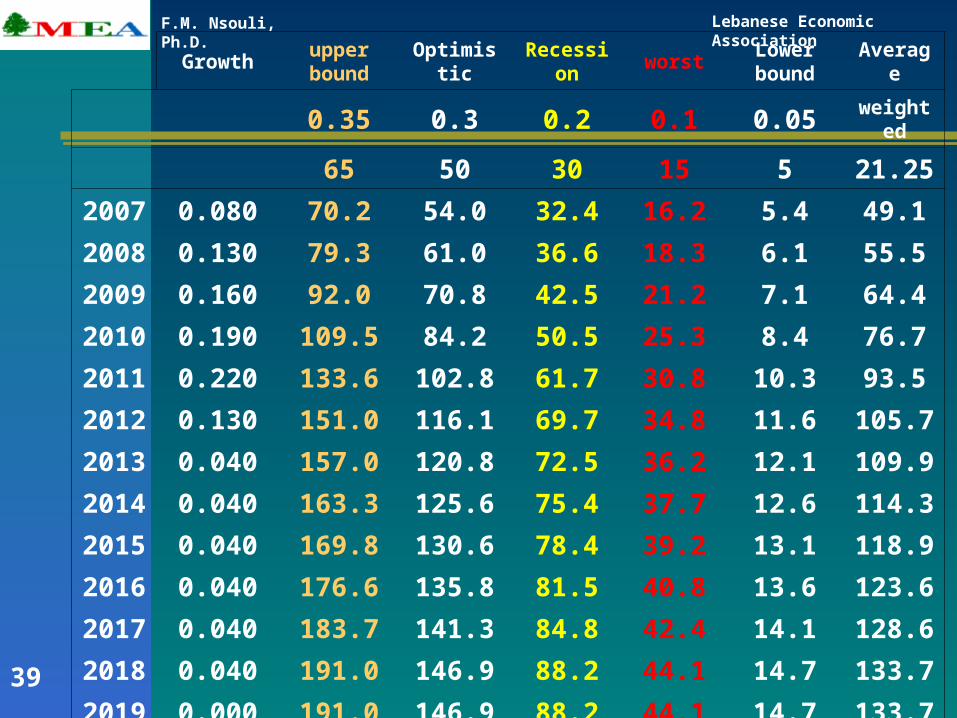

ValuationValuation The Five scenarios of expected net income are:

– Upper-bound Optimistic: represented by a year like 2006,had there not been a war, in which MEA was expecting a $65 mil in net revenue. Probability of 35%

– Optimistic: a year like 2004 which was stable, MEA earned a $50 million net revenue, this scenario is given a probability of 30%.

– Recession: year 2005 is an example, which was politically and economically unstable, with a probability of 20%.

– Worst: year 2006 is an example, a probability of 10%.– Lower-bound worst: a projected worst scenario,

probability of 5% .

39

F.M. Nsouli, Ph.D.

Lebanese Economic Association

Growthupper bound

Optimistic

Recession

worstLower bound

Average

0.35 0.3 0.2 0.1 0.05 weighted

65 50 30 15 521.2

5

2007

0.080 70.2 54.0 32.4 16.2 5.4 49.1

2008

0.130 79.3 61.0 36.6 18.3 6.1 55.5

2009

0.160 92.0 70.8 42.5 21.2 7.1 64.4

2010

0.190 109.5 84.2 50.5 25.3 8.4 76.7

2011

0.220 133.6 102.8 61.7 30.8 10.3 93.5

2012

0.130 151.0 116.1 69.7 34.8 11.6105.

7

2013

0.040 157.0 120.8 72.5 36.2 12.1109.

9

2014

0.040 163.3 125.6 75.4 37.7 12.6114.

3

2015

0.040 169.8 130.6 78.4 39.2 13.1118.

9

2016

0.040 176.6 135.8 81.5 40.8 13.6123.

6

2017

0.040 183.7 141.3 84.8 42.4 14.1128.

6

2018

0.040 191.0 146.9 88.2 44.1 14.7133.

7

2019

0.000 191.0 146.9 88.2 44.1 14.7133.

7

40

F.M. Nsouli, Ph.D.

Lebanese Economic Association

ValuationValuation Depreciation Calculation:

The depreciation method used is the simple straight line method based on the salvage value of the Aircrafts and the life expectancy for Airbus aircrafts.

Price

($ mil)Salvage Life Yearly

A319 60.4 4 25 2.37

A321 78 7 25 2.84

A330 158 10 25 6.18

41

F.M. Nsouli, Ph.D.

Lebanese Economic Association

ValuationValuation Adding Depreciation to the Net income,

then subtracting the cost of leasing (for the next 3 years as leasing contracts all end by 2010) to get Cash Flow.

Year 2007

2008

2009

2010

2011

2012

2013

2014

2015

NetIncome

49.1

55.5

64.4

76.7 93.5 105.7

109.9

114.3

118.9

AddDepreciatio

n

17 17 33.4

49.7 49.7 49.7 49.7 49.7 49.7

SubtractLease

9 7.5 6 0 0 0 0 0 0

CashFlow

57.2

65.1

91.8

126.4

143.3

155.4

159.6

164.0

168.6

42

F.M. Nsouli, Ph.D.

Lebanese Economic Association

ValuationValuation Three different discounted rates are

used:– Normal of 10% which is the actual

Lebanese bond yield, the probability of this rate to occur is 50%.

– Optimistic discounted rate of 7%, which is the expected bond yield (Paris 3 benefits expectation), with a probability of 35% .

– High discount rate of 12% which has a probability of 15%.

43

F.M. Nsouli, Ph.D.

Lebanese Economic Association

ValuationValuation

NPV

Disc RateProbability

7%0.35

10%0.5

12%0.15

Total ValueUp to yr 12

1028.2 855.5 762.1

•NPV of the cash flow up to year 12: NPV of the cash flow up to year 12: $901.9$901.9 mil. mil.•Value of Perpetuity at year 12 → ∞: Value of Perpetuity at year 12 → ∞: $1983$1983 mil. mil.•NPV of Perpetuity: NPV of Perpetuity: $686.0$686.0 mil. mil.

44

F.M. Nsouli, Ph.D.

Lebanese Economic Association

MEA Expected ValueMEA Expected Value

Adding the NPV of the cash flow up to year 12 with the NPV of the perpetuity, we get the average weighted value of MEA equal :

≈$1.588 billion

45

F.M. Nsouli, Ph.D.

Lebanese Economic Association

MEA Share PriceMEA Share Price The price should attract the highest

number of investors (domestic and international).

The Price should be attractive enough for “the small” investor. This will enhance the wide spread participation leading to widespread brand loyalty.

The most appropriate method to be used will be: IPO new issue (like: OTV ) or solidere split 10 for 1, (this will generate the maximum revenue possible) the proposed price :

10 $/share

46

F.M. Nsouli, Ph.D.

Lebanese Economic Association

Privatization TechniquePrivatization TechniqueThree phases:

1. Phase one: 24% of total outstanding shares offered as

IPOs to be listed in Beirut stock exchange. 25% of total outstanding shares to be sold to

a strategic partner.51% remains with BDL

2. Phase Two: 25%To be sold as IPOs in a period of 6 years.

3. Phase Three :26%To be sold as IPOs in a period of 6 years following phase two and three might be re-adjusted in the years to come according to the government’s and company’s need.

47

F.M. Nsouli, Ph.D.

Lebanese Economic Association

Expected ResultsExpected Results Lebanese Government:

• Maximizing treasury return.• Promote Lebanon international image.• Help financing public debt.• Meet some of the international

requirements• Open the road map for other SOE

privatization (Rafic El Hariri Int’l Airport)• Enhance Beirut stock exchange

performance:1. Increase capital market.2. Increase daily volume

trade.3. Increase liquidity.

48

F.M. Nsouli, Ph.D.

Lebanese Economic Association

Expected ResultsExpected Results MEA’s Benefits from Strategic Partner:

• A strategic partner will make the company more appealing for investors and customers at the same time.

• MEA will benefit from the expertise and some management/employee skills of the partner who should be “older” in both experience and field of aviation. The partner should preferably be a major airline company.

• MEA will benefit from all facilities regarding routes and airports in order to reduce its total cost.

• MEA will benefit from the partner’s network, both airlines could serve as feeders for each other.

• Further benefits could be taken when any of the two is in need of temporary extra flights, extra crew …

49

F.M. Nsouli, Ph.D.

Lebanese Economic Association

Expected ResultsExpected ResultsMEA :

– MEA will be able to increase its market share.

– MEA will be well prepared for new market entries and competition.

– MEA will be able to enhance its subsidiaries companies performance (MEAS, MEAG and MASCO).

– MEA will be able to generate more profit and increase share holder wealth.

50

F.M. Nsouli, Ph.D.

Lebanese Economic Association

Expected ResultsExpected Results

Consumer Satisfaction include:• High quality of services • Frequency of flights• New destinations• High security level• Attachment and confidence in

MEA brand name

51

F.M. Nsouli, Ph.D.

Lebanese Economic Association

VI. ConclusionVI. Conclusion In summary, the main and most

important weaknesses in Lebanon are the solvency of the state and the high exposure between the government and the banking system. This relation means that any weakness in one sector will directly affect the other and vice versa. The Lebanese government dependence on banks can be shifted to other public sectors by privatization, to avoid loss or failure of other sectors.

52

F.M. Nsouli, Ph.D.

Lebanese Economic Association

ConclusionConclusion Furthermore, privatization process is lengthy

for major transactions, mainly to assure transparency in the process. After receiving the “Cabinet Committee on Privatization” approval to privatize, it will typically take about 14 months to close a major transaction, even when no major restructuring of a company is required like MEA .This needs about three or four months to appoint a Financial Advisor and another three or four months to complete its legal, technical and financial due diligence and to propose a privatization strategy. Following the approval of the strategy, the marketing and bidding process may take four or five months (valuation efforts proceed in parallel), while it may take another one month after bidding to obtain approvals, finalize sale documents, and close the transaction.

53

F.M. Nsouli, Ph.D.

Lebanese Economic Association

ConclusionConclusion The privatization method chosen represents an

attractive financing vehicle for a growing company like MEA. This will increase company's net worth , facilitate future debt and equity financings. In addition to an increase in publicity and attention from the investment community.

MEA’s privatization along with other SOE’s privatizations will definitely put the Debt to GDP ratio into downward sloping trend!

MEA privatization process will attract new investors for other SOE’s with privatization potential.

Central Bank governor Mr. Riad Salameh said that the MEA will be offered for sale once there is a political consensus.

In order to put an end to corruption in Lebanon and in order for the Lebanese economy to become more efficient, Take it away from the politicians, privatize!